Attached files

| file | filename |

|---|---|

| EX-21 - SUBSIDIARIES - LUBYS INC | d249113dex21.htm |

| EX-32.1 - SECTION 906 CERTIFICATION OF CEO - LUBYS INC | d249113dex321.htm |

| EX-31.2 - SECTION 302 CERTIFICATION OF CFO - LUBYS INC | d249113dex312.htm |

| EX-32.2 - SECTION 906 CERTIFICATION OF CFO - LUBYS INC | d249113dex322.htm |

| EX-23.1 - CONSENT OF GRANT THORNTON LLP - LUBYS INC | d249113dex231.htm |

| EX-31.1 - SECTION 302 CERTIFICATION OF CEO - LUBYS INC | d249113dex311.htm |

| EX-10.(JJ) - AMENDMENT NO. 5 TO EMPLOYMENT AGREEMENT - HARRIS J. PAPPAS - LUBYS INC | d249113dex10jj.htm |

| EX-10.(CC) - AMENDMENT NO. 5 TO EMPLOYMENT AGREEMENT - CHRISTOPHER J. PAPPAS - LUBYS INC | d249113dex10cc.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended August 31, 2011

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period From to

Commission file number 001-08308

Luby’s, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 74-1335253 | |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification Number) |

13111 Northwest Freeway, Suite 600

Houston, Texas 77040

(Address of principal executive offices, including zip code)

(713) 329-6800

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on which registered | |

| Common Stock ($0.32 par value per share) | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ |

Accelerated filer x | |

| Non-accelerated filer ¨ |

Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the shares of common stock of the registrant held by nonaffiliates of the registrant as of February 8, 2011, was approximately $104,997,000 (based upon the assumption that directors and executive officers are the only affiliates).

As of November 9, 2011, there were 28,165,005 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following document are incorporated by reference into the designated parts of this Form 10-K:

Definitive Proxy Statement relating to 2012 annual meeting of shareholders (in Part III)

Table of Contents

Luby’s, Inc.

Form 10-K

Year ended August 31, 2011

| Page | ||||||

| Part I | ||||||

| Item 1 | 6 | |||||

| Item 1A | 10 | |||||

| Item 1B | 17 | |||||

| Item 2 | 17 | |||||

| Item 3 | 18 | |||||

| Item 4 | 18 | |||||

| Part II | ||||||

| Item 5 | 19 | |||||

| Item 6 | 21 | |||||

| Item 7 | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

22 | ||||

| Item 7A | 44 | |||||

| Item 8 | 45 | |||||

| Item 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

81 | ||||

| Item 9A | 81 | |||||

| Item 9B | 82 | |||||

| Part III | ||||||

| Item 10 | 83 | |||||

| Item 11 | 83 | |||||

| Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

83 | ||||

| Item 13 | Certain Relationships and Related Transactions, and Director Independence |

83 | ||||

| Item 14 | 83 | |||||

| Part IV | ||||||

| Item 15 | 84 | |||||

| Signatures | 89 | |||||

Table of Contents

Additional Information

We file reports with the Securities and Exchange Commission, including annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K. The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. We are an electronic filer, and the SEC maintains an Internet site at http://www.sec.gov that contains the reports, proxy and information statements, and other information that we file electronically. Our website address is www.lubys.com. Please note that our website address is provided as an inactive textual reference only. We make available free of charge through our website the annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. The information provided on our website is not part of this report, and is therefore not incorporated by reference unless such information is specifically referenced elsewhere in this report.

Compliance with New York Stock Exchange Requirements

We submitted to the New York Stock Exchange (“NYSE”) the CEO certification required by Section 303A.12(a) of the NYSE’s Listed Company Manual with respect to our fiscal year ended August 25, 2010. We expect to submit the CEO certification with respect to our fiscal year ended August 31, 2011 to the NYSE within 30 days after our annual meeting of shareholders. We are filing as an exhibit to this Form 10-K the certifications required by Section 302 of the Sarbanes-Oxley Act of 2002.

3

Table of Contents

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains statements that are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements contained in this Form 10-K, other than statements of historical facts, are “forward-looking statements” for purposes of these provisions, including any statements regarding:

| • | future operating results; |

| • | future capital expenditures, including expected reductions in capital expenditures; |

| • | future debt, including liquidity and the sources and availability of funds related to debt; |

| • | plans for our new prototype restaurants; |

| • | plans for expansion of our business; |

| • | scheduled openings of new units; |

| • | closing existing units; |

| • | effectiveness of management’s Cash Flow Improvement and Capital Redeployment Plan; |

| • | future sales of assets and the gains or losses that may be recognized as a result of any such sales; and |

| • | continued compliance with the terms of our 2009 Credit Facility. |

In some cases, investors can identify these statements by forward-looking words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “outlook,” “may” “should,” “will,” and “would” or similar words. Forward-looking statements are based on certain assumptions and analyses made by management in light of their experience and perception of historical trends, current conditions, expected future developments and other factors we believe are relevant. Although management believes that our assumptions are reasonable based on information currently available, those assumptions are subject to significant risks and uncertainties, many of which are outside of our control. The following factors, as well as the factors set forth in Item 1A of this Form 10-K and any other cautionary language in this Form 10-K, provide examples of risks, uncertainties, and events that may cause our financial and operational results to differ materially from the expectations described in our forward-looking statements:

| • | general business and economic conditions; |

| • | the impact of competition; |

| • | our operating initiatives, changes in promotional, couponing and advertising strategies and the success of management’s business plans; |

| • | fluctuations in the costs of commodities, including beef, poultry, seafood, dairy, cheese, oils and produce; |

| • | ability to raise menu prices and customers acceptance of changes in menu items; |

| • | increases in utility costs, including the costs of natural gas and other energy supplies; |

| • | changes in the availability and cost of labor, including the ability to attract qualified managers and team members; |

| • | the seasonality of the business; |

| • | collectability of accounts receivable; |

| • | changes in governmental regulations, including changes in minimum wages and health care benefit regulation; |

4

Table of Contents

| • | the effects of inflation and changes in our customers’ disposable income, spending trends and habits; |

| • | the ability to realize property values; |

| • | the availability and cost of credit; |

| • | weather conditions in the regions our restaurants operate; |

| • | costs relating to legal proceedings; |

| • | impact of adoption of new accounting standards; |

| • | effects of actual or threatened future terrorist attacks in the United States; |

| • | unfavorable publicity relating to operations, including publicity concerning food quality, illness or other health concerns or labor relations; and |

| • | the continued service of key management personnel. |

Each forward-looking statement speaks only as of the date of this Form 10-K, and we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Investors should be aware that the occurrence of the events described above and elsewhere in this Form 10-K could have material adverse effect on our business, results of operations, cash flows and financial condition.

5

Table of Contents

PART I

| Item 1. | Business |

Overview

Luby’s, Inc. (formerly, Luby’s Cafeterias, Inc.) was founded in 1947 in San Antonio, Texas. The Company was originally incorporated in Texas in 1959, with nine cafeterias in various locations, under the name Cafeterias, Inc. It became a publicly held corporation in 1973, then changed its name in 1981 to Luby’s Cafeterias, Inc. and joined the New York Stock Exchange in 1982. Luby’s, Inc. was reincorporated in Delaware on December 31, 1991 and was restructured into a holding company on February 1, 1997, at which time all of the operating assets were transferred to Luby’s Restaurants Limited Partnership, a Texas limited partnership composed of two wholly owned, indirect corporate subsidiaries. On July 9, 2010, Luby’s Restaurants Limited Partnership was converted into Luby’s Fuddruckers Restaurants, LLC, a Texas limited liability company (“LFR”). All restaurant operations are conducted by LFR. In this report, unless otherwise specified, “Luby’s,” “we,” “our,” “us” and “our company” refer to Luby’s, Inc., LFR and the consolidated subsidiaries of Luby’s, Inc.

On July 26, 2010, we, through our subsidiary, LFR, completed the acquisition of substantially all of the assets of Fuddruckers, Inc., Magic Brands, LLC and certain of their affiliates (collectively, “Fuddruckers”) for approximately $63.1 million of cash. LFR also assumed certain of Fuddruckers’ obligations, real estate leases and contracts. Upon the completion of the acquisition, LFR became the owner and operator of 56 Fuddruckers locations and 3 Koo Koo Roo Chicken Bistro (“Koo Koo Roo”) locations with franchisees currently operating an additional 130 locations.

Luby’s, Inc. is a multi-branded company operating in the restaurant industry and the contract food services industry. Our primary brands include Luby’s Cafeteria, Luby’s Culinary Contract Services, and Fuddruckers. Also included in our brands are Luby’s, Etc. and Koo Koo Roo Chicken Bistro.

As of November 9, 2011, we operated 155 restaurants located throughout the United States, as set forth in the table below. These establishments are located in close proximity to retail centers, business developments and residential areas. Of the 155 restaurants, 81 are located on property that we own and 74 are on leased premises.

| Total | ||||

| Texas: |

||||

| Houston Metro |

46 | |||

| Dallas/Fort Worth Metro |

13 | |||

| San Antonio Metro |

19 | |||

| Rio Grande Valley |

11 | |||

| Austin |

10 | |||

| Other Texas Markets |

15 | |||

| Arizona |

5 | |||

| California |

12 | |||

| Georgia |

3 | |||

| Illinois |

5 | |||

| Maryland |

3 | |||

| Virginia |

3 | |||

| Other States |

10 | |||

|

|

|

|||

| Total |

155 | |||

As of November 9, 2011, we operated culinary contract services at 21 locations; 15 in the Houston, Texas area, 3 in Louisiana, 2 in Denton, Texas and 1 in Austin, Texas. Luby’s Culinary Services provides food service management to healthcare, educational and corporate dining facilities.

6

Table of Contents

As of November 9, 2011, we had 60 franchisees operating 121 Fuddruckers restaurants, of which 116 are located in 30 states, 1 in Canada and 4 in Puerto Rico.

| Fuddruckers Franchises |

||||

| Texas: |

||||

| Houston Metro |

1 | |||

| Dallas/Fort Worth Metro |

9 | |||

| Other Texas Markets |

18 | |||

| California |

9 | |||

| Florida |

5 | |||

| Georgia |

3 | |||

| Idaho |

2 | |||

| Louisiana |

3 | |||

| Maryland |

2 | |||

| Massachusetts |

5 | |||

| Michigan |

6 | |||

| Missouri |

3 | |||

| Montana |

6 | |||

| Nebraska |

1 | |||

| Nevada |

3 | |||

| New Jersey |

5 | |||

| New Mexico |

3 | |||

| North Carolina |

2 | |||

| Oregon |

2 | |||

| Pennsylvania |

5 | |||

| South Carolina |

8 | |||

| South Dakota |

2 | |||

| Tennessee |

3 | |||

| Virginia |

3 | |||

| Wisconsin |

2 | |||

| Other States |

5 | |||

| Canada |

1 | |||

| Puerto Rico |

4 | |||

|

|

|

|||

| Total |

121 | |||

For additional information regarding our restaurant locations, please read “Properties” in Item 2 of Part I of this report.

We are headquartered in Houston, Texas, our largest restaurant market. Our corporate headquarters is located at 13111 Northwest Freeway, Suite 600, Houston, Texas 77040, and our telephone number at that address is (713) 329-6800. Our website is www.lubys.com.

Luby’s Cafeteria

Operations

Luby’s Cafeteria provides its customers with made-from-scratch quality food, value pricing, service and hospitality. Our cafeteria-style restaurants feature a unique concept format in today’s family and casual dining segment of restaurant companies. The cafeteria food delivery system allows customers to select freshly prepared items from the serving line, including entrées, vegetables, salads, desserts, breads and beverages, before transporting their selected items on serving trays to a table or booth of their choice in the dining area. Each restaurant offers 15 to 20 entrées, 12 to 14 vegetable dishes, 8 to 10 salads, and 10 to 12 varieties of desserts daily. Food is prepared in small quantities throughout serving hours, and frequent quality checks are conducted.

7

Table of Contents

Luby’s Cafeteria’s product offerings are home-style classic made from scratch favorites priced to appeal to a broad range of customers, including those customers that focus on fast wholesome choices, quality, variety and affordability. We have had particular success among families with children, shoppers, travelers, seniors, and business people looking for a quick, freshly prepared meal at a fair price. Our restaurants are generally open for lunch and dinner seven days a week and all of our restaurants sell food-to-go orders, which accounted for 14.1% of restaurant sales in fiscal year 2011.

Food is prepared fresh daily at our restaurants. Menus are reviewed periodically and new offerings and seasonal food preferences are regularly incorporated. Each restaurant is operated as a separate unit under the control of a general manager who has responsibility for day-to-day operations, including food production and personnel employment and supervision. Our philosophy is to grant authority to restaurant managers to direct the daily operations of their stores and, in turn, to compensate them on the basis of their performance. We believe this strategy is a significant factor contributing to the profitability of our restaurants.

Each general manager is supervised by an area leader. Each area leader is responsible for approximately 7 to 10 units, depending on location.

Quality control teams also help maintain uniform standards of food preparation, safety and sanitation. The teams visit each restaurant as necessary and work with the staff to confirm adherence to our recipes, train personnel in new techniques, and implement systems and procedures used universally throughout our company.

During fiscal year 2011, we spent approximately 0.6% of restaurant sales on marketing with particular emphasis on local restaurant promotions and outdoor billboards. We operate from a centralized purchasing arrangement to obtain the economic benefit of bulk purchasing and lower prices for most of our menu offerings. The arrangement involves a competitively selected prime vendor for each of our three major purchasing regions.

The number of Luby’s Cafeterias was 96 in fiscal years 2010 and 2011.

New Luby’s Prototype Restaurant

In August 2007, we introduced our new restaurant prototype design, with the opening of our first new store in over seven years, located in Cypress, Texas, a suburb north of Houston. This new prototype capitalizes on our core fundamentals of serving great food made-from-scratch and a convenient delivery system. In fiscal year 2008, we opened three new units employing this prototype design. Although we opened no new prototype units in fiscal years 2009, 2010 and 2011, we anticipate using and further modifying this prototype design as we execute our strategy to build new restaurants in markets where we believe we can achieve superior restaurant cash flows. One location was relocated into a new restaurant building directly across from its current location as a result of the landlord’s renovation plans.

Fuddruckers

Fuddruckers was founded upon the idea that guests deserve and crave a better burger experience. Fatigued by fast food quality, guests gravitated to Fuddruckers better burger concept.

To prove its commitment to serving not just better burgers, but the World’s Greatest Hamburgers, Fuddruckers designed an open kitchen where guests could see burgers freshly prepared from scratch all day. Central to the brand was the notion that nobody builds a better burger than you—so Fuddruckers pioneered the Build Your Own burger concept.

Fuddruckers serves fresh, 100% All-American premium-cut ready for oven beef. Vegetarian-fed through a combination of open grass grazing and grain, Fuddruckers beef is bred for taste on ranches only in the U.S.A. No

8

Table of Contents

fillers or artificial ingredients are ever added to Fuddruckers beef—and only the freshest cuts of beef with optimal marbling make the cut at Fuddruckers. Fuddruckers scratch-baked buns are made fresh all day in each restaurant’s bakery.

Guests take it from there at Fuddruckers Build Your Own market fresh produce bar where they pile it high with their choice of fresh veggies and signature Fuddruckers condiments.

While Fuddruckers’ signature burger accounts for approximately 47.0% of Fuddruckers restaurant sales, its menu also includes all-natural, free-range Fudds Exotics burgers, such as buffalo, fresh rib eye steak sandwiches, various grilled and breaded chicken breast sandwiches, hot dogs, a variety of tossed and specially prepared salads and soups, fish sandwiches, wedge-cut French fries, onion rings, soft drinks, handmade milkshakes, and bakery items. Beer and wine are served and, generally, account for less than 2% of restaurant sales.

Fuddruckers restaurants continue to feature casual, welcoming dining areas where Americana themed décor hang upon the walls.

Fuddruckers emphasizes simplicity in its operations. Restaurants generally have a total staff of one general manager, two or three assistant managers and 25 to 45 other associates, including full-time and part-time associates working in overlapping shifts. Since Fuddruckers generally utilizes a self-service concept, similar to quick casual, it typically does not employ waiters or waitresses.

Fuddruckers restaurant operations are currently divided into two regions, each supervised by an Area Vice President. The two regions are divided into a total of eight areas, each supervised by an Area Leader. On average, each Area Leader supervises seven restaurants.

We opened one Fuddruckers unit and acquired one unit from a franchisee, resulting in a fiscal 2011 year end count of 58 Fuddruckers restaurants and 3 Koo Koo Roo restaurants.

Franchising

Fuddruckers offers franchises in markets where it deems expansion to be advantageous to the development of the Fuddruckers concept and system of restaurants. The franchise agreements, after considering renewal periods, have an estimated term of 21 years. Franchise agreements typically grant franchisees an exclusive territorial license to operate a single restaurant within a specified area, usually a four-mile radius surrounding the franchised restaurant. As the new franchisor of Fuddruckers, Luby’s management will be developing its relationships with our franchisees over the coming years and beyond.

Franchisees bear all direct costs involved in the development, construction and operation of their restaurants. In exchange for a franchise fee, we provide franchise assistance in the following areas: site selection, prototypical architectural plans, interior and exterior design and layout, training, marketing and sales techniques, assistance by a Fuddruckers “opening team” at the time a franchised restaurant opens, and operations and accounting guidelines set forth in various policies and procedures manuals.

All franchisees are required to operate their restaurants in accordance with Fuddruckers standards and specifications, including controls over menu items, food quality and preparation. We require the successful completion of its training program by a minimum of three managers for each franchised restaurant. In addition, franchised restaurants are evaluated regularly by us for compliance with franchise agreements, including standards and specifications through the use of periodic, unannounced, on-site inspections and standards evaluation reports.

The number of franchised restaurants was reduced from 130 at fiscal year end 2010 to 122 at fiscal year end 2011.

9

Table of Contents

Intellectual Property

Luby’s, Inc. owns or is licensed to use valuable intellectual property including trademarks, service marks, patents, copyrights, trade secrets and other proprietary information, including the Luby’s and Fuddruckers logos, trade names and trademarks, which are of material importance to our business. Depending on the jurisdiction, trademarks and service marks generally are valid as long as they are used and/or registered. Patents, copyrights and licenses are of varying durations. The success of our business depends on the continued ability to use existing trademarks, service marks and other components of our brands in order to increase brand awareness and further develop branded products and we take steps to protect our intellectual property.

Culinary Contract Services

Our culinary contract services operation (“CCS”), branded as Luby’s Culinary Services, consists of a business line servicing healthcare, higher education and corporate dining clients. The healthcare accounts are full service and typically include in-room delivery, catering, vending, coffee service and retail dining. As of November 9, 2011, we had contracts with 5 long-term acute care hospitals, 5 acute care medical centers, 2 ambulatory surgical centers, 2 behavioral hospitals, 4 business and industry clients, and 3 higher education institutions. We have the unique ability to deliver quality services that include facility design and procurement as well as nutrition and branded food services to our clients. We anticipate allocating capital expenditures as needed to further develop our CCS business in fiscal year 2012.

Employees

As of November 9, 2011, we had a workforce of 7,348 employees consisting of restaurant management employees, non-management restaurants employees, CCS management employees, CCS non-management employees, and office and facility service employees. Employee relations are considered to be good. We have never had a strike or work stoppage, and we are not subject to collective bargaining agreements.

| Item 1A. | Risk Factors |

An investment in our common stock involves a high degree of risk. Investors should consider carefully the risks and uncertainties described below, and all other information included in this Annual Report on Form 10-K, before deciding whether to purchase our common stock. Additional risks and uncertainties not currently known to us or that we currently deem immaterial may also become important factors that may harm our business, financial condition or results of operations. The occurrence of any of the following risks could harm our business, financial condition and results of operations. The trading price of our common stock could decline due to any of these risks and uncertainties, and investors may lose part or all of their investment.

General economic factors may adversely affect our results of operations.

The protracted economic slowdown experienced in the United States beginning in fiscal year 2008 has continued through fiscal year 2011. Disposable consumer income and consumer confidence continues to be adversely affected. As a result of the deteriorating business and economic conditions affecting our customers, we have experienced reduced customer traffic and have lowered our menu prices, which has lowered our profit margins and adversely affected our results of operations. A further slowdown in the economy or other economic conditions affecting disposable consumer income, such as unemployment levels, inflation, fuel and other energy costs, and interest rates, may adversely affect our business by reducing overall consumer spending or by causing customers to shift their spending to our competitors, which could result in a further reduction in customer traffic and lowered menu prices leading to a further reduction in revenues and a reduction in our margins. Due to economic conditions, in October 2009 we adopted a Cash Flow Improvement and Capital Redeployment Plan which included closing 24 under performing stores in the first quarter of fiscal year 2010. Continued difficulties in the U.S. economy could require us to close additional restaurants in the future.

10

Table of Contents

The impact of inflation on food, labor and other aspects of our business also can negatively affect our results of operations. Commodity inflation in food, beverages and utilities can also impact our financial performance. Although we attempt to offset the effects of inflation through periodic menu price increases, cost controls and incremental improvement in operating margins, we may not be able to completely do so, which could negatively affect our results of operations.

Our ability to service our debt obligations is primarily dependent upon our future financial performance.

As of August 31, 2011, we had shareholders’ equity of approximately $165.0 million compared to approximately:

| • | $21.5 million of long-term debt; |

| • | $70.2 million of minimum operating lease commitments; and |

| • | $1.2 million of standby letters of credit. |

Our ability to meet our debt service obligations depends on our ability to generate positive cash flows from operations and proceeds for assets held for sale.

We realized positive cash flows from operating activities of $4.8 million in fiscal year 2009, $9.3 million in fiscal year 2010 and $16.5 million in fiscal year 2011. We may in the future incur negative cash flows. Our future cash flows from operating activities will be influenced by general economic conditions and by financial, business and other factors affecting our operations, many of which are beyond our control, and some of which are specified below. If we are unable to service our debt obligations, we may have to

| • | delay spending on maintenance projects and other capital projects, including new restaurant development; |

| • | sell equity securities; |

| • | sell assets; or |

| • | restructure or refinance our debt. |

Our debt, and the covenants contained in the instruments governing our debt, could have important consequences to you. For example, it could:

| • | result in a reduction of our credit rating, which would make it more difficult for us to obtain additional financing on acceptable terms; |

| • | require us to dedicate a substantial portion of our cash flows from operating activities to the repayment of our debt and the interest associated with our debt; |

| • | limit our operating flexibility due to financial and other restrictive covenants, including restrictions on incurring additional debt and creating liens on our properties; |

| • | place us at a competitive disadvantage compared with our competitors that have relatively less debt; |

| • | expose us to interest rate risk because certain of our borrowings are at variable rates of interest; and |

| • | make us more vulnerable to downturns in our business. |

If we are unable to service our debt obligations, we may not be able to sell equity securities, sell additional assets or restructure or refinance our debt. Our ability to generate sufficient cash flow from operating activities to pay the principal of and interest on our indebtedness is subject to market conditions and other factors which are beyond our control.

11

Table of Contents

We face the risk of adverse publicity and litigation, the cost of which could have a material adverse effect on our business and financial performance.

We may from time to time be the subject of complaints or litigation from customers alleging illness, injury or other food quality, health or operational concerns. Unfavorable publicity relating to one or more of our restaurants or to the restaurant industry in general may taint public perception of the Luby’s Cafeteria and Fuddruckers brands. Multi-unit restaurant businesses can be adversely affected by publicity resulting from poor food quality, illness or other health concerns or operating issues stemming from one or a limited number of restaurants. Publicity resulting from these allegations may materially adversely affect our business and financial performance, regardless of whether the allegations are valid or whether we are liable. In addition, we are subject to employee claims alleging injuries, wage and hour violations, discrimination, harassment or wrongful termination. In recent years, a number of restaurant companies have been subject to lawsuits, including class action lawsuits, alleging violations of federal and state law regarding workplace, employment and similar matters. A number of these lawsuits have resulted in the payment of substantial damages by the defendants. Regardless of whether any claims against us are valid or whether we are ultimately determined to be liable, claims may be expensive to defend and may divert time and money away from our operations and hurt our financial performance. A judgment significantly in excess of our insurance coverage, if any, for any claims could materially adversely affect our financial condition or results of operations.

We are subject to risks related to the provision of employee health care benefits.

We use a combination of insurance and self-insurance for workers’ compensation coverage and health care plans. We record expenses under those plans based on estimates of the costs of expected claims, administrative costs, stop-loss insurance premiums and expected health care trends. These estimates are then adjusted each year to reflect actual costs incurred. Actual costs under these plans are subject to variability that is dependent upon participant enrollment, demographics, and the actual costs of claims made. In the event our cost estimates differ from actual costs, we could incur additional unplanned health care costs, which could adversely impact our financial condition.

In March 2010, comprehensive health care reform legislation under the Patient Protection and Affordable Care Act and Health Care Education and Affordability Reconciliation Act was passed and signed into law. Among other things, the health care reform legislation includes guaranteed coverage requirements, eliminates pre-existing condition exclusions and annual and lifetime maximum limits, restricts the extent to which policies can be rescinded, and imposes new and significant taxes on health insurers and health care benefits. Provisions of the health care reform legislation become effective at various dates over the next several years. The Department of Health and Human Services, the National Association of Insurance Commissioners, the Department of Labor and the Treasury Department have yet to issue necessary enabling regulations and guidance with respect to the health care reform legislation.

Due to the breadth and complexity of the health care reform legislation, the lack of implementing regulations and interpretive guidance, and the phased-in nature of the implementation, it is difficult to predict the overall impact of the health care reform legislation on our business and the businesses of our franchisees over the coming years. Possible adverse effects of the health care reform legislation include reduced revenues, increased costs, exposure to expanded liability and requirements for us to revise the ways in which we conduct business or risk of loss of business. In addition, our results of operations, financial position and cash flows could be materially adversely affected. Our franchisees face the potential of similar adverse effects, and many of them are small business owners who may have significant difficulty absorbing the increased costs.

12

Table of Contents

We face intense competition, and if we are unable to compete effectively or if customer preferences change, our business and financial performance will be adversely affected.

The restaurant industry is intensely competitive and is affected by changes in customer tastes and dietary habits and by national, regional and local economic conditions and demographic trends. New menu items, concepts, and trends are constantly emerging. Our Luby’s Cafeteria and Fuddruckers brands offer a large variety of entrées, side dishes and desserts and our continued success depends, in part, on the popularity of our cuisine and cafeteria-style dining. A change away from this cuisine or dining style could have a material adverse effect on our results of operations. Changing customer preferences, tastes and dietary habits can adversely impact our business and financial performance. We compete on quality, variety, value, service, concept, price, and location with well-established national and regional chains, as well as with locally owned and operated restaurants. We face significant competition from family-style restaurants, fast-casual restaurants, and buffets as well as fast food restaurants. In addition, we also face growing competition as a result of the trend toward convergence in grocery, deli, and restaurant services, particularly in the supermarket industry, which offers “convenient meals” in the form of improved entrées and side dishes from the deli section. Many of our competitors have significantly greater financial resources than we do. We also compete with other restaurants and retail establishments for restaurant sites and personnel. We anticipate that intense competition will continue. If we are unable to compete effectively, our business, financial condition, and results of operations would be materially adversely affected.

Our growth plan may not be successful.

Depending on future economic conditions, we may not be able to open new restaurants in current or future fiscal years. Our ability to open and profitably operate new restaurants is subject to various risks such as the identification and availability of suitable and economically viable locations, the negotiation of acceptable terms for new locations, the need to obtain all required governmental permits (including zoning approvals) on a timely basis, the need to comply with other regulatory requirements, the availability of necessary contractors and subcontractors, the availability of construction materials and labor, the ability to meet construction schedules and budgets, the ability to manage union activities such as picketing or hand billing which could delay construction, increases in labor and building materials costs, the availability of financing at acceptable rates and terms, changes in weather or other acts of God that could result in construction delays and adversely affect the results of one or more restaurants for an indeterminate amount of time, our ability to hire and train qualified management personnel and general economic and business conditions. At each potential location, we compete with other restaurants and retail businesses for desirable development sites, construction contractors, management personnel, hourly employees and other resources.

If we are unable to successfully manage these risks, we could face increased costs and lower than anticipated revenues and earnings in future periods. We may be evaluating acquisitions or engaging in acquisition negotiations at any given time. We cannot be sure that we will be able to continue to identify acquisition candidates on commercially reasonable terms or at all. If we make additional acquisitions, we also cannot be sure that any benefits anticipated from the acquisition will actually be realized. Likewise, we cannot be sure that we will be able to obtain necessary financing for acquisitions. Such financing could be restricted by the terms of our debt agreements or it could be more expensive than our current debt. The amount of such debt financing for acquisitions could be significant and the terms of such debt instruments could be more restrictive than our current covenants. In addition, a prolonged economic downturn would adversely affect our ability to open new stores or upgrade existing units and we may not be able to maintain the existing number of restaurants in future fiscal years. We may not be able to renew existing leases and various other risks could cause a decline in the number of restaurants in future fiscal years and thus substantially reduce the results of operations.

Our Cash Flow Improvement and Capital Redeployment Plan may not be successful.

Pursuant to our Cash Flow Improvement and Capital Redeployment Plan adopted in October 2009, we closed underperforming units in the first quarter of fiscal year 2010. We have 10 company-owned properties and 4 ground leased properties remaining to be sold or settled. Our ability to dispose of these properties is subject to

13

Table of Contents

various risks, including depressed market values, availability of credit to potential buyers and a lack of qualified buyers. Accordingly, the proceeds we ultimately realize from the dispositions may be less than expected, or may take longer to realize. In addition, the terms of these transactions may be on terms that are unfavorable to us. If we are unable to sell our properties at our carrying value, we will incur additional losses. Moreover, if proceeds ultimately received from the sales are less than expected, our ability to redeploy capital to continue upgrades to our core base of restaurants, to pay down debt incurred as part of the purchase of Fuddruckers and to expand our culinary contract services business may be impaired. Additional locations may be added to the plan depending on future cash flow performance.

Non-performance under the debt covenants in our revolving credit facility could adversely affect and or limit our ability to respond to changes in our business.

As of August 31, 2011, we had outstanding long-term debt of $21.5 million. In August 2011, we amended our revolving credit facility to, among other things, expand the facility size to $50.0 million and to add certain financial covenants. Our debt covenants require certain minimum levels of financial performance as well as certain financial ratios. Our failure to comply with these covenants could result in an event of default that, if not cured or waived, could result in the acceleration of our loans outstanding and affect our ability to refinance by the termination date of September 1, 2014.

Regional events can adversely affect our financial performance.

Many of our restaurants and franchises are located in Texas, California and in the northern United States. Our results of operations may be adversely affected by economic conditions in Texas, California or the northern United States or the occurrence of an event of terrorism or natural disaster in any of the communities in which we operate. Also, given our geographic concentration, negative publicity relating to our restaurants could have a pronounced adverse effect on our overall revenues. Although we generally maintain property and casualty insurance to protect against property damage caused by casualties and natural disasters, inclement weather, flooding, hurricanes and other acts of God, these events can adversely impact our sales by discouraging potential customers from going out to eat or by rendering a restaurant or culinary contract services location inoperable for a significant amount of time.

An increase in the minimum wage and regulatory mandates could adversely affect our financial performance.

From time to time, the U.S. Congress and state legislatures have increased and will consider increases in the minimum wage. The restaurant industry is intensely competitive, and if the minimum wage is increased, we may not be able to transfer all of the resulting increases in operating costs to our customers in the form of price increases. In addition, because our business is labor intensive, shortages in the labor pool or other inflationary pressure could increase labor costs that could adversely affect our results of operations.

We may be required to recognize additional impairment charges.

We assess our long-lived assets as and when recognized by generally accepted accounting principles in the United States and determine when they are impaired. Based on market conditions and operating results, we may be required to record additional impairment charges, which would reduce expected earnings for the periods in which they are recorded.

We may not be able to realize our deferred tax assets.

Our ability to realize our deferred tax assets is dependent on our ability to generate taxable income in the future. If we are unable to generate enough taxable income in the future, we may incur additions to the valuation allowance which would reduce expected earnings for the periods in which they are recorded.

14

Table of Contents

Franchises may breach the terms of their franchise agreements in a manner that adversely affects our brands.

Franchisees are required to conform to specified product quality standards and other requirements pursuant to their franchise agreements in order to protect our brand and to optimize restaurant performance. However, franchisees may receive through the supply chain or produce sub-standard food or beverage products, which may adversely impact the reputation of our brands. Franchisees may also breach the standards set forth in their respective franchise agreements.

Labor shortages or increases in labor costs could adversely affect our business and results of operations.

Our success depends in part upon our ability to attract, motivate and retain a sufficient number of qualified employees, including regional managers, restaurant general managers and chefs, in a manner consistent with our standards and expectations. Qualified individuals that we need to fill these positions are in short supply and competition for these employees is intense. If we are unable to recruit and retain sufficient qualified individuals, our operations and reputation could be adversely affected. Additionally, competition for qualified employees could require us to pay higher wages, which could result in higher labor costs. If our labor costs increase, our results of operations will be negatively affected.

If we are unable to anticipate and react to changes in food, utility and other costs, our results of operations could be materially adversely affected.

Many of the food and beverage products we purchase are affected by commodity pricing, and as such, are subject to price volatility caused by production problems, shortages, weather or other factors outside of our control. Our profitability depends, in part, on our successfully anticipating and reacting to changes in the prices of commodities. Therefore, we enter into purchase commitments with suppliers when we believe that it is advantageous for us to do so. If commodity prices were to increase, we may be forced to absorb the additional costs rather than transfer these increases to our customers in the form of menu price increases. Our success also depends, in part, on our ability to absorb increases in utility costs. Our operating results are affected by fluctuations in the price of utilities. Our inability to anticipate and respond effectively to an adverse change in any of these factors could have a significant adverse effect on our results of operations.

Our business is affected by local, state and federal regulations.

The restaurant industry is subject to extensive federal, state and local laws and regulations. We are also subject to licensing and regulation by state and local authorities relating to health, health care, employee medical plans, sanitation, safety and fire standards, building codes and liquor licenses, federal and state laws governing our relationships with employees (including the Fair Labor Standards Act and applicable minimum wage requirements, overtime, unemployment tax rates, family leave, tip credits, working conditions, safety standards, healthcare and citizenship requirements), federal and state laws which prohibit discrimination, potential healthcare benefits legislative mandates, and other laws regulating the design and operation of facilities, such as the Americans With Disabilities Act of 1990.

As a publicly traded corporation, we are subject to various rules and regulations as mandated by the Securities and Exchange Commission and the New York Stock Exchange. Failure to timely comply with these rules and regulations could result in penalties and negative publicity.

We are subject to federal regulation and certain state laws which govern the offer and sale of franchises. Many state franchise laws contain provisions that supersede the terms of franchise agreements, including provisions concerning the termination or non-renewal of a franchise. Some state franchise laws require that certain materials be registered before franchises can be offered or sold in that state. The failure to obtain or retain licenses or approvals to sell franchises could adversely affect us and the franchisees.

15

Table of Contents

Termination of franchise agreements may disrupt restaurant performance.

Our franchise agreements are subject to termination by us in the event of default by the franchisee after applicable cure periods. Upon the expiration of the initial term of a franchise agreement, the franchisee generally has an option to renew the franchise agreement for an additional term. There is no assurance that franchisees will meet the criteria for renewal or will desire or be able to renew their franchise agreements. If not renewed, a franchise agreement, and payments required thereunder, will terminate. We may be unable to find a new franchisee to replace such lost revenues. Furthermore, while we will be entitled to terminate franchise agreements following a default that is not cured within the applicable grace period, if any, the disruption to the performance of the restaurants could materially and adversely affect our business.

The misuse of the Fuddruckers trademark by current or former franchisees or others may cause reputational damage which could adversely affect our business.

Franchisee noncompliance with the terms and conditions of the governing franchise agreement may reduce the overall goodwill associated with the Fuddruckers brand. Any negative actions could have a corresponding material adverse effect on our business and revenues.

Our planned culinary contract services expansion may not be successful.

Successful expansion of our culinary contract services depends on our ability to obtain new clients as well as retain and renew our existing client contracts. Our ability to do so generally depends on a variety of factors, including the quality, price and responsiveness of our services, as well as our ability to market these services effectively and differentiate ourselves from our competitors. We may not be able to renew existing client contracts at the same or higher rates or our current clients may turn to competitors, cease operations, elect to self-operate or terminate contracts with us. The failure to renew a significant number of our existing contracts would have a material adverse effect on our business and results of operations.

If we do not collect our accounts receivable, our financial results could be adversely affected.

A portion of our accounts receivable is concentrated in our culinary contract service operations among several customers. In addition, our franchises generate significant accounts receivables. Failure to collect from several of these accounts receivable could adversely affect the results of our operations.

If we lose the services of any of our key management personnel, our business could suffer.

The success of our business is highly dependent upon our key management personnel, particularly Christopher J. Pappas, our President and Chief Executive Officer, and Peter Tropoli, our Chief Operating Officer. The loss of the services of any key management personnel could have a material adverse effect upon our business.

Our business is subject to seasonal fluctuations, and, as a result, our results of operations for any given quarter may not be indicative of the results that may be achieved for the full fiscal year.

Our business is subject to seasonal fluctuations. Historically, our highest earnings have occurred in the third quarter of the fiscal year, as our revenues in most of our restaurants have typically been higher during the third quarter of the fiscal year. Similarly, our results of operations for any single quarter will not necessarily be indicative of the results that may be achieved for a full fiscal year.

Economic factors affecting financial institutions could affect our access to capital.

The syndicate of banks may not have the ability to provide us with capital under our existing Revolving Credit Facility. Our existing Revolving Credit Facility expires in September 2014 and we may not be able to amend or renew the facility with terms and conditions consistent with the existing facility.

16

Table of Contents

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

As of November 9, 2011, Luby’s Cafeterias had 95 operating locations with seating capacity for 250 to 300 customers at each location. We own the underlying land and buildings in which 67 of our Luby’s restaurants are located. Five of these restaurant properties contain excess building space, of which four properties are leased to tenants unaffiliated with Luby’s, Inc.

In addition to the owned locations, 28 Luby’s Cafeteria restaurants are held under leases, including 8 in regional shopping malls. The majority of the leases are fixed-dollar rentals. The majority of the leases require additional amounts paid related to property taxes, hazard insurance and maintenance of common areas. Of the 28 restaurant leases, the current terms of 8 expire between 2011 and 2014, and 20 thereafter. Of the 28 restaurant leases, 24 can be extended beyond their current terms at our option.

As of November 9, 2011, we operated 57 Fuddruckers locations and 3 Koo Koo Roo locations. Each Fuddruckers restaurant generally has seating capacity for 125 to 200 customers while each Koo Koo Roo has seating capacity for 90 to 125 customers. We own the underlying land and buildings in which 14 of our Fuddruckers restaurants are located. The 3 Koo Koo Roo locations are located on leased property.

In addition to the 14 owned Fuddruckers locations, 43 restaurants are held under leases. The majority of the leases are fixed-dollar rentals. The majority of the leases require additional amounts paid related to property taxes, hazard insurance and maintenance of common areas. Of the 43 restaurant leases, the current terms of 18 expire between 2011 and 2014, and 25 thereafter. Of the 43 restaurant leases, 27 can be extended beyond their current terms at our option.

As of November 9, 2011, we had 2 owned Luby’s Cafeteria properties with a carrying value of approximately $1.0 million in properties held for sale. In addition, 10 owned Luby’s Cafeteria properties with a carrying value of $11.0 million, 2 ground leases and 2 unimproved ground leases with a carrying value of zero are discontinued operations properties which are also for sale or lease.

We currently have four owned other use properties; one is used as a Bake Shop that supports the baked products for operating Luby’s Cafeteria. Three locations are currently leased to third party tenants utilizing the entire building.

We also own two unimproved land locations that are held for future use.

We lease approximately 31,000 square feet of corporate office space, which extends through 2016. The space is located on the Northwest Freeway in Houston, Texas in close proximity to many of our Houston restaurant locations.

We lease approximately 60,000 square feet of warehouse space for in-house repair, fabrication and storage in Houston, Texas. In addition, we lease approximately 3,200 square feet of warehouse and office space in Arlington, Texas.

We maintain general liability insurance and property damage insurance on all properties in amounts which management believes provide adequate coverage.

17

Table of Contents

| Item 3. | Legal Proceedings |

Certain current and former hourly restaurant employees filed a lawsuit against us in the U.S. District Court for the Southern District of Texas alleging violations of the Fair Labor Standards Act with respect to the inclusion of certain employees in a tip pool. The lawsuit sought back wages, penalties and attorney’s fees and was conditionally certified as a collective action in October 2008. On October 22, 2010, we agreed to a court settlement amount of $1.6 million, recognized in general and administrative expenses in the fourth quarter fiscal year 2010. We made related payments of $1.4 million as of August 31, 2011, as required by the settlement. Per the settlement, all claims had to be filed by August 31, 2011. Therefore, the settlement is complete and we recognized a $0.2 million reduction in general and administrative expenses in the fourth quarter of fiscal year 2011.

From time to time, we are subject to various other private lawsuits, administrative proceedings and claims that arise in the ordinary course of our business. A number of these lawsuits, proceedings and claims may exist at any given time. These matters typically involve claims from guests, employees and others related to issues common to the restaurant industry. We currently believe that the final disposition of these types of lawsuits, proceedings and claims will not have a material adverse effect on our financial position, results of operations or liquidity. It is possible, however, that our future results of operations for a particular quarter or fiscal year could be impacted by changes in circumstances relating to lawsuits, proceedings or claims.

| Item 4. | (Removed and Reserved) |

18

Table of Contents

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Stock Prices

Our common stock is traded on the New York Stock Exchange under the symbol “LUB.” The following table sets forth, for the last two fiscal years, the high and low sales prices on the New York Stock Exchange as reported in the consolidated transaction reporting system.

| Fiscal Quarter Ended |

High | Low | ||||||

| November 18, 2009 |

4.88 | 3.42 | ||||||

| February 10, 2010 |

3.82 | 3.25 | ||||||

| May 5, 2010 |

4.28 | 3.35 | ||||||

| August 25, 2010 |

5.38 | 3.67 | ||||||

| November 17, 2010 |

5.59 | 4.66 | ||||||

| February 9, 2011 |

6.97 | 5.39 | ||||||

| May 4, 2011 |

6.06 | 4.43 | ||||||

| August 31, 2011 |

6.19 | 4.31 | ||||||

As of November 9, 2011, there were 2,526 holders of record of our common stock. No cash dividends have been paid on our common stock since fiscal year 2000, and we currently have no intention to pay a cash dividend on our common stock. On November 9, 2011, the closing price of our common stock on the New York Stock Exchange was $4.26.

Equity Compensation Plans

Securities authorized under our equity compensation plans as of August 31, 2011, were as follows:

| (a) | (b) | (c) | ||||||||||

| Plan Category |

Number of Securities to be Issued Upon Exercise of Outstanding Options, Warrants and Rights |

Weighted-Average Exercise Price of Outstanding Options, Warrants and Rights |

Number of Securities Remaining Available for Future Issuance Under Equity Compensation Plans Excluding Securities Reflected in Column (a) |

|||||||||

| Equity compensation plans previously approved by security holders |

807,656 | $ | 9.16 | 839,716 | ||||||||

| Equity compensation plans not previously approved by security holders (1) |

29,627 | 6.74 | — | |||||||||

|

|

|

|

|

|||||||||

| Total |

837,283 | $ | 9.07 | 839,716 | ||||||||

|

|

|

|

|

|||||||||

| (1) | Represents the Luby’s, Inc. Non-employee Director Phantom Stock Plan. |

See Note 15, “Share-Based Compensation,” to our Consolidated Financial Statements included in Item 8 of Part II of this report.

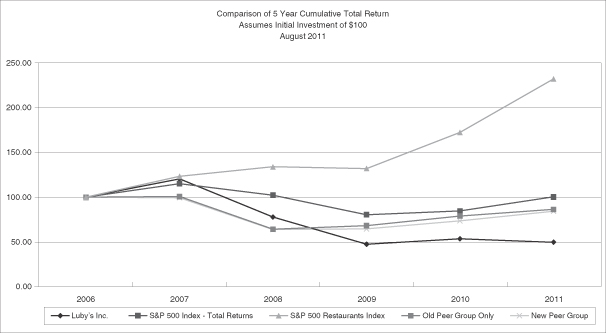

The following graph compares the cumulative total stockholder return on our common stock for the five fiscal years ended August 31, 2011, with the cumulative total return on the S&P SmallCap 600 Index and an industry peer group index. The peer group index consists of Bob Evans Farms, Inc., CBRL Group, Inc., Frisch Restaurant Group, O’Charley’s, Red Robin Gourmet Burgers and Ruby Tuesday Inc. These companies are multi-unit family and casual dining restaurant operators in the mid-price range.

19

Table of Contents

The cumulative total shareholder return computations set forth in the performance graph assume an investment of $100 on September 1, 2005, and the reinvestment of all dividends. The returns of each company in the peer group index have been weighed according to that company’s stock market capitalization.

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||||||

| Luby’s, Inc. |

100.00 | 120.52 | 78.03 | 47.85 | 53.90 | 50.05 | ||||||||||||||||||

| S&P 500 Index—Total Return |

100.00 | 115.13 | 102.32 | 80.72 | 84.68 | 100.35 | ||||||||||||||||||

| S&P 500 Restaurant Index |

100.00 | 123.38 | 133.86 | 132.06 | 172.31 | 231.82 | ||||||||||||||||||

| Old Peer Group Index Only |

100.00 | 100.70 | 64.36 | 68.55 | 79.05 | 86.49 | ||||||||||||||||||

| Old Peer Group Index + Lubys Inc. |

100.00 | 101.72 | 65.07 | 66.98 | 77.16 | 83.84 | ||||||||||||||||||

| New Peer Group Index Only |

100.00 | 99.43 | 64.29 | 65.01 | 73.63 | 84.52 | ||||||||||||||||||

| New Peer Group Index + Luby’s Inc. |

100.00 | 100.38 | 64.91 | 63.89 | 72.34 | 82.39 | ||||||||||||||||||

20

Table of Contents

| Item 6. | Selected Financial Data |

Five-Year Summary of Operations

| Fiscal Year Ended | ||||||||||||||||||||

| August 31, 2011 |

August 25, 2010 |

August 26, 2009 |

August 27, 2008 |

August 29, 2007 |

||||||||||||||||

| (371 days) | (364 days) | (364 days) | (364 days) | (364 days) | ||||||||||||||||

| (In thousands except per share data) | ||||||||||||||||||||

| Sales |

||||||||||||||||||||

| Restaurant sales |

$ | 325,383 | $ | 230,342 | $ | 245,799 | $ | 270,477 | $ | 276,069 | ||||||||||

| Culinary contract services |

15,619 | 13,728 | 12,970 | 8,205 | 2,065 | |||||||||||||||

| Franchise revenue |

7,092 | 645 | — | — | — | |||||||||||||||

| Vending revenue |

654 | 44 | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total sales |

348,748 | 244,759 | 258,769 | 278,682 | 278,134 | |||||||||||||||

| Income (loss) from continuing operations |

2,583 | (612 | ) | (14,062 | ) | 3,335 | 10,086 | |||||||||||||

| Income (loss) from discontinued operations (a) |

382 | (2,281 | ) | (12,356 | ) | (1,071 | ) | 777 | ||||||||||||

| Net income (loss) |

$ | 2,965 | $ | (2,893 | ) | $ | (26,418 | ) | $ | 2,265 | $ | 10,863 | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) per share from continuing operations: |

||||||||||||||||||||

| Basic |

$ | 0.09 | $ | (0.02 | ) | $ | (0.50 | ) | $ | 0.12 | $ | 0.39 | ||||||||

| Assuming dilution |

$ | 0.09 | $ | (0.02 | ) | $ | (0.50 | ) | $ | 0.12 | $ | 0.37 | ||||||||

| Income (loss) per share from discontinued operation: |

||||||||||||||||||||

| Basic |

$ | 0.01 | $ | (0.08 | ) | $ | (0.44 | ) | $ | (0.04 | ) | $ | 0.03 | |||||||

| Assuming dilution |

$ | 0.01 | $ | (0.08 | ) | $ | (0.44 | ) | $ | (0.04 | ) | $ | 0.03 | |||||||

| Net income (loss) per share |

||||||||||||||||||||

| Basic |

$ | 0.10 | $ | (0.10 | ) | $ | (0.94 | ) | $ | 0.08 | $ | 0.41 | ||||||||

| Assuming dilution |

$ | 0.10 | $ | (0.10 | ) | $ | (0.94 | ) | $ | 0.08 | $ | 0.40 | ||||||||

| Weighted-average shares outstanding |

||||||||||||||||||||

| Basic |

28,237 | 28,129 | 28,084 | 27,908 | 26,188 | |||||||||||||||

| Assuming dilution |

28,297 | 28,129 | 28,084 | 28,085 | 27,170 | |||||||||||||||

| Total assets |

$ | 228,020 | $ | 242,342 | $ | 199,406 | $ | 226,568 | $ | 219,686 | ||||||||||

| Total debt |

$ | 21,500 | $ | 41,500 | $ | — | $ | — | $ | — | ||||||||||

| Number of restaurants at fiscal year end |

156 | 154 | 119 | 123 | 128 | |||||||||||||||

| Number of franchised restaurants at fiscal year end |

122 | 130 | — | — | — | |||||||||||||||

| Number of Culinary Contract Services contracts at fiscal year end |

22 | 18 | 15 | 11 | 8 | |||||||||||||||

| Costs and Expenses |

||||||||||||||||||||

| (As a percentage of restaurant sales) |

||||||||||||||||||||

| Cost of food |

28.9 | % | 27.6 | % | 27.6 | % | 27.7 | % | 26.8 | % | ||||||||||

| Payroll and related costs |

34.8 | % | 36.0 | % | 36.3 | % | 34.3 | % | 33.5 | % | ||||||||||

| Other operating expenses |

23.7 | % | 22.2 | % | 23.0 | % | 23.1 | % | 21.4 | % | ||||||||||

| (a) | Our business plan approved in fiscal year 2010 called for the closure of more than 20 locations. In accordance with this plan, the entire fiscal activity of the applicable stores closed after the inception of the plan has been reclassified to discontinued operations. For comparison purposes, prior fiscal year’s results related to these same locations have also been reclassified to discontinued operations. Stores we close and classify as discontinued operations are significant in the number of stores closed. We believe the majority of cash flows lost will not be recovered and generated by the ongoing entity. The stores to be closed are included in a closure plan approved by our board of directors. We believe the majority of sales lost by closing a significant number of stores within a short period of time will not be recovered. In addition, there will not be any ongoing involvement or significant cash flows from the closed stores. Stores we close, but do not classify as discontinued operations, follow the implementation guidance in ASC 205-20-55 because cash flows are expected to be generated by the ongoing entity. There is some migration of customer traffic to existing or new locations, and ultimately the majority of sales lost by closing these stores is expected to be eventually replaced by sales from new and existing locations. |

21

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Management’s discussion and analysis of the financial condition and results of operations should be read in conjunction with the consolidated financial statements and footnotes for the fiscal years ended August 31, 2011 (“fiscal year 2011”), August 25, 2010 (“fiscal year 2010”), and August 26, 2009 (“fiscal year 2009”) included in Item 8 of this report.

Overview

In fiscal year 2011, we generated revenues primarily by providing quality food to customers at our 96 Luby’s Cafeteria branded restaurants located throughout Texas and three other states and 58 Fuddruckers restaurants, 3 Koo Koo Roo restaurants and 122 Fuddruckers franchises located throughout the U.S. On July 26, 2010, we became a multi-brand restaurant company with a national footprint through the acquisition of substantially all of the assets of Fuddruckers. The Fuddruckers acquisition added 59 Company-operated restaurants and a franchise network of 130 franchisee operated units. This acquisition further expanded our family-friendly, value-oriented portfolio of restaurants located in close proximity to retail centers, business developments and residential areas. In addition to our restaurant business model, we also provide culinary contract services for organizations that offer on-site food service, such as health care facilities, colleges and universities, as well as businesses and institutions.

In fiscal years 2011 and 2010, we continued to operate and compete, like many restaurant companies, in a slowly improving, albeit challenging economic, environment with customers seeking the most value for their dollar when they choose to dine away from home. Much of our focus during fiscal year 2011 centered around two goals: (1) to quickly integrate Fuddruckers restaurants into our organization and improve selected Fuddruckers facilities and processes in order to establish a base from which we can build and thus maximize the return on this investment. This included joint efforts with the business owners of the units in the franchise network. We also developed a new prototype for the Fuddruckers brand, built a Fuddruckers Express in one of our cafeteria units, tested the first-ever Fuddruckers drive-through at one unit, as well as tested various menu item upgrades, new menu options, new menu boards and installed exterior marquees to catch the attention of our customers and (2) to continue our at both of our restaurant brands to attract customers into our restaurants by redoubling our local store marketing initiatives and local community involvement. At our Cafeteria units, we continued developing store-specific menu offerings and limited time offers such as steak and shrimp on Friday and Saturday nights at select units, $2.00 and $3.00 entrée portions of our customer favorites (Luby’s fried fish and chicken fried steak) at lunch, and all-you-can-eat lunch or dinner buffets in certain locations. We also rolled out our all-you-can-eat breakfast buffets at a majority of our cafeteria locations, which significantly contributed to our year-over-year growth in customer count at our Luby’s Cafeteria units.

With the pressure of higher food commodity prices and impact on profit margins, we made modest price increases at both of our restaurant brands in the middle of fiscal year 2011 while continuing to offer excellent value to our guests. At the cafeteria units, some of these price increases reflected scaling back on some limited time offers at certain points during the year and certain daytimes during the week. The net result was an increase in same store sales of 2.5% at our cafeteria units. The sales increase at the cafeterias represented growth in customer count offset by a net decrease in average customer spend (modest price increases made mid-year only partially recovered price reductions made in the prior year). At our Fuddruckers restaurants, the sales growth represented growth in both customer counts and to a lesser extent an increase in average customer spend. Our goal in fiscal year 2012 will be to continue to balance the trade-off between customer growth and average customer spend. We will continue to seek to increase customer frequency by marketing quality offerings and building long term brand loyalty.

Capital spending increased to $11.0 million in fiscal year 2011 from the suppressed levels of fiscal year 2010. We continue to maintain the attractiveness of our Luby’s Cafeteria units and the Fuddruckers units that we acquired in July 2010, having made various upgrades to these locations in the past fiscal year. In fiscal 2012, we

22

Table of Contents

anticipate increasing our capital spending to between $15 million and $20 million, primarily for the remodeling of existing units and the construction of new restaurant units.

In this challenging economic environment, our strong balance sheet has allowed us to capitalize on the opportunity to increase the size of our revolving credit facility and acquire substantially all of the assets of Fuddruckers in July 2010. Since the acquisition, we have sold eight properties that were closed during or before our Cash Flow Improvement and Capital Redeployment Plan announced in October 2009. As a result, we have been able to use the proceeds from these property sales and cash generated from operations to aggressively pay down our debt balance to $21.5 million by the end of fiscal year 2011, representing over a 50% reduction in our outstanding debt balance.

Fiscal 2011 Review

Same-store restaurant sales at our Luby’s Cafeteria units increased 2.5% for fiscal year 2011 compared to fiscal year 2010. Same-store sales increased in the first three quarters in the fiscal year and turned slightly negative in the fourth quarter, compared to a relatively strong fourth quarter 2010 when we significantly increased our use of limited time offers to generate customer traffic and sales. Our increase in sales in fiscal year 2011 was generated by customer traffic growth, in large part due to our weekend breakfast offering, but at a lower overall ticket average. Fiscal year 2011 represents our first full year of same-store sales growth since fiscal year 2006.

Net income from continuing operations improved from a loss of $0.6 million, or $0.02 per share, on $244.8 million in total sales in fiscal year 2010 to a profit from continuing operations of $2.6 million, or $0.09 per share, on $348.7 million in total sales in fiscal year 2011.

Fiscal year 2011 net income improved by $5.9 million year-over-year. This profitability improvement was the result of the inclusion of a full year of results from Fuddruckers and growing sales in each of our brands, combined with careful cost management and operational focus. The following provides a brief summary of selected expenses:

| • | Food costs, as a percentage of restaurant sales increased to 28.9% in fiscal year 2011 from 27.6% in fiscal year 2010. The increase in food costs as a percentage of sales was driven primarily by higher food commodity costs, an increased impact from beef commodities due to the inclusion of the Fuddruckers units, and our ability to only partially pass along these higher food costs in the form of menu price increases. |

| • | Payroll and related costs as a percentage of sales declined primarily due to the inclusion of the Fuddruckers units, which generally operated at a lower labor costs due to the lower complexity of operations when compared to our cafeteria units. As a percentage of restaurant sales, payroll and related costs improved 120 basis points in fiscal year 2011 compared to fiscal year 2010 |

| • | As a percentage of restaurant sales, other operating expenses increased 150 basis points. The higher operating expenses as percentage of sales reflect the higher aggregate occupancy costs of the Fuddruckers restaurants due to the greater mix of leased properties over owned properties. As the Fuddruckers units were incorporated into our operations, we also incurred higher repairs and maintenance costs to improve the appearance and operations of selected restaurants. |

| • | Depreciation expense increased $2.0 million and reflects primarily the addition of Fuddruckers assets, partially offset by lower depreciation of our cafeteria assets. |

| • | General and administrative expenses increased by $4.0 million reflecting primarily incremental corporate staffing and related expenses to support the addition of the company-operated Fuddruckers units as well as the network of franchise restaurants. Fiscal year 2011 also included approximately $1.5 million in professional fees and integration expenses related to the acquisition of substantially all of the assets of Fuddruckers. |

23

Table of Contents

| • | Income taxes reflected a valuation allowance decrease of $0.5 million in fiscal year 2011 income from continuing operations of approximately $0.02 per share. |

Our culinary contract services (“CCS”) business continued to grow through the net addition of four new locations. We view this area as a growth business that generally requires less capital investment and more favorable percentage returns on invested capital. Our culinary contract services business generated $15.6 million in sales during fiscal year 2011 compared to $13.7 million in sales during fiscal year 2010.

In fiscal year 2011, we spent $11.0 million on capital expenditures, which primarily represented maintaining the attractiveness and efficiency of our restaurant units. During fiscal year 2011, we added leasehold improvements at a new Fuddruckers location in downtown Houston and at a relocated Luby’s restaurant in west Houston. We also acquired the assets at one former franchise location, including a building on a ground lease and the related furniture, fixtures and equipment.

Our long-term plan continues to focus on expanding both of our brands, including the Fuddruckers franchise network, as well as growing our CCS business. We are also committed to reducing debt through sales of properties where we have closed restaurants as well as using cash flow from operations. We believe our operational execution has improved through our commitment to higher operating standards, and we believe that we are well-positioned to enhance shareholder value over the long term.

Accounting Periods