Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - HALOZYME THERAPEUTICS, INC. | Financial_Report.xls |

| EX-32 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER AND CHIEF FINANCIAL OFFICER - HALOZYME THERAPEUTICS, INC. | d250665dex32.htm |

| EX-31.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER - HALOZYME THERAPEUTICS, INC. | d250665dex311.htm |

| EX-31.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER - HALOZYME THERAPEUTICS, INC. | d250665dex312.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2011

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to .

Commission File Number 001-32335

HALOZYME THERAPEUTICS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 88-0488686 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 11388 Sorrento Valley Road, San Diego, CA | 92121 | |

| (Address of principal executive offices) | (Zip Code) | |

(858) 794-8889

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The number of outstanding shares of the registrant’s common stock, par value $0.001 per share, was 103,691,643 as of November 2, 2011.

Table of Contents

INDEX

2

Table of Contents

PART I — FINANCIAL INFORMATION

CONDENSED CONSOLIDATED BALANCE SHEETS

| September 30, 2011 |

December 31, 2010 |

|||||||

| (Unaudited) | (Note) | |||||||

| ASSETS | ||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 66,329,358 | $ | 83,255,848 | ||||

| Accounts receivable |

6,237,904 | 2,328,268 | ||||||

| Inventory |

103,443 | 193,422 | ||||||

| Prepaid expenses and other assets |

4,297,814 | 3,720,896 | ||||||

|

|

|

|

|

|||||

| Total current assets |

76,968,519 | 89,498,434 | ||||||

| Property and equipment, net |

1,274,753 | 1,846,899 | ||||||

|

|

|

|

|

|||||

| Total Assets |

$ | 78,243,272 | $ | 91,345,333 | ||||

|

|

|

|

|

|||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 1,219,905 | $ | 3,820,368 | ||||

| Accrued expenses |

8,864,705 | 8,605,569 | ||||||

| Deferred revenue |

3,707,795 | 2,917,129 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

13,792,405 | 15,343,066 | ||||||

| Deferred revenue, net of current portion |

36,667,445 | 55,176,422 | ||||||

| Deferred rent, net of current portion |

728,259 | 474,389 | ||||||

| Commitments and contingencies (Note 11) |

||||||||

| Stockholders’ equity: |

||||||||

| Preferred stock — $0.001 par value; 20,000,000 shares authorized; no shares issued and outstanding |

- | - | ||||||

| Common stock — $0.001 par value; 150,000,000 shares authorized; 103,647,930 and 100,580,849 shares issued and outstanding at September 30, 2011 and December 31, 2010, respectively |

103,648 | 100,581 | ||||||

| Additional paid-in capital |

253,557,547 | 245,502,670 | ||||||

| Accumulated deficit |

(226,606,032) | (225,251,795) | ||||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

27,055,163 | 20,351,456 | ||||||

|

|

|

|

|

|||||

| Total Liabilities and Stockholders’ Equity |

$ | 78,243,272 | $ | 91,345,333 | ||||

|

|

|

|

|

|||||

| Note: | The condensed consolidated balance sheet at December 31, 2010 has been derived from audited financial statements at that date. It does not include, however, all of the information and notes required by U.S. generally accepted accounting principles for complete financial statements. |

See accompanying notes to condensed consolidated financial statements.

3

Table of Contents

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Revenues: |

||||||||||||||||

| Product sales |

$ | 1,156,903 | $ | 98,100 | $ | 1,487,822 | $ | 695,440 | ||||||||

| Revenues under collaborative agreements |

21,785,525 | 3,298,407 | 52,187,447 | 9,356,151 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues |

22,942,428 | 3,396,507 | 53,675,269 | 10,051,591 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating expenses: |

||||||||||||||||

| Cost of product sales |

11,723 | 7,214 | 201,675 | 96,413 | ||||||||||||

| Research and development |

13,514,352 | 12,448,865 | 42,647,265 | 35,840,475 | ||||||||||||

| Selling, general and administrative |

4,263,520 | 3,374,069 | 12,237,152 | 10,488,568 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total operating expenses |

17,789,595 | 15,830,148 | 55,086,092 | 46,425,456 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income (loss) |

5,152,833 | (12,433,641) | (1,410,823) | (36,373,865) | ||||||||||||

| Interest and other income, net |

12,360 | 24,065 | 56,586 | 25,889 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | 5,165,193 | $ | (12,409,576) | $ | (1,354,237) | $ | (36,347,976) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) per share: |

||||||||||||||||

| Basic |

$ | 0.05 | $ | (0.13) | $ | (0.01) | $ | (0.39) | ||||||||

| Diluted |

$ | 0.05 | $ | (0.13) | $ | (0.01) | $ | (0.39) | ||||||||

| Shares used in computing net income (loss) per share: |

||||||||||||||||

| Basic |

103,223,352 | 93,626,893 | 102,282,904 | 92,342,665 | ||||||||||||

| Diluted |

105,009,189 | 93,626,893 | 102,282,904 | 92,342,665 | ||||||||||||

See accompanying notes to condensed consolidated financial statements.

4

Table of Contents

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| Nine Months Ended September 30, |

||||||||

| 2011 | 2010 | |||||||

| Operating activities: |

||||||||

| Net loss |

$ | (1,354,237) | $ | (36,347,976) | ||||

| Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

| Share-based compensation |

3,916,329 | 3,745,976 | ||||||

| Depreciation and amortization |

851,613 | 1,164,162 | ||||||

| (Gain) loss on disposal of equipment |

(992) | 8,431 | ||||||

| Changes in operating assets and liabilities: |

||||||||

| Accounts receivable |

(3,909,636) | 1,621,833 | ||||||

| Inventory |

89,979 | 82,971 | ||||||

| Prepaid expenses and other assets |

(576,918) | (3,317,779) | ||||||

| Accounts payable and accrued expenses |

(2,183,864) | (2,184,007) | ||||||

| Deferred rent |

89,453 | (226,699) | ||||||

| Deferred revenue |

(17,718,311) | (2,557,349) | ||||||

|

|

|

|

|

|||||

| Net cash used in operating activities |

(20,796,584) | (38,010,437) | ||||||

|

|

|

|

|

|||||

| Investing activities: |

||||||||

| Purchases of property and equipment |

(271,521) | (315,807) | ||||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(271,521) | (315,807) | ||||||

|

|

|

|

|

|||||

| Financing activities: |

||||||||

| Proceeds from exercises of stock options |

4,141,615 | 737,267 | ||||||

| Proceeds from issuance of common stock, net |

- | 59,965,059 | ||||||

|

|

|

|

|

|||||

| Net cash provided by financing activities |

4,141,615 | 60,702,326 | ||||||

|

|

|

|

|

|||||

| Net (decrease) increase in cash and cash equivalents |

(16,926,490) | 22,376,082 | ||||||

| Cash and cash equivalents at beginning of period |

83,255,848 | 67,464,506 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of period |

$ | 66,329,358 | $ | 89,840,588 | ||||

|

|

|

|

|

|||||

| Supplemental disclosure of non-cash investing and financing activities: |

||||||||

| Accounts payable for purchases of property and equipment |

$ | 6,954 | $ | 109,705 | ||||

See accompanying notes to condensed consolidated financial statements.

5

Table of Contents

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

| 1. | Organization and Business |

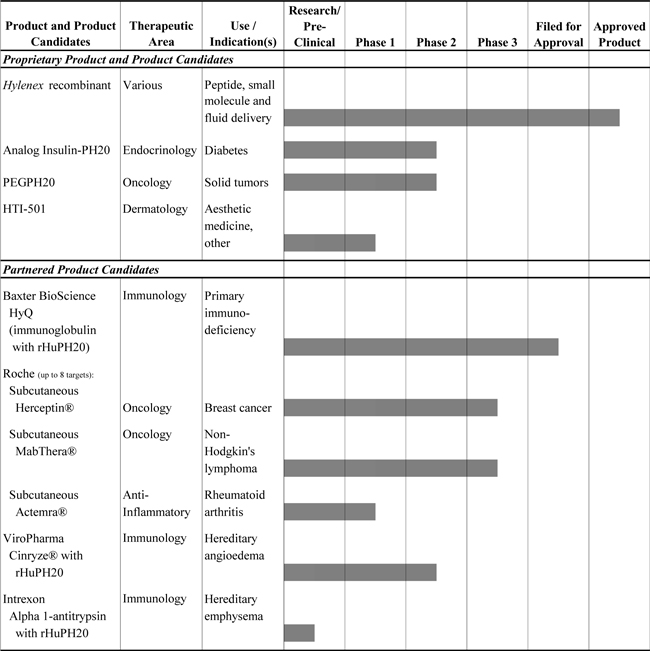

Halozyme Therapeutics, Inc. (“Halozyme” or the “Company”) is a biopharmaceutical company dedicated to the development and commercialization of recombinant human enzymes that either transiently modify tissue under the skin to facilitate injection of other therapies or correct diseased tissue structures for clinical benefit. The Company’s existing products and its products under development are based primarily on intellectual property covering the family of human enzymes known as hyaluronidases.

The Company’s operations to date have involved: (i) organizing and staffing its operating subsidiary, Halozyme, Inc.; (ii) acquiring, developing and securing its technology; (iii) undertaking product development for its existing products and a limited number of product candidates; and (iv) supporting the development of partnered product candidates. The Company currently has multiple proprietary programs in various stages of research and development. In addition, the Company has collaborative partnerships with F. Hoffmann-La Roche, Ltd. and Hoffmann-La Roche, Inc. (“Roche”), Baxter Healthcare Corporation (“Baxter”), ViroPharma Incorporated (“ViroPharma”) and Intrexon Corporation (“Intrexon”) to apply the Company’s proprietary Enhanze™ Technology to the partners’ biological therapeutic compounds. The Company also had a partnership with Baxter, under which Baxter had worldwide marketing rights for the Company’s marketed product, Hylenex® recombinant (hyaluronidase human injection), (the “Hylenex Partnership”). Hylenex recombinant is a human recombinant formulation of hyaluronidase that has received approval from the U.S. Food and Drug Administration (“FDA”) to facilitate subcutaneous fluid administration for achieving hydration; to increase the dispersion and absorption of other injected drugs; and in subcutaneous urography for improving resorption of radiopaque agents. In January 2011, the Company and Baxter mutually agreed to terminate the Hylenex Partnership. The Company’s technology is also being used in ICSI Cumulase®, a third party’s marketed product used for in vitro fertilization (“IVF”). Currently, the Company has received only limited revenue from the sales of active pharmaceutical ingredients (“API”) to the third party that produces ICSI Cumulase, in addition to other revenues from its collaborative partnerships.

| 2. | Summary of Significant Accounting Policies |

Basis of Presentation

The accompanying interim unaudited condensed consolidated financial statements have been prepared in accordance with United States generally accepted accounting principles (“U.S. GAAP”) and with the rules and regulations of the U.S. Securities and Exchange Commission (“SEC”) related to a quarterly report on Form 10-Q. Accordingly, they do not include all of the information and disclosures required by U.S. GAAP for a complete set of financial statements. These interim unaudited condensed consolidated financial statements and notes thereto should be read in conjunction with the audited consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2010, filed with the SEC on March 11, 2011. The unaudited financial information for the interim periods presented herein reflects all adjustments which, in the opinion of management, are necessary for a fair presentation of the financial condition and results of operations for the periods presented, with such adjustments consisting only of normal recurring adjustments. Operating results for interim periods are not necessarily indicative of the operating results for an entire fiscal year.

The condensed consolidated financial statements include the accounts of Halozyme Therapeutics, Inc. and its wholly owned subsidiary, Halozyme, Inc. All intercompany accounts and transactions have been eliminated.

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the amounts reported in the Company’s consolidated financial statements and accompanying notes. On an ongoing basis, the Company evaluates its estimates and judgments, which are based on historical and anticipated results and trends and on various other assumptions that management

6

Table of Contents

believes to be reasonable under the circumstances. By their nature, estimates are subject to an inherent degree of uncertainty and, as such, actual results may differ from management’s estimates.

Adoption of Recent Accounting Pronouncements

Effective January 1, 2011, the Company adopted on a prospective basis Financial Accounting Standards Board’s (“FASB”) Accounting Standards Update (“ASU”) No. 2010-17, Revenue Recognition (Topic 605): Milestone Method of Revenue Recognition (“Milestone Method”). ASU No. 2010-17 states that the Milestone Method is a valid application of the proportional performance model when applied to research or development arrangements. Accordingly, an entity can make an accounting policy election to recognize a payment that is contingent upon the achievement of a substantive milestone in its entirety in the period in which the milestone is achieved. The Milestone Method is not required and is not the only acceptable method of revenue recognition for milestone payments. The adoption of ASU No. 2010-17 did not have a material impact on the Company’s consolidated financial position or results of operations.

Effective January 1, 2011, the Company adopted on a prospective basis FASB’s ASU No. 2009-13, Revenue Recognition (Topic 605): Multiple-Deliverable Revenue Arrangements. ASU No. 2009-13 requires an entity to allocate arrangement consideration at the inception of an arrangement to all of its deliverables based on their relative selling prices. ASU No. 2009-13 eliminates the use of the residual method of allocation and requires the relative-selling-price method in all circumstances in which an entity recognizes revenue for an arrangement with multiple deliverables subject to Accounting Standards Code 605-25. The Company accounted for the collaborative arrangements with ViroPharma and Intrexon under the provisions of ASU No. 2009-13, which resulted in revenue recognition patterns that are materially different from those recognized for the Company’s existing multiple-element arrangements.

Pending Adoption of Accounting Pronouncements

In June 2011, the FASB issued ASU No. 2011-05, Comprehensive Income (Topic 220): Presentation of Comprehensive Income. In ASU No. 2011-05, an entity has the option to present the total of comprehensive income, the components of net income, and the components of other comprehensive income either in a single continuous statement of comprehensive income or in two separate but consecutive statements. In both choices, an entity is required to present each component of net income along with total net income, each component of other comprehensive income along with a total for other comprehensive income, and a total amount for comprehensive income. ASU No. 2011-05 eliminates the option to present the components of other comprehensive income as part of the statement of changes in stockholders’ equity. The amendments in ASU No. 2011-05 do not change the items that must be reported in other comprehensive income or when an item of other comprehensive income must be reclassified to net income. The amendments in ASU No. 2011-05 are effective for fiscal years, and interim periods within those years, beginning after December 15, 2011. The Company does not expect the adoption of ASU No. 2011-05 to have a material impact on its consolidated financial position or results of operations.

Revenue Recognition

The Company generates revenues from product sales and collaborative agreements. The Company recognizes revenues in accordance with the authoritative guidance for revenue recognition. The Company recognizes revenue when all of the following criteria are met: (1) persuasive evidence of an arrangement exists; (2) delivery has occurred or services have been rendered; (3) the seller’s price to the buyer is fixed or determinable; and (4) collectibility is reasonably assured.

Product Sales — Revenue from the sales of API for ICSI Cumulase is recognized when the transfer of ownership occurs, which is upon shipment to the Company’s distributor. The Company is obligated to accept returns for product that does not meet product specifications. Historically, the Company has not had any product returns as a result of not meeting product specifications.

Prior to the termination of the Hylenex Partnership with Baxter in January 2011, the Company supplied Baxter with API for Hylenex recombinant at its fully burdened cost plus a margin. Baxter filled and finished Hylenex recombinant and held it for subsequent distribution, at which time the Company ensured it met product specifications and released it as available for sale. Because of the Company’s continued involvement in the

7

Table of Contents

development and production process of Hylenex recombinant, the earnings process was not considered to be complete. Accordingly, the Company deferred the revenue and related product costs on the API for Hylenex recombinant until the product was filled, finished, packaged and released. Baxter could only return the API for Hylenex recombinant to the Company if it did not conform to the specified criteria set forth in the Hylenex Partnership or upon termination of such agreement. In addition, the Company received product-based payments upon the sale of Hylenex recombinant by Baxter, in accordance with the terms of the Hylenex Partnership. Product-based revenues were recognized as the Company earned such revenues based on Baxter’s shipments of Hylenex recombinant to its distributors when such amounts could be reasonably estimated. Effective January 7, 2011, the Company and Baxter mutually agreed to terminate the Hylenex Partnership and the associated agreements. See Note 7, “Deferred Revenue,” for further discussion.

Revenues under Collaborative Agreements — The Company entered into license and collaboration agreements under which the collaborative partners obtained worldwide exclusive rights for the use of the Company’s proprietary recombinant human PH20 enzyme (“rHuPH20”) in the development and commercialization of the collaborators’ biologic compounds. The collaborative agreements contain multiple elements including nonrefundable payments at the inception of the arrangement, license fees, exclusivity fees, payments based on achievement of specific milestones designated in the collaborative agreements, reimbursements of research and development services, payments for supply of rHuPH20 API for the collaborator and/or royalties on sales of products resulting from collaborative agreements. The Company analyzes each element of its collaborative agreements and considers a variety of factors in determining the appropriate method of revenue recognition of each element.

Prior to the adoption of ASU No. 2009-13 on January 1, 2011, in order for a delivered item to be accounted for separately from other deliverables in a multiple-element arrangement, the following three criteria had to be met: (i) the delivered item had standalone value to the customer, (ii) there was objective and reliable evidence of fair value of the undelivered items and (iii) if the arrangement included a general right of return relative to the delivered item, delivery or performance of the undelivered items was considered probable and substantially in the control of the vendor. For the collaborative agreements entered into prior to January 1, 2011, there was no objective and reliable evidence of fair value of the undelivered items. Thus, the delivered licenses did not meet all of the required criteria to be accounted for separately from undelivered items. Therefore, the Company recognizes revenue on nonrefundable upfront payments and license fees from these collaborative agreements over the period of significant involvement under the related agreements.

For new collaborative agreements or material modifications of existing collaborative agreements entered into after December 31, 2010, the Company follows the provisions of ASU No. 2009-13. In order to account for the multiple-element arrangements, the Company identifies the deliverables included within the agreement and evaluates which deliverables represent units of accounting. Analyzing the arrangement to identify deliverables requires the use of judgment, and each deliverable may be an obligation to deliver services, a right or license to use an asset, or another performance obligation. The deliverables under the Company’s collaborative agreements include (i) the license to the Company’s rHuPH20 technology, (ii) at the collaborator’s request, research and development services which are reimbursed at contractually determined rates, and (iii) at the collaborator’s request, supply of rHuPH20 API which is reimbursed at the Company’s cost plus a margin. A delivered item is considered a separate unit of accounting when the delivered item has value to the collaborator on a standalone basis based on the consideration of the relevant facts and circumstances for each arrangement. Factors considered in this determination include the research capabilities of the collaborator and the availability of research expertise in this field in the general marketplace.

Arrangement consideration is allocated at the inception of the agreement to all identified units of accounting based on their relative selling price. The relative selling price for each deliverable is determined using vendor specific objective evidence (“VSOE”), of selling price or third-party evidence of selling price if VSOE does not exist. If neither VSOE nor third-party evidence of selling price exists, the Company uses its best estimate of the selling price for the deliverable. The amount of allocable arrangement consideration is limited to amounts that are fixed or determinable. The consideration received is allocated among the separate units of accounting, and the applicable revenue recognition criteria are applied to each of the separate units. Changes in the allocation of the sales price between delivered and undelivered elements can impact revenue recognition but do not change the total revenue recognized under any agreement.

8

Table of Contents

Upfront license fee payments are recognized upon delivery of the license if facts and circumstances dictate that the license has standalone value from the undelivered items, which generally include research and development services and the manufacture of rHuPH20 API, the relative selling price allocation of the license is equal to or exceeds the upfront license fee, persuasive evidence of an arrangement exists, the Company’s price to the collaborator is fixed or determinable, and collectability is reasonably assured. Upfront license fee payments are deferred if facts and circumstances dictate that the license does not have standalone value. The determination of the length of the period over which to defer revenue is subject to judgment and estimation and can have an impact on the amount of revenue recognized in a given period.

The terms of the Company’s collaborative agreements provide for milestone payments upon achievement of certain development and regulatory events and/or specified sales volumes of commercialized products by the collaborator. Prior to the Company’s adoption of the Milestone Method, the Company recognized milestone payments upon the achievement of specified milestones if: (1) the milestone was substantive in nature and the achievement of the milestone was not reasonably assured at the inception of the agreement, (2) the fees were nonrefundable and (3) the Company’s performance obligations after the milestone achievement would continue to be funded by the Company’s collaborator at a level comparable to the level before the milestone achievement.

Effective January 1, 2011, the Company adopted on a prospective basis the Milestone Method. Under the Milestone Method, the Company recognizes consideration that is contingent upon the achievement of a milestone in its entirety as revenue in the period in which the milestone is achieved only if the milestone is substantive in its entirety. A milestone is considered substantive when it meets all of the following criteria:

| 1. | The consideration is commensurate with either the entity’s performance to achieve the milestone or the enhancement of the value of the delivered item(s) as a result of a specific outcome resulting from the entity’s performance to achieve the milestone, |

| 2. | The consideration relates solely to past performance, and |

| 3. | The consideration is reasonable relative to all of the deliverables and payment terms within the arrangement. |

A milestone is defined as an event (i) that can only be achieved based in whole or in part on either the entity’s performance or on the occurrence of a specific outcome resulting from the entity’s performance, (ii) for which there is substantive uncertainty at the date the arrangement is entered into that the event will be achieved and (iii) that would result in additional payments being due to the Company.

Reimbursements of research and development services are recognized as revenue during the period in which the services are performed as long as there is persuasive evidence of an arrangement, the fee is fixed or determinable and collection of the related receivable is probable. Revenue from the manufacture of rHuPH20 API is recognized when the API has met all specifications required for the collaborator acceptance and title and risk of loss have transferred to the collaborator. The Company does not directly control when any collaborator will request research and development services or supply of rHuPH20 API; therefore, the Company cannot predict when it will recognize revenues in connection with research and development services and supply of rHuPH20 API. Royalties to be received based on sales of licensed products by the Company’s collaborators incorporating the Company’s rHuPH20 API will be recognized as earned.

The collaborative agreements typically provide the collaborators the right to terminate such agreement in whole or on a product-by-product or target-by-target basis at any time upon 90 days prior written notice to the Company. There are no performance, cancellation, termination or refund provisions in any of the Company’s collaborative agreements that contain material financial consequences to the Company.

See Note 3, “Collaborative Agreements,” and Note 7, “Deferred Revenue,” for further discussion.

Cost of Product Sales

Cost of product sales consists primarily of raw materials, third-party manufacturing costs, fill and finish costs and freight costs associated with the sales of API for ICSI Cumulase and API for Hylenex recombinant. Cost of product sales also consists of the write-down of obsolete inventory.

9

Table of Contents

Research and Development Expenses

Research and development expenses include salaries and benefits, facilities and other overhead expenses, external clinical trials, research-related manufacturing services, contract services and other outside expenses. Research and development expenses are charged to operations as incurred when these expenditures relate to the Company’s research and development efforts and have no alternative future uses. Advance payments, including nonrefundable amounts, for goods or services that will be used or rendered for future research and development activities are deferred and capitalized. Such amounts will be recognized as an expense as the related goods are delivered or the related services are performed or such time when the Company does not expect the goods to be delivered or services to be performed.

Milestone payments that the Company makes in connection with in-licensed technology or product candidates are expensed as incurred when there is uncertainty in receiving future economic benefits from the in-licensed technology or product candidates. The Company considers the future economic benefits from the in-licensed technology or product candidates to be uncertain until such in-licensed technology or product candidates are approved for marketing by the FDA or comparable regulatory agencies in foreign countries or when other significant risk factors are abated. Management has viewed future economic benefits for all of the Company’s in-licensed technology or product candidates to be uncertain and has expensed these amounts for accounting purposes.

Clinical Trial Expenses

Expenses related to clinical trials are accrued based on the Company’s estimates and/or representations from service providers regarding work performed, including actual level of patient enrollment, completion of patient studies and clinical trials progress. Other incidental costs related to patient enrollment or treatment are accrued when reasonably certain. If the contracted amounts are modified (for instance, as a result of changes in the clinical trial protocol or scope of work to be performed), the Company modifies its accruals accordingly on a prospective basis. Revisions in the scope of a contract are charged to expense in the period in which the facts that give rise to the revision become reasonably certain. Historically, the Company has had no material changes in its clinical trial expense accruals that would have had a material impact on its consolidated results of operations or financial position.

Share-Based Compensation

Share-based compensation expense is measured at the grant date, based on the estimated fair value of the award, and is recognized as expense, net of estimated forfeitures, over the employee’s requisite service period. Total share-based compensation expense related to all of the Company’s share-based awards was allocated as follows:

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Research and development |

$ | 890,276 | $ | 691,266 | $ | 1,944,552 | $ | 2,049,134 | ||||||||

| Selling, general and administrative |

867,083 | 634,424 | 1,971,777 | 1,696,842 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Share-based compensation expense |

$ | 1,757,359 | $ | 1,325,690 | $ | 3,916,329 | $ | 3,745,976 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Share-based compensation expense per basic and diluted share |

$ | 0.02 | $ | 0.01 | $ | 0.04 | $ | 0.04 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Share-based compensation expense from: |

||||||||||||||||

| Stock options |

$ | 806,078 | $ | 1,035,496 | $ | 2,318,728 | $ | 3,131,890 | ||||||||

| Restricted stock awards and restricted stock units |

951,281 | 290,194 | 1,597,601 | 614,086 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | 1,757,359 | $ | 1,325,690 | $ | 3,916,329 | $ | 3,745,976 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

10

Table of Contents

Since the Company has a net operating loss carryforward as of September 30, 2011, no excess tax benefits for the tax deductions related to share-based awards were recognized in the interim unaudited condensed consolidated statements of operations. For the three months ended September 30, 2011 and 2010, employees exercised stock options to purchase 38,511 and 73,112 shares of common stock, respectively, for aggregate proceeds of approximately $79,000 and $240,000, respectively. For the nine months ended September 30, 2011 and 2010, employees exercised stock options to purchase 2,713,573 and 281,654 shares of common stock, respectively, for aggregate proceeds of approximately $4.1 million and $737,000, respectively.

As of September 30, 2011, total unrecognized estimated compensation cost related to non-vested stock options and non-vested restricted stock awards and restricted stock units granted prior to that date was approximately $6.2 million, and $1.8 million, respectively, which is expected to be recognized over a weighted-average period of approximately 2.5 years and eight months, respectively.

In May 2011, the Company’s stockholders approved the Company’s 2011 Stock Plan, which provides for the granting of up to a total of 6,000,000 shares of common stock (subject to certain limitations as described in the 2011 Stock Plan) to selected employees, consultants and non-employee members of the Company’s Board of Directors (“Outside Directors”) as stock options, stock appreciation rights, restricted stock awards (“RSAs”), restricted stock unit awards (“RSUs”) and performance awards. The 2011 Stock Plan is being utilized for the initial equity awards for new hires of the Company as well as for annual and performance equity awards for existing employees. Options granted under the 2011 Stock Plan generally have a 10-year term and vest at the rate of one-fourth of the shares on the first anniversary of the date of grant and 1/48 of the shares monthly thereafter. As of September 30, 2011, 5.4 million shares were available for future grants of share-based awards under the 2011 Stock Plan.

The 2011 Stock Plan replaced the Company’s prior stock plans, consisting of the Company’s 2008 Stock Plan, 2006 Stock Plan and 2004 Stock Plan (“Prior Plans”). The Prior Plans were terminated such that no additional awards could be granted thereunder but the terms of the Prior Plans remain in effect with respect to outstanding awards until they are exercised, settled, forfeited or otherwise canceled in full.

Comprehensive Income (Loss)

Comprehensive income (loss) is defined as the change in equity during a period from transactions and other events and circumstances from non-owner sources. Comprehensive income (loss) was the same as the Company’s net income (loss) for the reporting periods.

Fair Value Measurements

The Company follows the authoritative guidance for fair value measurements and disclosures which, among other things, defines fair value, establishes a consistent framework for measuring fair value and expands disclosure for each major asset and liability category measured at fair value on either a recurring or nonrecurring basis. Fair value is defined as an exit price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. As such, fair value is a market-based measurement that should be determined based on assumptions that market participants would use in pricing an asset or liability.

The framework for measuring fair value provides a hierarchy that prioritizes the inputs to valuation techniques used in measuring fair value as follows:

| Level 1 |

Quoted prices (unadjusted) in active markets for identical assets or liabilities; | |

| Level 2 |

Inputs other than quoted prices included within Level 1 that are either directly or indirectly observable; and | |

| Level 3 |

Unobservable inputs in which little or no market activity exists, therefore requiring an entity to develop its own assumptions about the assumptions that market participants would use in pricing. | |

11

Table of Contents

Cash equivalents of approximately $65.0 million and $79.8 million at September 30, 2011 and December 31, 2010, respectively, are carried at fair value and are classified within Level 1 of the fair value hierarchy because they are valued based on quoted market prices for identical securities. The Company has no instruments that are classified within Level 2 or Level 3.

| 3. | Collaborative Agreements |

Roche Partnership

In December 2006, the Company and Roche entered into the Roche Partnership, under which Roche obtained a worldwide, exclusive license to develop and commercialize product combinations of rHuPH20 and up to thirteen Roche target compounds resulting from the partnership. Under the terms of the Roche Partnership, Roche paid $20.0 million as an initial upfront license fee for the application of rHuPH20 to three pre-defined Roche biologic targets. Due to the Company’s continuing involvement obligations (for example, support activities associated with rHuPH20 enzyme), revenues from the upfront payment, exclusive designation fees and annual license maintenance fees were deferred and are being recognized over the term of the Roche Partnership. Roche may pay the Company further payments which could potentially reach a value of up to $111.0 million for the initial three exclusive targets dependent upon the achievement of specified clinical, regulatory and sales-based milestones.

Under the terms of the Roche Partnership, Roche will also pay the Company royalties on product sales for these first three targets. Through September 30, 2011, Roche has elected two additional exclusive targets. In 2010, Roche did not pay the annual license maintenance fee on five target slots. As a result, Roche has an option to select only three additional targets under the Roche Partnership, provided that Roche continues to pay annual exclusivity maintenance fees to the Company. For each of the additional five targets, Roche may pay the Company further upfront and milestone payments of up to $47.0 million per target, as well as royalties on product sales for each of these additional five targets. Additionally, Roche will obtain access to the Company’s expertise in developing and applying rHuPH20 to Roche targets. Under the terms of the Roche Partnership, the Company was obligated to scale up the production of rHuPH20 and to identify a second source manufacturer that would help meet anticipated production obligations arising from the Roche Partnership.

The Company has determined that the clinical and regulatory milestones are substantive; therefore, the Company expects to recognize such clinical and regulatory milestone payments as revenue upon achievement of the milestones. Given the challenges inherent in developing and obtaining approval for pharmaceutical and biologic products, there was substantive uncertainty whether any of the clinical and regulatory milestones would be achieved at the time the Roche Partnership was entered into. In addition, the Company has determined that the sales-based milestone payments are similar to royalty payments; therefore, the Company will recognize such sales-based milestone payments as revenue upon achievement of the milestones. In the three and nine months ended September 30, 2011, the Company recognized zero and $5.0 million, respectively, as revenue under collaborative agreements in accordance with the Milestone Method related to the achievement of certain clinical milestones pursuant to the terms of the Roche Partnership.

Gammagard Partnership

In September 2007, the Company entered into the Gammagard Partnership with Baxter, under which Baxter obtained a worldwide, exclusive license to develop and commercialize product combinations of rHuPH20, with a current Baxter product, GAMMAGARD LIQUID. Under the terms of the Gammagard Partnership, Baxter paid the Company a nonrefundable upfront payment of $10.0 million. Due to the Company’s continuing involvement obligations (for example, support activities associated with rHuPH20 enzyme), the $10.0 million upfront payment was deferred and is being recognized over the term of the Gammagard Partnership. Baxter may make further milestone payments totaling $37.0 million to the Company upon the achievement of regulatory approval for the licensed product candidate and specified sales volumes of commercialized product by Baxter. In addition, Baxter will pay royalties on the sales, if any, of the product that result from the collaboration. The Gammagard Partnership is applicable to both kit and formulation combinations. Baxter assumes all development, manufacturing, clinical, regulatory, sales and marketing costs under the Gammagard Partnership, while the Company is responsible for the supply of rHuPH20 enzyme. The Company performs research and development activities at the request of Baxter, which are reimbursed by Baxter under the terms of the Gammagard Partnership.

12

Table of Contents

In addition, Baxter has certain product development and commercialization obligations in major markets identified in the Gammagard Partnership.

The Company has determined that the regulatory milestones are substantive; therefore, the Company expects to recognize such regulatory milestone payments as revenue upon achievement of such milestones. Given the challenges inherent in developing and obtaining approval for pharmaceutical and biologic products, there was substantive uncertainty whether any of the regulatory events would be achieved at the time the Gammagard Partnership was entered into. In addition, the Company has determined that sales-based milestone payments are similar to royalty payments and, therefore, will be recognized as revenue upon achievement of the milestones. In the three and nine months ended September 30, 2011, the Company recognized zero and $3.0 million, respectively, as revenue under collaborative agreements in accordance with the Milestone Method related to the achievement of regulatory milestones pursuant to the terms of the Gammagard Partnership.

ViroPharma and Intrexon Partnerships

Effective May 10, 2011, the Company and ViroPharma entered into a collaboration and license agreement “ViroPharma Partnership”, under which ViroPharma obtained a worldwide exclusive license for the use of rHuPH20 enzyme in the development of a subcutaneous injectable formulation of ViroPharma’s commercialized product, Cinryze® (C1 esterase inhibitor [human]). In addition, the license provides ViroPharma with exclusivity to C1 esterase inhibition and to the Hereditary Angioedema, along with three additional orphan indications. Under the terms of the ViroPharma Partnership, ViroPharma paid a nonrefundable license fee of $9.0 million. In addition, the Company is entitled to receive an annual exclusivity fee of $1.0 million commencing on May 10, 2012 and on each anniversary of the effective date of the agreement thereafter until a certain development event occurs. ViroPharma is solely responsible for the development, manufacturing and marketing of any products resulting from this partnership. The Company is entitled to receive payments for research and development services and supply of rHuPH20 API if requested by ViroPharma. In addition, the Company is entitled to receive additional cash payments potentially totaling $44.0 million for a product for treatment of Hereditary Angioedema and $10.0 million for each product for treatment of each of three additional orphan indications upon achievement of development and regulatory milestones. The Company is also entitled to receive royalties on future product sales by ViroPharma. ViroPharma may terminate the agreement prior to expiration for any reason on a product-by-product basis upon 90 days’ prior written notice to the Company. Upon any such termination, the license granted to ViroPharma (in total or with respect to the terminated product, as applicable) will terminate and revert to the Company.

Effective June 6, 2011, the Company and Intrexon entered into a collaboration and license agreement “Intrexon Partnership”, under which Intrexon obtained a worldwide exclusive license for the use of rHuPH20 enzyme in the development of a subcutaneous injectable formulation of Intrexon’s recombinant human alpha 1-antitrypsin (rHuA1AT). Under the terms of the Intrexon Partnership, Intrexon paid a nonrefundable upfront license fee of $9.0 million. In addition, the Company is entitled to receive an annual exclusivity fee of $1.0 million commencing on June 6, 2012 and on each anniversary of the effective date of the agreement thereafter until a certain development event occurs. Intrexon is solely responsible for the development, manufacturing and marketing of any products resulting from this partnership. The Company is entitled to receive payments for research and development services and supply of rHuPH20 API if requested by Intrexon. In addition, the Company is entitled to receive additional cash payments potentially totaling $44.0 million for each product for use in the exclusive field and $10 million for each product for use in the non-exclusive field upon achievement of development and regulatory milestones. The Company is also entitled to receive escalating royalties on product sales and a cash payment of $10.0 million upon achievement of a specified sales volume of product sales by Intrexon. Intrexon may terminate the agreement prior to expiration for any reason on a product-by-product basis upon 90 days’ prior written notice to the Company. Upon any such termination, the license granted to Intrexon (in total or with respect to the terminated product, as applicable) will terminate and revert to the Company. Intrexon’s chief executive officer and chairman of its board of directors is also a member of the Company’s board of directors.

In accordance with ASU No. 2009-13, the Company identified the deliverables at the inception of the ViroPharma and Intrexon agreements which are the license, research and development services and API supply. The Company has determined that the license, research and development services and API supply individually represent separate units of accounting, because each deliverable has standalone value. The estimated selling prices for these units of accounting was determined based on market conditions, the terms of comparable collaborative arrangements for similar technology in the pharmaceutical and biotech industry and entity-specific factors such as the terms of the

13

Table of Contents

Company’s previous collaborative agreements, the Company’s pricing practices and pricing objectives and the nature of the research and development services to be performed for the partners. The arrangement consideration was allocated to the deliverables based on the relative selling price method. Based on the results of the Company’s analysis, the Company determined that the upfront payment was earned upon the granting of the worldwide, exclusive right to the Company’s technology to the collaborator in both the ViroPharma Partnership and Intrexon Partnership. However, the amount of allocable arrangement consideration is limited to amounts that are fixed or determinable; therefore, the amount allocated to the license was only to the extent of cash received. As a result, the Company recognized the $9.0 million upfront license fee received under the ViroPharma Partnership and the $9.0 million upfront license fee received under the Intrexon Partnership as revenues under collaborative agreements upon receipt of the upfront license fees in the quarter ended June 30, 2011.

The Company will recognize the exclusivity fees as revenues under collaborative agreements when they are earned. The Company will recognize reimbursements for research and development services as revenues under collaborative agreements as the related services are delivered. The Company will recognize revenue from sales of API as revenues under collaborative agreements when such API has met all required specifications by the partners and the related title and risk of loss and damages have passed to the partners. The Company cannot predict the timing of delivery of research and development services and API as they are at the partners’ requests.

The Company is eligible to receive additional cash payments upon the achievement by the partners of specified development, regulatory and sales-based milestones. The Company has determined that each of the development and regulatory milestones is substantive; therefore, the Company expects to recognize such development and regulatory milestone payments as revenues under collaborative agreements upon achievement in accordance with the Milestone Method. Given the challenges inherent in developing and obtaining approval for pharmaceutical and biologic products, there was substantive uncertainty whether any of the development and regulatory milestones would be met at the time these partnerships were entered into, and the milestones are based in part on the occurrence of a separate outcome resulting from the Company’s performance. In addition, the Company has determined that the sales-based milestone payment is similar to a royalty payment; therefore, the Company will recognize the sales-based milestone payment as revenue upon achievement of the milestone because the Company has no future performance obligations associated with the milestone. In September 2011, ViroPharma announced the initiation of a Phase 2 clinical study to evaluate the safety, pharmacokinetics and pharmacodynamics of subcutaneous administration of Cinryze in combination with rHuPH20 in subjects with hereditary angioedema. As a result, in the three months ended September 30, 2011 the Company recognized a $3.0 million milestone payment from ViroPharma as revenue under collaborative agreements in accordance with the Milestone Method related to the achievement of this development milestone pursuant to the terms of the ViroPharma Partnership.

| 4. | Inventory |

Inventory at September 30, 2011 consists of approximately $77,000 in raw materials used in the manufacture of ICSI Cumulase products and approximately $26,000 in work-in-process inventory for Hylenex recombinant. Inventory at December 31, 2010 consists of raw materials used in the manufacture of the Company’s Hylenex recombinant and ICSI Cumulase products. As of December 31, 2010, the reserve for Hylenex recombinant API inventory obsolescence was approximately $875,000. There was no such reserve as of September 30, 2011.

| 5. | Property and Equipment |

Property and equipment, net consists of the following:

| September 30, 2011 |

December 31, 2010 |

|||||||

| Research equipment |

$ | 4,534,207 | $ | 4,308,654 | ||||

| Computer and office equipment |

1,243,448 | 1,215,894 | ||||||

| Leasehold improvements |

1,002,912 | 998,368 | ||||||

|

|

|

|

|

|||||

| 6,780,567 | 6,522,916 | |||||||

| Accumulated depreciation and amortization |

(5,505,814) | (4,676,017) | ||||||

|

|

|

|

|

|||||

| $ | 1,274,753 | $ | 1,846,899 | |||||

|

|

|

|

|

|||||

14

Table of Contents

Depreciation and amortization expense totaled approximately $239,000 and $365,000 for the three months ended September 30, 2011 and 2010, respectively, and approximately $852,000 and $1.2 million for the nine months ended September 30, 2011 and 2010, respectively.

| 6. | Accrued Expenses |

Accrued expenses consist of the following:

| September 30, 2011 |

December 31, 2010 |

|||||||

| Accrued outsourced research and development expenses |

$ | 6,077,588 | $ | 3,647,762 | ||||

| Accrued compensation and payroll taxes |

2,182,913 | 3,045,950 | ||||||

| Accrued expenses |

604,204 | 1,911,857 | ||||||

|

|

|

|

|

|||||

| $ | 8,864,705 | $ | 8,605,569 | |||||

|

|

|

|

|

|||||

| 7. | Deferred Revenue |

Deferred revenue consists of the following:

| September 30, 2011 |

December 31, 2010 |

|||||||

| Collaborative agreements |

$ | 40,375,240 | $ | 48,761,361 | ||||

| Product sales |

- | 9,332,190 | ||||||

|

|

|

|

|

|||||

| Total deferred revenue |

40,375,240 | 58,093,551 | ||||||

| Less current portion |

3,707,795 | 2,917,129 | ||||||

|

|

|

|

|

|||||

| Deferred revenue, net of current portion |

$ | 36,667,445 | $ | 55,176,422 | ||||

|

|

|

|

|

|||||

Roche Partnership - In December 2006, the Company and Roche entered into the Roche Partnership under which Roche obtained a worldwide, exclusive license to develop and commercialize product combinations of rHuPH20and up to thirteen Roche target compounds. Under the terms of the Roche Partnership, Roche paid $20.0 million to the Company in December 2006 as an initial upfront payment for the application of rHuPH20 to three pre-defined Roche biologic targets. Through September 30, 2011, Roche has paid an aggregate of $19.25 million in connection with Roche’s election of two additional exclusive targets and annual license maintenance fees for the right to designate the remaining targets as exclusive targets. In 2010, Roche did not pay the annual license maintenance fees on five of the remaining eight target slots. As a result, Roche currently retains the option to exclusively develop and commercialize rHuPH20 with three additional targets through the payment of annual license maintenance fees.

Due to the Company’s continuing involvement obligations (for example, support activities associated with rHuPH20 enzyme), revenues from the upfront payment, exclusive designation fees and annual license maintenance fees were deferred and are being recognized over the term of the Roche Partnership. The Company recognized revenue from the upfront payment, exclusive designation fees and annual license maintenance fees under the Roche Partnership in the amounts of approximately $491,000 and $458,000 for the three months ended September 30, 2011 and 2010, respectively, and approximately $1.5 million for the nine months ended September 30, 2011 and 2010. Deferred revenue relating to the upfront payment, exclusive designation fees and annual license maintenance fees under the Roche Partnership was $31.4 million and $32.9 million as of September 30, 2011 and December 31, 2010, respectively.

Baxter Partnerships - In September 2007, the Company and Baxter entered into the Gammagard Partnership, under which Baxter obtained a worldwide, exclusive license to develop and commercialize product combinations of rHuPH20 with GAMMAGARD LIQUID. Under the terms of the Gammagard Partnership, Baxter paid the Company a nonrefundable upfront payment of $10.0 million. Due to the Company’s continuing involvement obligations (for example, support activities associated with rHuPh20 enzyme), the $10.0 million upfront payment was deferred and is being recognized over the term of the Gammagard Partnership. The Company recognized revenue from the upfront payment under the Gammagard Partnership in the amounts of approximately

15

Table of Contents

$121,000 for the three months ended September 30, 2011 and 2010 and approximately $362,000 and $400,000 for the nine months ended September 30, 2011 and 2010, respectively. Deferred revenue relating to the upfront payment under the Gammagard Partnership was $7.7 million and $8.1 million as of September 30, 2011 and December 31, 2010, respectively.

In February 2007, the Company and Baxter amended certain existing agreements for Hylenex recombinant and entered into the Hylenex Partnership for kits and formulations with rHuPH20. Under the terms of the Hylenex Partnership, Baxter paid the Company a nonrefundable upfront payment of $10.0 million. In addition, Baxter would make payments to the Company based on sales of the products covered under the Hylenex Partnership. Baxter had prepaid nonrefundable product-based payments totaling $10.0 million in connection with the execution of the Hylenex Partnership. Due to the Company’s continuing involvement obligations (for example, support activities associated with rHuPh20 enzyme), the $10.0 million upfront payment was initially deferred and was being recognized over the term of the Hylenex Partnership. The prepaid product-based payments were also deferred and were being recognized as product sales revenues as the Company earned such revenues from the sales of Hylenex recombinant by Baxter.

Effective January 7, 2011, the Company and Baxter mutually agreed to terminate the Hylenex Partnership and the associated agreements. The termination of these agreements does not affect the other relationships between the parties, including the application of the Company’s Enhanze Technology to Baxter’s GAMMAGARD LIQUID.

On July 18, 2011, the Company and Baxter entered into an agreement (the “Transition Agreement”) setting forth certain rights, data and assets to be transferred by Baxter to the Company during a transition period. Effective July 18, 2011, the Company has no future performance obligations to Baxter in connection with the Hylenex Partnership. Therefore, the Company recognized the unamortized deferred revenue of approximately $9.3 million relating to the prepaid product-based payments and the unamortized deferred revenue of approximately $7.6 million relating to deferred upfront payment from the Hylenex Partnership as revenues under collaborative agreements for the three months ended September 30, 2011. For the three months ended September 30, 2010, the Company recognized revenues under the Hylenex Partnership from the upfront payment in the amounts of approximately $117,000. No revenue relating to the prepaid product-based payments was recognized for the three months ended September 30, 2010. For the nine months ended September 30, 2011 and 2010, the Company recognized revenues under the Hylenex Partnership from the upfront payment in the amounts of approximately $7.8 million and $387,000, respectively, and from the product-based payments in the amounts of approximately $9.3 million and $332,000, respectively. Deferred revenues relating to the upfront payment and product-based payments under the Hylenex Partnership was $7.8 million and $9.3 million at December 31, 2010. There were no deferred revenues relating to the Hylenex Partnership at September 30, 2011.

In addition, pursuant to the terms of the Transition Agreement, Baxter no longer has the right to return the Hylenex recombinant API previously delivered to Baxter. Accordingly, the Company recognized approximately $991,000 of deferred revenue related to such Hylenex recombinant API as product sales revenue during the three months ended September 30, 2011.

| 8. | Net Income (Loss) Per Share |

Basic net income (loss) per common share (“EPS”) is computed by dividing net income (loss) for the period by the weighted-average number of common shares outstanding during the period, without consideration for common stock equivalents. Diluted net income (loss) per common share is computed by dividing net income (loss) for the period by the weighted-average number of common shares outstanding and potentially dilutive common shares outstanding. Dilutive potential common shares outstanding, determined using the treasury stock method, principally include: shares that may be issued under the Company’s stock options, RSAs and RSUs. For the three months ended September 30, 2011 and 2010, the Company has excluded approximately 1.9 million and 8.6 million shares, respectively, of stock options, unvested RSAs and unvested RSUs from the computation of diluted EPS because their impact would have been anti-dilutive. For the nine months ended September 30, 2011 and 2010, the Company has excluded approximately 5.9 million and 8.6 million shares of stock options, unvested RSAs and unvested RSUs from the computation of diluted EPS as their impact would have been anti-dilutive because of the Company’s net loss in these reporting periods.

16

Table of Contents

The following table sets forth the computation of basic and diluted EPS:

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Net Income (Loss) — Numerator: |

||||||||||||||||

| Net income (loss) for basic and diluted EPS |

$ | 5,165,193 | $ | (12,409,576) | $ | (1,354,237) | $ | (36,347,976) | ||||||||

| Shares — Denominator: |

||||||||||||||||

| Weighted-average shares for basic EPS |

103,223,352 | 93,626,893 | 102,282,904 | 92,342,665 | ||||||||||||

| Effect of dilutive options, RSAs and RSUs |

1,785,837 | - | - | - | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted-average shares for diluted EPS |

105,009,189 | 93,626,893 | 102,282,904 | 92,342,665 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic and diluted net income (loss) per share |

$ | 0.05 | $ | (0.13) | $ | (0.01) | $ | (0.39) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 9. | Stockholders’ Equity |

During the nine months ended September 30, 2011 and 2010, the Company issued an aggregate of 2,713,573 and 281,654 shares of common stock, respectively, in connection with the exercises of stock options at a weighted average exercise price of $1.70 and $2.62 per share, respectively, for net proceeds of approximately $4.1 million and $737,000, respectively. During the nine months ended September 30, 2011 and 2010, the Company granted 353,508 and 120,000 RSAs, with a weighted average grant-date fair value of $6.51 and $7.67 per share, respectively. Options to purchase approximately 5.4 million and 8.0 million shares of the Company’s common stock were outstanding as of September 30, 2011 and December 31, 2010, respectively. RSUs to purchase 163,000 shares of the Company’s common stock were outstanding as of September 30, 2011. There were no RSUs outstanding as of December 31, 2010.

During the nine months ended September 30, 2010, the Company also issued 8.3 million shares of common stock in a public offering at a price of $7.25 per share, generating approximately $60.0 million in net proceeds. In connection with this financing, the Company granted to an underwriter an option to purchase 1,245,000 shares of common stock at a price of $7.25 per share. The option was exercisable in the event that the underwriter sold more than 8.3 million shares of common stock. The option expired unexercised in October 2010.

| 10. | Restructuring Liability |

In October 2010, the Company completed a corporate reorganization to focus its resources on advancing its core proprietary programs and supporting strategic alliances with Roche and Baxter. This reorganization resulted in a reduction in the workforce of approximately 25 percent primarily in the discovery research and preclinical areas. The restructuring liability was approximately $117,000 as of December 31, 2010 and was paid in full as of September 30, 2011.

| 11. | Commitments and Contingencies |

Operating Leases - The Company’s administrative offices and research facilities are located in San Diego, California. The Company leases an aggregate of approximately 58,000 square feet of office and research space.

17

Table of Contents

In July 2007, the Company entered into a lease agreement (the “Original Lease”) with BC Sorrento, LLC (“BC Sorrento”) for the facilities located at 11388 Sorrento Valley Road, San Diego, California (“11388 Property”) for 27,575 square feet of office and research space commencing in September 2008 through January 2013. Under the terms of the Original Lease, the initial monthly rent payment was approximately $37,000 net of costs and property taxes associated with the operation and maintenance of the leased facilities, commencing in September 2008 and increased to approximately $73,000 starting in March 2009. Thereafter, the annual base rent was subject to approximately 4% annual increases each year throughout the term of the Original Lease. In addition, the Company received a certain tenant improvement allowance and free rent under the terms of the Original Lease. Effective September 2010, BMR-11388 Sorrento Valley Road LP (“BMR-11388”) acquired the 11388 Property and became the new landlord of the 11388 Property.

In June 2011, the Company entered into an amended and restated lease (the “11388 Lease”) with BMR-11388 for the 11388 Property commencing from June 2011 through January 2018. The 11388 Lease superseded the Original Lease. Under the terms of the 11388 Lease, the initial monthly rent payment is approximately $38,000 net of costs and property taxes associated with the operation and maintenance of the leased facilities, commencing in December 2011 and increasing to approximately $65,000 starting in January 2013. Thereafter, the annual base rent is subject to approximately 2.5% annual increases each year throughout the term of the 11388 Lease. In addition, the Company received a cash incentive of approximately $98,000, a tenant improvement allowance of $300,000 and free and reduced rent totaling approximately $744,000. Combined with the unamortized deferred rent under the Original Lease, unamortized deferred rent associated with the 11388 Lease of $733,000 and $545,000 was included in deferred rent as of September 30, 2011 and December 31, 2010, respectively.

In July 2007, the Company entered into a sublease agreement (the “11404 Sublease”) with Avanir Pharmaceuticals, Inc. (“Avanir”) for Avanir’s excess leased facilities located at 11404 Sorrento Valley Road, San Diego, California for 21,184 square feet of office and research space (“11404 Property”) for a monthly rent payment of approximately $54,000, net of costs and property taxes associated with the operation and maintenance of the subleased facilities. The 11404 Sublease expires in January 2013. The annual base rent is subject to approximately 4% annual increases each year throughout the terms of the 11404 Sublease. In addition, the Company received free rent totaling approximately $492,000, of which approximately $182,000 and $266,000 was included in deferred rent as of September 30, 2011 and December 31, 2010, respectively.

In April 2009, the Company entered into a sublease agreement (the “11408 Sublease”) with Avanir for 9,187 square feet located at 11408 Sorrento Valley Road, San Diego, California for office and research space (“11408 Property”), which expires in January 2013. The monthly rent payments, which commenced in January 2010, were approximately $21,000 and are subject to an annual increase of approximately 3%. Under terms of the 11408 Sublease, the Company received a tenant improvement allowance of $75,000, of which approximately $34,000 and $49,000 was included in deferred rent at September 30, 2011 and December 31, 2010, respectively.

In June 2011, the Company entered into a lease agreement (the “11404/11408 Lease”) with BMR-Sorrento Plaza LLC (“BMR-Sorrento”) for the 11404 Property and 11408 Property commencing in January 2013 through January 2018. Pursuant to the terms of the 11404/11408 Lease, the initial monthly rent payment is approximately $71,000 net of costs and property taxes associated with the operation and maintenance of the leased facilities, commencing in January 2013 and is subject to approximately 2.5% annual increases each year throughout the term of the 11404/11408 Lease.

The Company pays a pro rata share of operating costs, insurance costs, utilities and real property taxes incurred by the landlords for the subleased facilities.

18

Table of Contents

Additionally, the Company leases certain office equipment under operating leases. Approximate annual future minimum operating lease payments as of September 30, 2011 are as follows:

| Operating Leases | ||||

| Three months ending December 31, 2011 |

$ | 287,000 | ||

| Twelve months ending December 31, 2012 |

1,470,000 | |||

| Twelve months ending December 31, 2013 |

1,654,000 | |||

| Twelve months ending December 31, 2014 |

1,677,000 | |||

| Twelve months ending December 31, 2015 |

1,715,000 | |||

| Twelve months ending December 31, 2016 |

1,758,000 | |||

| Thereafter |

1,870,000 | |||

|

|

|

|||

| Total minimum lease payments |

$ | 10,431,000 | ||

|

|

|

|||

Legal Contingencies - From time to time, the Company is involved in legal actions arising in the normal course of its business. The Company is not presently subject to any material litigation nor, to management’s knowledge, is any litigation threatened against the Company that collectively is expected to have a material adverse effect on the Company’s consolidated cash flows, financial condition or results of operations.

In May 2010, the Company delivered a notice of breach to Baxter due to Baxter’s failure to provide Hylenex recombinant in accordance with the terms of the Hylenex Partnership. Baxter had contested the claims made in the Company’s initial notice of breach and asserted their own breach claims against the Company. Pursuant to the terms of the Transition Agreement, signed on July 18, 2011, Baxter’s breach claims against the Company were discharged.

19

Table of Contents

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

As used in this report, unless the context suggests otherwise, the terms “we,” “our,” “ours,” and “us” refer to Halozyme Therapeutics, Inc., and its wholly owned subsidiary, Halozyme, Inc., which are sometimes collectively referred to herein as “the Company.”

The following information should be read in conjunction with the unaudited condensed consolidated financial statements and notes thereto included in Item 1 of this Quarterly Report on Form 10-Q. Past financial or operating performance is not necessarily a reliable indicator of future performance, and our historical performance should not be used to anticipate results or future period trends.

Except for the historical information contained herein, this report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements reflect management’s current forecast of certain aspects of our future. Words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “estimate,” “think,” “may,” “could,” “will,” “would,” “should,” “continue,” “potential,” “likely,” “opportunity” and similar expressions or variations of such words are intended to identify forward-looking statements, but are not the exclusive means of indentifying forward-looking statements in this report. Additionally, statements concerning future matters such as the development or regulatory approval of new products, enhancements of existing products or technologies, third party performance under key collaboration agreements, revenue and expense levels and other statements regarding matters that are not historical are forward-looking statements. Such statements are based on currently available operating, financial and competitive information and are subject to various risks, uncertainties and assumptions that could cause actual results to differ materially from those anticipated or implied in our forward-looking statements due to a number of factors including, but not limited to, those set forth below under the section entitled “Risks Factors” and elsewhere in this Quarterly Report on Form 10-Q and our most recent Annual Report on Form 10-K.

Overview

We are a biopharmaceutical company dedicated to the development and commercialization of recombinant human enzymes that either transiently modify tissue under the skin to facilitate injection of other therapies or correct diseased tissue structures for clinical benefit. Our existing products and our products under development are based primarily on intellectual property covering the family of human enzymes known as hyaluronidases. Hyaluronidases are enzymes (proteins) that break down hyaluronan, or HA, which is a naturally occurring space-filling, gel-like substance that is a major component of both normal tissues throughout the body, such as skin and cartilage, and abnormal tissues such as tumors. Our primary technology, Enhanze™, is a proprietary delivery platform using our first approved recombinant human PH20 enzyme, or rHuPH20, a human synthetic version of hyaluronidase. rHuPH20 is a naturally occurring enzyme that temporarily degrades HA, thereby facilitating the penetration and diffusion of other drugs and fluids that are injected under the skin or in the muscle. Our proprietary rHuPH20 technology is applicable to multiple therapeutic areas and may be used to both expand existing markets and create new ones through the development of our own proprietary products. Through partnerships or other collaborations, the rHuPH20 technology may also be applied to existing and developmental products of biopharmaceutical companies that market drugs requiring or benefiting from injection via the subcutaneous route of administration.

Our operations to date have involved: (i) organizing and staffing our operating subsidiary, Halozyme, Inc.; (ii) acquiring, developing and securing our technology; (iii) undertaking product development for our existing products and a limited number of product candidates; and (iv) supporting the development of partnered product candidates. We continue to increase our focus on our proprietary product pipeline and have expanded investments in our proprietary product candidates. We currently have multiple proprietary programs in various stages of research and development. In addition, we currently have collaborative partnerships with F. Hoffmann-La Roche, Ltd and Hoffmann-La Roche, Inc., or Roche, Baxter Healthcare Corporation, or Baxter, ViroPharma Incorporated, or ViroPharma, and Intrexon Corporation, or Intrexon, to apply Enhanze™ Technology to the partners’ biological therapeutic compounds. We also had another partnership with Baxter, under which Baxter had worldwide marketing rights for our marketed product, Hylenex® recombinant (hyaluronidase human injection), or Hylenex Partnership. Hylenex recombinant is a recombinant formulation of hyaluronidase that has received the approval from the U.S. Food and Drug Administration, or FDA, to facilitate subcutaneous fluid administration for achieving hydration; to increase the dispersion and absorption of other injected drugs; and in subcutaneous urography for improving

20

Table of Contents

resorption of radiopaque agents. We and Baxter mutually agreed to terminate the Hylenex Partnership in January 2011. Our rHuPH20 technology is also being used in ICSI Cumulase®, a third party’s marketed product used for in vitro fertilization, or IVF. Currently, we have received only limited revenue from the sales of active pharmaceutical ingredients, or API, to the third party that produces ICSI Cumulase, in addition to other revenues from our partnerships.

In February 2007, we and Baxter amended certain existing agreements relating to Hylenex recombinant and entered into the Hylenex Partnership for kits and formulations with rHuPH20. In October 2009, Baxter commenced the commercial launch of Hylenex recombinant. Hylenex recombinant was voluntarily recalled in May 2010, because a portion of the Hylenex recombinant manufactured by Baxter was not in compliance with the requirements of the underlying Hylenex recombinant agreements. During the second quarter of 2011, we submitted the data that the FDA had requested to support the reintroduction of Hylenex recombinant. The FDA has approved the submitted data and has granted the reintroduction of Hylenex recombinant. We expect to reintroduce Hylenex recombinant by the end of 2011.