Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PNC FINANCIAL SERVICES GROUP, INC. | d250118d8k.htm |

The PNC

Financial Services Group, Inc. BancAnalysts Association of Boston

November 3, 2011

Exhibit 99.1 |

2

DRAFT

Cautionary Statement Regarding Forward-Looking

Information and Adjusted Information

This

presentation

includes

“snapshot”

information

about

PNC

used

by

way

of

illustration.

It

is

not

intended

as

a

full

business

or

financial

review

and

should

be

viewed

in

the

context

of

all

of

the

information

made

available

by

PNC

in

its

SEC

filings.

The

presentation

also

contains

forward-looking

statements

regarding

our

outlook

for

earnings,

revenues,

expenses,

capital

levels,

liquidity

levels,

asset

levels,

asset

quality

and

other

matters

regarding

or

affecting

PNC

and

its

future

business

and

operations.

Forward-looking

statements

are

necessarily

subject

to

numerous

assumptions,

risks

and

uncertainties,

which

change

over

time.

The

forward-looking

statements

in

this

presentation

are

qualified

by

the

factors

affecting

forward-looking

statements

identified

in

the

more

detailed

Cautionary

Statement

included

in

the

Appendix,

which

is

included

in

the

version

of

the

presentation

materials

posted

on

our

corporate

website

at

www.pnc.com/investorevents.

We

provide

greater

detail

regarding

some

of

these

factors

in

our

2010

Form

10-K

and

2011

Form

10-Qs,

including

in

the

Risk

Factors

and

Risk

Management

sections

of

those

reports,

and

in

our

subsequent

SEC

filings.

Our

forward-looking

statements

may

also

be

subject

to

other

risks

and

uncertainties,

including

those

we

may

discuss

in

this

presentation

or

in

SEC

filings,

accessible

on

the

SEC’s

website

at

www.sec.gov

and

on

PNC’s

corporate

website

at

www.pnc.com/secfilings.

We

have

included

web

addresses

in

this

presentation

as

inactive

textual

references

only.

Information

on

these

websites

is

not

part

of

this

presentation.

Future

events

or

circumstances

may

change

our

outlook

and

may

also

affect

the

nature

of

the

assumptions,

risks

and

uncertainties

to

which

our

forward-looking

statements

are

subject.

Forward-looking

statements

in

this

presentation

speak

only

as

of

the

date

of

this

presentation.

We

do

not

assume

any

duty

and

do

not

undertake

to

update

those

statements.

Actual

results

or

future

events

could

differ,

possibly

materially,

from

those

anticipated

in

forward-looking

statements,

as

well

as

from

historical

performance.

In

this

presentation,

we

sometimes

refer

to

adjusted

results

to

help

illustrate

the

impact

of

certain

types

of

items.

This

information

supplements

our

results

as

reported

in

accordance

with

GAAP

and

should

not

be

viewed

in

isolation

from,

or

a

substitute

for,

our

GAAP

results.

We

believe

that

this

additional

information

and

the

reconciliations

we

provide

may

be

useful

to

investors,

analysts,

regulators

and

others

as

they

evaluate

the

impact

of

these

respective

items

on

our

results

for

the

periods

presented

due

to

the

extent

to

which

the

items

are

not

indicative

of

our

ongoing

operations.

We

may

also

provide

information

on

pretax

pre-provision

earnings

(total

revenue

less

noninterest

expense)

and

on

tangible

book

value

per

share

(calculated

as

book

value

per

share

less

total

intangible

assets,

other

than

servicing

rights,

per

share).

We

believe

that

pretax

pre-provision

earnings,

a

non-GAAP

measure,

is

useful

as

a

tool

to

help

evaluate

the

ability

to

provide

for

credit

costs

through

operations,

and

that

tangible

book

value

per

share,

a

non-GAAP

measure,

is

useful

as

a

tool

to

help

evaluate

the

amount,

on

a

per

share

basis,

of

intangible

assets

other

than

servicing

rights

included

in

book

value.

Where

applicable,

we

provide

GAAP

reconciliations

for

such

additional

information,

including

in

the

Appendix.

In

certain

discussions,

we

may

also

provide

information

on

yields

and

margins

for

all

interest-earning

assets

calculated

using

net

interest

income

on

a

taxable-equivalent

basis

by

increasing

the

interest

income

earned

on

tax-exempt

assets

to

make

it

fully

equivalent

to

interest

income

earned

on

taxable

investments.

We

believe

this

adjustment

may

be

useful

when

comparing

yields

and

margins

for

all

earning

assets.

We

may

also

use

annualized,

proforma,

estimated

or

third

party

numbers

for

illustrative

or

comparative

purposes

only.

These

may

not

reflect

actual

results.

This

presentation

may

also

include

discussion

of

other

non-GAAP

financial

measures,

which,

to

the

extent

not

so

qualified

therein

or

in

the

Appendix,

is

qualified

by

GAAP

reconciliation

information

available

on

our

corporate

website

at

www.pnc.com

under

“About

PNC–Investor

Relations.” |

3

DRAFT

Today’s Discussion

PNC’s differentiated business model has delivered

strong results through the cycle

Investing for future growth

Balance sheet positioned to support client demand

Significant opportunity to deliver long-term

shareholder value

PNC Continues to Build a Great Company.

PNC Continues to Build a Great Company. |

4

DRAFT

Significant 2011 Achievements

PNC Is Positioned to Deliver Even Greater Shareholder Value.

PNC Is Positioned to Deliver Even Greater Shareholder Value.

YTD financial

summary

Net income

Diluted EPS from

net income

Return on

average assets

$2,578 million

$4.79

1.31%

Delivered strong financial results through exceptional client growth across businesses and

markets

Grew commercial loans

Maintained

a

high

quality

balance

sheet,

improved

overall

credit

quality

Disciplined expense management

Pending

RBC

Bank

(USA)

acquisition

will

provide

access

to

growth

markets

at

a

price

below

tangible book value

Continued to maintain strong capital levels and ratios and liquidity positions

YTD11 highlights

—

Increased common dividend 250% in second quarter

—

Issued $1 billion preferred stock

—

Issued $1.25 billion senior debt |

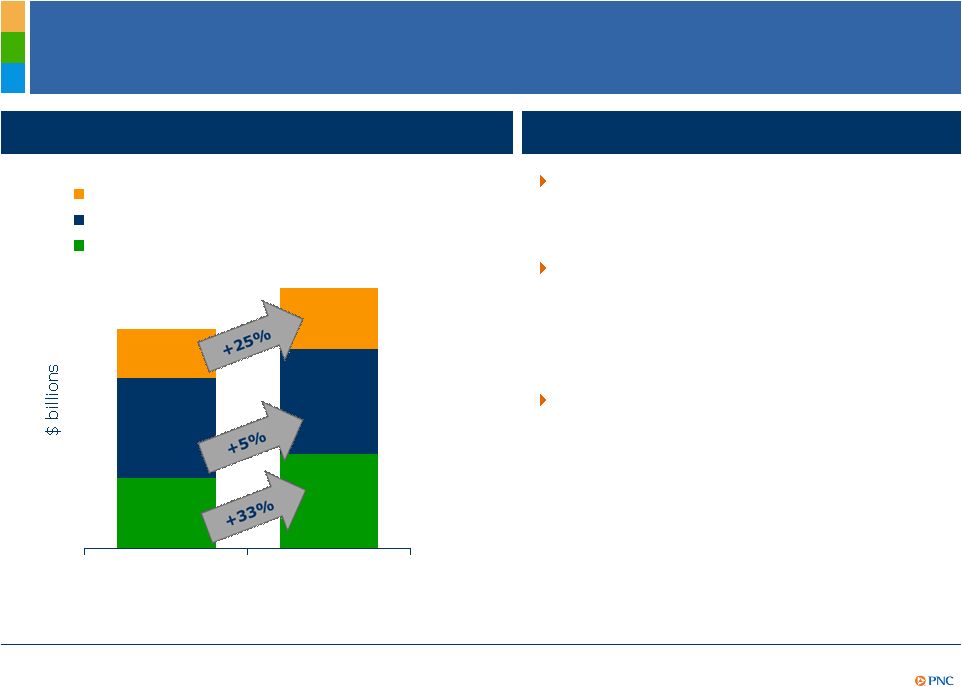

5

DRAFT

Delivering Strong Returns

YTD return on average assets

YTD return on Tier 1 common

capital²

Peer

Source:

SNL

DataSource,

First

Call

reports

and

company

reports,

as

available.

(1)

PNC

Sept.

30,

2011

Tier

1

common

and

Tier

1

common

ratio

estimated.

(2)

Return

on

Tier

1

common

capital

calculated

as

annualized

net

income

divided

by

estimated

Tier

1

common

capital.

Further

information is provided in the Appendix.

STI as of June 30, 2011.

9/30/11 Tier 1 common ratio¹

BAC

-.03%

BAC

-.06% |

6

DRAFT

942

1,076

Sept 10

Sept 11

Growing Customers –

Retail Banking

Strong results

December

2010

Goal

Free checking

Relationship checking³

September

2011

30%

68%

70%

(1)

Organic

growth

refers

to

consumer

and

small

business

customers

excluding

32,000

relationships

from

2Q11

acquisition.

(2)

Organic

growth

excludes

3,000

customers

acquired

by

acquisition

in

2Q11.

(3)

Relationship

checking

refers

to

accounts

with

a

committed

balance

level

or

self-

service accounts with lower cost of servicing.

YTD highlights

Checking relationships YTD

annualized organic growth

rate of 5.5% far exceeded

the 1.2% population growth

of our retail footprint

On track to achieve new

checking account mix target

of 70% relationship checking

Organic checking

relationship growth¹

Organic growth in online bill

payment active customers

New originations

Period end

48

225

YTD10

YTD11

2

+

+ |

7

DRAFT

Strong results

Corporate Banking New Cumulative Primary Client

1

Growth

1Q

2Q

3Q

4Q

New primary clients:

—

New

client

additions

represent

revenue

potential

of

$200

million

per

performance of existing clients

—

Grew

10%

each

year

for

two

years

while

improving

average

risk

rating

—

Referral

sales

to

Corporate

Banking

from Retail increased 34%

YTD highlights

YTD10

YTD11

37%

46%

Corporate Banking New Client Loan Utilization

256

565

869

0

250

500

750

1,000

2011 Goal

2011 Actual

New primary

clients increased

25% YoY

(1) A Corporate Banking primary client is defined as a corporate

banking relationship with annual revenue generation of $50,000 or more or,

within corporate banking, a commercial banking client relationship with annual revenue

generation of $10,000 or more. Growing Customers –

Corporate Banking |

8

DRAFT

Growing Customers –

Asset Management Group

(1)

Referral

sales

are

new

sales

to

clients

referred

to

AMG

by

Retail

Banking

or

Corporate

and

Institutional

Banking.

(2)

Primary

clients

are

client

relationships

with

annual

revenue

generation

of

$10,000

or

more.

(3)

Total

net

flows

defined

as

net

change

from

clients

including

dividends received.

YTD highlights

Total sales increased 38% in 3Q11 compared

with 3Q10

Expanding distribution in all markets with a

particular focus on higher growth markets

—

216

external

new

hires

in

the

first

nine

months

of

2011

–

primarily

front

line

talent

acquisition

YTD earnings impacted by higher marketing

costs from PNC Wealth Insight

SM

product

launch in 3Q

—

Accessible

to

over

12,000

clients

Strong results

Referral sales

1

YTD11 vs. YTD10

86%

New primary clients

2

YTD11 vs. YTD10

34%

$.1B

$1.3B

3Q11

3Q10

Discretionary AUM Total Net Flows |

9

DRAFT

3.71

Performance and Team Driven Culture

Reflects PNC’s brand attributes of ease, confidence and

achievement

Awarded to 29 companies worldwide for extraordinary ability

to create an engaged workplace culture

PNC is a three-time winner and the only U.S bank to be

recognized

4.04

4.21

4.40

4.34

4.40

4.49

4.55

4.35

4.41

4.44

4.44

4.43

4.41

4.48

4.00

4.50

5.00

4Q07

4Q08

4Q09

4Q10

2Q11

Employee

Engagement

Customer

Engagement

High employee and customer engagement

“Gallup Great Workplace Award”

recipient for 2011

Employee engagement shown for total bank branches. Source: Gallup.

4.43

4.38

NCC Conversions

Strongly

Agree

Agree |

10

DRAFT

Investing for Future Growth

Expanding into faster growing regions with

attractive market demographics

—

Chicago, Atlanta

1

, Charlotte

1

, Orlando

1

Adding relationship managers and product

specialists in targeted, under-penetrated growth

markets

—

Increasing distribution capacity

—

Product training

Opportunity to deliver PNC’s products and services

to new customers

—

Utilizing technology and market research on

changing customer behavior to provide customers

more choices

—

Leveraging cross sell synergies

Higher growth markets

People

Product capabilities

Large markets provide excellent C&IB

and Wealth Management opportunities

RBC Bank (USA)¹

Market Potential

Market Revenue Growth

(YTD10-YTD11)

Washington, DC

11%

Chicago

27%

Yielding results

(1) Acquisition pending. (2) Source: SNL DataSource as of September 30, 2011.

|

11

DRAFT

The Chicago Story –

“Go-To-Market Strategy”

Convert to PNC common platform

Initiate “Human Sigma”

in retail distribution

Increase brand awareness

Invest in product and relationship managers

Significant increase in PNC’s customer confidence and brand awareness

53%

55%

56%

54%

58%

41%

32%

22%

23%

23%

2007

2008

2009

2010

2011

Strategy

(1)

Confidence

is

measured

at

PNC

by

asking

“PNC

is

a

name

I

can

always

trust”

and

“PNC

always

delivers

on

what

they

promise.”

A

respondent

is

considered

Confident

if

they

answer

a

“5”

Strongly

Agree

to

both

items.

Source:

Gallup

June

2011.

(2)

Source:

TNS

Strategic

Market report as of 2Q11.

27%

29%

20%

28%

51%

55%

56%

58%

Pre-conversion

Post-conversion

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

Total Brand Awareness –

Chicago

2

National Customer Confidence

PNC customer confidence

1

US population

confidence in banking industry |

12

DRAFT

The Chicago Story –

Market Opportunity

Philadelphia

Chicago

Projected 5-year growth:

Population

.71%

1.86%

Household income

15.4%

16.6%

Market demographics:

Population (in millions)

5.9

9.7

Deposits (in millions)

$204,860

$291,896

Branches

1,892

3,214

Market opportunities:

Households²

(in millions)

2.2

3.5

Universities

64

74

Corporate

Banking¹

4,800

7,300

PNC’s presence:

Deposit market share

8.2%

4.1%

Branches

190

151

Source: SNL Database and Nielsen as of September 30, 2011. (1) Corporate banking prospects

include Large Corporate, Middle Market, Commercial Segment, Public Finance and a minor

amount of other segments. (2) Source: Nielsen. |

13

DRAFT

The Chicago Story –

Executing on the Opportunity

PNC’s demonstrated execution and revenue potential

Total Corporate Banking and AMG Sales

1

48%

68%

52%

32%

Non-Credit

Sales

Credit Sales

$26

$114

$52

Prior to

conversion of

Chicago

market

August 2011,

annualized

Philadelphia

Chicago

Philadelphia

Chicago

(1) Chicago market application systems conversion occurred in June 2010.

Pre-conversion Sales reflect the first six months of 2010, annualized. (2)

Year-to-date August 2011. Corporate Banking Cross-sell Revenue

2 |

14

DRAFT

Balance Sheet Management in a Low Rate

Environment

Drivers

Increase responsible lending to partially offset lower asset yields

Substantially reduce cost of funding to maintain net interest income

Maintain liquidity and strong capital position

Focus on risk-adjusted loan growth to mitigate impact of securities repricing

Lower funding cost

Strategies

Funding Cost Reduction

Opportunities

Expected 2012 Impact

(in millions)

Repricing CDs

$450-$500

Trust preferreds

Maturing debt

Deposit funding

Expected

2012

impact

compared

to

2011

assumes

an

extended

period

of

slow

economic

growth

and

low

interest

rates. |

15

DRAFT

Accelerating Commercial and Industrial Loan Growth

Source: Federal Reserve H8 reports for all domestic commercial banks. Seasonally

adjusted annual growth rate. PNC loan data from TARP reports. (1) PNC Corporate &

Institutional Banking quarterly utilization rates reflect the consolidation of Market Street Funding Corporation

beginning January 2010. 2011 represents year to date results through September 30, 2011.

Annual loan growth

Every percentage point increase in utilization

increases loan balances by $1.4B and

approximately $40M in annual net interest

income.

Utilization

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

PNC

All Commercial Banks

45%

46%

47%

48%

49%

50%

51%

52%

53%

PNC Corporate & Institutional

Banking Utilization

1 |

16

DRAFT

Loan Growth Momentum

Total Corporate & Institutional Banking

average loans increased in 3Q11 by 7%

compared with 3Q10

Loans have been steadily increasing in

Business Credit, Middle Market and

Corporate Finance since the end of 2010,

primarily driven by new client growth and

commitments

Average credit commitments per new

client has increased 60% YTD11 vs.

YTD10

YTD highlights

Average

loan

growth

primarily

driven

by

new

clients

9.1

9.6

6.4

8.5

4.4

5.5

3Q10

3Q11

Corporate Finance

Middle Market

Business Credit |

17

DRAFT

Highlights

Capital Management

Tier 1 common ratio

(1) Proforma estimate is based on PNC’s estimated Tier 1 common ratio of 10.5% as of

9/30/11, and includes the assumed benefit of 1.4%, which reflects First Call 2011 and

2012 estimates and current dividend payout, as well as the assumed decrease of 3.3%-3.8%, which reflects assumptions utilizing Basel II

methodology regarding credit, operating and market risk and includes the treatment of

BlackRock and sub-investment grade securities (assuming no AOCI double counting)

under Basel II, and assumes no common share issuance for the pending RBC Bank (USA) acquisition. This estimate is subject to

further regulatory guidance and clarity. The estimate is based on the phase-in of Basel

III rules in effect as of 2012. (2) Regulatory requirements include capital

conservation buffer. (3) Parent company liquidity coverage defined as liquid assets divided by funding obligations within a two year period.

Basel III requirements²

12/31/12

Proforma Basel III

8.0% -

8.5%¹

Proforma Basel III Tier 1 common ratio

estimated to be between 8.0-8.5% at

December 31,

2012²

–

Possible improvement assuming final

capital requirements reflect the inherent

risk profile in our sub-investment grade

securities

–

Assumes no common stock issuance to

fund pending acquisition of RBC Bank

(USA)

Strong liquidity position at September 30, 2011

–

Loan-to-deposit ratio of 82%

–

Parent company two year liquidity

coverage³

of 168%

Capital Priorities:

–

Investing in organic growth

–

Meeting regulatory requirements

–

Return capital to shareholders |

18

DRAFT

Delivering Long-Term Shareholder Value

Tangible book value per share¹

Pretax pre-provision earnings per share³

$17.58

$44.85

12/31/07

9/30/11

$7.06

$11.16

2007

2011

PNC

% change 2007-2011²

PNC

4

155%

87%

71%

48%

36%

24%

21%

-4%

-5%

-10%

-14%

-42%

-44%

58%

23%

17%

13%

11%

-7%

-29%

-36%

-43%

-55%

-57%

-68%

-84%

PNC

MTB

WFC

USB

JPM

COF

BBT

FITB

STI

CMA

RF

KEY

BAC

Peer

banks

identified

in

the

Appendix.

Source

for

banks

other

than

PNC:

SNL

DataSource.

(1)

Tangible

book

value

per

share

calculated

as

book

value

per

share

less

goodwill

and

other

intangible

assets

other

than

servicing

rights.

Further

information

is

provided

in

the

Appendix.

(2)

Percentage

change

for

2007

to

nine

months

ended

September

30,

2011,

annualized,

respectively.

(3)

Pretax,

pre-provision

earnings

are

from

continuing

operations

and

are

calculated

as

total

revenue

less

noninterest

expense.

Further

information

is

provided

in

the

Appendix.

(4)

2011

represents

pretax

pre-provision

earnings

for

the

nine

months

ended

September

30,

2011,

annualized,

divided

by

the

number

of

shares outstanding as of September 30, 2011.

% change 2007-2011²

PNC

WFC

USB

JPM

MTB

BBT

COF

BAC

CMA

FITB

STI

RF

KEY |

19

DRAFT

Cautionary Statement Regarding Forward-Looking

Information

This

presentation

includes

“snapshot”

information

about

PNC

used

by

way

of

illustration

and

is

not

intended

as

a

full

business

or

financial

review.

It

should not be viewed in isolation but rather in the context of all of the information made

available by PNC in its SEC filings. We

also

make

statements

in

this

presentation,

and

we

may

from

time

to

time

make

other

statements,

regarding

our

outlook

for

earnings,

revenues,

expenses,

capital

levels,

liquidity

levels,

asset

quality

and

other

matters

regarding

or

affecting

PNC

and

its

future

business

and

operations

that

are

forward-looking

statements

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act.

Forward-looking

statements

are

typically

identified

by

words

such

as

“believe,”

“plan,”

“expect,”

“anticipate,”

“see,”

“intend,”

“outlook,”

“project,”

“forecast,”

“estimate,”

“goal,”

“will,”

“should”

and

other

similar

words

and

expressions.

Forward-looking

statements

are

subject

to

numerous

assumptions,

risks

and

uncertainties,

which

change

over

time.

Forward-looking

statements

speak

only

as

of

the

date

made.

We

do

not

assume

any

duty

and

do

not

undertake

to

update

forward-looking

statements.

Actual

results

or

future

events

could

differ,

possibly

materially,

from

those

anticipated

in

forward-looking

statements,

as

well

as

from

historical performance.

Our forward-looking statements are subject to the following principal risks and

uncertainties. •Our businesses, financial results and balance sheet values are

affected by business and economic conditions, including the following:: o

Changes in interest rates and valuations in debt, equity and other financial markets.

o

Disruptions in the liquidity and other functioning of U.S. and global financial markets.

o

The

impact

on

financial

markets

and

the

economy

of

the

downgrade

by

Standard

&

Poor’s

of

U.S.

Treasury

obligations

and

other

U.S.

government-backed

debt,

as

well

as

issues

surrounding

the

level

of

U.S.

and

European

government

debt

and

concerns

regarding

the

credit

worthiness of certain sovereign governments in Europe.

o

Actions

by

Federal

Reserve,

U.S.

Treasury

and

other

government

agencies,

including

those

that

impact

money

supply

and

market

interest

rates.

o

Changes in customers’, suppliers’

and other counterparties’

performance and creditworthiness.

o

Slowing or failure of the current moderate economic recovery.

o

Continued

effects

of

aftermath

of

recessionary

conditions

and

uneven

spread

of

positive

impacts

of

recovery

on

the

economy

and

our

counterparties,

including

adverse

impacts

on

levels

of

unemployment,

loan

utilization

rates,

delinquencies,

defaults

and

counterparty

ability

to

meet credit and other obligations.

o

Changes

in

customer

preferences

and

behavior,

whether

due

to

changing

business

and

economic

conditions,

legislative

and

regulatory

initiatives, or other factors.

•Our

forward-looking

financial

statements

are

subject

to

the

risk

that

economic

and

financial

market

conditions

will

be

substantially

different

than

we

are

currently

expecting.

These

statements

are

based

on

our

current

view

that

the

modest

economic

expansion

will

persist

in

the

year

ahead

and

interest rates will remain very low.

Appendix |

20

DRAFT

Cautionary Statement Regarding Forward-Looking

Information (continued)

Appendix

•Legal

and

regulatory

developments

could

have

an

impact

on

ability

to

operate

our

businesses,

financial

condition,

results

of

operations,

competitive

position,

reputation,

or

pursuit

of

attractive

acquisition

opportunities.

Reputational

impacts

could

affect

matters

such

as

business

generation

and

retention,

liquidity,

funding,

and

ability

to

attract

and

retain

management.

These

developments

could

include:

o

Changes

resulting

from

legislative

and

regulatory

reforms,

including

broad-based

restructuring

of

financial

industry

regulation

and

changes

to

laws

and

regulations

involving

tax,

pension,

bankruptcy,

consumer

protection,

and

other

industry

aspects,

and

changes

in

accounting

policies

and

principles.

We

will

be

impacted

by

extensive

reforms

provided

for

in

the

Dodd-Frank

Wall

Street

Reform

and

Consumer

Protection

Act

(the

“Dodd-Frank

Act”)

and

otherwise

growing

out

of

the

recent

financial

crisis,

the

precise

nature,

extent

and

timing

of

which,

and

their

impact

on

us, remains uncertain.

o

Changes

to

regulations

governing

bank

capital

and

liquidity

standards,

including

due

to

the

Dodd-Frank

Act

and

to

Basel

III

initiatives.

o

Unfavorable

resolution

of

legal

proceedings

or

other

claims

and

regulatory

and

other

governmental

investigations

or

other

inquiries.

In

addition

to

matters

relating

to

PNC’s

business

and

activities,

such

matters

may

include

proceedings,

claims,

investigations,

or

inquiries

relating

to

pre

acquisition

business

and

activities

of

acquired

companies,

such

as

National

City.

These

matters

may

result

in

monetary

judgments

or

settlements

or

other

remedies,

including

fines,

penalties,

restitution

or

alterations

in

our

business

practices,

and

in

additional

expenses

and

collateral costs, and may cause reputational harm to PNC.

o

Results

of

regulatory

examination

and

supervision

process,

including

our

failure

to

satisfy

requirements

of

agreements

with

governmental

agencies.

o

Impact

on

business

and

operating

results

of

any

costs

associated

with

obtaining

rights

in

intellectual

property

claimed

by

others

and

of

adequacy

of

our

intellectual

property

protection

in

general.

•Business

and

operating

results

are

affected

by

our

ability

to

identify

and

effectively

manage

risks

inherent

in

our

businesses,

including,

where

appropriate,

through

effective

use

of

third-party

insurance,

derivatives,

and

capital

management

techniques,

and

to

meet

evolving

regulatory

capital

standards.

In

particular,

our

results

currently

depend

on

our

ability

to

manage

elevated

levels

of

impaired

assets.

•Business

and

operating

results

also

include

impacts

relating

to

our

equity

interest

in

BlackRock,

Inc.

and

rely

to

a

significant

extent

on

information

provided

to

us

by

BlackRock.

Risks

and

uncertainties

that

could

affect

BlackRock

are

discussed

in

more

detail

by

BlackRock

in

SEC

filings.

•Our

planned

acquisition

of

RBC

Bank

(USA)

presents

us

with

risks

and

uncertainties

related

both

to

the

acquisition

transaction

itself

and

its

integration

into

PNC

after

closing,

including:

o

Closing

is

dependent

on,

among

other

things,

receipt

of

regulatory

and

other

applicable

approvals,

the

timing

of

which

cannot

be

predicted

with

precision

at

this

point

and

which

may

not

be

received

at

all.

The

impact

of

closing

on

PNC’s

financial

statements

will

be

affected

by

the

timing

of

the transaction.

o

The

transaction

(including

integration

of

RBC

Bank

(USA)’s

businesses)

may

be

substantially

more

expensive

to

complete

than

anticipated.

Anticipated

benefits,

including

cost

savings

and

strategic

gains,

may

be

significantly

harder

or

take

longer

to

achieve

than

expected

or

may

not

be achieved in their entirety as a result of unexpected factors or events.

o

Our

ability

to

achieve

anticipated

results

from

this

transaction

is

dependent

also

on

the

following

factors,

in

part

related

to

the

state

of

economic

and

financial

markets:

the

extent

of

credit

losses

in

the

acquired

loan

portfolios

and

the

extent

of

deposit

attrition.

Also,

litigation

and

governmental

investigations

that

may

be

filed

or

commenced,

as

a

result

of

this

transaction

or

otherwise,

could

impact

the

timing

or

realization

of anticipated benefits to PNC. |

21

DRAFT

Cautionary Statement Regarding Forward-Looking

Information (continued)

Appendix

o

Integration

of

RBC

Bank

(USA)’s

business

and

operations

into

PNC,

which

will

include

conversion

of

RBC

Bank

(USA)’s

different

systems

and

procedures,

may

take

longer

than

anticipated

or

be

more

costly

than

anticipated

or

have

unanticipated

adverse

results

relating

to

RBC

Bank

(USA)’s

or

PNC’s

existing

businesses.

PNC’s

ability

to

integrate

RBC

Bank

(USA)

successfully

may

be

adversely

affected

by

the

fact

that

this

transaction will result in PNC entering several markets where PNC does not currently have any

meaningful retail presence. •In

addition

to

the

planned

RBC

Bank

(USA)

transaction,

we

grow

our

business

in

part

by

acquiring

from

time

to

time

other

financial

services

companies,

financial

services

assets

and

related

deposits.

These

other

acquisitions,

including

our

planned

acquisition

of

branches

and

related

deposits

in

metropolitan

Atlanta,

Georgia

from

Flagstar

Bank,

FSB,

often

present

risks

and

uncertainties

analogous

to

those

presented

by

the

RBC

Bank (USA) transaction, as well as, in some cases, with risks related to entering into new

lines of business. •Competition

can

have

an

impact

on

customer

acquisition,

growth

and

retention

and

on

credit

spreads

and

product

pricing,

which

can

affect

market

share,

deposits

and

revenues.

Industry

restructuring

in

the

current

environment

could

also

impact

our

business

and

financial

performance

through

changes

in

counterparty

creditworthiness

and

performance

and

in

competitive

and

regulatory

landscape.

Our

ability

to

anticipate

and

respond

to

technological changes can also impact our ability to respond to customer needs and meet

competitive demands. •Business

and

operating

results

can

also

be

affected

by

widespread

disasters,

dislocations,

terrorist

activities

or

international

hostilities

through

impacts on the economy and financial markets generally or on us or our counterparties

specifically. We

provide

greater

detail

regarding

some

of

these

factors

in

our

2010

Form

10-K

and

first

and

second

quarter

2011

Form

10-Qs,

including

Risk

Factors

and

Risk

Management

sections

of

those

reports,

and

our

subsequent

SEC

filings.

Our

forward-looking

statements

may

also

be

subject

to

other

risks

and

uncertainties,

including

those

we

may

discuss

elsewhere

in

this

presentation

or

in

SEC

filings,

accessible

on

the

SEC’s

website

at

www.sec.gov

and

on

our

corporate

website

at

www.pnc.com/secfilings.

We

have

included

these

web

addresses

as

inactive

textual

references

only.

Information on these websites is not part of this document.

Any

annualized,

proforma,

estimated,

third

party

or

consensus

numbers

in

this

presentation

are

used

for

illustrative

or

comparative

purposes

only

and

may

not

reflect

actual

results.

Any

consensus

earnings

estimates

are

calculated

based

on

the

earnings

projections

made

by

analysts

who

cover

that

company.

The

analysts’

opinions,

estimates

or

forecasts

(and

therefore

the

consensus

earnings

estimates)

are

theirs

alone,

are

not

those

of

PNC or its management, and may not reflect PNC’s or other company’s actual or

anticipated results. |

22

DRAFT

Non-GAAP to GAAP Reconcilement

Appendix

As of or for the nine months ended

In millions

Sept. 30, 2011

Tier 1 common capital (1)

$23,410

Reported net income

2,578

Reported net income, if annualized

3,447

Return on tier 1 common capital

14.7%

(1) Estimated for Sept. 30, 2011.

PNC

believes

that

return

on

tier

1

common

capital

is

useful

as

a

tool

to

help

measure

and assess a company's use of common equity.

As of

In millions except per share data

Dec. 31, 2007

Sept. 30, 2011

% Change

Common shareholders' equity

$14,847

$32,583

Common shares outstanding

341

526

Book value per common share

$43.60

$61.92

42%

Goodwill and other intangible assets other than servicing rights

$8,853

$8,990

Common shareholders' equity less intangible assets

$5,994

$23,593

Common shares outstanding

341

526

Tangible book value per common share

$17.58

$44.85

155%

PNC

believes

that

tangible

book

value

per

common

share,

a

non-GAAP

measure,

is

useful

as

a

tool

to

help

evaluate

the

amount,

on

a

per

share

basis,

of

goodwill

and

certain

other

intangible

assets

included

in

book

value

per common share. |

23

DRAFT

Non-GAAP to GAAP Reconcilement

Appendix

For the year ended

For the nine months ended

In millions except per share data

Dec. 31, 2007

September 30, 2011

% Change

Total revenue

$6,705

$10,777

Noninterest expense

4,296

6,386

Pretax

pre-provision earnings from continuing operations $2,409

$4,391

Pretax pre-provision earnings, annualized

$2,409

$5,871

Common shares outstanding

341

526

Annualized pretax pre-provision earnings per share

$7.06

$11.16

58%

PNC

believes

that

pretax,

pre-provision

earnings

from

continuing

operations,

a

non-GAAP

measure,

is

useful

as

a

tool

to

help evaluate the ability to provide for credit costs through operations.

|

24

DRAFT

Peer Group of Banks

Appendix

The PNC Financial Services Group, Inc.

PNC

BB&T Corporation

BBT

Bank of America Corporation

BAC

Capital One Financial, Inc.

COF

Comerica Inc.

CMA

Fifth Third Bancorp

FITB

JPMorgan Chase

JPM

KeyCorp

KEY

M&T Bank

MTB

Regions Financial Corporation

RF

SunTrust Banks, Inc.

STI

U.S. Bancorp

USB

Wells Fargo & Co.

WFC

Ticker |