Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Patriot Coal CORP | d248841d8k.htm |

November 1,

2011 Exhibit 99.1

Met Coke World Summit 2011 |

1

Some of the following information contains forward-looking statements within the meaning

of Section 27A of the Securities Act of 1933 and Section 21E of the Securities

Exchange Act of 1934, as amended, and is intended to come within the safe-harbor

protection provided by those sections. Forward-Looking Statements

Certain statements in this presentation are forward-looking as defined in the Private

Securities Litigation

Reform

Act

of

1995.

These

statements

involve

certain

risks

and

uncertainties

that

may

be

beyond our control and may cause our actual future results to differ materially from

expectations. We do not undertake to update our forward-looking

statements. Factors that could affect our results include, but are not limited

to: price volatility and demand, particularly in higher margin products; geologic,

equipment and operational risks associated with mining; changes in general economic

conditions, including coal, power and steel market conditions; coal mining laws and

regulations; the availability and costs of competing energy resources; legislative and

regulatory developments; risks associated with environmental laws and compliance,

including selenium-related matters; developments in

greenhouse

gas

emission

regulation

and

treatment;

negotiation

of

labor

contracts,

labor

availability

and relations; the outcome of pending or future litigation; changes in the costs to provide

healthcare to eligible active employees and certain retirees under postretirement

benefit obligations; increases to contribution requirements to multi-employer

retiree healthcare and pension funds; reductions of purchases or deferral of shipments

by major customers; availability and costs of credit; customer performance and credit

risks; inflationary trends; worldwide economic and political conditions; downturns in

consumer and company spending; supplier and contract miner performance and the

availability and cost of key equipment and commodities; availability and costs of

transportation; the Company’s ability to replace coal reserves; the outcome of

commercial negotiations involving sales contracts or other transactions; our ability

to respond to changing customer preferences; failure to comply

with

debt

covenants;

the

effects

of

mergers,

acquisitions

and

divestitures;

and

weather

patterns

affecting

energy

demand

or

disrupting

coal

supply.

The

Company

undertakes

no

obligation

(and

expressly

disclaims

any

such

obligation)

to

publicly

update

or

revise

any

forward-looking

statement,

whether

as

a

result

of

new

information,

future

events

or

otherwise.

For

additional

information

concerning

factors

that

could

cause

actual

results

to

materially

differ

from

those

projected

herein,

please

refer to the Company’s Form 10-K and Form 10-Q reports.

Statement on Forward-Looking Information |

Metallurgical

Market Overview Stabilized global and U.S. steel

mill utilization

Strong seaborne market

China is expected to be a net

importer of 30+ million tonnes

of met coal in 2011

Limited new global supply in the

intermediate term

Adequate U.S. port capacity

Met market expected to remain strong

2 |

Industry Trends

& Opportunities 3 |

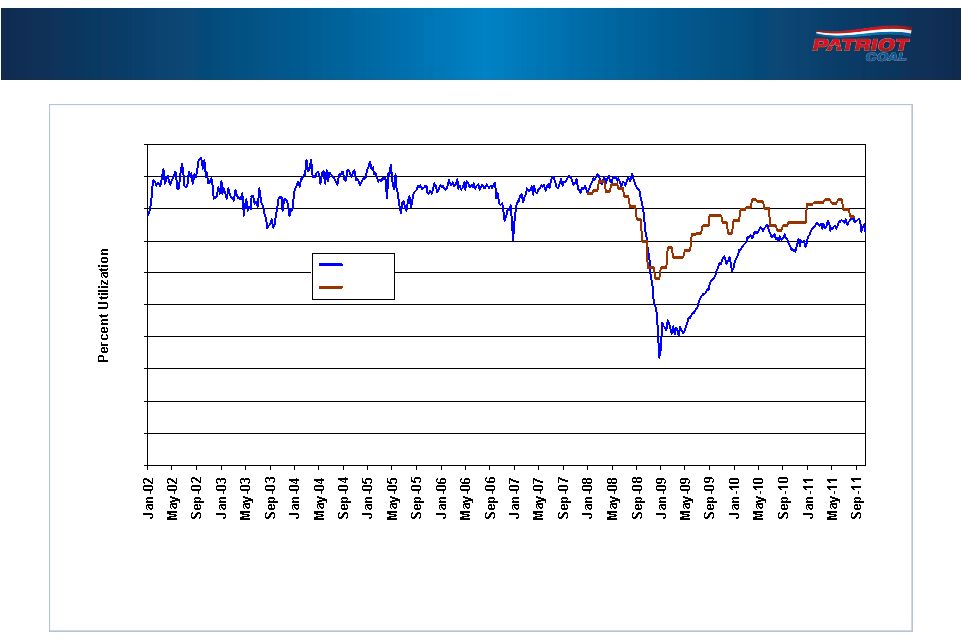

Domestic &

Global Steel Mill Utilization Both domestic & global steel mill utilization rates are

at 70-80% 0

10

20

30

40

50

60

70

80

90

100

U.S.

Global

Updated:

10/22/11

4 |

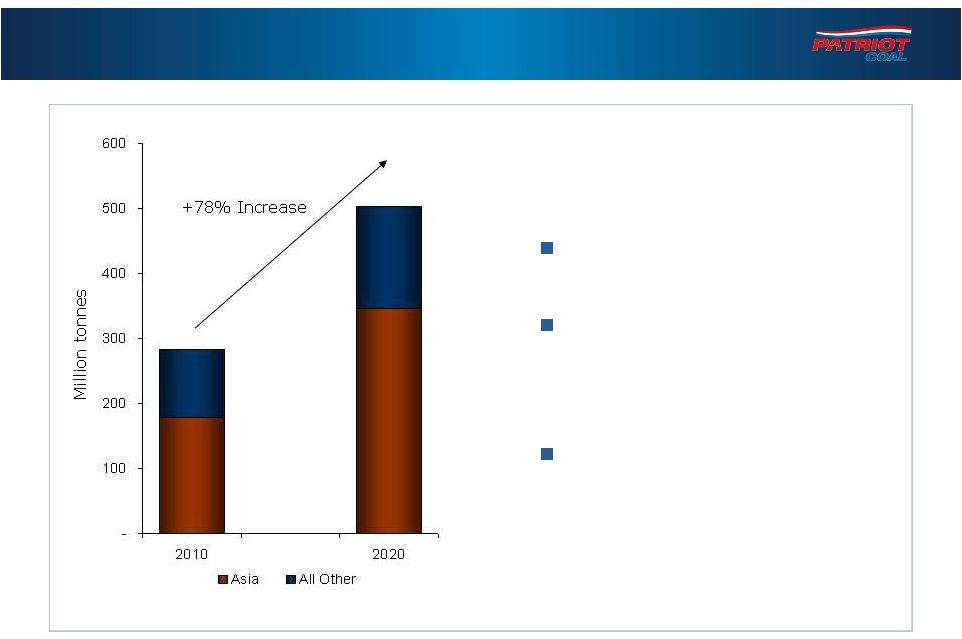

Strong Seaborne

Met Coal Demand Sustainable seaborne demand, led by Asia

Source: McCloskey

5

78% forecast increase in

seaborne met demand

Asian seaborne met

demand expected to

almost double between

2010 and 2020

Led by the urbanization of

Asian populations |

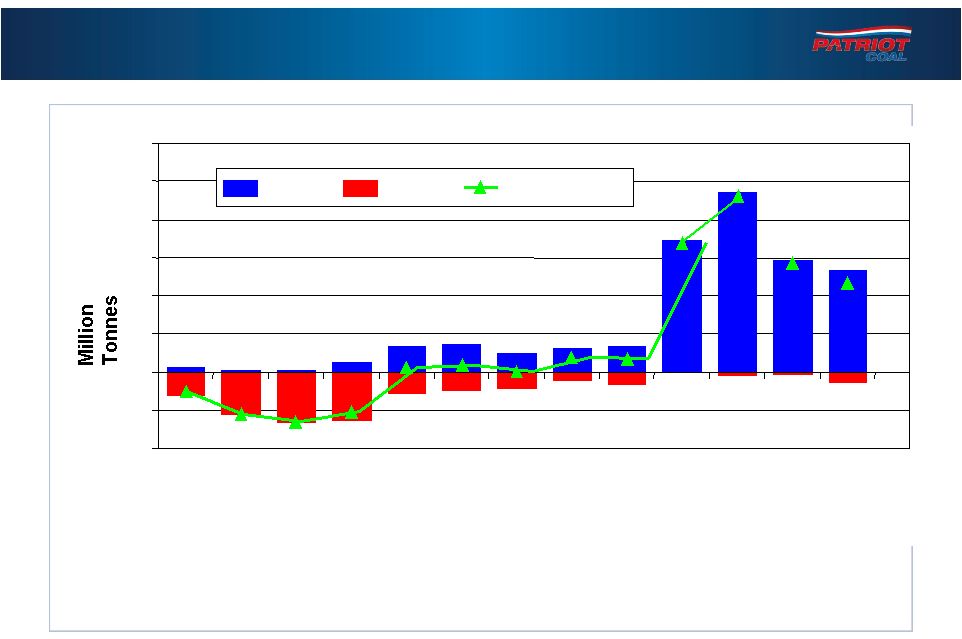

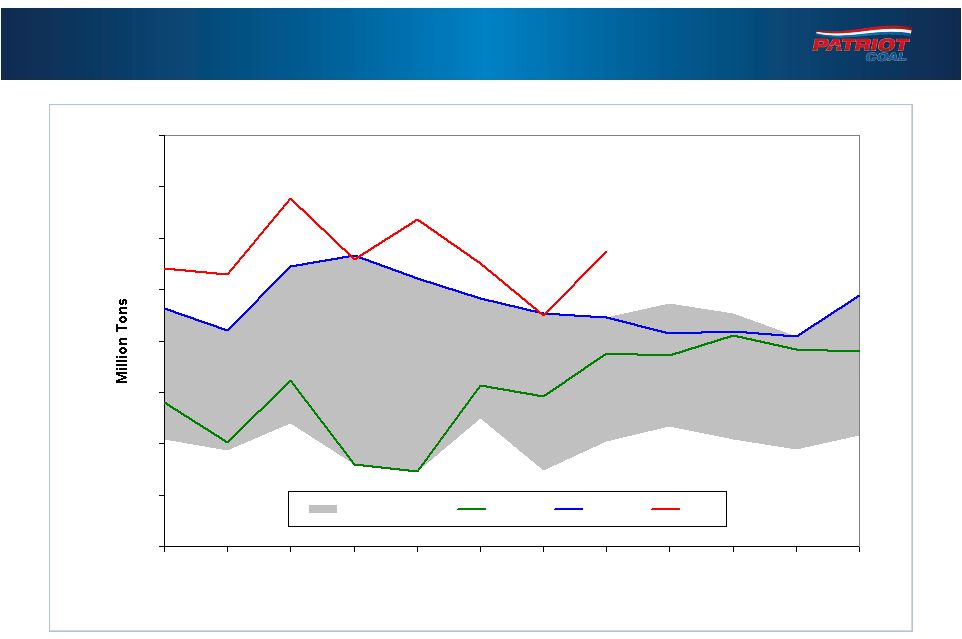

Chinese Met

Coal Trade Net imports of met coal by China remain strong

6

(20)

(10)

0

10

20

30

40

50

60

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

YTD

Aug

2010

YTD

Aug

2011

Imports

Exports

Net Imports

Source: IHS McCloskey |

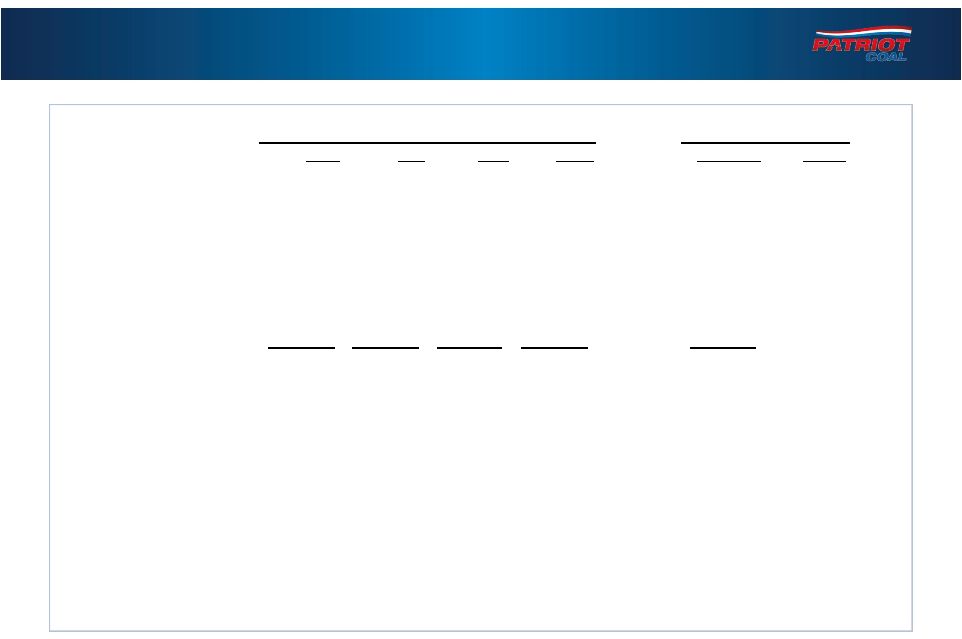

U.S.

Metallurgical Coal Production 7

High

Mid

Low

Total

Estimate

Notes

Alpha

14.6

3.6

1.8

19.9

23.6

1

Arch

6.6

-

1.4

8.0

9.7

2

Walter

-

-

7.2

7.2

6.3

3

Consol

2.4

-

4.6

7.0

10.3

4

Patriot

6.9

-

-

6.9

7.6

5

Cleveland-Cliffs

0.6

-

2.2

2.8

3.2

6

Alliance

1.0

-

-

1.0

1.0

7

Rhino

0.7

-

-

0.7

0.8

8

Others

12.5

4.4

4.4

21.4

22.0

9

Total Estimate

45.2

8.0

21.6

74.8

84.5

Notes:

1. Includes full year of Alpha and Massey; based on shipment

guidance of 9/21/11 2. Includes full year of Arch and

ICG; based on revised earnings guidance of 9/30/11 3.

Based on revised operating plans of 9/21/11 4. Based on

operations update of 10/13/11 5. Based on Q3 2011

earnings release 6. Based on Q2 2011 earnings

release 7. Based on Q2 2011 earnings release

8. Based on Q2 2011 earnings release

9. Patriot estimate

2010

2011 |

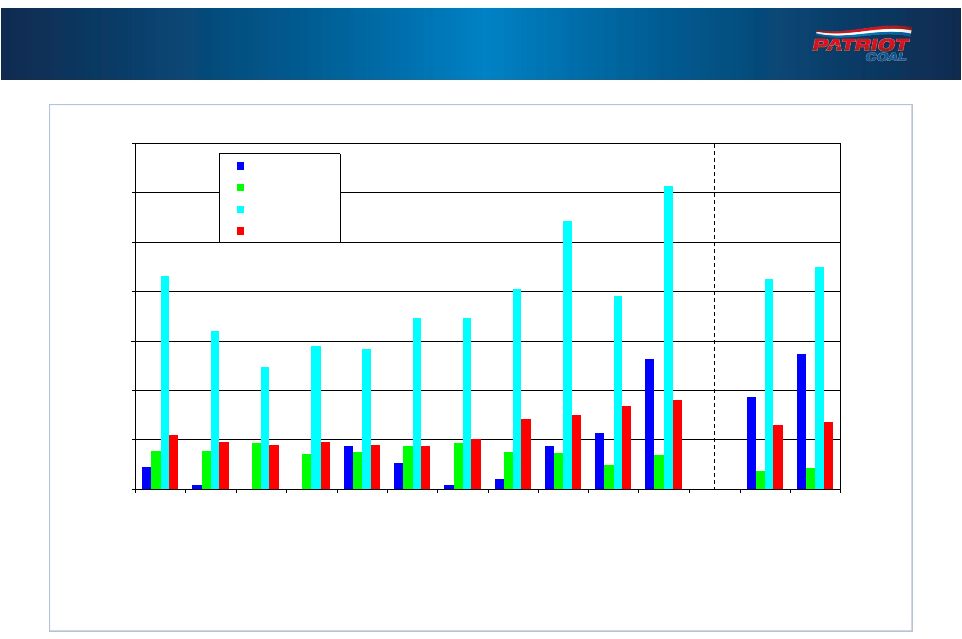

U.S. Exports of

Met Coal U.S. met exports are at historical highs

8

0

1

2

3

4

5

6

7

8

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

5-Year Range

2009

2010

2011 |

9

U.S. Met Coal Export Destinations

U.S. met exports are growing to three key regions

0

5

10

15

20

25

30

35

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

YTD

August

2010

YTD

August

2011

Asia

Canada

Europe/Africa

South America |

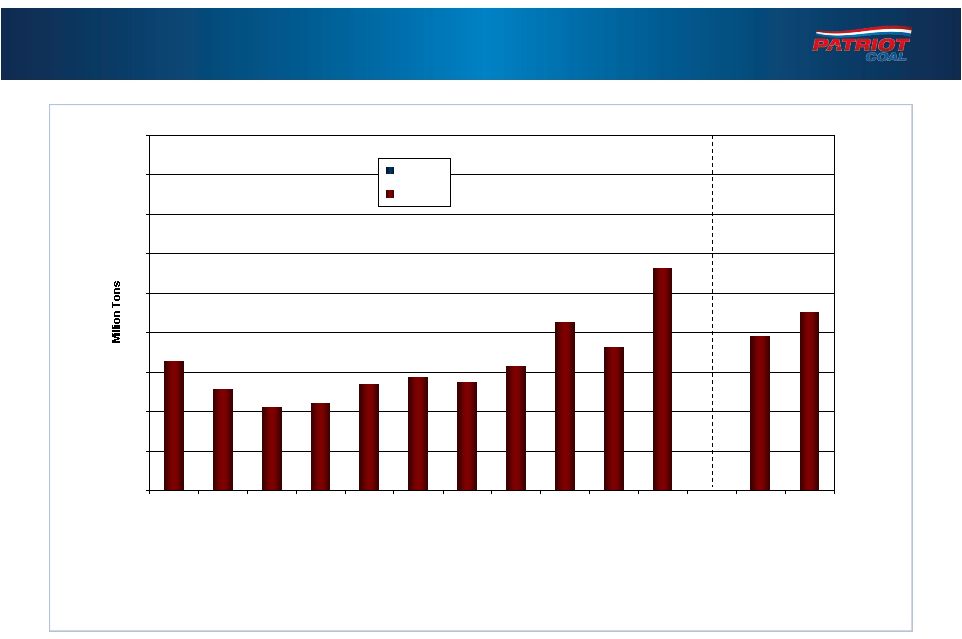

10

Increasing U.S. Met Coal Exports

YTD August met exports are more than any full year, except 2010

0

10

20

30

40

50

60

70

80

90

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

YTD

August

2010

YTD

August

2011

Thermal

Met

Updated:

10/25/11

Source: EVA |

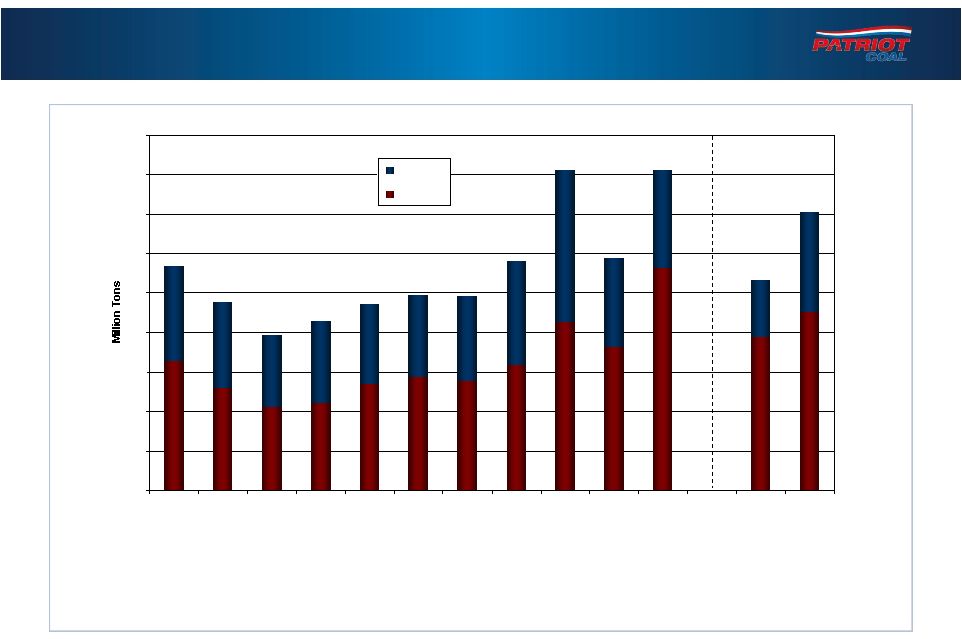

0

10

20

30

40

50

60

70

80

90

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

YTD

August

2010

YTD

August

2011

Thermal

Met

Updated:

10/25/11

Source: EVA

11

Increasing U.S. Total Coal Exports

U.S. coal exports to approximate 100 million tons in 2011

International buyers looking for geographic diversity of supply |

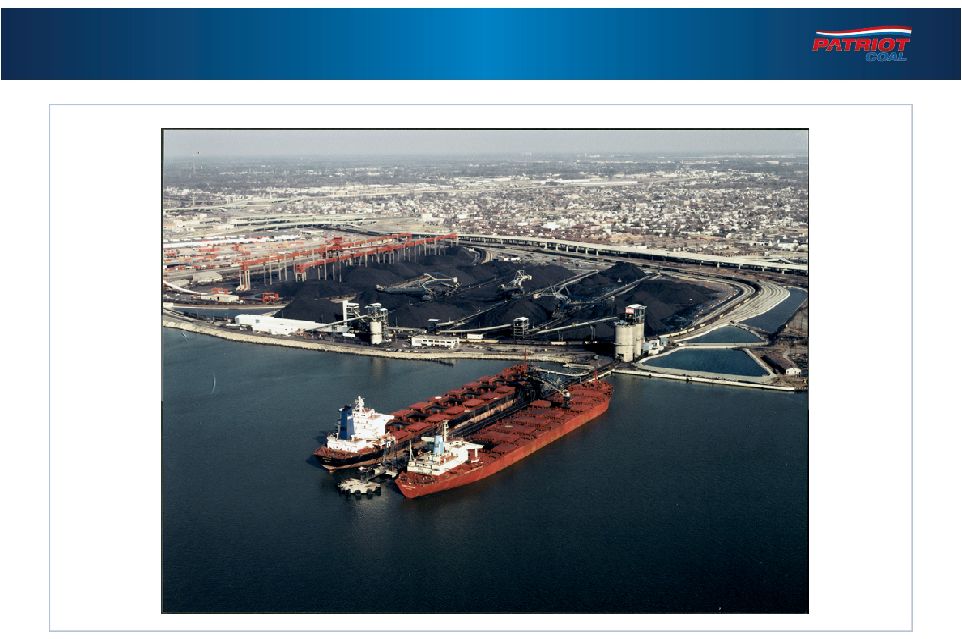

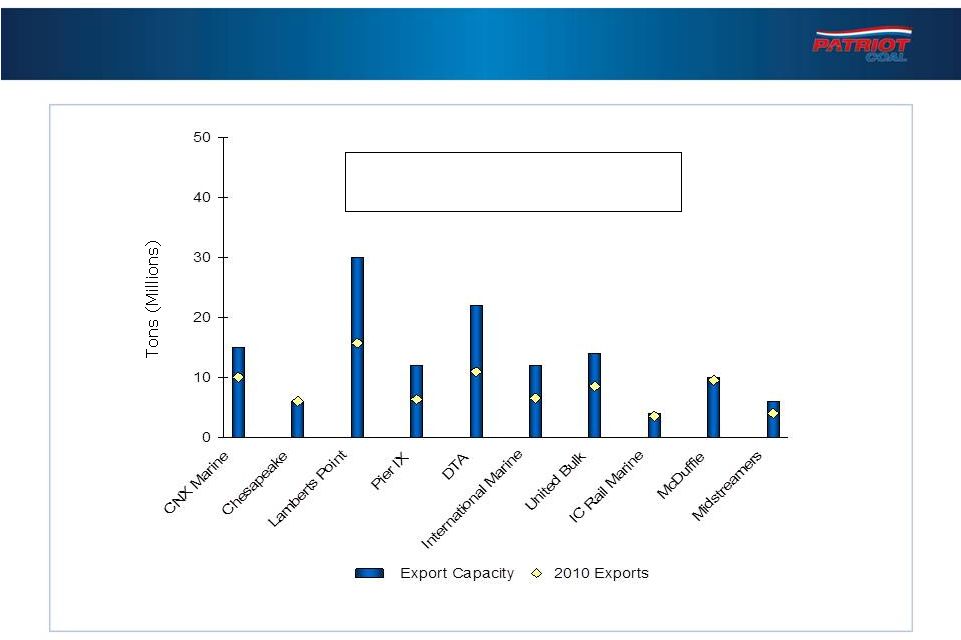

Adequate U.S.

Port Capacity Infrastructure adequate to handle expected exports

12

Total Export Capacity

131 MT

2010 Tons Shipped

81 MT |

Challenges

13 |

14

Why Global Coal Supply is Constrained

Global supply constraints are tightening markets

China

Constrained rail & truck

infrastructure makes

shipping within China

difficult

Indigenous met coal is

lower quality

Several years running

as significant net

importer

Indonesia, South Africa,

Russia, Vietnam

Domestic demand increases are

absorbing coal production that

was historically exported

Declining exports

U.S.

Depleting eastern reserves

Difficult permitting

Stricter interpretation of

safety rules

Supply increases will be

difficult

Australia

Regional infrastructure

constraints limit supply

increase

Australian production

recovering from record

rainfall in early 2011

Infrastructure needed to

supply global demand

India

Plentiful indigenous coal

reserves, but lower quality

Inadequate transportation

infrastructure

Colombia

Inadequate infrastructure

limiting further exports

Mongolia

Will eventually supply China

Much work & time to build

infrastructure

Ownership/structural

challenges

China

Constrained rail & truck

infrastructure makes

shipping within China

difficult

Indigenous met coal is

lower quality

Several years running

as significant net

importer

Indonesia, South Africa,

Russia, Vietnam

Domestic demand increases are

absorbing coal production that

was historically exported

Declining exports

U.S.

Depleting eastern reserves

Difficult permitting

Stricter interpretation of

safety rules

Supply increases will be

difficult

Australia

Regional infrastructure

constraints limit supply

increase

Australian production

recovering from record

rainfall in early 2011

Infrastructure needed to

supply global demand

Australia

Regional infrastructure

constraints limit supply

increase

Australian production

recovering from record

rainfall in early 2011

Infrastructure needed to

supply global demand

India

Plentiful indigenous coal

reserves, but lower quality

Inadequate transportation

infrastructure

Colombia

Inadequate infrastructure

limiting further exports

Colombia

Inadequate infrastructure

limiting further exports

Mongolia

Will eventually supply China

Much work & time to build

infrastructure

Ownership/structural

challenges |

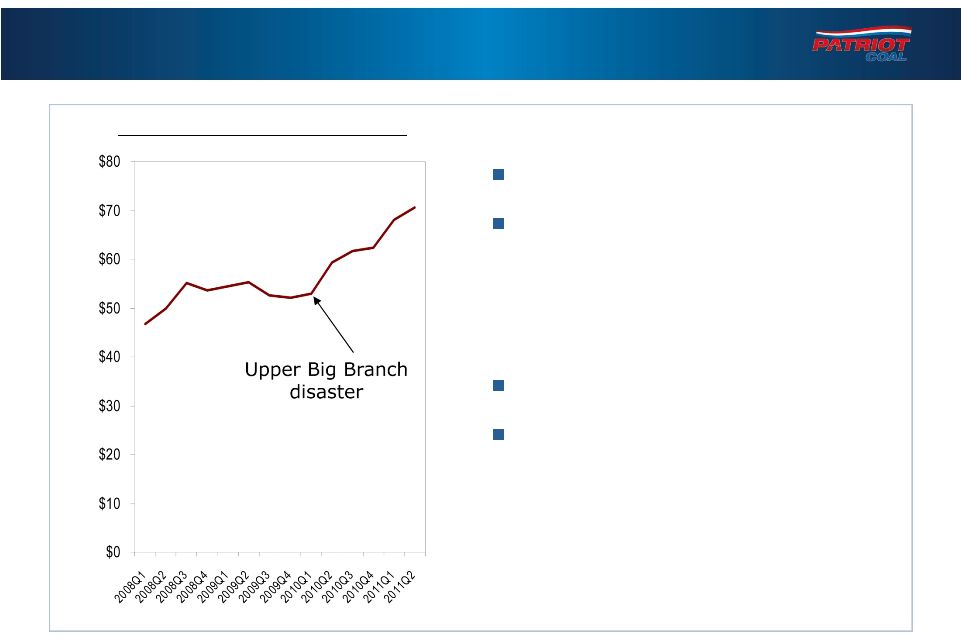

Higher

Industry Cost per Ton in Appalachia More difficult geology

Heightened regulatory scrutiny

–

MSHA and state inspections

–

MSHA & Army Corps of Engineers

permitting delays

–

Clean Water Act impediments

Availability of labor

Higher cost inputs

–

Labor

–

Diesel fuel

–

Steel-based equipment &

supplies

15

Industry Average Cost per Ton |

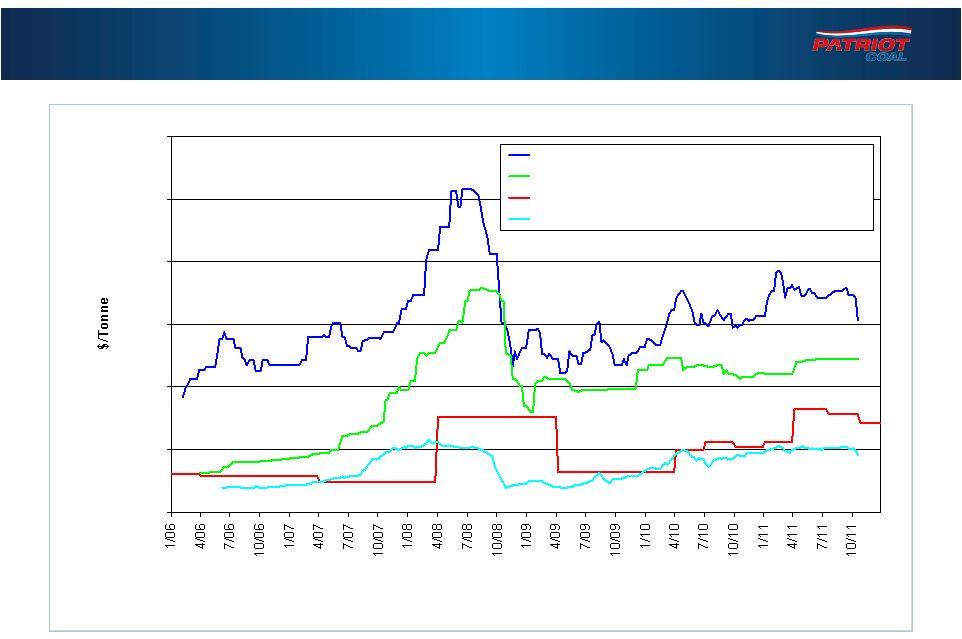

Steel Prices

versus Raw Material Costs Steel prices remain historically high

16

0

200

400

600

800

1,000

1,200

China Export Hot-Rolled Coil Steel, FOB main China Port

China Coke Export Price

Australian Hard Coking Coal, FOBT

Chinese Iron Ore Import Price

10/26/11

Updated:

Source: Metal Bulletin, Steel Business Briefing Commodities Research, McCloskey

|

-10

-5

0

5

10

15

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

India

China

Brazil

Australia

USA

Germany

UK

Japan

Source: Economist Intelligence Unit (The Economist)

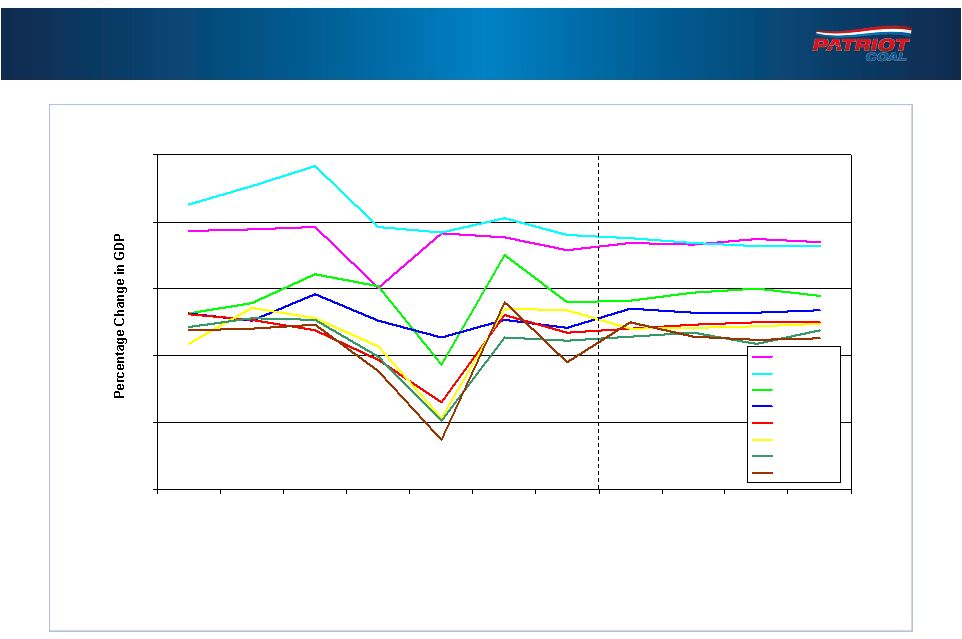

Concerns about Global Economies

17

Chinese & Indian economies expected to remain strong

All global economies growing |

Opportunities

for Patriot 18 |

How Patriot

Will Participate Strategy –

Focus on growth markets

–

Expand metallurgical coal production

–

Increase exports –

Both met and thermal

Leverage to the market

–

Met Build-Out to 11 million tons annually

–

Legacy thermal contract roll-off

Culture

–

Strong safety program & environmental stewardship

–

Disciplined approach, focused on planning and execution

Future growth

–

Organic –

Strong reserve base

–

M&A –

Bolt-on and transformational

Product & transportation flexibility

19 |

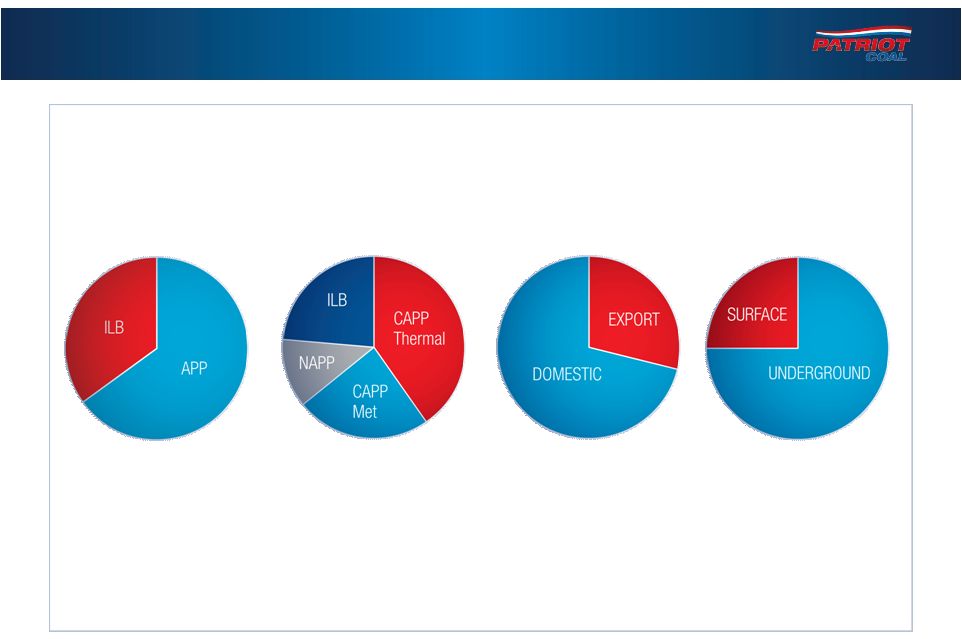

20

Product Diversification

Diverse locations, products & mining methods

Significant met & thermal coal exports

Mining

Method

YTD Sept ’11

Tons Sold

23.5 Million Tons

Reserves

1.9 Billion Tons

YTD Sept ’11

Shipments |

21

Multiple Basins & Coal Qualities

Northern Appalachia Thermal

Federal

Central Appalachia Metallurgical

Kanawha Eagle

Paint Creek/Winchester

Panther

Rocklick

Wells

Central Appalachia Thermal

Big Mountain

Blue Creek

Campbell’s Creek

Corridor G

Logan County

Illinois Basin Thermal

Bluegrass

Dodge Hill

Highland

Multiple quality & transportation options

Transportation Optionality

Rail

Barge

East Coast & Gulf exports |

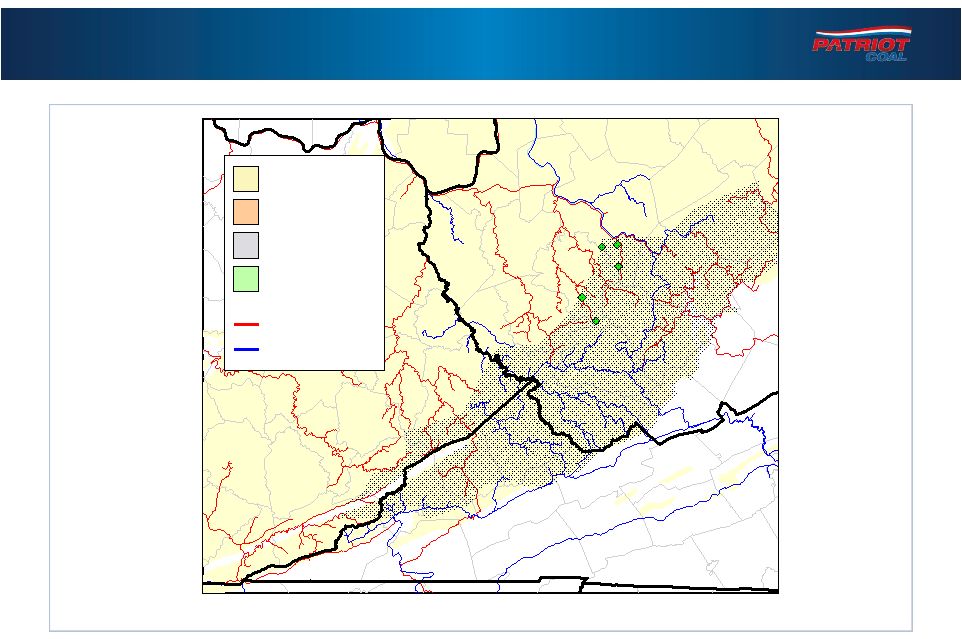

Patriot Met Coal

Complexes 22

Patriot produces premium high-volatile met coal

Rocklick

Wells

Winchester

Kanawha Eagle

Panther

Thermal

High-Vol

Mid-Vol

Low-Vol

CSX

NS |

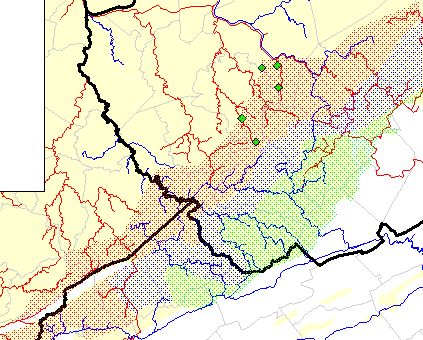

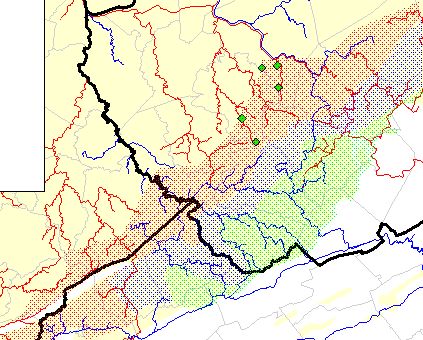

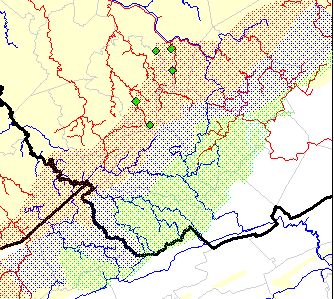

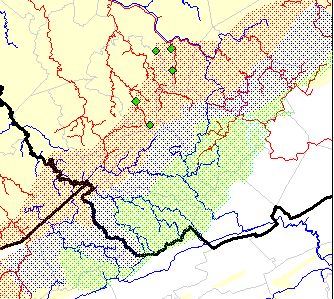

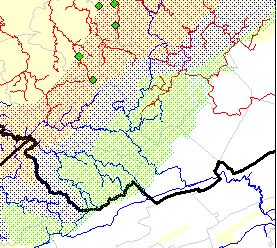

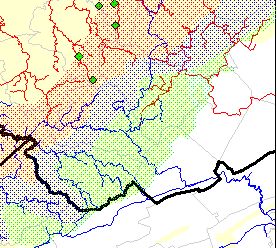

23

Opening new met mines to meet rising worldwide demand

Patriot Met Build-Out Program |

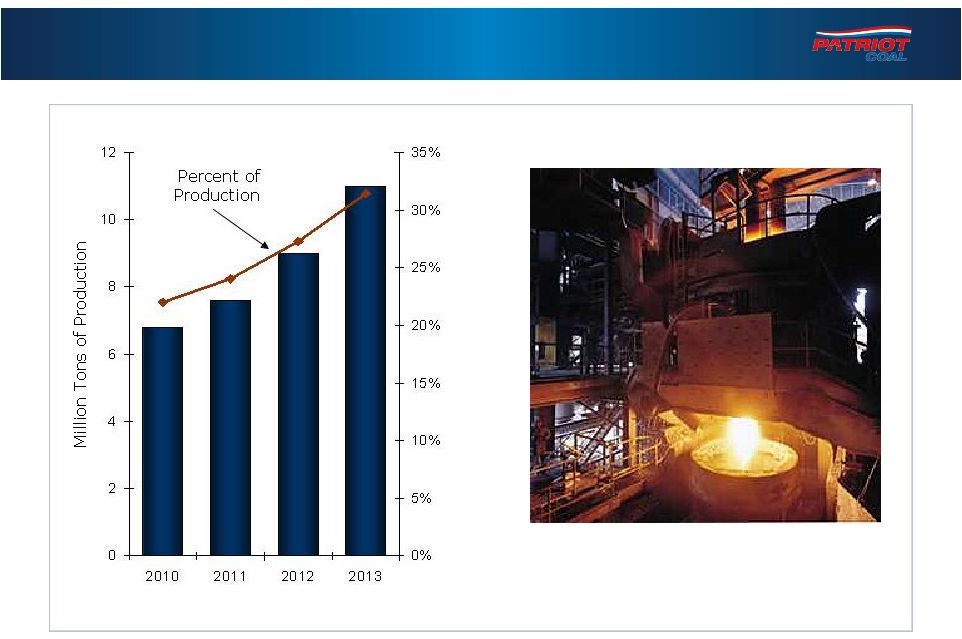

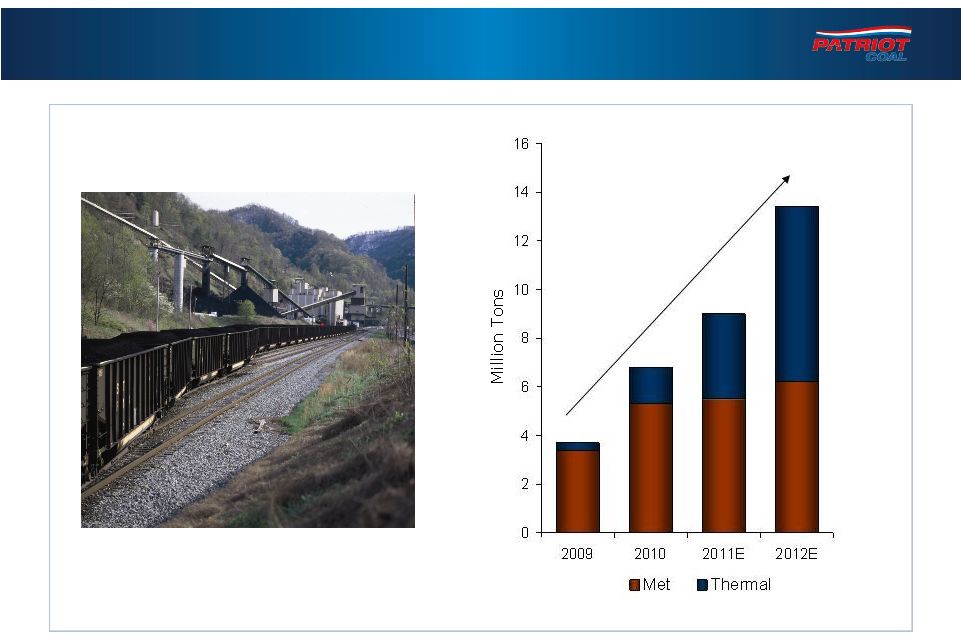

Increasing

Exports at Patriot Expect double-digit exports in 2012

+260% increase

24 |

Contact:

Janine Orf

Vice President –

Investor Relations

314.275.3680

jorf@patriotcoal.com

FINANCIAL COMMUNITY PRESENTATION

November 1, 2011

Met Coke World Summit 2011 |