Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SUSQUEHANNA BANCSHARES INC | d248623d8k.htm |

Exhibit 99.1 |

Susquehanna Bancshares, Inc.

Lititz, Pennsylvania

William J. Reuter –

Chairman and CEO

Drew K. Hostetter –

Chief Financial Officer

Michael M. Quick –

Chief Corporate Credit Officer |

Forward-Looking Statements

Forward-Looking Statements

During the course of this presentation, we may make projections and other

forward-looking statements regarding events or the future financial performance

of Susquehanna, including the impact of the acquisition of Abington

Bancorp and the planned acquisition of Tower Bancorp, as well as

projected

capital ratios, efficiency ratios, net income and earnings. We wish to

caution you that these forward-looking statements may differ materially

from actual results due to a number of risks and uncertainties. For a

more detailed description of the factors that may affect Susquehanna’s

operating results, we refer you to our filings with the Securities &

Exchange Commission, including our quarterly report on Form 10-Q for the

quarter ended June 30, 2011, and our annual report on Form 10-K for the

year ended December 31, 2010. Susquehanna assumes no obligation to update

the forward-looking statements made during this presentation.

For more information, please visit our Web site at:

www.susquehanna.net |

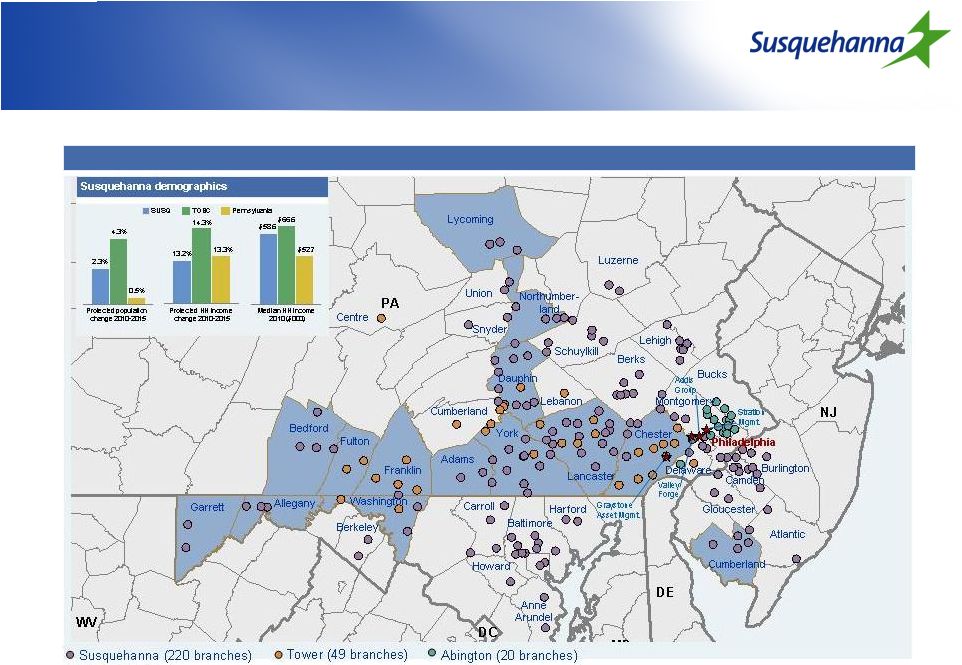

Geography

Susquehanna Profile

Susquehanna Profile

Overview

Size

Headquartered in Lititz, PA

Offers tailored products and services through its community bank, trust

and investment company, asset management, P&C insurance brokerage,

and leasing companies

240 branches in PA, NJ, MD, WV

$15.5 billion in assets

$10.3 billion in deposits

$6.1 billion in assets under management & administration

Shareholder

base

156.8 million shares outstanding

31,900 shareholders (record and street)

77% institutional holders

1 |

November

2008

Received

$300mm

TARP

preferred

equity

April 2002

Announced

acquisition

of Addis

Group

(Deal

value:

$17mm)

April 1998

Announced

acquisition

of Cardinal

Bancorp

(Deal

value:

$49mm)

April 1998

Announced

acquisition

of First

Capitol

Bank

(Deal

value:

$27mm)

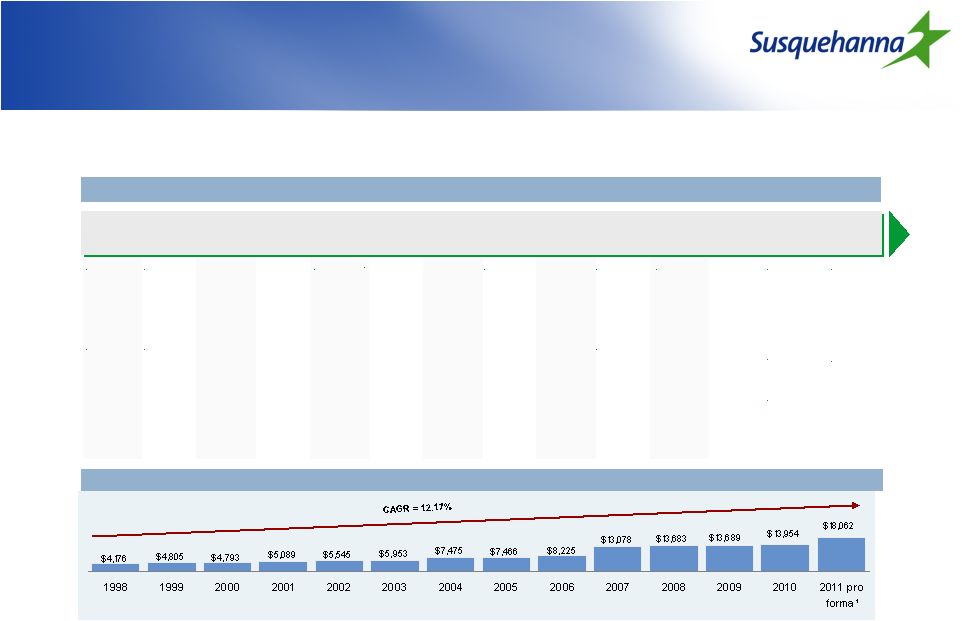

Susquehanna has built a strong

franchise over time

Susquehanna has built a strong

franchise over time

Assets ($ millions)

1998

2000

2001

November

1999

Announced

acquisition

of Hann

Finl. Corp.

(Deal value:

$42mm)

December

1999

Announced

acquisition

of Valley

Forge Asset

Mgmt

(Deal value:

$19mm)

2002

2004

December

2003

Announced

acquisition

of Patriot

Bank

(Deal value:

$210mm)

2006

2003

November

2005

Announced

acquisition

of Minotola

Bank

(Deal value

$166mm)

2005

2007

April 2007

Announced

acquisition

of

Community

Banks

(Deal value

$852mm)

December

2007

Announced

acquisition

of Stratton

Holding

Company

2008

2009

2010

2011

January

2011

Announced

acquisition

of Abington

Bancorp

(Deal value:

$268mm)

June 2011

Announced

acquisition

of Tower

Bancorp

(Deal value:

$345mm)

1999

Source: Company filings, FactSet, SNL Financial

¹

As of September 30, 2011; Pro forma for Abington and Tower acquisitions

2

March 2010

Raised

$345mm in

common

equity and

$50mm of

Trust

preferred

securities

April 2010

Repaid

$200mm

TARP

December

2010

Repaid the

remaining

$100mm

TARP |

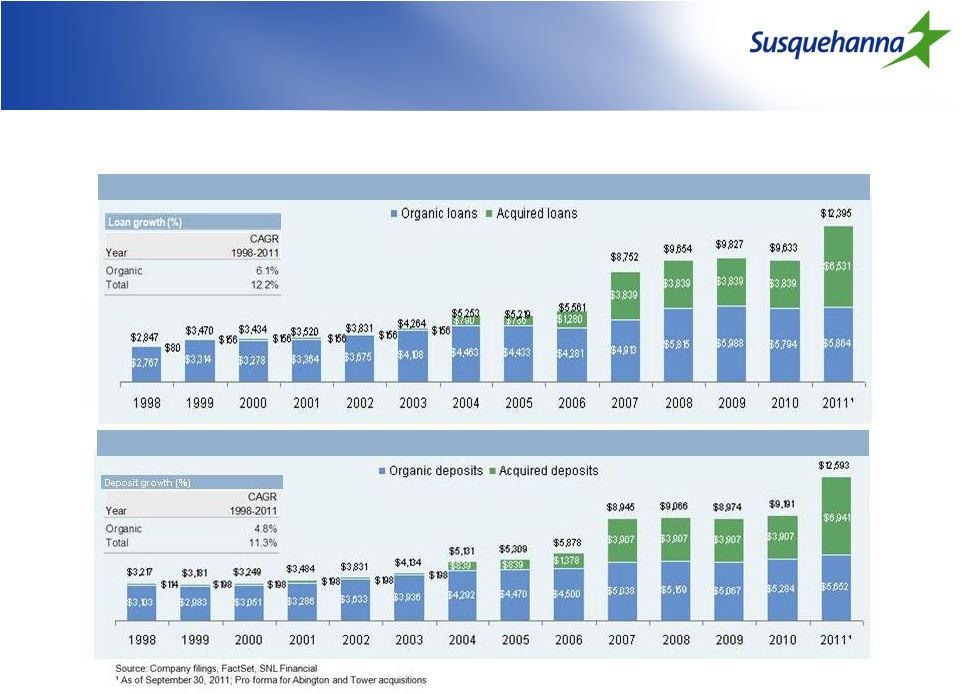

Strong

organic growth supported by acquisitions

Strong organic growth supported by

acquisitions

Loan growth ($mm)

Deposit growth ($mm)

3 |

Improved Market Position in Focus

Markets

Improved Market Position in Focus

Markets

Sorted by 2011 market rank

4

MSA

2005

2011

% Change

2005

2011

Change

Current Rank 1-3

Sunbury, PA

18.7%

21.7%

3.0%

1

1

Flat

Hagerstown-Martinsburg, MD-WV

19.0%

30.2%

11.2%

1

1

Flat

Lancaster, PA

12.9%

25.1%

12.2%

3

1

+ 2

Chambersburg, PA

13.4%

28.6%

15.2%

5

1

+ 4

Cumberland, MD-WV

24.8%

44.0%

19.2%

2

1

+ 1

Williamsport, PA

14.2%

13.1%

-1.1%

3

3

Flat

York-Hanover, PA

3.5%

12.7%

9.2%

11

3

+ 8

Gettysburg, PA

0.0%

10.3%

10.3%

N/A

3

N/A

Vineland-Millville-Bridgeton, NJ

0.0%

13.6%

13.6%

N/A

3

N/A

Current Rank 4-8

Selinsgrove, PA

8.4%

11.1%

2.7%

5

4

+ 1

Pottsville, PA

0.0%

10.6%

10.6%

N/A

4

N/A

Harrisburg-Carlisle, PA

0.0%

8.3%

8.3%

N/A

5

N/A

Baltimore-Towson, MD

2.0%

1.8%

-0.3%

9

7

+ 2

Lewisburg, PA

2.5%

2.2%

-0.3%

7

7

Flat

Atlantic City-Hammonton, NJ

0.0%

5.1%

5.1%

N/A

8

N/A

Philadelphia-Camden-Wilmington, PA-NJ-DE-MD

0.4%

2.2%

1.8%

24

8

+ 16

Reading, PA

2.9%

3.9%

1.0%

9

8

+ 1

Source: SNL Financial

MSA Rank by Market Share

Market Share |

Continues Susquehanna’s expansion

into attractive markets

Continues Susquehanna’s expansion

into attractive markets

5

Susquehanna pro forma¹

branch map

Source: SNL Financial

Note: Shaded counties indicate those in which Susquehanna holds a top 3 market

position ¹

Susquehanna pro forma includes Tower and Abington |

Few

independent players of scale Few independent players of scale

6

Deposit market share in Pennsylvania

Independent bank deposit market share in PA, MD, NJ

Source: SNL Financial

Note: Regulatory branch and deposit data as of June 30, 2011; banks and thrifts with

PA/MD/NJ deposits > 90% total deposits ¹

Susquehanna has 3 additional branches in West Virginia

Rank

Company

Deposits

% of Total DepositsBranches

1

Susquehanna (Proforma w/Tower)

$12.3

99%

2881

1

Fulton Financial Corp.

11.6

94%

252

2

Susquehanna Bancshares Inc.

10.2

99%

2391

3

Valley National Bancorp

8.1

83%

173

4

F.N.B. Corp.

7.1

96%

236

5

Investors Bancorp Inc. (MHC)

6.8

98%

78

6

National Penn Bancshares Inc.

6.0

100%

129

7

Northwest Bancshares Inc.

5.3

88%

148

8

Provident Financial Services Inc.

5.0

100%

83

9

First Commonwealth Financial Corp.

4.6

100%

112

10

Beneficial Mutual Bancorp Inc. (MHC)

3.8

100%

60

11

S&T Bancorp Inc.

3.3

100%

50

12

Dollar Bank Federal Savings Bank

3.2

66%

36

13

Sun Bancorp Inc.

2.8

100%

63

14

Sandy Spring Bancorp Inc.

2.4

92%

37

15

Lakeland Bancorp Inc.

2.2

100%

48

16

Tower Bancorp Inc.

2.2

100%

49

17

Kearny Financial Corp. (MHC)

2.2

100%

41

18

Firstrust Savings Bank

1.9

100%

24

19

Metro Bancorp Inc.

1.9

100%

33

Total PA / MD / NJ

Rank

Company

Branches

Deposits

($MM)

Market

Share (%)

1

PNC Financial Services Group Inc.

509

$ 62,259

20.7%

2

Wells Fargo & Co.

294

36,133

12.0%

3

Royal Bank of Scotland Group Plc

386

24,688

8.2%

4

Banco Santander SA

169

11,047

3.7%

5

Toronto-Dominion Bank

95

10,981

3.7%

6

Bank of New York Mellon Corp.

6

9,317

3.1%

7

Susquehanna Bancshares Inc. (Proforma w/Tower)

214

8,908

3.0%

7

M&T Bank Corp.

205

8,468

2.8%

8

Bank of America Corp.

99

8,253

2.8%

9

Fulton Financial Corp.

135

7,259

2.4%

10

F.N.B. Corp.

237

7,110

2.4%

11

Susquehanna Bancshares Inc.

167

6,821

2.3%

12

First Niagara Financial Group Inc.

136

6,450

2.2%

13

National Penn Bancshares Inc.

128

5,991

2.0%

14

Northwest Bancshares Inc.

143

4,997

1.7%

15

First Commonwealth Financial Corp.

112

4,556

1.5%

16

S&T Bancorp Inc.

50

3,365

1.1%

17

Dollar Bank Federal Savings Bank

36

3,204

1.1%

18

Huntington Bancshares Inc.

62

2,905

1.0%

19

Beneficial Mutual Bancorp Inc. (MHC)

35

2,237

0.7%

20

Tower Bancorp Inc.

47

2,087

0.7% |

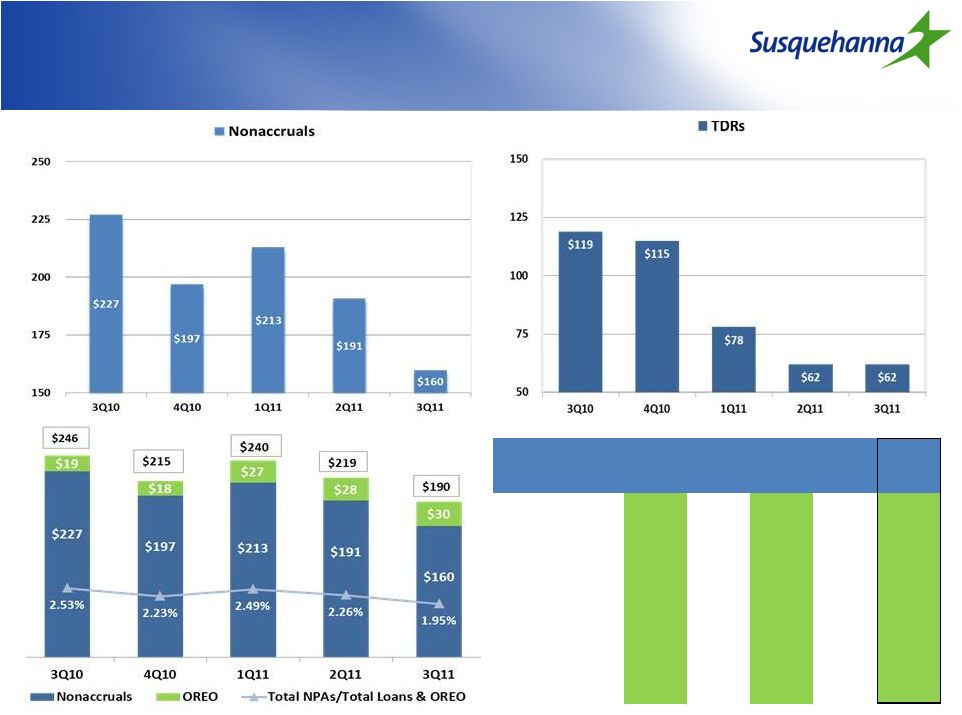

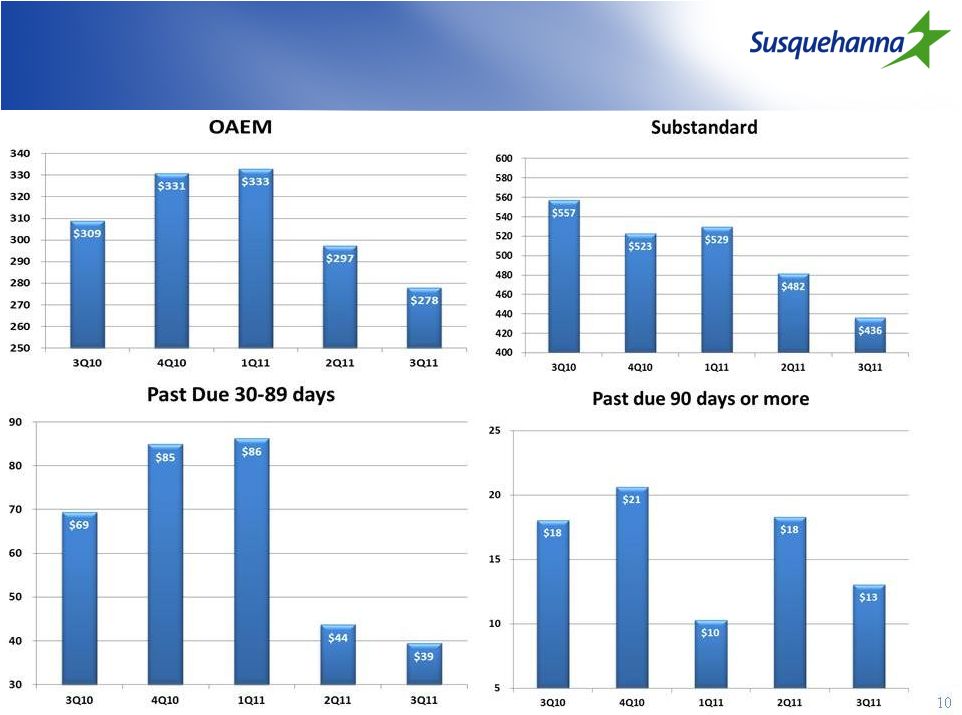

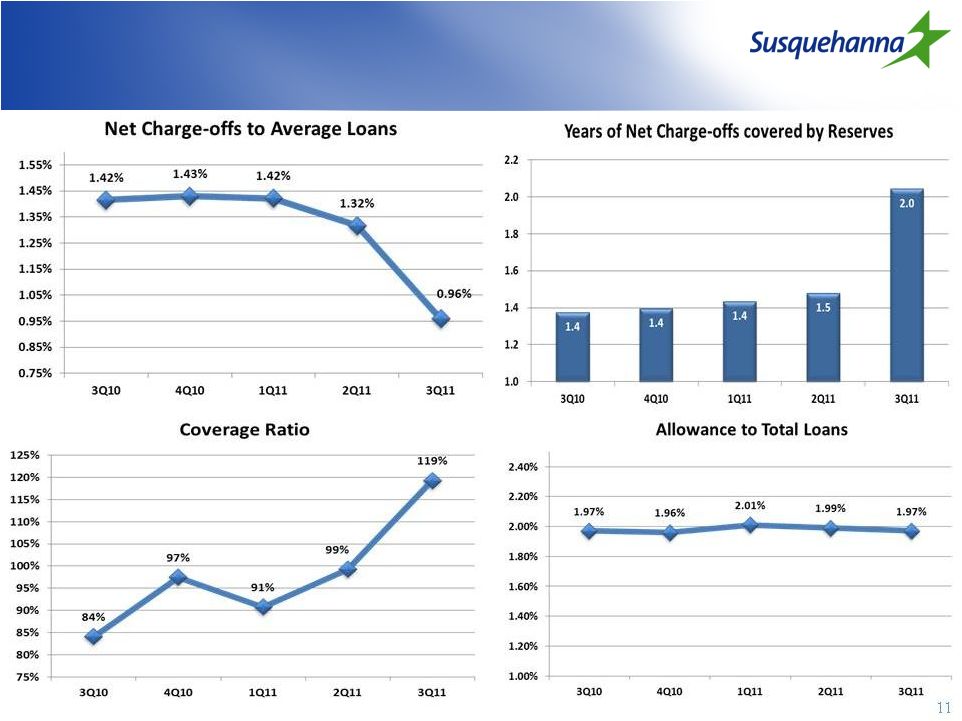

Third

Quarter Financial Highlights Third Quarter Financial Highlights

Significant Improvement in Credit Quality

NCO/Average Loans = 0.96%, 1

st

time below 1.00% since economic downturn

NPA/Loans & OREO = 1.95%, 1

st

time below 2.00% since economic downturn

Negative NPA Generation of $6M, 1

st

time negative since economic downturn

Loan portfolio contraction halted, as net loans & leases grew 1%

from prior

quarter

Core deposits increased 5.6% from prior quarter and 9.0% from prior year

Strong capital position that meets fully-phased-in requirements of Basel

III 7 |

Quarterly Loan Originations

Quarterly Loan Originations

8

Average

Balance

($ in Millions)

Balance

Originations

Balance

Originations

Balance

Originations

Balance

Originations

Balance

Originations

Commercial

1,632

91

1,609

106

1,558

63

1,549

120

1,531

154

Real Estate -

Const & Land

848

53

818

56

805

53

750

49

728

63

Real Estate -

1-4 Family Res

1,526

13

1,470

21

1,428

34

1,410

38

1,413

55

Real Estate -

Commercial

3,342

57

3,280

81

3,262

84

3,286

146

3,264

108

Real Estate -

HELOC

646

83

714

103

760

60

802

66

842

68

Tax-Free

253

17

245

10

292

58

305

12

317

7

Consumer Loans

565

35

589

31

612

33

646

44

685

45

VIE

227

-

219

-

214

-

206

-

201

-

Total

9,039

$

349

$

8,944

$

408

$

8,931

$

385

$

8,954

$

475

$

8,981

$

500

$

3Q10

4Q10

1Q11

2Q11

3Q11 |

Asset

Quality ($ in Millions)

Asset Quality

($ in Millions)

9

($ in millions)

3Q10

4Q10

1Q11

2Q11

3Q11

NPL's Beginning of Period

237.4

$

227.4

$

196.9

$

212.9

$

190.7

$

-

New NonAccruals

37.3

$

43.6

$

61.2

$

23.4

$

20.4

$

-

Cure/Exits/Other

(23.0)

$

(36.3)

$

(4.7)

$

(13.5)

$

(28.8)

$

-

Gross Charge-Offs

(17.7)

$

(25.9)

$

(27.4)

$

(21.7)

$

(14.8)

$

-

Transfer to OREO

(6.5)

$

(11.9)

$

(13.0)

$

(10.4)

$

(7.5)

$

NPL's End of Period

227.4

$

196.9

$

212.9

$

190.7

$

160.1

$ |

Asset

Quality ($ in Millions)

Asset Quality

($ in Millions) |

Asset

Quality Asset Quality |

Capital Ratios

Capital Ratios

Pro Forma

3/31/2012

At

9/30/2011

At

12/31/2010

Management Target

Tangible Common Equity

8.10%

7.74%

7.57%

7.50%

Tier 1 Common/RWA

10.20%

9.81%

9.58%

8.00%

Leverage

10.20%

10.39%

10.27%

6.00%

Tier 1 Risk-Based

12.60%

12.86%

12.65%

9.50%

Total Risk-Based

15.10%

14.93%

14.72%

11.50%

Capital at

3/31/2012

($ in millions)

Excess Over

Management Target

($ in millions)

Tangible Common Equity

$1,375

$ 97

Tier 1 Common Equity

1,397

295

Leverage

1,730

710

Tier 1 Capital

1,730

422

Total Risk-Based Capital

2,079

495

12 |

Efficiency Ratio

Efficiency Ratio

Key Initiatives

Abington Cost Saves of $8.0MM

Tower Cost Saves of $30.0MM

Susquehanna Cost Saves of $20.0MM

13

* Efficiency Ratio based on SNL Methodology |

Net

Income Net Income

14 |

Earnings Drivers

Earnings Drivers

15

($000)

3Q10

4Q10

1Q11

2Q11

3Q11

Q Average

2013

Avg. interest-earning assets

$12,070,477

$12,084,056

$12,141,223

$12,171,868

$12,275,793

$17,272,600

Net interest margin (FTE)

3.58%

3.61%

3.63%

3.62%

3.58%

3.52%

Net interest income

105,411

106,573

105,023

106,086

106,839

146,575

Noninterest income

35,407

39,788

37,467

37,054

36,800

44,975

Total revenue

140,818

146,361

142,490

143,140

143,639

191,550

Noninterest expense

96,212

95,971

95,883

101,157

100,745

113,900

Pre-tax, pre-provision income

44,606

50,390

46,607

41,983

42,894

77,650

Provision for loan losses

40,000

35,000

35,000

28,000

25,000

12,000

Pre-tax income

$4,606

$15,390

$11,607

$13,983

$17,894

$65,650 |

Investment Securities

Investment Securities

$ in millions

EOP Balance

QTR Yield

3Q10

4Q10

1Q11

2Q11

3Q11

Total Investment Securities

$2,372

$2,418

$2,480

$2,624

$2,700

Duration (years)

3.5

4.2

4.2

3.9

3.6

Yield

3.64%

3.73%

3.73%

3.61%

3.32%

Unrealized Gain/(Loss)

$36.7

($19.9)

($7.9)

$25.5

$42.0

16 |

Loan

Mix & Yield Loan Mix & Yield

17

$ in millions

Avg Bal QTR

INT % QTR

LOANS

Commercial

1,632

5.39%

1,609

5.33%

1,558

5.31%

1,549

5.10%

1,531

5.38%

Real Estate -

Const & Land

848

4.71%

818

4.75%

805

4.62%

750

4.74%

728

4.74%

Real Estate -

1-4 Family Res

1,526

5.99%

1,470

5.99%

1,428

5.93%

1,410

5.89%

1,413

5.81%

Real Estate -

Commercial

3,342

5.63%

3,280

5.67%

3,262

5.54%

3,286

5.51%

3,264

5.47%

Real Estate -

HELOC

646

3.69%

714

3.68%

760

3.65%

802

3.61%

842

3.60%

Tax-Free

253

6.20%

245

5.74%

292

5.74%

305

5.62%

317

6.06%

Consumer Loans

565

6.31%

589

6.31%

612

6.19%

646

6.18%

685

5.61%

Commercial Leases

274

8.09%

275

8.15%

267

8.28%

276

8.11%

285

7.92%

Consumer Leases

408

5.40%

389

5.35%

386

5.36%

390

5.13%

380

4.90%

VIE

227

4.74%

219

4.71%

214

4.67%

206

4.62%

201

4.58%

Total Loans

9,721

5.53%

9,608

5.51%

9,584

5.43%

9,620

5.37%

9,646

5.34%

3Q10

4Q10

1Q11

2Q11

3Q11 |

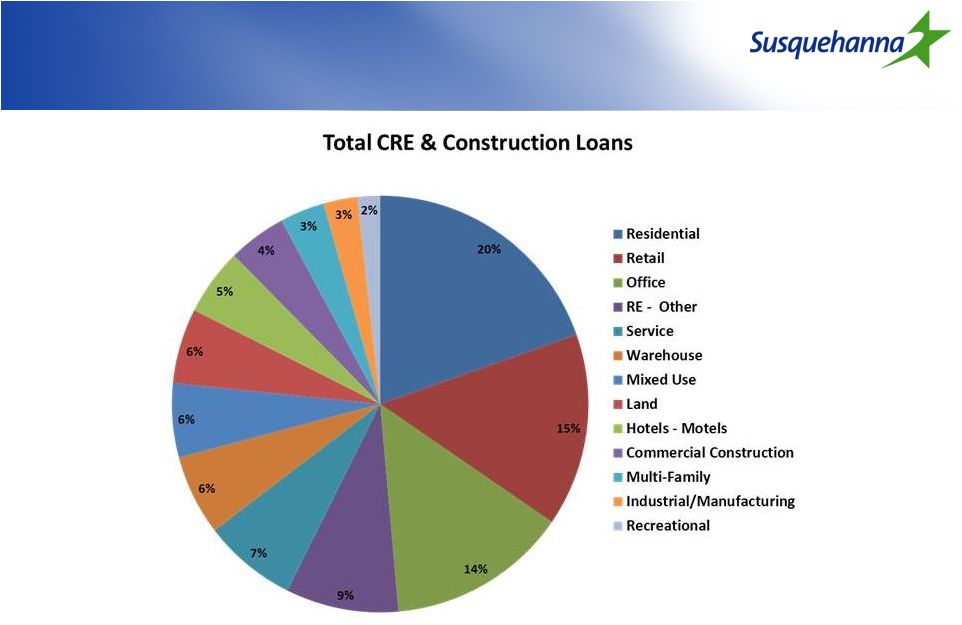

Collateral Type Distribution of

CRE -

3Q11

Collateral Type Distribution of

CRE -

3Q11

18 |

Deposit Mix & Cost by Product

Deposit Mix & Cost by Product

19

$ in millions

Avg Bal QTR

INT % QTR

Deposits

Demand

1,341

0.00%

1,380

0.00%

1,340

0.00%

1,382

0.00%

1,401

0.00%

Interest Bearing Demand

3,487

0.62%

3,638

0.62%

3,687

0.61%

3,653

0.58%

3,797

0.52%

Savings

770

0.15%

765

0.15%

780

0.15%

807

0.15%

797

0.14%

Certificates of Deposits

3,607

2.11%

3,470

2.00%

3,436

1.79%

3,501

1.62%

3,491

1.55%

Total Interest-Bearing Deposits

7,864

1.26%

7,873

1.18%

7,903

1.08%

7,961

0.99%

8,085

0.93%

Core Deposits/Total

60.8%

62.5%

62.8%

62.5%

63.2%

Loans(excluding VIE)/Deposits

103.1%

101.5%

101.4%

100.8%

99.6%

3Q10

4Q10

1Q11

2Q11

3Q11 |

Borrowing Mix & Cost

Borrowing Mix & Cost

20

$ in millions

Avg Bal QTR

INT % QTR

Borrowings

Short-Term Borrowings

590

0.38%

604

0.38%

748

0.33%

668

0.31%

632

0.32%

.

FHLB Advances

1117

3.99%

1105

3.19%

1100

3.09%

1116

2.91%

1,115

2.90%

Long Term Debt

719

5.09%

712

5.09%

701

5.24%

691

5.03%

679

4.78%

Total Borrowings

2,426

3.44%

2,421

3.05%

2,549

2.87%

2,475

2.80%

2,426

2.75%

Off Balance Sheet Swap Impact

525

0.17%

525

0.57%

525

0.54%

625

0.68%

675

0.76%

Total Borrowings Cost

2,426

3.61%

2,421

3.62%

2,549

3.41%

2,475

3.48%

2,426

3.51%

Avg Borrowings/Avg Total Assets

17.4%

17.3%

18.3%

17.6%

17.1%

3Q10

4Q10

1Q11

2Q11

3Q11 |

Strategic Objectives for 2011-2012

Strategic Objectives for 2011-2012

Continuing strong progress in improving credit quality

Completing acquisition and integration of Tower Bancorp

Growing loans, deposits and revenue

Increasing profitability and shareholder dividends

21 |

Appendix |

Strategic Acquisition of

Abington Bancorp |

Transaction Highlights

Transaction Highlights

Strong Strategic

Rationale

Attractive Financial

Returns

Low Risk

Low-risk fill-in acquisition of an in-market community bank in

Montgomery and Bucks counties

—

Adds 20 branches and $900mm of deposits; no branch overlap

Strengthens presence in attractive Montgomery and Delaware counties and provides

entry into Bucks County

—

Top 10 market share in Montgomery County –

20

th

wealthiest in U.S.

—

3 counties rank among top 5 highest HHI in PA

Tremendous opportunity for deposit, loan and fee income growth

—

Wealth management and insurance subsidiaries (Valley Forge, Stratton, and

Addis) located in Montgomery County with strong customer contacts

—

Expand Susquehanna’s in-market mortgage origination capability

—

Potential for commercial loan growth

20% IRR

100bps accretive to Tier I common at close

Breakeven to 2012 EPS, without considering benefits of excess capital

Comprehensive due diligence process

In-market transaction with similar demographics

Proven track record of integrating acquisitions

A -

1 |

Pro

Forma Financial Impact Pro Forma Financial Impact

Attractive financial returns:

20% IRR

60 bps accretive to TCE and 100bps to Tier I common

Breakeven accretion to SUSQ normalized EPS without considering any benefit from

excess capital; 3% accretive to SUSQ current 2012 median analyst

estimate¹ Tangible book value dilution less than 2%

Strong pro forma capital position (approximately $95mm capital accretive):

Assumptions:

8.5% cumulative lifetime credit losses through the cycle (since 2008)

Cost savings of $8.1mm or 31%², phased in 50% in 2011 and 100% in 2012

One time pre-tax restructuring charge of $21mm

A -

2

12/31/2010

Actual (%)

Pro forma (%)

TCE/TA

7.6%

8.2%

Tier I common

9.6%

10.6%

Tier I

12.7%

13.5%

Note: Based on SUSQ and ABBC stock prices at announcement

¹

Susquehanna normalized analyst estimate of $0.80 and 2012 analyst estimate of

$0.66 ²

Excluding stock based compensation expenses, core cost synergies are approximately

24% of non interest expenses |

Pricing Metrics

Pricing Metrics

Based on Jan. 26, 2011

(Announcement date)

1 day

Deal price per share ($)

$12.80

Implied premium (%)

10.3%

Price / 4Q net income (adjusted for excess capital)¹

24.1x

Price / Tangible book value

1.2x

Price / Adjusted tangible book value²

1.3x

Core deposit premium³

8.2%

Memo:

Susquehanna price per share ($)

$9.70

Financial information as of December 31, 2010

¹4Q 2010 net income annualized; price and earnings adjusted for excess capital of $95mm; assumes

1% pre-tax earnings on excess capital ²Adjusted for credit marks of $31mm and loan loss

reserve of $4mm ³ Core deposits of $680 excludes time deposits >$100mm

A -

3 |

Strategic Acquisition of Tower

Bancorp |

Transaction highlights

Transaction highlights

Strong Strategic

Rationale

Superior Financial

Returns

Low Risk

Acquisition of an in-market, growth oriented community bank with favorable

demographics in central and southeastern Pennsylvania with $2.2bn of

deposits Strengthens presence in attractive Chester County while

building scale in Lancaster and

Harrisburg

—

Top 3 market share in Chester County –

wealthiest in PA

Tremendous opportunity for deposit, loan and fee income growth

—

Attractive wealth management division, headquartered in Chester County with

$560mm AUM

—

Small business lending expertise

—

Complementary loan and deposit mix

Seasoned management team with a record of achieving growth

Deploys excess capital generated from Abington acquisition

Approximately 25% IRR

10% accretive to 2013 EPS

Tangible book value earn-back of ~5 years

Comprehensive due diligence process

In-market transaction

Proven track record of integrating acquisitions

Strong pro forma capital and balance sheet

A -

4 |

Consideration:

Fixed exchange ratio of 3.4696x (resulting in approximately 30.8 million

shares issued based on assumed Tower outstanding shares)

Fixed cash amount of $88mm

75% stock and 25% cash¹

Implied transaction value:¹

$345mm

Implied price per share:¹

$28.69 / Premium to closing price: 41%

Board composition:

Tower receives 3 seats on the pro forma 20 member Board of Directors

(including Abington transaction), and including 1 seat on the Executive

Committee

Due diligence:

Completed

Management

Andrew Samuel (Tower CEO) will become President and Chief Revenue

Officer of Susquehanna and will be appointed to the Susquehanna Board;

Jeffrey Renninger (Tower President & COO) and Janak Amin (CEO of

Graystone Tower Bank) to assume senior management positions at

Susquehanna Bank

Required approval:

Regulatory approval required

Shareholder approval required for SUSQ and TOBC

Termination fee:

$13.5mm (reflects 4% of transaction)

Anticipated closing:

1Q 2012

Transaction overview

Transaction overview

1

Based on Susquehanna stock price as of June 20, 2011; based on diluted shares of

12.0mm A -

5 |

Financial impact –

cost saves

Financial impact –

cost saves

($mm)

Cost savings of approximately 34% of Tower’s non-interest

expense¹ Driven by consolidation of branch network of Susquehanna and

Tower; approximately 25 branch closings anticipated between Susquehanna and

Tower History of deposit retention in prior acquisitions

Proven track record of delivery on cost savings

Compensation and benefits

$20.1

Occupancy

3.8

Systems and technology

2.2

Professional fees

0.9

Marketing & other

3.1

Total cost saves (pre-tax)

$30.0

One-time restructuring charge (pre-tax)

$63.0

A -

6

¹

Based on Tower’s core Q1 2011 non-interest expense annualized

|

Pricing metrics

Pricing metrics

A -

7

Tower acquisition

Precedent transactions2

Deal price per share ($)

$28.69

Implied premium

41%

24% - 57%

Price to 2012 EPS (IBES)

15.1x

Price to 2013 EPS (IBES)

12.8x

Price to tangible book value

1.5x

1.6x - 1.9x

Core deposit premium¹

6%

9% - 14%

Memo:

Susquehanna price per share

$8.34

Note: Financial information as of March 31, 2011; based on market data as of June 20, 2011

1

Core deposits of $1.9bn excludes time deposits of greater than $100k

2

Precedent transactions include First Niagara/NewAlliance, People's United/Danvers, Brookline/Bank of

Rhode Island and Valley/State |

3/31/2011

Pro forma

Current (%)

Pro forma ABBC (%)²

TOBC & ABBC (%)²

TCE / TA¹

7.7%

8.4%

7.8%

Tier I common

9.7%

10.5%

9.7%

Tier I capital

12.8%

13.5%

12.3%

Pro-forma financial impact

Pro-forma financial impact

Superior financial returns:

IRR of approximately 25%

Immediately accretive to EPS; 10% accretive to 2013 EPS

Tangible book value earn-back in ~5 years

Strong pro-forma capital position:

Assumptions:

Cost savings of $30mm, phased in 75% in 2012 and 100% in 2013; no revenue

synergies assumed One time pre-tax costs of $63mm

Core deposit intangibles of $22mm, amortized over 10 years

A -

8

¹

Includes deferred tax liabilities associated with intangibles

²

Pro forma adjustments assuming SUSQ share price as of June 20, 2011

|

Summary

Summary

A -

9

Expands Susquehanna’s footprint into highly attractive markets and

increases scale in existing markets

Superior financial returns; significant synergy potential

Considerable opportunity for small business lending and fee income

generation by delivering on Susquehanna’s full-service platform

Gain experienced, growth oriented management team with extensive

in-market knowledge |

Additional information about the

merger and where to find it

Additional information about the

merger and where to find it

In connection with the proposed merger, Susquehanna has filed a registration

statement on Form S-4 with the SEC on October 3, 2011, which contains a

joint proxy statement/prospectus of Susquehanna and Tower. The companies

will file with the SEC other relevant materials in connection with the merger and have mailed

the joint proxy statement/prospectus to their respective shareholders.

Investors and security holders of Susquehanna and Tower are urged to read the

proxy statement/prospectus and the other relevant materials because they

contain important information about Tower, Susquehanna and the merger. The

joint proxy statement/prospectus and other relevant materials and any other documents filed by

Susquehanna or Tower with the SEC, may be obtained free of charge at the SEC’s

Web site at http://www.sec.gov.

In addition, investors and security holders may obtain free copies of the documents

filed with the SEC by Tower by contacting Brent Smith, Tower Bancorp, Inc.,

telephone: 717-724-4666 or from Tower’s Web site at

www.towerbancorp.com. Investors and security holders may obtain free copies of the

documents filed with the SEC by Susquehanna by contacting Abram G. Koser, Susquehanna

Bancshares, Inc., 26 North Cedar Street, Lititz, PA 17543, telephone:

717-626-4721 or from Susquehanna’s web site at

www.susquehanna.net.

Susquehanna, Tower and their respective directors, executive officers and certain

other members of management and employees may be deemed

“participants” in the solicitation of proxies from shareholders of

Susquehanna and Tower in favor of the merger.

Information regarding the persons who may, under the rules of

the SEC, be considered participants in the solicitation of the shareholders of

Susquehanna and Tower in connection with the proposed merger will be set forth

in the joint proxy statement/prospectus when it is filed with the SEC. You can

find information about the executive officers and directors of Susquehanna in its Annual

Report on Form 10-K for the year ended December 31, 2010 and in its definitive

proxy statement filed with the SEC on March 18, 2011. You can find information

about Tower’s executive officers and directors in its Annual Report on

Form 10-K for the year ended December 31, 2010 and in its definitive proxy statement filed with the

SEC on April 8, 2011. |