Attached files

| file | filename |

|---|---|

| 8-K - 8-K - PVF CAPITAL CORP | d247725d8k.htm |

Continued Turnaround Progress

October 26, 2011

Celebrating Over 90 Years of Community Banking.

Exhibit 99.1 |

2

Safe

Harbor

Cautionary Note Regarding Forward-Looking Statements:

This presentation contains statements that are forward-looking, as that term is

defined by the Private Securities Litigation Act of 1995 or the Securities

and Exchange Commission in its rules, regulations and releases. PVF Capital

Corp. (the “Company”) intends that such forward- looking

statements be subject to the safe harbors created thereby. All forward-looking

statements are based on current expectation regarding important risk factors

including, but not limited to, interest rate changes, real estate values,

continued softening in the economy, which

could

materially

impact

credit

quality

trends

and

the

ability

to

generate

loans,

changes

in

the

mix of the Company’s business, competitive pressures, changes in accounting,

tax or regulatory practices or requirements and those risk factors detailed

in the Company’s periodic reports and registration statements filed

with the Securities and Exchange Commission. Accordingly, actual results may

differ from those expressed in the forward-looking statements, and the

making of such statements should not be regarded as a representation by the

Company or any other person that results expressed therein will be achieved. This

presentation contains time-sensitive information that reflects

management’s best analysis only as of the date hereof.

The

Company

does

not

undertake

an

obligation

to

publicly

update

or

revise

any

forward-looking statements to reflect new events, information or circumstances,

or otherwise. Further information concerning issues that could materially

affect financial performance related to forward-looking statements can

be found in the Company’s periodic filings with the Securities and

Exchange Commission. |

3

Use

of

Non-GAAP Financial

Measures

•

This presentation includes certain financial information determined by methods

other than in accordance with generally accepted accounting principles in

the United States (“GAAP”). One non-GAAP performance metric that

management believes is useful in analyzing underlying performance trends is

pre-tax, pre-credit provision income. This is the level of earnings

adjusted to exclude the impact of: –

provision expense and credit related charges involving the valuation and

disposition of other real estate owned, which are excluded because its

absolute level is elevated and volatile in times of economic stress;

–

available-for-sale and other securities gains/losses, which are excluded

because in times of economic stress securities market valuations may also

become particularly volatile; and –

certain

items

identified

by

management

to

be

outside

of

ordinary

banking

activities,

and/or

by

items

that,

while

they may be associated with ordinary banking activities, are so unusually large

that their outsized impact is believed by management at the time to be

infrequent or short-term in nature, which management believes may

distort the Company’s underlying performance trends.

•

Non-GAAP measures are not in accordance with, nor are they a substitute for,

GAAP measures. The Company’s non-GAAP financial measures are not

meant to be considered in isolation or as a substitute for the comparable

GAAP financial measures, and should be read only in conjunction with the

Company’s consolidated financial statements prepared in accordance with

GAAP. While the Company believes that non-GAAP financial measures

provide useful supplemental information to investors, there are very significant

limitations associated with their use. Non-GAAP financial measures are

not prepared in accordance with GAAP, may not be reported by all of the

Company’s competitors and may not be directly comparable to similarly titled

measures of the Company’s competitors

due

to

potential

differences

in

the

exact

methods

of

calculation.

The

Company

compensates

for

these

limitations by using these non-GAAP financial measures as supplements to GAAP

financial measures and by reviewing the reconciliations of the non-GAAP

financial measures to their most comparable GAAP financial measures.

•

A

reconciliation

of

non-GAAP

financial

measures

with

GAAP

financial

measures

is

attached

to

the

end

of

this

presentation. |

4

Mission Statement

Our mission is to become the financial institution of choice in

Northeast Ohio.

We will accomplish this with high quality people dedicated to

serving our customers, shareholders and the communities in

which we operate.

We will offer high quality products and services to better serve

consumers and businesses. |

5

Priorities

Improve operating performance and trends.

Address regulatory order.

Improve asset quality.

Enhance revenue generation.

Improve infrastructure.

Expand and enhance products and services.

Strengthen the depth of talent. |

6

Net loss of $9.7 million ($0.38 per share) for the fiscal year ended

June 30, 2011.

Earnings improvement constrained by the economic environment and

credit related costs.

Pre-tax, pre-provision income of $4.5 million in fiscal 2011 compared

with $1.6 million in fiscal 2010, excluding $17.6 million gain on debt

cancellation.

Strong mortgage banking activities in 2011 from a continued lower rate

environment. Mortgage revenue $2.0 million higher than prior fiscal year.

Net interest margin improvement of 40 basis points over prior fiscal year to

2.95%, with improved liquidity position and reduction in overall

risk profile.

Successfully managed expenses while accelerating problem asset

resolution, improving the infrastructure, and investing in personnel to

expand the business lines as part of our transition.

Financial Results |

7

Strengthen Balance Sheet

Repaid the $50 million repurchase agreement while maintaining a strong

liquidity position. This resulted in continued improvement in the risk profile

of the balance sheet.

Retired

the

remaining

brokered

deposits

while

maintaining

strong

core

deposit levels.

Sold a portion of the mortgage-backed securities portfolio which boosted

non-interest income by $1.2 million. |

8

Address Regulatory Order

October 2009, entered into an agreement with the Office of Thrift

Supervision (OTS) which required PVFC and the bank to:

By 12/31/09 -

meet and maintain core capital of at least 8.0% and total

risk-based capital of at least 12.0%.

By 12/31/10 -

reduce adversely classified assets to no more than 50%

of core capital plus the Allowance for Loan and Lease Losses (ALLL).

By 12/31/10 -

reduce adversely classified assets and assets designated

as special mention to no more than 65% of core capital plus ALLL.

|

9

Address Regulatory Order

At 6/30/11, Park View’s capital ratios remained strong and exceeded

prescribed regulatory levels.

The ratios were as follows:

6/30/2011

Requirement

Core Capital

8.63%

8.00%

Total Risk-Based Capital

12.87%

12.00% |

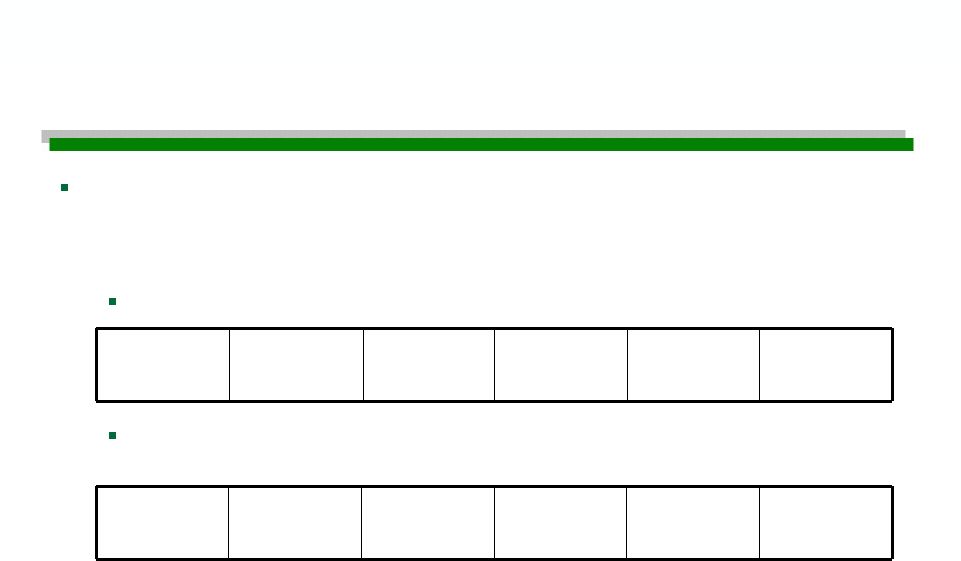

10

Address Regulatory Order

The Company continues progress toward achieving the adversely

classified assets ratios prescribed by regulators.

Asset quality ratios have improved as follows:

Adversely Classified Assets to Core Capital plus ALLL:

Adversely Classified Assets plus Assets Designated as Special

Mention to Core Capital plus ALLL:

*Ratios when factoring an additional $3 million of available capital.

Target

50.00%

6/30/10

88.60%

12/31/10

73.83%

6/30/11

68.60%

9/30/11

65.72%

9/30/11*

63.46%

Target

65.00%

6/30/10

117.32%

12/31/10

96.44%

6/30/11

87.80%

9/30/11

84.78%

9/30/11*

81.86% |

11

Address Regulatory Order

We continue to maintain a positive relationship with our regulators

following the transition this past July from the Office of Thrift

Supervision (OTS) to the Office of the Comptroller of the Currency

(OCC), for supervisory oversight for the Bank, and to the Federal

Reserve Bank (FRB) for supervisory oversight for PVF Capital Corp.

|

12

Improve Asset Quality

Have established targeted reduction plans relative to problem

assets.

Non-performing assets declined 25% during fiscal 2011.

Significant progress made toward our objective of meeting the

requirements of the regulatory order. Our objective is to meet the

regulatory target asset quality metrics by June 30, 2012.

|

13

Enhance Revenue Generation

Broadened our product offerings to generate revenue, enhance long-term

profitable

growth

and

strengthen

our

position

in

the

marketplace

as

a

community bank.

Expanded commercial banking and small business lending capabilities.

Initiated a focused SBA lending effort that is already generating revenue.

Continued to expand our residential mortgage product offerings and

improve delivery.

Introduced a completely new line of consumer and business products

including Treasury Management and Private Banking services.

Launched a newly redesigned website.

Introduced Park View Online, a new online banking and bill pay platform

with enhanced consumer and business capabilities.

Sales force emphasis to cross-sell products and services in order to deepen

customer relationships. |

14

Improve Infrastructure

Infrastructure enhancements include systems, products and services.

Systems:

Successful transition from a hosted to a service bureau environment with

the same core system provider.

New modules –

program/software upgrades to streamline and enhance

operations.

We continue to dramatically reduce the customization in our systems and

processes.

We continue to invest in our operating systems to streamline processes,

enhance performance and improve efficiencies. |

15

Expand and Enhance

Products and Services

Products and Services:

Online Banking

We recently introduced Park View Online, a new and enhanced online

banking and bill pay platform that will offer additional capabilities to our

business and retail customers.

Consumer products

Improved checking and savings accounts

FHA purchase and refinance loans

Enhanced home equity line of credit product

New business and Treasury Management products

Checking and savings accounts, including account analysis

SBA loans

ACH collections and disbursements through online banking

Wire Transfers through online banking

Remote Deposit Capture

Line of Credit Sweep product |

16

Expand and Enhance

Products and Services

Future enhancements will include:

Online, real-time ATM and Debit Card capabilities

New nationwide ATM network (NYCE) and ATM machines

Mobile banking

Jumbo mortgage loans

Private Banking branded checking account and Debit Card

Consumer lending products, including auto lending |

17

Jim Baemel

SVP, SBA Lending

Scott Keasel

AVP, SBA Lending

Ellen Minadeo

VP, Private Banking

Steve Levy

VP, C & I Lending

Strengthen the Depth of Talent |

18

Looking Forward

Aggressively pursue resolution of

regulatory issues. Continued improvement in core earnings. Add depth through the continued addition of talented

professionals. Continued commitment to delivering positive results to our

shareholders and constituents as we establish Park View as an

important community bank in Northeast Ohio.

Focus on building revenue generating capabilities. |

19

Non-GAAP

to

GAAP

Reconciliation

A reconciliation of net earnings reported under generally accepted accounting

principles to pre-tax, pre-credit provision income for the fiscal

years ending 2011 and 2010 is as follows (dollars in millions):

2011

2010

Net income (loss)

$(9.7)

$ 1.4

Federal income tax provision

0.1

0.7

Pre-tax income (loss)

(9.6)

2.1

Provision for loan losses

13.5

14.9

Loss/write-down on real estate owned

1.8

2.2

Securities gains

(1.2)

0.0

Less nonrecurring gains on cancellation of debt

0.0

(17.6)

Pre-tax, pre-credit provision income

$ 4.5

$ 1.6 |

20

Thank you for your continued support.

Celebrating Over 90 Years of Community Banking.

|