Attached files

| file | filename |

|---|---|

| EX-21.1 - SUBSIDIARIES OF OIL-DRI - Oil-Dri Corp of America | odcex21107312011.htm |

| EX-31.1 - CERTIFICATIONS PURSUANT TO RULE 13A - 14(A) - Oil-Dri Corp of America | odcex31107312011.htm |

| EX-11.1 - COMPUTATION OF NET INCOME PER SHARE - Oil-Dri Corp of America | odcex11107312011.htm |

| EX-32.1 - CERTIFICATIONS PURSUANT TO SECTION 1350 OF THE SARBANES-OXLEY ACT OF 2002 - Oil-Dri Corp of America | odcex32107312011.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - Oil-Dri Corp of America | odcex23107312011.htm |

| EX-99.1 - MINE SAFETY DISCLOSURE - Oil-Dri Corp of America | odcex99107312011.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended July 31, 2011

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from _____ to _____

___________________________

Commission File Number 001-12622

OIL-DRI CORPORATION OF AMERICA

Delaware | 36-2048898 |

(State or other jurisdiction of | (IRS. Employer Identification No.) |

incorporation or organization) | |

410 North Michigan Avenue, Suite 400, Chicago, Illinois 60611-4213

(312) 321-1515

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered |

Common Stock, par value $0.10 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act:

Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act:

Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days:

Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | o | Accelerated filer | ý | |

Non-accelerated filer | o | Smaller reporting company | o | |

(Do not check if a smaller reporting company) | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act):

Yes o No ý

The aggregate market value of Oil-Dri’s Common Stock owned by non-affiliates as of January 31, 2011 was $94,874,000.

Number of shares of each class of Oil-Dri’s capital stock outstanding as of September 30, 2011:

Common Stock – 5,110,925 shares

Class B Stock – 2,048,118 shares

Class A Common Stock – 0 shares

DOCUMENTS INCORPORATED BY REFERENCE

The following documents are incorporated by reference: Oil-Dri’s Proxy Statement for its 2011 Annual Meeting of Stockholders (“Proxy Statement”), which will be filed with the Securities and Exchange Commission (“SEC”) not later than November 28, 2011 (120 days after the end of Oil-Dri’s fiscal year ended July 31, 2011), is incorporated into Part III of this Annual Report on Form 10-K, as indicated herein.

CONTENTS

Item | Page | |||

1 | ||||

1A. | ||||

1B. | ||||

2 | ||||

3 | ||||

4 | ||||

5 | ||||

6 | ||||

7 | ||||

7A. | ||||

8 | ||||

9 | ||||

9A. | ||||

9B. | ||||

10 | ||||

11 | ||||

12 | ||||

13 | ||||

14 | ||||

3

CONTENTS (CONTINUED)

FORWARD-LOOKING STATEMENTS

Certain statements in this report, including, but not limited to, those under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and those statements elsewhere in this report and other documents we file with the SEC contain forward-looking statements that are based on current expectations, estimates, forecasts and projections about our future performance, our business, our beliefs and our management’s assumptions. In addition, we, or others on our behalf, may make forward-looking statements in press releases or written statements, or in our communications and discussions with investors and analysts in the normal course of business through meetings, webcasts, phone calls and conference calls. Words such as “expect,” “outlook,” “forecast,” “would,” “could,” “should,” “project,” “intend,” “plan,” “continue,” “believe,” “seek,” “estimate,” “anticipate,” “believe,” “may,” “assume,” variations of such words and similar expressions are intended to identify such forward-looking statements, which are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995.

Such statements are subject to certain risks, uncertainties and assumptions that could cause actual results to differ materially including, but not limited to, those described in Item 1A “Risk Factors” below and other reports filed with the SEC. Should one or more of these or other risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, intended, expected, believed, estimated, projected or planned. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Except to the extent required by law, we do not have any intention or obligation to update publicly any forward-looking statements after the distribution of this report, whether as a result of new information, future events, changes in assumptions or otherwise.

TRADEMARK NOTICE

Agsorb, Calibrin, Cat’s Pride, ConditionAde, Flo-Fre, Jonny Cat, KatKit, Oil-Dri, Pel-Unite, Perform, Poultry Guard, Pro Mound, Pure-Flo, Rapid Dry, Select, Terra-Green, and Ultra-Clear are all registered trademarks of Oil-Dri Corporation of America or of its subsidiaries. Pro’s Choice, Saular, Verge, Fresh & Light and Resorb are trademarks of Oil-Dri Corporation of America. Fresh Step is a registered trademark of The Clorox Company.

4

PART I

ITEM 1 – BUSINESS

In 1969, Oil-Dri Corporation of America was incorporated in Delaware as the successor to an Illinois corporation incorporated in 1946; the Illinois corporation was the successor to a partnership that commenced business in 1941. Except as otherwise indicated herein or as the context otherwise requires, references to “Oil-Dri,” the “Company,” “we,” “us” or “our” refer to Oil-Dri Corporation of America and its subsidiaries.

GENERAL BUSINESS DEVELOPMENTS

During fiscal 2011, our commitment to provide valuable products to our customers was rewarded with higher sales. Our efforts to add value to our products focused on new product development and promotion and on existing product improvements. The Retail and Wholesale Products Group saw increased sales of established branded cat litters and the development and introduction of our new Cat's Pride Fresh & Light cat litter product in the fourth quarter. Our Business to Business Products Group also experienced increased sales of our fluid purification and traditional agricultural products and of Verge, our engineered granule product that we introduced late in fiscal 2010. We were challenged by higher costs related to commodities, depreciation and labor which, combined with increased spending for product market research and promotion development, resulted in lower operating margins and overall results. We issued new debt, continued to invest in our capital assets and maintained a strong consolidated balance sheet during fiscal 2011. For more information on recent business developments, see Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” below.

PRINCIPAL PRODUCTS

We are a leader in developing, manufacturing and marketing sorbent products. Our sorbent products are principally produced from clay minerals, primarily consisting of montmorillonite and attapulgite and, to a lesser extent, other clay-like sorbent materials, such as Antelope shale, which we refer to collectively as our "clay" or our "minerals". Our sorbent technologies include absorbent and adsorbent products. Absorbents, like sponges, draw liquids up into their many pores. Examples of our absorbent clay products are Cat’s Pride and Jonny Cat branded premium cat litter, as well as other private label cat litters. We also produce Oil-Dri branded floor absorbents, Agsorb and Verge agricultural chemical carriers and ConditionAde, Calibrin and Pel-Unite animal feed binders. Adsorbent products attract impurities in liquids, such as metals and surfactants, and form low-level chemical bonds. Examples of our adsorbent products are Oil-Dri synthetic sorbents, which are used for industrial cleanup, and Pure-Flo, Perform and Select bleaching clay products, which act as a filtration media for edible oils, fats and tallows. Also, our Ultra-Clear product serves as a clarification aid for petroleum-based oils and by-products. Both our absorbent and adsorbent products are described in more detail below.

Cat Litter Products

We produce two types of cat litter products, traditional coarse and scoopable, both of which have absorbent and odor controlling characteristics. Scoopable litters have the additional characteristic of clumping when exposed to moisture, allowing the consumer to selectively dispose of the used portion of the litter. Our coarse and scoopable products are sold under our Cat’s Pride and Jonny Cat brand names. We also package and market Cat’s Pride Kat Kit and Jonny Cat cat litter in a disposable tray, as well as Cat's Pride and Jonny Cat litter pan liners. We manufacture Fresh Step brand coarse cat litter for The Clorox Company (“Clorox”). We also produce private label cat litters for other customers that are sold through independent food brokers and our sales force to major retail outlets.

We have two long-term supply arrangements (only one of which is material) under which we manufacture branded traditional litters for other marketers. Under these co-manufacturing relationships, the marketer controls all aspects of sales, marketing, and distribution, as well as the odor control formula, and we are responsible for manufacturing. Our material agreement is with Clorox, under which we have the exclusive right to supply Clorox’s requirements for Fresh Step coarse cat litter up to certain levels.

Industrial and Automotive Sorbent Products

We manufacture products from clay, polypropylene and recycled cotton materials that absorb oil, grease, water and other types of spills. These products are used in industrial, home and automotive environments. Our clay-based sorbent products, such as Oil-Dri branded floor absorbent, are used for floor maintenance in industrial applications to provide a non-slip and nonflammable

5

surface for workers. These floor absorbents are used in automotive repair facilities and car dealerships to absorb oil and grease. They are also used in home applications in garages and driveways. Our Oil-Dri branded polypropylene-based and cotton-based products are sold in various forms, such as pads, rolls, socks, booms and spill kits. These products are used to absorb oil, grease, water and most chemical spills.

Industrial and automotive sorbent products are sold through a distribution network that includes industrial, auto parts, safety, sanitary supply, chemical and paper distributors. These products are also sold through environmental service companies, mass merchandisers and catalogs.

Bleaching Clay and Clarification Aid Products

We produce an array of bleaching, purification and filtration applications used by edible oil and jet fuel processors around the world. Bleaching clays are used by edible oil processors to adsorb soluble contaminants that create oxidation problems. Our Pure-Flo and Perform bleaching clays remove impurities, such as trace metals, chlorophyll and color bodies, in various types of edible oils. Perform products provide increased activity for hard-to-bleach oils. Our Select adsorbents are used to remove contaminants in vegetable oil processing and can be used to prepare oil prior to the creation of biodiesel fuel. Our Ultra-Clear clarification aid is used as a filtration and purification medium for jet fuel and other petroleum-based products.

These products are marketed in the United States and in international markets. The products are supported by our team of technical sales employees as well as by agent representatives and the services of our research and development group.

Agricultural and Horticultural Products

We produce a wide range of granular and powdered mineral absorbent products that are used as carriers for crop protection chemicals, agricultural drying agents, bulk processing aids, growing media components and seed enhancement media. Our brands include: Agsorb, an agricultural chemical carrier and drying agent; Verge, an engineered granule agricultural chemical carrier; Flo-Fre, a highly absorbent microgranule flowability aid; and Terra-Green, a growing media supplement.

Agsorb and Verge carriers are used as an alternative to agricultural sprays. The clay granules absorb crop protection chemicals and are then delivered directly into, or on top of, the ground providing a more precise application than chemical sprays. Verge carriers are spherical, uniform-sized granules with very low dust. Agsorb drying agent is blended into fertilizer-pesticide blends applied by farmers to absorb moisture and improve flowability. Agsorb also acts as a flowability aid for fertilizers and chemicals used in the lawn and garden market. Flo-Fre microgranules are used by grain processors and other large handlers of bulk products to soak up excess moisture preventing caking. We employ technical sales people to market agricultural products in the United States.

Animal Health and Nutrition Products

We produce several products used in the livestock feed industry. Calibrin and ConditionAde branded enterosorbent products are used in animal feed to absorb naturally-occurring mycotoxins in the feed and thereby improve animal health and productivity. Pel-Unite and Pel-Unite Plus are specialized animal feed binders used in the manufacture of pelleted feeds. These products are sold through a network of feed products distributors in the United States and primarily through exclusive distribution agreements with animal health and nutrition products distributors in Latin America, Africa and Asia.

Sports Products

Pro’s Choice sports field products are used on baseball, football and soccer fields. Pro’s Choice soil conditioners are used in field construction or as top dressing to absorb moisture, suppress dust and improve field performance. Pro Mound packing clay is used to construct pitcher’s mounds and batter’s boxes. Rapid Dry drying agent is used to dry up puddles and slick spots after rain. Sports field products are used at all levels of play, including professional, college and high school and on municipal fields. These products are sold through a network of distributors specializing in sports turf products.

BUSINESS SEGMENTS

We have two reportable operating segments for financial reporting derived from the different characteristics of our two major customer groups: Retail and Wholesale Products Group and Business to Business Products Group. The Retail and Wholesale Products Group customers include mass merchandisers, wholesale clubs, drugstore chains, pet specialty retail outlets, dollar stores, retail grocery stores, distributors of industrial cleanup and automotive products, environmental service companies and sports field product users. The Business to Business Products Group customers include processors and refiners of edible oils, petroleum-

6

based oils and biodiesel fuel, manufacturers of animal feed and agricultural chemicals and marketers of consumer products.

Beginning in fiscal 2011, our sports field products were included in the Retail and Wholesale Products Group to reflect a change in management organization intended to better serve our customers. Certain financial information on both segments is contained in Note 2 of the Notes to the Consolidated Financial Statements and is incorporated herein by reference. Prior year segment information has been restated to reflect this change.

We do not manage our business, allocate resources or generate revenue data by product line. Any of our products may be sold in one or both of our operating segments. Information concerning total revenue of classes of similar products accounting for more than 10% of consolidated revenues in any of the last three fiscal years is not separately provided because it would be impracticable to do so.

FOREIGN OPERATIONS

Our wholly-owned subsidiary, Oil-Dri Canada ULC, is a manufacturer and marketer of branded and private label cat litter in the Canadian market place. Among its leading brands are Saular, Cat’s Pride and Jonny Cat. Our Canadian business also sells industrial granule floor absorbents, synthetic polypropylene sorbent materials and agricultural chemical carriers.

Our wholly-owned subsidiary, Oil-Dri (U.K.) Limited, is a manufacturer and marketer of industrial floor absorbents and cat litter. These products are marketed in the United Kingdom and Western Europe. Oil-Dri (U.K.) Limited also sells synthetic polypropylene sorbent materials, filtration units and plastic containment products.

Our wholly-owned subsidiary, Oil-Dri SARL, is a Swiss company that performs various management, customer service and administrative functions for international business of our domestic operations.

Our foreign operations are subject to the normal risks of doing business overseas, such as currency devaluations and fluctuations, restrictions on the transfer of funds and import/export duties. We were not materially impacted by these foreign currency fluctuations in any of our last three fiscal years. Certain financial information about our foreign and domestic operations is contained in Note 2 of the Notes to the Consolidated Financial Statements and is incorporated herein by reference.

CUSTOMERS

Sales to Wal-Mart Stores, Inc. (“Walmart”) and its affiliates accounted for approximately 21%, 20% and 26% of our total net sales for the fiscal years ended July 31, 2011, 2010 and 2009, respectively. Walmart is a customer in our Retail and Wholesale Products Group segment. During fiscal 2011, Walmart reinstated our branded scoopable litter following the reduction in the number of cat litter brands carried, including ours, during the first quarter of fiscal 2010. There are no customers in the Business to Business Products Group with sales equal to or greater than 10% of our total sales; however, sales to Clorox (a customer in our Business to Business Products Group) and its affiliates accounted for approximately 8%, 9% and 8% of total net sales for fiscal years 2011, 2010 and 2009, respectively. The degree of margin contribution of our significant customers in the Business to Business Products Group varies, with certain customers having a greater effect on our operating results. The loss of any customer other than those described in this paragraph would not be expected to have a material adverse effect on our business.

COMPETITION

Price, service, marketing, technical support, product quality and delivery are the principal methods of competition in our markets and competition has historically been very vigorous. Some of our competitors are large companies whose financial resources are substantially greater than ours.

In our Retail and Wholesale Products Group, we have six principal competitors, including one which is also a customer of ours. The cat litter market has been stable in recent years. Scoopable products have a majority of the cat litter market share followed by traditional coarse products. The overwhelming majority of all cat litter is mineral based; however, cat litters based on alternative strata such as paper, various agricultural waste products and silica gels have earned niche positions. The consumer trend away from regional grocery stores towards large national retailers, such as supercenter-type stores, dollar stores and pet specialty stores, has presented competitive challenges as well as opportunities. These stores enjoy substantial negotiating leverage over their suppliers, including us; however, our operations support nation-wide distribution, which gives us a potential advantage over smaller and regional manufacturers in selling to these stores.

In the Business to Business Products Group, we have 15 principal competitors. The agricultural chemical carrier portion of this segment has experienced competition from new technologies in the agricultural and horticultural markets. The bleaching

7

clay and fluids clarification aid portion of this Group operates in a highly cost competitive global marketplace. Product performance is also a primary competitive factor for these products. The animal health portion of this Group also operates in a global marketplace with price and performance competition from multi-national and local competitors.

PATENTS

We have obtained or applied for patents for certain of our processes and products sold to customers in both the Retail and Wholesale Products Group and the Business to Business Products Group. These patents expire at various times, beginning in February 2013. We expect no material impact on our business from the expiration of patents in the next year.

BACKLOG; SEASONALITY

At July 31, 2011, 2010 and 2009, our backlog of orders was approximately $5,145,000, $6,368,000, and $6,015,000, respectively. The value of backlog orders is determined by the number of tons on backlog order and the net selling prices. All backlog orders are expected to be filled within the next 12 months. We consider our business, taken as a whole, to be only moderately seasonal; however, business activities of certain customers (such as agricultural chemical manufacturers) are subject to such seasonal factors as crop acreage planted and product formulation cycles.

EFFECTS OF INFLATION

Inflation generally affects us by increasing the cost of employee wages and benefits, transportation, processing equipment, purchased raw materials and packaging, energy and borrowings under our credit facility. See Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Item 7A “Quantitative and Qualitative Disclosures About Market Risk” below.

RESERVES

We mine our clay on leased or owned land near our manufacturing facilities in Mississippi, Georgia, Illinois and California; we also have reserves in Nevada, Oregon and Tennessee. We estimate our proven mineral reserves are approximately 151,080,000 tons in aggregate and our probable reserves are approximately 146,835,000 tons in aggregate, for a total of 297,915,000 tons of mineral reserves. Based on our rate of consumption during fiscal year 2011, and without regard to any of our reserves in Nevada, Oregon and Tennessee, we consider our proven reserves adequate to supply our needs for over 40 years. Although we consider these reserves to be extremely valuable to our business, only a small portion of the reserves, those which were acquired in acquisitions, is reflected at cost on our balance sheet.

It is our policy to attempt to add to reserves in most years, but not necessarily in every year, an amount at least equal to the amount of reserves consumed in that year. We have a program of exploration for additional reserves and, although reserves have been acquired, we cannot assure that additional reserves will continue to become available. Our use of these reserves, and our ability to explore for additional reserves, are subject to compliance with existing and future federal and state statutes and regulations regarding mining and environmental compliance. During the fiscal year ended July 31, 2011, we utilized these reserves to produce a majority of the sorbent products that we sold.

Proven reserves are those reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from results of detailed sampling, and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well established. Probable reserves are computed from information similar to that used for proven reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation. We employ geologists and mineral specialists who estimate and evaluate existing and potential reserves in terms of quality, quantity and availability.

MINING OPERATIONS

We have conducted mining operations in Ripley, Mississippi since 1963, in Ochlocknee, Georgia since 1968, in Blue Mountain, Mississippi since 1989, in Mounds, Illinois since 1998 and in Taft, California since 2002. Our clay is surface mined on a year-round basis, generally using large earth moving scrapers, bulldozers, excavators or off-road trucks to remove overburden (non-usable material), and then loaded into dump trucks with backhoes or front end loaders for movement to the processing facilities. The mining and hauling of our clay is performed by us and by independent contractors. Our current operating mines range in distance from immediately adjacent to approximately 13 miles from the related processing plants. Processing facilities

8

are generally accessed from the mining areas by private roads and in some instances by public highways. Each of our processing facilities maintains inventories of unprocessed clay of approximately one week of production requirements. See Item 2 “Properties” below for additional information regarding our mining properties and operations.

The following schedule summarizes the net book value of land and other plant and equipment for each of our manufacturing facilities:

Land | Plant and Equipment | |||||||

(in thousands) | ||||||||

Ochlocknee, Georgia | $ | 8,497 | $ | 15,703 | ||||

Ripley, Mississippi | $ | 1,773 | $ | 12,263 | ||||

Mounds, Illinois | $ | 1,545 | $ | 4,110 | ||||

Blue Mountain, Mississippi | $ | 878 | $ | 11,211 | ||||

Taft, California | $ | 1,391 | $ | 3,576 | ||||

EMPLOYEES

As of July 31, 2011, we employed 815 persons, 54 of whom were employed by our foreign subsidiaries. Our corporate offices, research and development center and manufacturing facilities are adequately staffed and no material labor shortages are anticipated. Approximately 48 of our employees in the U.S. and approximately 26 of our employees in Canada are represented by labor unions, with whom we have entered into separate collective bargaining agreements. We consider our employee relations to be satisfactory.

ENVIRONMENTAL COMPLIANCE

Our mining and manufacturing operations and facilities in Georgia, Mississippi, California and Illinois are required to comply with state surface mining and wetland statutes. These domestic locations and our Canadian operations are subject to various federal, state and local statutes, regulations and ordinances which govern the discharge of materials, water and waste into the environment or otherwise regulate our operations. In recent years, environmental regulation has grown increasingly stringent, a trend that we expect will continue. We endeavor to be in compliance at all times and in all material respects with all applicable environmental controls and regulations. As a result, expenditures relating to environmental compliance have increased over the years; however, these expenditures have not been material. As part of our ongoing environmental compliance activities, we incur expenses in connection with reclaiming exhausted mining sites. Historically, reclamation expenses have not had a material effect on our cost of sales.

In addition to the environmental requirements relating to mining and manufacturing operations and facilities, there is increasing federal and state regulation with respect to the content, labeling, use, and disposal after use, of various products that we sell. We endeavor to be in compliance at all times and in all material respects with those regulations and to assist our customers in that compliance.

We cannot assure that, despite all commercially reasonable efforts, we will always be in compliance in all material respects with all applicable environmental regulation or with requirements regarding the content, labeling, use, and disposal after use, of our products; nor can we assure that from time to time enforcement of such requirements will not have a material adverse effect on our business. See Item 1A “Risk Factors” below for a discussion of these and other risks to our business.

ENERGY

We use natural gas, recycled oil and coal as permitted for energy sources in the processing of our clay products. Consistent with prior years, we have switched among the various energy sources during certain months due to seasonal availability and cost. See Item 7A “Quantitative and Qualitative Disclosures About Market Risk” below with respect to our use of forward contracts.

RESEARCH AND DEVELOPMENT

At our research and development facility in Vernon Hills, Illinois, we develop new products and applications and improve existing products. The facility’s staff (and various consultants they engage from time to time) consists of geologists, mineralogists and chemists. In the past several years, our research efforts have resulted in a number of new sorbent products and processes. The facility produces prototype samples and tests new products for customer trial and evaluation.

9

We spent approximately $1,933,000, $1,826,000, and $2,099,000 during the fiscal years ended July 31, 2011, 2010 and 2009, respectively, for research and development. None of this research and development was customer sponsored, and all research and development costs are expensed in the period in which incurred. See Note 1 of the Notes to the Consolidated Financial Statements.

AVAILABLE INFORMATION

This Annual Report on Form 10-K, as well as our quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to all of the foregoing reports, are made available free of charge on or through the “Investor Information” section of our website (www.oildri.com) as soon as reasonably practicable after such reports are electronically filed with or furnished to the SEC.

Information relating to corporate governance at Oil-Dri, including its Code of Ethics and Business Conduct, information concerning executive officers, directors and Board committees (including committee charters), and transactions in Oil-Dri securities by directors and officers, is available free of charge on or through the “Investor Information” section of our website at www.oildri.com. We are not including the information on our website as a part of, or incorporating it by reference into, this Annual Report on Form 10-K.

10

ITEM 1A – RISK FACTORS

We seek to identify, manage and mitigate risks to our business, but risk and uncertainty cannot be eliminated or necessarily predicted. You should consider the following factors carefully, in addition to other information contained in this Annual Report on Form 10-K, before deciding to purchase our securities.

Risks Related to our Business

Our future growth and financial performance depend in large part on successful new product introductions.

A significant portion of our net sales comes from the sale of mature products, such as coarse cat litter, floor absorbent and agricultural chemical carriers, which have had little or no volume growth (in fact, several have had volume declines) in recent fiscal years. Our future growth and financial performance will require that we successfully introduce new products or extend existing product offerings to meet emerging customer needs, technological trends and product market opportunities. We cannot be certain that we will achieve these goals. The development and introduction of new products generally require substantial and effective research, development and marketing expenditures, some or all of which may be unrecoverable if the new products do not gain market acceptance. New product development itself is inherently risky, as research failures, competitive barriers arising out of the intellectual property rights of others, launch and production difficulties, customer rejection and unexpectedly short product life cycles may occur even after substantial effort and expense on our part. Even in the case of a successful launch of a new product, the ultimate benefit we realize may be uncertain if the new product “cannibalizes” sales of our existing products beyond expected levels.

We face intense competition in our markets.

Our markets are highly competitive and we expect that both direct and indirect competition will increase in the future. Our overall competitive position depends on a number of factors including price, customer service and technical support, product quality and delivery. Some of our competitors, particularly in the sale of cat litter (the largest product in our Retail and Wholesale Products Group), are much larger and have substantially greater financial resources. The competition in the future may, in some cases, result in price reductions, reduced margins or loss of market share, any of which could materially and adversely affect our business, operating results and financial condition. If we fail to compete successfully based on these or other factors, our business, financial condition and future financial results could be materially and adversely affected.

Our periodic results may be volatile.

Our operating results have varied on a quarterly basis during our operating history and are likely to fluctuate significantly in the future. Our expense levels are based, in part, on our expectations regarding future net sales, and many of our expenses are fixed, particularly in the short term. We may be unable to adjust spending in a timely manner to compensate for any unexpected revenue shortfall. Any significant shortfall of net sales in relation to our expectations could negatively affect our quarterly operating results. Our operating results may be below the expectations of our investors as a result of a variety of factors, many of which are outside our control. Factors that may affect our quarterly operating results include:

• | fluctuating demand for our products and services; |

• | size and timing of sales of our products and services; |

• | the mix of products with varying profitability sold in a given quarter; |

• | changes in our operating costs including raw materials, energy, transportation, packaging, overburden removal, trade spending and marketing, wages and other employee-related expenses such as health care costs, and other costs; |

• | our ability to anticipate and adapt to rapidly changing conditions; |

• | introduction of new products and services by us or our competitors; |

• | our ability to successfully implement price increases and surcharges, as well as other changes in our pricing policies or those of our competitors; |

• | variations in purchasing patterns by our customers; |

• | the ability of major customers and other debtors to meet their obligations to us as they come due; |

• | our ability to successfully manage regulatory, intellectual property, tax and legal matters; |

• | the incurrence of restructuring, impairment or other charges; and |

• | general economic conditions and specific economic conditions in our industry and the industries of our customers. |

Accordingly, we believe that quarter-to-quarter comparisons of our operating results are not necessarily meaningful. Investors should not rely on the results of one quarter as an indication of our future performance.

11

Acquisitions involve a number of risks, any of which could cause us not to realize the anticipated benefits.

We intend from time to time to strategically explore potential opportunities to expand our operations and reserves through acquisitions. Identification of good acquisition candidates is difficult and highly competitive. If we are unable to identify attractive acquisition candidates, complete acquisitions, and successfully integrate the companies, businesses or properties that we acquire, our profitability may decline and we could experience a material adverse effect on our business, financial condition, or operating results. Acquisitions involve a number of inherent risks, including:

• | uncertainties in assessing the value, strengths, and potential profitability of acquisition candidates, and in identifying the extent of all weaknesses, risks, contingent and other liabilities (including environmental or mining safety liabilities), of those candidates; |

• | the potential loss of key customers, management and employees of an acquired business; |

• | the ability to achieve identified operating and financial synergies anticipated to result from an acquisition; |

• | problems that could arise from the integration of the acquired business; and |

• | unanticipated changes in business, industry or general economic conditions that affect the assumptions underlying our rationale for pursuing the acquisition. |

Any one or more of these factors could cause us not to realize the benefits we anticipate to result from an acquisition. Moreover, any acquisition opportunities we pursue could materially affect our liquidity and capital resources and may require us to incur indebtedness, seek equity capital or both. In addition, future acquisitions could result in our assuming more long-term liabilities relative to the value of the acquired assets than we have assumed in our previous acquisitions.

We depend on a limited number of customers for a large portion of our net sales.

A limited number of customers account for a large percentage of our net sales, as described in Item 1 "Business" above. The loss of or a substantial decrease in the volume of purchases by Walmart, Clorox or any of our other top customers would harm our sales and profitability. In addition, an adverse change in the terms of our dealings with, or in the financial wherewithal or viability of, one or more of our significant customers could harm our business, financial condition and results of operations.

We expect that a significant portion of our net sales will continue to be derived from a small number of customers and that the percentage of net sales represented by these customers may increase. As a result, changes in the strategies of our largest customers may reduce our net sales. These strategic changes may include a reduction in the number of brands they carry or a shift of shelf space to private label products or increased use of global or centralized procurement initiatives. In addition, our business is based primarily upon individual sales orders placed by customers rather than contracts with a fixed duration. Accordingly, most of our customers could reduce their purchasing levels or cease buying products from us on relatively short notice. While we do have long-term contracts with certain of our customers, including Clorox, even these agreements are subject to termination in certain circumstances. In addition, the degree of profit margin contribution of our significant customers varies. If a significant customer with a more favorable profit margin was to terminate its relationship with us or shift its mix of product purchases to lower-margin products, it would have a disproportionate adverse impact on our results of operations. If we lose a significant customer or if sales of our products to a significant customer materially decrease, it may have a material adverse effect on our business, financial condition and results of operations.

Price or trade concessions, or the failure to make them to retain customers, could adversely affect our sales and profitability.

The products we sell are subject to significant price competition. From time to time, we may need to reduce the prices for some of our products to respond to competitive and customer pressures and to maintain market share. These pressures are often exacerbated during an economic downturn. Any reduction in prices to respond to these pressures would reduce our profit margins. In addition, if our sales volumes fail to grow sufficiently to offset any reduction in margins, our results of operations would suffer. Because of the competitive environment facing many of our customers, particularly our high-volume mass merchandiser customers, these customers have increasingly sought to obtain price reductions, specialized packaging or other concessions from product suppliers. These business demands may relate to inventory practices, logistics or other aspects of the customer-supplier relationship. To the extent we provide these concessions, our profit margins are reduced. Further, if we are unable to maintain terms that are acceptable to our customers, these customers could reduce purchases of our products and increase purchases of products from our competitors, which would harm our sales and profitability.

12

Increases in energy and other commodity prices would increase our operating costs, and we may be unable to pass all these increases on to our customers in the form of higher prices.

If our energy costs increase disproportionately to our net sales, our earnings could be significantly reduced. Because we use energy, including natural gas, recycled oil, coal, electricity, diesel fuel and gasoline, to manufacture and transport our products, our operating costs increase if our energy costs rise. Increases in our operating costs may reduce our profitability if we are unable to pass all the increases on to our customers through price increases or surcharges. Sustained price increases or surcharges in turn may lead to declines in volume, and while we seek to project tradeoffs between price increases and surcharges, on the one hand, and volume, on the other, there can be no assurance that our projections will prove to be accurate.

Typically, our most significant energy requirements are for natural gas and recycled oil. We are subject to volatility in the price and availability of natural gas and recycled oil, as well as other sources of energy. In the past, we have endeavored to reallocate a portion of our energy needs among these different sources due to seasonal supply limitations and the higher cost of one particular fuel relative to other fuels; however, there can be no assurance that we will be able to effectively reallocate among different fuels in the future. From time to time, we may use forward purchase contracts or financial instruments to hedge the volatility of a portion of our natural gas and recycled oil costs. The success or failure of any such hedging transactions depends on a number of factors including, but not limited to, our ability to anticipate and manage volatility in energy prices, the general demand for natural gas and recycled oil by the manufacturing sector, seasonality and the weather patterns throughout the United States and the world.

The prices of other commodities such as paper, plastic resins, synthetic rubber, raw materials and steel significantly influence the costs of packaging, replacement parts and equipment we use in the manufacture of our products and the maintenance of our facilities. As a result, increases in the prices of these commodities generally increase the costs of the related materials we use. These increased materials costs present the same types of risks as described above with respect to increased energy costs.

Our business could be negatively affected by supply disruptions.

Supply disruptions could adversely affect our ability to manufacture or package our products. Some of our products require raw materials that are provided by a limited number of suppliers, or are demanded by other industries or are simply not available at times.

Reductions in inventory by our customers could adversely affect our sales and increase our inventory risk.

From time to time, customers in both our Retail and Wholesale Products Group and our Business to Business Products Group have reduced inventory levels as part of managing their working capital requirements. Any reduction in inventory levels by our customers would harm our operating results for the financial periods affected by the reductions. In particular, continued consolidation within the retail industry could potentially reduce inventory levels maintained by our retail customers, which could adversely affect our results of operations for the financial periods affected by the reductions. Similarly, inventory reductions by our agricultural chemical carrier customers or our contract cat litter manufacturing customers could also adversely affect our results of operations for the financial periods in which the reductions occur.

The value of our inventory may decline as a result of surplus inventory, price reductions or obsolescence. We must identify the right product mix and maintain sufficient inventory on hand to meet customer orders. Failure to do so could adversely affect our revenue and operating results. If circumstances change (for example, an unexpected shift in market demand, pricing or customer defaults) there could be a material impact on the net realizable value of our inventory. We maintain an inventory valuation reserve account against diminution in the value or salability of our inventory; however, there is no guaranty that these arrangements will be sufficient to avoid write-offs in excess of our reserves.

Environmental, health and safety matters create potential compliance and other liability risks.

We are subject to a variety of federal, state, local and foreign regulatory requirements relating to the environment and to health and safety matters. For example, our mining operations are subject to extensive governmental regulation on matters such as permitting and licensing requirements, workplace safety, plant and wildlife protection, wetlands protection, reclamation and restoration of mining properties after mining is completed, the discharge of materials into the environment, and the effects that mining has on groundwater quality and availability. We believe we have obtained all material permits and licenses required to conduct our present operations. We will, however, need additional permits and renewals of permits in the future.

The expense, liabilities and requirements associated with environmental, health and safety regulations are costly and

13

time-consuming and may delay commencement or continuation of exploration, mining or manufacturing operations. We have incurred, and will continue to incur, significant capital and operating expenditures and other costs in complying with environmental, health and safety laws and regulations. In recent years, regulation of environmental, health and safety matters has grown increasingly stringent, a trend that we expect will continue. Substantial penalties may be imposed if we violate certain of these laws and regulations even if the violation was inadvertent or unintentional. Failure to maintain or achieve compliance with these laws and regulations or with the permits required for our operations could result in substantial operating costs and capital expenditures, in addition to fines and administrative, civil or criminal sanctions, third-party claims for property damage or personal injury, cleanup and site restoration costs and liens, the issuance of injunctions to limit or cease operations, the suspension or revocation of permits and other enforcement measures that could have the effect of limiting our operations. Under the “joint and several” liability principle of certain environmental laws, we may be held liable for all remediation costs at a particular site and the amount of that liability could be material. In addition, future environmental laws and regulations could restrict our ability to expand our facilities or extract our existing reserves or could require us to acquire costly equipment or to incur other significant expenses in connection with our business. There can be no assurance that future events, including changes in any environmental requirements and the costs associated with complying with such requirements, will not have a material adverse effect on us.

Government regulation imposes significant costs on us, and future regulatory changes (or related customer responses to regulatory changes) could increase those costs or limit our ability to produce and sell our products.

In addition to the regulatory matters described above, our operations are subject to various federal, state, local and foreign laws and regulations relating to the manufacture, packaging, labeling, content, storage, distribution and advertising of our products and the conduct of our business operations. For example, in the United States, many of our products are regulated by the Food and Drug Administration, the Consumer Product Safety Commission and the Environmental Protection Agency and our product claims and advertising are regulated by the Federal Trade Commission. Most states have agencies that regulate in parallel to these federal agencies. In addition, our international sales and operations are subject to regulation in each of the foreign jurisdictions in which we manufacture, distribute or sell our products. There is increasing federal and state regulation with respect to the content, labeling, use, and disposal after use, of various products we sell. Throughout the world, but particularly in the European Union, there is also increasing government scrutiny and regulation of the food chain and products entering or affecting the food chain.

If we are found to be out of compliance with applicable laws and regulations in these or other areas, we could be subject to loss of customers and to civil remedies, including fines, injunctions, recalls or asset seizures, as well as potential criminal sanctions, any of which could have a material adverse effect on our business. Loss of or failure to obtain necessary permits and registrations could delay or prevent us from meeting product demand, introducing new products, building new facilities or acquiring new businesses and could adversely affect operating results. If these laws or regulations are changed or interpreted differently in the future, it may become more difficult or expensive for us to comply. In addition, investigations or evaluations of our products by government agencies may require us to adopt additional labeling, safety measures or other precautions, or may effectively limit or eliminate our ability to market and sell these products. Accordingly, there can be no assurance that current or future governmental regulation will not have a material adverse effect on our business or that we will be able to obtain or renew required governmental permits and registrations in the future.

We are also experiencing increasing customer scrutiny of the content and manufacturing of our products, particularly our products entering or affecting the food chain, in parallel with the increasing government regulation discussed above. Our customers may impose product specifications or other requirements that are different from, and more onerous than, applicable laws and regulations. As a result, the failure of our products to meet these additional requirements may result in loss of customers and decreased sales of our products even in the absence of any actual failure to comply with applicable laws and regulations. There can be no assurance that future customer requirements concerning the content or manufacturing of our products will not have a material adverse effect on our business.

We depend on our mining operations for a majority of our supply of sorbent minerals.

Most of our principal raw materials are sorbent minerals mined by us or independent contractors on land that we own or lease. While our mining operations are conducted in surface mines which do not present many of the risks associated with deep underground mining, our mining operations are nevertheless subject to many conditions beyond our control. Our mining operations are affected by weather and natural disasters, such as heavy rains and flooding, equipment failures and other unexpected maintenance problems, variations in the amount of rock and soil overlying our reserves, variations in geological conditions, fires and other accidents, fluctuations in the price or availability of supplies and other matters. Any of these risks could result in significant damage to our mining properties or processing facilities, personal injury to our employees, environmental damage, delays in mining or processing, losses or possible legal liability. We cannot predict whether or the extent to which we will suffer the impact of these and other conditions in the future.

14

We may not be successful in acquiring adequate additional reserves in the future.

We have an ongoing program of exploration for additional reserves on existing properties as well as through the potential acquisition of new owned or leased properties; however, there can be no assurance that our attempts to acquire additional reserves in the future will be successful. Our ability to acquire additional reserves in the future could be limited by competition from other companies for attractive properties, the lack of suitable properties that can be acquired on terms acceptable to us or restrictions under our existing or future debt facilities. We may not be able to negotiate new leases or obtain mining contracts for properties containing additional reserves or renew our leasehold interests in properties on which operations are not commenced during the term of the lease. Also, requirements for environmental compliance may restrict exploration or use of lands that might otherwise be utilized as a source of reserves.

We face risks as a result of our international sales and business operations.

We derived approximately 19% of our net sales from sales outside of the United States in the fiscal year ended July 31, 2011. Our ability to sell our products and conduct our operations outside of the United States is subject to a number of risks. Local economic, political and labor conditions in each country could adversely affect demand for our products or disrupt our operations in these markets, particularly when local political and economic conditions are unstable. In addition, international sales and operations are subject to currency exchange fluctuations, fund transfer restrictions and import/export duties, and international operations are subject to foreign regulatory requirements and issues, including with respect to environmental matters. Any of these matters could result in sudden, and potentially prolonged, changes in demand for our products. Also, we may have difficulty enforcing agreements and collecting accounts receivable through a foreign country’s legal system.

We may face product liability claims that are costly, create adverse publicity and may add further governmental regulation.

If any of the products that we sell cause harm to any of our customers or to consumers, we could be exposed to product liability lawsuits or governmental actions. If we are found liable under product liability claims, we could be required to pay substantial monetary damages or change our product formulations in response to governmental action. Further, even if we successfully defend ourselves against this type of claim, we could be forced to spend a substantial amount of money in litigation expenses, our management could be required to spend valuable time in the defense against these claims and our reputation could suffer, any of which could harm our business.

Failure to maintain effective internal control over financial reporting could have a material adverse effect on our business, operating results and stock price.

Section 404 of the Sarbanes-Oxley Act and related SEC rules require that we perform an annual management assessment of the design and effectiveness of our internal control over financial reporting and obtain an opinion from our independent registered public accounting firm on our internal control over financial reporting. Our assessment concluded that our internal control over financial reporting was effective as of July 31, 2011 and we obtained from our independent registered public accounting firm an unqualified opinion on our internal control over financial reporting; however, there can be no assurance that we will be able to maintain the adequacy of our internal control over financial reporting, as such standards are modified, supplemented or amended from time to time in future periods. Accordingly, we cannot assure that we will be able to conclude on an ongoing basis that we have effective internal control over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act. Moreover, effective internal control is necessary for us to produce reliable financial reports and is important to help prevent financial fraud. If we cannot provide reliable financial reports or prevent fraud, our business and operating results could be harmed, investors could lose confidence in our reported financial information, and the trading price of our Common Stock could drop significantly.

Risks Related to Our Common Stock

Our principal stockholders have the ability to control matters requiring a stockholder vote and could delay, deter or prevent a change in control of our company.

Under our Certificate of Incorporation, the holders of our Common Stock are entitled to one vote per share and the holders of our Class B Stock are entitled to 10 votes per share; the two classes generally vote together without regard to class (except that any amendment to our Certificate of Incorporation changing the number of authorized shares or adversely affecting the rights of Common Stock or Class B Stock requires the separate approval of the class so affected as well as the approval of both classes voting together). As a result, the holders of our Class B Stock exert control over us and thus limit the ability of other stockholders to influence corporate matters. Beneficial ownership of Common Stock and Class B Stock by the Jaffee Investment Partnership, L.P., and its affiliates (including Richard M. Jaffee, our Chairman, and Daniel S. Jaffee, his son and our President and Chief Executive Officer) provides them with the ability to control the election of our Board of Directors and the outcome of most matters

15

requiring the approval of our stockholders, including the amendment of certain provisions of our Certificate of Incorporation and By-Laws, the approval of any equity-based employee compensation plans and the approval of fundamental corporate transactions, including mergers and substantial asset sales. Through their concentration of voting power, our principal stockholders may be able to delay, deter or prevent a change in control of our company or other business combinations that might otherwise be beneficial to our other stockholders.

We are a “controlled company” within the meaning of the New York Stock Exchange (“NYSE”) rules and, as a result, qualify for, and intend to rely on, exemptions from certain corporate governance requirements.

We are a “controlled company” under the New York Stock Exchange Corporate Governance Standards. As a controlled company, we may rely on exemptions from certain NYSE corporate governance requirements that otherwise would be applicable, including the requirements:

• | that a majority of the board of directors consists of independent directors; |

• | that we have a nominating and governance committee composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities; |

• | that we have a compensation committee composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities; and |

• | that we conduct an annual performance evaluation of the nominating and corporate governance and compensation committees. |

We have previously relied on these exemptions, and we intend to continue to rely on them in the future. As a result, you may not have the same benefits and information available to stockholders of NYSE-listed companies that are subject to all of the NYSE corporate governance requirements.

The market price for our Common Stock may be volatile.

In recent periods, there has been volatility in the market price for our Common Stock. Furthermore, the market price of our Common Stock could fluctuate substantially in the future in response to a number of factors, including the following:

• | fluctuations in our quarterly operating results or the operating results of our competitors; |

• | changes in general conditions in the economy, the financial markets, or our industry; |

• | announcements of significant acquisitions, strategic alliances or joint ventures by us, our customers or our competitors; |

• | introduction of new products or services; |

• | increases in the price of energy sources and other raw materials; and |

• | other developments affecting us, our industry, customers or competitors. |

In addition, in recent years the stock market has experienced extreme price and volume fluctuations. This volatility has had a significant effect on the market prices of securities issued by many companies for reasons unrelated to their operating performance. These broad market fluctuations may materially adversely affect our Common Stock price, regardless of our operating results. Given its relatively small public float and average daily trading volume, our Common Stock may be relatively more susceptible to volatility arising from any of these factors. There can be no assurance that the price of our Common Stock will increase in the future or be maintained at its recent levels.

Future sales of our Common Stock could depress its market price.

Future sales of shares of our Common Stock could adversely affect its prevailing market price. If our officers, directors or significant stockholders sell a large number of shares, or if we issue a large number of shares, the market price of our Common Stock could significantly decline. Moreover, the perception in the public market that stockholders might sell shares of Common Stock could depress the market for our Common Stock. Our Common Stock’s relatively small public float and average daily trading volume may make it relatively more susceptible to these risks.

ITEM 1B – UNRESOLVED STAFF COMMENTS

None.

16

ITEM 2 – PROPERTIES

Real Property Holdings and Mineral Reserves

Land Owned | Land Leased | Land Unpatented Claims | Total | Estimated Proven Reserves | Estimated Probable Reserves | Total | |||||||||||||||

(acres) | (000's of tons) | ||||||||||||||||||||

California | 795 | — | 1,030 | 1,825 | 4,814 | 11,226 | 16,040 | ||||||||||||||

Georgia | 3,707 | 1,840 | — | 5,547 | 34,351 | 28,935 | 63,286 | ||||||||||||||

Illinois | 82 | 598 | — | 680 | 4,907 | 6,150 | 11,057 | ||||||||||||||

Mississippi | 2,156 | 999 | — | 3,155 | 80,692 | 94,523 | 175,215 | ||||||||||||||

Nevada | 535 | — | — | 535 | 23,316 | 2,976 | 26,292 | ||||||||||||||

Oregon | 340 | — | — | 340 | — | 25 | 25 | ||||||||||||||

Tennessee | 178 | — | — | 178 | 3,000 | 3,000 | 6,000 | ||||||||||||||

7,793 | 3,437 | 1,030 | 12,260 | 151,080 | 146,835 | 297,915 | |||||||||||||||

The Mississippi, Georgia, Tennessee, Nevada, California and Illinois properties are primarily mineral in nature, except our research and development facility which is included in the Illinois owned land. We mine sorbent minerals primarily consisting of montmorillonite and attapulgite and, to a lesser extent, other clay-like sorbent materials, such as Antelope shale. We employ geologists and mineral specialists who prepared the estimated reserves of these minerals in the table above. See also Item 1 “Business” above for further information about our reserves. The locations in the table above collectively produced approximately 844,000 tons in fiscal 2011, 863,000 tons in fiscal 2010 and 943,000 tons in fiscal 2009. Parcels of such land are also sites of manufacturing facilities operated by us. We own approximately one acre of land in Laval, Quebec, Canada, which is the site of the processing and packaging facility for our Canadian subsidiary.

MINING PROPERTIES

Our mining operations are conducted on leased or owned land. The Georgia, Illinois and Mississippi mining leases generally require that we pay a minimum monthly rental to continue the lease term. The rental payments are generally applied against a stated royalty related to the number of unprocessed, or in some cases processed, tons of mineral extracted from the leased property. Many of our mining leases have no stated expiration dates. Some of our leases, however, do have expiration dates ranging from 2014 to 2097. We would not experience a material adverse effect from the expiration or termination of any of these leases. We have a variety of access arrangements, some of which are styled as leases, for manufacturing at facilities that are not contiguous with the related mines. We would not experience a material adverse effect from the expiration or termination of any of these arrangements. See also Item 1 “Business” above for further information on our reserves.

Certain of our land holdings in California are represented by unpatented mining claims we lease from the Bureau of Land Management. These leases generally give us the contractual right to conduct mining or processing activities on the land covered by the claims. The validity of title to unpatented claims, however, is dependent upon numerous factual matters. We believe the unpatented claims we lease are in compliance with all applicable federal, state and local mining laws, rules and regulations. Future amendments to existing federal mining laws, however, could have a prospective effect on mining operations on federal lands and include, among other changes, the imposition of royalty fees on the mining of unpatented claims, the elimination or restructuring of the patent system and an increase in fees for the maintenance of unpatented claims. To the extent that future proposals may result in the imposition of royalty fees on unpatented lands, the mining of our unpatented claims may become economically unfavorable. We cannot predict the form that any such amendments might take or whether or when such amendments might be adopted. In addition, the construction and operation of processing facilities on these sites would require the approval of federal, state and local regulatory authorities. See Item 1A “Risk Factors” above for a discussion of other risks to our business related to our mining properties.

17

MINING AND MANUFACTURING METHODS

Mining and Hauling

We mine clay in open-pit mines in Georgia, Mississippi, Illinois and California. The mining and hauling operations are similar throughout the Oil-Dri locations, with the exception of California. The land to be mined is first stripped. The stripping process involves removing the overburden and preparing the site to allow the excavators to reach the desired clay. When stripping is completed, the excavators dig out and load the clay onto dump trucks. The trucks haul the clay directly to our processing plants where it is dumped in a clay yard and segregated by clay type if necessary. Generally, the mine sites are in close proximity to the processing plants; however, the maximum distance the clay is currently hauled to a plant is approximately 13 miles.

At our California mines the clay is excavated and hauled to a hopper. An initial crushing and screening operation is performed at the mine site before the trucks are loaded for delivery to the processing plant.

Processing

The processing of our clay varies depending on the level of moisture desired in the clay after the drying process. The moisture level is referred to as regular volatile moisture (“RVM”) or low volatile moisture (“LVM”).

RVM Clay: A front end loader is used to load the clay from the clay yard into the primary crusher. The primary crusher reduces the clay chunks to 2.0 inches in diameter or smaller. From the crusher, the clay is transported via a belt conveyor into the clay shed. A clay shed loader feeds the clay into a disintegrator which reduces the clay to particles 0.5 inches in diameter or smaller. The clay then feeds directly into the RVM kiln. The RVM kiln reduces the clay’s moisture content. From the RVM kiln, the clay moves through a series of mills and screens which further size and separate the clay into the desired particle sizes. The sized clay is then conveyed into storage tanks. The RVM processed clay can then be packaged or processed into LVM material.

LVM Clay: RVM clay is fed from storage tanks into the LVM kiln where the moisture content is further reduced. The clay then proceeds into a rotary cooler, then on to a screening circuit which separates the clay into the desired particle sizes.

In addition, certain fluid purification and animal health products are further processed into a powder form. We also use a proprietary process for our engineered granules to create spherical, uniform-sized granules.

Packaging

Once the clay has been dried to the desired level and sized the clay will be packaged. Our products have package sizes ranging from bags and jugs of cat litter to railcars of agricultural products. We also package some of our products into bulk (approximately one ton) bags or into bulk trucks. The size and delivery configuration of the finished product is determined by customer requirements.

18

FACILITIES

We operate manufacturing facilities on property owned or leased by us as shown on the map below:

Oil-Dri Corporation of America Plant Site Locations

Facilities | ||||

Location | Owned/Leased | Function | ||

Alpharetta, Georgia | Leased | Non-clay processing and packaging | ||

Bentonville, Arkansas | Leased | Sales office | ||

Blue Mountain, Mississippi | Both | Clay mining, manufacturing and packaging | ||

Chicago, Illinois | Leased | Principal executive office | ||

Coppet, Switzerland | Leased | Customer service office | ||

Laval, Quebec, Canada | Owned | Non-clay production and clay and non-clay packaging | ||

Mounds, Illinois | Owned | Clay mining, manufacturing and packaging | ||

Ochlocknee, Georgia | Owned | Clay mining, manufacturing and packaging | ||

Ripley, Mississippi | Owned | Clay mining, manufacturing and packaging | ||

Taft, California | Owned | Clay mining, manufacturing and packaging | ||

Vernon Hills, Illinois | Owned | Research and development | ||

Wisbech, United Kingdom | Leased | Non-clay production and clay and non-clay packaging | ||

We have no mortgages on the real property we own. The leases for the Alpharetta, Georgia facility and the Bentonville, Arkansas office expire in 2013. The lease for the Chicago, Illinois corporate office space expires in 2018. The lease for the Wisbech, United Kingdom facility expires in 2032. The lease for the Coppet, Switzerland office is on a year-to-year basis. We consider that our properties are generally in good condition, are well maintained and are suitable and adequate to carry on our business.

19

ITEM 3 – LEGAL PROCEEDINGS

We are party to various legal actions from time to time that are ordinary in nature and incidental to the operation of our business. While it is not possible at this time to determine with certainty the ultimate outcome of these or other lawsuits, we believe that none of the pending proceedings will have a material adverse effect on our business or financial condition.

ITEM 4 – [RESERVED]

20

PART II

ITEM 5 – MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our Common Stock is traded on the NYSE under the symbol ODC. There is no established trading market for our Class B Stock. There are no shares of Class A Common Stock currently outstanding. See Note 6 of the Notes to the Consolidated Financial Statements for a description of our Common Stock, Class B Stock and Class A Common Stock. The number of holders of record of Common Stock and Class B Stock on September 30, 2011 were 693 and 29, respectively, as reported by our transfer agent. In the last three years, we have not sold any securities which were not registered under the Securities Act of 1933.

The following table sets forth, for the periods indicated, the high and low sales price for our Common Stock listed on the NYSE and dividends per share paid on our Common Stock and Class B Stock.

Common Stock Price Range | Cash Dividends Per Share | |||||||||||||||

Low | High | Common Stock | Class B Common Stock | |||||||||||||

Fiscal 2011: | ||||||||||||||||

First Quarter | $ | 18.73 | $ | 22.20 | $ | 0.1600 | $ | 0.1200 | ||||||||

Second Quarter | 18.81 | 23.00 | 0.1600 | 0.1200 | ||||||||||||

Third Quarter | 18.74 | 22.17 | 0.1600 | 0.1200 | ||||||||||||

Fourth Quarter | 19.11 | 22.39 | 0.1700 | 0.1275 | ||||||||||||

Total | $ | 0.6500 | $ | 0.4875 | ||||||||||||

Fiscal 2010 | ||||||||||||||||

First Quarter | $ | 14.05 | $ | 17.40 | $ | 0.1500 | $ | 0.1125 | ||||||||

Second Quarter | 14.75 | 16.54 | 0.1500 | 0.1125 | ||||||||||||

Third Quarter | 15.10 | 20.76 | 0.1500 | 0.1125 | ||||||||||||

Fourth Quarter | 18.50 | 23.53 | 0.1600 | 0.1200 | ||||||||||||

Total | $ | 0.6100 | $ | 0.4575 | ||||||||||||

Dividends. Our Board of Directors determines the timing and amount of any dividends. Our Board of Directors may change its dividend practice at any time. The declaration and payment of future dividends, if any, will depend, among other things, upon our future earnings, capital requirements, financial condition, legal requirements, contractual restrictions and other factors that our Board of Directors deems relevant. Our 1998 Note Agreement with Prudential Financial, our Credit Agreement with Harris N.A. and our 2005 Note Agreement with The Prudential Insurance Company of America and Prudential Retirement Insurance and Annuity Company require that certain minimum net worth and tangible net worth levels are to be maintained. To the extent that these balances are not attained, our ability to pay dividends may be impaired. See Note 3 of the Notes to the Consolidated Financial Statements for further information about our note agreements.

Issuer Repurchase of Equity Securities. On October 10, 2005, our Board of Directors authorized the repurchase of up to 500,000 shares of Common Stock, with repurchases to be made from time to time at the discretion of our management and in accordance with applicable laws, rules and regulations. All shares under this authorization have been repurchased. On March 11, 2010 and also on March 11, 2011, our Board of Directors authorized the repurchase of an additional 250,000 shares of Common Stock. These authorizations do not have a stated expiration date. We did not repurchase any shares of our Common Stock in the three months ended July 31, 2011. As of July 31, 2011, a total of 366,877 shares of Common Stock may yet be repurchased under these authorizations. We do not have any current authorization from our Board of Directors to repurchase shares of Class B Stock.

21

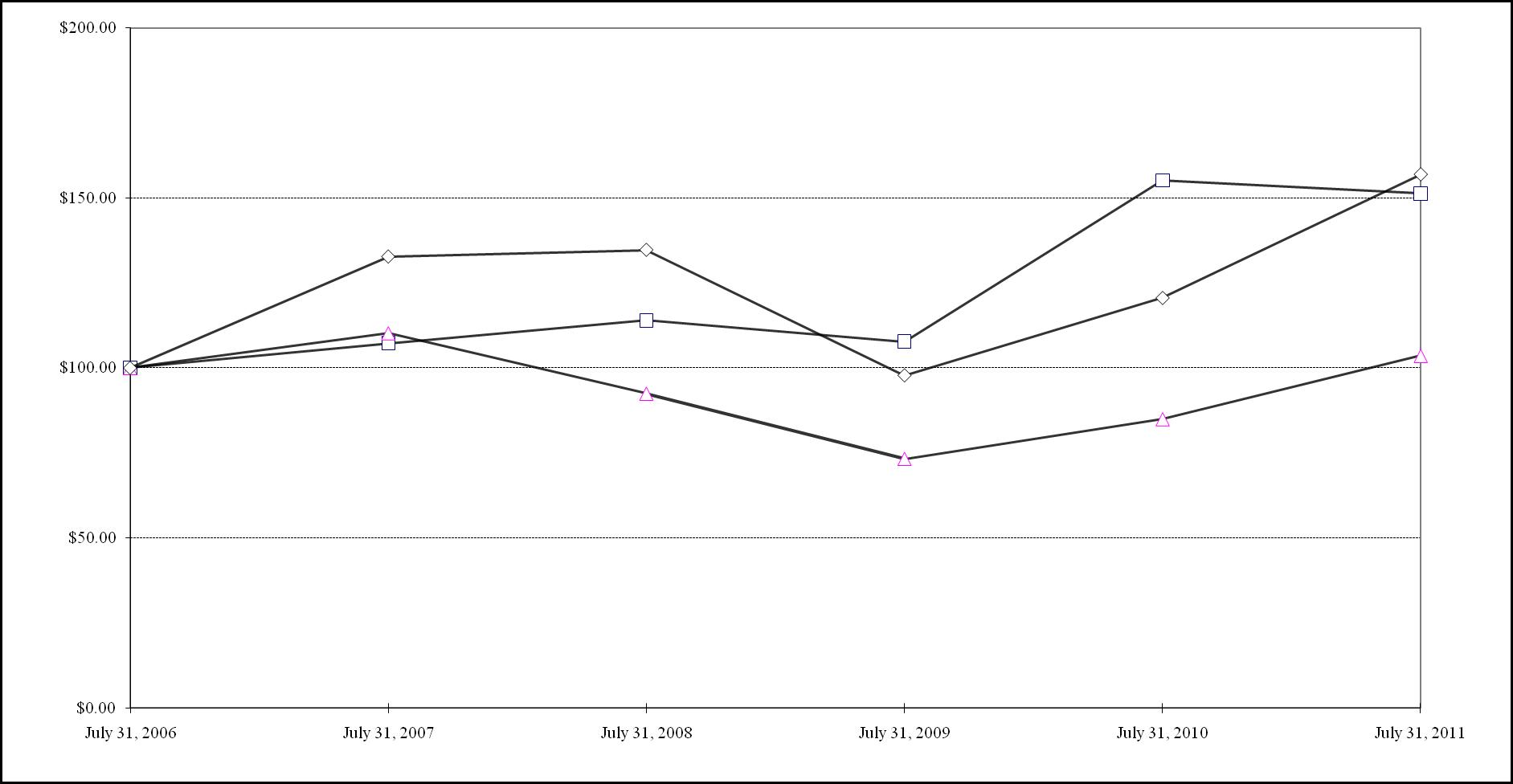

PERFORMANCE GRAPH

The following graph shows the annual cumulative total stockholders’ return for the five years ending July 31, 2011 on an assumed investment of $100 on July 31, 2006 in our Common Stock, the Russell Microcap Index and the Russell 2000-Material and Processing Economic Sector Index. Our Common Stock is included in the Russell Microcap Index and we consider the Russell 2000-Material and Processing Economic Sector Index to be our peer group. The graph assumes all dividends were reinvested. The historical stock price performance of our Common Stock is not necessarily indicative of future stock performance.

Comparative Five-Year Total Returns

Oil-Dri Corporation of America, Russell Microcap Index , Russell 2000-Materials & Processing Index

(Performance results through 7/31/2011)

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||||||||||||||||

ODC | o | $ | 100.00 | $ | 107.29 | $ | 113.94 | $ | 107.73 | $ | 155.10 | $ | 151.31 | ||||||||

Russell Microcap | r | $ | 100.00 | $ | 110.22 | $ | 92.46 | $ | 73.29 | $ | 84.96 | $ | 103.58 | ||||||||

Russell 2000-Materials & Processing | ∏ | $ | 100.00 | $ | 132.71 | $ | 134.67 | $ | 97.83 | $ | 120.54 | $ | 156.84 | ||||||||