Attached files

| file | filename |

|---|---|

| EX-21.1 - EXHIBITT 21.1 - Bohai Pharmaceuticals Group, Inc. | v235937_ex21-1.htm |

| EX-31.1 - EXHIBIT 31.1 - Bohai Pharmaceuticals Group, Inc. | v235937_ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Bohai Pharmaceuticals Group, Inc. | v235937_ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Bohai Pharmaceuticals Group, Inc. | v235937_ex32-1.htm |

| EX-32.2 - EXHIBIT 32.2 - Bohai Pharmaceuticals Group, Inc. | v235937_ex32-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the fiscal year ending June 30, 2011

|

OR

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the transition period from ________ to ________.

|

Commission file number 000-53401

Bohai Pharmaceuticals Group, Inc.

(Exact name of registrant as specified in its charter)

|

Nevada

|

98-0697405

|

|

|

(State or other jurisdiction

of incorporation or organization)

|

(IRS Employer

Identification number)

|

|

|

c/o Yantai Bohai Pharmaceuticals Group Co. Ltd.

No. 9 Daxin Road, Zhifu District

Yantai, Shandong Province, China

|

264000

|

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

+86(535)-685-7928

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

None

(Title of Class)

Name of each exchange on which registered

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

|

Non-accelerated filer ¨

|

Smaller reporting company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x.

The aggregate market value of the voting and non-voting common stock, other than shares held by persons who may be deemed affiliates of the registrant, computed by reference to the closing sales price for the registrant’s Common Stock on December 31, 2010, as reported on the OTC Bulletin Board, was approximately $13,299,122.

As of September 28, 2011, there were 17,861,085 outstanding shares of common stock of the registrant, par value $.001 per share.

DOCUMENTS INCORPORATED BY REFERENCE

None

Bohai Pharmaceuticals Group, Inc.

Annual Report on Form 10-K for the

Fiscal Year Ended June 30, 2011

TABLE OF CONTENTS

|

Page

|

||

|

Cautionary Note Regarding Forward Looking Statements

|

-i-

|

|

|

PART I

|

1

|

|

|

Item 1.

|

Business.

|

1

|

|

Item 1A.

|

Risk Factors.

|

23

|

|

Item 1B.

|

Unresolved Staff Comments.

|

44

|

|

Item 2.

|

Description of Properties.

|

44

|

|

Item 3.

|

Legal Proceedings.

|

44

|

|

PART II

|

45

|

|

|

Item 5.

|

Market for Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities Market Information.

|

45

|

|

Item 6.

|

Selected Financial Data.

|

45

|

|

Item 7.

|

Management’s Discussion and Analysis or Plan of Operation.

|

46

|

|

Item 7A.

|

Quantitative and Qualitative Disclosures about Market Risk.

|

58

|

|

Item 8.

|

Financial Statements and Supplementary Data.

|

58

|

|

Item 9.

|

Changes In and Disagreements with Accountants On Accounting and Financial Disclosure.

|

58

|

|

Item 9A.

|

Controls and Procedures.

|

59

|

|

Item 9B.

|

Other Information.

|

61

|

|

PART III

|

62

|

|

|

Item 10.

|

Directors, Executive Officers, Promoters and Control Persons; Compliance With Section 16(A) of the Exchange Act.

|

62

|

|

Item 11.

|

Executive Compensation

|

65

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management

|

67

|

|

Item 13.

|

Certain Relationships and Related Transactions and Director Independence.

|

68

|

|

Item 14.

|

Principal Accountant Fees and Services.

|

69

|

|

Part IV

|

70

|

|

|

Item 15.

|

Exhibits

|

70

|

|

FINANCIAL STATEMENTS

|

F-1

|

|

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

In addition to historical information, this Annual Report on Form 10-K contains forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. The forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those reflected in such forward-looking statements. Factors that might cause such a difference include, but are not limited to those discussed in the sections entitled “Business”, “Risk Factors”, and “Management’s Discussion and Analysis or Plan of Operation.” Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management’s opinions only as of the date thereof. We undertake no obligation to revise or publicly release the results of any revision of these forward-looking statements. Readers should carefully review the risk factors described in this Annual Report and in other documents that we file from time to time with the Securities and Exchange Commission.

In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “projects,” “potential,” “proposed,” “intended,” or “continue” or the negative of these terms or other comparable terminology. You should read statements that contain these words carefully, because they discuss our expectations about our future operating results or our future financial condition or state other “forward-looking” information. There may be events in the future that we are not able to accurately predict or control. You should be aware that the occurrence of any of the events described in our risk factors and other disclosures included in this Annual Report could substantially harm our business, results of operations and financial condition, and that upon the occurrence of any of these events, the trading price of our securities could decline. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, growth rates, and levels of activity, performance or achievements. Factors that may cause actual results, our performance or achievements, or industry results, to differ materially from those contemplated by such forward-looking statements include, without limitation:

|

|

·

|

our ability to generate or obtain through financing sufficient working capital to (i) fund the acquisition of Yantai Tianzheng (currently $12 million is due within 12 months, and a total of $29 million is due); (ii) satisfy our obligations under our convertible notes due January 5, 2012 (currently $10.45 million due) or (iii) otherwise to support our business plans;

|

|

|

·

|

our ability to integrate the business of Yantai Tianzheng and any future acquisitions into our business;

|

|

|

·

|

our ability to expand our product offerings and maintain the quality of our products;

|

|

|

·

|

the availability of government granted rights to exclusively manufacture or co-manufacture our products;

|

|

|

·

|

the availability of national healthcare reimbursement of our products;

|

|

|

·

|

our ability to manage our expanding operations and continue to fill customers’ orders on time;

|

|

|

·

|

our ability to maintain adequate control of our expenses allowing us to realize anticipated revenue growth;

|

|

|

·

|

our ability to maintain or protect our intellectual property;

|

|

|

·

|

our ability to maintain our proprietary technology;

|

|

|

·

|

the impact of government regulation in China and elsewhere, including the support provided by the Chinese government to the Traditional Chinese Medicine and healthcare sectors in China;

|

|

|

·

|

our ability to implement product development, marketing, sales and acquisition strategies and adapt and modify them as needed;

|

-i-

|

|

·

|

our implementation of required financial, accounting and disclosure controls and procedures and related corporate governance policies; and

|

|

|

·

|

our ability to anticipate and adapt to changing conditions in the Traditional Chinese Medicine and healthcare industries resulting from changes in government regulations, mergers and acquisitions involving our competitors, technological developments and other significant competitive and market dynamics.

|

Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results. The following discussion should be read in conjunction with our financial statements and the related notes that appear elsewhere in this report.

We cannot give any guarantee that these plans, intentions or expectations will be achieved. All forward-looking statements involve significant risks and uncertainties, and actual results may differ materially from those discussed in the forward-looking statements as a result of various factors, including those factors listed above and described in the “Risk Factors” section of this Annual Report.

-ii-

PART I

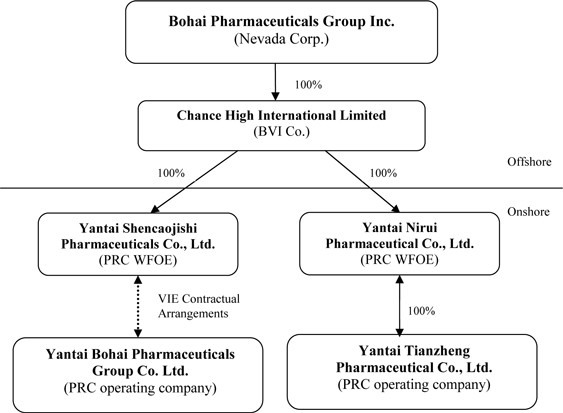

As used throughout this Annual Report, the terms “BOPH,” “Company,” “we,” “us,” or “our” refer to Bohai Pharmaceuticals Group, Inc., a Nevada corporation, together with:

(i) its wholly owned subsidiary, Chance High International Limited, a British Virgin Islands company (“Chance High”);

(ii) Chance High’s wholly owned subsidiary, Yantai Shencaojishi Pharmaceuticals Co., Ltd., a PRC company (“WFOE”);

(iii) Chance High’s wholly owned subsidiary, Yantai Nirui Pharmaceutical Co., Ltd., a PRC company (“WFOE II”);

(iv) the WFOE’s variable interest entity, Yantai Bohai Pharmaceuticals Group Co., Ltd., a PRC company (“Bohai”), which is our initial operating subsidiary; and

(v) WFOE II’s wholly owned subsidiary, Yantai Tianzheng Pharmaceutical Co., Ltd., a PRC company (“Yantai Tianzheng”), which we acquired in August 2011 and is our second operating subsidiary.

In this Annual Report, we sometimes refer to BOPH, Chance High, WFOE, WFOE II, Bohai and Yantai Tianzheng collectively as the “Group.” As used in this Annual Report, “China” or “the PRC” refers to the People’s Republic of China.

Item 1. Business.

Overview

We are engaged in the production, manufacturing and distribution in China of herbal pharmaceuticals based on traditional Chinese medicine, which we refer to herein as Traditional Chinese Medicine, or TCM. We are based in the city of Yantai, Shandong Province, China and our operations are exclusively in China.

Our medicines address rheumatoid arthritis, viral infections, gynecological diseases, cardio vascular issues and respiratory diseases. Our initial operating subsidiary Bohai obtained Drug Approval Numbers (or DANs) for 29 varieties of traditional Chinese herbal medicines in 2004, an additional 14 varieties in December 2010. Through our acquisition of Yantai Tianzheng in August 2011, we obtained DANs for another 5 varieties in August 2011. We currently produce 19 varieties of approved traditional Chinese herbal medicines in seven delivery systems: tablets, granules, capsules, formulations, concentrated powder, tincture and medicinal wine. Of these 19 products, 12 are prescription drugs and 7 are over the counter (or OTC) products.

Three of Bohai’s lead products, Tongbi Capsules and Tablets and Lung Nourishing Syrup, are eligible for reimbursement under China’s National Medical Insurance Program (or NRDL), which we believe significantly increases the marketability of these products. In addition to these lead products, three of our current products and five of our formulas we acquired in 2010 are eligible for NRDL reimbursement. In addition, one of our current products and four of our newly acquired formulas are currently included on the Chinese government's Essential Drug List (or EDL). Inclusion on either the EDL or NRDL allows for up to 100% insurance coverage by the Chinese government. Yantai Tianzheng owns five prescription products approved by the State Food and Drug Administration of China (which we refer to herein as the SFDA) and currently manufactures four of such products. Among Yantai Tianzheng’s products, Fangfengtongsheng Granule has an exclusive status and is on the EDL and NDRL. Zhengxintai Capsule is in the process of renewal its protective status and is currently on NDRL.

1

The Chinese government has previously awarded us exclusive rights to manufacture our Tongbi Capsules product. We share manufacturing rights with one or more manufacturers for our Anti-flu Granules product, which rights expire on July 9, 2012. We held the Certificates of Protected Variety of Traditional Chinese Medicine (Grade Two) (which we refer to herein as the Certificate of Protection) issued by the SFDA for Tongbi Capsules and Shangtongning Tablets, which give us exclusive or near-exclusive rights to manufacture and distribute these two medicines. The protection periods for both Tongbi Capsules and Shangtongning Tablets expired in September 2009. We submitted the application to extend such protection period for Tongbi Capsules on March 12, 2009. The SFDA approved our request and the protection period for Tongbi Capsules has been extended to September 13, 2016. We have decided to not submit an extension of protection application for Shangtongning Tablets, but will continue to manufacture this product.

Our strategy is to leverage the “protected” status and national insurance coverage for certain of our pharmaceutical products to aggressively increase market penetration throughout China, the world’s most populous nation. By utilizing our distribution platform, in addition to utilizing mass media and other marketing methods to build awareness of our brand, we have been able to and will continue to seek to significantly grow our revenues and earnings. In addition, as evidenced by our acquisition of Yantai Tianzheng, we may seek additional acquisition candidates or undertake other strategic transactions to broaden our product offerings and sales, marketing and manufacturing capabilities.

We are focusing a significant portion of our marketing efforts on our Lung Nourishing Syrup and expect to continue this effort over the next several years. Lung Nourishing Syrup( which we formerly referred to as “Lung Nourishing Cream”), an ingestible liquid product, is one of our most popular products, and its main ingredient, Laiyang Pear, to our knowledge, is not available in other similar pharmaceutical products. We applied for a patent for Lung Nourishing Syrup with its production method for the treatment of Lung Qi Deficiency Cough and Chronic Bronchitis, which application was approved by the State Intellectual Property Office of the PRC on June 23, 2010. The patent was awarded for a period of 20 years starting from the day of its application on September 12, 2007. For these reasons, we believe Lung Nourishing Syrup contains a novel formulation for the treatment of asthma and other common respiratory ailments with an emphasis on the improvement of overall lung function and health. We believe this represents an exceptional market opportunity.

Our business strategy also seeks to capitalize on new government programs established in early 2009 to extend health insurance coverage to previously uncovered Chinese citizens. The PRC government’s new health care policies are also designed to encourage the use of TCM and its approach to wellness and treatment of disease. As a result, the government continues to expand the number of TCMs eligible for reimbursement under national medical insurance programs. This has resulted in medical professionals working in the state-run medical facilities to increasingly prescribe and recommend TCM products of the type we manufacture and market. The state-run facilities provide the majority of medical care in China. Three of our lead products, Lung Nourishing Syrup and Tongbi Capsules and Tablets, are eligible for insurance reimbursement coverage, with others expected to follow. Currently public health officials in China are developing general consumer awareness of increasing problems and concerns with respiratory and lung health caused by pervasive national air pollution. This nationwide epidemic is an unfortunate by-product of the robust development of China’s expansive manufacturing and industrial activities. Increased air pollution is a cause and contributory factor to a range of acute respiratory illnesses including chronic conditions such as asthma. As a result, we intend to significantly increase our advertising for our Lung Nourishing Syrup.

As of the date of this Annual Report, we have approximately 847 employees operating from 21 offices throughout China. As we are committed to strong sales efforts, approximately 354 of our employees are sales representatives.

As is not uncommon for Chinese companies listed in the U.S., we control our Chinese operating subsidiary, Bohai, pursuant to a series of variable interest entity contractual agreements (the “VIE Agreements”), under which we assume management of the business activities of Bohai and have the right to appoint all executives and senior management and the members of the board of directors of Bohai. Under these arrangements, however, we do not, directly or indirectly, own any shares in Bohai, which are owned by Mr. Qu, our Chairman, President and Chief Executive Officer and two unaffiliated parties. Please see “Contractual Arrangements with Bohai and its Shareholders” below.

We do, however, directly own our Yantai Tianzheng operating subsidiary through WFOE II.

2

Background and Key Events

We were incorporated under the laws of the State of Nevada under the name Link Resources Inc. on January 9, 2008. Our principal office was in Calgary, Alberta, Canada. Prior to January 5, 2010, we were a public “shell” company in the exploration stage since our formation and had not yet realized any revenues. We entered into a Mineral Lease Agreement on April 1, 2008 for two mining claims in Pershing County, Nevada, in an area known as the Goldbanks East Prospect. We terminated the lease on July 7, 2009.

Share Exchange with Chance High

Pursuant to the Share Exchange Agreement entered into on January 5, 2010 (the “Share Exchange Agreement”), and related share exchange (the “Share Exchange”) by and among us, Chance High, and the shareholders of Chance High (the “Chance High Shareholders”), we acquired Chance High and its indirect, controlled subsidiary Bohai, a Chinese company engaged the production, manufacturing and distribution in China of herbal medicines, including capsules and other products, based on Traditional Chinese Medicine. The closing of the Share Exchange (the “Closing”) took place on January 5, 2010. As of the Closing, pursuant to the terms of the Share Exchange Agreement, we acquired all of the outstanding equity securities (the “Chance High Shares”) of Chance High from the Chance High Shareholders, and the Chance High Shareholders transferred and contributed all of their Chance High Shares to us. In exchange, we issued to Chance High Shareholders an aggregate of 13,162,500 newly issued shares of our common stock.

In addition, pursuant to the terms of the Share Exchange Agreement, Anthony Zaradic, our former sole officer and director (“Zaradic”), cancelled a total of 1,500,000 shares of common stock owned by him. As a further condition of the Share Exchange, effective as of January 5, 2010, Zaradic resigned from all of his positions with our company and Hongwei Qu (“Qu”), the former principal shareholder and Executive Director of Bohai, was appointed as our President, Chief Executive Officer, Interim Chief Financial Officer, Treasurer and Secretary and also, effective January 16, 2010, as our sole director. In June 2010, Mr. Qu relinquished the positions of Interim Chief Financial Officer, Treasurer and Secretary and we appointed Gene Hsiao as our Chief Financial Officer. On July 12, 2010, we appointed three independent directors to our board of directors.

January 5, 2010 Private Placement and Related Agreements

Securities Purchase Agreement. On January 5, 2010, we entered into a Securities Purchase Agreement (the “Securities Purchase Agreement”) with certain accredited investors (the “Investors”) and Euro Pacific Capital, Inc. (“Euro Pacific”), as representative of the Investors, relating to a private placement by us of 6,000,000 units consisting of Notes and Warrants, which we refer to herein as the private placement. The consummation of the private placement resulted in gross proceeds to us of $12,000,000 and net proceeds of approximately $9,700,000. Each unit consisted of a $2.00 principal amount, two year convertible Note and a three year Warrant to purchase one share of our common stock at $2.40 per share, subject to certain conditions. Euro Pacific acted as the lead placement agent and Chardan Capital Markets, LLC acted as co-placement agent of the private placement.

Registration Rights Agreement. In connection with the private placement, we entered into Registration Rights Agreement (the “Registration Rights Agreement”) with the Investors which sets forth the rights of the Investors to have the shares of common stock underlying the Notes and Warrants issued in the private placement registered with the Securities and Exchange Commission (“SEC”) for public resale. We filed such registration statement with the SEC, and registration statement was declared effective by the SEC on August 12, 2010.

Securities Escrow Agreement. Also in connection with the private placement, we entered into a Securities Escrow Agreement (the “Securities Escrow Agreement”) with Euro Pacific, as representative of the Investors, our principal shareholder, Glory Period Limited, a British Virgin Islands company that we refer to herein as Glory Period and which was the majority shareholder of Chance High prior to the Share Exchange, and Escrow, LLC, as escrow agent (the “Escrow Agent”). Pursuant to the Securities Escrow Agreement, Glory Period has pledged and deposited a stock certificate representing 1 million shares of our common stock (the “Escrow Shares”) into escrow in order to provide security to the Investors in the event of an occurrence of an event of default under the Notes. Upon the earlier to occur of the full repayment of all amounts due to the Investors under the Notes or the conversion of fifty percent of the principal face value of Notes into shares of common stock, the Investors’ rights in and to the Escrow Shares shall terminate. Glory Period is controlled by Qu through certain contractual relationships described elsewhere in this Annual Report.

3

Closing Escrow Agreement. Pursuant to a Closing Escrow Agreement (the “Closing Escrow Agreement”) that we entered into in connection with the private placement on December 10, 2009, we placed a total of $240,000 of proceeds from the private placement (the “Holdback Amount”) with the Escrow Agent. The Holdback Amount represents an amount sufficient to satisfy the payment to the Investors of one quarterly interest payment due on the aggregate principal amount of all Notes issued in the private placement. If, subject to certain conditions and after applicable notice and cure periods, an event of default is declared by Euro Pacific with respect to our failure to make a quarterly interest payment to Investors, the Escrow Agent shall disburse such portion of the Holdback Amount to the Investors, and we shall be obligated to deposit additional amounts equal to the Holdback Amount with Escrow Agent. At such time as seventy-five percent of the aggregate shares of common stock underlying the Notes have been issued upon conversion of the Notes, all remaining funds of the Holdback Amount shall promptly be disbursed to us.

Corporate Name Change

On January 29, 2010, we entered into an Agreement and Plan of Merger (the “Merger Agreement”) pursuant to which we merged with a newly formed, wholly owned subsidiary called Bohai Pharmaceuticals Group, Inc., a Nevada corporation (“Merger Sub” and such merger transaction, the “Merger”). Upon the consummation of the Merger, the separate existence of Merger Sub ceased and our shareholders became shareholders of the surviving company named Bohai Pharmaceuticals Group, Inc. As permitted by Chapter 92A.180 of Nevada Revised Statutes, the sole purpose of the Merger was to effect a change of our corporate name.

Changes of Our Independent Registered Accounting Firms

Effective January 29, 2010, upon the approval of our board of directors, we dismissed John Kinross-Kennedy as our independent registered public accountant and appointed Parker Randall CF (H.K.) CPA Limited (or Parker Randall) as our independent registered public accounting firm.

On June 24, 2011, the audit committee of our board of directors approved the dismissal of Parker Randall as our independent registered public accounting firm, effective as of June 28, 2011, and appointed Marcum Bernstein & Pinchuk LLP as our independent registered public accounting firm as of June 24, 2011.

Intangible Assets Transfer

On December 9, 2010, we entered into an Transfer Agreement of Intangible Assets (the “Transfer Agreement”) with Shandong Daxin Microbiology Pharmaceutical Industry Co., Ltd., a company incorporated in the People’s Republic of China (“Daxin”), pursuant to which Daxin agreed to transfer to us all rights and title in and to 14 Drug Approval Numbers (“DANs”) for 14 traditional Chinese medicines, which DANs were previously issued to Daxin by the Shandong Branch of the SFDA. The aggregate purchase price is RMB 48 million (approximately US$7,200,000). As of the date of the execution of the Transfer Agreement, the proposed transfer of the aforementioned 14 DANs has been approved by Shandong SFDA. Such purchase price has been paid in full.

Acquisition of Yantai Tianzheng

On August 8, 2011, WFOE II entered into a Share Purchase Agreement (the “SPA”) pursuant to which we acquired, from the three individual holders thereof, one hundred percent (100%) of the outstanding shares of Yantai Tianzheng. Under the terms of the SPA, WFOE II will purchase such shares from Mr. Jiangbo Chi, Ms. Shulian Wang and Mr. Bohai Yu. The percentage interests owned by Mr. Chi, Ms. Wang and Mr. Yu in Yantai Tianzheng, are 60%, 30% and 10%, respectively. The SPA also contained customary representations, warranties and covenants of the parties. Mr. Chi (the majority shareholder of Yantai Tianzheng) also entered into an agreement related to his employment by Yantai Tianzheng, ownership of his future work products and certain confidentiality and non-compete obligations.

4

The purchase price to be paid for Yantai Tianzheng is $35,000,000 in the aggregate. Pursuant to the SPA, the purchase price is payable in cash in the following installments:

1. The first cash payment in the aggregate amount of $ 6,000,000 was paid within 10 calendar days after the execution of the SPA.

2. The second cash payment in the amount of $12,000,000 will be payable within 6 months after the execution of the SPA, subject to certain conditions (unless otherwise waived), such as the performance of all “transition period” obligations related to renewal or extension of material operational agreements and employment agreements.

3. The third cash payment of $12,000,000 will be payable within 1 year after the execution of the SPA, subject to certain conditions (unless otherwise waived), such as amendment or obtainment of certain certificates and license necessary for consummation of the transaction.

4. The fourth cash payment of $5,000,000 will be payable within 18 months after the execution of the SPA, subject to certain conditions.

In addition, each installment requires satisfaction of conditions applicable to its prior payment(s), completion of assignment of certain licenses or certificates, and absence of a material adverse change affecting Yantai Tianzheng during the respective installment periods. In the event that WFOE II fails to pay any of the installments when due, such outstanding installment will be automatically converted into a two-year term loan owed by WFOE II to the Shareholders of Yantai Tianzheng, with interest accruing on any unpaid portion of such loan from its due date until such installment is paid in full at the rate of six percent (6%) per annum. As long as such interest payments are made on a timely basis and the outstanding principal of such loan and interest are satisfied in full within 2 years after the applicable installment failure date, WFOE II will not be deemed in breach or default under the SPA and will continue to possess full control and legal ownership over Yantai Tianzheng. Furthermore, even in the event of non-payment by WFOE II of any principal or interest under the loans as described above, or in the event of any other breach or default by WFOE II of the SPA, the remedies of the former Yantai Tianzheng Shareholders against WFOE II are limited solely to monetary damages, and in all instances such Shareholders will have no right to reclaim ownership of Yantai Tianzheng or demand that WFOE II in any way revert control or legal ownership over the shares of Yantai Tianzheng back to such shareholders.

The acquisition of Yantai Tianzheng marked a major milestone for our company. The acquisition expanded our product lines and will allow us to leverage our respective sales and distribution channels. Yantai Tianzheng’s current sales network spans over 14 major provinces as well as over 14 Tier 2 and Tier 3 cities, with products sold in over 1,100 hospitals across China. In addition, Yantai Tianzheng brings additional manufacturing capacity which meets GMP standards and will allow us to further expand our production. We plan to consolidate and integrate the two companies’ operations, which could provide substantial improvement in the operating efficiency of the combined companies.

Intangible Asset Impairment

During the fourth quarter of our 2011 fiscal year, we determinate that we will no longer manufacture or seek to develop a market for eight of our products due to a change of our business strategy resulting from our acquisition of Yantai Tianzheng. As a result of this decision, the total cost of these eight products, in the amount of $635,442, was charged to non-cash impairment loss during the 4th quarter of the fiscal year ended June 30, 2011. Even though we incurred an impairment loss for these eight products, we continue to retain a full ownership of these products and can still manufacture them at any time we deem desirable.

5

Corporate Structure and Related Agreements

Our organizational structure as of the date of this Annual Report is summarized below:

Chance High owns 100% of the issued and outstanding capital stock of the WFOE. On December 7, 2009, the WFOE entered into a series of variable interest entity contractual agreements (the “VIE Agreements”) with Bohai and its three shareholders, which include Qu (our Chairman, President and Chief Executive Officer, who owns 90% of Bohai’s shares) and two unaffiliated parties. Pursuant to the VIE Agreements, WFOE does not directly own the equity of our operating subsidiary, but rather effectively assumed management of the business activities of Bohai and has the right to appoint all executives and senior management and the members of the board of directors of Bohai. The VIE Agreements are comprised of a series of agreements, including a Consulting Services Agreement, Operating Agreement and Proxy Agreement, through which WFOE has the right to advise, consult, manage and operate Bohai for an annual fee in the amount of Bohai’s yearly net profits after tax. Additionally, Bohai’s Shareholders have pledged their rights, titles and equity interest in Bohai as security for WFOE to collect consulting and services fees provided to Bohai through an Equity Pledge Agreement. In order to further reinforce WFOE’s rights to control and operate Bohai, Bohai’s shareholders granted WFOE an exclusive right and option to acquire all of their equity interests in Bohai through an Option Agreement.

In addition, on December 7, 2009, Mr. Qu entered into a call option agreement (the “Call Option Agreement”) with Joshua Tan (“Tan”), the sole shareholder of Glory Period, a British Virgin Islands company, which was the majority shareholder of Chance High prior to the share exchange. The Call Option Agreement became effective upon the closing of the Share Exchange. Under the Call Option Agreement, Tan shall transfer up to 100% shares of Glory Period within the next 3 years to Qu for nominal consideration, which would give Qu indirect ownership of a significant percentage of our common stock. The Call Option Agreement provides that Tan shall not dispose any of the shares of Glory Period without Qu’s prior written consent.

6

Executive Offices

Our headquarters are located at No. 9 Daxin Road, Zhifu District, Yantai, Shandong Province, P.R. China 264000. Our telephone number is +86(535)-685-7928.

Overview of Traditional Chinese Medicine

In China, Traditional Chinese Medicine is not an alternative form of therapy but is used in the state-run hospitals alongside modern medicine. For its practitioners and advocates, TCM is a complete medical system that is used to treat disease in all its forms. TCM is also believed to promote long term wellness and vigor. Many modern-day drugs have been developed from herbal sources. These include drugs designed to treat asthma and hay fever such as ephedrine; hepatitis remedies from fruits and licorice roots and a number of anticancer agents from trees and shrubs.

For the Chinese, however, health is more than just the absence of disease. Chinese herbal medicine is not only intended to cure but to enhance the capacity for enjoyment, fulfillment and happiness. Accordingly, there are herbal drugs that are used to invigorate, nourish blood, calm tension and regulate menstruation.

The roots of TCM date back thousands of years and include a number of therapeutic approaches. These include herbal medications, acupuncture, dietary manipulation, massage and others. Very early works of Chinese medical literature date back as much as 2,500 years while other classics appeared approximately 2,000 years ago during the Han Dynasty. Medicine in China continued to develop throughout the Middle Ages when emperors commissioned the creation of various scholarly works that compiled and documented hundreds of medicines derived from herbs, animal sources and minerals. In addition, these works described their therapeutic uses. In the 1950s, TCM was further modernized and reformed by the PRC government.

The emphasis on wellness and the avoidance of disease is considered by some to be a key distinction between TCM and western medical practice which has been seen as more heavily oriented toward the treatment of disease and less toward prevention. While TCM has remained a substantial part of medical treatment in China and throughout East Asia, recent decades have seen increasing acceptance throughout the United States, Europe and elsewhere. This growth is, in part, driven by increasingly educated and empowered consumers of medical care who seek organic, natural and alternative approaches to western medical treatments and prescription drugs. Medical doctors are also accelerating the process of acceptance, as doctors trained in the western tradition in Europe, the United States and elsewhere are integrating TCM and alternative treatments in their everyday practice. Additionally, a growing number of physicians specifically trained in TCM, acupuncture and other modalities are opening offices in communities in the U.S. and around the world.

We believe that the sales of TCM in China reflect the central and still growing role these therapies play in medical care in that nation. According to Helmut Kaiser Consultancy, in 2005, total sales revenue for Chinese herbal medicine manufactured in China was $13.6 billion which accounted for 25.8% of all medicine manufactured in China. This segment had total profit of $1.76 billion which accounted for 29% of the total profit of the Chinese drug industry. In 2006, there were approximately 1,400 Chinese herbal medicine manufacturers with an annual growth rate of 15%, much higher than the comparable period GDP growth. According to Helmut Kaiser Consultancy, as a result of the increasing wealth of China and an aging population, it is estimated that by 2010, China will be the fifth largest market for herbal medicines in the world exceeding more than $24 billion in sales.

According to a published report by PricewaterhouseCoopers, in 2009 China had more than 7,000 distributors supplying pharmaceuticals to hospitals and pharmacies. According to such report, most Chinese seeking medical care go directly to the hospitals where more than 80% of the medicines used throughout China are prescribed. Only recently have chain drug stores begun to appear allowing drugs to be obtained in many areas without a visit to a hospital.

7

Our Products

Overview

Through our operating subsidiary Bohai, we obtained Drug Approval Numbers for 29 varieties of traditional Chinese herbal medicines in 2004 and an additional 14 varieties in December 2010 through a product acquisition and currently produce 15 TCM pharmaceutical products. Through our Yantai Tianzheng operating subsidiary, we hold 5 additional varieties of traditional Chinese herbal medicines, of which we currently produce four. Of our 19 products in production, 12 are prescription drugs and 7 are OTC products. All of our products are derived from herbal and organic sources.

The following is a list of the approved pharmaceutical products that we are producing with their intended uses:

Lung Nourishing Syrup. Lung Nourishing Syrup is designed to moisten the lung and relieve coughs and can be used to treat weak lung and chest tightness, poor chronic cough, shortness of spontaneous breath and chronic bronchitis.

Tongbi Capsules. This product is designed to promote blood circulation and relieve swelling and pain, and can be used to treat cold resistance, liver and kidney deficiency, arthralgia syndrome and rheumatoid arthritis.

Tongbi Tablets. Tongbi Tablets are designed to regulate and fortify the blood promote blood circulation and relieve swelling pain and can be used to treat alpine resistance, liver and kidney deficiency, including rheumatoid arthritis.

Shangtongning Tablets. This product is designed to alleviate pain and can be used to treat bruises.

Zhuangyuan shenhailong Medicinal Wine. This liquid product is designed to promote kidney function and can be used to treat the weakness waist and knee fatigue, insomnia and forgetfulness.

Danqi Tablet. This product is designed to improve blood circulation and can be used to treat blood stasis, cardio-thoracic pain, dizziness and headache, and menstrual pain.

Fukangning Tablet. This product is designed to improve blood circulation and can be used to treat blood stasis, cardio-thoracic pain, dizziness, headache and menstrual pain.

Bazhen Yimu Cream. This product is designed for menstruation conditioning and can be used to treat dizziness, palpitation, fatigue, weakness and other menstrual symptoms and can also be used to ease menstrual flow.

Huoxue Shujin Ting. This product is designed to promote blood circulation and relieve blood congestion, and can be used to treat pain in the waist and leg, numbness in the feet and hands and arthritis.

Anti-flu Granules. This product is designed to detoxify the body, and can be used to treat cold caused by exogenous wind-heat with symptoms such as fever, headache, stuffy nose, sneezing, pharyngodynia, generalized weakness and soreness.

Compound Manshanhong Syrup. This product is designed to relieve cough due to throat irritation and to prevent asthma symptoms.

Sanqi Shang Tablets. This product is designed to promote blood circulation and relieve blood congestion, numbness, pain or bruises in the body due to arthritis, acute or chronic sprain or neuralgia.

Stomach Nourishing Tablets. This product is designed to relieve heartburn, sour stomach, acid indigestion and stomach upset caused by chronic superficial gastritis.

8

Yangxue Anshen Tablets. This product is designed to improve blood circulation and to treat dizziness, palpitation, fatigue, weakness and other menstrual symptoms.

Shujin Huoxue Tablets. This product is designed to promote blood circulation and relieve blood congestion, and can be used to treat symptoms related to back pain, muscle paralysis, muscle spasm and acute or chronic sprain.

Fangfengtongsheng Granule. This product is used to treat fever, headache, constipation, measles and eczema.

Zhengxintai Capsule. This product is used to improve kidney function and treat coronary artery disease and angina.

Tongmai Granule. This product is used to treat ischemic heart and cerebrovascular diseases, arteriosclerosis and cerebral thrombosis

Bezoar Antipyrotic Tablet. This product is used to heat detoxificationeliminate heat from the body, swelling and pain.

Of our 19 products currently in production, 12 (Tongbi Tablets, Tongbi Capsules, Shangtongning Tablets, Danqi Tablets, Huoxue Shunjin Ting, Compound Manshanhong Syrup, Sanqi Shang Tablets, Shujin Huoxue Tablets, Tongmai Granule, Fangfengtongsheng Granule and Zhengxintai Capsule) are available only through prescription.

In addition to the 19 medicines currently in production, we hold the rights to produce 29 other herb-based pharmaceutical formulations. We anticipate that we will commence the manufacturing and distribution for these additional products if and when appropriate business conditions develop.

Product Types

Bohai has five production lines for the manufacturing of medicines in five forms, including tablets, granules, capsules, syrup, and medicinal wine. Our current production capacity is approximately:

|

|

·

|

1.35 billion tablets and 370 million capsules;

|

|

|

·

|

30 million bags granules;

|

|

|

·

|

20 million bottles/units of concentrated decoctions;

|

|

|

·

|

15 million bottles/units of syrup;

|

|

|

·

|

1 million bottles/units of tinctures; and

|

|

|

·

|

1 million bottles/units medical wine.

|

We believe that during the fiscal year ended June 30, 2011, on average, we operated at approximately 50% of our production capacity and we believe we are currently operating at approximately 60% of capacity. Yantai Tianzheng has annual production capacity of 400 million tablets, 300 million capsules and 250 million bags of granules respectively and operated on average at 35% of its production capacity for the period ended June 30, 2011

One of our pharmaceutical products has been granted “protected” status by the PRC government, a marketplace classification used by the government to regulate both production and distribution of traditional and herbal medicines in addition to the product formula right itself. These “protected” medicines are not patented in the traditional commercial sense but are essentially proprietary. The protection refers, in part, to standardizations of formulae which require that medicines of the same name have the same type and proportion of ingredients. The “protected” designation grants us exclusive manufacturing and distribution rights within China over certain protected products or with up to six manufacturers in other cases.

9

We have the exclusive rights to manufacture Tongbi Capsules and we share manufacturing rights with one or more manufacturers for Shangtongning Tablets and Anti-flu Granules. The exclusive rights usually have a term of seven years and can be extended for another seven year period after the initial seven year period elapses. The protection periods for both Tongbi Capsules and Shangtongning Tablets expired in September 2009 and we have filed an application for extending the protection period on March 12, 2009 for Tongbi Capsules. SFDA approved our request to extend the protection period for Tongbi Capsules to September 13, 2016. We have decided not to submit extension application of Shangtongning Tablets, because the SFDA shall not approve Certificate of Protection for Shangtongning Tablets or any other products that are currently produced by more than three manufacturers in China according to applicable Chinese SFDA regulations. The shared manufacturing rights for Anti-flu Granules expire on July 9, 2012.

During fiscal 2011, we expect to increase marketing and advertising of Tongbi Capsules and Tablets, which are formulated to treat various forms of arthritis. Sales of our Tongbi medicines are expected to grow in fiscal 2011 due to its protective status and strong demands of drug consumption resulting from health insurance reform in China. In addition to the Tongbi medicines and the Lung Nourishing Syrup, other substantial contributors to our revenues include its Shangtongning Tablets which are also expected to grow in fiscal 2011 due to strong demands of drug consumption resulting from health insurance reform in China and our marketing efforts. Sales of our OTC product Bazhen Yimu Cream, used to strengthen the immune system, the enhancement of physical strength and conditioning, are also projected to grow in fiscal 2011 due to strong demands of drug consumption resulting from health insurance reform in China. As our Tongbi Capsule has been included in the EDL for Shangdong Province, we will focus our marketing efforts in the rural hospitals in Shandong during fiscal 2012.

We will continue to promote four products being sold by Yantai Tianzheng under its current marketing strategy combined with our existing national sales efforts. In particular, we expect that sales from Yantai Tianzheng’s top two products (Fangfengtongsheng Granule and Zhengxintai Capsule) will continue to grow in 2012 due to their exclusive status and/or NDRL status.

We price our medicines well under government-mandated caps and at a premium to most competitors because we use high quality raw materials and rely on strict quality control and management to produce high quality finished products. We therefore believe, subject to applicable clinical analysis, that the purity, potency and effectiveness of our ingredients are superior to similar products in the Chinese marketplace. As Chinese pharmaceutical regulatory authorities continue to tighten drug regulations to improve Chinese drug quality and safety standards, future entry into the pharmaceutical industry has become an increasing challenge.

Overview of the Chinese Market

The People’s Republic of China is undergoing the world’s most important and powerful economic transformation. This transformation includes the confluence of its ancient culture with modern trends in business, technology and finance. As a result, Chinese operating companies are capitalizing on unmatched growth opportunities in this evolving and growing marketplace. Although average income is approximately one-tenth that of developed western nations, business growth and market reform-driven policies have given the country’s 1.3 billion citizens more purchasing power than ever.

According to a report published in Newsweek, total consumer spending in China reached $1.7 trillion in 2007, compared with $12 trillion in the U.S. In its China Consumer Survey published in January 2010, Credit Suisse found that household income in China of the bottom 20% of those surveyed rose by 50% since 2004, while the top 10% had grown 255% to around RMB 34,000 per month. Credit Suisse expects China’s share of global consumption to increase from 5.2% at US$1.72 trillion in 2009 to 23.1% at US$15.94 trillion in 2020, overtaking the U.S. as the largest consumer market in the world. Further, research on Chinese consumers by management consulting firm McKinsey classifies two million households out of a population of 1.3 billion as “wealthy,” based on fairly modest annual earnings of more than $30,000. An enormous middle class is rising, however, numbering some 70 million urban households, but these still earn $5,000-$10,000 a year. China’s National Bureau of Statistics, based on a random survey of 65,000 urban households in China, found that the average (annual) disposable income of urban residents in the first half of 2009 was U.S. $1,300, an increase of 9.8% compared to the same period last year. When price factors are deducted, this is equivalent to a real increase of 11.2%. The average consumption expenditure amount of urban residents in the first half of 2009 was U.S. $876, an increase of 8.9% compared to the same period last year. When price factors are deducted, this is equal to a real increase of 10.3%.

10

TCM Industry Drivers

We believe that demographic, governmental and related factors in the China will be favorable to growth and expansion of our business.

Growing Prosperity of the Chinese People. The increased spending power of China’s population continues to be reflected in the increased consumption of health products and medical services between 2007 and 2010. According to Euromonitor data, spending by Chinese people on these goods and services will increase from $100 billion in 2007 to $145 billion in 2010. According to the Southern Medicine Economic Institute of the SFDA, sales of TCM increased 20% in 2010 as compared to 2009 in selected hospitals in the cities of Beijing, Guangzhou, Nanjing, Chongqing, Chengdu, Xi'an, Harbin, Shenyang, and Zhengzhou. Overall sales of TCM in such hospitals increased at an annual rate of more than 20% during the past three years.

Population and Aging

|

|

·

|

The total population of China was 1.34 billion at the end of 2010, according to official government estimates.

|

|

|

·

|

Due to improved healthcare, the elderly population of China is growing.

|

|

|

·

|

The health/medical costs associated with care for elderly in China are approximately five (5x) times that of younger people.

|

|

|

·

|

China had 170 million elderly people in 2007 but will have an expected 230 million elderly by 2015 according to “Consumer Lifestyles in China: Consumer Trends, China’s Grey Population,” by Euromonitor, 2009.

|

|

|

·

|

The proportion of the China’s population aged 65 and over will rise from just 10% of the overall population in 1995 to 22% by 2030, according to the World Bank.

|

|

|

·

|

From 1995 to 2030 it is estimated that the ratio of working-age people to pensioners will decrease from 9.7:1 to 4.2:1. China’s national estimates vary slightly from World Bank figures, but still show in increase in the proportion of the population over 65 years from 7% in 2000 to 9.4% in 2007, according to China Country Profile 2009, The Economist Intelligence Unit Ltd.

|

Government Policies in Health Care and TCM. In April of 2009 the PRC government implemented a new national medical and health plan. Among other features, this new plan extended national medical insurance coverage to China’s rural areas, where the bulk of the population resides. This expanded coverage will eventually encompass virtually all of China’s 1.3 billion citizens, greatly expanding the market for TCM pharmaceuticals, as well as other health care products and services. This has led to massive potential for increased sales growth for Bohai and other providers of TCM pharmaceutical products.

According to Espicom Business Intelligence, by 2011, the PRC government’s health care investment will rise to $125 billion, compared with $96 billion for 2008. Direct health care subsidies of urban and rural residents will amount to $57 billion. China’s health care investment is expected to witness a growth of 19.7% and the overall growth rate will reach more than 25%.

Government Support of Traditional Chinese Medicine. Among its public health initiatives, the Chinese government officially supports use of TCM to enhance wellness and to treat chronic and acute diseases. The government has also commenced a program to evaluate TCM and herbal-based pharmaceuticals for coverage and reimbursement under national medical insurance. In 2002, TCM was declared a “national strategic industry” in the government’s “Development Outline of Traditional Chinese Medicine Modernization (2002 – 2010).”

11

Decreased Competition. According to the Information Office of the State Council of the PRC, prior to 2009, there were approximately 6,000 Chinese pharmaceutical manufacturers. That number is being significantly reduced through both marketplace attrition and direct government involvement, decreasing competition and increasing potential sales opportunities for the surviving companies. Other companies are expected to fail through lack of size and innovative and aggressive management. According to a 2009 report published by KMPG, of the approximately 4,500 pharmaceutical companies in China, the majority are small players with limited local market reach, and rapid consolidation between medium and large players in the sector is anticipated since the Chinese government has been encouraging industry consolidation with an effort to improve the Good Manufacturing Practice (GMP) standard, enforce GMP certification and to better control the pricing of drugs..

Growth Strategy

Our strategic initiatives for the foreseeable future are designed to aggressively capitalize on the health and wellness needs of increasingly wealthy and empowered consumer class in China. In particular, we are seeking to capitalize on the government policies that extended medical insurance in 2009 to hundreds of millions of Chinese citizens living in rural areas, representing a vast untapped market of potential consumers who previously lacked access to national medical insurance. As part of its reforms to expand and improve public health and medical care, the PRC government is promoting the use of herbal-based TCM and expanding insurance coverage to 100% of an increasing number of medicines.

Our strategic initiatives include the following:

Grow Hospital Presence. We have targeted over 600 hospitals in 100 locations throughout China for direct marketing of Bohai products. As part of this initiative, our sales team will expand its marketing activities to educate hospital personnel about our product lines and train hospital employees in the preventative and curative qualities of these products. The initial focus will capitalize on the best known and most popular of our products, such as Tongbi capsules and Shangtongning tablets, using these as door-openers for our other medicines

The average marketing cost to “open” each hospital to our products is $1,500. For our base Bohai business, we are currently targeting the following provinces and the number of hospitals in such provinces indicted below:

|

Cities

|

Number of Hospitals

|

|

|

Zhejiang

|

50

|

|

|

Jiangsu

|

40

|

|

|

Anhui

|

30

|

|

|

Shandong

|

300

|

|

|

Sichuan

|

50

|

|

|

Hunan

|

40

|

|

|

Henan

|

40

|

|

|

Yunnan

|

20

|

|

|

Fujian

|

40

|

|

|

Shanghai

|

40

|

|

|

Hubei

|

|

30

|

Build Awareness of the Lung Nourishing Syrup. We allocated a significant portion of the proceeds from our January 2010 private placement for brand-building and continue to dedicate resources to these efforts. We will primarily target consumers through television and print advertising to expand awareness of the uses and effectiveness of our Lung Nourishing Syrup. The advertising will incorporate targeting smokers and workers with occupational diseases as well as city dwellers exposed to smog. It is expected that the consumer television advertising program will initially be focused in the following areas:

12

|

TV Station Location

|

|

Shandong

|

|

Anhui

|

|

Hubei

|

|

Sichuan

|

|

Chongqing

|

|

Shanxi

|

|

Jiangsu

|

|

Liaoning

|

We spent approximately $15 million in advertising and promotion expense in fiscal year 2011 as compared to approximately $13 million in advertising and promotion expense in fiscal year 2010. As a result of our efforts in fiscal year 2011, sales from Lung Nourishing Syrup increased by 33% compared to last fiscal year. By the end of our fiscal 2011, we added more than 200 level 2 hospitals and more than 10 new drug store chains to our national network of retail locations in China currently selling our Lung Nourishing Syrup. As a result, we now sell Lung Nourishing Syrup in more than 1,600 level 2 hospitals and more than 36 drug store chains across China.

Expand to Rural Areas. We expect to execute a comprehensive marketing campaign targeting 100 rural counties as a result of the national government’s emphasis on expansion of healthcare and health insurance into the country’s rural areas. We plan on starting its rural marketing in Shandong, Anhui, Liaoning and Hubei. Our sales team will market its products to pharmacies, hospitals, physicians, herbal medicine experts, media outlets and other opinion leaders in these rural areas. The main purpose is to be listed in the New Rural Cooperative Medical Directory which is farmer-friendly and assists these rural dwellers with reimbursement of medical expenses.

Generally, the marketing cost of this professional relationship-building with each rural county is $3,000. Total estimated marketing costs in the New Rural Cooperative Medical Directory could be in excess of $1,000,000. We plan to continue our efforts in hiring additional sale people under our current strategy as national health reform continue to focus in the rural areas especially in Shandong province. All of these sales and marketing initiatives will involve both OTC and prescribed products.

Develop Our Product Lines and Product Awareness. Brand awareness marketing will include the promotion and introduction to new markets of the current popular Bohai products such as Tongbi Tablets, Lung Nourishing Syrup, Fangfengtongsheng Granule, and Zhengxintai Capsule. As part of our increase in sales and marketing staff, we plan to have special trainers and presenters who can conduct promotional events and seminars to increase awareness of our products.

Seek Acquisitions of Complimentary Companies or Assets. We believe that there may be TCM companies (such as Yantai Tianzheng) or assets in China that would be complimentary with our current product offerings and which could fit well with our sales and marketing platform. We may seek to acquire such assets or other companies as a means to grow our revenue and profitability.

Competitive Advantages

We believe there are several key factors that will continue to differentiate us from our competition in the PRC:

13

|

|

·

|

“Protected” Status of Key Bohai Product. One of our lead products (Tongbi Capsules) currently enjoys exclusive protected status by the PRC government. We have submitted an application for extending the protection period for this product. This status regulates competition, granting us exclusive or near-exclusive rights to manufacture and sell the protected products. SFDA approved our request to extend the protection period for Tongbi Capsules to September 13, 2016. We submitted to the SFDA our request for renewal of the protected status for Zhengxintai Capsule on February 26, 2010, and such request is currently being reviewed. We are in the process of applying for protected status for Fangfengtongsheng Granule, and such application was received by SFDA on June 30, 2010.

|

|

|

·

|

Patent Granted for Lead Product. We have received a patent in the PRC for our Lung Nourishing Syrup with its production method for the treatment of Lung Qi Deficiency Cough and Chronic Bronchitis. The patent was awarded for a period of 20 years starting from the day of its application on September 12, 2007. For these reasons, we believe Lung Nourishing Syrup contains a novel formulation for the treatment of asthma and other common respiratory ailments with an emphasis on the improvement of overall lung function and health. We believe this represents an exceptional market opportunity.

|

|

|

·

|

Insurance Coverage for Lead Bohai Products. Five of our lead products, Lung Nourishing Syrup, Tongbi Capsules and Tablets, Fangfengtongsheng Granule and Zhengxintai Capsule, are listed in the Catalogue Eligible for Medicine Reimbursement as of November 30, 2009. This means that these medicines are eligible for reimbursement under the national health insurance. We will seek to have additional (approximately 2-3) products listed in the catalogue.

|

|

|

·

|

Low Development Costs. We enjoy relatively low research and development (including acquisition) costs for our TCM products compared with western pharmaceuticals as our products are derived from recognized formulas.

|

|

|

·

|

Effective Sales Force. We maintain a highly trained sales force of approximately 354 people as of the date of this Annual Report.

|

The principal raw materials used for the production of our distributed products are honey, laiyang pear paste, Sichuan fritillaria, pangolin, and Chinese angelica. Raw materials, as well as packaging materials, are sourced from various independent suppliers in the PRC. We have no long term agreements with our suppliers, and purchase raw materials on a purchase order basis. We try to maintain relationships with at least two vendors for each major raw material in order to ensure a reliable supply of raw materials at reasonable prices. We believe there is ample supply in the market for the foreseeable future of the ingredients for our products.

Our principal suppliers include Anhui Dechang Pharmaceutical Tablet Co., Ltd., Shandong Yantai Medicine Purchasing and Supply Station, Zibo Taibao Forgery-proof Product Co., Ltd., and Zhejiang Yuhuan Kangning Medicine Packaging CO., Ltd. In the fiscal year ended June 30, 2011, one supplier accounted for over 10% of our purchases of raw materials, although currently no single supplier accounts for over15 % of our purchases of raw materials. Approximately 34% of the raw material is purchased from Anhui Dechang Pharmaceutical Tablet Co., Ltd., Shandong Yantai Medicine Purchasing and Supply Station and Shandong Cangli Medicine Co., Ltd.

Yantai Tianzheng’s major suppliers are Anhui Dechange Pharmaceutical Tablet Co., Ltd., Shandong Yantai Medical Materials Purchasing and Supply Station and Anguo Jinkangdi Medicine Co., Ltd. Approximately 35% of the raw material used by Yantai Tianzheng was purchased from Anhui Dechang Pharmaceutical.

Research and Development

We currently have limited resources to devote to and limited capabilities to conduct the development of new products and as such research and development activities are not presently material to our business. We have only one full-time employee who is engaged in research and development, so we are mainly dependent on a third-party, Yantai Tianzheng Medicine Research and Development Co., Ltd., to perform research and development for us. We currently have two products, namely Forsythia Capsule and Fern Injection, under research and development in association with Yantai Tianzheng Medicine Research and Development Co., Ltd.

14

We, like other TCM manufacturers, enjoy relatively low research and development expenses as most TCM medicines are based on standardized formulas. In 2008, SFDA promulgated a notice of registration of Chinese traditional medicine providing that TCM composed of classic prescriptions will be exempted from pharmacological and toxicological tests and studies. The notice defined classic prescription and classic TCM formulas as those herbal remedies recorded in ancient Chinese medicine books from Qing Dynasty or earlier which are currently widely used. According to such notice, the production and manufacturing of TCM products are subject to non-clinical safety studies only and exempted from pharmacological and toxicological tests and studies. Thus, TCM products are entitled to obtain faster SFDA approval. As such, we enjoy relatively low research and development expenses because most of our products are based on classic TCM formulas that are covered by this notice.

The research and development process includes toxicological tests, pharmalogical and qualitative research, preparation for production and other miscellaneous costs. We intend to introduce one new product by 2014 which is currently identified as a Shujin Pain Relief soft capsule. The total cost to develop this product is not expected to exceed $1,500,000. We may also seek to acquire new products through acquisitions of other TCM companies in the future.

We received a two-year government research grant totaling $144,000 (RMB 950,000) to fund the research and development of Menstrual Relief Tablet, a traditional Chinese medicine (TCM) for dysmenorrhea, or menstrual pain, currently in early-stage clinical development. The grant includes $91,000 (RMB 600,000) from the Ministry of Science and Technology of the People's Republic of China and $53,000 (RMB 350,000) from the Yantai local government. The grants are being given to companies to encourage the modernization of TCM drug-development in a manner more aligned with the typical development pathway of Western medicines.

Manufacturing

Although TCM is thousands of years old, we believe that our product manufacturing and procedures are the most modern and up-to-date available. We employ rigorous standards for product quality control and safety. The manufacturing facility owned by us is conducted in the city of Yantai in Shandong Province in a state-of-the-art 18,000 square-meter facility that meets or exceeds the latest Good Manufacturing and Quality Management Practice standards (referred to in China as “GMP”).

Yantai Tianzheng owns a manufacturing facility with a total area of 10,908.83 square meters (approximately 117,000 square feet) that also meets or exceeds the latest GMP.

GMP standards are the government’s benchmark for pharmaceutical manufacturers in China and must be met for the manufacturer to be eligible to market domestically or enter world markets. On March 31, 2009, we completed a GMP review which included examination of 225 items including development technology, production, quality assurance, quality control, material handling and engineering. As a result of that review, we were been re-certified for a new five-year period.

Through stringent application of GMP standards, the PRC government has reduced the number of marginal medicine manufacturers by one-third, from 6,000 to 4,000. The new GMP standards established in 2011 could potentially eliminated additional 500 medicine manufacturers. It is expected that TCM and pharmaceutical companies such as ours that have received full GMP approval by the government will enjoy the competitive benefits of their strict adherence to quality control, safety, health and manufacturing standards.

Our advanced and mechanized facilities utilize controlled, clean-room procedures with sophisticated water filtration and materials processing systems. The manufacturing staff consists of approximately 343 production employees and approximately 25 quality control inspectors as of June 30, 2011. We believe that we operated at approximately 60% of our manufacturing capacity during as of June 30, 2011.

In February 2010, we acquired land use right for a parcel of land totaling 333,335 square meters in Yantai City which we may use to expand our manufacturing capability.

15

Marketing, Sales and Distribution

Bohai’s products are sold either by prescription through hospitals or Over the Counter (OTC) through hospitals, local pharmacies and retail drug store chains. Sales and distribution are managed and executed by approximately 354 sales representatives located in 21 offices throughout China as of June 30, 2011. These employees are trained in all details of each product and are encouraged to develop strong ties with physicians, hospitals and pharmacies in their local areas.

Our distribution and marketing initiatives for the next several years will be focused on achieving the following goals:

Expand hospital presence. We intend to further develop business in over 600 hospitals in provinces we already serve including Shandong, Zhejiang, Jiangsu, Anhui, Sichuan, Hubei and other provinces. We believe that we will generate additional revenue from the newly developed hospitals in those provinces. During the fiscal year ended June 30, 2011, we added more than 200 level 2 hospitals and more than 10 new drug store chains to its national network of retail locations in China currently selling our Lung Nourishing Syrup. As a result, we now sells Lung Nourishing Syrup in approximately 1,600 level 2 hospitals and 36 drug store chains across China. Currently, we sell our products to more than 1,680 hospitals and medical centers in more than 20 provinces and special districts in China.

Expand distribution to the rural market. We believe that the Chinese government’s expansion in 2009 of national medical insurance reimbursement coverage to the rural population provides us with new and largely untapped markets. Some of our products, namely Lung Nourishing Syrup, Tongbi Capsules and Tongbi Tablets, have been listed in government’s New National Medical Insurance Catalogue in Shandong and Anhui Province as of November 30, 2009, and we expect to gain a competitive advantage in these newly accessible rural markets. With the addition of more than 200 level 2 hospitals and 10 drug store chains to our national distribution network during the fiscal year ended June 30, 2011, we expect considerable growth in our sales in the rural market.

Expand prescription medicine sales organization. A key element of our growth strategy is increased outreach to physicians. These outreach programs will focus on the eight current pharmaceutical products of ours that are available by prescription only and will typically take place at state-run hospitals where virtually all Chinese citizens obtain their medical care. Our educational training programs will be designed to inform doctors of the range of our pharmaceutical products including diseases or health/wellness concerns targeted and proper usage of the medicines.

Expand OTC team to drive market share. Our management intends to accelerate and expand sales of our OTC medicines through promotion and advertising targeting consumers. The marketing programs will principally utilize television, print advertising and news releases.

Acquisition of Yantai Tianzheng. Part of our ongoing marketing strategy is to consolidate Yantai Tianzheng’s sales team and distribution network with our own. Together, we sell 19 products to more than 2,700 hospitals and medical centers in China by working with more than 100 distributors and 300 plus sale people. We believe that the consolidation process for the two companies will take approximately 1 to 2 years to complete.

Competition

China’s domestic pharmaceutical industry is highly competitive, with hundreds of companies vying to reach consumers through more than 100,000 pharmacies. In some categories in which we compete there are many other companies offering the same competitive products. The market continues to attract new entrants because the per capita medicine consumption in China is still low, compared to developed countries, and that shows promise for substantial growth.

Competitive factors primarily include price and quality. We believe that we are able to effectively compete in our market segment in China based upon the quality of our product, given our new GMP certified manufacturing facility and our reputation in the market place.

16

Many of our current and potential competitors have significantly longer operating histories and significantly greater managerial, financial, marketing, technical and other competitive resources, as well as greater name recognition, than we do. These competitors may be able to respond more quickly to new or changing opportunities and customer requirements and may be able to undertake more extensive promotional activities, offer more attractive terms to customers or adopt more aggressive pricing policies. We cannot assure you that we will be able to compete effectively with current or future competitors or that the competitive pressures we face will not harm our business.

Intellectual Property

We market our products under the trademark “Xian Ge” which is registered with the PRC Trademark Bureau under the State Administration for Industry and Commerce. Currently, another company is licensed to utilize our registered trademark “Xian Ge”. We have also received a patent in the PRC for our Lung Nourishing Syrup with its production method for the treatment of Lung Qi Deficiency Cough and Chronic Bronchitis.

Government Regulation

We are subject to many general regulations governing business entities and their behavior in China and in any other jurisdiction in which we have operations. In particular, we are subject to laws and regulations covering food, dietary supplements and pharmaceutical products. Such regulations typically deal with licensing, approvals and permits. Any change in product licensing may make our products more or less available on the market. Such changes may have a positive or negative impact on the sale of our products and may directly impact the associated costs in compliance and our operational and financial viability.

Our only sales market is presently in China. We are subject to the Pharmaceutical Administrative Law, which governs the licensing, manufacturing, marketing and distribution of pharmaceutical products in China and sets penalties for violations of the law. We are also subject to the Food Sanitation Law, which provides for the food sanitation standards to be followed.

Under SFDA guidelines for licensing of pharmaceutical products, all pharmaceutical manufacturers must obtain and maintain GMP Certificate. We hold a GMP Certificate (No. Lu K0587), which was issued by Shandong Branch of SFDA on June 18, 2009 and a GMP Certificate (No. Lu L0763), which was issued by Shandong Branch of SFDA on November 15, 2010 for Yantai Tianzheng. Because our manufacturing facility has obtained the National GMP Certificate, we are authorized to produce products in seven modes which are tablets, capsules, granules, syrup, concentrated decoctions, tincture and medical wine. Such certificate expires on June 14, 2014 for us and on November 14, 2014 for Yantai Tianzheng and we will seek to renew the certificate before its expiration date.