Attached files

| file | filename |

|---|---|

| EX-10.5 - Panache Beverage, Inc. | ex10_5.htm |

| EX-10.3 - Panache Beverage, Inc. | ex10_3.htm |

| EX-10.4 - Panache Beverage, Inc. | ex10_4.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K/A

Amendment No 1

CURRENT REPORT

Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934

Date

of Report (Date of earliest event reported): August 19, 2011

PANACHE BEVERAGE INC.

(F/K/A BMX DEVELOMENT CORP.)

(Exact name of registrant as specified in its charter)

| Florida | 000-52670 | 20-2089854 |

(State or other jurisdiction of incorporation) |

(Commission File Number) |

(IRS Employer Identification No.) |

40 W. 23rd Street, 2nd Floor, New York, NY 10001

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (704) 904-2390

(Former name or former address, if changed since last report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

[ ] Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425).

[ ] Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12).

[ ] Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)).

[ ] Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)).

| (1) |

PANACHE BEVERAGE INC.

(F/K/A BMX DEVELOMENT CORP.)

CURRENT REPORT ON FORM 8-K

| Page |

| Item 2.01 | Completion of Acquisition or Disposition of Assets | 3 |

| Plan of Exchange | 3 | |

| Stock Purchase Agreement | 3 | |

| Description of Panache Beverage Inc. Business | 3 | |

| Risk Factors | 6-8 | |

| Security Ownership of Certain Beneficial Owners and Management | 9 | |

| Directors and Executive Officers | 9 | |

| Executive Compensation | 10 | |

| Certain Relationships and Related Transactions | 10 | |

| Description of Securities | 11 | |

| Item 3.02 | Unregistered Sales of Equity Securities | 14 |

| Item 5.01 | Changes in Control of Registrant | 15 |

| Item 5.02 | Departure of Directors or Principal Officers; Election of Diretors; Appointment of Principan Officers | 15 |

| Item 9.01 | Financial Statements and Exhibits | 16 |

| (2) |

This current report on Form 8-K is filed by Panache Beverage Inc., a Florida corporation (the “Registrant” or the “Company”), in connection with the items set forth below.

ITEM 2.01 COMPLETION OF ACQUISITION OR DISPOSITION OF ASSETS

PLAN OF EXCHANGE

On August 19, 2011, a Plan of Exchange (the “POE”) was executed by and among the Registrant, along with Michael J. Bongiovanni (“Mr. Bongiovanni”), an individual shareholder and its President / Chief Executive Officer, Panache LLC (“Panache”), a New York Limited Liability Company, James Dale, an individual member and Manager of Panache, and the individual members of Panache (collectively the “Panache Members”). According to the POE, the capital of the Registrant consists of 200,000,000 authorized shares of Common Stock, par value $0.001, of which 4,914,500 shares are issued and outstanding at the time of signing. The capital of Panache consists of 20 million authorized membership interest units, of which 20 million membership interest units are issued and outstanding.

Under the terms of the POE, the Registrant shall acquire one hundred percent (100%) of the issued and outstanding membership interest units of Panache from the Panache Members in exchange for a new issuance 17,440,000 shares of common stock of the Registrant to the Panache Members. Panache is currently 100% owned by Panache Members.

Pursuant to and at the closing of the POE, which occurred on August 19, 2011, the Registrant authorized Guardian Registrar & Transfer, Inc., its transfer agent, to issue to the Panache Members, 17,440,000 shares of common stock of Registrant pursuant to Rule 144 under the Securities Act of 1933, as amended, equivalent to approximately 90% of Registrant's then outstanding common stock, in exchange for all of the membership interest units of Panache owned by the Panache Members. Upon completion of the physical exchange of the share certificates, Panache became a wholly-owned subsidiary of the Registrant.

In addition, the POE contemplated that the exchange transaction will not immediately close but shall be conditioned upon (1) the Registrant eliminating all known or potential liabilities of the Registrant as of the closing date, including, but not limited to, any notes payable, loans payable, accounts payable and accrued expenses, accrued payroll and compensation, as well as any liabilities shown on its quarterly report for the period ended June 30, 2011 (FORM 10Q) filed with the Securities and Exchange Commission prior to the Closing and an acknowledgement from Mr. Bongiovanni and the Shareholders of the Registrant that they will be fully responsible for any unknown or undisclosed liabilities up until transfer of control under this Plan of Exchange; (2) the issuance of 17,440,000 new shares of Common Stock of the Registrant to the Panache Members, which should take no longer than 5 business days, (3) the resignation of Mr. Bongiovanni from the board of directors and as President and Chief Executive Officer of the Registrant and appointment of his successor(s) as designated by Panache and/or the Panache Members. All of these conditions to closing have been met, and Registrant, Panache, the Panache Members and the Majority Shareholders of Registrant declared the exchange transaction consummated on August 19, 2011.

The foregoing description of the terms of the POE is qualified in its entirety by reference to the provisions of the agreement included in the report, initially filed on August 24, 2011, which is incorporated by reference herein.

STOCK PURCHASE AGREEMENT

On August 19, 2011, James Dale (“Purchaser”), an individual resident of the State of New York entered into a Share Purchase Agreement (“Purchase Agreement”) with Mr. Bongiovanni, pursuant to which, Mr. Bongiovanni sold an aggregate of 2,560,000 of the Registrant’s common shares, par value $0.001 (the “Shares”) to the Purchaser, for an aggregate purchase price of $125,000. As a result of the closing of the Purchase Agreement, the Purchaser holds 52.1% of the Registrant’s outstanding capital stock resulting in a change in control of the Registrant.

The foregoing description of the terms of the Purchase Agreement is qualified in its entirety by reference to the provisions of the agreement included in the report, initially filed on August 24, 2011, which is incorporated by reference herein.

DESCRIPTION OF PANACHE BEVERAGE INC. BUSINESS

The Company was incorporated in Florida effective December 28, 2004 and provided motor cycle repair services to customers located in and around the Charlotte, North Carolina area. Subsequent to the POE, the Company has continued operations of Panache, an alcoholic beverage company specializing in the development and global sales and marketing of spirits brands, and no longer be engaged in the business of motor cycle repair services.

Panache was formed in November 2004 by James Dale as the import company of record for the premium vodka, 42 BELOW NZ. At that time, 42 BELOW was a publically traded company but lack of traction in the most important liquor market in the world, including the United States. Panache provided the marketing solution for 42 BELOW, and it became a brand available in 19 strategically selected states and was over-performing in top tier image accounts a year later. By mid-2005 42 BELOW was a major player in the business and was being noticed in the United States by major suppliers.

After noticing that 42 BELOW has replaced Grey Goose in numerous key accounts, Bacardi added 42 BELOW to a list of top threats to Grey Goose in the US. Shortly thereafter 42 BELOW was formally approached for global acquisition. At this stage Panache was responsible for over 50% of the total annual cases sold globally and was among the key driving factors in the success of the brand. These agreements were purchased as part of the settlement and purchase of the 42 BELOW Public Company in December 2006.

During this time Panache was developing its current pipeline brands Alchemia Vodka and Alibi Bourbon with an eye toward developing a value brand, which became Wodka.

Today, Panache has developed a unique set of wholesale and retail relationships as well as sales and marketing infrastructure and proprietary partnerships enabling it develop, roll out and exit its brands.

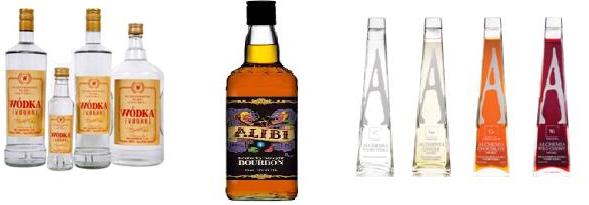

Our Brands

· Wódka (Vodka), produced by POLMOS Białystok, Poland

· Alchemia (Vodka) produced by POLMOS Białystok, Poland

· Alibi (Bourbon), distilled in Kentucky, USA

| (3) |

Our customers

The Company’s customer base will be developed through extending the marketing and sales strategy implemented successfully in New York State - to other key regions throughout the US. Unlike traditional growth plans, the Company must maintain its current marketing philosophy and avoid scaling the business through traditional block and tackle methods employed by the major spirits companies.

Competition

Industry and competitive information in this section and elsewhere in this report was compiled from various industry sources. While the Company believes that these sources are reliable, we cannot guarantee the accuracy of data and estimates obtained from these sources.

2010 U.S. Alcohol Industry Overview

The alcohol industry in the United States is highly competitive. There are 30,000 stores in the US selling beer, wine, and liquor with combined annual revenue of about $40 billion. No major companies dominate; individual states have different laws regulating liquor stores, complicating the ability to form national chains. The industry is highly fragmented: the top 50 companies account for 20 percent of sales.

Despite larger serving sizes, over the past decade the market shares of beer and wine have decreased, while the share of distilled spirits or hard liquor has risen significantly. Between 1995 and 2006, the market shares of both beer and wine decreased by 5 percent (from 60 to 55 percent for beer and from 12 to 7 percent for wine), while distilled spirits made up the difference, increasing by 10 percent.

Our Competitive Position

The Company portfolio of distilled spirits competes with numerous above premium, premium, low-calorie, popular priced, non-alcoholic, and imported brands. These competing brands are produced by international, national, regional and local brewers. The Company holds a ‘build and exit’ business mentality – its expertise lies in the strategic development and early growth of its brands establishing the Company’s assets as viable acquisition candidates for the major global spirits companies including Diageo, Bacardi, Future Brands, Pernod Ricard and Moet Hennessey. The Company’s goal is to sell brands individually as they mature while continuing to pipeline new brands in to the Company’s portfolio.

The Company’s products also compete with other alcohol beverages, including beer and wine, and thus their competitive position is affected by consumer preferences between and among these other categories.

Growth Strategy

Overview/General Strategy

Maintain and Disseminate Core Marketing Principles

Avoid becoming a traditional brand at all costs – as we grow, maintain the core principles that have made Wodka a real consumer brand.

Be a Movement

- Personalize and localize the brand – must have a human face

- Stand for something that people can get behind

- Champion the common man

- Create an environment where discovery happens

- Influencer the few who influence the rest

- Always utilize the power of the free press

Stay on Message

- The simplicity of our message has been key to our success, ensure we stay on message at all times

- Great Vodka, Priced Right – Premium Vodka without the Premium Price

Remain Aloof

- Develop the brand and its marketing in a vacuum – do not react to outside influences or trends

- Develop the brand and speak about the brand as if we were doing it for fun, not a business

- DO NOT MARKET AT PEOPLE – DO NOT TELL PEOPLE WHAT TO DO OR WHAT TO THINK

Create a Conversation

- Everything we do must be a conversation starter

- Don’t be afraid to make people question what Wodka is doing, confusion is ok as

Always Remember Glee

- Gay yes, but we can’t be afraid to be who we are and be proud of it

- We’re quirky and different – our packaging isn’t fancy and sometime people don’t understand us – that’s what makes us beautiful – sort of like the ugly girl in school

National Marketing Strategies

Focus our national strategies on the channels which are most synonymous with movement marketing to develop affinity and create scalable discovery of the brand at a national level. These three areas will be the overlay to everything Wodka does and will be managed at the national level, ensuring that all local/regional tactics are leveraged up through PR and social media.

Influencer Marketing

- The strategy of focusing on fewer people who, in turn, have influencer over a broader mass audience – rather than focusing directly from the brand to the mass market. Panache has successfully employed this strategy since launch through targeting image accounts on premise (atypical for value vodka), focusing on PR, focusing social media efforts on the industry bloggers rather than consumers, etc.

Social Media

- More and more social media is used by larger companies as an alternative to advertising; these companies are creating programs and measuring social media numerically (how many fans, likes, followers, etc.) which is not necessarily an indication of the success social media is having.

- Wodka is focused on generating true engagement through social media and using that engagement to push out the influencer media strategy. (discuss/reference fledgling Facebook strategy, blogger strategy, influencer strategy, etc.)

- MUST MAINTAIN GRASSROOTS, ORGANIC APPROACH

| (4) |

PR

- Utilize the power of the free media to scale and lend credible endorsement to the brand’s positioning, quality and existence – continue to generate business and trade media while focusing more on consumer media. With additional funding the big focus will be to secure hyper-local media coverage by leveraging the new marketing tactics rolled out regionally.

OOH

- Continue the use of OOH beyond just Van Wagner’s assets – the approach sync’s well with our grassroots approach and philosophy of using the medium beyond traditional awareness/branding and as a hook for social media and pr.

Marketing

Strategy by Region

Overview

Below is a brief outline of the tactical approach we’d employ by focus region – based on what works best for that region and where we believe marketing needs to support sales. All regions will use PR, social media and influencer marketing in addition to what is listed below.

United States – Major States

California

- Localized focus dividing up CA in to 7 regions (SD, OC, LA, Valley, Beaches, SF, East Bay)

- Localized OOH

- Strategic partnerships/endorsements with radio DJs

- Grocery chain support as built in to deals

- Event marketing

Texas

- Refine Wodka message for Texas market – must regionalize the brand to appeal to the Texas mind-set

- OOH in key markets

- Local print

Florida

- Florida broken up in to S. Florida and “Rest of State”

- Focus S. Florida efforts on Miami via event marketing

- Focus ROS on OOH and out of the box regional sponsorships with integrated media attached

- Grocery chain support as built in to deals

NY/NJ

- Continuation of OOH efforts in NY

- Event marketing

United States – Regions

Focus on securing low resource out of the box sponsorship opportunities in key regional, second tier markets. Opportunities must be fully integrated and provide Wodka with the ability to generate scale via PR, social media, etc. Focus markets by region include:

West

- Arizona, Nevada, Colorado

Midwest

- Illinois, Missouri, Ohio

East

- Connecticut, Massachusetts, Maryland, Pennsylvania

Southeast

- Georgia, North Carolina

United States – College Vertical

Wodka is uniquely positioned to succeed in a college vertical because:

- Price point

- Irreverent positioning

- “Permission” to market at an audience major spirits companies shy away (while staying within legal guidelines)

- Relationships and leverage generated from MMG’s position in nightlife

Focus on LDA consumers in high density college markets (where the college is the city) in three major conferences:

- Big 10, SEC, Big 12

Employ a grassroots takeover strategy in these markets through integrating the following tactics:

- Local ambassadors

- Focused sales efforts on and off-premise

- Guerrilla marketing/street teams

- PR and social media

Existing Facilities and Property Owned:

We currently occupy approximately 1,400 square feet of warehouse and administrative space for which we pay $1,000 per month. We feel this is adequate for our present and planned future operations. We do not have a written lease agreement, but rather occupy the space on a month-to-month basis. If we lose the use of our warehouse space, we believe we could replace the property at approximately the same monthly rate.

Intellectual Property:

As of September 21, 2011, we have the following intellectual property rights:

| Wodka Vodka: Serial Number | 77751777 |

| Alchemia Polish Vodka: Serial Number | 85114452 |

| Alchemia Chocolate Infused Vodka: Serial Number | 76673425 |

Alibi Bourbon and Whiskey: Serial Number 85430392

Customers

Panache’s sales do revolve around a few major customers. The following table depicts our 2 major customers and their percentage of current sales for the year 2010.

| Customers | Percentage of Revenues | ||||||

| 1. DOMAINE SELECT WINE ESTATES | 75 | % | |||||

| 2. PURE BEVERAGES PTY LTD | 25 | % | |||||

| Total: | 100 | % | |||||

Regulation

In the U.S., the distilled spirits business is regulated by federal, state, and local governments. These regulations govern many parts of Panache' operations, including marketing and advertising, transportation, distributor relationships, sales, and environmental issues. To operate their facilities, they must obtain and maintain numerous permits, licenses and approvals from various governmental agencies, including the U.S. Treasury Department; Alcohol and Tobacco Tax and Trade Bureau; the U.S. Department of Agriculture; the U.S. Food and Drug Administration; state alcohol regulatory agencies; and state and federal environmental agencies.

Governmental entities also levy taxes and may require bonds to ensure compliance with applicable laws and regulations. U.S. federal excise taxes on alcohol beverages currently approximate $15 per hectoliter. State excise taxes are levied at varying rates with an average rate of approximately $2 per hectoliter in 2010.

Legal Proceedings

The Company is not aware of any significant pending legal proceedings against it.

Employees

| Department | Number of Employees Within Department |

|---|---|

| Finance | 1 |

| Logistics | 1 |

| Sales | 1 |

| Total | 3 |

| (5) |

RISK FACTORS

An investment in our common stock being offered for resale by the selling shareholders is very risky. You should carefully consider the risk factors described below, together with all other information in this report before making an investment decision. Additional risks and uncertainties not presently foreseeable to us may also impair our business operations. If any of the following risks actually occurs, our business, financial condition or operating results could be materially and adversely affected. In such case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business and Industry

Competition in our markets could require us to reduce prices or increase capital and other expenditures or cause us to lose sales volume, any of which could have a material adverse effect on our business and financial results.

In most of our markets, our primary competitors have substantially greater financial, marketing, production and distribution resources than Panache, and are more diverse in terms of their geographies and brand portfolios. In all of the markets in which Panache operates, aggressive marketing strategies by these competitors could adversely affect our financial results. Moreover, each of our major markets is premature.

Our success as an enterprise depends largely on the success of relatively few products in several markets; the failure or weakening of one or more of these products or markets could materially adversely affect our financial results.

Our Wódka brand in the market represented more than half of our sales in 2010. Consequently, any material shift in consumer preferences away from our brands, or from the categories in which they compete, could have a material adverse effect on our business.

We rely on a small number of suppliers to obtain our products. The inability to renew the exclusive contracts with our suppliers could unfavorably affect our ability to continue our business.

Our goal is to sell brands individually as they mature while continuing to pipeline new brands in to our portfolio. Our expertise lies in the strategic development and early growth of our brands establishing our assets as viable acquisition candidates for the major global spirits companies. The inability to obtain new brands or to renew the existing brands before they mature could have a material adverse effect on our business.

Termination of one or more distribution agreements, which could have a material adverse effect on our business.

We distribute products of other distilled spirits companies through various joint ventures, licensing, distribution or other arrangements. The loss of one or more of these arrangements, as a result of industry consolidation or otherwise, could have a material adverse effect on the business and financial results of operations.

Changes in tax, environmental or other regulations or failure to comply with existing licensing, trade and other regulations could have a material adverse effect on our financial condition.

Our business is highly regulated by federal, state, provincial, and local laws and regulations in various countries regarding such matters as licensing requirements, trade and pricing practices, labeling, advertising, promotion and marketing practices, relationships with distributors, environmental matters, smoking bans at on-premise locations, and other matters. These laws and regulations are subject to frequent re-evaluation and political debate. Failure to comply with existing laws and regulations or changes in these laws and regulations or in tax, environmental, excise tax levels imposed or any other laws or regulations could result in the loss, revocation or suspension of our licenses, permits or approvals and could have a material adverse effect on our business, financial condition, and results of operations. Finally, advocates of prohibition and other severe restrictions on the marketing and sales of alcohol are becoming increasingly organized on a global basis, seeking to impose regulations to curtail substantially the consumption of alcohol, including distilled spirits, in developed and developing markets. To the extent such views gain traction in national regulations where we do or plan to do business, they could have a material adverse impact on our business and results of operations.

Our consolidated financial statements are subject to fluctuations in foreign exchange rates, most significantly the Polish Zloty (“PLN”).

Our products are primarily imported from Poland, the fluctuation of exchange rate between PLN and U.S. Dollars ("USD") will affect, perhaps adversely, the cost of goods sold in our financial statements, even if their cost in local currency value has not changed. To the extent that we fail to adequately manage these risks due to exchange rate, including if our hedging arrangements do not effectively or completely hedge changes in foreign currency rates, our results of operations may be materially and adversely impacted.

Our operations face significant exposure to changes in commodity prices, which could materially and adversely affect our operating results.

The supply and price of the raw materials and commodities, such as ryes and water, can be affected by a number of factors beyond our control, including market demand, global geopolitical events, frosts, droughts and other weather conditions, economic factors affecting growth decisions, plant diseases, and theft. To the extent any of the foregoing factors affect the prices of ingredients, our cost of goods sold could be materially and adversely impacted.

The success of our business relies heavily on brand image, reputation, and product quality.

It is important we have the ability to maintain and increase the image and reputation of our existing products. Concerns about product quality, even when unsubstantiated, could be harmful to our image and reputation of our products. Deterioration to our brand equity may have a material effect on our business and financial results.

Changes to the regulation of the distribution systems for our products could adversely impact our business.

In the U.S. market, there is a three-tier distribution system that has historically applied to the distribution of our products. That system is increasingly subject to the legal challenges on the basis that it allegedly interferes with interstate commerce. To the extent that such challenges are successful and require changes to the three-tier system, such changes could have a materially adverse impact on Panache.

Changes in various supply chain standards or agreements could adversely impact our business. Our business includes various joint venture and industry agreements which standardize parts of the supply chain system. Examples include warehousing and customer delivery systems organized under joint venture agreements with our suppliers. Any change in these agreements could have a material adverse impact on our business.

Climate change and water availability may negatively affect our business.

There is concern that a gradual increase in global average temperatures could cause significant changes in weather patterns around the globe and an increase in the frequency and severity of natural disasters. While cooler weather has historically been associated with increased sales of distilled spirits, changing weather patterns could result in decreased agricultural productivity in certain regions which may limit availability or increase the cost of key agricultural commodities, such as ryes and other cereal grains, which are important ingredients for our products. Increased frequency or duration of extreme weather conditions could also impair production capabilities, disrupt our supply chain or impact demand for our products. In addition, public expectations for reductions in greenhouse gas emissions could result in increased energy, transportation and raw material costs and may require us to make additional investments in facilities and equipment. As a result, the effects of climate change could have a long-term, material adverse impact on our business and results of operations. There are also water availability risks. Climate change may cause water scarcity and a deterioration of water quality in areas where we maintain brewing operations. The competition for water among domestic, agricultural and manufacturing users is increasing in some of our brewing communities. Even where water is widely available, water purification and waste treatment infrastructure limitations could increase costs or constrain our operations.

| (6) |

We are highly dependent on independent retailers in the United States to sell our products, with no assurance that these retailers will effectively sell our products.

We sell all of our products in the United States to retail outlets and the regulatory environment of many states makes it very difficult to expand our sales channel. Consequently, if we are not allowed or are unable to replace unproductive or inefficient retailers, our business, financial position, and results of operation may be adversely affected, which could have a material adverse effect on our business and financial results.

We will need to obtain additional debt and equity financing to complete subsequent stages of our business plan, including the funds required to expand our businesses.

We presently have limited operating capital. Current revenue is only sufficient to maintain our presence in the market. To meet future capital requirements necessary for the expansion of our business, we may issue additional securities in the future with rights, terms and preferences designated by our Board of Directors, without a vote of stockholders, which could adversely affect stockholder rights. Additional financing will likely cause dilution to our stockholders and could involve the issuance of securities with rights senior to our currently outstanding shares. There is no assurance that such financing will be sufficient, that the financing will be available on terms acceptable to us and at such times as required, or that we will be able to obtain the additional financing required, if any, for the continued operation and growth of our business. Any inability to raise necessary capital will have a material adverse effect on our ability to implement our business strategy and will have a material adverse effect on our revenues and net income.

We are exposed to risks from legislation requiring companies to evaluate internal control over financial reporting.

Section 404 of the Sarbanes-Oxley Act of 2002 (“Section 404”) required our management to start reporting on the operating effectiveness of our internal control over financial reporting for the years ended December 31, 2010 and 2009. We must continue an ongoing program of system and process evaluation and testing necessary to comply with these requirements. We expect that this program will require us to incur significant expenses and to devote additional resources to Section 404 compliance on an ongoing annual basis. We cannot predict how regulators will react or how the market prices of our securities will be affected in the event that our Chief Executive Officer and Chief Financial Officer determine that our internal control over financial reporting is not effective as defined under Section 404.

Our future success is dependent on our existing key employees and hiring and assimilating new key employees; our inability to attract or retain key personnel in the future would materially harm our business and results of operations.

Our success depends on the continuing efforts and abilities of our current management team. In addition, our future success will depend, in part, on our ability to attract and retain highly skilled employees, including management, logistics and sales personnel. We may be unable to identify and attract highly qualified employees in the future. In addition, we may not be able to successfully assimilate these employees or hire qualified personnel to replace them if they leave the Company. The loss of the services of any of our key personnel, the inability to attract or retain key personnel in the future, or delays in hiring required personnel could materially harm our business and results of operations.

If we make any acquisitions, they may disrupt or have a negative impact on our business.

Although we have no present plans for any specific acquisition, in the event that we make acquisitions, we could have difficulty integrating the acquired companies’ personnel and operations with our own. In addition, the key personnel of the acquired business may not be willing to work for us. We cannot predict the effect expansion may have on our core business. Regardless of whether we are successful in making an acquisition, the negotiations could disrupt our ongoing business, distract our management and employees and increase our expenses. In addition to the risks described above, acquisitions are accompanied by a number of inherent risks, including, without limitation, the following:

| · | the difficulty of integrating acquired products, services or operations; |

| · | the potential disruption of the ongoing businesses and distraction of our management and the management of acquired companies; |

| · | the difficulty of incorporating acquired rights or products into our existing business; |

| · | difficulties in disposing of the excess or idle facilities of an acquired company or business and expenses in maintaining such facilities; |

| · | difficulties in maintaining uniform standards, controls, procedures and policies; |

| · | the potential impairment of relationships with employees and customers as a result of any integration of new management personnel; |

| · | the potential inability or failure to achieve additional sales and enhance our customer base through cross-marketing of the products to new and existing customers; |

| · | the effect of any government regulations which relate to the business acquired; |

| · | potential unknown liabilities associated with acquired businesses or product lines, or the need to spend significant amounts to retool, reposition or modify the marketing and sales of acquired products or the defense of any litigation, whether of not successful, resulting from actions of the acquired company prior to our acquisition. |

Our business could be severely impaired if and to the extent that we are unable to succeed in addressing any of these risks or other problems encountered in connection with these acquisitions, many of which cannot be presently identified, these risks and problems could disrupt our ongoing business, distract our management and employees, increase our expenses and adversely affect our results of operations.

| (7) |

Risks Related to Ownership of our Common Stock

Volatility in our common stock price may subject us to securities litigation.

Stock markets, in general, have experienced in recent months, and continue to experience, significant price and volume volatility, and the market price of our common stock may continue to be subject to similar market fluctuations unrelated to our operating performance or prospects. This increased volatility, coupled with depressed economic conditions, could continue to have a depressing effect on the market price of our common stock. The following factors, many of which are beyond our control, may influence our stock price:

| • | announcements of technological or competitive developments; | |

| • | actual or anticipated fluctuations in our quarterly operating results; | |

| • | changes in financial estimates by securities research analysts; | |

| • | changes in the economic performance or market valuations of our competitors; | |

| • | additions or departures of our executive officers or other key personnel; | |

| • | release or expiration of lock-up or other transfer restrictions on our outstanding common stock; and | |

| • | sales or perceived sales of additional shares of our common stock. |

In addition, the securities market has, from time to time, experienced significant price and volume fluctuations that are not related to the operating performance of particular companies. Any of these factors could result in large and sudden changes in the volume and trading price of our common stock and could cause our stockholders to incur substantial losses. In the past, following periods of volatility in the market price of a company’s securities, stockholders have often instituted securities class action litigation against that company. If we were involved in a class action suit or other securities litigation, it would divert the attention of our senior management, require us to incur significant expense and, whether or not adversely determined, could have a material adverse effect on our business, financial condition, results of operations and prospects.

Our common stock is currently quoted on the Over-the Counter Bulletin Board quotation market under the symbol “BMXD”. To date, however, trading activity in our common stock has been extremely limited. There is no assurance as to the depth or liquidity of any such market or the prices at which holders may be able to sell the securities.

Our common stock is quoted on the Over-the Counter Bulletin Board quotation market under the symbol “BMXD”. To date, however, trading activity in our common stock has been extremely limited. There is also no assurance as to the depth or liquidity of any such market or the prices at which holders may be able to sell the securities. An investment in our common stock may be totally illiquid and investors may not be able to liquidate their investment readily or at all when they need or desire to sell.

Our common stock, if sold to investors in the United States may be considered "restricted securities", in which case the Securities may need to be sold in compliance with Rule 144, adopted under the Securities Act of 1933. Rule 144 provides, in essence, that holders of restricted securities, after holding restricted securities for one (1) year, may sell in broker/market maker transactions an amount equal to the greater of 1% of our outstanding common stock or the weekly average trading volume over the preceding four weeks, every three (3) months. There can be no assurance that a public market for the common stock will be present, or that Rule 144 will be available at the time an investor may wish to sell any shares purchased. Investors must be prepared to accept the fact that their investment is of a long-term nature and may not be readily liquidated.

There can be no assurance that that the conditions necessary to permit sales under Rule 144 will ever be satisfied. Moreover, there can be no assurance that any liquid market for our common stock will develop, or that, if a market develops, it will be sustained.

If we issue shares of preferred stock, your investment could be diluted or subordinated to the rights of the holders of preferred stock.

Our Board of Directors is authorized by our Certificate of Incorporation to establish classes or series of preferred stock and fix the designation, powers, preferences and rights of the shares of each such class or series without any further vote or action by our stockholders. Any shares of preferred stock so issued could have priority over our common stock with respect to dividend or liquidation rights. The issuance of shares of preferred stock, or the issuance of rights to purchase such shares, could be used to discourage an unsolicited acquisition proposal. For instance, the issuance of a series of preferred stock might impede a business combination by including class voting rights that would enable a holder to block such a transaction. In addition, under certain circumstances, the issuance of preferred stock could adversely affect the voting power of holders of our common stock. Although our Board of Directors is required to make any determination to issue preferred stock based on its judgment as to the best interests of our stockholders, our Board could act in a manner that would discourage an acquisition attempt or other transaction that some, or a majority, of our stockholders might believe to be in their best interests or in which such stockholders might receive a premium for their stock over the then-market price of such stock. Presently, our Board of Directors does not intend to seek stockholder approval prior to the issuance of currently authorized preferred stock, unless otherwise required by law or applicable stock exchange rules. Although we have no plans to issue any additional shares of preferred stock or to adopt any new series, preferences or other classification of preferred stock, any such action by our Board of Directors or issuance of preferred stock by us could dilute your investment in our common stock and warrants or subordinate your holdings to such shares of preferred stock.

Future issuances or sales, or the potential for future issuances or sales, of shares of our common stock, the conversion of preferred stock into our common stock, or the conversion of convertible notes into our common stock, may cause the trading price of our securities to decline and could impair our ability to raise capital through subsequent equity offerings.

We anticipate that we will issue significant number of shares of our common stock, preferred stock convertible into shares of our common stock, and convertible notes that may be converted into our common stock in connection with various financings and the repayment of debt. All of these issuances are under negotiation, may be at prices significantly below the market price. The additional shares of our common stock issued and to be issued in the future upon the conversion of debt could cause the market price of our common stock to decline, and could have an adverse effect on our earnings per share if and when we become profitable. In addition, future sales of a substantial number of shares of our common stock or other securities in the public markets, or the perception that these sales may occur, could cause the market price of our common stock to decline, and could materially impair our ability to raise capital through the sale of additional securities.

We do not anticipate paying cash dividends on our common stock in the foreseeable future.

We do not anticipate paying cash dividends in the foreseeable future on shares of our common stock. Presently, we intend to retain all of our earnings, if any, to finance development and expansion of our business. Consequently, your only opportunity to achieve a positive return on your investment in us will be if the market price of our common stock appreciates.

Our principal stockholder controls our business affairs, so you will have little or no participation in our business affairs.

Our current management will beneficially own over 50% of our outstanding common stock and will have full control over the affairs of the Company. The security holder will be able to continue to elect over a majority of our directors and to determine the outcome of the corporate actions requiring shareholder approval, regardless of how additional security holders of the Company may vote. The investors will have no ability to influence corporate actions.

Our stock is a penny stock. Trading of our stock may be restricted by the SEC’s penny stock regulations and the FINRA’s sales practice requirements, which may limit a stockholder’s ability to buy and sell our stock.

Our common shares may be deemed to be "penny stock" as that term is defined in Regulation Section "240.3a51-1" of the Securities and Exchange Commission (the "SEC"). Penny stocks are stocks: (a) with a price of less than U.S. $5.00 per share; (b) that are not traded on a "recognized" national exchange; (c) whose prices are not quoted on the NASDAQ automated quotation system (NASDAQ - where listed stocks must still meet requirement (a) above); or (d) in issuers with net tangible assets of less than U.S. $2,000,000 (if the issuer has been in continuous operation for at least three years) or U.S. $5,000,000 (if in continuous operation for less than three years), or with average revenues of less than U.S. $6,000,000 for the last three years.

Section "15(g)" of the United States Securities Exchange Act of 1934, as amended, and Regulation Section "240.15g(c)2" of the SEC require broker dealers dealing in penny stocks to provide potential investors with a document disclosing the risks of penny stocks and to obtain a manually signed and dated written receipt of the document before effecting any transaction in a penny stock for the investor’s account. Potential investors in the Company’s common shares are urged to obtain and read such disclosure carefully before purchasing any common shares that are deemed to be "penny stock".

Moreover, Regulation Section "240.15g-9" of the SEC requires broker dealers in penny stocks to approve the account of any investor for transactions in such stocks before selling any penny stock to that investor. This procedure requires the broker dealer to: (a) obtain from the investor information concerning his or her financial situation, investment experience and investment objectives; (b) reasonably determine, based on that information, that transactions in penny stocks are suitable for the investor and that the investor has sufficient knowledge and experience as to be reasonably capable of evaluating the risks of penny stock transactions; (c) provide the investor with a written statement setting forth the basis on which the broker dealer made the determination in (ii) above; and (d) receive a signed and dated copy of such statement from the investor confirming that it accurately reflects the investor’s financial situation, investment experience and investment objectives. Compliance with these requirements may make it more difficult for investors in the Company’s common shares to resell their common shares to third parties or to otherwise dispose of them. Security holders should be aware that, according to Securities and Exchange Commission Release No. 34-29093, dated April 17, 1991, the market for penny stocks has suffered in recent years from patterns of fraud and abuse. Such patterns include:

(i) control of the market for the security by one or a few broker-dealers that are often related to the promoter or issuer

(ii) manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases

(iii) boiler room practices involving high-pressure sales tactics and unrealistic price projections by inexperienced sales persons

(iv) excessive and undisclosed bid-ask differential and mark-ups by selling broker-dealers

(v) the wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired level, along with the resulting inevitable collapse of those prices and with consequent investor losses

Our management is aware of the abuses that have occurred historically in the penny stock market. Although we do not expect to be in a position to dictate the behavior of the market or of broker-dealers who participate in the market, management will strive within the confines of practical limitations to prevent the described patterns from being established with respect to our securities.

As an issuer of “penny stock” the protection provided by the federal securities laws relating to a forward-looking statement does not apply to us and as a result we could be subject to legal action.

Although federal securities laws provide a safe harbor for forward-looking statements made by a public company that files reports under the federal securities laws, this safe harbor is not available to issuers of penny stocks. As a result, if we are a penny stock, we will not have the benefit of this safe harbor protection in the event of any legal action based upon a claim that the material provided by us contained a material misstatement of fact or was misleading in any material respect because of our failure to include any statements necessary to make the statements not misleading. Such an action could hurt our financial condition.

The issuance of any of our equity securities pursuant to any equity compensation plans we intend to adopt may dilute the value of existing stockholders and may affect the market price of our stock.

In the future, we may issue to our officers, directors, employees and/or other persons equity based compensation under any equity based compensation plan we intend to adopt to provide motivation and compensation to our officers, employees and key independent consultants. The award of any such incentives could result in an immediate and potentially substantial dilution to our existing stockholders and could result in a decline in the value of our stock price. The exercise of these options and the sale of the underlying shares of common stock and the sale of stock issued pursuant to stock grants may have an adverse effect upon the price of our stock.

If we fail to comply with Section 404 of the Sarbanes-Oxley Act of 2002 our business could be harmed and our stock price could decline

Rules adopted by the SEC pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 require annual assessment of our internal control over financial reporting, and attestation of this assessment by our company's independent registered public accountants. The SEC extended the date to comply with the attestation requirements for non-accelerated filers, as defined by the SEC. Accordingly, we are subject to the rules requiring an annual assessment of our internal controls and the requirement to provide an attestation of management's assessment by our independent registered public accountants will first apply to our annual report for the 2010 fiscal year. The standards that must be met for management to assess the internal control over financial reporting as effective are complex, and require significant documentation, testing and possible remediation to meet the detailed standards. The attestation process by our independent registered public accountants is new and we may encounter problems or delays in completing the implementation of any requested improvements and receiving an attestation of our assessment by our independent registered public accountants. If we cannot assess our internal control over financial reporting as effective, or our independent registered public accountants are unable to provide an unqualified attestation report on such assessment, investor confidence and share value may be negatively impacted.

| (8) |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

The classes of equity securities of BMXD issued and outstanding are Common Stock, $.001 par value. The table on the following page sets forth, as of September 21, 2011, certain information with respect to the Common Stock beneficially owned by (i) each Director, nominee and executive officer of BMXD; (ii) each person who owns beneficially more than 5% of the Common Stock; and (iii) all Directors, nominees and executive officers as a group. The percentage of shares beneficially owned is based on there having been 24,537,891 shares of Common Stock outstanding as of September 21, 2011.

Name and Address of Beneficial Owner [1] |

Common Stock Beneficially Owned |

Percent of Class [2] | |

James Dale |

13,000,000 |

52.98% | |

| Agata Podedworny |

4,000,000 |

16.30% | |

MIS Beverage Holdings LLC [3] |

2,000,000 |

8.15% | |

[1] Unless otherwise specified, the address of each of the persons set forth hereto is in care of the Company at 40W. 23rd Street, 2nd Floor, New York, NY 10001.

[2] Based on 24,537,891 issued and outstanding shares of common stock.

[3] The 2,000,000 shares are owned in the name of MIS Beverage Holdings LLC., of which Maria Gordon is the controlling person. Maria Gordon is the wife of Brian Gordon, the Director of the Company.

The following table shows information as of September 21, 2011 with respect to each of the beneficial owners of the Company’s Common Stock by its executive officers, directors and nominee individually and as a group:

| Name and Address [1] | Position | Common Stock Beneficially Owned |

Percent of Shares [2] | |

| James Dale | Chief Executive Officer and Chairman |

13,000,000 |

52.98% | |

| Agata Podedworny [5] | Vice President of Logistics Director |

4,000,000 |

16.30% | |

| Sjoerd de Jong [5] |

Vice President of Sale Director |

1,000,000 |

4.08% | |

Brian Gordon [3] [5] |

Director |

2,000,000 Indirect |

8.15% | |

Dean A. Stewart [4] 13512 Glenwyck Lane Huntersville, North Carolina 28078 |

Director |

50,000 |

0.20% | |

All officers and directors as a group (4 persons named above) |

20,000,000 |

81.51% | ||

[1] Unless otherwise specified, the address of each of the persons set forth her eto is in ca re of the Company at 40W. 23rd Street, 2nd Floor, New York, NY 10001.

[2] Based on 24,537,891 issued and outstanding shares of common stock.

[3] The 2,000,000 shares are owned in the name of MIS Beverage Holdings LLC., of which Maria Gordon is the controlling person. Maria Gordon is the wife of Brian Gordon, the Director of the Company.

[4] Dean A. Stewart resigned from his position as Director of the Company, effective on or about September 9, 2011.

[5] The effective date of the directorship is on or about September 9, 2011.

DIRECTORS AND EXECUTIVE OFFICERS

The following sets forth information concerning the current Directors, nominees and executive officers of the Company, the principal positions with the Company held by such persons and the date such persons became a Director, nominee or executive officer. The Directors serve one year terms or until their successors are elected. The Company has not had standing audit, nominating or compensation committees or committees performing similar functions for the Board of Directors.

| Name | Age | Position | Appointment Date | |

| James Dale | 40 |

Chief Executive Officer and Chairman |

August 19, 2011 | |

| Agata Podedworny | 36 | Vice President of Logistics Director | September 9, 2011 | |

| Sjoerd de Jong | 36 |

Vice President of Sale Director |

September 9, 2011 | |

Brian Gordon |

37 | Director | September 9, 2011 | |

Biographies

Mr. James Dale – Chief Executive Officer and Chairman

Mr. Dale, aged 40, is the Chief Executive Officer of Panache LLC. Mr. Dale was born in New Delhi India and raised in Auckland NZ. Mr. Dale came to the US as 42 Below vodka's strategic North American partner in 2003 and was instrumental in the brands sale to Bacardi in 2007. After the trade sale, Mr. Dale developed brands which are currently part of Panache's expanding portfolio. Mr. Dale is not, and has not been, a participant in any transaction with the Registrant that requires disclosure under Item 404(a) of Regulation S-K. There is no family relationship between Mr. Dale and any director, executive officer, or person nominated or chosen by the Registrant to become a director or executive officer.

Ms. Agata Podedworny - Vice President of Logistics and Director

Ms. Podedworny, age 36, holds an international business and marketing degree from New York University and a JD degree from St John’s Law School. She is fluent in Polish and manages all logistics from the vodka supplier and distillery in Poland as well as manages all operations for nationally and internationally based Panache LLC customers. She is currently a director of Panache LLC and brand ambassador and principal for Alchemia Vodka.

Mr. Sjoerd de Jong - Vice President of Sale and Director

Mr. Sjoerd de Jong graduated from the University of Vermont in 1999 with a business degree in Community Development an Applied Economics. After college Mr. de Jong pursued a career in professional basketball in Holland for three years. Mr. de Jong joined Midnight Oil Company and quickly rose to become the general manager of all five MOC properties in New York. In 2003 Mr. de Jong joined forces with Mr. James Dale to become national sales director for 42 Below Vodka out of New Zealand. Mr. de Jong was responsible for building the brand’s image and sales from an on-premise market and helping bring it to a place where it was a viable brand to acquire (by Bacardi USA).

Currently, Sjoerd de Jong is the national sales director for all of Panache Imports brands (Wodka Vodka, Alchemia vodka and Alibi Bourbon) and a 4.29% share holder in the Company.

Mr. Brian Gordon - Director

Mr. Brian Gordon is the co-founder of MMG, who has been developing and directing marketing and advertising campaigns for spirits brands for over 12 years. Mr. Gordon has worked on a variety of campaigns for many of the major drinks companies including Diageo, Pernod Ricard and Moet Hennessey. Mr. Gordon brings extensive experience to Panache and its portfolio of brands. Gordon and his team have directed the marketing strategy and led the creative development for Wodka Vodka since its launch in July 2010.

No director, person nominated to become a director, executive officer, promoter or control persons of our company has been involved during the last five years in any of the following events that are material to an evaluation of his ability or integrity:

| · | Bankruptcy petitions filed by or against any business of which such person was a general partner or executive officer either at the time of the bankruptcy or within two years prior to that time. |

| · | Conviction in a criminal proceeding or being subject to a pending criminal proceeding (excluding traffic violations and other minor offenses). |

| · | Being subject to any order, judgment or decree, not subsequently reversed, suspended or vacated, of any court of competent jurisdiction, permanently or temporarily enjoining, barring or suspending or otherwise limiting his involvement in any type of business, securities or banking activities, or |

| · | Being found by a court of competition jurisdiction (in a civil action), the Securities and Exchange Commission or the Commodities Futures Trading Commission to have violated a federal or state securities or commodities law, and the judgment has not been reversed, suspended or vacated. |

The Company does not have a separately designated standing audit committee. Pursuant to Section 3(a)(58)(B) of the Exchange Act, the entire Board of Directors acts as an audit committee for the purpose of overseeing the accounting and financial reporting processes, and audits of the financial statements of the Company. The Commission recently adopted new regulations relating to audit committee composition and functions, including disclosure requirements relating to the presence of an "audit committee financial expert" serving on its audit committee. In connection with these new requirements, the Company's Board of Directors examined the Commission's definition of "audit committee financial expert" and concluded that the Company does not currently have a person that qualifies as such an expert. The Company has had minimal operations for the past two (2) years. Presently, there are only two (2) directors serving on the Company's Board, and the Company is not in a position at this time to attract, retain and compensate additional directors in order to acquire a director who qualifies as an "audit committee financial expert", but the Company intends to retain an additional director who will qualify as such an expert, as soon as reasonably practicable. While neither of our current directors meets the qualifications of an "audit committee financial expert", each of the Company's directors, by virtue of his past employment experience, has considerable knowledge of financial statements, finance, and accounting, and has significant employment experience involving financial oversight responsibilities. Accordingly, the Company believes that its current directors capably fulfill the duties and responsibilities of an audit committee in the absence of such an expert.

The Company does not have a nominating and compensation committees of the Board of Directors, or committees performing similar functions.

Section 16(a) Beneficial Ownership Reporting Compliance

Under Section 16(a) of the Exchange Act, all executive officers, directors, and each person who is the beneficial owner of more than 10% of the common stock of a company that files reports pursuant to Section 12 of the Exchange Act, are required to report the ownership of such common stock, options, and stock appreciation rights (other than certain cash-only rights) and any changes in that ownership with the Commission. Specific due dates for these reports have been established, and the Company is required to report, in this Schedule 14C, any failure to comply therewith during the fiscal year ended December 31. The Company believes that all of these filing requirements were satisfied by its executive officers, directors and by the beneficial owners of more than 10% of the Company’s common stock. In making this statement, the Company has relied solely on copies of any reporting forms received by it, and upon any written representations received from reporting persons that no Form 5 (Annual Statement of Changes in Beneficial Ownership) was required to be filed under applicable rules of the Commission.

| (9) |

EXECUTIVE COMPENSATION

Summary Compensation Table

The following table sets forth certain information regarding the annual and long-term compensation for services in all capacities to us for the prior fiscal years ended December 31, 2010, 2009, and 2008, of those persons who were either the chief executive officer during the last completed fiscal year or any other compensated executive officers as of the end of the last completed fiscal year, and whose compensation exceeded $100,000 for those fiscal periods.

SUMMARY COMPENSATION TABLE

| Annual compensation | Awards | Payouts | ||||||

| Name and Principal Position | Year |

Salary ($) |

Bonus ($) |

Other Annual Compensation ($) |

Restricted Stock Award(s) ($) |

Securities Underlying Options SARs(#) |

LTIP payouts ($) |

All Other Compensation ($) |

|

Michael J. Bongiovanni President and CEO |

2010 | --- | --- | --- | --- | --- | --- | --- |

| 2009 | --- | --- | --- | --- | --- | --- | --- | |

| 2008 | --- | --- | --- | --- | --- | --- | --- | |

|

Dean A. Stewart Vice President and CFO |

2010 | --- | --- | --- | --- | --- | --- | --- |

| 2009 | --- | --- | --- | --- | --- | --- | --- | |

| 2008 | --- | --- | --- | --- | --- | --- | --- | |

| (1) | Mr. Michael J. Bongiovanni resigned as the Company’s President and Chief Executive Officer on August 19, 2011 in connection with the change of control resulting from the closing of the Transactions. Mr. Michael J. Bongiovanni did not receive any compensation from the Company during his tenure as President and Chief Executive Officer. Mr. Bogiovanni resigned from his positions as President, Chief Executive Officer and Director of the Company on August 19, 2011, effective immediately.

|

| (2) | Mr. Dean A. Stewart resigned as the Company’s Vice President and Chief Financial Officer on August 26, 2011 in connection with the change of control resulting from the closing of the Transactions. Mr. Dean A. Stewart did not receive any compensation from the Company during his tenure as Vice President and Chief Financial Officer. Mr. Stewart resigned from his positions as Vice President and Chief Financial Officer on August 26, 2011, effective immediately, and resigned from his position as Director of the Company, effective on or about September 9, 2011.

|

Option Grants in Last Fiscal Year

Our current executive officers and directors have not and do not receive any compensation and have not received any restricted shares awards, options or any other payouts.

There are no annuity, pension or retirement benefits proposed to be paid to officers, directors or employees of the Company in the event of retirement at normal retirement date pursuant to any presently existing plan provided or contributed to by Company.

Employment Agreements

The Company has no employment agreements with any of its employees.

Directors’ and Officers’ Liability Insurance

The Company currently does not have insurance insuring directors and officers against liability; however, the Company is in the process of investigating the availability of such insurance.

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS

The following includes a summary of transactions since our incorporation on December 28, 2004, or any currently proposed transaction, in which we were or are to be a participant and the amount involved exceeded or exceeds the lesser of $120,000 or one percent of the average of our total assets at year end for the last two completed fiscal years, and in which any related person had or will have a direct or indirect material interest (other than compensation described under “Executive Compensation”). We believe the terms obtained or consideration that we paid or received, as applicable, in connection with the transactions described below were comparable to terms available or the amounts that would be paid or received, as applicable, in arm’s-length transactions.

· On August 19, 2011, the Company entered into and closed the POE among the Company, Mr. Bongiovanni, Panache and the Panache Member, pursuant to which, the Company acquired one hundred percent (100%) of the issued and outstanding membership interest units of Panache from the Panache Members in exchange for a new issuance 17,440,000 shares of common stock of the Company to the Panache Members. Upon completion of the physical exchange of the share certificates, Panache became a wholly-owned subsidiary of the Company.

· On August 19, 2011, a Purchase Agreement was entered among Mr. Bongiovanni and Mr. Dale, pursuant to which, Mr. Bongiovanni sold an aggregate of 2,560,000 shares of the Company’s Common Stock, par value $0.001 held by him to Mr. Dale, for an aggregate purchase price of $125,000. As a result of the consummation of the Transactions, Mr. Dale now holds 55.71% of the Company’s outstanding common stock resulting in a change in control of the Company.

- On June 9, 2011, the Company entered a services agreement with Greentree Financial Group Inc. (“Greentree”), which is a company part-owned by the Company’s prior President, pursuant to which Greentree received 520,000 shares of the Company’s common stock for consulting services in connection with the plan of exchange transaction discussed in Item 2.01, a copy of the agreement was attached hereto as exhibit 10.3. Additionally, Greentree received $16,275 for due diligence on the Company’s acquisition and $8,500 for one-year of XBRL EDGAR services that ends with the 2011 10K report. The Company also repaid a $5,000 loan to Greentree.

- On June 1, 2011, the Company entered a services agreement with Columbus Partners, LLC (“Columbus”), pursuant to which Columbus received 1,143,391 shares of the Company’s common stock for professional services rendered as described in the services agreement attached hereto as Exhibit 10.4.

- On September 2, 2011, the Company entered a services agreement with Wall Street Resources, Inc (“WSR”), pursuant to which WSR received 60,000 shares of the Company’s common stock for public relations services rendered as described in the services agreement attached hereto as Exhibit 10.5.

Except as set forth in our discussion above, none of our directors, director nominees or executive officers has been involved in any transactions with us or any of our directors, executive officers, affiliates or associates which are required to be disclosed pursuant to the rules and regulations of the SEC.

| (10) |

DESCRIPTION OF SECURITIES

Market For BMXD Common Equity, Related Stockholder Matters And Issuer Purchases Of Equity Securities

Market Information

Our common stock is traded the Over-The-Counter Bulletin Board under the symbol “BMXD”. The Over-The-Counter Bulletin Board is a quotation medium for subscribing members only. And only market makers can apply to quote securities on the Over-The-Counter Bulletin Board. Trading in the common stock in the over-the-counter market has been limited and sporadic and the quotations set forth below are not necessarily indicative of actual market conditions. Further, these prices reflect inter-dealer prices without retail mark-up, mark-down, or commission, and may not necessarily reflect actual transactions. The following tables set forth the high and low sale prices for our common stock as reported on the Electronic Bulletin Board for the periods indicated.

| 2009 and 2010 | High | Low |

| Quarter Ended 12/31/2008* | $ 1.80 | $ 1.01 |

| Quarter Ended 3/31/2009 | $ 2.05 | $ 1.01 |

| Quarter Ended 6/30/2009 | $ 1.70 | $ 1.01 |

| Quarter Ended 9/30/2009 | $ 1.20 | $ 1.05 |

| Quarter Ended 12/31/2009 | $ 1.20 | $ 1.05 |

| Quarter Ended 3/31/2010 | $ 1.10 | $ 0.85 |

| Quarter Ended 6/30/2010 | $ 0.85 | $ 0.25 |

| Quarter Ended 9/30/2010 | $ 0.25 | $ 0.20 |

| Quarter Ended 12/31/2010 | $ 0.20 | $ 0.20 |

| Quarter Ended 3/31/2011 | $ 0.20 | $ 0.20 |

| Quarter Ended 6/30/2011 | $ 0.85 | $ 0.20 |

*Our stock commenced trading on December 8, 2008

Agreements to Register

Not applicable.

Holders

As of September 21, 2011 there were 61 holders of record of our common stock.

Shares Eligible for Future Sale.

In general, under Rule 144 as currently in effect, any of our affiliates and any person or persons whose sales are aggregated with our affiliates, who has beneficially owned his or her restricted shares for at least six months, may be entitled to sell in the open market within any three-month period a number of shares of common stock that does not exceed the greater of (i) 1% of the then outstanding shares of our common stock, or (ii) the average weekly trading volume in the common stock during the four calendar weeks preceding such sale. Sales under Rule 144 are also affected by limitations on manner of sale, notice requirements, and availability of current public information about us. Non-affiliates who have held their restricted shares for one year may be entitled to sell their shares under Rule 144 without regard to any of the above limitations, provided they have not been affiliates for the three months preceding such sale.

Further, Rule 144A as currently in effect, in general, permits unlimited resales of restricted securities of any issuer provided that the purchaser is an institution that owns and invests on a discretionary basis at least $100 million in securities or is a registered broker-dealer that owns and invests $10 million in securities. Rule 144A allows our existing stockholders to sell their shares of common stock to such institutions and registered broker-dealers without regard to any volume or other restrictions. Unlike under Rule 144, restricted securities sold under Rule 144A to non-affiliates do not lose their status as restricted securities.

Dividends

We have not declared any cash dividends on our common stock since our inception and do not anticipate paying such dividends in the foreseeable future. We plan to retain any future earnings for use in our business. Any decisions as to future payment of dividends will depend on our earnings and financial position and such other factors, as the Board of Directors deems relevant.

Dividend Policy

All shares of common stock are entitled to participate proportionally in dividends if our Board of Directors declares them out of funds legally available. These dividends may be paid in cash, property or additional shares of common stock. We have not paid any dividends since our inception and presently anticipate that all earnings, if any, will be retained to develop our business. Any future dividends will be at the discretion of our Board of Directors and will depend upon, among other things, our future earnings, operating and financial condition, capital requirements, and other factors.

Our Shares are "Penny Stocks" within the Meaning of the Securities Exchange Act of 1934

Our Shares are "penny stocks" within the definition of that term as contained in the Securities Exchange Act of 1934, generally equity securities with a price of less than $5.00. Our shares will then be subject to rules that impose sales practice and disclosure requirements on certain broker-dealers who engage in certain transactions involving a penny stock.

Under the penny stock regulations, a broker-dealer selling penny stock to anyone other than an established customer or "accredited investor" must make a special suitability determination for the purchaser and must receive the purchaser's written consent to the transaction prior to the sale, unless the broker-dealer is otherwise exempt. Generally, an individual with a net worth in excess of $1,000,000 or annual income exceeding $200,000 individually or $300,000 together with his or her spouse is considered an accredited investor. In addition, unless the broker-dealer or the transaction is otherwise exempt, the penny stock regulations require the broker-dealer to deliver, prior to any transaction involving a penny stock, a disclosure schedule prepared by the Securities and Exchange Commission relating to the penny stock market. A broker-dealer is also required to disclose commissions payable to the broker-dealer and the Registered Representative and current bid and offer quotations for the securities. In addition a broker-dealer is required to send monthly statements disclosing recent price information with respect to the penny stock held in a customer's account, the account’s value and information regarding the limited market in penny stocks. As a result of these regulations, the ability of broker-dealers to sell our stock may affect the ability of Selling Security Holders or other holders to sell their shares in the secondary market. In addition, the penny stock rules generally require that prior to a transaction in a penny stock, the broker-dealer make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written agreement to the transaction.

These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for a stock that becomes subject to the penny stock rules. These additional sales practice and disclosure requirements could impede the sale of our securities, if our securities become publicly traded. In addition, the liquidity for our securities may be adversely affected, with concomitant adverse affects on the price of our securities. Our shares may someday be subject to such penny stock rules and our shareholders will, in all likelihood, find it difficult to sell their securities.

Voting Rights

Each share of common stock entitles the holder to one vote at meetings of shareholders. The holders are not permitted to vote their shares cumulatively. Accordingly, the holders of common stock holding, in the aggregate, more than fifty percent of the total voting rights can elect all of our directors and, in such event, the holders of the remaining minority shares will not be able to elect any of such directors. The vote of the holders of a majority of the issued and outstanding shares of common stock entitled to vote thereon is sufficient to authorize, affirm, ratify or consent to such act or action, except as otherwise provided by law.

Miscellaneous Rights and Provisions

Holders of common stock have no preemptive or other subscription rights, conversion rights, or redemption provisions. In the event of our dissolution, whether voluntary or involuntary, each share of common stock is entitled to share proportionally in any assets available for distribution to holders of our equity after satisfaction of all liabilities and payment of the applicable liquidation preference of any outstanding shares of preferred stock.

There is no provision in our charter or by-laws that would delay, defer, or prevent a change in our control.

Debt Securities

We have not issued any debt securities.

| (11) |

Dividend Rights

The common stock has no rights to dividends, except as the Board may decide in its discretion, out of funds legally available for dividends. We have never paid any dividends on our common stock, and have no plans to pay any dividends in the foreseeable future.

Common Stock Description

We are authorized to issue 200,000,000 shares of common stock, $.001 par value, of which 24,537,891 shares are currently issued and outstanding. The holders of shares of common stock have one vote per share. None of the shares have preemptive or cumulative voting rights, have any rights of redemption or are liable for assessments or further calls. The holders of common stock are entitled to dividends, when and as declared by the Board of Directors from funds legally available, and upon liquidation of us to share pro rata in any distribution to shareholders.

Transfer Agent

Guardian Registrar & Transfer, Inc., 7951 S.W. 6thStreet, Suite 216, Plantation, Florida, 33324, is our transfer agent and registrar for our common stock.

Warrants

As part of the issuance of common shares in 2009, we issued 18,500 stock warrants during the year 2009. No warrants were issued in 2010. These warrants expire in three years from issuance in the first quarter of 2009 and the exercise price is $2.00 per warrant. No warrants expired during 2010.

During the year ended December 31, 2009, we recorded an expense of $21,123 equal to the estimated fair value of the options at the date of grants. The fair market value was calculated using the Black-Scholes options pricing model, assuming approximately 1.28% risk-free interest, 0% dividend yield, 60% volatility, and a life of three years. The remaining life of the warrants as of December 31, 2010 is 1.25 years.