Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ENCORE CAPITAL GROUP INC | d236261d8k.htm |

Encore Capital Group

JMP Securities Financial Services

and Real Estate Conference

September 26, 2011

Exhibit 99.1 |

CAUTIONARY NOTE ABOUT FORWARD-LOOKING STATEMENTS

2

FORWARD-LOOKING STATEMENTS

The statements in this presentation that are not historical facts, including, most importantly,

those statements preceded by, or that include, the words “may,” “believe,”

“projects,” “expects,” “anticipates” or the negation thereof, or

similar expressions, constitute “forward- looking statements” within the meaning

of the Private Securities Litigation Reform Act of 1995 (the “Reform Act”).

These statements may include, but are not limited to, statements regarding our future operating

results and growth. For all “forward-looking statements,” the Company

claims the protection of the safe harbor for forward-looking statements contained in the

Reform Act. Such forward-looking statements involve risks, uncertainties and other

factors which may cause actual results, performance or achievements of the Company and

its subsidiaries to be materially different from any future results, performance or

achievements expressed or implied by such forward-looking statements. These risks,

uncertainties and other factors are discussed in the reports filed by the Company with the

Securities and Exchange Commission, including the most recent reports on Forms 10-K,

10-Q and 8-K, each as it may be amended from time to time. The Company disclaims any

intent or obligation to update these forward-looking statements. |

INVESTMENT HIGHLIGHTS

3

•

Investments made over the past few years have driven

significant improvements in collections, cash flow and earnings

•

Difficult regulatory environment being managed proactively

•

Expanding presence in India, combined with new strategic

initiatives, are expected to continue increasing cash flow from

operations

•

Demonstrated ability to raise and profitably deploy capital in

favorable and unfavorable business cycles |

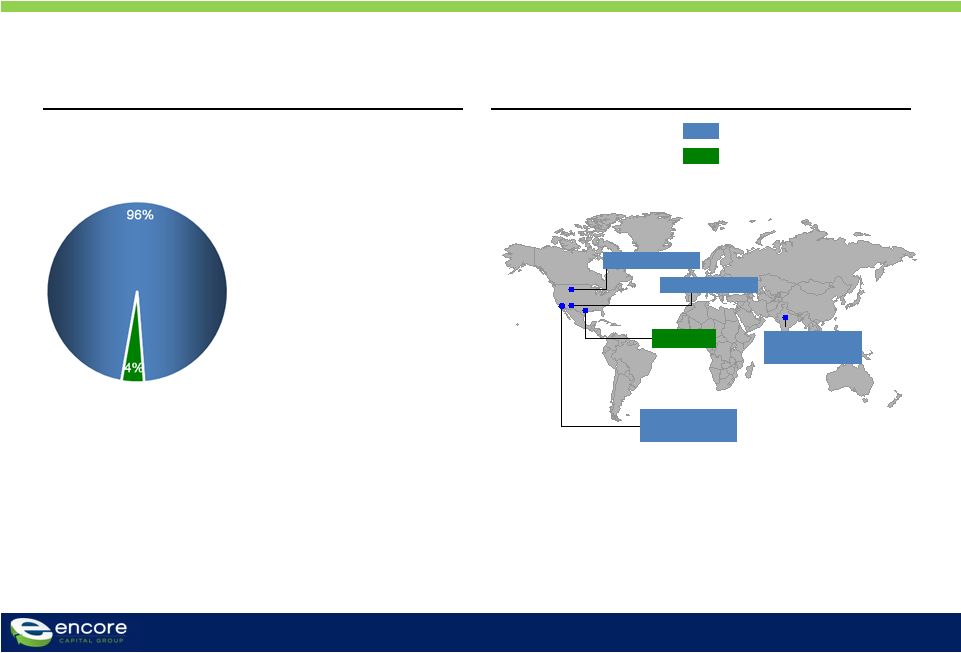

ENCORE

IS A LEADING PLAYER IN THE CONSUMER DEBT BUYING AND RECOVERY INDUSTRY

4

Revenue Composition

As of June 30, 2011

Global Capabilities

Debt Purchasing & Collections

Bankruptcy Servicing

•

Purchase and collection

of

charged-off unsecured

consumer receivables

(primarily credit card)

•

Robust business model

emphasizing consumer

intelligence and

operational

specialization

•

Invested ~$2.0 billion to

acquire receivables with a face

value of ~$61 billion

•

Acquired ~36 million consumer

accounts since

inception

•

Process secured consumer bankruptcy accounts for leading

auto

lenders and other financial institutions

•

Proprietary software dedicated to bankruptcy servicing

•

Operational platform that integrates lenders, trustees,

and

consumers

St Cloud, MN

Arlington, TX

Phoenix, AZ

Delhi, India

Call Center /

Technology Site

Call Center Site

Ascension

Call Center Site

San Diego, CA

Debt Purchasing & Collections

Bankruptcy Servicing

Headquarters/

Call Center Site |

STRATEGIC DECISIONS MADE OVER THE PAST DECADE

DEMONSTRATE OUR ABILITY TO FORESEE AND ADAPT TO CHANGE

5

•

Established our operating

center in India

•

Created an activity-level cost

database

•

Built and implemented the

industry’s first known ability-to-

pay (capability) model

Overconfidence and

Irrational Pricing

2005

2007

2006

2008

•

Created first generation

consumer-level underwriting

models

An Emerging

Market

Demand

Supply

2001

2002

2003

2004

Attractive

Opportunities

2009

2010

2011

•

Expanded access to

capital |

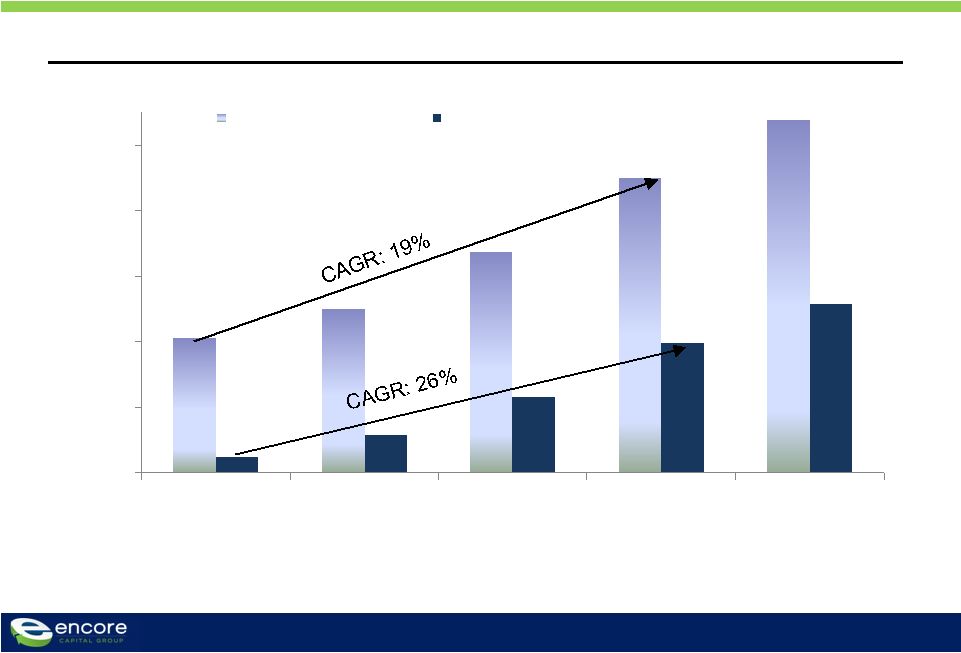

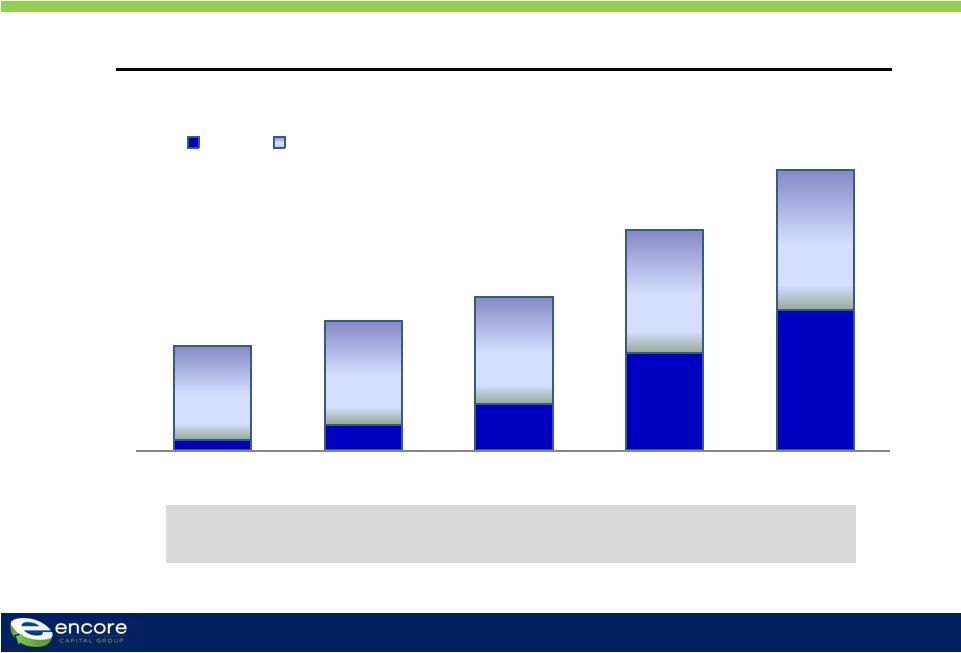

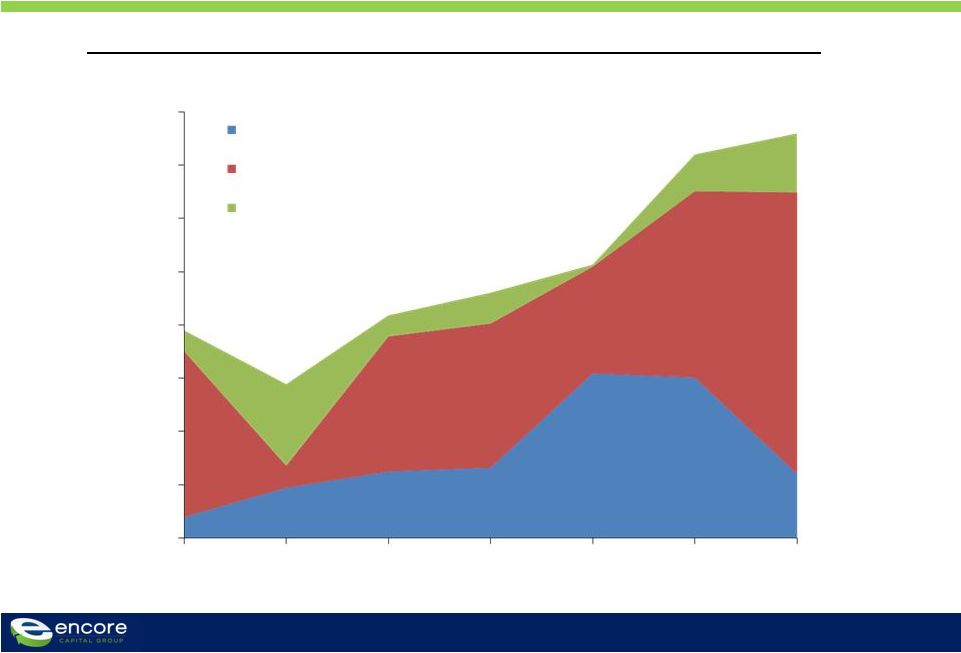

$150

$250

$350

$450

$550

$650

2007

2008

2009

2010

LTM**

Gross Collections

Adjusted EBITDA

AS A RESULT, WE HAVE GENERATED STRONG RESULTS DESPITE THE

MACROECONOMIC DOWNTURN

6

($ millions)

*

Adjusted EBITDA is a non-GAAP number. The Company considers Adjusted EBITDA to

be a meaningful indicator of operating performance and uses it as a measure to

assess the operating performance of the Company. See Reconciliation of Adjusted

EBITDA to GAAP Net Income at the end of this presentation **

LTM data as of 06/30/2011

Adjusted EBITDA* and Gross Collections by year |

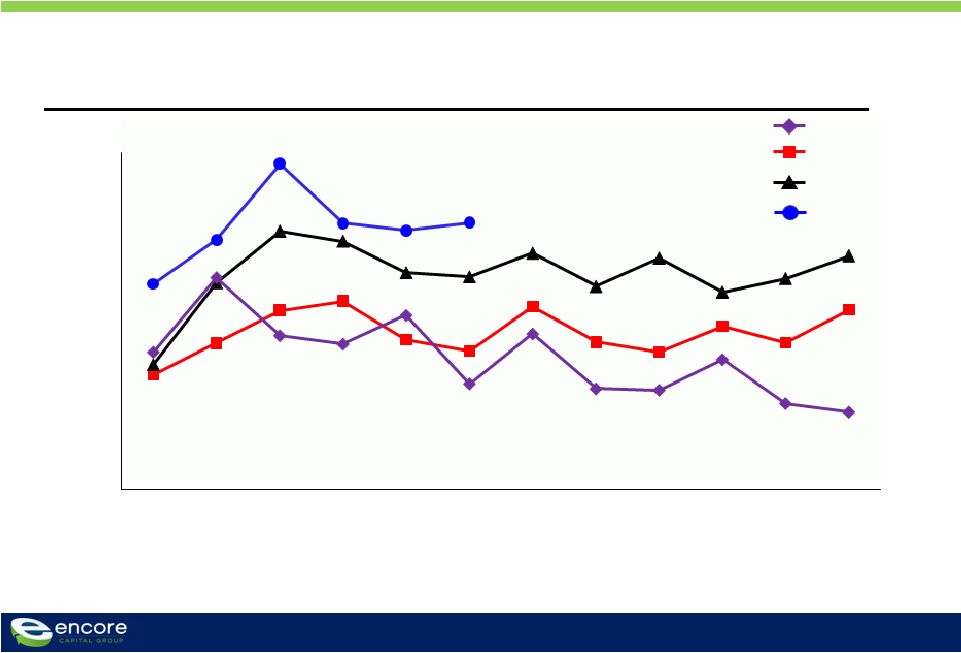

Metric

Recent trend

•

Payer rates

•

Upward

•

Average payment size

•

Stable

•

Payment style

•

More payment plans

•

Broken payer rates

•

Mild improvement

•

Settlement rates

•

Stable

7

OUR CONSUMERS HAVE SHOWN THAT THEY ARE RESILIENT |

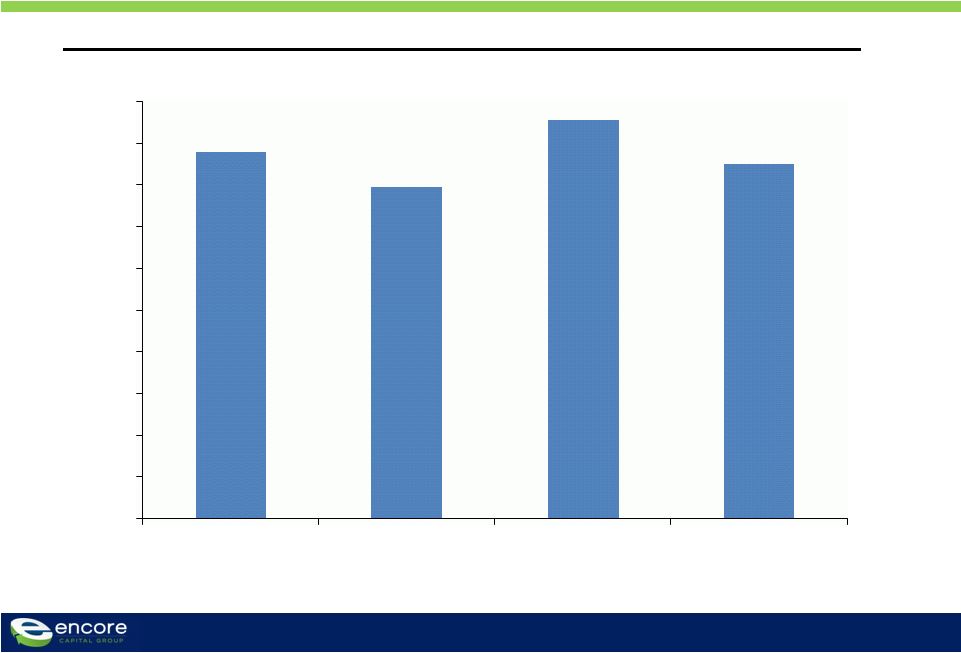

PAYER

RATES HAVE ACTUALLY INCREASED OVER THE PAST FEW YEARS

8

Overall payer rate for all active inventory

2008

0.8%

0.9%

1.0%

1.1%

1.2%

1.3%

1.4%

1.5%

1.6%

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2009

2010

2011 |

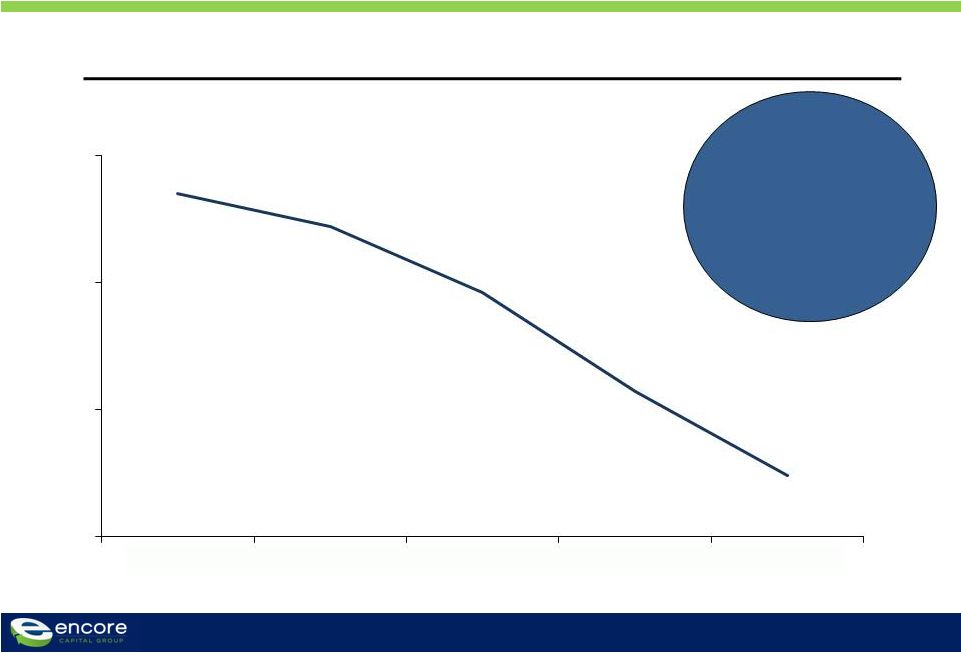

51.5

50.2

47.6

43.7

40.4

2007

2008

2009

2010

H1 2011

WE HAVE FUNDAMENTALLY CHANGED THE COST STRUCTURE OF THE

COMPANY OVER THE PAST FOUR YEARS

9

Overall Cost-to-Collect

(%)

An 1110 basis point

reduction in cost-to-

collect translated into

$43 million in cost

savings in H1 2011 |

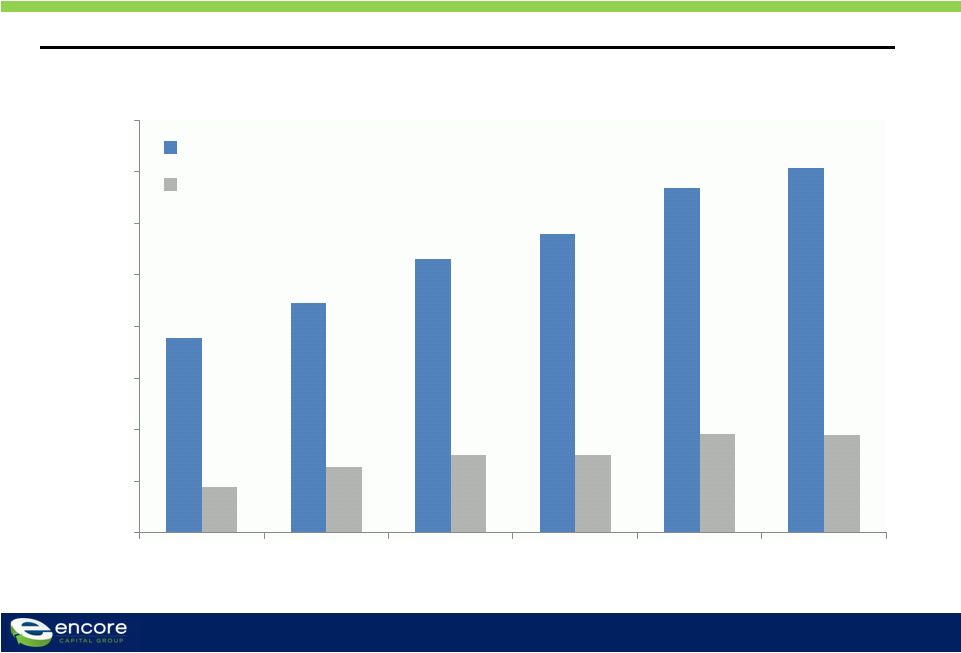

LED BY

OUR INDIA CENTER, WHICH IS EXPECTED TO PRODUCE HALF OF ALL 2011 CALL CENTER

COLLECTIONS 10

Collections from all Call Centers

Percent

of Total:

10%

19%

30%

44%

50%

2007

2008

2009

2010

2011E

India

U.S.

$126

$157

$186

$268

~$340

($ millions) |

11

DESPITE LOCAL WAGE INFLATION, WE HAVE BEEN ABLE TO MAINTAIN

OUR TOTAL COST PER EMPLOYEE

* Cost per FTE includes all India site costs

Monthly Cost per Account Manager (FTE)*

($)

$1,760

$

1,590

$1,910

$1,680

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2007

2008

2009

2010 |

WE

CONTINUE TO BUILD A SUBSTANTIAL RESERVOIR FOR THE FUTURE

12

Annual Estimated Remaining Gross Collection (ERC) and Total Debt

($ millions, at end of period)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2006

2007

2008

2009

2010

Q2 2011

ERC

Total Debt |

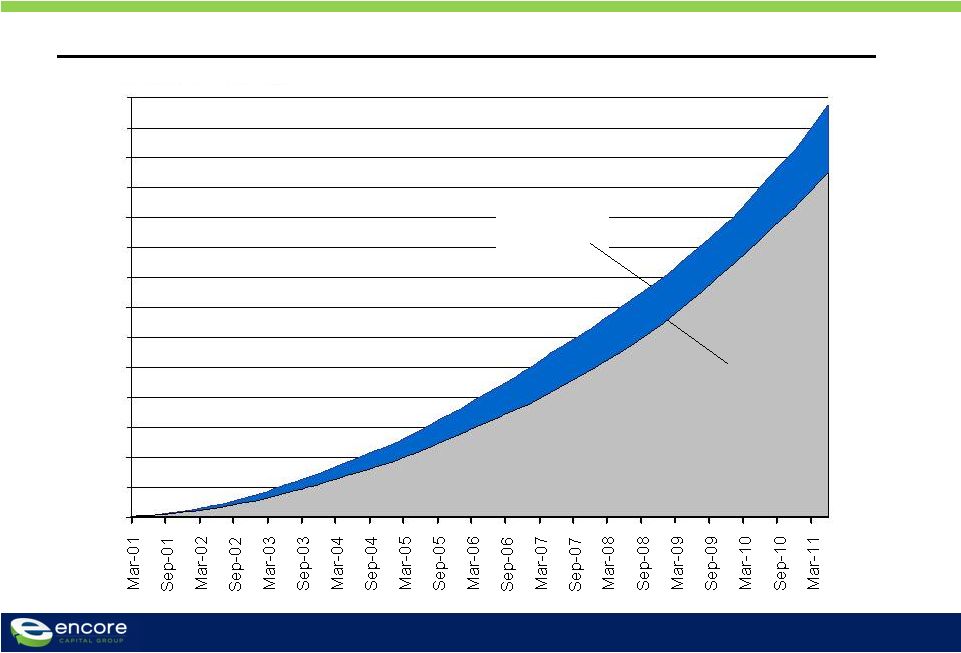

WE

BELIEVE OUR CURRENT ESTIMATE OF REMAINING COLLECTIONS IS CONSERVATIVE GIVEN OUR

HISTORY 13

Cumulative collections (initial expectation vs. actual)

($ millions, March 01 –

June 11)

Initial

projections

$-

$250

$500

$750

$1,000

$1,250

$1,500

$1,750

$2,000

$2,250

$2,500

$2,750

$3,000

$3,250

$3,500

Actual cash

collections |

OUR

ABILITY TO INCREASE PURCHASES IS A RESULT OF NOT BEING LIMITED TO A PARTICULAR

ASSET CLASS OR AGE OF RECEIVABLE 14

Historical Purchase Mix by Year, 2011 Estimate

($ millions)

$0

$50

$100

$150

$200

$250

$300

$350

$400

2005

2006

2007

2008

2009

2010

2011E

Fresh Credit Card

Older Credit Card

Telecom, BK, and other (combined) |

OUR

BUSINESS MODEL IS CRITICALLY IMPORTANT, AS IT PROVIDES THE CONSUMER WITH TIME

TO RECOVER 15

Timeframe

Process and

relationship

with consumers

Outcome

•

Charge-off threshold

extends a maximum of

6 months

Transactional

•

Attempt immediate

resolution during

delinquency cycle

(days 30 –

180)

•

Consumer is “charged-

off”

by issuer on day 181

•

Issuer offers to sell

unsecured, charged-off

debt or service through

3rd party agencies

•

Four-to-six month

collection cycle

Pressured

•

Artificial deadlines

•

Multiple collection

companies

•

Counterproductive

incentive structure

•

Consumer is

confused and

frustrated

•

Consumer has 84 months

to recover financially

Partnership

•

Create partnership strategy

and set goals

•

Tailor work strategies to

individual circumstances,

giving them time for a

consumer to recover

•

Maximizes likelihood of

repayment, creates

consistency, and ensures

that consumers are treated

fairly

CONTINGENCY

COLLECTION

AGENCY

ORIGINAL

CREDITOR |

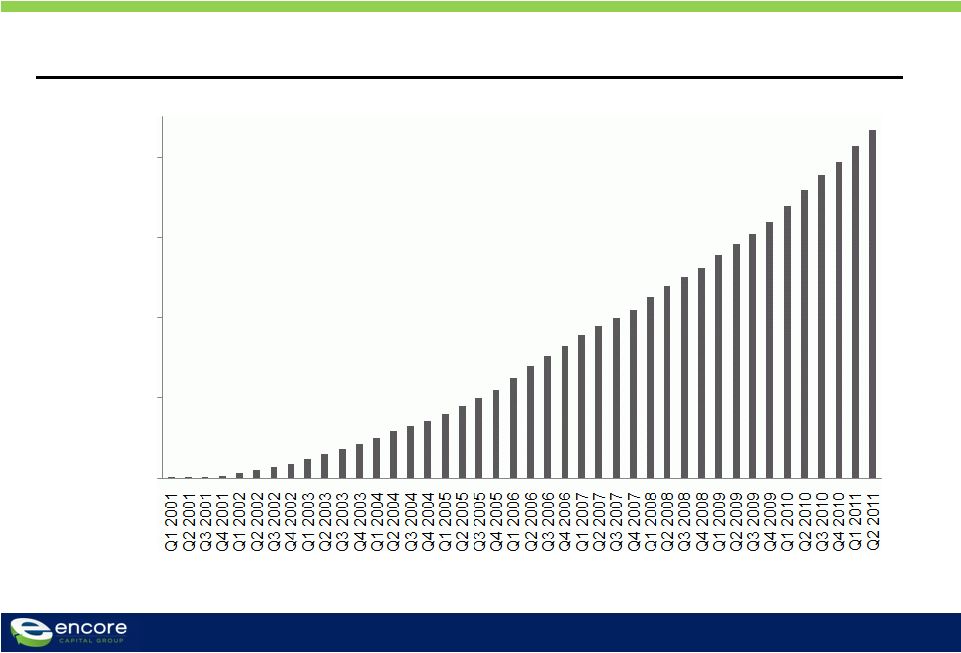

OUR

LONG-TERM MODEL HAS ALLOWED MORE THAN TWO MILLION CONSUMERS TO MOVE

TOWARD FINANCIAL RECOVERY 16

Consumers with whom we have partnered to retire their debt (cumulative)

-

500,000

1,000,000

1,500,000

2,000,000 |

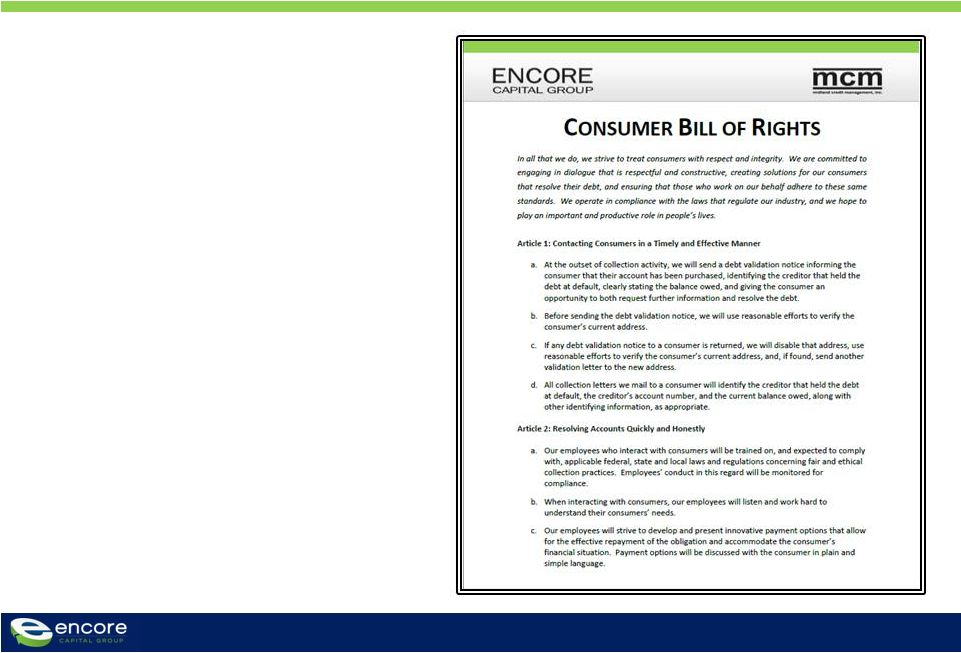

WE

HAVE TAKEN A LEADERSHIP STANCE BY OUTLINING OUR CORE PRINCIPLES IN AN

INDUSTRY-FIRST CONSUMER BILL OF RIGHTS 17

•

Clearly states what our consumers

should expect during the collection

process

•

Gives consumers concrete

assurances about our conduct

–

No interest once payments

are established, if maintained

–

No systematic messages left

–

Cessation of collections

under certain circumstances

•

Positions Encore as a company that

governmental entities should

consult with prior to enacting

regulations that impact the industry |

WE

BELIEVE LONG-TERM PROFITABILITY IN THIS INDUSTRY WILL BE DRIVEN BY

EXCELLENCE IN THREE KEY AREAS 18

Consumer-

level

underwriting

Superior

collection

approach

Low-cost

collection

platform |

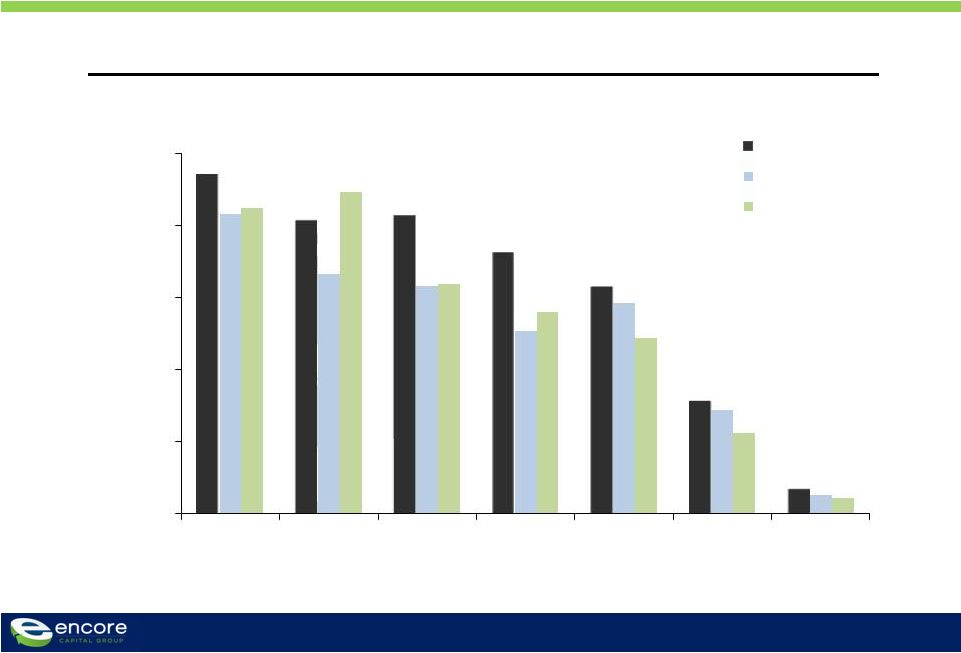

OUR

STRONG PORTFOLIO PURCHASING TRACK RECORD IS DRIVEN BY AN UNDERWRITING MODEL

FOCUSED ON INDIVIDUAL CONSUMERS 19

Deal Accuracy Since 2000

915

Total purchase

transactions

866

Total

profitable

deals

(39)

Principal not

fully recovered

(Count based on actual results plus forecast)

Principal recovered,

but not all servicing

costs

(10)

Since 2000, 95%

of our portfolio

purchases have

been profitable |

PURCHASING ACCURACY AND OUR ANALYTIC OPERATING MODEL

HAVE LED US TO CONSISTENTLY OUTPERFORM OUR PEERS

20

Cumulative Actual Collection Multiples by Vintage Year as of June 30, 2011

(Total Collections / Purchase Price)

Source: SEC Filings, Encore Capital Group Inc.

0.00x

0.50x

1.00x

1.50x

2.00x

2.50x

2005

2006

2007

2008

2009

2010

2011

ECPG

Peer 1

Peer 2 |

WE ARE

IN THE PROCESS OF BUILDING UPON OUR PRIOR SUCCESSES WITH POWERFUL STRATEGIC

INITIATIVES 21

Drive a meaningful portion of our legal

collections through internal resources

1.

Diversify our legal

platform

Create a world class near-shore facility

2.

Capture incremental

value through

increased offshore

activities

Collaborate with accomplished academics to

extend our deep consumer knowledge

3.

Develop new insights

about our consumers |

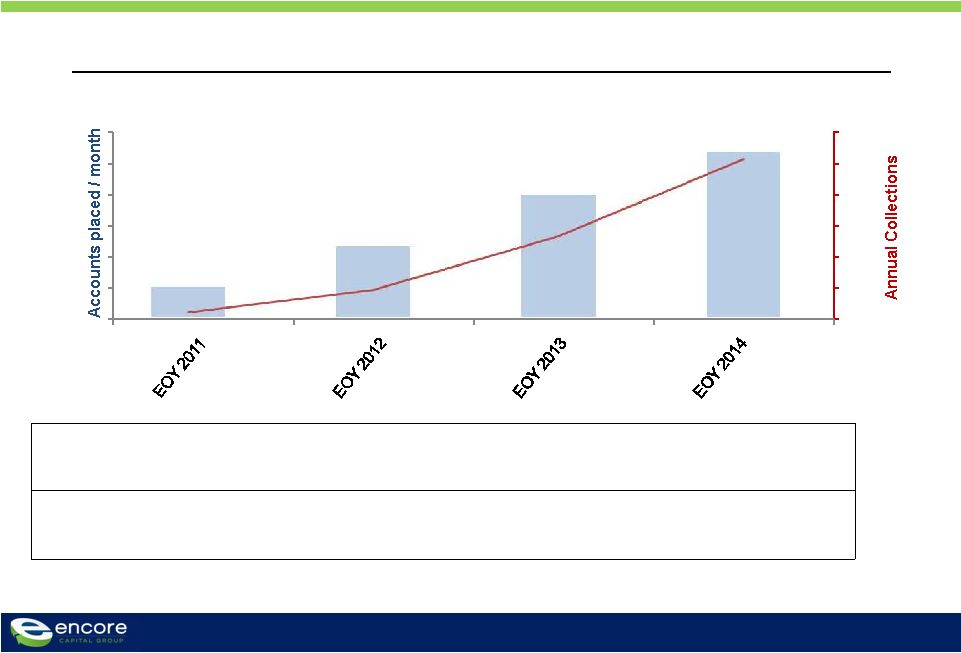

IT

WILL TAKE SOME TIME BEFORE THE INSOURCING OF LEGAL CONTRIBUTES TO THE BOTTOM

LINE 22

Number of

states

5

10

17

27

EoY

headcount

120-140

225-250

350-375

450-500

Placements, Collections

(#, $ millions)

$3

$18

$54

$104

$0

$20

$40

$60

$80

$100

$120 |

23

Spanish Account Inventory

(000s)

WE ARE ALSO ADDRESSING OUR GROWING POPULATION OF

SPANISH-SPEAKING CONSUMERS

Our presence in San

Diego and Phoenix

provides us with a

natural hiring pool, but

hiring cannot keep pace

with inventory growth

US-based Spanish

servicing is challenging

because of labor

availability and cost

520

661

845

950

1,100

0

200

400

600

800

1,000

1,200

H2 '09

H1 '10

H2 '10

H1 '11

H2 11 (E) |

FINALLY, WE ARE CREATING A CENTER OF EXCELLENCE DEDICATED

TO UNDERSTANDING FINANCIALLY DISTRESSED CONSUMERS

24

A new demographic

segment has emerged

It has unique features, is

growing, and has needs that

are only marginally served

by existing business models

Unique consumer

demographics

Focus on broader

population confounds

efforts to understand

and respond to new

population

Confusing policy

environment

Consumer decisions are

poorly understood, many

voices confuse the

issues, and discussions

often substitute

anecdotes for data

Accelerating industry

maturation

Leading companies now

capable of making

investments in R&D and

integrating their discoveries

Clear educational

opportunities

Strengthen personal finance,

planning, and credit skills

through focused outreach

and expert instruction |

SUMMARY

25

•

Investments made over the past few years have driven

significant improvements in collections, cash flow and earnings

•

Difficult regulatory environment being managed proactively

•

Expanding presence in India, combined with new strategic

initiatives, are expected to continue increasing cash flow from

operations

•

Demonstrated ability to raise and profitably deploy capital in

favorable and unfavorable business cycles |

APPENDIX |

APPENDIX A: CUMULATIVE COLLECTIONS BY PORTFOLIO VINTAGE

27

Cumulative Collections through June 30, 2011 (000’s)

Year

of

Purchase

Purchase

Price

<2005

2005

2006

2007

2008

2009

2010

2011

Total

CCM

<2005

$385,478

$749,791

$224,620

$164,211

$85,333

$45,893

$27,708

$19,986

$8,479

$1,326,021

3.4

2005

192,585

66,491

129,809

109,078

67,346

42,387

27,210

10,633

452,954

2.4

2006

141,028

42,354

92,265

70,743

44,553

26,201

10,367

286,483

2.0

2007

204,106

68,048

145,272

111,117

70,572

25,631

420,640

2.1

2008

227,872

69,049

165,164

127,799

50,634

412,646

1.8

2009

253,414

96,529

206,773

93,905

397,207

1.6

2010

359,305

125,853

156,051

281,904

0.8

2011

183,853

30,368

30,368

0.2

Total

$1,947,641

$749,791

$291,111

$336,374

$354,724

$398,303

$487,458

$604,394

$386,068

$3,608,223

1.9 |

APPENDIX B: RECONCILIATION OF ADJUSTED EBITDA

28

Reconciliation of Adjusted EBITDA to GAAP Net Income

(Unaudited, In Thousands)

Three Months Ended

Note: The

periods

3/31/07

through

12/31/08

have

been

adjusted

to

reflect

the

retrospective

application

of

ASC

470-20

3/31/07

6/30/07

9/30/07

12/31/07

3/31/08

6/30/08

9/30/08

12/31/08

3/31/09

6/30/09

9/30/09

12/31/09

3/31/10

6/30/10

9/30/10

12/31/10

3/31/11

6/30/11

GAAP net income, as reported

4,991

(1,515)

4,568

4,187

6,751

6,162

3,028

(2,095)

8,997

6,641

9,004

8,405

10,861

11,730

12,290

14,171

13,679

14,775

Interest expense

4,042

4,506

4,840

5,260

5,200

4,831

5,140

5,401

4,273

3,958

3,970

3,959

4,538

4,880

4,928

5,003

5,593

5,369

Contingent interest expense

3,235

888

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Pay-off of future contingent interest

-

11,733

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Provision for income taxes

3,437

(1,031)

1,315

2,777

4,509

4,225

2,408

(1,442)

5,973

4,166

5,948

4,609

6,490

6,749

6,632

9,075

8,601

9,486

Depreciation and amortization

869

840

833

810

722

766

674

652

623

620

652

697

673

752

816

958

1,053

1,105

Amount applied to principal on receivable portfolio

28,259

29,452

26,114

29,498

40,212

35,785

35,140

46,364

42,851

48,303

49,188

47,384

58,265

64,901

63,507

53,427

85,709

83,939

Stock-based compensation expense

801

1,204

1,281

1,001

1,094

1,228

860

382

1,080

994

1,261

1,049

1,761

1,446

1,549

1,254

1,765

1,810

Adjusted EBITDA

45,634

46,077

38,951

43,533

58,488

52,997

47,250

49,262

63,797

64,682

70,023

66,103

82,588

90,458

89,722

83,888

116,400

116,484

|