Attached files

| file | filename |

|---|---|

| 8-K - FORM8K - DYCOM INDUSTRIES INC | form8k.htm |

Exhibit 99-1

D.A. Davidson

10th Annual Engineering &

Construction Conference

September 20-21, 2011

10th Annual Engineering &

Construction Conference

September 20-21, 2011

1

Forward-Looking Statements and Non-GAAP

Information

Information

Forward-Looking Statements and

Non-GAAP Information

This presentation contains “forward-looking statements” which are statements relating to future events, future

financial performance, strategies, expectations, and competitive environment. All statements, other than

statements of historical facts, contained in this presentation, including statements regarding our future financial

position, future revenue, prospects, plans and objectives of management, are forward-looking statements.

Words such as “believe,” “expect,” “anticipate,” “estimate,” “intend,” “forecast,” “may,” “should,” “could,” “project,”

“looking ahead” and similar expressions, as well as statements in future tense, identify forward-looking

statements. You should not read forward-looking statements as a guarantee of future performance or results.

They will not necessarily be accurate indications of whether or at what time such performance or results will be

achieved. Forward-looking statements are based on information available at the time those statements are

made and/or management’s good faith belief at that time with respect to future events. Such statements are

subject to risks and uncertainties that could cause actual performance or results to differ materially from those

expressed in or suggested by the forward-looking statements. Important factors that could cause such

differences include, but are not limited to factors described under Item 1A, “Risk Factors” of the Company’s

Annual Report on Form 10-K for the year ended July 30, 2011, and other risks outlined in the Company’s

periodic filings with the Securities and Exchange Commission (“SEC”). The forward-looking statements in this

presentation are expressly qualified in their entirety by this cautionary statement. Except as required by law, the

Company may not update forward-looking statements even though its situation may change in the future.

financial performance, strategies, expectations, and competitive environment. All statements, other than

statements of historical facts, contained in this presentation, including statements regarding our future financial

position, future revenue, prospects, plans and objectives of management, are forward-looking statements.

Words such as “believe,” “expect,” “anticipate,” “estimate,” “intend,” “forecast,” “may,” “should,” “could,” “project,”

“looking ahead” and similar expressions, as well as statements in future tense, identify forward-looking

statements. You should not read forward-looking statements as a guarantee of future performance or results.

They will not necessarily be accurate indications of whether or at what time such performance or results will be

achieved. Forward-looking statements are based on information available at the time those statements are

made and/or management’s good faith belief at that time with respect to future events. Such statements are

subject to risks and uncertainties that could cause actual performance or results to differ materially from those

expressed in or suggested by the forward-looking statements. Important factors that could cause such

differences include, but are not limited to factors described under Item 1A, “Risk Factors” of the Company’s

Annual Report on Form 10-K for the year ended July 30, 2011, and other risks outlined in the Company’s

periodic filings with the Securities and Exchange Commission (“SEC”). The forward-looking statements in this

presentation are expressly qualified in their entirety by this cautionary statement. Except as required by law, the

Company may not update forward-looking statements even though its situation may change in the future.

This presentation includes certain “Non-GAAP” financial measures as defined by SEC rules. We believe that the

presentation of certain Non-GAAP financial measures provides information that is useful to investors because it

allows for a more direct comparison of our performance for the period with our performance in the comparable

prior-year periods. As required by the SEC, we have provided a reconciliation of those measures to the most

directly comparable GAAP measures on the Regulation G slides included at the end of this presentation. We

caution that Non-GAAP financial measures should be considered in addition to, but not as a substitute for, our

reported GAAP results.

presentation of certain Non-GAAP financial measures provides information that is useful to investors because it

allows for a more direct comparison of our performance for the period with our performance in the comparable

prior-year periods. As required by the SEC, we have provided a reconciliation of those measures to the most

directly comparable GAAP measures on the Regulation G slides included at the end of this presentation. We

caution that Non-GAAP financial measures should be considered in addition to, but not as a substitute for, our

reported GAAP results.

2

Positioned for strong equity returns

n A leading supplier of specialty contracting services to

telecommunication providers nationwide

telecommunication providers nationwide

n Telecommunications networks fundamental to economic progress

n End market opportunities driving organic growth, margin expansion

and increased earnings potential

and increased earnings potential

Ø Wireless backhaul

Ø Rural fiber networks

Ø Fiber deployments to businesses

Ø Wireless network upgrades

Ø FTTx deployments

n Capital allocation strategy designed to produce strong equity returns

3

Nationwide Footprint and Significant

Resources

Resources

n Headquartered in Palm Beach Gardens, Florida

n Nationwide footprint

} Operates in 48 states and in Canada

} 31 operating subsidiaries and hundreds of field offices

n Fiscal 2011 revenues of $1.036 billion grew organically 3.5% year over year, and

over 10% growth in Q4-11, including storm work of approximately $14 million

over 10% growth in Q4-11, including storm work of approximately $14 million

n Strong financial profile

} Cash and equivalents $44.8 million at July 30, 2011

} Availability on revolving credit agreement of $156.9 million at July 30, 2011

} 7.125% Senior Subordinated Notes due 2021

n Over 8,300 employees

Note: See “Regulation G Disclosure” slides for a reconciliation of GAAP to Non-GAAP financial measures.

4

Services Crucial to Customer Success

Engineering

Underground Facility Locating

Outside Plant & Equipment Installation

Premise Equipment Installation

Wireless Services

5

Contract Revenue $303.7 million

Quarter Ended July 30, 2011

6

Strong Secular Trend

Sources: U.S. Telecom, The Broadband Association

Cisco Visual Networking Index

U.S. National Bureau of Economic Analysis

“When the stability of an entire economy depends on the speed, intelligence, quality

of service, robustness and security of its Internet backbone, will a just good network

be good enough?”

of service, robustness and security of its Internet backbone, will a just good network

be good enough?”

John Chambers, Chairman and CEO, Cisco, Inc. - May 2011

7

Key Driver: Wireless Backhaul

“The returns associated with cell backhaul are very attractive, and they’re very

attractive with a single tenant. As you can imagine, once you have that fat pipe up to

that tower, there are multiple tenants that you can upsell to.”

attractive with a single tenant. As you can imagine, once you have that fat pipe up to

that tower, there are multiple tenants that you can upsell to.”

Mike Lovett, President and CEO, Charter Communications, Inc. - May 2011

•Very attractive returns to our customers

•Telephone, cable and other companies aggressively deploying fiber to

provide wireless backhaul services

provide wireless backhaul services

•Continues to provide significant growth opportunities

8

Key Driver: Rural Fiber Networks

The American Recovery and Reinvestment Act

(ARRA) provided the Department of Commerce’s

National Telecommunications and Information

Administration (NTIA) and the U.S. Department of

Agriculture’s Rural Utilities Service (RUS) with

$7.2 billion to expand broadband services in the

United States.

(ARRA) provided the Department of Commerce’s

National Telecommunications and Information

Administration (NTIA) and the U.S. Department of

Agriculture’s Rural Utilities Service (RUS) with

$7.2 billion to expand broadband services in the

United States.

Cumulatively, total Federal expenditures have now exceeded $280 million

(approximately seven percent of the total [NTIA] funds awarded) and have

been matched by recipient funds of more than $130 million.

(approximately seven percent of the total [NTIA] funds awarded) and have

been matched by recipient funds of more than $130 million.

NTIA BTOP Quarterly Program Status Report - June 2011

•Demand has absorbed significant industry capacity

•Dycom currently working on dozens of projects in eighteen states

•Meaningfully increased exposure to rural service providers

9

Key Driver: Fiber to Businesses

Addressable Business Services Market

$53.5 Billion

•Emerging as an industry battleground

•Multi-year cap-ex trajectory provides visible revenue opportunities

•Leverages Dycom’s existing cable engineering and construction resources

The small and medium business market reachable by every U.S. cable

company is $50 to $70 billion.

company is $50 to $70 billion.

Craig Moffett, Analyst, Sanford C. Bernstein & Co. - September 2010

Sources: Company Filings

Company Transcripts

10

Key Driver: Wireless Network Upgrades

“I would tell you that the range that we have for wireless CapEx - and really for the Company

as a whole -- is sort of in this mid-teens as a percentage of revenue. And with the technology

curves that we have coming in our business, I don't think you're going to be way below that or

whatever at any point in time.”

Pete Ritcher, SVP and CFO of Mobility and Consumer Markets, AT&T, Inc. - August 2011

•Wireless network spending increasing faster than overall spending

•Dycom entered wireless market via NeoCom acquisition in December 2010

•Strong growth opportunities as industry migrates from 3G to 4G technologies

Sources: CTIA

Collins Stewart, LLC

11

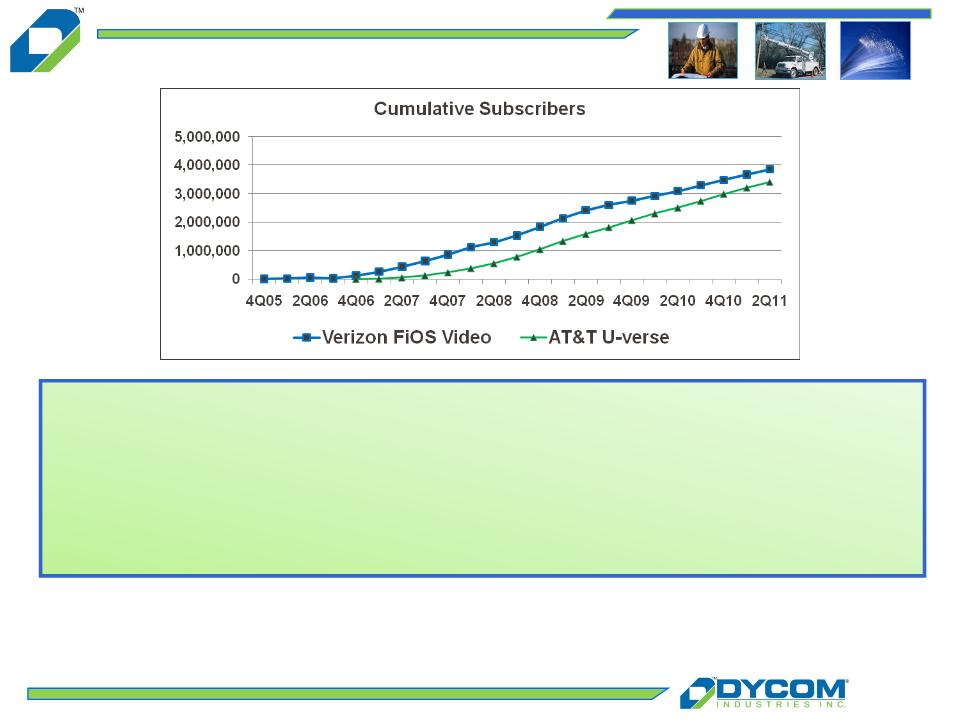

Key Driver: FTTx Deployments

“…we’ll continue to push fiber closer to the customers. Yes, we’re using the fiber to the tower

build to try to shorten the loops and get fiber to nodes at the same time, so that when you open

the trench once and take fiber out to the tower, you’re also trying to get some of the adjacent

areas as well. And I think just by being real smart with the capital and really continuing to push

fiber deeper and deeper into the network, you know, we’ll be successful over time competing

build to try to shorten the loops and get fiber to nodes at the same time, so that when you open

the trench once and take fiber out to the tower, you’re also trying to get some of the adjacent

areas as well. And I think just by being real smart with the capital and really continuing to push

fiber deeper and deeper into the network, you know, we’ll be successful over time competing

and delivering the speeds that our customers require.”

Stewart Ewing, EVP and CFO, CenturyLink, Inc. - August 2011

•A key competitive response by telephone companies to cable MSO’s

•CenturyLink, Dycom’s 3rd largest customer, just beginning scale deployments

•Dycom is leveraging prior, extensive FTTx experience with Verizon and AT&T

Sources: Company Filings

12

Why Dycom?

n Established customer relationships and reputation

n Broad geographic coverage

n Scale to satisfy customer time and service requirements

n Access to capital

n Responsive, local business units

13

Subsidiaries

Dycom’s Nationwide Presence

Local Credibility, National Capability

14

Focused on High Value Profitable Growth

n Positioned in front of emerging technology trends

which drive capital spending

which drive capital spending

n Deliberately targeting high quality, long-term industry

leaders which generate the vast majority of the

industry’s profitable opportunities

leaders which generate the vast majority of the

industry’s profitable opportunities

n Selectively acquiring businesses which complement

our existing footprint and enhance our customer

relationships

our existing footprint and enhance our customer

relationships

n Leveraging our scale and expertise to expand margins

through best practices

through best practices

15

Blue-chip, predominantly investment grade clients comprise the vast majority of revenue

Well Established Customers

Fiscal Year Ended July 30, 2011

Customer Revenue Breakdown

Comcast

AT&T

CenturyLink

Verizon

Windstream

Cablevision

Charter

Xcel Energy

Time Warner

Cable

Other

Duke Energy

16

Durable Customer Relationships

For comparison purposes, when customers have been combined through acquisition or merger, their revenues have been combined for all periods.

17

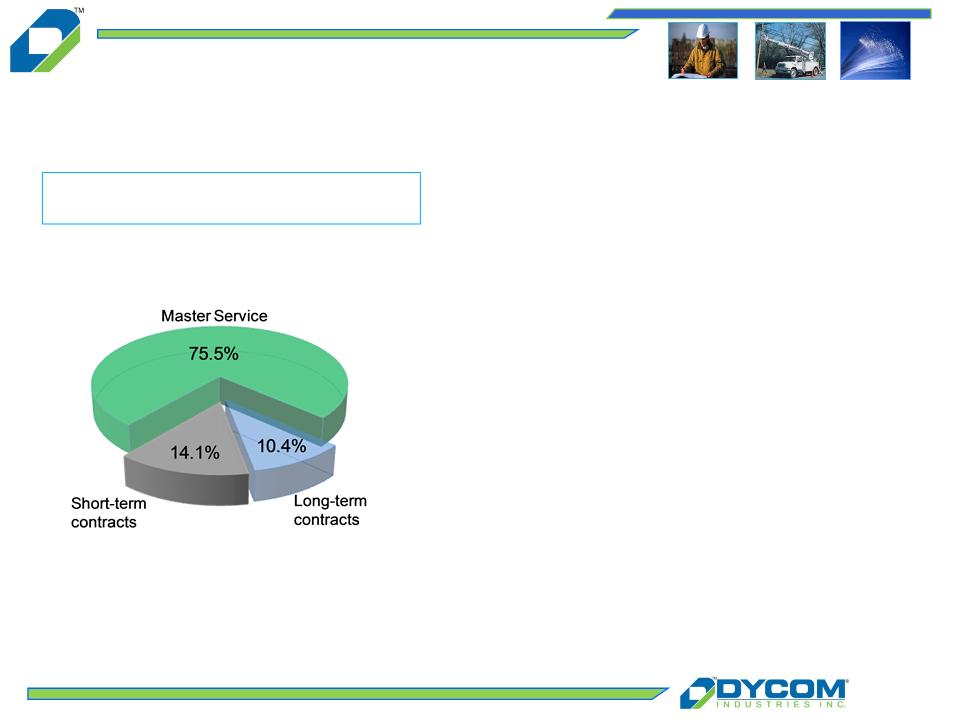

n Master Service Agreements (MSA’s)

} Multi-year, multi-million dollar

arrangements covering thousands of

individual work orders

arrangements covering thousands of

individual work orders

} Generally exclusive requirement

contracts

contracts

n Long-term contracts relate to specific

projects with terms in excess of one year from

the contract date

projects with terms in excess of one year from

the contract date

n As of July 30, 2011, Dycom was party to

approximately 200 MSA’s and other

arrangements with customers that extend

for periods of one or more years

for periods of one or more years

n Short-term contracts relate to spot market

requirements

requirements

n Significant majority of contracts are based on

units of delivery

units of delivery

Revenue By Contract Type

Fiscal Year Ended July 30, 2011

Fiscal Year Ended July 30, 2011

Anchored by Long-Term Agreements

18

Robust Cash Flow - Investing for Growth

$842 million

Cash flow from operations

Cash flow from operations

$184 million

provided by other financing and investing activities and beginning cash on hand

$349 million

Business

acquisitions

Business

acquisitions

$393 million

Capital

expenditures,

net

expenditures,

net

$284 million

Share

repurchases

Share

repurchases

Cumulative Cash Flows Fiscal 2002 - Fiscal 2011

Note: Amounts hereon represent cumulative cash flow amounts for fiscal 2002 - fiscal 2011;

See “Regulation G Disclosure” a summary of amounts.

See “Regulation G Disclosure” a summary of amounts.

19

Capital Allocated to Maximize

Shareholder Returns

Shareholder Returns

n Organic growth, robust free cash flow and renewed confidence in

industry outlook promotes capital allocation strategy to further

expand shareholder returns

industry outlook promotes capital allocation strategy to further

expand shareholder returns

n Acquisitions of NeoCom Solutions and Communication Services in

FY 2011 supplement organic growth and contribute to equity returns

FY 2011 supplement organic growth and contribute to equity returns

n Share repurchases of 13.9% of outstanding shares in fiscal 2011

creates incremental shareholder value and reduces equity claims on

future earnings

creates incremental shareholder value and reduces equity claims on

future earnings

Financial Update

21

nOrganic revenue growth trends improving

nMargins and earnings are expanding

nStrong balance sheet

nSolid cash flows and liquidity

nCapital structure designed to produce strong equity returns

Financial Overview

22

Organic Growth Returning

n Organic revenue growth has

increased since Q1-2010 reflecting

improved operating environment

and new contract awards

increased since Q1-2010 reflecting

improved operating environment

and new contract awards

n Organic growth accelerated in the

second half of FY 2011

second half of FY 2011

n NeoCom Solutions and

Communication Services

contributed aggregate revenues of

$33.8 million in FY 2011

Communication Services

contributed aggregate revenues of

$33.8 million in FY 2011

Note: See “Regulation G Disclosure” slides for a reconciliation of GAAP to Non-GAAP financial measures.

(a)Fiscal 2010 includes an incremental week as the result of our 52/53 week fiscal year.

(b)Quarterly organic revenue percentage excludes storm restoration services, revenues from acquired businesses

and is adjusted for the additional week in Q4-10 as a result of our 52/53 week fiscal year.

and is adjusted for the additional week in Q4-10 as a result of our 52/53 week fiscal year.

23

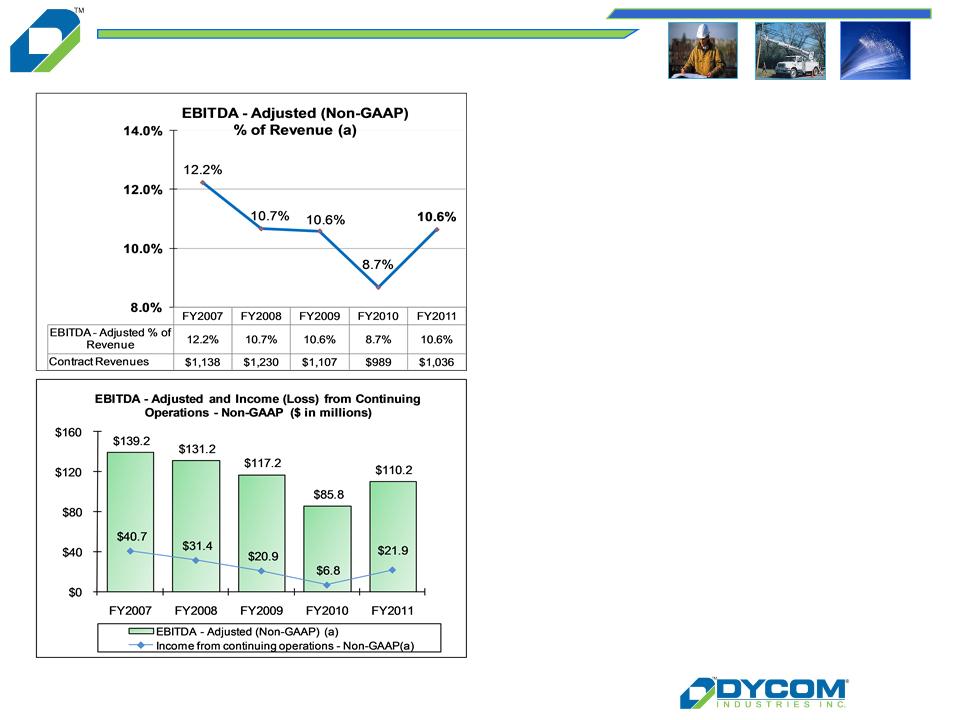

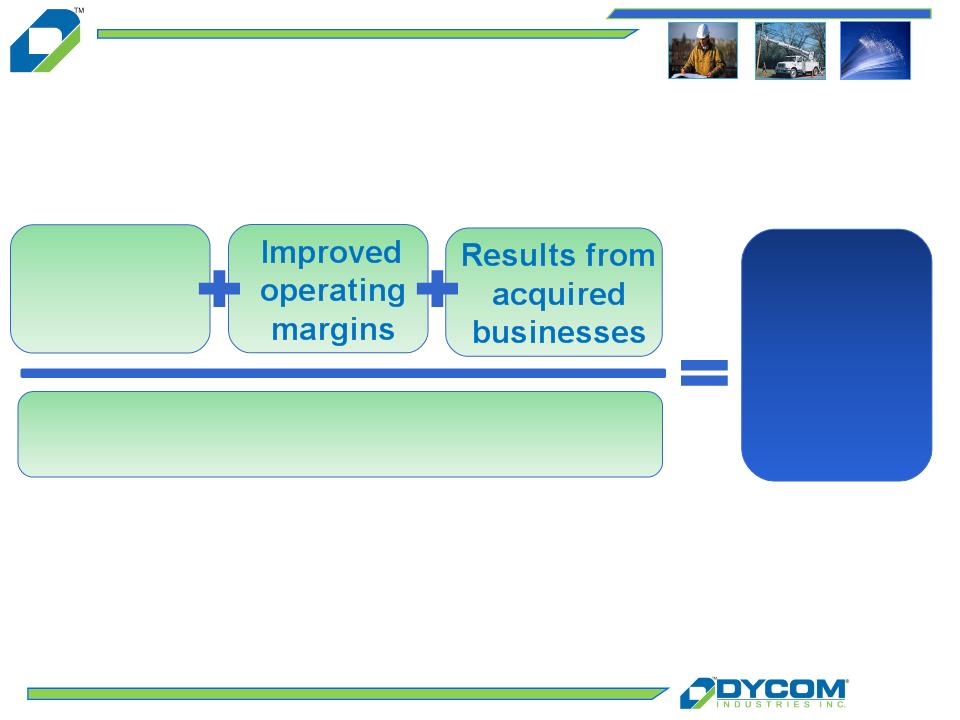

Margins and Earnings Expanding

n FY 2011 EBITDA -Adjusted

grew, driven by higher

revenues and improved cost

structure

grew, driven by higher

revenues and improved cost

structure

n Margins and earnings grew

at a higher rate than

revenue growth

at a higher rate than

revenue growth

Note: See “Regulation G Disclosure” slides for a reconciliation of GAAP to Non-GAAP financial measures.

(a)The amounts and percentages for EBITDA - Adjusted and amounts for Income from continuing operations -Non-

GAAP are Non-GAAP financial measures adjusted to exclude certain items.

GAAP are Non-GAAP financial measures adjusted to exclude certain items.

24

Accelerating through Q3 and Q4

n Growth in EBITDA-Adjusted %

expanded during FY 2011 and

improved each quarterly period

expanded during FY 2011 and

improved each quarterly period

n EBITDA -Adjusted growth

contributes to bottom line

expansion

contributes to bottom line

expansion

n Net income of $13.0 million,$0.38

per share in Q4-2011, represents

highest quarterly earnings per

share since the October 2000

quarter

per share in Q4-2011, represents

highest quarterly earnings per

share since the October 2000

quarter

Note: See “Regulation G Disclosure” slides for a reconciliation of GAAP to Non-GAAP financial measures.

(a)The amounts and percentages for EBITDA - Adjusted and amounts for Income from continuing operations -Non-

GAAP are Non-GAAP financial measures adjusted to exclude certain items.

GAAP are Non-GAAP financial measures adjusted to exclude certain items.

25

Strong Balance Sheet, Solid Cash Flow

n Financial profile positioned to address

emerging industry opportunities

emerging industry opportunities

} Fiscal 2021 maturity of Senior

Subordinated Notes

Subordinated Notes

} Net debt to EBITDA-Adjusted of 1.3x

suitable for growth (a)

suitable for growth (a)

} Increasing availability on Senior Credit

Agreement

Agreement

n Solid operating cash flows

Note: See “Regulation G Disclosure” slides for a reconciliation of GAAP to Non-GAAP financial measures.

(a)The ratio of Net debt to EBITDA-Adjusted is a Non-GAAP financial measure adjusted to exclude certain items.

(b)Capital expenditures are presented net of proceeds from the sale of assets.

26

Strategy for Success

Organic

Growth

Growth

Lower Share Count

Higher

Equity

Returns

Equity

Returns

Supplemental schedules

Regulation G Disclosures

28

Regulation G Disclosure

29

30

Regulation G Disclosure

The below table presents the Non-GAAP financial measures of EBITDA and Adjusted EBITDA for the respective periods. EBITDA and Adjusted EBITDA are Non-GAAP financial measures within the meaning of Regulation G

promulgated by the Securities and Exchange Commission. The Company defines EBITDA as earnings before interest, taxes, depreciation and amortization, and defines Adjusted EBITDA as earnings before interest, taxes,

depreciation and amortization, gain on sale of fixed assets, stock-based compensation expense and Adjusting items. The Company believes these Non-GAAP financial measures provide information that is useful to the Company’s

investors. The Company believes that this information is helpful in understanding period-over-period operating results separate and apart from items that may, or could, have a disproportionate positive or negative impact on the

Company’s results of operations in any particular period. Additionally, the Company uses these Non-GAAP financial measures to evaluate its past performance and prospects for future performance. EBITDA and Adjusted EBITDA

are not recognized terms under GAAP and do not purport to be an alternative to net income, operating cash flows, or a measure of earnings. Because all companies do not use identical calculations, this presentation of Non-GAAP

financial measures may not be comparable to other similarly titled measures of other companies. These tables present a reconciliation of EBITDA and Adjusted EBITDA to the most directly comparable GAAP measure.

promulgated by the Securities and Exchange Commission. The Company defines EBITDA as earnings before interest, taxes, depreciation and amortization, and defines Adjusted EBITDA as earnings before interest, taxes,

depreciation and amortization, gain on sale of fixed assets, stock-based compensation expense and Adjusting items. The Company believes these Non-GAAP financial measures provide information that is useful to the Company’s

investors. The Company believes that this information is helpful in understanding period-over-period operating results separate and apart from items that may, or could, have a disproportionate positive or negative impact on the

Company’s results of operations in any particular period. Additionally, the Company uses these Non-GAAP financial measures to evaluate its past performance and prospects for future performance. EBITDA and Adjusted EBITDA

are not recognized terms under GAAP and do not purport to be an alternative to net income, operating cash flows, or a measure of earnings. Because all companies do not use identical calculations, this presentation of Non-GAAP

financial measures may not be comparable to other similarly titled measures of other companies. These tables present a reconciliation of EBITDA and Adjusted EBITDA to the most directly comparable GAAP measure.

31

Regulation G Disclosure

The below table presents the Non-GAAP financial measures of EBITDA and Adjusted EBITDA for the respective periods. EBITDA and Adjusted EBITDA are Non-GAAP financial measures within the meaning of Regulation G

promulgated by the Securities and Exchange Commission. The Company defines EBITDA as earnings before interest, taxes, depreciation and amortization, and defines Adjusted EBITDA as earnings before interest, taxes,

depreciation and amortization, gain on sale of fixed assets, stock-based compensation expense and Adjusting items. The Company believes these Non-GAAP financial measures provide information that is useful to the Company’s

investors. The Company believes that this information is helpful in understanding period-over-period operating results separate and apart from items that may, or could, have a disproportionate positive or negative impact on the

Company’s results of operations in any particular period. Additionally, the Company uses these Non-GAAP financial measures to evaluate its past performance and prospects for future performance. EBITDA and Adjusted EBITDA

are not recognized terms under GAAP and do not purport to be an alternative to net income, operating cash flows, or a measure of earnings. Because all companies do not use identical calculations, this presentation of Non-GAAP

financial measures may not be comparable to other similarly titled measures of other companies. These tables present a reconciliation of EBITDA and Adjusted EBITDA to the most directly comparable GAAP measure.

promulgated by the Securities and Exchange Commission. The Company defines EBITDA as earnings before interest, taxes, depreciation and amortization, and defines Adjusted EBITDA as earnings before interest, taxes,

depreciation and amortization, gain on sale of fixed assets, stock-based compensation expense and Adjusting items. The Company believes these Non-GAAP financial measures provide information that is useful to the Company’s

investors. The Company believes that this information is helpful in understanding period-over-period operating results separate and apart from items that may, or could, have a disproportionate positive or negative impact on the

Company’s results of operations in any particular period. Additionally, the Company uses these Non-GAAP financial measures to evaluate its past performance and prospects for future performance. EBITDA and Adjusted EBITDA

are not recognized terms under GAAP and do not purport to be an alternative to net income, operating cash flows, or a measure of earnings. Because all companies do not use identical calculations, this presentation of Non-GAAP

financial measures may not be comparable to other similarly titled measures of other companies. These tables present a reconciliation of EBITDA and Adjusted EBITDA to the most directly comparable GAAP measure.

32

Regulation G Disclosure

33

Regulation G Disclosure

D.A. Davidson

10th Annual Engineering &

Construction Conference

September 20-21, 2011

10th Annual Engineering &

Construction Conference

September 20-21, 2011