Attached files

| file | filename |

|---|---|

| 8-K - PLUG POWER INC | esplugpower8k.htm |

| EX-99 - PLUG POWER INC | exhibit99-2.htm |

NASDAQ: PLUG

September 2011

The content of this presentation is PLUG POWER INC. PROPRIETARY AND CONFIDENTIAL. No part of this publication may be reproduced, stored in a retrieval

system, or transmitted in any form or by any means - electronic, mechanical, photocopying, recording or otherwise - without the permission of Plug Power Inc.

Copyright 2011 by Plug Power Inc.

Plug Power Inc. Safe Harbor Statement

This communication contains forward-looking statements within the meaning of the Private Securities Litigation

Reform Act of 1995, including but not limited to expectations regarding revenues and product orders and shipments

for 2011. These statements are based on current expectations that are subject to certain assumptions, risks and

uncertainties, any of which are difficult to predict, are beyond our control and that may cause our actual results to

differ materially from the expectations in our forward-looking statements including, but not limited to: the risk that we

continue to incur losses and might never achieve or maintain profitability, the risk that the additional capital we

expect we will need to raise to fund our operations beyond the first quarter of 2012 may not be available; our lack of

extensive experience in manufacturing and marketing products may impact our ability to manufacture and market

products on a profitable and large-scale commercial basis; the risk that unit orders will not ship, be installed and/or

converted to revenue, in whole or in part; the risk that pending orders may not convert to purchase orders, in whole

or in part; the risk that our continued failure to comply with NASDAQ’s listing standards may severely limit our ability

to raise additional capital; the cost and timing of developing, marketing and selling our products and our ability to

raise the necessary capital to fund such costs; the ability to achieve the forecasted gross margin on the sale of our

products; the actual net cash used for operating expenses may exceed the projected net cash for operating

expenses; the cost and availability of fuel and fueling infrastructures for our products; market acceptance of our

GenDrive systems; our ability to establish and maintain relationships with third parties with respect to product

development, manufacturing, distribution and servicing and the supply of key product components; the cost and

availability of components and parts for our products; our ability to develop commercially viable products; our ability

to reduce product and manufacturing costs; our ability to successfully expand our product lines; our ability to

improve system reliability for our GenDrive systems; competitive factors, such as price competition and competition

from other traditional and alternative energy companies; our ability to protect our intellectual property; the cost of

complying with current and future federal, state and international governmental regulations; and other risks and

uncertainties discussed under "Item IA-Risk Factors" in our annual report on Form 10-K for the fiscal year ended

December 31, 2010, filed with the Securities and Exchange Commission ("SEC") on March 31, 2011, and the

reports we file from time to time with the SEC. Plug Power does not intend to, and undertakes no duty to update

any forward-looking statements as a result of new information or future events.

2

Executive Summary

Plug Power is the marketshare leader in

alternative energy solutions for the Material

Handling market

First mover advantage - 85% market share

for fuel cell powered lift trucks

Proven value proposition with compelling

financial return

Customers include leading Fortune 500

Revenue guidance growth of 80-100% for

both 2011 and 2012

3

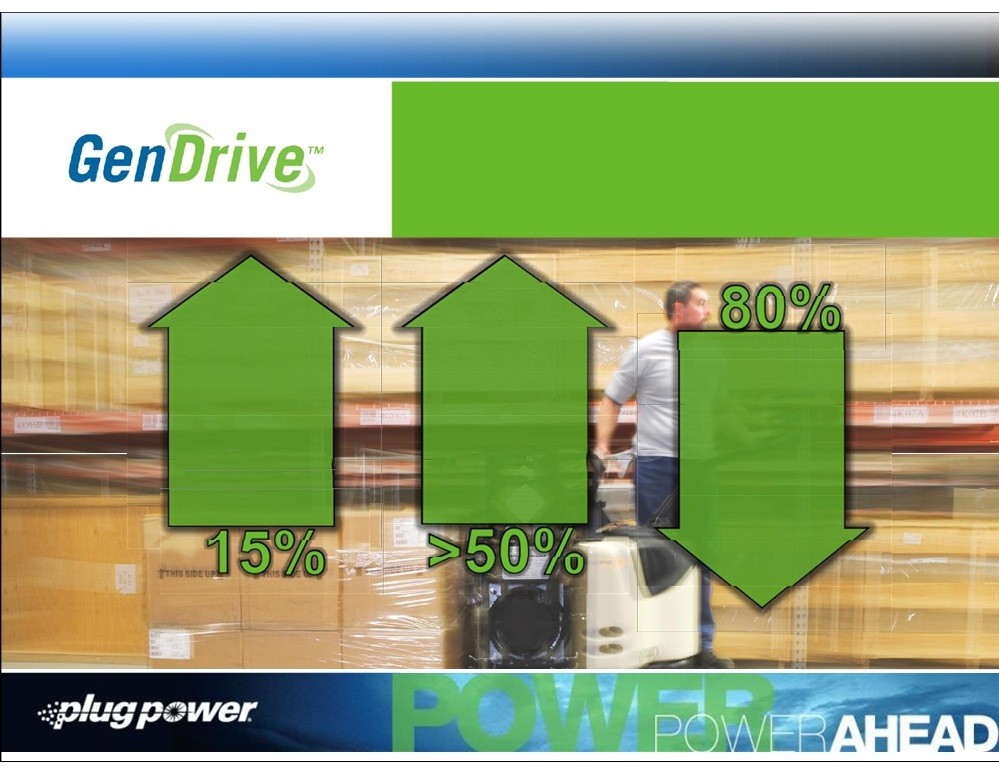

GenDrive

®

Value

Proposition

More Power.

More Productivity.

More of the Time.

Greenfield

IRR Payback

Reduce

Increase

< 1 yr

carbon

productivity

~$3M in

footprint up

up to 15%

savings*

to 80%

*Brownfield IRR >15% with payback <2 years; >$1M in savings typically

4

Global TAM for Class 1 – 5 Fuel Cell Powered Forklift Trucks

$19.9 Billion Market

Class 1

Class 2

Class 3

Sit-down Lift Trucks

Stand-up Reach Trucks

Rider Pallet Trucks

5

Customer Base is Building

6

Customer Success

3 sites on 100% hydrogen by end of Q3 2011 -

Houston, Front Royal and Philadelphia

Commitment for 5 additional sites - Boston,

Long Island, San Antonio, Los Angeles, and

Riverside

No battery infrastructure

Multi-distribution center commitment

Investigating opportunities for using fuel cells

with refrigerated trucks

Operates 100+ DCs with over 11,000 forklift

trucks

7

Customer Success

Three sites with over 300 forklift trucks powered

by Plug Power

Eliminated need to change out lead acid

batteries

Expected GHG reduction up to 72%, compared

to batteries charged from the grid

Negotiating future deals in North America

Operates 100+ DCs with close to 20,000 forklift

trucks; Future site expansion planned

8

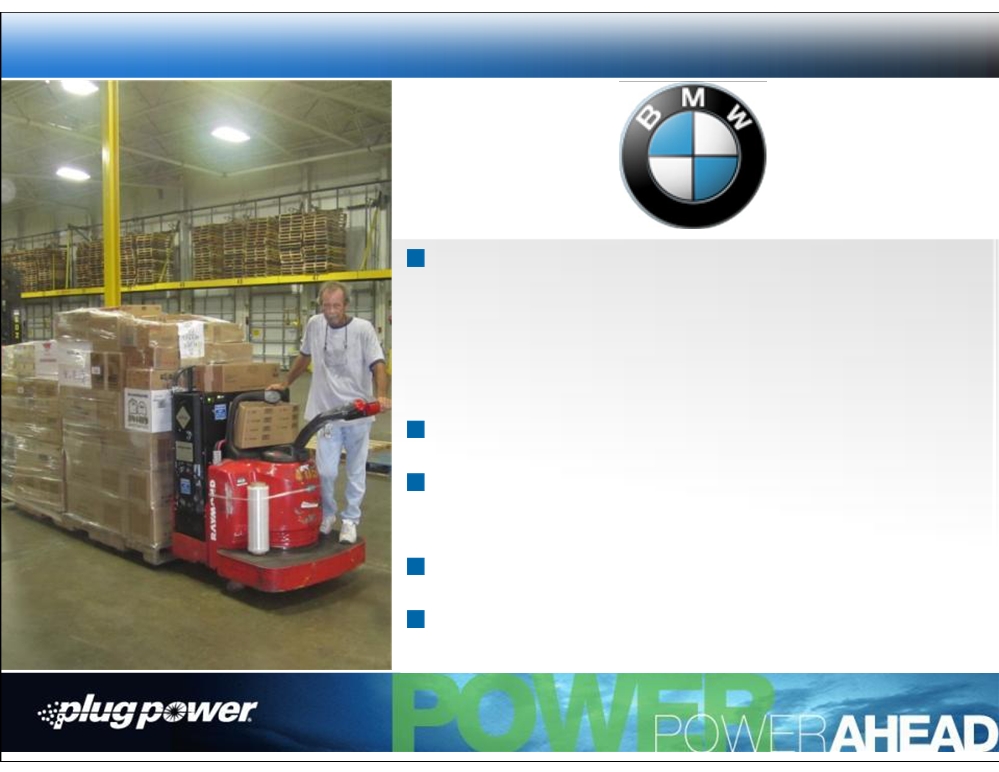

Customer Success

Site Success

•

Greer, South Carolina: 86 units

•

Mix of Class-1, -2 and -3

•

First BMW plant to use fuel cell-powered forklift

trucks

New facility built without battery infrastructure

Entire fleet deployed with GenDrive

®

fuel cell

power units

Affirming global commitment to sustainability

Adjacent 1.2M sq. ft. facility with 300+ trucks with

opportunity for conversion to fuel cells

9

Commercial Progress: Hydrogen Refueling and GenDrive

By End of 2011 (Projected):

~3,000 GenDrive units deployed

20,000-30,000 kg of Hydrogen dispensed weekly

1,200 GenDrive products deployed

6,000-10,000 refuelings each week

Over 95% of all NA refuelings are being done with

Plug Power products

10

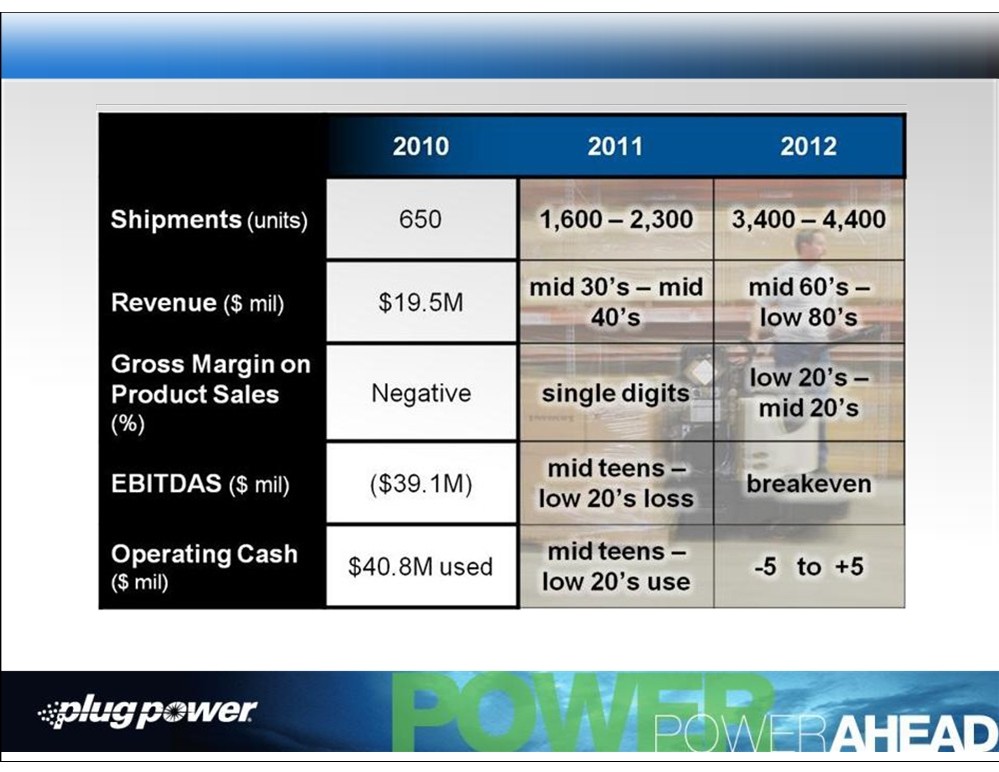

Financial Milestones

11

Gross Margin Improvement

2011 - Gross margin positive

2012 - Gross margin - 20% plus

Standardized

Improved

Reduction

componentry

leverage with

in materials

across

suppliers

product lines

12

Conclusion

First mover advantage - 85% marketshare

Global market of $19.9B

Revenue growth guidance 80-100% in 2011

and 2012

Tripled Product/Service revenue year over

year

Record 2010 and Q1 2011 orders with Q2

having largest backlog in company history

Expected profitability in 2012

30%+ gross margin potential

Significant decrease in operating expenses

from $58M to $16M

Compelling customer experience with

Fortune 500 client list

13