Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - RED METAL RESOURCES, LTD. | Financial_Report.xls |

| EX-32 - EXHIBIT 32 - RED METAL RESOURCES, LTD. | ex32.htm |

| EX-31.2 - EXHIBIT 31.2 - RED METAL RESOURCES, LTD. | ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - RED METAL RESOURCES, LTD. | ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

x

|

QUARTERLY REPORT UNDER SECTION 13 0R 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended: July 31, 2011

|

o

|

TRANSITION REPORT UNDER SECTION 13 0R 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from_______to_______

Commission file number 000-52055

|

RED METAL RESOURCES LTD.

|

|

(Exact name of small business issuer as specified in its charter)

|

|

Nevada

(State or other jurisdiction

of incorporation or organization)

|

20-2138504

(I.R.S. Employer

Identification No.)

|

|

195 Park Avenue, Thunder Bay Ontario, Canada P7B 1B9

(Address of principal executive offices) (Zip Code)

|

|

|

(807) 345-7384

(Issuer’s telephone number)

|

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filed,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

|

|

Non-accelerated filer

|

o

|

(Do not check if a smaller reporting company)

|

Smaller reporting company

|

x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). o Yes x No

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date. As of September 14, 2011 the number of shares of the registrant’s common stock outstanding was 16,939,634.

| PART I—FINANCIAL INFORMATION | 1 | |

|

ITEM

1. Financial Statements

|

1 | |

|

CONSOLIDATED BALANCE SHEETS

|

1 | |

|

CONSOLIDATED STATEMENTS OF OPERATIONS

|

2 | |

|

CONSOLIDATED

STATEMENT OF STOCKHOLDERS' EQUITY

|

3 | |

|

CONSOLIDATED

STATEMENTS OF CASH FLOWS

|

4 | |

|

ITEM

2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

10 | |

|

ITEM

3. Quantitative and Qualitative Disclosures about Market Risk

|

21 | |

|

ITEM 4. Controls and

Procedures.

|

21 | |

| PART II—OTHER INFORMATION | 21 | |

|

ITEM 1. Legal Proceedings

|

21 | |

|

ITEM 1A. Risk

Factors

|

22 | |

|

ITEM 2. Unregistered Sales of Equity Securities and Use of Proceeds

|

22 | |

|

ITEM 3. Defaults upon Senior Securities

|

22 | |

|

ITEM 4. (Removed and Reserved)

|

22 | |

|

ITEM 5. Other Information

|

22 | |

|

ITEM 6. Exhibits

|

22 |

PART I—FINANCIAL INFORMATION

Item 1. Financial Statements.

RED METAL RESOURCES LTD.

(AN EXPLORATION STAGE COMPANY)

CONSOLIDATED BALANCE SHEETS

(UNAUDITED)

|

July 31, 2011

|

January 31, 2011

|

|||||||

|

ASSETS

|

||||||||

|

Current assets

|

||||||||

|

Cash

|

$ | 480,368 | $ | 8,655 | ||||

|

Prepaids and other receivables

|

65,483 | 37,572 | ||||||

|

Total current assets

|

545,851 | 46,227 | ||||||

|

Fixed assets (net of amortization)

|

19,556 | - | ||||||

|

Unproved mineral properties

|

813,292 | 662,029 | ||||||

|

Total assets

|

$ | 1,378,699 | $ | 708,256 | ||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY (DEFICIT)

|

||||||||

|

Current liabilities

|

||||||||

|

Accounts payable

|

$ | 148,909 | $ | 196,657 | ||||

|

Accrued liabilities

|

86,017 | 91,990 | ||||||

|

Due to related parties

|

411,078 | 510,111 | ||||||

|

Notes payable to related party

|

65,867 | 113,648 | ||||||

|

Total liabilities

|

711,871 | 912,406 | ||||||

|

Stockholders' equity (deficit)

|

||||||||

|

Common stock, $0.001 par value, authorized 500,000,000, 16,939,634 and 10,216,301 issued and outstanding at July 31, 2011 and January 31, 2011

|

16,940 | 10,217 | ||||||

|

Additional paid in capital

|

4,864,676 | 2,913,300 | ||||||

|

Deficit accumulated during the exploration stage

|

(4,124,936 | ) | (3,056,819 | ) | ||||

|

Accumulated other comprehensive loss

|

(89,852 | ) | (70,848 | ) | ||||

|

Total stockholders' equity (deficit)

|

666,828 | (204,150 | ) | |||||

|

Total liabilities and stockholders' equity (deficit)

|

$ | 1,378,699 | $ | 708,256 | ||||

The accompanying notes are an integral part of these consolidated financial statements

1

RED METAL RESOURCES LTD.

(AN EXPLORATION STAGE COMPANY)

CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

|

Three months ended

|

Six months ended

|

From January 10,

|

||||||||||||||||||

|

July 31

|

July 31

|

2005 (Inception)

|

||||||||||||||||||

|

2011

|

2010

|

2011

|

2010

|

to July 31, 2011

|

||||||||||||||||

|

Revenue

|

||||||||||||||||||||

|

Royalties

|

$ | - | $ | - | $ | - | $ | - | $ | 15,658 | ||||||||||

|

Operating Expenses

|

||||||||||||||||||||

|

Administration

|

10,072 | 11,008 | 30,758 | 38,715 | 305,898 | |||||||||||||||

|

Advertising and promotion

|

60,559 | 17,338 | 101,086 | 57,609 | 426,196 | |||||||||||||||

|

Automobile

|

13,689 | 5,185 | 19,664 | 12,637 | 85,383 | |||||||||||||||

|

Bank charges

|

1,497 | (28 | ) | 4,133 | 1,786 | 20,745 | ||||||||||||||

|

Consulting fees

|

90,413 | 36,072 | 156,633 | 68,995 | 622,981 | |||||||||||||||

|

Interest on current debt

|

16,841 | 10,990 | 35,447 | 15,892 | 144,241 | |||||||||||||||

|

Mineral exploration costs

|

423,608 | 12,416 | 453,555 | 12,971 | 1,201,941 | |||||||||||||||

|

Office

|

11,978 | 898 | 15,315 | 3,227 | 42,621 | |||||||||||||||

|

Professional development

|

- | - | - | 4,008 | 5,116 | |||||||||||||||

|

Professional fees

|

58,351 | 15,387 | 106,256 | 52,517 | 574,535 | |||||||||||||||

|

Rent

|

3,498 | 3,107 | 6,954 | 6,233 | 48,643 | |||||||||||||||

|

Regulatory

|

7,400 | 6,925 | 15,398 | 11,440 | 64,044 | |||||||||||||||

|

Travel and entertainment

|

64,555 | 155 | 83,770 | 28,708 | 280,436 | |||||||||||||||

|

Salaries, wages and benefits

|

20,006 | - | 25,026 | 1,015 | 77,708 | |||||||||||||||

|

Foreign exchange loss

|

374 | (1,174 | ) | 11,213 | (623 | ) | 11,512 | |||||||||||||

|

Write-down of unproved mineral properties

|

- | - | 2,909 | - | 228,594 | |||||||||||||||

|

Total operating expenses

|

782,841 | 118,279 | 1,068,117 | 315,130 | 4,140,594 | |||||||||||||||

|

Net loss

|

$ | (782,841 | ) | $ | (118,279 | ) | $ | (1,068,117 | ) | $ | (315,130 | ) | $ | (4,124,936 | ) | |||||

|

Net loss per share - basic and diluted

|

$ | (0.05 | ) | $ | (0.01 | ) | $ | (0.07 | ) | $ | (0.03 | ) | ||||||||

|

Weighted average number of shares outstanding - basic and diluted

|

16,939,634 | 10,216,301 | 14,525,177 | 10,040,168 | ||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements

2

RED METAL RESOURCES LTD.

(AN EXPLORATION STAGE COMPANY)

CONSOLIDATED STATEMENT OF STOCKHOLDERS' EQUITY (DEFICIT)

FOR THE PERIOD FROM JANUARY 10, 2005 (INCEPTION) TO JULY 31, 2011

(UNAUDITED)

|

|

Common Stock Issued

|

|||||||||||||||||||||||

|

|

Number of

Shares |

Amount

|

Additional

Paid-in |

Accumulated

Deficit |

Accumulated

Other |

Total

|

||||||||||||||||||

|

Balance at January 10, 2005 (Inception)

|

- | $ | - | $ | - | $ | - | $ | - | $ | - | |||||||||||||

|

|

||||||||||||||||||||||||

|

Net loss

|

- | - | - | (825 | ) | - | (825 | ) | ||||||||||||||||

|

|

||||||||||||||||||||||||

|

Balance at January 31, 2005

|

- | - | - | (825 | ) | - | (825 | ) | ||||||||||||||||

|

|

||||||||||||||||||||||||

|

Common stock issued for cash

|

5,525,000 | 5,525 | 53,725 | - | - | 59,250 | ||||||||||||||||||

|

Common stock adjustment

|

45 | - | - | - | - | - | ||||||||||||||||||

|

Donated services

|

- | - | 3,000 | - | - | 3,000 | ||||||||||||||||||

|

Net loss

|

- | - | - | (12,363 | ) | - | (12,363 | ) | ||||||||||||||||

|

|

||||||||||||||||||||||||

|

Balance at January 31, 2006

|

5,525,045 | 5,525 | 56,725 | (13,188 | ) | - | 49,062 | |||||||||||||||||

|

|

||||||||||||||||||||||||

|

Donated services

|

- | - | 9,000 | - | - | 9,000 | ||||||||||||||||||

|

Net loss

|

- | - | - | (43,885 | ) | - | (43,885 | ) | ||||||||||||||||

|

|

||||||||||||||||||||||||

|

Balance at January 31, 2007

|

5,525,045 | 5,525 | 65,725 | (57,073 | ) | - | 14,177 | |||||||||||||||||

|

|

||||||||||||||||||||||||

|

Donated services

|

- | - | 2,250 | - | - | 2,250 | ||||||||||||||||||

|

Return of common stock to treasury

|

(1,750,000 | ) | (1,750 | ) | 1,749 | - | - | (1 | ) | |||||||||||||||

|

Common stock issued for cash

|

23,810 | 24 | 99,976 | - | - | 100,000 | ||||||||||||||||||

|

Net loss

|

- | - | - | (232,499 | ) | - | (232,499 | ) | ||||||||||||||||

|

|

||||||||||||||||||||||||

|

Balance at January 31, 2008

|

3,798,855 | 3,799 | 169,700 | (289,572 | ) | - | (116,073 | ) | ||||||||||||||||

|

|

||||||||||||||||||||||||

|

Common stock issued for cash

|

357,147 | 357 | 1,299,643 | - | - | 1,300,000 | ||||||||||||||||||

|

Net loss

|

- | - | - | (1,383,884 | ) | - | (1,383,884 | ) | ||||||||||||||||

|

Foreign currency exchange loss

|

- | - | - | - | (21,594 | ) | (21,594 | ) | ||||||||||||||||

|

Balance at January 31, 2009

|

4,156,002 | 4,156 | 1,469,343 | (1,673,456 | ) | (21,594 | ) | (221,551 | ) | |||||||||||||||

|

Common stock issued for cash

|

1,678,572 | 1,678 | 160,822 | - | - | 162,500 | ||||||||||||||||||

|

Common stock issued for debt

|

3,841,727 | 3,843 | 1,148,675 | - | - | 1,152,518 | ||||||||||||||||||

|

Net loss

|

- | - | - | (710,745 | ) | - | (710,745 | ) | ||||||||||||||||

|

Foreign currency exchange loss

|

- | - | - | - | (35,816 | ) | (35,816 | ) | ||||||||||||||||

|

|

||||||||||||||||||||||||

|

Balance at January 31, 2010

|

9,676,301 | 9,677 | 2,778,840 | (2,384,201 | ) | (57,410 | ) | 346,906 | ||||||||||||||||

|

Common stock issued for cash

|

540,000 | 540 | 134,460 | - | - | 135,000 | ||||||||||||||||||

|

Net loss for the six months ended July 31, 2010

|

- | - | - | (315,130 | ) | - | (315,130 | ) | ||||||||||||||||

|

Foreign currency exchange loss

|

- | - | - | - | (5,136 | ) | (5,136 | ) | ||||||||||||||||

|

Balance at July 31, 2010

|

10,216,301 | 10,217 | 2,913,300 | (2,699,331 | ) | (62,546 | ) | 161,640 | ||||||||||||||||

|

Common stock issued for cash

|

- | - | - | - | - | - | ||||||||||||||||||

|

Net loss

|

- | - | - | (357,488 | ) | - | (357,488 | ) | ||||||||||||||||

|

Foreign currency exchange loss

|

- | - | - | - | (8,302 | ) | (8,302 | ) | ||||||||||||||||

|

Balance at January 31, 2011

|

10,216,301 | 10,217 | 2,913,300 | (3,056,819 | ) | (70,848 | ) | (204,150 | ) | |||||||||||||||

|

Common stock issued for cash

|

6,290,000 | 6,290 | 1,821,809 | - | - | 1,828,099 | ||||||||||||||||||

|

Common stock issued for debt

|

433,333 | 433 | 129,567 | - | - | 130,000 | ||||||||||||||||||

|

Net loss for the six months ended July 31, 2011

|

- | - | - | (1,068,117 | ) | - | (1,068,117 | ) | ||||||||||||||||

|

Foreign currency exchange loss

|

- | - | - | - | (19,004 | ) | (19,004 | ) | ||||||||||||||||

|

Balance at July 31, 2011

|

16,939,634 | $ | 16,940 | $ | 4,864,676 | $ | (4,124,936 | ) | $ | (89,852 | ) | $ | 666,828 | |||||||||||

The accompanying notes are an integral part of these consolidated financial statements

3

RED METAL RESOURCES LTD.

(AN EXPLORATION STAGE COMPANY)

CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

|

For the six months

|

From January 10,

|

|||||||||||

|

Ended July 31,

|

2005 (Inception)

|

|||||||||||

|

2011

|

2010

|

to July 31, 2011

|

||||||||||

|

Cash flows used in operating activities:

|

||||||||||||

|

Net loss

|

$ | (1,068,117 | ) | $ | (315,130 | ) | $ | (4,124,936 | ) | |||

|

Adjustments to reconcile net loss to net cash used in operating activities:

|

||||||||||||

|

Donated services and rent

|

- | - | 14,250 | |||||||||

|

Write-down of unproved mineral properties

|

2,909 | - | 228,594 | |||||||||

|

Changes in operating assets and liabilities:

|

||||||||||||

|

Prepaids and other receivables

|

(27,911 | ) | (877 | ) | (65,483 | ) | ||||||

|

Accounts payable

|

(47,748 | ) | 55,191 | 148,910 | ||||||||

|

Accrued liabilities

|

(3,540 | ) | (29,882 | ) | 227,505 | |||||||

|

Due to related parties

|

(99,033 | ) | 145,599 | 749,102 | ||||||||

|

Accrued interest on notes payable to related party

|

3,318 | 1,329 | 77,068 | |||||||||

|

Net cash used in operating activities

|

(1,240,122 | ) | (143,770 | ) | (2,744,990 | ) | ||||||

|

Cash flows used in investing activities:

|

||||||||||||

|

Purchase of fixed assets

|

(19,556 | ) | - | (19,556 | ) | |||||||

|

Acquisition of unproved mineral properties

|

(156,605 | ) | (14,944 | ) | (1,183,374 | ) | ||||||

|

Net cash used in investing activities

|

(176,161 | ) | (14,944 | ) | (1,202,930 | ) | ||||||

|

Cash flows provided by financing activities:

|

||||||||||||

|

Cash received on issuance of notes payable to related party

|

78,901 | 50,000 | 933,291 | |||||||||

|

Proceeds from issuance of common stock

|

1,828,099 | 135,000 | 3,584,849 | |||||||||

|

Net cash provided by financing activities

|

1,907,000 | 185,000 | 4,518,140 | |||||||||

|

Effects of foreign currency exchange

|

(19,004 | ) | (5,136 | ) | (89,852 | ) | ||||||

|

Increase in cash

|

471,713 | 21,150 | 480,368 | |||||||||

|

Cash, beginning

|

8,655 | 7,951 | - | |||||||||

|

Cash, ending

|

$ | 480,368 | $ | 29,101 | $ | 480,368 | ||||||

|

Supplemental disclosures:

|

||||||||||||

|

Cash paid for:

|

||||||||||||

|

Income tax

|

$ | - | $ | - | $ | - | ||||||

|

Interest

|

$ | - | $ | - | $ | - | ||||||

The accompanying notes are an integral part of these consolidated financial statements

4

RED METAL RESOURCES LTD.

(AN EXPLORATION STAGE COMPANY)

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2011

(UNAUDITED)

NOTE 1 – ORGANIZATION AND BASIS OF PRESENTATION

Red Metal Resources Ltd. (the “Company”) was incorporated on January 10, 2005 under the laws of the state of Nevada as Red Lake Exploration, Inc. and changed its name to Red Metal Resources Ltd. on August 27, 2008. On August 21, 2007, the Company acquired a 99% interest in Minera Polymet Limitada (“Polymet”), a limited liability company formed on August 21, 2007 under the laws of the Republic of Chile. The Company is involved in acquiring and exploring mineral properties in Chile. The Company has not determined whether its properties contain mineral reserves that are economically recoverable.

Unaudited Interim Consolidated Financial Statements

The unaudited interim financial statements of the Company have been prepared in accordance with United States generally accepted accounting principles (“GAAP”) for interim financial information and the rules and regulations of the Securities and Exchange Commission (“SEC”). They do not include all information and footnotes required by GAAP for complete financial statements. However, except as disclosed herein, there have been no material changes in the information disclosed in the notes to the financial statements for the year ended January 31, 2011 included in the Company’s Annual Report on Form 10-K, filed with the SEC. The interim unaudited financial statements

should be read in conjunction with those financial statements included in Form 10-K. In the opinion of management, all adjustments considered necessary for fair presentation, consisting solely of normal recurring adjustments, have been made. Operating results for the six month period ended July 31, 2011 are not necessarily indicative of the results that may be expected for the year ending January 31, 2012.

Recent Accounting Pronouncements

The Company has reviewed recently issued accounting pronouncements and plans to adopt those that are applicable to it. It does not expect the adoption of these pronouncements to have a material impact on its financial position, results of operations or cash flows.

NOTE 2 – RELATED-PARTY TRANSACTIONS

The following amounts were due to related parties at July 31, 2011 and January 31, 2011:

|

July 31, 2011

|

January 31, 2011

|

|||||||

|

Due to a company owned by an officer

|

$ | 98,489 | $ | 228,330 | ||||

|

Due to a company controlled by directors

|

237,574 | 207,742 | ||||||

|

Due to a company controlled by a relative of the president

|

74,481 | 63,692 | ||||||

|

Due to a shareholder

|

534 | 10,347 | ||||||

|

Total due to related parties (a)

|

$ | 411,078 | $ | 510,111 | ||||

|

Note payable to a company owned by a relative of the president (b)

|

$ | 54,495 | $ | 52,902 | ||||

|

Note payable to a director (c)

|

- | 60,746 | ||||||

|

Note payable to a relative of the president (d)

|

11,372 | - | ||||||

|

Total notes payable to related parties

|

$ | 65,867 | $ | 113,648 | ||||

(a) Amounts due to related parties are unsecured, are due on demand, and bear no interest.

5

(b) The principal amount of the note payable to a related party is $50,000 US, is due on demand, unsecured and bears interest at 6% per annum. Interest of $4,495 and $2,902 had accrued as at July 31, 2011 and January 31, 2011, respectively.

(c) The principle amounts of the notes payable to a director were $0 and $10,000 US and $0 and $50,000 Cdn, at July 31, 2011 and January 31, 2011, respectively; they were payable on demand, unsecured and bore interest at 8% per annum. An equivalent of $50,000 US on the notes payable was converted into 166,666 units sold in the private placement offering completed on April 7, 2011. The remaining principal and accrued interest were paid in cash.

(d) The principal amount of the note payable due to a relative of the president is $11,000 and is due on demand, unsecured and bears interest at 8% per annum. Interest of $372 had accrued as at July 31, 2011.

During the six months ended July 31, 2011, the Company borrowed $70,000 US and $10,000 Cdn from its CFO. The notes payable were due on demand, unsecured and bore interest at 8% per annum compounded monthly. The CFO chose to convert the equivalent of $80,000 US in principal into 266,667 units sold in the private placement offering completed on April 7, 2011. The remaining principal and accrued interest were paid in cash.

Transactions with Related Parties

During the six months ended July 31, 2011 and 2010 the Company incurred the following expenses to related parties:

|

|

•

|

$145,766 and $65,933, respectively, in consulting and other business expenses to a company owned by the chief financial officer of the Company

|

|

|

•

|

$318,157 and $77,468, respectively, in administration, advertising and promotion, mineral exploration, travel and other business expenses to a company controlled by two directors

|

|

|

•

|

$37,526 and $32,014, respectively, in administration, automobile, rental, and other business expenses to a company owned by a major shareholder and a relative of the president

|

|

|

•

|

$21,797 and $12,591, respectively, in administration expenses, salary and other reimbursable expenses to a shareholder

|

The above amounts represent services provided directly by related parties or expenses paid by related parties on the Company’s behalf.

NOTE 3 – UNPROVED MINERAL PROPERTIES

|

July 31, 2011

|

January 31, 2011

|

|||||||

|

Unproved mineral properties, beginning

|

$ | 662,029 | $ | 643,481 | ||||

|

Acquisition

|

156,605 | 18,548 | ||||||

|

Unproved mineral properties written down

|

(5,342 | ) | - | |||||

|

Unproved mineral properties, ending

|

$ | 813,292 | $ | 662,029 | ||||

Farellon Property

Farellon Alto Uno al Ocho Mineral Claim

On April 25, 2008, the Company acquired the Farellon Alto Uno al Ocho mining claim located in the Commune of Freirina, Province of Huasco, III Region of Atacama, Chile for $550,000. The claim is subject to a 1.5% royalty on the net sales of minerals extracted from the property to a total of $600,000. The royalty payments are due monthly once exploitation begins, and are subject to minimum payments of $1,000 per month. The Company has no obligation to pay the royalty if it does not commence exploitation. At July 31, 2011, the Company had spent a total of $551,647 on the acquisition of this claim. At January 31, 2011, the Company had spent $550,844 on the acquisition of this

claim.

6

Cecil Mineral Claims

On September 17, 2008, the Company acquired the Cecil mining claims for $20,000. The claims are located near the Farellon property in commune of Freirina, Province of Huasco, III Region of Atacama, Chile. At July 31, 2011, the Company had spent a total of $38,651 on the acquisition of these claims and accrued $3,096 in unpaid property taxes. At January 31, 2011, the Company had spent $32,803 on the acquisition of these claims and accrued $3,096 in unpaid property taxes.

Perth Property

Perth Claims

On March 10, 2011, the Company purchased the Perth mining claims for $35,000. The properties are located in Sierra Pan de Azucar in commune of Freirina, Province of Huasco, III Region of Atacama, Chile. On March 14, 2011, the Company entered into an agreement relating to the Perth property with Revonergy Inc. Revonergy Inc. paid $35,000 on signing the agreement and can earn a 35% interest in the Perth property if it spends a minimum $1,450,000 on the three phase exploration program. Revonergy Inc. can earn a further 15% interest if it completes a preliminary feasibility study within four years from the signing of the agreement. At July 31, 2011, the Company had spent

$54,371 in acquisition costs for this property, which were offset against the joint venture payment of $35,000.

Mateo Property

Margarita Claim

On November 27, 2008, the Company acquired the Margarita mining claim for $16,072. At July 31, 2011, the Company had spent a total of $17,529 on the acquisition of this claim and accrued $667 in unpaid property taxes. At January 31, 2011, the Company had spent $17,078 on the acquisition of this claim and accrued $667 in unpaid property taxes.

Che Claims

On October 10, 2008, the Company acquired an option to purchase the Che Uno and Che Dos mining claims. Under the terms of the option, as amended, the Company agreed to pay $444 on December 2, 2008 as consideration for the option agreement and $20,000 by April 10, 2011 to acquire the Che claims. The Company exercised the option on April 7, 2011. The claims are subject to a 1% royalty on the net sales of minerals extracted from the property to a total of $100,000. The royalty payments are due monthly once exploitation begins and are not subject to minimum payments. The Company has no obligation to pay the royalty if it does not commence exploitation. At July 31, 2011, the

Company had spent a total of $22,631 on the acquisition of these claims and accrued $1,264 in unpaid property taxes. At January 31, 2011, the Company had spent $1,313 on the acquisition of these claims and accrued $1,264 in unpaid property taxes.

Irene Claims

On September 7, 2010 the Company entered into a purchase agreement with a related company to acquire the Irene claims. Under the terms of the agreement, as amended, the Company paid $45,174 (equivalent of 21 million Chilean pesos) on May 10, 2011 to exercise the option and purchase the Irene claims. At July 31, 2011, the Company had spent $47,174 in acquisition costs for these claims. At January 31, 2011, the Company capitalized $838 in the acquisition of these claims.

Mateo Exploration Claims

At July 31, 2011 the Company had spent a total of $13,452 on the acquisition of these claims and accrued $5,483 in unpaid property taxes and other costs. During the six months ended July 31, 2011 the Company decided not to maintain several Mateo claims and wrote off $3,694 in acquisition costs. At January 31, 2011, the Company had spent $6,833 on the acquisition of these claims and accrued $8,304 in unpaid property taxes and other costs.

7

Veta Negra Property

Veta Negra Claims

On June 30, 2011, the Company entered into agreement with a related company to acquire its options to purchase the Veta Negra and Exon mining claims and the Trixy exploration claims. Under the terms of the option, the Company agreed to pay $17,500 and to transfer its interest in several generative claims with the book value of $4,504. The remaining cost to purchase the above claims is $90,000 payable within 19 months. The claims are subject to a 1.5% royalty on the net sales of minerals extracted to a total of $500,000. The royalty payments are due monthly once exploitation begins. At July 31, 2011 the Company capitalized $4,504 when it transferred its interest in several generative

claims to the seller pursuant to this agreement.

Other Generative Claims

At July 31, 2011, the Company had spent a total of $1,924 in acquisition costs for generative claims and wrote off $1,648 of accrued property taxes. On January 31, 2011, the Company spent $5,209 in acquisition costs on these claims. See the Subsequent Event note for acquisition of additional generative claims.

Chilean Value Added Tax

At July 31, 2011 and January 31, 2011, the Company had capitalized $89,593 and $33,780, respectively, in Chilean value-added tax (VAT) as part of the unproved mineral claims. This VAT is recoverable from future VAT payable.

NOTE 4 – NON-CASH FINANCING TRANSACTIONS

The following table represents supplemental information on non-cash financing transactions for consolidated statements of cash flows for the six months ended July 31, 2011 and 2010 and for the period from January 10, 2005 (inception) to July 31, 2011.

Non-cash financing transactions

|

July 31, 2011

|

July 31, 2010

|

From January 10, 2005 (Inception) to July 31, 2011

|

||||||||||

|

Conversion of debt owed to related parties to shares of common stock

|

$ | - | $ | - | $ | 338,026 | ||||||

|

Conversion of notes payable to shares of common stock

|

130,000 | - | 874,500 | |||||||||

|

Conversion of accrued interest to shares of common stock

|

- | - | 69,992 | |||||||||

|

Total non-cash financing transactions

|

$ | 130,000 | $ | - | $ | 1,282,518 | ||||||

During the six months ended July 31, 2011, as part of the private placement offering completed on April 7, 2011, the Company’s CEO converted loans in the amount of $50,000 into 166,666 units at $0.30 per unit, and the Company’s CFO converted loans in the amount of $80,000 into 266,667 units at $0.30 per unit. Each unit consisted of one share of our common stock and a warrant for the purchase of one share of our common stock. The term of the warrant is two years and the exercise price is $0.50 per share.

During the six months ended July 31, 2010, the Company did not have any non-cash financing transactions.

From inception to July 31, 2011, the Company converted $338,026 in payables to related parties into 1,126,754 shares of its common stock at $0.30 per share; and $874,500 of loans and $69,992 of accrued interest on notes payable to related parties into 3,148,306 shares of our common stock at $0.30 per share.

8

NOTE 5 – COMMON STOCK

On October 2, 2009, the Company approved a share consolidation of 14 to 1.

On April 7, 2011, the Company issued 6,723,333 units at a price of $0.30 per unit. Each unit consists of one share of common stock and one share purchase warrant. The warrants have an exercise price of $0.50 per share and are exercisable for a period of two years. The warrants contain a call provision which allows the Company to call the warrants upon the occurrence of certain conditions. The net proceeds to the Company from the offering were approximately $1,862,462. Commissions of $58,900 were paid and 196,333 share purchase warrants were issued to agents in connection with this financing.

As part of the private placement of units described above, the Company’s CEO converted loans in the amount of $50,000 into 166,666 units and the Company’s CFO converted loans in the amount of $80,000 into 266,667 units.

Warrants

|

July 31, 2011

|

January 31, 2011

|

|||||||

|

Warrants, beginning

|

790,000 | 607,147 | ||||||

|

Granted

|

6,919,666 | 540,000 | ||||||

|

Expired

|

- | (357,147 | ) | |||||

|

Warrants, ending

|

7,709,666 | 790,000 | ||||||

The weighted average life and weighted average exercise price of the warrants at July 31, 2011 is 1.57 years and $0.48, respectively.

NOTE 6 – SUBSEQUENT EVENTS

On August 3, 2011 Minera Polymet entered into an option purchase agreement with unrelated vendors to acquire Este y Este Uno al Veinte claims in Chile. The purchase price for these claims is 100,000,000 pesos (approximately $219,000 US) and payable within 30 months, of which the first instalment of 5,000,000 pesos (approximately $11,000 US) was paid on August 3, 2011. The property is subject to 1.5% royalty on the net sales of minerals extracted from the property to a total of 100,000,000 pesos (approximately $219,000 US). The royalty payments are due monthly once exploitation begins, and are subject to maximum payment of 500,000 pesos (approximately $1,100 US) per month and no minimum

payment. The Company has no obligation to pay the royalty if it does not commence exploitation.

On September 2, 2011, the Company adopted the Red Metal Resources Ltd. 2011 Equity Incentive Plan (the “Plan”) and reserved 1,600,000 shares of the Company’s common stock for awards under the Plan. The Plan will terminate 10 years from the date of adoption. On September 2, 2011, the Company’s board of directors granted 1,040,000 options to purchase the Company’s common stock to certain officers, directors, and consultants, including 230,000 options granted to the Company’s Chief Executive Officer, Chief Financial Officer, and Vice President of Exploration, each. The options have an exercise price of $0.50 per share and a term of two

years.

9

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Forward-Looking Statements

This quarterly report on form 10-Q filed by Red Metal Resources Ltd. contains forward-looking statements. These are statements regarding financial and operating performance and results and other statements that are not historical facts. The words “expect,” “project,” “estimate,” “believe,” “anticipate,” “intend,” “plan,” “forecast,” and similar expressions are intended to identify forward-looking statements. Certain important risks could cause results to differ materially from those anticipated by some of the forward-looking statements. Some, but not all, of these risks include, among

other things:

|

|

•

|

general economic conditions, because they may affect our ability to raise money

|

|

|

•

|

our ability to raise enough money to continue our operations

|

|

|

•

|

changes in regulatory requirements that adversely affect our business

|

|

|

•

|

changes in the prices for minerals that adversely affect our business

|

|

|

•

|

political changes in Chile, which could affect our interests there

|

|

|

•

|

other uncertainties, all of which are difficult to predict and many of which are beyond our control

|

We caution you not to place undue reliance on these forward-looking statements, which reflect our management’s view only as of the date of this report. We are not obligated to update these statements or publicly release the results of any revisions to them to reflect events or circumstances after the date of this report or to reflect the occurrence of unanticipated events. You should refer to, and carefully review, the information in future documents we file with the Securities and Exchange Commission.

General

You should read this discussion and analysis in conjunction with our interim unaudited consolidated financial statements and related notes included in this Form 10-Q and the audited consolidated financial statements and related notes included in our annual report on Form 10-K for the fiscal year ended January 31, 2011. The inclusion of supplementary analytical and related information may require us to make estimates and assumptions to enable us to fairly present, in all material respects, our analysis of trends and expectations with respect to our results of operations and financial position taken as a whole. Actual results may vary from the estimates and assumptions we make.

Overview

Red Metal is a mineral exploration company engaged in locating, and eventually developing, mineral resources in Chile. Our business strategy is to identify, acquire and explore prospective mineral claims with a view to either developing them ourselves or, more likely, finding a joint venture partner with the mining experience and financial means to undertake the development. All of our claims are in the Candelaria IOCG belt in the Chilean Coastal Cordillera.

We have no revenue-generating operations and are dependent upon the equity markets for our working capital. Despite the current market volatility, prices of copper and gold overall are moving in a positive direction and we are optimistic that we can raise equity capital under these market conditions. We completed an offering of 6,723,333 units on April 7, 2011 at $0.30 per unit. Each unit consisted of one share of our common stock and one warrant for the purchase of one share of common stock exercisable at $0.50 per share for two years. We realized net proceeds of $1,862,462 from this offering.

On September 2, 2011 we adopted the Red Metal Resources Ltd. 2011 Equity Incentive Plan and reserved 1,600,000 shares of our common stock for awards under the Plan. On the same day we issued 1,040,000 stock options to directors, officers, employees and consultants who provide services to Red Metal. The options have an exercise price of $0.50 per share and a term of 2 years.

10

Consistent with our historical practices, we continue to monitor our costs in Chile by reviewing our mineral claims to determine whether they possess the geological indicators to economically justify the capital to maintain or explore them. Currently, we have three employees in Chile and four part time assistants for our exploration program on the Farellon and Mateo properties. Besides the property option agreements we have no long-term commitments. Most of our support there—such as, vehicles and office and equipment—is supplied under short-term contracts.

In September of 2009 we conducted a drilling program on our Farellon property which proved that further drilling of the property is warranted. Micon International Limited, from whom we commissioned a Canadian National Instrument 43-101 technical report summarizing the drilling results, has recommended that we conduct a two-phase drilling program. On June 25, 2011 we started a first phase of the program which was concluded on August 29, 2011. The drill program consisted of 2,234 meters of combined RC and diamond drilling. This phase’s main purpose was to define the structural controls on the mineralization and assist in defining the depth and nature of the sulphide mineralization. The cost of

this phase was approximately $650,000.

We also started an initial exploration program on the Mateo property, which includes geophysics, surface mapping, sampling, high resolution ground magnetic survey, and a 1,000-metre RC drill program. We budgeted $300,000 for this work and we have completed approximately half of it.

On March 14, 2011, we entered into a joint venture earn-in agreement on the Perth property with Revonergy Inc. According to the agreement Revonergy Inc. can earn a 35% interest in the Perth property if it spends a minimum $1,450,000 on a three-phase exploration program; and can earn a further 15% interest if it completes a preliminary feasibility study within four years from the signing of the agreement.

The cost and timing of all planned exploration programs are subject to the availability of qualified mining personnel, such as consulting geologists and geo-technicians, and drillers and drilling equipment. If we are unable to find the personnel and equipment that we need when we need them and at the prices that we have estimated today, we might have to revise or postpone our plans.

At July 31, 2011, we had a working capital deficit of $166,020 and $480,368 in cash. From the proceeds of the financing we completed on April 7, 2011, we have used $650,000 on the Farellon exploration program and $141,000 on the phase 1 Mateo mapping and geophysics.

Results of operations

summary of financial condition

Table 1 summarizes and compares our financial condition at the six months ended July 31, 2011 to the year-ended January 31, 2011.

Table 1: Comparison of financial condition

|

July 31, 2011

|

January 31, 2011

|

|||||||

|

Working capital (deficit)

|

$ | (166,020 | ) | $ | (866,179 | ) | ||

|

Current assets

|

$ | 545,851 | $ | 46,227 | ||||

|

Fixed assets

|

$ | 19,556 | - | |||||

|

Unproved mineral properties

|

$ | 813,292 | $ | 662,029 | ||||

|

Total liabilities

|

$ | 711,871 | $ | 912,406 | ||||

|

Common stock and additional paid in capital

|

$ | 4,881,616 | $ | 2,923,517 | ||||

|

Deficit

|

$ | (4,124,936 | ) | $ | (3,056,819 | ) | ||

11

comparison of prior quarterly results

Tables 2.1 and 2.2 present selected financial information for each of the past eight quarters.

Table 2.1: Summary of quarterly results (October 31, 2010 – July 31, 2011)

|

October 31,

2010

|

January 31,

2011

|

April 30,

2011

|

July 31,

2011

|

|||||||||||||

|

Revenue

|

– | – | – | – | ||||||||||||

|

Net loss

|

$ | (154,436 | ) | $ | (203,052 | ) | $ | (285,276 | ) | $ | (782,841 | ) | ||||

|

Basic and diluted loss per share

|

$ | (0.02 | ) | $ | (0.02 | ) | $ | (0.02 | ) | $ | (0.05 | ) | ||||

Table 2.2: Summary of quarterly results (October 31, 2009 – July 31, 2010)

|

October 31,

2009

|

January 31,

2010

|

April 30,

2010

|

July 31,

2010

|

|||||||||||||

|

Revenue

|

– | – | – | – | ||||||||||||

|

Net loss

|

$ | (105,334 | ) | $ | (204,061 | ) | $ | (196,851 | ) | $ | (118,279 | ) | ||||

|

Basic and diluted loss per share

|

$ | (0.02 | ) | $ | (0.03 | ) | $ | (0.02 | ) | $ | (0.01 | ) | ||||

During the quarter ended October 31, 2009 we conducted a drilling program on our Farellon property, which increased our mineral exploration costs. Excluding the recovery of written down unproved mineral property costs, our net loss for the third quarter of fiscal 2010 was $202,537. During the quarter ended January 31, 2010, we began preparation of the registration statement that was filed on April 10, 2010, which resulted in a substantial increase in our professional fees. During the quarter ended July 31, 2010, we maintained our investor-related activities on a moderate level and decreased our travel costs and professional fees, which resulted in a decrease in our net loss for the quarter. During

the quarters ended October 31, 2010 and January 31, 2011, we invested more in advertising activities and experienced higher professional fees associated with our year-end audit and capital-raising efforts. During the quarter ended April 30, 2011, aside from our regular day-to-day operations, we completed a private placement offering and began preparation of the registration statement on form S-1 that we filed on May 13, 2011. As a result of these activities, our professional and regulatory fees and other expenses increased. We also increased our mineral exploration activities on the Farellon and Mateo properties, which increased our exploration expenses. During the quarter ended July 31, 2011, we started a drilling program on our Farellon property which resulted in significant increases in our mineral exploration expenses, travel costs and salaries paid to geologists and

supporting staff working on the drilling program.

Selected Financial Results

three and six months ended july 31, 2011 and july 31, 2010

Our operating results for the three and six months ended July 31, 2011 and 2010 and the changes in the operating results between those periods are summarized in Table 3.

12

| Table 3: Changes in operating results | ||||||||||||||||||||||||

|

Three months

ended July 31,

|

Changes

between the

|

Six months

ended July 31,

|

Changes

between the

|

|||||||||||||||||||||

| 2011 | 2010 |

periods ended

July 31, 2011

and 2010

|

2011 | 2010 |

periods ended

July 31, 2011

and 2010

|

|||||||||||||||||||

|

Operating Expenses

|

||||||||||||||||||||||||

|

Administration

|

$ | 10,072 | $ | 11,008 | $ | (936 | ) | $ | 30,758 | $ | 38,715 | $ | (7,957 | ) | ||||||||||

|

Advertising and promotion

|

60,559 | 17,338 | 43,221 | 101,086 | 57,609 | 43,477 | ||||||||||||||||||

|

Automobile

|

13,689 | 5,185 | 8,504 | 19,664 | 12,637 | 7,027 | ||||||||||||||||||

|

Bank charges

|

1,497 | (28 | ) | 1,525 | 4,133 | 1,786 | 2,347 | |||||||||||||||||

|

Consulting fees

|

90,413 | 36,072 | 54,341 | 156,633 | 68,995 | 87,638 | ||||||||||||||||||

|

Interest on current debt

|

16,841 | 10,990 | 5,851 | 35,447 | 15,892 | 19,555 | ||||||||||||||||||

|

Mineral exploration costs

|

423,608 | 12,416 | 411,192 | 453,555 | 12,971 | 440,584 | ||||||||||||||||||

|

Office

|

11,978 | 898 | 11,080 | 15,315 | 3,227 | 12,088 | ||||||||||||||||||

|

Professional development

|

- | - | - | - | 4,008 | (4,008 | ) | |||||||||||||||||

|

Professional fees

|

58,351 | 15,387 | 42,964 | 106,256 | 52,517 | 53,739 | ||||||||||||||||||

|

Rent

|

3,498 | 3,107 | 391 | 6,954 | 6,233 | 721 | ||||||||||||||||||

|

Regulatory

|

7,400 | 6,925 | 475 | 15,398 | 11,440 | 3,958 | ||||||||||||||||||

|

Travel and entertainment

|

64,555 | 155 | 64,400 | 83,770 | 28,708 | 55,062 | ||||||||||||||||||

|

Salaries, wages and benefits

|

20,006 | - | 20,006 | 25,026 | 1,015 | 24,011 | ||||||||||||||||||

|

Foreign exchange loss

|

374 | (1,174 | ) | 1,548 | 11,213 | (623 | ) | 11,836 | ||||||||||||||||

|

Write-down of unproved mineral properties

|

- | - | - | 2,909 | - | 2,909 | ||||||||||||||||||

|

Net loss

|

$ | 782,841 | $ | 118,279 | $ | 664,562 | $ | 1,068,117 | $ | 315,130 | $ | 752,987 | ||||||||||||

Operating expenses. Our operating expenses increased by $664,562, or 562%, from $118,279 for the three months ended July 31, 2010 to $782,841 for the three months ended July 31, 2011.

On a year-to-date basis, our operating expenses increased by $752,987, or 239%, from $315,130 for the six months ended July 31, 2010 to $1,068,117 for the six months ended July 31, 2011.

The following are our most significant year-to-date changes:

|

|

•

|

During the six months ended July 31, 2011, we started a drilling program on our Farellon property and increased exploration activities on Mateo and Veta Negra properties, which resulted in a $440,584 increase in the mineral exploration expenses from $12,971 for the six months ended July 31, 2010 to $453,555 during the six months ended July 31, 2011.

|

|

|

•

|

During the second quarter drilling campaign we hired four assistant geotechnicians and additional office staff to keep up with the increased workload. This resulted in an increase of $24,011 in our salaries, wages & benefits expense from $1,015 during the six months ended July 31, 2010 to $25,026 during the six months ended July 31, 2011.

|

|

|

•

|

During the six months ended July 31, 2011, our travel and entertainment expenses increased from $28,708 to $83,770. The $55,062 increase was mainly associated with travel time incurred by consulting geologists during the current drilling program. These travel expenditures were budgeted under the exploration campaign.

|

|

|

•

|

Due to higher accounting and financial advisory requirements we incurred $156,633 in consulting fees during the six months ended July 31, 2011, an increase of $87,638 compared to $68,995 for the six months ended July 31, 2010.

|

|

|

•

|

During the six months ended July 31, 2011, we completed a private equity financing and filed a registration statement on form S-1, which resulted in an increase of $53,739 in our professional and legal fees.

|

|

|

•

|

To continue with our operational plans we increased our advertising and promotion costs by $43,477 during the six months ended July 31, 2011.

|

|

|

•

|

During the six months ended July 31, 2011, we expensed $35,447 in interest on current debt, an increase of $19,555 compared to $15,892 in interest expensed during the six months ended July 31, 2010. This increase was associated with larger outstanding payables, mainly to related parties.

|

|

|

•

|

During the six months ended July 31, 2011, we wrote down $2,909 in mineral property acquisition costs after we abandoned some of our Mateo exploration claims. During the six months ended July 31, 2010, we did not write down any of our properties.

|

13

Net loss. We had a net loss of $1,068,117 for the six months ended July 31, 2011, compared to a net loss of $315,130 for the six months ended July 31, 2010. The $752,987 increase in net loss was due to an active drilling program on our Farellon property, which resulted in increased exploration, travel and automobile costs, as well as increased salaries, wages and benefits; we also increased our advertising and promotion activities in order to seek additional external financing, which resulted in increased advertising costs, and consulting, professional and regulatory fees.

Liquidity

going concern

The consolidated financial statements included in this form 10-Q have been prepared on a going concern basis, which implies that we will continue to realize our assets and discharge our liabilities in the normal course of business. We have not generated any significant revenues from mineral sales since inception, have never paid any dividends and are unlikely to pay dividends or generate significant earnings in the immediate or foreseeable future. Our continuation as a going concern depends upon the continued financial support of our shareholders, our ability to obtain necessary debt or equity financing to continue operations, and the attainment of profitable operations. Our ability to achieve and

maintain profitability and positive cash flow depends upon our ability to locate profitable mineral claims, generate revenue from mineral production and control our production costs. Based upon our current plans, we expect to incur operating losses in future periods, which we plan to mitigate by controlling our operating costs and sharing mineral exploration expenses through joint venture agreements. In April 2011 we completed a financing of units consisting of our common stock and warrants to purchase shares of our common stock. We raised gross proceeds of $2,017,000. We expect these funds to be adequate to support our administrative overhead and complete current exploration campaigns on the Farellon and Mateo properties. However, we are continually reviewing potential properties to add to our portfolio. Suitable acquisitions and project

development will require additional financing. Until we earn enough revenue to support our operations, which may never happen, we will continue to be dependent on loans and sales of our equity or debt securities to continue our development and exploration activities. If we do not find sources of financing as and when we need them, we may be required to severely curtail, or even to cease, our operations. At July 31, 2011, we had a working capital deficit of $166,020 and accumulated losses of $4,124,936 since inception. These factors raise substantial doubt about our ability to continue as a going concern. We cannot assure you that we will be able to generate significant revenues in the future. Our consolidated financial statements do not give effect to any adjustments that would be necessary should we be unable to continue as a going concern and therefore be

required to realize our assets and discharge our liabilities in other than the normal course of business and at amounts different from those reflected in our financial statements.

internal and external sources of liquidity

To date we have funded our operations by selling our securities and borrowing funds, and, to a minor extent, from mining royalties.

14

Sources and uses of cash

Six months ended July 31, 2011 and 2010

Table 4 summarizes our sources and uses of cash for the six months ended July 31, 2011 and 2010.

| Table 4: Summary of sources and uses of cash | ||||||||

|

July 31,

|

||||||||

|

2011

|

2010

|

|||||||

|

Net cash provided by financing activities

|

$ | 1,907,000 | $ | 185,000 | ||||

|

Net cash used in operating activities

|

(1,240,122 | ) | (143,770 | ) | ||||

|

Net cash used in investing activities

|

(176,161 | ) | (14,944 | ) | ||||

|

Effect of foreign currency exchange

|

(19,004 | ) | (5,136 | ) | ||||

|

Net increase in cash

|

$ | 471,713 | $ | 21,150 | ||||

Net cash provided by financing activities. During the six months ended July 31, 2011, we issued 6,290,000 units at $0.30 per unit, for cash proceeds of $1,828,099, net of $58,900 in commissions paid to agents. Each unit consists of one share of our common stock and a two-year warrant exercisable for one share of common stock at $0.50 per share.

We borrowed $11,000 from the father of our president and $70,000 US and $10,000 Cdn (approximately $10,454 US) from our CFO, and repaid $14,956 in loans including accrued interest. We also recognized foreign exchange adjustment of $2,402 on $50,000 Cdn that we borrowed during the year ended January 31, 2011 from our CEO. See Non-cash financing transactions below.

During the six months ended July 30, 2010, we issued 540,000 shares of our common stock for $135,000, and borrowed $50,000 from a company owned by the father of a director.

Non-cash financing transactions. During the six months ended July 31, 2011, as part of the private placement offering completed on April 7, 2011, the Company’s CEO converted loans in the amount of $50,000 into 166,666 units and the Company’s CFO converted loans in the amount of $80,000 into 266,667 units.

During the six months ended July 31, 2010, we did not have any non-cash financing transactions.

Net cash used in operating activities. During the six months ended July 31, 2011, we used net cash of $1,240,122 in operating activities. We used $1,068,117 to cover operating costs and increased prepaids and other receivables by $27,911. We decreased accounts payable and accrued liabilities by $47,748 and $3,540, respectively. We also decreased accounts payable to related parties by $99,033. These uses of cash were offset by accrued interest on our notes payable to related parties of $3,318.

During the six months ended July 31, 2010, we used net cash of $143,770 in operating activities. We used $315,130 to cover operating costs and decreased our accrued liabilities and increased prepaid expenses and accounts receivable by $29,882 and $877 respectively. These uses of cash were offset by net increases in accounts payable of $55,191, consisting mainly of legal and audit fees incurred in preparing and filing our form 10 and the amendments to it; accounts payable to related parties of $145,599 for administration, consulting, advertising and promotion, office, automobile, mineral exploration, rental and travel expenses; and accrued interest on our notes payable to a related party of

$1,329.

Net cash used in investing activities. During the six months ended July 31, 2011, we spent $156,605 acquiring mineral claims and paying property taxes associated with our mineral claims. We capitalized Chilean value-added tax as part of the unproved mineral claims. This VAT is recoverable from future VAT payable. During the same period we used $19,556 to purchase a pick-up truck that will be used in operations.

During the six months ended July 31, 2010, we spent $14,944 acquiring mineral claims and options to acquire mineral claims.

Since inception through July 31, 2011, we have invested $1,183,374 acquiring our mineral claims.

15

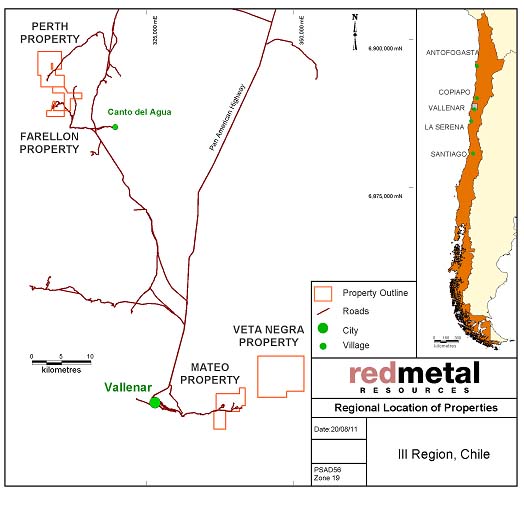

Unproved mineral properties

We have four active properties which we have assembled since the beginning of 2007— the Farellon, Perth, Mateo, and Veta Negra. These properties consist of both mining and exploration claims and are grouped into two district areas – Carrizal Alto area properties and Vallenar area properties.

Active properties

Our active properties as of the date of this filing are set out in Table 5. These properties are accessible by road from Vallenar as illustrated in Figure 1.

|

Table 5: Active properties

|

|||||||||

|

Property

|

Percentage, type of claim

|

Hectares

|

|||||||

|

Gross area

|

Net areaa

|

||||||||

|

Carrizal Alto area

|

|||||||||

|

Farellon

|

|||||||||

|

Farellon 1 – 8 claim

|

100%, mensura

|

66 | |||||||

|

Farellon 3 claim

|

100%, pedimento

|

300 | |||||||

|

Cecil 1 – 49 claim

|

100%, mensura

|

230 | |||||||

|

Cecil 1 – 40 and Burghley 1 – 60 claims

|

100%, manifestacion

|

500 | |||||||

| 1,096 | 1,096 | ||||||||

|

Perth

|

|||||||||

|

Perth 1 al 36 claim

|

100%, mensura

|

109 | |||||||

|

Lancelot I 1 al 30 claim

|

100%, mensura in process

|

300 | |||||||

|

Lancelot II 1 al 20 claim

|

100%, mensura in process

|

200 | |||||||

|

Rey Arturo 1 al 30 claim

|

100%, mensura in process

|

300 | |||||||

|

Merlin I 1 al 10 claim

|

100%, mensura in process

|

60 | |||||||

|

Merlin I 1 al 24 claim

|

100%, mensura in process

|

240 | |||||||

|

Galahad I 1 al 10 claim

|

100%, manifestacion

|

50 | |||||||

|

Galahad I A 1 al 46 claim

|

100%, manifestacion

|

230 | |||||||

|

Percival III 1 al 30 claim

|

100%, manifestacion

|

300 | |||||||

|

Tristan II 1 al 30 claim

|

100%, manifestacion

|

300 | |||||||

|

Tristan II A 1 al 5 claim

|

100%, manifestacion

|

15 | |||||||

|

Camelot claim

|

100%, pedimento

|

300 | |||||||

| 2,404 | |||||||||

|

Overlapped claims

|

(124 | ) | 2,280 | ||||||

|

Vallenar area

|

|||||||||

|

Mateo

|

|||||||||

|

Margarita claim

|

100%, mensura

|

56 | |||||||

|

Che 1 & 2 claims

|

100%, mensura

|

76 | |||||||

|

Irene & Irene II claims

|

100%, mensura

|

60 | |||||||

|

Mateo 1, 2, 3, 12, 13, 14 claims

|

100%, manifestacion

|

1,500 | |||||||

|

Mateo 4 and 5 claims

|

100%, pedimento

|

600 | |||||||

| 2,292 | |||||||||

|

Overlapped claims

|

(170 | ) | 2,122 | ||||||

|

Veta Negra

|

|||||||||

|

Veta Negra 1 al 7 claim

|

Option to purchase, mensura

|

28 | |||||||

|

Exon 1 al 4 claim

|

Option to purchase, mensura

|

16 | |||||||

|

Trixy 1 al 18

|

100%, pedimento

|

5,300 | |||||||

| 5,344 | |||||||||

|

Overlapped claims

|

(44 | ) | 5,300 | ||||||

| 10,798 | |||||||||

|

a Some pedimentos and manifestaciones overlap other claims. The net area is the total of the hectares we have in each property (i.e. net of our overlapped claims).

|

|||||||||

16

Figure 1: Location and access to active properties.

Capital resources

Our ability to acquire and explore our Chilean claims is subject to our ability to obtain the necessary funding. We expect to raise funds through loans from private or affiliated persons and sales of our debt or equity securities. We have no committed sources of capital. If we are unable to raise funds as and when we need them, we may be required to curtail, or even to cease, our operations.

On April 7, 2011, we completed a private equity financing for net proceeds after commissions, legal and closing fees of $1,862,462. We paid the placement agent a cash commission of $58,900 and issued a warrant to purchase 196,333 shares of common stock. The securities offered were not registered under the Securities Act of 1933 and may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements. On May 13, 2011, we filed registration statement on form S-1 to register 4,623,333 shares of our common stock, and 4,819,666 shares of common stock underlying warrants which were a part of the above private equity

financing.

Contingencies and commitments

We had no contingencies at July 31, 2011.

17

We have the following long-term contractual obligations and commitments:

|

|

•

|

Farellon royalty. We are committed to paying the vendor a royalty equal to 1.5% on the net sales of minerals extracted from the Farellon claims up to a total of $600,000. The royalty payments are due monthly once exploitation begins and are subject to minimum payments of $1,000 per month. We have no obligation to pay the royalty if we do not commence exploitation. As of the date of this report we have not commenced exploitation.

|

|

|

•

|

Che royalty. We are committed to paying a royalty equal to 1% of the net sales of minerals extracted from the claims to a maximum of $100,000 to the former owner. The royalty payments are due monthly once exploitation begins, and are not subject to minimum payments.

|

|

|

•

|

Veta Negra option. On June 30, 2011, Minera Farellon agreed to sell us its option to purchase the Veta Negra and Exon claims for $17,500. Under the terms of the option agreement we must pay $80,000 payable in two installments over 18 months to the vendor to exercise the option. If we exercise the option we are committed to paying the vendor a royalty equal to 1.5% of the net sales of minerals extracted from the claims to a total maximum of $500,000. The royalty can also be bought for $500,000 at any time. The royalty payments are due monthly once exploitation begins, and are not subject to minimum payments.

|

|

|

•

|

Este option. Under the terms of our option agreement to purchase Este claims , we are committed to paying 100,000,000 Chilean Pesos (approximately $219,000 US) payable in six installments over a period of 30 months to the vendors. If we exercise our option we are committed to paying the vendors a royalty equal to 1.5% of the net sales of minerals extracted from the claims to a maximum of 100,000,000 Chilean Pesos (approximately $219,000 US). The royalty payments are due monthly once exploitation begins, are subject to a monthly maximum payment of 500,000 pesos ($1,100 US) and no minimum payments.

|

Equity financing

To generate working capital, between January 31, 2009 and September 14, 2011 we issued 12,783,632 shares of our common stock and warrants for the purchase of 7,709,666 shares to raise $3,467,018 under Regulations S and D promulgated under the Securities Act of 1933.

We anticipate incurring operating losses in the foreseeable future and will require additional equity capital to support our operations and develop our business plan. If we succeed in completing future equity financing, the issuance of additional shares will result in dilution to our existing shareholders.

Debt financing

On February 22, 2010, we borrowed US $50,000 and issued a demand promissory note payable to the lender for the principal sum together with interest at 6% per annum. See Related-party transactions below.

On March 2, 2011, we borrowed US $11,000 and issued a demand promissory note payable to the lender for the principal sum together with interest at 8% per annum. See Related-party transactions below.

Challenges and risks

We do not anticipate generating any revenue over the next twelve months. We plan to fund our operations through any combination of equity or debt financing from the sale of our securities, private loans, joint ventures or through the sale of part interest in our mineral properties. Although we have succeeded in raising funds as we have needed them, we cannot assure you that this will continue in the future. Many things, such as the continued general downturn, worldwide, of the economy or a significant decrease in the price of minerals, could affect the willingness of potential investors to invest in risky ventures such as ours. In addition to the Perth joint venture earn-in agreement, we

may consider entering into a joint venture partnership with a more senior resource company to complete a mineral exploration program on other properties in Chile. If we enter into a joint venture arrangement, we would likely have to assign a percentage of our interest in our mineral claims to our joint venture partner in exchange for the funding.

18

Investments in and expenditures on mineral interests

Realization of our investments in mineral properties depends upon our maintaining legal ownership, producing from the properties or gainfully disposing of them.

Title to mineral claims involves risks inherent in the difficulties of determining the validity of claims as well as the potential for problems arising from the ambiguous conveyancing history characteristic of many mineral claims. Our contracts and deeds have been notarized, recorded in the registry of mines and published in the mining bulletin. We review the mining bulletin regularly to discover whether other parties have staked claims over our ground. We have discovered no such claims. To the best of our knowledge, we have taken the steps necessary to ensure that we have good title to our mineral claims.

Foreign exchange

We are subject to foreign exchange risk for transactions denominated in foreign currencies. Foreign currency risk arises from the fluctuation of foreign exchange rates and the degree of volatility of these rates relative to the United States dollar. We do not believe that we have any material risk due to foreign currency exchange.

Trends, events or uncertainties that may impact results of operations or liquidity

The economic crisis in the United States and the resulting economic uncertainty and market instability may make it harder for us to raise capital as and when we need it and have made it difficult for us to assess the impact of the crisis on our operations or liquidity and to determine if the prices we will receive on the sale of minerals will exceed the cost of mineral exploitation. If we are unable to raise cash, we may be required to cease our operations. Other than as discussed in this quarterly report, we know of no other trends, events or uncertainties that have or are reasonably likely to have a material impact on our short-term or long-term liquidity.

Off-balance sheet arrangements

We have no off-balance sheet arrangements and no non-consolidated, special-purpose entities.

Related-party transactions

Table 6 describes amounts that were due to related parties at the fiscal year ended January 31, 2011 and the period ended July 31, 2011.

|

Table 6: Due to related parties

|

||||||||

|

July 31, 2011

|

January 31, 2011

|

|||||||

|

Due to Da Costa Management Corp.

|

$ | 98,489 | $ | 228,330 | ||||

|

Due to Fladgate Exploration Consulting Corporation

|

$ | 237,574 | $ | 207,742 | ||||

|

Due to Minera Farellon Limitada

|

$ | 74,481 | $ | 63,692 | ||||

|

Due to Kevin Mitchell

|

$ | 534 | $ | 10,347 | ||||

During the six months ended July 31, 2011 and 2010 the Company incurred the following expenses with related parties:

|

|

•

|

$145,766 and $65,933, respectively, in consulting and other business expenses for services provided by Da Costa Management Corp., a company owned by our CFO and treasurer

|

|

|

•

|

$318,157 and $77,468 respectively, in administration, advertising and promotion, mineral exploration, travel and other business expenses for services provided by or paid on our behalf by Fladgate Exploration Consulting Corporation, a company controlled by our directors

|

|

|

•

|

$37,526 and $32,014, respectively, in administration, automobile, rental, and other business expenses for services provided by Minera Farellon Limitada, a company owned by Richard Jeffs, the father of our president

|

|

|

•

|

$21,797 and $12,591, respectively, in administration expenses, salary and other reimbursable expenses due to Kevin Mitchell

|

19

On April 1, 2011, we engaged Fladgate Exploration to manage the exploration programs on our properties in Chile. The engagement is expected to last until December 2011 although either party can cancel it with a 30 days’ notice. Under the terms of the engagement Fladgate agreed to supply its professional geo consulting services within the industry standard rates with a $50,000 retainer paid after the signing of the agreement. This agreement was conducted in the normal course of operations on terms no less favorable than terms available to or from independent third parties.

Notes payable to related parties

Table 7 describes the promissory notes and accrued interest payable to related parties at July 31, 2011, and January 31, 2011.

| Table 7: Note payable to related parties | ||||||||

|

July 31,

2011

|

January 31,

2011

|

|||||||

|

Note payable to the company owned by Richard Jeffs a

|

$ | 54,495 | $ | 52,902 | ||||

|

Note payable to Richard Jeffs b

|

11,372 | – | ||||||

|

Notes payable to Caitlin Jeffs c

|

– | 60,746 | ||||||

|

Total notes payable to related parties

|

$ | 65,867 | $ | 113,648 | ||||

|

aThe principle amount is $50,000. It is payable on demand, unsecured and bears interest at 6% per annum compounded monthly. Interest of $4,495 had accrued as at July 31, 2011.

b The principle amount is $11,000. It is payable on demand, unsecured and bears interest at 8% per annum compounded monthly. Interest of $372 had accrued as at July 31, 2011.

c The principle amounts of the notes payable to Caitlin Jeffs were $10,000 US and $50,000 Cdn. They were payable on demand, unsecured and bore interest at 8% per annum compounded monthly. Interest of $1,837 had accrued as at April 8, 2011 when the notes were paid in full.

|

||||||||

Critical Accounting Estimates

An appreciation of our critical accounting judgments is necessary to understand our financial results. These policies may require that we make difficult and subjective judgments regarding uncertainties, and as a result, such estimates may significantly impact our financial results. The precision of these estimates and the likelihood of future changes depend on a number of underlying variables and a range of possible outcomes. Other than our accounting for the fair value of our unproved mineral properties, accruals for accounting, auditing, legal expenses and mineral property costs, our critical accounting policies do not involve the choice between alternative methods of

accounting. We have applied our critical accounting judgments consistently.

Reclassifications

Certain comparative amounts in the accompanying consolidated financial statements have been reclassified to conform to the current year’s presentation. These reclassifications had no effect on the consolidated results of operations or financial position for any year presented.

20

Unproved mineral property costs

We have been in the exploration stage since our inception on January 10, 2005 and have not yet generated significant revenue from our operations. We are primarily engaged in acquiring and exploring mining claims. We expense our mineral exploration costs as we incur them. When we have determined that a mineral claim can be economically developed as a result of establishing proven and probable reserves, we capitalize the costs then incurred to develop the claim and will amortize them using the units-of-production method over the estimated life of the probable reserve. If mineral claims are subsequently abandoned or impaired we will charge capitalized costs to operations.

Financial instruments

Our financial instruments include cash, accounts receivable, accounts payable, accrued liabilities, accrued professional fees and accrued mineral property costs. The fair value of these financial instruments approximates their carrying values due to their short maturities.

Recently Adopted Accounting Guidance

The Company has reviewed recently issued accounting pronouncements and plans to adopt those that are applicable to it. We do not expect the adoption of these pronouncements to have a material impact on our financial position, results of operations or cash flows.

As a smaller reporting company, we are not required to provide this disclosure.

Item 4. Controls and Procedures.

(a) Disclosure Controls and Procedures

Caitlin Jeffs, our chief executive officer and president, and John da Costa, our chief financial officer, have evaluated the effectiveness of our disclosure controls and procedures (as the term is defined in Rules 13a-15 and 15d-15 under the Securities Exchange Act of 1934) as of the end of the period covered by this report (the “evaluation date”). Based on their evaluation, they have concluded that, as of the evaluation date, our disclosure controls and procedures are effective to ensure that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is recorded, processed, summarized and reported within the time periods specified

in the Securities and Exchange Commission’s rules and forms.

(b) Changes in internal control over financial reporting

During the period covered by this report, there were no changes to our internal control over financial reporting that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

PART II—OTHER INFORMATION

Item 1. Legal Proceedings.

We are not a party to any pending legal proceedings and, to the best of our knowledge, none of our properties or assets is the subject of any pending legal proceedings.

21

Item 1A. Risk Factors.

As a smaller reporting company we are not required to provide this information.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds.

None.

Item 3. Defaults upon Senior Securities.

None.

Item 4. (Removed and Reserved).

Item 5. Other Information.

None

Item 6. Exhibits.