Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SunCoke Energy, Inc. | d230863d8k.htm |

KeyBanc Capital

Markets 2011 Basic Materials & Packaging Conference

September 13, 2011

Exhibit 99.1 |

1

Safe Harbor Statement

Some

of

the

information

included

in

this

presentation

contains

“forward-looking

statements”

(as

defined

in

Section

27A

of

the

Securities

Act of

1933, as amended and Section 21E of the Securities Exchange Act of 1934, as

amended). Such forward-looking statements are based on management’s

beliefs and assumptions and on information currently available. Forward-looking statements include the information concerning

Suncoke’s possible or assumed future results of operations, business

strategies, financing plans, competitive position, potential growth

opportunities, potential operating performance improvements, effects resulting from

our separation from Sunoco, the effects of competition and the effects of

future legislation or regulations. Forward-looking statements include all statements that are not historical facts and may be

identified

by

the

use

of

forward-looking

terminology

such

as

the

words

“believe,”

“expect,”

“plan,”

“intend,”

“anticipate,”

“estimate,”

“predict,”

“potential,”

“continue,”

“may,”

“will,”

“should”

or the negative of these terms or similar expressions. Forward-looking

statements involve risks, uncertainties and assumptions. Actual results may

differ materially from those expressed in these forward-looking statements. You should not

put undue reliance on any forward-looking statements.

In accordance with the safe harbor provisions of the Private Securities Litigation

Reform Act of 1995, SunCoke has included in its filings with the Securities

and Exchange Commission cautionary language identifying important factors (but not necessarily all the important factors) that

could cause actual results to differ materially from those expressed in any

forward-looking statement made by SunCoke. For more information

concerning

these

factors,

see

SunCoke's

Securities

and

Exchange

Commission

filings.

All

forward-looking

statements

included

in

this

presentation

are

expressly

qualified

in

their

entirety

by

such

cautionary

statements.

SunCoke

undertakes

no

obligation

to

update

publicly any

forward-looking statement (or its associated cautionary language) whether as a

result of new information or future events or otherwise. This presentation

includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures.

Reconciliations of non-GAAP financial measures to GAAP financial measures are

provided in the Appendix at the end of the presentation. Investors

are

urged

to

consider

carefully

the

comparable

GAAP

measures

and

the

reconciliations

to

those

measures

provided

in

the

Appendix,

or on our website at www.suncoke.com. |

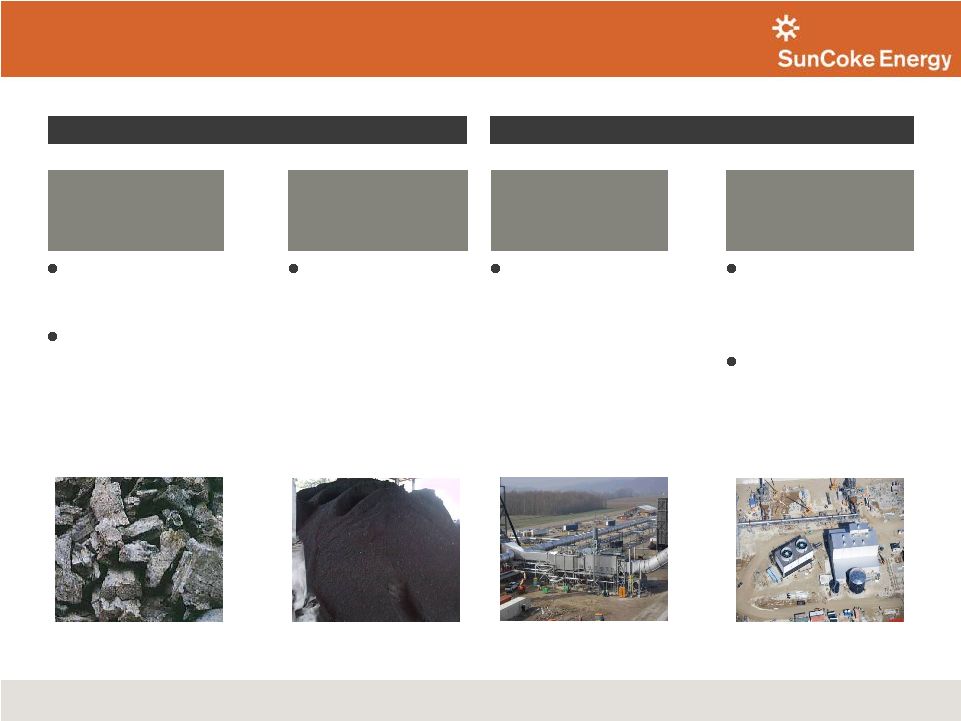

2

SunCoke at a Glance

Business Mix

Cokemaking Capacity

Pro Forma Adjusted EBITDA

(2010)*

Sales and Other Operating Revenue

(2010)

$197 million*

$1.3 billion

Largest independent producer of high-quality

metallurgical coke in the Americas

-

Over 45 years of production experience

2010 total revenue and adjusted EBITDA of

$1.3 billion and $227 million, respectively

Five cokemaking facilities (four in U.S. and one in

Brazil) with a sixth facility expected to start-up in Q4

2011

-

Approximately 5.9 million tons per year

cokemaking capacity including new facility

-

Grown capacity from 2.5 million tons in 2005 to

5.4 million tons in 2010

Secure, long-term contracts with leading steelmakers

who have been increasingly outsourcing coke

production to SunCoke

Metallurgical coal mining operations in Virginia and

West Virginia

-

1.2 million tons of metallurgical coal production

annually

-

Expect production to double to 2.4–2.5 million tons

per annum by mid-2013

Approximately 1,180 employees (980 U.S. / 200 Brazil)

Expect Sunoco to complete spin-off within 12 months

of IPO

International

Coke

8%

*Excludes Corporate Segment

Other

Domestic

Coke

74%

Jewell Coke

23%

International

Coke

3%

Coal Mining

0%

Coal

Mining

12%

Other

Domestic

Coke

55%

Jewell

Coke

25%

0

1

2

3

4

5

6

7

2004

2005

2006

2007

2008

2009

2010

2011E

2012E

Jewell

Indiana Harbor

Haverhill I

Vitória

Haverhill II

Granite City

Middletown |

3

Strategically-Located Cokemaking Facilities and Mines

International Operations

(1) Expected start-up in Q4 2011.

(2) SunCoke holds a preferred interest of $41 million in Vitória and is the

operator. Our U.S. facilities are located in close proximity to all U.S. integrated

steelmaking facilities Vitória

(2)

(ArcelorMittal)

Capacity: 1,700kt

Brazil

Indiana Harbor

(ArcelorMittal)

Capacity: 1,220kt

Haverhill

(ArcelorMittal /

AK Steel)

Capacity: 1,100kt

Granite City

(US Steel)

Capacity: 650kt

Domestic Operations

Cokemaking facility under construction

Existing cokemaking facilities

Coal mining

Jewell

(ArcelorMittal)

Capacity: 720kt

Middletown

(1)

(AK Steel)

Capacity: 550kt

(Expect production to double to

2.4–2.5mtpy by mid-2013)

Jewell Coal

1.2mtpy

Premium mid-vol

Reserves: 85mt

Harold Keene

0.3mtpy

High-vol A/B

Reserves: 21mt |

4

Delivering Coke and Energy to Customers

Coke

Energy

Blast Furnace Coke

Electric Power

Steam

Breeze

or

Nut Coke

and/or

and

Key raw material in

blast furnace iron-

making process

Acts as a reductant

and burden in the

blast furnace

Small-sized coke

fines screened from

the blast furnace-

sized coke

production

Heat recovery steam

generators (“HRSG”)

capture waste heat

from the coking

process to make

low-pressure,

saturated steam

HRSGs produce high-

pressure, superheated

steam for power

generation

Facilities generate

~9 MW electric power

each hour per 110,000

tons of annual coke

production |

5

Our Industry-Leading Heat Recovery

Coke Oven Technology |

6

SunCoke’s Oven vs. By-Product Ovens

SunCoke’s technology is the industry’s environmental standard and provides many

advantages over the traditional cokemaking process

SunCoke Heat Recovery

Traditional By-Product

Pressurization

Negative pressure

Positive pressure

Air Emissions

MACT standard for new batteries

Potential for emission of hazardous

compounds

Power Generation

Cogenerates power

Power consuming process

Hazardous Inputs

None

Yes – sulfuric acid

Volatile Organic Compounds

Complete combustion

No combustion

Solid Wastes

No toxic solid wastes

Process produces toxic waste streams

Water Usage

No wastewater discharges

Requires wastewater treatment facility

|

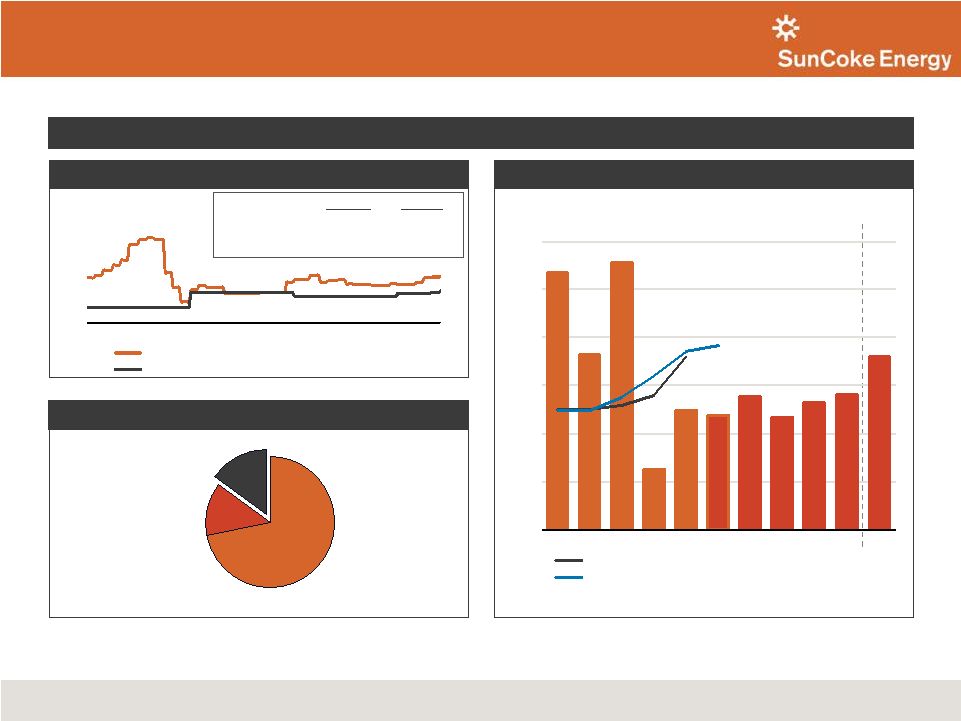

7

Strong Industry Fundamentals

World Crude Steel Production

Source:

CRU, The Annual Outlook for Metallurgical Coke 2011.

We expect significant infrastructure investment in

emerging markets to drive steel demand growth

Coke/blast furnace iron production is expected to

remain the dominant process

-

China: ~90%

-

World: ~70%

-

U.S.: ~40%

(Tons in millions)

World Coke Consumption

Source: CRU, The Annual Outlook for Metallurgical Coke 2011.

(Tons in millions)

We expect demand to increase with growing

integrated steel production

Aging coke infrastructure

-

44% of existing global coke capacity (excluding

China and CIS) is over 30 years old

-

53% of North American coke capacity is over 30

years old

-

SunCoke’s U.S. growth has been driven by

coke battery replacement

641

497

906

1,248

1,562

2,319

2005

2010

2021E

China

Asia (ex China)

Europe

N. America

CIS

Rest of World

2005

2010

2021E

China

Asia (ex China)

Europe

N. America

CIS

Rest of World |

8

$200

$325

$450

$575

$700

Jan-08

Jan-09

Jan-10

Jan-11

Chinese Metallurgical Coke (FOB China port - adds $45-$60/ton)

SunCoke –

Other Domestic Coke

SunCoke's North American Industry Position

Chinese Coke Price vs. Representative SunCoke Price

North American Coke Capacity

North American Coke Imports

SunCoke has the opportunity to displace higher cost coke imports

Source: CRU, The Annual Outlook for Metallurgical Coke 2011.

SunCoke

Chinese

Q2 2011 Average:

$359

$440

2010 Average:

$336

$414

2008-2010 Average:

$326

$430

(Tons in millions)

Source:

CRU, The Annual Outlook for Metallurgical Coke 2011.

(1)

Represents SunCoke’s domestic cokemaking capacity weighted by the number of months each

facility operated during that year.

(1)

(1)

Other Domestic Coke sales and other operating revenues divided by tons sold.

2010 Total Capacity: 24.5 million tons

Integrated coke

72%

Merchant coke

13%

SunCoke

15%

(US$ / ton)

5.4

3.6

5.6

1.3

2.5

2.4

2.8

2.3

2.6

2.8

3.6

–

1.0

2.0

3.0

4.0

5.0

6.0

2006

2007

2008

2009

2010

2011E

2012E

2013E

2014E

2015E

2021E

SunCoke domestic coke sales volumes

SunCoke weighted-average domestic cokemaking capacity

(1) |

9

SunCoke’s Value Proposition

Permits and Approvals

Engineering, Procurement &

Construction

Capital Funding and Ownership

A competitive turnkey coke solution which produces a consistent stream of earnings

Operating Cost Component

(Pass-Through)

Fixed Fee

(Profit and Return on Capital)

Coal Cost Component

(Pass-Through)

Take-Or-Pay

Taxes, Transportation and Future

Environmental Costs (Pass-Through)

Coke fee

Energy fee

SunCoke

Energy

Customer

Typical Key Coke Sales Agreement Provisions

What SunCoke Offers

Plant Production and Environmental

Compliance

Reliability and Quality of Coke Supply |

10

Focused Growth Strategy

Maintain our technological advantage through the development or

acquisition of new technologies

Expand our domestic coal production from current reserves and pursue

selective reserve additions

Maintain liquidity and financial flexibility to facilitate growth

We believe

SunCoke

Energy is

uniquely

positioned for

continued

investment and

earnings

growth

Maintain our consistent focus on operational excellence, safety and

environmental stewardship

Continue to grow our North American cokemaking businesses; with

portion of future coke capacity reserved for market sales

Grow our international footprint with a focus on key growth markets

Growth Initiatives

Foundations for Growth |

11

Coke Development

North

America

Brazil

Ongoing discussions with multiple customers for new coke capacity

Our Focus / Activities

Market Drivers

China

Exploring partner opportunities to enter market

Import displacement

Battery replacements

New blast furnace

construction

Largest blast furnace

steel market

India

New blast furnace

construction

Import displacement

Coke Expansion Focused on 4 Key Markets

Early stages of permitting an anticipated 1.1 million tons of coke

per year potential new cokemaking facility in Kentucky

MOU for minority investment in Global Coke Limited |

12

0.4-0.5 million tons expected

surface mining

1.2 million tons

current production capacity

0.3 million tons HKCC acquisition

0.5 million tons expected Jewell

expansion

Coal Development

Doubling Our Production

Planned Growth

Current Operations

Underground

Mining

Surface

Mining

Selective

Reserve

Additions

2.4-2.5 million tons per annum

(Expect to double current production

by mid-2013)

+

+

+

=

106 million tons of proven

and probable reserves

Reserve life of 50+ years

Expected 500,000 tons per

year expansion of Jewell Coal

-

Mid-2013 completion

expected

-

Expect total cost of $25

million

Evaluating HKCC expansion

Limited highwall mining at

HKCC

Signed agreement to extract

additional surface tons

-

Expect 1.3 million tons

over 3 years beginning in

2012

Acquired Harold Keene Coal

Companies in January 2011

Evaluating selective,

opportunistic additions of

coal reserves |

13

$171

$187

$297

2008

2009

2010

$117

$159

$184

$157

$230

$227

2008

2009

2010

$840

$1,145

$1,327

2008

2009

2010

Historical Financial Summary

Total Revenues

Adjusted EBITDA

Note:

See Appendix for reconciliation.

Grey colored bars represent Pro Forma Adjusted EBITDA for ArcelorMittal settlement.

Net Cash Provided by Operating Activities

($ in millions)

Strong growth in earnings and cash flow driven by coke expansion

($ in millions)

($ in millions) |

14

722

714

715

1,214

1,164

1,140

690

928

1,103

62

635

2008

2009

2010

Q2 '11*

Jewell

Indiana Harbor

Haverhill

Granite City

2,626

2,868

3,593

Domestic Coke Financial Summary

(Jewell Coke & Other Domestic Coke)

Domestic Coke Production

Domestic Coke Pro Forma Adjusted EBITDA

(1)

for ArcelorMittal

Settlement and Coal Transfer Price Impacts

(Tons in thousands)

($ in millions, except per ton amounts)

Other

Domestic

Coke:

1,904

Other

Domestic

Coke:

2,154

Other

Domestic

Coke:

2,878

Jewell Coke

Other Domestic Coke

Pro Forma Adjusted EBITDA/ton

Other

Domestic

Coke:

745

922

$36

(1) For a reconciliation of Pro Forma Adjusted EBITDA to operating income, please

see the appendix.

168

276

301

177

*Q2 ‘11 scale is annualized

*Q2 ‘11 scale is annualized

$46

$41

$49

$11

$48

$36

$109

$25

$36/ton

$27/ton

$44/ton

$39/ton

2008

2009

2010

Q2 '11*

$94

$76

$159 |

15

1,233

1,214

1,277

334

1,179

1,134

1,104

340

54

73

149

24

2008

2009

2010

Q2 '11

Coal sales

Coal production

Coal purchases

Coal Mining Financial Summary

Coal Sales, Production and Purchases

Avg. Sales Price/Ton

(1)

and Cost/Ton

Coal Mining Pro Forma Adjusted EBITDA

(5)

for Coal Transfer Price

Impact

(Tons in thousands)

($ in millions, except per ton amounts)

Pro Forma Adjusted EBITDA

Pro Forma Adjusted EBITDA / ton

Coal cash cost

Purchased coal cost

($ per ton)

(5) For a reconciliation of Pro Forma Adjusted EBITDA to operating income, please see

the appendix. $11

(2)

(1)

Average Sales Price is the weighted average sales price for all coal sales volumes, includes

sales to affiliates and sales to Jewell Coke established via a transfer pricing

agreement. The transfer price per ton to Jewell Coke was $89.96, $100.19, $103.74 and

$156.12 for 2008, 2009, 2010 and Q2 ‘11, respectively.

(2)

Pro Forma Sales Price is the Average Sales Price adjusted to set the internal transfer price on

Jewell Coke coal purchase volumes equal to the Jewell Coke coal component contract

price. The per ton coal cost component included in the Jewell Coke contract was

approximately $106, $155, $130 and $165 for 2008, 2009, 2010, and Q2 ‘11 respectively.

(3)

Mining and preparation costs, excluding depreciation, depletion and amortization, divided by

coal production volume.

(4)

Costs of purchased raw coal divided by purchased coal volume.

$25/ton

$56/ton

$19/ton

$34/ton

2008

2009

2010

Q2 '11

$31

$69

$24

$80

$92

$106

$126

$41

$43

$88

$85

$147

$125

$162

$92

$100

$104

2008

2009

2010

Q2 '11

Average Sales Price

Pro Forma Sales Price

$155

$106

(3)

(4) |

16

Second Quarter Overview

(1) For a reconciliation of Adjusted EBITDA to net income and operating income,

please see the appendix. Q2

‘11

vs.

Q2

’10

•

Year-over-year quarterly results reflect unfavorable impact of

ArcelorMittal settlement, and relocation and public company readiness

costs •

Net Income Attributable to Net Parent Investment of $22.4 million in Q2 ‘11

vs. $44.3 million in Q2 ’10

•

Adjusted EBITDA

(1)

of $37.6 million in Q2 ‘11 vs. $68.7 million in Q2 ’10

Q2

‘11

vs.

Q1

’11

•

Improvement over Q1 ‘11 driven by stronger Indiana Harbor performance

and better utilization rates across all Coke Operations

•

Adjusted EBITDA

(1)

of $37.6 million in Q2 ‘11 vs. $26.6 million in Q1 ’11

|

17

Capital Expenditures

•

Expect 2011 Capital Expenditures of $231 million, up $15 million vs. 2010

•

Middletown and coal expansion represents expansion capital

•

First Half 2011 capital expenditures totaled $128 million

Capital Expenditures

$187

$170

$181

$28

$46

$50

$304

$215

$216

$231

2008

2009

2010

2011E

Ongoing

Expansion

In Millions

$289

$16 |

18

Cash Flows and Financial Position

Capital Structure

Liquidity

Growth Funding

Dividend Policy

•

Issued $700M in debt in the form of $300M Term

Loan and $400M Senior Notes

•

Repaid intercompany payable to Sunoco of $575 million with

balance of the net proceeds retained for general corporate purposes

•

Sufficient liquidity (cash and undrawn revolver) to

support growth strategy and allow opportunistic

acquisitions

•

Will continue to invest operating cash flows into

expansion projects

•

Dividends or share buybacks not considered at this

time |

19

Near-term Growth Drivers (2012/2013)

Middletown

•

On track for start-up in Q4

Indiana Harbor

•

No anticipated contractual production shortfall in 2012/2013

•

$50M –

$100M estimated spending to support contract extension

•

Contract renewal negotiations in process

Coal Expansion

•

Addressing tight labor market challenges

•

Expect to reach 350K tons annualized rate in 2012 and 500K annualized

rate by mid-2013

•

Executed contract mining agreement with Revelation Energy, LLC to

mine approximately 1.3 million tons of surface reserves over 3 years

|

20

Long-term Growth Drivers (2013 and Beyond)

International

–

Brazil, China and India

•

Steel is growing in emerging economies, led by China and India

•

India is attractive for us given expected growth in primary coke

demand and coke supply/demand balance

•

Memorandum of Understanding with Global Coke

Next U.S. Coke Plant

•

Permitting process in Kentucky underway

•

Also assessing alternative sites in other states

•

Expect plant to be 1.1 million tons in capacity with portion reserved for

market coke sales

•

Engineering design targeting CAPEX/ton reductions over Middletown

|

21

Appendix |

22

Management Team

Name

Position

Years of

experience

Previous experience

Fritz Henderson

Chief Executive Officer

26

General Motors

Michael Thomson

President and Chief Operating Officer

28

Public Service Enterprise Group, Corning

Mark Newman

Senior Vice President and Chief Financial

Officer

25

Ally Financial, General Motors

Denise Cade

Senior Vice President, General Counsel

and Corporate Secretary

21

PPG Industries, Shaw Pittman LLP

Matthew McGrath

Senior Vice President, Corporate Strategy

and Business Development

21

Public Service Enterprise Group

Michael White

Senior Vice President, Operations

30

Sunoco, Lyondell-Equistar, Exxon

Jim Mullins

Vice President, Coal Operations

35

Arch Coal, Island Creek Coal

Fay West

Vice President and Controller

19

United Continental, PepsiAmericas

Ryan Osterholm

Director, Finance and Investor Relations

13

Public Service Enterprise Group

SunCoke’s management team represents a combination of deep industry knowledge,

international experience and broad management/technical skills

|

23

Board of Directors

Name

Affiliation

Employment History

Board affiliations

Fritz Henderson

SunCoke Energy

SunCoke Energy, Inc; General Motors

Compuware Corp.

Alvin Bledsoe

Independent

PricewaterhouseCoopers LLP

Crestwood Midstream Partners

Robert Darnall

Independent

Inland Steel Industries; Ispat North America, Inc.

Stacy Fox

Sunoco

Sunoco, Inc.; Roxbury Group; Collins & Aikman

Corporation

Peter Hamilton

Independent

Brunswick Corporation

Spectra Energy Corp.

Michael Hennigan

Sunoco

Sunoco Logistics Partners L.P.; Sunoco, Inc.

Brian MacDonald

Sunoco

Sunoco, Inc.; Dell, Inc.

Sunoco Logistics and American

Red Cross (Southeastern, PA

chapter)

Charmian Uy

Sunoco

Sunoco, Inc.; American Express; General Motors

Dennis Zeleny

Sunoco

Sunoco, Inc.; Sunoco Logistics Partners L.P.;

Caremark RX, LLC

|

24

Definitions

•

Adjusted

EBITDA

represents

earnings

before

interest,

taxes,

depreciation,

depletion

and

amortization

(“EBITDA”)

adjusted for sales discounts and the deduction of income attributable to

non-controlling interests in our Indiana Harbor cokemaking

operations.

EBITDA

reflects

sales

discounts

included

as

a

reduction

in

sales

and

other

operating

revenue.

The sales discounts represent the sharing with our customers of a portion of

nonconventional fuels tax credits, which reduce our income tax expense.

However, we believe that our Adjusted EBITDA would be inappropriately penalized if

these

discounts

were

treated

as

a

reduction

of

EBITDA

since

they

represent

sharing

of

a

tax

benefit

which

is

not

included

in EBITDA. Accordingly, in computing Adjusted EBITDA, we have added back these

sales discounts. Our Adjusted EBITDA also reflects the deduction of income

attributable to noncontrolling interest in our Indiana Harbor cokemaking

operations. EBITDA and Adjusted EBITDA do not represent and should not be

considered alternatives to net income or operating income under GAAP and may

not be comparable to other similarly titled measures of other businesses.

Management believes Adjusted EBITDA is an important measure of the operating

performance of the company’s assets and is indicative of the

Company’s ability to generate cash from operations. •

Pro

Forma

Adjusted

EBITDA

represents

Adjusted

EBITDA

adjusted

for

the

ArcelorMittal

settlement

impact

and

coal

transfer price impacts. The Jewell Coke and Coal Mining results have been adjusted

to set the internal transfer price to equal the coal component contract

price in Jewell Coke’s coke sales price for coal sales volumes sold to Jewell Coke

under the transfer pricing agreement. Management believes Pro Forma Adjusted

EBITDA provides transparency into the underlying profitability of

these respective segments for the periods presented. |

25

Reconciliations

($ in million, except where indicated)

(1)

Pro forma impact from equalizing coal transfer price to Jewell Coke with Jewell Coke coal cost

component. Assumes coal-to-coke yield of 68%. Jewell

Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

Net Income

$146

Add: Depreciation, Depletion and Amortization

48

Subtract: Interest Income (Primarily from Affiliates)

(24)

5

Subtract: Capitalized Interest

(1)

Add (Subtract): Income Tax Expense (Benefit)

47

EBITDA

$151

$74

$15

($4)

($14)

$222

–

12

–

–

–

12

–

(7)

–

–

–

(7)

Adjusted EBITDA

$151

$79

$15

($4)

($14)

$227

Add (Subtract): Pro Forma Impact of ArcelorMittal Settlement

(78)

18

–

–

–

(60)

4

13

–

–

–

16

(1)

(28)

–

–

28

–

–

Pro Forma Adjusted EBITDA

$49

$109

$15

$24

($14)

$184

Sales Volumes (thousands of tons)

721

2,917

–

1,277

–

Pro Forma Adjusted EBITDA per Ton ($ per ton)

$69

$37

$19

Operating Income (Loss)

$147

$39

$15

($11)

($15)

$174

Add: Depreciation, Depletion and Amortization

4

35

0

8

1

48

EBITDA

$151

$74

$15

($4)

($14)

$222

Fiscal year ended December 31, 2010

Add: Sales Discounts Provided to Customers Due to Sharing of Nonconventional Fuels Tax Credits

Add (Subtract): Net (Income) Loss Attributable to Noncontrolling Interests

Add: Interest Cost – Affiliate

Add: Legal and Settlement Charges Related to ArcelorMittal Settlement and Indiana Harbor

Arbitration Add (Subtract): Pro Forma Coal Transfer Price Impact |

26

Reconciliations (Cont’d)

($ in million, except where indicated)

(1)

Pro forma impact from equalizing coal transfer price to Jewell Coke with Jewell Coke coal cost

component. Assumes coal-to-coke yield of 68%. Jewell

Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

Net Income

$211

Add: Depreciation, Depletion and Amortization

32

Subtract: Interest Income (Primarily from Affiliates)

(25)

6

Subtract: Capitalized Interest

(1)

Add (Subtract): Income Tax Expense (Benefit)

21

EBITDA

$182

$36

$23

$11

($9)

$244

–

8

–

–

–

8

–

(22)

–

–

–

(22)

Adjusted EBITDA

$182

$23

$23

$11

($9)

$230

Add (Subtract): Pro Forma Impact of ArcelorMittal Settlement

(84)

13

–

–

–

(71)

(1)

(58)

–

–

58

–

–

Pro Forma Adjusted EBITDA

$41

$36

$23

$69

($9)

$159

Sales Volumes (thousands of tons)

694

2,119

1,214

Pro Forma EBITDA per Ton ($ per ton)

$59

$17

$56

Operating Income (Loss)

$178

$15

$23

$5

($9)

$212

Add: Depreciation, Depletion and Amortization

5

22

0

6

0

32

EBITDA

$182

$36

$23

$11

($9)

$244

Fiscal year ended December 31, 2009

Add: Sales Discounts Provided to Customers Due to Sharing of Nonconventional Fuels Tax Credits

Add (Subtract): Net (Income) Loss Attributable to Noncontrolling Interests

Add: Interest Cost – Affiliate

Add (Subtract): Pro Forma Coal Transfer Price Impact |

27

Reconciliations (Cont’d)

($ in million, except where indicated)

(1)

Pro forma impact from equalizing coal transfer price to Jewell Coke with Jewell Coke coal cost

component. Assumes coal-to-coke yield of 68%. Fiscal year ended December 31,

2008 Jewell

Coke

Other

Domestic Coke

International

Coke

Coal

Mining

Corporate

and Other

Total

Net Income

$133

Add: Depreciation, Depletion and Amortization

25

Subtract: Interest Income (Primarily from Affiliates)

(28)

11

Subtract: Capitalized Interest

(4)

Add (Subtract): Income Tax Expense (Benefit)

38

EBITDA

$119

$50

$5

$14

($13)

$175

–

1

–

–

–

1

–

(19)

–

–

–

(19)

Adjusted EBITDA

$119

$32

$5

$14

($13)

$157

Add (Subtract): Pro Forma Impact of ArcelorMittal Settlement

(56)

16

–

–

–

(40)

Add (Subtract): Pro Forma Coal Transfer Price Impact

(1)

(17)

–

–

17

–

–

Pro Forma Adjusted EBITDA

$46

$48

$5

$31

($13)

$117

Sales Volumes (thousands of tons)

727

1,901

1,233

Pro Forma Adjusted EBITDA per Ton ($ per ton)

$63

$25

$25

Operating Income (Loss)

$114

$35

$5

$10

($13)

$151

Add: Depreciation, Depletion and Amortization

5

15

0

4

0

25

EBITDA

$119

$50

$5

$14

($13)

$175

Add: Sales Discounts Provided to Customers Due to Sharing of Nonconventional Fuels Tax Credits

Add (Subtract): Net (Income) Loss Attributable to Noncontrolling Interests

Add: Interest Cost – Affiliate |

28

Reconciliations (Cont’d)

Jewell Coke

Other

Domestic Coke

International

Coke

Coal Mining

Corporate

and Other

Total

Net Income

$23,993

Add: depreciation, depletion and amortization

14,605

Subtract: interest income (primarily from affiliates)

(5,763)

1,723

Subtract: capitalized interest

(399)

Add (Subtract): income tax expense (benefit)

1,881

EBITDA

$12,892

$23,695

$843

$9,144

($10,534)

$36,040

Add: sales discounts provided to customers due to sharing of nonconventional fuels tax

credits 3,174

3,174

(1,573)

(1,573)

Adjusted EBITDA

$12,892

$25,296

$843

$9,144

($10,534)

$37,641

Add (Subtract): coal transfer price impact

(2,334)

2,334

-

Pro Forma Adjusted EBITDA without coal transfer impact

$10,558

$25,296

$843

$11,478

($10,534)

$37,641

Sales Volumes (thousands of tons)

170

757

412

334

Pro Forma Adjusted EBITDA per Ton

$62

$33

$34

Operating Income (Loss)

$11,559

$14,059

$788

$5,964

($10,935)

$21,435

Add: Depreciation, Depletion and Amortization

1,333

9,636

55

3,180

401

14,605

EBITDA

$12,892

$23,695

$843

$9,144

($10,534)

$36,040

For the Three Months Ended June 30, 2011 (Unaudited)

($ in million, except where indicated)

Add (Subtract): net (income) loss attributable to noncontrolling interests

Add:

interest

cost -

affiliate |

29

Reconciliations (Cont’d)

Jewell Coke

Other

Domestic Coke

International

Coke

Coal Mining

Corporate

and Other

Total

Net Income

$47,550

Add: depreciation, depletion and amortization

11,107

Subtract: interest income (primarily from affiliates)

(6,039)

Add:

interest

1,701

Subtract: capitalized interest

(127)

Add (Subtract): income tax expense (benefit)

14,774

EBITDA

$53,044

$18,716

$7

$107

($2,908)

$68,966

2,980

2,980

(3,256)

(3,256)

Adjusted EBITDA

$53,044

$18,440

$7

$107

($2,908)

$68,690

Add (Subtract): pro forma impact of ArcelorMittal settlement

(23,600)

4,300

(19,300)

Add (Subtract): coal transfer price impact

(15,219)

15,219

-

Pro Forma Adjusted EBITDA without ArcelorMittal settlement and coal transfer price impact

$22,740

$7

$15,326

($2,908)

$49,390

Sales Volumes (thousands of tons)

191

718

422

314

Pro Forma Adjusted EBITDA per Ton

$74

$32

$49

Operating Income (Loss)

$51,945

$10,793

($18)

($1,818)

($3,043)

$57,859

Add: Depreciation, Depletion and Amortization

1,099

7,923

25

1,925

135

11,107

EBITDA

$53,044

$18,716

$7

$107

($2,908)

$68,966

For the Three Months Ended June 30, 2010 (Unaudited)

$14,225

($ in million, except where indicated)

Add (subtract): net (income ) loss attributable to noncontrolling interests

Add: sales discounts provided to customers due to sharing of nonconventional fuels tax

credits cost -

affiliate |

30

($ in million, except where indicated)

Reconciliations (Cont’d)

Jewell Coke

Other

Domestic Coke

International

Coke

Coal Mining

Corporate

and Other

Total

Net Income

$5,655

Add: depreciation, depletion and amortization

13,020

Subtract: interest income (primarily from affiliates)

(5,717)

1,500

Subtract: capitalized interest

(312)

Add (Subtract): income tax expense (benefit)

3,139

EBITDA

$19,054

($857)

$988

$4,296

($6,196)

$17,285

Add: sales discounts provided to customers due to sharing of nonconventional fuels tax

credits 3,125

3,125

6,171

6,171

Adjusted EBITDA

$19,054

$8,439

$988

$4,296

($6,196)

$26,581

Add (Subtract): coal transfer price impact

(8,042)

8,042

-

Pro Forma Adjusted EBITDA without coal transfer price impact

$11,012

$8,439

$988

$12,338

($6,196)

$26,581

Sales Volumes (thousands of tons)

175

697

362

386

Pro Forma Adjusted EBITDA per Ton

$63

$12

$32

Operating Income (Loss)

$17,953

($9,472)

$935

$1,577

($6,728)

$4,265

Add: Depreciation, Depletion and Amortization

1,101

8,615

53

2,719

532

13,020

EBITDA

$19,054

($857)

$988

$4,296

($6,196)

$17,285

For the Three Months Ended March 31, 2011 (Unaudited)

Add:

interest

cost -

affiliate

Add (Subtract): net (income) loss attributable to noncontrolling interests

|