Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - DUNKIN' BRANDS GROUP, INC. | d8k.htm |

Dunkin’

Dunkin’

Brands Group, Inc.

Brands Group, Inc.

August 2011

August 2011

Exhibit 99.1 |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. Forward-looking statements

Certain

information

contained

in

this

presentation,

particularly

information

regarding

future

economic

performance, finances, and expectations and objectives of management constitutes

forward-looking statements. Forward-looking statements can be

identified by the fact that they do not relate strictly to historical

or

current

facts

and

are

generally

contain

words

such

as

“believes,”

“expects,”

“may,”

“will,”

“should,”

“seeks,”

“approximately,”

“intends,”

“plans,”

“estimates”

or “anticipates”

or similar expressions.

Our forward-looking statements are subject to risks and uncertainties such as

the ongoing level of profitability of our franchisees and licensees, prices

and availability of coffee and other raw materials, our substantial

indebtedness, changes in the quick service restaurant industry, ability or inability to meet our

growth projections as well as other risks described more fully in our filings with

the Securities and Exchange Commission. These risks and uncertainties

may cause actual results to differ materially from those projected or

implied by the forward-looking statement. Forward-looking statements

are based on current expectations and assumptions and currently available

data

and

are

neither

predictions

nor

guarantees

of

future

events

or

performance.

You

should

not

place

undue reliance on forward-looking statements, which speak only as of the date

hereof. We do not undertake to update or revise any

forward-looking statements after they are made, whether as a result of

new

information,

future

events,

or

otherwise,

except

as

required

by

applicable

law.

Regulation G

This presentation contains certain non-GAAP measures which are provided to

assist in an understanding of the Dunkin’

Brands Group, Inc. business and its performance.

These measures should always

be

considered in conjunction with the appropriate GAAP measure.

Reconciliations of non-GAAP amounts to

the relevant GAAP amount are provided as an attachment to these slides.

2 |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. Strong platform for continued growth

Our key business strengths

Strong and established brands with leading market positions

Two strong and highly recognized global brands that generated LTM

franchisee-reported sales of $7.9 bn

(1)

Strong comp store sales trajectory

Significant opportunities to grow brands globally

Over 16,000 global locations with significant opportunity for domestic and

international growth Invested during downturn to position ourselves for

growth Franchised business model provides platform for growth

Nearly 100% franchised business model generates high margins with low capex

requirements, driving cash flow generation

Store-level

economics

generates

franchisee

demand

for

additional

restaurants

3

1. Last twelve months (“LTM”) ending June 25, 2011

Highly experienced, aligned and motivated management team with franchise “operating”

philosophy |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. Two leading global brands

each with over 60 years of heritage

Source:

NPD Group/CREST for year ending February 2011; Omnibus Awareness Study, July

2010; Brand Keys

4

Over 95% aided brand awareness in U.S.

#1 in QSR customer loyalty for 5 straight years

1 bn+ cups of coffee sold in the U.S. annually

#1 position in Hot/Regular/Flavored/Decaf Coffee,

Iced Coffee, Donuts, Bagels and Muffins

Over 50% share of New England coffee servings and

morning meal traffic

36 U.S. states and in 31 other countries

1,000+ ice cream flavors

95% aided brand awareness in U.S

#1 hard serve ice cream position in U.S.

#1 market share positions in Fast Food Ice Cream

category in Japan and South Korea in 2010

45 U.S. states and in 46 other countries

America Runs on Dunkin’

®

More Flavors, More Fun™ |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. LTM Franchisee-Reported Sales

1

U.S.

$6.0 bn

(77%)

Intl

$1.8bn

(23%)

$6.2bn

(78%)

$1.7bn

(22%)

Global Points of Distribution

2

9,867

(60%)

6,560

(40%)

U.S.

9,348

(57%)

Intl

7,079

(43%)

Substantial global platform across both brands

5

1. Last twelve months (“LTM”) ending June 25, 2011

2. Data through Q2 2011 |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 6

Note: Fiscal year-end changed from August to December starting in 2006. POD

represents a single store or kiosk; combo stores count as one POD for each

brand. Franchisee-reported sales ($mm)

Franchisee-reported sales ($mm)

PODs

PODs

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. Consistent track record of growth

|

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 7

Highly experienced management team

Name

Title

Past experience

Nigel Travis

Chief Executive Officer, Dunkin’

Brands and President, Dunkin’

Donuts U.S.

President

&

Chief

Executive

Officer

of

Papa

John’s,

President

&

Chief

Operating

Officer

of

Blockbuster

and

SVP Burger King

Neil Moses

Chief Financial Officer

Executive

Vice

President

/

Chief

Financial

Officer

of

Parametric

Technology

Corporation

John Costello

Chief Global Marketing & Innovation

Officer

Executive Vice President of Merchandising and Marketing at Home Depot, Senior

Executive Vice President of Sears, Senior Vice President of Marketing &

Sales at Pepsi-Cola USA and Chief Global Marketing Officer of

Yahoo!

Paul Twohig

Chief Operating Officer, Dunkin’

Donuts U.S.

Senior

Vice

President

of

Starbucks;

Executive

Vice

President

and

Chief

Operating

Officer

of

Panera

Bread

Company

John Dawson

Chief Development Officer, U.S.

Vice President of Worldwide Restaurant Development for McDonald’s

Corporation Neal Yanofsky

President, International

President of Panera Bread Company

Bill Mitchell

Senior Vice President & Brand

Officer, Baskin-Robbins U.S.

President of Global Operations for Papa John’s

Richard Emmett

Senior Vice President & General

Counsel

Former Executive Vice President and Chief Legal Officer of Quiznos, Senior Vice

President and General Counsel of Papa Johns

Christine Deputy

Senior Vice President, Chief Human

Resources Officer

Vice President of Asia Pacific Human Resources for Starbucks

Karen Raskopf

Senior Vice President, Chief

Communications Officer

Senior Vice President of Corporate Communications for 7-Eleven and

Blockbuster Dan Sheehan

Chief Information Officer

Senior Vice President/Chief Information Officer for ADVO

Srinivas Kumar

President & Chief Operating Officer,

Baskin-Robbins International

General Manager of Galadari (largest Baskin-Robbins licensee worldwide)

Tony Pavese

Chief Operating Officer, Dunkin’

Donuts International

Chief Operating Officer for Popeye’s International

|

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 8

Our growth strategy |

Focused growth strategies across each segment

8% of 2010 revenue

73% of 2010 revenue

19% of 2010 revenue

Increase comparable

store sales and

profitability in DD U.S.

Continue DD U.S.

contiguous store

expansion

Increase comparable

store sales growth of BR

U.S.

Drive accelerated

international growth

across both brands

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 9 |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 10

Dunkin’

Donuts U.S. strategy

Drive comparable store sales and profitability

•

Successful product innovation record with strong pipeline

•

Differentiated brand platform with high-impact marketing

•

Operations-focused culture driving improved in-store

experience

Accelerate profitable and contiguous POD growth

•

Among one of the industry-leading expansion track records

•

Significant opportunity across U.S. |

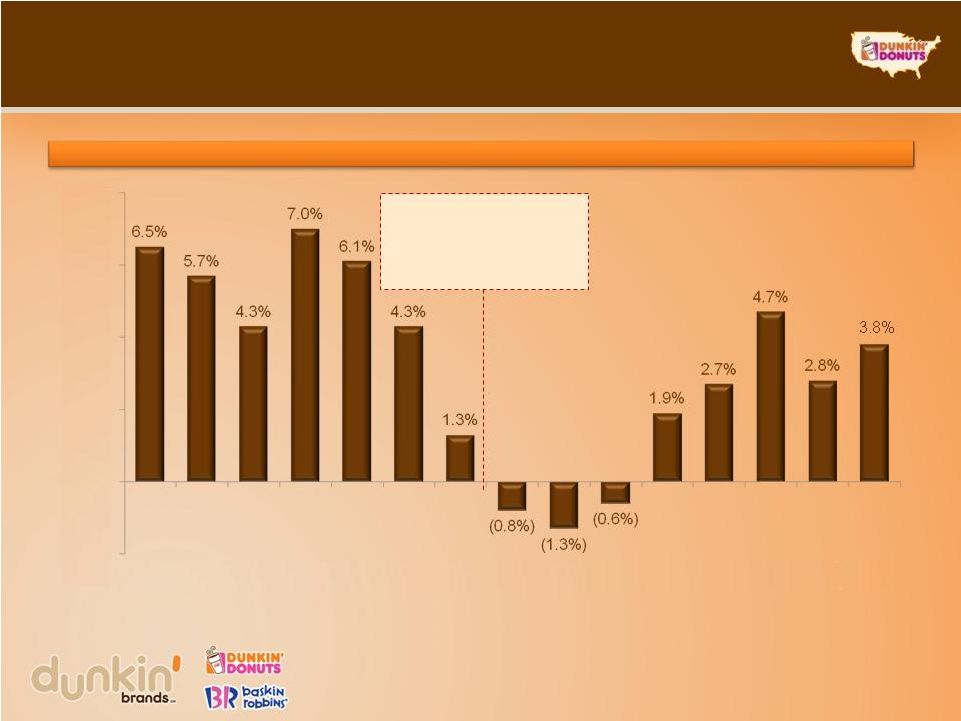

11

Strong comp growth momentum

Resilient comp performance throughout economic cycles

Note: Fiscal year-end changed from August to December starting in 2006

45 consecutive

quarters of

comparable store

sales growth

Confidential information: Copying, dissemination or distribution of this information is strictly

prohibited. 2001

2002

2003

2004

2005

2006

2007

2008

2009

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

(2.0%)

0.0%

2.0%

4.0%

6.0%

8.0%

Dunkin’

Donuts U.S. comparable store sales growth |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 12

Powerful track record of product innovation

1995

1996

1998

Fruit Coolatta

®

2000

Dunkaccino

®

Hot chocolate

2001

Vanilla Chai

2003

2004

2005

Turbo Ice

®

Tropicana

®

Coolatta

®

9 iced coffee and hot

coffee flavors

2008

DD Smart

®

Flatbreads

2010

2009

Wake-Up Wrap

®

2011

Big n’

Toasty

Shaped donuts

Dunkin’

K-Cups

Frozen Iced Tea

Hot

espresso

platform

Iced lattes

Bagel

twists

Coolatta

®

mixology

PM

snacks

Hazelnut and

French Vanilla

Coffee

excellence

Breakfast

sandwiches

Bagels |

High

impact marketing with broad reach 13

Strong heritage in traditional media

Growing interactive, internet

and social media

Produce news “buzz”

from Limited Time

Offerings

TV, Radio, Print, PR, POP,

Local Marketing

Strong grocery

coffee business

Growing loyalty

program

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 14

Intense focus on restaurant level

operational support

Clearly defined store

standards

Strong remodel program

Strong support to

franchisees and

restaurant managers with

training and marketing

Effective systems for

back-office management

People &

systems

Great guest

experience

Profitable

topline sales

Strong guest satisfaction score trends |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 15

Our U.S. development opportunity |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 16

An industry leader in U.S. development

Disciplined development process

Attracting and selecting quality

franchisees

Rigorous market planning

and site selection

An industry leader in U.S.

development

Phased market

development

2010 net U.S. store development

Source:

SEC

filings

and

Dunkin’

Brands

-148

+20

806 |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 17

Platform to drive accelerated development pace

Tremendous potential for

contiguous growth

•

200+ million in untapped population

New store pipeline momentum

•

50% increase in 2010 over 2009

Expanding lender base

Constant focus on unit economics

•

Approximately 23% reduction in

build-out cost for end-cap drive-thru

locations in the last three years

•

Over $220mm reduction in supply

chain costs between 2008 and Q1

2011

Store-level

economics

–

traditional

stores

Average initial capex

(1)

$474,000

Average unit volumes

(1)

$855,000

Sales to capital ratio

1.8x

1. 2010 cohort of new traditional stores, excludes gas & convenience

90%+ of new development in

2010 from existing franchisees

Unit economics generate new

franchisee demand |

Confidential information: Copying, dissemination or distribution of this

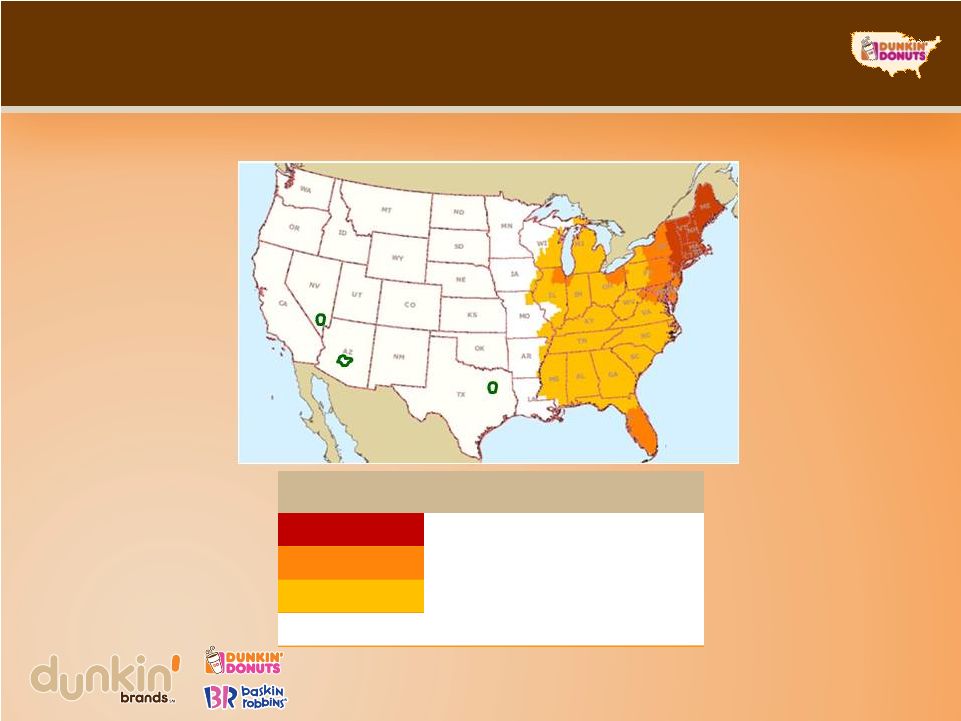

information is strictly prohibited. Region

Population

(mm)

Stores

(1)

Penetration

Core

36.0

3,720

1:9,700

Eastern Established

53.8

2,151

1:25,000

Eastern Emerging

88.7

792

1:112,100

West

130.0

109

1:1,193,000

18

Significant opportunity for profitable growth

1. As of 12/25/2010 |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 19

Proven ability to increase penetration

in Established markets

Core

Established

Emerging

33%

2010 net new

open (% of total)

(1)

36%

28%

West

3%

1. Represents entire region, not select DMAs

Total penetration of select

established markets |

Confidential information: Copying, dissemination or distribution of this

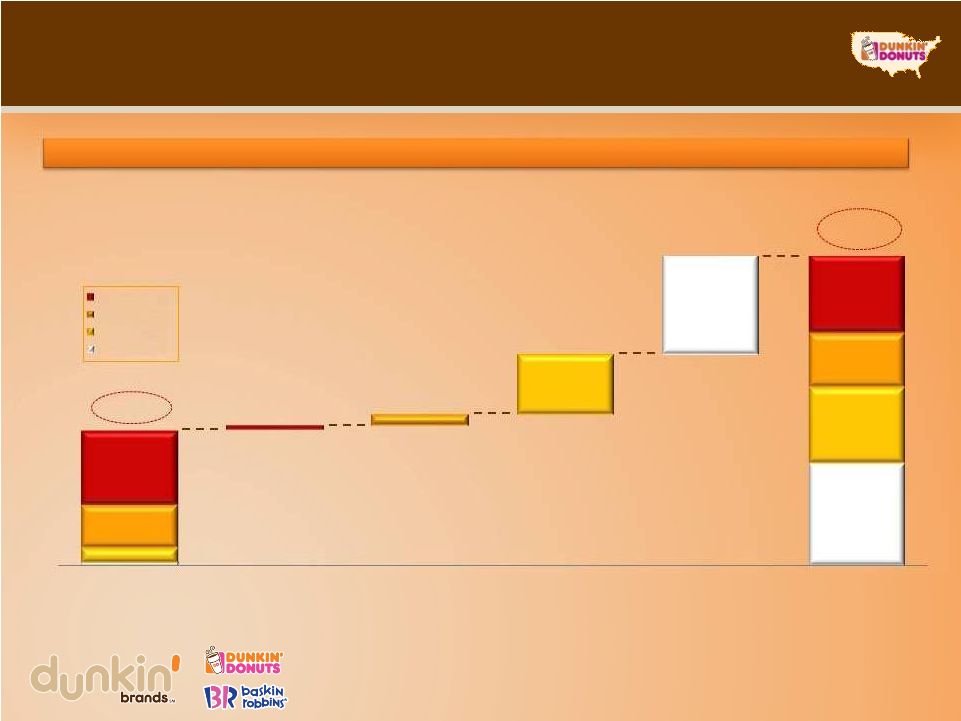

information is strictly prohibited. 20

Significant long-term expansion opportunity

~15,000

6,772

DD pro forma penetration

1:9,200

1:20,000

1:23,000

1:25,000

1:20,000

~5,109

~3,792

2,151

~2,701

3,720

~3,920

~200

~550

~3,000

5,000

2010

Core

Established

Emerging

West

Long

-

term

Core

Established

Emerging

West

109

792

~

Dunkin’

Donuts U.S. bridge to long-term goal (existing stores + new net

development) |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 21

Our international growth opportunity |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. History of successful international

growth particularly in Asia Dunkin’

Brands is among the largest U.S. QSR companies overseas

by unit count

Renewed focus on strengthening international segments under new

leadership

Emphasis on improving penetration in existing markets, given strong

concept acceptance

Leverage brands’

strengths to grow in markets with significant potential

•

Baskin-Robbins has close-to-universal product appeal

•

Dunkin’

Donuts’

platform allows for localization and flexibility

Drive accelerated international growth

for both brands

22

2007

–

2010

International

Growth

13% International SWS CAGR

9% International POD CAGR |

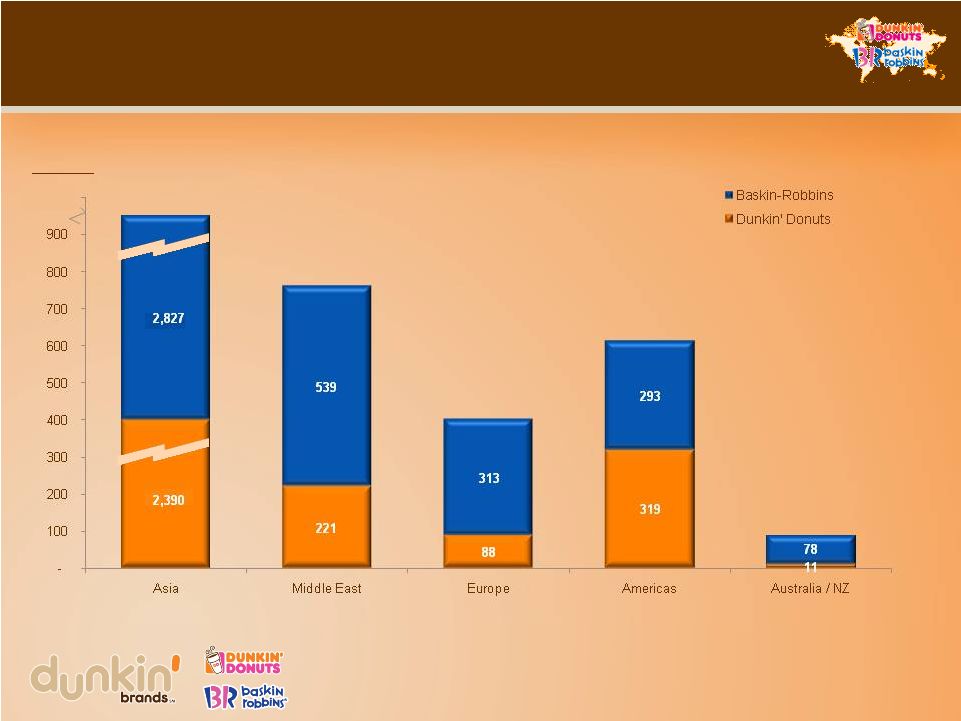

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. Note:

Unit count as of Q2 2011

Both brands have strong international

presence with significant growth potential

23

Store count:

6,000

5,217

401

324

89

760 |

24

Dynamic and differentiated international brands

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. Drive growth in established markets

(Japan, Korea and Middle East)

Accelerate China growth for both brands

Build-out emerging markets (Russia and Latin America)

Launch Dunkin’

Donuts in India

450 –

500 planned 2011 net openings

Focused international growth priorities

25 |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 26

Continue to re-energize Baskin-Robbins U.S.

Leveraging 65-year heritage and 95% aided brand awareness

Implementing focused strategic plan aimed at improving comp sales

•

Sharpening brand differentiation

•

Improving operations and marketing

•

Optimizing supply chain to increase franchisee profitability

•

Introducing standardized retail technology

•

Accelerating store transfer program

Early results are encouraging

•

Reached an all-time high in overall guest satisfaction

•

Increased franchisee engagement

•

Improving comp sales trend |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 27

Financial highlights |

28

Our unique investor proposition

Asset-lite model / low capex requirements

•

Restaurant buildout costs borne by franchisees

•

Franchisee-owned

DD

supply

chain

network

Less affected by store-level costs (i.e. commodities)

than most QSRs

•

Revenues driven off franchisee topline sales

•

Collaboration with franchisees to maximize

restaurant profitability

Proven ability to drive comp store sales growth

Accelerating POD development

Leverageable cost structure with industry-leading

operating margins

Ability to further leverage G&A

Cash flow generation and deleveraging

1.

Represents operating income before amortization and impairment

Attractive business model

Long-term growth opportunity

FY 2010 operating income margin

2010 capex vs. peers (% of EBITDA)

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. Pro Forma capital structure

29

($mm)

Actual

6/25/11

Pro forma

IPO

6/25/11

Cash and Cash Equivalents

(1)

$146

$129

Revolving Credit Facility

0

0

Term Loan B

(2)

1,497

1,497

Capital leases

5

5

Total Secured Debt

$1,502

$1,502

Senior Unsecured Notes

(2)

375

0

Total Debt

$1,877

$1,502

Total Secured Net Debt

(3)

/ Adjusted EBITDA

(4)

4.9x

4.9x

Total Net Debt

(3)

/ Adjusted EBITDA

(4)

6.2x

4.9x

Adjusted EBITDA

(4)

/ Interest Expense

(5)

2.4x

4.5x

1.

Amount includes cash held for advertising funds or reserved for gift

card/certificate programs 2.

Debt balances exclude original issue discount

3.

Total debt is net of original issue discount and excludes cash held or reserved for

gift card/gift certificate programs of $59mm 4.

Adjusted EBITDA reflects LTM 6/25/2011 Credit Agreement EBITDA of $289.2mm

5.

Actual interest expense is $120.5mm (representing annualized interest

post-November 2010 refinancing, as per the Credit Agreement), and $64.8mm for pro forma IPO

Pro Forma capital structure at 6/25/2011 |

30

Long-term earnings model

Strong, predictable revenue growth

•

U.S. consolidated comps in the

2–4% range

•

Total net unit development of

approximately 3–5% with

opportunity to accelerate

Highly leverageable cost structure

•

Drives margin expansion of

150–200 bps per year

Strong free cash flow

•

Facilitates earnings growth through

deleveraging or shareholder payout

6–8% revenue growth

10–12% operating income

(excl. intangibles

amortization) growth

15%+ EPS (excl. intangibles

amortization) growth

Drivers

Long-term targets

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. Strong platform for continued growth

Our key business strengths

Strong and established brands with leading market positions

Two strong and highly recognized global brands that generated LTM

franchisee-reported sales of $7.9 bn

(1)

Strong comp store sales trajectory

Significant opportunities to grow brands globally

Over 16,000 global locations with significant opportunity for domestic and

international growth Invested during downturn to position ourselves for

growth Franchised business model provides platform for growth

Nearly 100% franchised business model generates high margins with low capex

requirements, driving cash flow generation

Store-level

economics

generates

franchisee

demand

for

additional

restaurants

31

1. Last twelve months (“LTM”) ending June 25, 2011

Highly experienced, aligned and motivated management team with franchise “operating”

philosophy |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 32 |

Confidential information: Copying, dissemination or distribution of this

information is strictly prohibited. 33

Attachment –

Non-GAAP Reconciliation

Fiscal Year 2010

($ in mm)

As Percentage of

Total Revenue

Operating income

$193.5

33.5%

Adjustments:

Amortization of intangible assets

32.5

5.6%

Impairment charges

7.1

1.2%

Adjusted operating income

$233.1

40.4%

Adjusted operating income is reconciled to operating income for fiscal year 2010 as

follows: |