Attached files

| file | filename |

|---|---|

| EX-31.1 - Sino Agro Food, Inc. | v233570_ex31-1.htm |

| EX-32.1 - Sino Agro Food, Inc. | v233570_ex32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q/A

(Amendment No. 1)

(Mark One)

For the quarterly period ended March 31, 2011

OR

|

¨

|

TRANSACTION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ___________________________ to ___________________________

Commission file number: 000-54191

|

SINO AGRO FOOD, INC.

|

|

(Exact Name of Registrant as Specified in Its Charter)

|

|

Nevada

|

33-1219070

|

|

|

(State of Other Jurisdiction of Incorporation or

Organization)

|

(I.R.S. Employer Identification Number)

|

|

|

Room 3711, China Shine Plaza

No. 9 Lin He Xi Road

Tianhe County, Guangzhou City, P.R.C.

(201) 471-0988

|

510610

|

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

|

(860) 20 22057860

|

(Registrant’s Telephone Number, Including Area Code)

|

N/A

|

(Former Name, Former Address and Former Fiscal Year, If Changed Since Last Report)

Copies to:

The Sourlis Law Firm

Joseph M. Patricola, Esq.

The Courts of Red Bank

130 Maple Avenue, Suite 9B2

Red Bank, New Jersey 07701

Direct: (732) 618-2843

Office: (732) 530-9007

Fax: (732) 530-9008

JoePatricola@SourlisLaw.com

www.SourlisLaw.com

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” "non-accelerated filer" and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

|

¨

|

Accelerated filer

|

¨

|

|

Non-accelerated filer

|

¨

|

Smaller reporting company

|

x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

As of August 16, 2011, there were 62,894,262 shares of Common Stock issued and outstanding.

EXPLANATORY NOTE

This Amendment No. 1 on Form 10-Q/A (the “Amendment”) amends the Quarterly Report on Form 10-Q of Sino Agro Food, Inc. for the fiscal quarter ended March 31, 2011, originally filed with the Securities and Exchange Commission (“SEC”) on May 20, 2011 (the “Original Filing”). This Form 10-Q/A revises certain disclosures related to Management’s Discussion and Analysis, in particular the discussion pertaining to the Consolidated Results of Operations for the three months ended March 31, 2011, and revisions to the Statements of Cash Flows, in particular disclosures related to detailed cash flows of discontinued operations. This Form 10-Q/A does not attempt to modify or update any other disclosures set forth in the Original Filing. There are no changes to the body of the Form 10-Q other than the above-mentioned corrections. Additionally, this amended Form 10-Q/A, except for the amended information, speaks as of the filing date of the Original Filing and does not update or discuss any other developments affecting us subsequent to the date of the Original Filing.

TABLE OF CONTENTS

|

Page

|

||

|

PART I – FINANCIAL INFORMATION

|

||

|

Item 1.

|

Financial Statements

|

1

|

|

Item 2.

|

Management’s Discussion and Analysis of Financial Condition and Plan of Operations

|

33

|

|

Item 3.

|

Quantitative and Qualitative Disclosures About Market Risk

|

47

|

|

Item 4T.

|

Controls and Procedures

|

47

|

|

PART II – OTHER INFORMATION

|

||

|

Item 1.

|

Legal Proceedings

|

48

|

|

Item 1A.

|

Risk Factors

|

48

|

|

Item 2.

|

Unregistered Sale of Equity Securities and Use of Proceeds

|

48

|

|

Item 3.

|

Defaults Upon Senior Securities

|

48

|

|

Item 4.

|

Submission of Matters to a Vote of Security Holders

|

48

|

|

Item 5.

|

Other Information

|

48

|

|

Item 6.

|

Exhibits

|

51

|

|

SIGNATURES

|

52

|

|

SINO AGRO FOOD, INC. AND SUBSIDIARIES

QUARTERLY FINANCIAL REPORT

FOR THE THREE MONTHS ENDED MARCH 31, 2011

SINO AGRO FOOD, INC.

CONSOLIDATED BALANCE SHEETS

|

March 31, 2011

|

December 31, 2010

|

|||||||

|

(Unaudited)

|

(Audited)

|

|||||||

|

$

|

$

|

|||||||

|

ASSETS

|

||||||||

|

Current assets

|

||||||||

|

Cash and cash equivalents

|

482,916 | 3,890,026 | ||||||

|

Inventories

|

1,799,040 | 8,913,127 | ||||||

|

Deposits and prepaid expenses

|

5,346,988 | 14,229,711 | ||||||

|

Accounts receivable, net of allowance for doubtful accounts

|

8,421,189 | 12,803,771 | ||||||

|

Other receivables

|

59,253,946 | 3,967,680 | ||||||

|

Total current assets

|

75,304,079 | 43,804,315 | ||||||

|

Property and equipment

|

||||||||

|

Property and equipment, net of accumulated depreciation

|

2,529,149 | 17,155,782 | ||||||

|

Construction in progress

|

2,618,774 | 2,231,475 | ||||||

|

Land use rights, net of accumulated amortization

|

14,403,057 | 16,829,410 | ||||||

|

Total property and equipment

|

19,550,980 | 36,216,667 | ||||||

|

Other assets

|

||||||||

|

Goodwill

|

724,940 | 12,000,000 | ||||||

|

Proprietary technologies, net of accumulated amortization

|

7,198,836 | 7,287,883 | ||||||

|

Long term accounts receivable

|

8,459,044 | 8,459,044 | ||||||

|

License rights

|

1 | 1 | ||||||

|

Total other assets

|

16,382,821 | 27,746,928 | ||||||

|

Total assets

|

111,237,880 | 107,767,910 | ||||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY

|

||||||||

|

Current liabilities

|

||||||||

|

Accounts payable and accrued expenses

|

741,369 | 390,846 | ||||||

|

Billings in excess of costs and estimated earnings on uncompleted contracts

|

430,767 | - | ||||||

|

Dividends payable

|

206,356 | 210,262 | ||||||

|

Other payables

|

6,592,587 | 1,412,290 | ||||||

|

Total current liabilities

|

8,759,501 | 2,939,594 | ||||||

|

Other liabilities

|

||||||||

|

Long term debt

|

- | 3,776,435 | ||||||

|

Total liabilities

|

8,759,501 | 6,716,029 | ||||||

|

Commitments and contingencies

|

- | - | ||||||

|

Stockholders' equity

|

||||||||

|

Preferred stock: $0.001 par value (10,000,000 shares authorized, 0 share issued and outstanding as of March 31, 2011 and December 31, 2010, respectively)

|

- | - | ||||||

|

Series A preferred stock: $0.001 par value (100 shares authorized, 100 shares issued and outstanding as of March 31, 2011 and December 31, 2010, respectively)

|

- | - | ||||||

|

Series B convertible preferred stock: $0.001 par value) (10,000,000 shares authorized, 7,000,000 shares issued and outstanding) as of March 31, 2011 and December 31, 2010, respectively)

|

7,000 | 7,000 | ||||||

|

Common stock: $0.001 par value (100,000,000 shares authorized, 56,795,136 and 55,474,136 shares issued and oustanding as of March 31, 2011 and December 31, 2010, respectively)

|

56,795 | 55,474 | ||||||

|

Additional paid - in capital

|

60,481,191 | 58,586,362 | ||||||

|

Retained earnings

|

36,134,835 | 25,019,971 | ||||||

|

Accumulated other comprehensive income

|

1,234,698 | 3,804,116 | ||||||

|

Total Sino Agro Food, Inc. and subsidiaries stockholders' equity

|

97,914,519 | 87,472,923 | ||||||

|

Non - controlling interest

|

4,563,860 | 13,578,958 | ||||||

|

Total stockholders' equity

|

102,478,379 | 101,051,881 | ||||||

|

Total liabilities and stockholders' equity

|

111,237,880 | 107,767,910 | ||||||

The accompanying notes are an integral part of these consolidated financial statements

1

SINO AGRO FOOD, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

|

Three months ended

|

Three months ended

|

|||||||

|

March 31, 2011

|

March 31, 2010

|

|||||||

|

(Unaudited)

|

(Unaudited)

|

|||||||

|

|

$

|

$

|

||||||

|

Continuing operations

|

||||||||

|

Revenue

|

3,121,531 | 300,000 | ||||||

|

Cost of goods sold

|

1,190,615 | - | ||||||

|

Gross profit

|

1,930,916 | 300,000 | ||||||

|

General and administrative expenses

|

(690,146 | ) | (514,336 | ) | ||||

|

Net income from operations

|

1,240,770 | (214,336 | ) | |||||

|

Other income (expenses)

|

||||||||

|

Other income

|

9,302 | - | ||||||

|

Gain (loss) of extinguishment of debts

|

92,926 | (4,565,180 | ) | |||||

|

Interest expense

|

(3,172 | ) | (2,927 | ) | ||||

|

Net income (expenses)

|

99,056 | (4,568,107 | ) | |||||

|

Net income before income taxes

|

1,339,826 | (4,782,443 | ) | |||||

|

Provision for income taxes

|

- | - | ||||||

|

Net income (loss) from continuing operations

|

1,339,826 | (4,782,443 | ) | |||||

|

Less: Net (income) loss attributable to the non - controlling interest

|

(428,913 | ) | 10,647 | |||||

|

Net income (loss) from continuing operations attributable to the Sino Agro Food, Inc. and subsidiaries

|

910,913 | (4,771,796 | ) | |||||

|

Discontinued operations

|

||||||||

|

Net income from discontinued operations

|

19,941,880 | 2,057,268 | ||||||

|

Less: Net income attributable to the non - controlling interest

|

(9,737,929 | ) | (452,599 | ) | ||||

|

Net income from discontinued operations attributable to the Sino Agro Food, Inc. and subsidiaries

|

10,203,951 | 1,604,669 | ||||||

|

Net income (loss) attributable to the Sino Agro Food, Inc. and subsidiaries

|

11,114,864 | (3,167,127 | ) | |||||

|

Other comprehensive income (loss)

|

||||||||

|

Foreign currency translation gain (loss)

|

1,175,674 | (293,090 | ) | |||||

|

Comprehensive income (loss)

|

12,290,538 | (3,460,217 | ) | |||||

|

Less: other comprehensive (income) loss attributable to the non - controlling interest

|

(293,918 | ) | 58,618 | |||||

|

Comprehensive income (loss) attributable to the Sino Agro Food, Inc. and subsidiaries

|

11,996,620 | (3,401,599 | ) | |||||

|

Earnings (loss) per share attributable to Sino Agro Food, Inc. and subsidiaries common stockholders:

|

||||||||

|

From continuing and discontinued operations

|

||||||||

|

Basic

|

$ | 0.20 | $ | (0.06 | ) | |||

|

Diluted

|

$ | 0.18 | $ | (0.06 | ) | |||

|

Earnings (loss) per share attributable to Sino Agro Food, Inc. and subsidiaries common stockholders:

|

||||||||

|

From continuing operations

|

||||||||

|

Basic

|

$ | 0.02 | $ | (0.09 | ) | |||

|

Diluted

|

$ | 0.01 | $ | (0.09 | ) | |||

|

Weighted average number of shares outstanding:

|

||||||||

|

Basic

|

56,502,325 | 54,088,199 | ||||||

|

Diluted

|

63,502,325 | 54,088,199 | ||||||

The accompanying notes are an integral part of these consolidated financial statements

2

SINO AGRO FOOD, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

Three months ended

|

Three months ended

|

|||||||

|

March 31, 2011

|

March 31, 2010

|

|||||||

|

(Unaudited)

|

(Unaudited)

|

|||||||

|

$

|

$

|

|||||||

|

Cash flows from operating activities

|

||||||||

|

Net income (loss) from continuing operations

|

1,339,826 | (4,782,443 | ) | |||||

|

Adjustments to reconcile net income (loss) from continuing operations to net cash from operations:

|

||||||||

|

Depreciation

|

40,353 | 281,991 | ||||||

|

Amortization

|

189,792 | 710,508 | ||||||

|

(Gain) loss on extinguishment of debts

|

(92,926 | ) | 4,565,180 | |||||

|

Changes in operating assets and liabilities:

|

||||||||

|

Increase in inventories

|

(381,707 | ) | (45,946 | ) | ||||

|

Decrease(increase) in deposits and prepaid expenses

|

8,438 | 894,116 | ||||||

|

Increase in due from a director

|

- | (1,194,817 | ) | |||||

|

Increase in due to a director

|

113,081 | - | ||||||

|

Increase in accounts payable and accrued expenses

|

372,932 | 24,473 | ||||||

|

Increase (decrease) in other payables

|

16,347,616 | (994,602 | ) | |||||

|

(Increase) decrease in accounts receivable

|

(1,662,144 | ) | 321,442 | |||||

|

Increase in billings in excess of costs and estimated earnings on uncompleted contracts

|

430,767 | - | ||||||

|

(Increase) decrease in other receivables

|

(13,060,168 | ) | (507,152 | ) | ||||

|

Net cash provided by (used in) operating activities

|

3,645,860 | (727,250 | ) | |||||

|

Cash flows from investing activities

|

||||||||

|

Purchases of property and equipment

|

(6,449 | ) | (266,951 | ) | ||||

|

Acquisition of land use rights

|

(704,388 | ) | - | |||||

|

Payment for construction in progress

|

(387,298 | ) | (193,791 | ) | ||||

|

Net cash used in investing activities

|

(1,098,135 | ) | (460,742 | ) | ||||

|

Cash flows from financing activities

|

||||||||

|

Dividends paid

|

(3,905 | ) | - | |||||

|

Net cash used in financing activities

|

(3,905 | ) | - | |||||

|

Net cash provided by (used in) continuing operations

|

2,543,820 | (1,187,992 | ) | |||||

|

Cash flows from discontinued operations

|

||||||||

|

Net cash provided by operating activities

|

- | 2,422,578 | ||||||

|

Net cash used in investing activities

|

(2,433,497 | ) | (1,957,888 | ) | ||||

|

Net cash provided by financing activities

|

- | - | ||||||

|

Net cash (used in) provided by discontinued operations

|

(2,433,497 | ) | 464,690 | |||||

|

Effects on exchange rate changes on cash

|

(3,517,433 | ) | 1,213,276 | |||||

|

(Decrease) increase in cash and cash equivalents

|

(3,407,110 | ) | 489,974 | |||||

|

Cash and cash equivalents, beginning of period

|

3,890,026 | 2,360,587 | ||||||

|

Cash and cash equivalents, end of period

|

482,916 | 2,850,561 | ||||||

|

Less: cash and cash equivalents at the end of the period - discontinued operation

|

- | (2,471,897 | ) | |||||

|

Cash and cash equivalents at the end of the period - continuing operations

|

482,916 | 378,664 | ||||||

|

Supplementary disclosures of cash flow information:

|

||||||||

|

Cash paid for interest

|

3,172 | 120,999 | ||||||

|

Cash paid for income taxes

|

- | - | ||||||

|

Non - cash transactions

|

||||||||

|

1,321,000 (2010: 4,747,000) shares of common stock issued for settlement of debts

|

1,989,000 | 1,158,650 | ||||||

|

Disposal proceeds receivable of sale of subsidiaries, HYT and ZX

|

44,295,612 | - | ||||||

|

Land use rights payable due to related parties

|

6,339,493 | - | ||||||

The accompanying notes are an integral part of these consolidated financial statements

3

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

1.

|

CORPORATE INFORMATION

|

|

|

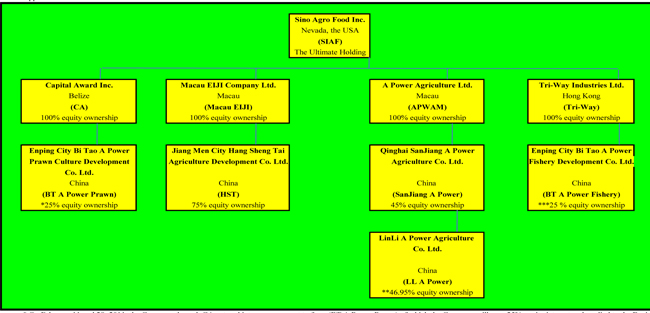

Sino Agro Food, Inc. (“the Company”) (formerly known as Volcanic Gold, Inc. and A Power Agro Agriculture Development, Inc.) Company”) is an International Business Corporation incorporated on October 1, 1974 in the State of Nevada, United States of America.

|

|

|

The Company was engaged in the mining and exploration business but ceased its mining and exploring business on October 14, 2005. On August 24, 2007, the Company entered into a Merger and Acquisition Agreement with Capital Award Inc. (“CA”) and its subsidiaries Capital Stage Inc. (“CS”) and Capital Hero Inc. (“CH”). Effective the same date, CA, a Belize Corporation, completed a reverse merger transaction with SIAF. SIAF acquired all the outstanding common stock of CA from Capital Adventure, a shareholder of CA for 32,000,000 shares of the company’s common stock.

|

|

|

On August 24, 2007 the Company changed its name from Volcanic Gold, Inc. to A Power Agro Agriculture Development, Inc. On December 8, 2007, the Company officially changed its name to Sino Agro Food, Inc.

|

|

|

On September 5, 2007, the Company acquired three existing businesses in the People’s Republic of China (“PRC”):

|

|

|

a)

|

Hang Yu Tai Investment Limited (“HYT”), a company incorporated in Macau, the owner of a 78% equity interest in ZhongXingNongMu Ltd (“ZX”), a company incorporated in the PRC;

|

|

|

b)

|

Tri-way Industries Limited (“TRW”), a company incorporated in Hong Kong;

|

|

|

c)

|

Macau Eiji Company Limited (“MEIJI”), a company incorporated in Macau, the owner of 75% equity interest in Enping City Juntang Town Hang Sing Tai Agriculture Co. Ltd. (“HST”), a PRC corporate Sino-Foreign joint venture. HST was disposed in 2010.

|

On November 27, 2007, MEIJI and HST established a corporate Sino - Foregin joint venture, Jiang Men City Heng Sheng Tai Agriculture Development Co. Ltd. (“JHST”), a company incorporated in the PRC with MEIJI owning a 75% interest and HST owning a 25% interest.

On November 26, 2008, SIAF established Pretty Mountain Holdings Limited. (“PMH”), a company incorporated in Hong Kong with a 80% equity interest. On May 25, 2009, PMH formed a corporate Sino-Foregin joint venture, Qinghai Sanjiang A Power Agriculture Co. Ltd (“SJAP”), incorporated in the People’s Republic of China of which PMH owns a 45% equity interest . The remaining 55% equity interest in SJAP is owned by the following entities:

|

|

•

|

Qinghai Province Sanjiang Group Company Limited (English translation) (“Qinghai Sanjiang”), a company owned by the PRC with major business activities in the agriculture industry; and

|

|

|

•

|

Guangzhou City Garwor Company Limited (English translation) (“Garwor”), a private limited company incorporated in the PRC, specializing in sales and marketing.

|

|

|

•

|

SJAP is engaged in the business of manufacturing bio-organic fertilizer, livestock feed and development of other agriculture projects in the County of Huangyuan, in the vicinity of the Xining City, Qinghai Province, PRC.

|

4

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

1.

|

CORPORATE INFORMATION (CONTINUED)

|

In September, 2009, the Company carried out an internal re-organization of its corporate structure and business, and formed a 100% owned subsidiary A Power Agro Agriculture Development (Macau) Limited (APWAM) which was formed in Macau. APWAM then acquired PMH’s 45 % equity interest in SJAP. By virtue of the Assignment, APWAM assumed all obligations and liabilities of PMH under the Sino Foreign Joint Venture Agreement. On September 9, 2010, application was made by the Company to the Companies Registry of Hong Kong for deregistration of PMH under Section 291AA of the Hong Kong Companies Ordinance. On January 28, 2011, PMH was dissolved.

On May 7, 2010, Qinghai Sanjiang sold and transferred its equity interest in SJAP to Garwor. The aforesaid sale and transfer was approved by the State Administration for Industry And Commerce of Xining City Government of the People’s Republic of China. As a result, SJAP was owned by APWAM with a 45% interest and Garwor with a 55% interest.

On February 15, 2011 and on March 29, 2011, the Company entered the agreement and memorandum of understanding, respectively to sell 100% equity interest in HYT group (including HYT and ZX) for $45,000,000 and the effective date is January 1, 2011.

The Company applied to form Enping City Bi Tao A Power Fishery Development Co. Limited (EBAPFD) and Enping City Bi Tao A Power Prawn Culture Development Co. Limited (EBAPCD), both of which the Company would own a 25% equity interest. The approvals of the formation of EBAPFD and EBAPCD by the relevant authorities of the PRC Government are pending.

The Company’s principal executive office is located at Room 3711, China Shine Plaza, No. 9 Lin He Xi Road, Tianhe District, Guangzhou City, Guangdong Province, PRC 510610.

The nature of the operations and principal activities of Sino Agro Food, Inc. and its subsidiaries are described in Note 2.2.

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

|

2.1 FISCAL YEAR

The Company has adopted December 31 as its fiscal year end.

5

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.2 REPORTING ENTITY

The accompanying consolidated financial statements include the following entities:

|

Name of subsidiaries

|

Place of incorporation

|

Percentage of interest

|

Principal activities

|

|||

|

Capital Award Inc. ("CA")

|

Belize

|

100% (12.31..2010: 100%) directly

|

Fishery development and holder of A-Power Technology master license.

|

|||

|

Capital Stage Inc. ("CS")

|

Belize

|

100% (12.31.2010: 100%) indirectly

|

Dormant

|

|||

|

Capital Hero Inc. ("CH")

|

Belize

|

100% (12.31.2010: 100%) indirectly

|

Dormant

|

|||

|

Tri-way Industries Limited ("TRW")

|

Hong Kong, PRC

|

100% (12.31.2010: 100%) directly

|

Investment holding, holder of enzyme technology master license for manufacturing of livestock feed and bio-organic fertilizer and has not commenced its planned business of fish farm operations.

|

|||

|

Pretty Mountain Holdings Limited ("PMH")

|

Hong Kong, PRC

|

0% (12.31.2010: 80%) directly

|

Dissolved on January 28, 2011

|

|||

|

Macau Eiji Company Limited ("MEIJI")

|

Macau, PRC

|

100% (12.31.2010: 100%) directly

|

Disposed on February 15, 2011 (2010: Investment holding

|

|||

|

Jiang Men City Heng Sheng Tai Agriculture Development Co. Ltd ("JHST")

|

PRC

|

75% (12.31.2010: 75%) directly

|

Hylocereus Undatus Plantation ("HU Plantation"). The Company has not commenced beef business.

|

|||

|

Hang Yu Tai Investment Limited ("HYT")

|

Macau, PRC

|

0% (12.31.2010: 100%) directly

|

Disposed on February 15, 2011 (2010: Investment holding)

|

|||

|

ZhongXingNongMu Co. Ltd ("ZX")

|

PRC

|

0% (12.31.2010: 78%) indirectly

|

Disposed on February 15, 2011 (2010: Dairy production and manufacturing of organic fertilizer,livestock feed, and beef cattle and plantation of crops and pasture)

|

|||

|

A Power Agro Agriculture Development (Macau) Limited ("APWAM")

|

Macau, PRC

|

100% (12.31.2010: 100%) directly

|

Investment holding

|

|||

|

Name of variable interest entity

|

Place of incorporation

|

Percentage of interest

|

Principal activities

|

|||

|

Qinghai Sanjiang A Power Agriculture Co., Ltd ("SJAP")

|

|

PRC

|

|

45% (12.31.2010: 45%) indirectly

|

|

Manufacturing of organic fertilizer,livestock feed, and beef cattle and plantation of crops and pastures

|

6

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.3 BASIS OF PRESENTATION

The consolidated financial statements are prepared in accordance with generally accepted accounting principles in the United States of America ("US GAAP").

Interim results are not necessarily indicative of results for a full year. The information included in this interim report should be read in conjunction with the information included in the Company’s annual report on Form 10-K for the fiscal year ended December 31, 2010.

2.4 BASIS OF CONSOLIDATION

The consolidated financial statements include the financial statements of SIAF, its subsidiaries CA, CS, CH, TRW, MEIJI, HJST, ZX, PMH. HYT and APWAM and its variable interest entity SJAP. All material inter-company transactions and balances have been eliminated in consolidation. HYT and ZX were derecognized as subsidiaries since 1 January 2011 and PMH was dissolved on January 28, 2011.

SIAF, CA, CS, CH, TRW, MEIJI, JHST, APWAM and SJAP are hereafter referred to as (“the Company”).

2.5 BUSINESS COMBINATION

The Company adopted the accounting pronouncements relating to business combination (primarily contained in ASC Topic 805 “Business Combinations”), including assets acquired and liabilities assumed arising from contingencies. These pronouncements established principles and requirements for how the acquirer of a business recognizes and measures in its financial statements the identifiable assets acquired, the liabilities assumed, and any non-controlling interest in the acquisition as well as provides guidance for recognizing and measuring the goodwill acquired in the business combination and determines what information to disclose to enable users of the financial statements to evaluate the nature and financial effects of the business combination. In addition, these pronouncements eliminate the distinction between contractual and non-contractual contingencies, including the initial recognition and measurement criteria and require an acquirer to develop a systematic and rational basis for subsequently measuring and accounting for acquired contingencies depending on their nature. Our adoption of these pronouncements will have an impact on the manner in which we account for any future acquisitions.

2.6 NON - CONTROLLING INTEREST IN CONSOLIDATED FINANCIAL STATEMENTS

The Company adopted the accounting pronouncement on non-controlling interests in consolidated financial statements, which establishes accounting and reporting standards for the non-controlling interest in a subsidiary and for the deconsolidation of a subsidiary. This guidance is primarily contained in ASC Topic “Consolidation”. It clarifies that a non-controlling interest in a subsidiary is an ownership interest in the consolidated financial statements. The adoption of this standard has not had material impact on our consolidated financial statements.

7

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.7 USE OF ESTIMATES

The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States requires management to make assumptions and estimates that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the dates of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting periods covered thereby. Actual results could differ from these estimates. Judgments and estimates of uncertainties are required in applying the Company’s accounting policies in certain areas. The following are some of the areas requiring significant judgments and estimates: determinations of the useful lives of assets, estimates of allowances for doubtful accounts, cash flow and valuation assumptions in performing asset impairment tests of long-lived assets, estimates of the realizability of deferred tax assets and inventory reserves.

2.8 REVENUE RECOGNITION

The Company’s revenue recognition policies are in compliance with ASC Topic 605. Sales revenue is recognized when all of the following have occurred: (i) persuasive evidence of an arrangement exists, (ii) delivery has occurred or services have been rendered, (iii) the price is fixed or determinable, and (iv) the ability to collect is reasonably assured. These criteria are generally satisfied at the time of shipment when risk of loss and title passes to the customer. License fee income is recognized on the accrual basis in accordance with the underlying agreements.

Revenues from the Company's fishery development contract services are performed under fixed-price contracts. Revenues under long-term contracts are accounted for under the percentage-of-completion method of accounting in accordance with the Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") Topic 605, Revenue Recognition ("ASC 605"). Under the percentage-of-completion method, the Company estimates profit as the difference between total estimated revenue and total estimated cost of a contract and recognizes that profit over the contract term. The percent of cost incurred determines the amount of revenue to be recognized. Payment terms are generally defined by the installation contract and as a result may not match the timing of the costs incurred by the Company and the related recognition of revenue. Such differences are recorded as either costs or estimated earnings in excess of billings on uncompleted contracts or billings in excess of costs and estimated earnings on uncompleted contracts. The Company determines a customer’s credit worthiness at the time an order is accepted. Sudden and unexpected changes in a customer’s financial condition could put recoverability at risk.

The percentage of completion method requires the ability to estimate several factors, including the ability of the customer to meet its obligations under the contract, including the payment of amounts when due. If we determine that collectability is not assured, we will defer revenue recognition and use methods of accounting for the contract such as completed contract method until such time we determine that collectability is reasonably assured or through the completion of the project.

For fixed-price contracts, the Company uses the ratio of cost incurred to date on the contract (excluding uninstalled direct materials) to management's estimate of the contract's total cost, to determine the percentage of completion on each contract. This method is used as management considers expended costs to be the best available measure of progression of these contracts. Contract cost includes all direct material, subcontract and labor costs and those indirect costs related to contract performance, such as supplies, tool repairs and depreciation. The Company accounts for maintenance and repair services under the guidance of ASC 605 as the services provided relate to construction work. Contract costs incurred to date and expected total contract costs are continuously monitored during the term of the contract. Changes in job performance, job conditions, job conditions, and estimated profitability arising from contract penalty, change orders and final contract settlements may result in revisions to the estimated profitability during the contract. These changes, which include contracts with estimated costs in excess of estimated revenues, are recognized in contract costs in the period in which the revisions are determined. Profit incentives are included in revenues when their realization is reasonably assured. At the point the Company anticipates a loss on a contract, the Company estimates the ultimate loss through completion and recognizes that loss in the period in which the possible loss was identified.

8

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.8 REVENUE RECOGNITION

The Company will not provide warranties to customers on a basis customary to the industry; however, the customers can claim warranty directly from product manufacturers. Historically, the Company has no warranty claims history in the past.

The Company recognizes revenue when the fishery development contract services are rendered, structure is delivered and title has passed. Sales revenue represents the invoiced value of fishery development contract services, net of business tax. All of the Company’s fishery development consultancy services revenue that are earned in the PRC are subject to a Chinese business tax at a rate of 0% of the gross fishery development contract service income approved by the Chinese local government.

2.9 COST OF GOODS SOLD

Cost of goods sold consists primarily of direct purchase cost of merchandise goods, and related levies.

2.10 SHIPPING AND HANDLING

Shipping and handling costs related to cost of goods sold are included in general and administrative expenses which totaled $0 for the three months ended March 31, 2011 and 2010, respectively.

2.11 ADVERTISING

Advertising costs are included in general and administrative expenses which totaled $nil for the three months ended March 31, 2011 and 2010, respectively.

2.12 FOREIGN CURRENCY TRANSLATION AND OTHER COMPREHENSIVE INCOME

The reporting currency of the Company is the U.S. dollars. The functional currency of the Company is the Chinese Renminbi (RMB).

For those entities whose functional currency is other than the U.S. dollars, all assets and liabilities are translated into U.S. dollars at the exchange rate on the balance sheet date; shareholders’ equity is translated at historical rates and items in the statements of income and of cash flows are translated at the average rate for the period. Because cash flows are translated based on the average translation rate, amounts related to assets and liabilities reported in the statements of cash flows will not necessarily agree with changes in the corresponding balances in the balance sheets. Translation adjustments resulting from this process are included in accumulated other comprehensive income in the statements of shareholders’ equity. Transaction gains and losses that arise from exchange rate fluctuations on transactions denominated in a currency other than the functional currency are included in the statements of income and comprehensive income as incurred.

Accumulated other comprehensive income in the consolidated statement of shareholders’ equity amounted to $1,234,698 as of March 31, 2011 and $3,804,116 as of December 31, 2010. The balance sheet amounts with the exception of equity at March 31, 2011 and December 31, 2010 were translated at RMB 6.57 to $1.00 and RMB6.62 to $1.00, respectively. The average translation rates applied to the statements of income and comprehensive income and of cash flows for the three months ended March 31, 2011 and March 31, 2010 were RMB6.59to $1.00 and RMB6.81 to $1.00, respectively.

9

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.13 CASH AND CASH EQUIVALENTS

The Company considers all highly liquid securities with original maturities of three months or less when acquired to be cash equivalents. Cash and cash equivalents kept with financial institutions in People’s Republic of China (“PRC”) are not insured or otherwise protected. Should any of those institutions holding the Company’s cash become insolvent, or the Company is unable to withdraw funds for any reason, the Company could lose the cash on deposit on that institution.

2.14 ACCOUNTS RECEIVABLE

The Company maintains reserves for potential credit losses on accounts receivable. Management reviews the composition of accounts receivable and analyzes historical bad debts, customer concentrations, customer credit worthiness, current economic trends and changes in customer payment patterns to evaluate the adequacy of these reserves. Reserves are recorded primarily on a specific identification basis.

The standard credit period of the Company’s most of client is three months. The collection period over 1 year is classified as long term accounts receivable. Management evaluates the collectability of the receivables at least quarterly. Provisions for doubtful accounts as of March 31, 2011 and December 31, 2010 are $nil.

2.15 INVENTORIES

Inventories are valued at the lower of cost (determined on a weighted average basis) and net realizable value.

Costs incurred in bringing each product to its location and conditions are accounted for as follows:

|

-

|

raw materials – purchase cost on a weighted average basis;

|

|

-

|

manufactured finished goods and work-in-progress – cost of direct materials and labor and a proportion of manufacturing overhead based on normal operation capacity but excluding borrowing costs; and

|

|

-

|

retail and wholesale merchandise finished goods – purchase cost on a weighted average basis.

|

Net realizable value is the estimated selling price in the ordinary course of business, less estimated costs of completion and the estimated costs necessary to make the sale.

2.16 PROPERTY AND EQUIPMENT

Property and equipment are stated at cost less accumulated depreciation and any accumulated impairment losses. Such costs include the cost of replacing parts that are eligible for capitalization when the cost of replacing the parts is incurred. Similarly, when each major inspection is performed, its cost is recognized in the carrying amount of the property and equipment as a replacement only if it is eligible for capitalization. The assets’ residual values, useful lives and depreciation methods are reviewed, and adjusted if appropriate, at each financial year-end.

Depreciation is calculated on a straight-line basis over the estimated useful lives of the assets.

|

Milk cows

|

10 years

|

|

Plant and machinery

|

5 - 10 years

|

|

Structure and leasehold improvements

|

10 -20 years

|

|

Mature seed

|

20 years

|

|

Furniture, fixtures and equipment

|

2.5 - 10 years

|

|

Motor vehicles

|

5 -10 years

|

10

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.16 PROPERTY AND EQUIPMENT (CONTINUED)

An item of property and equipment is removed from the accounts upon disposal or when no future economic benefits are expected to arise from the continued use of the asset. Any gain or loss arising on disposal of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the item) is included in the consolidated statements of income in the period the item is disposed.

2.17 GOODWILL

Goodwill is an asset representing the fair economic benefits arising from other assets acquired in a business combination that are not individually identified and separately recognized. Goodwill is tested for impairment on an annual basis at the end of the company’s fiscal year, or when impairment indicators arise. The Company uses a fair-value-based approach to test for impairment at the level of each reporting unit. The Company directly acquired MEIJI which is engaged in Hu Plantation. As a result of this acquisition, the Company recorded goodwill in the amount of $724,940. This goodwill represents the fair value of the assets acquired in these acquisitions over the cost of the assets acquired.

2.18 PROPRIETARY TECHNOLOGIES

The Company has determined that technological feasibility is established at the time a working model of products is completed. A master license of stock feed manufacturing technology was acquired and the costs of acquisition are capitalized as proprietary technologies when technological feasibility has been established. Proprietary technologies are intangible assets of finite lives. Proprietary technologies are amortized using the straight line method over their estimated lives of 25 years. Management evaluates the recoverability of proprietary technologies on an annual basis of the end of the company’s fiscal year, or when impairment indicators arise. As required by ASC Topic 350 “Intangible – Goodwill and Other”, the Company uses a fair-value-based approach to test for impairment.

2.19 CONSTRUCTION IN PROGRESS

Construction in progress represents direct costs of construction as well as acquisition and design fees incurred. Capitalization of these costs ceases and the construction in progress is transferred to property and equipment when substantially all the activities necessary to prepare the assets for their intended use are completed. No depreciation is provided until construction is completed and the asset is ready for its intended use.

2.20 LAND USE RIGHTS

Land use rights represent acquisition of land use right rights of agriculture land from farmers and are amortized on the straight line basis over their respective lease periods. The lease period of agriculture land is in the range from 30 years to 60 years. Land use rights purchase prices were determined in accordance with the 2007 PRC Government’s minimum lease payments of agriculture land and mutually agreed between the company and the vendors.

2.21 VARIABLE INTEREST ENTITY

An entity (investee) in which the investor has obtained less than a majority-owned interest, according to the Financial Accounting Standards Board (FASB). A variable interest entity (VIE) is subject to consolidation if A VIE is an entity meeting one of the following three criteria as elaborated in ASC Topic 810-10, Consolidation.

(a) equity-at-risk is not sufficient to support the entity's activities

(b) As a group, the equity-at-risk holders cannot control the entity; or

(c) The economics do not coincide with the voting interest

If a firm is the primary beneficiary of a VIE, the holdings must be disclosed on the balance sheet. The primary beneficiary is defined as the person or company with the majority of variable interests A corporation formed, owned, and operated by two or more businesses (ventures) as a separate and discrete business or project (venture) for their mutual benefit is defined as a joint venture

11

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.22 INCOME TAXES

The Company accounts for income taxes under the provisions of ASC Topic 740 "Accounting for Income Taxes". Under ASC Topic 740, deferred tax assets and liabilities are determined based on the difference between the financial statement carrying amounts and the tax bases of assets and liabilities using enacted tax rates in effect in the years in which the differences are expected to reverse.

The provision for income tax is based on the results for the year as adjusted for items, which are non-assessable or disallowed. It is calculated using tax rates that have been enacted or substantively enacted at the balance sheet date. Deferred tax is accounted for using the balance sheet liability method in respect of temporary differences arising from differences between the carrying amount of assets and liabilities in the financial statements and the corresponding tax basis used in the computation of assessable tax profit. In principle, deferred tax liabilities are recognized for all taxable temporary differences, and deferred tax assets are recognized to the extent that it is probable that taxable profit will be available against which deductible temporary differences can be utilized.

Deferred income taxes are calculated at the tax rates that are expected to apply to the period when the asset is realized or the liability is settled. Deferred tax is charged or credited in the income statement, except when it related to items credited or charged directly to equity, in which case the deferred tax is also dealt with in equity. Deferred tax assets and liabilities are offset when they relate to income taxes levied by the same taxation authority and the Company intends to settle its current tax assets and liabilities on a net basis.

ASC Topic 740 also prescribes a more-likely-than-not threshold for financial statement recognition and measurement of a tax position taken, or expected to be taken, in a tax return. ASC Topic 740 also provides guidance related to, among other things, classification, accounting for interest and penalties associated with tax positions, and disclosure requirements. Any interest and penalties accrued related to unrecognized tax benefits will be recorded in tax expense.

2.23 POLITICAL AND BUSINESS RISK

The Company's operations are carried out in the PRC. Accordingly, the Company's business, financial condition and results of operations may be influenced by the political, economic and legal environment in the PRC, and by the general state of the PRC's economy. The Company's operations in the PRC are subject to specific considerations and significant risks not typically associated with companies in North America and Western Europe. The Company's results may be adversely affected by changes in governmental policies with respect to laws and regulations, anti-inflationary measures, currency conversion and remittance abroad, and rates and methods of taxation, among other things.

2.24 CONCENTRATION OF CREDIT RISK

Cash includes cash at bank and demand deposits in accounts maintained with banks within the People’s Republic of China. Total cash in these banks on March 31, 2011 and December 31, 2010 amounted to $134,841 and $3,525,224, respectively of which no deposits are covered by insurance. The Company has not experienced any losses in such accounts and believes it is not exposed to any risks on its cash in bank accounts.

Accounts receivable are derived from revenue earned from customers located primarily in the People’s Republic of China. The Company perform ongoing credit evaluations of customers and have not experienced any material losses to date.

12

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

2.24 CONCENTRATION OF CREDIT RISK (CONTINUED)

The Company had 5 major customers whose revenue individually represented the following percentages of the Company’s total revenue:

|

Three months

|

Three months

|

|||||||

|

ended

|

ended

|

|||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Customer A

|

38.99 | % | - | |||||

|

Customer B

|

17.05 | % | - | |||||

|

Customer C

|

14.04 | % | - | |||||

|

Customer D

|

10.97 | % | - | |||||

|

Customer E

|

9.87 | % | - | |||||

|

Customer F

|

- | 39.04 | % | |||||

|

Customer G

|

- | 35.73 | % | |||||

|

Customer H

|

- | 17.90 | % | |||||

|

Customer I

|

- | 7.33 | % | |||||

| 90.92 | % | 100.00 | % | |||||

The company had 5 major customers whose accounts receivable balance individually represented of the Company’s total accounts receivable as follows:

|

March 31, 2011

|

December 31, 2010

|

|||||||

|

Customer A

|

32.01 | % | 28.37 | % | ||||

|

Customer B

|

18.13 | % | 16.85 | % | ||||

|

Customer C

|

13.27 | % | 12.55 | % | ||||

|

Customer D

|

7.36 | % | - | |||||

|

Customer E

|

6.54 | % | 14.00 | % | ||||

|

Customer F

|

- | 7.49 | % | |||||

| 77.31 | % | 79.26 | % | |||||

2.25 IMPAIRMENT OF LONG-LIVED ASSETS AND INTANGIBLE ASSETS

In accordance with ASC Topic 360, “Property, Plant and Equipment”, long-lived assets to be held and used are analyzed for impairment whenever events or changes in circumstances indicate that the related carrying amounts may not be recoverable. The Company reviews the carrying amount of its long-lived assets, including intangibles, for impairment, each reporting period. An asset is considered impaired when estimated future cash flows are less than the carrying amount of the asset. In the event the carrying amount of such asset is considered not recoverable, the asset is adjusted to its fair value. Fair value is generally determined based on discounted future cash flow. As of March 31, 2011 and December 31, 2010, the Company determined no impairment charges were necessary.

13

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.26 EARNINGS PER SHARE

As prescribed in ASC Topic 260 “Earnings per Share”, Basic Earnings per Share (“EPS”) is computed by dividing net income available to common stockholders by the weighted average number of common stock shares outstanding during the year. Diluted EPS is computed by dividing net income available to common stockholders by the weighted-average number of common stock shares outstanding during the year plus potential dilutive instruments such as stock options and warrants. The effect of stock options on diluted EPS is determined through the application of the treasury stock method, whereby proceeds received by the Company based on assumed exercises are hypothetically used to repurchase the Company’s common stock at the average market price during the period.

For the three months ended March 31, 2011 and 2010, basic earnings (loss) per share from continuing and discontinued operations attributable to Sino Agro Food, Inc. and subsidiaries common stockholders amount to $0.19 and $(0.06), respectively. For the three months ended March 31, 2011 and 2010, diluted earnings (loss) per share from continuing and discontinued operations attributable to Sino Agro Food, Inc. and subsidiaries common stockholders amount to $0.18 and $(0.06), respectively.

For the three months ended March 31, 2011 and 2010, basic earnings (loss) per share from continuing operations attributable to Sino Agro Food, Inc. and subsidiaries common stockholders amount to $0.02 and $(0.09), respectively. For the three months ended March 31, 2011 and 2010, diluted earnings (loss) per share from continuing operations attributable to Sino Agro Food, Inc. and subsidiaries common stockholders amount to $0.01 and $(0.09), respectively.

2.27 ACCUMULATED OTHER COMPREHENSIVE INCOME

ASC Topic 220 “Comprehensive Income” establishes standards for reporting and displaying comprehensive income and its components in financial statements. Comprehensive income is defined as the change in stockholders’ equity of a business enterprise during a period from transactions and other events and circumstances from non-owner sources. The comprehensive income for all periods presented includes both the reported net income and net change in cumulative translation adjustments.

2.28 RETIREMENT BENEFIT COSTS

PRC state managed retirement benefit programs are defined contribution plans and the payments to the plans are charged as expenses when employees have rendered service entitling them to the contribution.

2.29 STOCK-BASED COMPENSATION

The Company adopts both ASC Topic 718, “Compensation - Stock Compensation” and ASC Topic 505-50,“Equity-Based Payments to Non-Employees” using the fair value method in which an entity issues its equity instruments to acquire goods and services from employees and non-employees. Stock compensation for stock granted to non-employees has been determined in accordance with this accounting standard and the accounting standard regarding accounting for equity instruments that are issued to other than employees for acquiring, or in conjunction with selling goods or services, as the fair value of the consideration received or the fair value of equity instruments issued, whichever is more reliably measured. This accounting standard allows the “simplified” method to determine the term of employee options when other information is not available. Under ASC Topic 718 and ASC Topic 505-50, stock compensation expenses is measured at the grant date on the value of the option or restricted stock and is recognized as expenses, less expected forfeitures, over the requisite service period, which is generally the vesting period.

2.30 FAIR VALUE OF FINANCIAL INSTRUMENTS

The Company follows paragraph 825-10-50-10 of the FASB Accounting Standards Codification for disclosures about fair value of its financial instruments and paragraph 820-10-35-37 of the FASB Accounting Standards Codification (“Paragraph 820-10-35-37”) to measure the fair value of its financial instruments. Paragraph 820-10-35-37 establishes a framework for measuring fair value in accounting principles generally accepted in the United States of America (U.S. GAAP), and expands disclosures about fair value measurements. To increase consistency and comparability in fair value measurements and related disclosures, Paragraph 820-10-35-37 establishes a fair value hierarchy which prioritizes the inputs to valuation techniques used to measure fair value into three (3) broad levels. The fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities and the lowest priority to unobservable inputs. The three (3) levels of fair value hierarchy defined by Paragraph 820-10-35-37 are described below:-

14

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.30 FAIR VALUE OF FINANCIAL INSTRUMENTS (CONTINUED)

|

|

Level 1

|

Quoted market prices available in active markets for identical assets or liabilities as of the reporting date.

|

|

|

Level 2

|

Pricing inputs other than quoted prices in active markets included in Level 1, which are either directly or indirectly observable as of the reporting date.

|

|

Level 3

|

Pricing inputs that are generally observable inputs and not corroborated by market data.

|

The carrying amounts of the Company’s financial assets and liabilities, such as cash and accrued expenses, approximate their fair values because of the short maturity of these instruments.

The Company does not have any assets or liabilities measured at fair value on a recurring or a non-recurring basis, consequently, the Company did not have any fair value adjustments for assets and liabilities measured at fair value at March 31, 2011 or December 31, 2010, nor gains or losses are reported in the statements of income and comprehensive income that are attributable to the change in unrealized gains or losses relating to those assets and liabilities still held at the reporting date for the fiscal period ended March 31, 2011 or March 31, 2010.

2.31 NEW ACCOUNTING PRONOUNCEMENTS

The Company does not expect any recent accounting pronouncements to have a material effect on the Company’s financial position, results of operations, or cash flows.

In January 2010, FASB issued ASU No. 2010-01 Accounting for Distributions to Shareholders with Components of Stock and Cash. The amendments in this Update clarify that the stock portion of a distribution to shareholders that allows them to elect to receive cash or stock with a potential limitation on the total amount of cash that all shareholders can elect to receive in the aggregate is considered a share issuance that is reflected in EPS prospectively and is not a stock dividend for purposes of applying Topics 505 and 260 (Equity and Earnings Per Share). The amendments in this update are effective for interim and annual periods ending on or after December.

In January 2010, FASB issued ASU No. 2010-02 regarding accounting and reporting for decreases in ownership of a subsidiary. Under this guidance, an entity is required to deconsolidate a subsidiary when the entity ceases to have a controlling financial interest in the subsidiary. Upon deconsolidation of a subsidiary, and entity recognizes a gain or loss on the transaction and measures any retained investment in the subsidiary at fair value. In contrast, an entity is required to account for a decrease in its ownership interest of a subsidiary that does not result in a change of control of the subsidiary as an equity transaction. This ASU clarifies the scope of the decrease in ownership provisions, and expands the disclosures about the deconsolidation of a subsidiary or de-recognition of a group of assets. This ASU is effective for beginning in the first interim or annual reporting period ending on or after December 31, 2009. The Company does not expect the adoption of this ASU to have a material impact on its consolidated financial statements In January 2010, FASB issued ASU No. 2010-02 – Accounting and Reporting for Decreases in Ownership of a Subsidiary – a Scope Clarification. The amendments in this Update affect accounting and reporting by an entity that experiences a decrease in ownership in a subsidiary that is a business or nonprofit activity. The amendments also affect accounting and reporting by an entity that exchanges a group of assets that constitutes a business or nonprofit activity for an equity interest in another entity. The amendments in this update are effective beginning in the period that an entity adopts SFAS No. 160, “Non-controlling Interests in Consolidated Financial Statements – An Amendment of ARB No. 51.” If an entity has previously adopted SFAS No. 160 as of the date the amendments in this update are included in the Accounting Standards Codification, the amendments in this update are effective beginning in the first interim or annual reporting period ending on or after December 15, 2009. The amendments in this update should be applied retrospectively to the first period that an entity adopted SFAS No. 160. The Company adopted this standard and has determined the standard does not have material effect on the Company’s consolidated financial statements.

15

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.31 NEW ACCOUNTING PRONOUNCEMENTS (CONTINUED)

In January 2010, FASB issued ASU No. 2010-06 – Improving Disclosures about Fair Value Measurements. This update provides amendments to Subtopic 820-10 that requires new disclosure as follows: 1) Transfers in and out of Levels 1 and 2. A reporting entity should disclose separately the amounts of significant transfers in and out of Level 1 and Level 2 fair value measurements and describe the reasons for the transfers. 2) Activity in Level 3 fair value measurements. In the reconciliation for fair value measurements using significant unobservable inputs (Level 3), a reporting entity should present separately information about purchases, sales, issuances, and settlements (that is, on a gross basis rather than as one net number). This update provides amendments to Subtopic 820-10 that clarify existing disclosures as follows: 1) Level of disaggregation. A reporting entity should provide fair value measurement disclosures for each class of assets and liabilities. A class is often a subset of assets or liabilities within a line item in the statement of financial position. A reporting entity needs to use judgment in determining the appropriate classes of assets and liabilities. 2) Disclosures about inputs and valuation techniques. A reporting entity should provide disclosures about the valuation techniques and inputs used to measure fair value for both recurring and nonrecurring fair value measurements. Those disclosures are required for fair value measurements that fall in either Level 2 or Level 3.The new disclosures and clarifications of existing disclosures are effective for interim and annual reporting periods beginning after December 15, 2009, except for the disclosures about purchases, sales, issuances, and settlements in the roll forward of activity in Level 3 fair value measurements. Those disclosures are effective for fiscal years beginning after December 15, 2010, and for interim periods within those fiscal years. The Company is currently evaluating the impact of this ASU, however, the Company does not expect the adoption of this ASU to have a material impact on its consolidated financial statements.

In February 2010, the FASB issued Accounting Standards Update 2010-09, “Subsequent Events (Topic 855): Amendments to Certain Recognition and Disclosure Requirements,” or ASU 2010-09. ASU 2010-09 primarily rescinds the requirement that, for listed companies, financial statements clearly disclose the date through which subsequent events have been evaluated. Subsequent events must still be evaluated through the date of financial statement issuance; however, the disclosure requirement has been removed to avoid conflicts with other SEC guidelines. ASU 2010-09 was effective immediately upon issuance and was adopted in February 2010.

In April 2010, the FASB issued Accounting Standards Update 2010-13,"Compensation-Stock Compensation (Topic 718): Effect of Denominating the Exercise Price of a Share-Based Payment Award in the Currency of the Market in Which the Underlying Equity Security Trades," or ASU 2010-13. ASU 2010-13 provides amendments to Topic 718 to clarify that an employee share-based payment award with an exercise price denominated in currency of a market in which a substantial porting of the entity's equity securities trades should not be considered to contain a condition that is not a market, performance, or service condition. Therefore, an entity would not classify such an award as a liability if it otherwise qualifies as equity. The amendments in this Update are effective for fiscal years, and interim periods within those fiscal years, beginning on or after December 15, 2010. The Company does not expect the adoption of ASU 2010-17 to have a significant impact on its consolidated financial statements.

In April 2010, the FASB issued Accounting Standard Update 2010-17, "Revenue Recognition-Milestone Method (Topic 605): Milestone Method of Revenue Recognition" or ASU 2010-17. This Update provides guidance on the recognition of revenue under the milestone method, which allows a vendor to adopt an accounting policy to recognize all of the arrangement consideration that is contingent on the achievement of a substantive milestone (milestone consideration) in the period the milestone is achieved.

The pronouncement is effective on a prospective basis for milestones achieved in fiscal years and interim periods within those years, beginning on or after June 15, 2010. The adoption of ASU 2010-17 does not have any significant impacts on the consolidated financial statements.

16

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

2.

|

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

|

2.31 NEW ACCOUNTING PRONOUNCEMENTS (CONTINUED)

In July 2010, the FASB issued ASU 2010-20, “Disclosures about the Credit Quality of Financing Receivables and the Allowance for Credit Losses.” This update amends codification topic 310 on receivables to improve the disclosures that an entity provides about the credit quality of its financing receivables and the related allowance for credit losses. As a result of these amendments, an entity is required to disaggregate by portfolio segment or class certain existing disclosures and provide certain new disclosures about its financing receivables and related allowance for credit losses. This guidance is being phased in, with the new disclosure requirements for period end balances effective as of December 31, 2010, and the new disclosure requirements for activity during the reporting period are effective March 31, 2011. The troubled debt restructuring disclosures in this ASU have been delayed by ASU 2011-01 “Deferral of the Effective Date of Disclosures about Troubled Debt Restructurings in Update No. 2010-20,” which was issued in January 2011.

In December 2010, the FASB issued Accounting Standards Update 2010-28 which amend “Intangibles- Goodwill and Other” (Topic 350). The ASU modifies Step 1 of the goodwill impairment test for reporting units with zero or negative carrying amounts. For those reporting entities, they are required to perform Step 2 of the goodwill impairment test if it is more likely than not that a goodwill impairment exists. An entity should consider whether there are any adverse qualitative factors indicating that impairment may exist. The qualitative factors are consistent with the existing guidance in Topic 350, which requires that goodwill of a reporting unit be tested for impairment between annual tests if an event occurs or circumstances changes that would more likely than not reduce the faire value of a reporting unit below its carrying amount. ASU 2010-28 is effective for fiscal years, and interim periods within those years beginning after December 15, 2010. Early adoption is not permitted. The Company is currently evaluating the impact of this ASU; however, the Company does not expect the adoption of this ASU will have a material impact on its consolidated financial statements.

In December 2010, the FASB issued Accounting Standards Update 2010-29 which address diversity in practice about the interpretation of the pro forma revenue and earnings disclosure requirements for business combinations (Topic 805). This ASU specifies that if a public entity presents comparative financial statements, the entity should disclose revenue and earnings of the combined entity as though the business combination(s) that occurred during the current year had occurred as of the beginning of the comparable prior annual reporting period only. This ASU also expands the supplemental pro forma disclosures under Topic 805 to include a description of the nature and amount of material, nonrecurring pro forma adjustments directly attributable to the business combination included in the reported pro forma revenue and earnings. ASU 2010-29 is effective prospectively for business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after December 15, 2010. Early adoption is permitted. The Company is currently evaluating the impact of this ASU and expected the adoption of this ASU will have an impact on its future business combinations.

17

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

3.

|

SEGMENT INFORMATION

|

The Company establishes standards for reporting information about operating segments on a basis consistent with the Company’s internal organization structure as well as business segments and major customers in financial statements. The Company operates in three principal reportable segments: Fishery Development Division, and HU Plantation Division and Organic Fertilizer and Bread Grass Division and discontinued Dairy Production Division since January 1, 2011.

|

Three months ended March 31, 2011

|

||||||||||||||||||||||||

|

Continuing operations

|

Discontinued

operations

|

|||||||||||||||||||||||

|

Fishery

Development

Division

|

HU

Plantation

Division

|

Organic

Fertilizer

and Bread

Grass

Division

|

Corporate and

others

|

Dairy

Production

Division

|

Total

|

|||||||||||||||||||

|

$

|

$

|

$

|

$

|

$

|

$

|

|||||||||||||||||||

|

Revenue

|

1,559,745 | - | 1,561,786 | - | - | 3,121,531 | ||||||||||||||||||

|

Net income (loss)

|

920,798 | (19,799 | ) | 355,681 | (345,767 | ) | 10,203,951 | 11,114,864 | ||||||||||||||||

|

Total assets

|

19,634,875 | 22,246,476 | 5,403,607 | 63,952,922 | - | 111,237,880 | ||||||||||||||||||

|

For the three months ended March 31, 2010

|

||||||||||||||||||||||||

|

Continuing operations

|

Discontinued

operations

|

|||||||||||||||||||||||

|

Fishery

Development

Division

|

HU

Plantation

Division

|

Organic

Fertilizer

and Bread

Grass

Division

|

Corporate and

others

|

Dairy

Production

Division

|

Total

|

|||||||||||||||||||

|

$

|

$

|

$

|

$

|

$

|

$

|

|||||||||||||||||||

|

Revenue

|

300,000 | - | - | - | 4,111,322 | 4,411,322 | ||||||||||||||||||

|

Net income (loss)

|

286,496 | (31,942 | ) | - | (5,026,350 | ) | 1,604,669 | (3,167,127 | ) | |||||||||||||||

|

Total assets

|

14,097,403 | 10,814,097 | - | 20,565,911 | 40,943,667 | 86,421,078 | ||||||||||||||||||

18

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

4.

|

INCOME TAXES

|

United States of America

SIAF was incorporated in the United States of America. SIAF has no trading operations in United States of America and no US corporate tax has been provided in the financial statements of SIAF.

China

Beginning January 1, 2008, the new Enterprise Income Tax (“EIT”) law replaced the existing laws for Domestic Enterprises (“DEs”) and Foreign Invested Enterprises (“FIEs”). The new standard EIT rate of 25% replaced the 33% rate currently applicable to both DEs and FIEs. The Company is currently evaluating the impact that the new EIT will have on its financial condition. Beginning January 1, 2008, China unified the corporate income tax rule on foreign invested enterprises and domestic enterprises. The unified corporate income tax rate is 25%.

Under new tax legislation of China beginning January 2008, the agriculture, dairy and fishery sectors are exempted from enterprise income taxes.

No EIT has been provided in the financial statements of CA, ZX, JHST and SJAP since they are exempted from EIT for the three months ended March 31, 2011 and 2010 as they are within the agriculture, dairy and fishery sectors and ZX had been derecognized as a subsidiary since January 1, 2011.

Belize and Malaysia

CA, CS and CH are international business companies incorporated in Belize, and are exempted from corporation tax of Belize.

All sales invoices of CA were issued by its representative office in Malaysia and its trading and service activities are conducted in China. As the Malaysia tax law imposed on a territorial basis and not on a worldwide basis, CA’s income is not subject to Malaysia corporation tax.

No Belize and Malaysia corporation tax have been provided in the financial statements of CA for the three months ended March 31, 2011 and 2010.

Hong Kong

No Hong Kong profits tax has been provided in the financial statements of PMH and TRW, since they did not earn any assessable profits for the for the three months ended March 31, 2011 and 2010 and PHM was dissolved on January 28, 2011.

Macau

No Macau Corporation tax has been provided in the financial statements of HYT, APWAM and MEIJI since they did not earn any assessable profits for the three months ended March 31, 2011 and 2010 and HYT had been derecognized as a subsidiary since January 1, 2011.

19

SINO AGRO FOOD, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

|

6.

|

NET INCOME FROM DISCONTINUED OPERATIONS

|

On February 15, 2011 and on March 29, 2011, the Company entered the agreement and memorandum of understanding, respectively to sell 100% equity interest in HYT group (including HYT and ZX) to Mr. Xin Ming Sun, director of ZhongXingNong Nu Co., Ltd for $45,000,000 and the effective date is January 1, 2011. HYT group contributed revenue and net income of Dairy Production Division. As the Dairy Production Division represented a separate business segment, the disposal group has been treated as a discontinued operation in this quarterly financial report. The post-tax result of the Dairy Production Division has been disclosed as a discontinued operation in the consolidated statements of income and comprehensive income.

|

Three months ended

|

Three months ended

|

|||||||||

|

Note

|

March 31, 2011

|

March 31, 2010

|

||||||||

|

(Unaudited)

|

(Unaudited)

|

|||||||||

|

$

|

$

|

|||||||||

|

Revenue

|

- | 4,111,322 | ||||||||

|

Cost of goods sold

|

- | 1,824,741 | ||||||||

|

Gross profit

|

- | 2,286,581 | ||||||||

|

General and administrative expenses

|

- | (111,241 | ) | |||||||

|

Net income from operations

|

- | 2,175,340 | ||||||||

|

Interest expense

|

- | (118,072 | ) | |||||||

|

Net income before income taxes

|

- | 2,057,268 | ||||||||

|

Net income from disposal of subsidiaries

|

(a)

|

19,941,880 | - | |||||||

|

Net income before income taxes

|

19,941,880 | 2,057,268 | ||||||||

|

Provision for income taxes

|

- | - | ||||||||

|

Net income from discontinued operations

|

19,941,880 | 2,057,268 | ||||||||

|