Attached files

| file | filename |

|---|---|

| 8-K - ROSE UPDATED COMPANY PRESENTATION - NBL Texas, LLC | rosepres.htm |

Rosetta Resources Inc.

Speaker: Randy L. Limbacher

August 2011

www.rosettaresources.com / NASDAQ: ROSE

High Asset Quality - Executing Business Plan - Future Growth Catalysts - Financial Strength

Exhibit 99.1

2

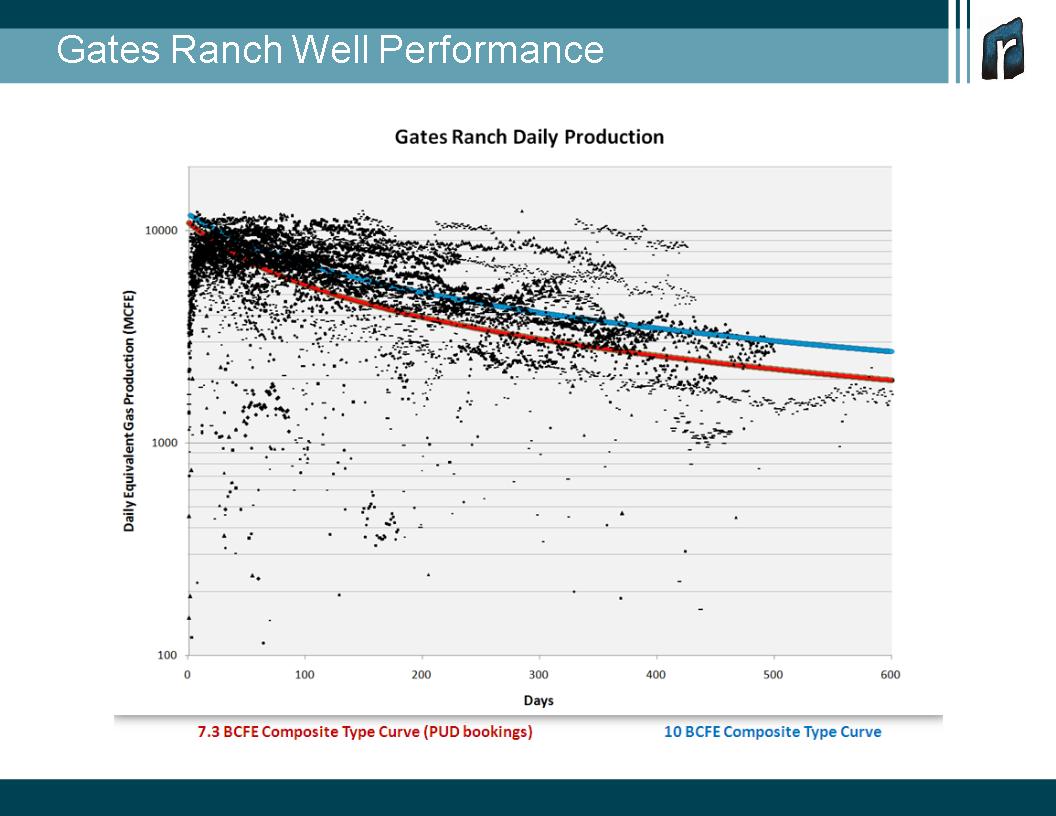

– Doubled proved reserves to 970 Bcfe at mid-year 2011.

– Increased gross estimated ultimate recovery to 10 Bcfe per

Gates Ranch Eagle Ford well.

Gates Ranch Eagle Ford well.

– Set record levels of daily equivalent gas and liquids

production.

production.

– Expanded Southern Alberta Basin horizontal drilling program.

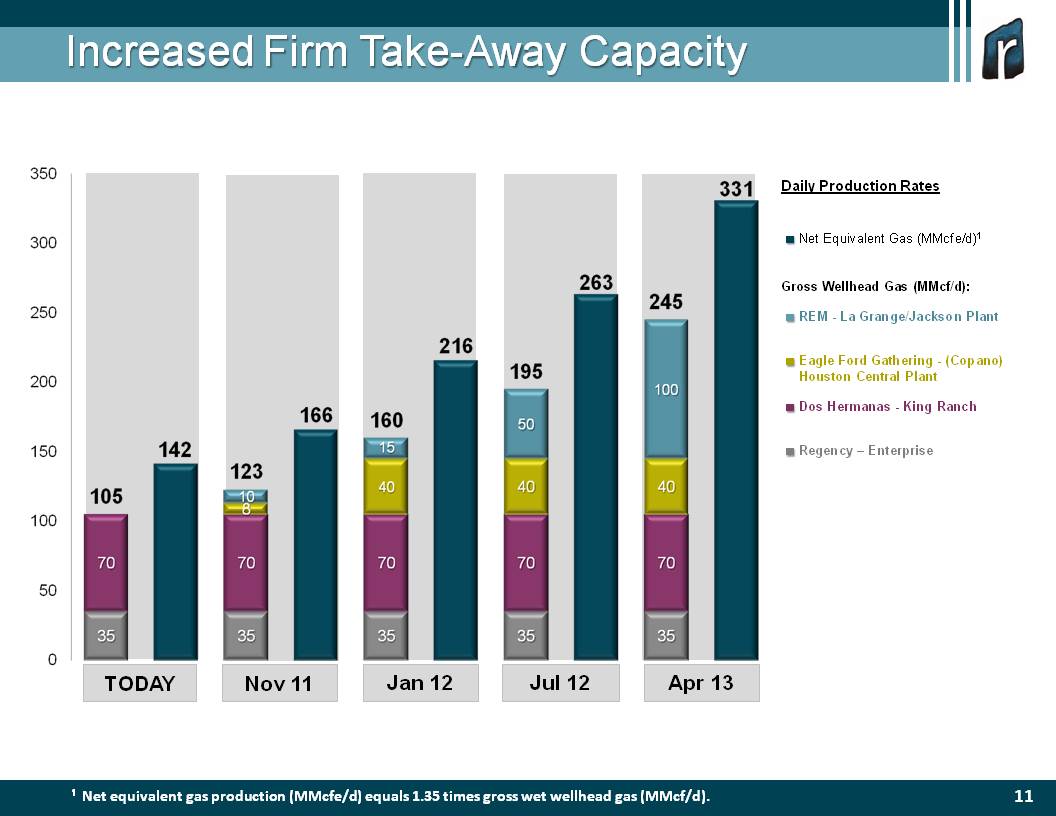

– Increased daily firm transportation and processing capacity

from Eagle Ford by 20 percent.

from Eagle Ford by 20 percent.

– Increased 2011 Capital Budget to $475 million.

Year-to-Date Highlights

3

– Asset Base High Graded

– Executing Business Plan

– Testing Growth Catalysts

– Financial Strength

Agenda

4

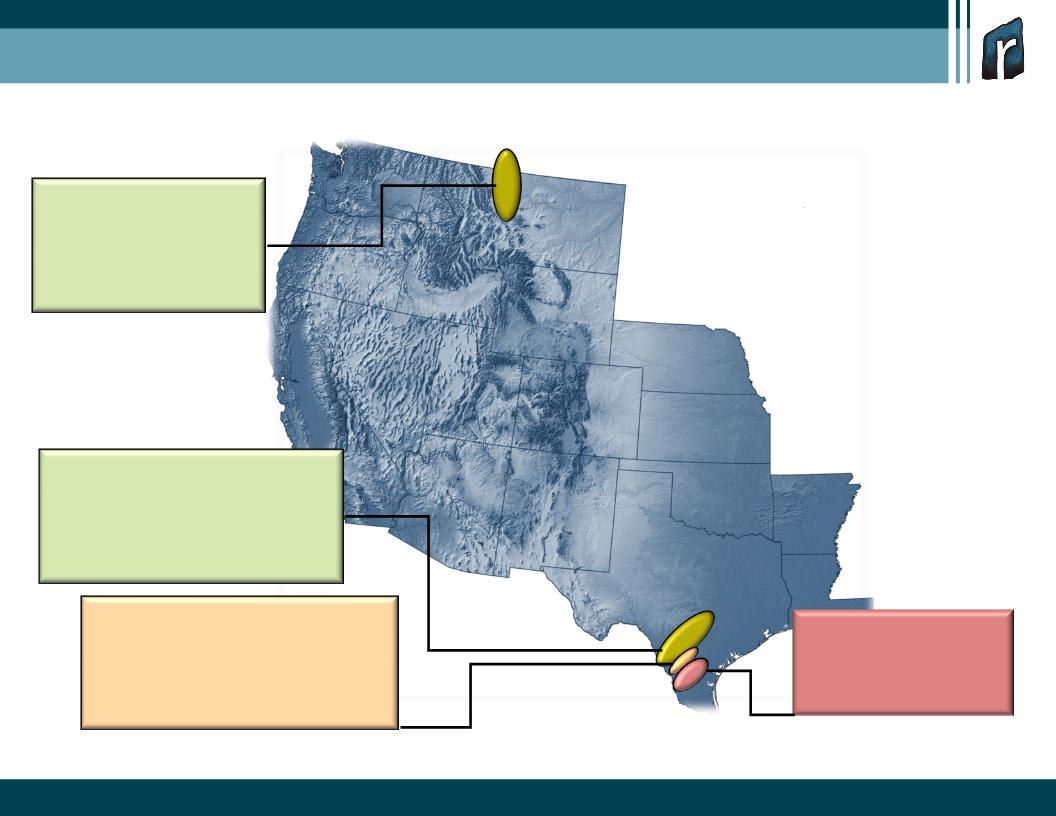

Asset Base High Graded

5

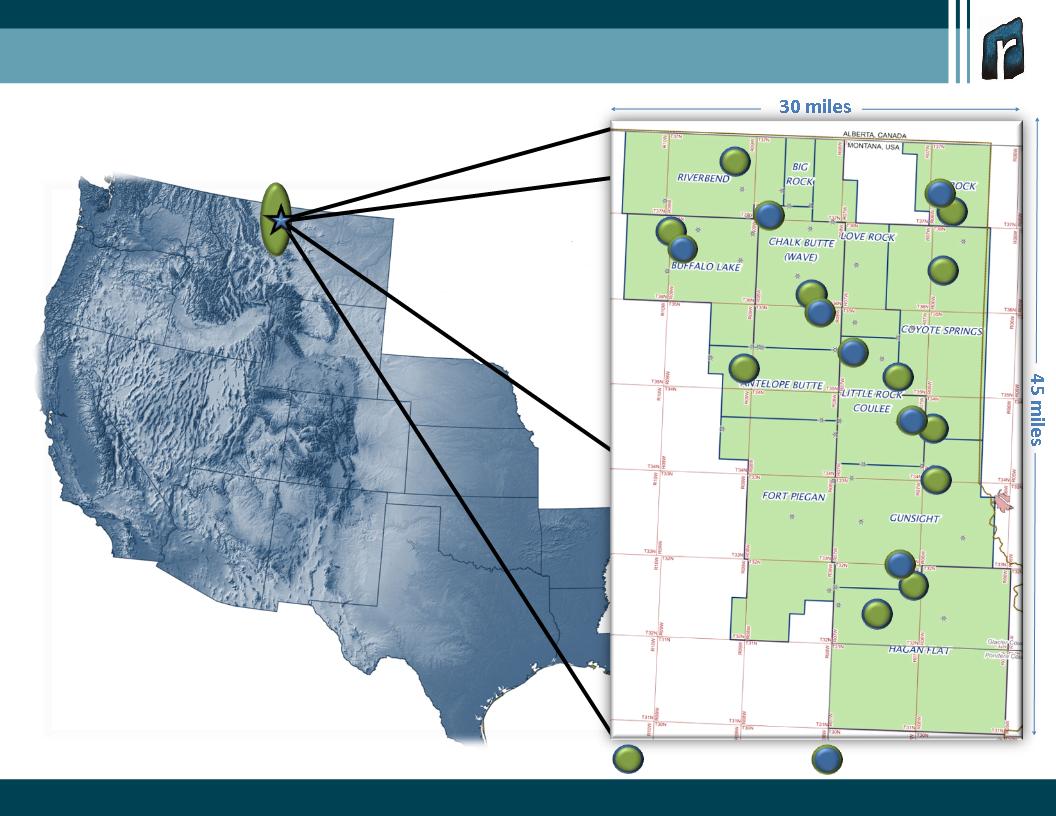

Alberta Basin

300,000 net acres

6 BBOE hydrocarbon resource in place

1500 potential locations

Exploration underway

11 delineation wells completed

7 horizontal wells planned (2011)

Eagle Ford Liquids

50,000 net acres

20 TCFE hydrocarbon resource in place

450 potential remaining locations (excluding infill)

36 horizontal wells completed*

125 MMcfe/d net*

6-10 years of potential remaining inventory

Eagle Ford Dry Gas

15,000 net acres

5 TCFE hydrocarbon resource in place

145 potential locations (excluding infill)

4 horizontal wells completed*

5 MMcfe/d net*

3-4 years of remaining inventory

South Texas

(Non-Eagle Ford)

100,000 net acres

Numerous stacked reservoirs

20 MMcfe/d net*

* End of 2Q 2011

Asset Base High Graded

6

Executing Business Plan

7

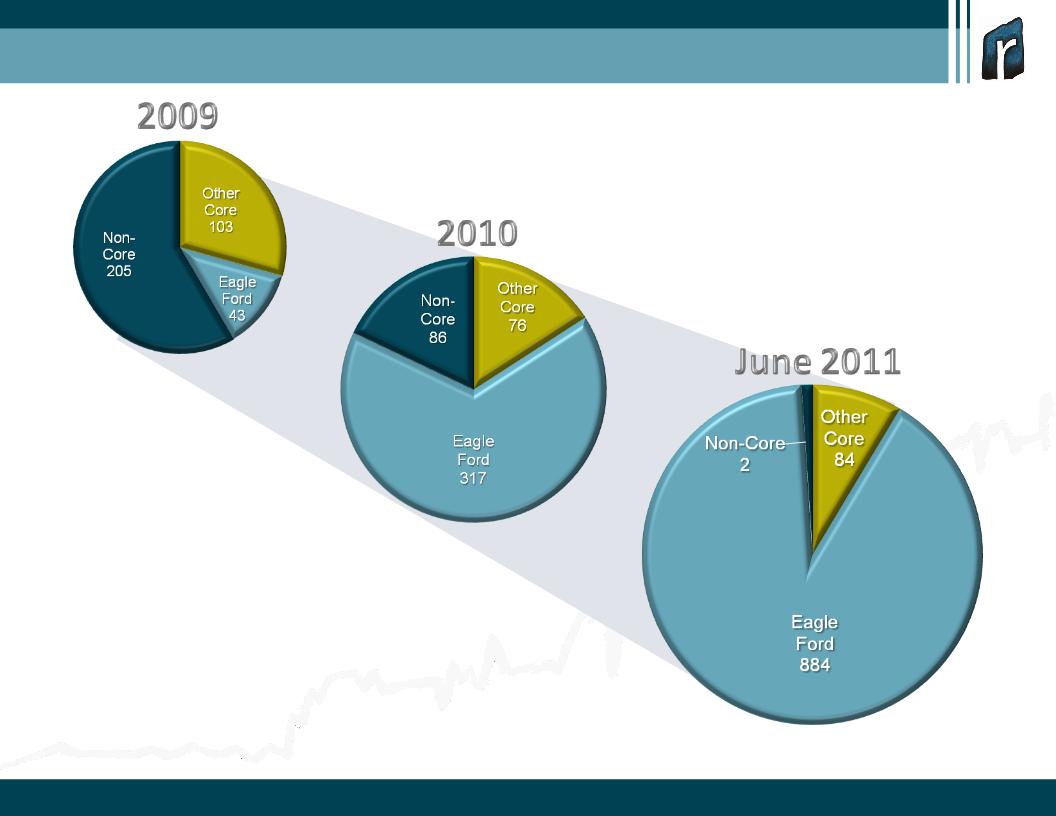

Proved Reserves - Doubled Since YE 2010

■ Eagle Ford

■ Other Core

■ Non-Core

351 Bcfe

479 Bcfe

970 Bcfe

8

Year-end 2011: 58 wells*

* Completed wells

9 miles

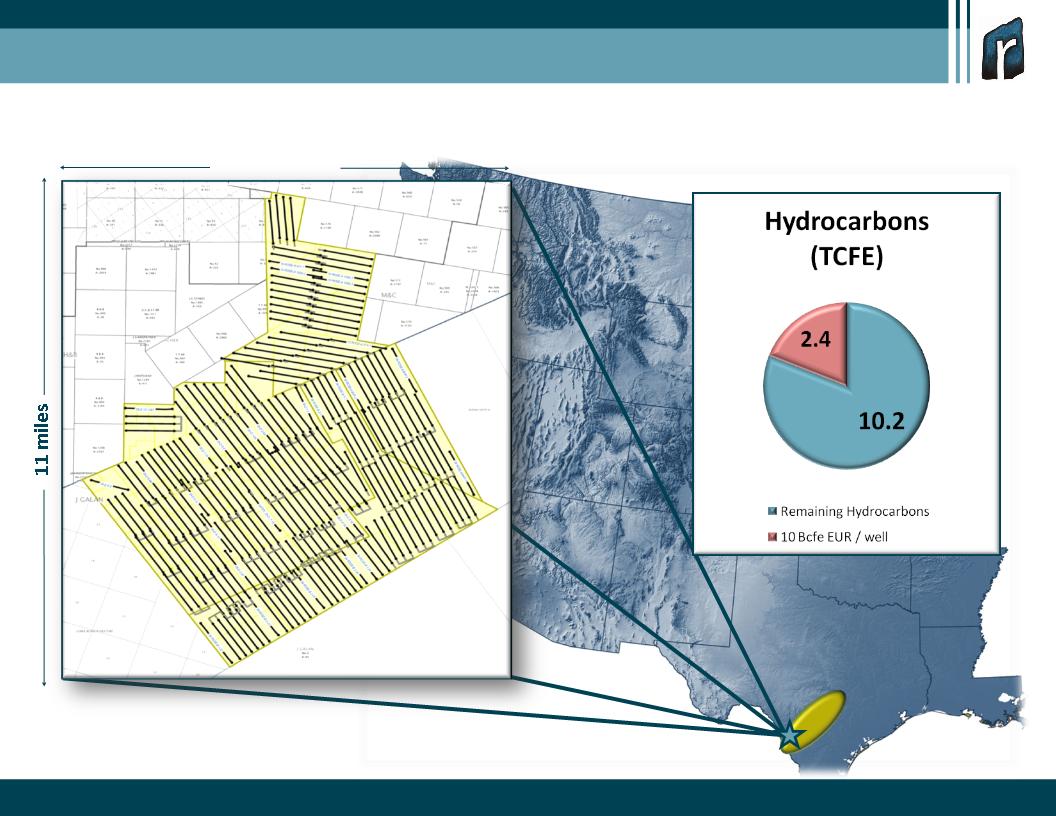

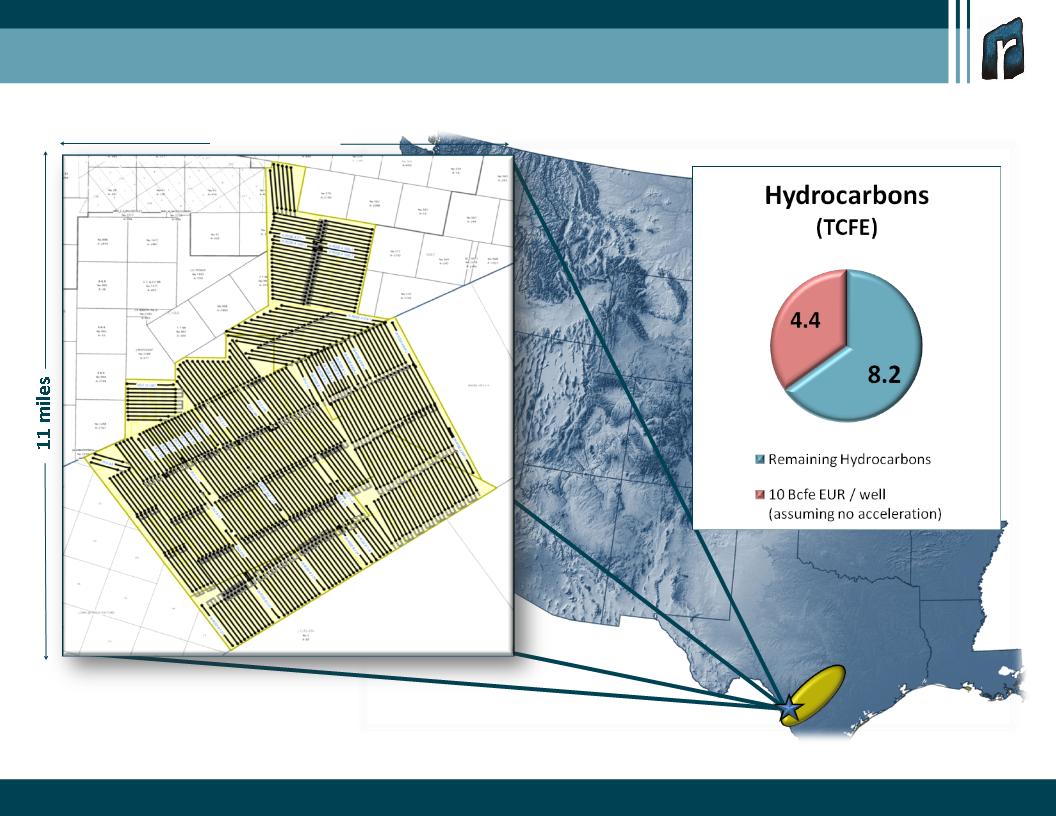

More than 12 TCFE of “hydrocarbons in place” have been delineated and are

now being exploited…

now being exploited…

Gates Ranch

9

10

Field Development: 236 wells*

*Excludes infill drilling

9 miles

Using our current development pace, well spacing, and type curve, we will have continued

development through 2016…while recovering approximately 20% of the hydrocarbons in place…

development through 2016…while recovering approximately 20% of the hydrocarbons in place…

Gates Ranch

12

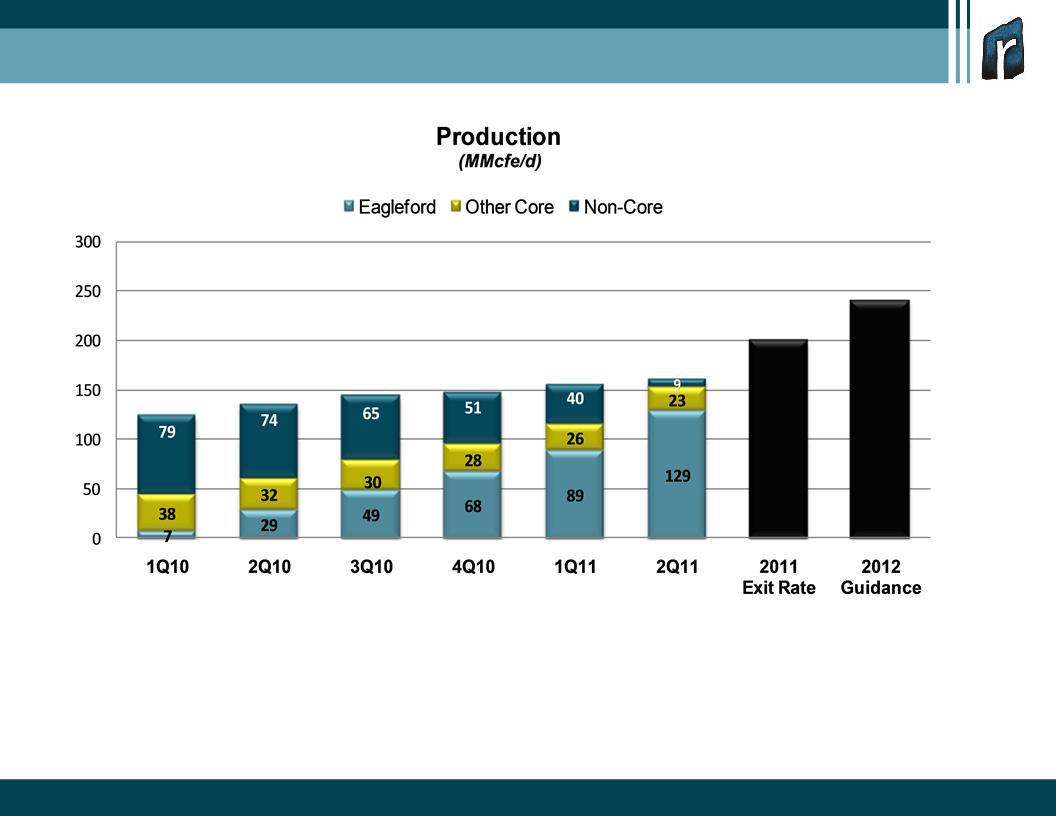

Strong Exit Rates and 2012 Growth Projected

190-200

220-240

13

Testing Growth Catalysts

14

* Includes 50- to 60-acre infill drilling which will be tested during the latter part of 2011.

Field Development: 441 wells*

9 miles

Gates Ranch Infill Drilling

15

|

Area

|

Window

|

Net

Acreage |

|

Gates Ranch

|

Liquids

|

26,500

|

|

Non-Gates Ranch

|

Liquids

|

23,500

|

|

Encinal Area

|

Dry Gas

|

15,000

|

|

TOTAL

|

|

65,000

|

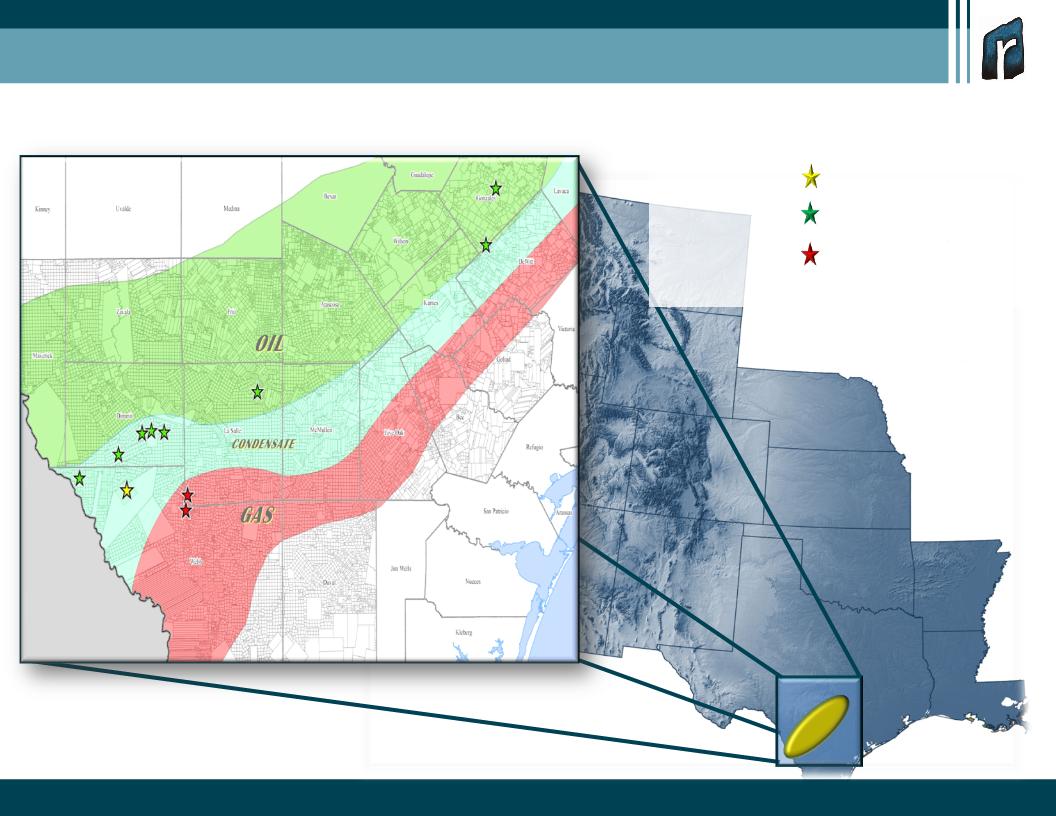

Other Eagle Ford Areas

16

Delineation Wells (11)

Current 7-well HZ Program

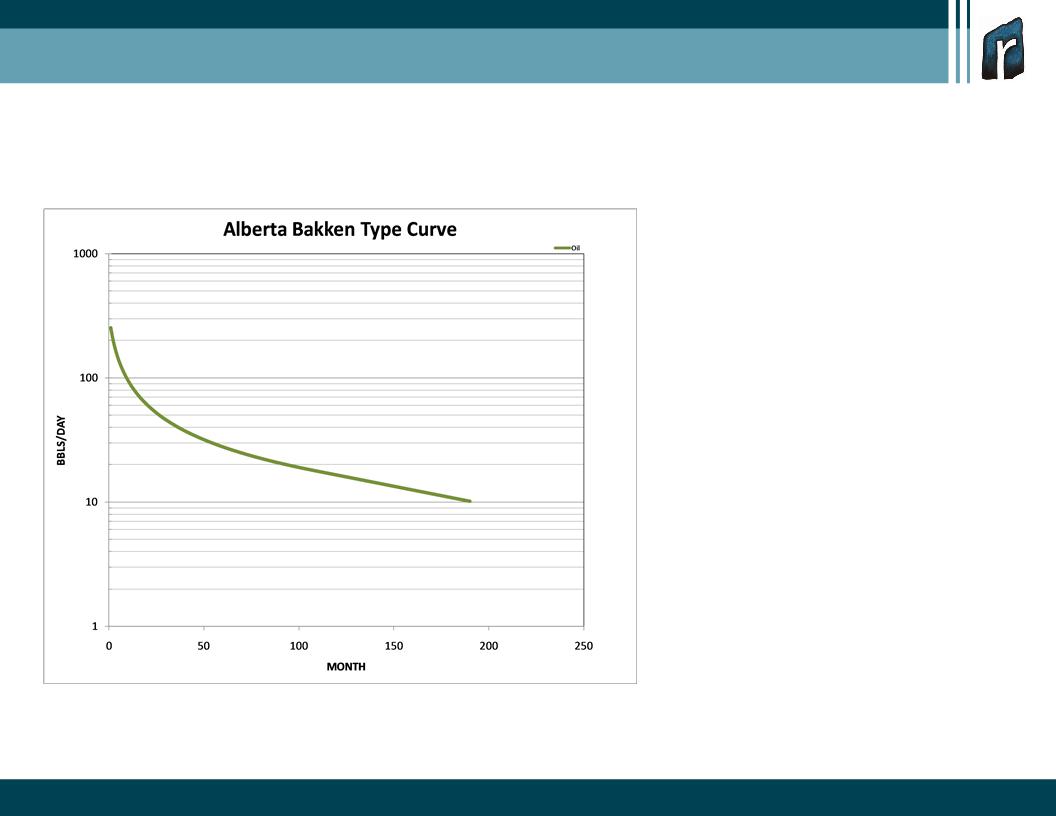

Expanded Southern Alberta Basin Horizontal Drilling

17

Well Performance Parameters

§ 250 IP BOEPD (gross)

§ 185,000 BOE EUR (gross)

§ 160-acre spacing

§ $4 million well costs

Southern Alberta Basin

Representative Base Case Economic Model

|

Per Well Economics (BFIT)

|

||

|

Pricing ($/BBL WTI)

|

$85

|

$95

|

|

ROR (%)

|

21.3

|

35.1

|

|

NPV 10% ($M)

|

931

|

1,926

|

|

F/D ($/BOE)

|

27.46

|

27.46

|

18

Financial Strength

19

Lower Cost Structure

|

|

Six Months Ended

|

||||||

|

S/Mcfe

|

|

June 30, 2011

(Actual)

|

|

|

July-December, 2011

(Guidance Range)

|

||

|

Direct LOE

|

$

|

0.59

|

|

$

|

0.36

|

$

|

0.40

|

|

Workovers

|

|

0.02

|

|

|

0.02

|

|

0.03

|

|

Insurance

|

|

0.02

|

|

|

0.02

|

|

0.02

|

|

Ad Valorem Tax

|

|

0.19

|

|

|

0.10

|

|

0.12

|

|

Production Taxes

|

|

0.16

|

|

|

0.18

|

|

0.22

|

|

Treating, Transportation & Marketing

|

|

0.29

|

|

|

0.60

|

|

0.66

|

|

G&A, excluding stock-based compensation

|

|

0.74

|

|

|

0.56

|

|

0.62

|

|

Interest Expense

|

|

0.40

|

|

|

0.29

|

|

0.32

|

|

DD&A

|

|

2.36

|

|

|

1.73

|

|

1.91

|

20

50

20

6,950

5,400

3,750

21

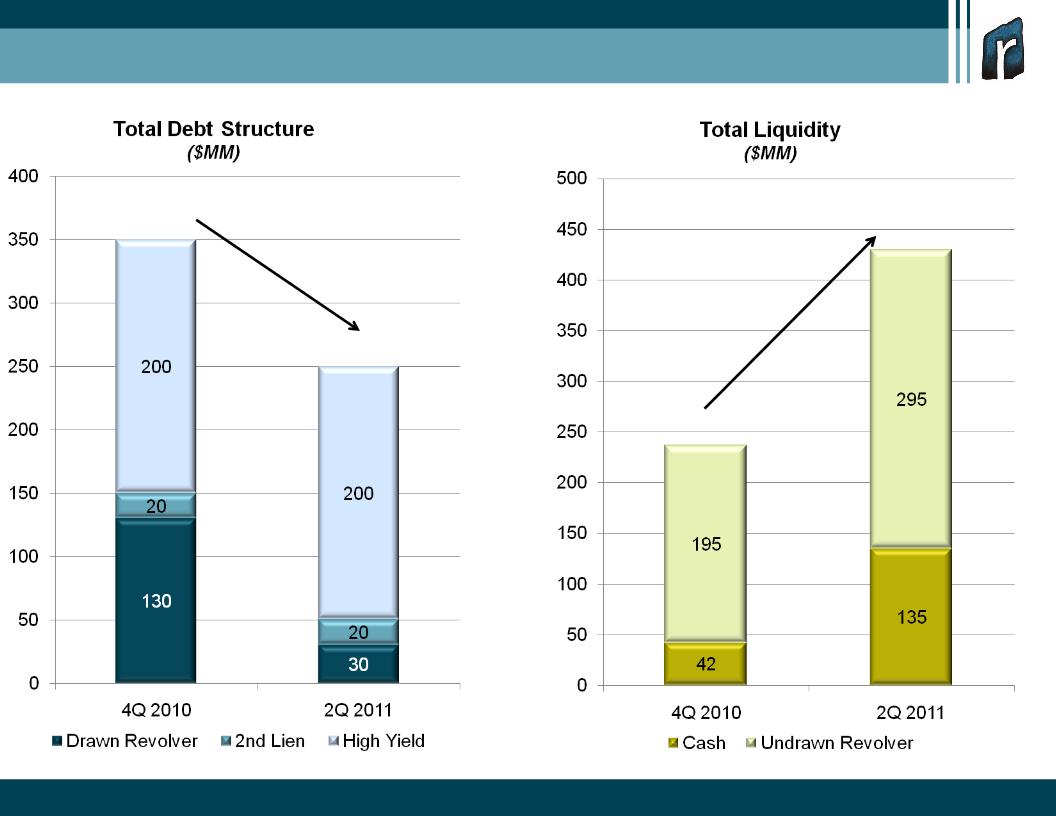

Debt and Liquidity

350

250

430

237

22

|

(MM)

|

2Q 2011

|

4Q 2010

|

|

Long-Term Debt

|

$250

|

$350

|

|

Total Stockholder’s Equity

|

547

|

529

|

|

TOTAL

|

$797

|

$879

|

|

|

|

|

|

Capitalization

|

|

|

|

- Debt

|

31%

|

40%

|

|

- Capital

|

69%

|

60%

|

|

TOTAL

|

100%

|

100%

|

Capital Structure

23

– Asset Base High Graded

– Divestiture program complete

– South Texas focus

– Alberta Basin option

– Strong Eagle Ford project inventory

– Executing Business Plan

– Proved reserves doubled since 12/31/10

– Gates Ranch recoveries increased

– Increased firm take-away capacity

– Strong exit rates and 2012 growth projected

– Testing Growth Catalysts

– Gates Ranch infill

– Other Eagle Ford areas

– Expanded Alberta Basin horizontal program

– Financial Strength

– Lower cost structure

– $430MM in liquidity

Summary

24

This presentation includes forward-looking statements, which give the Company's current expectations or

forecasts of future events based on currently available information. Forward-looking statements are

statements that are not historical facts, such as expectations regarding drilling plans, including the

acceleration thereof, production rates and guidance, resource potential, incremental transportation capacity,

exit rate guidance, net present value, development plans, progress on infrastructure projects, exposures to

weak natural gas prices, changes in the Company's liquidity, changes in acreage positions, expected

expenses, expected capital expenditures, and projected debt balances. The assumptions of management and

the future performance of the Company are subject to a wide range of business risks and uncertainties and

there is no assurance that these statements and projections will be met. Factors that could affect the

Company's business include, but are not limited to: the risks associated with drilling of oil and natural gas

wells; the Company's ability to find, acquire, market, develop, and produce new reserves; the risk of drilling

dry holes; oil and natural gas price volatility; derivative transactions (including the costs associated therewith

and the abilities of counterparties to perform thereunder); uncertainties in the estimation of proved, probable,

and possible reserves and in the projection of future rates of production and reserve growth; inaccuracies in

the Company's assumptions regarding items of income and expense and the level of capital expenditures;

uncertainties in the timing of exploitation expenditures; operating hazards attendant to the oil and natural gas

business; drilling and completion losses that are generally not recoverable from third parties or insurance;

potential mechanical failure or underperformance of significant wells; availability and limitations of capacity in

midstream marketing facilities, including processing plant and pipeline construction difficulties and operational

upsets; climatic conditions; availability and cost of material, supplies, equipment and services; the risks

associated with operating in a limited number of geographic areas; actions or inactions of third-party operators

of the Company's properties; the Company's ability to retain skilled personnel; diversion of management's

attention from existing operations while pursuing acquisitions or dispositions; availability of capital; the

strength and financial resources of the Company's competitors; regulatory developments; environmental risks;

uncertainties in the capital markets; general economic and business conditions (including the effects of the

worldwide economic recession); industry trends; and other factors detailed in the Company's most recent

Form 10-K, Form 10Q and other filings with the Securities and Exchange Commission. If one or more of these

risks or uncertainties materialize (or the consequences of such a development changes), or should underlying

assumptions prove incorrect, actual outcomes may vary materially from those forecasted or expected. The

Company undertakes no obligation to publicly update or revise any forward-looking statements except as

required by law.

forecasts of future events based on currently available information. Forward-looking statements are

statements that are not historical facts, such as expectations regarding drilling plans, including the

acceleration thereof, production rates and guidance, resource potential, incremental transportation capacity,

exit rate guidance, net present value, development plans, progress on infrastructure projects, exposures to

weak natural gas prices, changes in the Company's liquidity, changes in acreage positions, expected

expenses, expected capital expenditures, and projected debt balances. The assumptions of management and

the future performance of the Company are subject to a wide range of business risks and uncertainties and

there is no assurance that these statements and projections will be met. Factors that could affect the

Company's business include, but are not limited to: the risks associated with drilling of oil and natural gas

wells; the Company's ability to find, acquire, market, develop, and produce new reserves; the risk of drilling

dry holes; oil and natural gas price volatility; derivative transactions (including the costs associated therewith

and the abilities of counterparties to perform thereunder); uncertainties in the estimation of proved, probable,

and possible reserves and in the projection of future rates of production and reserve growth; inaccuracies in

the Company's assumptions regarding items of income and expense and the level of capital expenditures;

uncertainties in the timing of exploitation expenditures; operating hazards attendant to the oil and natural gas

business; drilling and completion losses that are generally not recoverable from third parties or insurance;

potential mechanical failure or underperformance of significant wells; availability and limitations of capacity in

midstream marketing facilities, including processing plant and pipeline construction difficulties and operational

upsets; climatic conditions; availability and cost of material, supplies, equipment and services; the risks

associated with operating in a limited number of geographic areas; actions or inactions of third-party operators

of the Company's properties; the Company's ability to retain skilled personnel; diversion of management's

attention from existing operations while pursuing acquisitions or dispositions; availability of capital; the

strength and financial resources of the Company's competitors; regulatory developments; environmental risks;

uncertainties in the capital markets; general economic and business conditions (including the effects of the

worldwide economic recession); industry trends; and other factors detailed in the Company's most recent

Form 10-K, Form 10Q and other filings with the Securities and Exchange Commission. If one or more of these

risks or uncertainties materialize (or the consequences of such a development changes), or should underlying

assumptions prove incorrect, actual outcomes may vary materially from those forecasted or expected. The

Company undertakes no obligation to publicly update or revise any forward-looking statements except as

required by law.

Forward-Looking Statements and Terminology Used

25

For filings reporting year-end 2010 reserves, the SEC permits the optional disclosure of probable and possible

reserves. The Company has elected not to report probable and possible reserves in its filings with the

SEC. We use the term “net risked resources” to describe the Company’s internal estimates of volumes of

natural gas and oil that are not classified as proved reserves but are potentially recoverable through

exploratory drilling or additional drilling or recovery techniques. Estimates of unproved resources are by their

nature more speculative than estimates of proved reserves and accordingly are subject to substantially greater

risk of actually being realized by the Company. Estimates of unproved resources may change significantly as

development provides additional data, and actual quantities that are ultimately recovered may differ

substantially from prior estimates. We use the term “BFIT NPV10” to describe the Company’s estimate of

before income tax net present value discounted at 10 percent resulting from project economic evaluation. The

net present value of a project is calculated by summing future cash flows generated by a project, both inflows

and outflows, and discounting those cash flows to arrive at a present value. Inflows primarily include revenues

generated from estimated production and commodity prices at the time of the analysis. Outflows include

drilling and completion capital and operating expenses. Net present value is used to analyze the profitability of

a project. Estimates of net present value may change significantly as additional data becomes available, and

with adjustments in prior estimates of actual quantities of production and recoverable reserves, commodity

prices, capital expenditures, and/or operating expenses.

reserves. The Company has elected not to report probable and possible reserves in its filings with the

SEC. We use the term “net risked resources” to describe the Company’s internal estimates of volumes of

natural gas and oil that are not classified as proved reserves but are potentially recoverable through

exploratory drilling or additional drilling or recovery techniques. Estimates of unproved resources are by their

nature more speculative than estimates of proved reserves and accordingly are subject to substantially greater

risk of actually being realized by the Company. Estimates of unproved resources may change significantly as

development provides additional data, and actual quantities that are ultimately recovered may differ

substantially from prior estimates. We use the term “BFIT NPV10” to describe the Company’s estimate of

before income tax net present value discounted at 10 percent resulting from project economic evaluation. The

net present value of a project is calculated by summing future cash flows generated by a project, both inflows

and outflows, and discounting those cash flows to arrive at a present value. Inflows primarily include revenues

generated from estimated production and commodity prices at the time of the analysis. Outflows include

drilling and completion capital and operating expenses. Net present value is used to analyze the profitability of

a project. Estimates of net present value may change significantly as additional data becomes available, and

with adjustments in prior estimates of actual quantities of production and recoverable reserves, commodity

prices, capital expenditures, and/or operating expenses.

Forward-Looking Statements and Terminology Used (cont.)