Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CAPITAL ONE FINANCIAL CORP | d8k.htm |

| EX-99.2 - EXHIBIT 99.2 - CAPITAL ONE FINANCIAL CORP | dex992.htm |

1

August 10, 2011

Acquisition of HSBC Domestic Card Business

Acquisition of HSBC Domestic Card Business

Investor Presentation

Investor Presentation

Exhibit 99.1 |

| 2

Forward Looking Statements

Forward Looking Statements

This presentation contains forward-looking statements within the meaning of the

Private Securities Litigation Reform Act giving Capital One’s

expectations or predictions of future financial or business performance or conditions. Such forward-

looking statements include, but are not limited to, statements about the projected

impact and benefits of the acquisition by Capital One of the HSBC domestic

credit card businesses, including future financial and operating results, Capital One’s

plans, objectives, expectations and intentions and other statements that are not

historical facts. These forward-looking statements are subject to

numerous assumptions, risks and uncertainties which change over time. Forward-looking

statements speak only as of the date they are made and Capital One assumes no duty

to update forward-looking statements.

In addition to factors previously disclosed in Capital One’s filings with the

U.S. Securities and Exchange Commission and those identified elsewhere in

this presentation, the following factors, among others, could cause actual results to differ

materially from forward-looking statements or historical performance: the

possibility that regulatory and other approvals and conditions

to

the

transaction

are

not

received

or

satisfied

on

a

timely

basis

or

at

all;

the

possibility

that

modifications

to

the

terms of the transaction may be required in order to obtain or satisfy such

approvals or conditions; the possibility that Capital One will not receive

third-party consents necessary to fully realize the anticipated benefits of the transaction; the

possibility

that

Capital

One

may

not

fully

realize

the

projected

cost

savings

and

other

projected

benefits

of

the

acquisition

of

the HSBC domestic credit card businesses in the event that Capital One's pending

acquisition of the ING Direct business does not close timely or at all;

changes in the anticipated timing for closing the transaction; difficulties and delays in

integrating the HSBC domestic credit card businesses or fully realizing projected

cost savings and other projected benefits of the transaction; business

disruption during the pendency of or following the transaction; the inability to sustain revenue

and earnings growth; changes in interest rates and capital markets; diversion of

management time on transaction-related issues; reputational risks and

the reaction of customers and counterparties to the transaction; and changes in asset quality

and credit risk as a result of the transaction.

Annualized, pro forma, projected and estimated numbers are used for illustrative

purposes only, are not forecasts and may not reflect actual results.

|

| 3

Transaction Summary

Transaction Summary

Receivables Purchased

$29.6 billion

Premium Offered

8.75% cash premium or $2.59 billion as of June 30, 2011

Approvals

Customary OCC approval

Platform Acquired

Partnership infrastructure

Real estate and data centers

Capital

Tier 1 common equity ratio expected to be in the mid-9 percent range at

the

end

of

the

second

quarter

of

2012,

including

planned

capital

raise

of approximately $1.25 billion; Capital One has the option of issuing

$750 million of the $1.25 billion to HSBC at $39.23 per share (the

average of the closing prices of Capital One shares on August 8 & 9,

2011)

Intangibles & Goodwill

Goodwill of ~$1.2 billion

Purchased Credit Card Relationship intangible of $2.9 billion

Fair Value Mark

2.8% fair value mark

Restructuring Charges

$420 million

Operating Expense

Synergies

$350 million, or 23% of HSBC Domestic Card business expense base

Expected Closing

Second Quarter 2012 |

4

The HSBC domestic credit card business is attractive

The HSBC domestic credit card business is attractive

Profitable

national-scale

card business

Profitable

through Great

Recession

Strong

management

team

Premier retail

partnership

franchise |

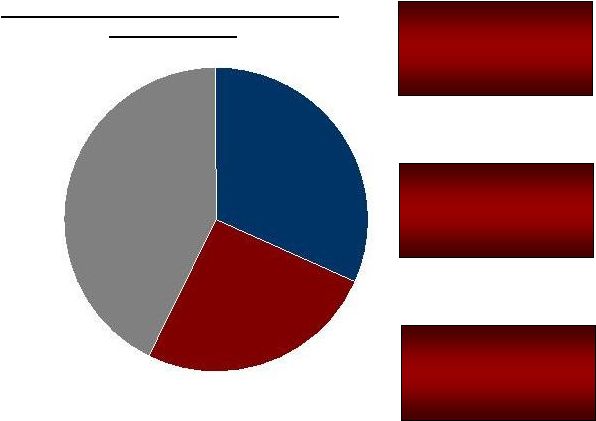

5

Retail

Partnerships*

Co-Branded

Partnerships*

Bank Card

The HSBC domestic credit card portfolio is comprised of

The HSBC domestic credit card portfolio is comprised of

three business segments

three business segments

•

General Motors and AFL-CIO co-

branded cards

•

3.3MM active accounts

•

21 partnerships, including Neiman

Marcus, Saks Fifth Avenue and

Best Buy

•

13.6MM active accounts

Card Portfolio Business Segments (~$30B)

($B as of 5/31/11)

•

Primarily MasterCard branded

•

10.3MM active accounts

•

Includes some run-off portfolios

*The transfer of certain partnerships in the HSBC domestic credit card portfolio will require the

consent of the applicable partners. To the extent that the Company does not obtain the

consent of any such partner, that partner's relationship and related card balances will be excluded from the sale to the Company.

Source: HSBC financials

Bank Card

$9.4

Co-Branded

Partnerships

$7.6

Retail

Partnerships

$12.7 |

HSBC

has built a premier partnership franchise HSBC has built a premier partnership

franchise 6 |

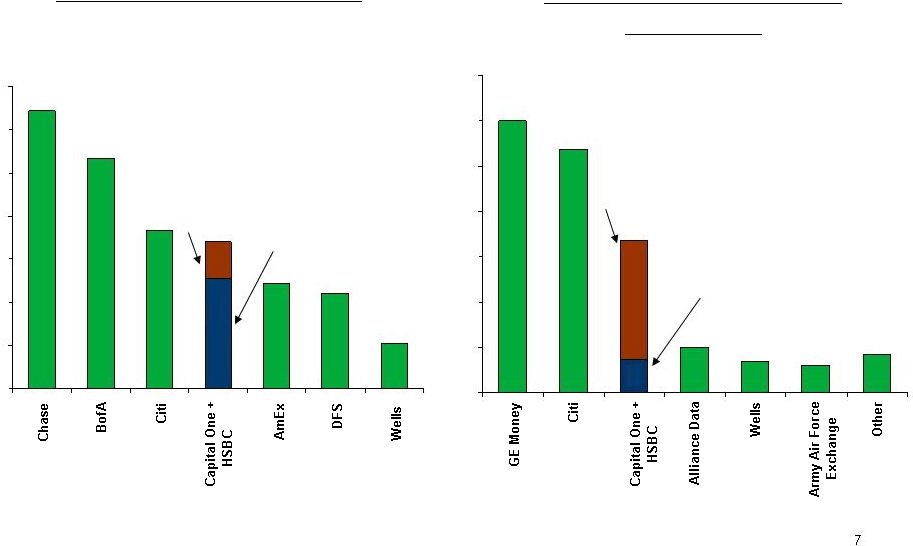

7

Acquiring the HSBC domestic credit card business

Acquiring the HSBC domestic credit card business

significantly expands and enhances our Card franchise

significantly expands and enhances our Card franchise

$B

U.S. Credit Card Outstandings

Q1 2011

U.S. Private Label Retail Card

Outstandings

2010 Year-End

$B

$68

Capital One

HSBC

$17

Capital One

HSBC

*Chase includes WaMu; B of A is US consumer card; Citi excludes Citi Holdings,

Capital One is domestic card; HSBC excludes ~$13B of retail HSBC partnership

outstandings; AmEx excludes charge-card, Discover includes business

card. Source: Company reports, Nilson 2011, HSBC financials

$21

$44

$73

$107

$129

$49

$51

$0

$20

$40

$60

$80

$100

$120

$140

$4

$4

$3

$5

$27

$30

$4

$0

$5

$10

$15

$20

$25

$30

$35 |

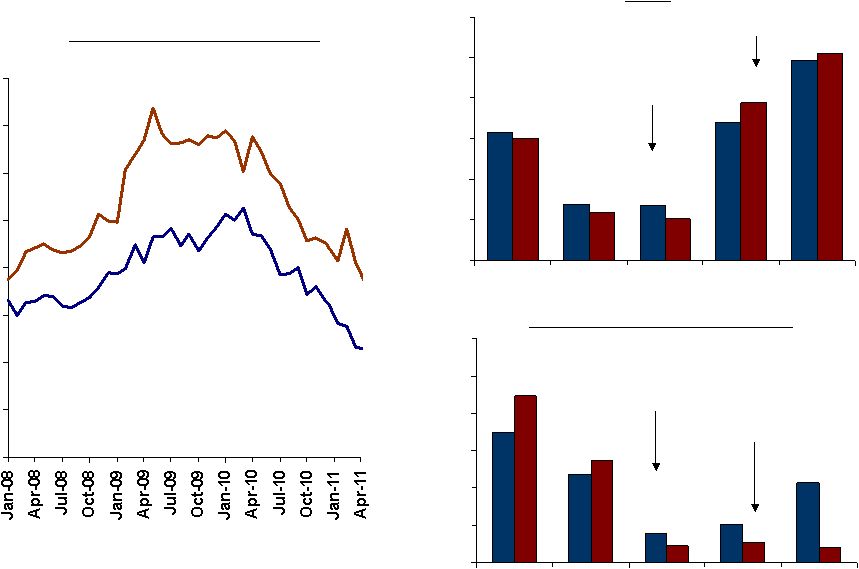

8

HSBC’s domestic credit card business remained profitable

HSBC’s domestic credit card business remained profitable

throughout the Great Recession

throughout the Great Recession

3.2%

1.4%

1.4%

3.4%

4.9%

3.9%

5.1%

1.0%

3.0%

1.2%

0%

1%

2%

3%

4%

5%

6%

2007

2008

2009*

2010

Q1 2011

ROA

2007 –

Q1 2011

Capital One

HSBC

Note: Data shown is post-tax. HSBC post-tax figures calculated by

assuming a 35% tax rate. COF data is Domestic Card. Accounting is IFRS

for HSBC. HSBC P&L includes GPCC & PLCC.

Source: Company Data

*HSBC Q2 09 excludes $350MM (post-tax) goodwill charge.

3.5%

2.4%

0.8%

1.0%

2.1%

4.5%

0.4%

0.5%

0.5%

2.7%

0%

1%

2%

3%

4%

5%

6%

2007

2008

2009*

2010

Q1 2011

ROA excluding Allowance

2007 –

Q1 2011

Capital One

HSBC

0%

2%

4%

6%

8%

10%

12%

14%

16%

Capital One

Domestic Card

HSBC

Total Book

Monthly Charge-Off Rate |

9

We expect the acquisition of HSBC’s domestic credit card

We expect the acquisition of HSBC’s domestic credit card

business to deliver compelling financial and strategic results

business to deliver compelling financial and strategic results

•

High-teens GAAP and operating EPS

accretion in 2013

•

Return on invested capital greater

than 25% in 2013

•

IRR greater than 20%

•

ROTE improvement of ~400 basis

points in 2013

•

Strong EPS accretion drives 4 year

earn back of expected tangible book

value per share dilution

•

Strong capital generation

Compelling Strategic

Value

Attractive Deal

Economics

•

Expands and enhances card

franchise

•

Establishes market leading

partnership platform

•

27MM new active accounts

•

Technology and capabilities

significantly advance partnership

franchise

•

Excellent fit with Capital One’s

proven capabilities in credit card

business

•

Significant financial and

strategic upside

•

Low business execution risk

Anticipated deal economics assume closing of ING Direct acquisition and are based

on IBES EPS estimates pro-forma for the ING Direct acquisition |