Attached files

| file | filename |

|---|---|

| EX-23.3 - EX-23.3 - CPG INTERNATIONAL INC. | a2203483zex-23_3.htm |

| EX-23.4 - EX-23.4 - CPG INTERNATIONAL INC. | a2203483zex-23_4.htm |

| EX-23.2 - EX-23.2 - CPG INTERNATIONAL INC. | a2203483zex-23_2.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on August 5, 2011

Registration No. 333-173678

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 2

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CPG INTERNATIONAL INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

3080 (Primary Standard Industrial Classification Code Number) |

20-2779385 (I.R.S. Employer Identification Number) |

888 North Keyser Avenue

Scranton, Pennsylvania 18504

(570) 558-8000

(Address, including zip code, and telephone number, including

area code, of registrant's principal executive offices)

Scott C. Harrison

Chief Financial Officer

888 North Keyser Avenue

Scranton, Pennsylvania 18504

(570) 558-8000

(Name, address, including zip code,

and telephone number, including area code, of agent for service)

| Copies to: | ||

Andrew B. Barkan, Esq. Fried, Frank, Harris, Shriver & Jacobson LLP One New York Plaza New York, New York 10004 (212) 859-8000 |

Marc D. Jaffe, Esq. Ian D. Schuman, Esq. Latham & Watkins LLP 885 Third Avenue New York, New York 10022 (212) 906-1200 |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check One):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý | Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) |

||

|---|---|---|---|---|

Common Stock, $0.01 par value |

$150,000,000 | $17,415 | ||

|

||||

- (1)

- Estimated

solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933.

- (2)

- Including

additional shares of common stock that may be purchased pursuant to the underwriters' overallotment option.

- (3)

- Previously paid.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Subject to Completion, dated August 5, 2011

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS

CPG International Inc.

Common Stock

This is the initial public offering of our common stock. We are offering shares of our common stock and the selling stockholder is offering shares. We will not receive any proceeds from sale of shares held by the selling stockholder. No public market currently exists for our common stock. Certain members of our management and board of directors as well as entities affiliated with AEA Investors LP, our sponsor, have an equity interest in the selling stockholder.

We have applied to list our common stock on the New York Stock Exchange under the symbol "AZEK."

We anticipate that the initial public offering price will be between $ and $ per share.

Investing in our common stock involves risks. See "Risk Factors" beginning on page 19 of this prospectus.

| |

Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Price to the public |

$ | $ | |||||

Underwriting discounts and commissions |

$ | $ | |||||

Proceeds to us (before expenses) |

$ | $ | |||||

Proceeds to the selling stockholder (before expenses) |

$ | $ | |||||

We and the selling stockholder have granted the underwriters the option to purchase additional shares of common stock on the same terms and conditions set forth above if the underwriters sell more than shares of common stock in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2011.

| Barclays Capital | Deutsche Bank Securities | Credit Suisse |

Prospectus dated , 2011

i

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by or on behalf of us that we have referred to you. We have not, the selling stockholder has not and the underwriters have not authorized any other person to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. This prospectus does not constitute an offer to sell, or solicitation of an offer to buy, to any person in any jurisdiction in which such an offer to sell or solicitation would be unlawful. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus, regardless of its time of delivery or of any sales of shares of our common stock. Our business, financial condition, results of operations or cash flows may have changed since such date.

This prospectus includes market and industry data that we obtained from a market study by L.E.K. Consulting LLC, or L.E.K., which we commissioned in March 2011, as well as from publicly available industry sources, including studies and reports by Harvard University's Joint Center for Housing Studies, the U.S. Federal Reserve and the U.S. Census Bureau. In addition, this prospectus includes market and industry data that we prepared primarily based on our management's knowledge and experience in the markets in which we operate, together with information obtained from surveys, reports by market research firms, our customers, distributors, suppliers, trade and business organizations and other contacts in the markets in which we operate. Market share data is subject to change and may be limited by the availability of raw data, the voluntary nature of the data gathering process and other limitations inherent in any statistical survey of market shares. In addition, customer preferences are subject to change. References herein to our being a leader in a market or product category refer to our belief that we have a leading market share position in each specified market based on sales dollars, unless the context otherwise requires, and do not take into account non-synthetic competitive products. In addition, the discussions herein regarding our various markets are based on how we define the markets for our products, which products may be either part of larger overall markets or markets that include other types of products. When we use the term "North America" in this prospectus, we are referring to the United States and Canada.

Unless stated otherwise herein, all market share and market size data about the exterior trim market, deck market, rail market, bathroom partition market and locker market, and other markets for synthetic products, as well as our position and the positions of our competitors within these markets, including our products relative to our competitors, are based on the market study by L.E.K. that we commissioned, excluding those estimates that are qualified by our belief. In developing its market study, L.E.K. utilized primary research and analysis together with certain third party data. In those instances where L.E.K.'s market study contains ranges of market share, market size, growth rates and other data, we have presented in this prospectus the midpoint of such ranges.

For an overview of the industry sources that we cite in this prospectus, see "Business—Our Industry and End-Markets—Industry Sources."

This prospectus includes trademarks and service marks owned by us, including CPG International™, AZEK®, Scranton Products®, Vycom®, Celtec®, Corrtec™, Flametec®, Hiny Hiders®, Playboard®, Procell®, Resistall™, Sanatec®, Seaboard®, TuffTec Lockers®, Arbor Collection®, Harvest Collection®, Acacia®, Cobre®, Fawn®, Kona®, Morado®, Redland Rose®, Sedona®, Silver Oak™ and Tahoe®, as well as trademarks and service marks owned by third parties.

ii

This summary highlights selected information about our business and about this offering contained elsewhere in this prospectus. It does not contain all of the information that may be important to you. You should carefully read this entire prospectus, including the matters discussed in the section entitled "Risk Factors" and the consolidated financial statements and the related notes, before investing in our common stock. Unless the context otherwise requires, references in this prospectus to "our company," "we," "our" or "us" (or similar terms) refer to CPG International Inc. together with its consolidated subsidiaries. The term "Holdings" refers to CPG International Holdings LP, the owner of 100% of our common stock prior to the completion of this offering and the selling stockholder in this offering. Unless otherwise stated or the context otherwise requires, operating data in this prospectus relating to our business, including without limitation the number of distribution locations, distributors, dealers, retail outlets and registered contractors, are as of March 31, 2011. References herein to "conversion" refer to an increase in the use of low maintenance synthetic building products in replacement of or substitution for building products made of other materials, in particular wood, wood composites and metal.

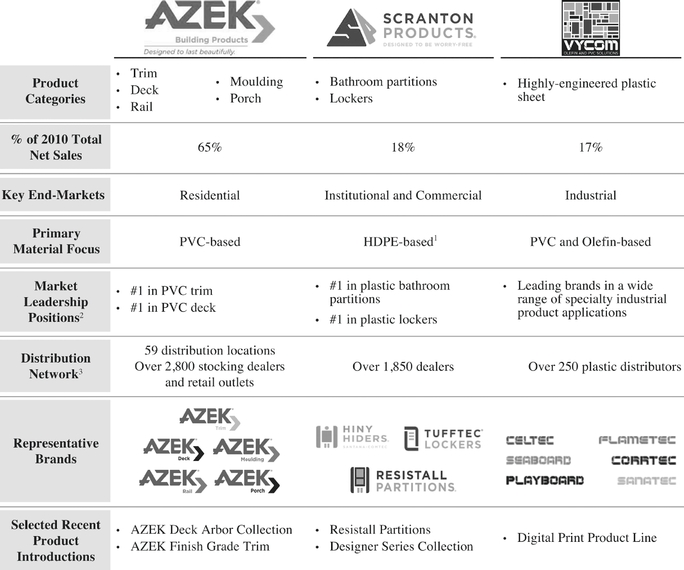

We are a leading manufacturer and innovator of low maintenance, premium branded synthetic building products that are replacing wood, wood composites, metal and other materials in the residential, institutional, commercial and industrial end-markets. Across each of our three operating segments, AZEK® Building Products, Scranton Products® and Vycom®, we have market-leading brands and products that offer a compelling value proposition, including enhanced durability and quality, attractive aesthetics and lower installation, maintenance and life cycle costs. We offer exterior residential building solutions including trim, deck, rail, moulding and porch products through our AZEK Building Products, or AZEK, segment, interior institutional and commercial solutions including bathroom partitions and lockers through our Scranton Products, or Scranton, segment and highly-engineered industrial plastic sheet products through our Vycom segment. AZEK holds the #1 market share position in the North American polyvinyl chloride, or PVC, trim and deck markets, Scranton Products holds the #1 market share position in the plastic bathroom partition and plastic locker markets and Vycom is a recognized leader in several of its target markets.

Our products are currently in the early growth stage of their life cycles, and we believe we will continue to outperform our markets by taking advantage of the significant conversion, penetration and market expansion opportunities that exist. We continue to drive increased material conversion towards our products through product innovation, an extensive and growing sales and distribution network targeting and educating key influencers and decision makers, and selected acquisitions. Since 2001, we have grown our sales by a compound annual growth rate, or CAGR, of approximately 15.0% to $327.5 million for the year ended December 31, 2010.

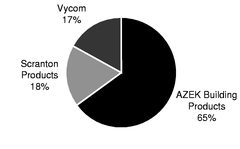

We operate on a national basis in all 50 states and in Canada. Our three operating segments are end-market focused and operate under the same philosophy of identifying market needs and being the first to provide impactful and innovative solutions for the most demanding applications. The following charts show our 2010 sales by segment and by estimated end-market.

2010 Sales by Segment |

2010 Sales by Estimated End-Market |

|

|

|

1

The following table provides an overview of our three operating segments:

- 1

- In this prospectus, we refer to high-density polyethylene as "HDPE."

- 2

- According to L.E.K. See "Market and Industry Data."

- 3

- Numbers reflected are approximate as of March 31, 2011.

We sell our low maintenance synthetic products into a variety of large, attractive segments within the U.S. construction market, which includes residential, institutional, commercial and industrial end-markets. We also sell certain Vycom products into industrial original equipment manufacturer, or OEM, markets. Overall demand for building products is driven by a number of factors, including consumer confidence, availability of credit, trends in the construction cycle and general economic cycles. Examples of specific industry dynamics that we believe impact our company include increasing demand for low maintenance products and lower life cycle costs, greater focus on energy efficiency and homeowners' desire for increased use of outdoor living space. We believe these trends have and will continue to drive growth in our specific end-markets at a rate above the broader U.S. construction market. In addition, according to a market study by L.E.K. that we commissioned in March 2011, these

2

addressable end-markets, which collectively represented approximately $4.9 billion in 2010 sales, are in the midst of significant material conversion from wood, wood composites, metal and other materials to synthetic products made from materials including PVC and HDPE. Synthetic materials are increasingly being substituted for traditional building materials such as wood and metal, due to their aesthetics, lower life cycle costs and greater overall value proposition. Synthetic building products were first introduced decades ago in the residential window and siding markets and have the number one market share in those markets today. As a result of the successful penetration of these early applications and continued advances in material science and manufacturing, synthetic materials have more recently increased their share in other building product segments such as deck, trim and rail within the residential market, and bathroom partitions and lockers in the institutional and commercial markets.

We believe low maintenance synthetic products offer a compelling value proposition, including enhanced durability and quality, attractive aesthetics and lower installation, maintenance and life cycle costs relative to traditional and other materials, such as wood, wood composites and metal. For example, over a projected 20 year period, L.E.K. estimates that cellular PVC-based deck products will have approximately 50% lower life cycle costs than wood and wood composites. Cellular PVC-based products have continued to take market share from traditional materials and other synthetic materials, due to their superior product qualities. For example, according to L.E.K., penetration of low maintenance products, of which cellular PVC-based is the largest category, in the approximately $1.8 billion deck market has nearly tripled from 4% in 2008 to 11% in 2010 and is anticipated to continue to increase over the next several years.

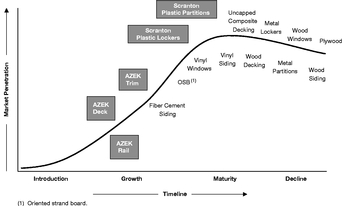

The following table illustrates the size of the addressable market opportunity by sales dollars for select product categories and the anticipated increase in penetration of low maintenance products over the next several years. In addition, the following chart presents an illustrative penetration curve of our synthetic product categories compared to certain building products made of other materials.

Selected Addressable Market Opportunities

($ in millions)

| |

|

Low Maintenance Penetration |

||||

|---|---|---|---|---|---|---|

| |

2010 Total North American Market Size (All Materials) |

|||||

| |

2010 | 2015E | ||||

Trim |

$1,050-1,150 | 17-19% | 21-23% | |||

Deck |

$1,700-1,800 | 10-12% | 19-21% | |||

Rail |

$1,400-1,500 | 6-8% | 13-15% | |||

Partitions |

$250-270 | 33-38% | 35-40% | |||

Lockers |

$290-310 | 4-5% | 5-6% | |||

Source: L.E.K.

Building Products Illustrative Penetration Curve

Source: L.E.K.

Over the last several years, the general economy, and particularly the U.S. construction market, experienced a significant downturn. However, we began to see recovery in many of our end-markets beginning in 2010. The outlook for the residential repair and remodeling market, which was more resilient through the recent economic downturn than the new construction market, is favorable, driven by positive demographic trends and a growing and aging housing stock. L.E.K. expects the residential repair and remodeling market to grow by a CAGR of approximately 4% between 2010 and 2015. The outlook for new residential construction in the United States also is favorable, supported by continued household formation, population growth, attractive mortgage rates and low new home inventory levels. Harvard University's Joint Center for Housing Studies expects that the number of households in the

3

United States will grow by approximately 1.3 million to 1.5 million per year on average between 2010 and 2020, or a total of approximately 12.5 million to 14.8 million additional households, over the same time period. L.E.K.'s housing starts forecast from 2010 to 2015 estimates a CAGR of approximately 19%, with new housing starts reaching approximately 1.4 million in 2015. While 2010 remained challenging in our institutional and commercial end-markets, these markets are late-cycle in nature and are expected to benefit from greater access to financing and a continued general economic recovery. L.E.K. forecasts that U.S. commercial construction markets will increase by a CAGR of approximately 8% and the education segment of the institutional construction market will increase by a CAGR of approximately 2%, in each case from 2010 to 2015. The industrial market is tied to the health of the industrial economy as commonly represented as growth in industrial production, which L.E.K. forecasts to grow at an annual rate of approximately 3% through 2015.

For an overview of the industry sources that we cite in this prospectus, see "Business—Our Industry and End-Markets—Industry Sources."

Market leader in large, attractive and high growth sectors. We maintain leading market positions in a number of highly attractive, large and underpenetrated markets in the early stages of material conversion. Our AZEK brand currently holds the #1 market share position in the North American PVC trim and deck markets. In 2010, the total market size for all materials in the trim, deck and rail markets was approximately $4.3 billion and, at AZEK, we are currently pursuing additional opportunities within the broader North American exterior residential building products market. In addition, Scranton Products currently holds the #1 market share position in plastic bathroom partitions and plastic lockers, and Vycom is a recognized leader in several of its target markets. Overall, at Scranton and Vycom, we are currently pursuing approximately $800 million of market opportunities.

Our high quality synthetic products are currently in the early growth stage of their life cycles, and we believe that we will continue to outperform our markets by taking advantage of the significant conversion, penetration and market expansion opportunities that exist. For example, according to L.E.K., PVC trim, low maintenance deck and premium rail products are expected to grow from approximately 18%, 11% and 7% of the total U.S. trim, deck and rail markets, respectively, based on 2010 sales to 22%, 20% and 14% by 2015. Additionally, we believe that the anticipated recovery in the residential, institutional, commercial and industrial construction markets will further provide an opportunity for growth.

Premium brands supported by unwavering commitment to product quality, innovation and service. Our flagship brands are recognized for high quality products within their respective residential, institutional, commercial and industrial end-markets. For example, ProSales magazine's most recent study of professional dealers found that AZEK Deck is the #1 deck brand "most likely to be stocked." At Scranton Products, we are the #1 specified brand by architects in bathroom partitions. Similarly, our various Vycom brands are highly recognized in their specific market categories. We have achieved our premium brand reputation because of our unwavering commitment to consistently provide high quality and innovative products, and a high level of customer service. We proactively work with and solicit feedback from distributors, dealers, architects, contractors, builders and consumers to better develop products that address unmet customer needs, reduce costs, increase ease of installation and improve aesthetics. These efforts are supported by our research and development, or R&D, process that has resulted in 28 successful new product introductions in the last two years. For the year ended December 31, 2010, our new products introduced in the last two years represented 15.3% of our total sales.

Broad and expanding product offering with superior performance characteristics. We believe our products provide a superior value proposition throughout our supply chain from distributors to dealers

4

and retailers, contractors, builders, architects and ultimately to consumers. The performance characteristics of our products relative to competing products result in lower installation, maintenance and life cycle costs. AZEK's trim, deck, rail, moulding and porch products are aesthetically similar to finished wood but are stain, split and scratch resistant, do not rot or warp, are impervious to water and insect infestation, do not require paint or stains for protection, are easier to mill and fabricate and hold paint longer if paint is desired. As a result, our AZEK trim and deck products have lower life cycle costs than traditional and other materials, such as wood and wood composites. For example, over a projected 20 year period, L.E.K. estimates that cellular PVC-based deck products will have approximately 50% lower life cycle costs than wood and wood composites. For contractors and builders, the performance and workability characteristics of our AZEK products contribute to lower installation costs and fewer call-backs from consumers. The products we offer through our Scranton Products and Vycom segments have similar attributes valued by our customers. As a result of our products' excellent performance characteristics, we have also developed high customer satisfaction and brand loyalty.

We believe the breadth and depth of our product offering gives us a significant competitive advantage in the marketplace. Through our strong manufacturing and technical capabilities and commitment to innovation, we focus on consistently expanding our product offering and the markets we serve. We have one of the broadest synthetic product offerings in our industry segment. Within the past five years we have expanded our AZEK product line from offering primarily trim products to currently offering a broad range of exterior residential building products including trim, deck, rail, moulding and porch. As a result of our product expansion, we believe we have tripled the average potential spend per home for our AZEK products over the past five years.

Comprehensive and growing sales and distribution network. We have developed a tailored sales and distribution strategy focused on educating key influencers and decision makers along the entire supply chain, which we believe will continue to drive further conversion, penetration and growth for our products. We sell our AZEK products through a two-step distribution system across the United States and in Canada, utilizing 59 independent distribution locations that cover over 2,800 stocking dealers and retail outlets supplying more than 2,850 AZEK-registered contractors. We recently expanded AZEK's presence in the retail channel and expect to significantly increase our presence in home centers for our AZEK Deck product. We sell Scranton Products through a national network of more than 1,850 dealers who sell to institutional and commercial customers across the United States and in Canada. Vycom is sold to a national network of more than 250 plastic distributors across the United States, Canada and Latin America, who sell primarily to OEMs.

We significantly invested in our sales force infrastructure across each operating segment through the recent economic downturn by increasing headcount, enhancing training, and implementing a highly integrated customer relationship management, or CRM, system to increase sales efficiency. We also recently realigned our entire sales force to maximize downstream pull-through demand. We supplement the efforts of our sales force with a variety of marketing strategies and tools that include more than 4,000 contractor sample kits and 1,150 display kiosks, product literature, print, TV and radio advertising, trade shows, internet marketing and social media initiatives, sales training and our AZEK University program to educate distributors, dealers, architects, contractors and builders on the advantages of our products. We believe that our distribution strategy, sales and education efforts, and strong customer relationships provide a strong competitive advantage and are difficult for our competitors to replicate.

Strong technical and manufacturing capabilities. Our disciplined, process-oriented operations are built on a foundation that includes deep technical expertise, proprietary material formulations, a broad range of extrusion capabilities, meaningful scale and capacity, and post-extrusion value-add capabilities that enable innovation and expansion into new markets. We are a low-cost, vertically integrated manufacturer focused on continuous improvement and critical-to-quality processes which allow us to obtain high throughput and lower unit production costs while maintaining product integrity. We

5

continued to make capital investments in our technical capabilities and manufacturing systems throughout the recent economic downturn, which we believe will drive operating leverage as we continue to grow our businesses.

Strength of operating model supports growth and overall financial profile. We believe that our operating model has driven our strong growth and market outperformance as well as the development of our industry-leading suite of high quality, innovative products. We believe we provide a superior value proposition throughout the supply chain through our focus on innovation, our technical manufacturing capabilities, our commitment to providing excellent customer service, and the quality of our products. Through our downstream focused sales force infrastructure, go-to-market strategy, and extensive and growing distribution network, we have successfully positioned our products as premium brands within their respective market categories.

Despite the challenging economic environment, our substantial indebtedness, which totaled $325.5 million as of March 31, 2011, and fluctuating raw material prices, we have continued to profitably grow our businesses over the past several years. In the year ended December 31, 2010, we achieved consolidated revenue growth of 23% over 2009, driven by strong gains at AZEK and Vycom of 30% and 53%, respectively. We have also maintained attractive margins, returns on capital and strong free cash flow generation, and we continue to invest in our businesses.

Committed and experienced management team. We have an experienced and committed management team led by our Chief Executive Officer, Eric Jungbluth. Mr. Jungbluth has significant experience in the building products industry including prior roles as President of The HON Company (division of HNI Corporation) and President of Allsteel Inc. as well as leadership positions at Moen Incorporated (division of Fortune Brands), Kirsh (division of Newell), and Warner Lambert. Our senior management team has extensive experience in branding, channel management, new product development, and creating world-class business processes. Collectively, our senior management team has over 120 years of cumulative industry or related industry experience, with certain members having held leadership positions at a number of leading industrial companies, including Sherwin Williams Paint Company, James Hardie Building Products, Silgan Plastics, Gunlocke Company, SI Handling Systems, Lutron Electronics, and Lockheed Martin Company.

Capitalize on continued material conversion and market penetration opportunities. We believe that we will continue to realize significant growth due to our focused efforts to drive material conversion and market penetration of our products, particularly in exterior residential applications for AZEK. We intend to increase conversion and penetration in our markets by educating key influencers and decision makers, which in turn creates pull-through demand for our products. Our integrated approach to understanding the needs and preferences throughout our supply chain enables us to drive conversion by customizing our products to address key shortcomings of alternative products. Our business strategy and marketing efforts are also focused on driving market penetration through a tailored regional market approach. Through these initiatives, we plan to continue to increase the size of the market for our products and enhance growth opportunities beyond our existing product portfolio.

Continue to introduce innovative new products in existing and adjacent markets. We have a history of being a first-to-market innovator focused on R&D and continued product innovation. We utilize a market-focused and solutions-driven approach to innovation by soliciting feedback from distributors, dealers, contractors, builders, architects and consumers in order to develop products that appropriately address their unmet needs. These efforts are supported by our in-house R&D process led by a dedicated staff committed to innovation and continuous improvement of our products. As a result of this strategy, we have developed a robust new product pipeline, which includes new trim, deck, rail, moulding and porch applications, and we are currently developing potential products in the siding

6

category. However, we will need to conduct testing of these products prior to any market introduction. Products that we have developed within the last two years represented 15.3% of our sales for the year ended December 31, 2010, and we believe this trend will continue to grow going forward. We believe that our downstream-focused approach allows us to anticipate market trends and needs, thereby creating additional conversion opportunities, expanding the size of our addressable market, enhancing our overall growth opportunities, and further differentiating us from our competition.

Expand and enhance awareness of our premium brands. The strength of our flagship brands is driven by our reputation for quality and innovation. We developed our strong brand identity by consistently offering a high quality product and by focusing on achieving a high level of customer satisfaction. We intend to continue to invest in our branding efforts through product literature, print, TV and radio advertising, tradeshows, internet marketing and social media initiatives, and sales training. We have also successfully extended our brand through strategic product acquisitions such as Procell (now AZEK Deck) and Composatron (now AZEK Rail) and believe this will continue to be an opportunity in the future. Our continued success is dependent on the strength of our AZEK brand and the performance of our AZEK products, which represent a significant portion of our net sales. We believe that the successful execution of our brand strategy will allow us to accelerate our conversion rate, increase market penetration and enter new end-markets.

Continue to expand our distribution network and sales force. We distribute our products through an extensive and growing multi-channel national distribution network. Since 2001, we have increased the number of AZEK stocking dealers and retail outlets from 150 to over 2,800, including a recent introduction and expansion of our big-box retail presence. While we have significantly expanded our distribution network over the past several years, there still remain sizeable geographic and market expansion opportunities going forward in all of our operating segments. For example, according to L.E.K., the use of low maintenance deck products, of which cellular PVC is the largest category, as a percentage of total deck purchases is expected to increase from approximately 11% in 2010 to 20% in 2015 based on sales. We have also realigned our sales force to enhance geographic and channel coverage and to increase downstream pull-through demand. By continuing to expand our distribution network and to invest in our sales force infrastructure, we seek to accelerate the penetration of our products and expand the size of our addressable markets.

Leverage and enhance our operational and technical capabilities. Our strong extrusion, materials science and overall technical capabilities provide an excellent opportunity to drive innovation and further expand our markets. We believe our process-driven and disciplined operational approach and focus on continuous improvement enables us to continue to innovate, improve product quality and further reduce costs. Through our scalable operating model, we plan to continue making investments that will enhance our extrusion and materials formulation expertise with a view to maintaining our market leading positions, stimulating growth and enhancing our overall financial profile.

Investing in our common stock involves a high degree of risk. You should consider carefully all of the information in this prospectus prior to investing in our common stock. The risks associated with our business include, among other things:

- •

- Our business could be materially and adversely affected by volatility and disruption to the economy;

- •

- Our financial performance is dependent on raw material prices, as well as the continued availability of raw materials;

- •

- Our continued success is dependent on the performance of our AZEK products, which represent a significant portion of our net sales;

7

- •

- We face competition in each of our businesses and our customers may not continue to purchase our products;

- •

- If we fail to successfully develop new and improved products, our business may be materially and adversely affected;

- •

- Our sales, cash flows from operations and results of operations may decrease if our relations with our key distributors

decline;

- •

- If we are unable to meet future capital requirements, our business may be adversely affected;

- •

- Our substantial indebtedness could adversely affect our financial condition;

- •

- Our credit agreements impose significant operating and financial restrictions, which may prevent us from capitalizing on

business opportunities and taking some actions; and

- •

- Because AEA Investors controls a significant percentage of our common stock, it may control all major corporate decisions and its interests may conflict with the interests of other holders of our common stock.

See "Risk Factors" for a description of these and other risks of investing in our common stock.

Our History and Corporate Information

With a focus on manufacturing excellence and quality over the past 27 years, we have been first to market with a number of low maintenance, premium branded synthetic building products that offer compelling value propositions. Our transition from a plastic sheet manufacturer to an advanced materials and solutions provider began in 1990, when we saw an opportunity to extend further into the value chain by targeting the bathroom partition market. In 1999, we entered the residential building products market with our Trimtec cellular PVC trim product that subsequently was rebranded to AZEK Trim in 2001. Since May 2005, AEA Investors LP and certain of its affiliates, or AEA Investors, have owned a majority interest in our company. Since that time, we have continued to innovate and expand our product offering and have continued to enhance our brands through selected strategic acquisitions, including:

- •

- Santana Products (April 2006): We combined Santana Products with our

existing partition business to form the basis of what is now our Hiny Hiders® plastic bathroom partition product line.

- •

- Procell Decking Systems (January 2007): The integration and rebranding of

Procell Decking Systems, or Procell, into our AZEK Deck brand and our extensive distribution network has been critical to our recent success in the deck market. We not only successfully integrated the

acquisition, but also leveraged AZEK's existing brand equity to bolster Procell's product profile and significantly increase its sales. We have also utilized our product development strength to

improve the color and aesthetics of the products.

- •

- Composatron (February 2008): Compos-A-Tron Manufacturing Inc., or Composatron, was a manufacturer of composite railing systems for the residential housing market, which we rebranded as AZEK Rail. In integrating the acquisition, we leveraged AZEK's existing brand equity to bolster the product profile and utilized our product development strength to improve the color and aesthetics of the railing systems and simplify the installation process.

CPG International Inc. is a Delaware corporation. Our principal executive offices are located at 888 North Keyser Avenue, Scranton, Pennsylvania 18504. Our telephone number is (570) 558-8000 and our website can be found at www.cpgint.com. Information on our website is not deemed to be a part of this prospectus. For charts illustrating our organizational structure both prior to and after giving effect to this offering, see "—Organizational Structure."

8

AEA Investors is one of the most experienced global private investment firms. Founded in 1968, AEA Investors currently manages over $4.2 billion of capital for an investor group that includes former and current CEOs of major multinational corporations, family groups, endowment funds and institutions from around the world. With a staff of more than 60 investment professionals and offices in New York, Stamford, London, Munich, Hong Kong and Shanghai, AEA Investors focuses on investing in companies in the industrial products, specialty chemicals, consumer products and services sectors. AEA Investors has particular expertise in the building products sector. In addition to CPG International, AEA Investors' current building products investments include Henry Company and SRS Roofing Supply. Past building products investments include Dal-Tile International, OSI Sealants (through the investment in Sovereign Specialty Chemicals) and TempRite (through the investment in Noveon).

9

Common stock offered by us |

shares. |

|

Common stock offered by the selling stockholder |

shares. |

|

Total offering |

shares. |

|

Common stock to be outstanding after this offering |

shares. |

|

Overallotment option |

The underwriters have an option to purchase a maximum of additional shares of common stock from us and the selling stockholder to cover overallotments. The underwriters can exercise this option at any time within 30 days from the date of this prospectus. |

|

Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting underwriting discounts and estimated offering expenses, will be approximately $ million, assuming the shares are offered at $ (the midpoint of the offering price range set forth on the front cover of this prospectus). We intend to use the net proceeds from shares that we sell to repay $ million of the outstanding principal amount of our indebtedness under and for general corporate purposes. We will not receive any proceeds from the sale of shares by the selling stockholder. Certain members of our management and board of directors as well as entities affiliated with AEA Investors, our sponsor, have an equity interest in the selling stockholder. See "Use of Proceeds." |

|

Dividend policy |

We do not intend to pay any dividends on our common stock in the foreseeable future. See "Dividend Policy." |

|

Proposed New York Stock Exchange symbol |

"AZEK." |

|

Risk factors |

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 19 of this prospectus for a discussion of factors you should carefully consider before investing in our common stock. |

Unless otherwise indicated, the information in this prospectus:

- •

- assumes no exercise of the overallotment option by the underwriters;

- •

- assumes an initial public offering price of $ per share, the midpoint of the offering price range set forth

on the front cover of this prospectus; and

- •

- gives effect to our amended and restated certificate of incorporation and our amended and restated bylaws, which will be in effect prior to the consummation of this offering.

Prior to the effectiveness of the registration statement of which this prospectus forms a part, the number of authorized shares of our common stock will be increased to shares, and each share of common stock then outstanding will be split into shares of common stock by way of a stock split. Unless we specifically state otherwise, the share information in this prospectus reflects the

10

increase in the authorized number of shares of our common stock and the stock split. Following the completion of this offering (and following any exercise of the overallotment option by the underwriters or the expiration of such option), Holdings, the owner of 100% of our common stock prior to this offering, intends to distribute to all of the holders of its class A limited partnership interest units, or Class A Units, and class B limited partnership interest units, or Class B Units, in accordance with and as contemplated by the limited partnership agreement of Holdings (i) the cash proceeds it receives from this offering, less expenses and amounts used to repay outstanding indebtedness of Holdings, and (ii) all remaining shares of our common stock that it holds at such time. After that distribution, Holdings will be dissolved, and former holders of the Class A Units and the Class B Units will then directly hold shares of our common stock. We refer to the foregoing distribution by Holdings and subsequent dissolution of Holdings as the "Distribution."

11

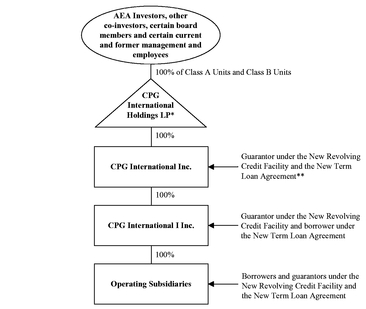

The chart below summarizes our ownership and organizational structure as of the date of this prospectus, prior to giving effect to this offering.

- *

- The general partner of CPG International Holdings LP is CPG Holding I LLC, which is an affiliate of AEA

Investors.

- **

- On February 18, 2011, we entered into a new secured revolving credit facility, which we refer to as the "New Revolving Credit Facility," and a new senior secured term loan agreement, which we refer to as the "New Term Loan Agreement." See "Description of Certain Indebtedness."

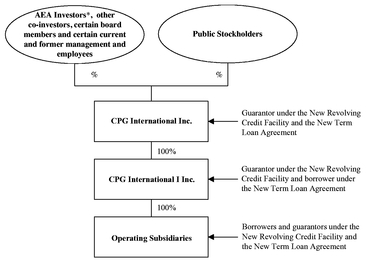

The chart below summarizes our ownership and organizational structure after giving effect to this offering, the stock split and the Distribution.

- *

- Upon completion of this offering, the stock split and the Distribution, AEA Investors will beneficially own approximately % of the voting power of our outstanding common stock. Through this beneficial ownership and a stockholders agreement, which provides voting control over additional shares of our common stock, AEA Investors will control approximately % of the voting power of our outstanding common stock.

12

The summary financial data presented below as of and for the years ended December 31, 2010, 2009 and 2008 have been derived from our audited consolidated financial statements. The audited consolidated financial statements as of December 31, 2010 and 2009 and for the years ended December 31, 2010, 2009 and 2008 are included elsewhere in this prospectus. The summary financial data presented below as of March 31, 2011 and for the three months ended March 31, 2011 and 2010 have been derived from our unaudited condensed consolidated financial statements, which are included elsewhere in this prospectus and have been prepared on the same basis as the audited consolidated financial statements included elsewhere herein. In our opinion, the interim data reflect all adjustments, consisting only of normal and recurring adjustments, necessary for a fair presentation of results for these periods. The operating results for any interim period are not necessarily indicative of the results that may be expected for any other interim period or for a full year.

You should read this data in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and the related notes included elsewhere in this prospectus.

| |

Three Months Ended March 31, |

Year Ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Dollars in thousands) |

2011 | 2010 | 2010 | 2009 | 2008 | ||||||||||||

| |

(unaudited) |

|

|

|

|||||||||||||

Statement of Operations Data: |

|||||||||||||||||

Net sales |

$ | 114,622 | $ | 94,667 | $ | 327,535 | $ | 266,875 | $ | 305,240 | |||||||

Cost of sales |

(81,276 | ) | (65,098 | ) | (226,670 | ) | (173,328 | ) | (235,099 | ) | |||||||

Gross profit |

33,346 | 29,569 | 100,865 | 93,547 | 70,141 | ||||||||||||

Selling, general and administrative expenses |

(15,529 | ) | (14,395 | ) | (56,489 | ) | (57,392 | ) | (50,644 | ) | |||||||

Lease termination expense |

— | — | — | (657 | ) | — | |||||||||||

(Loss) gain on sale of property |

(12 | ) | — | (336 | ) | (525 | ) | 21 | |||||||||

Impairment of goodwill and long-lived assets |

— | (599 | ) | (599 | ) | (14,408 | ) | (40,000 | ) | ||||||||

Operating income (loss) |

17,805 | 14,575 | 43,441 | 20,565 | (20,482 | ) | |||||||||||

Loss on debt extinguishment |

(7,339 | ) | — | — | — | — | |||||||||||

Interest expense, net |

(6,682 | ) | (7,471 | ) | (30,854 | ) | (31,347 | ) | (34,905 | ) | |||||||

Foreign currency gain (loss) |

14 | 78 | 92 | 336 | (215 | ) | |||||||||||

Miscellaneous, net |

— | 7 | 243 | 29 | 153 | ||||||||||||

Income (loss) before income taxes |

3,798 | 7,189 | 12,922 | (10,417 | ) | (55,449 | ) | ||||||||||

Income tax benefit (expense) |

734 | (3,998 | ) | (3,569 | ) | 111 | 7,095 | ||||||||||

Net income (loss) |

$ | 4,532 | $ | 3,191 | $ | 9,353 | $ | (10,306 | ) | $ | (48,354 | ) | |||||

Weighted average shares outstanding (basic and diluted)(1) |

10 | 10 | 10 | 10 | 10 | ||||||||||||

Net income (loss) per share (basic and diluted)(1) |

$ | 453 | $ | 319 | $ | 935.3 | $ | (1,030.6 | ) | $ | (4,835.4 | ) | |||||

13

| |

Three Months Ended March 31, |

Year Ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Dollars in thousands) |

2011 | 2010 | 2010 | 2009 | 2008 | ||||||||||||

| |

(unaudited) |

|

|

|

|||||||||||||

Pro Forma Statement of Operations Data: |

|||||||||||||||||

Pro forma interest expense, net(2) |

$ | $ | |||||||||||||||

Pro forma net income(2) |

$ | $ | |||||||||||||||

Pro forma weighted average shares outstanding(3) |

|||||||||||||||||

Basic |

|||||||||||||||||

Diluted |

|||||||||||||||||

Pro forma net income per share(2)(3) |

|||||||||||||||||

Basic |

$ | $ | |||||||||||||||

Diluted |

$ | $ | |||||||||||||||

Other Financial Data: |

|||||||||||||||||

Capital expenditures |

$ | 5,568 | $ | 3,490 | $ | 15,346 | $ | 6,258 | $ | 6,282 | |||||||

Adjusted EBITDA(4) |

$ | 24,584 | $ | 21,277 | $ | 67,519 | $ | 60,873 | $ | 46,339 | |||||||

Adjusted EBITDA margin(4) |

21.4 | % | 22.5 | % | 20.6 | % | 22.8 | % | 15.2 | % | |||||||

Statement of Cash Flows Data: |

|||||||||||||||||

Net cash (used in) provided by operating activities |

$ | (46,044 | ) | $ | (31,151 | ) | $ | 26,976 | $ | 37,441 | $ | 36,315 | |||||

Net cash used in investing activities |

$ | (5,568 | ) | $ | (3,490 | ) | $ | (15,346 | ) | $ | (7,179 | ) | $ | (47,887 | ) | ||

Net cash provided by (used in) financing activities |

$ | 14,862 | $ | 8,491 | $ | (7,097 | ) | $ | (8,602 | ) | $ | 24,123 | |||||

Balance Sheet Data (at end of period): |

|||||||||||||||||

Cash and cash equivalents |

$ | 12,339 | $ | 49,072 | $ | 44,501 | $ | 22,586 | |||||||||

Total assets |

$ | 574,611 | $ | 553,084 | $ | 539,404 | $ | 538,905 | |||||||||

Total debt(5) |

$ | 325,518 | $ | 305,578 | $ | 307,355 | $ | 314,253 | |||||||||

Total shareholder's equity |

$ | 148,442 | $ | 143,403 | $ | 138,009 | $ | 146,926 | |||||||||

- (1)

- Does

not give effect to the -for-one stock split which will occur prior to the effectiveness of the registration

statement of which this prospectus forms a part.

- (2)

- As

adjusted to give effect to the following transactions as if they had occurred as of the beginning of the period presented: (i) the payment in

full, and termination of, our old revolving credit facility, dated as of February 13, 2008, which we refer to as the "Old Revolving Credit Facility," and our old term loan agreement, dated as

of February 29, 2008, which we refer to as the "Old Term Loan Agreement," (ii) the repurchase and redemption in full of our Senior Floating Rate Notes due 2012, which we refer to as the

"Floating Rate Notes," and our 101/2% Senior Notes due 2013, which we refer to as the "Fixed Rate Notes" (we refer to the Floating Rate Notes and the Fixed Rate Notes collectively as

the "Old Notes"), (iii) the incurrence of $285.0 million of indebtedness under the New Term Loan Agreement, (iv) the incurrence of $40.0 million of indebtedness under the

New Revolving Credit Facility, (v) this offering, (vi) the repayment of $ million of the outstanding principal amount of our indebtedness

under from

the proceeds of this offering and (vii) each of the related adjustments mentioned below.

- Adjustments to net income for the three months ended March 31, 2011 reflect (i) a $ million decrease in interest expense (see the reconciliation of historical interest expense to pro forma interest expense below), (ii) a $ million increase in income tax expense due to higher income before taxes relating to our pro forma net income and (iii) the removal of $ million of AEA Investors management fees. Adjustments to net income for the year

14

ended December 31, 2010 reflect (i) a $ million decrease in interest expense (see the reconciliation of historical interest expense to pro forma interest expense below), (ii) a $ million increase in income tax expense due to higher income before taxes relating to our pro forma net income and (iii) the removal of $ million of AEA Investors management fees. Pro forma net income for the three months ended March 31, 2011 and the year ended December 31, 2010 does not give effect to the payment of management termination fees to AEA Investors of $ .

- The following is a reconciliation of historical net income to pro forma net income for the three months ended March 31, 2011 and the year ended December 31, 2010:

| (Dollars in thousands) |

Three Months Ended March 31, 2011 |

Year Ended December 31, 2010 |

|||||

|---|---|---|---|---|---|---|---|

Net income |

$ | 4,532 | $ | 9,353 | |||

Decrease in interest expense, net(a) |

|||||||

Increase in income tax expense(b) |

|||||||

Removal of management fee(c) |

|||||||

Pro forma net income |

$ | $ | |||||

- (a)

- See

the reconciliation of historical interest expense to pro forma interest expense below.

- (b)

- Reflects

an increase of $ million and $ in income tax expense for the three months ended March 31, 2011

and the

year ended December 31, 2010, respectively, for the related tax effects of the pro forma adjustments. The tax impact is based upon an increase of pro forma income before taxes of

$ million and $ million, respectively, and a statutory tax rate

of %.

- (c)

- Reflects the removal of $ million and $ million of AEA Investors management fees for the three months ended March 31, 2011 and the year ended December 31, 2010, respectively.

- The following is a reconciliation of historical interest expense to pro forma interest expense for the three months ended March 31, 2011 and the year ended December 31, 2010:

| (Dollars in thousands) |

Three Months Ended March 31, 2011 |

Year Ended December 31, 2010 |

|||||

|---|---|---|---|---|---|---|---|

Interest expense, net(a) |

$ | 6,682 | $ | 30,854 | |||

Decrease resulting from refinancing transactions effected prior to this offering(b) |

|||||||

Decrease resulting from use of proceeds of this offering(c) |

|||||||

Pro forma interest expense, net |

$ | $ | |||||

- (a)

- Includes

the amortization of approximately $0.5 million and $2.2 million of deferred financing costs classified as interest expense for the

three months ended March 31, 2011 and the year ended December 31, 2010, respectively.

- (b)

- Reflects (i) the payment in full, and termination of, the Old Term Loan Agreement and the Old Revolving Credit Facility, (ii) the repurchase and redemption in full of the Old Notes, (iii) the incurrence of $285.0 million of indebtedness under the New Term Loan Agreement and (iv) the incurrence of $40.0 million of indebtedness under the New Revolving Credit Facility, in each case, as if it had occurred as of the beginning of the period presented. The

15

calculated reductions in interest expense are based upon the assumed reduction in our average cost of debt by percentage points throughout the periods presented, as well as the assumed reduction in our total indebtedness of $ million as a result of these transactions. The New Term Loan Agreement and the New Revolving Credit Facility have variable interest rates based on (i) the base rate (prime rate) plus a spread, or (ii) adjusted LIBOR plus a spread or (iii) a combination thereof. Each 0.125 percentage points change in the assumed interest rate used in the calculation of pro forma interest expense would change our interest expense on the indebtedness under the New Term Loan Agreement and the New Revolving Credit Facility by $0.4 million for the year ended December 31, 2010 and by $0.1 million for the quarter ended March 31, 2011.

- (c)

- Assumes repayment of $ million of the outstanding principal amount of our indebtedness under , which bears interest at a rate of % per annum, from the proceeds of this offering, as if it had occurred as of the beginning of the period presented.

- (3)

- Gives

effect to (i) the -for-one stock split which will occur prior to the effectiveness of the registration

statement of which this prospectus forms a part and (ii) the shares of our common stock to be issued by us in this offering. Pro forma basic net income per share consists of pro forma

net income divided by the pro forma basic weighted average common shares outstanding. Pro forma diluted net income per share consists of pro forma net income divided by the pro forma diluted weighted

average common shares outstanding.

- (4)

- We

present Adjusted EBITDA because we believe it assists investors and analysts in comparing our operating performance across reporting periods on a

consistent basis by excluding items that we do not believe are indicative of our core operating performance. In addition, we utilize Adjusted EBITDA in the calculation of financial covenants under our

New Revolving Credit Facility and our New Term Loan Agreement, as well as in the determination of compensation for members of our senior management team. "Adjusted EBITDA," which is defined as

"Consolidated EBITDA" under our credit agreements, represents net income (loss) before interest expense, income tax expense and depreciation and amortization, or EBITDA, as further adjusted to exclude

certain other items as set forth in the reconciliation presented below. "Adjusted EBITDA margin" is our Adjusted EBITDA as a representative percentage of net sales, and we believe our Adjusted EBITDA

margin is useful in measuring our profitability. You are encouraged to evaluate each adjustment and whether you consider each to be appropriate. In addition, in evaluating Adjusted EBITDA, you should

be aware that in the future, we may incur expenses similar to the adjustments in the presentation of Adjusted EBITDA. Our presentation of Adjusted EBITDA should not be construed as an inference that

our future results will be unaffected by unusual or non-recurring items.

- Adjusted

EBITDA and Adjusted EBITDA margin are not recognized financial measures under generally accepted accounting principles in the United

States, or GAAP, and may not be comparable to similarly titled measures used by other companies in our industry or across different industries. Adjusted EBITDA and, as a result, Adjusted EBITDA

margin, have limitations as analytical tools and you should not consider them in isolation, or as a substitute for analysis of our results as reported under GAAP. Some of these limitations

include:

- •

- Adjusted EBITDA does not reflect our cash expenditures, or future requirements, for capital expenditures or contractual

commitments;

- •

- Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs;

16

- •

- Adjusted EBITDA does not reflect the significant interest expense, or the cash requirements necessary to service interest

or principal payments, on our outstanding debt;

- •

- Adjusted EBITDA does not reflect depreciation and amortization, which are non-cash charges, although the

assets being depreciated and amortized will likely have to be replaced in the future, nor does Adjusted EBITDA reflect any cash requirements for such replacements;

- •

- non-cash compensation is and will remain a key element of our overall long-term incentive

compensation package, although we exclude it as an expense when evaluating our ongoing operating performance for a particular period; and

- •

- Adjusted EBITDA does not reflect the impact of certain cash charges resulting from matters we consider not to be

indicative of our ongoing operations.

- We

compensate for these limitations by relying primarily on our GAAP results and using Adjusted EBITDA only as supplemental information.

- The following is a reconciliation of our net income (loss) to Adjusted EBITDA and a calculation of Adjusted EBITDA margin:

| |

Three Months Ended March 31, |

Year Ended December 31, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Dollars in thousands) |

2011 | 2010 | 2010 | 2009 | 2008 | |||||||||||

| |

(unaudited) |

|

|

|

||||||||||||

Net income (loss)(a) |

$ | 4,532 | $ | 3,191 | $ | 9,353 | $ | (10,306 | ) | $ | (48,354 | ) | ||||

Interest expense, net(a) |

6,682 | 7,471 | 30,854 | 31,347 | 34,905 | |||||||||||

Income tax (benefit) expense |

(734 | ) | 3,998 | 3,569 | (111 | ) | (7,095 | ) | ||||||||

Depreciation and amortization |

5,403 | 5,509 | 21,339 | 21,604 | 21,491 | |||||||||||

EBITDA |

15,883 | 20,169 | 65,115 | 42,534 | 947 | |||||||||||

Impairment of goodwill and long-lived assets(b) |

— | 599 | 599 | 14,408 | 40,000 | |||||||||||

Disposal of fixed assets(c) |

12 | 11 | 336 | 525 | — | |||||||||||

Relocation and severance costs(d) |

169 | 62 | 63 | 886 | 973 | |||||||||||

Facility charges(e) |

— | 18 | 19 | 657 | 26 | |||||||||||

Management fee and expenses(f) |

383 | 391 | 1,561 | 1,740 | 1,855 | |||||||||||

Fees associated with debt extinguishment(g) |

7,886 | — | — | — | — | |||||||||||

Fees related to market study(h) |

306 | — | — | — | — | |||||||||||

Registration expenses related to Old Notes(i) |

(64 | ) | 13 | 38 | 26 | 309 | ||||||||||

Non-cash compensation charge(j) |

9 | 14 | 36 | 97 | 118 | |||||||||||

Acquisition-related items(k) |

— | — | (248 | ) | — | 2,111 | ||||||||||

Adjusted EBITDA |

$ | 24,584 | $ | 21,277 | $ | 67,519 | $ | 60,873 | $ | 46,339 | ||||||

Net sales |

$ | 114,622 | $ | 94,667 | $ | 327,535 | $ | 266,875 | $ | 305,240 | ||||||

Adjusted EBITDA margin |

21.4 | % | 22.5 | % | 20.6 | % | 22.8 | % | 15.2 | % | ||||||

- (a)

- Net income (loss) and interest expense each includes the amortization of deferred financing costs classified as interest expense in the amount of approximately $0.5 million for each of the three month periods ended March 31, 2011 and 2010 and approximately $2.2 million, $2.3 million and $2.1 million for each of the years ended December 31, 2010, 2009 and 2008, respectively.

17

- (b)

- For

the three months ended March 31, 2010 and the year ended December 31, 2010, this represents the write-down of manufacturing

equipment related to the consolidation of our two Canadian manufacturing facilities into one facility. For the year ended December 31, 2009, this represents the write-down of our

goodwill related to the completion of our impairment analysis for 2008 during the first quarter of 2009. For the year ended December 31, 2008, this represents the write-down of our

goodwill and trademarks.

- (c)

- Represents

the disposal of various fixed assets.

- (d)

- For

the three months ended March 31, 2011, this represents $0.2 million of severance costs. For the three months ended March 31, 2010,

this represents $13,000 of severance costs and $49,000 of relocation costs for members of our management team. For the year ended December 31, 2010, this represents $42,000 of severance costs

and $20,000 of relocation costs for members of our management team. For the year ended December 31, 2009, this represents $0.3 million of severance costs attributable to our former AZEK

president and $0.5 million of costs related to relocation for members of our management team. For the year ended December 31, 2008, $0.8 million represents relocation related to

the hiring of members of our management team.

- (e)

- For

the three months ended March 31, 2010 and the year ended December 31, 2010, this represents expenses related to the consolidation of our

two Canadian manufacturing facilities into one facility. For the year ended December 31, 2009, this represents termination costs of $0.2 million related to the consolidation of our

administrative offices into one of our manufacturing facilities in Pennsylvania and $0.4 million related to the consolidation of our two Canadian manufacturing facilities into one facility. For

the year ended December 31, 2008, this represents the $26,000 settlement expense related to the closing costs of the sale of the Winfield Avenue facility.

- (f)

- Represents

the AEA Investors management fee and expenses that were charged during the periods presented. Upon consummation of this offering, the AEA

Investors management fee is expected to be terminated and we will be required to pay management termination fees of $ . See "Certain Relationships and Related Party Transactions."

- (g)

- For

the three months ended March 31, 2011, this represents $7.4 million of debt refinancing fees associated with the loss on debt

extinguishment and $0.5 million of third party fees associated with the debt refinancing.

- (h)

- For

the three months ended March 31, 2011, this represents costs of $0.3 million related to a market study completed in preparation of this

offering.

- (i)

- Represents

financing charges related to the market making registration statement for the Old Notes.

- (j)

- Represents

non-cash compensation charges related to our Class B Unit Equity Program.

- (k)

- For the year ended December 31, 2010, this represents a settlement related to the share purchase agreement for the acquisition of Composatron, which we acquired on February 29, 2008. For the year ended December 31, 2008, this represents (i) $0.6 million of integration costs from the Composatron acquisition and (ii) $1.5 million of a non-cash fair value adjustment to increase inventory to its estimated selling price at February 29, 2008, in connection with the Composatron acquisition, which increase was then recognized as an increase to cost of sales during the period from March 1, 2008 to December 31, 2008 as the related inventory was sold.

- (5)

- Includes capital lease obligations.

18

Investing in our common stock involves a high degree of risk. You should carefully consider the risk factors set forth below as well as the other information contained in this prospectus, including "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes, before deciding to buy shares of our common stock. Any of the following risks could materially adversely affect our business, financial condition, results of operations or cash flows. In such case, the market price of our common stock could decline, and you may lose all or part of your investment in our common stock. Information contained in this section may be considered "forward-looking statements." See "Cautionary Note Regarding Forward-Looking Statements" for a discussion of certain qualifications regarding such statements.

Our business could be materially and adversely affected by volatility and disruption to the economy.

Our business is affected by a number of economic factors, including the level of economic activity in the markets in which we operate. The demand for our products by our customers depends, in part, on general economic conditions and business confidence levels. The capital and credit markets have in recent times been experiencing significant volatility and disruption. These conditions, combined with volatile oil and natural gas prices, declining business and consumer confidence and increased unemployment, precipitated an economic slowdown and severe recession in recent years. The difficult conditions in these markets and the overall economy affect our business in a number of ways. For example:

- •

- Sales in the residential, institutional and commercial construction markets correlate closely to the number of homes,

buildings and schools that are built or renovated, which in turn is influenced by factors such as interest rates, inflation, the strength or weakness of the U.S. dollar, gross domestic product levels,

consumer confidence and spending habits, demographic trends, unemployment rates, state and local government revenues and spending on schools and other macroeconomic factors over which we have no

control. Sales in our industrial OEM markets are also affected by macroeconomic factors, in particular gross domestic product levels and industrial production. Any decline in economic activity as a

result of these factors could result in a decreased demand for our products, which would materially adversely impact our sales and profitability.

- •

- In general, demand for new home construction as well as institutional and commercial construction may be materially

adversely affected by increases in interest rates or the reduced availability of financing. Although interest rates have been low during the past few years, as interest rates rise, the ability of

prospective buyers to finance purchases of new homes may be materially adversely affected. As a result, our business, financial condition and results of operations may also be materially adversely

impacted. The residential repair and remodeling market, in which we make a large portion of our sales, tends to be less sensitive to changes in interest rates. However, reduced availability of

financing or any changes in tax laws related to mortgages and home equity financings could materially adversely affect sales in the residential new construction and repair and remodeling markets. For

example, beginning in 2007, the mortgage finance market was negatively impacted by the fallout in the subprime mortgage market, reducing the amounts residential home lenders were willing to finance as

a result of tighter lending practices. This condition continues to exist in the market today.

- •

- Our bathroom partition and locker systems are sold primarily in the institutional segment, which includes universities, K-12 schools, government and municipal buildings and facilities, parks, military bases, hospitals and prisons, as well as commercial establishments, such as restaurants,

19

- •

- Dry petrochemical resin prices and the prices of other raw materials we use may continue to fluctuate as a result of

volatility in natural gas and crude oil prices and demand in the broader economy. Due to the uncertainty of oil and natural gas prices, we cannot reasonably estimate our ability to successfully

recover any price increases. See "—Our financial performance is dependent on raw material prices, as well as the continued availability of raw materials."

- •

- Market conditions could result in our key distributors experiencing financial difficulties and/or electing to limit

spending, which in turn could result in decreased sales and earnings for us. See "—Our sales, cash flows from operations and results of operations may decrease if our relations with our

key distributors decline."

- •

- Although we believe we have sufficient liquidity under the New Revolving Credit Facility, under extreme market conditions there can be no assurance that such funds will continue to be available or sufficient. In such a case, we may not be able to successfully obtain additional financing on favorable terms, or at all. If we are unable to obtain the required capital or if our costs become prohibitively high, our business would be materially adversely affected.

retailers and stadiums. The demand for these products, whether in connection with replacement orders or new construction, is impacted by the economy, and in particular gross domestic product levels. As a result of institutional budgeting, we may experience a decrease in sales up to a year or more after a decline in gross domestic product levels. Decline in demand in the institutional construction market can be attributed to increased operational costs such as pension and healthcare costs that may reduce amounts available for school construction costs. Furthermore, sales to schools and other public institutions may be impacted by budget cuts by state and local governments, including as a result of lower than anticipated tax revenues.

We cannot predict market conditions or the state of the overall economy, and difficult economic conditions may materially and adversely affect our financial results. In addition, there can be no assurance that any U.S. government actions taken for the purpose of stabilizing the financial markets will have a beneficial impact on the economy. For example, in 2009, the U.S. government provided eligible home buyers a tax credit that was extended until April 30, 2010. As a result of the home buyers' tax credit, the residential construction market improved during the first and second quarters of 2010, but experienced a decline in the third and fourth quarters of 2010, following expiration of the credits. There is no evidence that the residential construction market will improve during 2011.

Our financial performance is dependent on raw material prices, as well as the continued availability of raw materials.

The primary raw materials we use in the manufacture of our products are various petrochemical resins, primarily PVC and olefins, including HDPE and polypropylene, or PP. In addition, we utilize a variety of other additives including modifiers, titanium dioxide, or TiO2, and pigments. Our financial performance therefore is dependent to a substantial extent on the markets for these various materials.

The capacity, supply and demand for resins, additives and the petrochemical intermediates from which they are produced are subject to cyclical price fluctuations and other market disturbances, including supply shortages. Throughout the course of previous supply shortages we were able to maintain necessary raw material supplies. However, in the event of another industry-wide general shortage of resins and other additives we use, a shortage or discontinuation of certain types or grades of materials purchased from one or more of our suppliers or a supplier's declaration of force majeure, we may not be able to arrange for alternative sources of materials. Any such shortage may materially negatively impact our production process as well as our competitive position versus companies that are able to better or more cheaply source materials.

20

We purchase our raw materials directly from major petrochemical and chemical suppliers. We have long-standing relationships as well as guaranteed supply with some of these suppliers but we have no fixed-price contracts with any of our major vendors. Material purchases are made in accordance with our manufacturing specifications, and are based primarily on price and quality. Prices are negotiated on a continuous basis and we have not entered into hedges with respect to our raw material costs. We generally buy resin and other materials on an as-needed basis but have occasionally made strategic purchases of larger quantities.

Prices of our key materials may continue to fluctuate, including as a result of changes in natural gas, crude oil, ethylene, methyl methacrylate, or MMA, and TiO2 prices, among other factors. The instability in the world market for petroleum and TiO2 and in the North American ethylene, MMA and natural gas markets could materially adversely affect the prices and general availability of raw materials. Over the past several years, we have at times experienced rapidly increasing material prices primarily due to the increased cost of oil, natural gas, ethylene, MMA and TiO2. Due to the uncertainty of these prices, we cannot reasonably estimate our ability to successfully recover any price increases. Even if we are able to pass these price increases on to our customers, we may not be able to do so on a timely basis, our gross margins could decline and we may not be able to implement other price increases for our products. To the extent that increases in the cost of materials cannot be passed on to our customers, or the duration of time lags associated with a pass through becomes significant, such increases may have a material adverse effect on our profitability and cash flow. Also, increases in material prices could negatively impact our competitive position as compared to products made of other materials, such as wood and metal, that are not affected by changes in the price of our raw materials.