Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - POTLATCHDELTIC CORP | d8k.htm |

POTLATCH CORPORATION

AUGUST 2011

POTLATCH CORPORATION

Eric J. Cremers

Vice President, Finance and Chief Financial Officer

Deutsche Bank Conference –

Boston

Exhibit 99.1 |

POTLATCH CORPORATION

2

Forward-Looking Statements

This presentation contains certain forward-looking statements within the meaning of the Private

Litigation Reform Act of 1995 as amended, including without limitation statements about future

company performance, the company’s business model, strength of the company’s balance

sheet and credit metrics, dividend levels and yields, direction of markets and the economy, management of

timberlands to optimize values, projected inland private timber growth and harvest, future harvest

levels and their relation to market trends, impact of the pine beetle on North American lumber

supply, forecasts of North American exports of lumber to China, softwood stumpage price trends,

forecast of U.S. housing starts, the company’s capital structure, weighted average cost of debt, cash flow

generation, Canadian/U.S. dollar exchange rate, “organic” and “inorganic” funds

available for distribution, funds available for distribution, real estate business potential

and land development potential, real estate value opportunities, biomass opportunities,

forecasts of U.S. biomass consumed to produce electricity, management of the output of our Wood

Products facilities, asset coverage, debt repayment, and dividend policy. These

forward-looking statements are based on current expectations, estimates, assumptions and

projections that are subject to change, and actual results may differ materially from the forward-looking statements.

Factors that could cause actual results to differ materially include, but are not limited to, changes

in timberland values; changes in timber harvest levels on the company’s lands; changes in

timber prices; changes in policy regarding governmental timber sales; changes in the United

States and international economies; changes in the level of domestic construction activity; changes in

international tariffs, quotas and trade agreements involving wood products; changes in domestic and

international demand for wood products; changes in production and production capacity in the

forest products industry; competitive pricing pressures for the company’s products;

unanticipated manufacturing disruptions; changes in general and industry-specific environmental laws and

regulations; unforeseen environmental liabilities or expenditures; weather conditions; changes in fuel

and energy costs; changes in raw material and other costs; the ability to satisfy complex rules

in order to remain qualified as a REIT; changes in tax laws that could reduce the

benefits associated with REIT status; and other risks and uncertainties described from time to time in the

company’s public filings with the Securities and Exchange Commission. All

forward-looking statements are made as of the date of this presentation, and the company

does not undertake to update any forward-looking statements. |

POTLATCH CORPORATION

3

Converted to tax efficient REIT in 2006

Single level of taxation

Lower cost of capital

Fourth largest US Timber REIT

1.5 million acres of owned timberland

Growing real estate business

Five wood products manufacturing facilities

Enterprise value of $1.7 billion

(1)

Market cap of ~$1.4 billion

Net debt

(2)

of ~$300 million

Attractive

dividend

at

$2.04

per

share,

yielding

5.6%

(1)

Strong balance sheet with solid credit metrics

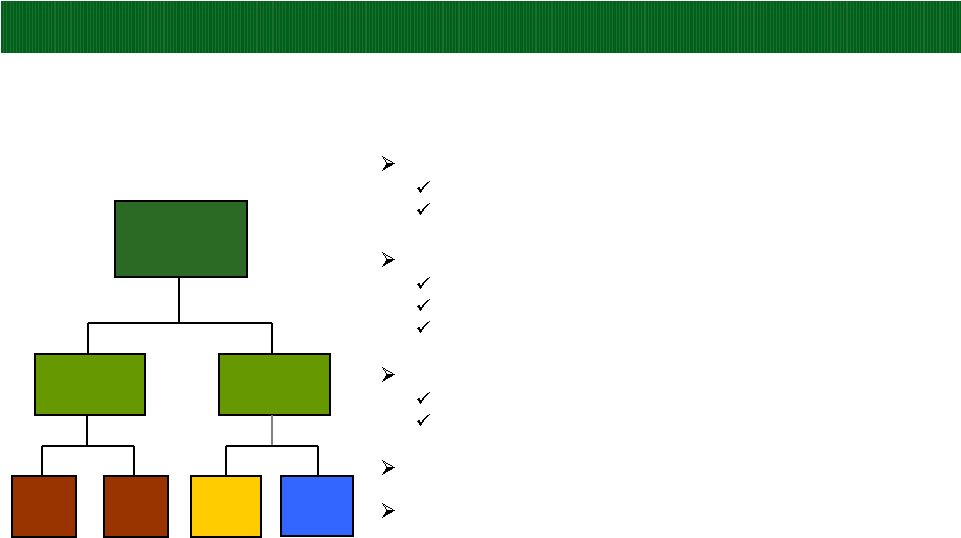

Company Overview

Potlatch

Corporation

(REIT)

Resource

(Timberlands)

Taxable REIT

Subsidiaries

North

South

Real

Estate

Wood

Products

(1)

Based on July 12, 2011, closing stock price of $36.32 a share.

(2)

We define net debt as the total of short-term and long-term debt less cash

and short-term investments, see reconciliation on page 31. |

POTLATCH CORPORATION

4

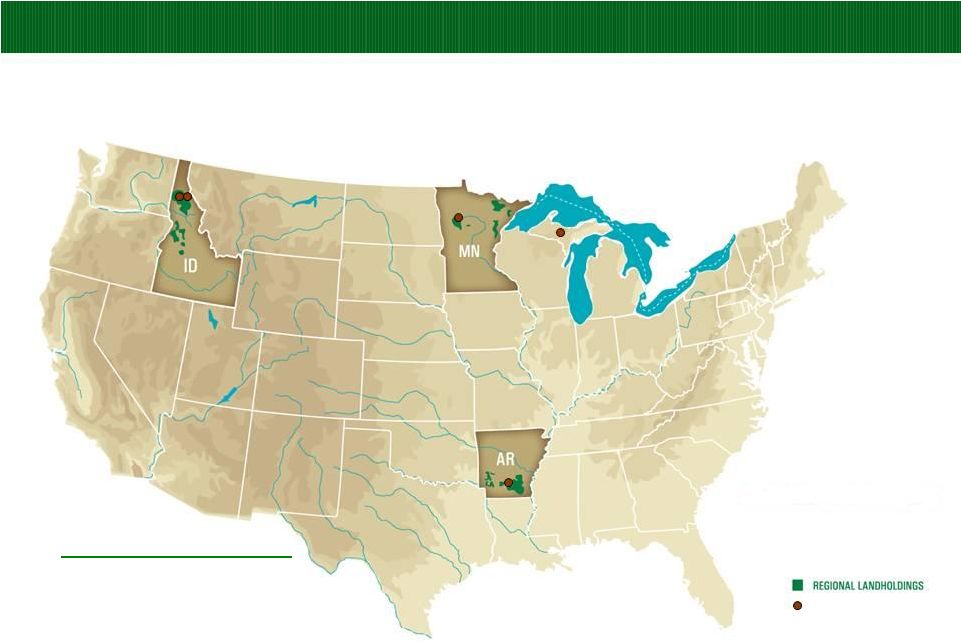

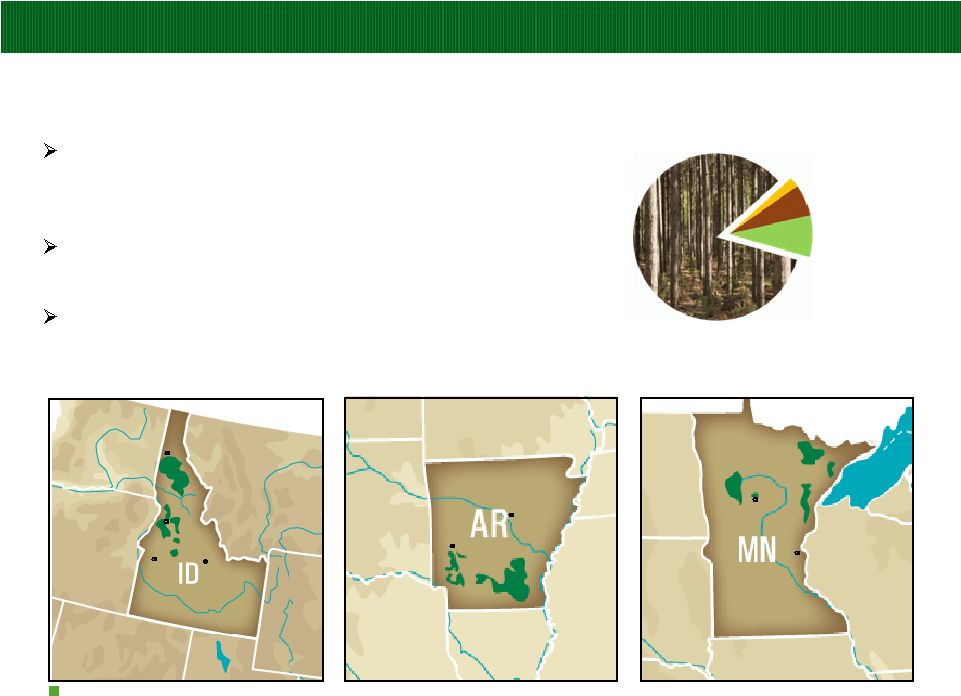

Wood Products

Manufacturing Facilities

Idaho:

818,000 acres

Arkansas:

408,000 acres

Minnesota:

228,000 acres

Total:

1,454,000 acres Timberlands

(1)

(1)

As of June 30, 2011.

Potlatch owns approximately 1.5 million acres of FSC-certified timberland in

Arkansas, Idaho and Minnesota and five wood products manufacturing

facilities Potlatch Business Overview

[818,000 acres]

[818,000 acres]

[228,000 acres]

[228,000 acres]

[408,000

acres] [408,000 acres]

408,000 acres] |

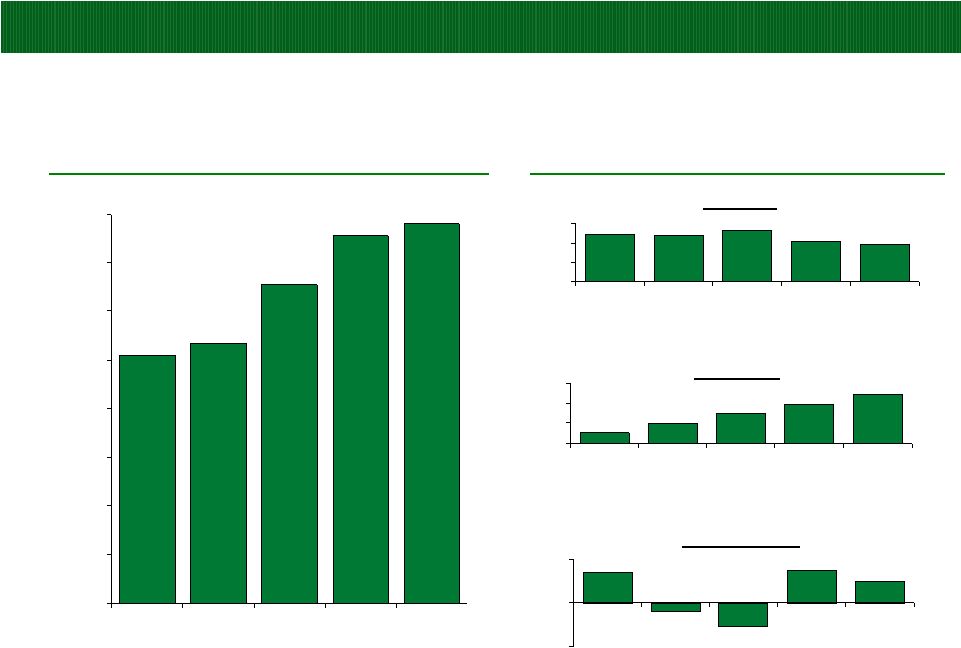

POTLATCH CORPORATION

5

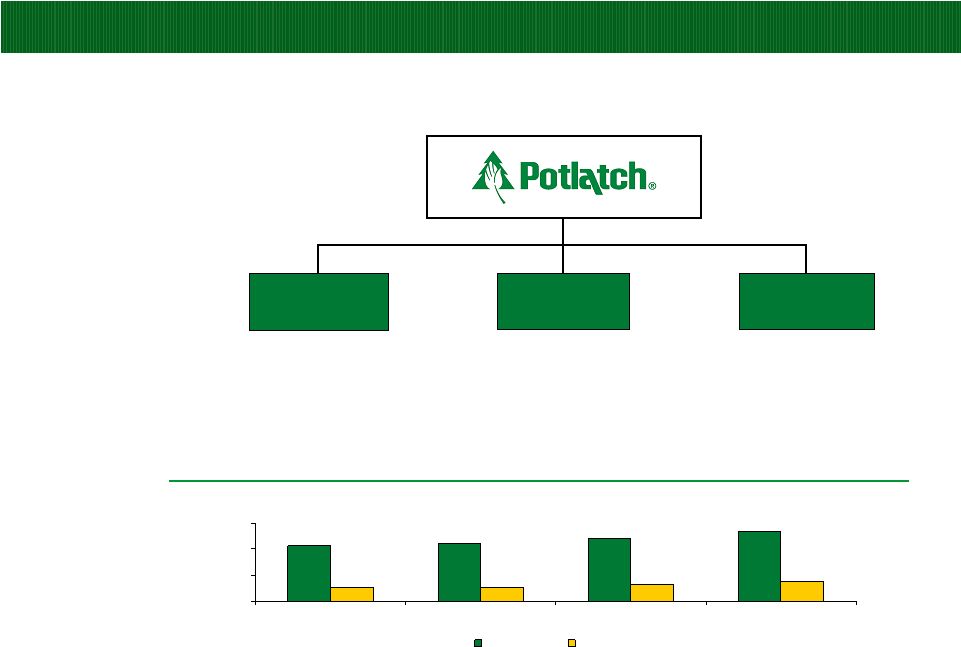

Potlatch Financial Overview

($ in millions)

2010 Segment Revenues

(1)

2010 Segment EBITDDA

(2)

Segment EBITDDA Margin

(3)

Resource

$226

$83

36.7%

Real Estate

$85

$79

92.9%

Wood

Products

$274

$15

5.5%

Historical Consolidated Revenue and EBITDDA

$423

$440

$476

$539

$102

$107

$131

$151

$0

$200

$400

$600

2007

2008

2009

2010

Revenue

EBITDDA

(2)

(1)

Segment revenues and EBITDDA presented prior to intersegment eliminations.

(2) See page 36 of this presentation for definitions of EBITDDA and segment EBITDDA, and

page 30 for reconciliations to most comparable GAAP measures.

(3) Segment EBITDDA Margin is defined as Segment EBITDDA divided by Segment

Revenues.

|

POTLATCH CORPORATION

0.0

1.0

2.0

3.0

4.0

5.0

2004

2005

2006

2007

2008

2009

2010

2011F

~ 2 to 3

Years

Forward

Sawlogs

Pulpwood

$72

$80

$70

$53

$60

$59

$27

$34

$36

$33

$34

$32

$0

$25

$50

$75

$100

2006

2007

2008

2009

2010

Q2 2011

YTD

Sawlogs ($/ton)

Pulpwood ($/ton)

6

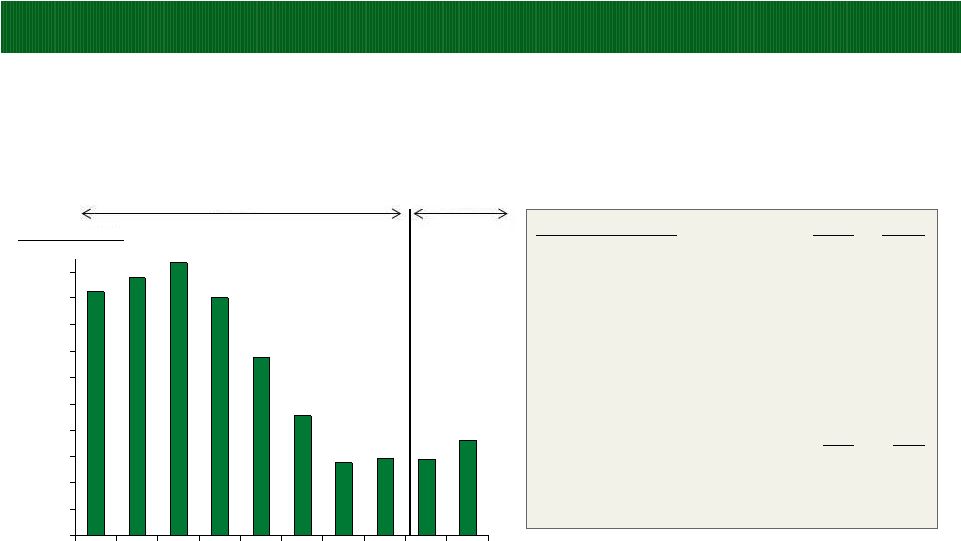

Attractive Timber Inventory & Harvest Profile

Allows active management of harvest

volumes to correspond with the

strength or weakness in timber prices

Attractive distribution of timber across

age-classes

Flexibility to monetize sawlog or pulpwood

harvests

Overall, harvest volume increasing

over time

4.2 million tons estimated in 2011

4.6

-

4.8

million

tons

expected

in

2

-

3

years

Highly leveraged to sawlog pricing

$7/ton price increase in 2010 produced

incremental EBITDDA of $21 million

Fee Harvest Log Volume

Timber Prices

3.0

3.3

3.3

3.9

4.4

3.8

~4.6

$/Ton

Tons in millions

4.2

4.2 |

POTLATCH CORPORATION

7

Total Housing Starts

Housing starts are presently far below the long-term average

(in thousands)

Source: U.S. Census Bureau

0

500

1,000

1,500

2,000

2,500

71

73

75

77

79

81

83

85

87

89

91

93

95

97

99

01

03

05

07

09

Year

Average Starts Since 1971:

1.5 million |

POTLATCH CORPORATION

Million U.S. Starts

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

U.S. Housing Starts Forecast

Single Family & Multifamily Only

Source: APA: Housing Starts: June 2011

(1)

RBC: Royal Bank of Canada

(2)

FEA: Forest Economic Advisors

(3)

NAR: National Association of Realtors

Actual

Forecast

8

Forecasts (000)

2011

2012

RBC

(1)

-July 15

600

799

Wells Fargo-June 29

590

760

NAHB-June 29

589

775

FEA

(2)

-June 30

587

726

NAR

(3)

-July

6

584

768

RISI-June 30

580

630

Mesirow Financial-July 11

570

710

APA-June 15

545

630

Average

581

725

*FEA:

Forest Economic Advisors. *NAR: National Assoc. of Realtors.

*RBC: Royal Bank of Canada |

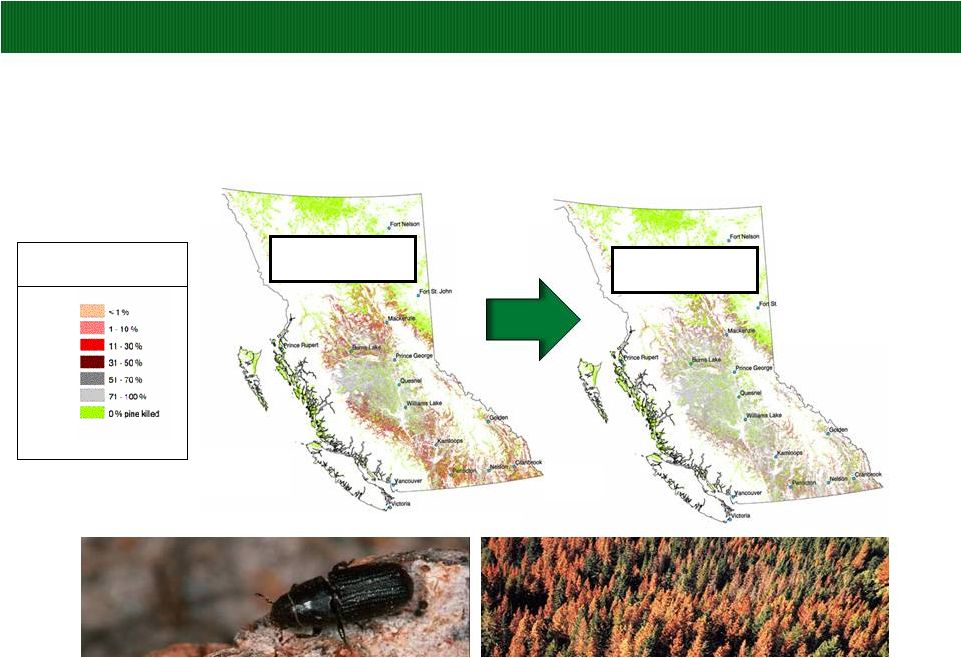

POTLATCH CORPORATION

Impact of the Pine Beetle on North American Lumber Supply

Source:

British Columbia Ministry of Forest and Range

9

Combined with Eastern Canadian harvest reductions of 20%, the pine beetle in British

Columbia is projected to lower North American lumber supply up to 15% over

the next few years, depending on lumber price levels.

Cumulative Percentage of

Pine Killed

British Columbia

2013

British Columbia

2009 |

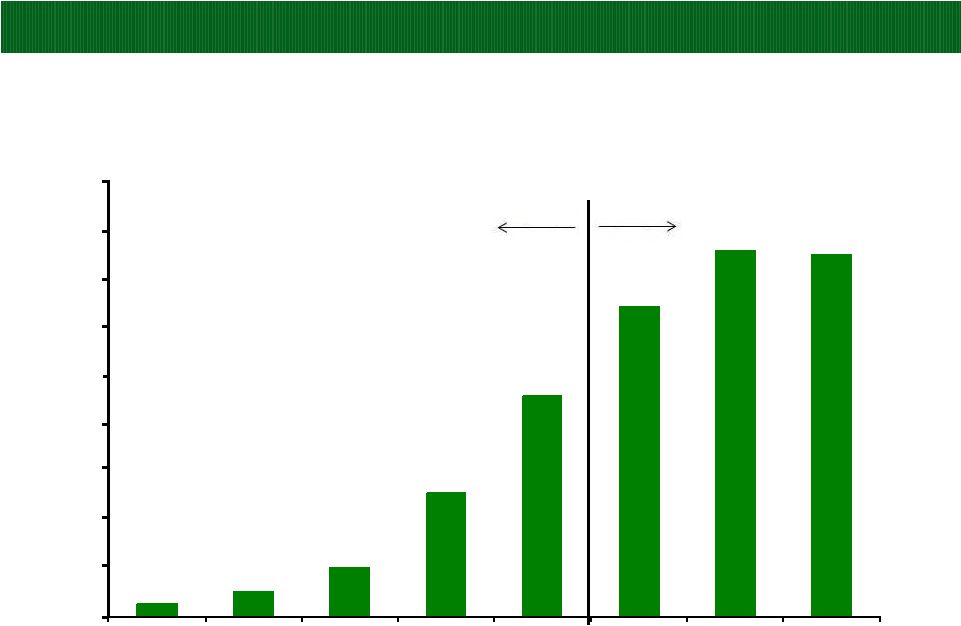

POTLATCH CORPORATION

10

North American Exports of Lumber to China as a % of North American Production

Actual

0.2%

0.5%

1.0%

2.6%

4.6%

6.4%

7.6%

7.5%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2006

2007

2008

2009

2010

2011

2012

2013

Forecast

Source: RISI North American Lumber Forecast, May 2011 & Potlatch Internal Forecast.

|

POTLATCH CORPORATION

0

50

100

150

200

250

300

1990

1994

1998

2002

2006

2010

2014

2018

2022

2026

2030

2034

U.S. Biomass Consumed to Produce Electricity

(1)

(Millions Green Tons)

11

Actual

Forecast

(1) EIA Annual Energy Outlook 2011 & Potlatch Estimates.

|

POTLATCH CORPORATION

Random Lengths Pricing for KD SYP (West) #2 2x6

($/MBF)

12

$150

$200

$250

$300

$350

$400

$450

2007

2008

2009

2010

2006

2005

2011

(1)

(1) Pricing through July 2011. |

POTLATCH CORPORATION

Wood Products Segment

$41

$13

$14

($4)

($11)

$15

$10

-$20

$0

$20

$40

$60

2005

2006

2007

2008

2009

2010

LTM

Q2 2011

13

Five manufacturing facilities, lumber and plywood

Sell to wholesalers for use in homebuilding and construction

Potlatch operates four sawmills in Idaho, Arkansas, Minnesota and Michigan as

well as one industrial-grade plywood mill in Idaho

Actively manage output of facilities to match supply and demand

$ in millions

(1)

(2)

Note: See page 36 of this presentation for the definition of segment EBITDDA, and page 30

for reconciliation to most comparable GAAP measure. (1)

Wood Products EBITDDA excludes $31 million for Canadian lumber settlement.

(2)

Wood Products EBITDDA includes asset impairment charge of $3 million.

Wood Products Segment EBITDDA |

POTLATCH CORPORATION

14

Rural Real Estate

~95,000 acres

Frequently assess acreage to maximize

value through sale of non-core timberland

real estate

More than 3,000 miles of desirable water

frontage

More than 9 million people live within three

states of ownership

Potlatch Timberlands

(1)

Core Timberland

~1.2 million acres

Non-Strategic Timberland

~15,000 acres

HBU/Development

~125,000 acres

Land Portfolio

Idaho:

818,000 acres

Arkansas:

408,000 acres

Minnesota:

228,000 acres

(1)

As of June 30, 2011.

Real Estate Overview

Coeur d’Alene

Boise

Sun Valley

McCall

Little Rock

Hot Springs

Brainerd

Minneapolis

St. Paul |

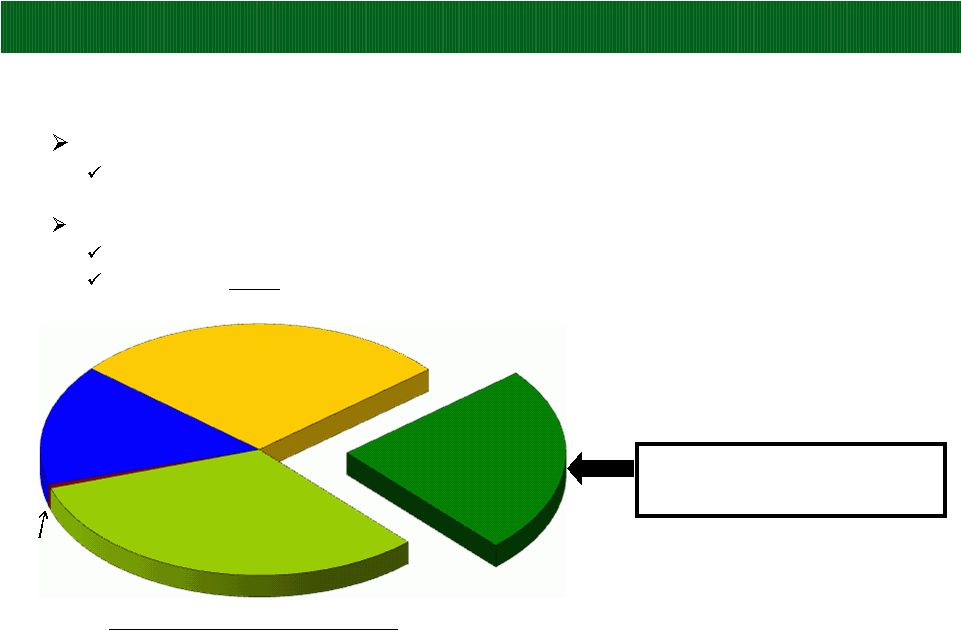

POTLATCH CORPORATION

15

Value Opportunities Are Unique to Each Category

CONSERVATION

EASEMENT

NON-STRATEGIC

TIMBERLAND

RURAL REAL

ESTATE

HIGHER-BETTER-USE

DEVELOPMENT

$400 to $1,000 per acre

$500 to $1,500 per acre

$1,000 to $1,500 per acre

$2,000 to $7,000 per acre

120,000

Opportunity dependent

10,000 to 20,000 acres

90,000 to 100,000 acres

120,000 to 130,000 acres

Characteristics:

-

Habitat related

-

Appropriate payment for

opportunity sold

-

Selective core lands

Characteristics:

-

Fringe of ownership

-

Location disadvantage

-

Higher operation cost

-

Capital allocation focus

Characteristics:

-

Fringe of ownership

-

Opportunity varies by

geographic market

-

Location disadvantage

-

Higher operation cost

-

Capital allocation focus

Characteristics:

-

Market position

properties

-

Investor interest

-

Explore proper land use

and entitlements

-

Emerging development

focus

LOWER VALUE

OPPORTUNITIES

HIGHER VALUE

OPPORTUNITIES |

POTLATCH CORPORATION

16

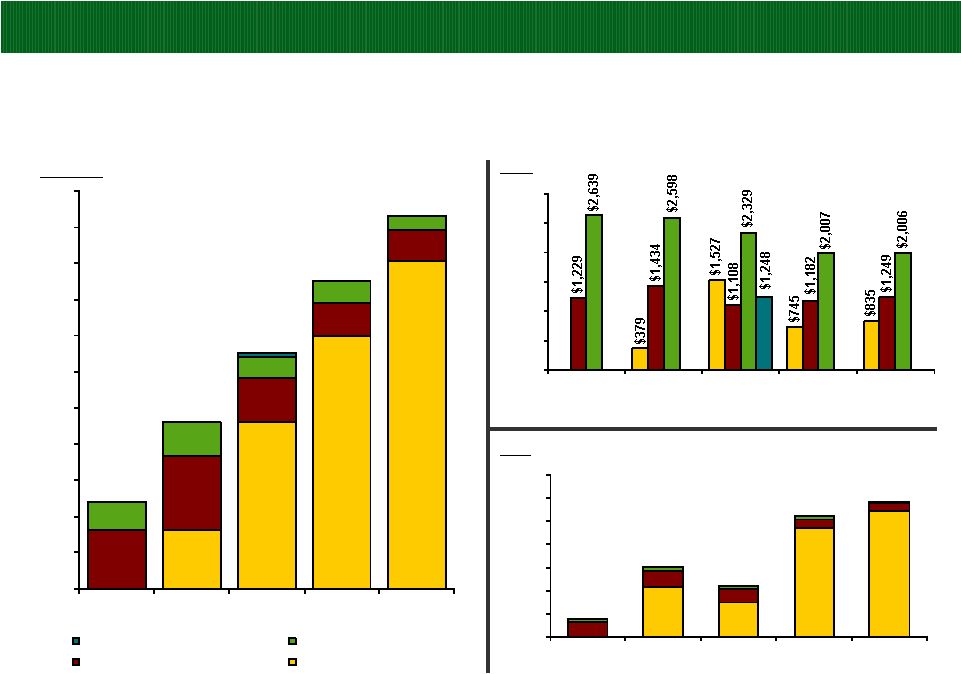

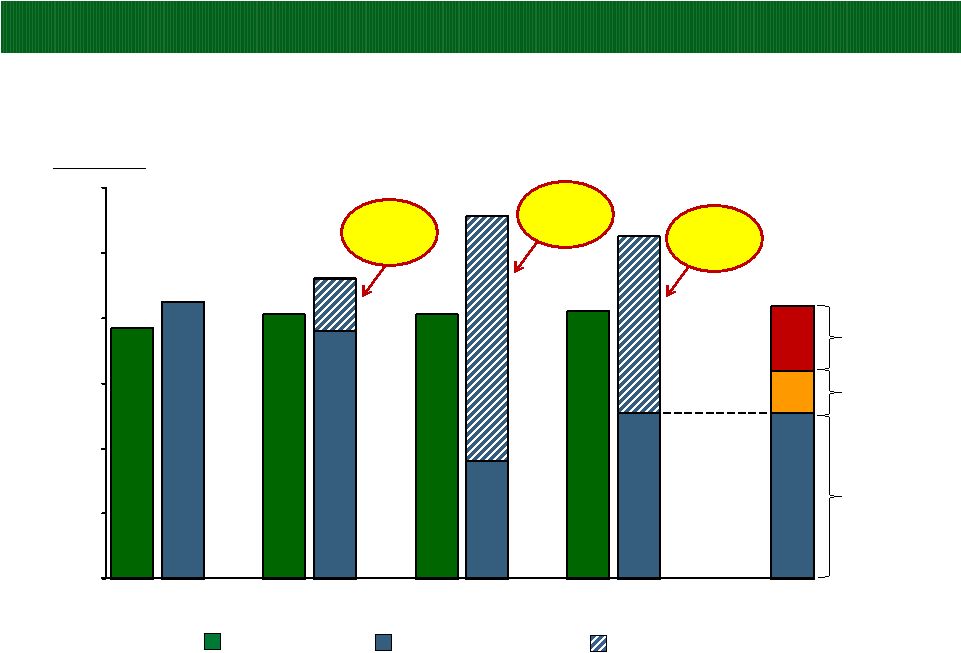

Significant Real Estate Portfolio

Realization of Non-Core Timberland Asset Value

$24.1

$46.1

$65.4

16,175

60,669

44,786

(1)

Segment Revenue in 2008 excludes sale of building.

(2)

Excludes the sale of the Boardman, Oregon tree farm of 17,000 acres.

$ in millions

$85.2

104,737

(2)

$103.3

117,482

16.3

46.1

70.1

90.8

16.2

20.5

12.5

9.2

8.4

7.9

9.3

5.6

5.9

4.1

1.2

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

2007

2008

2009

2010

LTM

Q2 2011

Segment Revenue

Conservation Easement

HBU/Development

Rural Real Estate

Non-Strategic Timberland

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2007

2008

2009

2010

LTM

Q2 2011

$/Acre

Price Per Acre

42,841

30,168

93,974

108,721

13,166

14,266

11,234

7,796

6,698

3,009

3,562

2,430

2,967

2,063

954

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2007

2008

2009

2010

LTM

Q2 2011

Acres

Acres Sold

(1) |

POTLATCH CORPORATION

Potlatch Timberland Holdings

17

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

2005

2006

2007

2008

2009

1,471

(3)

1,468

218

1,653

36

(61)

1,628

(45)

1,583

(105)

1,478

Acres (000’s)

PCH Owned Acreage at End of Period

PCH Acquired Acreage During the Year

PCH Sold Acreage During the Year

2010

(33)

(1)

(1)

Includes the sale of the Boardman, Oregon tree farm of 17,000 acres.

(2)

Acreage through June 30, 2011.

(24)

2011

1,454

(2) |

POTLATCH CORPORATION

18

Balance Sheet Review

ASSETS

Cash and short-term investments

75

$

Other current assets

64

Long-term assets

602

Total assets

741

$

LIABILITIES & EQUITY

Current liabilities

81

$

Long-term debt

343

Other liabilities

134

Total liabilities

558

Equity

183

Total liabilities & equity

741

$

June 30, 2011

($ in millions)

Strong credit metrics

$150

million

revolver

expiring

December

2013

(1)

$68 million of fixed rate debt swapped to

floating as of June 30, 2010

$63 million of floating rate debt outstanding

Maturities

in

2012

-

2018

6.8% weighted average cost of debt (including

interest rate swaps)

8.9 weighted average years to maturity

7.1% weighted average cost of debt (all at fixed rate)

(1) Per an amendment to our credit agreement, the revolver decreased to

$150 million from $250 million, effective February 4, 2011. |

POTLATCH CORPORATION

19

Conservative Leverage and Interest Coverage Ratios

(1)

as of June 30, 2011

Financial

Actual

Covenant

6/30/2011

Requirements

55.4%

70.0%

16.9%

N/A

5.58x

2.75x

(2)

3.27x

(3)

3.00x

Debt

to

Total

Capitalization

(1)

Net Debt to Enterprise Value

LTM EBITDDA to Interest Expense

Collateral Coverage

(1)

Calculated per our bank credit agreement, using an accumulated other comprehensive loss

“AOCL” exclusion. Per an amendment to the credit agreement, the Minimum

Collateral Coverage ratio increased to 3.00 and the Maximum Funded Indebtedness to Capitalization

ratio increased to 70.0% effective as of February 4, 2011.

(2)

This requirement will increase to 3.00 on October 1, 2011. (3)

Updated for new appraisal dated June 15, 2011.

Note: We define net debt as the total of short-term and long-term debt less cash and

short-term investments, see page 31 for reconciliation. See page 36 of this presentation

for the definition of EBITDDA and page 30 for reconciliation to most comparable GAAP measure.

|

POTLATCH CORPORATION

20

Strong Asset Coverage

Arkansas Timberland

408,000 Acres

Secured Idaho Timberland

352,000 Acres

Unsecured Idaho Timberland

466,000 Acres

Wisconsin

Timberland

1,000 Acres

Minnesota Timberland

228,000 Acres

Total

=

Approx.

1.5

Million

Acres

Represents 24% of our acres, but the

appraisal represents approximately

41% of our enterprise value

(1)

Updated for new appraisal dated June 15, 2011. The appraisal uses comparable

transactions and discounted cash flow analyses for purposes of the valuation. There is no assurance

that sales could be effected at the appraised values or as to the timing of sales.

The calculation of discounted cash flows involves projection of future market conditions, harvest levels

and

other

factors,

all

of

which

could

vary

materially

from

those

projected.

There

is

no

implication

that

the

company’s

other

timberlands

would

have

a

similar

value

per

acre.

(2)

Enterprise value is defined as market capitalization value plus net debt as of June

30, 2011. $150 million revolver requires collateral

Another $66 million of debt is secured pari-passu along with the

revolver The

$216

million

of

debt

is

secured

with

352,000

acres

of

‘core’

Idaho

Timberland

Appraisal

on

this

352,000

acres

=

$707

million

(1)

Compares

to

entire

Potlatch

enterprise

value

of

$1.7

billion

(2) |

POTLATCH CORPORATION

Conservative Capital Structure –

Long Term Debt Maturity Profile

($ in millions)

21

Mandatory principal repayments of only $79 million through 2016

(1) $5 million maturity paid in January, 2011 with cash on hand.

(1)

$0

$22

$8

$21

$23

$5

$5

$14

$150

$0

$0

$3

$0

$66

$7

$43

$0

$50

$100

$150

$200

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026 |

POTLATCH CORPORATION

Strong Cash Flow Generation

($ in millions)

$102

$107

$131

$151

$156

$0

$20

$40

$60

$80

$100

$120

$140

$160

2007

2008

2009

2010

LTM

Q2 2011

22

Total

EBITDDA

$97

$95

$105

$83

$78

$0

$40

$80

$120

2007

2008

2009

2010

LTM

Q2 2011

Resource

$21

$41

$60

$79

$97

$0

$40

$80

$120

2007

2008

2009

2010

LTM

Q2 2011

Real Estate

$14

($4)

($11)

$15

$10

-$20

$0

$20

2007

2008

2009

2010

LTM

Q2 2011

Wood Products

Segment

EBITDDA

(1)

See page 36 of this presentation for the definition of EBITDDA and Segment EBITDDA,

and page 30 for a reconciliation to most comparable GAAP measures. (2)

Consolidated and Wood Products EBITDDA includes a $3 million asset impairment

charge taken in 2009. (2)

(2)

(1)

(1) |

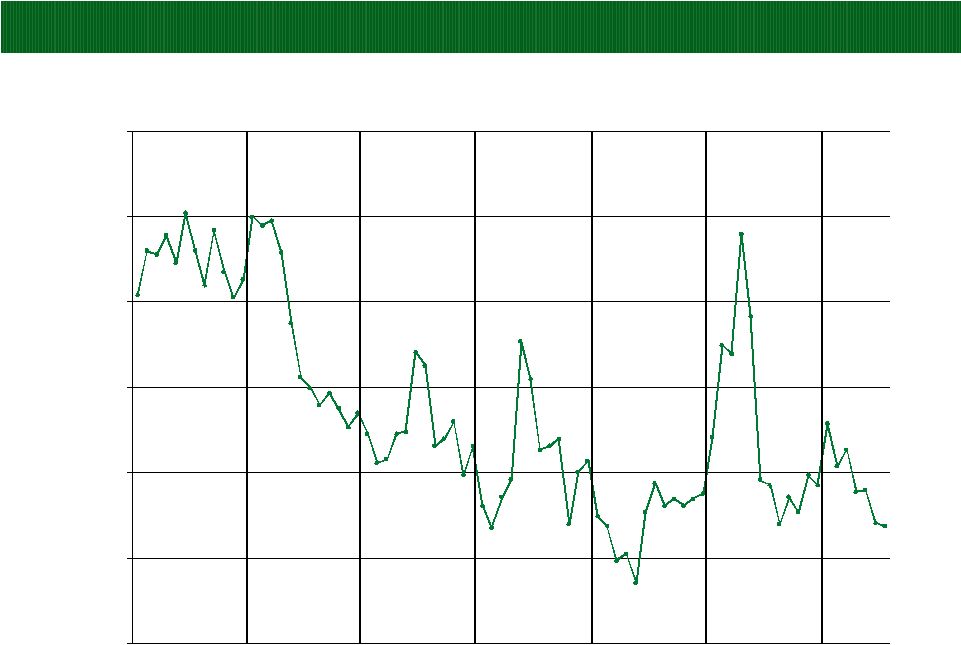

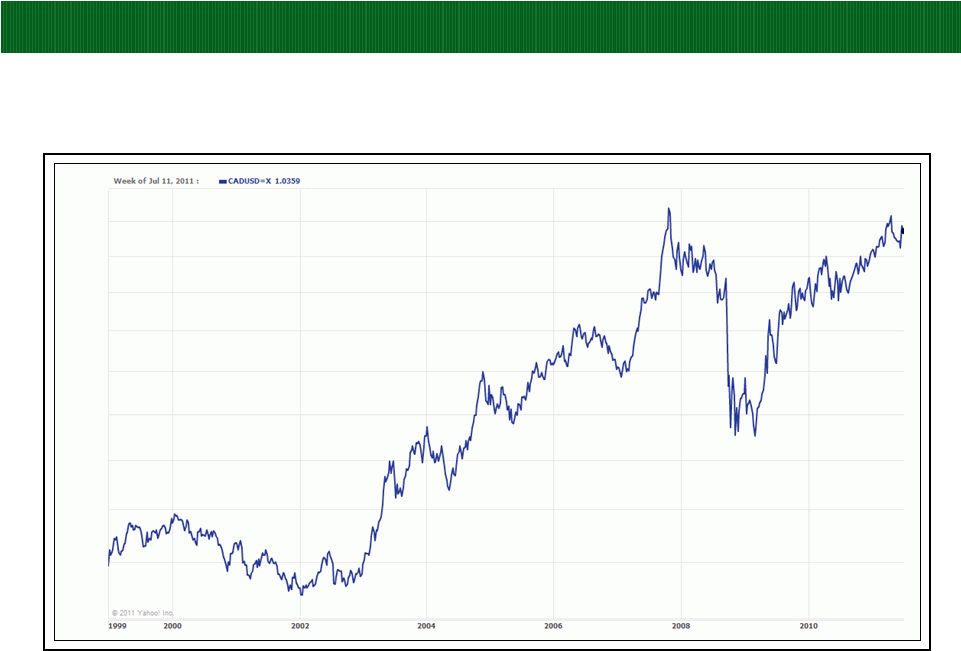

POTLATCH CORPORATION

Exchange Rate

Canadian Dollar to U.S. Dollar

23

$1.05

$1.00

$0.95

$0.90

$0.85

$0.80

$0.75

$0.70

$0.65 |

POTLATCH CORPORATION

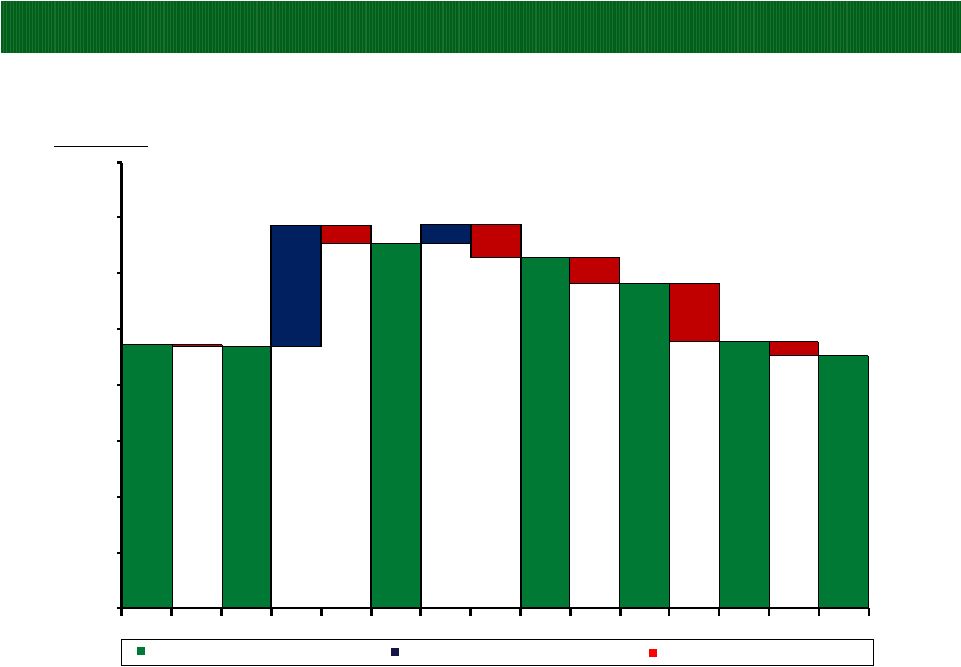

Funds Available for Distribution (FAD)

($ in millions)

$85

$92

$111

$105

$112

$77

$81

$81

$82

$82

$0

$20

$40

$60

$80

$100

$120

2007

2008

2009

2010

LTM

Q2 2011

FAD

Dividend Distribution

24

Note:

See page 36 of this presentation for the definition of FAD, and see page 32 for a

reconciliation to most comparable GAAP measure. Excludes dividend distribution of

Clearwater Paper stock in 2008. |

POTLATCH CORPORATION

Organically Earning Our Dividend is Within Reach

25

$0

$20

$40

$60

$80

$100

$120

Dividend

"Organic" FAD

"Inorganic "FAD

2007

2008

2009

2010

~2-3 Years

Forward

Baseline:

2010 “Organic”

FAD

Impact of a 10%

increase in sawlog

prices from 2010

Impact of an increase

in the harvest level to

4.6 million tons

AR and WI

Non-Strategic

Timberland Sale

Timber Deed &

AR Non-Strategic

Timberland Sale

MN Non-Strategic

Timberland Sale

($ in millions)

Note:

See page 36 of this presentation for the definition of inorganic and organic FAD, and see page 32 for

a calculation organic/inorganic FAD. |

POTLATCH CORPORATION

26

Attractive Dividend

Potlatch's dividend policy has been

driven primarily by the performance

of its timber and real estate

businesses

We continue to pay our quarterly

dividend at $0.51/share since we

increased it from $0.49/share in Q3

2007

Our peers

(2)

have significantly

lower dividend yield (avg. = 3.7%)

At current dividend levels, a 3.7% yield

for Potlatch equates to $55 stock price

Source: Factset. Market data as of July 12, 2011.

(1)

Dividend yield calculated as annualized last quarter dividend divided by the

closing stock price. (2) Plum Creek and Rayonier.

Potlatch

Dividend

Yield

(1)

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Jan-2008

Sep-2008

May-2009

Jan-2010

Sep-2010

May-2011

Avg. 6.4%

5.6% |

POTLATCH CORPORATION

27

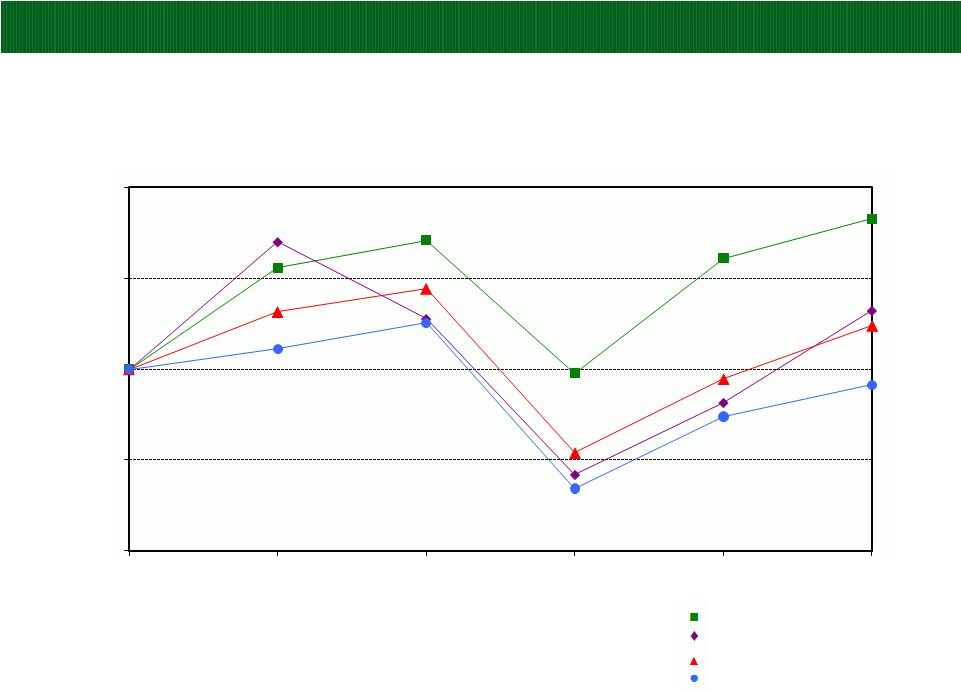

Stock Price Performance

Comparison

of

Five-Year

Total

Returns

(1)

Potlatch Corporation

NAREIT Equity Index

S&P 500 Composite

2010 Peer Group

(2)

(1) Assumes $100 was invested on December 31, 2005. Total return assumes

quarterly reinvestment of dividends. (2) Our

Peer

Group

companies

are

Deltic

Timber

Corp.;

Plum

Creek

Timber

Co.,

Inc.;

Rayonier

Inc.;

St.

Joe

Co.;

Universal

Forest

Products

Inc.;

and

Weyerhaeuser

Co.

$50

$75

$100

$125

$150

12/31/05

12/31/06

12/31/07

12/31/08

12/31/09

12/31/10 |

POTLATCH CORPORATION

28

Conclusion

Potlatch maintains a very attractive asset base of 1.5 million acres of

timberland We have the ability to meaningfully expand high margin sawlog

harvest levels Wood Products business stabilized and generating solid cash

flow Real Estate segment low risk, high margin

Attractive dividend with improving coverage

Strong balance sheet with attractive debt cost and maturity profile

Industry trends beginning to turn positive

Housing starts beginning to grow, albeit slowly

Exports to China from North America continue to expand

Pine beetle to impact supply from Canada

Biomass continues to hold promise |

Appendix

POTLATCH CORPORATION

AUGUST 2011 |

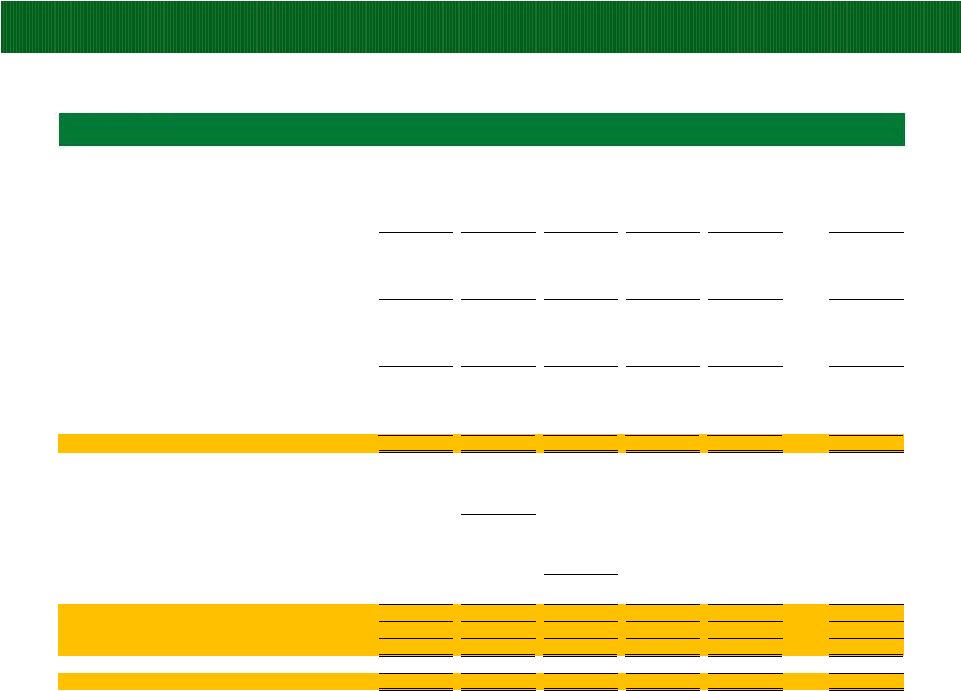

POTLATCH

CORPORATION 30

EBITDDA and Segment EBITDDA Reconciliation

($ in millions)

(1)

Wood Products EBITDDA excludes $31 million for Canadian lumber settlement.

(2)

Consolidated and Wood Products EBITDDA includes a $3 million asset impairment charge taken in

2009. 2005

2006

(1)

2007

2008

2009

(2)

2010

LTM

Q2 2011

Consolidated

Earnings from continuing operations

74

$

73

$

81

$

40

$

43

$

Less:

Income tax benefit (provision)

17

25

16

(5)

(2)

Add:

Net cash interest expense

15

20

20

26

25

Depreciation, depletion, and amortization

26

30

35

31

31

Basis of real estate sold

4

9

11

49

55

Consolidated EBITDDA

102

$

107

$

131

$

151

$

156

$

Resource

Operating income

82

$

76

$

82

$

62

$

59

$

Depreciation, depletion, and amortization

15

19

23

21

19

Resource Segment EBITDDA

97

$

95

$

105

$

83

$

78

$

Real Estate

Operating income

17

$

32

$

49

$

30

$

43

$

Basis of real estate sold

4

9

11

49

54

Real Estate Segment EBITDDA

21

$

41

$

60

$

79

$

97

$

Wood Products

Operating income (loss)

29

$

2

$

4

$

(14)

$

(21)

$

7

$

2

$

Depreciation

12

11

10

10

10

8

8

Wood Products Segment EBITDDA

41

$

13

$

14

$

(4)

$

(11)

$

15

$

10

$

Fiscal Year |

POTLATCH CORPORATION

31

Potlatch Net Debt Reconciliation

($ in millions)

June 30

2007

2008

2009

2010

2011

Long-term debt

321

$

221

$

368

$

363

$

343

$

Current installments on long-term debt

-

101

-

5

21

Current notes payable

110

129

-

-

-

Cash

(9)

(1)

(2)

(6)

(7)

Short-term investments

(22)

(3)

(53)

(85)

(68)

Net Debt

400

$

447

$

313

$

277

$

289

$

At December 31 |

POTLATCH CORPORATION

32

Organic/Inorganic FAD Calculation

($ in millions)

(1) Excludes distribution of Clearwater Paper stock in 2008.

2007

2008

2009

2010

LTM

Q2 2011

Operating income (loss):

Resource

Baseline Income

82

$

76

$

82

$

62

$

59

$

62

$

Increase to 4.6 million tons

-

-

-

-

-

11

10% increase in sawlog prices from 2010

-

-

-

-

-

21

Resource

82

76

82

62

59

-

94

Real Estate

17

32

49

30

43

17

Wood Products

4

(14)

(21)

7

2

19

Eliminations and adjustments

1

(1)

8

2

2

-

104

93

118

101

106

130

Corporate administration

(32)

(25)

(33)

(30)

(34)

(32)

Net cash interest expense

(15)

(20)

(20)

(26)

(25)

(25)

Income tax benefit (provision)

17

25

16

(5)

(4)

(5)

Earnings from continuing operations

74

73

81

40

43

68

Depreciation, depletion and amortization

26

30

35

31

31

29

Basis of real estate sold

4

9

11

49

55

3

Capital expenditures

(19)

(20)

(16)

(15)

(17)

(18)

Funds Available for Distribution

85

$

92

$

111

$

105

$

112

$

82

$

Inorganic FAD:

Minnesota non-strategic sale (after tax income)

14

$

Basis of real estate sold

2

Arkansas non-strategic sale (after tax income)

24

$

Basis of real estate sold

2

Timber deed (after tax income)

42

Depletion

7

Arkansas/Wisconsin non-strategic sale (after tax income)

11

$

11

$

Basis of real estate sold

43

43

Total inorganic FAD

-

$

16

$

75

$

54

$

54

$

-

$

Organic FAD

85

$

76

$

36

$

51

$

58

$

82

$

Total FAD

85

$

92

$

111

$

105

$

112

$

82

$

Distributions

to

Common

Stockholders

(1)

77

$

81

$

81

$

82

$

82

$

82

$

~2-3 Years

Forward |

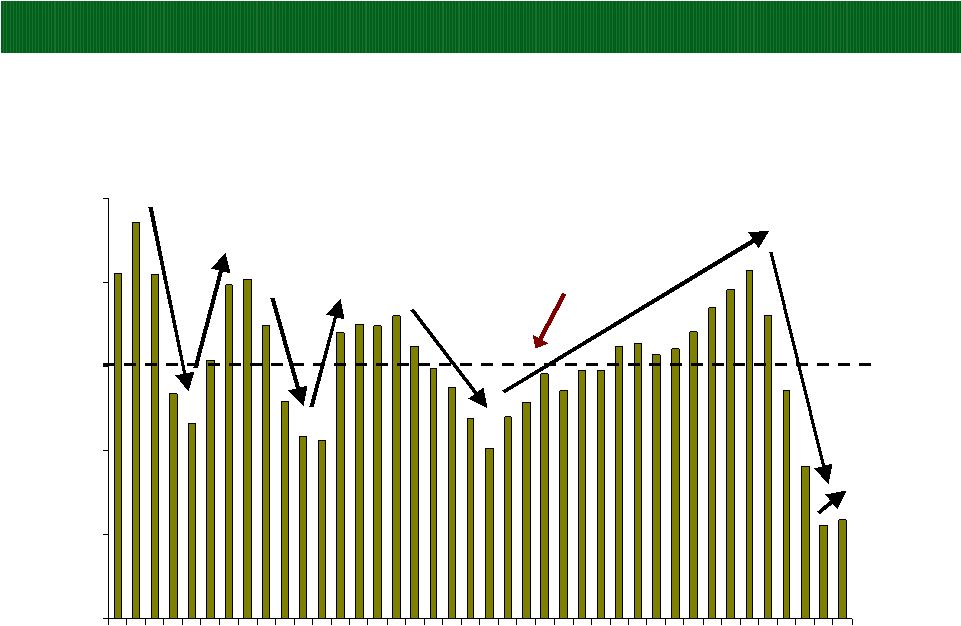

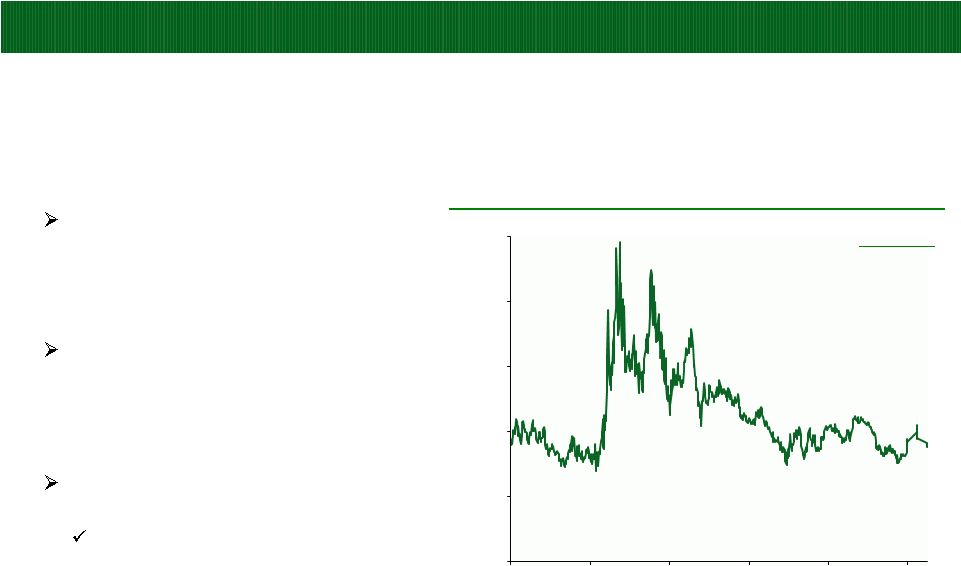

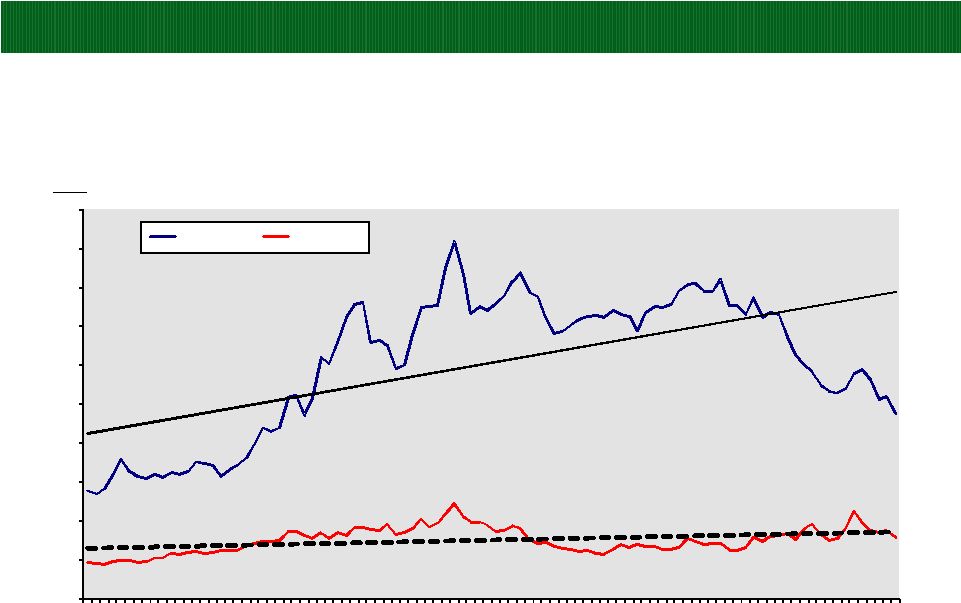

POTLATCH CORPORATION

33

Softwood Stumpage Price Trends

Southwide Average Nominal Prices

Source: Timber Mart-South, updated through June 30, 2011.

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

$/Ton

Years

Pine Sawtimber

Pine Pulpwood

2010 |

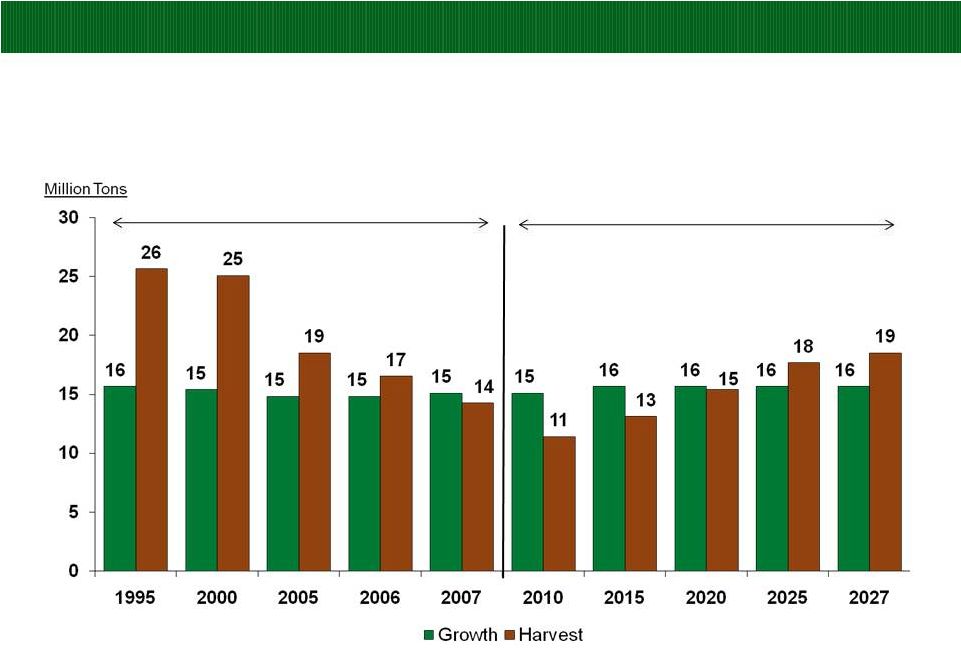

POTLATCH CORPORATION

Projected Inland Private Timber Growth and Harvest (1995-2027)

34

Source: F2M and Potlatch Corporation

Actual

Forecast |

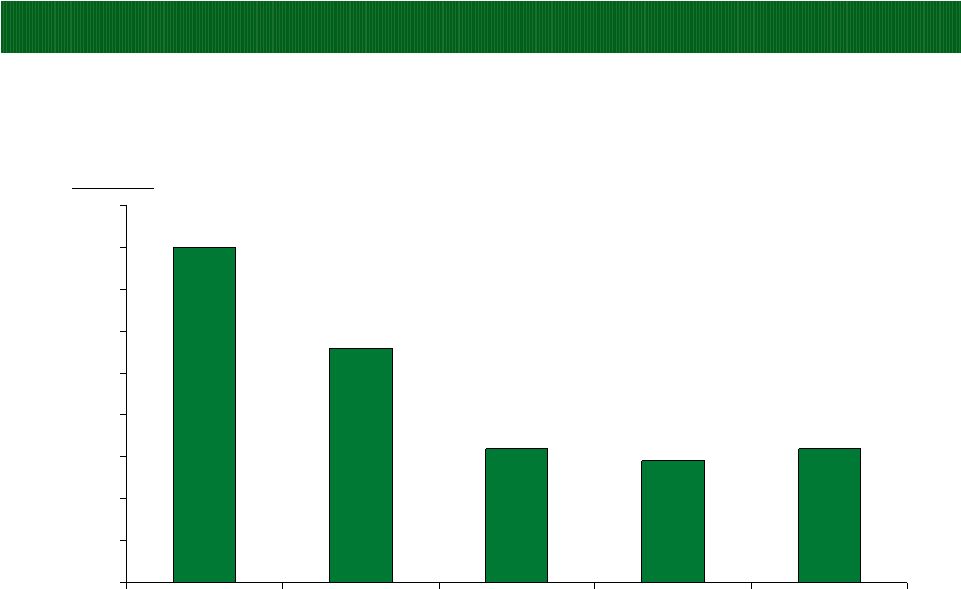

POTLATCH

CORPORATION Inland Private Sawtimber

Inventory –

Private Lands (1995-2007)

Inland West (Idaho, Eastern Washington, and Western Montana)

510

486

462

459

462

430

440

450

460

470

480

490

500

510

520

1995

2000

2005

2006

2007

Million Tons

35

Source: F2M and Potlatch Corporation |

POTLATCH CORPORATION

,

,

,

36

Definitions of Non-GAAP Measures

EBITDDA

is

a

non-GAAP

measure

that

management

uses

to

evaluate

the

cash

generating

capacity

of

the

company.

The

most

directly

comparable

GAAP measure is net earnings. EBITDDA, as we define it, is net earnings from

continuing operations adjusted for net cash interest expense,

provision/benefit for income taxes, depreciation, depletion and amortization and

the basis of real estate sold from continuing operations. It should not

be considered as an alternative to net earnings computed under GAAP.

Funds

Available

for

Distribution

(FAD)

is

a

non-GAAP

measure.

FAD,

as

defined

in

the

indenture

governing

our

senior

notes,

is

earnings from

continuing operations, plus depreciation, depletion and amortization, plus basis of

real estate sold, and minus capital expenditures. For purposes of this

definition, capital expenditures exclude all expenditures relating to direct or indirect timberland purchases in excess of $5 million. We do not use

FAD

as,

nor

should

it

be

considered

to

be,

an

alternative

to

net

cash

provided

by

operating

activities

computed

under

GAAP

as

an

indicator

of

our

operating

performance,

or

as

an

indicator

of

our

ability

to

fund

our

cash

needs.

FAD,

as

defined

in

the

indenture

governing

our

senior

notes

may

not be

comparable with measures of similar titles reported by other companies.

Inorganic

FAD

as

used

in

this

presentation

is

FAD

from

certain

large

transactions.

Inorganic

FAD

equals

transaction

income

less

income

tax,

if

any,

plus depletion or basis of real estate sold.

Organic

FAD

as

used

in

this

presentation

is

calculated

by

subtracting

inorganic

FAD

from

Funds

Available

for

Distribution

(FAD),

as

defined

above.

Segment

EBITDDA

from

continuing

operations

as

we

define

it,

is

segment

operating

income

(loss)

adjusted

for

depreciation,

depletion,

amortization and the basis of real estate sold. |