Attached files

| file | filename |

|---|---|

| 8-K - DEX ONE CORPORATION 8-K - DEX ONE Corp | a6808169.htm |

| EX-99.1 - EXHIBIT 99.1 - DEX ONE Corp | a6808169_ex991.htm |

Exhibit 99.2

Second Quarter 2011 Results Information Package July 28, 2011 Dex One

Second Quarter Highlights Posts strong EBITDA and free cash flow Maintains industry leading margins and cash flow conversion Expands digital capabilities Introduces new digital solutions Completes new partnerships with leading digital companies, including Google Forms several new product-focused partnerships Updates full year guidance Increases EBITDA and free cash flow outlook 1

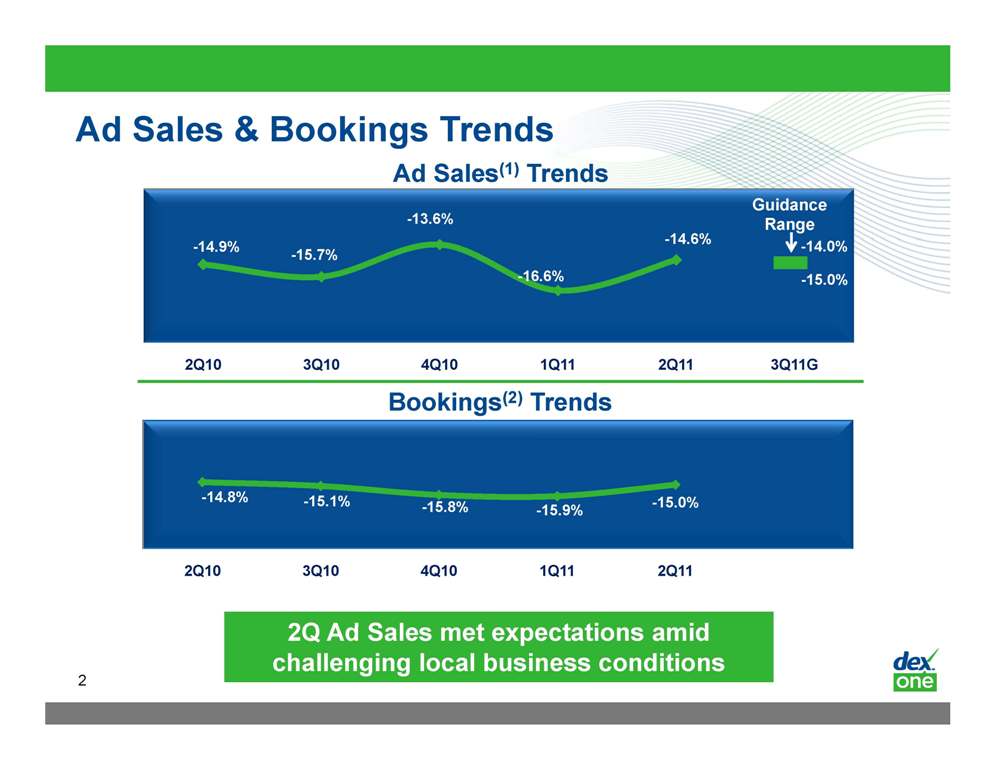

Ad Sales & Bookings Trends -13.6% -14 6% Guidance Range Ad Sales(1) Trends -14.9% -15.7% -16.6% 14.6% -14.0% -15.0% 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11G Bookings(2) Trends -14.8% -15.1% -15.8% -15.9% -15.0% 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11G 2Q 2 Sales met expectations amid challenging local business conditions

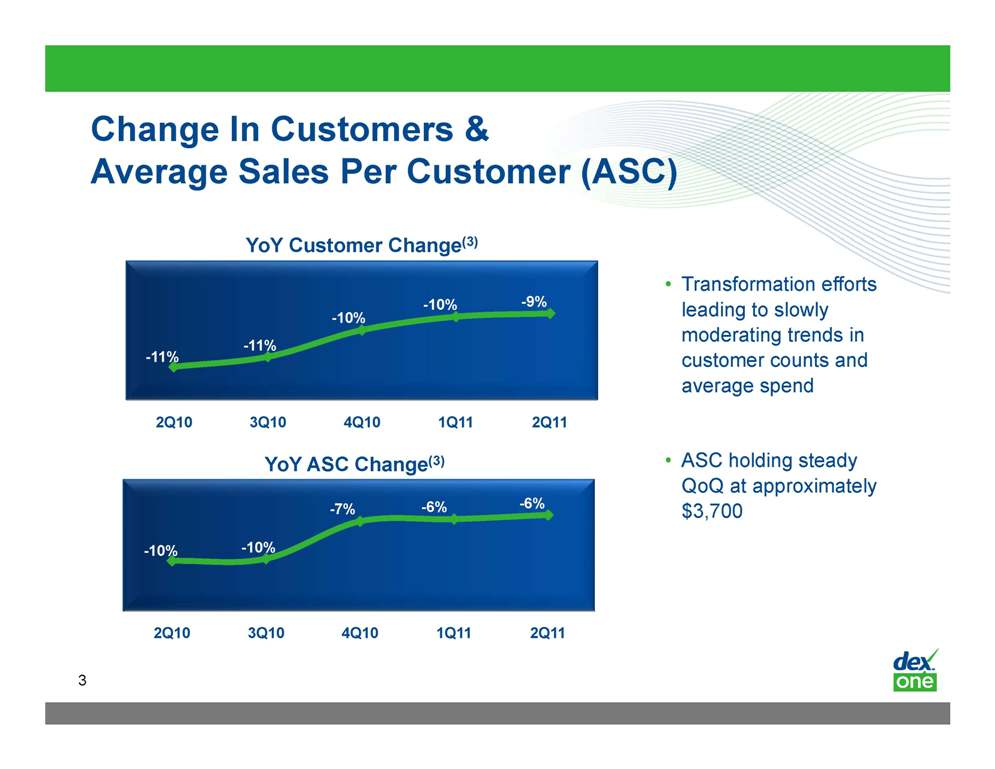

Change In Customers & Average Sales Per Customer (ASC) (3) -10% -10% -9% YoY Customer Change(• Transformation efforts leading to slowly moderating trends -11% -11% 2Q10 3Q10 4Q10 1Q11 2Q11 in customer counts and average spend -7% -6% -6% • ASC holding steady QoQ at approximately $3,700 YoY ASC Change(3) -10% -10% 2Q10 3Q10 4Q10 1Q11 2Q11 3

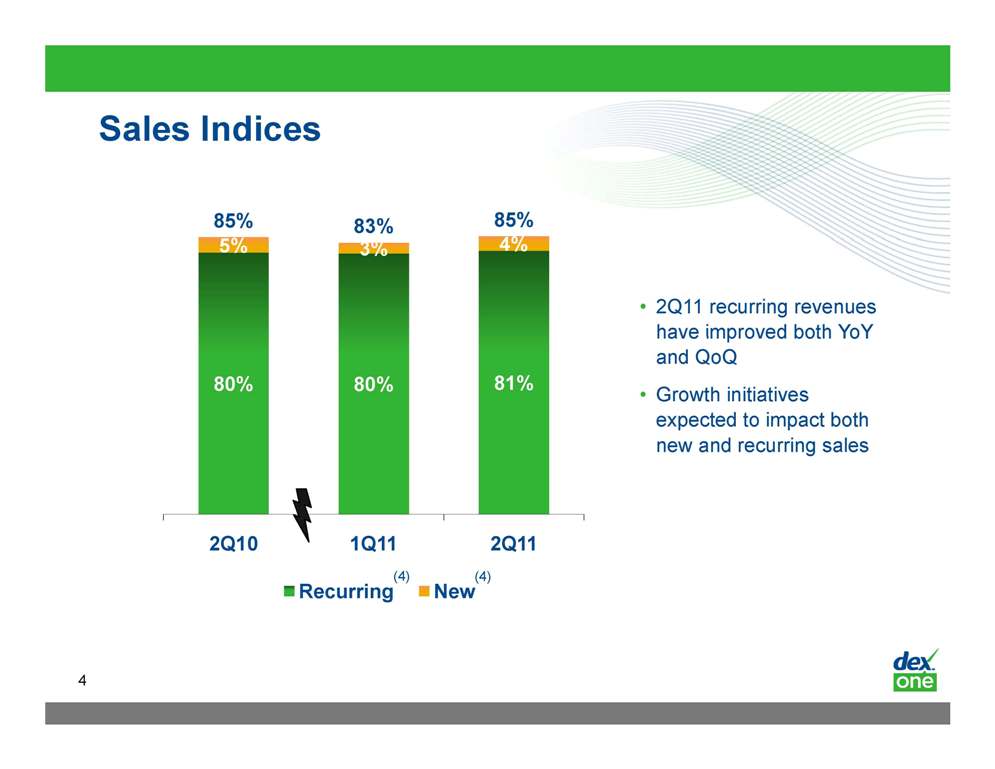

Sales Indices 5% 4% 85% 83% 85% 3% • 2Q11 recurring revenues improved YoY 80% 80% 81% have both and QoQ • Growth initiatives expected to impact both new and recurring sales 2Q10 1Q11 2Q11 Recurring New (4) (4) 4

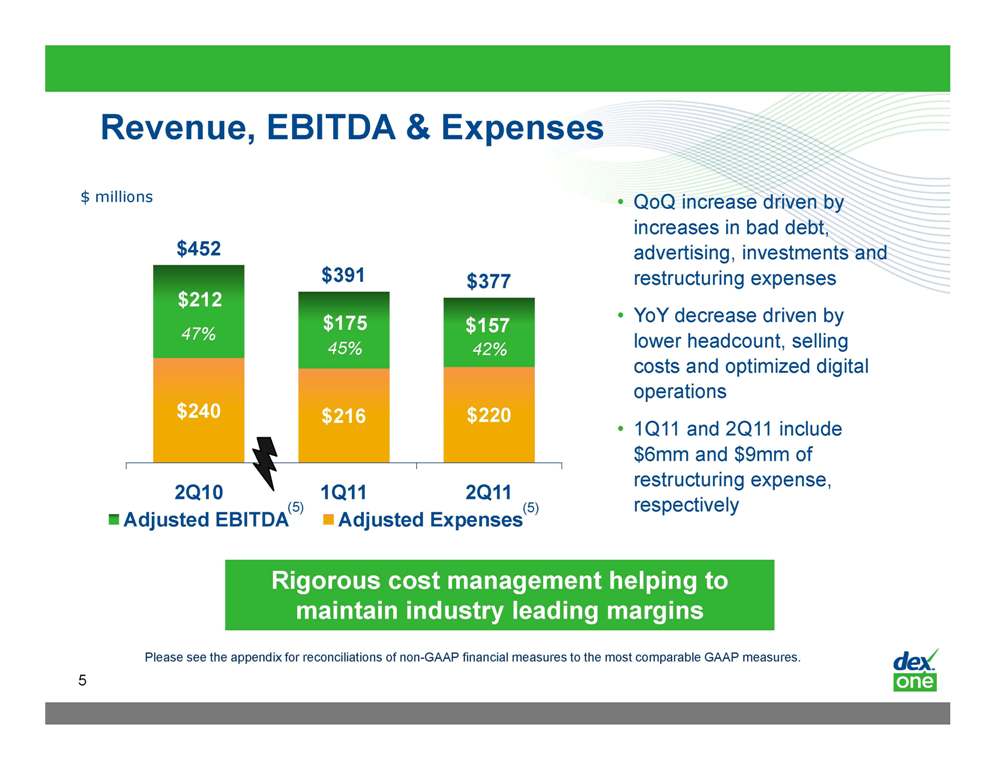

Revenue, EBITDA & Expenses , QoQ increase driven by increases in bad debt, $ millions advertising, investments and restructuring expenses YoY decrease driven by $212 $175 $157 $452 $391 $377 47% lower headcount, selling costs and optimized digital operations $240 $216 $220 45% 42% 1Q11 and 2Q11 include $6mm and $9mm of restructuring expense, respectively 2Q10 1Q11 2Q11 Adjusted EBITDA Adjusted Expenses (5) (5) Rigorous cost management helping to maintain industry leading margins 5 Please see the appendix for reconciliations of non GAAP financial measures to the most comparable GAAP measures.

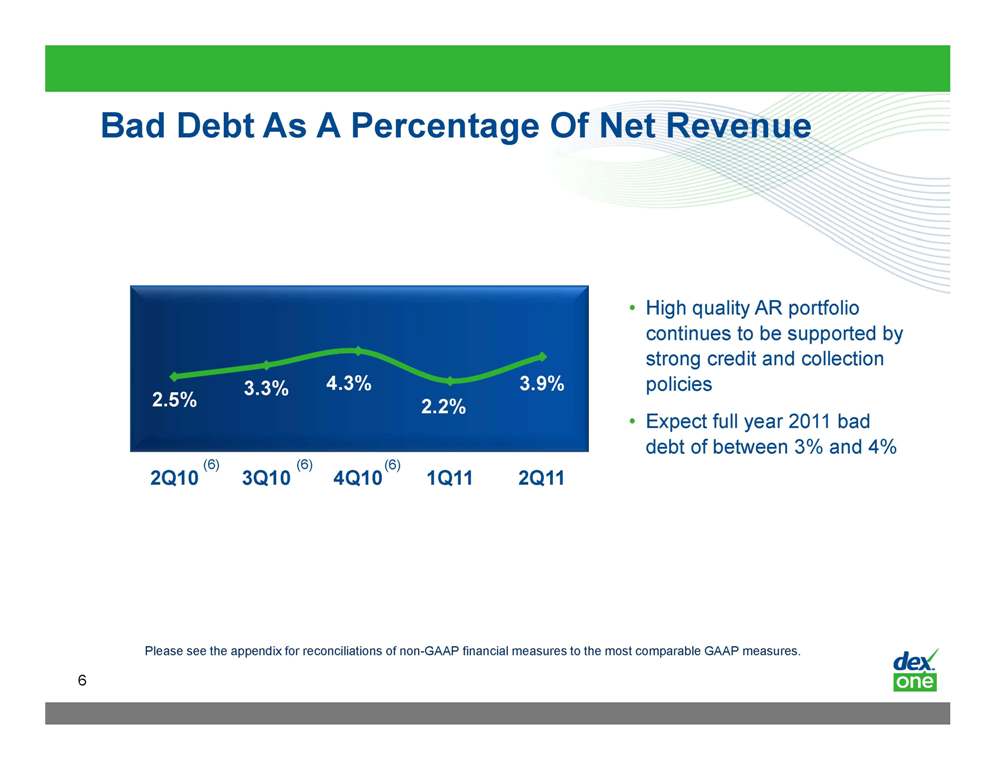

Bad Debt As A Percentage Of Net Revenue High quality AR portfolio continues supported to be by strong credit and collection policies Expect full year 2011 bad 2.5% 3.3% 4.3% 2.2% 3.9% debt of between 3% and 4% 2Q10 3Q10 4Q10 1Q11 2Q11 (6) (6) (6) 6 Please see the appendix for reconciliations of non-GAAP financial measures to the most comparable GAAP measures.

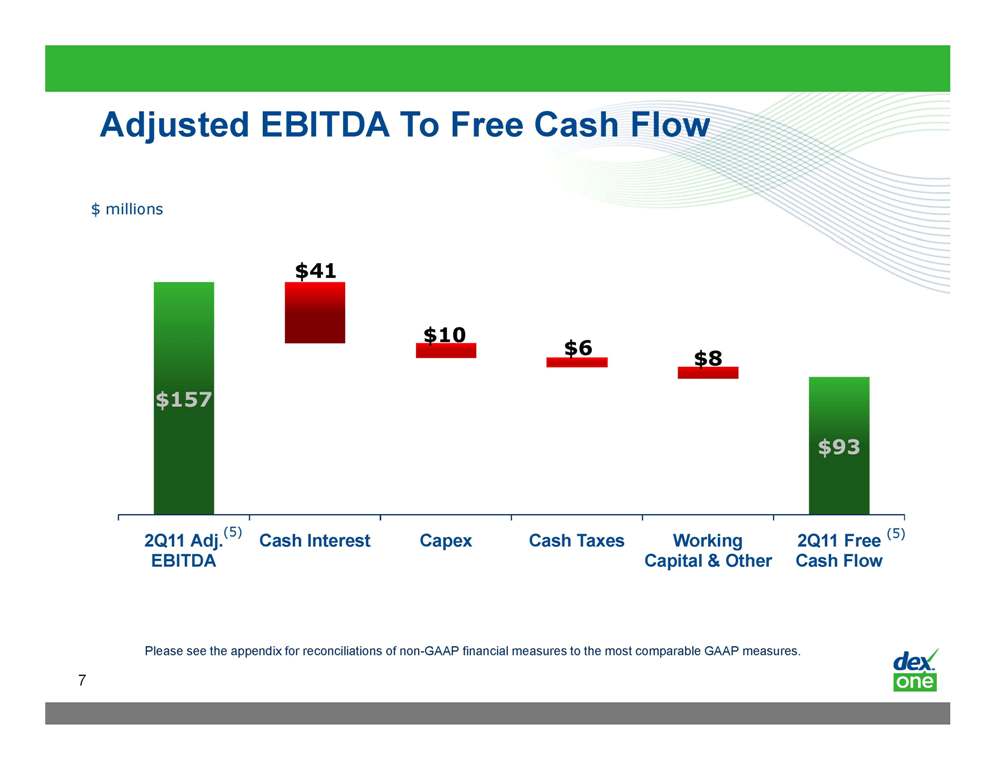

Adjusted EBITDA To Free Cash Flow $ millions $41 $10 $157 $6 $8 $93 (5) (5) 2Q11 Adj. EBITDA Cash Interest Capex Cash Taxes Working Capital & Other 2Q11 Free Cash Flow Please see the appendix for reconciliations of non-GAAP financial measures to the most comparable GAAP measures. 7

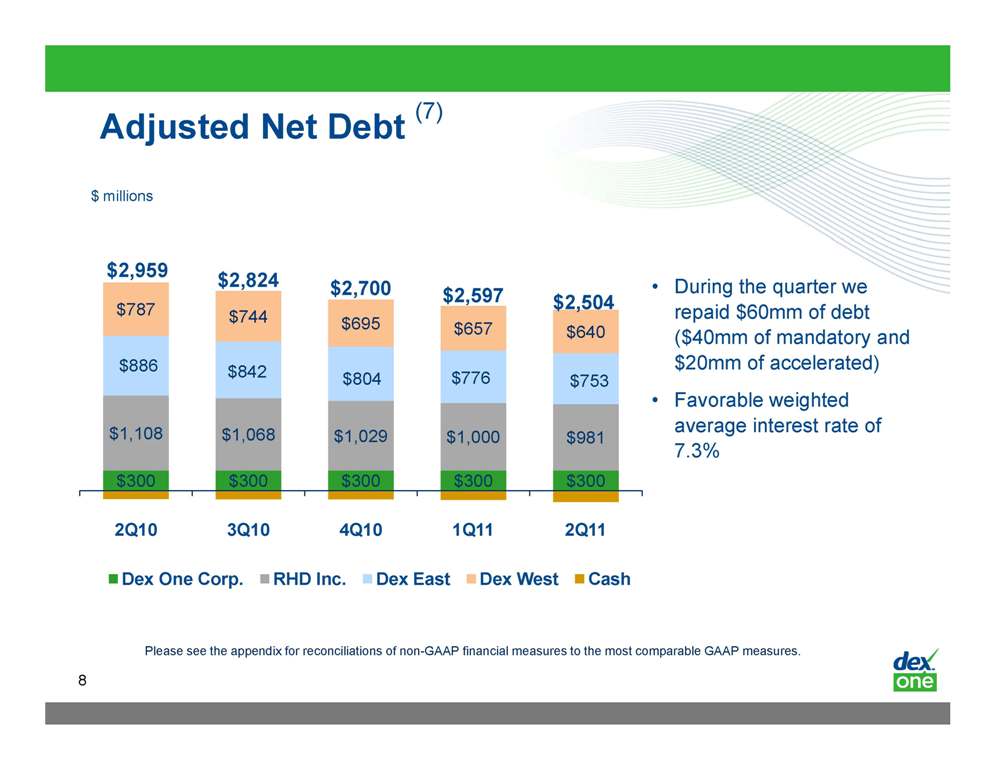

Adjusted Net Debt (7) $ millions $787 $744 $695 $ 657 $640 $2,959 $2,824 $2,700 $2,597 $2,504 During the quarter we repaid $60mm of debt $1 108 $1 068 $1 029 $1 000 $981 $886 $842 $804 $776 $753 ($40mm of mandatory and $20mm of accelerated) Favorable weighted average interest rate of $300 $300 $300 $300 $300 1,108 1,068 1,029 1,000 2Q10 3Q10 4Q10 1Q11 2Q11 7.3% Dex One Corp. RHD Inc. Dex East Dex West Cash 8 Please see the appendix for reconciliations of non-GAAP financial measures to the most comparable GAAP measures.

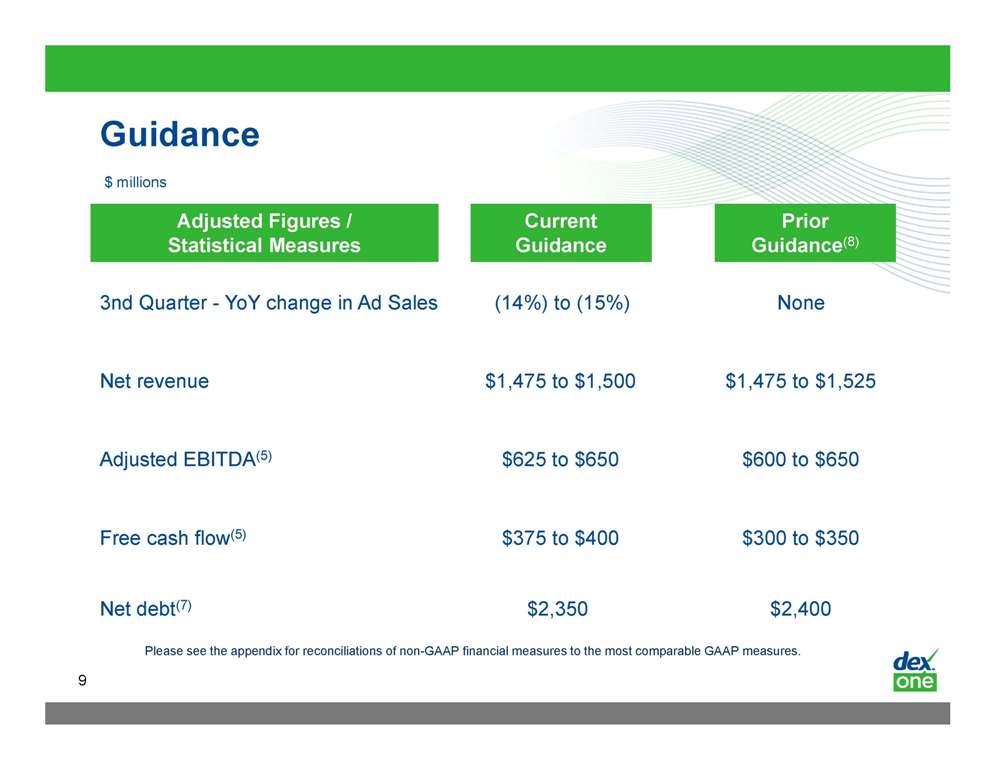

Guidance Prior (8) Adjusted Figures / Current $ millions 3nd Quarter - YoY change in Ad Sales (14%) to (15%) None Guidance(Statistical Measures Guidance Net revenue $1,475 to $1,500 $1,475 to $1,525 Adjusted EBITDA(5) $625 to $650 $600 to $650 (5) $ $ Free cash flow(375 to $ 400 300 to $ 350 Net debt(7) $2,350 $2,400 Please see the appendix for reconciliations of non-GAAP financial measures to the most comparable GAAP measures. 9

Safe Harbor Statement Certain statements contained in this presentation regarding Dex One Corporation’s future operating results, performance, business plans, prospects, guidance and any other statements not constituting historical fact are “forward-looking statements” subject to the safe harbor created by the Private Securities Litigation Reform Act of 1995. Where possible, the words “believe,” “expect,” “anticipate,” “intend,” “should,” “will,” “would,” “planned,” “estimated,” “potential,” “goal,” “outlook,” “may,” “predicts,” “could,” or the negative of such terms, or other comparable expressions as they relate to Dex One Corporation or its management have been used to identify such forward-looking statements All expressions, management, forward statements. forward-looking statements reflect only Dex One Corporation’s current beliefs and assumptions with respect to future business plans, prospects, decisions and results, and are based on information currently available to Dex One Corporation. Accordingly, the statements are subject to significant risks, uncertainties and contingencies, which could cause Dex One Corporation’s actual operating results, performance or business plans or prospects to differ materially from those expressed in, or implied by, these statements. Factors that could cause actual results to differ materially from current expectations include risks and other factors described in Dex One Corporation’s publicly available reports filed with the SEC, which contain a discussion of various factors that may affect Dex One Corporation’s business or financial results. Such risks and other factors, which in some instances are beyond Dex One Corporation’s control, include: the continuing decline in the use of print directories; increased competition, particularly from existing and emerging online technologies; ongoing weak economic conditions and continued decline in advertising sales; our ability to collect trade receivables from customers to whom we extend credit; our ability to generate sufficient cash to service our debt; our ability to comply with the financial covenants contained in our debt agreements and the potential impact to operations and liquidity as a result of restrictive covenants in such debt agreements; our ability to refinance or restructure our debt on reasonable terms and conditions as might be necessary from time to time; increasing interest rates; changes in the company’s and the company’s subsidiaries credit ratings; changes in accounting standards; regulatory changes and judicial rulings impacting our business; adverse results from litigation, governmental investigations or tax related proceedings or audits; the effect of labor strikes, lock-outs and negotiations; successful realization of the expected benefits of acquisitions, divestitures and joint ventures; our ability to maintain agreements with CenturyLink and AT&T and other major Internet search and local media companies; our reliance on thirdparty vendors for various services; and other events beyond our control that may result in unexpected adverse operating results. Dex One Corporation is not responsible for updating the information contained in this presentation beyond the published date, or for changes made to this document by wire services or Internet service providers. This presentation is being furnished to the SEC through a Form 8-K. The Company’s Quarterly Report on Form 10-Q for the period ended June 30, 2011 to be filed with the SEC may contain updates to the information included in this presentation. We reference non-GAAP financial measures in this presentation. Please see the appendix for a reconciliation of non-GAAP measures to the most comparable GAAP measures. 10

Endnotes 1) Advertising sales is a non-GAAP statistical measure and consist of sales of advertising in print directories distributed during the period and Internet-based products and services with respect to which such advertising first appeared publicly during the period. 2) Bookings is a non GAAP statistical measure and represent sales activity associated our print and non-with directories Internet-based products and services during the period. Bookings associated with our local customers represent signed contracts during the period. Bookings associated with our national customers represent what has been published or fulfilled during the period. 3) Figures are calculated on a rolling 4 quarter basis and are adjusted to make them comparable across periods. 4) Recurring = the aggregate marketing dollars spent by returning clients as a percent of total sales in the prior year New = the aggregate marketing dollars spent by clients who did not purchase marketing solutions or services from Dex One in the previous year as a percent of total sales in the prior year 5) 2Q10 results have been adjusted to exclude the impact of certain items such as fresh start accounting and reorganization expense. Adjusted results for 1Q11 and 2Q11 include restructuring expense. All periods exclude the impact of stock-based compensation expense and long-term incentive program. 6) 2Q10, 3Q10 and 4Q10 percentages based on adjusted net revenue and excludes the impact of certain items such as fresh start accounting. 7) Represents principal outstanding, which includes the fair value discount. These figures differ from GAAP balances. 8) Previously disclosed on May 2, 2011. 11

APPENDIX 12

GAAP Reconciliations – Fresh Start And Other Adjustments The Company adopted fresh start accounting and reporting effective February 1, 2010, the Fresh Start Reporting Date. The financial statements as of the Fresh Start Reporting Date report the results of Dex One with no beginning retained earnings or accumulated deficit. Any presentation of Dex One represents the financial position and results of operations of a new reporting entity and is not comparable to prior periods presented by the Predecessor Company. The financial statements for periods ended prior to the Fresh Start Reporting Date do not include the effect of any changes in the Predecessor Company's capital structure or changes in the fair value of assets and liabilities as a result of fresh start accounting. As a result of the deferral and amortization method of revenue recognition, recognized gross advertising revenues reflect the amortization of advertising sales consummated in prior periods as well as in the current period. The adoption of fresh start accounting had a significant impact on the financial position and results of operations of the Company subsequent to the Fresh Start Reporting Date. Fresh start accounting precluded us from recognizing deferred revenue of $290.9 million and certain deferred expenses of $62.3 million during the three months ended June 30, 2010, respectively, associated with advertising sales fulfilled prior to the Fresh Start Reporting Date. Thus, our reported results for the three months ended June 30, 2010 were not indicative of our underlying operating and financial performance and are not comparable to any current period presentation. Accordingly, management has provided a non-GAAP analysis that compares the Company’s GAAP results for the three months ended June 30, 2011 to Non GAAP Adjusted Results for the three months ended June 30, 2010. Management believes that these non-GAAP financial measures are important indicators of our operations because they exclude items that may not be indicative of, or related to, our core operating results, and provide a better baseline for analyzing our underlying business. Non GAAP Adjusted Results adjusts GAAP results of the Company for the three months ended June 30, 2010 to ( i) eliminate the fresh start accounting impact on revenue and certain related expenses noted above and (ii) exclude cost-uplift recorded under fresh start accounting of $3.3 million for the three months ended June 30, 2010. Deferred directory costs, such as print, paper, distribution and commissions, related to directories that have not yet been published and have been recorded at fair value, determined as (a) the estimated billable value of the published directory less (b) the expected costs to complete the directory, plus (c) a normal profit margin. This incremental fresh start accounting adjustment to step up the recorded value of the deferred directory costs to fair value is hereby referred to as “cost-uplift.” Cost-uplift has been amortized over the terms of the applicable directories, not to exceed twelve months. Fresh start accounting had an immaterial impact on our results of operations for the three months ended June 30, 2011 and therefore, we have not adjusted our GAAP results for this period. Management believes that the presentation of Non-GAAP Adjusted Results will help financial statement users better understand the material impact fresh start accounting had on the Company’s results of operations for the three months ended June 30, 2010 and also offers a non-GAAP normalized comparison to GAAP results of the Company for the three months ended June 30, 2011. The Non-GAAP Adjusted Results presented below are reconciled to the most comparable GAAP measures. While the Non-GAAP Adjusted Results exclude the effects of fresh start accounting, it must be noted that the Non-GAAP Adjusted Results are not comparable to the Company’s GAAP results for the three months ended June 30 2011 and should not be treated as such We strongly encourage investors and Company s 30, such. stockholders to review our financial statements and publicly filed reports in their entirety and not rely on any single financial measure. 13

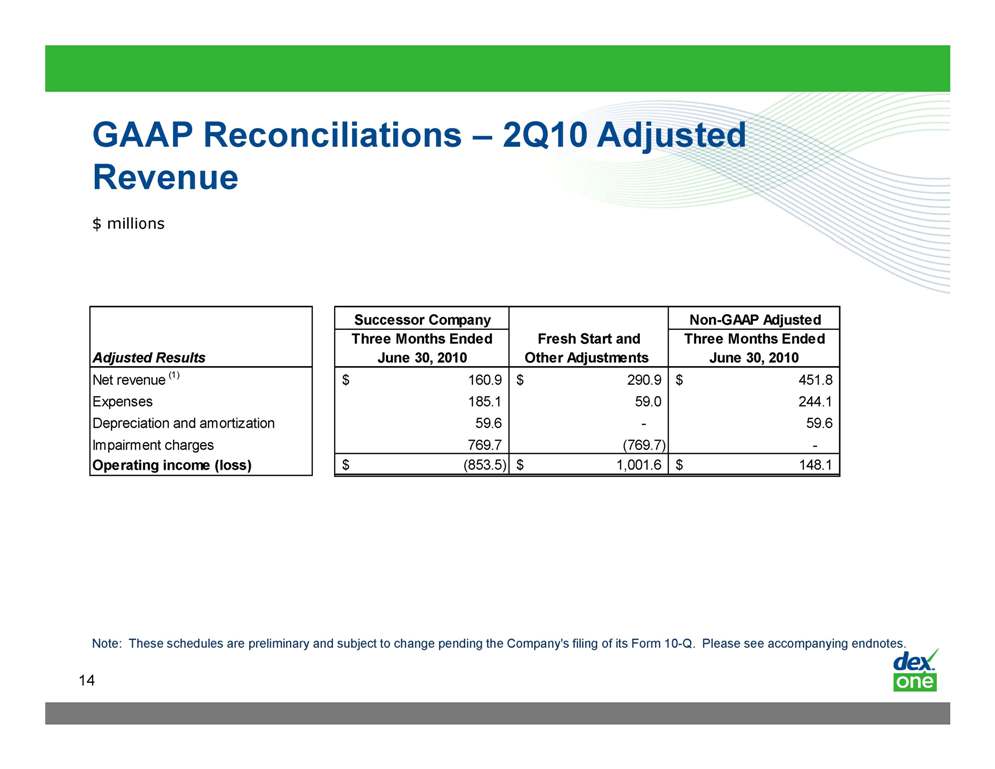

GAAP – Reconciliations 2Q10 Adjusted Revenue $ millions Successor Company Non-GAAP Adjusted Three Months Ended Fresh Start and Three Months Ended Adjusted Results June 30, 2010 Other Adjustments June 30, 2010 Net revenue (1) 160.9 $ 290.9 $ 451.8 $ Expenses 185.1 59.0 244.1 Depreciation and amortization 59.6 - 59.6 Impairment charges 769.7 (769.7) - Operating income (loss) (853.5) $ 1,001.6 $ 148.1 $ Note: These schedules are preliminary and subject to change pending the Company's filing of its Form 10-Q. Please see accompanying endnotes. 14

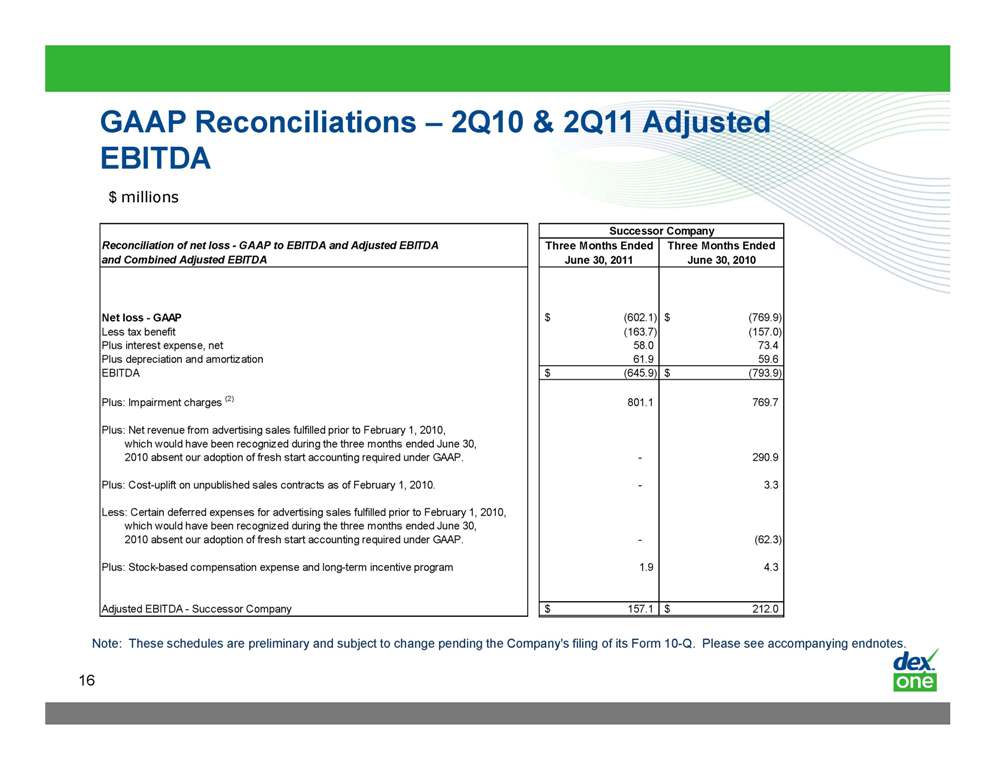

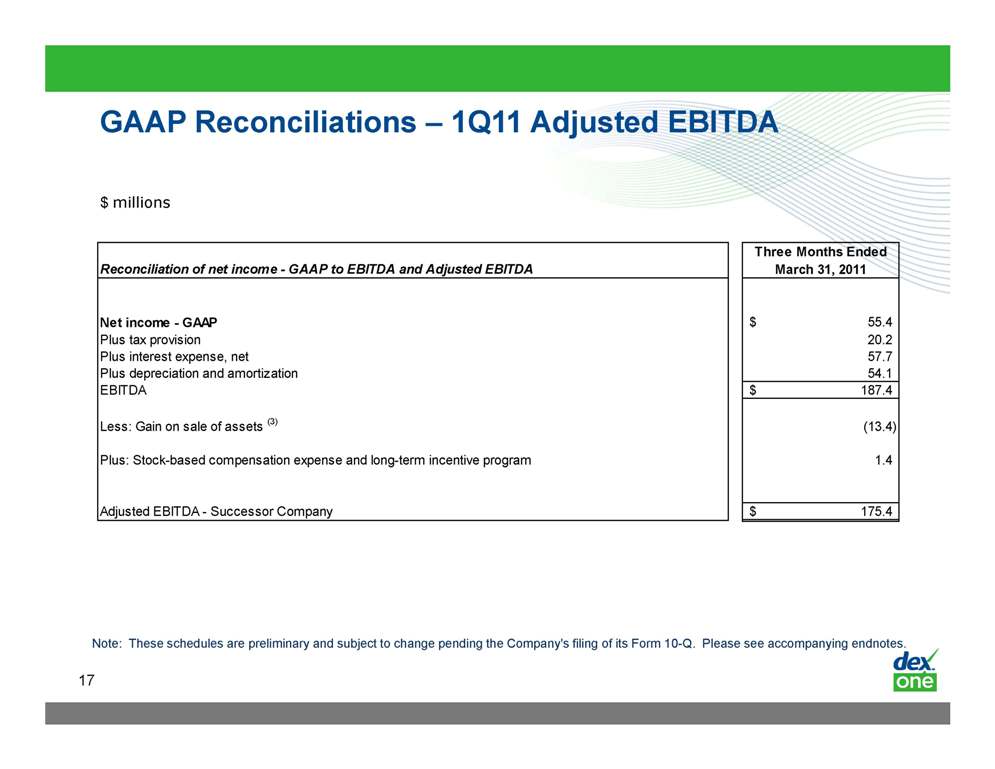

GAAP Reconciliations – 2Q10, 1Q11 & 2Q11 Adjusted EBITDA EBITDA and Adjusted EBITDA are not measurements of operating performance computed in accordance with GAAP and should not be considered as a substitute for net income (loss) prepared in conformity with GAAP. In addition, EBITDA may not be comparable to similarly titled measures of other companies. Management believes that these non-financial measures are important indicators of our operations because they exclude items that may not be indicative of, or related to, our core operating results, and provide a better baseline for analyzing our underlying business. Adjusted EBITDA of the Successor Company for the three months ended June 30, 2010 is determined by adjusting EBITDA (i) to eliminate the fresh start accounting impact on revenue and certain expenses, (ii) to exclude the impact of cost-uplift recorded under fresh start accounting, (iii) exclude goodwill and non-goodwill intangible asset impairment charges and (iv) adjust for stock-based compensation expense and long-term incentive program. Adjusted EBITDA of the Successor Company for the three months ended March 31, 2011 is determined by adjusting EBITDA for (i) stock-based compensation expense and long-term incentive program and (ii) gain on sale of stock long assets. Adjusted EBITDA of the Successor Company for the three months ended June 30, 2011 is determined by adjusting EBITDA for (i) impairment charges and (ii) stock-based compensation expense and long-term incentive program. 15

GAAP Reconciliations – 2Q10 & 2Q11 Adjusted $ millions EBITDA Successor Company Reconciliation of net loss - GAAP to EBITDA and Adjusted EBITDA Three Months Ended Three Months Ended and Combined Adjusted EBITDA June 30, 2011 June 30, 2010 Net loss - GAAP (602.1) $ (769.9) $ Less tax benefit ( 163.7) ( 157.0) ) ) Plus interest expense, net 58.0 73.4 Plus depreciation and amortization 61.9 59.6 EBITDA (645.9) $ (793.9) $ Plus: Impairment charges (2) 801.1 769.7 Plus: Net revenue from advertising sales fulfilled prior to February 1, 2010, which would have been recognized during the three months ended June 30, 2010 absent our adoption of fresh start accounting required under GAAP. - 290.9 Plus: Cost-uplift on unpublished sales contracts as of February 1, 2010. - 3.3 Less: Certain deferred expenses for advertising sales fulfilled prior to February 1, 2010, which would have been recognized during the three months ended June 30, 2010 absent our adoption of fresh start accounting required under GAAP. - (62.3) Plus: Stock-based compensation expense and long-term incentive program 1.9 4.3 Adjusted EBITDA - Successor Company 157.1 $ 212.0 $ 16 Note: These schedules are preliminary and subject to change pending the Company's filing of its Form 10-Q. Please see accompanying endnotes.

GAAP Reconciliations – 1Q11 Adjusted EBITDA $ millions Three Months Ended Reconciliation of net income - GAAP to EBITDA and Adjusted EBITDA March 31, 2011 Net income - GAAP 55.4 $ Plus tax provision 20.2 Plus interest expense, net 57.7 Plus depreciation and amortization 54.1 EBITDA 187.4 $ Less: Gain on sale of assets (3) ( 13.4) ) Plus: Stock-based compensation expense and long-term incentive program 1.4 Adjusted EBITDA - Successor Company 175.4 $ 17 Note: These schedules are preliminary and subject to change pending the Company's filing of its Form 10-Q. Please see accompanying endnotes.

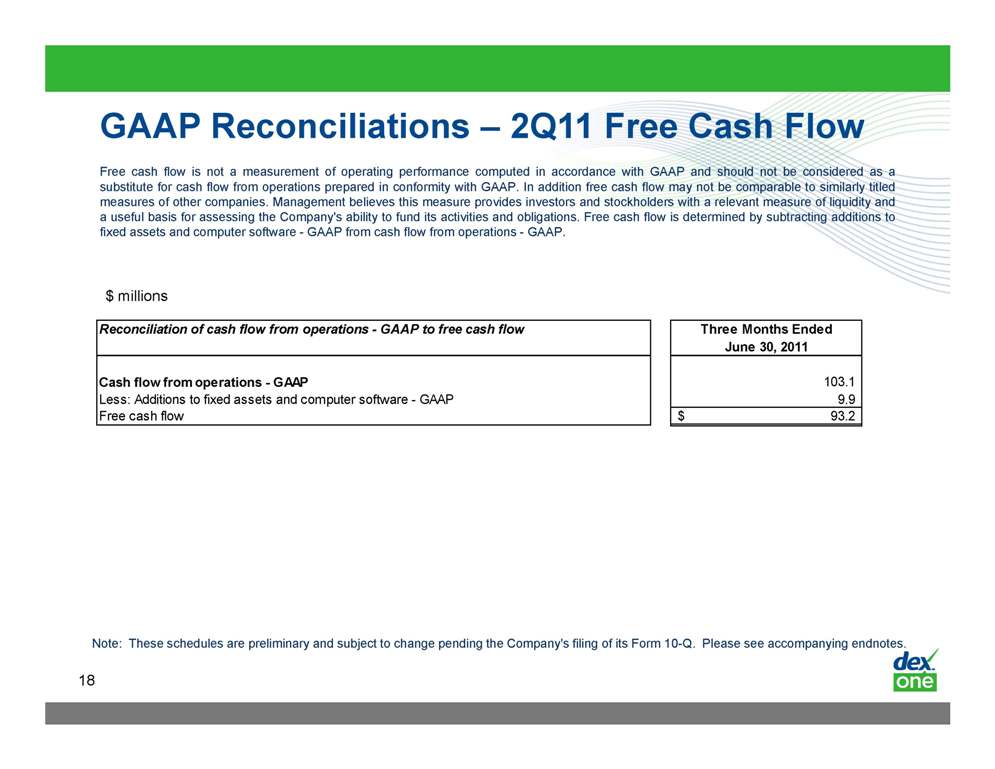

GAAP Reconciliations – 2Q11 Free Cash Flow Free cash flow is not a measurement of operating performance computed in accordance with GAAP and should not be considered as a substitute for cash flow from operations prepared in conformity with GAAP. In addition free cash flow may not be comparable to similarly titled measures of other companies. Management believes this measure provides investors and stockholders with a relevant measure of liquidity and a useful basis for assessing the Company's ability to fund its activities and obligations. Free cash flow is determined by subtracting additions to fixed assets and computer software - GAAP from cash flow from operations - GAAP. $ millions Reconciliation of cash flow from operations - GAAP to free cash flow Three Months Ended June 30, 2011 Cash flow from operations - GAAP 103.1 Less: Additions to fixed assets and computer software - GAAP 9.9 Free cash flow 93.2 $ 18 Note: These schedules are preliminary and subject to change pending the Company's filing of its Form 10-Q. Please see accompanying endnotes.

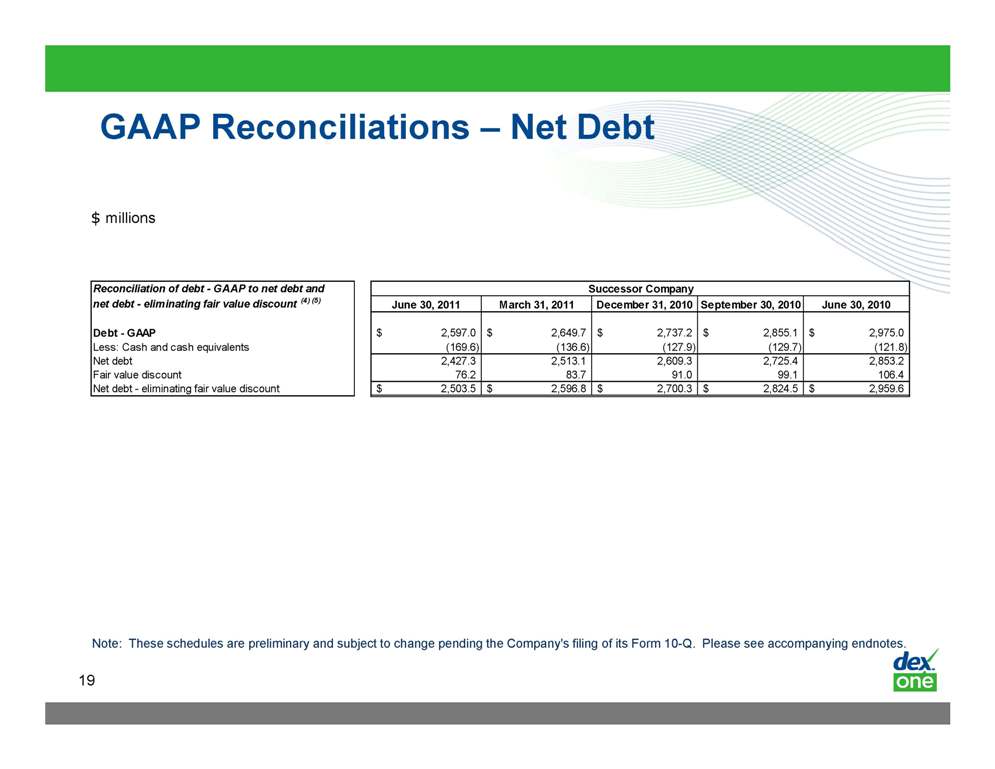

GAAP Reconciliations – Net Debt $ millions Reconciliation of debt - GAAP to net debt and net debt – eliminating fair value discount (4) (5) June 30, 2011 March 31, 2011 December 31, 2010 September 30, 2010 June 30, 2010 Debt - GAAP 2,597.0 $ 2,649.7 $ 2,737.2 $ 2,855.1 $ 2,975.0 $ Successor Company Less: Cash and cash equivalents (169.6) (136.6) (127.9) (129.7) (121.8) Net debt 2,427.3 2,513.1 2,609.3 2,725.4 2,853.2 Fair value discount 76.2 83.7 91.0 99.1 106.4 Net debt - eliminating fair value discount 2,503.5 $ 2,596.8 $ 2,700.3 $ 2,824.5 $ 2,959.6 $ 19Note: These schedules are preliminary and subject to change pending the Company's filing of its Form 10-Q. Please see accompanying endnotes.

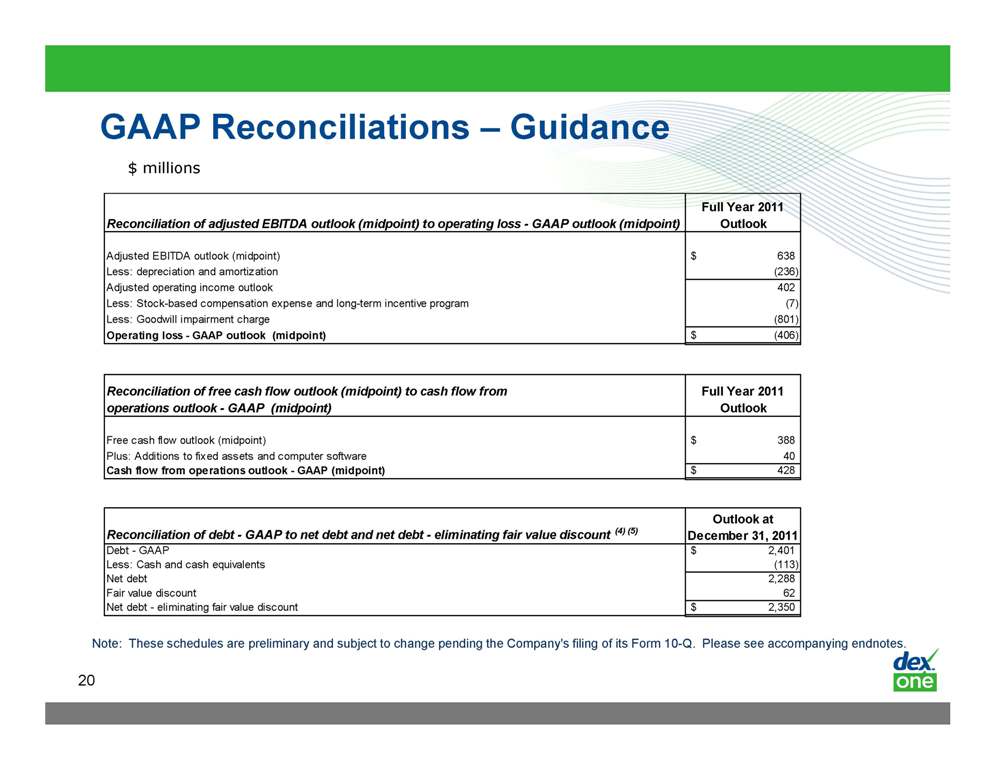

GAAP Reconciliations – Guidance $ millions Full Year 2011 Reconciliation of adjusted EBITDA outlook (midpoint) to operating loss - GAAP outlook (midpoint) Outlook Adjusted EBITDA outlook (midpoint) 638 $ Less: depreciation and amortization (236) Adjusted operating income outlook 402 Less: Stock-based compensation expense and long-term incentive program (7) Less: Goodwill impairment charge (801) Operating loss – GAAP outlook (midpoint) (406) $ Reconciliation of free cash flow outlook (midpoint) to cash flow from Full Year 2011 operations outlook - GAAP (midpoint) Outlook Free cash flow outlook (midpoint) 388 $ Plus: Additions to fixed assets and computer software 40 Cash flow from operations outlook - GAAP (midpoint) 428 $ (4) Outlook at Reconciliation of debt - GAAP to net debt and net debt - eliminating fair value discount (5) December 31, 2011 Debt - GAAP 2,401 $ Less: Cash and cash equivalents (113) Net debt 2,288 Fair value discount 62 Net debt - eliminating fair value discount 2,350 $ 20 Note: These schedules are preliminary and subject to change pending the Company's filing of its Form 10-Q. Please see accompanying endnotes.

Reconciliation 1) Our advertising revenues are earned primarily from the sale of advertising in yellow pages directories we publish. Advertising revenues also include revenues from our Internet-based marketing solutions including online directories, such as DexKnows.com and DexNet. Advertising revenues are affected by several factors, including changes in the quantity and size of advertisements, acquisition of new clients, renewal rates of existing clients, premium advertisements sold, changes in advertisement pricing, the introduction of new marketing solutions, an increase in competition and more fragmentation in the local business search market and general economic factors. Revenues with respect to print advertising and Internet-based marketing solutions that are sold with print advertising are recognized under the deferral and amortization method whereby revenues are initially deferred when a directory is published, net of sales claims and allowances, and recognized ratably over the directory’s life, which is typically 12 months. Revenues with respect to Internet-based marketing solutions that are sold standalone, such as DexNet, are recognized ratably over the life of the contract commencing when they are first delivered or fulfilled. Revenues with respect to our marketing solutions that are non-performance based are recognized ratably over the life of the contract commencing when they are first delivered or fulfilled. Revenues with respect to our marketing solutions that are performance-based are recognized as the service is delivered or fulfilled. 2) Based upon our announcement in May 2011 of the impending departure of our Executive Vice President and Chief Financial Officer the continued decline Officer, in the trading value of our debt and equity securities and revisions made to our long-term forecast, the Company concluded there were indicators of impairment as of May 31, 2011. As a result, we performed impairment tests of our goodwill, definite-lived intangible assets and other long lived assets as of May 31, 2011. The impairment testing results for recoverability of our definite-lived intangible assets and other long-lived assets indicated they were recoverable and thus no impairment test was required as of May 31, 2011. Based upon the testing results of our goodwill, we determined that the remaining goodwill assigned to each of our reporting units was fully impaired and thus recognized an aggregate goodwill impairment charge of $801.1 million during the three and six months ended June 30, 2011, which was recorded at each of our reporting units. As of June 30, 2011, the Company has no recorded goodwill at any of its reporting units. We have removed the goodwill impairment charge from GAAP results for the three and six months ended June 30, 2011. 3) On February 14, 2011, we completed the sale of substantially all net assets of Business.com. As a result, we recognized a gain on sale of these assets of $13.4 million during the six months ended June 30, 2011. 4) In conjunction with our adoption of fresh start accounting, an adjustment was established to record our outstanding debt at fair value on the Fresh Start Reporting Date The Company was required to record our amended and restated credit facilities at a discount as a result of their fair value on the Fresh Date. Start Reporting Date. Therefore, the carrying amount of these debt obligations is lower than the principal amount due at maturity. This fair value adjustment is amortized as an increase to interest expense over the remaining term of the respective debt agreements and does not impact future scheduled interest or principal payments. The unamortized fair value adjustment resulting from fresh start accounting was $76.2 million at June 30, 2011. 5) Net debt represents total debt less cash and cash equivalents on the respective date. Net debt – eliminating fair value discount eliminates the fair value discount as a result of fresh start accounting described in Note 4 and represents principal amounts due at maturity. 21 Note: These schedules are preliminary and subject to change pending the Company's filing of its Form 10-Q.