Attached files

| file | filename |

|---|---|

| EX-23.1 - 22nd Century Group, Inc. | v229053_ex23-1.htm |

| EX-10.20 - 22nd Century Group, Inc. | v229053_ex10-20.htm |

As filed with the Securities and Exchange Commission on July 20, 2011

Registration No. 333-173420

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

22nd CENTURY GROUP, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

(State or other jurisdiction of

Incorporation or organization)

|

5194

(Primary Standard Industrial

Classification Code Number)

|

98-0468420

(I.R.S. Employer

Identification No.)

|

8201 Main Street, Suite 6

Williamsville, New York 14221

(716) 270-1523

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Joseph Pandolfino

Chief Executive Officer

22nd Century Group, Inc.

8201 Main Street, Suite 6

Williamsville, New York 14221

(716) 270-1523

(Address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Patrick G. Quick, Esq.

Thomas L. James, Esq.

Teri L. Champ, Esq.

Foley & Lardner LLP

777 East Wisconsin Avenue

Milwaukee, Wisconsin 53202-5306

(414) 271-2400

Approximate date of commencement of proposed sale to the public: As soon as practicable after the Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company x

CALCULATION OF REGISTRATION FEE

|

Title of each class of

securities to be registered

|

Amount to be

registered (1)

|

Proposed

maximum

offering price

per share (2)

|

Proposed

maximum

aggregate

offering

price(2)

|

Amount of

registration fee

(3)

|

||||||||||||

|

Common stock, par value $0.00001 per share

|

5,434,446 | $ | 1.25 | $ | 6,793,057.50 | $ | 788.68 | |||||||||

|

(1)

|

Pursuant to Rule 416 under the Securities Act of 1933, as amended, the number of shares of common stock registered hereby is subject to adjustment to prevent dilution resulting from stock splits, stock dividends or similar transactions.

|

|

(2)

|

Estimated solely for the purpose of determining the amount of the registration fee, based on the average of the high and low sale prices of the common stock as reported by the OTC Bulletin Board on April 6, 2011 in accordance with Rule 457(c) under the Securities Act of 1933.

|

|

(3)

|

The registration fee was previously paid on April 8, 2011.

|

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

|

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and the selling stockholders are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

|

SUBJECT TO COMPLETION, DATED JULY 20, 2011

PROSPECTUS

22nd CENTURY GROUP, INC.

5,434,446 Shares of Common Stock

This prospectus relates to the offering by the selling stockholders of 22nd Century Group, Inc. of up to 5,434,446 shares of common stock, par value $0.00001 per share. These shares were privately issued to the selling stockholders in connection with a private placement and merger transaction. We will not receive any proceeds from the sale of common stock by the selling stockholders.

The selling stockholders have advised us that they will sell the shares of common stock from time to time in broker’s transactions, in the open market, on the OTC Bulletin Board, in privately negotiated transactions or a combination of these methods, at market prices prevailing at the time of sale, at prices related to the prevailing market prices or at negotiated prices. We will pay the expenses incurred to register the shares for resale, but the selling stockholders will pay any underwriting discounts, commissions or agent’s commissions related to the sale of their shares of common stock.

Our common stock is traded on the OTC Bulletin Board under the symbol “XXII.OB”. On July 15, 2011, the closing sale price of our common stock was $1.25 per share.

Investing in our common stock involves risks. Before making any investment in our securities, you should read and carefully consider risks described in the “Risk Factors” section beginning on page 9 of this prospectus.

You should rely only on the information contained in this prospectus or any prospectus supplement or amendment thereto. We have not authorized anyone to provide you with different information. This prospectus may only be used where it is legal to sell these securities. The information in this prospectus is only accurate on the date of this prospectus, regardless of the time of any sale of securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This date of this prospectus is July___, 2011

You should rely only on the information contained in this prospectus. We have not authorized any other person to provide you with information that is different from that contained in this prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. The selling stockholders are offering to sell and seeking offers to buy these securities only in jurisdictions where offers and sales are permitted. You should assume that the information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

TABLE OF CONTENTS

|

Page

|

||

|

PROSPECTUS SUMMARY

|

1

|

|

|

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

|

8

|

|

|

RISK FACTORS

|

9

|

|

|

PRINCIPAL AND SELLING STOCKHOLDERS

|

28

|

|

|

USE OF PROCEEDS

|

32

|

|

|

DIVIDEND POLICY

|

32

|

|

|

DETERMINATION OF OFFERING PRICE

|

32

|

|

|

MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

|

32

|

|

|

SECURITIES AUTHORIZED FOR ISSUANCE UNDER EQUITY COMPENSATION PLANS

|

33

|

|

|

BUSINESS

|

35

|

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

57

|

|

|

DIRECTORS AND EXECUTIVE OFFICERS

|

64

|

|

|

EXECUTIVE COMPENSATION

|

67

|

|

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS

|

71

|

|

|

PLAN OF DISTRIBUTION

|

73

|

|

|

DESCRIPTION OF SECURITIES

|

75

|

|

|

LEGAL MATTERS

|

79

|

|

|

EXPERTS

|

79

|

|

|

WHERE YOU CAN FIND MORE INFORMATION

|

79

|

|

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

|

80

|

|

|

INDEX TO FINANCIAL STATEMENTS

|

F-1

|

|

|

EXHIBIT INDEX

|

E-1

|

i

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus. This summary is not complete and does not contain all the information that should be considered before investing in our common stock. Investors should read the entire prospectus carefully, including the more detailed information contained herein under the “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements” sections and our consolidated financial statements and the notes to those financial statements.

As used in this prospectus, unless the context otherwise requires, the “Company,” “we,” “us” and “our” refer to 22nd Century Group, Inc., a Nevada corporation, as well as its subsidiaries, 22nd Century Limited, LLC, a Delaware limited liability company, and Goodrich Tobacco Company, LLC, a Delaware limited liability company, taken as a whole, and also refer to the operations of 22nd Century Limited, LLC prior to the merger on January 25, 2011, as discussed below, which resulted in 22nd Century Limited, LLC becoming our wholly-owned subsidiary. Hereinafter, 22nd Century Limited, LLC is sometimes referred to as “22nd Century.”

Our Company

Overview

We are a plant biotechnology company and a global leader in modifying the content of nicotinic alkaloids in tobacco plants through genetic engineering and plant breeding. We control 90 issued patents, of which we own 8 issued patents and we have the exclusive license to an additional 90 issued patents in an aggregate of 79 countries where at least 75% of the world’s smokers reside. Additionally, we control 45 pending patent applications, of which we own 29 and have an exclusive license to 16. In the U.S., patents that currently cover our products expire in 2019 through 2022. Also in the U.S., patent applications that we expect will cover our products would, if patents are granted in connection with such applications, expire in 2024 through 2028. However, there is no guarantee that patents will be granted in response to such patent applications and therefore cover our products. Our two worldwide exclusive licenses, one from North Carolina State University (“NCSU”) and the other from National Research Council of Canada, Plant Biotechnology Institute in Saskatoon, Canada (“NRC”), each involve multiple patent families, patent applications and patents. The exclusive rights under each of these two license agreements expire on the date on which the last patent covered by the subject license expires in the country or countries where such patents are in effect, which is expected to be from 2022 through 2028, respectively. We believe our proprietary technology provides us with opportunities in the global market for approved smoking cessation aids and the emerging market for modified risk tobacco products, which is a term that we explain below; however, we have not yet identified any specific countries or developed any timelines or cost estimates for international expansion of our business.

Our January 25, 2011 Private Placement Offering (as defined under the “Recent Developments” section on page 5) of 5,434,446 Units (as defined under the “Recent Developments” section), which we collectively refer to in this prospectus as “PPO Securities,” resulted in approximately $3.4 million in net cash proceeds and a reduction of debt obligations to shareholders that were on the balance sheet at December 31, 2010 of approximately $614,000, which were exchanged for equity interests in the Private Placement Offering. This offering involves the resale of common stock, and we have registered that resale to satisfy registration rights related to the PPO Securities. We will not receive any proceeds from the sale of common stock under this prospectus.

We plan to use a material portion of the proceeds from the Private Placement Offering to complete a Phase II-B clinical trial which is necessary to seek approval from the U.S. Food and Drug Administration (“FDA”) for X-22, our prescription smoking cessation aid in development. We believe the cost of completing the Phase II-B trial is approximately $1.1 million, of which we have paid approximately one-third as of March 31, 2011. We have designated our upcoming phase II clinical trial as a “Phase II-B” clinical trial because (i) we are looking for continued indications of clinical efficacy and safety in larger groups of patients in our clinical trial, and (ii) very low nicotine (VLN) cigarettes made from the Company’s VLN tobacco have already demonstrated efficacy in previous Phase II trials, specifically the Phase II trial at the University of Minnesota which had a very similar protocol compared to our upcoming phase II clinical trial. However, “Phase II-B” is not an official FDA designation.

1

There is no guarantee that X-22 will obtain the necessary approvals from the FDA to be marketed as a smoking cessation aid. We estimate the cost of completing the Phase III trials is approximately $10 million. We currently plan to seek to raise approximately $15 million in the fourth quarter of 2011 through the sale of our common stock and/or securities convertible into common stock to fund Phase III trials, modified risk exposure studies and our general working capital requirements. At this time, we have not yet attempted to obtain any approval for X-22 outside of the U.S., and there is no guarantee that we will be able to obtain any approval for X-22 outside of the U.S. (for those countries that require such regulatory approvals). We are currently in default under the terms of our exclusive worldwide license agreement with North Carolina State University (“NCSU”) for failure to timely pay certain amounts owed under the license agreement. We have requested that NCSU defer payment of these amounts. Should NCSU choose instead to invoke its right to terminate this license agreement, we would have 60 days notice to cure the payment default, and if we did not cure the payment default within such 60-day period and the license terminated, our business would be materially and adversely affected. If NCSU does not agree to a deferment of the unpaid balance owing under the license agreement and we pay such balance, we may not have sufficient funds to pay in full the cost of our Phase II-B clinical trial for X-22 (as described in more detail throughout this prospectus).

Our net sales for the three month period ended March 31, 2011 were $117,456 mainly from our research cigarette program. For the year ended December 31, 2010, we had total sales of $49,784 from our research cigarette program. Our net loss for the three month period ended March 31, 2011 was approximately $652,000, or $0.03 per diluted common share. For the year ended December 31, 2010, our net loss was $1,423,647, or $0.11 per diluted common share. Total assets were $3,410,431 at March 31, 2011, compared to $2,800,520 at December 31, 2010. Total current liabilities were $1,458,997 at March 31, 2011, compared to $4,823,635 at December 31, 2010. Total liabilities, including long term liabilities, were $5,197,747 at March 31, 2011, including our warrant derivative liability of $3,061,750, compared to $4,889,192 at December 31, 2010, which did not include any warrant derivative liability. As of March 31, 2011, we had working capital of approximately $0.5 million compared to negative working capital of approximately $4.1 million at December 31, 2010. The improvement in our working capital position of $4.6 million was mainly a result of proceeds from the January 25, 2011 Private Placement Offering and the transfer from accounts payable of $587,000 to notes payable as part of payment arrangements with two vendors for past due amounts we owed, offset by our net loss for the three months ended March 31, 2011. As reported in our Annual Report on Form 8-K/A as filed with the SEC on March 23, 2011, our independent registered public accounting firm expressed substantial doubt as to whether we can continue as a going concern. Even in light of our receipt of the proceeds of the Private Placement Offering, we cannot guarantee our ability to continue as a going concern.

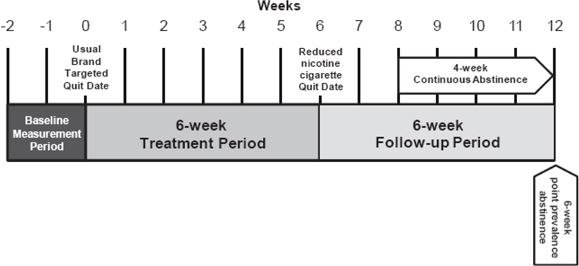

We have met with the FDA regarding the remaining clinical trials for X-22 and based on the FDA’s guidance, we plan to conduct a Phase II-B trial and two larger and concurrent Phase III trials with the same protocols. X-22 will be a prescription-only kit containing very low nicotine (“VLN”) cigarettes made from our proprietary tobacco, which has approximately 95% less nicotine compared to tobacco in existing “light” cigarettes. The therapy protocol allows the patient to smoke our VLN cigarettes without restriction over the six-week treatment period to facilitate the goal of the patient quitting smoking by the end of the treatment period. Although further research and clinical trials are needed to determine efficacy of X-22, we believe this therapy protocol has thus far been successful because VLN cigarettes made from our proprietary tobacco satisfy smokers’ cravings for cigarettes while (i) greatly reducing nicotine exposure and nicotine dependence and (ii) extinguishing the association between the act of smoking and the rapid delivery of nicotine. We believe X-22 will be more attractive to smokers than other therapies since it smokes and tastes like a typical cigarette, involves the same smoking behavior, and does not expose the smoker to any new drugs or new side effects (other than the exposure and side effects from smoking cigarettes in general) that may occur when a person is exposed to a new drug. There is no guarantee that X-22 will obtain the necessary approvals from the FDA to be marketed as a smoking cessation aid.

Independent studies, including two Phase II clinical trials, have demonstrated that VLN cigarettes made from our proprietary VLN tobacco are at least as effective as FDA-approved smoking cessation aids. As we describe further in the Technology Platform and Intellectual Property section, X-22 is a cigarette that contains our proprietary VLN tobacco. We believe X-22 will be well-positioned as a smoking cessation product by motivating and encouraging more smokers to attempt to quit smoking, although there is no assurance that these results will occur.

The 2009 Family Smoking Prevention and Tobacco Control Act (“Tobacco Control Act”) granted the FDA authority over the regulation of all tobacco products. While it prohibits the FDA from banning cigarettes outright, it allows the FDA to require the reduction of nicotine or any other compound in tobacco and cigarette smoke. The Tobacco Control Act also banned all sales in the U.S. of cigarettes with flavored tobacco (other than menthol). As of June 2010, all cigarette companies were required to cease the use of the terms “low tar,” “light” and “ultra light” in describing cigarettes sold in the U.S. Besides numerous other regulations, including certain marketing restrictions, for the first time in history, a U.S. regulatory agency will scientifically evaluate cigarettes that may pose lower health risks as compared to conventional cigarettes.

The Tobacco Control Act establishes procedures for the FDA to regulate the labeling and marketing of modified risk tobacco products, which includes cigarettes that (i) reduce exposure to tobacco smoke toxins and/or (ii) pose lower health risks, as compared to conventional cigarettes (“Modified Risk Cigarettes”). The Tobacco Control Act requires the FDA to issue specific regulations and guidance regarding applications that must be submitted to the FDA for the authorization to label and market Modified Risk Cigarettes. The FDA has yet to release its regulations regarding modified risk tobacco products. However, based in part on the timelines contained in the Tobacco Control Act, we expect the FDA to issue such regulations and guidance within the next year.

2

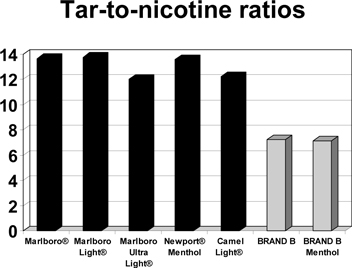

Although we believe that two of our cigarette products, which we refer to as BRAND A and BRAND B, will qualify as Modified Risk Cigarettes, further research and exposure studies are needed for the FDA to make this determination. Compared to commercial cigarettes, we believe the tobacco in BRAND A has approximately 95% less nicotine than tobacco in cigarettes previously marketed as “light” cigarettes, and BRAND B’s smoke contains the lowest amount of “tar” per milligram of nicotine. There is no guarantee that X-22 will obtain the necessary approvals from the FDA to be marketed as a smoking cessation aid, and there is no guarantee that Brand A or Brand B will obtain the necessary authorizations from the FDA to be classified as Modified Risk Cigarettes. We have not attempted to obtain approval of X-22 or authorization of our Modified Risk Cigarettes outside of the United States, and there is no guarantee that we will be able to gain such approval or such authorization for these products outside of the United States (for those countries that require such regulatory authorizations).

The net proceeds of the Private Placement Offering will not be sufficient to enable us to complete the FDA approval process for X-22 and/or the FDA authorization process for our Modified Risk Cigarettes. We will require additional capital beyond the net proceeds of the Private Placement Offering to complete these activities. We may not be able to obtain additional debt or equity financing on favorable terms, if at all. If we raise additional funds through the issuance of equity securities, our stockholders may experience substantial dilution, or the equity securities may have rights, preferences or privileges senior to those of existing stockholders. If we raise additional funds through debt financings, these financings may involve significant cash payment obligations and covenants that restrict our ability to operate our business and make distributions to our stockholders. We also could elect to seek funds through arrangements with collaborators. To the extent that we raise additional funds through collaboration and licensing arrangements, it may be necessary to relinquish some rights to our technologies or our potential products or grant licenses on terms that are not favorable to us. We currently plan to seek to raise approximately $15 million in the fourth quarter of 2011 through the sale of our common stock and/or securities convertible into common stock to fund Phase III trials, modified risk exposure studies and our general working capital requirements.

Within our two product categories, the Tobacco Control Act offers us the following specific advantages:

Smoking Cessation Aids

FDA approval must be obtained, as has been the case for decades, before a product can be marketed for quitting smoking. The Tobacco Control Act provides that products for quitting smoking or smoking cessation be considered for “Fast Track” designation by the FDA. The “Fast Track” programs of the FDA are intended to facilitate development and expedite review of drugs to treat serious and life-threatening conditions so that an approved product can reach the market expeditiously. We believe that X-22 will qualify for “Fast Track” designation by the FDA. However, there is no guarantee that X-22 will qualify for “Fast Track” designation at the FDA.

Modified Risk Cigarettes

We intend to seek FDA authorization to market BRAND A and BRAND B as Modified Risk Cigarettes. We believe that BRAND A and BRAND B will achieve significant market share in the global cigarette market among smokers who will not quit but are interested in reducing the harmful effects of smoking. We believe this new regulatory environment represents a paradigm shift for the tobacco industry. The Tobacco Control Act allows the FDA to mandate the use of reduced-risk technologies across all conventional tobacco products or cigarettes. We expect this to create opportunities for us to license our proprietary technology and/or tobaccos to larger competitors. There is no guarantee that Brand A or Brand B will obtain the necessary authorizations from the FDA to be classified as Modified Risk Cigarettes. Further research and exposure studies are needed for the FDA to make this determination

3

RED SUN and MAGIC Cigarettes

Our subsidiary, Goodrich Tobacco Company, LLC (f/k/a Xodus, LLC), has introduced two super-premium priced cigarette brands, RED SUN and MAGIC, into the U.S. market in the first quarter of 2011. Super-premium priced means brands that are priced higher than national premium brands such as Marlboro® Newport® and Camel®. Both brands are available in regular and menthol and all four brand styles are king size, packaged in hinge-lid hard packs. We intend to focus our marketing efforts on tobacconists, smoke shops and tobacco outlets. We believe that the ban in 2009 by the FDA of all flavored cigarettes (with the exception of menthol) has resulted in a product void in these tobacco channels. According to Tobacco Merchants Association, flavored cigarettes (besides menthol), mainly clove cigarettes, were approximately 1% of the U.S. cigarette market (3.25 billion cigarettes equating to $0.7 billion) before the ban on such cigarettes in June 2009, when the Tobacco Control Act became law. Since these were super-premium priced products (priced up to 60% higher than the best selling national brands), they were mainly distributed in specialty tobacco channels such as tobacconists, smoke shops and tobacco outlets, which collectively are about 10,000 stores in the U.S., a small fraction of the hundreds of thousands of stores that sell cigarettes in the U.S.

Certain wholesalers and retailers are now seeking other specialty cigarettes to replace the banned flavored cigarettes. We believe that certain U.S. cigarette wholesalers and retailers will, among other reasons, purchase RED SUN and MAGIC to replace their lost sales of flavored cigarettes as well as potential lost sales of “light” and “ultra light” cigarettes, since as of June 2010, all cigarette companies were required to cease the use of the terms “low tar,” “light” and “ultra light.”

Government Research Cigarettes

The National Institute on Drug Abuse (“NIDA”), a component of the National Institutes of Health (“NIH”), provides the scientific community with controlled and uncontrolled research chemicals and drug compounds in its Drug Supply Program. In 2009, NIDA included an option to develop and produce research cigarettes with ten different levels of nicotine, including a minimal (placebo) level, or Research Cigarette Option, in its request for proposals for a five-year contract for Preparation and Distribution of Research and Drug Products. We have agreed, as a subcontractor to RTI International (“RTI”) pursuant to RTI’s contract with NIDA for the Research Cigarette Option, to supply modified nicotine cigarettes to NIDA. In August 2010, we met with officials from NIDA, FDA, RTI, the National Cancer Institute and the Centers for Disease Control and Prevention to finalize certain aspects of the design of these research cigarettes. These research cigarettes are distributed under the mark SPECTRUM.

In 2010, we received our first purchase order of $152,660 which included a design phase fee of $40,604. In March 2011, the Company received a revised purchase order and authorization to bill $112,000 for manufacture planning and material procurement for 9 million cigarettes from RTI. Payment was received on May 2, 2011. The Company received an additional purchase order from RTI for approximately $680,000 in May 2011 to ship the 9 million research cigarettes. Approximately 4 million cigarettes out of the 9 million were shipped to and received by RTI on July 6, 2011. We believe that the revenue from the sale of SPECTRUM, plus direct orders of other cigarettes from researchers, will be approximately $825,000 in 2011 and $3 million over the next 5 years. As a subcontractor, we do not have a formal contractual arrangement at this time with RTI to purchase additional SPECTRUM cigarettes or with other researchers, and there is no guarantee that we will receive future orders from RTI or other researchers.

Technology Platform and Intellectual Property

Our proprietary technology enables us to decrease or increase the level of nicotine in tobacco plants by decreasing or increasing the expression of gene(s) responsible for nicotine production in the tobacco plant using genetic engineering. For example, we believe that one of our proprietary tobacco varieties contains the lowest nicotine content of any tobacco ever commercialized, with approximately 95% less nicotine than tobacco in leading “light” cigarette brands. We believe that, as opposed to extracting nicotine from tobacco, this proprietary tobacco grows with virtually no nicotine without adversely affecting the other leaf constituents important to a cigarette’s characteristics, including taste and aroma. Our genetic engineering processes suppress an enzyme involved in synthesis of a nicotine precursor in the roots of the tobacco plant. Roots of the tobacco plant produce nicotine which is transported to the rest of the plant. We believe levels of certain compounds in the tobacco leaf of our genetically engineered variety are not substantially different than that of conventional tobacco, except for the large reduction in nicotine and related compounds. We believe, based on analyses of a range of chemical constituents in smoke from cigarettes made from VLN tobacco, that the smoke is highly similar to smoke from conventional cigarettes, except for the large reduction in nicotine and related compounds. Furthermore, subjective ratings of our products’ smoking characteristics approximate those of conventional cigarettes. Therefore, we believe the taste and aroma characteristics are within the range of typical cigarettes.

4

Our proprietary technology is covered by 12 patent families consisting of 98 issued patents in 79 countries, 8 of which we own and 90 of which are exclusively licensed to us, and approximately 45 pending patent applications, of which we own 29 pending patent applications and have an exclusive license to 16 pending patent applications. A “patent family” is a set of patents granted in various countries to protect a single invention. Our patent coverage in the United States, which we believe is the most valuable smoking cessation market and cigarette market, consists of 14 issued patents and 7 pending applications. In the U.S., patents that currently cover our products expire in 2019 through 2022. Also in the U.S., patent applications that we expect will cover our products would, if patents are granted in connection with such applications, yield patents that expire in 2024 through 2028. However, there is no guarantee that patents will be granted in response to such patent applications and therefore cover our products. Our two worldwide exclusive licenses, one from North Carolina State University (“NCSU”) and the other from National Research Council of Canada, Plant Biotechnology Institute in Saskatoon, Canada (“NRC”), each involve multiple patent families, patent applications and patents. The exclusive rights under each of these two license agreements expire on the date on which the last patent covered by the subject license expires in the country or countries where such patents are in effect, which is expected to be from 2022 through 2028, respectively. In China, which we consider the world’s largest cigarette market, we own or have the exclusive license to use 5 issued patents and 3 pending patent applications. We also have the exclusive right to license and sublicense these patent rights. The patents owned by or exclusively licensed to us are issued in countries where we believe approximately 75% of the world’s smokers reside. As a result of these patents, patent applications and licenses, we believe we have exclusive worldwide rights to all uses of the following genes responsible for nicotine content in tobacco plants: QPT, A622, NBB1, MPO and genes for several transcription factors. Similarly, we believe we have exclusive rights to plants with altered nicotine content produced from modifying expression of these genes and tobacco products produced from these plants.

We own various registered trademarks in the United States. We also have exclusive rights to plant variety protection, or PVP, certificates in the United States (issued by the U.S. Department of Agriculture) and Canada. A PVP certificate prevents anyone other than the owner/licensee from planting a plant variety for 20 years in the U.S. or 18 years in Canada. The protections of PVP are independent of, and in addition to, patent protection.

While we have performed searches for third-party intellectual property rights that may affect our ability to commercialize our potential products, we have not performed searches for those third-party intellectual property rights that may raise freedom-to-operate issues, nor have we obtained legal opinions regarding the commercialization of our potential products. Therefore, there may be patents of which we are unaware that may affect our ability to commercialize our potential products.

Recent Developments

On January 25, 2011, we entered into an Agreement and Plan of Merger and Reorganization with 22nd Century Acquisition Subsidiary, our wholly-owned Delaware limited liability company subsidiary, or Acquisition Sub, and 22nd Century. On that date, Acquisition Sub merged with and into 22nd Century, and 22nd Century, as the surviving entity, became our wholly-owned subsidiary. In this prospectus, we refer to the merger and reorganization transactions consummated on January 25, 2011 as the “Merger.”

Prior to the consummation of the Merger, 22nd Century completed a private placement of units of its securities, or “Units”, with each Unit consisting of one limited liability company membership interest of 22nd Century and a five-year warrant to purchase one half of one (1/2) limited liability company membership interest of 22nd Century at an exercise price of $1.50 per whole limited liability company membership interest of 22nd Century. We refer to the offering in this prospectus as the “Private Placement Offering.” 22nd Century also issued warrants to purchase its limited liability company membership interests to a financial advisor for financial advisory services rendered in connection with the Private Placement Offering.

Prior to the closing of the Merger, we transferred all of our pre-Merger operating assets and liabilities pursuant to the terms of a split-off agreement (the “Split-Off Agreement”), to our wholly-owned subsidiary, Touchstone Split Corp., a Delaware corporation (the “Split-Off Subsidiary”). Thereafter, pursuant to the Split-Off Agreement, we transferred all of the outstanding capital stock of the Split-Off Subsidiary to our then-sole director in exchange for $1.00, such consideration being deemed to be adequate by our pre-Merger Board of Directors (the “Board”).

5

At the closing of the Merger, each limited liability company membership interest of 22nd Century issued and outstanding immediately prior to the closing of the Merger was exchanged for one share of our common stock, and each warrant to purchase limited liability company membership interests of 22nd Century was exchanged for one warrant of like tenor and term to purchase shares of our common stock. An aggregate of 21,434,446 shares of common stock and warrants to purchase an aggregate of 8,151,980 shares of common stock were issued to the holders of Units of 22nd Century, and immediately following the closing of the Merger an aggregate of 26,759,646 shares of common stock were issued and outstanding and an aggregate of 8,651,980 shares are common stock were reserved for issuance pursuant to the exercise of warrants to purchase shares of common stock.

In connection with the Merger, our Board was expanded to five members. The sole officer and sole member of the Board prior to the closing of the Merger, David Rector, resigned as an officer and a director after the closing of the Merger. The current members of our Board are Joseph Pandolfino, Henry Sicignano III, Joseph Alexander Dunn, Ph.D., James W. Cornell and Steven Katz. Messrs. Cornell and Katz and Dr. Dunn qualify as “independent” directors under the applicable definition of the NASDAQ Global Market (“NASDAQ”) listing standards, so that a majority of the Company’s Board members are “independent.” Although the Company’s securities are not currently traded on the NASDAQ or any other exchange, which would require that the Company’s Board include a majority of directors that are “independent,” the Company has elected to do so anyhow as part of its corporate governance policies. Our current executive officers are Joseph Pandolfino, Chief Executive Officer, Henry Sicignano III, President and Secretary, Michael R. Moynihan, Ph.D., Vice President of Research & Development, and C. Anthony Rider, Chief Financial Officer and Treasurer. Each of Messrs. Pandolfino, Sicignano and Rider was an executive officer of 22nd Century prior to the closing of the Merger.

Following the closing of the Merger, there were 26,759,646 shares of Common Stock issued and outstanding. Approximately 59.8% of such issued and outstanding shares were held by individuals and entities that were holders of limited liability company membership interests of 22nd Century prior to consummation of the Private Placement Offering, approximately 20.3% were held by the investors in the Private Placement Offering and approximately 19.9% were held by the pre-Merger stockholders of Parent.

On April 1, 2011, under our 2010 equity incentive plan (“EIP”), the Board granted an aggregate of 1,150,000 shares of our common stock to our officers and directors and options to purchase an aggregate of 35,000 shares of our common stock to our employees.

The Merger is being accounted for as a reverse acquisition and recapitalization of 22nd Century for financial accounting purposes whereby 22nd Century is deemed to be the acquirer for accounting and financial reporting purposes. Consequently, the assets and liabilities and the historical operations that will be reflected in the financial statements prior to the Merger will be those of 22nd Century and will be recorded at the historical cost basis of 22nd Century, and the consolidated financial statements after completion of the Merger will include the assets and liabilities of the Company and 22nd Century, historical operations of 22nd Century and operations of the Company beginning on the closing date of the Merger. As a result, all the historical financial information reported in this prospectus is the financial information of 22nd Century.

We have entered into an agreement with a federally licensed cigarette manufacture to produce RED SUN, MAGIC, SPECTRUM, BRAND A, BRAND B and the clinical trial cigarettes for X-22.

We were incorporated under the laws of the State of Nevada on September 12, 2005 under the name Touchstone Mining Limited. We changed our name to 22nd Century Group, Inc. on November 23, 2010 in anticipation of the Merger with 22nd Century. Our principal executive offices are located at 8201 Main Street, Suite 6, Williamsville, New York 14221. The telephone number at our principal executive offices is (716) 270-1523. Our website address is www.xxiicentury.com. Information contained on our website is not deemed part of this prospectus.

6

|

Common stock currently outstanding

|

27,909,646 shares (1) (2)

|

|

Common stock offered by us

|

None

|

|

Common stock offered by the selling stockholders

|

5,434,446 shares

|

|

Use of Proceeds

|

We will not receive any proceeds from the sale of common stock offered by this prospectus.

|

|

Risk Factors

|

See “Risk Factors” and other information included in this prospectus for a discussion of factors that you should consider before deciding to invest in shares of our common stock.

|

|

OTC Bulletin Board Symbol

|

XXII.OB

|

|

(1)

|

As of July 15, 2011

|

|

(2)

|

Assumes that all other outstanding warrants and options are not exercised

|

7

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. This prospectus includes statements regarding our plans, goals, strategies, intentions, beliefs or current expectations. These statements are expressed in good faith and based upon a reasonable basis when made, but there can be no assurance that these expectations will be achieved or accomplished. These forward looking statements can be identified by the use of terms and phrases such as “believe,” “plan,” “intend,” “anticipate,” “target,” “estimate,” “expect,” and the like, and/or future-tense or conditional constructions “may,” “could,” “should,” etc. Items contemplating or making assumptions about, actual or potential future sales, market size, collaborations, and trends or operating results also constitute forward-looking statements.

These forward-looking statements are only predictions, are uncertain and involve substantial known and unknown risks, uncertainties and other factors which may cause our (or our industry’s) actual results, levels of activity or performance to be materially different from any future results, levels of activity or performance expressed or implied by these forward-looking statements. The “Risk Factors” section of this prospectus sets forth detailed risks, uncertainties and cautionary statements regarding our business and these forward-looking statements.

Since our common stock is considered a “penny stock,” we are ineligible to rely on the safe harbor for forward-looking statements provided in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act.

We cannot guarantee future results, levels of activity or performance. You should not place undue reliance on these forward-looking statements, which speak only as of the date that they were made. These cautionary statements should be considered with any written or oral forward-looking statements that we may issue in the future. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to reflect actual results, later events or circumstances or to reflect the occurrence of unanticipated events. You should carefully review and consider the various disclosures made by us in our reports filed with the Securities and Exchange Commission which attempt to advise interested parties of the risks and factors that may affect our business, financial condition, results of operation and cash flows. If one or more of these risks or uncertainties materialize, or if the underlying assumptions prove incorrect, our actual results may vary materially from those expected or projected.

8

RISK FACTORS

An investment in shares of our common stock is highly speculative and involves a high degree of risk. We face a variety of risks that may affect our operations or financial results and many of those risks are driven by factors that we cannot control or predict. The following discussion addresses those risks that management believes could materially adversely affect our business, financial condition and results of operation. Only those investors who can bear the risk of loss of their entire investment should participate in this offering. Prospective investors should carefully consider the following risk factors in evaluating an investment in our common stock.

Risks Related to Our Business and Operations

We may not be able to continue as a going concern.

Recurring losses from operations, our limited working capital of approximately $503,000 as of March 31, 2011 (approximately $4.1 million at December 31, 2010), shareholders’ deficit of $1.8 million as of March 31, 2011 ($2.1 million at December 31, 2010) and the uncertainty of obtaining additional financing on a timely basis, raise doubt about our ability to continue as a going concern. The report of our independent registered public accounting firm on our financial statements for the year ended December 31, 2010, includes an emphasis of a matter paragraph expressing substantial doubt whether we can continue as a going concern. Even in light of our receipt of the proceeds of the Private Placement Offering, we cannot guarantee our ability to continue as a going concern.

We have had a history of losses, and we may be unable to achieve or sustain profitability.

We experienced net losses of approximately $652,000 for the first three months of 2011 and $1.4 million and $1.2 million during the years ended December 31, 2010 and 2009, respectively. We expect to continue to incur net losses and negative operating cash flows in the foreseeable future and cannot be certain that we will ever achieve profitability. Since 2007, we have received only limited licensing revenue from a former licensee and have achieved limited revenue of product sales. We will need to spend significant capital to fulfill planned operating goals and conduct clinical studies, achieve regulatory approvals and, subject to such approvals, successfully produce products for commercialization. In addition, as a public company, we will incur significant legal, accounting and other expenses that we did not incur as a private company.

We have a history of negative cash flow, and our ability to generate positive cash flow is uncertain.

We had negative cash flow before financing activities of approximately $2,177,000 during the first three months of 2011 and $1,018,000 and $172,000 during the years ended December 31, 2010 and 2009, respectively. We anticipate that we will continue to have negative cash flow for the foreseeable future as we will continue to incur increased expenses from seeking regulatory approvals, including clinical trials and exposure studies, sales and marketing, and general and administrative expenses, as well as to purchase inventory. Our business will also require significant amounts of working capital to support our growth. Therefore, we may need to raise additional investment capital to achieve growth, and we may not achieve sufficient revenue growth to generate positive future cash flow. An inability to generate positive cash flow for the foreseeable future or raise additional capital on reasonable terms may decrease our long-term viability.

Our limited operating history makes it difficult to evaluate our current business and future prospects.

We have been in existence since 1998, but our activities have been limited primarily to licensing and funding research and development activities. Our limited operating history may make it difficult to evaluate our current business and our future prospects. We have encountered and will continue to encounter risks and difficulties frequently experienced by growing companies in rapidly changing industries, including increasing expenses as we continue to grow our business. If we do not manage these risks successfully, our business will be harmed.

9

We have no experience in managing growth. If we fail to manage our growth effectively, we may be unable to execute our business plan or address competitive challenges adequately.

We currently have six employees. Any growth in our business will place a significant strain on our managerial, administrative, operational, financial, information technology and other resources. We intend to further expand our overall business, customer base, employees and operations, which will require substantial management effort and significant additional investment in our infrastructure. We will be required to continue to improve our operational, financial and management controls and our reporting procedures and we may not be able to do so effectively. As such, we may be unable to manage our growth effectively.

Our working capital requirements involve estimates based on demand expectations and may decrease or increase beyond those currently anticipated, which could harm our operating results and financial condition.

We have no experience in selling smoking cessation products or Modified Risk Cigarettes on a commercial basis. As a result, we intend to base our funding and inventory decisions on estimates of future demand. If demand for our products does not increase as quickly as we have estimated or drops off sharply, our inventory and expenses could rise, and our business and operating results could suffer. Alternatively, if we experience sales in excess of our estimates, our working capital needs may be higher than those currently anticipated. Our ability to meet any demand for our products may depend on our ability to arrange for additional financing for any ongoing working capital shortages, since it is likely that cash flow from sales will lag behind our investment requirements.

The net proceeds of the Private Placement Offering will not be sufficient to enable us to complete the FDA approval process for our X-22 smoking cessation product and the FDA authorization process for our Modified Risk Cigarettes.

We will require additional capital in the future beyond the net proceeds of the Private Placement Offering to complete the FDA approval process for our X-22 smoking cessation product and the FDA authorization process for our Modified Risk Cigarettes. In particular, we currently plan to seek to raise approximately $15 million in the fourth quarter of 2011 through the sale of our common stock and/or securities convertible into common stock to fund Phase III trials, modified risk exposure studies and our general working capital requirements. However, we may not be able to obtain additional debt or equity financing on favorable terms, if at all. We believe the cost of the Phase II-B trial is approximately $1.1 million, of which we have paid approximately 45 percent as of July 15, 2011. We estimate the cost of completing the Phase III trials to be approximately $10 million. We estimate that the cost of completing the FDA authorization process for each of our potential Modified Risk Cigarettes is estimated to be at least $1 million. However, this depends on the regulations expected to be released by FDA within the next year. If we raise additional funds through the issuance of equity securities as we currently plan to seek to do, our stockholders may experience substantial dilution, or the equity securities may have rights, preferences or privileges senior to those of existing stockholders. If we raise additional funds through debt financings, these financings may involve significant cash payment obligations and covenants that restrict our ability to operate our business and make distributions to our stockholders. We also could elect to seek funds through arrangements with collaborators. To the extent that we raise additional funds through collaboration and licensing arrangements, it may be necessary to relinquish some rights to our technologies or our potential products or grant licenses on terms that are not favorable to us.

Due to market conditions and the status of our product development activities, additional funding may not be available to us on acceptable terms, or at all. Having insufficient funds may require us to delay, scale back or eliminate some or all of our clinical programs or to relinquish greater rights to potential products at an earlier stage of development or on less favorable terms than we would otherwise choose. Our failure to raise additional financing would adversely affect our ability to maintain, develop, enhance or grow our business, take advantage of future opportunities or respond to competitive pressures. If we cannot raise additional capital on acceptable terms, we may not be able to, among other things:

|

|

·

|

continue or complete clinical trials of our X-22 smoking cessation aid;

|

|

|

·

|

continue or complete the steps necessary to seek FDA authorization of our Modified Risk Cigarettes;

|

|

|

·

|

develop or enhance our potential products or introduce new products;

|

|

|

·

|

expand our development, sales and marketing and general and administrative activities;

|

|

|

·

|

attract tobacco growers, customers or manufacturing and distribution partners;

|

|

|

·

|

acquire complementary technologies, products or businesses;

|

|

|

·

|

expand our operations in the United States or internationally;

|

|

|

·

|

hire, train and retain employees; or

|

10

|

|

·

|

respond to competitive pressures or unanticipated working capital requirements.

|

Continued instability in the credit and financial market conditions may negatively impact our business, results of operations, and financial condition.

Financial markets in the United States, Canada, Europe and Asia continue to experience disruption, including, among other things, significant volatility in security prices, declining valuations of certain investments, severely diminished liquidity and credit availability. Business activity across a wide range of industries and regions continues to be reduced and local governments and many businesses are still in serious difficulty due to the lack of consumer spending and the lack of liquidity in the credit markets. As a clinical-stage biotechnology company, we rely on third parties for several important aspects of our business, including the supply of tobacco, manufacturing and distribution of our products, development of our potential products, and conduct of our clinical trials. Such third parties may be unable to satisfy their commitments to us due to tightening of global credit from time to time, which would adversely affect our business. The continued instability in the credit and financial market conditions may also negatively impact our ability to access capital and credit markets and our ability to manage our cash balance. While we are unable to predict the continued duration and severity of the adverse conditions in the United States and other countries, any of the circumstances mentioned above could adversely affect our business, financial condition, operating results and cash flow or cash position.

We will depend on the success of our X-22 smoking cessation aid and our Modified Risk Cigarettes and we may not be able to successfully commercialize these potential products.

Our goal is to develop products whose potential for risk reduction can be substantiated and that meet adult smokers’ taste expectations. We may not succeed in these efforts. If we do not succeed, but one or more of our competitors do, we may be at a competitive disadvantage. The success of our business depends in part on our ability to obtain FDA approval for our X-22 smoking cessation aid and FDA authorization under the Tobacco Control Act to market our BRAND A and BRAND B cigarettes as Modified Risk Cigarettes. The FDA has yet to release its regulations regarding modified risk tobacco products. We have not obtained approval to market X-22 in any jurisdiction, nor have we obtained authorization to market our BRAND A or BRAND B cigarettes as Modified Risk Cigarettes, and we cannot predict whether we will be able to obtain such approval or authorizations, or if regulators will permit the marketing of tobacco products with claims of reduced risk to consumers. Any failure to obtain such approval or authorizations would significantly undermine the commercial viability of the applicable product. If we fail to successfully commercialize these products in the United States, we may be unable to generate sufficient revenue to sustain and grow our business, and our business, financial condition, results of operations and cash flows will be adversely affected.

We will depend on third parties to manufacture our products.

We currently do not intend to manufacture any of our products and depend on contract manufacturers to produce our products according to our specifications, in sufficient quantities, on time, in compliance with appropriate regulatory standards and at competitive prices. We currently do not have an arrangement with any contract manufacturer to produce our final version of X-22 smoking cessation aid once it is approved by the FDA.

Manufacturers supplying our potential products must comply with FDA regulations which require, among other things, compliance with the FDA’s evolving regulations on Current Good Manufacturing Practices (“cGMP(s)”), which are enforced by the FDA through its facilities inspection program. The manufacture of products at any facility will be subject to strict quality control, testing and record keeping requirements, and continuing obligations regarding the submission of safety reports and other post-market information. We cannot guarantee that our current contract manufacturer will pass FDA and/or similar inspections in foreign countries to produce the final version of our X-22 smoking cessation aid, or that future changes to cGMP manufacturing standards will not also affect the manufactures of our other products. Therefore, we may have to build our own manufacturing facility which would require additional capital.

11

We will mainly depend on third parties to market, sell and distribute our products, and we currently have no commercial arrangements for the marketing, sale or distribution of our X-22 smoking cessation aid.

We expect to depend on third parties to a great extent to market, sell and distribute our products and we currently have no arrangements with third parties in place to provide such services for our X-22 smoking cessation aid. We cannot be sure that we will be able to enter into such arrangements on acceptable terms, or at all.

If we are unable to enter into marketing, sales and distribution arrangements with third parties for our X-22 smoking cessation aid, we would need to incur significant sales, marketing and distribution expenses in connection with the commercialization of X-22 and any future potential products. We do not currently have a dedicated sales force, and we have no experience in the sales, marketing and distribution of pharmaceutical products. Developing a sales force is expensive and time-consuming, and we may not be able to develop this capacity. If we are unable to establish adequate sales, marketing and distribution capabilities, independently or with others, we may not be able to generate significant revenue and may not become profitable.

If our X-22 smoking cessation aid does not gain market acceptance among physicians, patients, third-party payers and the medical community, we may be unable to generate significant revenue.

Our X-22 smoking cessation aid may not achieve market acceptance among physicians, patients, third-party payers and others in the medical community. If we receive FDA approval for the marketing of X-22 as a smoking cessation aid in the U.S., the degree of market acceptance could depend upon a number of factors, including:

|

|

·

|

limitations on the indications for use for which X-22 may be marketed ;

|

|

|

·

|

the establishment and demonstration in the medical community of the clinical efficacy and safety of our potential products and their potential advantages over existing products;

|

|

|

·

|

the prevalence and severity of any side effects;

|

|

|

·

|

the strength of marketing and distribution support; and/or

|

|

|

·

|

sufficient third-party coverage or reimbursement.

|

The market may not accept our X-22 smoking cessation aid, based on any number of the above factors. Even if the FDA approves the marketing of X-22 as a smoking cessation aid, there are other FDA-approved products available and there will also be future competitive products which directly compete with X-22. The market may choose to continue utilizing such existing or future competitive products for any number of reasons, including familiarity with or pricing of such products. The failure of any of our potential products to gain market acceptance could impair our ability to generate revenue, which could have a material adverse effect on our future business, financial condition, results of operations and cash flows.

Our principal competitors in the smoking cessation market have, and any future competitors may have, greater financial and marketing resources than we do, and they may therefore develop products or other technologies similar or superior to ours or otherwise compete more successfully than we do.

We have no experience in selling smoking cessation products. Competition in the smoking cessation aid products industry is intense, and we may not be able to successfully compete in the market. In the market for FDA-approved smoking cessation aids, our principal competitors include Pfizer Inc., GlaxoSmithKline PLC, Perrigo Company, Novartis International AG, and Niconovum AB, a subsidiary of Reynolds American Inc. The industry consists of major domestic and international companies, most of which have existing relationships in the markets into which we plan to sell, as well as financial, technical, marketing, sales, manufacturing, scaling capacity, distribution and other resources and name recognition substantially greater than ours. In addition, we expect new competitors will enter the markets for our products in the future. Potential customers may choose to do business with our more established competitors, because of their perception that our competitors are more stable, are more likely to complete various projects, can scale operations more quickly, have greater manufacturing capacity, are more likely to continue as a going concern and lend greater credibility to any joint venture. If we are unable to compete successfully against manufacturers of other smoking cessation products, our business could suffer, and we could lose or be unable to obtain market share.

12

We face intense competition in the market for our RED SUN and MAGIC cigarettes and our BRAND A and BRAND B cigarettes, and our failure to compete effectively could have a material adverse effect on our profitability and results of operations.

Cigarette companies compete primarily on the basis of product quality, brand recognition, brand loyalty, taste, innovation, packaging, service, marketing, advertising, retail shelf space and price. We are subject to highly competitive conditions in all aspects of our business and we may not be able to effectively market and sell our RED SUN and MAGIC cigarettes or other cigarettes we may introduce to the market, even if we are able to market our BRAND A and BRAND B cigarettes as Modified Risk Cigarettes. The competitive environment and our competitive position can be significantly influenced by weak economic conditions, erosion of consumer confidence, competitors’ introduction of low-price products or innovative products, higher cigarette taxes, higher absolute prices and larger gaps between price categories, and product regulation that diminishes the ability to differentiate tobacco products. Domestic competitors include Philip Morris USA, Reynolds American Inc., Lorillard Inc., Commonwealth Brands, Inc., Liggett Group LLC, Vector Tobacco Inc. and Star Scientific Inc. International competitors include Philip Morris International, British American Tobacco, Japan Tobacco Inc. and regional and local tobacco companies; and, in some instances, government-owned tobacco enterprises, principally in China, Egypt, Thailand, Taiwan, Vietnam and Algeria.

Our MAGIC cigarettes and our BRAND A cigarettes may have relatively low sales volume in the future.

A third-party, former licensee marketed cigarettes containing our proprietary VLN tobacco in the past on a limited basis that yielded low sales volumes. Our marketing and sales of our MAGIC cigarettes and BRAND A cigarettes which contain our proprietary VLN tobacco may also result in low sales volume.

Our competitors may develop products that are less expensive, safer or more effective, which may diminish or eliminate the commercial success of any potential product that we may commercialize.

If our competitors market products that are less expensive, safer or more effective than our potential products, or that reach the market before our potential products, we may not achieve commercial success. The market may choose to continue utilizing existing products for any number of reasons, including familiarity with or pricing of these existing products. The failure of our X-22 smoking cessation aid or our cigarette brands to compete with products marketed by our competitors would impair our ability to generate revenue, which would have a material adverse effect on our future business, financial condition, results of operations and cash flows. Our competitors may:

|

|

·

|

develop and market products that are less expensive or more effective than our proposed products;

|

|

|

·

|

commercialize competing products before we or our partners can launch our proposed products;

|

|

|

·

|

operate larger research and development programs or have substantially greater financial resources than we do;

|

|

|

·

|

initiate or withstand substantial price competition more successfully than we can;

|

|

|

·

|

have greater success in recruiting skilled technical and scientific workers from the limited pool of available talent;

|

|

|

·

|

more effectively negotiate third-party licenses and strategic relationships; and

|

|

|

·

|

take advantage of acquisition or other opportunities more readily than we can.

|

In addition, if we fail to stay at the forefront of technological change, we may be unable to compete effectively. Our competitors may render our technologies obsolete by advances in existing technological approaches or the development of new or different approaches, potentially eliminating the advantages that we believe we derive from our research approach and proprietary technologies.

13

Government mandated prices, production control programs, shifts in crops driven by economic conditions and adverse weather patterns may increase the cost or reduce the quality of the tobacco and other agricultural products used to manufacture our products.

We depend upon independent tobacco producers to grow our specialty proprietary tobaccos with specific nicotine contents for our products. As with other agricultural commodities, the price of tobacco leaf can be influenced by imbalances in supply and demand, and crop quality can be influenced by variations in weather patterns, diseases and pests. We must also compete with other tobacco companies for contract production with independent tobacco growers. Tobacco production in certain countries is subject to a variety of controls, including government mandated prices and production control programs. Changes in the patterns of demand for agricultural products could cause farmers to plant less tobacco. Any significant change in tobacco leaf prices, quality and quantity could affect our profitability and our business.

Our future success depends on our ability to retain key personnel.

Our success will depend to a significant extent on the continued services of our senior management team, and in particular Joseph Pandolfino, our Chief Executive Officer, Henry Sicignano III, our President, and Michael Moynihan, Ph.D., our Vice President of R&D. The loss or unavailability of any of these individuals may significantly delay or prevent the development of our potential products and other business objectives by diverting management’s attention to transition matters. Identification of suitable management replacements, if any, could have a material adverse effect on our business, operating results, cash flows and financial condition. While each of these individuals is party to employment agreements with us, they could terminate their relationships with us at any time, and we may be unable to enforce any applicable employment or non-compete agreements.

We also rely on consultants and advisors to assist us in formulating our research and development, manufacturing, distribution, marketing and sales strategies. All of our consultants and advisors are either self-employed or employed by other organizations, and they may have conflicts of interest or other commitments, such as consulting or advisory contracts with other organizations, that may affect their ability to contribute to us.

Product liability claims, product recalls or other claims could cause us to incur losses or damage our reputation.

The risk of product liability claims or product recalls, and associated adverse publicity, is inherent in the development, manufacturing, marketing and sale of cigarettes and smoking cessation products. We do not currently have product liability insurance for our products or our potential products and do not expect to be able to obtain product liability insurance at reasonable commercial rates for these products. Any product recall or lawsuit seeking significant monetary damages may have a material adverse affect on our business and financial condition. A successful product liability claim against us could require us to pay a substantial monetary award. We cannot assure you that such claims will not be made in the future.

We may be unable to complete or integrate acquisitions effectively, which may adversely affect our growth, profitability and results of operations.

We may pursue acquisitions as part of our business strategy. However, we cannot be certain that we will be able to identify attractive acquisition targets, obtain financing for acquisitions on satisfactory terms or successfully acquire identified targets. Additionally, we may not be successful in integrating acquired businesses into our existing operations or achieving projected synergies. Competition for acquisition opportunities in the industries in which we operate may rise, thereby increasing our costs of making acquisitions or causing us to refrain from making further acquisitions. These and other acquisition-related factors could negatively and adversely impact our growth, profitability and results of operations.

Risks Related to Regulatory Approvals and Insurance Reimbursement

If we fail to obtain FDA and foreign regulatory approvals of X-22 as a smoking cessation aid and FDA authorization to market BRAND A and BRAND B as Modified Risk Cigarettes, we will be unable to commercialize these potential products in and outside the U.S., other than the sale of our BRAND A and BRAND B cigarettes as conventional cigarettes.

There can be no assurance that our X-22 smoking cessation aid will be approved by the FDA, European Medicines Agency (“EMA”), or any other governmental body. In addition, there can be no assurance that all necessary approvals will be granted for our potential products or that review or actions will not involve delays caused by requests for additional information or testing that could adversely affect the time to market for and sale of our potential products. Even if X-22 is approved by the FDA, the FDA may require the product to only be prescribed to patients who have already failed to quit smoking with another approved therapy. Further, failure to comply with applicable regulatory requirements can, among other things, result in the suspension of regulatory approval as well as possible civil and criminal sanctions.

14

The development, testing, manufacturing and marketing of our potential products are subject to extensive regulation by governmental authorities in the United States and throughout the world. In particular, the process of obtaining approvals by the FDA, EMA and other international FDA-equivalent agencies in targeted countries is costly and time consuming, and the time required for such approval is uncertain. Our X-22 smoking cessation aid must undergo rigorous clinical testing and an extensive regulatory approval process mandated by the FDA or EMEA. Such regulatory review includes the determination of manufacturing capability and product performance. Generally, only a small percentage of pharmaceutical products are ultimately approved for commercial sale.

The scope of review, including product testing and exposure studies, to be required by the FDA under the Tobacco Control Act in order for cigarettes such as BRAND A and BRAND B to be marketed as Modified Risk Cigarettes has not yet been fully established. We may be unsuccessful in establishing that BRAND A or BRAND B are Modified Risk Cigarettes, and we may fail to demonstrate that either BRAND A or BRAND B significantly reduces exposure to certain tobacco smoke toxins. Even if we are able to demonstrate reduced exposure to certain tobacco smoke toxins, the FDA may decide that allowing a reduced risk claim is not in the best interest of the public health, and the FDA may not allow us to market our BRAND A and/or BRAND B cigarettes as Modified Risk Cigarettes. The FDA may prevent us from selling BRAND A or BRAND B or both products in the U.S. market before the FDA makes a determination of whether to authorize us to market our BRAND A or BRAND B cigarettes as Modified Risk Cigarettes. Furthermore, the FDA could force us to remove from the U.S. market our other tobacco products such as RED SUN or MAGIC.

If we fail to comply with extensive regulations enforced by the FDA and other agencies, the commercialization of our potential products could be prevented, delayed or halted.

There is no guarantee that we will obtain the necessary approvals and authorizations from the FDA for X-22 to be marketed as a smoking cessation aid or for Brand A or Brand B to be classified as Modified Risk Cigarettes. Clinical trials and the manufacturing and marketing of X-22, BRAND A and BRAND B are subject to extensive regulation by various government authorities. We have not received marketing approval for our X-22 smoking cessation aid, nor have we applied for or received FDA authorization to market BRAND A or BRAND B cigarettes as Modified Risk Cigarettes. The process of obtaining FDA and other required regulatory approvals and authorizations is lengthy and expensive, and the time required for such approvals and authorizations is uncertain. The processes are affected by such factors as:

|

|

·

|

the severity of the disease involved;

|

|

|

·

|

the quality of submissions relating to the potential product;

|

|

|

·

|

the potential product’s clinical efficacy and safety;

|

|

|

·

|

the strength of the chemistry and manufacturing control of the process;

|

|

|

·

|

the manufacturing facility’s compliance;

|

|

|

·

|

the availability of alternative treatments;

|

|

|

·

|

the risks and benefits demonstrated in clinical trials; and

|

|

|

·

|

the patent status and marketing exclusivity rights of certain innovative products.

|

Any regulatory approval or authorization that we receive for our potential products may also be subject to limitations on the indicated uses for which the product may be marketed or contain requirements for potentially costly post-marketing follow-up studies. The subsequent discovery of previously unknown problems with the product, including adverse events of unanticipated severity or frequency, may result in restrictions on the marketing of the product and/or withdrawal of the product from the market.

15

Manufacturing, labeling, storage and distribution activities in the United States also are subject to strict regulation and licensing by the FDA. The manufacturing facilities for biopharmaceutical products and tobacco products are subject to periodic inspection by the FDA and other regulatory authorities and from time to time, these agencies may send notice of deficiencies as a result of such inspections. Our failure, or the failure of our contractors’ manufacturing facilities, to continue to meet regulatory standards or to remedy any deficiencies could result in corrective action by the FDA or these other authorities, including the interruption or prevention of marketing, closure of our contractors’ manufacturing facilities, and fines or penalties.