Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF PRICEWATERHOUSECOOPERS LLP - Manning & Napier, Inc. | dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on July 1, 2011

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

MANNING & NAPIER, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 6282 | 45-2609100 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

290 Woodcliff Drive

Fairport, New York 14450

(585) 325-6880

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Richard B. Yates

Chief Legal Officer

Manning & Napier, Inc.

290 Woodcliff Drive

Fairport, New York 14450

(585) 325-6880

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Harold Levine Irwin A. Kishner Herrick, Feinstein LLP 2 Park Avenue New York, New York 10016 (212) 592-1400 |

Raymond B. Check Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, New York 10006 (212) 225-2000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer þ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price (1)(2) |

Amount of registration fee |

||||||

| Class A common stock, $0.01 par value per share |

$ | 250,000,000 | $ | 29,025 | ||||

| (1) | Includes additional shares of Class A common stock which the underwriters have the option to purchase to cover overallotments, if any. |

| (2) | Estimated solely for purposes of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated July 1, 2011

PROSPECTUS

Shares

Class A Common Stock

This is Manning & Napier, Inc.’s initial public offering. We are selling shares of our Class A common stock and the selling stockholder is selling shares of our Class A common stock. We will not receive any proceeds from the sale of shares to be offered by the selling stockholder.

We expect the public offering price to be between $ and $ per share. Currently, no public market exists for the shares. After pricing of the offering, we expect that the shares will trade on the under the symbol “MN.”

Upon completion of this offering, William Manning, our Chairman and controlling stockholder, will hold a majority of the combined voting power of our capital stock through his ownership of 100% of our outstanding Class B common stock.

Investing in our Class A common stock involves risks that are described in the “Risk Factors” section beginning on page 16 of this prospectus.

| Per Share |

Total |

|||||||

| Public offering price |

$ | $ | ||||||

| Underwriting discount |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

| Proceeds, before expenses, to the selling stockholder |

$ | $ | ||||||

The underwriters may also exercise their option to purchase up to an additional shares of the Class A common stock from us at the public offering price, less the underwriting discount, for 30 days after the date of this prospectus to cover overallotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares will be ready for delivery on or about , 2011.

BofA Merrill Lynch

The date of this prospectus is , 2011.

Table of Contents

| Page | ||||

| 1 | ||||

| 16 | ||||

| 35 | ||||

| 36 | ||||

| 46 | ||||

| 47 | ||||

| 48 | ||||

| 49 | ||||

| Unaudited Pro Forma Combined Consolidated Financial Information |

50 | |||

| Selected Historical Combined Consolidated Financial And Other Data |

57 | |||

| Management’s Discussion And Analysis Of Financial Condition And Results Of Operations |

60 | |||

| 82 | ||||

| 94 | ||||

| 97 | ||||

| 101 | ||||

| 114 | ||||

| 115 | ||||

| 117 | ||||

| 120 | ||||

| Material U.S. Federal Tax Considerations For U.S. And Non-U.S. Holders Of Our Class A Common Stock |

122 | |||

| 126 | ||||

| 132 | ||||

| 132 | ||||

| 132 | ||||

| F-1 | ||||

i

Table of Contents

We are responsible for the information contained in this prospectus and in any free writing prospectus we may authorize to be delivered to you. We have not, and the selling stockholder and the underwriters have not, authorized anyone to give you any other information, and take no responsibility for any other information that others may give you. We and the selling stockholder are offering to sell, and seeking offers to buy, shares of our Class A common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our Class A common stock.

BASIS OF PRESENTATION

Except as otherwise indicated herein or as the context otherwise requires, in this prospectus:

| • | “Manning & Napier,” “the Company,” “we,” “our,” and “us” refers to Manning & Napier, Inc. and, unless the context otherwise requires, its direct and indirect subsidiaries, including Manning & Napier Group, and predecessors, including the Manning & Napier Companies; |

| • | “Manning & Napier Group” refers to Manning & Napier Group, LLC, a limited liability company organized under the laws of the State of Delaware, and, unless the context otherwise requires, its direct and indirect subsidiaries and predecessors; |

| • | “M&N Group Holdings” refers to M&N Group Holdings, LLC, a limited liability company organized under the laws of the State of Delaware; |

| • | “Manning & Napier Companies” refers to, collectively, Manning & Napier Advisors, Inc., or MNA, Manning & Napier Advisory Advantage Corporation, or AAC, Manning & Napier Alternative Opportunities, Inc., or MNAO, Manning & Napier Capital Company, LLC, or MNCC, Manning & Napier Investor Services, Inc., or MNBD, Manning & Napier Information Services, LLC, or MNIS, and Perspective Partners LLC, or PPI, each as in effect prior to the reorganization transactions; |

| • | “Manning & Napier Associates” refers to Manning & Napier Associates, LLC, a limited liability company organized under the laws of the State of New York and an affiliate of Manning & Napier. |

| • | “this offering” refers to the offering of our Class A common stock offered hereby; |

| • | “collective investment trusts” refers to the pools of retirement plan assets maintained by a bank or trust company that we manage; |

| • | “portfolios” refers to the separate accounts in which we manage our clients’ investments and the mutual funds, collective investment trusts or other pooled investment vehicles for which we are investment adviser or sub-advisor; |

| • | “management services” refers to the investment management services we provide to clients who engage us to manage their investments; and |

| • | “client” and “clients” refer to investors who access our management services. |

In this prospectus, we rely on and refer to certain market and industry data and forecasts related thereto. We obtained this information and these statistics from sources other than us, which we have supplemented where necessary with information from publicly available sources and our own internal estimates. We use these sources and estimates and believe them to be reliable, but we cannot give you any assurance that any of the projected results will be achieved.

None of the information in this prospectus or the registration statement of which this prospectus forms a part constitutes either an offer or a solicitation to buy or sell any of our products, nor is any such information a recommendation for any of our products or management services.

ii

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that may be important to you. You should read the entire prospectus carefully together with our combined consolidated financial statements and the related notes appearing elsewhere in this prospectus before you decide to invest in our Class A common stock. This prospectus contains forward-looking statements, which involve risks and uncertainties. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of certain factors, including those discussed under the heading “Risk Factors” and other sections of this prospectus.

Overview

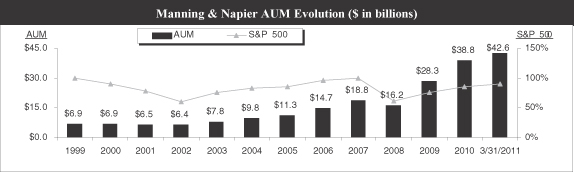

We are an independent investment management firm that provides a broad range of investment solutions through separately managed accounts, mutual funds and collective investment trust funds. Founded in 1970, we offer equity and fixed income portfolios as well as a range of blended asset portfolios, such as life cycle funds, that use a mix of stocks and bonds. Since 1999, we have achieved strong relative growth in discretionary assets under management, or AUM. From December 31, 1999 through March 31, 2011, our AUM has increased from $6.9 billion to $42.6 billion, representing a compound annual growth rate of 17.5% during a period that included two significant bear markets. Our growth in AUM resulted in an increase in our revenues from $50.2 million for the year ended December 31, 1999 to $255.5 million for the year ended December 31, 2010.

Note: Reflects our AUM over the periods indicated compared to the performance of the market, represented by the benchmarked return of the S&P 500 relative to its level at the end of 1999. Data as of December 31 of each respective year, unless otherwise indicated.

We employ a disciplined investment process that seeks to avoid areas of speculation and invest in what we view as under-valued market segments, under the principle that today’s market prices drive future potential investment return. Initially, this approach helped us build a strong client base of high net worth individuals and middle market institutions, and we maintain these relationships in many targeted geographic regions. This foundation allowed us to expand our business to serve the needs of larger institutions, investment consultants and other intermediaries, which has been a strong driver of recent growth.

We have focused on building an internal organization of specialists to provide additional consultative services beyond investment management, which we believe helps us build close relationships with our clients through multiple service touch points and a solutions-oriented approach. Taken together with strong investment performance across portfolios, our consultative, total-solutions approach has allowed us to achieve a significantly lower-than-industry average annual separate account cancellation rate through difficult market environments. According to Cerulli Associates, the average annual industry redemption rate, or cancellation rate, for separate accounts was 23.3% for the period 2002 through 2010 and 24.9% over the last five years ending December 31,

1

Table of Contents

2010, as compared to our average annual cancellation rates of 3.9% and 3.6%, respectively, during such periods. We have experienced net positive cash flows in both our separate accounts and our mutual funds for each of the last four years and thus far in 2011.

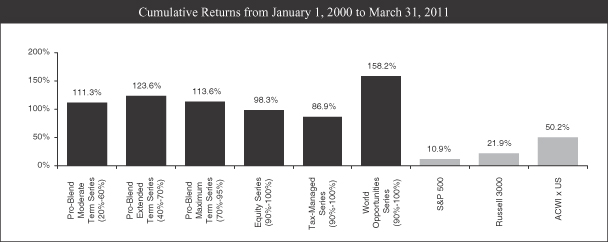

Our research process is analyst- and team-driven. Our mutual funds have earned a number of industry accolades, including a finalist ranking for Morningstar’s international manager of the decade and multiple Lipper awards. As of March 31, 2011, 15 of the 17 funds eligible for Morningstar ratings, representing 87% of our total mutual fund AUM, are rated four or five stars by Morningstar. From January 1, 2000 through March 31, 2011, a period of time that included two significant bear markets, many of our mutual funds and similarly managed separate account portfolios experienced strong cumulative returns well in excess of the returns earned by broad equity market indexes.

Note: Represents cumulative returns for the mutual funds set forth above from January 1, 2000 to March 31, 2011. Percentages in parentheses represent mutual fund equity range.

We have separate account portfolios that mirror each of the mutual funds illustrated above, each of which has earned similar cumulative investment returns to those we have earned for our mutual funds.

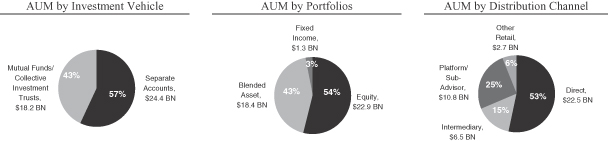

We offer our investment management capabilities primarily through direct sales to high net worth individuals and institutions, as well as through third-party intermediaries, including wirehouse brokers, independent financial advisors, and institutional investment consultants. Our AUM as of March 31, 2011 by investment vehicle, portfolios and distribution channel were as follows:

As of March 31, 2011, we had 414 employees, including William Manning, our Chairman and controlling stockholder, and the 47 other employee-owners, most of whom are based in Fairport, New York.

2

Table of Contents

Immediately following the completion of this offering, these employee-owners will collectively own approximately % of Manning & Napier Group, through which we conduct all of our business. Our culture of employee ownership strongly aligns our interests with those of our clients’ by delivering strong investment performance and solutions.

Industry Trends

We believe the following key market trends will continue to drive the growth of our business and increase the value of our service offerings:

Increased Focus on Management of Employee Benefit Plans. Rapidly rising healthcare costs are eroding the ability of many employees to fund adequate retirement savings and employers are increasingly concerned with the financial hurdles their employees face. According to Deloitte Consulting LLP, approximately 75% of employers surveyed indicate that they plan to make or have already made changes to the design of their health and welfare plans to address these concerns. At the same time, employees increasingly are looking for customized advice. We believe employers will be increasingly interested in working with providers that can take a holistic view of benefit plan design and can help solve problems with both retirement benefit plans and health benefit plans.

Growth of Defined Contribution Plans and Enhanced Role for Life Cycle Funds. We believe the large and growing retirement savings industry increasingly requires investment advice and retirement help for employees. As a result of the Pension Protection Act of 2006 and subsequent U.S. Department of Labor guidelines, plan sponsors are now actively seeking automatic retirement savings solutions for their employees. We expect auto-enrollment will be a driver of even greater participant balances in the future and life cycle funds, and target date funds in particular, will continue to see increased demand as more plan sponsors use such funds as the default option within their plans. Cerulli Associates estimates assets in life cycle funds will increase by 40% per year from 2009 through 2015. We believe life cycle and target date fund providers with a documented track record of proven results will garner increasing assets in this space, especially when bundled with broad employee education services.

Focus on Intergenerational Planning. A 2011 U.S. Trust survey of Americans with at least $3 million in investments indicates that nearly 40% do not have a comprehensive estate plan and more than 27% have never discussed intergenerational wealth transfer with their financial advisor. We anticipate significant opportunities for investment managers that can position themselves as trusted advisors to high net worth investors.

Heightened Interest in Risk Management. Following the credit crisis and global bear market in 2008 and early 2009, investors and financial advisors have become increasingly interested in absolute return strategies, or strategies that seek positive returns over full market cycles. A 2010 survey of financial advisors and brokers by Putnam Investments states that 59% of advisors were likely to recommend absolute return strategies to their clients. We believe our active and unconstrained investment approach within our blended asset class portfolios is well suited to meet the demand for absolute return strategies using traditional asset classes and is likely to be less expensive than alternative investment-based strategies with similar absolute return goals.

Demand for Non-U.S. Investments. With more than 50% of the global market capitalization represented by non-U.S. companies, U.S. investors are increasingly looking to diversify their assets through non-U.S. investments. We believe U.S. investors are under-allocated in global equities relative to global benchmarks, particularly in the defined contribution channel, with only 7% of defined contribution assets invested in non-U.S. equities. We believe investors will strive to select managers with experience and proven results to meet their more diversified and global investing requirements as well as those with the flexibility to allocate assets to and within foreign markets, among both developed and emerging countries.

3

Table of Contents

Our Competitive Strengths

Team-Based Investment Approach. We rely on a team-based investment approach and a robust investment process that has resulted in consistent returns over time that are well in excess of market benchmarks. Our investment team consists of 39 “bottom-up” equity research analysts with global industry responsibilities and 27 “top-down” economists, statistical analysts and fixed income analysts. Investment decisions are overseen by our Senior Research Group, which is a team of ten senior analysts who manage our portfolios. We believe this team approach, rather than relying on traditional individual portfolio managers, has provided and will continue to provide consistency to our investment process and results over the long-term.

Track Record of Consistent Investment Excellence through Multiple Market Cycles. We have a track record of superior long-term investment returns across our key portfolios relative to our competitors and the relevant benchmarks. Fifteen of our 17 mutual funds, representing more than $15 billion in AUM, have a Morningstar rating of 4 or 5 stars. Lipper Fund Awards 2010 named Manning & Napier’s World Opportunities Series as the “Best International Multi-Cap Core Fund over 10 years” and their 2011 Fund Awards named our International Series as the “Best International Multi-Cap Core Fund” over three years. Our track record of consistent outperformance is instrumental in attracting and retaining clients as well as in maintaining good relationships with consultants who recommend our services.

High Client Retention through a Solutions-Oriented Approach. Our average annual separate account cancellation rate was 3.6% over the last five years ending December 31, 2010, as compared to an industry rate of 25% according to Cerulli Associates. For many of our clients, we provide an array of services to help them identify their funding and investment requirements and then design solutions that are specific to the client’s needs. We believe our long history of providing consultative services to complement our investment process has allowed us to form stronger relationships with our clients and has helped to reduce turnover during challenging market environments.

Strong Record of Net New Business Generation. Our AUM and revenue has grown consistently over the period from December 31, 1999 to March 31, 2011 despite two bear markets. We have experienced positive net cash flows every quarter since the last stock market peak in the fourth quarter of 2007. Our contraction in AUM during the 2008-2009 market downturn was relatively mild primarily due to continued strong new business flows driven by our absolute return orientation and our low client cancellation rate. Our strong organic growth has allowed us to maintain positive revenue momentum during periods of sustained market declines and establish a solid base to build on during periods of economic expansion.

Culture of Product Innovation. We have a company-wide culture of product innovation that is designed to anticipate the needs of the clients we serve. For example, we developed our first life cycle mutual fund in 1993, when there were only seven life cycle funds listed on Morningstar. More recently, we launched technology driven products and services to assist both employers and employees with their health and wealth planning. Given our culture of innovation, we believe that we are well-positioned to take advantage of new opportunities in the ever-changing marketplace.

Diversified Client Base through Multiple Channels. We distribute our products and services through direct sales as well as by leveraged distribution through financial intermediaries, platforms and investment consultants. Overall, our client base is well-diversified across both individual and institutional client types, with our largest direct client relationship representing only 1.3% of our total AUM as of March 31, 2011. As of March 31, 2011, our largest third-party relationship accounted for approximately 5% of our total AUM. This broad distribution has made our business less susceptible to losses from any one client or channel and has contributed to the stability of our earnings.

4

Table of Contents

Experienced Management Team and Investment Professionals. In 2003, William Manning turned over management responsibilities to our current executive management team. This team has, on average, 22 years of experience with our company and an average of 28 years of experience in the asset management industry. Patrick Cunningham has been with us since 1992 and was named our chief executive officer in June 2010, and the majority of the members of our Senior Research Group started their investment careers with us. These long-standing tenures illustrate the continuity and commitment of our team that we believe will be important to our success in the future.

Our Strategy

Our strategy for continued success is focused on the following:

Expand our Direct Channel. Our high-touch direct distribution channel has allowed us to build strong relationships with our clients over time. We plan to expand our direct sales presence geographically, filling in new regions along the east coast and expanding farther west. Our direct channel will remain focused on identifying geographic regions within which our representatives form key relationships with centers of influence, business owners and other referral networks.

Broaden our Intermediary Channel. We are focused on the attractive 401(k) marketplace, which is characterized by positive cash flows and low cancellation rates. In addition to building relationships directly with plan sponsors, we are focusing our wholesale staff on identifying advisors and other financial intermediaries that work primarily with defined contribution plans. We expect significant future growth opportunities within this channel as we begin to target wire-house advisors, retirement plan advisors and other intermediaries that work with small- to mid-sized 401(k) plans.

Focus on the Convergence of Health and Wealth Benefits. Our strong relationship with employers positions us well for the opportunities provided by the convergence of health and wealth benefits in employer decision making. We are focused on providing consultative services to employers to address these key concerns through unique plan design alternatives and technology-based tools to help employers and advisors effectively reach large numbers of employees with tailored retirement and health plan guidance. We will continue to develop and potentially acquire products and services to help employers best address these key issues regarding retirement and health benefit plans.

Develop New Products in Response to Market Opportunities. The on-going development of products and consultative services in response to current and prospective client needs has been a source of significant growth. We remain committed to understanding the key areas of concern for various client types and developing solutions to meet these needs. Continued product and service development will likely require building additional resources and areas of expertise, and we are continuing to add resources where solving key problems can strengthen our relationships with clients.

Summary Risk Factors

An investment in our Class A common stock involves substantial risks and uncertainties. These risks and uncertainties include, among others, the following:

| • | Our revenues are dependent on the market value and composition of our AUM, all of which are subject to fluctuation due to factors outside of our control. |

| • | The loss of key investment professionals or members of our senior management team could have an adverse effect on our business. |

| • | We derive substantially all of our revenues from contracts and relationships that may be terminated upon short or no notice. |

5

Table of Contents

| • | We may be required to reduce the fees we charge, which could have an adverse effect on our profit margins and results of operations. |

| • | Several of our portfolios involve investing principally in the securities of non-U.S. companies, which involve foreign currency exchange, tax, political, social and economic uncertainties and risks. |

| • | Control of a majority of the combined voting power of our capital stock by William Manning, and ownership of % of Manning & Napier Group’s ownership interests by our existing owners, including William Manning, may give rise to conflicts of interest. |

The foregoing is not a comprehensive list of the risks and uncertainties we face. Investors should carefully consider all of the information in this prospectus, including information under “Risk Factors,” prior to making an investment in our Class A common stock.

Structure and Reorganization

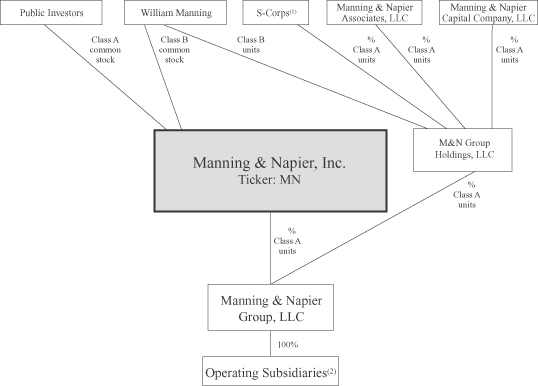

The diagram below depicts our organizational structure after the reorganization transactions and the consummation of this offering.

| (1) | Represents Manning & Napier Advisors, Inc., Manning & Napier Advisory Advantage Corporation, Manning & Napier Investor Services, Inc. and Manning & Napier Alternative Opportunities, Inc. |

| (2) | Represents (i) the newly formed limited liability companies which will have assets contributed by Manning & Napier Advisors, Inc., Manning & Napier Advisory Advantage Corporation, Manning & Napier Investor Services, Inc. and Manning & Napier Alternative Opportunities, Inc., and (ii) Perspective Partners LLC, Manning & Napier Information Services, LLC and Exeter Trust Company. |

6

Table of Contents

Reorganization Transactions

We will enter into a series of transactions to reorganize our capital structure in connection with this offering. We refer throughout this prospectus to the transactions described below as the reorganization transactions or the reorganization.

Revisions to our Organizational Structure. Prior to the reorganization transactions and this offering, we were a group of privately-held, affiliated companies comprising the Manning & Napier Companies. Five of these companies were majority owned by William Manning, our Chairman and controlling stockholder, with a minority interest held by 47 of our employees, and two of these companies were majority owned by William Manning, with a minority interest held by B. Reuben Auspitz, our Vice-Chairman. See “Our Structure and Reorganization—Structure Prior to the Reorganization Transactions.”

Prior to the reorganization transactions and this offering, we had a mandatory redemption obligation upon the death of William Manning to pay a formula-derived amount to his estate. Our liability related to this mandatory redemption obligation was calculated each fiscal quarter, and the change in the liability was reflected as a non-cash interest expense. Such mandatory obligation will terminate immediately prior to the consummation of this offering and we will no longer reflect non-cash interest expense or the liability related to such obligation. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Capital Stock. Immediately prior to the consummation of this offering, we will amend and restate our certificate of incorporation to authorize two classes of common stock, Class A common stock and Class B common stock. We will issue shares of Class A common stock to the public pursuant to this offering and, immediately prior to the consummation of this offering, we will issue shares of our Class B common stock to William Manning and shares of our Class A common stock to the selling stockholder. Each share of Class A common stock will entitle its holder to one vote per share. The holder of our Class B common stock will have a majority of the combined voting power of our capital stock through his ownership of 100% of our outstanding Class B common stock. See “Description of Capital Stock.”

Equity Ownership Interests. In connection with the reorganization transactions, additional ownership interests in M&N Group Holdings will be granted to William Manning. In addition, certain of the Manning & Napier Companies will amend and restate their respective shareholders’ agreements, pursuant to which, among other things, the vesting terms related to the current ownership interests of our employees, including our named executive officers other than William Manning, will be amended. Such individuals will be entitled to 15% of their pre-reorganization ownership interests upon the consummation of this offering, and an additional 5% of such ownership interests will vest as of each of the first, second and third anniversaries of the consummation of this offering, provided such individuals are employed by us as of such date (employment-based vesting). The remaining ownership interests will be subject to performance-based vesting as of each of the first, second and third anniversaries of this offering (subject to an initial two-year lockup period and other selling restrictions), to be determined by a vesting committee of MNA (performance-based vesting). Such new vesting terms will not result in dilution to the number of outstanding shares of our Class A common stock. As a result of such vesting requirements, we will recognize non-cash compensation charges which will be fully realized by the end of 2014. We will also recognize an additional one-time non-cash compensation charge in 2011 related to the additional ownership interests that will be granted to William Manning.

Notwithstanding these vesting requirements, the amended and restated shareholders’ agreements will provide that, in the event William Manning sells any portion of his interests in the Manning & Napier Companies following the consummation of this offering, our other employee-owners will have the right to sell a pro rata amount of such individuals’ ownership interest in Manning & Napier Group, and if any individual does not at such time have fully vested ownership interests sufficient to allow such participation, an amount of their ownership interests will vest to the extent necessary to allow them to participate in the pro rata sale. In addition, the board of

7

Table of Contents

directors of MNA has limited the aggregate sales in any calendar year by our employees, other than William Manning, of their respective interests to a number of shares equal to 1.5% (or such higher percentage as determined by the board of directors of MNA in its sole discretion) of the number of shares that would be outstanding immediately after this offering if M&N Group Holdings exchanged 100% of its units for shares of our Class A common stock. This 1.5% limit will not apply to ownership interests entitled to vest as a result of sales by William Manning as described above or to the employment-based vesting as described above.

See “Our Structure and Reorganization—Equity Ownership Interests.”

Exchange Agreement. Prior to the consummation of this offering, we will enter into an exchange agreement with M&N Group Holdings, the direct holder of all of the Class A units of Manning & Napier Group that are not held by us, which in the aggregate is equivalent to % of our Class A common stock on a fully diluted as-exchanged basis.

Pursuant to the terms and conditions of the exchange agreement, prior to this offering, M&N Group Holdings exchanged Class A units of Manning & Napier Group for shares of our Class A common stock, of which shares are being sold in this offering by M&N Group Holdings on behalf of William Manning and shares are being sold in this offering by M&N Group Holdings on behalf of certain of our employees, including our named executive officers.

In addition, subject to certain restrictions set forth in the exchange agreement:

| • | with respect to the Class A units and Class B units of Manning & Napier Group, which are sometimes collectively referred to herein as units, that are attributable to the interests of William Manning in M&N Group Holdings, commencing on the first anniversary of this offering, M&N Group Holdings may exchange up to 15% of such units (equivalent to shares of our Class A common stock on a fully diluted as-exchanged basis) per year on behalf of William Manning; provided, that with respect to the exchanges permitted as of the first anniversary of the consummation of this offering, the 15% limit will be reduced by the units exchanged for shares of our Class A common stock sold in this offering on his behalf; and |

| • | with respect to the Class A units of Manning & Napier Group that are attributable to the interests of the other holders of M&N Group Holdings, all of whom are our employees, including our named executive officers, other than William Manning: |

| - | commencing on the first anniversary of the consummation of this offering, M&N Group Holdings may exchange up to 5% of such Class A units (equivalent to shares of our Class A common stock on a fully diluted as-exchanged basis) on behalf of such holders; and |

| - | commencing on the second anniversary of the consummation of this offering, M&N Group Holdings may exchange the remaining Class A units, subject to the vesting requirements and selling restrictions as set forth above. |

For any units of Manning & Napier Group exchanged following the consummation of this offering, we will (i) pay an amount of cash equal to the number of units exchanged multiplied by the value of one share of our Class A common stock, or, at our election, (ii) issue shares of our Class A common stock on a one-for-one basis, subject, in each case, to customary adjustments for stock splits, stock dividends and reclassifications and other similar transactions. As we receive units of Manning & Napier Group that are exchanged, our ownership of Manning & Napier Group will increase.

8

Table of Contents

In addition, we intend to award equity-based incentives to certain employees pursuant to the Manning & Napier, Inc. 2011 Equity Compensation Plan, or the 2011 Plan, to align their interests with our stockholders. From time to time following the consummation of this offering, the holders of units of Manning & Napier Group granted pursuant to the 2011 Plan, if any, shall become parties to the exchange agreement. Following the satisfaction of any vesting conditions set forth in the applicable agreements granting such holders such units or as otherwise determined by the compensation committee, such holders may exchange such units for (i) an amount of cash equal to the number of units exchanged multiplied by the value of one share of our Class A common stock, or, at our election, (ii) shares of our Class A common stock on a one-for-one basis, subject, in each case, to customary adjustments for stock splits, stock dividends and reclassifications and other similar transactions. As we receive units of Manning & Napier Group that are exchanged, our ownership of Manning & Napier Group will increase.

See “Our Structure and Reorganization—Offering Transactions—Exchange Agreement.”

Tax Receivable Agreement. Simultaneously with this offering, we will enter into a tax receivable agreement with the holders of Class A units of Manning & Napier Group, under which we will be required to pay to the holders of such Class A units 85% of the applicable cash savings, if any, in U.S. federal, state, local and foreign income tax that we actually realize, or are deemed to realize in certain circumstances, in periods after this offering as a result of any step-up in tax basis in Manning & Napier Group’s assets resulting from (i) our purchases or exchanges of such Class A units for cash or shares of our Class A common stock (including the exchanges of Class A units in connection with the reorganization transactions) and (ii) payments under the tax receivable agreement, including any tax benefits related to imputed interest deemed to be paid by us as a result of such agreement.

There is a possibility that not all of the 85% of the applicable cash savings will be paid to the exchanging holder of Class A units at the time described above. If we determine that, all or a portion of such applicable tax savings is in doubt, we will pay to the holders of such Class A units the amount attributable to the portion of the applicable tax savings that we determine is not in doubt and pay the remainder at such time as we reasonably determine the actual tax savings or that the amount is no longer in doubt.

See “Our Structure and Reorganization—Offering Transactions—Tax Receivable Agreement.”

Our Principal Stockholder

Upon and after the consummation of this offering, William Manning will hold a majority of the combined voting power of our capital stock through his ownership of 100% of our outstanding Class B common stock. Accordingly, William Manning will have the ability to approve or disapprove certain transactions and matters, including material corporate transactions.

Corporate Information

We were incorporated on June 22, 2011 under the laws of the State of Delaware. Our principal executive office is located at 290 Woodcliff Drive, Fairport, New York 14450, and our telephone number at that office is (585) 325-6880. The website address of our operating company is www.manning-napier.com. This website and information contained on, or that can be accessed through, the website are not part of this prospectus.

9

Table of Contents

THE OFFERING

| Class A common stock offered by us |

shares of Class A common stock. |

| Class A common stock offered by M&N Group Holdings, the selling stockholder |

shares of Class A common stock. |

| Class A common stock to be outstanding immediately after this offering |

shares of Class A common stock. If all units of Manning & Napier Group, other than those held by us, were exchanged for shares of our Class A common stock immediately after the reorganization, shares of Class A common stock would be outstanding immediately after this offering. |

| Class B common stock to be outstanding immediately after this offering |

shares of Class B common stock. |

| Use of proceeds |

We estimate that our net proceeds from this offering will be approximately $ million, based on an assumed initial public offering price of $ per share (the mid-point of the price range set forth on the cover page of this prospectus) and after deducting underwriting discounts and commissions and estimated offering expenses payable by us of $ million. We will not receive any proceeds from the sale of Class A common stock by the selling stockholder participating in this offering. The selling stockholder will receive all of the net proceeds from the sale of its shares of Class A common stock in this offering. |

| We intend to use the net proceeds from the sale of our Class A common stock in this offering for general corporate purposes and strategic growth opportunities, including potential acquisitions. The net proceeds the selling stockholder receives from this offering will be distributed to the individuals, including William Manning, on whose behalf the selling stockholder is selling shares of our Class A common stock in this offering. See “Use of Proceeds.” |

| Risk factors |

See “Risk Factors” on page 16 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our Class A common stock. |

| Voting rights |

One vote per share of Class A common stock. The holder of our Class B common stock will control a majority of the vote on all matters submitted to a vote of stockholders. |

| Dividend policy |

Upon the completion of this offering, we will have no material assets other than our ownership of Class A units of Manning & Napier Group. Accordingly, our ability to pay dividends will depend on distributions from Manning & Napier Group. We intend to cause Manning & Napier Group to make distributions to us with available |

10

Table of Contents

| cash generated from its subsidiaries’ operations in an amount sufficient to cover any dividends we may pay. If Manning & Napier Group makes such distributions, any other holders of its units will be entitled to receive equivalent distributions on a pro rata basis. |

| The declaration and payment of all future dividends, if any, will be at the sole discretion of our board of directors. In determining the amount of any future dividends, our board of directors will take into account: |

| • | the financial results of Manning & Napier Group; |

| • | our available cash, as well as anticipated cash requirements, including any debt servicing; |

| • | our capital requirements and the capital requirements of our subsidiaries, including Manning & Napier Group; |

| • | contractual, legal, tax and regulatory restrictions on, and implications of, the payment of dividends by us to our stockholders or by Manning & Napier Group to us, including the obligation of Manning & Napier Group to make tax distributions to its unitholders, including us; |

| • | general economic and business conditions; and |

| • | any other factors that our board of directors may deem relevant. |

| Following this offering, we intend to pay quarterly cash dividends. We expect that our first dividend will be paid in the quarter of and will be approximately $ per share of our Class A common stock. However, there is no assurance that sufficient cash will be available to pay any such dividends. See “Dividend Policy.” |

| Listing symbol |

“MN” |

The number of shares of our Class A common stock to be outstanding after the completion of this offering excludes shares of Class A common stock reserved for issuance upon the exchange of units of Manning & Napier Group held by or that may be granted to M&N Group Holdings.

Unless otherwise indicated, all information in this prospectus assumes and reflects:

| • | an initial public offering price of $ per share, the mid-point of the estimated initial public offering price range set forth on the cover page of this prospectus; and |

| • | no exercise by the underwriters of their right to purchase up to an aggregate of additional shares to cover overallotments, if any. |

11

Table of Contents

Summary Selected Historical and Pro Forma Combined Consolidated Financial Data

The following tables set forth summary selected historical combined consolidated financial data of the Manning & Napier Companies as of the dates and for the periods indicated. The summary selected combined consolidated statements of income data for the years ended December 31, 2008, 2009 and 2010, and the summary selected combined consolidated statements of financial condition data as of December 31, 2009 and 2010 have been derived from the Manning & Napier Companies’ audited combined consolidated financial statements included elsewhere in this prospectus. The summary selected combined consolidated statements of income data for the three months ended March 31, 2010 and 2011 and the summary selected combined consolidated statement of financial condition as of March 31, 2011 have been derived from the Manning & Napier Companies’ unaudited combined consolidated financial statements included elsewhere in this prospectus. These unaudited combined consolidated financial statements have been prepared on substantially the same basis as our audited combined consolidated financial statements and include all adjustments that we consider necessary for a fair statement of our combined consolidated statements of income and financial condition for the periods and as of the dates presented therein. Our results for the three months ended March 31, 2011 are not necessarily indicative of our results for a full fiscal year.

The following table also presents the summary selected unaudited pro forma combined consolidated financial data of Manning & Napier, to give effect to all of the transactions described under “Unaudited Pro Forma Combined Consolidated Financial Information,” including the reorganization transactions and this offering. You should read the following summary selected historical combined consolidated financial data of the Manning & Napier Companies and the unaudited pro forma financial information of Manning & Napier together with “Our Structure and Reorganization,” “Unaudited Pro Forma Combined Consolidated Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the historical combined consolidated financial statements and related notes included elsewhere in this prospectus.

12

Table of Contents

| Manning & Napier Companies | Manning & Napier, Inc. | |||||||||||||||||||||||||||

| Year Ended December 31, |

Three Months Ended March 31, |

Pro

Forma Year Ended December 31, |

Pro Forma Three Months Ended March 31, |

|||||||||||||||||||||||||

| 2008 | 2009 | 2010 | 2010 | 2011 | 2010 | 2011 | ||||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||||||||

| (in millions, except per share data) | ||||||||||||||||||||||||||||

| Statements of income data: |

||||||||||||||||||||||||||||

| Operating revenues |

||||||||||||||||||||||||||||

| Investment management services revenues |

$ | 145.6 | $ | 162.7 | $ | 255.5 | $ | 57.2 | $ | 78.0 | $ | $ | ||||||||||||||||

| Total operating revenues |

145.6 | 162.7 | 255.5 | 57.2 | 78.0 | |||||||||||||||||||||||

| Operating expenses |

||||||||||||||||||||||||||||

| Compensation and related costs |

46.3 | 55.6 | 78.4 | 16.8 | 22.9 | (1) | (1) | |||||||||||||||||||||

| Sub-transfer agent and shareholder service costs |

13.1 | 19.9 | 36.8 | 8.5 | 11.7 | |||||||||||||||||||||||

| Other operating costs |

20.7 | 22.3 | 25.3 | 5.8 | 6.2 | |||||||||||||||||||||||

| Total operating expenses |

80.1 | 97.8 | 140.5 | 31.1 | 40.8 | |||||||||||||||||||||||

| Total operating income |

65.5 | 64.9 | 115.0 | 26.1 | 37.2 | |||||||||||||||||||||||

| Non-operating income (loss) |

||||||||||||||||||||||||||||

| Interest expense on shares subject to mandatory redemption (2) |

(6.7 | ) | (10.0 | ) | (61.2 | ) | (16.2 | ) | (13.3 | ) | ||||||||||||||||||

| Interest expense |

(0.1 | ) | — | (0.1 | ) | — | — | |||||||||||||||||||||

| Interest and dividend income |

0.6 | 0.1 | 0.1 | — | — | |||||||||||||||||||||||

| Net capital gains (losses) on investments |

0.1 | (0.2 | ) | — | — | — | ||||||||||||||||||||||

| Total non-operating income (loss) |

(6.1 | ) | (10.1 | ) | (61.2 | ) | (16.2 | ) | (13.3 | ) | ||||||||||||||||||

| Income before provision for income taxes |

59.4 | 54.8 | 53.8 | 9.9 | 23.9 | |||||||||||||||||||||||

| Provision for income taxes |

0.4 | 0.4 | 0.7 | 0.2 | 0.2 | |||||||||||||||||||||||

| Net income |

$ | 59.0 | $ | 54.4 | $ | 53.1 | $ | 9.7 | $ | 23.7 | $ | $ | ||||||||||||||||

| Less: net income attributable to noncontrolling interests |

||||||||||||||||||||||||||||

| Net income attributable to Manning & Napier, Inc. |

||||||||||||||||||||||||||||

| Per share data: |

||||||||||||||||||||||||||||

| Net income per share |

||||||||||||||||||||||||||||

| Weighted average shares used in basic and diluted net income per share |

||||||||||||||||||||||||||||

| (1) | In connection with the reorganization transactions, certain of the Manning & Napier Companies will modify the vesting terms related to the current ownership interests of our employees, including our named executive officers, other than William Manning. Such individuals will be entitled to 15% of their ownership interests upon the consummation of this offering, and 15% of their ownership interests over the subsequent three years. The remaining ownership interests will be subject to performance-based vesting over such three year period (subject to an initial two-year lockup period and other selling restrictions), to be determined by a vesting committee of MNA. Such new vesting terms will not result in dilution to the number of outstanding shares of our Class A common stock. As a result of such vesting requirements, we will recognize non-cash compensation charges through 2014. |

| (2) | Within interest expense, we have recognized expenses related to a mandatory redemption obligation upon the death of William Manning to pay a formula-driven amount to his estate. Our liability related to this mandatory redemption obligation was calculated each fiscal quarter, and the change in the liability was reflected as non-cash interest expense. Such mandatory redemption obligation will terminate immediately prior to the consummation of this offering and we will no longer reflect non-cash interest expense or the liability related to such obligations. |

13

Table of Contents

| Manning & Napier Companies |

Manning & Napier, Inc. |

|||||||||||||||

| As of December 31, |

As of March 31, |

Pro Forma as of March 31, |

||||||||||||||

| 2009 | 2010 | 2011 | 2011 | |||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||

| (in millions) | ||||||||||||||||

| Statements of financial condition data: |

||||||||||||||||

| Total assets |

$ | 53.4 | $ | 68.3 | $ | 90.1 | $ | |||||||||

| Shares liability subject to mandatory redemption (1) |

109.1 | 170.3 | 183.6 | |||||||||||||

| Total liabilities |

136.7 | 212.1 | 219.2 | |||||||||||||

| (1) | Prior to this offering, we had a mandatory redemption obligation upon the death of William Manning to pay a formula-driven amount to his estate. Our liability related to this mandatory redemption obligation was calculated each fiscal quarter, and the change in the liability was reflected as non-cash interest expense. Such mandatory redemption obligation will terminate immediately prior to the consummation of this offering and we will no longer reflect non-cash interest expense or the liability related to such obligation. |

| Manning & Napier Companies | Manning & Napier, Inc. | |||||||||||||||||||||||||||

| Year Ended December 31, | Three Months Ended March 31, |

Pro Forma Year Ended December 31, |

Pro Forma Three Months Ended March 31, |

|||||||||||||||||||||||||

| 2008 | 2009 | 2010 | 2010 | 2011 | 2010 | 2011 | ||||||||||||||||||||||

| (in millions, except per share data) | ||||||||||||||||||||||||||||

| Selected unaudited operating data: |

||||||||||||||||||||||||||||

| Assets under management (1) |

$ | 16,231.4 | $ | 28,271.3 | $ | 38,841.7 | $ | 31,192.8 | $ | 42,564.1 | $ | $ | ||||||||||||||||

| Adjusted EBITDA (2) |

66.7 | 65.8 | 116.4 | 26.4 | 37.5 | |||||||||||||||||||||||

| Economic net income (2) |

||||||||||||||||||||||||||||

| Economic net income per share |

||||||||||||||||||||||||||||

| Net client cash flows(3) |

3,099.7 | 6,698.9 | 6,464.0 | 1,917.6 | 2,036.0 | |||||||||||||||||||||||

| Market appreciation (depreciation)(4) |

(5,664.0 | ) | 5,341.0 | 4,106.4 | 1,003.9 | 1,686.4 | ||||||||||||||||||||||

| (1) | Reflects the amount of money we managed for our clients as of the last day of the period. |

| (2) | Our management uses non-GAAP financial measures to evaluate the profitability and efficiency of our business model. See page 15 of this prospectus for a reconciliation of these non-GAAP financial measures. Our non-GAAP financial measures may differ from similar measures used by other companies, even if similar terms are used to identify such measures. |

| (3) | Reflects the amount of money our clients placed with us for management, and withdrew from our management, during the period, excluding appreciation (depreciation) due to market performance and fluctuations in exchange rates. |

| (4) | Represents the appreciation (depreciation) of the value of our AUM during the period due to market performance and fluctuations in exchange rates, as well as income, such as dividends, earned on AUM. |

14

Table of Contents

Our management uses Adjusted EBITDA, economic income and economic net income as financial measures to evaluate the profitability and efficiency of our business model. Adjusted EBITDA, economic income and economic net income are not presented in accordance with GAAP. Economic income excludes from income before provision for income taxes:

| • | the non-cash interest expense associated with the liability for shares subject to mandatory redemption; and |

| • | the reorganization-related share based compensation, which results in non-cash compensation expense reported over the vesting period. |

Historically, EBITDA has included adjustments for provision for income taxes, interest income and expense and depreciation and amortization. On a pro forma basis, Adjusted EBITDA also includes an adjustment for reorganization-related share based compensation. Economic net income assumes that all of our economic income would be subject to federal, state and local income tax.

| Manning & Napier Companies | Manning & Napier, Inc. | |||||||||||||||||||||||||||

| Year Ended December 31, |

Three Months Ended March 31, |

Pro Forma Year Ended December 31, |

Pro Forma Three Months Ended March 31, |

|||||||||||||||||||||||||

| 2008 | 2009 | 2010 | 2010 | 2011 | 2010 | 2011 | ||||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||||||||

| (dollar amounts in million, except for per share data) | ||||||||||||||||||||||||||||

| Reconciliation of non-GAAP financial measures: |

||||||||||||||||||||||||||||

| Net income |

$ | 59.0 | $ | 54.4 | $ | 53.1 | $ | 9.7 | $ | 23.7 | $ | $ | ||||||||||||||||

| Provision for income taxes |

0.4 | 0.4 | 0.7 | 0.2 | 0.2 | |||||||||||||||||||||||

| Income before provision for income taxes |

59.4 | 54.8 | 53.8 | 9.9 | 23.9 | |||||||||||||||||||||||

| Reorganization-related share-based compensation(1) |

||||||||||||||||||||||||||||

| Interest expense on shares subject to mandatory redemption(2) |

6.7 | 10.0 | 61.2 | 16.2 | 13.3 | |||||||||||||||||||||||

| Economic income |

66.1 | 64.8 | 115.0 | 26.1 | 37.2 | |||||||||||||||||||||||

| Interest expense |

0.1 | — | 0.1 | — | — | |||||||||||||||||||||||

| Interest income |

(0.6 | ) | (0.1 | ) | (0.1 | ) | — | — | ||||||||||||||||||||

| Depreciation and amortization |

1.1 | 1.1 | 1.4 | 0.3 | 0.3 | |||||||||||||||||||||||

| Adjusted EBITDA |

$ | 66.7 | $ | 65.8 | $ | 116.4 | $ | 26.4 | $ | 37.5 | ||||||||||||||||||

| Economic income |

66.1 | 64.8 | 115.0 | 26.1 | 37.2 | |||||||||||||||||||||||

| Pro forma provision for income taxes |

||||||||||||||||||||||||||||

| Economic net income |

||||||||||||||||||||||||||||

| Economic net income per share |

||||||||||||||||||||||||||||

| Operating revenue |

$ | 145.6 | $ | 162.7 | $ | 255.5 | $ | 57.2 | $ | 78.0 | ||||||||||||||||||

| Net income margin percentage |

40.5 | % | 33.4 | % | 20.8 | % | 17.0 | % | 30.4 | % | ||||||||||||||||||

| Adjusted EBITDA margin percentage |

45.8 | % | 40.4 | % | 45.6 | % | 46.2 | % | 48.1 | % | ||||||||||||||||||

| Economic net income margin percentage |

||||||||||||||||||||||||||||

| (1) | In connection with the reorganization transactions, certain of the Manning & Napier Companies will modify the vesting terms related to the current ownership interests of our employees, including our named executive officers, other than William Manning. Such individuals will be entitled to 15% of their ownership interests upon the consummation of this offering, and 15% of their ownership interests over the subsequent three years. The remaining ownership interests will be subject to performance-based vesting over such three year period (subject to an initial two-year lockup period and other selling restrictions), to be determined by a vesting committee of MNA. Such new vesting terms will not result in dilution to the number of outstanding shares of our Class A common stock. As a result of such vesting requirements, we will recognize non-cash compensation charges through 2014. |

| (2) | Within interest expense, we have recognized expenses related to a mandatory redemption obligation upon the death of William Manning to pay a formula-driven amount to his estate. Our liability related to this mandatory redemption obligation was calculated each fiscal quarter, and the change in the liability was reflected as non-cash interest expense. Such mandatory redemption obligation will terminate immediately prior to the consummation of this offering and we will no longer reflect non-cash interest expense or the liability related to such obligation. |

15

Table of Contents

Investing in our Class A common stock involves a high degree of risk. You should carefully consider the risks described below, together with the other information contained in this prospectus, before making your decision to invest in shares of our Class A common stock. We cannot assure you that any of the events discussed in the risk factors below will not occur. These risks could have an adverse impact on our business, results of operations, financial condition and cash flows. If any of the following risks develops into an actual event, the trading price of our Class A common stock could decline, and you could lose all or part of your investment.

Risks Related to our Business

Our revenues are dependent on the market value and composition of our AUM, all of which are subject to fluctuation due to factors outside of our control.

We derive the majority of our revenue from investment management fees, typically calculated as a percentage of the market value of our AUM. As a result, our revenues are dependent on the value and composition of our AUM, all of which are subject to fluctuation due to many factors, including:

| • | Declines in prices of securities in our portfolios. The prices of the securities held in the portfolios we manage may decline due to any number of factors beyond our control, including, among others, declining stock or commodities markets, a general economic downturn, political uncertainty or acts of terrorism. |

| • | Redemptions and other withdrawals. Our investors generally may withdraw their funds at any time, on very short notice and without any significant penalty. A substantial portion of our revenue is derived from investment advisory agreements that are terminable by clients upon short notice or no notice and investors in the mutual funds we advise can redeem their investments in those funds at any time without prior notice. Our growth in AUM in recent years has included new clients and portfolios that may not have the same client retention characteristics as we have experienced in the past. In addition, in a declining stock market, the pace of redemptions could accelerate. |

| • | Investment performance. If our portfolios perform poorly as compared with our competitors or applicable third-party benchmarks, or the rankings of mutual funds we manage decline, we may lose existing AUM and have difficulty attracting new assets. |

| • | Declines in fixed income markets. For fixed income investments, the value of our AUM may decline as a result of changes in interest rates, available liquidity in the markets in which a security trades, an issuer’s actual or perceived creditworthiness, or an issuer’s ability to meet its obligations. |

If any of these factors cause a decline in our AUM, it would result in lower investment management fees. If our revenues decline without a commensurate reduction in our expenses, our net income will be reduced and our business will be adversely affected.

The loss of key investment professionals or members of our senior management team could have an adverse effect on our business.

We depend on the skills and expertise of qualified investment professionals and our success depends on our ability to retain key employees, including members of our senior management team. Our investment professionals possess substantial experience in investing and have been primarily responsible for the historically strong investment performance we have achieved. We particularly depend on our Senior Research Group, which is a team of ten senior analysts who manage our portfolios, and our executive management team, which is a group of five individuals led by Patrick Cunningham, our chief executive officer. The loss of any of these key individuals could limit our ability to successfully execute our business strategy and could have an adverse effect on our business.

16

Table of Contents

Any of our investment or management professionals may resign at any time, subject to various covenants not to compete with us. In addition, employee-owners are subject to additional covenants not to compete. We do not carry any key man insurance on any employees at this time.

Competition for qualified investment, management, marketing and client service professionals is intense and we may fail to successfully attract and retain qualified personnel in the future. Our ability to attract and retain these personnel will depend heavily on the amount and structure of compensation and opportunities for equity ownership we offer. In connection with our transition to a public company, we intend to implement a compensation structure that uses a combination of cash and equity-based incentives as appropriate. We intend for overall compensation levels to remain commensurate with amounts paid to our named executive officers and other key employees in the past. However, our compensation may not be effective to recruit and retain the personnel we need, especially if our equity-based compensation does not return significant value to employees. Any cost-reduction initiative or adjustments or reductions to compensation could negatively impact our ability to retain key personnel. In addition, changes to our management structure, corporate culture and corporate governance arrangements, including the changes associated with, and resulting from, our reorganization and this offering, could negatively impact our ability to retain key personnel.

We derive substantially all of our revenues from contracts and relationships that may be terminated upon short or no notice.

We derive substantially all of our revenues from investment advisory and sub-advisor agreements, all of which are terminable by clients upon short notice or no notice and without any significant penalty. Our investment management agreements with mutual funds, as required by law, are generally terminable by the funds’ board of directors or a vote of the majority of the funds’ outstanding voting securities on not more than 60 days’ written notice. After an initial term, each fund’s investment management agreement must be approved and renewed annually by such fund’s board, including by its independent members. In addition, all of our separate account clients and some of the pooled investment vehicles, including mutual funds, that we sub-advise have the ability to re-allocate all or any portion of the assets that we manage away from us at any time with little or no notice. These investment management agreements and mutual fund and collective investment trust client relationships may be terminated or not renewed for any number of reasons. The decrease in revenues that could result from the termination of a material client relationship or group of client relationships could have an adverse effect on our business.

We may be required to reduce the fees we charge, which could have an adverse effect on our profit margins and results of operations.

Our current fee structure may be subject to downward pressure due to a variety of factors, including a trend in recent years toward lower fees in the investment management industry. We may be required to reduce fees with respect to both the separate accounts we manage and the mutual funds we advise. In addition, we may charge lower fees to attract future new business as compared to our existing business, which may result in us having to reduce our fees with respect to our existing business accordingly. The investment management agreements pursuant to which we advise mutual funds are terminable on short notice and, after an initial term, are subject to an annual process of review and renewal by the funds’ boards. As part of that annual review process, the fund board considers, among other things, the level of compensation that the fund has been paying us for our services, and that process may result in the renegotiation of our fee structure or increase our obligations, thus increasing the cost of our performance. Any fee reductions on existing or future new business could have an adverse effect on our profit margins and results of operations.

Several of our portfolios involve investing principally in the securities of non-U.S. companies, which involve foreign currency exchange risk, and tax, political, social and economic uncertainties and risks.

As of March 31, 2011, approximately 37% of our AUM across all of our portfolios was invested in securities of non-U.S. companies. Fluctuations in foreign currency exchange rates could negatively affect the

17

Table of Contents

returns of our clients who are invested in these strategies. In addition, an increase in the value of the U.S. dollar relative to non-U.S. currencies is likely to result in a decrease in the U.S. dollar value of our AUM, which, in turn, could result in lower revenue since we report our financial results in U.S. dollars.

Investments in non-U.S. issuers may also be affected by tax positions taken in countries or regions in which we are invested as well as political, social and economic uncertainty, particularly as a result of the recent decline in global economic conditions. Declining tax revenues may cause governments to assert their ability to tax the local gains and/or income of foreign investors (including our clients), which could adversely affect clients’ interests in investing outside their home markets. Many financial markets are not as developed, or as efficient, as the U.S. financial markets and, as a result, those markets may have limited liquidity and higher price volatility and lack established regulations. Liquidity may also be adversely affected by political or economic events, government policies, social or civil unrest within a particular country, and our ability to dispose of an investment may also be adversely affected if we increase the size of our investments in smaller non-U.S. issuers. Non-U.S. legal and regulatory environments, including financial accounting standards and practices, may also be different, and there may be less publicly available information about such companies. These risks could adversely affect the performance of our strategies that are invested in securities of non-U.S. issuers and may be particularly acute in the emerging or less developed markets in which we invest.

We derive a substantial portion of our revenues from our Core Non-U.S. Equity portfolios.

As of March 31, 2011, approximately 31% of our AUM were invested in our Core Non-U.S. Equity portfolios. As a result, a substantial portion of our operating results depends upon the performance of our Core Non-U.S. Equity portfolios, and our ability to retain client assets in such portfolios. If a significant portion of the investors in our Core Non-U.S. Equity portfolios decide to withdraw their investments or terminate their investment management agreements for any reason, including poor investment performance or adverse market conditions, our revenues from these portfolios would decline, which could have an adverse effect on our earnings and financial condition.

The investment performance and/or the growth of our AUM may be constrained if appropriate investment opportunities are not available or if we close certain of our portfolios.

Our ability to deliver strong investment performance depends in large part on our ability to identify appropriate investment opportunities in which to invest client assets. If we are unable to identify sufficient appropriate investment opportunities for existing and new client assets on a timely basis, our investment performance could be adversely affected. The risk that sufficient appropriate investment opportunities may be unavailable is influenced by a number of factors, including general market conditions, and is likely to increase as and if our AUM increases, particularly if these increases occur very rapidly.

If we determine that sufficient investment opportunities are not available for some or all of our portfolios, or we believe that in order to continue to produce attractive returns from some or all of our portfolios we should limit the growth of those strategies, as we have done in the past, we may choose to limit the growth of the portfolio by limiting the rate at which we accept additional client assets for management under the portfolio, closing the portfolio to all or substantially all new investors or otherwise taking action to limit the flow of assets into the portfolio. If we misjudge the point at which it would be optimal to limit access to or close a portfolio, the investment performance of the portfolio could be negatively impacted. In addition, if we close access to a portfolio, we may offer a new portfolio to our clients, but we cannot guarantee that such new portfolio will attract clients or perform in a manner consistent with the closed portfolio.

The significant growth we have experienced over the past nine years has been and may continue to be difficult to sustain, and we may have difficulty managing our growth effectively.

Our AUM have increased from $6.4 billion as of December 31, 2002 to $42.6 billion as of March 31, 2011. The rapid growth in our AUM represents a significant rate of growth that has been and may continue to be

18

Table of Contents

difficult to sustain. In particular, as the absolute amount of our AUM increases, it will be more difficult to maintain levels of growth similar to those we have experienced in the past. The future growth of our business will depend on, among other things:

| • | our ability to retain key investment professionals; |

| • | our ability to devote sufficient resources to maintaining existing portfolios and to selectively develop new portfolios; |

| • | our success in achieving superior investment performance from our portfolios; |

| • | our ability to maintain and extend our distribution capabilities; |

| • | our ability to deal with changing market conditions; |

| • | our ability to maintain adequate financial and business controls; and |

| • | our ability to comply with new legal and regulatory requirements arising in response to both the increased sophistication of the investment management industry and the significant market and economic events of the last few years. |

Unless our growth results in an increase in our revenues that is proportionate to the increase in our costs associated with this growth, our future profitability will be adversely affected. In addition, failure to successfully diversify into new asset classes may adversely affect our growth strategy and our future profitability.

Our portfolios may not obtain attractive returns under certain market conditions or at all.

The goal of our investment process is to provide competitive absolute returns over full market cycles. Accordingly, our portfolios may not perform well during certain periods of time or under certain market conditions as compared to benchmarks or other investment managers’ strategies, which may negatively affect our ability to retain clients and attract new clients. We are likely to be most out of favor when the markets are running on price momentum and market prices become disconnected from underlying investment fundamentals, as was the case during the late 1990s as the technology market and mega cap stocks fueled the broad market upward. During and shortly following such periods of relative under performance, we are likely to see our highest levels of client turnover, even if our absolute returns are positive. Loss of client assets and the failure to attract new clients could adversely affect our revenues and growth.

The historical returns of our existing portfolios may not be indicative of their future results or of the portfolios we may develop in the future.

We have presented the historical returns of our existing portfolios under “Business—Our Competitive Strengths—Track Record of Consistent Investment Excellence through Multiple Market Cycles.” The historical returns of our portfolios and the ratings and rankings we or the mutual funds that we advise have received in the past should not be considered indicative of the future results of these portfolios or of any other portfolios that we may develop in the future. The investment performance we achieve for our clients varies over time and the variance can be wide. The ratings and rankings we or the mutual funds we advise have received are typically revised monthly. The historical performance and ratings and rankings included in this prospectus are as of March 31, 2011 and for periods then ended except where otherwise stated. The performance we have achieved and the ratings and rankings received at subsequent dates and for subsequent periods may be higher or lower and the difference could be material. Our portfolios’ returns have benefited during some periods from investment opportunities and positive economic and market conditions. In other periods, such as in 2008 and the first quarter of 2009, general economic and market conditions have negatively affected our portfolios’ returns. These negative conditions may occur again, and in the future we may not be able to identify and invest in profitable investment opportunities within our current or future portfolios.

19

Table of Contents

We depend on third-party distribution sources to market our portfolios and access our client base.