Attached files

| file | filename |

|---|---|

| EX-1.1 - FORM OF UNDERWRITING AGREEMENT - Aegerion Pharmaceuticals, Inc. | dex11.htm |

| EX-23.2 - CONSENT OF ERNST & YOUNG LLP - Aegerion Pharmaceuticals, Inc. | dex232.htm |

Table of Contents

As filed with the Securities and Exchange Commission on June 20, 2011

Registration No. 333-174944

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

AEGERION PHARMACEUTICALS, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 2834 | 20-2960116 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

101 Main Street, Suite 1850,

Cambridge, Massachusetts 02142

(617) 500-7867

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Marc D. Beer

Chief Executive Officer

Aegerion Pharmaceuticals, Inc.

101 Main Street, Suite 1850,

Cambridge, Massachusetts 02142

(617) 500-7867

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to:

| Jocelyn M. Arel, Esq. Goodwin Procter LLP 53 State Street Boston, Massachusetts 02109 (617) 570-1000 |

Christine A. Pellizzari, Esq. Executive Vice President, General Counsel and Secretary Aegerion Pharmaceuticals, Inc. 135 US Highway 202/206 South, Suite 15, Bedminster, New Jersey 07921 (908) 707-2100 |

Donald J. Murray, Esq. Dewey & LeBoeuf LLP 1301 Avenue of the Americas New York, New York 10019-6092 (212) 259-8000 |

Approximate date of commencement of proposed sale to public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ |

Accelerated filer ¨ | |||

| Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company ¨ | |||

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1) (2) |

Amount of Registration Fee(3)(4) | ||

| Common Stock, par value $0.001 per share |

$86,606,500 | $10,055.01 | ||

| (1) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933. |

| (2) | Includes shares of common stock that the underwriters have an option to purchase to cover over-allotments, if any. |

| (3) | Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price. |

| (4) | A registration fee of $9,595.39 has been paid previously in connection with this Registration Statement based on an estimate of the aggregate offering price. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JUNE 20, 2011

PRELIMINARY PROSPECTUS

4,250,000 Shares

Common Stock

We are offering 3,250,000 shares of common stock, and the Selling Stockholders identified in this prospectus are offering an additional 1,000,000 shares of our common stock. We will not receive any of the proceeds from the sale of the shares being sold by the Selling Stockholders.

Our common stock is quoted on The NASDAQ Global Market under the symbol “AEGR.” On June 17, 2011, the last reported sale price of our common stock was $17.72 per share.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 9.

| Per Share | Total | |||||||

| Public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

| Proceeds, before expenses, to the Selling Stockholders |

$ | $ | ||||||

The underwriters may also purchase up to an additional 637,500 shares from us and certain of the Selling Stockholders, at the public offering price, less the underwriting discounts and commissions, within 30 days of the date of this prospectus to cover over-allotments, if any. If the underwriters exercise this option in full, the total underwriting discounts and commissions will be $ , total proceeds to the Selling Stockholders, before expenses, will be $ , and total proceeds to us, before expenses, will be $ .

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock on or about , 2011.

Joint Book-Running Managers

| Jefferies | Deutsche Bank Securities |

Co-Managers

| Leerink Swann | Needham & Company, LLC | Collins Stewart |

The date of this prospectus is , 2011.

Table of Contents

| Page | ||||

| 1 | ||||

| 9 | ||||

| 40 | ||||

| 42 | ||||

| 44 | ||||

| 44 | ||||

| 45 | ||||

| 47 | ||||

| 49 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

51 | |||

| 65 | ||||

| 91 | ||||

| 96 | ||||

| 113 | ||||

| 120 | ||||

| 123 | ||||

| 128 | ||||

| 132 | ||||

| 135 | ||||

| 135 | ||||

| 135 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by or on behalf of us or to which we have referred you. We have not authorized anyone to provide you with information that is different. We are offering to sell shares of our common stock, and seeking offers to buy shares of our common stock, only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of our common stock.

For investors outside the United States: Neither we, the Selling Stockholders nor any of the underwriters have taken any action to permit a public offering of the shares of our common stock or the possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. Before you decide to invest in our common stock, you should read the entire prospectus carefully, including the “Risk Factors” section and the financial statements and related notes appearing at the end of this prospectus.

Our Company

We are an emerging biopharmaceutical company focused on the development and commercialization of novel therapeutics to treat severe lipid disorders. Lipids are naturally occurring molecules, such as cholesterol and triglycerides that are transported in the blood. Our lead compound, lomitapide, is a microsomal triglyceride transfer protein inhibitor, or MTP-I, which limits secretion of cholesterol and triglycerides from the intestines and the liver, the main sources of circulating lipids in the body. We are initially developing lomitapide as an oral, once-a-day treatment for patients with a rare genetic lipid disorder called homozygous familial hypercholesterolemia, or HoFH. These patients are at very high risk of experiencing life threatening events at an early age as a result of extremely elevated cholesterol levels in the blood and, as a result have a substantially reduced life span relative to unaffected individuals. We believe that lomitapide, either on a stand-alone basis or in combination with other drugs, has the potential to help these patients achieve recommended target levels of low-density lipoprotein cholesterol, or LDL-C.

We are currently evaluating lomitapide in a pivotal Phase III clinical trial for the treatment of patients with HoFH. On May 31, 2011, we announced the results of this trial, through 56 weeks of treatment. We believe based on our prior discussions with the U.S. Food and Drug Administration, or FDA, that these results demonstrate sufficient long-term safety and efficacy to support the submission of our New Drug Application, or NDA, for lomitapide. We refer to these week 56 results as our Filing Data, and we will later supplement the Filing Data with data reflecting the full 78-week trial duration. Before we can submit an NDA, we must complete additional clinical and non-clinical studies to assess various other aspects of lomitapide. On June 15, 2011, we met with the FDA, which informed us that it is not opposed to our submitting our NDA based on the Filing Data. We plan to submit our NDA to the FDA and a Marketing Authorization Application, or MAA, to the European Medicines Agency, or EMA, before the end of 2011.

Assuming we obtain approval, in anticipation of our commercial launch of lomitapide initially in the United States and European Union, we have begun to recruit a team of sales representatives and medical education specialists who are experienced in marketing drugs for the treatment of rare, often genetic, disorders. We initially plan to hire a medical education, marketing and sales force of approximately 15 people in the United States and approximately 18 people in the European Union. We also are evaluating other markets to determine other geographies where we will commercialize lomitapide, either alone or in partnership with others.

We are planning a Phase III pediatric clinical trial to evaluate lomitapide for the treatment of pediatric and adolescent patients (> 7 to < 18 years of age) with HoFH. In addition to HoFH, we are also in the process of developing a protocol for a Phase III clinical trial of lomitapide for the treatment of adult patients with a severe genetic form of elevated triglycerides, or hypertriglyceridemia, called familial chylomicronemia, or FC. In October 2010, the EMA granted lomitapide orphan drug designation for the treatment of FC. In March 2011, the FDA granted lomitapide orphan drug designation for the same indication. In October 2007, the FDA granted lomitapide orphan drug designation for the treatment of HoFH. In the United States, orphan drug designation is given to a drug intended to treat a rare disease or condition, which is generally a disease or condition that affects fewer than 200,000 individuals in the United States. If our NDA for lomitapide receives the first FDA approval for the disease for which it has such designation, it is entitled to orphan drug exclusivity, which means that the FDA may not approve any other applications to market the same drug for the same indication, except in very limited circumstances, for seven years. The EMA generally grants orphan drug designation to drugs that may offer therapeutic benefits for life-threatening or chronically debilitating conditions affecting not more than five in

1

Table of Contents

10,000 people in the European Union. In the European Union, orphan drug designation provides ten years of market exclusivity following drug approval, although the exclusivity period may be reduced to six years if the designation criteria are no longer met.

To date, we have not generated revenue from the sale of any product, and we do not expect to generate significant revenue unless and until we obtain marketing approval of, and commercialize, lomitapide. As of March 31, 2011, we had an accumulated deficit of $97.8 million.

Lomitapide

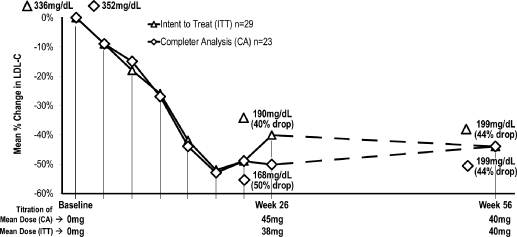

We are currently evaluating lomitapide in an ongoing pivotal Phase III clinical trial for the treatment of patients with HoFH. We completed enrollment for this single-arm, open-label trial in March 2010 with a total of 29 patients. Three of these patients withdrew their consent to participate in the trial and three patients discontinued treatment due to gastrointestinal adverse events. The 23 patients remaining in the trial have completed the 26 week period of therapy after which the primary efficacy endpoint was measured, and the 56 week period of therapy during which the Filing Data were collected. As of the date of this prospectus, 19 of these patients have completed the entire 78 weeks of the trial. We expect to complete this trial in the third quarter of 2011.

Researchers at the University of Pennsylvania, or UPenn, completed a Phase II clinical trial of lomitapide for the treatment of patients with HoFH in 2004. In addition to the UPenn trial, lomitapide has been evaluated in 13 Phase I and five Phase II clinical trials. A total of 915 patients were treated with lomitapide in these Phase I and Phase II trials, including the patients in the UPenn trial. Currently, there are no MTP-Is approved by the FDA for any indication.

Early clinical trials of lomitapide produced meaningful percent reductions in LDL-C levels, but patients discontinued use of lomitapide at a high rate due to gastrointestinal adverse events, such as diarrhea, nausea and vomiting. In addition, a small proportion of patients experienced elevations in liver enzymes and increased mean levels of fat in the liver, or hepatic fat, both of which have also been observed in our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH. We believe the high rate of discontinuations due to gastrointestinal adverse events in the early clinical trials of lomitapide resulted in large part from the failure to employ dose titration, which is the gradual increase in dosing over time to allow the body to adapt to the impact of a higher dose coupled with a low fat diet. Patients in our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH, where dose titration has been employed, have also experienced adverse gastrointestinal events, but to a lesser extent than those experienced in the earlier clinical trials.

Patient Populations of Interest

We are initially developing lomitapide for the treatment of the small number of patients with the rare genetic disorder HoFH. Patients with untreated HoFH have extremely high LDL-C levels, typically between 500 mg/dL and 1,000 mg/dL, and, as a result, are at severely high risk of experiencing premature cardiovascular events, such as a heart attack or stroke. In a report that we commissioned, L.E.K. Consulting LLC, or LEK, an international business consulting firm, estimated that the total number of addressable patients with symptoms consistent with HoFH in each of the United States and, collectively, Germany, the United Kingdom, France, Italy and Spain, which are referred to in this prospectus as the European Union Five, is approximately 3,000 patients, or a combined total of approximately 6,000 patients. LEK’s estimate of the addressable patient population is primarily based on, among other things, physician estimates of patients who have symptoms customarily present in patients definitively diagnosed with HoFH, meaning patients with one of the following: (i) documented functional mutations in both LDL receptor alleles or alleles known to affect LDL receptor functionality, (ii) skin fibroblast LDL receptor activity that is 20 percent less than normal, (iii) untreated total cholesterol greater than 500 mg/dL and triglycerides less than 300 mg/dL with both parents having documented total cholesterol greater than 250 mg/dL or (iv) average fasting LDL-C greater than 300 mg/dL on maximally tolerated lipid lowering therapy as decided by the treating physician. Our pivotal Phase III clinical trial specifically included patients

2

Table of Contents

meeting criteria (i), (ii) or (iii). While many patients in our ongoing pivotal Phase III clinical trial also met diagnostic criterion (iv), it was not explicitly one of the inclusion criteria for the trial. The FDA has stated that defining HoFH patients as those with average fasting LDL-C greater than 300 mg/dL on maximally tolerated lipid lowering therapy, in other words diagnosing patients through method (iv), closely resembles the severe refractory heterozygous familial hypercholesterolemia population. Therefore, these patients may be outside of the HoFH population. The total addressable market opportunity for lomitapide for the treatment of patients with HoFH will ultimately depend upon, among other things, the diagnosis criteria included in the final label for lomitapide, if approved for sale in this indication, acceptance by the medical community, patient access, product pricing and reimbursement.

We also believe that lomitapide has the potential to treat patients with the rare genetic disorder FC, who have extremely high levels of blood triglycerides, or TGs, generally greater than 2,000 mg/dL. These patients are at an increased risk of developing acute pancreatitis, a significant and sometimes life-threatening inflammation of the pancreas. In the report that we commissioned, LEK estimated that, subject to certain factors, there are a total of approximately 1,000 patients in the United States and the European Union Five with FC who could be eligible for treatment with lomitapide.

We believe that lomitapide may also be useful for the treatment of elevated lipid levels in broader patient populations, such as those suffering from heterozygous familial hypercholesterolemia, patients who are statin intolerant and patients with severe hypertriglyceridemia that is brought on by factors other than FC. If we elect to develop lomitapide for broader patient populations, we would plan to do so selectively either on our own or by establishing alliances with one or more pharmaceutical company collaborators, depending on, among other things, the applicable indications, the related development costs and our available resources.

Limitations of Currently Available Treatment Options

Currently available treatment options for patients with HoFH are extensive but, even when combined together, are often ineffective in significantly reducing LDL-C levels to recommended target levels. The clinical approach for patients with HoFH typically involves an aggressive treatment plan to reduce lipid levels as much as possible through dietary modifications, a combination of available lipid lowering drug therapies and, in many cases, plasma apheresis, which is a mechanical filtration of the blood similar to kidney dialysis. Drug therapies include statins, cholesterol absorption inhibitors and bile acid sequestrants.

Similarly, currently available treatment options for patients with FC are often ineffective in lowering TG levels to recommended target levels. The clinical approach for patients with FC, whose TG levels are generally greater than 2,000 mg/dL, typically involves dietary modifications to lower the intake of dietary fat, the use of omega-3 fatty acids and fibrates. However, these treatments are often inadequate to lower TG levels below 500 mg/dL, the level at which patients are at an increased risk for developing acute pancreatitis. Because of the severely elevated TG levels in this patient population, reducing TG levels to this extent may require reductions in TG levels of 75% or more from baseline.

Our Strategy

Our objective is to develop and commercialize drugs to treat patients with rare lipid related disorders who are at very high risk of experiencing life threatening events at an early age. To achieve this objective, we plan to:

| § | Prepare and submit our NDA for lomitapide for the treatment of patients with HoFH based on our Filing Data. |

| § | Complete our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH and, submit the data collected through week 78 of this trial to the FDA to complete our NDA submission and to the EMA to complete our MAA submission. |

| § | Prepare to commercialize lomitapide for the treatment of patients with HoFH through our planned direct medical education, marketing, and sales force in the Unites States and the European Union. |

3

Table of Contents

| § | Initiate a Phase III pediatric clinical trial in pediatric and adolescent patients (> 7 to < 18 years of age) with HoFH. |

| § | Initiate a Phase III clinical trial of lomitapide for the treatment of adult patients with FC. |

| § | Apply to make lomitapide available for use in France under a cohorte Autorisation Temporaire d’Utilisation or Temporary Authorization to Use, or ATU, to permit the compassionate use of a non-approved drug. |

| § | Selectively seek to expand our geographic distribution capabilities and potentially address broader patient populations for lomitapide. |

Risks Associated with Our Business

Our business is subject to numerous risks, as more fully described in the section entitled “Risk Factors” immediately following this prospectus summary, including the following:

| § | We currently depend entirely on the success of our lead compound, lomitapide, which we are developing initially for the treatment of patients with HoFH. We are also developing a protocol for a clinical trial of lomitapide for the treatment of adult patients with FC. We may not receive marketing approval for, or successfully commercialize, lomitapide for any indication. |

| § | The numbers of patients suffering from HoFH and FC are small and have not been established with precision. If the actual number of patients with either of these conditions is smaller than we estimate or if any approval that we obtain is based on a narrower definition of these patient populations, our revenue and ability to achieve profitability will be adversely affected, possibly materially. For example, the FDA has stated that our functional HoFH definition of patients with average fasting LDL-C greater than 300 mg/dL on maximally tolerated lipid lowering therapy closely resembles the severe refractory heterozygous familial hypercholesterolemia population. This means that these patients may ultimately be considered to be outside the HoFH population, reducing the estimated 6,000-patient addressable population. |

| § | In earlier preclinical studies and clinical trials, lomitapide was associated with undesirable side effects, such as adverse gastrointestinal events, elevated liver enzymes and increases in mean hepatic fat levels. Patients in our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH have also experienced such undesirable side effects. Lomitapide may continue to cause such side effects or have other properties that could delay or prevent its marketing approval or result in adverse limitations in any approved labeling or on distribution and use of the product. |

| § | We plan to submit our NDA for lomitapide based on our Filing Data, which is prior to completion of our pivotal Phase III clinical trial. If data obtained during the last 22 weeks of the trial are unfavorable, our ability to commercialize lomitapide may be adversely affected. |

| § | Failures or delays in the commencement or completion of preclinical or clinical testing could result in increased costs to us and delay, prevent or limit our ability to generate revenue. |

| § | The preparation and submission of our NDA may take longer than we currently believe it will, which could result in increased costs to us and delay, prevent or limit our ability to generate revenue. |

| § | Our NDA may be subject to review by an FDA advisory committee, which may not render positive feedback to the FDA or could result in increased costs to us and delay, prevent or limit our ability to generate revenue. |

| § | If we receive marketing approval for lomitapide or any other product candidate, our sales will be limited unless the product achieves broad market acceptance for its indications. |

4

Table of Contents

| § | If we fail to obtain or maintain orphan drug exclusivity for lomitapide, we will have to rely on our data and marketing exclusivity, if any, and on our intellectual property rights, which may reduce the length of time we can prevent competitors from selling lomitapide. |

| § | We currently depend on a single third-party manufacturer to produce our preclinical and clinical drug supplies and intend to rely upon third-party manufacturers to produce commercial supplies of lomitapide. This may increase the risk that we will not have sufficient quantities of lomitapide or such quantities at an acceptable cost, which could delay, prevent or impair our clinical development and commercialization of lomitapide. |

| § | We may not obtain an ATU, or obtaining an ATU may adversely affect our ability to set market prices outside of France, either of which could have an adverse effect on our financial results. |

Corporate Information

We were founded in 2005 as a Delaware corporation. Our principal executive offices are located at 101 Main Street, Cambridge, Massachusetts 02142, and our telephone number is (617) 500-7867. Our web site address is www.aegerion.com. The information on, or that can be accessed through, our web site is not part of this prospectus. We have included our web site address as an inactive textual reference only.

Aegerion is a registered trademark of Aegerion Pharmaceuticals, Inc. in the United States and a trademark in other countries. This prospectus also includes other trademarks of Aegerion Pharmaceuticals, Inc. and other persons. Except where the context requires otherwise, in this prospectus “Company,” “Aegerion,” “we,” “us” and “our” refer to Aegerion Pharmaceuticals, Inc.

5

Table of Contents

THE OFFERING

| Common stock offered by us |

3,250,000 shares |

| Common stock offered by the Selling Stockholders |

1,000,000 shares |

| Common stock to be outstanding after this offering |

20,914,641 shares |

| Over-allotment option |

We and the Selling Stockholders have granted the underwriters an option for 30 days from the date of this prospectus to purchase up to 637,500 additional shares of common stock to cover over-allotments. |

| Use of proceeds |

We plan to use the net proceeds of this offering to prepare and submit our NDA and complete the marketing approval process, to complete clinical and non-clinical studies needed for our NDA submission and our pivotal Phase III clinical trial of lomitapide for the treatment of HoFH, to commercially launch lomitapide for the treatment of patients with HoFH, to advance the clinical development of lomitapide for the treatment of pediatric and adolescent patients (> 7 to < 18 years of age) with HoFH and of adult patients with FC and any remainder to fund working capital, capital expenditures and other general corporate purposes, including repayment of the principal loan balance as it comes due under our loan and security agreement, or the Loan and Security Agreement, with Hercules Technology II, L.P. and Hercules Technology III, L.P., collectively the Hercules Funds. We will not receive any proceeds from the shares sold by the Selling Stockholders. For a more complete description of our intended use of the net proceeds from this offering, see “Use of Proceeds.” |

| NASDAQ Global Market symbol |

“AEGR” |

| Risk factors |

You should read the “Risk Factors” section of this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

The number of shares of common stock to be outstanding after this offering is based on 17,664,641 actual shares of common stock outstanding as of May 31, 2011. The number of shares of common stock to be outstanding after this offering excludes:

| § | 2,174,642 shares of common stock issuable upon the exercise of options outstanding as of May 31, 2011 at a weighted average exercise price of $4.79 per share; |

| § | 29,890 shares of restricted common stock subject to vesting as of May 31, 2011; |

| § | 107,779 shares of common stock subject to outstanding warrants outstanding as of May 31, 2011, with a exercise price of $6.68 per share; and |

| § | 2,814,971 additional shares of common stock available for future issuance under our 2010 Stock Option and Incentive Plan, or 2010 Option Plan, as of May 31, 2011, which is subject to an annual increase of shares of common stock available for issuance under the 2010 Option Plan equal to four percent of the number of shares of common stock issued and outstanding on the immediately preceding December 31. |

Except as otherwise indicated, all information in this prospectus reflects or assumes no exercise of the underwriters’ over-allotment option.

6

Table of Contents

SUMMARY FINANCIAL DATA

You should read the following summary financial data together with the “Capitalization,” “Selected Financial Data,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of this prospectus and our financial statements and the related notes appearing at the end of this prospectus. We have derived the statement of operations data for the years ended December 31, 2008, 2009 and 2010 from our audited financial statements appearing at the end of this prospectus. We have derived the statement of operations data for the three months ended March 31, 2010 and 2011 and the balance sheet data as of March 31, 2011 from our unaudited financial statements appearing at the end of this prospectus. We have derived the statement of operations data for the period from February 4, 2005 (inception) to March 31, 2011 from our unaudited financial statements appearing at the end of this prospectus. The unaudited financial statements have been prepared on the same basis as our audited financial statements and include, in the opinion of management, all adjustments that management considers necessary for a fair presentation of the financial information set forth in those statements. Our historical results for any prior period are not necessarily indicative of results expected in any future period and our interim results are not necessarily indicative of results for a full year.

| Year Ended December 31, | Three Months Ended March 31, |

Period from February 4, 2005 (inception) to March 31, |

||||||||||||||||||||||

| 2008 | 2009 | 2010 | 2010 | 2011 | 2011 | |||||||||||||||||||

| (in thousands, except share and per share data) | (Unaudited) | |||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||||

| Costs and Expenses: |

||||||||||||||||||||||||

| Research and Development |

$ | 17,712 | $ | 7,041 | $ | 7,629 | $ | 1,066 | $ | 3,297 | $ | 53,164 | ||||||||||||

| General and administrative |

5,185 | 3,075 | 5,921 | 972 | 3,490 | 28,036 | ||||||||||||||||||

| Total costs and expenses |

22,897 | 10,116 | 13,550 | 2,038 | 6,787 | 81,200 | ||||||||||||||||||

| Loss from operations |

(22,897 | ) | (10,116 | ) | (13,550 | ) | (2,038 | ) | (6,787 | ) | (81,200 | ) | ||||||||||||

| Interest expense |

(1,127 | ) | (2,083 | ) | (2,404 | ) | (601 | ) | (113 | ) | (7,010 | ) | ||||||||||||

| Interest income |

533 | 177 | 109 | 18 | 68 | 2,784 | ||||||||||||||||||

| Change in fair value of warrant liability |

91 | (174 | ) | (416 | ) | — | — | (263 | ) | |||||||||||||||

| Other than temporary impairment on securities |

(1,665 | ) | — | (30 | ) | — | — | (2,466 | ) | |||||||||||||||

| Other income, net |

31 | — | 244 | — | — | 275 | ||||||||||||||||||

| Loss before income taxes |

(25,035 | ) | (12,196 | ) | (16,047 | ) | (2,622 | ) | (6,832 | ) | (87,879 | ) | ||||||||||||

| Benefit from income taxes |

— | — | 1,793 | 1,793 | — | 1,793 | ||||||||||||||||||

| Net loss |

(25,035 | ) | (12,196 | ) | (14,254 | ) | (829 | ) | (6,832 | ) | (86,086 | ) | ||||||||||||

| Less accretion of preferred stock dividends and other deemed dividends |

(6,242 | ) | (3,287 | ) | (8,751 | ) | (862 | ) | — | (23,663 | ) | |||||||||||||

| Net loss attributable to common stockholders |

$ | (31,277 | ) | $ | (15,483 | ) | $ | (23,005 | ) | $ | (1,691 | ) | $ | (6,832 | ) | $ | (109,750 | ) | ||||||

| Net loss attributable to common stockholders per share — basic and diluted |

$ | (20.92 | ) | $ | (9.35 | ) | $ | (5.07 | ) | $ | (0.99 | ) | $ | (0.39 | ) | |||||||||

| Weighted-average shares outstanding — basic and diluted |

1,495,375 | 1,656,732 | 4,537,407 | 1,701 | 17,642 | |||||||||||||||||||

7

Table of Contents

| As of March 31, 2011 | ||||||||

| (Actual) | (As adjusted)(1) | |||||||

| (Unaudited) | ||||||||

| Balance Sheet Data: |

||||||||

| Cash and cash equivalents |

$ | 46,828 | $ | 100,505 | ||||

| Total assets |

50,014 | 103,691 | ||||||

| Long term debt |

10,000 | 10,000 | ||||||

| Deficit accumulated during the development stage |

(97,821 | ) | (97,821 | ) | ||||

| Total stockholders’ equity |

$ | 35,613 | 89,290 | |||||

| (1) | As adjusted to give effect to the sale by us in this offering of 3,250,000 shares of common stock at an assumed public offering price of $17.72 per share, after deducting underwriting discounts and commissions and the estimated offering expenses payable by us, and the application of the net proceeds as described under “Use of Proceeds.” |

Each $1.00 increase (decrease) in the public offering price per share would increase (decrease) each of cash and cash equivalents, total assets and total stockholders’ equity by approximately $3.1 million, assuming that the number of shares we are offering, as set forth on the cover page of this prospectus, remains the same and that the underwriters do not exercise their over-allotment option. Depending on market conditions and other considerations at the time we price this offering, we may sell a greater or lesser number of shares than the number set forth on the cover page of this prospectus. An increase (decrease) of 1,000,000 in the number of shares we are offering would increase (decrease) each of cash and cash equivalents, total assets and total stockholders’ equity by approximately $16.7 million, assuming the public offering price per share remains the same. An increase of 1,000,000 in the number of shares we are offering, together with a $1.00 increase in the public offering price per share, would increase each of cash and cash equivalents, total assets and total stockholders’ equity by approximately $20.7 million. A decrease of 1,000,000 in the number of shares we are offering, together with a $1.00 decrease in the public offering price per share, would decrease each of cash and cash equivalents, total assets and total stockholders’ equity by approximately $18.8 million. This information is illustrative only, and following the pricing of this offering, we will update this information based on the actual public offering price and other terms of this offering.

8

Table of Contents

Investing in our common stock involves a high degree of risk. Before you decide to invest in our common stock, you should consider carefully the risks described below, together with the other information contained in this prospectus, including our financial statements and the related notes appearing at the end of this prospectus. We believe the risks described below are the risks that are material to us as of the date of this prospectus. If any of the following risks occur, our business, financial condition, results of operations and future growth prospects could be materially and adversely affected. In these circumstances, the market price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Financial Position and Capital Requirements

We have incurred significant operating losses since our inception, and anticipate that we will incur continued losses for the foreseeable future.

We are a development stage company with a limited operating history. To date, we have primarily focused on developing our lead compound, lomitapide. We have funded our operations to date primarily through proceeds from the private placement of convertible preferred stock, convertible debt, venture debt and the proceeds from our initial public offering. We have incurred losses in each year since our inception in February 2005. Our net losses were approximately $25.0 million, $12.2 million and $14.3 million for the years ended December 31, 2008, 2009 and 2010, respectively, and $0.8 million and $6.8 million for the quarters ended March 31, 2010 and 2011, respectively. As of March 31, 2011, we had an accumulated deficit of approximately $97.8 million. Substantially all of our operating losses resulted from costs incurred in connection with our development programs and from general and administrative costs associated with our operations.

The losses we have incurred to date, combined with expected future losses, have had and will continue to have an adverse effect on our stockholders’ equity and working capital. We expect our research and development expenses to increase in connection with our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH and our planned Phase III pediatric clinical trial to evaluate lomitapide for the treatment of pediatric and adolescent patients (> 7 to < 18 years of age) with HoFH, Phase III clinical trial of lomitapide for the treatment of adult patients with FC and other potential studies or clinical trials of lomitapide. In addition, if we obtain marketing approval for lomitapide, we will likely incur significant sales, marketing, in-licensing and outsourced manufacturing expenses, as well as continued research and development expenses. In addition, we have incurred and expect to continue to incur additional costs associated with operating as a public company. As a result, we expect to continue to incur significant and increasing operating losses for the foreseeable future. Because of the numerous risks and uncertainties associated with developing pharmaceutical products, we are unable to predict the extent of any future losses or when we will become profitable, if at all.

We have not generated any revenue from lomitapide or any other product candidate and may never be profitable.

Our ability to become profitable depends upon our ability to generate revenue. To date, we have not generated any revenue from our development stage product candidates, including our lead compound, lomitapide, and we do not know when, or if, we will generate any revenue. We do not expect to generate significant revenue unless or until we obtain marketing approval of, and commercialize, lomitapide. Our ability to generate revenue depends on a number of factors, including our ability to:

| § | submit our NDA based on our Filing Data with the FDA, and submit our MAA with the EMA; |

| § | successfully complete our ongoing pivotal Phase III clinical trial for the treatment of patients with HoFH; |

| § | develop and obtain regulatory approval for a protocol for a Phase III pediatric clinical trial to evaluate lomitapide for treatment of pediatric and adolescent patients (> 7 to < 18 years of age) with HoFH; |

9

Table of Contents

| § | develop and obtain regulatory approval for a protocol for a Phase III clinical trial of lomitapide for the treatment of adult patients with FC; |

| § | contract for the manufacture of commercial quantities of lomitapide at acceptable cost levels if marketing approval is received; and |

| § | establish sales and marketing capabilities to effectively market and sell lomitapide in the United States and the European Union. |

Even if lomitapide is approved for commercial sale in one or both of the initial indications that we are pursuing, the diagnosis criteria in the final label may define the patient populations narrowly thus limiting intended users, or lomitapide may not gain market acceptance or achieve commercial success. In addition, we anticipate incurring significant costs associated with commercializing any approved product. We may not achieve profitability soon after generating product revenue, if ever. If we are unable to generate product revenue, we will not become profitable and may be unable to continue operations without continued funding.

We may need substantial additional capital in the future. If additional capital is not available, we will have to delay, reduce or cease operations.

We may need to raise additional capital to fund our operations and to develop and commercialize lomitapide. Our future capital requirements may be substantial and will depend on many factors including:

| § | the results of our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH; |

| § | the cost, timing and outcomes of seeking marketing approval of lomitapide for the treatment of patients with HoFH in the United States and the European Union; |

| § | our ability to develop and obtain regulatory approval for a protocol for a Phase III pediatric clinical trial to evaluate lomitapide for treatment of pediatric and adolescent patients (> 7 to < 18 years of age) with HoFH; |

| § | our ability to develop and obtain regulatory approval for a protocol for a Phase III clinical trial of lomitapide for the treatment of adult patients with FC; |

| § | if regulatory approval for the Phase III clinical trial of lomitapide for the treatment of adult patients with FC is obtained, the cost and timing associated with conducting such clinical trial; |

| § | the cost of filing, prosecuting and enforcing patent claims; |

| § | exploration, clinical trials and possible label expansion of lomitapide for use in broader patient populations; |

| § | the costs associated with commercializing lomitapide if we receive marketing approval, including the cost and timing of establishing sales and marketing capabilities to market and sell lomitapide for the treatment of patients with HoFH; and |

| § | subject to receipt of marketing approval, revenue received from sales of approved products, if any, in the future. |

Based on our current operating plan, we anticipate that the net proceeds of this offering, together with our existing cash, cash equivalents and borrowing capacity under our Loan and Security Agreement with the Hercules Funds, will be sufficient to enable us to maintain our currently planned operations, including our continued product candidate development, at least through the next 24 months. However, changing circumstances may cause us to consume capital significantly faster than we currently anticipate. In February 2011, we entered into the Loan and Security Agreement with the Hercules Funds, for a $25.0 million credit facility. At the closing of the Loan and Security Agreement, we received an initial advance of $10.0 million, with interest-only payments for thirteen months. We may request additional term loan advances of up to $15.0 million. As of the date of this prospectus, we have a principal amount of $10.0 million outstanding under the

10

Table of Contents

Loan and Security Agreement. Other than the Loan and Security Agreement with the Hercules Funds, we have no committed external sources of funds. Additional financing may not be available when we need it or may not be available on terms that are favorable to us. In addition, we may seek additional capital due to favorable market conditions or strategic considerations, even if we believe we have sufficient funds for our current or future operating plans. If adequate funds are not available to us on a timely basis, or at all, we may be required to:

| § | terminate or delay clinical trials or other development activities for lomitapide for one or more indications for which we are developing lomitapide, in particular any clinical trial we initiate for the treatment of adult patients with FC; or |

| § | alter or scale back our continued establishment of sales and marketing capabilities or other activities that may be necessary to commercialize lomitapide. |

Raising additional capital may cause dilution to our existing stockholders, restrict our operations or require us to relinquish rights.

We may seek additional capital through a combination of private and public equity offerings, debt financings and collaborations and strategic and licensing arrangements. To the extent that we raise additional capital through the sale of equity or convertible debt securities, your ownership interest will be diluted, and the terms may include liquidation or other preferences that adversely affect your rights as a stockholder. Debt financing, if available, would result in increased fixed payment obligations and may involve agreements that include covenants limiting or restricting our ability to take specific actions such as incurring debt, making capital expenditures or declaring dividends. If we raise additional funds through collaboration, strategic alliance and licensing arrangements with third parties, we may have to relinquish valuable rights to our technologies, future revenue streams or product candidates, or grant licenses on terms that are not favorable to us.

Our limited operating history makes it difficult to evaluate our business and prospects.

We were incorporated in February 2005. Our operations to date have been limited to organizing and staffing our company and conducting product development activities, primarily for lomitapide. Consequently, any predictions about our future performance may not be as accurate as they could be if we had a longer operating history and experience in generating revenue. In addition, as a relatively young business, we may encounter unforeseen expenses, difficulties, complications, delays and other known and unknown factors.

Risks Associated with Product Development and Commercialization

We currently depend entirely on the success of our lead compound, lomitapide, which we are developing initially for the treatment of patients with HoFH. We are also developing a protocol for a clinical trial of lomitapide for the treatment of adult patients with FC. We may not receive marketing approval for, or successfully commercialize, lomitapide for any indication.

We are initially developing our lead compound, lomitapide, for the treatment of patients with HoFH, and are developing protocols for clinical trials of lomitapide for the treatment of pediatric patients with HoFH and adult patients with FC. Our business currently depends entirely on the successful development and commercialization of lomitapide. We have not yet demonstrated an ability to obtain marketing approval for any product candidate, we have no drug products for sale currently and we may never be able to develop marketable drug products. The research, testing, manufacturing, labeling, approval, sale, marketing and distribution of drug products are subject to extensive regulation by the FDA and other regulatory authorities in the United States and other countries, which regulations differ from country to country. We are not permitted to market lomitapide or any other product candidate in the United States until we receive approval of an NDA from the FDA, or in any foreign countries until we receive the requisite approval from such countries. We have not submitted an NDA to the FDA or comparable applications to other regulatory authorities or received marketing approval for lomitapide or any other product candidate.

11

Table of Contents

Obtaining approval of an NDA is an extensive, lengthy, expensive and uncertain process, and the FDA may delay, limit or deny approval of lomitapide for many reasons, including:

| § | we may not be able to demonstrate to the satisfaction of the FDA that lomitapide is safe and effective for any indication; |

| § | the results of clinical trials may not meet the level of statistical significance or clinical significance required by the FDA for approval; |

| § | the FDA may disagree with the number, design, size, conduct or implementation of our clinical trials; |

| § | the FDA may not find the data from preclinical studies and clinical trials sufficient to demonstrate that lomitapide’s clinical and other benefits outweighs its safety risks; |

| § | the FDA may disagree with our interpretation of data from preclinical studies or clinical trials and require that we conduct one or more additional trials; |

| § | the FDA may not accept data generated at our clinical trial sites; |

| § | the data collected from preclinical studies and clinical trials of any product candidate that we develop may not be sufficient to support the submission of an NDA; |

| § | the FDA may have difficulties scheduling an advisory committee meeting in a timely manner or the advisory committee may recommend against approval of our application or may recommend that the FDA require, as a condition of approval, additional preclinical studies or clinical trials, limitations on approved labeling or distribution and use restrictions; |

| § | the FDA may impose limitations on approved labeling, such as narrowing the diagnosis criteria for an indication thus limiting intended users; |

| § | the FDA may require development of a risk evaluation and mitigation strategy, or REMS, as a condition of approval; |

| § | the FDA may identify deficiencies in the manufacturing processes or facilities of third party manufacturers with which we enter into agreements for clinical and commercial supplies; or |

| § | the FDA may change its approval policies or adopt new regulations. |

Before we submit an NDA to the FDA for lomitapide for the treatment of patients with HoFH, we must complete our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH. In addition, we must complete other preclinical and clinical studies, such as a thorough QT study in healthy volunteers to evaluate the effect of lomitapide on the heart’s electrical cycle, known as the QT interval, studies to evaluate the interaction of lomitapide with other drugs, and a study of lomitapide in patients who are renally impaired. If, following submission, our NDA is not accepted for substantive review or approved, the FDA may require that we conduct additional clinical and non-clinical studies before it will reconsider our application.

In particular, it is possible that the FDA may not consider the results of our ongoing single-arm, dose titration, open-label pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH, once completed, to be sufficient for approval of lomitapide for this indication. For example, because the FDA normally requires two pivotal clinical trials to approve an NDA, even if we achieve favorable results in our ongoing pivotal Phase III clinical trial, the FDA may require that we conduct a second Phase III clinical trial if the FDA does not find the results to be sufficiently persuasive. Although the FDA has informed us that it is not opposed to our submitting an NDA based on the results of our ongoing Phase III clinical trial, it is possible that, even if we achieve favorable results in our ongoing Phase III clinical trial, the FDA may require us to conduct a second Phase III clinical trial, possibly using a different design, including if the FDA does not find the results from the single trial to be sufficiently persuasive. In addition, it is possible that the FDA could require that we conduct a clinical outcomes study for lomitapide for the treatment of patients with HoFH, demonstrating a reduction in cardiovascular events, either prior to or after the submission of our NDA. If the FDA requires additional studies or trials, we would incur increased costs and delays in the marketing approval process, which may require us to

12

Table of Contents

expend more resources than we have available. In addition, the FDA may not consider as sufficient our clinical trial strategy or any additional required studies or trials that we perform and complete. For example, the FDA may not accept our plan for a single Phase III clinical trial of lomitapide for the treatment of adult patients with FC.

Finally, any final labeling may be approved with limitations. For example, FDA has stated that our functional HoFH definition of patients with average fasting LDL-C greater than 300 mg/dL on maximally tolerated lipid lowering therapy closely resembles the severe refractory heterozygous familial hypercholesterolemia population. Thus, FDA may narrow the diagnosis criteria for HoFH included in the final label for lomitapide and these patients may be considered to be outside the HoFH population, reducing the estimated 6,000-patient addressable population.

The FDA may require an advisory committee to review and render an opinion on the NDA, which may be negative or may delay approval or limit lomitapide’s marketability.

The FDA has informed us that review of the NDA for lomitapide for the treatment of patients with HoFH at an FDA advisory committee meeting is highly likely. The FDA is not bound by the recommendation of an advisory committee, which is composed of clinicians, statisticians and other experts, but it generally follows such recommendations. The FDA may have difficulties scheduling an advisory committee meeting in a timely manner or the advisory committee may recommend against approval of our application or may recommend that the FDA require, as a condition of approval, additional preclinical studies or clinical trials, limitations on approved labeling or distribution and use restrictions. This would delay and increase the cost of the review process. Any delay in obtaining, or an inability to obtain, marketing approval could prevent us from commercializing lomitapide, generating revenue and achieving profitability.

We plan to submit our NDA for lomitapide based on our Filing Data, which is prior to completion of our pivotal Phase III clinical trial. If data obtained during the last 22 weeks of the trial are unfavorable, our ability to commercialize lomitapide may be adversely affected.

We are currently evaluating lomitapide in a pivotal Phase III clinical trial for the treatment of patients with HoFH. We anticipate that this trial will be completed in the third quarter of 2011. Unfavorable results or outcomes in this or other trials for lomitapide prior to its 78-week completion point would be a major set-back for the lomitapide development programs and for us. An unfavorable outcome in this trial may require us to delay, reduce the scope of, or eliminate this product development program, which could have a material adverse effect on us and the value of our common stock.

The numbers of patients suffering from HoFH and FC are small and have not been established with precision. If the actual number of patients with either of these conditions is smaller than we estimate or if any approval that we obtain is based on a narrower definition of these patient populations, our revenue and ability to achieve profitability will be adversely affected, possibly materially. For example, the FDA has stated that our functional HoFH definition of patients with average fasting LDL-C greater than 300 mg/dL on maximally tolerated lipid lowering therapy closely resembles the severe refractory heterozygous familial hypercholesterolemia population. This means that these patients may ultimately be considered to be outside the HoFH population.

There is no patient registry or other method of establishing with precision the actual number of patients with HoFH or FC in any geography. In a report that we commissioned, L.E.K. Consulting LLC, or LEK, an international business consulting firm, estimated that the total number of addressable patients with symptoms consistent with HoFH in each of the United States and, collectively, Germany, the United Kingdom, France, Italy and Spain, which are referred to herein as the European Union Five, is approximately 3,000 patients, or a combined total of approximately 6,000 patients. In the report that we commissioned, LEK estimated that there are approximately 1,000 patients in the United States and the European Union Five with FC who could be eligible for treatment with lomitapide. The total addressable market opportunity for lomitapide for the treatment of patients with HoFH or FC will ultimately depend upon, among other things, the diagnosis criteria included in the final label for lomitapide, if approved for sale for these indications, acceptance by the medical community

13

Table of Contents

and patient access, product pricing, and reimbursement. If the actual number of HoFH or FC patients is lower than we believe or if any approval that we obtain is based on a narrower definition of these patient populations, then the potential markets for lomitapide for these indications will be smaller than we anticipate. For example, the FDA has stated that our functional HoFH definition of patients with average fasting LDL-C greater than 300 mg/dL on maximally tolerated lipid lowering therapy closely resembles the severe refractory heterozygous familial hypercholesterolemia population. This means these patients may ultimately be considered to be outside the HoFH population, reducing the estimated 6,000-patient addressable population. Moreover, the medical literature has historically estimated a prevalence of HoFH, based solely on persons with the HoFH genotype, at approximately one person per million. In any event, if lomitapide is approved for either HoFH or FC, our product revenue may be limited, and it may be more difficult for us to achieve or maintain profitability.

In addition, we currently plan to seek approval of lomitapide initially for the treatment of patients with HoFH who are 18 years of age or older. To support approval for younger patients, we plan to initiate a Phase III pediatric clinical trial of lomitapide for the treatment of pediatric and adolescent patients (> 7 to < 18 years of age) with HoFH, but we do not expect to submit a supplemental NDA to expand our labeling to include this patient population prior to 2014. As a result, any FDA approval would likely, at least initially, be limited to use for treating adult patients with lomitapide. This would limit our initial product revenue and may make it more difficult for us to achieve or maintain profitability. We expect that our approach to seeking approval of lomitapide for FC also will involve initially seeking marketing approval solely for the adult patient population.

We may not obtain an ATU, or obtaining an ATU may adversely affect our ability to set market prices outside of France, either of which could have an adverse effect on our financial results.

We currently intend to apply for a Temporary Authorization for Use for lomitapide in France based on the Phase III clinical trial. An ATU is intended for drugs that treat serious or rare diseases where no suitable therapeutic alternative is available in France, and it allows such drugs to be used in a small number of patients prior to marketing approval. Obtaining an ATU from the French Health Products Safety Agency, or Afssaps, requires satisfying a number of conditions and involves a lengthy and complicated application process. Specifically, we will need to demonstrate, among other things, the following:

| § | lomitapide treats a serious or rare pathology; |

| § | other suitable treatments for such a pathology are not available in France; and |

| § | the benefit of lomitapide outweighs the risk. |

Though we believe lomitapide qualifies under the ATU’s requirements, the Afssaps may not agree that any or all of these conditions are satisfied. Specifically, the Afssaps may determine that apheresis or the drug Zocor are suitable treatments for HoFH, both of which are now available in France. Also, the Afssaps may find the data from the pivotal Phase III trial less compelling than data from a clinical trial conducted in France. Even if Afssaps were to grant an ATU for lomitapide, the Afssaps may suspend, withdraw or modify the terms of the ATU for reasons of public health or if the conditions leading to the granting of the ATU change.

If Afssaps grants an ATU for lomitapide, a price level will be negotiated with the French authorities. This negotiated price may adversely affect the market prices in other countries or jurisdictions where we may sell lomitapide if it is lower than the price that would have otherwise been set in such geographies.

We may not be able to generate enough revenue to cover our operating costs due to pricing or demand issues for lomitapide.

In 2007, the FDA granted lomitapide “orphan drug” status for the treatment of HoFH. “Orphan drug” designation is generally given to drugs that treat a rare disease or condition, defined, in part, as a patient population of fewer than 200,000 in the United States. In a report that we commissioned, LEK estimated that the total number of addressable patients with symptoms consistent with HoFH in each of the United States and, collectively, Germany, the United Kingdom, France, Italy and Spain, which are referred to in this prospectus as the European Union Five, is approximately 3,000 patients, or a combined total of approximately 6,000 patients. However, the

14

Table of Contents

FDA may not agree with the diagnostic criteria LEK employed to estimate the number of patients with HoFH and may define the HoFH population more narrowly. Regardless, with such a small potential patient market, we will need to set and charge a price for lomitapide that is significantly higher than that of most pharmaceuticals in order to generate enough revenue to fund our operating costs.

If our estimate regarding the number of patients in the United States are too high, or if our estimates about the achievable per-dose price for lomitapide are too high, we may not be able to generate revenue and meet our operating costs in the timeframe that we expect, or at all.

In earlier preclinical studies and clinical trials, lomitapide was associated with undesirable side effects, such as adverse gastrointestinal events, elevated liver enzymes and increases in mean hepatic fat levels. Patients in our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH have also experienced such undesirable side effects. Lomitapide may continue to cause such side effects or have other properties that could delay or prevent its marketing approval or result in adverse limitations in any approved labeling or on distribution and use of the product.

Undesirable side effects caused by lomitapide or any other product candidate that we develop could cause us, regulatory authorities or institutional review boards to interrupt, delay or halt clinical trials and could result in the delay or denial of marketing approval by the FDA or other regulatory authorities. In earlier studies conducted by us, researchers at the University of Pennsylvania, or UPenn, and Bristol-Myers Squibb Company, or BMS, lomitapide was associated with undesirable side effects. We have also observed some of these side effects to a lesser extent in our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH.

For example, in early Phase I and Phase II clinical trials of lomitapide conducted by BMS and UPenn, doses between 25 mg and 100 mg were associated with a very high rate of gastrointestinal adverse events, such as diarrhea, nausea and vomiting, as well as the accumulation of fat in the liver, or hepatic fat, in a significant percentage of patients and elevated liver enzymes in some patients. Although we believe that the high rate of discontinuations in these early Phase I and Phase II clinical trials due to gastrointestinal adverse events resulted in large part from the failure to employ dose titration, which is the gradual increase in dosing over time to allow the body to adapt to the impact of a higher dose, this may not be the case. Patients in our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH, where dose titration has been employed, have also experienced adverse gastrointestinal events, but to a lesser extent than those experienced in earlier clinical trials. Even if lomitapide gains marketing approval, if marketing experience or future clinical trials demonstrate an increased risk of gastrointestinal side effects, lomitapide may not gain market acceptance over other drugs approved for the treatment of the same indications that do not have such side effects and could be subject to adverse regulatory action by the FDA or foreign regulatory authorities.

A subset of patients in earlier Phase I and Phase II clinical trials of lomitapide experienced increased levels of liver enzymes, an indicator of liver cell damage and, in some cases, liver toxicity. Increases in liver enzymes observed in these earlier clinical trials were typically greater with higher doses of lomitapide, but occurred in some cases at lower doses. For example, in a Phase II clinical trial of lomitapide for the treatment of patients with HoFH, clinically significant elevations in the liver enzyme alanine transaminase, or ALT, were observed in three of six patients. In one patient, the dose of lomitapide was temporarily reduced per protocol, after which ALT returned to lower levels. The patient subsequently was able to resume the earlier, higher dose and continue to be titrated to the maximum dose. In the other two patients, transient elevations in ALT returned to lower levels with continued treatment. In our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH, as of May 31, 2011, four of the 23 patients remaining in the trial had experienced ALT elevations greater than five times the upper limit of normal. Of these four patients, three underwent a temporary dose reduction and have maintained study drug at a stable dose. One patient discontinued treatment for a period of seven weeks, after which time treatment was reinstated and the patient was able to maintain a stable dose and complete the trial per protocol. No patients have been removed from the trial due to liver function test elevations.

A subset of patients in earlier Phase I and Phase II clinical trials of lomitapide also experienced increases in mean hepatic fat levels. Although increases in hepatic fat in earlier clinical trials were typically greater with higher

15

Table of Contents

doses of lomitapide, increases also occurred in some cases at lower doses. For example, in a completed 12 week Phase II clinical trial of lomitapide, mean hepatic fat levels increased from week zero to week four, but then plateaued. In our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH, as of September 30, 2010, 22 patients who had hepatic fat measurements taken experienced an increase in hepatic fat from a mean of 1.0% to 9.0% at 26 weeks of treatment. Of the 23 patients that completed 56 weeks of treatment as of May 31, 2011 21 patients had hepatic fat measurements available. These 21 patients had a mean hepatic fat level of 7.3% at this measurement time. The threshold for mild steatosis, a condition of hepatic fat accumulation, is in the range of 5 to 6% fat. In addition, the median change in hepatic fat from baseline in these patients was 5.7% at 26 weeks of treatment and 4.4% at 56 weeks of treatment. Some studies suggest that patients who have hepatic steatosis that results from pre-existing conditions, such as obesity and type 2 diabetes, may be at an increased risk for more severe long-term liver consequences, such as hepatic inflammation and fibrosis. However, the consequences of hepatic steatosis that results from other factors, are unclear.

We will also provide to the FDA an analysis of biomarkers for hepatic inflammation and fibrosis using stored samples from a prior Phase II clinical trial as well as samples from our ongoing Phase III trial to better determine lomitapide’s impact on these biomarkers as a proxy for more significant liver complications. If the results of this analysis indicate a risk of hepatic inflammation and fibrosis, or if patients in our ongoing pivotal Phase III clinical trial of lomitapide for the treatment of patients with HoFH or future clinical trials have clinically significant hepatic fat accumulation or significantly elevated liver enzymes or other liver related side effects, the FDA or other regulatory authorities could delay or deny marketing approval for lomitapide. Also, even if lomitapide is approved, if marketing experience or future clinical trials demonstrate hepatic fat accumulation, significantly elevated liver enzymes or other liver related side effects, lomitapide may not gain market acceptance over other drugs approved for the treatment of the same indications that do not have such side effects and could be subject to adverse regulatory action by the FDA or foreign regulatory authorities.

In a 104 week dietary carcinogenicity study of lomitapide in mice, significantly increased incidences of tumors in the small intestine and liver were observed. The relationship of these findings in mice is uncertain with regard to human safety because they did not occur in a dose-related manner and liver tumors are common spontaneous findings in the strain of mice used in this study. In a 104 week oral carcinogenicity study of lomitapide in rats, there were no significant incidences of tumors. We submitted the results of both studies to the FDA in March 2011. Although the clinical significance of the findings in mice is unknown, marketing approval could be delayed, limited, or prevented as a result of these carcinogenicity data or carcinogenicity data from the rat study or ongoing clinical trials. Also, even if lomitapide is approved, if marketing experience or future preclinical studies or clinical trials demonstrate potential carcinogenicity, lomitapide may not gain market acceptance over other drugs approved for the treatment of the same indications that do not have such side effects and could be subject to adverse regulatory action by the FDA or foreign regulatory authorities.

Even if lomitapide or any other product candidate that we develop receives marketing approval, we or others may later identify undesirable side effects caused by the product, and in that event a number of potentially significant negative consequences could result, including:

| § | regulatory authorities may suspend or withdraw their approval of the product; |

| § | regulatory authorities may require the addition of labeling statements, such as warnings or contraindications or distribution and use restrictions; |

| § | regulatory authorities may require us to issue specific communications to healthcare professionals, such as “Dear Doctor” letters; |

| § | regulatory authorities may issue negative publicity regarding the affected product, including safety communications; |

| § | we may be required to change the way the product is administered, conduct additional preclinical studies or clinical trials or restrict the distribution or use of the product; |

| § | we could be sued and held liable for harm caused to patients; and |

| § | our reputation may suffer. |

16

Table of Contents

Any of these events could prevent us from achieving or maintaining market acceptance of the affected product candidate and could substantially increase commercialization costs.

Failures or delays in the commencement or completion of preclinical or clinical testing could result in increased costs to us and delay, prevent or limit our ability to generate revenue.

Failures or delays in the commencement or completion of preclinical studies or clinical testing could significantly affect our product development costs and delay, prevent or limit our ability to generate revenue. We do not know whether planned preclinical studies or clinical trials will begin on time or be completed on schedule, if at all. The commencement and completion of preclinical studies or clinical trials can be delayed or prevented for a number of reasons, including:

| § | findings in preclinical studies, such as the existence of pulmonary phospholipidosis, which is the accumulation in lung cells of phospholipids, or lipids with attached phosphate groups, or carcinogenicity; |

| § | difficulties obtaining regulatory approval to commence a clinical trial or complying with conditions imposed by a regulatory authority regarding the scope or term of a clinical trial; |

| § | delays in reaching or failing to reach agreement on acceptable terms with prospective contract research organizations, or CROs, and trial sites, the terms of which can be subject to extensive negotiation and may vary significantly among different CROs and trial sites; |

| § | insufficient or inadequate supply or quality of a product candidate or other materials necessary to conduct our clinical trials; |

| § | difficulties obtaining institutional review board, or IRB, approval to conduct a clinical trial at a prospective site; |

| § | challenges recruiting and enrolling patients to participate in clinical trials for a variety of reasons, including size and nature of patient population, proximity of patients to clinical sites, eligibility criteria for the trial, nature of trial protocol, the availability of approved effective treatments for the relevant disease and competition from other clinical trial programs for similar indications; |

| § | severe or unexpected drug-related side effects experienced by patients in a clinical trial; and |

| § | difficulties retaining patients who have enrolled in a clinical trial but may be prone to withdraw due to rigors of the trials, lack of efficacy, side effects or personal issues, or who are lost to further follow-up. |

Clinical trials may also be delayed or terminated as a result of ambiguous or negative interim results. In addition, a clinical trial may be suspended or terminated by us, the FDA, the IRBs at the sites where the IRBs are overseeing a trial, or a data safety monitoring board, or DSMB, overseeing the clinical trial at issue, or other regulatory authorities due to a number of factors, including:

| § | failure to conduct the clinical trial in accordance with regulatory requirements or our clinical protocols; |

| § | inspection of the clinical trial operations or trial sites by the FDA or other regulatory authorities; |

| § | unforeseen safety issues or lack of effectiveness; and |

| § | lack of adequate funding to continue the clinical trial. |

For example, in June 2007, we discontinued a Phase II clinical trial of lomitapide because of suspected microbial contamination, which we believe resulted in patients experiencing gastrointestinal adverse events at a rate, severity and time of onset inconsistent with prior clinical data for lomitapide. After extensive testing and other investigation, we believe that the bacterium B. cereus, which is most often identified with food borne illness, was introduced into the active pharmaceutical ingredient, or API, of the clinical supplies of the drug used in this trial. The existence of microbial contamination by B. cereus is consistent with the nature and intensity of the adverse events experienced in this trial. In previous clinical trials, all of which were conducted using a different lot of API, adverse events were milder, less frequent and typically experienced only after a few days of treatment. We subsequently manufactured a new lot of API and a new lot of clinical supplies utilizing a previously tested lot of

17

Table of Contents