Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Kraton Corp | d8k.htm |

Kraton Overview

Macquarie Capital

June 2011

Exhibit 99.1 |

Forward-Looking

Statement Disclaimer 2

This presentation may include “forward-looking statements” that reflect our plans, beliefs,

expectations and current views with respect to, among other things, future events and financial

performance. Forward-looking statements are often characterized by the use of words

such as “believes,” “estimates,” “expects,” “projects,”

“may,” “intends,” “plans” or “anticipates,” or by discussions of

strategy, plans or intentions. All forward- looking statements in this presentation are made

based on management's current expectations and estimates, which involve risks, uncertainties and

other factors that could cause actual results to differ materially from those expressed in

forward-looking statements. Readers are cautioned not to place undue reliance on forward-

looking statements. These risks and uncertainties are more fully described in “Part I. Item 1A.

Risk Factors” contained in our Annual Report on 10-K, as filed with the Securities and

Exchange Commission and as subsequently updated in our Quarterly Reports on Form 10-Q, and

include risks related to: conditions in the global economy and capital markets; our reliance on

LyondellBasell Industries for the provision of significant operating and other services; the

failure of our raw materials suppliers to perform their obligations under long- term supply

agreements, or our inability to replace or renew these agreements when they expire; limitations in

the availability of raw materials we need to produce our products in the amounts or at the prices

necessary for us to effectively and profitably operate our business; competition in our

end-use markets, by other producers of SBCs and by producers of products that can be

substituted for our products; our ability to produce and commercialize technological innovations;

our ability to protect our intellectual property, on which our business is substantially

dependent; infringement of our products on the intellectual property rights of others;

seasonality in our Paving and Roofing business; financial and operating constraints related to our

substantial level of indebtedness; product liability claims and other lawsuits arising from

environmental damage or personal injuries associated with chemical manufacturing; political and

economic risks in the various countries in which we operate; the inherently hazardous nature of

chemical manufacturing; health, safety and environmental laws, including laws that govern our

employees’ exposure to chemicals deemed harmful to humans; regulation of our customers,

which could affect the demand for our products or result in increased compliance costs;

international trade, export control, antitrust, zoning and occupancy and labor and employment

laws that could require us to modify our current business practices and incur increased costs; our

relationship with our employees; loss of key personnel or our inability to attract and retain new

qualified personnel; fluctuations in currency exchange rates ; the fact that we do not enter into

long-term contracts with our customers; a decrease in the fair value of our pension assets,

which could require us to materially increase future funding of the pension plan; and

concentration of ownership among our principal stockholder, which may prevent new investors from

influencing significant corporate decisions. We assume no obligation to update such information.

Further information concerning issues that could materially affect financial performance related

to forward looking statements can be found in our periodic filings with the Securities and

Exchange Commission. |

GAAP Disclaimer

3

This presentation includes the use of both GAAP (generally accepted accounting

principles) and non-GAAP financial measures. The non-GAAP financial measures are

EBITDA and Adjusted EBITDA. The most directly comparable GAAP financial measure

is net income/loss. A reconciliation of the non-GAAP financial measures used in this

presentation to the most directly comparable GAAP measure is included herein. We

consider EBITDA and Adjusted EBITDA important supplemental measures of our

performance and believe they are frequently used by investors and other interested

parties in the evaluation of companies in our industry. EBITDA and Adjusted EBITDA

have limitations as analytical tools and should not be considered in isolation or as a

substitute for analysis of our results under GAAP in the United States. |

37%

21%

42%

4

Kraton Overview

We invented and commercialized Styrenic Block

Copolymer (SBC) technology nearly 50 years ago.

We believe that we hold #1 market share positions in

each of our end-use markets providing industrial,

consumer and geographical diversification that is second

to none.

We design and manufacture customized SBC polymer

and compound solutions to meet our leading customers’

specific innovation needs.

We produce the following:

Unhydrogenated Styrenic Block Copolymers (USBCs).

Hydrogenated Styrenic Block Copolymers (HSBCs).

Isoprene Rubber and Isoprene Rubber Latex.

We currently offer approximately 800 products to more

than 700 customers, in over 60 countries.

We employ approximately 880 people in 9 locations in all

major regions of the world.

2010

revenue

of

$1,228

million

and

Adjusted

EBITDA

(1)

of

$195 million; 16% margin.

(1)

Adjusted EBITDA is GAAP EBITDA excluding management fees, restructuring and related charges,

non-cash expenses, and the gain on extinguishment of debt.

(2)

Management estimates.

2010 Revenue by End-Use

(2)

2010 Revenue by Geography

(2)

North and

South

America

Europe,

Middle

East &

Africa

Asia Pacific

32%

28%

31%

7%

2%

Paving and

Roofing

Adhesives,

Sealants and

Coatings

Other

Emerging

Businesses

Advanced

Materials

Clear SBC Market Leader Globally |

5

Investment Highlights

Leadership

Clear leader in the fast growing, attractive SBC market

More

than

1.6x

the

size

of

our

largest

competitor

in

each

of

our

end-use

markets

The only producer with a global footprint and service capabilities

Innovation-

Driven Top-

Line Growth

Most-productive innovator of new SBC polymers

Successfully leveraging product knowledge and technical expertise to commercialize

next generation of innovative solutions

Earnings

Growth

Driven by compelling organic growth platforms, expanding presence in Asia, sustained

volume growth and new product introductions

Margin

enhancement

through

continued

“Smart

Pricing”

strategy

and

innovation

Created meaningful operating leverage through significant improvement in cost structure

Investing

capital

in

high-return

projects

–

driving

profitable

growth

in

key

products

and

geographies

Experience

Strong leadership team demonstrating continuous improvement in productivity,

innovation and margin improvement

High

Barriers to

Entry

Patented technology, custom designed product, process excellence, global reach

and customer relationships create strong competitive position that cannot be

matched by existing or potential competitors

Competitive position allows for price leadership

Best-in-class service levels: 100% of products delivered on-demand on-time

|

6

SBCs Enhance Performance Attributes

Durability

Elasticity

Impact

Soft Touch

Clarity

Adhesion

We are a Highly Engineered, Performance Materials Business

Recyclable |

7

Before Kraton

After Kraton

Kraton Makes Products Better

Stretch in legs only

(Spandex)

Not a fitted garment

High leakage rate

Overall improvement in stretch

(where it’s needed)

Better fit

Low leakage rate

Kraton market share: 50%

2001

–

2009

CAGR:

11.5%

Kraton material as % of Diaper cost: <2%

Phthalate plasticizers are

used to make PVC soft

but they can leach from

finished products and

create health concerns

Limited recyclability

PVCs are unsafe when

burned or incinerated

improperly

Environmentally

friendly

–

100%

recyclable

Kraton imparts softness, toughness and clarity

Plasticizer & chlorine free

Kraton material as % of finished product cost: <5% |

8

SBCs Are a Growth Industry

SBC Industry Volume (kT)

(1)

SBCs Grow Faster Than GDP

Adoption and penetration of SBCs into

new applications and end-markets lead to

industry growth of ~2x global GDP

Growing demand from emerging

economies

Innovation and new SBC product

introductions

End use application growth (e.g.,

PVC alternatives for wire & cable

and medical applications such as IV

bags, etc.)

Growing demand for

environmentally friendly and greener

alternatives in electronics, medical,

automotive and baby care markets

Low cost relative to value added /

performance with limited substitution risk

(1)

Management Estimates. Excludes footwear end-use in which Kraton does not actively compete

675

1,112

1,599

2001

2009

2014 |

9

Clear Leader in Attractive Markets

#1

~77%

Adhesives, Sealants,

and Coatings

Advanced Materials

#1

~74%

Paving and Roofing

#1

~63%

Emerging Businesses

(4)

#1

100%

32%

30%

28%

7%

1.9x

2.0x

1.6x

N/A

Source:

Management estimates.

(1)

Based on 2010 sales of $1,228 million.

(2)

Industry volume growth from 2001-2009, Emerging Businesses growth rate refers to Kraton’s

Isoprene Rubber (“IR”) and Isoprene Rubber Latex (“IRL”) growth from 2005-2009.

(3)

Management’s estimates vs. next largest competitor based on 2009 sales.

(4)

The Emerging Businesses end use market includes our IR and IRL business. We believe that we are the

only major third-party supplier of IR and IRL, and therefore end use market share metrics

are not meaningful. #1 Market Position and More than 1.6x the Size of Our Closest

Competitors Top 4 Market

Share

5.9%

7.4%

6.5%

26.8%

2010 Revenue

(1)

Growth

(2)

Market Position

Kraton Market

Share Relative To

#2 Competitor

(3) |

10

Unparalleled Global Manufacturing and Service

Capability

Belpre, Ohio U.S.

Manufacturing Facility

Global Headquarters

Houston, Texas U.S.

Innovation Center

Paulinia, Brazil

Manufacturing Facility

Innovation Center

Mont St. Guibert,

Belgium

Technical Service Office

Wesseling, Germany

Manufacturing Facility

Kashima, Japan

Innovation Center

Manufacturing

Joint Venture

Berre, France

Manufacturing Facility

Amsterdam,

Innovation Center

Netherlands

Shanghai, China

Customer Service and

Technical Center |

20%

14%

13%

12%

14%

13%

11%

5%

2005

2006

2007

2008

2009

2010

Q1'11

TTM

Target

11

Profit Growth Through Innovation

Approximately 1,053 patents

granted and 349 pending

Innovation continuously

repositions sales mix, improves

margins and drives growth

Step-change advancement of

Big 6 Innovation Priorities

Wire and cable solutions

Elastic nonwovens

NEXAR™

membrane

technology

Oilfield service applications

Protective films

Automotive soft skin solutions

Innovation

Share

of

Total

Revenue

(%)

(1)

(1)

Innovation revenue defined as revenues of new products (e.g., new polymer, new application of an

existing polymer or new step out production technology) introduced within the last 5

years Vision 20/20: 20% of revenue at 20% margin premium

Increased in Period of

Strong Volume

Growth in Base

Business |

Compelling Organic

Growth Platforms 12

Advanced

Materials

Adhesives,

Sealants &

Coatings

Paving and

Roofing

Emerging markets growth.

Expansion into new and differentiated markets, such as

white elastomeric roof coatings, protective films, oilfield

service applications, spray and extrusion coatings, hot melt

adhesives, elastic adhesives, labels and sealant

applications.

Superior performing SBS modified emulsions for asphalt

modification.

Low VOC roof coating formulations for superior water

resistance, improved adhesion and reduced installation cost.

“Green”

PVC alternatives for the wire and cable industry.

Enabling technology for high performance fabric solutions.

“Soft Touch”

solutions for the automotive industry.

Co-extrusion technology for protective films.

Applications

Cariflex™

Isoprene

Rubber and

Isoprene

Rubber Latex

CariflexTM Isoprene Rubber and Isoprene Rubber Latex

Medical

applications

–

surgical

gloves,

medical

components.

Material

substitution

–

condoms.

NEXAR

®

–

high-end

membrane

technology

HiMA

Protective Films

Soft Skins

IRL Gloves |

Innovation-led Top

Line Growth Tremendous growth

Rapidly capture share from $2.2 billion

natural rubber latex industry

Margins well in excess of rest of business

Kraton maintains ~86% market share

Challenging process technology to replicate

for competitors and new entrants

IR line conversion at Belpre, Ohio will be

complete second quarter 2011

IRL capacity expansion of Paulinia, Brazil

facility completed May 2011

Increased IRL capacity by approximately

33%

Case

Study:

IR

and

IR

Latex

Revenue

Growth

13

Key Attributes

$15

$22

$23

$35

$86

$79

$61

2005

2006

2007

2008

2009

2010

TTM

Q1'11

(US$ in millions) |

27

62

149

2001

2009

2014

Investing for Growth In Asia

14

Asia

Pacific

SBC

market

–

53%

of

global SBC consumption by volume in

2009

(1)

In 2010 Asia Pacific accounted for

21% of our total revenue, with 43%

derived from higher margin HSBC

products

In 2010 relocated Shanghai, China

office to a new facility (double the size

of the previous location)

Expanded warehouse capacity in

Shanghai Waigaoqiao Free Trade

Zone

Proposed HSBC expansion in Asia

Forecast strong worldwide growth in HSBC

driven by innovation

Initiated project assessment for a new 30 kT

per year HSBC plant in Asia

Site selection expected Q2 2011 with start-

up as early as second half of 2013

Asia is an important component of Kraton’s growth strategy

(1)

Management estimates. Includes SBC consumption for footwear, a market in which Kraton does not

actively compete. Asian HSBC Industry Demand Trends (kT) |

15

$151

$176

$255

$301

2007

2008

2009

2010

Historical Financial

Summary

$1,066

$920

$1,171

$1,228

2007

2008

2009

2010

$91

$152

$68

$195

2007

2008

2009

2010

358

313

260

307

2007

2008

2009

2010

Volume (kT)

Revenue

(1)

Gross Profit

Adjusted EBITDA

(2)

Margin:

14.2%

21.8%

18.1%

24.5%

Margin:

6.4%

13.0%

9.9%

15.8%

(1)

Excludes by-product revenue.

(2)

Adjusted EBITDA is GAAP EBITDA excluding management fees, restructuring and related charges,

non-cash expenses, and the gain on extinguishment of debt.

US $ in millions |

Impact of Monomer

Volatility 16

Kraton has demonstrated its core competence of managing volatility in monomer costs by raising

prices and passing through costs

We

have

implemented

44

price

increases

since

our

IPO

in

December

2009,

including

24

year-to-date

$568

$537

$805

$976

$918

$632

$707

$781

$849

$864

$1,046

$970

$810

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Gross

Profit

per

Ton

@

LIFO

$636

$664

$1,054

$932

$190

$501

$865

$998

$949

$1,034

$1,024

$885

$1,068

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Gross Profit per Ton @ FIFO

-

-$34.3

-$9.3

-$1.7

-$8.1

Quarterly

Impact

of

LIFO

to

FIFO

Adjustment

$5.2

$11.9

$22.3

$12.8

$13.3

$7.3

$14.7

$21.0

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

$2.3 |

17

Drivers of Free Cash Flow

$195

million

2010

Adjusted

EBITDA

(1)

Meaningful

operating

leverage

–

$50

million

of

annualized

net

cost

reduction

since 2008

Favorable demand drivers are expected to drive strong volume growth

Attractive

Earnings

Power

Historical

annual

maintenance

capex

of

$16

-

$22

million

Low Level of

Maintenance

Capex

$36 million of cash at March 31, 2011

Net Debt-to-Cap ratio of 41.5% at March 31, 2011, with Net Debt to Adjusted

EBITDA of 1.7x

Refinanced

balance

sheet

February

2011

–

No

significant

debt

maturities

until

2015

Capital Structure

2011 full-year tax rate of approximately 9%

$282 million NOL balance as of December 31, 2010

Low Cash

Tax Rate

Reduced quantity of finished goods inventory by nearly 20% excluding isoprene

rubber build, since year end 2006, with minimal impact on service levels

Target working capital (excl. cash) at 25%-27% of revenue

Moderate

Working Capital

Needs

(1)

Adjusted EBITDA is GAAP EBITDA excluding sponsor fees, restructuring and related charges, non-cash

expenses, and the gain on extinguishment of debt |

Expertise in market

and application development, high quality manufacturing, customer service offering, and core

end-use focus Provide

application-based

solutions

to

meet

customers’

needs

Commercialize

next

generation

of

innovations,

e.g.,

Nexar™

non-woven

and

industrial

fibers,

oilfield service applications, automotive soft skins, etc.

Margin enhancement by improving or eliminating marginally profitable products

Extract value for complexity

Continue to identify opportunities to contract with key customers

Proactively manage raw material price volatility

Evaluating options for additional HSBC capacity in Asia

Complete Polyisoprene rubber (IR) expansion at Belpre, Ohio and Isoprene rubber latex (IRL)

capacity expansion at Paulinia, Brazil

Evaluate options for future expansion of isoprene rubber latex capacity

Identify / pursue additional opportunities for cost reduction and productivity improvement

Execute on new IR manufacturing capacity at Belpre

Leverage

Leadership

Position

Drive Growth

Through

Innovation

Continue

Smart Pricing

Invest in

Growth and

Infrastructure

Continuous

Productivity

Improvement

Go-Forward Business Strategy

18 |

Appendix

19 |

Advanced Materials End

Use Review 20

TTM Revenue Profile

Change in Sales Revenue

End Use Revenue

Change in Sales Revenue

US $ in millions

AM |

Adhesives, Sealants and

Coatings End Use Review TTM Revenue Profile

Change in Sales Revenue

21

End Use Revenue

US $ in millions

ASC |

Paving and Roofing

End-Use Review 22

TTM Revenue Profile

Change in Sales Revenue

End Use Revenue

Change in Sales Revenue

US $ in millions

P&R |

Emerging Businesses End

Use Review 23

TTM Revenue Profile

Sales Revenue

End Use Revenue

US $ in millions

US $ in millions |

2010 Operating Revenue

and Adjusted EBITDA (1)

Walk

Operating Revenue

Adjusted EBITDA

US $ in millions

24

(1)

Adjusted EBITDA is GAAP EBITDA excluding management fees, restructuring and related charges,

non- cash expenses, and the gain on extinguishment of debt.

$968

$1,228

$167

$160

$(19)

$(48)

FY 2009

Volume

Price

FX

By-Product

FY 2010

$91

$195

$74

$160

$(111)

$(13)

$(6)

2009

Volume

Price

COGS

R&D/SG&A

FX/Other

2010 |

Volume (kT)

Selected Financial Trends –

Q1 2011

(1)

Adjusted EBITDA is GAAP EBITDA excluding restructuring and related charges, non-cash

compensation expenses, and loss on the extinguishment of debt.

25

Revenue

(US $ in Millions)

Gross Profit and Gross Margin

(US $ in Millions)

$69

$59

$87

25.3%

20.6%

25.2%

0

20

40

60

80

100

120

Q1 10

Q4 10

Q1 11

$273

$288

$345

$0

$50

$100

$150

$200

$250

$300

$350

Q1 10

Q4 10

Q1 11

Adjusted EBITDA

(1)

(US $ in Millions)

$43

$34

$56

15.6%

11.9%

16.2%

0

10

20

30

40

50

60

70

80

Q1 10

Q4 10

Q1 11

Adjusted

EBITDA

Margin |

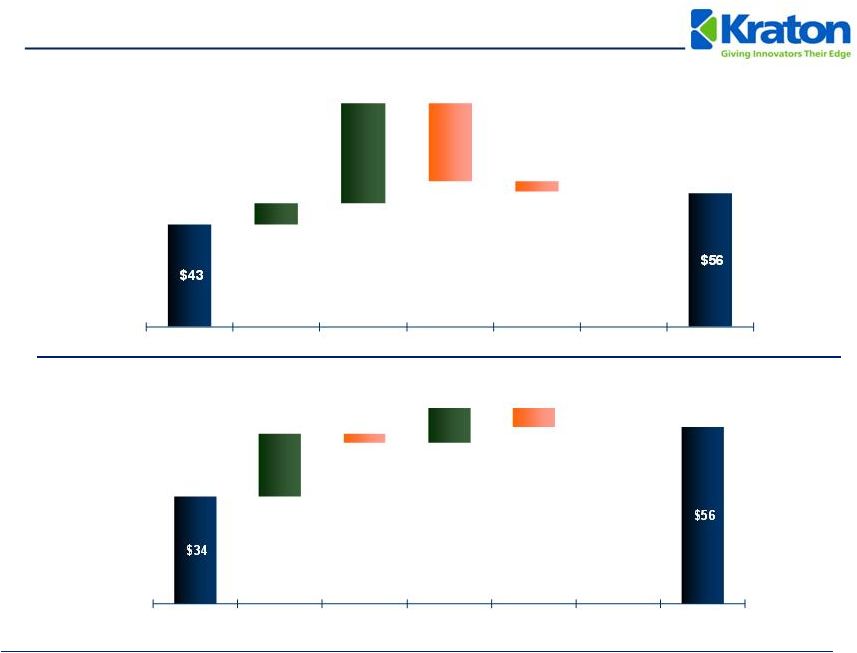

Q1 2011 Adjusted

EBITDA (1)

Walk

Q1 2011 vs. Q4 2010

Q1 2011 vs. Q1 2010

US $ in millions

(1)

Adjusted EBITDA is GAAP EBITDA excluding restructuring and related charges, non-cash

compensation expenses, and loss on the extinguishment of debt.

26

Q1 2010

Volume

Price

COGS

R&D/SG&A

FX/Other

Q1 2011

Q1 2011

Volume

Price

COGS

R&D/SG&A

FX/Other

Q1 2011

$9

$42

$(33)

$-

$(4)

$20

$(3)

$11

$-

$(6) |

Selected 2011

Estimates Working capital (excluding cash) as a % of

revenue

25% to 27%

Capital spending

$80 to $85 million

Interest expense

(1)

~$31 million

Research & development

~$27 million

SG&A

~ $100 million

Depreciation and amortization

~$61 million

Book tax rate

~9%

27

(1)Includes accelerated write-off of deferred financing costs associated with the debt

refinancing of $5 million. |