Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - CIT GROUP INC | e43938_8k.htm |

| EX-99.1 - PRESENTATION - CIT GROUP INC | e43938ex99_1.htm |

EXHIBIT 99.2

|

2011 AMERICAN FINANCIAL SERVICES Glenn Votek, Executive Vice President and Treasurer June 8, 2011 |

Important Notices

This presentation contains forward-looking statements within the meaning of applicable federal securities laws that are based upon our current expectations and assumptions concerning future events, which are subject to a number of risks and uncertainties that could cause actual results to differ materially from those anticipated. The words “expect,” “anticipate,” “estimate,” “forecast,” “initiative,” “objective,” “plan,” “goal,” “project,” “outlook,” “priorities,” “target,” “intend,” “evaluate,” “pursue,” “commence,” “seek,” “may,” “would,” “could,” “should,” “believe,” “potential,” “continue,” or the negative of any of those words or similar expressions is intended to identify forward-looking statements. All statements contained in this presentation, other than statements of historical fact, including without limitation, statements about our plans, strategies, prospects and expectations regarding future events and our financial performance, are forward-looking statements that involve certain risks and uncertainties. While these statements represent our current judgment on what the future may hold, and we believe these judgments are reasonable, these statements are not guarantees of any events or financial results, and our actual results may differ materially. Important factors that could cause our actual results to be materially different from our expectations include, among others, the risk that CIT is unsuccessful in refining and implementing its strategy and business plan, the risk that CIT’s changes in its management team affects CIT’s ability to react to and address key business and regulatory issues, the risk that CIT is delayed in transitioning certain business platforms to CIT Bank and may not succeed in developing a stable, long-term source of funding, and the risk that CIT continues to be subject to liquidity constraints and higher funding costs. Further, there is a risk that the valuations resulting from our fresh start accounting analysis, which are inherently uncertain, will differ significantly from the actual values realized, due to the complexity of the valuation process, the degree of judgment required, and changes in market conditions and economic environment. We describe these and other risks that could affect our results in Item 1A, “Risk Factors,” of our latest Annual Report on Form 10-K filed with the Securities and Exchange Commission. Accordingly, you should not place undue reliance on the forward-looking statements contained in this presentation. These forward-looking statements speak only as of the date on which the statements were made. CIT undertakes no obligation to update publicly or otherwise revise any forward-looking statements, except where expressly required by law.

This presentation is to be used solely as part of CIT management's continuing investor communications program. This presentation shall not constitute an offer or solicitation in connection with any securities.

|

|

2 |

Key Messages

-

Strong franchise

-

Aggressively restructuring the liability profile

-

Bank strategy is well underway

-

Improved risk management and controls

-

Strong capital and liquidity position

|

|

3 |

CIT Overview

| Bank Holding Company With Over 100 Years Commercial Lending Experience |

| Focused on Small Businesses and Middle-Market Companies |

| Solid Business Operating Within Attractive Markets Generating High-yielding Assets |

| $51 Billion in Assets and Market Capitalization Over $8 Billion |

|

|

4 |

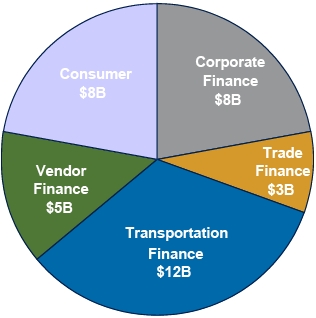

Financial Solutions for Small Business and Middle Market Companies

| Corporate Finance |

Lending, leasing, advisory and other financial services to small and middle market companies |

| Trade Finance |

Factoring, lending, receivables management and trade finance to companies in retail supply chain |

| Transportation Finance |

Lending, leasing and advisory services to the transportation industry, principally aerospace and rail |

| Vendor Finance |

Financing and leasing solutions to manufacturers and distributors around the globe |

| Consumer | Liquidating pool of largely government-guaranteed student loans |

Finance and Leasing Assets (1)

Total $36 Billion

(1) Finance and Leasing assets include loans, operating leases and assets held for sale; data as of 3/31/2011

|

|

5 |

Significant Progress Since the Beginning of 2010

| Hire and Retain Key Personnel |

|

| Restructure and Refine Business Model |

|

| Develop and Implement Plan to Reduce Funding Costs |

|

| Continue to Build Hybrid Funding Model |

|

| Improve Bank Holding Company Capabilities |

|

|

|

6 |

Financial Performance Reflects Strategic Initiatives

| 2010 | 1Q11 | ||

|

|

|||

| Pre-Tax Income | $768 Million | $136 Million | |

|

|

|||

| Net Income | $517 Million | $66 Million | |

|

|

|||

| EPS (diluted) | $2.58 | $0.33 | |

|

|

|||

| 12/31/09 | 12/31/10 | 3/31/11 | |

|

|

|||

| Total Assets | $60 Billion | $51 Billion | $51 Billion |

|

|

|||

| Total Capital Ratio | 14.3% | 19.9% | 21.0% |

|

|

|||

| Book Value | $8.4 Billion | $8.9 Billion | $9.0 Billion |

| $41.99 per share | $44.48 per share | $44.85 per share | |

|

|

|||

| Tangible Book Value | $7.9 Billion | $8.5 Billion | $8.6 Billion |

| $39.48 per share | $42.50 per share | $42.97 per share | |

|

|

|||

|

|

7 |

Operational Progress: Business Update and Priorities

| Update | Priorities | ||

| Corporate Finance |

|

|

|

|

|

|||

| Trade Finance |

|

|

|

|

|

|||

| Transportation Finance |

|

|

|

|

|

|||

| Vendor Finance |

|

|

|

|

|

8 |

2011 Business Objectives

| 1 | Focus on growth in our commercial businesses, domestically and internationally |

| 2 | Improve profitability, including reducing our cost of capital and operating expenses |

| 3 | Expand the role of CIT Bank, both asset origination and funding capabilities |

| 4 | Advance our risk management, compliance and control functions |

| 5 | Substantially satisfy the open items in the Written Agreement |

|

|

9 |

Strategic Principles

| Controlled asset growth with strong risk management oversight |

| Balanced combination of Bank and Holding Company funding |

| Generate attractive ROA and ROE with moderate leverage |

| Attain investment grade ratings |

|

|

10 |

Long-term Target: Normalized Profit Model

| Key Metrics | Long-Term Target (1) |

Drivers / Assumptions |

| Finance Margin | 3.00% - 4.00% |

|

| Credit Provision | (0.75%) - (1.00%) |

|

| Other Income | 1.50% - 2.00% |

|

| Operating Expense | (2.00%) - (2.25%) |

|

| Pre-Tax Earnings | 2.00% - 2.50% |

|

| Taxes | (0.25%) - (0.75%) |

|

| Net Income (ROAEA) | 1.50% - 2.00% |

|

| ROE (Common Equity) | 10% - 15% |

|

| Key Assumptions |

|

Long-term Target reflects “steady state” performance objectives

(1) Expressed as percentages of average earning assets, except ROE

|

|

11 |

Financial Operating Models Vary by Segment

| Key Metrics (1) | Corporate Finance |

Trade Finance |

Transportation Finance |

Vendor Finance |

| Finance Margin | Medium | Low | Medium | High |

| Credit Provision | Medium | Low | Low | High |

| Other Income | Medium | High | Low | Medium |

| Operating Expenses | Medium | High | Low | High |

| ROA | Medium | Medium | High | Medium |

| Capital Required | Medium | Low | High | Low |

| Return on Economic Capital | All Segments Capable of Generating Double-Digit Risk-Adjusted ROEs | |||

| Key Performance Drivers |

|

|

|

|

(1) High, Medium and Low classifications are relative to Long-Term Target ranges

|

|

12 |

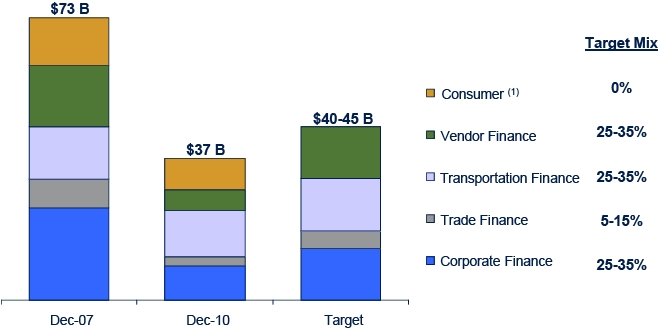

Portfolio Mix Evolving

Finance and Leasing Assets by Segment

-

Over $7 billion assets sold since January 2010 (pre-FSA)

-

Commercial portfolio optimization efforts near complete

-

Returning focus to growth in core commercial franchises

(1) Consumer consists of a liquidating pool of largely government-guaranteed student loans

|

|

13 |

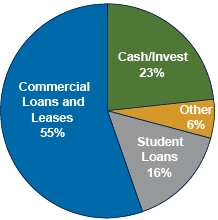

Factors Impacting Economic Margin

-

Balance Sheet Composition

-

$28 billion in core commercial portfolio

-

$11 billion of cash and short-term investments

-

~$8 billion of government-guaranteed student loans

-

-

High-cost Debt

-

Significant progress lowering costs

-

Opportunity for further reductions

-

$18 billion of 7% Series A/C Notes outstanding

-

$3 billion of 1st Lien debt at 6.25% current rate; trading well above par

-

-

Deposits < 15% of funding today

-

-

Other Factors

-

Asset sensitive in a low interest rate environment

-

Non-accrual percentages still well above historic norms

-

Total Assets - $51 billion (1)

(1) Data as of March 31, 2011

|

|

14 |

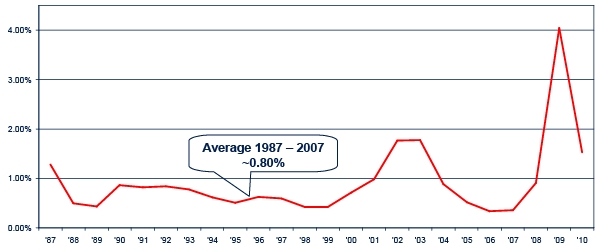

Credit Trends

25-Year Net Charge-off History (1)

-

Provision of 75 –100 bps of AEA implies ~100 bps of net charge-offs to AFR

-

Recent losses well-above 100 bps (consumer and cash-flow)

-

Historic losses well-below 100 bps (more Vendor assets in mix today)

-

(1) Excludes credit related losses on discontinued operations (including home lending) which were significant in 2008 Data may not be comparable due to changes in portfolio mix and reporting

|

|

15 |

Credit Underwriting Framework

| Risk Appetite |

| Authorities |

| Modeling & Scenario Analysis |

| Governance |

|

|

16 |

Capital Position is Strong

- Capital ratios (1) well above regulatory commitments and economic requirements

| CIT | CIT-Bank | Peers (2) | |

|

|

|||

| Tier 1 Capital | 20.1% | 56.1% | 10-15% |

| Total Capital | 21.0% | 56.5% | 13-18% |

| Leverage Ratio | 17.2% | 25.6% | 9-13% |

|

|

|||

- Implemented new economic capital framework in January

Based on “BASEL II – like” construct

Holistic view of risk:

Asset

Credit

Interest Rate

Model

Operational

FX & other

Allocations commenced 1Q 2011

“Excess” capital held at corporate

Ongoing review/refinement of models

|

|

|

| Capital Allocations by Segment (1) (3) | |

|

|

|

| Corporate Finance | 12% |

| Trade Finance | 9% |

| Transportation Finance | 15% |

| Vendor Finance | 10% |

| Consumer | 6% |

|

|

|

| Total Requirement (inc Corporate) | ~12% |

|

|

|

(1) Data as of March 31, 2011

(2) Peers consist of over a dozen banks and specialty finance companies

(3) Capital expressed as a percentage of Risk-weighted assets and is subject to change

|

|

17 |

Liquidity

-

Cash serves as key source of liquidity

-

Satisfies funding and other operating obligations

-

Protects against severe stress scenarios

-

Lack of access to capital markets or other funding sources

-

Customer line draws

-

Market volatility impacting collateral posting requirements

-

Other unanticipated funding obligations

-

|

|

|

| ($US MM) | Cash at 3/31/11 |

|

|

|

| Bank Holding Company | $6.2 |

| CIT Bank | 1.2 |

| Operating Subsidiaries | 1.1 |

| Restricted | 3.3 |

|

|

|

| Total Cash and Investments | $11.8 |

| Percentage of Total Assets | 23.3% |

| Bank Holding Company Cash to Total | |

| Assets | 12.2% |

|

|

18 |

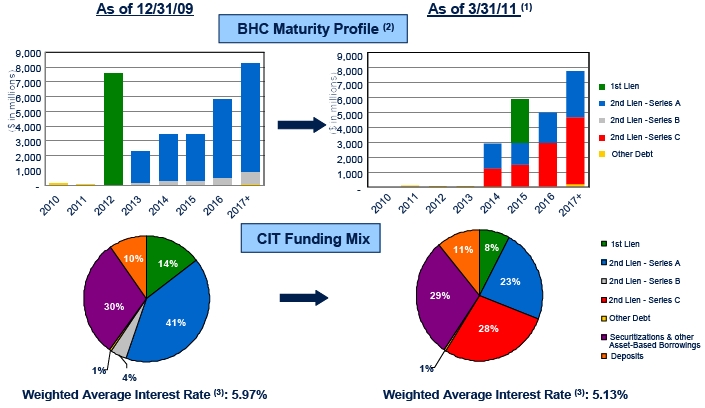

Extended Liquidity Horizon and Improved Debt Composition

(1) Pro forma for $2.5 billion Series A redemption in May 2011 and $8.8 billion Series A to C Exchange expected to close in June 2011

(2) BHC maturity profiles exclude secured debt that is primarily repaid with pledged collateral cash flows

(3) Excludes all FSA adjustments and amortization of fees and expenses

|

|

19 |

Summary

-

Strong franchise

-

Leadership positions intact

-

-

Commercial portfolio optimization near completion

-

Focus on prudent growth returning

-

Aggressively restructuring the liability profile

-

Repaid / Refinanced $13 billion of high cost debt

-

-

Significant progress addressing covenants via the consent solicitation / exchange

-

Bank strategy is well underway

-

Successful transfer of SBL platform to be followed with transfer of Vendor platform (pending regulatory approvals)

-

-

Increased loan origination at CIT Bank with volume from all segments

-

Expansion and diversification of deposit funding

-

Improved risk management and controls

-

Key personnel hired and enhanced processes/controls implemented

-

-

Making progress addressing items in the Written Agreement

-

Strong capital and liquidity position

|

|

20 |

|

Questions?

|