Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934

Date of report (Date of earliest event reported): May 3, 2011

Emmaus Holdings, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 000-53072 | 41-2254389 |

| (State or Other Jurisdiction | (Commission File Number) | (IRS Employer Identification No.) |

| of Incorporation) |

| 20725 S. Western Avenue, Suite 136, Torrance, CA 90501 | ||

|

(Address, including zip code, off principal executive offices)

|

||

|

Registrant’s telephone number, including area code 310-214-0065

|

||

| AFH ACQUISITION IV, INC. | ||

| 9595 Wilshire Blvd., Suite 700, Beverly Hills, CA 90212 | ||

|

(Former Name or Former Address, if Changed Since Last Report)

|

||

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Item 1.01 Entry into a Material Definitive Agreement.

Pursuant to an Agreement and Plan of Merger, dated April 21, 2011 (the “Merger Agreement”), by and among AFH Acquisition IV, Inc. (“AFH IV”), AFH Merger Sub, Inc. (“AFH Merger Sub”), AFH Holding and Advisory, LLC (“AFH Advisory”), and Emmaus Medical, Inc. (“Emmaus Medical”), Emmaus Medical merged with and into AFH Merger Sub with Emmaus Medical continuing as the surviving entity (the “Merger”). Upon the closing of the Merger, AFH IV changed its name from “AFH Acquisition IV, Inc.” to “Emmaus Holdings, Inc.”

Reference is made to Item 2.01 for a description of the Merger Agreement, the Merger and the related transactions. The description of the Merger Agreement is qualified in its entirety by reference to the complete text of the Merger Agreement, which is attached hereto as Exhibit 2.1 and incorporated by reference herein. You are urged to read the entire Merger Agreement and the other exhibits attached hereto.

In connection with the Merger Agreement, we entered into a share cancellation agreement (the “Cancellation Agreement”) pursuant to which the Company’s majority stockholder, AFH Holding and Advisory LLC canceled 1,827,750 shares of our common stock on the closing date of the Merger.

In connection with the consummation of the Merger, we entered into a Registration Rights Agreement, dated May 3, 2011 (the “Registration Rights Agreement”), for the benefit of the pre-Merger stockholders of AFH IV (the “Existing AFH IV Stockholders”) and certain former holders of Emmaus Medical common stock who hold less than 10% of our outstanding shares as of the closing of the Merger (the “Emmaus Medical Stockholders”). Pursuant to the Registration Rights Agreement, the Existing AFH Stockholders and the Emmaus Medical Stockholders will have certain “piggyback” registration rights on registration statements filed after the Merger is consummated other than registration statements (i) filed in connection with any employee stock option or other benefit plan, (ii) for an exchange offer or offering of securities solely to our existing stockholders, (iii) for an offering of debt that is convertible into our equity securities, (iv) for a dividend reinvestment plan or (v) for an offering of our equity securities underwritten by Sunrise Securities Corp. We will bear the expenses incurred in connection with the filing of any such registration statements.

The preceding summaries of the Cancellation Agreement and the Registration Rights Agreement are qualified in their entirety by reference to the complete text of the Cancellation Agreement and the Registration Rights Agreement, which are attached hereto as Exhibit 10.1 and 10.2, respectively, and incorporated by reference herein. You are urged to read the entire Cancellation Agreement and Registration Rights Agreement attached hereto.

Item 2.01 Completion of Acquisition or Disposition of Assets.

OVERVIEW

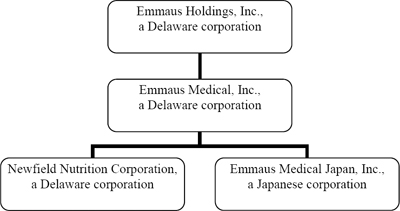

As used in this report, unless otherwise indicated, the terms “we,” “Company” and “Emmaus” refer to Emmaus Holdings, Inc., a Delaware corporation, formerly known as AFH Acquisition IV, Inc., and its wholly-owned subsidiary Emmaus Medical, and its wholly-owned subsidiaries, Newfield Nutrition Corporation, a Delaware corporation, and Emmaus Medical Japan, Inc., a Japanese corporation.

HISTORY

AFH IV was incorporated in the State of Delaware on September 24, 2007 and was originally organized as a “blank check” shell company to investigate and acquire a target company or business seeking the perceived advantages of being a publicly held corporation.

On May 3, 2011, AFH IV (i) closed a reverse merger transaction, described below, pursuant to which AFH IV became the 100% parent of Emmaus Medical, (ii) assumed the operations of Emmaus Medical and its subsidiaries and (iii) changed its name from “AFH Acquisition IV, Inc.” to “Emmaus Holdings, Inc.”

Emmaus Medical, LLC was organized on December 20, 2000. In October 2003, Emmaus Medical, LLC conducted a reorganization and merged with Emmaus Medical, Inc., a Delaware corporation originally incorporated on

2

September 12, 2003. Through this merger with Emmaus Medical, LLC into Emmaus Medical, Emmaus Medical acquired the exclusive patent rights for a treatment for sickle cell disease (“SCD”).

We are engaged in the discovery, development and commercialization of treatments and therapies for rare diseases, an area that management believes has traditionally been underserved by large pharmaceutical companies. We believe that there are attractive niche markets and financial opportunities for companies such as ours that specialize in treatments for rare diseases.

CORPORATE STRUCTURE

The corporate structure of the Company is illustrated as follows:

Our principal executive offices and corporate offices are located at 20725 S. Western Avenue, Ste. 136, Torrance, CA 90501-1884. Our telephone number is 310-214-0065.

PRINCIPAL TERMS OF THE MERGER

Upon consummation of the Merger, (i) each outstanding share of Emmaus Medical common stock was exchanged for 29.48548924976 shares of AFH IV common stock, (ii) each outstanding Emmaus Medical option and warrant, which was exercisable for one share of Emmaus Medical common stock, was exchanged for an option or warrant, as applicable, exercisable for 29.48548924976 shares of AFH IV common stock; and (iii) each outstanding convertible note of Emmaus Medical, which was convertible for one share of Emmaus Medical common stock, was exchanged for a convertible note exercisable for 29.48548924976 shares of AFH IV common stock. As a result of the Merger, holders of Emmaus Medical common stock, options, warrants and convertible notes received 20,673,714 shares of our common stock, options and warrants to purchase an aggregate of 316,186 shares of our common stock, and convertible notes to purchase an aggregate of 260,098 shares of our common stock. Securityholders of Emmaus Medical held 85% of our issued and outstanding common stock on a fully diluted basis upon the closing of the Merger. Immediately after the closing of the Merger, we had 24,423,714 shares of common stock, no shares of preferred stock, options to purchase 23,590 shares of common stock, warrants to purchase 292,596 shares of common stock and convertible notes exercisable for 260,098 shares of common stock issued and outstanding.

On May 3, 2011 after the closing of the Merger, AFH IV changed its corporate name from “AFH Acquisition IV, Inc.” to “Emmaus Holdings, Inc.” Our shares of common stock are not currently listed or quoted for trading on any national securities exchange or national quotation system. We intend to apply for the listing of our common stock on the NYSE Amex or the NASDAQ Global Market.

The transactions contemplated by the Merger Agreement were intended to be a “tax-free” reorganization pursuant to the provisions of Sections 351 and/or 368(a) of the Internal Revenue Code of 1986, as amended.

3

The Merger resulted in a change in control of our company from AFH Advisory, which is owned by Mr. Amir F. Heshmatpour, to the former securityholders of Emmaus Medical. In connection with the change in control, the persons set forth below were appointed to our Board of Directors and elected as officers in the positions set forth opposite their names. Mr. Heshmatpour, an officer and director of AFH IV prior to the consummation of the Merger Agreement, resigned from all of his officer positions with AFH IV at the time the transaction was consummated, but continues as a member of our Board of Directors. The appointments of the new officers and directors were effective on the closing of the Merger.

|

Name

|

Position

|

|

|

Yutaka Niihara, M.D., MPH

|

President and Chief Executive Officer

|

|

|

Willis C. Lee

|

Chief Operating Officer and Director

|

|

|

Lan T. Tran

|

Chief Administrative Officer and Corporate Secretary

|

|

|

Yasushi Nagasaki

|

Chief Financial Officer

|

|

|

Steve Warnecke

|

Director

|

|

|

Henry A. McKinnell, Jr., Ph.D.,

|

Chairman of the Board

|

|

|

Amir Heshmatpour

|

Director

|

|

|

Douglas W. Wilmore, M.D.

|

Director

|

Prior to the closing of the Merger, AFH Advisory canceled an aggregate of 1,827,750 shares of AFH IV common stock pursuant to a Share Cancellation Agreement executed in connection with the Merger Agreement. AFH Advisory did not receive any consideration for the cancellation of the shares. The cancellation of the shares was accounted for as a contribution to capital. The number of shares cancelled was determined based on negotiations with AFH Advisory, the majority stockholder of AFH IV, and Emmaus Medical. Emmaus Medical and AFH Advisory negotiated an estimated value of Emmaus Medical and its subsidiaries, an estimated value of the shell company, and the mutually desired capitalization of the company resulting from the Merger. With respect to the determination of the amount of shares cancelled, the value of the shell company was derived primarily from its utility as a public company platform, including its good corporate standing and its timely public reporting status. We did not consider registering our own securities directly as a viable option for accessing the public markets. The services provided by AFH Advisory were not a consideration in determining this aspect of the transaction. Under these circumstances and based on these factors, Emmaus Medical and AFH Advisory agreed upon the number of shares to be cancelled.

Emmaus Medical agreed to reimburse AFH Advisory an aggregate of $900,000, consisting of $500,000 for the identification of AFH IV and providing consulting services related to coordinating the Merger and managing the interrelationship of legal and accounting activities (the “Services”) and $400,000 for expenses incurred in connection with providing the Services, including, but not limited to, conducting a financial analysis of Emmaus Medical and conducting due diligence on Emmaus Medical and its subsidiaries. AFH Advisory is entitled, in its sole discretion, to either be reimbursed such costs in cash from the proceeds of any public offering conducted by the Company or convert such amount (or any portion thereof) into five-year warrants to purchase additional shares of our common stock at a valuation equal to 75% of fair market value of the common stock if the Company closes a public offering. If the Company does not consummate a public offering with minimum gross proceeds of $5 million, then the Company is responsible for 50% of the transaction costs associated with the Merger and 50% of the cost of the sale of AFH IV. The Company granted AFH Advisory exclusive rights to act as its advisor in connection with all financings and mergers and acquisitions until November 10, 2012 and the right to appoint two board members to the Company’s board of directors upon the closing of the Merger.

EMMAUS HOLDINGS, INC.’S BUSINESS

Overview

We are engaged in the discovery, development, and commercialization of innovative and cost-effective treatments and therapies, areas that we believe have traditionally been underserved by large pharmaceutical companies. We believe that there are attractive niche markets and financial opportunities for companies such as ours that specialize in treatments for rare diseases. Over time, we plan to expand our business to include developing and marketing products to treat more common diseases. The primary focus of our business is the late-stage development of the amino

4

acid L-glutamine as a prescription drug for the treatment of sickle cell disease (“SCD”). To a lesser extent, we are also engaged in the marketing and sale of NutreStore® [L-glutamine powder for oral solution] and promotion of Zorbtive® [somatropin (rDNA origin) for injection], as a treatment for short bowel syndrome (“SBS”) and the sale of L-glutamine as a nutritional supplement under the brand name AminoPure®. Since inception, we have generated minimal revenues from the sale and/or promotion of NutreStore®, Zorbtive® and AminoPure®.

Industry and Market Opportunity

We focus on developing treatments and therapies for rare diseases. Rare diseases, pursuant to the Rare Disease Act of 2002, defines a “rare disease” as any disease or condition that affects less than 200,000 persons in the United States. In Japan, a rare disease is one that affects fewer than 50,000 persons in Japan. The European Commission on Public Health defines a rare disease as a life-threatening or chronically debilitating disease which is of such low prevalence, namely affecting fewer than 1 in 2,000 people, that special combined efforts are needed to address it.

Sickle Cell Disease

We are currently engaged in a Phase III clinical trial of L-glutamine as a treatment for SCD, for which we hope to obtain approval from the U.S. Food and Drug Administration (“FDA”) in 2013. SCD affects about 70,000 to 100,000 persons in the U.S. and over 4 million people worldwide as of September 2010.

SCD is an inherited blood disorder that affects red blood cells. Red blood cells contain hemoglobin which allows red blood cells to carry oxygen from the air in the lungs to all parts of the body. Normal red blood cells contain hemoglobin A. In contrast, the bone marrow of people with SCD produces red blood cells with a different form of hemoglobin called hemoglobin S (S stands for sickle). When a person has SCD, rather than remaining round, smooth and flexible, the red blood cells become sickle (crescent) shaped, inflexible, and sticky as they release oxygen to other tissues in the body. These abnormally shaped cells become rigid and lodge in the capillaries when oxygen is released from the cells’ hemoglobin, causing blockages and preventing the normal flow of oxygen to the surrounding tissue. SCD diseased red blood cells also tend to clump together, further impeding circulation.

Normal red blood cells live for about 120 days before they are replaced with new ones. In sharp contrast, sickle-shaped red blood cells are destroyed faster, in about 16 days, and cannot always be replaced quickly. As a result, people with SCD are often anemic. Sickle cell disease includes sickle cell anemia (which results from two hemoglobin S genes), sickle ß-thalassemia (one hemoglobin S and one ß-thalassemia gene), hemoglobin SC disease (one hemoglobin S and one hemoglobin C), and the somewhat rare disease hemoglobin C Harlem. These hereditary diseases often affect individuals of African American heritage, and increasingly, Hispanic populations. People of Mediterranean, Middle Eastern, and South East Asian descent are also afflicted with the disease, but to a lesser degree.

The complications of sickle cell disease occur when sickle-shaped red blood cells block veins which then can cause pain in the arms, legs, back and stomach, bones, skin and other parts of the body, as well as long-term organ damage, diminished exercise tolerance, increased stroke and infection rate, and decreased lifespan. “Sickle cell crisis” is a broad term that describes several different conditions, particularly aplastic crisis, which is temporary bone marrow aplasia; hemolytic crisis, which is acute red cell destruction, leading to jaundice; and vaso-occlusive crisis, which is severe pain due to infarctions located in the bones, joints, lungs, liver, spleen, kidney, eye, or central nervous system. The acute pain of a sickle cell crisis generally persists for several days, and is usually followed by a dull, aching pain, which generally ends after several weeks, although it may persist between crises. Acute chest syndrome, which can often lead to death, is a particularly serious complication of SCD and is commonly accompanied by infections in the lungs. SCD sufferers often experience shortness of breath and SCD children patients often experience abdominal pain. Pain in the bones is a common symptom due to blockage of blood circulation, which damages bones and the bone marrow (the site of most red blood cell production). Sudden attacks of pain also commonly occur in the fingers and toes and in other bones and joints (known as “hand-foot syndrome.”) The liver may become enlarged, causing great abdominal pain; nausea, low-grade fever, and increasing jaundice can occur when the liver is affected.

SCD patients, on average, experience about three sickle cell crises per year that are severe enough to require hospitalization, and their symptoms are treated with nonsteroidal anti-inflammatory drugs (NSAIDs), narcotics (e.g. morphine, codeine and oxycodone), other pain relief medicines, and blood transfusions. SCD patients also require frequent visits to emergency rooms and urgent care facilities. A sickle cell crisis is usually followed by a period of

5

remission. If a patient recovers after a sickle cell crisis, she can resume a relatively normal life between crises. SCD patients also suffer from a variety of other ailments including stroke, complications from anemia, kidney failure, infection, problems in the genital-urinary tract, liver failure, gallbladder disease, problems in the bones and joints, and other medical complications. Patients who survive infancy are subject to other medical problems, including impaired physical development, gum disease, scarring of the retina, and leg sores.

We have acquired the rights to develop a treatment approach for SCD covered under U.S. Patent No. 5,693,671, entitled “L-glutamine Therapy for Sickle Cell Disease and Thalassemia” issued on December 2, 1997 to Niihara et al. Emmaus Medical is the exclusive worldwide licensee of this patent. For further information of the terms of this license, please refer to the full text of the license, which is attached as Exhibit 10.6 to this report. The license agreement is effective until the expiration of the patent in 2016. L-glutamine is a conditionally essential amino acid that has long been used as a non-pharmaceutical nutritional supplement. A conditionally essential amino acid is an amino acid that the body can naturally synthesize, but under certain circumstances, the body is unable to synthesize such amino acid and it must be supplied by diet or supplement. Emmaus’ treatment involves SCD patients orally consuming 30 gm/day of pharmaceutical grade L-glutamine for adults, and 0.6 gm/kg of body weight for infants and children, up to 30 gm/day.

In red blood cells, pyridine nucleotides, nicotinamide adenine dinucleotide (NAD) and its reduced form NADH, are the major molecules that regulate and prevent oxidative damage. Sickle red blood cells have a significantly increased rate of transport of one of the major precursors of NAD, glutamine. It was proposed that the SCD red blood cell is attempting to improve NAD redox potential by increasing transport of glutamine. Analysis of the chemistry of NAD synthesis in red blood cells has suggested that with glutamine supplementation to sickle red blood cells, the NAD synthesis will further increase, which would prevent the sickle red blood cells from being oxidative damaged, and make the sickle red blood cells less adhesive to small blood vessels, leading to less obstruction or blockage of small blood vessels, which is a major cause of the problems that sickle cell patients face.

Short Bowel Syndrome

We currently sell one prescription pharmaceutical product, NutreStore® [L-glutamine powder for oral solution], in the United States and have the exclusive right to promote another prescription pharmaceutical product, Zorbtive® [somatropin (rDNA origin) for injection], in the United States. Each of these products has received FDA approval to treat SBS.

SBS is a condition affecting people who have had half or more of their small intestine surgically removed or who have a congenital defect or a disease affecting the small intestine, such as Crohn’s disease and inflammatory bowel disease. The small bowel plays a significant role in nutrient absorption and those with SBS experience malnourishment due to an inadequate absorption of nutrients and fluids. Some symptoms of SBS include malnutrition, diarrhea, abdominal bloating, fatigue, fat in the stool (steatorrhea), cramping, heartburn, bacterial infections, anemia, depression, gallstones and kidney stones. Complications of SBS include organ failure due to malnourishment or malnutrition which could lead to death.

For years, the standard treatment for SBS has been changes in diet, intravenous (IV) feeding (also called “parenteral nutrition”), vitamin and mineral supplements, and medication to relieve symptoms. Long term IV feeding is expensive, is inconvenient to the patient, and can be harmful to the body.

In 2004, a new and patented treatment regime, US Patent No. 5,288,703 (the “SBS Patent”), was approved by the FDA. This treatment comprises of a man-made human growth hormone (hGH), namely Zorbtive® [somatropin (rDNA origin) for injection] in combination with NutreStore® [L-glutamine powder for oral solution] and a specialized diet.

The treatment is comprised of Zorbtive® and NutreStore® in combination with a specialized diet. Zorbtive® is administered by injection for four weeks, and NutreStore® is orally taken for 16 weeks. Treatment with NutreStore® alone with a specialized diet, Zorbtive® alone with a specialized diet, and Zorbtive® and NutreStore® together with a specialized diet all help the small intestine take in more water, electrolytes and nutrients and reduce the volume and frequency of IV feedings and the problems caused thereby. Study results show that the treatment has the potential to reduce the mean weekly frequency of intravenous parenteral nutrition from 5.4 days to 1.2 days per week after 4 weeks

6

of treatment, as well to reduce the required weekly volume and caloric content. Published pharmacoeconomic studies have shown that when Zorbtive® is used in SBS patients, the average savings (including the costs of Zorbtive®) are about $85,000 over two years over traditional parenteral nutrition treatment. Moreover, when Zorbtive® and NutreStore® are used together, there are superior results, namely a greater reduction in a patient’s requirement for parenteral nutrition, which would lead to even greater cost savings to insurers.

In October 2007, we became the exclusive sublicensee of the SBS Patent for the U.S. market, including the rights to distribute the L-glutamine treatment for SBS under the trademark NutreStore® in the U.S., and commercially launched NutreStore® in June 2008. EMD Serono, Inc. granted Emmaus the exclusive right to promote Zorbtive® in the United States in December 2008. In December 2010, we were awarded a five-year contract by the U.S. Department of Veterans Affairs for our NutreStore® product. Internationally, we are in the last stages of seeking approval to market NutreStore® in Hong Kong and have received a Certificate of Free Sale from the FDA to export NutreStore® to Hong Kong.

AminoPure® Business

We sell L-glutamine as a nutritional supplement under the brand name AminoPure® through our indirect wholly owned subsidiary, Newfield Nutrition Corporation. AminoPure® is made up of pure USP grade L-glutamine that the body needs when a person is under physical exertion, stress, or is sick. L-glutamine has been shown by scientific data to help with gastro intestinal health and to support the body’s natural immune response.

AminoPure® is currently sold through retail stores in several states and via importers and distributors in Japan. We have started to export AminoPure® to Taiwan and plan to expand sales of AminoPure® into the Philippines and South Korea in the near future. We added a new distributor, PMAI, a subsidiary of JFC International, Inc., a leading distributor of Japanese foods in Asian-American communities in the United States, in November 2010 to take advantage of its retail outlet network in the United States.

Nutritional supplements are regulated by FDA and we must comply with numerous federal and state laws and regulations related to the AminoPure® product’s testing, manufacture, labeling, packaging, storage, distribution, recordkeeping and reporting.

Sales of AminoPure® have steadily increased in recent years. Sales increased 121.2% in the year ended December 31, 2010 as compared to the year ended December 31, 2009 and 78% in the year ended December 31, 2009 as compared to the year ended December 31, 2008. However, despite the increase in sales of AminoPure®, we have generated minimal revenues from the sale of from AminoPure® and NutreStore® since our inception and the sale of such products are not part of our principal operations.

CellSeed Investment

In January 2009, Emmaus made a strategic investment in CellSeed, Inc. (“CellSeed”), a Japanese company engaged in the research and development, manufacture and sale of temperature-responsive cell culture equipment, which is a cell sheet tissue-engineering platform tool, and application products, as well as cell sheet tissue engineered medical products and application products. Emmaus currently owns a 3% stake in CellSeed, a public company traded on the JASDAQ NEO market in Tokyo, Japan. We entered into a Joint Research and Development Agreement and an Individual Agreement with CellSeed, described below under the heading “Intellectual Property” to pursue collaborative opportunities with CellSeed.

Competitive Strengths

We believe the following strengths contribute to our competitive advantages:

Experienced management team

Our senior management team has extensive business and industry experience, including an understanding of the pharmaceutical industry and changing technologies. Our President and Chief Executive Officer, Yutaka Niihara, M.D., MPH, has extensive knowledge of our operations and our patents, being one of the initial patentees for the

7

technology for the treatment with SCD. Dr. Niihara has extensive research experience in the field of SCD and other blood diseases, is widely published scientist in the area of SCD and actively treats SCD patients. Members of our senior management team also have significant experience with respect to key aspects of our operations and product candidates.

Strategic Supplier Relationships with Major Suppliers of Pharmaceutical Grade L-Glutamine.

Ajinomoto, U.S.A., through its parent company, the Ajinomoto Company in Japan, has provided free of charge L-glutamine for our completed clinical work, including our completed Phase II clinical trials. Ajinomoto is also providing L-glutamine for our Phase III clinical trials without charge. We have supplier relationships with Ajinomoto and the only other major supplier of pharmaceutical grade L-glutamine, Kyowa Hakko U.S.A, the U.S. subsidiary of Kyowa Hakko Kogyo Co., Ltd. We currently source L-glutamine from Kyowa Hakko U.S.A. for our NutreStore® product.

Orphan Drug Act – Federal Subsidies.

We obtained Orphan Drug Designation, which provides numerous advantages, for the L-glutamine therapy for SCD under Application number 01-1459 on August 1, 2001. As a designated orphan drug, we receive a 50% tax credit for clinical research. Furthermore, our new drug application fee is waived, and upon obtaining FDA approval, we will receive seven years of exclusive marketing rights for the SCD indication, independent of the patent protection. In addition, we will not be required to pay the annual establishment fee and product fee, which were $425,600 and $71,520, respectively, for the fiscal year ended December 31, 2009 and $457,200 and $79,720, respectively, for the fiscal year ended December 31, 2010.

Our Strategy

Our goal is to be a leading pharmaceutical company focused on the development and commercialization of proprietary branded products and product candidates to treat rare diseases. We intend to achieve this goal by:

Maximizing the value of our L-glutamine treatment for SCD

We are currently in phase III clinical trials of our L-glutamine treatment for SCD. We believe our treatment could have advantages over traditional treatments for SCD, including cost savings. We intend to undertake activities to prepare for the commercialization of this treatment. When and if this treatment is approved by the FDA, we intend to commercialize our L-glutamine SCD treatment and may enter into strategic relationships with third parties.

Establishing strategic collaborations

We intend to seek opportunities to enter into strategic collaborations with leading pharmaceutical and biotechnology companies to commercialize our product candidates to drive growth and profitability. We believe that leveraging the capabilities of third parties will allow us to add efficiency to our operations and expand our commercial reach.

Pursuing acquisitions to broaden our drug candidates and product offerings

We will consider strategic acquisitions that will provide us with a broader range of drug candidates and product offerings. When evaluating potential acquisition targets, we will consider factors such as market position, growth potential and earnings prospects and strength and experience of management.

Governmental Regulation of Pharmaceutical and Biotechnology Industries

Regulation by governmental authorities in the U.S. and foreign countries is a significant factor in the development, manufacture, and expected marketing of our drug product candidates and in our ongoing research and development activities. The nature and extent to which such regulation will apply to us will vary depending on the nature of any drug product candidates developed.

8

In particular, human therapeutic products are subject to rigorous preclinical and clinical testing and other approval procedures of the FDA and similar regulatory authorities in other countries. Various federal and state statutes and regulations also govern or influence research, testing, manufacturing, safety, efficacy, labeling, packaging, storage, distribution and record-keeping related to such products and their marketing. The process of obtaining these approvals and the subsequent compliance with the appropriate federal and state statutes and regulations requires substantial time and financial resources. Any failure by us or our collaborators to obtain, or any delay in obtaining, regulatory approval could adversely affect the marketing of any of our drug product candidates, our ability to receive product revenues, and our liquidity and capital resources.

Before obtaining regulatory approvals for the commercial sale of L-glutamine as a treatment for any of our products under development, we must demonstrate through preclinical studies and clinical trials that the product is safe and efficacious for use in each target indication. The results from preclinical studies and early clinical trials might not be predictive of results that will be obtained in large-scale testing. Our clinical trials might not successfully demonstrate the safety and efficacy of any product candidates or result in marketable products.

In order to clinically test, manufacture, and market products for therapeutic use, we and our third-party collaborators will have to satisfy mandatory procedures and safety and effectiveness standards established by various regulatory bodies. In the U.S., the Public Health Service Act and the Federal Food, Drug, and Cosmetic Act, as amended, and the regulations promulgated thereunder, and other federal and state statutes and regulations govern, among other things, the research, testing, manufacture, labeling, packaging, storage, distribution, record keeping, approval, advertising, and promotion of our current and proposed product candidates. Product development and approval within this regulatory framework takes a number of years and involves the expenditure of substantial resources.

The steps required by the FDA before new drug products may be marketed in the U.S. include.

| ● | completion of preclinical studies; | |

| ● | the submission to the FDA of a request for authorization to conduct clinical trials on an investigational new drug application, or IND, which must become effective before clinical trials may commence; | |

| ● |

adequate and well-controlled Phase 1, Phase 2 and Phase 3 clinical trials to establish and confirm the safety and efficacy of a drug candidate;

|

|

| ● |

submission to the FDA of a new drug application, or NDA, for the drug candidate for marketing approval; and

|

|

| ● | review and approval of the NDA by the FDA before the product may be shipped or sold commercially. |

In addition to obtaining FDA approval for each product, each product manufacturing establishment must be registered with the FDA and undergo an inspection prior to the approval of an NDA. Each manufacturing facility and its quality control and manufacturing procedures must also conform and adhere at all times to the FDA’s cGMP regulations. In addition to preapproval inspections, the FDA and other government agencies regularly inspect manufacturing facilities for compliance with these requirements. If, as a result of these inspections, the FDA determines that any equipment, facilities, laboratories or processes do not comply with applicable FDA regulations and conditions of product approval, the FDA may seek civil, criminal, or administrative sanctions and/or remedies against us, including the suspension of the manufacturing operations and market withdrawal of marketed product. Manufacturers must expend substantial time, money and effort in the area of production and quality control to ensure full technical compliance with these standards.

Preclinical testing includes laboratory evaluation and characterization of the safety and efficacy of a drug and its formulation. Preclinical testing results are submitted to the FDA as a part of an IND which must become effective prior to commencement of clinical trials. Clinical trials are typically conducted in three sequential phases following submission of an IND. Phase 1 represents the initial administration of the drug to a small group of humans, either patients or healthy volunteers, typically to test for safety (adverse effects), dosage tolerance, absorption, distribution, metabolism, excretion and clinical pharmacology, and, if possible, to gain early evidence of effectiveness. Phase 2

9

involves studies in a small sample of the actual intended patient population to assess the efficacy of the drug for a specific indication, to determine dose tolerance and the optimal dose range and to gather additional information relating to safety and potential adverse effects. Once an investigational drug is found to have some efficacy and an acceptable safety profile in the targeted patient population, Phase 3 studies are initiated to further establish clinical safety and efficacy of the therapy in a broader sample of the general patient population, in order to determine the overall risk-benefit ratio of the drug and to provide an adequate basis for any physician labeling. During all clinical studies, we must adhere to Good Clinical Practice, or GCP, standards and applicable human subject protections standards. The results of the research and product development, manufacturing, preclinical studies, clinical studies and related information are submitted in an NDA to the FDA.

The process of completing clinical testing and obtaining FDA approval for a new drug is likely to take a number of years and require the expenditure of substantial resources. If an application is submitted, there can be no assurance that the FDA will review and approve the NDA. Even after initial FDA approval has been obtained, further studies, including post-market studies, might be required to provide additional data on safety and will be required to gain approval for the use of a product as a treatment for clinical indications other than those for which the product was initially tested and approved. Also, the FDA will require post-market reporting and might require surveillance programs to monitor the side effects of the drug. Results of post-marketing programs might limit or expand the further marketing of the products. Further, if there are any modifications to the drug, including changes in indication, manufacturing process, labeling or a change in manufacturing facility, an NDA supplement might be required to be submitted to the FDA prior to or corresponding with that change.

The rate of completion of any clinical trials will be dependent upon, among other factors, the rate of patient enrollment. Patient enrollment is a function of many factors, including the size of the patient population, the nature of the trial, the number of clinical sites, the availability of alternative therapies and drugs, the proximity of patients to clinical sites and the eligibility criteria for the study. Delays in planned patient enrollment might result in increased costs and delays, which could have a material adverse effect on us.

Failure to comply with applicable FDA requirements may result in a number of consequences that could materially and adversely affect us. Failure to adhere to approved trial standards and GCPs in conducting clinical trials could cause the FDA to place a clinical hold on one or more studies which would delay research and data collection necessary for product approval. Noncompliance with GCPs could also have a negative impact on the FDA’s evaluation of an NDA. Failure to adhere to GMPs and other applicable requirements could result in FDA enforcement action and in civil and criminal sanctions, including but not limited to fines, seizure of product, refusal of the FDA to approve product approval applications, withdrawal of approved applications, and prosecution.

Whether or not FDA approval has been obtained, approval of a product by regulatory authorities in foreign countries must be obtained prior to the commencement of marketing of the product in those countries. The requirements governing the conduct of clinical trials and product approvals vary widely from country to country, and the time required for approval might be longer or shorter than that required for FDA approval. Although there are some procedures for unified filings for some European countries, in general, each country at this time has its own procedures and requirements. There can be no assurance that any foreign approvals would be obtained. In most cases, if the FDA has not approved a drug product candidate for sale in the U.S., the drug product candidate may be exported for sale outside of the U.S. only if it has been approved in any one of the following: the European Union, Canada, Australia, New Zealand, Japan, Israel, Switzerland and South Africa. Specific FDA regulations govern this process.

In addition to the regulatory framework for product approvals, we and our collaborative partners must comply with federal, state, and local laws and regulations regarding occupational safety, laboratory practices, the use, handling and disposition of radioactive materials, environmental protection and hazardous substance control, and other local, state, federal and foreign regulation. All facilities and manufacturing processes used by third parties to produce our drug candidates for clinical use in the United States must conform with cGMPs. These facilities and practices are subject to periodic regulatory inspections to ensure compliance with cGMP requirements. Their failure to comply with applicable regulations could extend, delay, or cause the termination of clinical trials conducted for our drug candidates. The impact of government regulation upon us cannot be predicted and could be material and adverse. We cannot accurately predict the extent of government regulation that might result from future legislation or administrative action.

Clinical Trials

10

We have conducted a number of clinical trials with the goal of obtaining FDA approval to market and sell L-glutamine as a treatment for SCD. The FDA approval process begins with laboratory testing and then moves on to the clinical trial stage. In July 1994, Dr. Niihara started a pilot clinical trial using L-glutamine as an oral supplement to SCD patients. The study showed based on the preclinical data and demonstrated that oral consumption of L-glutamine by SCD patients increases the concentration of the reduced form of NAD, NADH, and its redox status. Clinically, all the patients who participated in the study reported an increase in their energy level and decrease in the severity of chronic pain with treatment.

In a Phase II, 12-week open label study conducted in 1995, Dr. Niihara found a significant decrease in the incidence and severity of sickle cell crisis in selected patients who experience unusually frequent episodes of sickle cell crisis. A Phase II blind clinical trial to assess the reduction of sickle cell crisis and chronic pain, which started in 1997 and was funded by the National Institutes of Health, the results of which were released in January 2003, demonstrated statistically significant reduction of chronic pain, while a strong trend toward significance was observed in the reduction in sickle cell crises. Another Phase II open label clinical trial, which started in 2000 and was funded by the FDA, the results of which were released in April 2009, directed to exercise tolerance, demonstrated that patients on L-glutamine have improved physical stamina with no significant side effects.

In April 2009, Emmaus completed an 80 patient Phase II clinical trial funded by the FDA directed to reduce the incidence of sickle cell crisis as its primary indication. The trial took place at the following institutions: the Los Angeles Biomedical Research Institute at Harbor-UCLA Medical Center (“LABioMed”); Emory University, Atlanta, Georgia; Kaiser Permanente, Bellflower, California; the University of Medicine and Dentistry of New Jersey (Robert Wood Johnson Medical School), New Brunswick, NJ; and the Jacobi Medical Center-North Bronx Healthcare Network, Bronx, New York. This study showed clinical significance for reducing the incidence of sickle cell crisis (more than a 50% reduction in incidence of sickle cell crisis) but due to a higher than expected drop out rate, the statistical significance was not high enough to support Emmaus’ direct submission of a new drug application to the FDA. However, the safety of L-glutamine was well demonstrated in this trial. This Phase II clinical trial was managed by the contract research organization, ClinDatrix, Inc.

In April 2009, the FDA authorized Emmaus to begin a larger Phase III clinical trial directed to study L-glutamine as an experimental agent to reduce sickle cell crisis. Patient enrollment began in mid-2010 and as of February 2011, we have signed contracts with 15 sickle cell study sites across the United States and have enrolled 33 patients. We aim to complete Phase III clinical trial enrollment by the end of 2011. This Phase III trial will include an interim analysis after 24 weeks of the 48-week study period and we expect that it will involve 200+ patients at between 20 and 25 clinical trial sites around the country.

Status of FDA Approvals and Orphan Drug Designation

The FDA has already approved of L-glutamine as a treatment for short bowel syndrome. Accordingly, instead of the more involved approval process of Section 505(b)(1) of the Federal Food, Drug, and Cosmetic Act (“FD&C Act”) that is required for the first medical indication of a drug, Emmaus will proceed under Section 505(b)(2) of the FD&C Act, which provides a more streamlined and easier approval process for subsequent indications of a drug. Consequently, we believe that our Phase III clinical trial directed to reduce sickle cell crises will likely be considered a pivotal study for purposes of applying for FDA marketing approval under Section 505(b)(2).

The FDA Modernization Act of 1997 codified the FDA’s policy of granting “fast track” review of certain therapies targeting “orphan” indications and other therapies intended to treat severe or life threatening diseases and having potential to address unmet medical needs. Orphan indications are defined by the FDA as having a prevalence of less than 200,000 patients in the U.S. We obtained Orphan Drug designation for L-glutamine as a sickle cell disease treatment from the FDA on August 1, 2001. This designation waived the new drug application fee (presently over $1 million) and annual establishment and product fees, provided a 50% tax credit for clinical work, and, if the product is approved, will provide exclusive marketing rights for the SCD indication for seven years.

We have obtained Fast Track designation for the L-glutamine therapy for SCD. Fast Track designation will provide us with many advantages over the normal FDA approval process, including the right to submit modules of the

11

new drug application (NDA) in portions (“rolling submission”), rather than all at once, and the opportunity to have more FDA interaction.

Product Sourcing and Packaging

We plan to obtain our pharmaceutical grade L-glutamine from the Japanese food, amino acid and pharmaceutical company, the Ajinomoto Company, and from the Japanese pharmaceutical company Kyowa Hakko. The Ajinomoto Company and Kyowa Hakko together produce the vast majority of pharmaceutical grade L-glutamine approved for sale in the U.S. The manufacture of large quantities of pharmaceutical grade L-glutamine is a complex and expensive undertaking, and is therefore not an easy market for third parties to enter. We currently source L-glutamine from Kyowa Hakko U.S.A. for our NutreStore® product. As part of our sourcing agreements, we plan to enter into exclusive long term supply contracts with these manufacturers for L-glutamine for SCD treatment that will also require that these companies agree not to sell L-glutamine as a nutritional supplement or pharmaceutical for sickle cell disease applications. However, there is no assurance that we will be able to obtain such terms or economically attractive terms for obtaining pharmaceutical grade L-glutamine from these proposed suppliers, or that the suppliers will not experience an interruption in supply that could materially and adversely affect our business.

We expect that the product will be packaged by an FDA approved facility. Anderson Packaging, Inc., of Rockville, Illinois, has handled the packaging for our Phase II and III clinical trials of L-glutamine for SCD and we plan to use the same company for commercial packaging of the product. Anderson Packaging, Inc. packaged L-glutamine for the clinical trials that resulted in the FDA’s marketing approval for L-glutamine for short bowel syndrome using the same dose and packaging protocol as the Company expects to use for treatment of SCD. Prior FDA approval of packaging types and protocols does not guarantee future approval of packaging types and protocols.

Sales and Marketing

We have three full time pharmaceutical sales representatives. Our sales representatives conduct weekly teleconferences with management to share current product information and sales strategies and the employees at our headquarters to assist with any immediate patient and physician needs.

As we expand our sales of L-glutamine for SBS and commercialize our L-glutamine treatment for SCD, we intend to increase the size of our sales staff. We intend to employ only sales staff personnel who have experience and training in the U.S. with the sale of prescription pharmaceuticals. Sales representatives will receive continuing training, education and development to ensure that our sales staff has current knowledge of our products as well as the current Compliance Program Guidance for Pharmaceutical Manufacturers published by the U.S. Department of Health and Human Services, Office of Inspector General, the provisions of the Code on Interactions with Healthcare Professionals created by the Pharmaceutical Research and Manufacturers of America (“PhRMA Code”) and the FDA’s regulatory limitations on promotional activities.

After obtaining FDA approval for the SCD indication, we intend to focus our sales and marketing efforts across several different groups, including patients, their physicians and care providers, hospitals and treatment centers, insurance carriers, non-profit associations, and collaborating pharmaceutical companies. Our in-house product specialists and sales representatives will focus on the following tasks as part of our marketing strategy:

|

|

●

|

promote our L-glutamine therapy to SCD specialist physicians;

|

|

|

●

|

promote awareness of our L-glutamine therapy at all U.S. community-based treatment centers;

|

|

|

●

|

develop L-glutamine therapy collateral materials and informational packets to educate patients and physicians and garner industry support;

|

|

|

●

|

establish collaborative relationships with non-profit organizations that focus on SCD; and

|

|

|

●

|

identify international opportunities for our L-glutamine therapy.

|

Our target customers for Zorbtive® and NutreStore® are SBS patients, as well as their local treating medical centers and physicians. Patient and physician awareness of the Zorbtive® and NutreStore® brands will be key to our success. We intend to exhibit at trade shows and other events and maintain websites with current information on

12

Zorbtive® and NutreStore® to strengthen these two brands. In addition, we will continue to place advertisements in medical journals, such as the Journal of Parenteral and Enteral Nutrition (JPEN) and the American Journal of Gastroenterology to raise awareness of Zorbtive® and NutreStore® with healthcare professionals. In addition, we have purchased prescriber data in order to increase our outreach to physicians identified in the data. We will also work with patient support organizations, such as the Oley Foundation and ASPEN, to promote our SBS treatments.

Research and Development

For the years ended December 31, 2010 and 2009, we expended $1.1 million and $0.5 million, respectively, in research and development costs related to our L-glutamine treatment for SCD.

Intellectual Property

We rely on a combination of patent, licenses, trademark and trade secret protection and other unpatented proprietary information to protect our intellectual property rights and to maintain and enhance our competitiveness in the pharmaceutical industry. While we do not currently have any patents, but have 2 patent licenses with third parties.

We also rely on unpatented technologies to protect the proprietary nature of our products. We require that our management team and key employees enter into confidentiality agreements that require the employees to assign the rights to any inventions developed by them during the course of their employment with us. All of the confidentiality agreements include non-solicitation provisions that remain effective during the course of employment and for periods following termination of employment.

Licenses and Promotional Rights Agreements

In October 2007, Emmaus became the exclusive sublicensee of US Patent No. 5,288,703 (the “SBS Patent”) for the U.S. market, including the rights to distribute the L-glutamine treatment for the treatment of SBS under the trademark NutreStore® in the U.S., and commercially launched NutreStore® in June 2008. Pursuant to the sublicense, as amended by an assignment and transfer agreement, we are require to pay a royalty of 10% of adjusted gross sales of NutreStore® to Cato Holding Company (“Cato”) through 2016. We are also required to pay to Cato Holding Company a royalty of 1% of gross sales of L-glutamine as a treatment for SCD and thalassemia for a period of five years from the date of the first commercial sale of such product. The sublicense is subject to a sublicense that Cato Holding Company holds from Ares Trading, S.A. (the “Ares License”), and if the Ares License is terminated for any reason, then our sublicense with Cato will also terminate.

EMD Serono, Inc. granted us the exclusive right to promote Zorbtive® in the United States in December 2008 pursuant to a promotional rights agreement. We use the same sales force to promote and market Zorbtive® and NutreStore®. While we have the exclusive right to promote and market Zorbtive® in the United States, EMD Serono actually sells the product. The promotional rights agreement provides that no royalties are payable from EMD Serono to us until unit sales exceed 16,016. The threshold has not yet been met and we have received no royalties pursuant to the agreement. After the unit sales exceed the threshold, EMD Serono is required to pay us a commission equal to $300,000, plus 35% of annual net sales from unit sales that exceed 16,017 but are less than or equal to 32,032 units; 50% of annual net sales from unit sales that exceed 32,033 but are less than or equal to 80,080 units; and 60% of annual net sales from unit sales that exceed 80,080 units. The agreement terminates upon expiration of U.S. Patent No. 5,288,703, which expires on October 7, 2011.

On April 8, 2011, Emmaus Medical entered into a Joint Research and Development Agreement (the “Research Agreement”) and an Individual Agreement (the “Individual Agreement”) with CellSeed. Pursuant to the Research Agreement, the Company and CellSeed formed a relationship regarding the future research and development of cell sheet engineering regenerative medicine products (the “Products”), and the future commercialization of such Products. The parties will enter into individual agreements for each project or task conducted pursuant to the Research Agreement defining the details of such project. All intellectual property rights created in the course of the Research Agreement and any individual agreement, including rights made jointly by the employees of the Company and CellSeed or made solely by the employee(s) of the other party based on confidential information or intellectual property rights exchanged between the parties, will be owned jointly by the Company and CellSeed. Intellectual property rights related to the Products that are developed solely by one party’s employees independently from confidential information and

13

intellectual property rights of the other party, shall be owned by the party whose employees made such invention, provided however, that such party will grant a worldwide, perpetual, irrevocable, non-exclusive, royalty free, fully paid up, sub-licensable, transferable license of such rights to the other party. Pursuant to the Individual Agreement, CellSeed granted the Company an exclusive right to manufacture, sell, market and distribute Cultured Autologous Oral Mucosal Epithelial Cell-Sheets (“CAOMECS”) for the cornea in the United States. CellSeed shall disclose its accumulated information package (the “Package”) for the joint development of CAOMECS to Emmaus Medical. Pursuant to the Research Agreement, the Company agreed to pay CellSeed $8,500,000 within 30 days of the completion of all of the following: (i) the execution of the Research Agreement; (ii) the execution of the Individual Agreement; and (iii) CellSeed’s delivery of the Package to Emmaus. Pursuant to the Individual Agreement, the Company agreed to pay $1,500,000 to CellSeed within 30 days of CellSeed’s delivery of the Package to the Company and a royalty to be agreed upon by the parties. The parties will determine the rate at which profits from the net sales of CAOMECS in the United States will be split between the parties. The Individual Agreement will remain in effect until CellSeed’s patents used for the CAOMECS expire in the United States, unless terminated earlier by the parties.

Trademarks

We currently own 3 U.S. trademarks, including “Emmaus Medical,” “NutreStore” and “AminoPure” and one Japanese trademark for “AminoPure.”

Our success will depend in part on our ability to obtain patents and preserve other intellectual property rights covering the design and operation of our products. We intend to seek patents on our products when we deem it commercially appropriate. The process of seeking patent protection can be lengthy and expensive, and there can be no assurance that patents will be issued for currently pending or future applications or that our existing patents or any new patents issued will be of sufficient scope or strength or provide meaningful protection or any commercial advantage to us. We may be subject to, or may initiate, litigation or patent office interference proceedings, which may require significant financial and management resources. The failure to obtain necessary licenses or other rights or the advent of litigation arising out of any such intellectual property claims could have a material adverse effect on our operations.

Competition

The development and commercialization of pharmaceutical products is very competitive and characterized by extensive research efforts and rapid technological progress. Competition in our industry occurs on a number of fronts, including developing and bringing new products to market before our competitors, developing new products to provide the same benefits as existing products at lower cost and developing new products to provide benefits superior to those of existing products. We face competition from other pharmaceutical companies, particularly those that provide alternative drugs to treat SCD and SBS, as well as other entities that develop alternative therapies that could limit the market for our L-glutamine product.

We currently face two competing treatments for SCD treatment, one of which being Bristol-Myers Squibb’s Hydroxyurea and the other being bone marrow transplants. Additionally, gene therapy techniques hold promise as a potential treatment for a variety of genetic diseases, including SCD, however, there are currently many questions about the efficacy of gene therapy and when such therapies could become available to treat diseases such as SCD.

Presently, the most prevalent therapy for patients with SBS is parenteral nutrition. However, as outlined above, Emmaus’ products NutreStore® and Zorbtive® can be used to reduce the volume and frequency of parenteral nutrition therapy for most patients.

Because L-glutamine is currently sold as a nutritional supplement, there is risk that both of the Company’s pharmaceutical products for treatment of SCD and SBS may experience competition with providers of L-glutamine in nutritional supplement form. In fact, when dealing with a method patent directed to new uses for old compounds, there is always a risk that the medication can be obtained from unauthorized sources, and sold at cut-rate prices, known as the “generic leakage” problem. More generally, generic leakage results when a barrier to competition, e.g. a patent, expires or is invalidated, suddenly opening up the formerly price protected (and relatively expensive) product to competition from relatively inexpensive generic products. As a result, consumers will tend to purchase more of the cheaper generic product and less of the expensive product. However, the Company believes generic leakage will not be a major factor for a number of reasons, including but not limited to insurance/reimbursement factors, pricing strategies, regulatory

14

barriers to market entry, distribution mechanisms, FDA-administered market exclusivity protections, intellectual property protections, and other factors inherent in the FDA regulatory differences between pharmaceuticals and nutritional supplements.

Our competitors may have products that have been approved or are in advanced development and may succeed in developing drugs that are more effective, safer and more affordable or more easily administered than ours or that achieve commercialization sooner than our products.

Employees

As of December 31, 2010, we had 11 employees, 10 of which are full time, as well as two independent sales representatives and four consultants. We have not experienced any work stoppages and we consider our relations with our employees to be good.

Properties

We lease approximately 4,540 square feet of office space at our headquarters at 20725 S. Western Avenue, Ste. 136, Torrance, CA 90501-1884, at a base rent of $5,552 per month. This lease, which was to expire on May 31, 2011, was extended by the parties for an additional term beginning on June 1, 2011 and expiring on May 31, 2012. During the extension period, the monthly rent will be $4,994. In addition, we lease two office suites at 3870 Del Amo Boulevard, Torrance California under two separate leases: Suite 506 (approximately 1,400 square feet) at a base rent of $1,610 per month; and Suite 507 (approximately 1,300 square feet) at a base rent of $1,690 per month. The lease for Suite 506 will expire on August 19, 2011; the lease for Suite 507 will expire on February 28, 2013. Approximately 490 square feet of Suite 506 and 480 square feet of Suite 507 are currently subleased to an unaffiliated entity on a month to month basis. We do not expect to experience any difficulties in renewing our leases, or finding additional or replacement office and warehouse space, at their current or more favorable rates.

Legal Proceedings

We are not involved in any material legal proceedings outside of the ordinary course of our business.

15

RISK FACTORS

Any investment in our common stock involves a high degree of risk. Investors should carefully consider the risks described below and all of the information contained in this report before deciding whether to purchase our common stock. Our business, financial condition or results of operations could be materially adversely affected by these risks if any of them actually occur. Our shares of common stock are not currently listed or quoted for trading on any national securities exchange or national quotation system. If and when our common stock is traded, the trading price could decline due to any of these risks, and an investor may lose all or part of his or her investment. Some of these factors have affected our financial condition and operating results in the past or are currently affecting us. This Current Report on Form 8-K also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks described below and elsewhere in this report.

We have incurred losses since inception, have limited cash resources and anticipate that we will continue to incur substantial losses for the foreseeable future.

Emmaus Medical is still in the development stage. As of December 31, 2010, we had an accumulated deficit of $12.8 million since our inception in 2000. Our net losses were $3.8 million and $2.6 million for the years ended December 31, 2010 and 2009, respectively. These losses resulted principally from costs incurred in our research and development programs and from our general and administrative expenses. We have had limited revenue, have sustained significant operating losses, and are likely to sustain operating losses in the foreseeable future.

We expect to continue to incur significant and increasing negative cash flow and operating losses as we continue our research activities, conduct clinical trials, and seek regulatory approvals for our L-glutamine treatment for SCD. These losses, among other things, have had and will continue to have an adverse effect on our stockholders’ equity, total assets and working capital. We believe, based on our current operating plan, that our cash, cash equivalents and marketable securities will be sufficient to fund our operations for the next 15 months. Because of the numerous risks and uncertainties associated with drug development, we are unable to predict the extent of any future losses, whether or when we will be able to commercialize our L-glutamine treatment for SCD, or when we will become profitable, if at all. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis.

Our recurring operating losses have raised substantial doubt regarding our ability to continue as a going concern.

Our recurring operating losses raise substantial doubt about our ability to continue as a going concern. As a result, our independent registered public accounting firm included an explanatory paragraph in its report on our financial statements as of and for the year ended December 31, 2010 with respect to this uncertainty. The perception of our ability to continue as a going concern may make it more difficult for us to obtain financing for the continuation of our operations and could result in the loss of confidence by investors, suppliers and employees.

We will require substantial additional funding and may be unable to raise capital when needed, which could force us to delay, reduce or eliminate planned activities or result in our inability to continue as a going concern.

We may require additional capital to pursue planned clinical trials and regulatory approvals, as well as further research and development and marketing efforts for our products and potential products. Our future capital requirements will depend on, and could increase significantly as a result of, many factors, including:

|

|

●

|

the duration and results of the clinical trials for our various products going forward;

|

|

|

●

|

unexpected delays or developments in seeking regulatory approvals;

|

|

|

●

|

the time and cost in preparing, filing, prosecuting, maintaining and enforcing patent claims;

|

|

|

●

|

other unexpected developments encountered in implementing our business development and commercialization strategies; and

|

16

|

|

●

|

the outcome of litigation, if any, and further arrangements, if any, with collaborators.

|

We may attempt to raise additional funds through public or private financings, collaborations with other pharmaceutical companies or financing from other sources. Additional funding may not be available on terms which are acceptable to us. If adequate funding is not available to us on reasonable terms, we may need to delay, reduce or eliminate one or more of our product development programs or obtain funds on terms less favorable than we would otherwise accept. To the extent that additional capital is raised through the sale of equity securities or securities convertible into or exchangeable for equity securities, the issuance of those securities could result in dilution to our stockholders. Moreover, the incurrence of debt financing could result in a substantial portion of our future operating cash flow, if any, being dedicated to the payment of principal and interest on such indebtedness and could impose restrictions on our operations. This could render us more vulnerable to competitive pressures and economic downturns.

If we are unsuccessful in raising additional required funds, we may be required to delay, scale-back or eliminate plans or programs relating to our business. In addition, if we do not meet our payment obligations to third parties as they come due, we may be subject to litigation claims. Even if we are successful in defending against these claims, litigation could result in substantial costs and be a distraction to management, and may result in unfavorable results that could further adversely impact our financial condition.

Raising additional capital may cause dilution to our existing stockholders, restrict our operations or require us to relinquish rights.

We may seek additional capital through a combination of private and public equity offerings, debt financings and collaborations and strategic and licensing arrangements. To the extent that we raise additional capital through the sale of equity or convertible debt securities, your ownership interest will be diluted, and the terms may include liquidation or other preferences that adversely affect your rights as a stockholder. Debt financing, if available, would result in increased fixed payment obligations and may involve agreements that include covenants limiting or restricting our ability to take specific actions such as incurring debt, making capital expenditures or declaring dividends. If we raise additional funds through collaboration, strategic alliance and licensing arrangements with third parties, we may have to relinquish valuable rights to our technologies, future revenue streams or product candidates, or grant licenses on terms that are not favorable to us.

Our business is subject to extensive government regulation, which could cause delays in the development and commercialization of our drug products, impose significant costs on us or provide advantages to our larger competitors.

The FDA and similar agencies in foreign countries impose substantial requirements upon the development, manufacture and marketing of drugs. They require laboratory and clinical testing procedures, manufacturing, labeling, registration, notification, clearance or approval, marketing, distribution, recordkeeping, reporting and promotion, and other costly and time-consuming procedures. Satisfaction of clearance or approval requirements typically takes several years or more and varies substantially from country to country as well as upon the type, complexity and novelty of the therapeutic product.

The effect of government regulation may be to delay marketing of products for a considerable or indefinite period of time, to impose costly procedures upon our activities and to furnish a competitive advantage to larger companies that compete with us. There can be no assurance that the FDA or other regulatory clearance or approval for any products developed by us will be granted on a timely basis, if at all, or, once granted, that clearances or approvals will not be withdrawn or other regulatory actions taken which might limit our ability to market our proposed products. Any such delay in obtaining or failure to obtain such clearance or approvals would adversely affect us, the manufacturing and marketing of the products we intend to develop and our ability to generate product revenue.

We cannot assure you that we will be able to complete our clinical trial programs successfully within any specific time period, or if such clinical trials take longer to complete than we project, our ability to execute our current business strategy will be adversely affected.

We do not know if our current clinical trials for our L-glutamine treatment for SCD will be completed on schedule or at all. Even if completed, we do not know if these trials will produce clinically meaningful results sufficient

17

to support an application for marketing approval. Whether or not and how quickly we complete clinical trials is dependent in part upon the rate at which we are able to obtain regulatory clearance to commence clinical trials, engage clinical trial sites and medical investigators, reach agreement on acceptable clinical trial agreement terms or clinical trial protocols with medical investigators or clinical trial sites or institutional review boards and, thereafter, the rate of enrollment of patients, and the rate to collect, clean, lock and analyze the clinical trial database.

Patient enrollment is a function of many factors, including the design of the protocol, the size of the patient population, the proximity of patients to and availability of clinical sites, the eligibility criteria for the study, the perceived risks and benefits of the drug under study and of the control drug, if any, the efforts to facilitate timely enrollment in clinical trials, the patient referral practices of physicians, the existence of competitive clinical trials, and whether existing or new drugs are approved for the indication. If we experience delays in identifying and contracting with sites and/or in patient enrollment/completion in our clinical trial programs, we may incur additional costs and delays in our development programs, and may not be able to complete our clinical trials on a cost-effective or timely basis. Accordingly, we may not be able to complete the clinical trials within an acceptable time frame, if at all. If we or any third party have difficulty obtaining clinical drug materials or enrolling a sufficient number of patients to conduct its clinical trials as planned, or if enrolled patients do not complete the trial as planned, we or a third party may need to delay or terminate ongoing clinical trials, which could negatively affect our business.

Clinical trials often require the enrollment of large numbers of patients, and suitable patients may be difficult to identify and recruit. Our ability to enroll sufficient numbers of patients in our clinical trials depends on many factors, including the size of the patient population, the nature and design of the protocol, the proximity of patients to clinical sites, the eligibility criteria for the trial, competing clinical trials and the availability of approved effective drugs. In addition, patients may withdraw from a clinical trial or be unwilling to follow our clinical trial protocols for a variety of reasons. If we fail to enroll and maintain the number of patients for which the clinical trial was designed, the statistical power of that clinical trial may be reduced which would make it harder to demonstrate that the product candidate being tested in such clinical trial is safe and effective. Additionally, we may not be able to enroll a sufficient number of qualified patients in a timely or cost-effective manner.

The drug development process to obtain FDA approval is very costly and time consuming and if we cannot complete our clinical trials in a cost-effective manner, our results of operations may be adversely affected.

Even with the granting of orphan drug status and fast track designation, the cost associated with the successful development of the L-glutamine treatment for SCD is uncertain. Costs of clinical trials may vary significantly over the life of a project owing but not limited to the following:

|

|

●

|

the duration of the clinical trial;

|

|

|

●

|

the number of sites included in the trials;

|

|

|

●

|

the countries in which the trial is conducted;

|

|

|

●

|

the length of time required to enroll eligible patients;

|

|

|

●

|

the number of patients that participate in the trials;

|

|

|

●

|

the number of doses that patients receive;

|

|

|

●

|

the drop-out or discontinuation rates of patients;

|

|

|

●

|

per patient trial costs;

|

|

|

●

|

potential additional safety monitoring or other studies requested by regulatory agencies;

|

|

|

●

|

the duration of patient follow-up;

|

|

|

●

|

the efficacy and safety profile of the product candidate;

|

|

|

●

|

the costs and timing of obtaining regulatory approvals; and

|

|

|

●

|

the costs involved in enforcing or defending patent claims or other intellectual property rights.

|

If we are unable to control the costs of our clinical trials and conduct our trials in a cost-effective manner, our results of operations may be adversely affected.

We may be required to suspend, repeat or terminate our clinical trials if they do not meet regulatory requirements, the results are negative or inconclusive or adversely affect the necessary human subject

18

protections, or if the trials are not well designed, which may result in significant negative repercussions on our business and financial condition.