Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - TESSERA TECHNOLOGIES INC | d8k.htm |

| EX-99.1 - PRESS RELEASE - TESSERA TECHNOLOGIES INC | dex991.htm |

Exhibit 99.2

Q1 2011 Earnings Prepared Remarks

Summary Results

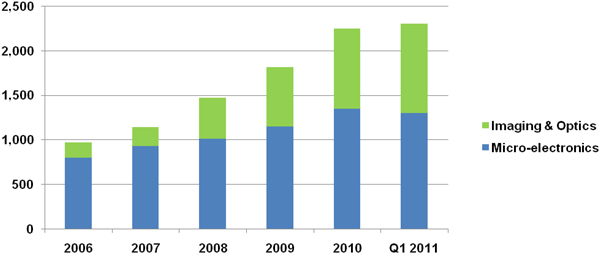

Total Tessera Technologies, Inc. revenue for the first quarter of 2011 was $67.8 million, compared to $64.3 million of total revenue in the first quarter of 2010. Micro-electronics revenue for the first quarter of 2011 was $53.6 million, compared to $55.8 million in the prior year first quarter, which included a $3.0 million settlement payment from United Test and Assembly Center Ltd. (UTAC). Imaging & Optics total revenue was $14.2 million, up 66% compared to first quarter 2010 Imaging & Optics revenue of $8.5 million. One of the main Imaging & Optics revenue drivers was increased royalties from our Extended Depth of Field (EDoF) technology, as the number of handsets shipped with our EDoF technology increased compared to the prior quarter.

First quarter of 2011 GAAP Net income was $11.2 million, or $0.22 per diluted share. Non-GAAP Net income was $19.0 million, or $0.36 per diluted share. First quarter of 2010 GAAP Net income was $9.8 million, or $0.20 per diluted share. First quarter of 2010 Non-GAAP Net income was $17.8 million, or $0.35 per diluted share. Cash, cash equivalents, and investments at March 31, 2011, were $499.5 million, an increase of $24.5 million in the quarter.

Segment Review

Micro-electronics

In our Micro-electronics segment, we develop, license and deliver advanced integrated circuit (IC) packaging solutions that are primarily used in the high growth mobile wireless and DRAM device markets. The majority of Tessera’s revenue consists of per unit royalties paid to us for use of our Micro-electronics’ patents and technologies under a Tessera Compliant Chip (TCC) license agreement, which typically provides licensees access to approximately 250 U.S. and foreign Tessera patents.

Our overall Micro-electronics patents and patent applications number approximately 1,300, many of which read on technologies in practice today. Our patented solutions have been licensed to a broad array of companies, and we have ongoing licensing programs to secure other companies’ access to our patented solutions. Historically, our primary licensing program was our TCC program, which encompasses our semiconductor packaging technology and patents. More recently, we have created a new program that focuses on technologies and patent classes outside of traditional semiconductor packaging such as DRAM circuitry design and memory modules.

1

If negotiations with companies that ship products incorporating our intellectual property (IP) are unsuccessful, we may pursue legal action to ensure fair payment for use of our IP and to protect our licensees in good standing. We may pursue such matters in court or before the International Trade Commission (ITC), which in each case is typically a multi-year process.

In the DRAM market, our chip scale packaging (CSP) solutions are used in high volume for DRAM chips such as DDR2 and DDR3 that Gartner forecasts will be in high volume production through at least 2015. In addition, we believe our current and next generation solutions have been optimized to meet the performance and cost requirements for future DRAM, such as DDR4. Our next generation solutions include single chip and multi-chip packages as well as technologies related to memory chip circuitry and memory modules, amongst others; these additional technologies are not included in our TCC license agreements.

In the mobile wireless device market, our CSP, multi chip packaging (MCP) and package on package (POP) solutions are used for chips such as baseband processors, Digital Signal Processors (DSP) and Power Management ICs that are used in mobile wireless devices such as smartphones. We believe some of the major chip companies operating in the mobile wireless device market are manufacturing products using our technology without fairly compensating Tessera. In addition, those that have a license to a single portfolio of technologies may benefit from licensing additional portfolios. We are pursuing multiple licensing strategies to remedy both situations.

Early in the second quarter of 2011, we announced the formation of a new group within our Micro-electronics segment specifically charged with developing, acquiring and monetizing semiconductor technologies beyond packaging. This group, which operates through a subsidiary named Invensas Corporation, is led by Simon McElrea, who has more than 15 years of executive, technical and operational management experience in semiconductor and green technology businesses. Invensas pursues both licensing and product development, supported by an initial portfolio of approximately 280 patents and patent applications. Its current focus is on circuitry design, memory modules, 3-D architecture, and advanced interconnect technologies, among other areas. We are continuing our research and development activities in our traditional semiconductor packaging efforts as well. And, we intend to offer the benefits of all these new technologies to companies with whom we are in licensing discussions. We believe these new technologies will increase the value we provide to our licensees, as it will bring multiple levels of intellectual property innovation to consumer electronic devices.

2

Finally, with regard to our innovative silent air cooling technology, we are pursuing a product model versus a licensing model. We are on track to be ready for high volume manufacturing in the fourth quarter of 2011, utilizing an outsourced manufacturing supply chain. Our first commercial product will be used in the ultra thin elite laptop market.

Imaging & Optics

In our Imaging & Optics segment, our solutions include innovative lens designs, digital image processing algorithms, and micro electro mechanical systems (MEMS) camera modules that provide cost-effective, small form-factor, high-quality camera functionality in consumer electronics devices. Our primary end market for Imaging & Optics is camera phones. We also license our imaging technologies into the digital still camera market and manufacture and sell optical products into specialist applications.

This segment is led by Bob Roohparvar, who as previously announced joined Tessera as our new president of Imaging & Optics in March of 2011. Bob comes to Tessera from Flextronics, Inc. and brings a wealth of technical expertise, extensive consumer optics market knowledge, deep industry relationships, and high volume manufacturing experience. We have reorganized all Imaging & Optics business units under a single subsidiary named DigitalOptics Corporation to more effectively leverage our R&D resources, marketing expertise and customer relationships. Bob and his team are analyzing our extensive portfolio of Imaging & Optics technologies, products and associated roadmaps, exploring possible strategies to maximize the opportunities in the Imaging & Optics space we see ahead of us.

Turning to the first quarter of 2011, Imaging & Optics revenue grew approximately 66% to $14.2 million year-over-year. Items that contributed to this increase were an uptick in sales of our Micro-optics products and increased royalties from our EDoF technology. We expect our EDoF royalty growth will generally track that of the overall EDoF market, which industry analyst Techno Systems Research forecasts will grow to more than 120 million camera phones with EDoF in 2011.

3

We completed a 15% workforce reduction in our Imaging & Optics segment in the first quarter of 2011, primarily in the Micro-optics and Embedded Image Enhancement business lines. The resulting streamlined organization is focused on four areas – EDoF, zoom, MEMS auto-focus, and Micro-optics.

We made progress in the first quarter of 2011 with the signing of our first zoom licensee, Samsung. Zoom is an innovative solution combining lens design with software that delivers near optical system performance within the size and cost constraints of today’s wireless device market. This is our first time implementing our zoom technology and addressing the related significant technical requirements. We believe we will receive our first zoom royalties in the second half of 2012, with royalties ramping in 2013.

With regard to MEMS auto-focus, we remain on track to be high volume manufacturing ready by the end of 2011. MEMS auto-focus is expected to be a significant growth driver for us in 2012 and beyond.

As previously announced, we believe Imaging & Optics may grow more quickly and better serve its customers as a stand-alone entity. As such, we are evaluating multiple alternatives to that end with our financial advisor, GCA Savvian Advisors, LLC, including, among others, a spin-off transaction.

4

Patent Assets

We continue to foster innovation and dedicate significant resources to inventing and acquiring new technology. High-quality patents are the international currency of innovation. As of March 31, 2011, Tessera and its subsidiaries owned approximately 2,300 domestic and international patents and patent applications. Nearly 1,300 of these patents and patent applications are for technologies related to our Micro-electronics segment. Approximately 1,000 patents and patent applications are for technologies related to our Imaging & Optics segment. The lives of certain patents extend to March 2030.

5

Financial Discussion

Quarterly Revenue

| Q1 2011 | Q1 2010 | Y-o-Y % | Q4 2010 | Q-o-Q % | ||||||||||||||||

| Total Revenue |

$ | 67.8 | $ | 64.3 | 5 | % | $ | 80.4 | (16 | %) | ||||||||||

| Micro-electronics |

$ | 53.6 | $ | 55.8 | (4 | %) | $ | 71.2 | (25 | %) | ||||||||||

| Imaging & Optics |

$ | 14.2 | $ | 8.5 | 66 | % | $ | 9.2 | 53 | % | ||||||||||

| Imaging & Optics – Royalties |

$ | 4.9 | $ | 2.3 | 113 | % | $ | 3.5 | 39 | % | ||||||||||

(in Millions, except %)

Revenue for the first quarter of 2011 was $67.8 million which was near the high end of our $65 million to $68 million guidance provided in our January 27, 2011 earnings report.

Total Micro-electronics revenue was $53.6 million which included a $1.0 million license fee. Sequential revenues decreased $17.6 million or 25%. As we indicated in our fourth quarter prepared remarks, five licensees or former licensees are in breach of contract or have not renewed their license agreements. Approximately $8.7 million of the sequential decline in revenue was attributable to these licensees or former licensees. Additionally, fourth quarter 2010 revenues benefited by a royalty payment of $6.0 million from UTAC as a result of our 2010 settlement and a $2.3 million catch up royalty payment. Excluding the aforementioned five current and former licensees who are either in breach of contract or who have not renewed their license agreements, our first quarter 2011 recurring royalties decreased approximately $0.6 million sequentially, due primarily to higher shipments in the prior quarter for several new products at one of our licensees.

Relative to the prior year, first quarter 2011 Micro-electronics revenue was down $2.2 million, or 4%. First quarter 2010 revenue benefited from a royalty payment of $3.0 million from UTAC as a result of our 2010 settlement and included approximately $8.0 million in revenue from the aforementioned five licensees or former licensees who are in breach of contract or have not renewed. The company did not receive payment in the first quarter 2011 from these companies, the amount of which was more than offset by increased royalties of $8.1 million from licensees in good standing.

6

Imaging & Optics total revenue in the first quarter of 2011 was $14.2 million and consisted of royalties, license fees, and product and services revenue. Royalty and license revenue was $8.7 million, up 65% quarter-over-quarter and 179% year-over-year. Sequential royalty and license revenue increased $3.5 million due to increased EDoF royalties and one-time items including a $2.0 million license fee and $0.6 million of royalties for our embedded image enhancement technology. Royalties were $4.9 million, up 39% sequentially and up 113% year-over-year and included the aforementioned one-time catch up royalty payment of $0.6 million. Products and services revenue was $5.5 million, an increase of $1.5 million from Micro-optics sales related to stronger lithography sales.

Quarterly GAAP Results

Total GAAP operating expenses in the first quarter of 2011 were $51.7 million as follows:

| • | Cost of revenues: $5.5 million; |

| • | R&D: $18.6 million; |

| • | SG&A: $19.5 million; |

| • | Litigation expense: $6.0 million; and |

| • | Restructuring expense: $2.1 million. |

Included in the GAAP operating expenses above are the following:

| • | Stock-based compensation expense: $6.1 million; and |

| • | Amortization of acquired intangibles: $4.1 million. |

In addition, other income, net of expense, was $0.6 million, and GAAP tax expense was $5.5 million, representing a 33% effective tax rate for the quarter. The first quarter effective tax rate was lower than our guide of 39% due to higher than expected foreign earnings.

First quarter total GAAP operating expenses were down 6% or $3.3 million quarter-over-quarter. The sequential decrease was mainly due to higher non-recurring expenses in the fourth quarter 2010 than the first quarter 2011. As a reminder, we announced the cessation of development of our wafer-level optics technology in our October 28, 2010 prepared remarks and recognized a $3.5 million impairment charge in the fourth quarter of 2010. In the first quarter of 2011 we recognized a non-recurring reduction-in-workforce restructuring charge of $2.1 million. Additionally, SG&A expense decreased by $1.3 million sequentially mainly related to a reduction in patent analysis related materials. Litigation expense was down $0.2 million or 3% sequentially.

7

Quarterly GAAP Net Income and EPS

| Q1 2011 | Q1 2010 | Y-o-Y % | Q4 2010 | Q-o-Q % | ||||||||||||||||

| GAAP Net Income |

$ | 11.2 | $ | 9.8 | 12 | % | $ | 13.5 | (18 | %) | ||||||||||

| GAAP EPS |

$ | 0.22 | $ | 0.20 | $ | 0.27 | ||||||||||||||

| Fully Diluted Shares |

51,267 | 50,123 | 50,942 | |||||||||||||||||

(in Millions, except per share and % data)

Quarterly Non-GAAP Results

Total Non-GAAP operating expenses in the first quarter of 2011 were $41.5 million as follows:

| • | Cost of revenues: $3.7 million; |

| • | R&D: $15.4 million; |

| • | SG&A: $14.3 million; |

| • | Litigation expense: $6.0 million; and |

| • | Restructuring expense: $2.1 million. |

First quarter total Non-GAAP operating expenses were up $0.8 million or 2% quarter-over-quarter primarily related to the $2.1 million reduction-in-work force charge recognized in the first quarter of 2011. Cost of revenues was up $0.3 million or 6% quarter-over-quarter, due to the increase in product sales. R&D expense was down $0.3 million or 2% quarter-over-quarter, primarily due to a decrease in depreciation expense related to the fourth quarter 2010 impairment of certain wafer-level optics fixed assets which have been classified as available-for-sale and no longer depreciated. SG&A expenses were down $1.1 million or 7% quarter-over-quarter mainly related to a decrease in patent analysis related materials.

Non-GAAP results exclude stock-based compensation, charges for acquired in-process research and development, acquired intangibles amortization, impairment charges on long-lived assets, and related tax effects. We have included a detailed reconciliation between our GAAP and Non-GAAP net income in both our earnings release and on our web site for your convenient reference.

8

Quarterly Non-GAAP Net Income and EPS

Tax adjustments in the first quarter of 2011 for Non-GAAP items were approximately $2.4 million.

| Q1 2011 | Q1 2010 | Y-0-Y % | Q4 2010 | Q-o-Q % | ||||||||||||||||

| Non-GAAP Net Income |

$ | 19.0 | $ | 17.8 | 3 | % | $ | 23.1 | (18 | %) | ||||||||||

| Non-GAAP EPS |

$ | 0.36 | $ | 0.35 | $ | 0.44 | ||||||||||||||

| Fully Diluted Shares |

52,548 | 51,009 | 52,509 | |||||||||||||||||

(in Millions, except per share and % data)

Balance Sheet Metrics

We ended the quarter with $499.5 million in cash, cash equivalents, and investments, a $24.5 million increase over the prior quarter. Net cash provided by operations for the quarter was $22.0 million.

Second Quarter 2011 Guidance

Total revenue for the second quarter 2011 will range between $75.5 million and $78.5 million, which compares to second quarter 2010 total revenue of $74.6 million.

Micro-electronics revenue will range between $65 million and $67 million, all of which will be royalties and license fees. As a comparison, second quarter 2010 Micro-electronics royalties and license fees were $65.1 million.

Our second quarter 2011 guidance reflects, similar to the first quarter 2011, no revenue from the five licensees or former licensees that are either in breach of contract or have not renewed their license agreements. We continue to pursue legal redress based on our long standing practice of ensuring fair payment for use of our IP and protecting our licensees in good standing. The timing of resolution of these litigation and arbitration matters is difficult to predict.

Two major DRAM manufacturers have volume pricing adjustments in their licenses that may cause, only for these two DRAM manufacturers when unit shipment volumes are high, our aggregate annual DRAM royalty revenue to grow less rapidly than annual growth in overall unit shipments in the DRAM market.

9

Our second quarter 2011 revenue is expected to benefit by $10 million to $12 million due to the annual reset of the volume pricing adjustments with these two DRAM manufacturers, along with other factors.

Second quarter 2011 Imaging & Optics revenue, in total, is expected to range between $10.5 million and $11.5 million. This compares to second quarter 2010 Imaging & Optics revenue of $9.5 million.

Second quarter 2011 Imaging & Optics royalties and license fees are expected to be approximately $5.0 million to $5.5 million. Sequentially, royalties and license fees are expected to be down $3.4 million principally due to non-recurring royalty and license fees and seasonality in our EDoF royalties. For reference, royalties and license fees were $3.3 million in the second quarter of 2010, which included $0.9 million of license fees and $2.4 million of royalties.

Second quarter 2011 products and services revenue is expected to range between $5.5 million and $6.0 million. For reference, products and services revenue was $6.2 million in the second quarter of 2010.

Second quarter 2011 Non-GAAP operating expenses, less litigation expense, are expected to range between $35 million and $36 million.

Non-GAAP cost of revenues is expected to be down approximately 3% to 7% sequentially.

Non-GAAP R&D is expected to be up approximately 9% to 12% sequentially as we anticipate additional non-recurring engineering and material cost to support the continued advancement of both our MEMS and silent air cooling technologies previously anticipated to occur in the first quarter 2011.

Non-GAAP SG&A is expected to up approximately 3% to 6% sequentially.

We expect our litigation expense in the second quarter of 2011 to be slightly higher in comparison to the prior quarter. We anticipate continued efforts related to the Hynix antitrust action, the Amkor arbitration, the UTAC Taiwan Corporation breach of contract case, the Sony and Renesas Electronics Corporation patent infringement cases, and legal activity related to appeals pending in the U.S. Court of Appeals for the Federal Circuit.

10

We expect second quarter 2011 stock-based compensation to be approximately $6.6 million and amortization charges to be $4.3 million.

Our estimated tax rate for fiscal year 2011 is expected to be in the range of 35% to 37%.

Finally, while our policy is to guide one quarter forward, we did want to comment on the potential impact of the earthquake in Japan and related events. First and foremost, our heartfelt sympathy goes out to the victims of these tragic events. Although we do not anticipate any significant impact on our financial performance in the second quarter, the extent of the impact beyond the second quarter has not yet been determined.

Litigation Review

On March 29, 2011, the U.S. Court of Appeals for the Federal Circuit (the “Federal Circuit”) ruled in our favor by denying the respondents’ request for a rehearing of its decision upholding the ITC’s Final Determination in Tessera’s favor in our ITC 605 Wireless case. The respondents have 90 days within which to petition the U.S. Supreme Court on this matter. We intend to pursue our stayed district court actions after the stays currently in effect in those cases are lifted, which we expect will occur once the appellate process is completed.

In the appeal of the ITC 630 DRAM case, we participated in oral argument before the Federal Circuit on January 14, 2011, and await the Court’s ruling.

A third matter, Powertech Technology, Inc. v. Tessera, is also before the Federal Circuit. This case was originally filed in the U.S. District Court for the Northern District of California in March of 2010 by Powertech Technology Inc. (PTI), which sought a declaratory judgment of noninfringement and invalidity of Tessera’s U.S. Patent No. 5,663,106. In June 2010, the District Court granted Tessera’s motion to dismiss the complaint for lack of subject matter jurisdiction, and afterwards PTI appealed. Principal and reply briefs have been filed and oral arguments are currently scheduled for May 4, 2011.

The Tessera v. Hynix antitrust lawsuit, which we filed in 2006, is now before the California Superior Court in San Francisco. We are progressing through the final remaining aspects of the pretrial phase of the case, but the Court has not yet set a trial date.

11

Similarly, we are making progress in the Amkor arbitration, which began in August 2009. Post-trial briefing on Phase I of the case was completed in the first quarter and a trial on Phase II is scheduled to begin in August 2011. As a reminder, the previous Amkor arbitration took approximately three years before being resolved in Tessera’s favor.

In addition, we are prosecuting a lawsuit in the U.S. District Court for the Northern District of California against UTAC Taiwan Corporation for breach of contract and breach of the covenant of good faith and fair dealing. The lawsuit also seeks declaratory relief. We also are prosecuting a patent infringement lawsuit against Sony and Renesas Electronics Corporation in the U.S. District Court for the District of Delaware. Both of these cases remain in their preliminary phases.

Patent Reform

As a technology innovator, we are very interested in the current patent reform debate. In the first quarter of 2011, the U.S. Senate passed S. 23, the America Invents Act, and the House of Representatives is currently considering H.R. 1249, which has the same title and many of the same provisions.

We strongly support the provision in each bill that would end the diversion of U.S. Patent and Trademark Office (USPTO) fees. The USPTO needs all possible resources to reduce its backlog of over one million patents.

We are against provisions that we believe would hamper a patent owner’s ability to enforce all rights conferred by a patent, including the right to prevent others from using and selling a patented invention.

We are also against provisions that would create a patent litigation and re-examination system that would tilt the playing field in ways that protect the interest of large infringers but undermine the enforceability of patent rights to the detriment of innovation-based job growth.

Finally, although the proposed first-to-file provision in each bill may have little negative impact on companies like Tessera, which are financially and professionally better situated than many to quickly file multiple patent applications, we believe such a dramatic change in the law may have a significant negative impact on the American economy as a whole. The current, longstanding, and uniquely American first-to-invent system better protects entrepreneurs and small companies, those entities that are primarily responsible for job creation in our current economy.

12

Safe Harbor Statement

This document contains forward-looking statements, which are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve risks and uncertainties that could cause actual results to differ significantly from those projected, particularly with respect to the company’s financial results, the impact of the reorganization of our Imaging & Optics segment, the impact of the retention of GCA Savvian Advisors, LLC as the company’s financial advisor, the exploration of various alternatives for the Imaging & Optics business, the size of market opportunities, growth of the company’s served markets, industry and technology trends, use of the company’s technology in additional applications, impact of volume pricing adjustments in our Micro-electronics segment and revenue growth in our Imaging & Optics segment, future investment and development resources, the expansion of the company’s intellectual property portfolios, and the company’s IP protection efforts, including litigation. Material factors that may cause results to differ from the statements made include changes to the company’s plans or operations relating to its businesses and groups, market or industry conditions; delays, setbacks or losses relating to our intellectual property or intellectual property litigations, or any invalidation or limitation of our key patents; fluctuations in our operating results due to the timing of new license agreements and royalties, or due to legal costs; changes in patent laws, regulation or enforcement, or other factors that might affect our ability to protect our intellectual property; the risk of a decline in demand for semiconductor products; failure by the industry to adopt our technologies; competing technologies; the future expiration of our patents; the future expiration of our license agreements and the cessation of related royalty income; the failure or refusal of licensees to pay royalties; failure to identify or complete a favorable transaction with respect to the Imaging & Optics business; failure to achieve the growth prospects and synergies expected from acquisition transactions; and delays and challenges associated with integrating acquired companies with our existing businesses. You are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date of this release. Tessera’s filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended Dec. 31, 2010 include more information about factors that could affect the company’s financial results. Tessera assumes no obligation to update information contained in this press release. Although this release may remain available on Tessera’s website or elsewhere, its continued availability does not indicate that Tessera is reaffirming or confirming any of the information contained herein.

13

Non-GAAP Financial Measures

In addition to disclosing financial results calculated in accordance with U.S. generally accepted accounting principles (GAAP), this document contains non-GAAP financial measures adjusted for either one-time or ongoing non-cash acquired intangibles amortization charges, acquired in-process research and development, all forms of stock-based compensation, impairment charges on long-lived assets, and related tax effects. The non-GAAP financial measures also exclude the effects of FASB Accounting Standards Codification Topic 718 – Stock Compensation upon the number of diluted shares used in calculating non-GAAP earnings per share. Management believes that the non-GAAP measures used in this report provide investors with important perspectives into the company’s ongoing business performance. The non-GAAP financial measures disclosed by the company should not be considered a substitute for, or superior to, financial measures calculated in accordance with GAAP, and the financial results calculated in accordance with GAAP and reconciliations to those financial statements should be carefully evaluated. The non-GAAP financial measures used by the company may be calculated differently from, and therefore may not be comparable to, similarly titled measures used by other companies.

14