Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 906 - Duff & Phelps Corp | v219843_ex32-1.htm |

| EX-10.1 - FORM OF PERFORMANCE - VESTING RESTRICTED STOCK AWARD AGREEMENT - Duff & Phelps Corp | v219843_ex10-1.htm |

| EX-32.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 906 - Duff & Phelps Corp | v219843_ex32-2.htm |

| EX-31.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 302 - Duff & Phelps Corp | v219843_ex31-1.htm |

| EX-31.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 302 - Duff & Phelps Corp | v219843_ex31-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

þ

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934.

|

For the quarterly period ended March 31, 2011

OR

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934.

|

Commission File Number: 001-33693

DUFF & PHELPS CORPORATION

(Exact name of registrant as specified in its charter)

|

DELAWARE

|

20-8893559

|

|

(State of other jurisdiction or

incorporation or organization)

|

(I.R.S. employer

identification no.)

|

55 East 52nd Street, 31st Floor

New York, New York 10055

(Address of principal executive offices)

(Zip code)

(212) 871-2000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer þ Non-accelerated filer o Smaller reporting company o

Indicated by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes o No þ

The number of shares outstanding of the registrant’s Class A common stock, par value $0.01 per share, was 31,401,784 as of April 15, 2011. The number of shares outstanding of the registrant’s Class B common stock, par value $0.0001 per share, was 11,072,746 as of April 15, 2011.

|

DUFF & PHELPS CORPORATION

|

|

AND SUBSIDIARIES

|

|

TABLE OF CONTENTS

|

|

Part I. Financial Information

|

|

|

Item 1. Financial Statements

|

1

|

|

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

|

22

|

|

Item 3. Quantitative and Qualitative Disclosures About Market Risk.

|

37

|

|

Item 4. Controls and Procedures.

|

37

|

|

Part II. Other Information

|

|

|

Item 1. Legal Proceedings

|

38

|

|

Item 1A. Risk Factors

|

38

|

|

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds

|

38

|

|

Item 3. Defaults Upon Senior Securities

|

39

|

|

Item 4. (Removed and Reserved)

|

39

|

|

Item 5. Other Information

|

39

|

|

Item 6. Exhibits

|

40

|

|

Signatures

|

41

|

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements.

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

(In thousands, except per share amounts)

(Unaudited)

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Revenue

|

$ | 85,046 | $ | 89,164 | ||||

|

Reimbursable expenses

|

1,892 | 2,798 | ||||||

|

Total revenue

|

86,938 | 91,962 | ||||||

|

Direct client service costs

|

||||||||

|

Compensation and benefits (includes $4,935 and $3,717 of equity-based

|

||||||||

|

compensation for the three months ended March 31, 2011 and 2010,

|

||||||||

|

respectively)

|

46,908 | 48,598 | ||||||

|

Other direct client service costs

|

1,429 | 1,988 | ||||||

|

Acquisition retention expenses (includes $82 of equity-based

|

||||||||

|

compensation for the three months ended March 31, 2011)

|

82 | — | ||||||

|

Reimbursable expenses

|

1,937 | 2,854 | ||||||

| 50,356 | 53,440 | |||||||

|

Operating expenses

|

||||||||

|

Selling, general and administrative (includes $1,523 and $1,453 of equity-

|

||||||||

|

based compensation for the three months ended March 31, 2011 and

|

||||||||

|

2010, respectively)

|

24,322 | 24,084 | ||||||

|

Depreciation and amortization

|

2,489 | 2,493 | ||||||

|

Merger and acquisition costs

|

194 | — | ||||||

|

Charge from impairment of certain intangible assets

|

— | 674 | ||||||

| 27,005 | 27,251 | |||||||

|

Operating income

|

9,577 | 11,271 | ||||||

|

Other expense/(income), net

|

||||||||

|

Interest income

|

(28 | ) | (24 | ) | ||||

|

Interest expense

|

57 | 92 | ||||||

|

Other expense/(income)

|

(7 | ) | (15 | ) | ||||

| 22 | 53 | |||||||

|

Income before income taxes

|

9,555 | 11,218 | ||||||

|

Provision for income taxes

|

3,064 | 3,650 | ||||||

|

Net income

|

6,491 | 7,568 | ||||||

|

Less: Net income attributable to noncontrolling interest

|

2,378 | 3,295 | ||||||

|

Net income attributable to Duff & Phelps Corporation

|

$ | 4,113 | $ | 4,273 | ||||

|

Weighted average shares of Class A common stock outstanding

|

||||||||

|

Basic

|

26,910 | 24,986 | ||||||

|

Diluted

|

27,615 | 25,780 | ||||||

|

Net income per share attributable to stockholders of Class A

|

||||||||

|

common stock of Duff & Phelps Corporation (Note 4)

|

||||||||

|

Basic

|

$ | 0.15 | $ | 0.16 | ||||

|

Diluted

|

$ | 0.14 | $ | 0.16 | ||||

|

Cash dividends declared per common share

|

$ | 0.08 | $ | 0.05 | ||||

See accompanying notes to the condensed consolidated financial statements.

- 1 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except per share amounts)

(Unaudited)

|

March 31,

|

December 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

ASSETS

|

||||||||

|

Current assets

|

||||||||

|

Cash and cash equivalents

|

$ | 78,429 | $ | 113,328 | ||||

|

Accounts receivable (net of allowance for doubtful accounts of $1,738 and $1,347

|

||||||||

|

at March 31, 2011 and December 31, 2010, respectively)

|

61,159 | 60,358 | ||||||

|

Unbilled services

|

28,758 | 23,101 | ||||||

|

Prepaid expenses and other current assets

|

12,206 | 7,479 | ||||||

|

Net deferred income taxes, current

|

— | 2,555 | ||||||

|

Total current assets

|

180,552 | 206,821 | ||||||

|

Property and equipment (net of accumulated depreciation of $27,918 and $26,375

|

||||||||

|

at March 31, 2011 and December 31, 2010, respectively)

|

29,404 | 29,250 | ||||||

|

Goodwill

|

139,396 | 139,170 | ||||||

|

Intangible assets (net of accumulated amortization of $21,683 and $20,656

|

||||||||

|

at March 31, 2011 and December 31, 2010, respectively)

|

29,517 | 30,407 | ||||||

|

Other assets

|

4,404 | 2,638 | ||||||

|

Investments related to deferred compensation plan (Note 9)

|

25,339 | 23,151 | ||||||

|

Net deferred income taxes, non-current

|

114,037 | 116,789 | ||||||

|

Total non-current assets

|

342,097 | 341,405 | ||||||

|

Total assets

|

$ | 522,649 | $ | 548,226 | ||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY

|

||||||||

|

Current liabilities

|

||||||||

|

Accounts payable

|

$ | 2,964 | $ | 2,397 | ||||

|

Accrued expenses

|

6,455 | 11,254 | ||||||

|

Accrued compensation and benefits

|

7,936 | 39,875 | ||||||

|

Liability related to deferred compensation plan, current portion (Note 9)

|

811 | 1,314 | ||||||

|

Deferred revenues

|

3,261 | 2,427 | ||||||

|

Net deferred income taxes, current

|

293 | — | ||||||

|

Other current liabilities

|

— | 430 | ||||||

|

Due to noncontrolling unitholders, current portion

|

5,640 | 5,640 | ||||||

|

Total current liabilities

|

27,360 | 63,337 | ||||||

|

Liability related to deferred compensation plan, less current portion (Note 9)

|

24,672 | 21,764 | ||||||

|

Other long-term liabilities

|

16,720 | 16,676 | ||||||

|

Due to noncontrolling unitholders, less current portion

|

104,251 | 103,885 | ||||||

|

Total non-current liabilities

|

145,643 | 142,325 | ||||||

|

Total liabilities

|

173,003 | 205,662 | ||||||

|

Commitments and contingencies (Note 10)

|

||||||||

|

Stockholders' equity

|

||||||||

|

Preferred stock (50,000 shares authorized; zero issued and outstanding)

|

— | — | ||||||

|

Class A common stock, par value $0.01 per share (100,000 shares authorized; 31,402 and 30,166

|

||||||||

|

shares issued and outstanding at March 31, 2011 and December 31, 2010, respectively)

|

314 | 302 | ||||||

|

Class B common stock, par value $0.0001 per share (50,000 shares authorized; 11,073 and 11,151

|

||||||||

|

shares issued and outstanding at March 31, 2011 and December 31, 2010, respectively)

|

1 | 1 | ||||||

|

Additional paid-in capital

|

239,132 | 232,644 | ||||||

|

Accumulated other comprehensive income

|

1,682 | 1,400 | ||||||

|

Retained earnings

|

18,562 | 16,923 | ||||||

|

Total stockholders' equity of Duff & Phelps Corporation

|

259,691 | 251,270 | ||||||

|

Noncontrolling interest

|

89,955 | 91,294 | ||||||

|

Total stockholders' equity

|

349,646 | 342,564 | ||||||

|

Total liabilities and stockholders' equity

|

$ | 522,649 | $ | 548,226 | ||||

See accompanying notes to the condensed consolidated financial statements.

- 2 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(Unaudited)

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Cash flows from operating activities:

|

||||||||

|

Net income

|

$ | 6,491 | $ | 7,568 | ||||

|

Adjustments to reconcile net income

|

||||||||

|

to net cash used in operating activities:

|

||||||||

|

Depreciation and amortization

|

2,489 | 2,493 | ||||||

|

Equity-based compensation

|

6,540 | 5,170 | ||||||

|

Bad debt expense

|

856 | 600 | ||||||

|

Net deferred income taxes

|

5,966 | 4,734 | ||||||

|

Other

|

15 | 277 | ||||||

|

Charge from impairment of certain intangible assets

|

— | 674 | ||||||

|

Changes in assets and liabilities providing/(using) cash:

|

||||||||

|

Accounts receivable

|

(1,657 | ) | 2,194 | |||||

|

Unbilled services

|

(5,657 | ) | (2,770 | ) | ||||

|

Prepaid expenses and other current assets

|

(64 | ) | 222 | |||||

|

Other assets

|

(987 | ) | 503 | |||||

|

Accounts payable and accrued expenses

|

(9,212 | ) | (5,488 | ) | ||||

|

Accrued compensation and benefits

|

(27,993 | ) | (22,706 | ) | ||||

|

Deferred revenues

|

834 | 685 | ||||||

|

Other liabilities

|

57 | (649 | ) | |||||

|

Net cash used in operating activities

|

(22,322 | ) | (6,493 | ) | ||||

|

Cash flows from investing activities:

|

||||||||

|

Purchase of property and equipment

|

(769 | ) | (1,518 | ) | ||||

|

Business acquisitions, net of cash acquired

|

(466 | ) | (481 | ) | ||||

|

Purchase of investments

|

(3,000 | ) | (2,975 | ) | ||||

|

Net cash used in investing activities

|

(4,235 | ) | (4,974 | ) | ||||

|

Cash flows from financing activities:

|

||||||||

|

Proceeds from exercises of IPO Options

|

268 | 28 | ||||||

|

Repurchases of Class A common stock

|

(5,815 | ) | (1,618 | ) | ||||

|

Dividends

|

(2,492 | ) | (1,403 | ) | ||||

|

Distributions and other payments to noncontrolling unitholders

|

(1,386 | ) | (1,343 | ) | ||||

|

Other

|

— | (3 | ) | |||||

|

Net cash used in financing activities

|

(9,425 | ) | (4,339 | ) | ||||

|

Effect of exchange rate on cash and cash equivalents

|

1,083 | (1,526 | ) | |||||

|

Net decrease in cash and cash equivalents

|

(34,899 | ) | (17,332 | ) | ||||

|

Cash and cash equivalents at beginning of period

|

113,328 | 107,311 | ||||||

|

Cash and cash equivalents at end of period

|

$ | 78,429 | $ | 89,979 | ||||

See accompanying notes to the condensed consolidated financial statements.

- 3 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

AND COMPREHENSIVE INCOME

(In thousands)

(Unaudited)

|

Stockholders of Duff & Phelps Corporation

|

||||||||||||||||||||||||||||||||||||||||

|

Accumulated

|

||||||||||||||||||||||||||||||||||||||||

|

Total

|

Additional |

Other

|

||||||||||||||||||||||||||||||||||||||

|

Stockholders'

|

Comprehensive

|

Common Stock - Class A

|

Common Stock - Class B

|

Paid-in

|

Comprehensive

|

Retained

|

Noncontrolling

|

|||||||||||||||||||||||||||||||||

|

Equity

|

Income

|

Shares

|

Dollars

|

Shares

|

Dollars

|

Capital

|

Income

|

Earnings

|

Interest

|

|||||||||||||||||||||||||||||||

|

Balance as of December 31, 2010

|

$ | 342,564 | 30,166 | $ | 302 | 11,151 | $ | 1 | $ | 232,644 | $ | 1,400 | $ | 16,923 | $ | 91,294 | ||||||||||||||||||||||||

|

Comprehensive income

|

||||||||||||||||||||||||||||||||||||||||

|

Net income for the three months ended March 31, 2011

|

6,491 | $ | 6,491 | — | — | — | — | — | — | 4,113 | 2,378 | |||||||||||||||||||||||||||||

|

Currency translation adjustment

|

1,431 | 1,431 | — | — | — | — | — | 290 | — | 1,141 | ||||||||||||||||||||||||||||||

|

Amortization of post-retirement benefits, net of tax

|

(39 | ) | (39 | ) | — | — | — | — | — | (8 | ) | — | (31 | ) | ||||||||||||||||||||||||||

|

Total comprehensive income

|

7,883 | $ | 7,883 | — | — | — | — | — | 282 | 4,113 | 3,488 | |||||||||||||||||||||||||||||

|

Issuance of Class A common stock for acquisitions

|

289 | 18 | — | — | — | 211 | — | — | 78 | |||||||||||||||||||||||||||||||

|

Exchange of New Class A Units

|

— | 77 | 1 | (77 | ) | — | (1 | ) | — | — | — | |||||||||||||||||||||||||||||

|

Net issuance of restricted stock awards

|

(4,667 | ) | 1,284 | 13 | — | — | (3,452 | ) | — | — | (1,228 | ) | ||||||||||||||||||||||||||||

|

Adjustment to Tax Receivable Agreement as a

|

||||||||||||||||||||||||||||||||||||||||

|

result of the exchange of New Class A Units

|

76 | — | — | — | — | 76 | — | — | — | |||||||||||||||||||||||||||||||

|

Issuance for exercises of IPO Options

|

113 | 7 | — | — | — | 83 | — | — | 30 | |||||||||||||||||||||||||||||||

|

Forfeitures

|

(1 | ) | (75 | ) | (1 | ) | (1 | ) | — | — | — | — | — | |||||||||||||||||||||||||||

|

Equity-based compensation

|

6,929 | — | — | — | — | 5,088 | — | — | 1,841 | |||||||||||||||||||||||||||||||

|

Income tax windfall/(shortfall) on equity-based compensation

|

817 | — | — | — | — | 817 | — | — | — | |||||||||||||||||||||||||||||||

|

Distributions to noncontrolling unitholders

|

(1,109 | ) | — | — | — | — | (816 | ) | — | — | (293 | ) | ||||||||||||||||||||||||||||

|

Change in ownership interests between periods

|

— | — | — | — | — | 4,976 | — | — | (4,976 | ) | ||||||||||||||||||||||||||||||

|

Deferred tax asset effective tax rate conversion

|

359 | — | — | — | — | 341 | — | — | 18 | |||||||||||||||||||||||||||||||

|

Repurchases of Class A common stock pursuant to

|

||||||||||||||||||||||||||||||||||||||||

|

publicly announced program

|

(1,133 | ) | (75 | ) | (1 | ) | — | — | (835 | ) | — | — | (297 | ) | ||||||||||||||||||||||||||

|

Dividends on Class A common stock

|

(2,474 | ) | — | — | — | — | — | — | (2,474 | ) | — | |||||||||||||||||||||||||||||

|

Balance as of March 31, 2011

|

$ | 349,646 | 31,402 | $ | 314 | 11,073 | $ | 1 | $ | 239,132 | $ | 1,682 | $ | 18,562 | $ | 89,955 | ||||||||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

- 4 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

AND COMPREHENSIVE INCOME/(LOSS)

(In thousands)

(Unaudited)

|

Stockholders of Duff & Phelps Corporation

|

||||||||||||||||||||||||||||||||||||||||

|

Accumulated

|

||||||||||||||||||||||||||||||||||||||||

|

Total

|

Additional |

Other

|

||||||||||||||||||||||||||||||||||||||

|

Stockholders'

|

Comprehensive

|

Common Stock - Class A

|

Common Stock - Class B

|

Paid-in

|

Comprehensive

|

Retained

|

Noncontrolling

|

|||||||||||||||||||||||||||||||||

|

Equity

|

Income

|

Shares

|

Dollars

|

Shares

|

Dollars

|

Capital

|

Income/(Loss)

|

Earnings

|

Interest

|

|||||||||||||||||||||||||||||||

|

Balance as of December 31, 2009

|

$ | 313,757 | 27,290 | $ | 273 | 12,974 | $ | 1 | $ | 207,210 | $ | 693 | $ | 6,709 | $ | 98,871 | ||||||||||||||||||||||||

|

Comprehensive income

|

||||||||||||||||||||||||||||||||||||||||

|

Net income for the three months ended March 31, 2010

|

7,568 | $ | 7,568 | — | — | — | — | — | — | 4,273 | 3,295 | |||||||||||||||||||||||||||||

|

Currency translation adjustment

|

(1,525 | ) | (1,525 | ) | — | — | — | — | — | (1,037 | ) | — | (488 | ) | ||||||||||||||||||||||||||

|

Amortization of post-retirement benefits

|

12 | 12 | — | — | — | — | — | 8 | — | 4 | ||||||||||||||||||||||||||||||

|

Total comprehensive income

|

6,055 | $ | 6,055 | — | — | — | — | — | (1,029 | ) | 4,273 | 2,811 | ||||||||||||||||||||||||||||

|

Sale of Class A common stock

|

(3 | ) | — | — | — | — | (3 | ) | — | — | — | |||||||||||||||||||||||||||||

|

Issuance of Class A common stock for acquisitions

|

322 | 19 | — | — | — | 222 | — | — | 100 | |||||||||||||||||||||||||||||||

|

Exchange of New Class A Units

|

— | 22 | — | (22 | ) | — | — | — | — | — | ||||||||||||||||||||||||||||||

|

Net issuance of restricted stock awards

|

(1,603 | ) | 1,352 | 14 | — | — | (1,108 | ) | — | — | (509 | ) | ||||||||||||||||||||||||||||

|

Adjustment to Tax Receivable Agreement as a

|

||||||||||||||||||||||||||||||||||||||||

|

result of the exchange of New Class A Units

|

34 | — | — | — | — | 34 | — | — | — | |||||||||||||||||||||||||||||||

|

Issuance for exercise of IPO Options

|

18 | 1 | — | — | — | 12 | — | — | 6 | |||||||||||||||||||||||||||||||

|

Forfeitures

|

(1 | ) | (63 | ) | (1 | ) | (7 | ) | — | — | — | — | — | |||||||||||||||||||||||||||

|

Equity-based compensation

|

5,755 | — | — | — | — | 3,923 | — | — | 1,832 | |||||||||||||||||||||||||||||||

|

Income tax benefit on equity-based compensation

|

72 | — | — | — | — | 72 | — | — | — | |||||||||||||||||||||||||||||||

|

Distributions to noncontrolling unitholders

|

(1,343 | ) | — | — | — | — | (917 | ) | — | — | (426 | ) | ||||||||||||||||||||||||||||

|

Change in ownership interests between periods

|

— | — | — | — | — | 4,031 | (2 | ) | — | (4,029 | ) | |||||||||||||||||||||||||||||

|

Deferred tax asset effective tax rate conversion

|

57 | — | — | — | — | 475 | — | — | (418 | ) | ||||||||||||||||||||||||||||||

|

Dividends on Class A common stock

|

(1,417 | ) | — | — | — | — | — | — | (1,417 | ) | — | |||||||||||||||||||||||||||||

|

Balance as of March 31, 2010

|

$ | 321,703 | 28,621 | $ | 286 | 12,945 | $ | 1 | $ | 213,951 | $ | (338 | ) | $ | 9,565 | $ | 98,238 | |||||||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

- 5 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Note 1 - DESCRIPTION OF BUSINESS

Duff & Phelps Corporation (the “Company”) is a leading provider of independent financial advisory and investment banking services. Its mission is to help its clients protect, maximize and recover value by providing independent advice on issues involving highly technical and complex assessments in the areas of valuation, transactions, financial restructuring, disputes and taxation. The Company believes that the Duff & Phelps brand is associated with experienced professionals who give trusted guidance in a responsive manner. The Company serves a global client base through offices in 24 cities, comprised of offices in 17 U.S. cities, including New York, Chicago, Dallas and Los Angeles, and seven international offices located in Amsterdam, London, Munich, Paris, Shanghai, Tokyo and Toronto.

Note 2 - BASIS OF PRESENTATION

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America and with the rules and regulations of the United States Securities and Exchange Commission (“SEC”) for interim financial reporting, and include all adjustments which are, in the opinion of management, necessary for a fair presentation. The financial statements require the use of management estimates and include the accounts of the Company, its controlled subsidiaries and other entities consolidated as required by accounting principles generally accepted in the United States of America (“GAAP”). References to the “Company,” “its” and “itself,” refer to Duff & Phelps Corporation and its subsidiaries, unless the context requires otherwise.

The balance sheet at December 31, 2010 was derived from audited financial statements, but does not include all disclosures required by GAAP. Accordingly, certain information and footnote disclosures normally included in financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to such rules and regulations. In management’s opinion, all adjustments necessary for a fair presentation are reflected in the interim periods presented. All significant intercompany accounts and transactions have been eliminated in consolidation.

Recently Adopted Accounting Pronouncements

Effective January 1, 2011, the Company adopted the Financial Accounting Standards Board’s (“FASB”) Accounting Standards Update (“ASU”) No. 2009-13, Multiple-Deliverable Revenue Arrangements. ASU 2009-13 supersedes certain guidance in FASB ASC 605-25, Revenue Recognition–Multiple-Element Arrangements and requires an entity to allocate arrangement consideration at the inception of an arrangement to all of its deliverables based on their relative selling prices (the relative-selling-price method). ASU 2009-13 eliminates the use of the residual method of allocation in which the undelivered element is measured at its estimated selling price and the delivered element is measured as the residual of the arrangement consideration, and requires the relative-selling-price method in all circumstances in which an entity recognizes revenue for an arrangement with multiple deliverable subject to ASU 2009-13. The adoption of ASU 2009-13 did not have a material effect on the Company’s consolidated financial statements.

Critical Accounting Policies

There have been no significant changes in new accounting pronouncements or in our critical accounting policies and estimates from those that were disclosed in our Annual Report on Form 10-K for the year ended December 31, 2010. The Company believes that the disclosures herein are adequate so that the information presented is not misleading; however, it is suggested that these financial statements be read in conjunction with the financial statements and the notes thereto in our Annual Report on Form 10-K for the year ended December 31, 2010. The financial data for the interim periods may not necessarily be indicative of results to be expected for the year.

- 6 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Note 3 - NONCONTROLLING INTEREST

As described in the Company’s Annual Report on Form 10-K for the year ended December 31, 2010, the Company has sole voting power in and controls the management of D&P Acquisitions, LLC and its subsidiaries (“D&P Acquisitions”), which collectively represent the operating subsidiaries of the Company. As a result, the Company consolidates the financial results of D&P Acquisitions and records noncontrolling interest for the economic interest in D&P Acquisitions held by the existing unitholders to the extent the book value of their interest in D&P Acquisitions is greater than zero. The Company’s economic interest in D&P Acquisitions totaled 73.9% at March 31, 2011. The noncontrolling unitholders’ interest in D&P Acquisitions totaled 26.1% at March 31, 2011.

Net income attributable to the noncontrolling interest on the statement of operations represents the portion of earnings or loss attributable to the economic interest in D&P Acquisitions held by the noncontrolling unitholders. Noncontrolling interest on the balance sheet represents the portion of net assets of D&P Acquisitions attributable to the noncontrolling unitholders based on the portion of total units of D&P Acquisitions owned by such unitholders (“New Class A Units”). The ownership of the New Class A Units is summarized as follows:

|

Duff &

|

Non-

|

|||||||||||

|

Phelps

|

controlling

|

|||||||||||

|

Corporation

|

Unitholders

|

Total

|

||||||||||

|

December 31, 2010

|

30,166 | 11,151 | 41,317 | |||||||||

|

Issuance of Class A common stock for acquisitions

|

18 | — | 18 | |||||||||

|

Exchange to Class A common stock

|

77 | (77 | ) | — | ||||||||

|

Net issuance of restricted stock awards

|

1,284 | — | 1,284 | |||||||||

|

Issuance for exercises of IPO Options

|

7 | — | 7 | |||||||||

|

Repurchases of Class A common stock

|

||||||||||||

|

pursuant to publicly announced program

|

(75 | ) | — | (75 | ) | |||||||

|

Forfeitures

|

(75 | ) | (1 | ) | (76 | ) | ||||||

|

March 31, 2011

|

31,402 | 11,073 | 42,475 | |||||||||

|

Percent of total

|

||||||||||||

|

December 31, 2010

|

73.0 | % | 27.0 | % | 100 | % | ||||||

|

March 31, 2011

|

73.9 | % | 26.1 | % | 100 | % | ||||||

A reconciliation from “Income before income taxes” to “Net income attributable to the noncontrolling interest” and “Net income attributable to Duff & Phelps Corporation” is detailed as follows:

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Income before income taxes

|

$ | 9,555 | $ | 11,218 | ||||

|

Less: provision for income taxes for entities

|

||||||||

|

other than Duff & Phelps Corporation(a)(b)

|

(560 | ) | (920 | ) | ||||

|

Income before income taxes, as adjusted

|

8,995 | 10,298 | ||||||

|

Ownership percentage of noncontrolling interest(d)

|

26.4 | % | 32.0 | % | ||||

|

Net income attributable to noncontrolling interest

|

2,378 | 3,295 | ||||||

|

Income before income taxes, as adjusted, attributable

|

||||||||

|

to Duff & Phelps Corporation

|

6,617 | 7,003 | ||||||

|

Less: provision for income taxes of Duff & Phelps

|

||||||||

|

Corporation(a)(c)

|

(2,504 | ) | (2,730 | ) | ||||

|

Net income attributable to Duff & Phelps Corporation

|

$ | 4,113 | $ | 4,273 | ||||

|

(a)

|

The consolidated provision for income taxes is equal to the sum of (i) the provision for income taxes for entities other than Duff & Phelps Corporation and (ii) the provision for income taxes of Duff & Phelps Corporation. The consolidated provision for income taxes totaled $3,064 and $3,650 for the three months ended March 31, 2011 and 2010, respectively.

|

|

(b)

|

The provision for income taxes for entities other than Duff & Phelps Corporation represents taxes imposed directly on Duff & Phelps, LLC, a wholly-owned subsidiary of D&P Acquisitions, and its subsidiaries, such as taxes imposed on certain domestic subsidiaries (e.g., Rash & Associates, L.P.), taxes imposed by certain foreign jurisdictions, and taxes imposed by certain local and other jurisdictions (e.g., New York City). Since Duff & Phelps, LLC is taxed as a partnership and a flow-through entity for U.S. federal and state income tax purposes, there is no provision for these taxes on income allocable to the noncontrolling interest.

|

|

(c)

|

The provision of income taxes of Duff & Phelps Corporation includes all U.S. federal and state income taxes.

|

|

(d)

|

Income before income taxes, as adjusted, is allocated to the noncontrolling interest based on the total New Class A Units vested for income tax purposes (“Tax-Vested Units”) owned by the noncontrolling interest as a percentage of the aggregate amount of all Tax-Vested Units. This percentage may not necessarily correspond to the total number of New Class A Units at the end of each respective period.

|

- 7 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Distributions and Other Payments to Noncontrolling Unitholders

The following table summarizes distributions and other payments to noncontrolling unitholders, as described more fully below:

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Distributions for taxes

|

$ | 266 | $ | 608 | ||||

|

Other distributions

|

1,120 | 735 | ||||||

|

Payments pursuant to the Tax Receivable Agreement

|

— | — | ||||||

| $ | 1,386 | $ | 1,343 | |||||

Distributions for taxes

As a limited liability company, D&P Acquisitions does not incur significant federal or state and local taxes, as these taxes are primarily the obligations of the members of D&P Acquisitions. As authorized by the Third Amended and Restated LLC Agreement of D&P Acquisitions, D&P Acquisitions is required to distribute cash, generally, on a pro rata basis, to its members to the extent necessary to provide funds to pay the members' tax liabilities, if any, with respect to the earnings of D&P Acquisitions. The tax distribution rate has been set at 45% of each member’s allocable share of taxable income of D&P Acquisitions. D&P Acquisitions is only required to make such distributions if cash is available for such purposes as determined by the Company. The Company expects cash will be available to make these distributions. Upon completion of its tax returns with respect to the prior year, D&P Acquisitions may make true-up distributions to its members, if cash is available for such purposes, with respect to actual taxable income for the prior year.

Other distributions

Concurrent with the payment of dividends to shareholders of Class A common stock, holders of New Class A Units receive a corresponding distribution per vested unit. These amounts will be treated as a reduction in basis of each member’s ownership interests. Pursuant to the terms of the Third Amended and Restated LLC Agreement of D&P Acquisitions, a corresponding amount per unvested unit was deposited into a segregated account and will be distributed once a year with respect to units that vested during that year. Any amounts related to unvested units that forfeit are returned to the Company.

- 8 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Payments pursuant to the Tax Receivable Agreement

As a result of the Company’s acquisition of New Class A Units of D&P Acquisitions, the Company expects to benefit from depreciation and other tax deductions reflecting D&P Acquisitions' tax basis for its assets. Those deductions will be allocated to the Company and will be taken into account in reporting the Company’s taxable income. Further, as a result of a federal income tax election made by D&P Acquisitions applicable to a portion of the Company’s acquisition of New Class A Units of D&P Acquisitions, the income tax basis of the assets of D&P Acquisitions underlying a portion of the units the Company has and will acquire (pursuant to the exchange agreement) will be adjusted based upon the amount that the Company has paid for that portion of its New Class A Units of D&P Acquisitions.

The Company has entered into a tax receivable agreement (“TRA”) with the existing unitholders of D&P Acquisitions (for the benefit of the existing unitholders of D&P Acquisitions) that provides for the payment by the Company to the unitholders of D&P Acquisitions of 85% of the amount of cash savings, if any, in U.S. federal, state and local income tax that the Company realizes (i) from the tax basis in its proportionate share of D&P Acquisitions' goodwill and similar intangible assets that the Company receives as a result of the exchanges and (ii) from the federal income tax election referred to above. D&P Acquisitions expects to make future payments under the TRA to the extent cash is available for such purposes.

As of March 31, 2011, the Company recorded a liability of $109,891, representing the payments due to D&P Acquisitions’ unitholders under the TRA (see current and non-current portion of “Due to noncontrolling unitholders” on the Company’s Condensed Consolidated Balance Sheets).

Within the next 12 month period, the Company expects to pay $5,640 of the total amount. The basis for determining the current portion of the payments due to D&P Acquisitions’ unitholders under the TRA is the expected amount of payments to be made within the next 12 months. The long-term portion of the payments due to D&P Acquisitions’ unitholders under the tax receivable agreement is the remainder. Payments are anticipated to be made annually over 15 years, commencing from the date of each event that gives rise to the TRA benefits, beginning with the date of the closing of the IPO on October 3, 2007. The payments are made in accordance with the terms of the TRA. The timing of the payments is subject to certain contingencies including Duff & Phelps Corporation having sufficient taxable income to utilize all of the tax benefits defined in the TRA.

To determine the current amount of the payments due to D&P Acquisitions’ unitholders under the TRA, the Company estimated the amount of taxable income that Duff & Phelps Corporation has generated over the previous fiscal year. Next, the Company estimated the amount of the specified TRA deductions at year end. This was used as a basis for determining the amount of tax reduction that generates a TRA obligation. In turn, this was used to calculate the estimated payments due under the TRA that the Company expects to pay in the next 12 months. These calculations are performed pursuant to the terms of the TRA.

Obligations pursuant to the TRA are obligations of Duff & Phelps Corporation. They do not impact the noncontrolling interest. These obligations are not income tax obligations and have no impact on the tax provision or the allocation of taxes. Furthermore, the TRA has no impact on the allocation of the provision for income taxes to the Company’s net income. In general, items of income and expense are allocated on the basis of member’s ownership interests pursuant to the Third Amended and Restated Limited Liability Company Agreement of Duff & Phelps Acquisitions, LLC.

- 9 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Note 4 - EARNINGS PER SHARE

Basic earnings per share (“EPS”) measures the performance of an entity over the reporting period. Diluted earnings per share measures the performance of an entity over the reporting period while giving effect to all potentially dilutive common shares that were outstanding during the period. The treasury stock method is used to determine the dilutive potential of stock options, restricted stock awards and units, performance-vesting restricted stock awards and units, and New Class A Units and Class B common stock that are exchangeable into the Company’s Class A common stock.

In accordance with FASB ASC 260, Earnings Per Share, all outstanding unvested share-based payments that contain rights to nonforfeitable dividends participate in the undistributed earnings with the common stockholders and are therefore participating securities. Companies with participating securities are required to apply the two-class method in calculating basic and diluted net income per share.

The Company’s restricted stock awards are considered participating securities as they receive nonforfeitable dividends at the same rate as the Company’s Class A common stock. The computation of basic and diluted net income per share is reduced for a presumed hypothetical distribution of earnings to the holders of the Company’s unvested restricted stock. Accordingly, the effect of the allocation reduces earnings available for common stockholders.

The Company’s performance-vesting restricted stock awards are not considered participating securities as the related dividends are forfeitable to the extent the performance conditions are not met.

The following is a reconciliation of the numerator and denominator used in the basic and diluted EPS calculations:

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Basic and diluted net income per share:

|

||||||||

|

Numerator

|

||||||||

|

Net income available to holders of Class A common stock

|

$ | 4,113 | $ | 4,273 | ||||

|

Earnings allocated to participating securities

|

(193 | ) | (269 | ) | ||||

|

Earnings available for common stockholders

|

$ | 3,920 | $ | 4,004 | ||||

|

Denominator for basic net income per share of Class A common stock

|

||||||||

|

Weighted average shares of Class A common stock

|

26,910 | 24,986 | ||||||

|

Denominator for diluted net income per share of Class A common stock

|

||||||||

|

Weighted average shares of Class A common stock

|

26,910 | 24,986 | ||||||

|

Add dilutive effect of the following:

|

||||||||

|

Restricted stock awards and units

|

705 | 794 | ||||||

|

Dilutive weighted average shares of Class A common stock

|

27,615 | 25,780 | ||||||

|

Basic income per share of Class A common stock

|

$ | 0.15 | $ | 0.16 | ||||

|

Diluted income per share of Class A common stock

|

$ | 0.14 | $ | 0.16 | ||||

- 10 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Anti-dilution is the result of (i) the allocation of income or loss associated with the exchange of New Class A Units for Class A common stock and (ii) outstanding options exceeding those outstanding under the treasury stock method. Accordingly, the following shares were anti-dilutive and excluded from this calculation:

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Weighted average New Class A Units outstanding

|

11,130 | 12,966 | ||||||

|

Weighted average IPO Options outstanding

|

1,650 | 1,812 | ||||||

The potential dilutive effect of the Company’s performance-vesting restricted stock awards and units were excluded from the calculation as the performance conditions had not been met as of the period ended March 31, 2011.

In addition, shares of Class B common stock do not share in the earnings of the Company and are therefore not participating securities. Accordingly, basic and diluted earnings per share of Class B common stock have not been presented.

- 11 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Note 5 - EQUITY-BASED COMPENSATION

For a detailed description of past equity-based compensation activity, please refer to the Company’s Annual Report on Form 10-K for the year ended December 31, 2010. There have been no significant changes in the Company’s equity-based compensation accounting policies and assumptions from those that were disclosed in the Company’s Annual Report on Form 10-K for the year ended December 31, 2010.

Equity-based compensation with respect to (a) grants of Legacy Units, (b) options to purchase shares of the Company’s Class A common stock granted in connection with the IPO (“IPO Options”) and (c) restricted stock awards and units and performance-vesting restricted stock awards and units issued in connection with the Company’s ongoing long-term compensation program (“Ongoing RSAs”) is detailed in the table below:

|

Three Months Ended

|

Three Months Ended

|

|||||||||||||||||||||||

|

March 31, 2011

|

March 31, 2010

|

|||||||||||||||||||||||

|

Client

|

Client

|

|||||||||||||||||||||||

|

Service

|

SG&A

|

Total

|

Service

|

SG&A

|

Total

|

|||||||||||||||||||

|

Legacy Units

|

$ | 95 | $ | 130 | $ | 225 | $ | 265 | $ | 332 | $ | 597 | ||||||||||||

|

IPO Options

|

138 | 54 | 192 | 333 | 153 | 486 | ||||||||||||||||||

|

Ongoing RSAs

|

4,784 | 1,339 | 6,123 | 3,119 | 968 | 4,087 | ||||||||||||||||||

|

Total

|

$ | 5,017 | $ | 1,523 | $ | 6,540 | $ | 3,717 | $ | 1,453 | $ | 5,170 | ||||||||||||

Legacy Units

The following table summarizes activity for New Class A Units attributable to equity-based compensation during the three months ended March 31, 2011:

|

New

|

||||

|

Class A Units

|

||||

|

Attributable to

|

||||

|

Equity-Based

|

||||

|

Compensation

|

||||

|

Balance as of December 31, 2010

|

1,530 | |||

|

Redeemed or exchanged

|

(77 | ) | ||

|

Forfeited

|

(1 | ) | ||

|

Balance as of March 31, 2011

|

1,452 | |||

|

Vested

|

1,324 | |||

|

Unvested

|

128 | |||

- 12 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

IPO Options

The following table summarizes option activity during the three months ended March 31, 2011:

|

Weighted

|

||||||||

|

Average

|

||||||||

|

IPO

|

Grant Date

|

|||||||

|

Options

|

Fair Value

|

|||||||

|

Balance as of December 31, 2010

|

1,661 | $ | 7.33 | |||||

|

Exercised

|

(7 | ) | 7.33 | |||||

|

Forfeited

|

(10 | ) | 7.33 | |||||

|

Balance as of March 31, 2011

|

1,644 | $ | 7.33 | |||||

|

Vested

|

1,258 | |||||||

|

Unvested

|

386 | |||||||

|

Weighted average exercise price

|

$ | 16.00 | ||||||

|

Weighted average remaining contractual term

|

6.50 | |||||||

|

Total intrinsic value of exercised options

|

$ | 9 | ||||||

|

Total fair value of vested options

|

$ | 9,222 | ||||||

|

Aggregate intrinsic value of outstanding options

|

$ | — | ||||||

|

Options expected to vest

|

1,629 | |||||||

|

Aggregate intrinsic value of options expected to vest

|

$ | — | ||||||

Restricted Stock

Restricted stock awards and restricted stock units are granted as a form of incentive compensation and are accounted for similarly. Corresponding expense is recognized based on the fair market value of the Company’s Class A common stock on the date of grant over the service period. Restricted stock units are generally contingent on continued employment and are converted to common stock when restrictions on transfer lapse after three years.

Performance-vesting restricted stock awards and units are granted as a form of incentive compensation and accounted for similarly. Performance-vesting restricted stock awards and units will become non-forfeitable on the third anniversary of the date of grant if and to the extent certain targets of total shareholder return are attained. Expense for performance-vesting restricted stock awards and units is recognized based on their calculated fair market value as of the date of grant using a lattice model. They are expensed over a three year period from the date of grant.

During the three months ended March 31, 2011, the Company issued 1,656 Ongoing RSAs related to annual bonus incentive compensation, performance incentive initiatives, promotions and recruiting efforts. The restrictions on transfer and forfeiture provisions are generally eliminated after three years for all awards granted to non-executives with certain exceptions related to retiree eligible employees and termination of employees without cause. Of the 1,656 Ongoing RSAs granted, 205 awards are performance-vesting restricted stock awards or units and are subject to the vesting provisions described previously.

Of the 1,656 Ongoing RSAs granted, 140 restricted stock awards and 130 performance stock awards were granted to executives on March 2, 2011 and March 11, 2011, respectively. For grants made to executives, the restrictions on transfer and forfeiture provisions on 65 of the restricted stock awards are eliminated annually over three years based on ratable vesting and the restrictions on 75 of the restricted stock awards lapse after three years.

- 13 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

The following table summarizes award activity:

|

Weighted

|

Weighted

|

|||||||||||||||

|

Restricted

|

Average

|

Restricted

|

Average

|

|||||||||||||

|

Stock

|

Grant Date

|

Stock

|

Grant Date

|

|||||||||||||

|

Awards

|

Fair Value

|

Units

|

Fair Value

|

|||||||||||||

|

Balance as of December 31, 2010

|

3,432 | $ | 15.13 | 303 | $ | 15.03 | ||||||||||

|

Granted

|

1,356 | 15.69 | 95 | 15.71 | ||||||||||||

|

Converted to Class A common stock upon

|

||||||||||||||||

|

lapse of restrictions

|

(821 | ) | 13.07 | (44 | ) | 11.73 | ||||||||||

|

Forfeited

|

(75 | ) | 17.00 | (1 | ) | 16.66 | ||||||||||

|

Balance as of March 31, 2011

|

3,892 | $ | 15.72 | 353 | $ | 15.62 | ||||||||||

|

Vested

|

— | — | ||||||||||||||

|

Unvested

|

3,892 | 353 | ||||||||||||||

|

Performance-

|

Performance-

|

|||||||||||||||

|

Vesting

|

Weighted

|

Vesting

|

Weighted

|

|||||||||||||

|

Restricted

|

Average

|

Restricted

|

Average

|

|||||||||||||

|

Stock

|

Grant Date

|

Stock

|

Grant Date

|

|||||||||||||

|

Awards

|

Fair Value

|

Units

|

Fair Value

|

|||||||||||||

|

Balance as of December 31, 2010

|

— | $ | — | — | $ | — | ||||||||||

|

Granted

|

183 | 7.52 | 22 | 7.83 | ||||||||||||

|

Converted to Class A common stock upon

|

||||||||||||||||

|

lapse of restrictions

|

— | — | — | — | ||||||||||||

|

Forfeited

|

— | — | — | — | ||||||||||||

|

Balance as of March 31, 2011

|

183 | $ | 7.52 | 22 | $ | 7.83 | ||||||||||

|

Vested

|

— | — | ||||||||||||||

|

Unvested

|

183 | 22 | ||||||||||||||

For all equity-based compensation awards, forfeitures are estimated at the time an award is granted and revised, if necessary, in subsequent periods if actual forfeitures differ from those estimates. Pre-vesting forfeitures were estimated to be between 2% and 21% as of March 31, 2011 based on historical experience and future expectations.

The total unamortized compensation cost related to all non-vested awards was $36,595 at March 31, 2011. A tax benefit of $4,612 and $229 was recognized for the stock options issued in conjunction with the IPO and Ongoing RSAs for the three months ended March 31, 2011 and 2010, respectively.

- 14 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Note 6 - FAIR VALUE MEASUREMENTS

The following table presents assets and liabilities measured at fair value on a recurring basis as of March 31, 2011:

|

Quoted Prices

|

||||||||||||||||

|

in Active

|

Significant

|

|||||||||||||||

|

Markets for

|

Other

|

Significant

|

||||||||||||||

|

Identical

|

Observable

|

Unobservable

|

||||||||||||||

|

Assets

|

Inputs

|

Inputs

|

||||||||||||||

|

Description

|

(Level 1)

|

(Level 2)

|

(Level 3)

|

Total

|

||||||||||||

|

Investments held in conjunction with

|

||||||||||||||||

|

deferred compensation plan(1)

|

$ | — | $ | 25,339 | $ | — | $ | 25,339 | ||||||||

|

Total assets

|

$ | — | $ | 25,339 | $ | — | $ | 25,339 | ||||||||

|

Benefits payable in conjunction with

|

||||||||||||||||

|

deferred compensation plan(1)

|

$ | — | $ | 25,483 | $ | — | $ | 25,483 | ||||||||

|

Total liabilities

|

$ | — | $ | 25,483 | $ | — | $ | 25,483 | ||||||||

For comparative purposes, the following table presents assets and liabilities measured at fair value on a recurring basis as of December 31, 2010:

|

Quoted Prices

|

||||||||||||||||

|

in Active

|

Significant

|

|||||||||||||||

|

Markets for

|

Other

|

Significant

|

||||||||||||||

|

Identical

|

Observable

|

Unobservable

|

||||||||||||||

|

Assets

|

Inputs

|

Inputs

|

||||||||||||||

|

Description

|

(Level 1)

|

(Level 2)

|

(Level 3)

|

Total

|

||||||||||||

|

Investments held in conjunction with

|

||||||||||||||||

|

deferred compensation plan(1)

|

$ | — | $ | 23,151 | $ | — | $ | 23,151 | ||||||||

|

Total assets

|

$ | — | $ | 23,151 | $ | — | $ | 23,151 | ||||||||

|

Benefits payable in conjunction with

|

||||||||||||||||

|

deferred compensation plan(1)

|

$ | — | $ | 23,078 | $ | — | $ | 23,078 | ||||||||

|

Total liabilities

|

$ | — | $ | 23,078 | $ | — | $ | 23,078 | ||||||||

|

(1)

|

The investments held and benefits payable to participants in conjunction with the deferred compensation plan were primarily based on quoted prices for similar assets in active markets. Changes in the fair value of the investments are recognized as an increase or decrease in compensation expense. Changes in the fair value of the benefits payables to participants are recognized as a corresponding offset to compensation expense. The net impact of changes in fair value is not material. The deferred compensation plan is further discussed in Note 9.

|

The Company does not have any material financial assets in a market that is not active.

- 15 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Note 7 - LONG-TERM DEBT

On July 15, 2009, Duff & Phelps, LLC entered into a credit agreement with Bank of America, N.A., as administrative agent and the lenders from time to time party thereto ("Credit Agreement"), providing for a $30,000 senior secured revolving credit facility (“Credit Facility”), including a $10,000 sub-limit for the issuance of letters of credit. The proceeds of the facility are permitted to be used for working capital, permitted acquisitions and general corporate purposes. The maturity date is July 15, 2012 and amounts borrowed may be voluntarily prepaid at any time without penalty or premium, subject to customary breakage costs.

There were no amounts outstanding under the Credit Facility at March 31, 2011 or through the filing date of this Quarterly Report on Form 10-Q. As of March 31, 2011, the Company had $4,134 of outstanding letters of credit of which $3,685 were issued against the Credit Facility. These letters of credit were issued in connection with real estate leases.

Loans under the Credit Facility will, at the Company's option, bear interest on the principal amount outstanding at either (a) a rate equal to LIBOR, plus an applicable margin or (b) a base rate, plus an applicable margin. The applicable margin rate will be based on the Company's most recent consolidated leverage ratio and ranges from 1.75% to 2.50% per annum depending on the Company's consolidated leverage ratio. In addition, the Company is required to pay an unused commitment fee on the actual daily amount of the unutilized portion of the commitments of the lenders at a rate ranging from 0.25% to 0.50% per annum, based on the Company's most recent consolidated leverage ratio. Based on the Company’s consolidated leverage ratio at March 31, 2011, the Company qualifies for the 1.75% applicable margin and 0.25% unused commitment fee.

The Credit Agreement contains customary representations and warranties and customary affirmative and negative covenants, including, among others, limitations on (a) the incurrence of liens, (b) the incurrence of indebtedness, (c) the ability to make dividends and distributions, as well as redeem and repurchase equity interests, and (d) acquisitions, mergers, consolidations and sales of assets. In addition, the Credit Agreement contains financial covenants that do not permit (a) a total leverage ratio of greater than 2.75 to 1.00 until the quarter ending September 30, 2010, and 2.50 to 1.00 thereafter and (b) a consolidated fixed charge coverage ratio of less than 2.00 to 1.00 until September 30, 2010, and 1.25 to 1.00 thereafter. The financial covenants are tested on the last day of each fiscal quarter based on the last four fiscal quarter periods. Management believes that the Company was in compliance with all of its covenants as of March 31, 2011. The Credit Agreement permits dividend payments or other distributions in the Company’s common stock or other equity interests subject to certain limitations.

The obligation of the Company to pay amounts outstanding under the Credit Facility may be accelerated upon the occurrence of an "Event of Default" as defined in the Credit Agreement. The Company's obligations under the Credit Agreement are guaranteed by D&P Acquisitions, and certain domestic subsidiaries of the Company (collectively, the "Guarantors"). The Credit Agreement is secured by a lien on substantially all of the personal property of the Company and each of the Guarantors.

- 16 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Note 8 - INCOME TAXES

The Company’s effective tax rate is summarized in the following table:

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Provision for income taxes

|

$ | 3,064 | $ | 3,650 | ||||

|

Effective income tax rate

|

32.1 | % | 32.5 | % | ||||

The tax provision for the current year period is based on our estimate of the Company’s annualized income tax rate. The effective tax rate is calculated by dividing the provision for income taxes by income before income taxes.

The Company's effective tax rate includes a rate benefit attributable to the fact that the Company’s subsidiaries operate as a series of limited liability companies and other flow-through entities which are not subject to federal income tax. Accordingly, a portion of the Company's earnings are not subject to corporate level taxes. This favorable impact is partially offset by the impact of certain permanent items, primarily attributable to certain compensation related expenses that are not deductible for tax purposes.

The Company accounts for uncertainties in income tax positions in accordance with FASB ASC 740, Income Taxes. A reconciliation of the beginning and ending amount of unrecognized tax benefit is summarized as follows:

|

Balance as of December 31, 2010

|

$ | 535 | ||

|

Additional based on tax positions related to the current year

|

26 | |||

|

Additional based on tax positions related to prior years

|

14 | |||

|

Balance as of March 31, 2011

|

$ | 575 |

The Company recognizes interest income and expense related to income taxes as a component of interest expense and penalties as a component of selling, general and administrative expenses.

The Company and its subsidiaries file income tax returns in the U.S. federal jurisdiction and various states and foreign jurisdictions. Duff & Phelps, LLC and D&P Acquisitions are open for federal income tax purposes from 2007 forward. These entities are not subject to federal income taxes as they are flow-through entities. The Company is open for federal income tax purposes beginning in 2007.

With respect to state and local jurisdictions and countries outside of the United States, the Company and its subsidiaries are typically subject to examination for four to five years after the income tax returns have been filed. Although the outcome of tax audits is always uncertain, the Company believes that adequate amounts of tax, interest and penalties have been provided for in the accompanying consolidated financial statements for any adjustments that might be incurred due to state, local or foreign audits.

- 17 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Note 9 - DEFERRED COMPENSATION PLAN

The Company maintains the Duff & Phelps Deferred Compensation Plan (“Deferred Compensation Plan”) for key employees. This plan is detailed further in our Annual Report on Form 10-K for the year ended December 31, 2010.

Under the terms of the plan, the Company established a “rabbi trust” as a vehicle for accumulating assets to pay benefits under the plan. Payments under the plan may be paid from the general assets of the Company or from the assets of any such rabbi trust. Payment from any such source reduces the obligation owed to the participant or beneficiary. The rabbi trust invests in an investment vehicle structured as a corporate-owned life insurance (“COLI”) policy with a cash surrender value that mirrors the payable to the participants of the plan and tracks the value of the plan assets. Participants can earn a return on their deferred compensation that is based on hypothetical investment funds. The policy is redeemable on demand in an amount equal to the cash surrender value. The cash surrender value approximates fair value.

The following table summarizes the fair market value of the rabbi trust and the corresponding liability owed to participants:

|

March 31,

|

December 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Fair market value of investments in rabbi trust

|

$ | 25,339 | $ | 23,151 | ||||

|

Payable to participants of the plan

|

25,483 | 23,078 | ||||||

The fair market value of the investments in the rabbi trust is included in “Investments related to the deferred compensation plan” with the corresponding deferred compensation obligation included in current and non-current portion of liability related to the deferred compensation plan on the Consolidated Balance Sheets. Changes in the fair value of the investments are recognized as compensation expense (or credit). Changes in the fair value of the benefits payables to participants are recognized as a corresponding offset to compensation expense (or credit). The net impact of changes in fair value is not material.

Note 10 - COMMITMENTS AND CONTINGENCIES

The Company is involved in various claims or disputes arising in the normal course of business. Management does not believe that these matters would have a material adverse effect on the Company's financial position, results of operations or liquidity.

- 18 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

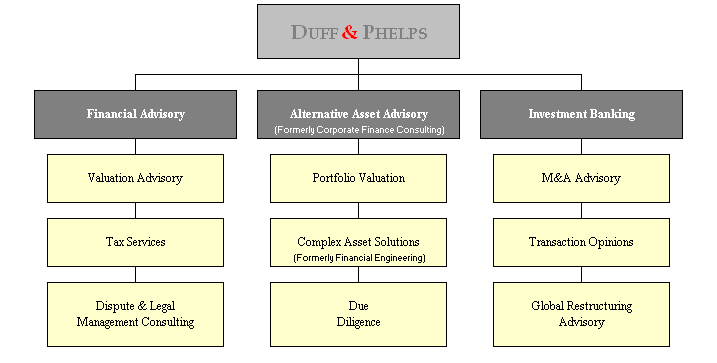

Note 11 - SEGMENT INFORMATION

The Company provides services through three segments: Financial Advisory, Alternative Asset Advisory (formerly Corporate Finance Consulting) and Investment Banking. Effective January 1, 2011, the Company renamed its Corporate Finance Consulting segment Alternative Asset Advisory to more appropriately define the services offered by this segment. In addition, our Alternative Asset Advisory segment previously included services associated with Strategic Value Advisory. This service line was primarily integrated into Financial Advisory. As a result, prior period results have been restated to reflect this change.

The Financial Advisory segment provides services associated with valuation advisory, tax, and dispute and legal management consulting. The Alternative Asset Advisory segment provides services related to portfolio valuation, complex asset solutions (i.e., financial engineering) and due diligence. The Investment Banking segment provides merger and acquisition advisory services, transaction opinions and restructuring advisory services.

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Financial Advisory

|

||||||||

|

Revenue (excluding reimbursables)

|

$ | 58,597 | $ | 57,040 | ||||

|

Segment operating income

|

$ | 9,582 | $ | 7,706 | ||||

|

Segment operating income margin

|

16.4 | % | 13.5 | % | ||||

|

Alternative Asset Advisory

|

||||||||

|

Revenue (excluding reimbursables)

|

$ | 13,485 | $ | 11,778 | ||||

|

Segment operating income

|

$ | 3,222 | $ | 2,814 | ||||

|

Segment operating income margin

|

23.9 | % | 23.9 | % | ||||

|

Investment Banking

|

||||||||

|

Revenue (excluding reimbursables)

|

$ | 12,964 | $ | 20,346 | ||||

|

Segment operating income

|

$ | — | $ | 5,057 | ||||

|

Segment operating income margin

|

0.0 | % | 24.9 | % | ||||

|

Total

|

||||||||

|

Revenue (excluding reimbursables)

|

$ | 85,046 | $ | 89,164 | ||||

|

Segment operating income

|

$ | 12,804 | $ | 15,577 | ||||

|

Net client reimbursable expenses

|

(45 | ) | (56 | ) | ||||

|

Equity-based compensation associated with Legacy Units and IPO options

|

(417 | ) | (1,083 | ) | ||||

|

Depreciation and amortization

|

(2,489 | ) | (2,493 | ) | ||||

|

Acquisition retention expenses

|

(82 | ) | — | |||||

|

Merger and acquisition costs

|

(194 | ) | — | |||||

|

Charge from impairment of certain intangible assets

|

— | (674 | ) | |||||

|

Operating income

|

$ | 9,577 | $ | 11,271 | ||||

- 19 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Revenue attributable to geographic area is summarized as follows:

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

North America

|

$ | 77,217 | $ | 77,071 | ||||

|

Europe

|

6,804 | 11,208 | ||||||

|

Asia

|

1,025 | 885 | ||||||

|

Revenue (excluding reimbursables)

|

$ | 85,046 | $ | 89,164 | ||||

There was no intersegment revenue during the periods presented. The Company does not maintain separate balance sheet information by segment.

For segment reporting purposes, management uses certain estimates and assumptions to allocate revenue and expenses. Revenue and expenses attributable to reportable segments are generally based on which segment and product line a client service professional is a dedicated member. As a result, revenue recognized that relate to the cross utilization of client service professionals across reportable segments occur each period depending on the expertise required for each engagement. In the three months ended March 31, 2011 and 2010, the Financial Advisory segment (primarily Valuation Advisory services) recognized revenue of $3,288 and $3,543 from the cross utilization of its client service professionals on engagements from the Alternative Asset Advisory segment (primarily Portfolio Valuation services), respectively.

- 20 -

DUFF & PHELPS CORPORATION AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

(Unaudited)

Note 12 - RELATED PARTY TRANSACTIONS

Lovell Minnick Partners

Entities affiliated with Lovell Minnick Partners are holders of Class B common stock and an equivalent number of New Class A Units. Two managing directors of Lovell Minnick Partners serve as independent directors on the Company’s Board of Directors.

D&P Acquisitions made distributions to entities affiliated with Lovell Minnick Partners as summarized in the following table:

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Distributions for taxes

|

$ | 44 | $ | 59 | ||||

|

Other distributions

|

289 | 181 | ||||||

| $ | 333 | $ | 240 | |||||

Distributions for taxes and other distributions are further described in Note 3.

Vestar Capital Partners

Entities affiliated with Vestar Capital Partners are holders of Class B common stock and an equivalent number of New Class A Units. A managing director of Vestar Capital Partners serves as independent directors on the Company’s Board of Directors.

D&P Acquisitions made distributions to entities affiliated with Vestar Capital Partners as summarized in the following table:

|

Three Months Ended

|

||||||||

|

March 31,

|

March 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Distributions for taxes

|

$ | 57 | $ | 74 | ||||

|

Other distributions

|

402 | 251 | ||||||

| $ | 459 | $ | 325 | |||||

Distributions for taxes and other distributions are further described in Note 3.

Note 13 - SUBSEQUENT EVENTS

Declaration of Quarterly Dividend

On April 27, 2011, the Company announced that its board of directors had declared a quarterly dividend of $0.08 per share on its outstanding Class A common stock. The dividend is payable on May 27, 2011 to shareholders of record on May 17, 2011. Concurrent with the payment of the dividend, the Company will also be distributing $0.08 per unit to holders of New Class A Units.

- 21 -

|

Item 2.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations.

|

Disclosure Regarding Forward-Looking Statements

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), which reflect the Company’s current views with respect to, among other things, future events and financial performance. The Company generally identifies forward looking statements by terminology such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “could,” “should,” “seeks,” “approximately,” “predicts,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of those words or other comparable words. Any forward-looking statements contained in this discussion are based upon our historical performance and on our current plans, estimates and expectations. The inclusion of this forward-looking information should not be regarded as a representation by us, or any other person that the future plans, estimates or expectations contemplated by us will be achieved. Such forward-looking statements are subject to various risks and uncertainties and assumptions relating to our operations, financial results, financial condition, business prospects, growth strategy and liquidity. If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may vary materially from those indicated in these statements. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements and the risk factors section that are included in our Annual Report on Form 10-K for the year ended December 31, 2010 and any subsequent filings of our Quarterly Reports on Form 10-Q. The forward-looking statements included in this Quarterly Report on Form 10-Q are made only as of the date of this filing with the Securities and Exchange Commission. The Company does not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

Critical Accounting Policies and Estimates