Attached files

| file | filename |

|---|---|

| EX-23.2 - Teucrium Commodity Trust | v219519_ex23-2.htm |

As filed with the Securities and Exchange Commission on April 26, 2011

Registration No. 333-167590

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 2

to

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

Teucrium Commodity Trust

(Registrant)

Delaware

(State or other jurisdiction of incorporation or organization)

6799

(Primary Standard Industrial Classification Code Number)

27-6715889

(I.R.S. Employer Identification No.)

c/o Teucrium Trading, LLC

232 Hidden Lake Road

Building A

Brattleboro, Vermont 05301

Phone: (802) 257-1617

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Sal Gilbertie

President

Teucrium Trading, LLC

232 Hidden Lake Road

Building A

Brattleboro, Vermont 05301

Phone: (802) 257-1617

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copy to:

W. Thomas Conner, Esq.

Sutherland Asbill & Brennan LLP

1275 Pennsylvania Avenue, N.W.

Washington, DC 20004

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

|

Non-accelerated filer o

(Do not check if a smaller reporting company)

|

Smaller reporting company x

|

CALCULATION OF REGISTRATION FEE

|

Title of Securities

to be Registered

|

Amount

to be

Registered

|

Proposed

Maximum

Offering Price

Per Share*

|

Proposed

Maximum

Aggregate

Offering Price*

|

Amount of

Registration

Fee

|

||||||||||||

|

Common units of Teucrium Soybean Fund, a series of the Registrant

|

10,000,000 | $ | 25.00 | $ | 250,000,000 | $ | 29,025.00** | |||||||||

|

*

|

Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(d) under the Securities Act of 1933.

|

|

**

|

Previously paid.

|

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and the Sponsor and the Trust are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

|

Preliminary Prospectus

|

Subject to Completion April ___, 2011

|

Teucrium Soybean Fund

10,000,000 Shares

Teucrium Soybean Fund (the “Fund”) is a commodity pool that is a series of Teucrium Commodity Trust (“Trust”), a Delaware statutory trust. The Fund will issue common units representing fractional undivided beneficial interests in such Fund, called “Shares.” The Fund intends to continuously offer creation baskets consisting of 50,000 Shares at their net asset value (“NAV”) to “Authorized Purchasers” (as defined below) through Foreside Fund Services, LLC, which is the marketing agent for Shares of the Fund (the “Marketing Agent”). Authorized Purchasers, in turn, may offer to the public Shares of any baskets they create. Authorized Purchasers will sell such Shares, which will be listed on the NYSE Arca exchange (“NYSE Arca”), to the public at per-Share offering prices that are expected to reflect, among other factors, the trading price of the Shares on the NYSE Arca, the NAV of the Fund at the time the Authorized Purchaser purchased the Creation Baskets and the NAV at the time of the offer of the Shares to the public, the supply of and demand for Shares at the time of sale, and the liquidity of the markets for soybean interests. The prices of Shares offered by Authorized Purchasers are expected to fall between the Fund’s NAV and the trading price of the Shares on the NYSE Arca at the time of sale. The Fund’s Shares may trade in the secondary market at prices that are lower or higher than their NAV per Share. Fund Shares will be listed on the NYSE Arca under the symbol “SOYB.”

The investment objective of the Fund is to have the daily changes in percentage terms of the Fund’s NAV per Share reflect the daily changes in percentage terms of a weighted average of the closing settlement prices for three soybean futures contracts. The Fund’s sponsor is Teucrium Trading, LLC (the “Sponsor”).

This is a best efforts offering; the Marketing Agent is not required to sell any specific number or dollar amount of Shares, but will use its best efforts to sell Shares. An Authorized Purchaser is under no obligation to purchase Shares. This is intended to be a continuous offering that will terminate on _________, 2013 (two years from the date of this prospectus), unless suspended or terminated at any earlier time for certain reasons specified in this prospectus or unless extended as permitted under the rules under the Securities Act of 1933. See “Prospectus Summary – The Shares” and “Creation and Redemption of Shares – Rejection of Purchase Orders” below.

Investing in the Fund involves significant risks. See “What Are the Risk Factors Involved with an Investment in the Fund?” beginning on page [ ]. The Fund is not a mutual fund registered under the Investment Company Act of 1940 and is not subject to regulation under such Act.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION (“SEC”) NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THE SECURITIES OFFERED IN THIS PROSPECTUS, OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS COMMODITY POOL NOR HAS THE COMMISSION PASSED ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

This prospectus is in two parts: a disclosure document and a statement of additional information. These parts are bound together, and both contain important information.

|

Per share

|

Per Basket

|

|||||||

|

Price of the Shares*

|

$ | 25.00 | $ | 1,250,000 | ||||

* Based on closing net asset value on [date]. The price may vary based on net asset value in effect on a particular day.

COMMODITY FUTURES TRADING COMMISSION

RISK DISCLOSURE STATEMENT

YOU SHOULD CAREFULLY CONSIDER WHETHER YOUR FINANCIAL CONDITION PERMITS YOU TO PARTICIPATE IN A COMMODITY POOL. IN SO DOING, YOU SHOULD BE AWARE THAT COMMODITY INTEREST TRADING CAN QUICKLY LEAD TO LARGE LOSSES AS WELL AS GAINS. SUCH TRADING LOSSES CAN SHARPLY REDUCE THE NET ASSET VALUE OF THE POOL AND CONSEQUENTLY THE VALUE OF YOUR INTEREST IN THE POOL. IN ADDITION, RESTRICTIONS ON REDEMPTIONS MAY AFFECT YOUR ABILITY TO WITHDRAW YOUR PARTICIPATION IN THE POOL.

FURTHER, COMMODITY POOLS MAY BE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT, AND ADVISORY AND BROKERAGE FEES. IT MAY BE NECESSARY FOR THOSE POOLS THAT ARE SUBJECT TO THESE CHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR ASSETS. THIS DISCLOSURE DOCUMENT CONTAINS A COMPLETE DESCRIPTION OF EACH EXPENSE TO BE CHARGED THIS POOL BEGINNING AT PAGE [ ] AND A STATEMENT OF THE PERCENTAGE RETURN NECESSARY TO BREAK EVEN, THAT IS, TO RECOVER THE AMOUNT OF YOUR INITIAL INVESTMENT, AT PAGE [ ].

THIS BRIEF STATEMENT CANNOT DISCLOSE ALL THE RISKS AND OTHER FACTORS NECESSARY TO EVALUATE YOUR PARTICIPATION IN THIS COMMODITY POOL. THEREFORE, BEFORE YOU DECIDE TO PARTICIPATE IN THIS COMMODITY POOL, YOU SHOULD CAREFULLY STUDY THIS DISCLOSURE DOCUMENT, INCLUDING A DESCRIPTION OF THE PRINCIPAL RISK FACTORS OF THIS INVESTMENT, AT PAGE [ ].

YOU SHOULD ALSO BE AWARE THAT THIS COMMODITY POOL MAY TRADE FOREIGN FUTURES OR OPTIONS CONTRACTS. TRANSACTIONS ON MARKETS LOCATED OUTSIDE THE UNITED STATES, INCLUDING MARKETS FORMALLY LINKED TO A UNITED STATES MARKET, MAY BE SUBJECT TO REGULATIONS WHICH OFFER DIFFERENT OR DIMINISHED PROTECTION TO THE POOL AND ITS PARTICIPANTS. FURTHER, UNITED STATES REGULATORY AUTHORITIES MAY BE UNABLE TO COMPEL THE ENFORCEMENT OF THE RULES OF REGULATORY AUTHORITIES OR MARKETS IN NON-UNITED STATES JURISDICTIONS WHERE TRANSACTIONS FOR THE POOL MAY BE EFFECTED.

THIS POOL HAS NOT COMMENCED TRADING AND DOES NOT HAVE ANY PERFORMANCE HISTORY.

TEUCRIUM SOYBEAN FUND

TABLE OF CONTENTS

|

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

|

iii

|

|

|

PROSPECTUS SUMMARY

|

1

|

|

|

Principal Offices of the Fund and the Sponsor

|

1

|

|

|

Breakeven Point

|

1

|

|

|

Overview of the Fund

|

1

|

|

|

The Shares

|

4

|

|

|

The Fund’s Investments in Soybean Interests

|

5

|

|

|

Principal Investment Risks of an Investment in the Fund

|

6

|

|

|

Principal Offices of the Fund and the Sponsor

|

8

|

|

|

Financial Condition of the Fund

|

8

|

|

|

Defined Terms

|

8

|

|

|

Breakeven Analysis

|

8

|

|

|

The Offering

|

10

|

|

|

WHAT ARE THE RISK FACTORS INVOLVED WITH AN INVESTMENT IN THE FUND?

|

14

|

|

|

Risks Associated With Investing Directly or Indirectly in Soybean

|

14

|

|

|

The Fund’s Operating Risks

|

19

|

|

|

Risk of Leverage and Volatility

|

26

|

|

|

Over-the-Counter Contract Risk

|

27

|

|

|

Risk of Trading in International Markets

|

28

|

|

|

Tax Risk

|

28

|

|

|

THE OFFERING

|

29

|

|

|

The Fund in General

|

29

|

|

|

The Sponsor

|

30

|

|

|

The Trustee

|

35

|

|

|

Operation of the Fund

|

36

|

|

|

Futures Contracts

|

40

|

|

|

Cleared Soybean Swaps

|

43

|

|

|

Over-the-Counter Derivatives

|

43

|

|

|

Benchmark Performance

|

44

|

|

|

The Soybean Market

|

44

|

|

|

The Fund’s Investments in Treasury Securities, Cash and Cash Equivalents

|

45

|

|

|

Other Trading Policies of the Fund

|

45

|

|

|

The Service Providers

|

46

|

|

|

Fees to be Paid by the Fund

|

48

|

|

|

Form of Shares

|

48

|

|

|

Transfer of Shares

|

49

|

|

|

Inter-Series Limitation on Liability

|

49

|

|

|

Plan of Distribution

|

50

|

|

|

The Flow of Shares

|

52

|

|

|

Calculating NAV

|

52

|

|

|

Creation and Redemption of Shares

|

53

|

|

|

Secondary Market Transactions

|

57

|

|

|

Use of Proceeds

|

57

|

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

58

|

|

|

The Trust Agreement

|

61

|

|

|

The Sponsor Has Conflicts of Interest

|

64

|

|

|

Interests of Named Experts and Counsel

|

65

|

|

|

Provisions of Federal and State Securities Laws

|

65

|

|

|

Books and Records

|

66

|

|

|

Analysis of Critical Accounting Policies

|

66

|

|

|

Statements, Filings, and Reports to Shareholders

|

66

|

|

|

Fiscal Year

|

67

|

i

|

Governing Law; Consent to Delaware Jurisdiction

|

67

|

|

|

Legal Matters

|

67

|

|

|

Privacy Policy

|

67

|

|

|

U.S. Federal Income Tax Considerations

|

68

|

|

|

Investment By ERISA Accounts

|

77

|

|

|

INFORMATION YOU SHOULD KNOW

|

79

|

|

|

WHERE YOU CAN FIND MORE INFORMATION

|

80

|

|

|

TEUCRIUM TRADING, LLC — INDEX TO FINANCIAL STATEMENTS

|

81

|

|

|

Appendix A Glossary of Defined Terms

|

|

117

|

Until [date] (25 days after the date of this prospectus), all dealers effecting transactions in the offered Shares, whether or not participating in this distribution, may be required to deliver a prospectus. This requirement is in addition to the obligations of dealers to deliver a prospectus when acting as underwriters and with respect to unsold allotments or subscriptions.

ii

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus includes “forward-looking statements” which generally relate to future events or future performance. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential” or the negative of these terms or other comparable terminology. All statements (other than statements of historical fact) included in this prospectus that address activities, events or developments that will or may occur in the future, including such matters as movements in the commodities markets and indexes that track such movements, the Fund’s operations, the Sponsor’s plans and references to the Fund’s future success and other similar matters, are forward-looking statements. These statements are only predictions. Actual events or results may differ materially. These statements are based upon certain assumptions and analyses the Sponsor has made based on its perception of historical trends, current conditions and expected future developments, as well as other factors appropriate in the circumstances. Whether or not actual results and developments will conform to the Sponsor’s expectations and predictions, however, is subject to a number of risks and uncertainties, including the special considerations discussed in this prospectus, general economic, market and business conditions, changes in laws or regulations, including those concerning taxes, made by governmental authorities or regulatory bodies, and other world economic and political developments. See “What Are the Risk Factors Involved with an Investment in the Fund?” Consequently, all the forward-looking statements made in this prospectus are qualified by these cautionary statements, and there can be no assurance that actual results or developments the Sponsor anticipates will be realized or, even if substantially realized, that they will result in the expected consequences to, or have the expected effects on, the Fund’s operations or the value of its Shares.

iii

PROSPECTUS SUMMARY

This is only a summary of the prospectus and, while it contains material information about the Fund and its Shares, it does not contain or summarize all of the information about the Fund and the Shares contained in this prospectus that is material and/or which may be important to you. You should read this entire prospectus, including “What Are the Risk Factors Involved with an Investment in the Fund?” beginning on page [ ], before making an investment decision about the Shares. In addition, this prospectus includes a statement of additional information that follows and is bound together with the primary disclosure document. Both the primary disclosure document and the statement of additional information contain important information.

Principal Offices of the Fund and the Sponsor

The principal office of the Trust and the Fund is located at 232 Hidden Lake Road, Building A, Brattleboro, Vermont 05301. The telephone number is (802) 257-1617. The Sponsor’s principal office is also located at 232 Hidden Lake Road, Building A, Brattleboro, Vermont 05301, and its telephone number is also (802) 257-1617.

Breakeven Point

The amount of trading income required for the redemption value of a Share at the end of one year to equal the initial selling price of the Share, assuming an initial selling price of $25.00, is $0.39 or 1.53% of the initial selling price. For more information, see “Breakeven Analysis” below.

Overview of the Fund

Teucrium Soybean Fund (the “Fund” or “Us” or “We”), is a commodity pool that will issue Shares that may be purchased and sold on the NYSE Arca. The Fund is a series of the Teucrium Commodity Trust (“Trust”), a Delaware statutory trust organized on September 11, 2009. The Fund is one of seven series of the Trust; each series operates as a separate commodity pool. Additional series of the Trust may be created in the future. The Trust and the Fund operate pursuant to the Trust’s Amended and Restated Declaration of Trust and Trust Agreement (the “Trust Agreement”). The Fund was formed and is managed and controlled by the Sponsor, Teucrium Trading, LLC. The Sponsor is a limited liability company formed in Delaware on July 28, 2009 that is registered as a commodity pool operator (“CPO”) with the Commodity Futures Trading Commission (“CFTC”) and is a member of the National Futures Association (“NFA”). The Sponsor first intends to use this prospectus on or about _____, 2011, the date of this prospectus.

The investment objective of the Fund is to have the daily changes in percentage terms of the Shares’ net asset value (“NAV”) reflect the daily changes in percentage terms of a weighted average of the closing settlement prices for three futures contracts for soybeans (“Soybean Futures Contracts”) that are traded on the Chicago Board of Trade (“CBOT”). Except as described in the following paragraph, the three Soybean Futures Contracts will be: (1) second-to-expire CBOT Soybean Futures Contract, weighted 35%, (2) the third-to-expire CBOT Soybean Futures Contract, weighted 30%, and (3) the CBOT Soybean Futures Contract expiring in the November following the expiration month of the third-to-expire contract, weighted 35%. (The weighted average of the three Soybean Futures Contracts is referred to herein as the “Benchmark,” and the three Soybean Futures Contracts that at any given time make up the Benchmark are referred to herein as the “Benchmark Component Futures Contracts.”)

Soybean Futures Contracts traded on the CBOT expire on a specified day in seven different months: January, March, May, July, August, September and November. However, there is generally a less liquid market for the Soybean Futures Contracts expiring in August (the “August Contract”) and September (the “September Contract” and, together with the August Contract, the “Excluded Contracts”), and the Sponsor has determined not to incorporate the Excluded Contracts into the Benchmark calculation. Accordingly, during the period when the Excluded Contracts are the second-to-expire and third-to-expire Soybean Futures Contract, the fourth-to-expire and fifth-to-expire Soybean Futures Contracts will take the place of the second-to-expire and third-to-expire Soybean Futures Contracts, respectively, as Benchmark Component Futures Contracts. Similarly, when the August Contract is the third-to-expire Soybean Futures Contract, the fifth-to-expire Soybean Futures Contract will take the place of the August Contract as a Benchmark Component Futures Contract, and when the September Contract is the second-to-expire Soybean Futures Contract, the third-to-expire and fourth-to-expire Soybean Futures Contracts will be Benchmark Component Futures Contracts.

The Fund seeks to achieve its investment objective by investing under normal market conditions in Benchmark Component Futures Contracts or, in certain circumstances, in other Soybean Futures Contracts traded on the CBOT or on foreign exchanges. In addition, and to a limited extent, the Fund also may invest in exchange-traded options on Soybean Futures Contracts and in soybean-based swap agreements that are cleared through the CBOT or its affiliated provider of clearing services (“Cleared Soybean Swaps”) in furtherance of the Fund's investment objective. Once position limits in Soybean Futures Contracts are applicable, the Fund's intention is to invest first in Cleared Soybean Swaps to the extent practicable under the position limits applicable to Cleared Soybean Swaps and appropriate in light of the liquidity in the Cleared Soybean Swap market, and then in contracts and instruments such as cash-settled options on Soybean Futures Contracts and forward contracts, swaps other than Cleared Soybean Swaps, and other over-the-counter transactions that are based on the price of soybean and Soybean Futures Contracts (collectively, “Other Soybean Interests,” and together with Soybean Futures Contracts and Cleared Soybean Swaps, “Soybean Interests”). See “The Offering – Futures Contracts” below. By utilizing certain or all of these investments, the Sponsor will endeavor to cause the Fund's performance to closely track that of the Benchmark. The Sponsor expects to manage the Fund’s investments directly, although it has been authorized by the Trust to retain, establish the terms of retention for, and terminate third-party commodity trading advisors to provide such management. The Sponsor is also authorized to select futures commission merchants to execute the Fund’s transactions in Soybean Futures Contracts.

The Fund seeks to achieve its investment objective primarily by investing in Soybean Interests such that daily changes in the Fund’s NAV will be expected to closely track the changes in the Benchmark. The Fund’s positions in Soybean Interests will be changed or “rolled” on a regular basis in order to track the changing nature of the Benchmark. For example, five times a year (on the dates on which certain Soybean Futures Contracts expire), a particular Soybean Futures Contract will no longer be a Benchmark Component Futures Contract, and the Fund’s investments will have to be changed accordingly. In order that the Fund’s trading does not cause unwanted market movements and to make it more difficult for third parties to profit by trading based on such expected market movements, the Fund’s investments typically will not be rolled entirely on that day, but rather will typically be rolled over a period of several days.

The following chart identifies the specific Soybean Futures Contracts that will be used in the calculation of the Benchmark at any point in a given year, based on the same 35%/30%/35% weighting methodology described above.

|

Period

|

Benchmark Component Futures Contracts

|

|

|

From expiration of January Year 0 contract until expiration of March Year 0 contract

|

May Year 0, July Year 0 and November Year 0

|

|

|

From expiration of March Year 0 contract until expiration of May Year 0 contract

|

July Year 0, November Year 0 and November Year 1

|

|

|

From expiration of May Year 0 contract until expiration of September Year 0 contract

|

November Year 0, January Year 1 and November Year 1

|

|

|

From expiration of September Year 0 contract until expiration of November Year 0 contract

|

January Year 1, March Year 1 and November Year 1

|

|

|

From expiration of November Year 0 contract until expiration of January Year 1 contract

|

|

March Year 1, May Year 1 and November Year 1

|

Consistent with achieving the Fund’s investment objective of closely tracking the Benchmark, the Sponsor may for certain reasons cause the Fund to enter into or hold Soybean Futures Contracts other than the Benchmark Component Futures Contracts, Cleared Soybean Swaps and/or Other Soybean Interests. For example, certain Cleared Soybean Swaps have standardized terms similar to, and are priced by reference to, a corresponding Benchmark Component Futures Contract. Additionally, Other Soybean Interests that do not have standardized terms and are not exchange-traded, referred to as “over-the-counter” Soybean Interests, can generally be structured as the parties to the Soybean Interest contract desire. Therefore, the Fund might enter into multiple Cleared Soybean Swaps and/or over-the-counter Soybean Interests intended to exactly replicate the performance of each of the three Benchmark Component Futures Contracts, or a single over-the-counter Soybean Interest designed to replicate the performance of the Benchmark as a whole. Assuming that there is no default by a counterparty to an over-the-counter Soybean Interest, the performance of the Soybean Interest will necessarily correlate exactly with the performance of the Benchmark or the applicable Benchmark Component Futures Contract. The Fund’s might also enter into or hold Soybean Interests other than Benchmark Component Futures Contracts to facilitate effective trading, consistent with the discussion of the Fund’s “roll” strategy in the preceding paragraph. In addition, the Fund might enter into or hold Soybean Interests that would be expected to alleviate overall deviation between the Fund’s performance and that of the Benchmark that may result from certain market and trading inefficiencies or other reasons. By utilizing certain or all of the investments described above, the Sponsor will endeavor to cause the Fund’s performance to closely track that of the Benchmark.

2

The Fund invests in Soybean Interests to the fullest extent possible without being leveraged or unable to satisfy its expected current or potential margin or collateral obligations with respect to its investments in Soybean Interests. After fulfilling such margin and collateral requirements, the Fund will invest the remainder of its proceeds from the sale of baskets in obligations of the United States government (“Treasury Securities”) or cash equivalents, and/or merely hold such assets in cash (generally in interest-bearing accounts). Therefore, the focus of the Sponsor in managing the Fund is investing in Soybean Interests and in Treasury Securities, cash and/or cash equivalents. The Fund will earn interest income from the Treasury Securities and/or cash equivalents that it purchases and on the cash it holds through the Fund’s custodian, the Bank of New York Mellon (the “Custodian”).

The Sponsor endeavors to place the Fund’s trades in Soybean Interests and otherwise manage the Fund’s investments so that the Fund’s average daily tracking error against the Benchmark will be less than 10 percent over any period of 30 trading days. More specifically, the Sponsor will endeavor to manage the Fund so that A will be within plus/minus 10 percent of B, where:

|

|

·

|

A is the average daily change in the Fund’s NAV for any period of 30 successive valuation days, i.e., any trading day as of which the Fund calculates its NAV, and

|

|

|

·

|

B is the average daily change in the Benchmark over the same period.

|

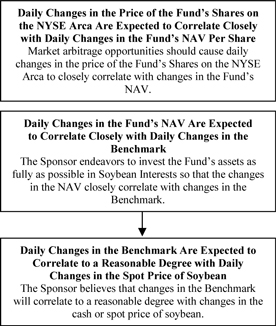

The Sponsor believes that market arbitrage opportunities will cause the Fund’s Share price on the NYSE Arca to closely track the Fund’s NAV per share. The Sponsor believes that the net effect of this expected relationship and the expected relationship described above between the Fund’s NAV and the Benchmark will be that the changes in the price of the Fund’s Shares on the NYSE Arca will closely track, in percentage terms, changes in the Benchmark.

The Sponsor employs a “neutral” investment strategy intended to track the changes in the Benchmark regardless of whether the Benchmark goes up or goes down. The Fund’s “neutral” investment strategy is designed to permit investors generally to purchase and sell the Fund’s Shares for the purpose of investing indirectly in the soybean market in a cost-effective manner. Such investors may include participants in the soybean industry and other industries seeking to hedge the risk of losses in their soybean-related transactions, as well as investors seeking exposure to the soybean market. Accordingly, depending on the investment objective of an individual investor, the risks generally associated with investing in the soybean market and/or the risks involved in hedging may exist. In addition, an investment in the Fund involves the risks that the changes in the price of the Fund’s Shares will not accurately track the changes in the Benchmark, and that changes in the Benchmark will not closely correlate with changes in the price of soybean on the spot market. Furthermore, as noted above, the Fund also invests in short-term Treasury Securities, cash and/or cash equivalents to meet its current or potential margin or collateral requirements with respect to its investments in Soybean Interests and to invest cash not required to be used as margin or collateral. The Fund does not expect there to be any meaningful correlation between the performance of the Fund’s investments in Treasury Securities/cash/cash equivalents and the changes in the price of soybean or Soybean Interests. While the level of interest earned on or the market price of these investments may in some respects correlate to changes in the price of soybean, this correlation is not anticipated as part of the Fund’s efforts to meet its objective. This and certain risk factors discussed in this prospectus may cause a lack of correlation between changes in the Fund’s NAV and changes in the price of soybean. The Sponsor does not intend to operate the Fund in a fashion such that its per share NAV will equal, in dollar terms, the spot price of a bushel or other unit of soybean or the price of any particular Soybean Futures Contract.

3

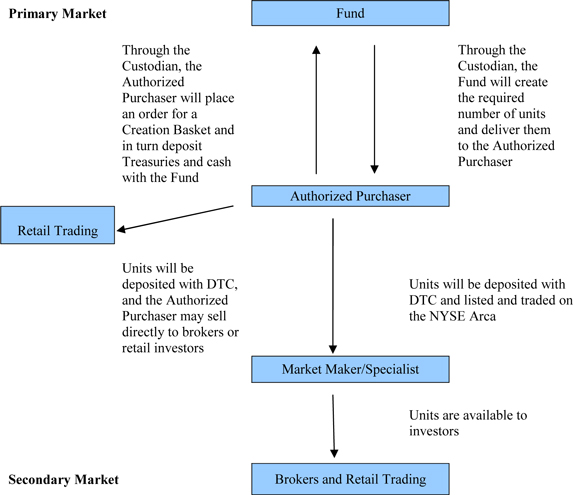

The Fund creates and redeems Shares only in blocks called Creation Baskets and Redemption Baskets, respectively. Only Authorized Purchasers may purchase or redeem Creation Baskets or Redemption Baskets. An Authorized Purchaser is under no obligation to create or redeem baskets, and an Authorized Purchaser is under no obligation to offer to the public Shares of any baskets it does create. Baskets are generally created when there is a demand for Shares, including, but not limited to, when the market price per share is at (or perceived to be at) a premium to the NAV per share. Similarly, baskets are generally redeemed when the market price per share is at (or perceived to be at) a discount to the NAV per share. Retail investors seeking to purchase or sell Shares on any day are expected to effect such transactions in the secondary market, on the NYSE Arca, at the market price per share, rather than in connection with the creation or redemption of baskets.

The Fund will commence making the investments described in this prospectus as quickly as practicable (no more than three business days) after the initial Creation Basket is sold. All proceeds from the sale of subsequent Creation Baskets will also be invested as quickly as practicable in such investments. The Fund’s cash and investments are held through the Fund’s Custodian, in accounts with the Fund’s commodity futures brokers or in collateral accounts with respect to over-the-counter Soybean Interests. There is no stated maximum time period for the Fund’s operations and the Fund will continue until all Shares are redeemed or the Fund is liquidated pursuant to the terms of the Trust Agreement.

There is no specified limit on the maximum amount of Creation Baskets that can be sold. At some point, however, applicable position limits on Soybean Futures Contracts, Cleared Soybean Swaps or Other Soybean Interests may practically limit the number of Creation Baskets that will be sold if the Sponsor determines that the other investment alternatives available to the Fund at that time will not enable it to meet its stated investment objective.

Shares may also be purchased and sold by individuals and entities that are not Authorized Purchasers in smaller increments than Creation Baskets on the NYSE Arca. However, these transactions are effected at bid and ask prices established by specialist firm(s). Like any listed security, Shares of the Fund can be purchased and sold at any time a secondary market is open.

In managing the Fund’s assets, the Sponsor does not use a technical trading system that automatically issues buy and sell orders. Instead, each time one or more baskets are purchased or redeemed, the Sponsor will purchase or sell Soybean Interests with an aggregate market value that approximates the amount of cash received or paid upon the purchase or redemption of the basket(s).

Note to Secondary Market Investors: The Shares can be directly purchased from or redeemed by the Fund only in Creation Baskets or Redemption Baskets, respectively, and only by Authorized Purchasers. Each Creation Basket and Redemption Basket consists of 50,000 Shares and therefore may require a commitment of over a million dollars (e.g., 50,000 Shares times an initial Share price of $25.00 equals $1.25 million). Accordingly, investors who do not have such resources or who are not Authorized Purchasers should be aware that some of the information contained in this prospectus, including information about purchases and redemptions of Shares directly with the Fund, is only relevant to Authorized Purchasers. Shares will be listed and traded on the NYSE Arca under the ticker symbol “SOYB” and may be purchased and sold as individual Shares. Individuals interested in purchasing Shares in the secondary market should contact their broker. Shares purchased or sold through a broker may be subject to commissions.

Except when aggregated in Redemption Baskets, Shares are not redeemable securities. There is no guarantee that Shares will trade at prices that are at or near the per-Share NAV.

The Shares

The Shares are registered as securities under the Securities Act of 1933 (“1933 Act”) and the Securities Exchange Act of 1934 (the “Exchange Act”) and do not provide dividend rights or conversion rights and there will not be sinking funds. The Shares may only be redeemed when aggregated in Redemption Baskets as discussed under “Creation and Redemption of Shares” and holders of Fund shares (“Shareholders”) generally will not have voting rights as discussed below under “The Trust Agreement – Voting Rights.” Cumulative voting is neither permitted nor required and there are no preemptive rights. The Trust Agreement provides that, upon liquidation of the Fund, its assets will be distributed pro rata to the Shareholders based upon the number of Shares held. Each Shareholder will receive its share of the assets in cash or in kind, and the proportion of such share that is received in cash may vary from Shareholder to Shareholder, as the Sponsor in its sole discretion may decide.

4

The offering of Shares under this prospectus is a continuous offering under Rule 415 of the 1933 Act and will terminate on _________, 2013 (two years from the date of this prospectus). The offering may be extended beyond such date as permitted under the rules under 1933 Act. The offering will terminate before such date or before the end of any extension period if all of the registered Shares have been sold. However, the Sponsor expects to cause the Trust to file one or more additional registration statements as necessary to permit additional Shares to be registered and offered on an uninterrupted basis. This offering may also be suspended or terminated at any time for certain specified reasons, including if and when suitable investments for the Fund are not available or practicable. See “Creation and Redemption of Shares – Rejection of Purchase Orders” below. As discussed above, the minimum purchase requirement for Authorized Purchasers is a Creation Basket, which consists of 50,000 Shares. Under the plan of distribution, the Fund does not require a minimum purchase amount for investors who purchase Shares from Authorized Purchasers. There are no arrangements to place funds in an escrow, trust, or similar account.

The Fund’s Investments in Soybean Interests

A brief description of the principal types of Soybean Interests in which the Fund may invest is set forth below.

|

|

·

|

A futures contract is an exchange-traded contract traded with standard terms that calls for the delivery of a specified quantity of a commodity at a specified price, on a specified date and at a specified location.

|

|

|

·

|

A swap agreement is a bilateral contract to exchange a periodic stream of payments determined by reference to a notional amount, with payment typically made between the parties on a net basis. For instance, in the case of soybean swap, the Fund may be obligated to pay a fixed price per bushel of soybeans and be entitled to receive an amount per bushel equal to the current value of an index of soybean prices, the price of a specified Soybean Futures Contract, or the average price of a group of Soybean Futures Contracts such as the Benchmark. The Fund expects to invest primarily in Cleared Soybean Swaps, rather than over-the-counter soybean swaps.

|

The Fund may also invest to a lesser extent in the following types of Soybean Interests:

|

|

·

|

Swap agreements other than Cleared Soybean Swaps (i.e., over-the-counter soybean swaps).

|

|

|

·

|

A forward contract is an over-the-counter bilateral contract for the purchase of sale of a specified quantity of a commodity at a specified price, on a specified date and at a specified location.

|

|

|

·

|

An option on a futures contract, forward contract or a commodity on the spot market gives the buyer of the option the right, but not the obligation, to buy or sell a futures contract, forward contract or commodity, as applicable, at a specified price on or before a specified date. The seller, or writer, of the option is obligated to take a position in the underlying interest at a specified price opposite to the option buyer if the option is exercised. Options on futures contracts, like the future contracts to which they relate, are standardized contracts traded on an exchange, while options on forward contracts and commodities generally are individually negotiated, over-the-counter, bilateral contracts.

|

Unlike exchange-traded contracts, over-the-counter contracts expose the Fund to the credit risk of the other party to the contract. (As discussed below, exchange-traded contracts may expose the Fund to the risk of the clearing broker’s and/or the exchange clearing house(s)’ bankruptcy.) The Sponsor does not currently intend to purchase and sell soybeans in the “spot market” for the Fund. Spot market transactions are cash transactions in which the buyer and seller agree to the immediate purchase and sale of a commodity, usually with a two-day settlement period. In addition, the Sponsor does not currently intend that the Fund will enter into or hold spot month Soybean Futures Contracts, except that spot month contracts that were formerly second-to-expire contracts may be held for a brief period until they can be disposed of in accordance with the Fund’s roll strategy.

5

A more detailed description of Soybean Interests and other aspects of the soybean and Soybean Interest markets can be found later in this prospectus.

As noted, the Fund invests in Soybean Futures Contracts, including those traded on the CBOT, and in Cleared Soybean Swaps cleared through CBOT affiliates. The Fund expressly disclaims any association with the CBOT or endorsement of the Fund by such exchanges and acknowledges that “CBOT” and “Chicago Board of Trade” are registered trademarks of such exchanges.

Principal Investment Risks of an Investment in the Fund

An investment in the Fund involves a degree of risk. Some of the risks you may face are summarized below. A more extensive discussion of these risks appears beginning on page [ ].

|

|

·

|

Unlike mutual funds, commodity pools and other investment pools that manage their investments so as to realize income and gains for distribution to their investors, the Fund generally will not distribute dividends to Shareholders. You should not invest in the Fund if you will need cash distributions from the Fund to pay taxes on your share of income and gains of the Fund, if any, or for other purposes.

|

|

|

·

|

Investors may choose to use the Fund as a means of investing indirectly in soybeans, and there are risks involved in such investments. The risks and hazards that are inherent in soybean production may cause the price of soybean to fluctuate widely. Global price movements for soybean are influenced by, among other things: weather conditions, crop failure, production decisions, governmental policies, changing demand, the soybean harvest cycle, and various economic and monetary events. Soybean production is also subject to domestic and foreign regulations that materially affect operations.

|

|

|

·

|

To the extent that investors use the Fund as a means of investing indirectly in soybeans, there is the risk that the changes in the price of the Fund’s Shares on the NYSE Arca will not closely track the changes in spot price of soybeans. This could happen if the price of Shares traded on the NYSE Arca does not correlate closely with the Fund’s NAV; the changes in the Fund’s NAV do not correlate closely with changes in the Benchmark; or the changes in the Benchmark do not correlate closely with changes in the cash or spot price of soybeans. This is a risk because if these correlations are not sufficiently close, then investors may not be able to use the Fund as a cost-effective way to invest indirectly in soybeans or as a hedge against the risk of loss in soybean-related transactions.

|

|

|

·

|

The Sponsor has limited experience operating commodity pools. Although the Sponsor currently sponsors seven commodity pools (the Teucrium Funds), only three have commenced operations. Prior to June 9, 2010, the Sponsor had never operated a commodity pool.

|

|

|

·

|

The Fund has no operating history, so there is no performance history to serve as a basis for you to evaluate an investment in the Trust.

|

|

|

·

|

The price relationship between the near month Soybean Futures Contract to expire and the Benchmark Component Futures Contracts will vary and may impact both the Fund’s total return over time and the degree to which such total return tracks the total return of soybean price indices. In cases in which the near month contract’s price is lower than later-expiring contracts’ prices (a situation known as “contango” in the futures markets), then absent the impact of the overall movement in soybean prices the value of the Benchmark Component Futures Contracts would tend to decline as they approach expiration. In cases in which the near month contract’s price is higher than later-expiring contracts’ prices (a situation known as “backwardation” in the futures markets), then absent the impact of the overall movement in soybean prices the value of the Benchmark Component Futures Contracts would tend to rise as they approach expiration.

|

6

|

|

·

|

Investors, including those who directly participate in the soybean market, may choose to use the Fund as a vehicle to hedge against the risk of loss and there are risks involved in hedging activities. While hedging can provide protection against an adverse movement in market prices, it can also preclude a hedger’s opportunity to benefit from a favorable market movement.

|

|

|

·

|

The Fund seeks to have the changes in its Shares’ NAV in percentage terms track changes in the Benchmark in percentage terms, rather than profit from speculative trading of Soybean Interests. The Sponsor therefore endeavors to manage the Fund so that the Fund’s assets are, unlike those of many other commodity pools, not leveraged (i.e., so that the aggregate value of the Fund’s unrealized losses from its investments in Soybean Interests at any time will not exceed the value of the Fund’s assets). There is no assurance that the Sponsor will successfully implement this investment strategy. If the Sponsor permits the Fund to become leveraged, you could lose all or substantially all of your investment if the Fund’s trading positions suddenly turn unprofitable. These movements in price may be the result of factors outside of the Sponsor’s control and may not be anticipated by the Sponsor.

|

|

|

·

|

The Fund may invest in Other Soybean Interests. To the extent that these Other Soybean Interests are contracts individually negotiated between their parties, they may not be as liquid as Soybean Futures Contracts and will expose the Fund to credit risk that its counterparty may not be able to satisfy its obligations to the Fund.

|

|

|

·

|

The Fund invests primarily in Soybean Interests that are traded or sold in the United States. However, a portion of the Fund’s trades may take place in markets and on exchanges outside the United States. Some non-U.S. markets present risks because they are not subject to the same degree of regulation as their U.S. counterparts. In some of these non-U.S. markets, the performance on a contract is the responsibility of the counterparty and is not backed by an exchange or clearing corporation and therefore exposes the Fund to credit risk. Trading in non-U.S. markets also leaves the Fund susceptible to fluctuations in the value of the local currency against the U.S. dollar.

|

|

|

·

|

The structure and operation of the Fund may involve conflicts of interest. For example, a conflict may arise because the Sponsor and its principals and affiliates may trade for themselves. In addition, the Sponsor has sole current authority to manage the investments and operations, and the interests of the Sponsor may conflict with the Shareholders’ best interests.

|

|

|

·

|

You will have no rights to participate in the management of the Fund and will have to rely on the duties and judgment of the Sponsor to manage the Fund.

|

|

|

·

|

The Fund pays fees and expenses that are incurred regardless of whether it is profitable.

|

|

|

·

|

Regulation of the financial markets is extensive and dynamic. On July 21, 2010, “The Dodd-Frank Wall Street Reform and Consumer Protection Act” was signed into law. This new law contains broad changes to the financial services industry including provisions changing the regulation of commodity interests. Such changes include the requirement that position limits on most types of commodity futures contracts be established; new registration, recordkeeping, capital and margin requirements for “swap dealers” and “major swap participants”; the forced use of clearinghouse mechanisms for most over-the-counter transactions; and the aggregation, for purposes of position limits, of all positions relating to a particular commodity held by a single entity and its affiliates, whether such positions exist on U.S. futures exchanges, non-U.S. futures exchanges, or in over-the-counter contracts. The new law and the rules to be promulgated thereunder may negatively impact the Fund’s ability to meet its investment objective.

|

For additional risks, see “What Are the Risk Factors Involved with an Investment in the Fund?”

7

The principal office of the Trust and the Fund is located at 232 Hidden Lake Road, Building A, Brattleboro, Vermont 05301. The telephone number is (802) 257-1617. The Sponsor’s principal office is also located at 232 Hidden Lake Road, Building A, Brattleboro, Vermont 05301.

Financial Condition of the Fund

The Fund’s NAV is determined as of the earlier of the close of the New York Stock Exchange or 4:00 p.m. New York time on each day that the NYSE Arca is open for trading.

Defined Terms

For a glossary of defined terms, see Appendix A.

Breakeven Analysis

The breakeven analysis below indicates the approximate dollar returns and percentage returns required for the redemption value of a hypothetical $25.00 initial investment in a single Share to equal the amount invested twelve months after the investment was made. This breakeven analysis refers to the redemption of baskets by Authorized Purchasers and is not related to any gains an individual investor would have to achieve in order to break even. The breakeven analysis is an approximation only.

|

Assumed initial selling price per Share

|

$ | 25.00 | ||

|

Sponsor’s Fee (1.00%)(1)

|

$ | 0.25 | ||

|

Creation Basket Fee(2)

|

$ | 0.01 | ||

|

Estimated Brokerage Fees (0.02%)(3)

|

$ | 0.01 | ||

|

Other Fund Fees and Expenses(4)

|

$ | 0.15 | ||

|

Interest Income (0.13%)(5)

|

$ | (0.03 | ) | |

|

Amount of trading income (loss) required for the redemption value at the end of one year to equal the initial selling price of the Share

|

$ | 0.39 | ||

|

Percentage of initial selling price per share

|

1.53 | % |

(1) The Fund is obligated to pay the Sponsor a management fee at the annual rate of 1.00% of the Fund’s average daily net assets, payable monthly.

(2) Authorized Purchasers are required to pay a Creation Basket fee of $500 for each order they place to create one or more baskets. An order must be at least one basket, which is 50,000 Shares. This breakeven analysis assumes a hypothetical investment in a single Share so the Creation Basket fee is $.01 (500/50,000).

(3) The Fund determined this amount as follows. Assuming that the price of a Share is $25.00, the Fund would receive $1,250,000 upon the sale of a Creation Basket (50,000 Shares multiplied by $25.00). Assuming that this entire amount is invested in Soybean Futures Contracts and that there is no change in the settlement price of such contracts, the Fund would be required to purchase approximately 18 Soybean Futures Contracts to support the Creation Basket ($1,250,000 divided by $69,425, the value of the July 2011 Soybean Futures Contract as of February 15, 2010, which is used to approximate the price of the Benchmark Component Futures Contracts). In order to reflect changes in the Benchmark Component Futures Contracts, the Fund would have to replace one-third (approximately 6) of the contracts it holds with new contracts five times per year. Assuming further that futures commission merchants charge approximately $4.00 per Soybean Futures Contract for each purchase or sale, the annual futures commission merchant charge would be approximately $240.00 (12 total Soybean Futures Contract transactions (6 purchases and 6 sales) multiplied by five times per year multiplied by $4.00). As a percentage of the total investment of $1,250,000, this annual commission expense would be approximately 0.02%.

(4) Other Fund Fees and Expenses include legal, printing, accounting, custodial, administration, bookkeeping, transfer agency and marketing agent costs. The per-share cost of these fixed or estimated fees has been calculated assuming that the Fund has $30 million in assets and assuming certain fee reimbursements from the Sponsor. If a minimum assets of $2.5 million is used, Other Fund Fees and Expenses would equal $1.80 per share, and the amount of trading income required to break even would be $2.04 per share or 8.16%. If a maximum offering proceeds of $250 million is assumed, Other Fund Fees and Expenses would equal $0.09 per Share, and the amount of trading income required to break even would be $0.33 per share or 1.29%.

8

(5) The Fund earns interest on funds it deposits with the futures commission merchant and the Custodian and it estimates that the interest rate will be 0.13% based on the interest rate on three-month Treasury Bills as of February 15, 2011. The actual rate may vary.

9

The Offering

|

Offering

|

The Fund will offer Creation Baskets consisting of 50,000 Shares through the Marketing Agent to Authorized Purchasers. Authorized Purchasers may purchase Creation Baskets consisting of 50,000 Shares at the Fund’s NAV, which is expected to initially be $25.00. The initial Authorized Purchaser intends to offer the Shares of the initial Creation Basket(s) publicly. The initial Creation Basket is expected to be purchased by the initial Authorized Purchaser on the day the SEC declares the registration statement effective. The Shares are expected to begin trading on the NYSE Arca on the day following the purchase of the initial Creation Basket(s) by the initial Authorized Purchaser.

|

|

|

Use of Proceeds

|

The Sponsor will apply substantially all of the Fund’s assets toward investing in Soybean Interests, Treasury Securities, cash and/or cash equivalents. The Sponsor will deposit a portion of the Fund’s net assets with the futures commission merchant, Newedge USA, LLC, or other custodians to be used to meet its current or potential margin or collateral requirements in connection with its investment in Soybean Interests. The Fund will use only Treasury Securities, cash and/or cash equivalents to satisfy these requirements. The Sponsor expects that all entities that will hold or trade the Fund’s assets will be based in the United States and will be subject to United States regulations. The Sponsor believes that approximately 5% to 10% of the Fund’s assets will normally be committed as margin for Soybean Futures Contracts and collateral for Cleared Soybean Swaps and Other Soybean Interests. However, from time to time, the percentage of assets committed as margin/collateral may be substantially more, or less, than such range. The remaining portion of the Fund’s assets will be held in Treasury Securities, cash and/or cash equivalents by the Custodian. All interest income earned on these investments is retained for the Fund’s benefit.

|

|

|

NYSE Arca Symbol

|

“SOYB”

|

|

|

Creation and Redemption

|

Authorized Purchasers pay a $500 fee for each order to create one or more Creation Baskets, and a $500 fee per Redemption Basket redeemed. Authorized Purchasers are not required to sell any specific number or dollar amount of Shares. The per share price of Shares offered in Creation Baskets on any day after the effective date of the registration statement relating to this prospectus is the total NAV of the Fund calculated as of the close of the NYSE Arca on that day divided by the number of issued and outstanding Shares.

|

10

11

|

Fund Expenses

|

The Fund pays the Sponsor a management fee at an annual rate of 1.00% of the Fund’s average daily net assets. The Fund is also responsible for other ongoing fees, costs and expenses of its operations, including (i) brokerage and other fees and commissions incurred in connection with the trading activities of the Fund; (ii) expenses incurred in connection with registering additional Shares of the Fund or offering Shares of the Fund after the time any Shares have begun trading on NYSE Arca; (iii) the routine expenses associated with the preparation and, if required, the printing and mailing of monthly, quarterly, annual and other reports required by applicable U.S. federal and state regulatory authorities, Trust meetings and preparing, printing and mailing proxy statements to Shareholders; (iv) the payment of any distributions related to redemption of Shares; (v) payment for routine services of the Trustee, legal counsel and independent accountants; (vi) payment for routine accounting, bookkeeping, custody and transfer agency services, whether performed by an outside service provider or by Affiliates of the Sponsor; (vii) postage and insurance; (viii) costs and expenses associated with client relations and services; (ix) costs of preparation of all federal, state, local and foreign tax returns and any taxes payable on the income, assets or operations of the Fund; and (x) extraordinary expenses (including, but not limited to, legal claims and liabilities and litigation costs and any indemnification related thereto). The Sponsor will bear the costs and expenses related to the initial offer and sale of Shares, including registration fees paid or to be paid to the SEC, FINRA or any other regulatory body; none of the costs and expenses related to the initial offer and sale of Shares are chargeable to the Fund, and the Sponsor may not recover any of these costs and expenses from the Fund. Total fees to be paid by the Fund are currently estimated to be approximately 1.62% for the twelve-month period ending ______, 2012, though this amount may change in future years. The Sponsor may, in its discretion, pay or reimburse the Fund for, or waive a portion of its management fee to offset, expenses that would otherwise be borne by the Fund.

|

|

|

General expenses of the Trust will be allocated among the existing Funds and any future series of the Trust as determined by the Sponsor in its discretion. The Trust may be required to indemnify the Sponsor, and the Trust and/or the Sponsor may be required to indemnify the Trustee, Marketing Agent or Administrator, under certain circumstances.

|

12

|

The Trust and the Fund shall continue in existence from the date of their formation in perpetuity, unless the Trust or the Fund, as the case may be, is sooner terminated upon the occurrence of certain events specified in the Trust Agreement, including the following: (1) the filing of a certificate of dissolution or cancellation of the Sponsor or revocation of the Sponsor’s charter or the withdrawal of the Sponsor, unless shareholders holding a majority of the outstanding shares of the Trust elect within ninety (90) days after such event to continue the business of the Trust and appoint a successor Sponsor; (2) the occurrence of any event which would make the existence of the Trust or the Fund unlawful; (3) the suspension, revocation, or termination of the Sponsor’s registration as a CPO with the CFTC or membership with the NFA; (4) the insolvency or bankruptcy of the Trust or the Fund; (5) a vote by the shareholders holding at least seventy-five percent (75%) of the outstanding shares of the Trust to dissolve the Trust, subject to certain conditions; and (6) the determination by the Sponsor to dissolve the Trust or the Fund, subject to certain conditions. Upon termination of the Fund, the affairs of the Fund shall be wound up and all of its debts and liabilities discharged or otherwise provided for in the order of priority as provided by law. The fair market value of the remaining assets of the Fund shall then be determined by the Sponsor. Thereupon, the assets of the Fund shall be distributed pro rata to the Shareholders in accordance with their Shares.

|

||

|

Authorized Purchasers

|

|

We expect the initial Authorized Purchaser to be ________________, and we expect that there will be additional Authorized Purchasers in the future. A list of Authorized Purchasers will be available from the Marketing Agent. Authorized Purchasers must be (1) registered broker-dealers or other securities market participants, such as banks and other financial institutions, that are not required to register as broker-dealers to engage in securities transactions, and (2) DTC Participants. To become an Authorized Purchaser, a person must enter into an Authorized Purchaser Agreement with the Marketing Agent.

|

13

WHAT ARE THE RISK FACTORS INVOLVED WITH AN INVESTMENT IN THE FUND?

You should consider carefully the risks described below before making an investment decision. You should also refer to the other information included in this prospectus, which includes the Fund’s and the Sponsor’s financial statements and the related notes.

Risks Associated With Investing Directly or Indirectly in Soybeans

Investing in Soybean Interests subjects the Fund to the risks of the soybean market, and this could result in substantial fluctuations in the price of the Fund’s Shares.

The Fund is subject to the risks and hazards of the soybean market because it invests in Soybean Interests. The risks and hazards that are inherent in the soybean market may cause the price of soybeans to fluctuate widely. If the changes in percentage terms of the Fund’s Shares accurately track the percentage changes in the Benchmark or the spot price of soybeans, then the price of its Shares will fluctuate accordingly.

|

|

·

|

The price and availability of soybeans is influenced by economic and industry conditions, including but not limited to supply and demand factors such as: crop disease; weed control; water availability; various planting, growing, or harvesting problems; severe weather conditions such as drought, floods, heavy rains, frost, or natural disasters that are difficult to anticipate and which cannot be controlled; uncontrolled fires, including arson; challenges in doing business with foreign companies; legal and regulatory restrictions; transportation costs; interruptions in energy supply; currency exchange rate fluctuations; and political and economic instability. Additionally, demand for soybeans is affected by changes in international, national, regional and local economic conditions, and demographic trends. The increased production of soybean crops in South America and the rising demand for soybeans in emerging nations such as China and India have increased competition in the soybean market.

|

|

|

·

|

The supply of soybeans could be reduced by the spread of soybean rust. Soybean rust is a wind-borne fungal disease that attacks soybeans. Although soybean rust can be killed with chemicals, chemical treatment increases production costs for farmers.

|

|

|

·

|

Soybean production is subject to United States and foreign policies and regulations that materially affect operations. Governmental policies affecting the agricultural industry, such as taxes, tariffs, duties, subsidies, incentives, acreage control, and import and export restrictions on agricultural commodities and commodity products, can influence the planting of certain crops, the location and size of crop production, the volume and types of imports and exports, and industry profitability. Additionally, soybean production is affected by laws and regulations relating to, but not limited to, the sourcing, transporting, storing and processing of agricultural raw materials as well as the transporting, storing and distributing of related agricultural products. Soybean producers also may need to comply with various environmental laws and regulations, such as those regulating the use of certain pesticides. In addition, international trade disputes can adversely affect agricultural commodity trade flows by limiting or disrupting trade between countries or regions.

|

|

|

·

|

Because processing soybean oil can create trans-fats, the demand for soybean oil may decrease due to heightened governmental regulation of trans-fats or trans-fatty acids. The U.S. Food and Drug Administration currently requires food manufacturers to disclose levels of trans-fats contained in their products, and various local governments have enacted or are considering restrictions on the use of trans-fats in restaurants. Several food processors have either switched or indicated an intention to switch to oil products with lower levels of trans-fats or trans-fatty acids.

|

|

|

·

|

In recent years, there has been increased global interest in the production of biofuels as alternatives to traditional fossil fuels and as a means of promoting energy independence. Soybeans can be converted into biofuels such as biodiesel. Accordingly, the soybean market has become increasingly affected by demand for biofuels and related legislation.

|

14

|

|

·

|

The costs related to soybean production could increase and soybean supply could decrease as a result of restrictions on the use of genetically modified soybeans, including requirements to segregate genetically modified soybeans and the products generated from them from other soybean products.

|

|

|

·

|

Seasonal fluctuations in the price of soybeans may cause risk to an investor because of the possibility that Share prices will be depressed because of the soybean harvest cycle. In the futures market, fluctuations are typically reflected in contracts expiring in the harvest season (i.e., contracts expiring during the fall are typically priced lower than contracts expiring in the winter and spring). Thus, seasonal fluctuations could result in an investor incurring losses upon the sale of Fund Shares, particularly if the investor needs to sell Shares when the Benchmark Component Futures Contracts are, in whole or part, Soybean Futures Contracts expiring in the fall.

|

The Benchmark is not designed to correlate exactly with the spot price of soybeans and this could cause the changes in the price of the Shares to substantially vary from the changes in the spot price of soybeans. Therefore, you may not be able to effectively use the Fund to hedge against soybean-related losses or to indirectly invest in soybeans.

The Benchmark Component Futures Contracts reflect the price of soybeans for future delivery, not the current spot price of soybeans, so at best the correlation between changes in such Soybean Futures Contracts and the spot price of soybeans will be only approximate. Weak correlation between the Benchmark and the spot price of soybeans may result from the typical seasonal fluctuations in soybean prices discussed above. Imperfect correlation may also result from speculation in Soybean Interests, technical factors in the trading of Soybean Futures Contracts, and expected inflation in the economy as a whole. If there is a weak correlation between the Benchmark and the spot price of soybeans, then the price of Shares may not accurately track the spot price of soybeans and you may not be able to effectively use the Fund as a way to hedge the risk of losses in your soybean-related transactions or as a way to indirectly invest in soybeans.

Changes in the Fund’s NAV may not correlate well with changes in the price of the Benchmark. If this were to occur, you may not be able to effectively use the Fund as a way to hedge against soybean-related losses or as a way to indirectly invest in soybeans.

The Sponsor endeavors to invest the Fund’s assets as fully as possible in Soybean Interests so that the changes in percentage terms in the NAV closely correlate with the changes in percentage terms in the Benchmark. However, changes in the Fund’s NAV may not correlate with the changes in the Benchmark for various reasons, including those set forth below:

|

|

·

|

The Fund does not intend to invest only in the Benchmark Component Futures Contracts. While its investments in Soybean Futures Contracts other than the Benchmark Component Futures Contracts, Cleared Soybean Swaps and Other Soybean Interests would be for the purpose of causing the Fund’s performance to track that of the Benchmark most effectively and efficiently, the performance of these Soybean Interests may not correlate well with the performance of the Benchmark Component Futures Contracts, resulting in a greater potential for error in tracking price changes in those futures contracts. Additionally, if the trading market for Soybean Futures Contracts is suspended or closed, the Fund may not be able to purchase these investments at the last reported price for such investments.

|

|

|

·

|

The Fund will incur certain expenses in connection with its operations, and will hold most of its assets in income-producing, short-term securities for margin and other liquidity purposes and to meet redemptions that may be necessary on an ongoing basis. These expenses and income will cause imperfect correlation between changes in the Fund’s NAV and changes in the Benchmark.

|

15

|

|

The Sponsor may not be able to invest the Fund’s assets in Soybean Interests having an aggregate notional amount exactly equal to the Fund’s NAV. As a standardized contract, a single Soybean Futures Contracts or Cleared Soybean Swap is for a specified amount of soybean, and the Fund’s NAV and the proceeds from the sale of a Creation Basket is unlikely to be an exact multiple of that amount. In such case, the Fund could not invest the entire proceeds from the purchase of the Creation Basket in such futures contracts. (For example, assuming the Fund receives $1,250,000 for the sale of a Creation Basket and that the value (i.e., the notional amount) of a Soybean Futures Contract is $69,425, the Fund could only enter into 18 Soybean Futures Contracts with an aggregate value of $1,249,650). While the Fund may be better able to achieve the exact amount of exposure to the soybean market through the use of over-the-counter Other Soybean Interests, there is no assurance that the Sponsor will be able to continually adjust the Fund’s exposure to such Other Soybean Interests to maintain such exact exposure. Furthermore, as noted above, the use of Other Soybean Interests may itself result in imperfect correlation with the Benchmark. Any amounts not invested in Soybean Interests will be held in short-term Treasury Securities, cash and/or cash equivalents.

|

|

|

·

|

As Fund assets increase, there may be more or less correlation. On the one hand, as the Fund grows it should be able to invest in Soybean Futures Contracts with a notional amount that is closer on a percentage basis to the Fund’s NAV. For example, if the Fund’s NAV is equal to 4.9 times the value of a single futures contract, it can purchase only four futures contracts, which would cause only 81.6% of the Fund’s assets to be exposed to the soybean market. On the other hand, if the Fund’s NAV is equal to 100.9 times the value of a single Soybean Futures Contract, it can purchase 100 such contracts, resulting in 99.1% exposure. However, at certain asset levels the Fund may be limited in its ability to purchase Soybean Futures Contracts due to position limits or accountability levels. In these instances, the Fund would likely invest to a greater extent in Soybean Interests not subject to these restrictions. To the extent that the Fund invests in Cleared Soybean Swaps and Other Soybean Interests, the correlation between the Fund’s NAV and the Benchmark may be lower. In certain circumstances, position limits or accountability levels could limit the number of Creation Baskets that will be sold.

|

If changes in the Fund’s NAV do not correlate with changes in the Benchmark, then investing in the Fund may not be an effective way to hedge against soybean-related losses or indirectly invest in soybeans.

Changes in the price of the Fund’s Shares on the NYSE Arca may not correlate perfectly with changes in the NAV of the Fund’s Shares. If this variation occurs, then you may not be able to effectively use the Fund to hedge against soybean-related losses or to indirectly invest in soybeans.

While it is expected that the trading prices of the Shares will fluctuate in accordance with the changes in the Fund’s NAV, the prices of Shares may also be influenced by other factors, including the supply of and demand for the Shares, whether for the short term or the longer term. There is no guarantee that the Shares will not trade at appreciable discounts from, and/or premiums to, the Fund’s NAV. This could cause the changes in the price of the Shares to substantially vary from the changes in the spot price of soybeans, even if the Fund’s NAV was closely tracking movements in the spot price of soybeans. If this occurs, you may not be able to effectively use the Fund to hedge the risk of losses in your soybean-related transactions or to indirectly invest in soybeans.

The Fund may experience a loss if it is required to sell Treasury Securities or cash equivalents at a price lower than the price at which they were acquired.

If the Fund is required to sell Treasury Securities or cash equivalents at a price lower than the price at which they were acquired, the Fund will experience a loss. This loss may adversely impact the price of the Shares and may decrease the correlation between the price of the Shares, the Benchmark, and the spot price of soybeans. The value of Treasury Securities and other debt securities generally moves inversely with movements in interest rates. The prices of longer maturity securities are subject to greater market fluctuations as a result of changes in interest rates. While the short-term nature of the Fund’s investments in Treasury Securities and cash equivalents should minimize the interest rate risk to which the Fund is subject, it is possible that the Treasury Securities and cash equivalents held by the Fund will decline in value.

16

Certain of the Fund’s investments could be illiquid, which could cause large losses to investors at any time or from time to time.

The Fund may not always be able to liquidate its positions in its investments at the desired price. As to futures contracts, it may be difficult to execute a trade at a specific price when there is a relatively small volume of buy and sell orders in a market. Limits imposed by futures exchanges or other regulatory organizations, such as position limits and price fluctuation limits, may contribute to a lack of liquidity with respect to some exchange-traded Soybean Interests. In addition, over-the-counter contracts and cleared swaps may be illiquid because they are contracts between two parties and generally may not be transferred by one party to a third party without the counterparty’s consent. Conversely, a counterparty may give its consent, but the Fund still may not be able to transfer an over-the-counter Soybean Interest to a third party due to concerns regarding the counterparty’s credit risk.

A market disruption, such as a foreign government taking political actions that disrupt the market in its currency, its soybean production or exports, or in another major export, can also make it difficult to liquidate a position. Unexpected market illiquidity may cause major losses to investors at any time or from time to time. In addition, the Fund does not intend at this time to establish a credit facility, which would provide an additional source of liquidity, but instead will rely only on the Treasury Securities, cash and/or cash equivalents that it holds to meet its liquidity needs. The anticipated large value of the positions in Soybean Interests that the Sponsor will acquire or enter into for the Fund increases the risk of illiquidity. Because Soybean Interests may be illiquid, the Fund’s holdings may be more difficult to liquidate at favorable prices in periods of illiquid markets and losses may be incurred during the period in which positions are being liquidated.

If the nature of the participants in the futures market shifts such that soybean purchasers are the predominant hedgers in the market, the Fund might have to reinvest at higher futures prices or choose Other Soybean Interests.