Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - People's United Financial, Inc. | d8k.htm |

| EX-99.1 - EARINGS PRESS RELEASE DATED 4/20/2011 - People's United Financial, Inc. | dex991.htm |

1

st

Quarter 2011 Earnings Conference Call

April 20, 2011

Exhibit 99.2

*

*

*

*

*

*

*

*

*

*

*

* |

1

Certain statements contained in this release are forward-looking in nature.

These include all statements about People's United Financial's plans,

objectives, expectations and other statements that are not historical facts,

and usually use words such as "expect," "anticipate," "believe" and similar expressions.

Such statements represent management's current beliefs, based upon information

available at the time the statements are made, with regard to the matters

addressed. All forward-looking statements are subject to risks and

uncertainties that could cause People's United Financial's actual results or financial condition

to differ materially from those expressed in or implied by such statements. Factors

of particular importance to People’s United Financial include, but are

not limited to: (1) changes in general, national or regional economic

conditions; (2) changes in interest rates; (3) changes in loan default and charge-off rates; (4)

changes in deposit levels; (5) changes in levels of income and expense in

non-interest income and expense related activities; (6) residential

mortgage and secondary market activity; (7) changes in accounting and

regulatory guidance applicable to banks; (8) price levels and conditions in the public

securities markets generally; (9) competition and its effect on pricing, spending,

third-party relationships and revenues; (10) the successful integration

of acquired companies; and (11) possible changes in regulation resulting

from or relating to recently enacted financial reform legislation. People's United

Financial does not undertake any obligation to update or revise any

forward-looking statements, whether as a result of new information,

future events or otherwise. Forward Looking Statement

|

2

Operating earnings of $53.8 million, or $0.15 per share

Net interest margin of 4.16%; up 29 bps from Q4 2010

Total loan growth of $195MM or 4.5% linked-quarter annualized

Deposit growth of $177MM or 3.9% linked-quarter annualized

Strong non-interest income

Efficiency ratio improved to 66.2%

NPAs as a percentage of originated loans, REO and repossessed assets

fell to 1.96% from 2.09% as of Q4 2010

Proxy

statement/prospectus

mailed

to

Danvers

shareholders

on

April

8

th

and

the

Danvers

shareholder

vote

has

been

set

for

May

13

th

First Quarter 2011 Results

Overview |

3

Kirk Walters hired as Chief Financial Officer effective March 16th. He is

also a member of the Board at both the holding company and the bank

Expanding asset-based and multi-family lending activities

Boston: deposits at de novo branches grew $29MM in 1Q11, strong

1Q11 loan bookings and 2Q11 pipeline

Long Island: 7% core deposit growth since acquisition close, healthy

residential and home equity originations, booking C&I loans

Increased dividend to $0.63/share annually. Dividend yield is ~4.9%

Repurchased $60.7 million of stock in 1Q11 (4.6 million shares at an

average price of $13.09)

Recent Initiatives |

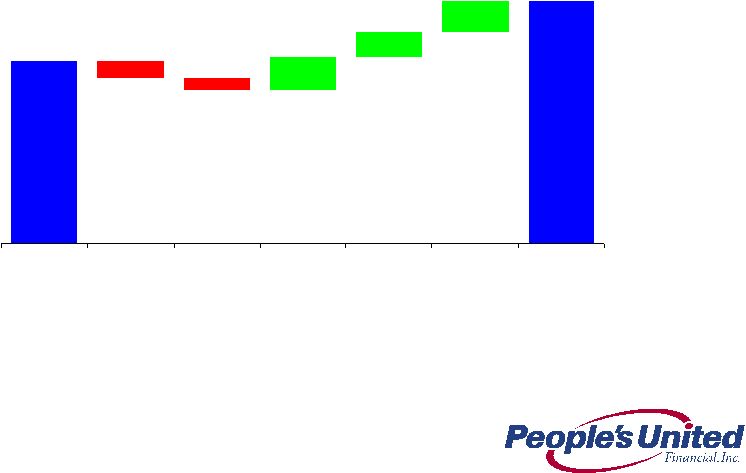

4

Net Interest Margin

Linked Quarter Change

4

3.87%

4.16%

-0.08%

-0.06%

0.16%

0.12%

0.15%

Q4 2010

Margin

Hedge Income

Decrease

Calendar Days

PUEF

Accretion

Adjustment

Investment Mix

& Yield

Full Quarter

Smithtown &

River

Q1 2011

Margin |

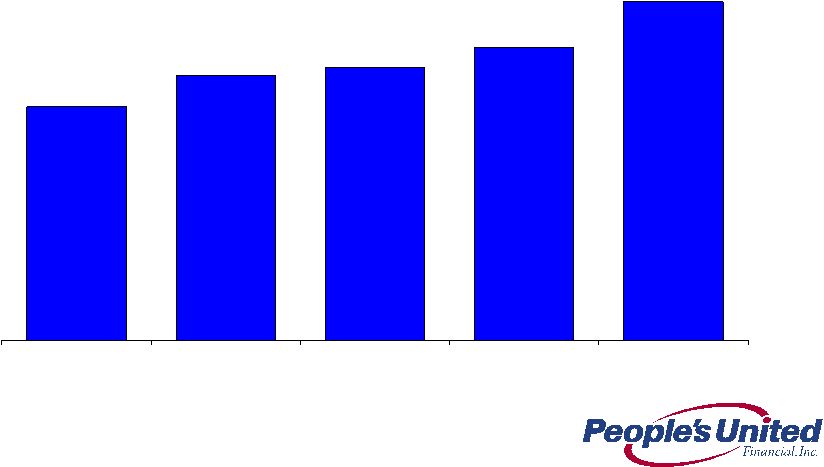

5

Net Interest Margin

Last Five Quarters

5

3.49%

3.69%

3.74%

3.87%

4.16%

1Q 2010

2Q 2010

3Q 2010

4Q 2010

1Q 2011 |

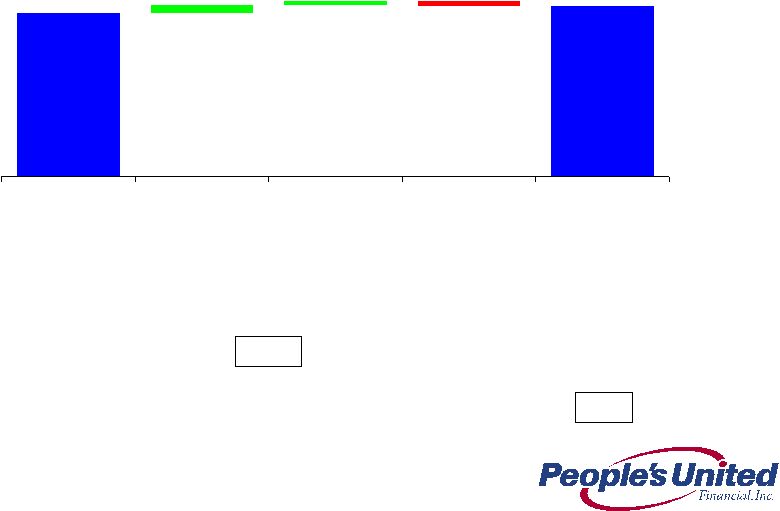

6

Loans

Linked Quarter Change

(in $ millions)

6

Annualized

Linked Quarter Change:

11.0%

12.3%

(30.3%)

Originated Annualized

Linked Quarter Change:

11.4%

Total Annualized

Linked Quarter Change:

4.5%

17,328

277

136

(218)

17,523

Dec 31, 2010

Commercial

Banking

Retail & Business

Banking

Acquired

Mar 31, 2011 |

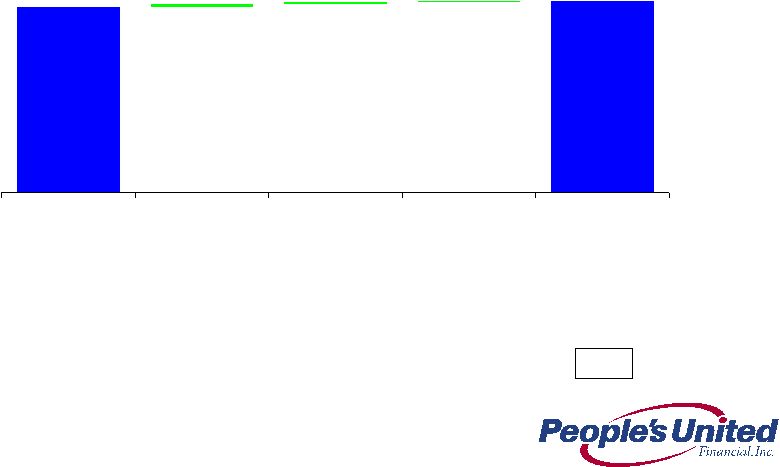

7

Deposits

Linked Quarter Change

(in $ millions)

7

Annualized

Linked Quarter Change:

2.1%

64.9%

5.9%

Total Annualized

Linked Quarter Change:

3.9%

17,933

18,110

34

63

80

Dec 31, 2010

Legacy

De Novo

Acquired

Mar 31, 2011 |

8

Non-interest income

Linked Quarter Change

(in $ millions)

1Q11

4Q10

Q-o-Q (%)

Investment management fees

$8.2

$7.9

4%

Insurance revenue

7.9

6.9

14%

Brokerage commissions

3.2

2.9

10%

Total wealth management

19.3

17.7

9%

Bank service charges

31.0

30.7

1%

Net gain on sales of loans

5.5

0.0

NM

Net gain on sales of res. mtg loans

3.1

4.2

(26%)

Bank owned life insurance

1.2

1.0

20%

Merchant services income, net

1.0

1.1

(9%)

Net security gains (losses)

0.1

(1.0)

NM

Other non-interest income

13.4

14.4

(7%)

Total non-interest income

$74.6

$68.1

10%

$5.5MM of gains on non-performing loan sales from the acquired

Smithtown portfolio, full quarter contribution from Smithtown and

RiverBank, strength across the board in wealth management

|

9

Non-interest expenses increased just 2% over 4Q10 in spite of a full

quarter of Smithtown and RiverBank expenses

Non-Interest Expense

Linked Quarter Change

(in $ millions)

1Q11

4Q10

Q-o-Q (%)

Compensation & Benefits

$105.4

$98.3

7%

Occupancy & Equipment

33.1

28.1

18%

Prof. and outside services

15.9

19.8

(20%)

Amort. of acq. related intangibles

5.9

6.1

(3%)

Merger-related expenses

3.1

4.8

(35%)

Other non-interest expense

39.4

42.0

(6%)

Total non-interest expense

$202.8

$199.1

2% |

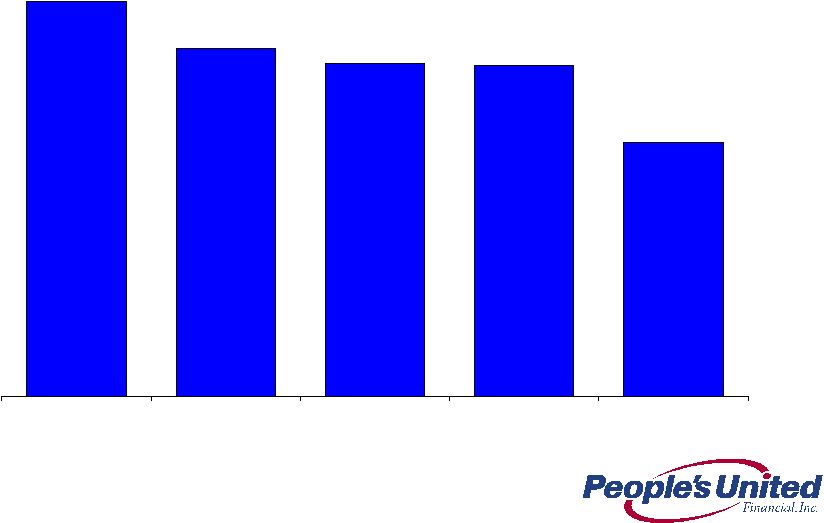

10

Efficiency Ratio

Historical Trend

75%

72%

71%

71%

66%

1Q 2010

2Q 2010

3Q 2010

4Q 2010

1Q 2011 |

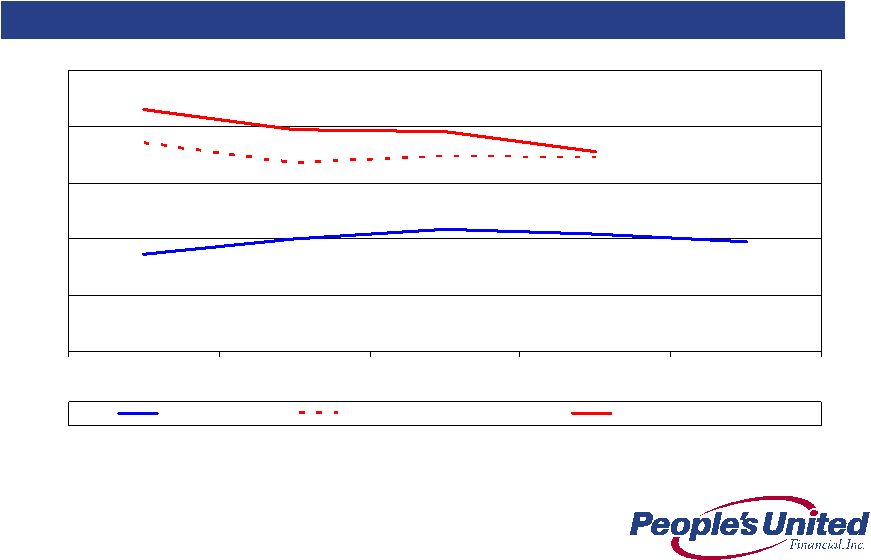

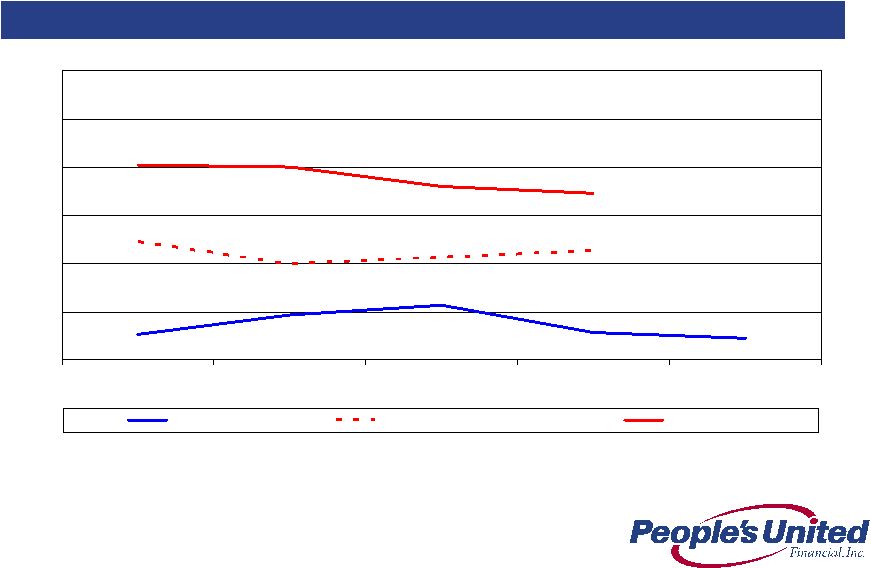

11

Last Five Quarters

1.96

2.09

3.46

3.55

0.00

1.00

2.00

3.00

4.00

5.00

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

PBCT

Peer Group Median

Top 50 Banks by Assets

Asset Quality

NPAs / Loans & REO* (%)

*

Non-performing

assets

(excluding

acquired

non-performing

loans)

as

a

percentage

of

originated

loans

plus

all

REO

and

repossessed

assets;

acquired

non-performing

loans

excluded

as

risk

of

loss

has

been

considered

by

virtue

of

our

estimate

of

acquisition-date

fair

value

and/or

the

existence

of

an

FDIC

loss

sharing

agreement

Source: SNL Financial and Company filings |

12

Last Five Quarters

0.22

0.28

1.13

1.73

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

PBCT

Peer Group Mean

Top 50 Banks

Asset Quality

Net Charge-Offs / Avg. Loans (%)

Source: SNL Financial and Company filings |

13

Allowance for Loan Losses

Coverage Detail

(in $ millions)

1Q11

ALLL

% of

Originated

Loans

% of

Originated

NPLs

CRE

$78.4

1.57%

109%

C&I

60.5

1.56%

124%

Equipment Finance

26.8

1.84%

69%

Residential

6.3

0.25%

9%

Home Equity

3.0

0.16%

29%

Other Consumer

2.5

1.30%

576%

Total

$177.5

1.19%

74%

Commercial Banking

$165.7

1.61%

104%

Retail Banking

11.8

0.26%

15% |

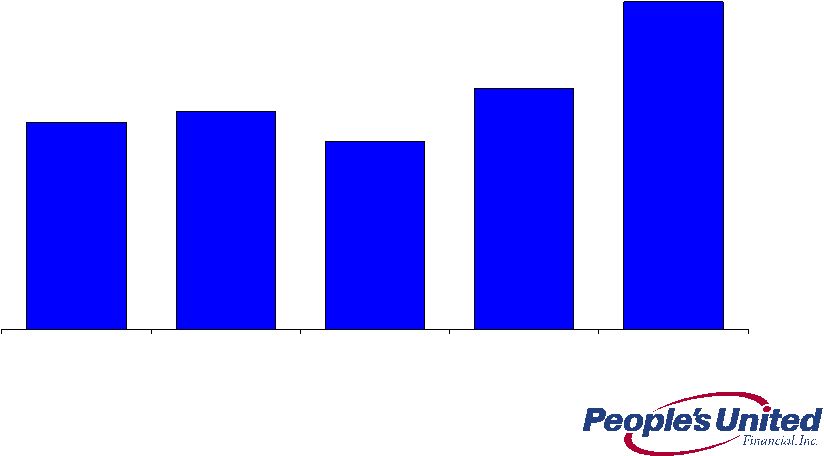

14

Operating ROAA Progress

Last Five Quarters

0.55%

0.58%

0.50%

0.64%

0.87%

1Q 2010

2Q 2010

3Q 2010

4Q 2010

1Q 2011 |

15

Capital Deployment

Primary

focus

is

to

deploy

capital

via

organic

growth

–

“new

markets,

new

products, cross-sell”

Announced an increase to our dividend (19th consecutive annual dividend

increase), our dividend yield is ~4.9%

Repurchased $61MM of stock in 1Q11 at a weighted average price of $13.09

Prohibited from repurchasing shares until the Danvers Bancorp deal

closes

Acquisitions

Danvers Bancorp shareholder vote set for May 13th

Building

relationships

with

banks

$1BN

-

$20BN

in

asset

size

Maintaining price discipline in light of challenging industry conditions

|

16

Summary

Premium brand built over 169 years

High quality Northeast footprint characterized by wealth, density and

commercial activity

Strengthened leadership team

Low cost of deposits

Strong net interest margin

Superior asset quality

Focus on relationship-based banking

Growing

loans

and

deposits

within

footprint

-

in

two

of

the

largest

MSAs

in

the country (New York City, #1 and Boston, #10)

Significantly more asset sensitive than peers

Pro forma tangible common equity ratio of ~12%

Sustainable Competitive Advantage |

Q

& A *

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

* |

Appendix

*

*

*

*

*

*

*

*

*

*

*

* |

19

We

expect

that

interest

rates

will

not

rise

in

2011.

However,

we

do

expect

rates

to

rise

in

2012 and beyond

Given short term interest rates are so low and are expected to remain low for the near

term, we have added to our securities portfolio

For Q4 2010 we were 3.5x –

4.5x as asset sensitive as the estimated median of our

peers

For every 100bps increase in the Fed Funds rate, our net interest income is

projected to increase by ~$40MM on an annualized basis

Notes:

1.

Analysis is as of 12/31/10 filings

2.

Data as of 12/31/10 SEC filings, where exact +100bps shock up scenario data was not

provided PBCT interpolated based on data disclosed 3.

Data as of 12/31/10 filings, where exact +200bps shock up scenario data was

not provided PBCT interpolated based on data disclosed Asset

Sensitivity Net Interest Income at Risk ¹

Analysis involves PBCT estimates, see notes below

Change in Net Interest Income

Scenario

Lowest

Amongst Peers

Highest

Amongst Peers

Peer Median

PBCT Multiple to

Peer Median

Shock Up

100bps ²

-0.7%

5.6%

1.0%

3.5x

Shock Up

200bps ³

-1.0%

11.2%

2.4%

4.5x |

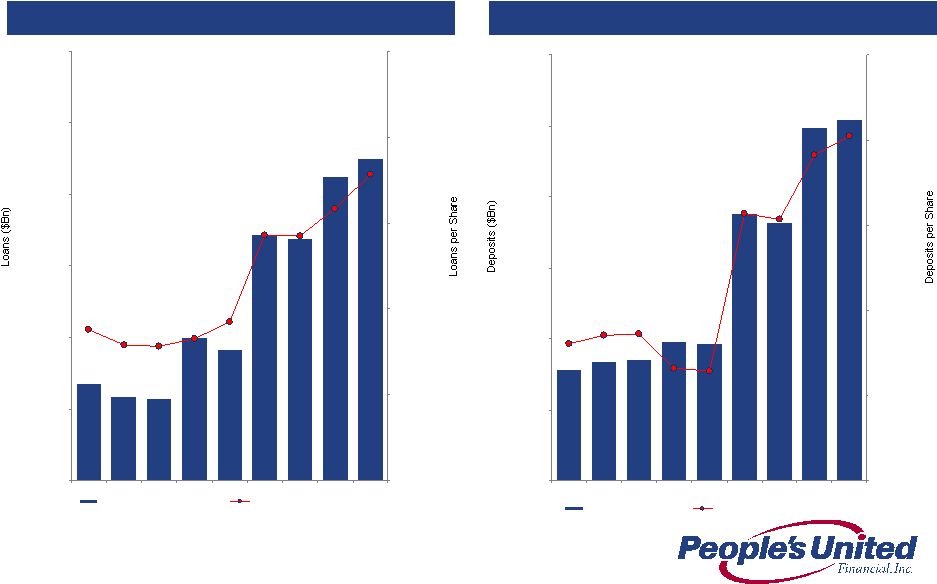

20

Loans

Deposits

Growing Future Earnings Per Share

Loans and Deposits per Share

* Pro forma for FIF acquisition

* *Pro forma for SMTB & LSBX acquisitions

**

*Pro

forma

for

DNBK

acquisition

$12.5

$14.0

$15.5

$17.0

$18.5

$20.0

$21.5

1Q09

2Q09

3Q09

4Q09*

1Q10

2Q10**

3Q10**

4Q10***

1Q11***

$35.00

$40.00

$45.00

$50.00

$55.00

$60.00

Gross Loans ($Bn)

Loans per share

$12.5

$14.0

$15.5

$17.0

$18.5

$20.0

$21.5

1Q09

2Q09

3Q09

4Q09*

1Q10

2Q10**

3Q10**

4Q10***

1Q11***

$35.00

$40.00

$45.00

$50.00

$55.00

$60.00

Deposits ($Bn)

Deposits per share |

For

more information, investors may contact: Peter Goulding, CFA

203-338-6799

peter.goulding@peoples.com

*

*

*

*

*

*

*

*

*

*

*

* |