Attached files

| file | filename |

|---|---|

| EX-31.1 - EXERCISE FOR LIFE SYSTEMS, INC. | ex31_1.htm |

| EX-32.1 - EXERCISE FOR LIFE SYSTEMS, INC. | ex32_1.htm |

| EX-14.1 - EXERCISE FOR LIFE SYSTEMS, INC. | ex14_1.htm |

U.S. Securities and Exchange Commission

Washington, D.C. 20549

FORM 10-K

| [X] | Annual Report Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 for the Fiscal Year Ended December 31, 2010 |

| [ ] | Transition Report Under Section 13 or 15(d) of The Securities Exchange Act of 1934 for the Transition Period from _______ to _______ |

Commission File Number: 333-153589

EXERCISE FOR LIFE SYSTEMS, INC.

(Exact name of small business issuer as specified in its charter)

| North Carolina | 22-3464709 |

| (State or other jurisdiction of | (IRS Employer Identification No.) |

| incorporation or organization) |

92 Gleneagles View, Cochrane, Alberta, Canada

(Address of principal executive offices)

(403) 932-1801

(Issuer's telephone number)

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, $.0001 par value

(Title of Class)

Indicate by check mark if the registrant is a well-know seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [x]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act

Yes [ ] No [x]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [x] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit and post such files).

Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 if Regulation S-K (229.405 of this Chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy of information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K.

Yes [ ] No [x]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | £ |

| Non-accelerated filer | £ (Do not check if a smaller reporting company) |

| Accelerated filer | £ |

| Smaller reporting company | S |

Indicate by check mark whether the registrant is a shell company (as defined in rule 12b-2 of the exchange act).

Yes [ ] No [x]

The Registrant’s revenues for its fiscal year ended December 31, 2010 were $47,808.

The aggregate market value of the voting stock and non-voting common equity on April 15, 2011 (consisting of Common Stock, $0.0001 par value per share) held by non-affiliates was approximately $760,296 based upon the most recent sales price for such Common Stock on said date ($0.09). On April 15, 2011, there were 40,000,000 shares of our Common Stock issued and outstanding, of which approximately 8,447,737 shares were held by non-affiliates.

Number of shares of common stock, par value $.0001, outstanding as of April 15, 2011: 40,000,000

DOCUMENTS INCORPORATED BY REFERENCE

None

CAUTIONARY STATEMENT REGARDING FORWARD LOOKING INFORMATION

The discussion contained in this 10-K under the Securities Exchange Act of 1934, as amended, contains forward-looking statements that involve risks and uncertainties. The issuer's actual results could differ significantly from those discussed herein. These include statements about our expectations, beliefs, intentions or strategies for the future, which we indicate by words or phrases such as "anticipate," "expect," "intend," "plan," "will," "we believe," "the Company believes," "management believes" and similar language, including those set forth in the discussions under "Notes to Financial Statements" and "Management's Discussion and Analysis or Plan of Operation" as well as those discussed elsewhere in this Form 10-K. We base our forward-looking statements on information currently available to us, and we assume no obligation to update them. Statements contained in this Form 10-K that are not historical facts are forward-looking statements that are subject to the "safe harbor" created by the Private Securities Litigation Reform Act of 1995.

| (1) |

PART I:

Item 1. Business

Item 1A. Risk Factors

Item 1B. Unresolved Staff Comments

Item 2. Properties

Item 3. Legal Proceedings

Item 4. Submission of Matters to a Vote of Security Holders

PART II:

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Item 6. Selected Financial Data

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

Item 8. Financial Statements and Supplementary Data

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

Item 9A. Controls and Procedures

Item 9A(T). Controls and Procedures

Item 9B. Other Information

PART III:

Item 10. Directors, Executive Officers and Corporate Governance

Item 11. Executive Compensation

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

Item 13. Certain Relationships and Related Transactions, and Director Independence

Item 14. Principal Accounting Fees and Services

PART IV:

Item 15. Exhibits, Financial Statement Schedules

SIGNATURES:

| (2) |

ITEM 1. BUSINESS

Our Company

Exercise for Life Systems, Inc. (the “Company”, “EFLS”) was incorporated in New Jersey in 1996 as A.J. Glaser, Inc. and redomiciled to North Carolina in 2006. In 2008, the Company amended its North Carolina Articles of Incorporation to change its name to Exercise for Life Systems, Inc.

On February 10, 2011, the Company entered into a Plan of Exchange agreement with MediaMatic Ventures Inc., a privately-held company incorporated under the laws of the Province of Alberta, Canada (“MMV”), and the shareholders of MMV (the “MMV Shareholders”). Pursuant to the agreement, on February 11, 2011 we purchased all 15,685,692 of the issued and outstanding common shares of MMV from the MMV Shareholders in exchange for issuing 28,000,000 shares of our common stock to the MMV Shareholders. MMV and MMV Shareholders represented that on the date of the agreement MMV had total assets of at least $3,200,000 and liabilities of not greater than $850,000 (excluding contingent liabilities).

The completion of the share exchange was conditioned upon, among other things:

| (1) our eliminating all of our known or potential liabilities as of the closing date, including, but not limited to, any accounts payable, accrued expenses, and any liabilities shown on its quarterly report for the period ended September 30, 2010; Adam Slazer, our prior President and sole officer (“Mr. Slazer”) and our pre-exchange shareholders are fully responsible for any unknown or undisclosed liabilities incurred prior to transfer of control under the exchange; |

| (2) in the event that there comes to exist any expenses concerning any known or unknown lawsuit, legal dispute or any correlation expense caused by the pre-exchange Company and its shareholders, Mr. Slazer and the pre-exchange shareholders shall undertake full responsibility and afford the correlation expenses after the closing; |

| (3) stock certificates representing 9,884,730 shares of our common stock (representing approximately 85% of our outstanding stock prior to the consummation of the exchange) owned by Adam Slazer are being delivered for cancellation, in consideration for which Jeremy Ostrowski, one of the MMV shareholders, is providing a $75,000 promissory note; the promissory note will not bear interest, will be due on August 9, 2011, and will be collateralized by 375,000 shares of our common stock owned the two of our pre-exchange shareholders; |

As required by the exchange agreement, our directors prior to the exchange have resigned and five persons identified herein were appointed our directors. In addition, Adam Slazer, has resigned as our President and sole officer and Jeremy Ostrowski has been appointed as our President and sole officer.

The share exchange is being accounted for as an acquisition for accounting purposes, as MMV is now our wholly owned subsidiary. Consequently, the assets, liabilities and historical operations of MMV will only be reflected in our consolidated financial statements after the completion of the share exchange, as will our operations since the closing of the share exchange.

As a result of the exchange, we have adopted the business of MMV, which is the providing of multimedia kiosks throughout Canada.

Description of Business

Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements. To the extent that any statements made in this report contain information that is not historical, these statements are essentially forward-looking. Forward-looking statements can be identified by the use of words such as “expects”, “plans”, “will”, “may,”, “anticipates”, “believes”, “should”, “intends”, “estimates”, and other words of similar meaning. These statements are subject to risks and uncertainties that cannot be predicted or quantified and, consequently, actual results may differ materially from those expressed or implied by such forward-looking statements. Such risks and uncertainties include, without limitation, our ability to raise additional capital to finance our activities; the effectiveness, profitability and marketability of our products; legal and regulatory risks associated with the share exchange; the future trading of our common stock; our ability to operate as a public company; our ability to protect our proprietary information; general economic and business conditions; the volatility of our operating results and financial condition; our ability to attract or retain qualified senior management personnel and research and development staff; and other risks detailed from time to time in our filings with the Securities and Exchange Commission (the “SEC”), or otherwise.

Information regarding market and industry statistics contained in this report is included based on information available to us that we believe is accurate. It is generally based on industry and other publications that are not produced for purposes of securities offerings or economic analysis. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and the additional uncertainties accompanying any estimates of future market size, revenue and market acceptance of products and services. We do not undertake any obligation to publicly update any forward-looking statements. As a result, investors should not place undue reliance on these forward-looking statements.

| (3) |

Previous Business

Before we closed the transactions contemplated by the Plan of Exchange, we were a full-service operator of personal fitness training in and around the Lake Norman area of Charlotte, North Carolina. We operated from our training facility located at East Field Road, Suite 200-311 Huntersville, NC 28078. By operating our fitness center in a major metropolitan area such as Charlotte, North Carolina, we were able to offer city-wide training services, providing more value to clients and differentiating ourselves from “mom and pop” competitors while achieving operating efficiencies.

Current Business

Upon acquiring MMV on February 10, 2011 pursuant to the Plan of Exchange, we adopted the business of MMV. We are now a leading provider of multimedia kiosks throughout Canada. MMV operates the only WiFi enabled kiosk providing multimedia content, including DVD’s, video games and music; both digitally and physically. As of July 2010, MMV’s DVD kiosks were in over 80 locations in leading retailers, securing MMV as the second largest provider in Canada.

Market Opportunity

Multimedia kiosks providing both digital and physical content are a rapidly growing market. In 2007, the market leader in physical DVD kiosk rentals, RedBox, surpassed Blockbuster for number of US locations.

As traditional brick and mortar video stores are shutting down due to alternative solutions and high fixed costs, even historic market leaders such as Blockbuster have begun to adapt, particularly through a recent partnerships with NCR as the provider of their own DVD kiosks. In 2009, DVD Kiosks represented 19% ($950 million) of all DVD rentals and is estimated to reach upwards of 30% ($1.3 billion) by 2010. It is predicted that the US market can support 60,000 DVD kiosks, which should be reached in 2014, and is expected to generate sales of $2 billion.

The DVD rental business continues to be the 3rd largest source of movie revenue, while online rentals (ON-DEMAND, etc.) only generate a small amount of the total.

Product Overview

MMV’s DVD kiosks are highly portable condensing more than 700 square feet into 7 square feet containing more than 1000 titles that are managed by a highly technical backend content management system, including the following features:

Digital downloading

Utilizing MMV’s built in WiFi technology, customers can download digital content from any MMV kiosk through a variety of devices including computer, iPad, iTouch, PDA device, USB, Digital home boxes and any device with similar capabilities located within 100 yards of a kiosk.

24/7 Central “Remote” Monitoring System

Monitored remotely, MMV has 24/7 insight into its machines, including DVD inventory and rentals by location and technical issues. MMV has the ability to fix most technical and customer-related issues remotely as well as to manage the inventory of individual kiosks.

| (4) |

IP Connected

MMV DVD kiosks are connected via IP into a customer-accessible network such that customers can go online to view and rent/purchase items for all locations.

Pre-reserve titles

Consumers have the ability to “pre-reserve” their favorite titles via the MMV website. Based on the customer’s location, they are able to pick a specific location and reserve their preferred title prior to physically renting the DVD.

Multiple User Interface

In the event multiple users wish to download digital content from a single kiosk, MMV’s broadband allows up to 6 concurrent users to download their titles.

Digital advertising

Newer versions of MMV’s DVD kiosks are equipped with an LCD monitor that is able to provide movie previews and paid advertisements.

Touch screen monitor

Customers are able to interact directly with the DVD kiosks via an easy to use touch screen monitor.

Multi-tied product offering

MMV offers two payment solutions to rentals: single unit rental and monthly subscription. Customers can either pay on a per/rental basis or can sign up for a monthly subscription allowing unlimited rentals (2 DVD’s at a time). Subscription revenue typically accounts for over 30% of MMV’s monthly revenues.

CHIP Pre-paid membership

MMV offers a pre-paid membership card, which may be used to receive gifts and discounts at all MMV DVD kiosk locations.

Private label

MMV allows large retailers to private label the MMV kiosk box with their own brand.

Competitive Edge

MMV’s DVD kiosks offer a variety of features that are not available from the current competition:

Digital Downloads

MMV has the only WiFi-enabled DVD Kiosk currently in the market with digital download capabilities. With download speeds of 110MB per second, by December 2011 MMV plans to offer over 100,000 titles (movies and music) that may be downloaded digitally. Utilizing its remote content management system, MMV allows users to request specific titles at specific kiosks locations to be downloaded. If a title is not currently available at a location, but is in the system, MMV can easily switch out titles enabling the customer to have access to their preferred content. Upon a digital rental of a title, depending on the terms, the title will be removed from the device after an allotted amount of time.

No competitor offers any digital download capabilities.

Video Games

MMV operates the only kiosks to offer both DVD movies and video games in all of their kiosk locations. To date, video games have a higher margin than DVD’s and have been a strong revenue producer in several locations.

Subscription Mode

MMV is the only DVD kiosk provider to offer two rental models; single unit rentals or a monthly subscription. Customers have the ability use either a single unit rental or can sign up for a monthly subscription allowing unlimited rentals (2 DVD’s at a time).

| (5) |

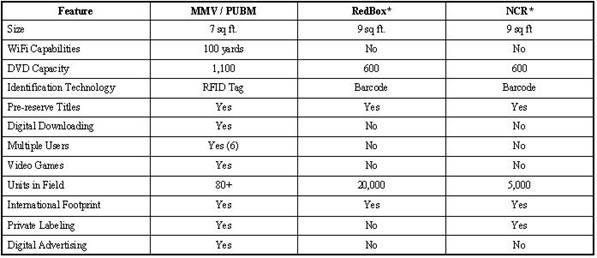

Competition

MMV’s business faces competition from many other providers of movie content, from traditional stores, such as Blockbuster and Hollywood Video, to other self-service kiosks, such as Blockbuster Express, to online or postal providers, such as Netflix, to other movie distribution rental channels, such as pay-per-view, video-on-demand, online streaming, premium television, basic cable, and network and syndicated television, many of whom may be more experienced in the business or have more resources than we do or otherwise compete with us in this segment of our business as described above.

The following table provides a comparison of the features provided by MMV and its two major competitors in the providing of self-service kiosks, RedBox and NCR.

*Estimates

Coinstar Inc. is a multi-national company offering a range of 4th Wall® solutions for retailers’ storefronts. RedBox, through its parent company Coinstar ,operates the largest DVD kiosks network, with over 20,000 locations and 2009 revenues in excess of $700 million.

NCR Corporation is a global technology company that provides innovative products and services to help businesses build stronger relationships with its customers. Focused particularly in automatic teller machines and self-service kiosks, NCR has recently purchased several smaller DVD kiosk providers (TNR and DVD Play) and has a partnership with Blockbuster to be the kiosk provider for Blockbuster Express.

There are a variety of small regional multimedia kiosk companies in operation, but due to the intense capital requirements and inability to obtain top tier locations, these companies are often not viewed as significant long-term competitors.

Revenue Model

MMV purchases and places a corporate-owned DVD kiosk in a retail location subject to a revenue share agreement (90/10) with the site-owner. MMV is responsible for operating and maintaining the kiosks.

A typical contract for a corporate kiosk provides for an initial 12-month term. After the initial term, MMV has the sole right to extend the term up to 2 to 3 additional years, with automatic renewals. MMV has the right to remove any unit at its sole discretion, including but not limited to unprofitability of the location or due to technical issues.

MMV also developed a franchise model for DVD kiosks. Litigation presently is pending with certain franchisees as described under “Description of Business – Legal Proceedings.” Pending the resolution of such litigation, MMV has suspended its franchise model.

| (6) |

Pipeline

MMV has a pipeline of potential kiosk locations estimated at over 3,000. Several include:

Husky Energy

MMV has a signed contract to provide over 350 DVD kiosks to Husky Oil locations in Alberta, British Columbia, Manitoba and Saskatchewan.

Ash Payment Systems

MMV has entered into a joint venture with Ash Payment Systems (“APS”) to provide MMV’s DVD kiosks on an exclusive basis in at least 500 locations in the Eastern Canada provinces. APS is a leader in the payments industry specializing in payment hardware, payment processing services, self-service retail platforms and technical support services. APS will use its relationships in the territory and deploy and train staff and manage inventory and payments using the same kiosks used by us in Western Canada. APS partners include Pizza Hut Canada, Gino’s Pizza, VIRGIN Mobile, Petro-Canada, Domino’s Pizza. The agreement is for five years subject to annual renewals thereafter. Gross profits are divided equally between MMV and ASP.

iMOZI Canada Inc.

MMV has entered into exclusive purchase agreements, dated June 15, 2010 and October 8, 2010, with iMOZI Canada Inc. pursuant to which it will purchase goods and equipment, including 500 indoor and outdoor vending kiosks and related software to operate the kiosks. MMV provides the Internet access for the kiosks. The agreement is in effect until MMV has purchased 500 units.

Intellectual Property

We have not filed for any protection of our name or trademark. As a distribution company we do not directly own any of the intellectual property rights attached to any of the products we distribute.

Research and Development

We did not incur any research and development expenses from our inception to December 31, 2010.

Reports to Security Holders

We are subject to the reporting and other requirements of the Securities Exchange Act and we intend to furnish our shareholders with annual reports containing financial statements audited by our independent auditors and to make available quarterly reports containing unaudited financial statements for each of the first three quarters of each year.

The public may read and copy any materials that we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The address of that site is www.sec.gov.

Seasonality

MMV’s business generally experiences lower revenue in the spring due in part to improved weather and Daylight Savings Time, and in September and October, due in part to the beginning of the school year and the introduction of the new television season. The year-end and summer holiday months have historically been the highest revenue months for kiosk services.

| (7) |

ITEM 1A. RISK FACTORS

Our business and an investment in our securities are subject to a variety of risks. The following risk factors describe the most significant events, facts or circumstances that could have a material adverse effect upon our business, financial condition, results of operations, ability to implement our business plan and the market price for our securities. Many of these events are outside of our control. The risks described below are not the only ones facing our company. Additional risks not presently known to us or that we consider immaterial based on information currently available to us may also materially adversely affect us. If any of the events anticipated by the risks described herein occur, our business, cash flow, results of operations and financial condition could be materially adversely affected. In such case, the trading price of our common stock could decline and investors in our common stock could lose all or part of their investment.

Risks relating to our Business

Our new business has a limited operating history which makes it difficult to evaluate our future prospects and your investment.

MMV was organized as an Alberta, Canada corporation on February 8, 2007 and has a limited operating history. No assurances can be given that we will be able to successfully maintain and develop our business or meet our business objectives.

Our operating expenses will be high and there can be no assurances that we will achieve or maintain profitability.

We will have significant capital and operating expenses and significant losses and expects such losses to continue as we grow our business. Prior to earning revenue from our principal business, we must expand our product offerings and increase our sales. No assurances can be given that we will succeed in those efforts. However, if such tasks are achieved, we still will need to develop revenue channels to achieve and sustain profitability. It is possible that we may never achieve sustained profitability and, even if we do, we may not sustain or increase profitability on a quarterly or an annual basis in the future. If we are not successful in becoming profitable, we may be forced to curtail or cease operations.

In order to meet our short-term and long-term business goals, we will likely need additional funding.

It is likely that we will have insufficient capital to fund the growth of our business and will require additional financing to meet our business objectives. We can provide no assurances that we will obtain such additional funding on terms favorable to us. The overall development costs for maintaining the long-term viability of we are substantially in excess of this offering. This Company may partner with other entities and employ alternative financing structures.

We operates in a highly competitive market and may encounter competitors having greater resources and experience.

There can be no assurances that other competitors will not develop products or services that are superior to ours. There are numerous large and small competitors in our exact market space. If we cannot successfully compete against these companies, our business, results of operations and financial condition are likely to be materially and adversely affected.

Defects, failures or security breaches in and inadequate upgrade of or changes to our operating systems could harm our business.

The operation of the kiosks and equipment relating to our business depends on sophisticated software, hardware, computer networking and communication services that may contain undetected errors or may be subject to failures or complications. These errors, failures or complications may arise particularly when new, changed or enhanced products or services are added. In the past, there have been limited delays and disruptions resulting from upgrading or improving these operating systems. Future upgrades, improvements or changes that may be necessary to expand and maintain our business could result in delays or disruptions or may not be timely or appropriately made, any of which could seriously harm our operations.

Certain aspects of the operating systems relating to our business are outsourced to third-party providers. Accordingly, the effectiveness of these operating systems is to a certain degree dependent on the actions and decisions of third-party providers.

| (8) |

We depend upon third-party manufacturers, suppliers and service providers for key components and substantial support for our kiosks and equipment.

We conduct limited manufacturing operations and depend on outside parties to manufacture key components of our kiosks and equipment. We intend to continue to expand our installed base of machines and equipment. Such expansion may be limited by the manufacturing capacity of our third-party manufacturers and suppliers. Third-party manufacturers may not be able to meet our manufacturing needs in a satisfactory and timely manner. If there is an unanticipated increase in demand for kiosks, we may be unable to meet such demand due to manufacturing constraints.

Some key hardware components used in the kiosks are obtained from a limited number of suppliers. We may be unable to continue to obtain an adequate supply of these components in a timely manner or, if necessary, from alternative sources. If we are unable to obtain sufficient quantities of components or to locate alternative sources of supply on a timely basis, we may experience delays in installing or maintaining our kiosks, which could seriously harm our business, financial condition and results of operations.

We must attract and retain qualified personnel to be successful, and competition for qualified personnel is intense in our market.

Our success will depend to a significant extent upon the contributions of our key management and business development personnel. We must attract and retain highly talented and seasoned individuals to lead our business. Our success will depend on our ability to identify, attract and retain qualified design, sales, marketing, business development and finance personnel. The competition in our industry makes it difficult to retain key personnel and to recruit new qualified personnel. If we do not succeed in hiring and retaining candidates with appropriate qualifications, our revenues and product development efforts could be harmed.

We may not be able to adequately protect our intellectual property.

Our intellectual property is and will continue to be one of our most important assets and we expect to utilize significant resources to protect it. Our ability to compete effectively will depend substantially on our efforts in developing and maintaining proprietary aspects of our intellectual property. Moreover, there can be no assurances that any future patents, copyrights or trademarks that may be issued as a result of our applications will offer any degree of protection to our products against competitive products. Our technology may infringe on intellectual property owned by competitors. There can be no assurances that competitors, many of whom have substantial resources, will not seek to apply for and obtain patents, trademarks, or copyrights that will prevent, limit, or interfere with our ability to make, use, or sell its products. In addition, if we cannot protect our domain names, our ability to successfully brand our name and our products and services will be impaired.

We may be adversely affected by currency fluctuations.

Our operating results and cash flow are affected by changes in the Canadian dollar exchange rate relative to the currencies of other countries. Exchange rate movements can have a significant impact on results as a significant portion of our operating costs are incurred in Canadian and other currencies and a significant portion of our revenues may be earned in U.S. dollars.

| (9) |

Risks Related to the Market for our Securities

Sales of substantial amounts of our common stock in the open market could depress our stock price.

If substantial amounts of our common stock are sold in the public market following the exchange transaction, the market price of our common stock may decrease substantially. These sales might also make it more difficult for us to sell equity or equity-related securities at a time and price that we otherwise would deem appropriate.

Our stock price may fluctuate substantially.

The market price for our common stock may be affected by a number of factors, including those described above and the following:

| • | the announcement of new products and services or product and service enhancements by us or our competitors; |

| • | actual or anticipated quarterly variations in our results of operations or those of its competitors; |

| • | changes in earnings estimates or recommendations by securities analysts that may follow our stock; |

| • | developments in our industry; and |

| • | general market conditions and other factors, including factors unrelated to our operating performance or the operating performance of our competitors. |

In addition, the stock market in general has experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of particular companies. Broad market and industry trends may also materially and adversely affect the market price of our common stock, regardless of our actual operating performance. Volatility in the market price and trading volume of our common stock may prevent our stockholders from selling their shares profitably. In the past, following periods of volatility in the market price of a company’s securities, securities class-action litigation has often been initiated against that company. Class-action litigation could result in substantial costs and a diversion of management’s attention and resources.

| (10) |

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

We currently rent 8,181 square feet of commercial space in Cochrane, Canada, for which we pay $63,000 per year. The facilities are adequate for our use. The lease expires on January 1, 2014.

ITEM 3. LEGAL PROCEEDINGS

We may occasionally become involved in various lawsuits and legal proceedings arising in the ordinary course of business. However, litigation is subject to inherent uncertainties and an adverse result in these or other matters may arise from time to time that may have an adverse affect on our business, financial conditions or operating results. We currently are not aware of any such legal proceedings or claims that will have, individually or in the aggregate, a material adverse affect on our business, financial condition or operating results except as follows:

On May 5, 2010, MMV had a claim filed against them from a franchisee. The claim named MMV as a defendant and the franchisee as a plaintiff. The plaintiff is seeking a rescission of the franchise agreement and a refund of franchise funds paid in the amount of $325,000 paid, together with a claim for additional damages of $500,000. There has been a judgment registered with Canada’s Queens Bench in the amount of $325,000. MMV’s management estimates that they can settle the claim in the amount of $325,000 and have recorded a contingency loss in expectation of this settlement.

On May 11, 2010, MMV commenced a lawsuit against former sales agents of MMV due to the fact that the defendants started a competing business contrary to a contract which is alleged they entered into with MMV. The amount of the lawsuit is yet to be determinable regarding the settlement amount of the lawsuit as of the date of these financial statements.

On May 13, 2010, MMV had a civil claim filed against them from a franchisee for alleged additional net profits owed to them during the time that MMV operated video kiosks in its stores. The claim named MMV as the defendant and the franchisee as the plaintiff. The claim amount is for $25,000. MMV’s management estimates that they can settle the civil claim for the amount of $25,000 and have recorded a contingency loss in expectation of this settlement.

On August 18, 2010, MMV had a Statement of Claim filed against them from multiple franchisees alleging that MMV sold a franchise to them and that MMV breached the requirements of the Franchises Act of Alberta, Canada. The claim named MMV as a defendant and the multiple franchisees as a plaintiff. The plaintiffs are also seeking rescission of the franchise purchase contracts together with a refund of their monies, or alternatively damages for loss of profits aggregating $2,100,000. The plaintiffs further claim alternatively that there was a fraudulent misrepresentation made by MMV and claim damages in the amount of approximately $5,700,000. MMV’s management estimates that they can settle the claims for the amount of $2,100,000 and have recorded a contingency loss in expectation of this settlement.

On September 7, 2010, MMV had a Statement of Claim filed against them from a franchisee. The claim named MMV as a defendant and the franchisees as the plaintiff. The claim alleges that MMV breached the franchise contract and a breach of the Franchises Act of Alberta, Canada whereby the plaintiff claims recession of the Franchise Agreement and recovery of net losses in the amount of $55,000. There was a judgment filed with Canada’s Queen’s Bench on December 3, 2010 for no specified amount. The judgment gave the plaintiffs claim against the owner’s personal residence. The plaintiffs have informed the owner that they would consider settlement for MMV’s public shares and discharge the judgment filed. MMV’s management estimates that they can settle the claim in the amount of $55,000 and have recorded a contingency loss in expectation of this settlement.

On September 29, 2010, there was a Statement of Claim filed against MMV from franchisees. The claim named MMV as a defendant and the franchisees as a plaintiff. The claim alleges that MMV breached the Franchises Act of Alberta, Canada. The plaintiffs are claiming $250,000 in damages and lost profits. The plaintiffs have indicated to MMV and council that they would settle for MMV’s public shares in exchange of settlement of lawsuits. MMV filed a Statement of Defense on December 17, 2010. MMV’s management estimates that they can settle the claim in the amount of $250,000 and have recorded a contingency loss in expectation of this settlement.

On October 18, 2010, there was a Statement of Claim filed against MMV. The claim named MMV as a defendant and a former equipment leasing vendor as a plaintiff. The plaintiff claimed that MMV breached a lease equipment contract. MMV’s management estimates that they can settle the claim in the amount of $17,000 and have recorded a contingency loss in expectation of the settlement.

| (11) |

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

None.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Trading Market for Common Equity

Our common stock is quoted on the Electronic Bulletin Board under the symbol, EFLS.OB. Trading in the common stock in the over-the-counter market has been limited and sporadic and the quotations set forth below are not necessarily indicative of actual market conditions. Further, these prices reflect inter-dealer prices without retail mark-up, mark-down, or commission, and may not necessarily reflect actual transactions. The following tables set forth the high and low sale prices for our common stock as reported on the Electronic Bulletin Board for the periods indicated.

| Interim Period | Low | High | ||

| Interim Period ended March 31, 2011 | $ | .13 | $ | .13 |

| Fiscal 2010 | ||||

| Quarter ended March 31, 2010 | $ | .025 | $ | .025 |

| Quarter ended June 30, 2010 | $ | .02 | $ | .02 |

| Quarter ended September 30, 2010 | $ | .01 | $ | .01 |

| Quarter ended December 31, 2010 | $ | .02 | $ | .02 |

| Fiscal 2009 | ||||

| Quarter ended March 31, 2009 | $ | .12 | $ | .12 |

| Quarter ended June 30, 2009 | $ | .17 | $ | .17 |

| Quarter ended September 30, 2009 | $ | .085 | $ | .085 |

| Quarter ended December 31, 2009 | $ | .15 | $ | .15 |

Dividends

We have never paid a cash dividend on our common stock. The payment of dividends may be made at the discretion of our Board of Directors, and will depend upon, among other things, our operations, capital requirements, and overall financial condition. There are no contractual restrictions on our ability to declare and pay dividends.

Preferred Stock

We currently have zero shares of preferred stock outstanding.

Number of Holders

As of April 15, 2011, we had 59 active common shareholders of record.

Securities Authorized for Issuance Under Equity Compensation Plans

As of the date of this Report, we have not authorized any equity compensation plan, nor has our Board of Directors authorized the reservation or issuance of any securities under any equity compensation plan.

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

On February 10, 2011, the Company entered into a Plan of Exchange agreement with MediaMatic Ventures Inc., a privately-held company incorporated under the laws of the Province of Alberta, Canada (“MMV”), and the shareholders of MMV (the “MMV Shareholders”). Pursuant to the agreement, on February 11, 2011 we purchased all 15,685,692 of the issued and outstanding common shares of MMV from the MMV Shareholders in exchange for issuing 28,000,000 shares of our common stock to the MMV Shareholders. MMV and MMV Shareholders represented that on the date of the agreement MMV had total assets of at least $3,200,000 and liabilities of not greater than $850,000 (excluding contingent liabilities).

At the closing, we also issued 3,980,000 shares of our common stock to one person who had provided advice in connection with the transaction, 2,737,867 shares of our common stock to each of two persons who assumed responsibility for paying certain of our obligations as required by the exchange agreement and who had provided advice in connection with the transaction, and 876,946 shares to Adam Slazer for his assistance in connection with the transaction. As a result, we issued an aggregate of 38,332,680 shares of our common stock, all of which are restricted securities.

Purchases of Equity Securities by the Small Business Issuer and Affiliated Purchasers

None.

Transfer Agent

Our transfer agent is Guardian Registrar & Transfer, Inc. located at 7951 SW 6th Street, Suite 216, Plantation, Florida 33324.

| (12) |

ITEM 6. SELECTED FINANCIAL DATA

If the registrant qualifies as a smaller reporting company as defined by Rule 229.10(f)(1), it is not required to provide the information required by this Item.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OR PLAN OF OPERATION

Forward Looking Statements

Certain statements in this report, including statements of our expectations, intentions, plans and beliefs, including those contained in or implied by "Management's Discussion and Analysis" and the Notes to Consolidated Financial Statements, are "forward-looking statements", within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), that are subject to certain events, risks and uncertainties that may be outside our control. The words “believe”, “expect”, “anticipate”, “optimistic”, “intend”, “will”, and similar expressions identify forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. We undertake no obligation to update or revise any forward-looking statements. These forward-looking statements include statements of management's plans and objectives for our future operations and statements of future economic performance, information regarding our expansion and possible results from expansion, our expected growth, our capital budget and future capital requirements, the availability of funds and our ability to meet future capital needs, the realization of our deferred tax assets, and the assumptions described in this report underlying such forward-looking statements. Actual results and developments could differ materially from those expressed in or implied by such statements due to a number of factors, including, without limitation, those described in the context of such forward-looking statements, our expansion strategy, our ability to achieve operating efficiencies, our dependence on distributors, capacity, suppliers, industry pricing and industry trends, evolving industry standards, domestic and international regulatory matters, general economic and business conditions, the strength and financial resources of our competitors, our ability to find and retain skilled personnel, the political and economic climate in which we conduct operations and the risk factors described from time to time in our other documents and reports filed with the Securities and Exchange Commission (the "Commission"). Additional factors that could cause actual results to differ materially from the forward-looking statements include, but are not limited to: 1) our ability to successfully develop and deliver our product; 2) our ability to compete effectively with other companies in the same industry; 3) our ability to raise sufficient capital in order to effectuate our business plan; and 4) our ability to retain our key executive.

Critical Accounting Policies And Estimates

The preparation of our financial statements requires us to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reported period. A critical accounting policy is one that is both very important to the portrayal of our financial condition and results, and requires management’s most difficult, subjective or complex judgments. Typically, the circumstances that make these judgments difficult, subjective and/or complex have to do with the need to make estimates about the effect of matters that are inherently uncertain.

RECENT ACCOUNTING PRONOUNCEMENTS

| (13) |

FASB Accounting Standards Codification

(Accounting Standards Update (“ASU”) 2009-01)

In June 2009, FASB approved the FASB Accounting Standards Codification (“the Codification”) as the single source of authoritative nongovernmental GAAP. All existing accounting standard documents, such as FASB, American Institute of Certified Public Accountants, Emerging Issues Task Force and other related literature, excluding guidance from the Securities and Exchange Commission (“SEC”), have been superseded by the Codification. All other non-grandfathered, non-SEC accounting literature not included in the Codification has become nonauthoritative. The Codification did not change GAAP, but instead introduced a new structure that combines all authoritative standards into a comprehensive, topically organized online database. The Codification is effective for interim or annual periods ending after September 15, 2009, and impacts the Company’s consolidated financial statements as all future references to authoritative accounting literature will be referenced in accordance with the Codification. There have been no changes to the content of the Company’s financial statements or disclosures as a result of implementing the Codification during the fiscal year ended December 31, 2009.

As a result of the Company’s implementation of the Codification during the fiscal year ended December 31, 2009, previous references to new accounting standards and literature are no longer applicable. In the current annual consolidated financial statements, the Company will provide reference to both new and old guidance to assist in understanding the impacts of recently adopted accounting literature, particularly for guidance adopted since the beginning of the current fiscal year but prior to the Codification.

Subsequent Events

(Included in Accounting Standards Codification (“ASC”) 855 “Subsequent Events”, previously SFAS No. 165 “Subsequent Events”)

SFAS No. 165 established general standards of accounting for and disclosure of events that occur after the balance sheet date, but before the consolidated financial statements are issued or available to be issued (“subsequent events”). An entity is required to disclose the date through which subsequent events have been evaluated and the basis for that date. For public entities, this is the date the consolidated financial statements are issued. SFAS No. 165 does not apply to subsequent events or transactions that are within the scope of other GAAP and did not result in significant changes in the subsequent events reported by the Company. SFAS No. 165 became effective for interim or annual periods ending after June 15, 2009 and did not impact the Company’s consolidated financial statements. The Company evaluated for subsequent events through the issuance date of the Company’s consolidated financial statements. No recognized or non-recognized subsequent events were noted.

Determination of the Useful Life of Intangible Assets

(Included in ASC 350 “Intangibles — Goodwill and Other”, previously FSP SFAS No. 142-3 “Determination of the Useful Lives of Intangible Assets”)

FSP SFAS No. 142-3 amended the factors that should be considered in developing renewal or extension assumptions used to determine the useful life of a recognized intangible asset under previously issued goodwill and intangible assets topics. This change was intended to improve the consistency between the useful life of a recognized intangible asset and the period of expected cash flows used to measure the fair value of the asset under topics related to business combinations and other GAAP. The requirement for determining useful lives must be applied prospectively to intangible assets acquired after the effective date and the disclosure requirements must be applied prospectively to all intangible assets recognized as of, and subsequent to, the effective date. FSP SFAS No. 142-3 became effective for consolidated financial statements issued for fiscal years beginning after December 15, 2008, and interim periods within those fiscal years. The adoption of FSP SFAS No. 142-3 did not impact the Company’s consolidated financial statements.

Noncontrolling Interests

(Included in ASC 810 “Consolidation”, previously SFAS No. 160 “Noncontrolling Interests in Consolidated Financial Statements an amendment of ARB No. 51”)

SFAS No. 160 changed the accounting and reporting for minority interests such that they will be recharacterized as noncontrolling interests and classified as a component of equity. SFAS No. 160 became effective for fiscal years beginning after December 15, 2008 with early application prohibited. The Company implemented SFAS No. 160 at the start of fiscal 2009 and no longer records an intangible asset when the purchase price of a noncontrolling interest exceeds the book value at the time of buyout. The adoption of SFAS No. 160 did not have any other material impact on the Company’s financial statements.

| (14) |

Consolidation of Variable Interest Entities — Amended

(To be included in ASC 810 “Consolidation”, SFAS No. 167 “Amendments to FASB Interpretation No. 46(R)”)

SFAS No. 167 amends FASB Interpretation No. 46(R) “Consolidation of Variable Interest Entities regarding certain guidance for determining whether an entity is a variable interest entity and modifies the methods allowed for determining the primary beneficiary of a variable interest entity. The amendments include: (1) the elimination of the exemption for qualifying special purpose entities, (2) a new approach for determining who should consolidate a variable-interest entity, and (3) changes to when it is necessary to reassess who should consolidate a variable-interest entity. SFAS No. 167 is effective for the first annual reporting period beginning after November 15, 2009, with earlier adoption prohibited. The Company will adopt SFAS No. 167 in fiscal 2010 and does not anticipate any material impact on the Company’s financial statements.

Off-Balance Sheet Arrangements

We have not entered into any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources and would be considered material to investors. Certain officers and directors of the Company have provided personal guarantees to our various lenders as required for the extension of credit to the Company.

Accounting Policies Subject to Estimation and Judgment

Management’s Discussion and Analysis of Financial Condition and Results of Operations are based upon our financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States. When preparing our financial statements, we make estimates and judgments that affect the reported amounts on our balance sheets and income statements, and our related disclosure about contingent assets and liabilities. We continually evaluate our estimates, including those related to revenue, allowance for doubtful accounts, reserves for income taxes, and litigation. We base our estimates on historical experience and on various other assumptions, which we believe to be reasonable in order to form the basis for making judgments about the carrying values of assets and liabilities that are not readily ascertained from other sources. Actual results may deviate from these estimates if alternative assumptions or condition are used

RESULTS OF OPERATIONS FOR THE YEARS ENDED DECEMBER 31, 2010 AND 2009

Revenues

The Company had revenues of $47,808 for the year ended December 31, 2010 compared to revenues of $45,666 during the year ended December 31, 2009. The revenues in both years of 2010 and 2009 were due to our previous business in connection with personal fitness training in and around the Lake Norman area of Charlotte, North Carolina.

Since the consummation of share exchange with MMV, we have adopted the business of MMV, which is the provider of multimedia kiosks throughout Canada. We expected our sales in 2011 would significantly increase resulting from product rentals and franchise sales.

Cost of Sales

Cost of revenue for the years ended December 31, 2010 and 2009 primarily includes supplement costs, weight loss products, maintaining equipment, and purchasing new equipment, which was $9,648 and $9,215, respectively. The cost of revenues as a percentage of revenues was 20.2% for both 2010 and 2009.

We expected our cost of revenues in 2011 would be in connection with amortization of DVD purchases because the business would be changed from personal fitness training to multimedia rental.

Operating Expenses

The Company had operating expenses of $80,512 and $64,788 for the years ended December 31, 2010 and 2009, respectively, including the expenses incurred for remaining a public company accounts.

We expected our operating expenses would significantly increase in 2011 resulting from the multimedia rental business.

| (15) |

Income/Losses

We had a net loss of $44,277 and $28,337 for the years ended December 31, 2010 and 2009, respectively. The net losses in both 2010 and 2009 were due primarily to gross profits not sufficient to cover operational expenses, which were $80,512 and $64,788 for the years ended December 31, 2010 and 2009, respectively.

We expected we would be profitable resulting from the multimedia rental business. However, there can be no assurance that we will achieve or maintain profitability, or that any revenue growth will take place in the future.

Impact of Inflation

We believe that inflation has had a negligible effect on operations since inception. We believe that we can offset inflationary increases in the cost of operations by increasing sales and improving operating efficiencies.

Liquidity And Capital Resources

Net cash flows used in operating activities were $3,769 for the year ended December 31, 2010, compared to net cash flows of $3,023 provided by operating activities for the year ended December 31, 2009. Negative cash flows in 2010 were primarily attributable to net loss of $44,277, offset by non-cash expenses such as depreciation of $2,751 and common stock issued for services of $25,000, plus the increase in accounts payable in amount of $10,832. Positive cash flows in 2009 were due primarily to the increase in accounts payable in the amount of $28,609, partially offset by the net loss of $28,337.

During the year ended December 31, 2010, the Company issued 25,000 restricted common shares to an unrelated service provider in exchange for web design, hosting services, annual web site content updates, annual domain name registration and an online marketing program rendered during such year pursuant to a private placement made under Regulation 504. These shares were priced at the private placement price of $1 per share which approximated the fair value of the services rendered. The Company recorded $25,000 in non-cash consulting expense in the accompanying statements of operations during the year ended December 31, 2010 for these shares.

There were no cash flows from investing activities for the years ended December 31, 2010 and 2009.

There were no cash flows from financing activities for the years ended December 31, 2010 and 2009.

We had $1,149 cash as of December 31, 2010. On the short-term basis, we will be required to raise a significant amount of additional funds over the next 12 months to sustain operations. On the long-term basis, we will potentially need to raise capital to grow and develop our business.

It is likely that we will require significant additional financing within the next 12 months and if we are unable to raise the needed funds on an acceptable basis, we may be forced to cease operations.

Going Concern

As shown in the accompanying consolidated financial statements, we have suffered recurring losses from operation to date. We have a retained deficiency of $243,327 as of December 31, 2010. These factors raise substantial doubt about our ability to continue as a going concern.

Due to business worsening, a poor economic climate and cash at low levels, management has elected to search for acquisition candidates to enhance value to its shareholders.

| (16) |

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not applicable.

ITEM 8. FINANCIAL STATEMENTS

The report of the independent Registered Public Accounting Firm appears on page 22 and financial statements and notes to financial statements appear on page 23-37.

| (17) |

--------

CONSOLIDATED FINANCIAL STATEMENTS

EXERCISE FOR LIFE SYSTEMS, INC.

December 31, 2010

--------

| (18) |

CONTENTS

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM 20

CONSOLIDATED BALANCE SHEETS 21

CONSOLIDATED STATEMENTS OF OPERATIONS 22

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY (DEFICIT) 23

CONSOLIDATED STATEMENTS OF CASH FLOWS 24

NOTES TO FINANCIAL STATEMENTS 25 - 31

| (19) |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors:

Exercise For Life Systems, Inc.

We have audited the consolidated balance sheets of Exercise For Life Systems, Inc. as of December 31, 2010 and 2009, and the related consolidated statements of operations, stockholders’ equity (deficit), and cash flows for the years then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Exercise for Life Systems, Inc. as of December 31, 2010 and 2009, and the results of its consolidated operations and its cash flows for the years then ended in conformity with U.S. generally accepted accounting principles.

The accompanying financial statements have been prepared assuming the Company will continue as a going concern. The Company has suffered a loss in 2010 and in 2009, has negative working capital, and generated a negative internal cash flow from operations in 2010 that raises substantial doubt about its ability to continue as a going concern. Management’s plans in regard to these matters are described in Note 7. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Silberstein Ungar, PLLC

Bingham Farms, Michigan

April 13, 2011

| (20) |

| EXERCISE FOR LIFE SYSTEMS, INC. | ||||||||

| CONSOLIDATED BALANCE SHEETS | ||||||||

| AS OF DECEMBER 31, 2010 AND DECEMBER 31, 2009 | ||||||||

| ASSETS | 2010 | 2009 | ||||||

| (Restated) | ||||||||

| CURRENT ASSETS: | ||||||||

| Cash | $ | 1,149 | $ | 4,918 | ||||

| TOTAL CURRENT ASSETS | 1,149 | 4,918 | ||||||

| FIXED ASSETS: | ||||||||

| Machinery and equipment | 13,763 | 13,763 | ||||||

| Accumulated depreciation | (13,454 | ) | (10,703 | ) | ||||

| TOTAL FIXED ASSETS | 309 | 3,060 | ||||||

| TOTAL ASSETS | $ | 1,458 | $ | 7,978 | ||||

| LIABILITIES AND STOCKHOLDERS' EQUITY (DEFICIT) | ||||||||

| CURRENT LIABILITIES | ||||||||

| Accounts payable | $ | 43,154 | $ | 53,322 | ||||

| Accrued interest payable | 1,925 | — | ||||||

| Promissory note payable | 21,000 | — | ||||||

| TOTAL CURRENT LIABILITIES | 66,079 | 53,322 | ||||||

| STOCKHOLDERS' EQUITY (DEFICIT) | ||||||||

| Common stock ($.0001 par value, 100,000,000 shares authorized; 11,552,050 and 11,527,050 shares issued and outstanding at December 31, 2010 and December 31, 2009, respectively) | 1,155 | 1,153 | ||||||

| Additional paid in capital | 177,551 | 152,553 | ||||||

| Accumulated deficit | (243,327 | ) | (199,050 | ) | ||||

| TOTAL STOCKHOLDERS' EQUITY (DEFICIT) | (64,621 | ) | (45,344 | ) | ||||

| TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY (DEFICIT) | $ | 1,458 | $ | 7,978 | ||||

The accompanying notes are an integral part of these financial statements

| (21) |

| EXERCISE FOR LIFE SYSTEMS, INC. | ||||||||

| CONSOLIDATED STATEMENTS OF OPERATIONS | ||||||||

| FOR THE YEARS ENDED DECEMBER 31, 2010 AND 2009 | ||||||||

| For The Year | ||||||||

| Ended December 31, | ||||||||

| 2010 | 2009 | |||||||

| Restated | ||||||||

| REVENUES: | ||||||||

| Sales | $ | 47,808 | $ | 45,666 | ||||

| Cost of sales | (9,648 | ) | (9,215 | ) | ||||

| Gross profit | 38,160 | 36,451 | ||||||

| EXPENSES: | ||||||||

| Selling, general and administrative expenses | 80,512 | 64,788 | ||||||

| Total expenses | 80,512 | 64,788 | ||||||

| (Loss) from operations | $ | (42,352 | ) | $ | (28,337 | ) | ||

| Interest expense | (1,925 | ) | — | |||||

| Loss before income taxes | (44,277 | ) | (28,337 | ) | ||||

| Provision for income taxes | — | — | ||||||

| NET (LOSS) | $ | (44,277 | ) | $ | (28,337 | ) | ||

| Basic and fully diluted net (loss) per common share: | $ | * | $ | * | ||||

| Weighted average common shares outstanding | 11,551,776 | 11,527,050 | ||||||

| * less than $.01 per share | ||||||||

| The accompanying notes are an integral part of these financial statements | ||||||||

| (22) |

| EXERCISE FOR LIFE SYSTEMS, INC. | |||||

| CONSOLIDATED STATEMENT OF STOCKHOLDERS' EQUITY | |||||

| FOR THE YEARS ENDED DECEMBER 31, 2010 AND 2009 | |||||

| Total | ||||||||||||||||||||

| Additional | Accumulated | Stockholders' | ||||||||||||||||||

| Common Stock | Paid-in | Deficit | Equity (Deficit) | |||||||||||||||||

| Shares | Amount | Capital | (Restated) | (Restated) | ||||||||||||||||

| Balances, December 31, 2008 | 11,527,050 | $ | 1,153 | $ | 152,553 | $ | (170,713 | ) | $ | (17,007 | ) | |||||||||

| Net loss for the year ended December 31, 2009 | — | — | — | (28,337 | ) | (28,337 | ) | |||||||||||||

| Balances, December 31, 2009 | 11,527,050 | $ | 1,153 | $ | 152,553 | $ | (199,050 | ) | $ | (45,344 | ) | |||||||||

| Common stock issued for services rendered | 25,000 | 2 | 24,998 | — | 25,000 | |||||||||||||||

| Net loss for the year ended December 31, 2010 | — | — | — | (44,277 | ) | (44,277 | ) | |||||||||||||

| Balances, December 31, 2010 | 11,552,050 | $ | 1,155 | $ | 177,551 | $ | (243,327 | ) | $ | (64,621 | ) | |||||||||

| The accompanying notes are an integral part of these financial statements | ||||||||||||||||||||

| (23) |

| EXERCISE FOR LIFE SYSTEMS, INC. | ||||||||

| CONSOLIDATED STATEMENTS OF CASH FLOWS | ||||||||

| FOR THE YEARS ENDED DECEMBER 31, 2010 AND 2009 | ||||||||

| 2010 | 2009 | |||||||

| Restated | ||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net (loss) | $ | (44,277 | ) | $ | (28,337 | ) | ||

| Adjustments to reconcile net (loss) to net cash provided by (used in) operations: | ||||||||

| Depreciation | 2,751 | 2,751 | ||||||

| Common stock issued for services rendered and expensed | 25,000 | — | ||||||

| Increase in operating liabilities: | ||||||||

| Accounts payable | 10,832 | 28,609 | ||||||

| Accrued interest payable | 1,925 | — | ||||||

| NET CASH PROVIDED BY (USED IN) OPERATING ACTIVITIES | (3,769 | ) | 3,023 | |||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Proceeds from sale of common stock to investors | — | — | ||||||

| NET CASH PROVIDED BY OPERATING ACTIVITIES | — | — | ||||||

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | (3,769 | ) | 3,023 | |||||

| CASH AND CASH EQUIVALENTS, | ||||||||

| BEGINNING OF THE YEAR | 4,918 | 1,895 | ||||||

| END OF THE YEAR | $ | 1,149 | $ | 4,918 | ||||

| OTHER NON-CASH FINANCING ACTIVITIES: | ||||||||

| Conversion of accounts payable into notes payable | $ | 21,000 | $ | — | ||||

The accompanying notes are an integral part of these financial statements

| (24) |

EXERCISE FOR LIFE SYSTEMS, INC.

NOTES TO FINANCIAL STATEMENTS

For the Years Ended December 31, 2010 and 2009

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Business Activity

Exercise For Life Systems, Inc., (the “Company”) offers personal fitness training services and products and is located in the Charlotte, North Carolina area. The Company was incorporated in New Jersey in 1996 as A.J. Glaser, Inc. and later incorporated in North Carolina in 2006 also as A.J. Glaser, Inc. (“A. J. Glaser”) On June 9, 2008, the Company filed an amendment to the Articles of Incorporation with the Secretary of State of North Carolina to change its corporate name to Exercise For Life Systems, Inc. (FKA A.J. Glaser, Inc.). This amendment also changed the par value of the common stock from $1 per share to $.0001 per share and increased the authorized common shares from 100 shares to 100,000,000 shares.

In September 2008, the Company (legal acquirer) executed a Plan of Exchange with A.J. Glaser (accounting acquirer), whereby we exchanged 100 shares of our common stock for all of the issued and outstanding shares of A.J.Glaser, Inc. As a result, A.J.Glaser became the wholly-owned subsidiary of the Company.

The above mentioned stock exchange transaction has been accounted for as a reverse acquisition and recapitalization of the Company whereby the New Jersey corporation is deemed to be the accounting acquirer (legal acquiree) and the North Carolina corporation to be the accounting acquiree (legal acquirer). The accompanying consolidated financial statements are in substance those of the New Jersey corporation, with the assets and liabilities, and revenues and expenses, of the North Carolina corporation being included effective from the date of stock exchange transaction. The North Carolina corporation is deemed to be a continuation of the business of the New Jersey corporation. Accordingly, the accompanying consolidated financial statements include the following:

(1) The balance sheet consists of the net assets of the accounting acquirer at historical cost and the net assets of the accounting acquiree at historical cost

(2) the financial position, results of operations, and cash flows of the acquirer for all periods presented as if the recapitalization had occurred at the beginning of the earliest period presented and the operations of the accounting acquiree from the date of stock exchange transaction.

Basis of Presentation

The financial statements include the accounts of Exercise For Life Systems, Inc. under the accrual basis of accounting.

Management’s Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates. The financial statements above reflect all of the costs of doing business.

Income Taxes

The Company accounts for income taxes under Section 740-10-30 of the FASB Accounting Standards Codification. Deferred income tax assets and liabilities are determined based upon differences between the financial reporting and tax bases of assets and liabilities and are measured using the enacted tax rates and laws that will be in effect when the differences are expected to reverse. Deferred tax assets are reduced by a valuation allowance to the extent management concludes it is more likely than not that the assets will not be realized. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the statements of operations in the period that includes the enactment date.

Fair Value of Financial Instruments

The Company’s financial instruments are cash, accrued interest payable, promissory note payable, and accounts payable. The recorded values of cash and payables approximate their fair values based on their short-term nature.

Comprehensive Income (Loss) - The Company reports comprehensive income and its components following guidance set forth by section 220-10 of the FASB Accounting Standards Codification which establishes standards for the reporting and display of comprehensive income and its components in the consolidated financial statements. There were no items of comprehensive income (loss) applicable to the Company during the period covered in the financial statements.

Loss Per Share - Net loss per common share is computed pursuant to section 260-10-45 of the FASB Accounting Standards Codification. Basic net loss per share is computed by dividing net loss by the weighted average number of shares of common stock outstanding during the period. Diluted net loss per share is computed by dividing net loss by the weighted average number of shares of common stock and potentially outstanding shares of common stock during each period. There were no potentially dilutive shares outstanding as of December 31, 2010 and 2009.

Long-Lived Assets - The Company evaluates the recoverability of its fixed assets and other assets in accordance with section 360-10-15 of the FASB Accounting Standards Codification for disclosures about Impairment or Disposal of Long-Lived Assets. Disclosure requires recognition of impairment of long-lived assets in the event the net book value of such assets exceeds its expected cash flows. If so, it is considered to be impaired and is written down to fair value, which is determined based on either discounted future cash flows or appraised values. The Company adopted the statement on inception. No impairments of these types of assets were recognized during the years ended December 31, 2010 and 2009.

| (25) |

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT.)

Property and Equipment - Property and equipment is stated at cost. Depreciation is provided by the straight-line method over the estimated economic life of the property and equipment remaining from five to seven years.

When assets are sold or retired, their costs and accumulated deprecation are eliminated from the accounts and any gain or loss resulting from their disposal is included in the statement of operations.

The Company recognizes an impairment loss on property and equipment when evidence, such as the sum of expected future cash flows (undiscounted and without interest charges), indicates that future operations will not produce sufficient revenue to cover the related future costs, including depreciation, and when the carrying amount of the asset cannot be realized through sale. Measurement of the impairment loss is based on the fair value of the assets.

Revenue Recognition – Revenue is recognized when fitness training services are completed provided collection from the client of the resulting receivable is probable. Revenue from product sales is recognized when the products are shipped.

Risk and Uncertainties - The Company is subject to risks common to companies in the service industry, including, but not limited to, litigation, development of new technological innovations and dependence on key personnel.

Cash and Cash Equivalents - For purposes of the Statements of Cash Flows, the Company considers highly liquid investments with an original maturity of three months or less to be cash equivalents.

Share-Based Payments - The Company accounts for stock-based compensation using the fair value method following the guidance set forth in section 718-10 of the FASB Accounting Standards Codification for disclosure about Stock-Based Compensation. This section requires a public entity to measure the cost of employee services received in exchange for an award of equity instruments based on the grant-date fair value of the award (with limited exceptions). That cost will be recognized over the period during which an employee is required to provide service in exchange for the award- the requisite service period (usually the vesting period). No compensation cost is recognized for equity instruments for which employees do not render the requisite service.

Advertising Costs - Advertising costs are expensed as incurred. The Company does not incur any direct-response advertising costs.

Recent Accounting Pronouncements - The Company has reviewed all recently issued, but not yet effective, accounting pronouncements and do not believe the future adoption of any such pronouncements may be expected to cause a material impact on its financial condition or the results of its operations.

FASB Accounting Standards Codification

(Accounting Standards Update (“ASU”) 2009-01)

In June 2009, FASB approved the FASB Accounting Standards Codification (“the Codification”) as the single source of authoritative nongovernmental GAAP. All existing accounting standard documents, such as FASB, American Institute of Certified Public Accountants, Emerging Issues Task Force and other related literature, excluding guidance from the Securities and Exchange Commission (“SEC”), have been superseded by the Codification. All other non-grandfathered, non-SEC accounting literature not included in the Codification has become nonauthoritative. The Codification did not change GAAP, but instead introduced a new structure that combines all authoritative standards into a comprehensive, topically organized online database. The Codification is effective for interim or annual periods ending after September 15, 2009, and impacts the Company’s consolidated financial statements as all future references to authoritative accounting literature will be referenced in accordance with the Codification. There have been no changes to the content of the Company’s financial statements or disclosures as a result of implementing the Codification during the fiscal year ended December 31, 2009.

As a result of the Company’s implementation of the Codification during the fiscal year ended December 31, 2009, previous references to new accounting standards and literature are no longer applicable. In the current annual consolidated financial statements, the Company will provide reference to both new and old guidance to assist in understanding the impacts of recently adopted accounting literature, particularly for guidance adopted since the beginning of the current fiscal year but prior to the Codification.

Subsequent Events

(Included in Accounting Standards Codification (“ASC”) 855 “Subsequent Events”, previously SFAS No. 165 “Subsequent Events”)

SFAS No. 165 established general standards of accounting for and disclosure of events that occur after the balance sheet date, but before the consolidated financial statements are issued or available to be issued (“subsequent events”). An entity is required to disclose the date through which subsequent events have been evaluated and the basis for that date. For public entities, this is the date the consolidated financial statements are issued. SFAS No. 165 does not apply to subsequent events or transactions that are within the scope of other GAAP and did not result in significant changes in the subsequent events reported by the Company. SFAS No. 165 became effective for interim or annual periods ending after June 15, 2009 and did not impact the Company’s consolidated financial statements.

Determination of the Useful Life of Intangible Assets

(Included in ASC 350 “Intangibles — Goodwill and Other”, previously FSP SFAS No. 142-3 “Determination of the Useful Lives of Intangible Assets”)

| (26) |