Attached files

| file | filename |

|---|---|

| EX-21.1 - LIST OF SUBSIDIARIES - MAVERICK MINERALS CORP | exhibit21-1.htm |

| EX-32.1 - CERTIFICATION - MAVERICK MINERALS CORP | exhibit32-1.htm |

| EX-31.1 - CERTIFICATION - MAVERICK MINERALS CORP | exhibit31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______________ to______________

Commission file number 000-25515

MAVERICK MINERALS

CORPORATION

(Exact name of registrant as specified in

its charter)

| Nevada | 88-0410480 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 2501 Lansdowne Ave., | |

| Saskatoon, Saskatchewan, Canada | S7J 1H3 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code 306-343-5799

Securities registered under Section 12(b) of the Act:

| None | N/A |

| Title of each class | Name of each exchange on which registered |

Securities registered under Section 12(g) of the Act:

Common Stock, $0.001 par value

(Title of class)

Indicate by checkmark if the registrant is a well-known seasoned

issuer, as defined in Rule 405 of the Securities Act.

Yes [

] No [X]

Indicate by checkmark if the registrant is not required to file

reports pursuant to Section 13 or 15(d) of the Act.

Yes [

] No [X]

Indicate by checkmark whether the registrant has (1) filed all

reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days.

Yes [X]

No [ ]

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-T (§232.405 of this chapter) during the preceding 12 months (or for such

shorter period that the registrant was required to submit and post such files).

Yes [ ] No [ ]

Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by checkmark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | (Do not check if a smaller reporting | Accelerated filer [ ] |

| company) | ||

| Non-accelerated filer [ ] | Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell company

(as defined in Rule 12b-2 of the Act).

Yes [

] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $1,765,580.70 based on a price of $1.30 per share, being the average of the bid and asked price of the registrant’s common equity on June 30, 2010.

APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes [ ] No [ ] N/A

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. 12,152,617 issued and outstanding as of March 30, 2011.

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) any annual report to security holders; (2) any proxy or information statement; and (3) any prospectus filed pursuant to Rule 424(b) or (c) of the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980). Not Applicable

-2-

PART I

Forward Looking Statements.

This annual report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors” and the risks set out below, any of which may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. These risks include, by way of example and not in limitation:

- risks and uncertainties relating to the interpretation of drill results, the geology, grade and continuity of mineral deposits;

- results of initial feasibility, pre-feasibility and feasibility studies, and the possibility that future exploration, development or mining results will not be consistent with our expectations;

- mining and development risks, including risks related to accidents, equipment breakdowns, labour disputes or other unanticipated difficulties with or interruptions in production;

- the potential for delays in exploration or development activities or the completion of feasibility studies;

- risks related to the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses;

- risks related to commodity price fluctuations;

- the uncertainty of profitability based upon our history of losses;

- risks related to failure to obtain adequate financing on a timely basis and on acceptable terms for our planned exploration and development projects;

- risks related to environmental regulation and liability;

- risks that the amounts reserved or allocated for environmental compliance, reclamation, post- closure control measures, monitoring and on-going maintenance may not be sufficient to cover such costs;

- risks related to tax assessments;

- political and regulatory risks associated with mining development and exploration; and

- other risks and uncertainties related to our prospects, properties and business strategy.

This list is not an exhaustive list of the factors that may affect any of our forward-looking statements. These and other factors should be considered carefully and readers should not place undue reliance on our forward-looking statements.

Forward looking statements are made based on management’s beliefs, estimates and opinions on the date the statements are made and we undertake no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

Our financial statements are stated in United States dollars (US$) and are prepared in accordance with United States Generally Accepted Accounting Principles.

In this annual report, unless otherwise specified, all dollar amounts are expressed in United States dollars and all references to “common stock” refer to the shares of common stock in our capital stock.

-3-

As used in this annual report, the terms “we”, “us”, “our”, the “Company” and “Maverick” mean Maverick Minerals Corporation and our subsidiary, Eskota Energy Corporation, unless otherwise indicated.

ITEM 1. BUSINESS

Corporate History

We were incorporated in the State of Nevada on August 27, 1998 under the name “Pacific Cart Services Ltd.” Following our incorporation, we pursued opportunities in the business of franchising fast food distributor systems.

We were not successful in implementing our business plan as a fast food distributor systems business. As management of our company investigated opportunities and challenges in the business of being a fast food distributor systems company, management realized that the business did not present the best opportunity for our company to realize value for our shareholders. Accordingly, we abandoned our previous business plan.

On March 22, 2002, we changed our name to Maverick Minerals Corporation to reflect our change in focus to holding and developing mineral and resource projects. We are an exploration stage company that has not yet generated or realized any revenues from our business operations.

From November 2001 until February 2003, we held a 100% interest in the Silver, Lead, Zinc, Keno Hill mining camp in Yukon, Canada through our then subsidiary, Gretna Capital Corporation. Despite a tenure marked by historic maintenance cost reductions and extensive research into a new hydrometallurgical approach to production and environmental remediation at the mine site, the project endured through a period of low commodity prices. On January 1, 2003 we defaulted on a payment of Cdn$1,050,000 required under an agreement of purchase and sale for the acquisition of an interest in the project. Due to the default, the Company was divested of its claims by its creditors by way of court action which culminated on February 14, 2003.

On April 21, 2003 we closed a transaction, as set out in the Purchase Agreement with UCO Energy Corporation (“UCO”) to purchase the outstanding equity of UCO. To facilitate the transaction, we issued 3,758,040 common shares in exchange for all the issued and outstanding common shares of UCO. As a result of the transaction, the former shareholders of UCO held approximately 90% of the issued and outstanding common shares of Maverick. A net distribution of $944,889 was recoded in connection with the common stock of Maverick for the acquisition of UCO in respect of the Company’s net liabilities at the acquisition date. UCO was in the business of pursuing opportunities in the coal mining industry. From July 7, 2003 until March 5, 2004, we were engaged in the waste coal recovery business by way of a lease agreement at the Old Ben Mine near Sesser, Illinois. We extracted coal fines from holding ponds with a leased dredge and subsequently dried them in a fines plant and sold the dried product to an electrical utility. The operation was conducted in our wholly owned subsidiary UCO.

Effective March 5, 2004, we were in default of our lease agreement that granted access to the waste coal. Default was a function of equipment malfunction and equipment lease default. Extensive efforts to refinance our coal recovery activities were undertaken post default in an effort to return to production. These efforts proved unsuccessful. In April, 2004 Maverick instituted new management at the annual meeting of its wholly-owned subsidiary, UCO Energy Corp. Subsequent to these events, our subsidiary reached a settlement agreement with the lessor of the coal lands and the lessor of our dredging equipment. The settlement provided for a mutual release between our subsidiary and each lessor independently.

Maverick incorporated a wholly-owned subsidiary, Eskota Energy Corporation, Inc. (“Eskota”) a Texas company, in August, 2005. Eskota entered into an Assignment Agreement with Veneto Exploration LLC of Plano, Texas (“Veneto”) on August 18, 2005 pursuant to which we acquired certain petroleum and natural gas rights and leases, know as the S. Neill Unitized lease (the “Eskota Leases”) comprising a 75%+/- NRI and 100% working interest in approximately 6,000 acres in central Texas approximately 9 miles east of the town of Sweetwater, in exchange for a $1,400,000 note payable. An additional $375,000 cash was paid by the Company for the acquisition of the Eskota Leases.

-4-

Eskota was to receive all revenue rightfully owed under the above noted leases. Eskota agreed to contribute not less than $400,000 towards capital improvements on the said lease and equipment during the first twelve months after closing. The parties agreed to negotiate a reasonable covenant to ensure these expenditures were made. A note payable was signed on August 31, 2005 between Eskota and Veneto whereby Eskota promised to pay Veneto $700,000 before August 31, 2006, and $700,000 by May 31, 2007. In light of the above deadlines and the fact that the purchase price was predicated partially on down hole success from the initial re-works, management determined that it was not prudent to proceed with further investment on the property and that settlement discussions should begin with Veneto for a mutual release and return of the property and retirement of the promissory note of $1,400,000 issued by the Company. The effect of the initial failure to increase production from the first two attempts to restore the existing wells was reflected in an asset impairment charge taken by the Company of $419,959 on its fiscal year end financial statement dated December 31, 2005.

In June 2005, the Company cancelled 5,437,932 common shares, under an agreement with certain stockholders, which included the former stockholders of UCO, and two other stockholders including the CEO of the Company. The former stockholders of UCO surrendered the majority of the shares which was approximately 95% of the total common shares that they held at the time. As a result of the share cancellation, one single common stockholder emerged as the majority stockholder with approximately 76% of the total issued and outstanding common shares.

In December 2005, Veneto gave notice to Eskota and Eskota’s customers, to direct any cash payments relating to the Eskota Leases to Veneto directly as a result of non-payment of various payables by Eskota in relation to the Eskota Leases. As a result of this action, all revenues generated from the Eskota Leases were recognized by Veneto, and any expenses and obligations arising from the Eskota Leases after the notice was given, were assumed by Veneto. As a result, Eskota did not recognize revenue or operating expenses from the Eskota Leases during the year ended December 31, 2006.

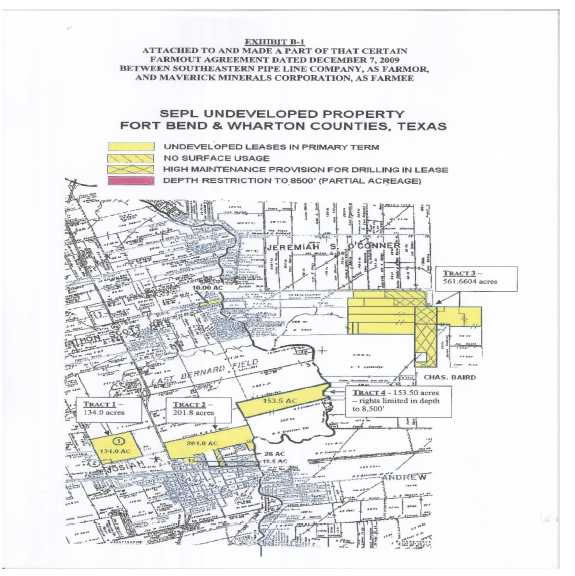

On December 14, 2009, we entered into a farm-out agreement (the “Farmout Agreement”) with Southeastern Pipe Line Company (“SEPL”) pursuant to which we acquired the right to earn an interest in certain oil and gas mineral leases located in Fort Bend and Wharton Counties, Texas (collectively, the “Leases”) and to the lands covered thereby. As a result of the closing of the Farmout agreement, our company ceased to be a shell company as defined in Rule 12b-2 of the United States Securities Exchange Act of 1934, as amended.

On July 27, 2010, we entered into a data purchase agreement with two individuals (collectively the “Vendors”), pursuant to which the Company agreed to purchase from the Vendors geologic data relating to certain oil and gas mineral leases located in Texas, including among other things: electric logs, seismic work, seismic reprocessing, data from the Texas Railroad Commission. In consideration for the acquisition of the geologic data from the Vendors the Company agreed to issue an aggregate of 350,000 shares of the common stock of the Company to the Vendors.

Recent Corporate Developments

Since the commencement of our fourth quarter ended December 31, 2010, we experienced the following significant corporate developments:

| 1. |

In October, 2010 we engaged a Texas based contractor to commence drill site construction in preparation for the drilling of the Company’s Initial Test Well in Fort Bend County, Texas which occured in December, 2010. The construction of location services included widening of an existing 2,000 foot access road and foundational re-enforcement with crushed limestone. In addition, contractors constructed the requisite drilling pad of approximately 1.5 acres in anticipation of rig mobilization. |

| 2. |

The Company entered into a letter agreement dated December 6, 2010 (the “Letter Agreement”) with an accredited investor (the “Purchaser”) pursuant to which the Purchaser and his nominee acquired a fifteen percent (15%) working interest in the Company’s initial test well being drilled in Fort Bend County, Texas having the permitted name of Lankford Trust No. 1 (the “Well”) for the sum of $500,000. In accordance with the terms of the Letter Agreement, the Company and the Purchaser concurrently entered into a joint operating agreement dated effective December 6, 2010 pursuant to which each party agreed to pay or deliver, or cause to be paid or delivered, all burdens and liabilities on its share of the production in regards to the Well, but not in excess of thirty percent (30%) and to indemnify, defend and hold the other party free from any liability therefore. As a condition of the Letter Agreement and joint operating agreement, the Purchaser and/or their nominees will be entitled to receive a 25% share from any proceeds of the Well until such time as their initial investment of $500,000 has been repaid after which time the distribution to the Purchaser reverts to 15% in accordance with their interest in the Well. |

-5-

| 3. |

Effective December 7, 2010, the Company entered into a joint operating agreement with Arrowdog, LLP (“Arrowdog”) pursuant to which Arrowdog acquired a three percent (3%) working interest in the Well for the sum of $150,000. Pursuant to the terms of the joint operating agreement each party agreed to pay or deliver, or cause to be paid or delivered, all burdens and liabilities on its share of the production in regards to the Well, but not in excess of thirty percent (30%) and to indemnify, defend and hold the other party free from any liability therefore. As a condition of the agreement Arrowdog will be carried for a 3% working interest to completion or P & A without further cost. Thereafter, Arrowdog will be responsible for their pro- rata share of expenses for maintenance and production with the Company. |

| 4. |

Effective December 21, 2010, the Company completed a private placement of 500,000 shares of its common stock at a price of $0.50 for gross proceeds of $250,000 to an offshore subscriber pursuant to Regulation S of the Securities Act of 1933. The shares were issued subsequent to year end. |

| 5. |

On January 22, 2011 Maverick successfully completed drilling its Initial Test Well to 13,500 on the Company's 4,513 acre Farm-Out property in Fort Bend County, Texas. The Initial Test Well was spud on December 9, 2010 and reached its targeted depth of 13,500 feet on day 44 of the drilling program. The Company’s independent log analyst and project engineer concurred at that time that the targeted Wilcox zones were not commercially productive, despite the presence of significant down hole pressure and strong natural gas shows during drilling. The target sands were very poorly developed and not suitable for a completion attempt. Accordingly, the decision was made to not set production casing and to look up hole for completion opportunities. The first completion attempt was a potential oil reservoir near 8,000’. The Yegua sand was indicated as potentially productive from open hole log analysis but proved to be non- productive after testing. The second completion attempt was made on a shallow Miocene zone. There had not been an open hole log across this interval but a significant gas show was seen on the mud log while drilling this interval. The zone was perforated and swab tested during the week of March 14-19, 2011 but yielded no significant gas. Maverick’s engineers have as of the date of this annual report completed plugging the Lankford Trust No. 1 pursuant to regulations of the Texas Railway Commission. Management’s intent is to conduct further work on log and seismic data in order to determine whether or not to abandon the Initial Test Well. As a result of test results showing that zones drilled were not commercially productive management determined that the direct costs capitalized in relation to the Initial Test Well were impaired. |

| 6. |

Effective February 28, 2011 the Company entered into debt settlement and subscription agreements with two subscribers pursuant to which the Company settled an aggregate of $50,000 debt in consideration of the issuance of 50,000 shares. The debt related to certain amounts owed to Art Brokerage Inc. that were assigned to third parties. The shares were issued to two U.S. Persons (as such term is defined in Regulation S of the Securities Act of 1933) who represented that they were each accredited investors as such term is defined in Rule 502 of Regulation D of the Securities Act of 1933. |

Our Current Business

We are currently an exploration stage company engaged in the acquisition, exploration, and development of prospective oil and gas properties. Our current business focus is to implement the terms of the Farmout Agreement pursuant to which we intend to earn an interest in certain oil and gas mineral leases located in Fort Bend and Wharton Counties, Texas owned by Southeastern Pipe Line Company (“SEPL”). Subject to receipt of additional financing our initial operations during the next quarter are to attempt a completion in the newly discovered oil targets and determining if the initial test well is viable. If the well is not viable, we intend to plug the well. Our 2010 drilling program targeted the Wilcox Trend, a vast depositional sand zone with a history of natural gas and condensate production. The Wilcox Trend is articulated into the upper, middle, and lower Wilcox.

-6-

In October, 2010 we engaged a Texas based contractor to commence drill site construction in preparation for the drilling of the Company’s Initial Test Well Fort Bend County, Texas in December, 2010. The construction of location services included widening of an existing 2,000 foot access road and foundational re-enforcement with crushed limestone. In addition, contractors constructed the requisite drilling pad of approximately 1.5 acres in anticipation of rig mobilization. On January 22, 2011 Maverick successfully completed drilling its Initial Test Well to 13,500 on the Company's 4,513 acre Farm-Out property in Fort Bend County, Texas. The initial test well was spud on December 9, 2010 and reached its targeted depth of 13,500 feet on day 44 of the drilling program. The Company’s independent log analyst and project engineer concurred at that time that the targeted Wilcox zones were not commercially productive, despite the presence of significant down hole pressure and strong natural gas shows during drilling. The target sands were very poorly developed and not suitable for a completion attempt. Accordingly, the decision was made to not set production casing and to look up hole for completion opportunities. The first completion attempt was a potential oil reservoir near 8,000’. The Yegua sand was indicated as potentially productive from open hole log analysis but proved to be non-productive after testing. The second completion attempt was made on a shallow Miocene zone. There had not been an open hole log across this interval but a significant gas show was seen on the mud log while drilling this interval. The zone was perforated and swab tested during the week of March 14-19, 2011 but yielded no significant gas. Maverick’s engineers have as of the date of this annual report completed plugging the Lankford Trust No. 1 pursuant to regulations of the Texas Railway Commission. Concurrent with our entry into the Farmout Agreement, we acquired from a consulting geologist, detailed proprietary geology on the property subject to the Farmout Agreement. The dataset includes seismic and geological interpretations of the underlying geology from historic data. In addition, we obtained access to log data from a well drilled to 12,200 feet in 2003 on the Farm-Out Acreage. Management’s intent is to conduct further work on log and seismic data in order to determine whether or not to abandon the Initial Test Well.

As a result of test results showing that zones drilled were not commercially productive management determined that the direct costs capitalized in relation to the Initial Test Well were impaired.

Management determined that costs relating to drilling and direct exploration and asset retirement obligation costs, plus 25% of all costs relating to the Farm-Out Acreage as a whole should be considered evaluated costs and thus be subject to amortization. Besides drilling, exploration and asset retirement obligation costs, which are directly related to the Initial Test Well, the Company also included 25% of all other costs relating to the Farm-Out Acreage as a whole in its impairment assessment on the basis that these costs were incurred in connection with the Farmout Agreement where it is previously disclosed (Note 3(iv)) that one of the conditions of the Farmout Agreement is the completion of the drilling of at least four wells and thus determined it appropriate to include 25% of these costs in the impairment assessment on the Initial Test Well. The costs were offset against the incidental revenue of $650,000 received from selling working interests relating to the Initial Test Well.

Farm-out Agreement with Southeastern Pipe Line Company

On December 14, 2009, we entered into a farmout agreement with Southeastern Pipe Line Company pursuant to which we acquired the right to earn an interest in certain oil and gas mineral leases located in Fort Bend and Wharton Counties and to the lands covered thereby (collectively, the “Leases”). The Farmout Agreement is subject to certain conditions, including the following:

| (i) |

Payment of a non-refundable fee of $350,000 to SEPL (the “Fee”), which fee has been paid; | |

| (ii) |

Commencement of continuous and actual drilling operations on an oil or gas well (the “Initial Test Well”) to an objective formation (as such term is defined in the agreement) on the undeveloped Leases on or prior to December 14, 2010 (the “Completion Date”) which condition has been met; | |

| (iii) |

Completion of drilling on every drillable tract of the undeveloped Leases prior to commencing drilling operations on the developed Leases; | |

| (iv) |

Completion of the drilling of at least four wells on the undeveloped acreage to the objective formation and commence commercial production on such wells within 120 days after completion of drilling with the option to pay $250,000 per well to opt out of the requirement to drill up to two of the four wells; | |

| (v) |

Upon earning the interest in the Leases, Maverick agrees to enter into a Joint Operating Agreement in the form of AAPL 610 Model Form 1989 with 2005 COPAS accounting procedure to govern operations by the parties on the Leases, and SEPL agrees to assign its 100% interest in the Leases to Maverick subject to reserving an overriding royalty interest equal to the difference between all the existing lease burdens of record in effect as of October 7, 2009 and 30%, thereby delivering to Maverick a 70% net royalty interest in the Leases; and |

-7-

| (vi) |

Maverick granting an option to SEPL pursuant to which SEPL, may, after all drilling and completion costs have been recovered by Maverick, back-in 25% of an eight-eighths working interest (subject to proportionate reduction if Maverick’s acreage covers less than the entirety of the mineral interest under the proration spacing unit drilled), on a well-by-well basis. |

Pursuant to the terms of the Farmout Agreement, provided we establish commercial production and meet the earning requirements for the Initial Test Well, we have an option to develop additional wells (“Subsequent Wells”) within one hundred and eighty days after the completion of the Initial Test Well which was completed on March 20, 2011, substitute Initial Test Well or a Subsequent Well. Also, pursuant to the terms of the agreement we agreed to indemnify SEPL and its affiliates from all claims arising from the drilling or operations of the Initial Test Well or any Subsequent Well.

Sale of 15% Working Interest in Lankford Trust No. 1 Well

The Company entered into a letter agreement dated December 6, 2010 (the “Letter Agreement”) with an accredited investor (the “Purchaser”) pursuant to which the Purchaser and his nominee acquired a fifteen percent (15%) working interest in the Company’s initial test well being drilled in Fort Bend County, Texas having the permitted name of Lankford Trust No. 1 (the “Well”) for the sum of $500,000.

In accordance with the terms of the Letter Agreement, the Company and the Purchaser concurrently entered into a joint operating agreement dated effective December 6, 2010 pursuant to which each party agreed to pay or deliver, or cause to be paid or delivered, all burdens and liabilities on its share of the production in regards to the Well, but not in excess of thirty percent (30%) and to indemnify, defend and hold the other party free from any liability therefore. As a condition of the Letter Agreement and joint operating agreement, the Purchaser and/or their nominees will be entitled to receive a 25% share from any proceeds of the Well until such time as their initial investment of $500,000 has been repaid after which time the distribution to the Purchaser reverts to 15% in accordance with their interest in the Well. The sale of the 15% working interest in the Well closed on December 21, 2010.

Sale of 3% Working Interest in Lankford Trust No. 1 Well

Effective December 7, 2010, the Company entered into a joint operating agreement with Arrowdog, LLP (“Arrowdog”) pursuant to which Arrowdog acquired a three percent (3%) working interest in the Well for the sum of $150,000. Pursuant to the terms of the joint operating agreement each party agreed to pay or deliver, or cause to be paid or delivered, all burdens and liabilities on its share of the production in regards to the Well, but not in excess of thirty percent (30%) and to indemnify, defend and hold the other party free from any liability therefore. As a condition of the agreement Arrowdog will be carried for a 3% working interest to completion or Plug and Abandon without further cost. Thereafter, Arrowdog will be responsible for their pro-rata share of expenses for maintenance and production with the Company.

Competition

We are an exploration stage company engaged in the acquisition of a prospective mineral or oil and gas properties. We compete with other natural resource exploration companies for financing and for the acquisition of new mineral properties. Many of the natural resource exploration companies with whom we compete have greater financial and technical resources than those available to us. Accordingly, these competitors may be able to spend greater amounts on acquisitions of mineral properties of merit, on exploration of their mineral properties and on development of their mineral properties. In addition, they may be able to afford more geological expertise in the targeting and exploration of mineral properties. This competition could result in competitors having mineral properties of greater quality and interest to prospective investors who may finance additional exploration and development. This competition could adversely impact on our ability to achieve the financing necessary for us to conduct further exploration of our mineral properties.

-8-

We also compete with other junior natural resource exploration companies for financing from a limited number of investors that are prepared to make investments in junior natural resource exploration companies. The presence of competing junior natural resource exploration companies may impact on our ability to raise additional capital in order to fund our exploration programs if investors are of the view that investments in competitors are more attractive based on the merit of the mineral properties under investigation and the price of the investment offered to investors.

We also compete with other junior and senior natural resource exploration companies for available resources, including, but not limited to, professional geologists, camp staff, helicopter or float planes, mineral exploration supplies and drill rigs.

Compliance with Government Regulation

Our business is subject to various federal, state and local laws and governmental regulations that may be changed from time to time in response to economic or political conditions. We are required to comply with the environmental guidelines and regulations established at the local levels for our field activities and access requirements on our permit lands and leases. Any development activities, when determined, will require, but not be limited to, detailed and comprehensive environmental impact assessments studies and approvals of local regulators.

Environmental legislation provides for restrictions and prohibitions on spills, releases or emissions of various substances produced in association with the mining and oil and gas industries which could result in environmental liability. A breach or violation of such legislation may result in the imposition of fines and penalties. In addition, certain types of operations require the submission and approval of environmental impact assessments. Environmental assessments are increasingly imposing higher standards, greater enforcement, fines and penalties for non-compliance. Environmental assessments of proposed projects carry a heightened degree of responsibility for companies, directors, officers and employees. The cost of compliance in respect of environmental regulation has the potential to reduce the profitability of any future revenues that our company may generate.

Employees

We have no employees other than Robert Kinloch, our president, chief executive officer, chief financial officer and our sole director and Donald Kinloch, our secretary and treasurer. We anticipate that we will be conducting most of our business through agreements with consultants and third parties. We do not have an employment agreement with any of our officers or our sole director.

ITEM 1A. RISK FACTORS

Our common shares are considered speculative. Prospective investors should consider carefully the risk factors set out below.

We are an exploration stage company implementing a new business plan.

We are an exploration stage company with only a limited operating history upon which to base an evaluation of our current business and future prospects, and we have just begun to implement our business plan. If we do discover oil or gas resources in commercially exploitable quantities on any of our properties, we will be required to expend substantial sums of money to establish the extent of the resource, develop processes to extract it and develop extraction and processing facilities and infrastructure. If we discover a major reserve, there can be no assurance that such a reserve will be large enough to justify commercial operations, nor can there be any assurance that we will be able to raise the funds required for development on a timely basis. If we cannot raise the necessary capital or complete the necessary facilities and infrastructure, our business may fail. There is no assurance that we will be able to drill an initial test well on the property subject to the Farmout Agreement within the timeline set out in the agreement or at all. Failure to do so will result in the loss of all our interest in the Farmout Agreement with SEPL.

-9-

We have had negative cash flows from operations and if we are not able to obtain further financing, our business operations may fail.

We had negative working capital of $1,262,665 as of December 31, 2010. We do not expect to generate any revenues for the foreseeable future. Accordingly, we will require additional funds, either from equity or debt financing, to maintain our daily operations and to develop any wells under the Farmout Agreement. Obtaining additional financing is subject to a number of factors, including market prices for oil and gas, investor acceptance of our interest pursuant to the Farmout Agreement, and investor sentiment. Financing, therefore, may not be available on acceptable terms, if at all. The most likely source of future funds presently available to us is through the sale of equity capital. Any sale of share capital, however, will result in dilution to existing shareholders. If we are unable to raise additional funds when required, we may be forced to delay our plan of operation and our entire business may fail.

We currently do not generate revenues, and as a result, we face a high risk of business failure.

The only interest in property we have is pursuant to the Farmout Agreement. From the date of our incorporation, we have primarily focused on the location and acquisition of mineral and oil and gas properties. We have not generated any revenues to date. In order to generate revenues, we will incur substantial expenses in the evaluation and development of the Initial Well. We therefore expect to incur significant losses into the foreseeable future. We recognize that if we are unable to generate significant revenues from our activities, our entire business may fail. There is no history upon which to base any assumption as to the likelihood that we will be successful in our plan of operation, and we can provide no assurance to investors that we will generate any operating revenues or achieve profitable operations.

Our independent auditors have expressed substantial doubt about our ability to continue as a going concern, which may hinder our ability to obtain future financing.

We incurred net loss of $5,300,187 and a net loss of $3,433,469 for the years ended December 31, 2010 and 2009, respectively. At December 31, 2010, we had an accumulated deficit of $10,536,274 and a negative working capital of $1,262,665.

These circumstances raise substantial doubt about our ability to continue as a going concern, as described in the explanatory paragraph to our independent auditors’ report on our consolidated financial statements for the year ended December 31, 2010. Although our consolidated financial statements raise substantial doubt about our ability to continue as a going concern, they do not reflect any adjustments that might result if we are unable to continue our business.

If we are required for any reason to repay our outstanding secured convertible debentures or any other indebtedness, we would be required to deplete our working capital, if available, or raise additional funds.

If we are required to repay the secured convertible debentures or any other indebtedness for any reason, we would be required to use our limited working capital and raise additional funds. If we are unable to repay the secured convertible debentures or any other indebtedness when required, we may be required to sell substantial assets of our company. In addition, the lenders could commence legal action against our company and foreclose on all of our assets to recover the amounts due. Any such sale or legal action would require our company to curtail or possibly cease our operations.

Market conditions or operation impediments may hinder our access to oil and gas markets or delay our potential production.

Our ability to develop the Farm Out Acreage depends in part upon the availability, proximity and capacity of pipelines, natural gas gathering systems and processing facilities. This dependence is heightened where this infrastructure is less developed. Therefore, even if drilling results are positive in certain areas of our oil and gas properties, a new gathering system may need to be built to handle the potential volume of oil and gas produced. We might be required to shut in wells, at least temporarily, for lack of a market or because of the inadequacy or unavailability of transportation facilities. If that were to occur, we would be unable to realize revenue from those wells until arrangements were made to deliver production to market.

-10-

Even if we are able to establish any oil or gas reserves on the Farm Out Acreage, our ability to produce and market oil and gas is affected and also may be harmed by:

-

inadequate pipeline transmission facilities or carrying capacity;

-

government regulation of natural gas and oil production;

-

government transportation, tax and energy policies;

-

changes in supply and demand; and

-

general economic conditions.

The potential profitability of oil and gas ventures depends upon factors beyond the control of our company.

The potential profitability of oil and gas properties is dependent upon many factors beyond our control. For instance, world prices and markets for oil and gas are unpredictable, highly volatile, potentially subject to governmental fixing, pegging, controls, or any combination of these and other factors, and respond to changes in domestic, international, political, social, and economic environments. Additionally, due to worldwide economic uncertainty, the availability and cost of funds for production and other expenses have become increasingly difficult, if not impossible, to project. These changes and events may materially affect our financial performance.

Adverse weather conditions can also hinder drilling operations. A productive well may become uneconomic in the event water or other deleterious substances are encountered which impair or prevent the production of oil and/or gas from the well. In addition, production from any well may be unmarketable if it is impregnated with water or other deleterious substances. The marketability of oil and gas, which may be acquired or discovered, will be affected by numerous factors beyond our control. These factors include the proximity and capacity of oil and gas pipelines and processing equipment, market fluctuations of prices, taxes, royalties, land tenure, allowable production and environmental protection. These factors cannot be accurately predicted and the combination of these factors may result in our company not receiving an adequate return on invested capital.

Oil and gas operations are subject to comprehensive regulation, which may cause substantial delays or require capital outlays in excess of those anticipated causing an adverse effect on our company.

Oil and gas operations are subject to federal, state, and local laws relating to the protection of the environment, including laws regulating removal of natural resources from the ground and the discharge of materials into the environment. Oil and gas operations are also subject to federal, state, and local laws and regulations, which seek to maintain health and safety standards by regulating the design and use of drilling methods and equipment. Various permits from government bodies are required for drilling operations to be conducted; no assurance can be given that such permits will be received. Environmental standards imposed by federal, provincial, or local authorities may be changed and any such changes may have material adverse effects on our activities. Moreover, compliance with such laws may cause substantial delays or require capital outlays in excess of those anticipated, thus causing an adverse effect on us. Additionally, we may be subject to liability for pollution or other environmental damages, which it may elect not to insure against due to prohibitive premium costs and other reasons. To date we have not been required to spend any material amount on compliance with environmental regulations. However, we may be required to do so in future and this may affect our ability to expand or maintain our operations.

Exploratory drilling involves many risks and we may become liable for pollution or other liabilities, which may have an adverse effect on our financial position.

Drilling operations generally involve a high degree of risk. Hazards such as unusual or unexpected geological formations, power outages, labor disruptions, blow-outs, sour gas leakage, fire, inability to obtain suitable or adequate machinery, equipment or labour, and other risks are involved. We may become subject to liability for pollution or hazards against which we cannot adequately insure or which we may elect not to insure. Incurring any such liability may have a material adverse effect on our financial position and operations.

-11-

Shortages of rigs, equipment, supplies and personnel could delay or otherwise adversely affect our cost of operations or our ability to operate according to our business plans.

If drilling activity increases worldwide, a shortage of drilling and completion rigs, field equipment and qualified personnel could develop. These costs have recently increased sharply and could continue to do so. The demand for and wage rates of qualified drilling rig crews generally rise in response to the increasing number of active rigs in service and could increase sharply in the event of a shortage. Shortages of drilling and completion rigs, field equipment or qualified personnel could delay, restrict or curtail our exploration and development operations, which could in turn harm our operating results.

The geographic concentration of all of our properties in Texas subjects us to an increased risk of loss of revenue or curtailment of production from factors affecting those areas.

The geographic concentration of all of our leasehold interests in Texas means that our properties could be affected by the same event should the regions experience:

-

severe weather;

-

delays or decreases in production, the availability of equipment, facilities or services;

-

delays or decreases in the availability of capacity to transport, gather or process production; or

-

changes in the regulatory environment.

The oil and gas exploration and production industry is historically a cyclical industry and market fluctuations in the prices of oil and gas could adversely affect our business.

Prices for oil and gas tend to fluctuate significantly in response to factors beyond our control. These factors include:

-

weather conditions in the United States and wherever our property interests are located;

-

economic conditions, including demand for petroleum-based products, in the United States and the rest of the world;

-

actions by OPEC, the Organization of Petroleum Exporting Countries;

-

political instability in the Middle East and other major oil and gas producing regions;

-

governmental regulations, both domestic and foreign;

-

domestic and foreign tax policy;

-

the pace adopted by foreign governments for the exploration, development, and production of their national reserves;

-

the price of foreign imports of oil and gas;

-

the cost of exploring for, producing and delivering oil and gas;

-

the discovery rate of new oil and gas reserves;

-12-

-

the rate of decline of existing and new oil and gas reserves;

-

available pipeline and other oil and gas transportation capacity;

-

the ability of oil and gas companies to raise capital;

-

the overall supply and demand for oil and gas; and

-

the availability of alternate fuel sources.

Changes in commodity prices may significantly affect our capital resources, liquidity and expected operating results. Price changes will directly affect revenues and can indirectly impact expected production by changing the amount of funds available to reinvest in exploration and development activities. Reductions in oil and gas prices not only reduce revenues and profits, but could also reduce the quantities of reserves that are commercially recoverable. Significant declines in prices could result in non-cash charges to earnings due to impairment.

Changes in commodity prices may also significantly affect our ability to estimate the value of producing properties for acquisition and divestiture and often cause disruption in the market for oil and gas producing properties, as buyers and sellers have difficulty agreeing on the value of the properties. Price volatility also makes it difficult to budget for and project the return on acquisitions and the development and exploitation of projects. We expect that commodity prices will continue to fluctuate significantly in the future.

Our interests are held in the form of leases that we may be unable to retain.

The interest in our property are held under leases and working interests in leases. If we or the holder of a lease fails to meet the specific requirements of the lease regarding delay or non-payment of rental payments or we or the holder of the lease fail to meet the minimum level of evaluation some or all of our leases may terminate or expire. There can be no assurance that any of the obligations required to maintain each lease will be met. The termination or expiration of our leases or the working interests relating to leases may reduce our opportunity to exploit a given prospect for oil production and thus have a material adverse effect on our business, results of operation and financial condition.

We may not be able to develop oil and gas reserves on a timely and/or economically viable basis.

Our Farmout Agreement with SEPL requires us to commence commercial production on our Initial Test Well within 120 days after completion of drilling. To the extent that we succeed in discovering oil and/or natural gas reserves on our Initial Test Well, we cannot assure that we will be able to commence commercial production on our Initial Test Well within the 120 days nor can we assure that these reserves will be capable of production levels we project or in sufficient quantities to be commercially viable. On a long-term basis, our viability depends on our ability to find or acquire, develop and commercially produce additional oil and gas reserves. Without the addition of reserves through exploration, acquisition or development activities, our reserves and production will decline over time as reserves are produced. Our future reserves will depend not only on our ability to develop then-existing properties, but also on our ability to identify and acquire additional suitable producing properties or prospects, to find markets for the oil and natural gas we develop and to effectively distribute our production into our markets. We may not be able to find, develop or acquire additional reserves at acceptable costs.

Future oil and gas exploration may involve unprofitable efforts, not only from dry wells, but from wells that are productive but do not produce sufficient net revenues to return a profit after drilling, operating and other costs. Completion of a well does not assure a profit on the investment or recovery of drilling, completion and operating costs.

-13-

Any change to government regulation/administrative practices may have a negative impact on our ability to operate and our profitability.

The laws, regulations, policies or current administrative practices of any government body, organization or regulatory agency in the United States, Canada, or any other jurisdiction, may be changed, applied or interpreted in a manner which will fundamentally alter the ability of our company to carry on our business. The actions, policies or regulations, or changes thereto, of any government body or regulatory agency, or other special interest groups, may have a detrimental effect on us. Any or all of these situations may have a negative impact on our ability to operate and/or our profitability.

If we are unable to hire and retain key personnel, we may not be able to implement our plan of operation and our business may fail.

Our success will be largely dependent on our ability to hire and retain highly qualified personnel. This is particularly true in the highly technical businesses of mineral and oil and gas exploration. These individuals may be in high demand and we may not be able to attract the staff we need. In addition, we may not be able to afford the high salaries and fees demanded by qualified personnel, or we may fail to retain such employees after they are hired. At present, we have not hired any key personnel. Our failure to hire key personnel when needed will have a significant negative effect on our business.

Because our executive officers do not have formal training specific to oil and gas exploration, there is a higher risk our business will fail.

While Robert Kinloch, our director and one of our executive officer, has experience managing a mineral exploration company, he does not have formal training as a geologist. Donald Kinloch does not have formal training specific to mineral and gas exploration. Accordingly, our management may not fully appreciate many of the specific requirements related to working within the mining and oil and gas industry. Our management decisions may not take into account standard engineering or managerial approaches commonly used by such companies. Consequently, our operations, earnings, and ultimate financial success could be negatively affected due to our management’s lack of experience in the industry.

Our executive officers have other business interests, and as a result, they may not be willing or able to devote a sufficient amount of time to our business operations, thereby limiting the success of our company.

Robert Kinloch presently spends approximately 60% of his business time and Donald Kinloch presently spends approximately 20% of his business time on business management services for our company. At present, both Robert and Donald Kinloch spend a reasonable amount of time in pursuit of our company’s interests. Due to the time commitments from Robert and Donald Kinloch’s other business interests, however, they may not be able to provide sufficient time to the management of our business in the future and our business may be periodically interrupted or delayed as a result of their other business interests.

Risks Relating to Our Common Stock

If we issue additional shares in the future, it will result in the dilution of our existing shareholders.

Our articles of incorporation authorize the issuance of up to 750,000,000 shares of common stock with a par value of $0.001 per share. Our board of directors may choose to issue some or all of such shares to acquire one or more businesses or to provide additional financing in the future. The issuance of any such shares will reduce the book value and market price of the outstanding shares of our common stock. If we issue any such additional shares, such issuance will reduce the proportionate ownership and voting power of all current shareholders. Further, such issuance may result in a change of control of our corporation.

Our common stock is illiquid and shareholders may be unable to sell their shares.

There is currently a limited market for our common stock and we can provide no assurance to investors that a market will develop. If a market for our common stock does not develop, our shareholders may not be able to re-sell the shares of our common stock that they have purchased and they may lose all of their investment. Public announcements regarding our company, changes in government regulations, conditions in our market segment or changes in earnings estimates by analysts may cause the price of our common shares to fluctuate substantially. In addition, stock prices for junior oil and gas companies fluctuate widely for reasons that may be unrelated to their operating results. These fluctuations may adversely affect the trading price of our common shares.

-14-

Penny stock rules will limit the ability of our stockholders to sell their stock.

The Securities and Exchange Commission has adopted regulations which generally define “penny stock” to be any equity security that has a market price (as defined) less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Our securities are covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and “accredited investors”. The term “accredited investor” refers generally to institutions with assets in excess of $5,000,000 or individuals with a net worth in excess of $1,000,000 or annual income exceeding $200,000 or $300,000 jointly with their spouse. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form prepared by the Securities and Exchange Commission which provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction and monthly account statements showing the market value of each penny stock held in the customer’s account. The bid and offer quotations, and the broker-dealer and salesperson compensation information, must be given to the customer orally or in writing prior to effecting the transaction and must be given to the customer in writing before or with the customer’s confirmation. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to these penny stock rules. Consequently, these penny stock rules may affect the ability of broker-dealers to trade our securities. We believe that the penny stock rules discourage investor interest in and limit the marketability of our common stock.

The Financial Industry Regulatory Authority, or FINRA, has adopted sales practice requirements which may also limit a shareholder’s ability to buy and sell our stock.

In addition to the “penny stock” rules described above, FINRA has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low priced securities will not be suitable for at least some customers. FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock and have an adverse effect on the market for its shares.

Because of the early stage of development and the nature of our business, our securities are considered highly speculative.

Our securities must be considered highly speculative, generally because of the nature of our business and the early stage of our development. We are engaged in the business of identifying, acquiring, exploring and developing commercial reserves of oil and gas. Our properties are in the exploration stage only and are without known reserves of oil and gas. Accordingly, we have not generated any revenues nor have we realized a profit from our operations to date and there is little likelihood that we will generate any revenues or realize any profits in the short term. Any profitability in the future from our business will be dependent upon locating and developing economic reserves of oil and gas, which itself is subject to numerous risk factors as set forth herein. Since we have not generated any revenues, we will have to raise additional monies through the sale of our equity securities or debt in order to continue our business operations.

-15-

We do not intend to pay dividends on any investment in the shares of stock of our company.

We have never paid any cash dividends and currently do not intend to pay any dividends for the foreseeable future. To the extent that we require additional funding currently not provided for in our financing plan, our funding sources may prohibit the payment of a dividend. Because we do not intend to declare dividends, any gain on an investment in our company will need to come through an increase in the stock’s price. This may never happen and investors may lose all of their investment in our company.

Risks Related to Our Company

Our by-laws contain provisions indemnifying our officers and directors.

Our by-laws provide the indemnification of our directors and officers to the fullest extent legally permissible under the Nevada corporate law against all expenses, liability and loss reasonably incurred or suffered by him in connection with any action, suit or proceeding. Furthermore, our by-laws provide that our board of directors may cause our company to purchase and maintain insurance for our directors and officers, and we have implemented director and officer insurance coverage.

Our by-laws do not contain anti-takeover provisions and thus our management and directors may change if there is a take-over of our company.

We do not currently have a shareholder rights plan or any anti-takeover provisions in our by-laws. Without any anti-takeover provisions, there is no deterrent for a take-over of our company. If there is a take-over of our company, our management and directors may change.

Because our director and officers are residents of other countries other than the United States, investors may find it difficult to enforce, within the United States, any judgments obtained against our director and officers.

Our director and officers are nationals and/or residents of countries other than the United States, and all or a substantial portion of such persons’ assets are located outside the United States. As a result, it may be difficult for investors to enforce within the United States any judgments obtained against our officers or director, including judgments predicated upon the civil liability provisions of the securities laws of the United States or any state thereof.

-16-

ITEM 2. PROPERTIES.

Executive Offices

Our principal business offices are located at 2501 Lansdowne Ave., Saskatoon, Saskatchewan, Canada S7J 1H3. These premises are provided to us without cost by our president, Robert Kinloch. Our offices consist of approximately 200 square feet. We believe that our current lease arrangements provide adequate space for our foreseeable future needs.

Acquisition of East Bernard Prospect Properties

On December 14, 2009, we entered into a farm out agreement with Southeastern Pipe Line Company pursuant to which we acquired the right to earn an interest in certain oil and gas mineral leases located in Fort Bend and Wharton Countires, Texas (the “Leases”) covering 4,520 acres of land. The Leases are divided into developed acreage and undeveloped acreage. We can only earn a right in the developed acreage if we successfully develop the undeveloped acreage. See Item 1 “Farm out Agreement with Southeastern Pipe Line Company” above.

-17-

Location of Farmout Acreage

History of East Bernard Prospect

The Leases cover 4,520 acres of land and offsets contiguous acreage owned by Conoco-Philips presently producing natural gas and oil and known as the “Cooley Field”. The Cooley Field and the development area of the Leases are located inside a “Fairway” running from northeast to southwest. The boundaries of the Fairway are clearly defined by the Depo fault on the north boundary and the Cooley fault on the south which are the major structural features of the productive zone and which acted as a trap for the hydrocarbons in this immediate area and elsewhere in the Wilcox trend. Gas was first discovered on the Cooley Field in 1983 and the date of first production from TRRC records was October, 1997. The prospective productive deep zone in the East Bernard Prospect and throughout the area is known as the “Meek Sand” which is found in the Wilcox section. The Wilcox is the primary objective of Maverick’s planned drilling program. The Wilcox section is a known zone of hydrocarbons extending through-out South Texas and into the Gulf of Mexico.

-18-

2010 Drill Program

In October, 2010 we engaged a Texas based contractor to commence drill site construction in preparation for the drilling of the Company’s Initial Test Well Fort Bend County, Texas in December, 2010. The construction of location services included widening of an existing 2,000 foot access road and foundational re-enforcement with crushed limestone. In addition, contractors constructed the requisite drilling pad of approximately 1.5 acres in anticipation of rig mobilization. On January 22, 2011 Maverick successfully completed drilling its Initial Test Well to 13,500 on the Company's 4,513 acre Farm-Out property in Fort Bend County, Texas.

The initial test well was spud on December 9, 2010 and reached its targeted depth of 13,500 feet on day 44 of the drilling program. The Company’s independent log analyst and project engineer concurred at that time that the targeted Wilcox zones were not commercially productive, despite the presence of significant down hole pressure and strong natural gas shows during drilling. The target sands were very poorly developed and not suitable for a completion attempt. Accordingly, the decision was made to not set production casing and to look up hole for completion opportunities. The first completion attempt was a potential oil reservoir near 8,000’.

The Yegua sand was indicated as potentially productive from open hole log analysis but proved to be non-productive after testing. The second completion attempt was made on a shallow Miocene zone. There had not been an open hole log across this interval but a significant gas show was seen on the mud log while drilling this interval. The zone was perforated and swab tested during the week of March 14-19, 2011 but yielded no significant gas. Maverick’s engineers have as of the date of this annual report completed plugging the Lankford Trust No. 1 pursuant to regulations of the Texas Railway Commission. Management’s intent is to conduct further work on log and seismic data in order to determine whether or not to abandon the Initial Test Well.

-19-

As a result of test results showing that zones drilled were not commercially productive management determined that the direct costs capitalized in relation to the Initial Test Well were impaired. Management’s intent is to conduct further work on log and seismic data in order to determine whether or not to abandon the Initial Test Well.

Management determined that costs relating to drilling and direct exploration and asset retirement obligation costs, plus 25% of all costs relating to the Farm-Out Acreage as a whole should be considered evaluated costs and thus be subject to amortization. Besides drilling, exploration and asset retirement obligation costs, which are directly related to the Initial Test Well, the Company also included 25% of all other costs relating to the Farm-Out Acreage as a whole in its impairment assessment on the basis that these costs were incurred in connection with the Farmout Agreement where it is previously disclosed (Note 3(iv)) that one of the conditions of the Farmout Agreement is the completion of the drilling of at least four wells and thus determined it appropriate to include 25% of these costs in the impairment assessment on the Initial Test Well. The costs were offset against the incidental revenue of $650,000 received from selling working interests relating to the Initial Test Well.

ITEM 3. LEGAL PROCEEDINGS.

We know of no material, active, or pending legal proceeding against our company, nor are we involved as a plaintiff in any material proceeding or pending litigation where such claim or action involves damages for more than 10% of our current assets. There are no proceedings in which any of our company’s directors, officers, or affiliates, or any registered or beneficial shareholders, is an adverse party or has a material interest adverse to our company’s interest.

ITEM 4. (REMOVED AND RESERVED).

-20-

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Market for Securities

Our common shares were quoted for trading on the OTC Bulletin Board on June 21, 1999 under the symbol “PFCS”. On February 15, 2002 our symbol changed to “MAVM” and on May 22, 2003 our symbol changed to “MVRM”. On August 29, 2006, our stock was delisted from the OTC Bulletin Board and on August 31, 2006, it commenced trading on the Pink Sheets LLC under the symbol “MVRM”. On July 7, 2009 our shares of common stock were quoted for trading on the OTC Bulletin Board under the symbol “MVRM” and on December 31, 2009 our symbol changed to “MVRMD”. On February 23, 2011 our securities were quoted exclusively on the OTC Markets Group Inc. under the symbol “MVRM”.

The following quotations obtained from the OTC Markets Group Inc. reflect the high and low bids for our common stock based on inter-dealer prices, without retail mark-up or mark-down or commission and may not represent actual transactions.

The high and low bid prices of our common stock for the periods indicated below are as follows:

| Quarter Ended | High* | Low* |

| December 31, 2010 | $5.00 | $1.20 |

| September 30, 2010 | $1.50 | $1.02 |

| June 30, 2010 | $1.75 | $0.65 |

| March 31, 2010 | $1.11 | $0 |

| December 31, 2009 | $1.00 | $0.20 |

| September 30, 2009 | $0.50 | $0.30 |

| June 30, 2009 | $0.90 | $0.10 |

| March 31, 2009 | $0.70 | $0.10 |

*Prices shown have been adjusted to reflect the ten for one reverse split effected on December 31, 2009.

Pacific Stock Transfer Company, of 4045 South Spencer Street, Suite 403 Las Vegas, NV 89119 (telephone: 702.361.3033; facsimile 702.433.1979) is the registrar and transfer agent for our shares of common stock.

Holders of our Common Stock

As of March 30, 2011, we have 150 registered stockholders and 12,152,617 shares issued and outstanding.

Dividend Policy

We have not paid any cash dividends on our common stock and have no present intention of paying any dividends on the shares of our common stock. Our future dividend policy will be determined from time to time by our board of directors.

-21-

Recent Sales of Unregistered Securities

Other than as disclosed below or in the Company’s periodic reports the Company did not sell any equity securities during the period covered by this annual report that were not registered under the Securities Act of 1933.

Effective February 28, 2011 the Company entered into debt settlement and subscription agreements (the with two subscribers pursuant to which the Company settled an aggregate of $50,000 debt in consideration of the issuance of 50,000 shares. The shares were issued pursuant to Regulation D of the Securities Act of 1933 to two U.S. Persons (as such term is defined in Regulation S of the Securities Act of 1933) who represented that they were each accredited investors as such term is defined in Rule 502 of Regulation D of the Securities Act of 1933.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

On June 1, 2009, our board of directors adopted our 2009 Stock Option Plan. The purpose of our 2009 stock option plan is to retain the services of valued key employees and consultants of our company. Under the plan, the plan administrator is authorized to grant stock options to acquire up to a total of up to 7,500,000 shares of our common stock. On July 31, 2009 we filed a consent solicitation on Schedule 14A to seek stockholder approval of our 2009 Stock Option Plan. On August 3, 2009 we received majority stockholder consent approving our 2009 stock option plan. In August, 2009 we granted an aggregate of 145,000 options to acquire shares of our common stock at an exercise price of $0.40 per share to certain of our officers, employees and consultants under the 2009 option plan. In September, 2010 we granted an aggregate of 1,100,000 options to acquire shares of our common stock at an exercise price of $1.05 per share exercisable until August 20, 2015 to certain of our directors and officers under the 2009 option plan. On January 13, 2011 we granted options to acquire an aggregate of 50,000 shares of our common stock at an exercise price of $1.50 per share exercisable until January 13, 2013 to two consultants under the 2009 option plan.

The following table provides a summary of the number of stock options granted under the 2009 Plan, the weighted average exercise price and the number of stock options remaining available for issuance under the Company’s option plans as at December 31, 2010:

Number of securities to be issued upon exercise of outstanding options, warrants and rights |

Weighted-Average exercise price of outstanding options, warrants and rights |

Number of

securities remaining available for future issuance under equity compensation plan | |

| Equity compensation plans not approved by security holders | 1,245,000 | $1.03 | 6,255,000 |

Purchase of Equity Securities by the Issuer and Affiliated Purchasers

We did not purchase any of our shares of common stock or other securities during the year ended December 31, 2010.

ITEM 6. SELECTED FINANCIAL DATA.

Not Applicable.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION

The following discussion should be read in conjunction with our audited financial statements and the related notes that appear elsewhere in this annual report. The following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward looking statements. Factors that could cause or contribute to such differences include those discussed below and elsewhere in this annual report.

-22-

Our audited consolidated financial statements are stated in United States dollars and are prepared in accordance with United States generally accepted accounting principles.

Plan of Operation

We are currently an exploration stage company engaged in the acquisition, exploration, and development of prospective oil and gas properties in Texas. Our current business focus is to implement the terms of the Farmout Agreement, entered into by the Company in December 2009, pursuant to which we intend to earn an interest in certain oil and gas mineral leases located in Fort Bend and Wharton Counties, Texas presently owned by SEPL. Our Plan of Operation will begin with a review of the data obtained through the drilling of our Initial Test Well. Based on the results of that review, the Company will determine if the acquisition of further geophysical data is warranted both for the present drill site block and the Farm Out Acreage as a whole. The Company remains in compliance with the performance timetable as set out in the Farm Out Agreement on the date of the filing of this report. Thereafter, a decision will be made with respect to drilling a second exploration well, subject to suitable financing on terms acceptable to the Company, but in any event no such drilling is contemplated before the third quarter of 2011 in keeping with the terms of the Company’s Farm Out Agreement.

The Company is reviewing a small number of new opportunities for oil and gas exploration and development in Texas, some of which have production components as well as development opportunities. The Company believes that it is feasible to contemplate, based on discussions with interested parties, a stock predicated acquisition based on the strong capital structure that was implemented by the Company in 2010. Management will review these opportunities diligently; however, no guarantee can be given that any transaction as outlined herein will occur in the time frame covered by this Plan of Operation.

Finally, the Company has a history of acquiring mineral properties outside of the oil and gas arena including silver and coal properties previously owned and produced by the Company. At a time of strong commodity markets for these and other metals and minerals, the Company will not hesitate to exploit any opportunity to utilize its experience gained over the past decade to enter into an agreement for the acquisition and development of a metal or minerals property.

2010 Drilling Program

In connection with our 2010 drilling program under the Farmout Agreement we completed the following:

-