Attached files

| file | filename |

|---|---|

| 8-K - UPDATED INVESTOR PRESENTATION - NBL Texas, LLC | rose8k.htm |

Rosetta Resources Inc.

Randy Limbacher

Chairman, CEO & President

April 11, 2011

www.rosettaresources.com / NASDAQ: ROSE

All statements, other than statements of historical fact, included in this presentation are forward-looking

statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking

statements are statements that are not historical facts, such as expectations regarding drilling plans, changes in

acreage positions, and expected capital expenditures. The assumptions of management and the future

performance of the Company are subject to a wide range of business risks and uncertainties and there is no

assurance that these statements and projections will be met. Factors that could affect the Company's business

include, but are not limited to: the risks associated with drilling of oil and natural gas wells; the Company's ability

to find, acquire, market, develop, and produce new reserves; the risk of drilling dry holes; oil and natural gas

price volatility; uncertainties in the estimation of proved, probable, and possible reserves and in the projection of

future rates of production and reserve growth; inaccuracies in the Company's assumptions regarding items of

income and expense and the level of capital expenditures; uncertainties in the timing of exploitation

expenditures; operating hazards attendant to the oil and natural gas business; drilling and completion losses that

are generally not recoverable from third parties or insurance; potential mechanical failure or underperformance

of significant wells; pipeline capacity availability and pipeline construction difficulties; climatic conditions;

availability and cost of material and equipment; the risks associated with operating in a limited number of

geographic areas; availability of capital; timing of planned divestitures; regulatory developments; environmental

risks; general economic and business conditions (including the effects of the worldwide economic recession); the

amount and expected benefit of hedging arrangements; industry trends; and other factors detailed in the

Company's most recent Form 10-K and other filings with the Securities and Exchange Commission. If one or

more of these risks or uncertainties materialize (or the consequences of such a development change), or should

underlying assumptions prove incorrect, actual outcomes may vary materially from those forecasted or

expected. The Company undertakes no obligation to publicly update or revise any forward-looking statements

except as required by law.

statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking

statements are statements that are not historical facts, such as expectations regarding drilling plans, changes in

acreage positions, and expected capital expenditures. The assumptions of management and the future

performance of the Company are subject to a wide range of business risks and uncertainties and there is no

assurance that these statements and projections will be met. Factors that could affect the Company's business

include, but are not limited to: the risks associated with drilling of oil and natural gas wells; the Company's ability

to find, acquire, market, develop, and produce new reserves; the risk of drilling dry holes; oil and natural gas

price volatility; uncertainties in the estimation of proved, probable, and possible reserves and in the projection of

future rates of production and reserve growth; inaccuracies in the Company's assumptions regarding items of

income and expense and the level of capital expenditures; uncertainties in the timing of exploitation

expenditures; operating hazards attendant to the oil and natural gas business; drilling and completion losses that

are generally not recoverable from third parties or insurance; potential mechanical failure or underperformance

of significant wells; pipeline capacity availability and pipeline construction difficulties; climatic conditions;

availability and cost of material and equipment; the risks associated with operating in a limited number of

geographic areas; availability of capital; timing of planned divestitures; regulatory developments; environmental

risks; general economic and business conditions (including the effects of the worldwide economic recession); the

amount and expected benefit of hedging arrangements; industry trends; and other factors detailed in the

Company's most recent Form 10-K and other filings with the Securities and Exchange Commission. If one or

more of these risks or uncertainties materialize (or the consequences of such a development change), or should

underlying assumptions prove incorrect, actual outcomes may vary materially from those forecasted or

expected. The Company undertakes no obligation to publicly update or revise any forward-looking statements

except as required by law.

Forward-Looking Statements

2

Cautionary Statement Concerning Resources

The United States Securities and Exchange Commission permits oil and gas companies, in their filings with the SEC, to

disclose only proved, probable and possible reserves that a company anticipates as of a given date to be economically

and legally producible by application of development projects to known accumulations. We may use certain terms in this

presentation, such as “Risked Project Inventory,” “Project Counts,” “Net Risked Resources,” “Total Resources,” “Unrisked

Potential,” “Unrisked Original Resources in Place,” and “Unrisked EUR Potential” that the SEC's guidelines strictly

prohibit us from including in filings with the SEC. These estimates are by their nature more speculative than estimates of

proved reserves and accordingly are subject to substantially greater risk of actually being realized.

disclose only proved, probable and possible reserves that a company anticipates as of a given date to be economically

and legally producible by application of development projects to known accumulations. We may use certain terms in this

presentation, such as “Risked Project Inventory,” “Project Counts,” “Net Risked Resources,” “Total Resources,” “Unrisked

Potential,” “Unrisked Original Resources in Place,” and “Unrisked EUR Potential” that the SEC's guidelines strictly

prohibit us from including in filings with the SEC. These estimates are by their nature more speculative than estimates of

proved reserves and accordingly are subject to substantially greater risk of actually being realized.

For filings for year-end 2009 and forward, the SEC permits the optional disclosure of probable and possible

reserves. The Company has elected not to report probable and possible reserves in its filings with the SEC. We use the

term “net risked resources” to describe the Company’s internal estimates of volumes of natural gas and oil that are not

classified as proved reserves but are potentially recoverable through exploratory drilling or additional drilling or recovery

techniques. Estimates of unproved resources are by their nature more speculative than estimates of proved reserves

and accordingly are subject to substantially greater risk of actually being realized by the Company. Estimates of

unproved resources may change significantly as development provides additional data, and actual quantities that are

ultimately recovered may differ substantially from prior estimates.

reserves. The Company has elected not to report probable and possible reserves in its filings with the SEC. We use the

term “net risked resources” to describe the Company’s internal estimates of volumes of natural gas and oil that are not

classified as proved reserves but are potentially recoverable through exploratory drilling or additional drilling or recovery

techniques. Estimates of unproved resources are by their nature more speculative than estimates of proved reserves

and accordingly are subject to substantially greater risk of actually being realized by the Company. Estimates of

unproved resources may change significantly as development provides additional data, and actual quantities that are

ultimately recovered may differ substantially from prior estimates.

BFIT NPV10

We use the term “BFIT NPV10” to describe the Company’s estimate of before income tax net present value discounted at

10 percent resulting from project economic evaluation. The net present value of a project is calculated by summing future

cash flows generated by a project, both inflows and outflows, and discounting those cash flows to arrive at a present

value. Inflows primarily include revenues generated from estimated production and commodity prices at the time of the

analysis. Outflows include drilling and completion capital and operating expenses. Net present value is used to analyze

the profitability of a project. Estimates of net present value may change significantly as additional data becomes

available, and with adjustments in prior estimates of actual quantities of production and recoverable reserves, commodity

prices, capital expenditures, and/or operating expenses.

10 percent resulting from project economic evaluation. The net present value of a project is calculated by summing future

cash flows generated by a project, both inflows and outflows, and discounting those cash flows to arrive at a present

value. Inflows primarily include revenues generated from estimated production and commodity prices at the time of the

analysis. Outflows include drilling and completion capital and operating expenses. Net present value is used to analyze

the profitability of a project. Estimates of net present value may change significantly as additional data becomes

available, and with adjustments in prior estimates of actual quantities of production and recoverable reserves, commodity

prices, capital expenditures, and/or operating expenses.

Forward-Looking Statements (Cont.)

3

– Capital spending of $339 MM

– High return/high value programs received vast majority of funding

– Capital exceeded internal cash flows, but balanced with asset sales

beginning cash and revolver borrowings

beginning cash and revolver borrowings

– 2010 asset sales are ~$90MM

– Production growth

– Annual production rate of 138 MMcfe/d

– Exit rate of 157 MMcfe/d

– Eagle Ford exit rate of 86 MMcfe/d

– Reserve growth

– Double digit reserve growth rate

Rosetta Resources - 2010 Highlights

4

Rosetta Resources Key Statistics

|

Reserves Inventory in BCFE

|

2010

|

2009

|

Percent

Increase |

|

Proved Reserves

|

479

|

351

|

36%

|

|

Risk Adjusted Inventory (1)

|

1,897

|

812

|

134%

|

|

Average Shares Outstanding (Diluted)

|

52.1MM

|

51.0MM

|

2%

|

1) Excludes PUD’s

5

– $360 MM Capital Budget in 2011

– Focus on Eagle Ford

– 90% of 2011 capital allocated to Eagle Ford

– 40 wells planned

– Fracture stimulation services agreement in place

– Pipeline and processing capacity expanded

– Shift to liquids accelerates

– Southern Alberta Basin evaluation continues

– Six wells drilled

– Additional five wells to be drilled by early 2011

– Completions planned for 2011

– Additional asset sales scheduled

– DJ Basin

– Sacramento Basin

– Strong alignment with stakeholders remains fundamental driver

2011 Program

6

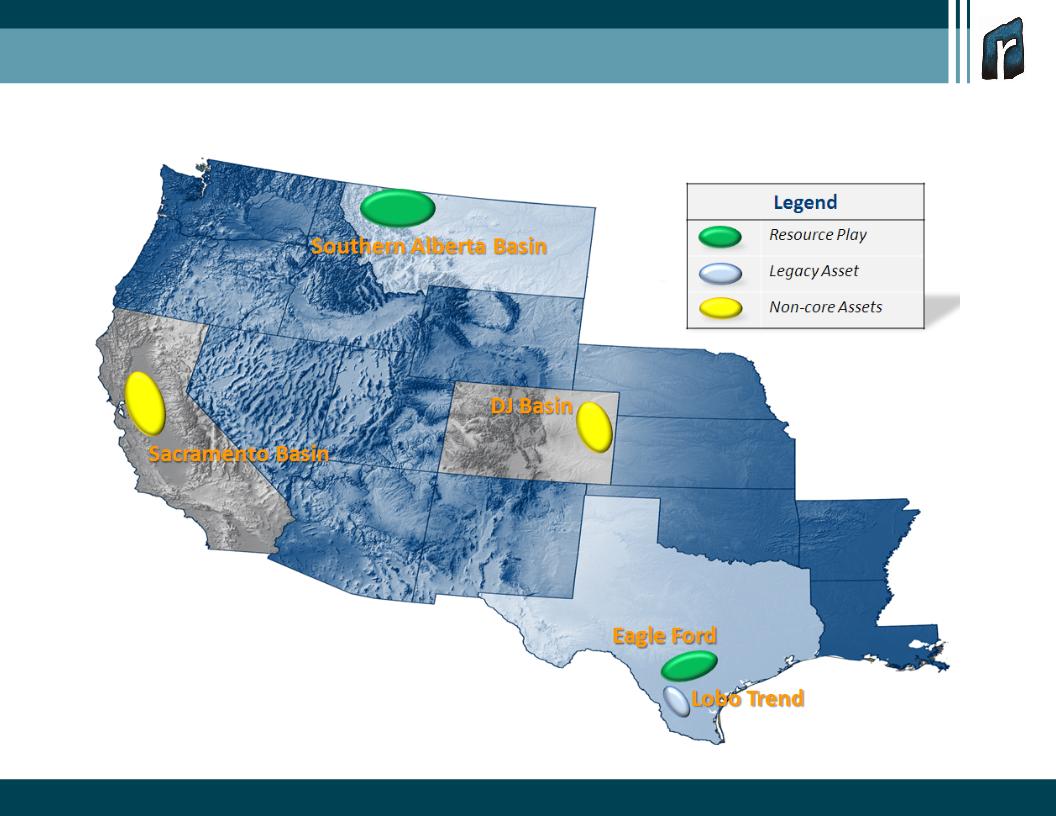

Rosetta Asset Portfolio Status

7

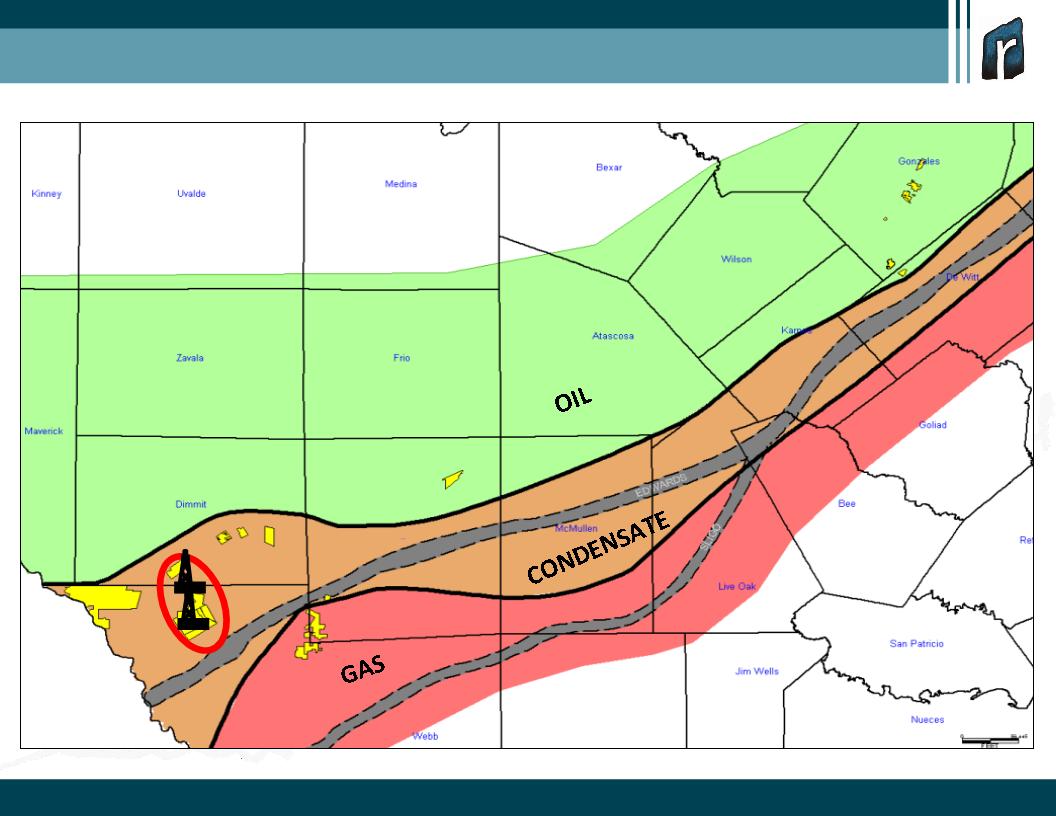

Eagle Ford

|

Area

|

Hydrocarbon Window

|

Net Acres

|

|

Gates Ranch Area

|

Condensate

|

29,960

|

|

Central Dimmit

|

Oil

|

7,450

|

|

Encinal Area

|

Dry Gas

|

14,500

|

|

Gonzales Area

|

Oil

|

6,500

|

|

NE LaSalle Area

|

Oil

|

3,450

|

|

Western Webb

|

Condensate

|

3,000

|

|

Total

|

77% Liquids

|

64,860

|

Rosetta’s drilling focus has been primarily on the Gates Ranch Area, however, we

have embarked on the delineation of our other liquids-rich areas…

have embarked on the delineation of our other liquids-rich areas…

9

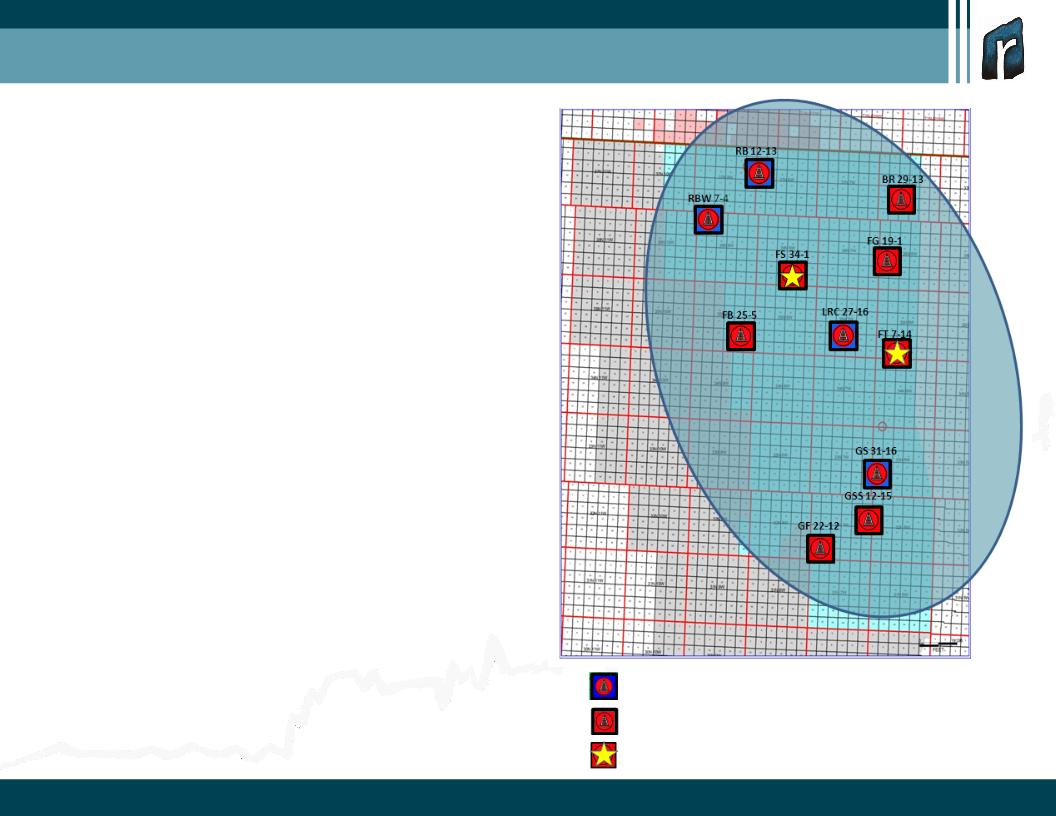

Gates Ranch Area

10

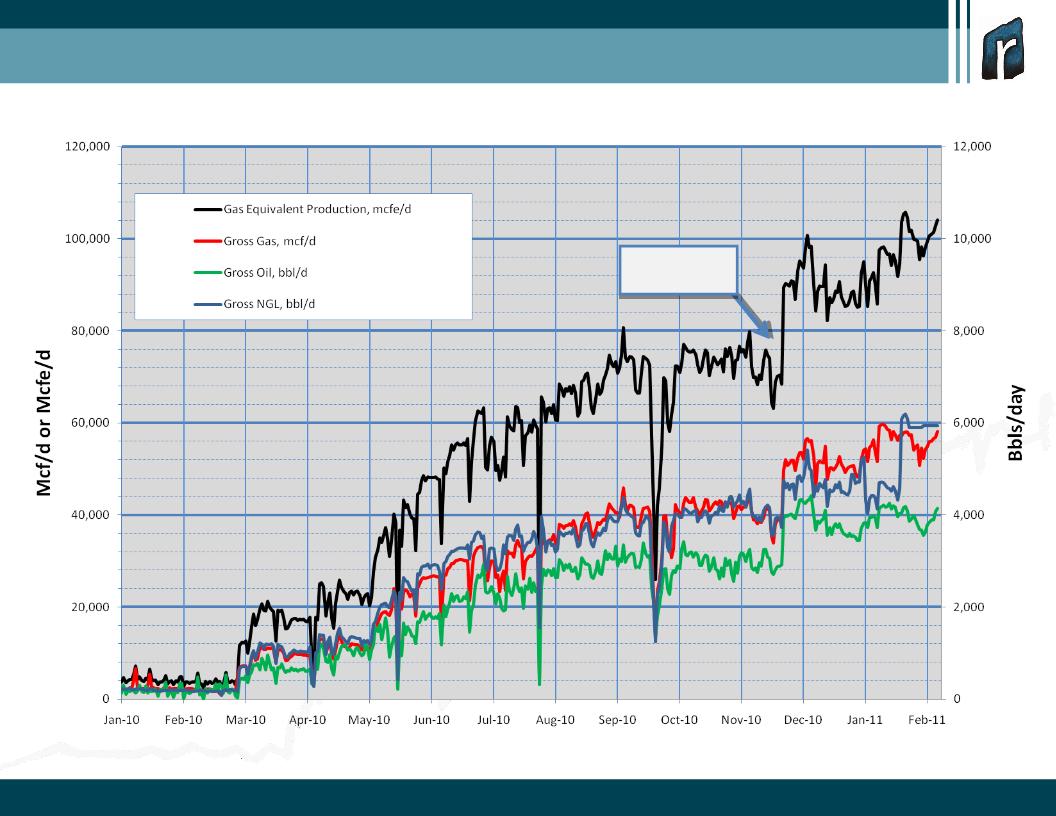

Gates Ranch-Gross Daily Production

Dos Hermanas

in service

in service

11

Eagle Ford - Gates Ranch

12

Wells Drilled - 2009 & 2010

Planned Wells - 2011

Gates Ranch Proper - Drilling Activities

Inception to date and planned for 2011

Inception to date and planned for 2011

13

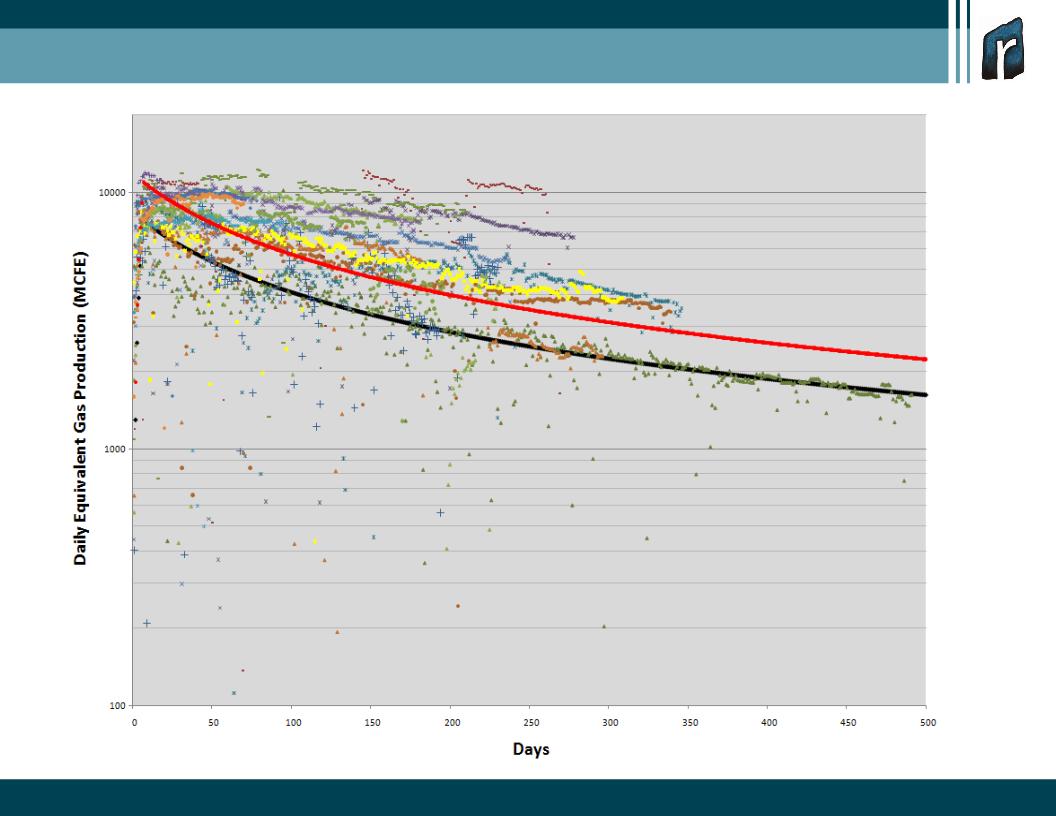

Gates Ranch Proper - Individual Well Performance

Normalized actual results versus internal 7.2 Bcfe P50 curve and P90 PUD booking curve

7.2 BCFE

(Internal model)

5.3 BCFE

(PUD booking)

14

|

Area

|

Initial

Gas Rate

(mmcfpd)

|

Initial

Oil Rate

(bopd)

|

EUR

(bcfe)

|

NPV Per

Well BFIT10

($MM)

|

Discounted

Payout

(years)

|

Post 2010

Inventory

(Net Wells)

|

NPV Per Area

BFIT10

($)

|

|

Gates North Type Curve

|

5.0

|

450

|

6.7

|

13.0

|

1.6

|

150

|

$1.950 billion

|

|

Gates South Type Curve

|

7.0

|

350

|

8.1

|

14.1

|

1.4

|

90

|

$1.269 billion

|

|

Gates Ranch Type Curve

|

5.7

|

412

|

7.2

|

13.4

|

1.5

|

240

|

$3.219 billion

|

Notes:

• Gates Ranch proper only (26,500 net acres)

• 100 acre well spacing

• $8.25 mm total well cost

• Strip pricing effective 10/26/2010

• “Per area” values are “per well” values multiplied by post 2010 net inventory

Gates Ranch Valuation

On average, a typical well has a 7.2 BCFE EUR and a BFIT NPV of $13.4 MM…

15

– Dos Hermanas in service December 2010

– Firm gathering and processing reaches 85 MMcfe/d

– Revised agreement in place:

– Dimmit lateral in service 2nd quarter 2011

– Dos Hermanas capacity to increase by 20 MMcfe/d in 3rd quarter 2011

– Velocity oil pipeline and terminal in place January 2011

– Rosetta to access new gathering and processing in 4th quarter 2011

with total capacity of 115 MMcf/d

with total capacity of 115 MMcf/d

– Total capacity to reach 205 MMcf/d by 2013

Eagle Ford Gathering

16

– Southern Alberta Basin specifics

– Devonian Shale oil play in NW Montana

– Williston Basin analog

– Depths ranging from 4,500’ to 7,500’ TVD

– Current position

– 300,000 undeveloped net acres

– Resource in place

– 13 - 15 MMBoe per square mile

– Assessment to date

– Continuous reservoir deposition throughout

position

position

– Continuous oil accumulation throughout position

– Operational Status

– Multi-well vertical program near completion

– Multi-well horizontal program about to commence

Southern Alberta Basin Opportunity is Unique

Drilled & Tested

Drilled

Drilling

17

|

Acres

|

Lessor

|

Terms

|

|

200,000

|

Blackfeet Indian Nation

|

• 5 year option with 2 well per year drilling requirement for 10 well total.

• With each commercial well, Rosetta earns the right to lease 20,000 acres

surrounding that well for a 10 year term. • Continuous drilling obligation of 1 well per 9 months beginning on the 4th

year. |

|

30,000

|

WAVE Energy

|

• Terms similar to option acreage.

|

|

52,000

|

Allottee (Blackfeet Families)

|

• Typically 5 year lease terms, with option to extend term at the end of the

primary period. |

|

18,000

|

Fee Acreage

|

|

Southern Alberta Basin

Acreage Recap

Acreage Recap

18

– Conservative and disciplined approach to financial management

– Ample debt coverage

– Debt to proved reserves of $0.72/Mcfe

– Debt to proved developed reserves of $1.46/Mcfe

– Actively manage and monitor use of debt

– Debt to book cap @ 40%

– Debt to EBITDAX < 1.75x

– Maintain high level of liquidity throughout cycles

– Asset sales to “balance” 2011 capital program

– Reinvest cash flow in business: no dividend or share repurchases

planned

planned

Financial Strategy

1 Adjusted for the high yield offering

19

– High quality and low risk diversified proved asset base

– 479 Bcfe of proved reserves

– 9.8 year reserve life

– 51 % proved developed

– Financial flexibility

– Credit facility with $325MM borrowing base

– Debt to book cap @ 40%

– Borrowing capacity, including available cash of ~$240MM

Financial Strength

1 Adjusted for the high yield offering

20

– Selective hedging program:

– Oil hedges of 3,200 Bbl/d in 2011/3,400 Bbl/d in 2012/2,600 in 2013

– NGL Hedges of 1,679 Bbl/d in 2011/1,950 Bbl/d in 2012

– Gas hedges of 50,000 MMBtu/d in 2011/20,000 MMBtu/d in 2012

– Fracture stimulation services/agreement in place

– 2 year term

– 3 weeks per month

– Favorable pricing

– Transportation and processing

– 115 MMcf/d capacity total in 4th quarter of 2011

– 205 MMcf/d capacity total by 2013

Risk Management

21

– Focus on high return Eagle Ford inventory

– Production guidance dependent on divestiture timing

– 160-170 MMcfe/d including divestment properties

– DJ Basin/California expected to produce approximately 35 MMcfe/d for full year

– 2011 exit rate, excluding divestment properties, to range from 155-165

MMcfe/d

MMcfe/d

– Divest additional legacy assets to fund development

– Simplify and reduce unit cost structure

– Focus on returns

– Test Southern Alberta Basin position

2011 Program

22

Rosetta Resources Inc.

Randy Limbacher

Chairman, CEO & President

April 11, 2011

www.rosettaresources.com / NASDAQ: ROSE