Attached files

| file | filename |

|---|---|

| EX-3.1 - EXHIBIT 3.1 - Telidyne, Inc. | exhibit3-1.htm |

| EX-31.1 - EXHIBIT 31.1 - Telidyne, Inc. | exhibit31-1.htm |

| EX-32.2 - EXHIBIT 32.2 - Telidyne, Inc. | exhibit32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - Telidyne, Inc. | exhibit31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Telidyne, Inc. | exhibit32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2010

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to _____________

Commission File No. 000-53432

TEC TECHNOLOGY, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 13-4013027 |

| (State or other jurisdiction of incorporation or | (I.R.S. Employer Identification No.) |

| organization) |

Xinqiao Industrial Park

Jingde County, Anhui

Province

Shenzhen 242600

People’s Republic of China

(Address of principal executive offices)

(+86) 755 8323-2722

(Registrant’s

telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Exchange Act: Common Stock, $0.001 par value

Indicate by check mark if the registrant is a well-known

seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [

] No [X]

Indicate by check mark if the registrant is not required to file

reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [

] No [X]

Indicate by check mark whether the registrant (1) has filed all

reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days.

Yes [X] No

[ ]

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Website, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such

shorter period that the registrant was required to submit and post such files)

Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer [ ] | Accelerated Filer [ ] | |

| Non-Accelerated Filer [ ] | (Do not check if a smaller reporting company) | Smaller reporting company [X] |

Indicate by check mark whether registrant is a shell company (as

defined in Rule 12b-2 of the Act)

Yes [

] No [X]

As of June 30, 2010 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the shares of the registrant’s common stock held by non-affiliates (based upon the closing price of such shares as quoted on the OTC Bulletin Board maintained by the Financial Industry Regulatory Authority) was approximately $28.9 million. Shares of the registrant’s common stock held by each executive officer and director and each person who owns 10% or more of the outstanding common stock have been excluded from the calculation in that such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

There were a total of 30,181,552 shares of the registrant’s common stock outstanding as of March 30, 2011.

DOCUMENTS INCORPORATED BY REFERENCE

None.

| Annual Report on Form 10-K |

| For the Fiscal Year Ended December 31, 2010 |

TABLE OF CONTENTS

Special Note Regarding Forward Looking Statements

In addition to historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We use words such as “believe,” “expect,” “anticipate,” “project,” “target,” “plan,” “optimistic,” “intend,” “aim,” “will” or similar expressions which are intended to identify forward-looking statements. Such statements include, among others, those concerning market and industry segment growth and demand and acceptance of new and existing products; any projections of sales, earnings, revenue, margins or other financial items; any statements of the plans, strategies and objectives of management for future operations; any statements regarding future economic conditions or performance; as well as all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, including those identified in Item 1A, “Risk Factors” included herein, as well as assumptions, which, if they were to ever materialize or prove incorrect, could cause the results of the Company to differ materially from those expressed or implied by such forward-looking statements.

Readers are urged to carefully review and consider the various disclosures made by us in this report and our other filings with the SEC. These reports attempt to advise interested parties of the risks and factors that may affect our business, financial condition and results of operations and prospects. The forward-looking statements made in this report speak only as of the date hereof and we disclaim any obligation, except as required by law, to provide updates, revisions or amendments to any forward-looking statements to reflect changes in our expectations or future events.

Use of Terms

Except where the context otherwise requires and for the purposes of this report only:

| • |

the “Company,” “we,” “us,” and “our” refer to the combined business of TEC Technology, Inc., a Delaware corporation, and its consolidated subsidiaries, TEC HK, TEC Tower, ZTEC and STT; |

|

| |

| • |

“TEC HK” refers to TEC Technology Limited, a Hong Kong limited company; |

|

| |

| • |

“TEC Tower” refers to Anhui TEC Tower Co., Ltd., a PRC limited company; |

|

| |

| • |

“ZTEC” refers to Zhejiang TEC Tower Co., Ltd., a PRC limited company; |

|

| |

| • |

“STT” refers to Shuncheng Taida Technology Co., Ltd., a PRC limited company; |

|

| |

| • |

“Hong Kong” refers to the Hong Kong Special Administrative Region of the People’s Republic of China; |

|

| |

| • |

“PRC” and “China” refer to the People’s Republic of China; |

|

| |

| • |

“SEC” refers to the Securities and Exchange Commission; |

|

| |

| • |

“Exchange Act” refers the Securities Exchange Act of 1934, as amended; |

|

| |

| • |

“Securities Act” refers to the Securities Act of 1933, as amended; |

|

| |

| • |

“Renminbi” and “RMB” refer to the legal currency of China; and |

|

| |

| • |

“U.S. dollars,” “dollars” and “$” refer to the legal currency of the United States. |

1

PART I

ITEM 1. BUSINESS.

Business Overview

Through our indirect Chinese subsidiaries, we are primarily engaged in the design, production and sale of transmission towers and related products used in high voltage electric power transmission and wireless communications. We sell our tower products to prime contractors on large transmission projects for electric utility companies or telecommunications service providers, who are developing and constructing projects for end customers. Our electric transmission towers currently support 35kv, 110kv, 220kv, and 500kv transmission lines and we plan to build towers that support Ultra High Voltage (UHV) tower lines of 750+kv DC or 1000+kv AC transmission lines. Our wireless communication towers include single-tube towers, 4-strut towers and roof top towers for the 2G, 3G, and microwave market. We plan to expand our business in the near future to enter the communication base station system integration market and to offer tower installation and maintenance services. Our towers are primarily made of steel, but some contain aluminum or other alloy materials.

Our revenues currently are, and historically have been, generated from the sale of our tower products. In the future, we expect to offer installation and technical services that we believe will generate an additional revenue stream, however, to date, we have not generated material revenues from such services.

Our headquarters are located in Anhui Province in southeastern China and our international sales network is primarily operated from our branch offices in the Shenzhen Special Economic Zone and Beijing.

Our Corporate History and Background

We were originally organized under the laws of the State of Florida on July 22, 1988 under the name Sea Green, Inc. On June 3, 1998, we changed our name to Americom Networks Corp. and on July 10, 1998, we changed our name to Americom Networks International, Inc. From our inception until we ceased active business operations in May 1999, we engaged in various business endeavors and pursued several lines of business including the development and marketing of telecommunications systems to high-volume users for use or resale.

On February 6, 2008, we effected a redomestication from Florida to Delaware by merging with Americom Networks International, Inc., a corporation that we established in the State of Delaware solely to effect the reincorporation.

On August 15, 2008, we changed our name to Highland Ridge, Inc. and our primary business became the search for a potential merger candidate or a business to acquire.

On May 4, 2010, we completed a reverse acquisition transaction through a share exchange with TEC HK and its sole shareholder, Mr. Hua Peng Phillip Wong, pursuant to which we acquired 100% of the issued and outstanding capital stock of TEC HK in exchange for 19,194,421 shares of our common stock, which constituted 63.6% of our issued and outstanding capital stock on a fully-diluted basis as of and immediately after the consummation of the reverse acquisition. For accounting purposes, the share exchange was treated as a reverse acquisition, with TEC HK as the accounting acquirer and TEC Technology, Inc. as the acquired party.

As a result of the reverse acquisition of TEC HK, our business became the business of TEC HK and its subsidiaries, namely, the design, production and sale of transmission towers and related products used in high voltage electric power transmission and wireless communications. On June 9, 2010, we changed our name to TEC Technology, Inc. to more accurately reflect our new business operations.

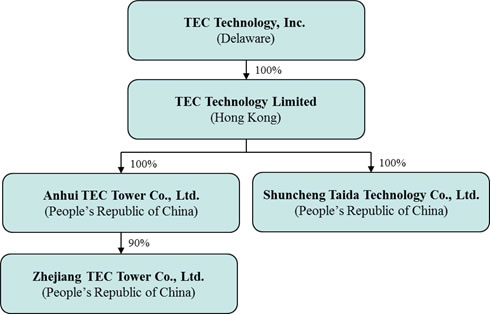

Our Corporate Structure

All of our business operations are conducted through our Chinese operating subsidiaries, TEC Tower, ZTEC and STT. The chart below presents our current corporate structure.

2

Our Products

Our electric transmission and wireless communications product lines include angle steel towers, steel pipe towers and transmission cable towers, constructed primarily of steel, aluminum or other alloy materials.

Electric Transmission Towers

Our electric transmission towers currently support 35kv, 110kv, 220kv and 500kv, and we have recently applied certifications to produce towers for the 750kv electric transmission lines. We plan to develop towers that support Ultra High Voltage (UHV) tower lines of 1000+kv AC transmission lines as the market evolves beyond testing phases.

Wireless Communications Towers

Our wireless communications towers include single-tube towers, 4-strut towers and roof top towers for the 2G, 3G, and microwave market.

We are also in the early stages of developing expertise to produce wireless communication base stations, which typically include towers, air conditioning units, transformers, equipment procurement, power connection, site survey, installation, and after-sales services. Once we are able to develop this full product and service offering, we plan to expand our business by offering services to customers under separate tower maintenance contracts. Profit margins from base station contracts are typically higher than margins from product sales, however, to be fully engaged in the base station business we will have to develop or acquire additional capabilities in terms of design, procurement, and services.

3

In the future we expect to expand our business to offer tower installation and maintenance services.

Our Raw Materials and Suppliers

The major raw materials for our tower products are angle iron, plate, steel beams, bolts and welding wire. We acquire our primary raw materials from a variety of sources. We have some long-term steel purchase contracts in order to reduce the negative effects of steel price fluctuation, but we also have some short-term contracts or make one-time purchases to take advantage of favorable pricing. Our primary suppliers are Jiangyin Jincheng Steel Co., Ltd., Hangzhou Fuyang Fuhao Hot Dip Galvanizing Co., Ltd. and Hangzhou Fangshun Materials Co., Ltd., whose purchases accounted for approximately 14.61%, 11.94% and 10.47% of our cost of raw materials for the year ended December 31, 2010, respectively.

Our Customers and Marketing Efforts

Our direct customers typically are specialized construction companies which serve as a prime contractor and builder on transmission projects constructed for our ultimate end customers, electric utility companies and telecommunication service providers. We usually obtain our customers by succeeding in a competitive bidding process where subcontracts are awarded to companies, like us, which submit the most favorable bids on a transmission project. We have found that a successful bid is usually predicated on a variety of factors including pricing, terms of delivery, product design and quality, industry experience and reputation and time to delivery, among other factors.

During fiscal year 2010, our three largest customers were Shenzhen ZTE Kangxun Electronics Co., Ltd., Shanxi Jinneng Steel Structure Co., Ltd. and Inner Mongolia Hengxin Tower Co., Ltd., whose purchases accounted for approximately 24.89% , 18.83% and 11.77% of our revenue for the year ended December 31, 2010, respectively. No other customer accounted for more than 10% of our total revenue in 2010.

The electric utility companies and telecommunication companies that use our tower products in their transmission facilities are mainly located in Shanxi Province and the Inner Mongolia Autonomous Region in northern China, and in Guangdong Province and Guizhou Province in heavily populated southern China, and include ZTE Corporation, the State Grid Corp of China, the China Southern Grid, Huawei Technologies Co. Ltd. and Reliance Communications, among others.

We have also made efforts in some overseas markets where our products have developed positive brand recognition. We believe that we are one of only a few PRC-based electric transmission tower companies selling products abroad. In India and Southeast Asia, we currently partner with large contractors such as Huawei and ZTE Corporation to perform contracts in these markets, and in Africa, we have independently established sales centers to directly serve this market.

We generally seek to obtain certifications from main contractors in these overseas markets and then bid on their particular projects. We currently hold certifications from Huawei, ZTE Corporation, Nokia Ericsson, and Reliance, which allow us to bid as subcontractors on their projects. The table below is a sampling of our overseas projects:

| Region |

Contract Details |

| India |

We manufactured and delivered 691 nos. of 403B steel tower with India Reliance Telecom Company in 2008 and expect to conduct more direct sales in India. |

| Southeast Asia |

In 2009, we supplied transmission products to Multi-Link Engineering of Malaysia for transmission projects in Papua New Guinea. We plan to conduct more direct sales in Southeast Asia in the future. |

| Africa |

We have performed on contracts for steel tower manufacturing and machining in Africa, cooperating with Huawei Company for sale to Zambia, Tanzania and Uganda. We have also supplied $7.3 million of tower equipment to ZTE Corporation for 2G/3G infrastructure development in Ethiopia. We plan to extend our sales network to South Africa. |

| Hong Kong |

We have cooperated with OMAX GLOBAL in Hong Kong in the production of communication towers in Hong Kong. |

When we successfully bid on a transmission project and secure a sub-contract for the purchase of our tower products, we are expected to promptly deliver to the prime contractor and/or end-customer, an acceptable tower design plan, as well as a supply and construction schedule, usually ranging from one to six months. During this time, we assemble and procure the raw materials that are needed in the tower manufacturing process from our raw material inventory and, occasionally, by special order from third party vendors. The steel used in our towers must be galvanized prior to the preparation of each piece for the tower parts so we usually outsource this process to specialized galvanization companies. Upon completing the components, we then test-assemble a percentage of the towers ordered. If the pieces connect according the specifications, we then load the components onto trucks or trains and ship them to the customer’s installation site. We plan to expand our business to offer the installation and service of our towers with end users.

4

Competition

The domestic electric transmission tower products and service market is highly competitive and fragmented. We believe that no single company in China holds more than a 3% market share. We believe that successful companies in the domestic electric transmission market compete effectively based on product and customer certification, delivery scheduling and capacity, pricing and customer retention. Competition in the domestic and international wireless communication market is based primarily on subcontracting from large equipment providers, such as Huawei and Nokia Ericsson.

Our primary competition comes from domestic companies such as Meteno Communication Technologies, Qixing Tower and Nanjing Daji Towers. Meteno Communication Technologies works solely with wireless communication towers and Qixing Tower participates in the wireless communication market. Additional competition comes from large international companies such as Valmont Industries, Inc. (NYSE:VMI) that are both larger than us in terms of assets and sales volume and possess greater name recognition, assets, personnel, sales, and financial resources. However, these competitors generally have higher prices for their products, and most of them do not have distribution networks in China that are as developed as ours.

We believe that the quality of our product and service offerings and our relatively low labor costs enable us to compete favorably in the market for electric and wireless transmission towers and distinguish us from many of our competitors, especially our international competitors. Although we generally win contracts by our delivery schedule and reputation in the market, our pricing is competitive. Our focus on quality and service allows us to bid for most projects, but through a lack of sufficient working capital, we sometimes elect to abstain from bidding during the third and fourth quarters which are generally busier. We also sometimes work with Qixing Tower and Nanjing Daji Towers on larger projects where they serve as the primary contractor.

Research and Development

Our research and development activities focus on developing innovative tower products. As of December 31, 2010, we had 16 employees dedicated to research and development. We expect to engage in continuous research and development, to enhance our product and service offerings in our core areas. In addition, we plan to expand our research and development team to support our planned entry into the communication base station and electric system market.

Intellectual Property

We currently hold exclusive licenses for five patents, three of which are licensed from Anhui University of Technology and Science and the other two from the Hangzhou Tianye Communication Equipment Co., Ltd. The table below summarizes our exclusive licenses:

| Description | Licensor | Scope | Term |

| valve spring disassembly device | Anhui University of Technology and Science | Exclusive license for five (5) years granted June 17, 2009 | 10 years |

| mechanical lift | Anhui University of Technology and Science | Exclusive license for five (5) years granted June 17, 2009 | 10 years |

| U-shape bolt disassembly device | Anhui University of Technology and Science | Exclusive license for five (5) years granted May 27, 2009 | 10 years |

| main distribution frame test scheduling module | Hangzhou Tianye Communication Equipment Co., Ltd. | Exclusive license for five (5) years granted April 2, 2008 | 10 years |

| security unit of main distribution frame | Hangzhou Tianye Communication Equipment Co., Ltd. | Exclusive license for five (5) years granted December 6, 2008 | 10 years |

5

We expect to renew our licenses as they expire. We also own our domain name, tectower.com, which has been registered since August 14, 2007.

Employees

As of December 31, 2010, we employed a total of 323 employees. The following table sets forth the number of our employees by function.

| Function | Number of Employees | |

| Sales and Marketing Department | 33 | |

| Procurement Department | 3 | |

| Technical and Research and Development Department | 16 | |

| Management, Financial, and Administrative Office | 44 | |

| Production and Quality Control | 227 | |

| Total | 323 |

Approximately 295 of our employees are located in our executive offices in Anhui, 8 employees are located in Shenzhen, 2 employees are located in Beijing, 10 employees are located in Zhejiang, and 10 employees are located in overseas.

Our employees in China participate in a state pension plan organized by Chinese municipal and provincial governments. We are required to contribute monthly to the plan at the rate of 23% of an employee’s average monthly salary. In addition, we are required by Chinese law to cover employees in China with various types of social insurance. We believe that we are in material compliance with the relevant PRC employment laws.

Insurance

We do not have any business liability, interruption or litigation insurance coverage for our operations in China. Insurance companies in China offer limited business insurance products. While business interruption insurance is available to a limited extent in China, we have determined that the risks of interruption, cost of such insurance and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. Therefore, we are subject to business and product liability exposure. See Item 1A, “Risk Factors – Risks Related to Our Business – We have limited insurance coverage in China.”

Regulation

Because our primary operating subsidiaries are located in China, we are subject to China’s national and local laws, including those outlined below. We believe that we are in material compliance with all registrations and requirements for the issuance and maintenance of all licenses required by the governing bodies, and that all license fees and filings are current.

Environmental Matters

We are subject to various governmental regulations related to environmental protection. Our manufacturing facilities are subject to various pollution control regulations with respect to noise, water and air pollution and the disposal of waste and hazardous materials, including, China’s Environmental Protection Law, China’s Law on the Prevention and Control of Water Pollution and its implementing rules, China’s Law on the Prevention and Control of Air Pollution and its implementing rules, China’s Law on the Prevention and Control of Solid Waste Pollution, and China’s Law on the Prevention and Control of Noise Pollution. We are subject to periodic inspections by local environmental protection authorities. Our operating subsidiaries have received certifications from the relevant PRC government agencies in charge of environmental protection indicating that their business operations are in material compliance with the relevant PRC environmental laws and regulations. We are not currently subject to any pending actions alleging any violations of applicable PRC environmental laws.

6

Foreign Currency Exchange

All of our sales revenue and expenses are denominated in RMB. Under the PRC foreign currency exchange regulations applicable to us, RMB is convertible for current account items, including the distribution of dividends, interest payments, trade and service-related foreign exchange transactions. Currently, our PRC operating subsidiaries may purchase foreign currencies for settlement of current account transactions, including payments of dividends to us, employee salaries (even if employees are based outside of China), and payment for equipment purchases outside of China, without the approval of the State Administration of Foreign Exchange of the People's Republic of China, or SAFE, by complying with certain procedural requirements. Conversion of RMB for capital account items, such as direct investment, loan, security investment and repatriation of investment, however, is still subject to the approval of SAFE. In particular, if our PRC operating subsidiaries borrow foreign currency through loans from us or other foreign lenders, these loans must be registered with SAFE, and if we finance the subsidiaries by means of additional capital contributions, these capital contributions must be approved by certain government authorities, including the Ministry of Commerce, or MOFCOM, or their respective local branches. These limitations could affect our PRC operating subsidiaries' ability to obtain foreign exchange through debt or equity financing. In the event of a liquidation of our PRC subsidiaries, SAFE approval is required before the remaining proceeds can be expatriated from China.

Taxation

On March 16, 2007, the National People's Congress of China passed a new Enterprise Income Tax Law, or EIT Law, and on November 28, 2007, the State Council of China passed its implementing rules, which took effect on January 1, 2008. Before the implementation of the EIT Law, foreign invested enterprises, or FIEs, established in the PRC, unless granted preferential tax treatments by the PRC government, were generally subject to an earned income tax, or EIT, rate of 33.0%, which included a 30.0% state income tax and a 3.0% local income tax. The EIT Law and its implementing rules impose a unified EIT of 25.0% on all domestic-invested enterprises and FIEs, unless they qualify under certain limited exceptions. Despite these changes, the EIT Law gives FIEs established before March 16, 2007, or Old FIEs, a five-year grandfather period during which they can continue to enjoy their existing preferential tax treatments. During this five-year grandfather period, the Old FIEs which enjoyed tax rates lower than 25% under the original EIT law will be subject to gradually increased EIT rates over a 5-year period until their tax rate reaches 25%. In addition, the Old FIEs that are eligible for other preferential tax treatments by the PRC government under the original EIT law are allowed to continue enjoying their preference until these preferential treatment periods expire. Since January 2010, TEC Tower has qualified as a government recognized High- and New-Technology Enterprise and was subject to a reduced EIT rate of 15% for 2010.

In addition to the changes to the current tax structure, under the EIT Law, an enterprise established outside of China with " de facto management bodies" within China is considered a resident enterprise and will normally be subject to an EIT of 25% on its global income. The implementing rules define the term " de facto management bodies" as " an establishment that exercises, in substance, overall management and control over the production, business, personnel, accounting, etc., of a Chinese enterprise." If the PRC tax authorities subsequently determine that we should be classified as a resident enterprise, then our organization's global income will be subject to PRC income tax of 25%. For detailed discussion of PRC tax issues related to resident enterprise status, see Item 1A, " Risk Factors - Risks Related to Doing Business in China - Under the New Enterprise Income Tax Law, we may be classified as a ‘resident enterprise' of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC stockholders.

In addition, the EIT Law and its implementing rules generally provide that a 10% withholding tax applies to China-sourced income derived by non-resident enterprises for PRC enterprise income tax purposes unless the jurisdiction of incorporation of such enterprises'shareholder has a tax treaty with China that provides for a different withholding arrangement. TEC Tower and STT are considered FIEs and are directly held by our subsidiary in Hong Kong. According to a 2006 tax treaty between the Mainland and Hong Kong, dividends payable by an FIE in China to the company in Hong Kong who directly holds at least 25% of the equity interests in the FIE will be subject to a no more than 5% withholding tax. We expect that such 5% withholding tax will apply to dividends paid to TEC HK by TEC Tower and STT, but this treatment will depend on our status as a non-resident enterprise.

Pursuant to the Provisional Regulation of China on Value Added Tax and its implementing rules, all entities and individuals that are engaged in the sale of goods, the provision of repairs and replacement services and the importation of goods in China are generally required to pay value added tax, or VAT, at a rate of 17.0% of the gross sales proceeds received, less any deductible VAT already paid or borne by the taxpayer. Further, when exporting goods, the exporter is entitled to some or all of the refund of VAT that it has already paid or borne.

7

Dividend Distributions

Substantially all of our sales are earned by our PRC subsidiaries. However, PRC regulations restrict the ability of our PRC subsidiaries to make dividends and other payments to its offshore parent company. PRC legal restrictions permit payments of dividends by our PRC subsidiaries only out of their accumulated after-tax profits, if any, determined in accordance with PRC accounting standards and regulations. Our PRC subsidiaries are also required under PRC laws and regulations to allocate at least 10% of their annual after-tax profits determined in accordance with PRC GAAP to a statutory general reserve fund until the amounts in said fund reaches 50% of our registered capital. Allocations to these statutory reserve funds can only be used for specific purposes and are not transferable to us in the form of loans, advances, or cash dividends.

Circular 75

In October 2005, SAFE issued the Notice on Relevant Issues in the Foreign Exchange Control over Financing and Return Investment Through Special Purpose Companies by Residents Inside China, generally referred to as Circular 75, which required PRC residents to register with the competent local SAFE branch before establishing or acquiring control over an offshore special purpose company, or SPV, for the purpose of engaging in an equity financing outside of China on the strength of domestic PRC assets originally held by those residents. Amendments to registrations made under Circular 75 are required in connection with any increase or decrease of capital, transfer of shares, mergers and acquisitions, equity investment or creation of any security interest in any assets located in China to guarantee offshore obligations.

In the case of an SPV which was established, and which acquired a related domestic company or assets, before the implementation date of Circular 75, a retroactive SAFE registration was required to have been completed before March 31, 2006. Failure to comply with the requirements of Circular 75 may result in fines and other penalties under PRC laws for evasion of applicable foreign exchange restrictions. Any such failure could also result in the SPV's affiliates being impeded or prevented from distributing their profits and the proceeds from any reduction in capital, share transfer or liquidation to the SPV, or from engaging in other transfers of funds into or out of China.

As we stated under Item 1A, " Risk factors—Risks Related to Doing Business in China—Failure to comply with PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident stockholders to personal liability, limit our ability to acquire PRC companies or to inject capital into PRC subsidiaries, limit our PRC subsidiaries' ability to distribute profits to us or otherwise materially adversely affect us," we have asked our stockholders, who are PRC residents as defined in Circular 75, to register with the relevant branch of SAFE, as currently required, in connection with their equity interests in us and our acquisitions of equity interests in our PRC subsidiaries. However, many of the terms and provisions in Circular 75 remain unclear and implementation by central SAFE and local SAFE branches of Circular 75 has been inconsistent since their adoption. Therefore, we cannot predict how Circular 75 will affect our business operations or future strategies. For example, our present and prospective PRC subsidiaries' ability to conduct foreign exchange activities, such as the remittance of dividends and foreign currency-denominated borrowings, may be subject to compliance with Circular 75 by our PRC resident beneficial holders.

Mergers and Acquisitions

On August 8, 2006, six PRC regulatory agencies promulgated the Regulation on Mergers and Acquisitions of Domestic Companies by Foreign Investors, or the 2006 M&A Rule, which became effective on September 8, 2006. According to the 2006 M&A Rule, a " Round-trip Investment" is defined as having taken place when a PRC business that is owned by PRC individual(s) is sold to a non-PRC entity that is established or controlled, directly or indirectly, by those same PRC individual(s). Under the 2006 M&A Rules, any Round-trip Investment must be approved by MOFCOM and any indirect arrangement or series of arrangements which achieves the same end result without the approval of MOFCOM is a violation of PRC law.

On May 4, 2010, our Chairman and CEO, Mr. Chun Lu, entered into an option agreement with Mr. Hua Peng Phillip Wong, pursuant to which Mr. Lu was granted an option to acquire 17,797,372 shares our common stock currently owned by Mr. Wong for an exercise price of $1,000,000. Mr. Lu may exercise this option, in whole but not in part, during the period commencing on the 365th day following of the date of the option agreement and ending on the second anniversary of the date thereof. After Mr. Lu exercises this option, he will be our controlling stockholder. His acquisition of our equity interest, or the Acquisition, is required to be registered with the competent administration of industry and commerce authorities, or AIC, in Beijing. Mr. Lu will also be required to make filings with the Beijing SAFE, to register the Company and its non-PRC subsidiaries to qualify them as SPVs, pursuant to Circular 75.

8

As we stated under Item 1A, “Risk factors—Risks Related to Doing Business in China—Our business and financial performance may be materially adversely affected if the PRC regulatory authorities determine that our acquisition of TEC HK constitutes a Round-trip Investment without MOFCOM approval,” the PRC regulatory authorities may take the view that the Acquisition and the reverse acquisition of TEC HK are part of an overall series of arrangements which constitute a Round-trip Investment because at the end of these transactions Mr. Lu will become the majority owner and effective controlling party of a foreign entity that acquired ownership of our Chinese subsidiaries. The PRC regulatory authorities may also take the view that the registration of the Acquisition with the relevant AIC in Beijing and the filings with the Beijing SAFE may not be evidence that the Acquisition has been properly approved because the relevant parties did not fully disclose to the AIC, SAFE or MOFCOM the overall restructuring arrangements, the existence of the reverse acquisition of TEC HK and its link with the Acquisition. If the PRC regulatory authorities take the view that the Acquisition constitutes a Round-trip Investment without MOFCOM approval, they could invalidate our acquisition and ownership of our Chinese subsidiaries. We believe that if this takes place, we may be able to find a way to re-establish control of our Chinese subsidiaries’ business operations through a series of contractual arrangements rather than an outright purchase of our Chinese subsidiaries, but we cannot assure you that such contractual arrangements will be protected by PRC law or that we can receive as complete or effective economic benefit and overall control of our Chinese subsidiaries’ business than if the Company had direct ownership of our Chinese subsidiaries. In addition, we cannot assure you that such contractual arrangements can be successfully effected under PRC law.

ITEM 1A. RISK FACTORS.

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this report, before making an investment decision. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment. You should read the section entitled “Special Note Regarding Forward Looking Statements” above for a discussion of what types of statements are forward-looking statements, as well as the significance of such statements in the context of this report.

RISKS RELATED TO OUR BUSINESS

Our products often are subject to customer testing, inspection and approval.

We frequently supply our tower design services and tower products to prime contractors under subcontractor agreements which incorporate terms of the prime contract and often include the testing, inspection and approval requirements that are a precondition of payment to us by the prime contractor and/or the end-customer. Although we endeavor to satisfy the requirements of each of these contracts to which we are a party, no assurance can be given that the necessary approval of our products and services will be granted on a timely basis or at all, and that we will receive any payments due to us. In some cases, we may be dependent on subcontractors to complete other portions of these projects which may also delay payments to us. Any failure to obtain these approvals and payments may have a material adverse effect on our business and future financial performance

In order to grow at the pace expected by management, we will require additional capital to support our long-term growth strategies. If we are unable to obtain additional capital in future years, we may be unable to proceed with our plans and we may be forced to curtail our operations.

Our working capital requirements and the cash flow provided by future operating activities, if any, will vary greatly from quarter to quarter, depending on the volume of business during the period and payment terms with our customers. We will require additional working capital to support our long-term growth strategies, which includes identifying suitable targets for horizontal or vertical mergers or acquisitions so as to enhance the overall productivity and benefit from economies of scale. However, due to the uncertainty arising out of domestic and global economic conditions and the ongoing tightening of domestic credit markets, we may not be able to generate adequate cash flows or obtain adequate levels of additional financing, whether through equity financing, debt financing or other sources. Even if we are able to get additional financing, it might not be on terms that are favorable to the Company. Furthermore, additional financings could result in significant dilution to our earnings per share or the issuance of securities with rights superior to our current outstanding securities, including registration rights. If we are unable to raise additional financing, we may be unable to implement our long-term growth strategies, develop or enhance our products and services, take advantage of future opportunities or respond to competitive pressures on a timely basis, if at all. In addition, a lack of additional financing could force us to substantially curtail operations.

9

Our business could be adversely affected by reduced levels of cash, whether from operations or from borrowings.

Historically, our principal sources of funds have been cash flows from operations and borrowings from banks and other institutions. Our commercial short term bank loans totaled $12.9 million as of December 31, 2010. Our operating and financial performance may generate less cash and result in our failing to comply with our credit agreement covenants. We were in material compliance with these covenants in 2010, however, our ability to remain compliant in the future will depend on our future financial performance and may be affected by events beyond our control. There can be no assurance that we will generate sufficient earnings and cash flow to remain in compliance with the credit agreement, or that we will be able to obtain future amendments to the credit agreement to avoid a default. In the event of a default, there can be no assurance that we could negotiate a new credit agreement or that we could obtain a new credit agreement with satisfactory terms and conditions within a reasonable time period.

Our business and operations will suffer if prime contractors or end- customers prove to be not creditworthy.

In our industry, companies such as ours that are subcontractors on large transmission construction projects are often subject to the terms of a prime contract, including payment terms. We sometimes do not receive full payment on a project until the prime contractor is paid by the end-customer. Consequently, we extend credit to some of our customers while generally requiring no collateral. Generally, our customers pay in installments, with a portion of the payment upfront, a portion of the payment upon receipt of our products by our customers and before the installation, and a portion of the payment after the installation of our products and upon satisfaction of our customer. Sometimes, a small portion of the payment will not be paid until after a certain period following the installation. We perform ongoing credit evaluations of our customers' financial condition and generally have no difficulties in collecting our payments. However, if we encounter future problems collecting amounts due from our clients or if we experience delays in the collection of amounts due from our clients, our liquidity could be negatively affected. In order to reduce collection risks, we have turned down some opportunities that we believed carried unfavorable payment terms. Our customers are primarily large enterprises with strong recurring cash flow. We believe that we will be able to collect current amounts due from our customers.

If our suppliers fail to perform their contractual obligations, our ability to provide services and products to our customers, as well as our ability to obtain future business, may be harmed.

Many of our products include parts and raw materials procured from other companies upon which we rely to provide a portion of the products that we provide to our customers. There is a risk that we may have disputes with our suppliers, including disputes regarding the quality and timeliness of parts and raw materials provided by these suppliers. A failure by one or more of our suppliers to satisfy the agreed-upon contracts may materially and adversely impact our ability to perform our obligations to our customers, could expose us to liability and could have a material adverse effect on our ability to compete for future contracts and orders.

Because steel is a key material in our business operations, we are subject to the fluctuations in the steel and iron ore market

The primary raw material for our products is steel. Steels prices have fluctuated greatly in recent years. We have taken measures to offset the negative effect of price fluctuations, and entered into long-term supplier relationship with some steel producers at variable prices relative to the market price. However, we cannot predict the future trends of steel prices, and large swings in steel price might greatly affect our profitability.

10

Our success relies on our management’s ability to understand the electric transmission and wireless communication industries.

We target the rapidly evolving electric transmission and wireless communication markets for tower and related products and services. As such, it is critical that our management is able to understand industry trends and make good strategic business decisions. If our management is unable to identify industry trends and act in response to such trends in a way that is beneficial to us, our business will suffer.

If we are unable to respond to the rapid changes in our industries and changes in our customers’ requirements and preferences, our business, financial condition and results of operations could be adversely affected.

If we are unable, for technological, legal, financial or other reasons, to adapt in a timely manner to changing market conditions or customer requirements, we could lose customers and market share. The electric transmission and wireless communication industries are characterized by fairly rapid technological change. Changes in customer requirements and preferences, the frequent introduction of new products and services embodying new technologies and the emergence of new industry standards and practices could render our existing products, services and systems obsolete. The nature of products and services in the electric transmission and wireless communication industries and their rapid evolution will require that we continually improve the performance, features and reliability of our products and services. Our success will depend, in part, on our ability to:

-

enhance our existing products and services;

-

anticipate changing customer requirements by designing, developing, and launching new products and services that address the increasingly sophisticated and varied needs of our current and prospective customers; and

-

respond to technological advances and emerging industry standards and practices on a cost-effective and timely basis.

The development of additional products and services involves significant technological and business risks and requires substantial expenditures and lead time. If we fail to introduce products with new technologies and standards in a timely manner, or adapt our products to these new technologies and standards, our business, financial condition and results of operations could be adversely affected. We cannot assure you that even if we are able to introduce new products or adapt our products to new technologies and standards that our products will gain acceptance among our customers. In addition, from time to time, we or our competitors may announce new products, product enhancements or technological innovations that have the potential to replace or shorten the life cycles of our existing products and that may cause customers to refrain from purchasing our existing products, resulting in inventory obsolescence.

Management has determined that there is a material weakness in our internal controls over financial reporting which even if quickly remedied, could weaken the market’s confidence in our financial statements and lead to fluctuations in our stock price.

As directed by Section 404 of the Sarbanes-Oxley Act of 2002, the SEC adopted rules requiring public companies to include a report of management on the company’s internal controls over financial reporting in their annual reports, including Form 10-K. In addition, the independent registered public accounting firm auditing a company’s financial statements must also attest to and report on the operating effectiveness of our internal controls. We are subject to the requirement to provide management report on the company’s controls over financial reporting and a report of our management for the 2010 fiscal year is included under Item 9A of this annual report. The auditor attestation is not required as we are currently a smaller reporting company. The portion of this process completed thus far has revealed material weaknesses in internal controls that will require remediation. See “Item 9A. Control and Procedures.” The remediation process may also be expensive and time consuming, and even though the management is committed to improving its internal controls, management can give no assurance that the remediation effort will be completed on time or be effective. In addition, management can give no assurance that additional material weaknesses in internal controls will not be discovered. Management also can give no assurance that the process of evaluation and the auditor’s attestation will be completed on time, when required. The disclosure of a material weakness, even if quickly remedied, could weaken the market’s confidence in our financial statements and lead to fluctuations in our stock price, especially if a restatement of financial statements for past periods is required. In addition, if we are unable to adequately design our internal control systems, or prepare an " internal control report" to the satisfaction of our auditors, our auditors may issue a qualified opinion on our financial statements.

11

We may not be able to maintain or improve our competitive position in the electric transmission and wireless communication industries, and we expect this competition to continue to be intense.

China's electric transmission and wireless communication industries are large and established, though rapidly evolving. Our primary competition comes from domestic companies such as Meteno Communication Technologies, Qixing Tower, and Nanjing Daji Towers. Additional competition comes from large international companies such as Valmont Industries, Inc. (NYSE:VMI). Some of our international competitors are larger than us and possess greater name recognition, assets, personnel, sales and financial resources. These entities may be able to respond more quickly to changing market conditions by developing new products and services that meet customer requirements or are otherwise superior to our products and services and may be able to more effectively market their products than we can because they have significantly greater financial, technical and marketing resources than we do. They may also be able to devote greater resources than we can to the development, promotion and sale of their products. Increased competition could require us to reduce our prices, result in our receiving fewer customer orders, and result in our loss of market share. We cannot assure you that we will be able to distinguish ourselves in a competitive market. To the extent that we are unable to successfully compete against existing and future competitors, our business, operating results and financial condition could be materially adversely affected.

If we are unable to attract and retain senior management and qualified technical and sales personnel, our operations, financial condition and prospects will be materially adversely affected.

Our future success depends in part on the contributions of our management team and key technical and sales personnel and our ability to attract and retain qualified new personnel. In particular, our success depends on the continuing employment of our Chief Executive Officer, Mr. Chun Lu, our Vice President of Sales and Marketing, Mr. Debin Chen, and our Chief Technology Officer, Mr. Baojia He. There is significant competition in our industry for qualified managerial, technical and sales personnel and we cannot assure you that we will be able to retain our key senior managerial, technical and sales personnel or that we will be able to attract, integrate and retain other such personnel that we may require in the future. If we are unable to attract and retain key personnel in the future, our business, operations, financial condition, results of operations and prospects could be materially adversely affected.

Management's estimates and assumptions affect reported amounts of expenses and changes in those estimates could impact operating results.

We recognize export tax refund as assets for the expected future tax consequences of events which are included in the financial statements or tax returns. In assessing the whether tax refund assets are realizable, management makes certain assumptions about whether the tax refunds assets will be realized. We expect the tax refund assets currently recorded to be fully realizable, however there can be no assurance that changes in government policies could lead to uncertainties in the future.

We have limited insurance coverage in China.

We do not have any business liability, interruption or litigation insurance coverage for our operations in China. While business interruption insurance and other types of insurance are available to a limited extent in China, we have determined that the risks of interruption, cost of such insurance and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. Therefore, our existing insurance coverage may not be sufficient to cover all risks associated with our business. As a result, we may be required to pay for financial and other losses, damages and liabilities, including those caused by natural disasters and other events beyond our control, out of our own funds, which could have a material adverse effect on our business, financial condition and results of operations.

Our limited ability to protect our licensed intellectual property, and the possibility that this technology could inadvertently infringe technology owned by others, may adversely affect our ability to compete.

We currently hold exclusive licenses for five patents, three of which are licensed from Anhui University of Technology and Science and the other two from the Hangzhou Tianye Communication Equipment Co., Ltd. A successful challenge to the ownership of this technology by third parties could materially damage our business prospects. Our competitors may assert that the technologies or products infringe on their patents or proprietary rights. We may be required to obtain from others licenses that may not be available on commercially reasonable terms, if at all. Problems with intellectual property rights could increase the cost of our products or delay or preclude our new product development and commercialization. If infringement claims against us or our licensors are deemed valid, we may not be able to obtain appropriate licenses on acceptable terms or at all. Litigation could be costly and time-consuming but may be necessary to protect our technology license positions or to defend against infringement claims.

12

Environmental regulations impose substantial costs and limitations on our operations.

We are subject to various national and local environmental laws and regulations in China concerning issues such as air emissions, wastewater discharges, and solid waste management and disposal. These laws and regulations can restrict or limit our operations and expose us to liability and penalties for non-compliance. While we believe that our facilities are in material compliance with all applicable environmental laws and regulations, the risks of substantial unanticipated costs and liabilities related to compliance with these laws and regulations are an inherent part of our business. It is possible that future conditions may develop, arise or be discovered that create new environmental compliance or remediation liabilities and costs. While we believe that we can comply with existing environmental legislation and regulatory requirements and that the costs of compliance have been included within budgeted cost estimates, compliance may prove to be more limiting and costly than anticipated.

Our business and reputation as a provider of transmission and communication towers may be adversely affected by product defects or performance.

We believe that we offer high quality products that are reliable and competitively priced. If our products do not perform to specifications, we might be required to redesign or recall those products or pay substantial damages. Such an event could result in significant expenses, disrupt sales and affect our reputation and that of our products. In addition, product defects could result in substantial product liability. We do not have product liability insurance. If we face significant liability claims, our business, financial condition, and results of operations would be adversely affected.

If we become directly subject to the recent scrutiny, criticism and negative publicity involving U.S.-listed Chinese companies, we may have to expend significant resources to investigate and resolve the matter which could harm our business operations, stock price and reputation and could result in a loss of your investment in our stock, especially if such matter cannot be addressed and resolved favorably.

Recently, U.S. public companies that have substantially all of their operations in China, particularly companies like us which have completed so-called reverse merger transactions, have been the subject of intense scrutiny, criticism and negative publicity by investors, financial commentators and regulatory agencies, such as the United States Securities and Exchange Commission. Much of the scrutiny, criticism and negative publicity has centered around financial and accounting irregularities and mistakes, a lack of effective internal controls over financial accounting, inadequate corporate governance policies or a lack of adherence thereto and, in many cases, allegations of fraud. As a result of the scrutiny, criticism and negative publicity, the publicly traded stock of many U.S. listed Chinese companies has sharply decreased in value and, in some cases, has become virtually worthless. Many of these companies are now subject to shareholder lawsuits, SEC enforcement actions and are conducting internal and external investigations into the allegations. It is not clear what effect this sector-wide scrutiny, criticism and negative publicity will have on our company, our business and our stock price. If we become the subject of any unfavorable allegations, whether such allegations are proven to be true or untrue, we will have to expend significant resources to investigate such allegations and/or defend our company. This situation will be costly and time consuming and distract our management from growing our company. If such allegations are not proven to be groundless, our company and business operations will be severely and your investment in our stock could be rendered worthless.

RISKS RELATED TO DOING BUSINESS IN CHINA

Changes in China's political or economic situation could harm us and our operating results.

13

Economic reforms adopted by the Chinese government have had a positive effect on the economic development of the country, but the government could change these economic reforms or any of the legal systems at any time. This could either benefit or damage our operations and profitability. Some of the things that could have this effect are:

-

Level of government involvement in the economy;

-

Control of foreign exchange;

-

Methods of allocating resources;

-

Balance of payments position;

-

International trade restrictions; and

-

International conflict.

The Chinese economy differs from the economies of most countries belonging to the Organization for Economic Cooperation and Development, or OECD, in many ways. For example, state-owned enterprises still constitute a large portion of the Chinese economy, and weak corporate governance and the lack of a flexible currency exchange policy still prevail in China. As a result of these differences, we may not develop in the same way or at the same rate as might be expected if the Chinese economy was similar to those of the OECD member countries.

Future government regulations or other standards could have an adverse effect on our operations.

Our operations are subject to a variety of laws, regulations and licensing requirements of national and local authorities in the PRC. We are required to obtain licenses or permits from the PRC central government and from Anhui province, where we operate, and to meet certain standards in the conduct of our business. The loss of such licenses, or the imposition of conditions to the granting or retention of such licenses, could have an adverse effect on us. In the event that these laws, regulations and/or licensing requirements change, we may be required to modify our operations or to utilize resources to maintain compliance with such rules and regulations. In addition, new regulations may be enacted that could have an adverse effect on us.

Uncertainties with respect to the PRC legal system could limit the legal protections available to you and us.

We conduct substantially all of our business through our subsidiaries in the PRC. Our subsidiaries are generally subject to laws and regulations applicable to foreign investments in China and, in particular, laws applicable to foreign-invested enterprises. The PRC legal system is based on written statutes, and prior court decisions may be cited for reference but have limited precedential value. Since 1979, a series of new PRC laws and regulations have significantly enhanced the protections afforded to various forms of foreign investments in China. However, since the PRC legal system continues to evolve rapidly, the interpretations of many laws, regulations, and rules are not always uniform, and enforcement of these laws, regulations, and rules involve uncertainties, which may limit legal protections available to you and us. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention. In addition, all of our executive officers and directors are residents of China and not of the United States, and substantially all the assets of these persons are located outside the United States. As a result, it could be difficult for investors to affect service of process in the United States or to enforce a judgment obtained in the United States against our Chinese operations and subsidiaries.

You may have difficulty enforcing judgments against us.

Most of our assets are located outside of the United States and all of our current operations are conducted in the PRC. In addition, all of our directors and officers are nationals and residents of countries other than the United States. A substantial portion of the assets of these persons is located outside the United States. As a result, it may be difficult for you to effect service of process within the United States upon these persons. It may also be difficult for you to enforce in U.S. courts judgments on the civil liability provisions of the U.S. federal securities laws against us and our officers and directors, most of whom are not residents in the United States and the substantial majority of whose assets are located outside of the United States. In addition, there is uncertainty as to whether the courts of the PRC would recognize or enforce judgments of U.S. courts. Our counsel as to PRC law has advised us that the recognition and enforcement of foreign judgments are provided for under the PRC Civil Procedures Law. Courts in China may recognize and enforce foreign judgments in accordance with the requirements of the PRC Civil Procedures Law based on treaties between China and the country where the judgment is made or on reciprocity between jurisdictions. China does not have any treaties or other arrangements that provide for the reciprocal recognition and enforcement of foreign judgments with the United States. In addition, according to the PRC Civil Procedures Law, courts in the PRC will not enforce a foreign judgment against us or our directors and officers if they decide that the judgment violates basic principles of PRC law or national sovereignty, security, or the public interest. So it is uncertain whether a PRC court would enforce a judgment rendered by a court in the United States.

14

The PRC government exerts substantial influence over the manner in which we must conduct our business activities.

The PRC government has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to operate in China may be harmed by changes in its laws and regulations, including those relating to taxation, import and export tariffs, environmental regulations, land use rights, property, and other matters. We believe that our operations in China are in material compliance with all applicable legal and regulatory requirements. However, the central or local governments of the jurisdictions in which we operate may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on our part to ensure our compliance with such regulations or interpretations.

Accordingly, government actions in the future, including any decision not to continue to support recent economic reforms and to return to a more centrally planned economy or regional or local variations in the implementation of economic policies, could have a significant effect on economic conditions in China or particular regions thereof and could require us to divest ourselves of any interest we then hold in Chinese properties or joint ventures.

Future inflation in China may inhibit our ability to conduct business in China.

In recent years, the Chinese economy has experienced periods of rapid expansion and highly fluctuating rates of inflation. During the past ten years, the rate of inflation in China has been as high as 5.9% and as low as -0.8% . These factors have led to the adoption by the Chinese government, from time to time, of various corrective measures designed to restrict the availability of credit or regulate growth and contain inflation. High inflation may in the future cause the Chinese government to impose controls on credit and/or prices, or to take other action, which could inhibit economic activity in China, and thereby harm the market for our products and our company.

Restrictions on currency exchange may limit our ability to receive and use our sales effectively.

The majority of our sales will be settled in RMB and U.S. dollars, and any future restrictions on currency exchanges may limit our ability to use revenue generated in RMB to fund any future business activities outside China or to make dividend or other payments in U.S. dollars. Although the Chinese government introduced regulations in 1996 to allow greater convertibility of the RMB for current account transactions, significant restrictions still remain, including primarily the restriction that foreign-invested enterprises may only buy, sell or remit foreign currencies after providing valid commercial documents, at those banks in China authorized to conduct foreign exchange business. In addition, conversion of RMB for capital account items, including direct investment and loans, is subject to governmental approval in China, and companies are required to open and maintain separate foreign exchange accounts for capital account items. We cannot be certain that the Chinese regulatory authorities will not impose more stringent restrictions on the convertibility of the RMB.

Fluctuations in exchange rates could adversely affect our business and the value of our securities.

The value of our common stock will be indirectly affected by the foreign exchange rate between the U.S. dollar and RMB and between those currencies and other currencies in which our sales may be denominated. Appreciation or depreciation in the value of the RMB relative to the U.S. dollar would affect our financial results reported in U.S. dollar terms without giving effect to any underlying change in our business or results of operations. Fluctuations in the exchange rate will also affect the relative value of any dividend we issue that will be exchanged into U.S. dollars, as well as earnings from, and the value of, any U.S. dollar-denominated investments we make in the future.

Since July 2005, the RMB has no longer been pegged to the U.S. dollar. Although the People's Bank of China regularly intervenes in the foreign exchange market to prevent significant short-term fluctuations in the exchange rate, the RMB may appreciate or depreciate significantly in value against the U.S. dollar in the medium to long term. Moreover, it is possible that in the future PRC authorities may lift restrictions on fluctuations in the RMB exchange rate and lessen intervention in the foreign exchange market.

15

Very limited hedging transactions are available in China to reduce our exposure to exchange rate fluctuations. To date, we have not entered into any hedging transactions. While we may enter into hedging transactions in the future, the availability and effectiveness of these transactions may be limited, and we may not be able to successfully hedge our exposure at all. In addition, our foreign currency exchange losses may be magnified by PRC exchange control regulations that restrict our ability to convert RMB into foreign currencies.

Restrictions under PRC law on our PRC subsidiaries' ability to make dividends and other distributions could materially and adversely affect our ability to grow, make investments or acquisitions that could benefit our business, pay dividends to you, and otherwise fund and conduct our business.

Substantially all of our sales are earned by our PRC subsidiaries. However, as discussed more fully under Item 1, " Business - Regulation - Dividend Distributions," PRC regulations restrict the ability of our PRC subsidiaries to make dividends and other payments to their offshore parent company. Any limitations on the ability of our PRC subsidiaries to transfer funds to us could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends and otherwise fund and conduct our business.

Failure to comply with PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident stockholders to personal liability, limit our ability to acquire PRC companies or to inject capital into PRC subsidiaries, limit our PRC subsidiaries' ability to distribute profits to us or otherwise materially adversely affect us.

In October 2005, SAFE issued the Notice on Relevant Issues in the Foreign Exchange Control over Financing and Return Investment Through Special Purpose Companies by Residents Inside China, generally referred to as Circular 75. Circular 75 requires PRC residents to register with the competent local SAFE branch before establishing or acquiring control over an SPV for the purpose of engaging in an equity financing outside of China. See Item 1, " Business - Regulation - Circular 75" for a detailed discussion of Circular 75 and its implementation.

We have asked our stockholders, who are PRC residents as defined in Circular 75, to register with the relevant branch of SAFE as currently required in connection with their equity interests in us and our acquisitions of equity interests in our PRC subsidiaries. However, we cannot provide any assurances that they can obtain the above SAFE registrations required by Circular 75. Moreover, because of uncertainty over how Circular 75 will be interpreted and implemented, and how or whether SAFE will apply it to us, we cannot predict how it will affect our business operations or future strategies. For example, our present and prospective PRC subsidiaries' ability to conduct foreign exchange activities, such as the remittance of dividends and foreign currency-denominated borrowings, may be subject to compliance with Circular 75 by our PRC resident beneficial holders.

Our business and financial performance may be materially adversely affected if the PRC regulatory authorities determine that our acquisition of TEC HK constitutes a Round-trip Investment without MOFCOM approval.

On August 8, 2006, six PRC regulatory agencies promulgated the Regulation on Mergers and Acquisitions of Domestic Companies by Foreign Investors, referred to as the 2006 M&A Rule, which regulate " Round-trip Investments," defined as having taken place when a PRC business that is owned by PRC individual(s) is sold to a non-PRC entity that is established or controlled, directly or indirectly, by those same PRC individual(s). See Item 1, " Business - Regulation - Mergers and Acquisitions" for a detailed discussion of the 2006 M&A Rule.

The PRC regulatory authorities may take the view that Mr. Chun Lu's acquisition of our equity interest (following exercise of his option) and the reverse acquisition of TEC HK are part of an overall series of arrangements which constitute a Round-trip Investment because at the end of these transactions, Mr. Lu will become the majority owner and effective controlling party of a foreign entity that acquired ownership of our Chinese subsidiaries. The PRC regulatory authorities may also take the view that the registration of the Acquisition with the relevant AIC in Beijing and the filings with the Beijing SAFE may not be evidence that the Acquisition has been properly approved because the relevant parties did not fully disclose to the AIC, SAFE or MOFCOM the overall restructuring arrangements, the existence of the reverse acquisition and its link with the Acquisition. If the PRC regulatory authorities take the view that the Acquisition constitutes a Round-trip Investment under the 2006 M&A Rule, we cannot assure you we may be able to obtain the approval required from MOFCOM.

16

If the PRC regulatory authorities take the view that the Acquisition constitutes a Round-trip Investment without MOFCOM approval, they could invalidate our acquisition and ownership of our Chinese subsidiaries. Additionally, the PRC regulatory authorities may take the view that the Acquisition constitutes a transaction which requires the prior approval of the China Securities Regulatory Commission, or CSRC, before MOFCOM approval is obtained. We believe that if this takes place, we may be able to find a way to re-establish control of our Chinese subsidiaries' business operations through a series of contractual arrangements rather than an outright purchase of our Chinese subsidiaries, but we cannot assure you that such contractual arrangements will be protected by PRC law or that we can receive as complete or effective economic benefit and overall control of our Chinese subsidiaries' business than if the Company had direct ownership of our Chinese subsidiaries. In addition, we cannot assure you that such contractual arrangements can be successfully effected under PRC law. If we cannot obtain MOFCOM or CSRC approval if required by the PRC regulatory authorities to do so, and if we cannot put in place or enforce relevant contractual arrangements as an alternative and equivalent means of control of our Chinese subsidiaries, our business and financial performance will be materially adversely affected.

Under the New Enterprise Income Tax Law, we may be classified as a " resident enterprise" of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC stockholders.

The EIT Law and its implementing rules became effective on January 1, 2008. Under the EIT Law, an enterprise established outside of China with " de facto management bodies" within China is considered a " resident enterprise," meaning that it can be treated in a manner similar to a Chinese enterprise for enterprise income tax purposes. The implementing rules of the EIT Law define de facto management as " substantial and overall management and control over the production and operations, personnel, accounting, and properties" of the enterprise.