Attached files

| file | filename |

|---|---|

| EX-31.2 - CERTIFICATION - CFN Enterprises Inc. | ex31-2.htm |

| EX-31.1 - CERTIFICATION - CFN Enterprises Inc. | ex32-1.htm |

| EX-23.1 - CONSENT - CFN Enterprises Inc. | ex23-1.htm |

| EX-31.1 - CERTIFICATION - CFN Enterprises Inc. | ex31-1.htm |

| EX-10.21 - LOAN AGREEMENT - CFN Enterprises Inc. | ex10-21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to _________.

Commission file number 000-52635

|

ACCELERIZE NEW MEDIA, INC.

|

||

|

(Exact name of registrant as specified in its charter)

|

|

Delaware

|

20-3858769

|

|

|

(State of Incorporation)

|

(IRS Employer Identification No.)

|

|

204 RIVERSIDE AVENUE, NEWPORT BEACH, CALIFORNIA 92663

|

||

|

(Address of principal executive offices) (Zip Code)

|

Registrant's telephone number, including area code: (949) 515 2141

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $0.001

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by checkmark whether the registrant submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer [ ] Accelerated filer [ ]

Non-accelerated filer [ ] Smaller reporting company [X]

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [ X]

The aggregate market value of the common equity voting shares of the registrant held by non-affiliates on June 30, 2010, the registrant's most recently completed second fiscal quarter, was $7,002,092. For purposes of this calculation, an aggregate of 11,000,000 shares of Common Stock were held by the directors and officers of the registrant on June 30, 2010 and have been included in the number of shares of Common Stock held by affiliates.

The number of the registrant’s shares of Common Stock outstanding as of March 29, 2011: 35,803,593.

In this Annual Report on Form 10-K, the terms the “Company,” “Accelerize”, “we”, “us” or “our” refers to Accelerize New Media, Inc., unless the context indicates otherwise.

WARNING CONCERNING FORWARD LOOKING STATEMENTS

THIS ANNUAL REPORT CONTAINS STATEMENTS WHICH CONSTITUTE FORWARD LOOKING STATEMENTS WITHIN THE MEANING OF THE FEDERAL SECURITIES LAWS. ALSO, WHENEVER WE USE WORDS SUCH AS “BELIEVE”, “EXPECT”, “ANTICIPATE”, “INTEND”, “PLAN”, “ESTIMATE” OR SIMILAR EXPRESSIONS, WE ARE MAKING FORWARD LOOKING STATEMENTS. FOR EXAMPLE, WHEN WE DISCUSS THE INTERNET MARKET TRENDS, AND SPECIFICALLY, THE GROWTH IN ON-LINE ADVERTISING, LEAD GENERATION, PERFORMANCE BASED MARKETING, AND SOFTWARE-AS-A-SERVICE, AND OUR EXPECTATIONS BASED ON SUCH TRENDS, WE ARE USING FORWARD LOOKING STATEMENTS. THESE FORWARD LOOKING STATEMENTS ARE BASED UPON OUR PRESENT INTENT, BELIEFS OR EXPECTATIONS, BUT FORWARD LOOKING STATEMENTS ARE NOT GUARANTEED TO OCCUR AND MAY NOT OCCUR. ACTUAL RESULTS MAY DIFFER MATERIALLY FROM THOSE CONTAINED IN OR IMPLIED BY OUR FORWARD LOOKING STATEMENTS AS A RESULT OF VARIOUS FACTORS.

IMPORTANT FACTORS THAT COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE IN OUR FORWARD LOOKING STATEMENTS INCLUDE, AMONG OTHERS, GENERAL MARKET CONDITIONS, INCLUDING THE RECENT DOWNTURN IN THE ECONOMY AND THE GROWTH IN CONSUMER DEBT, REGULATORY DEVELOPMENTS AND OTHER CONDITIONS WHICH ARE NOT WITHIN OUR CONTROL.

OTHER RISKS MAY ADVERSELY IMPACT US, AS DESCRIBED MORE FULLY IN THIS ANNUAL REPORT UNDER “ITEM 1A. RISK FACTORS.”

YOU SHOULD NOT PLACE UNDUE RELIANCE UPON FORWARD LOOKING STATEMENTS.

EXCEPT AS REQUIRED BY LAW, WE UNDERTAKE NO OBLIGATION TO UPDATE OR REVISE ANY FORWARD LOOKING STATEMENTS AS A RESULT OF NEW INFORMATION, FUTURE EVENTS OR OTHERWISE.

|

ACCELERIZE NEW MEDIA, INC.

2010 ANNUAL REPORT ON FORM 10-K

|

||

|

Table of Contents

|

||

|

PART I

|

||

|

Page

|

||

|

Item 1.

|

Business

|

4

|

|

Item 1A.

|

Risk Factors

|

8

|

|

Item 1B.

|

Unresolved Staff Comments

|

14

|

|

Item 2.

|

Properties

|

14

|

|

Item 3.

|

Legal Proceedings

|

14

|

|

Item 4.

|

[Removed and Reserved]

|

14

|

|

PART II

|

||

|

Item 5.

|

Market For The Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities`

|

14

|

|

Item 6.

|

Selected Financial Data

|

16

|

|

Item 7.

|

Management ’s Discussion and Analysis of Financial Condition and Results of Operations

|

16

|

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

21

|

|

Item 8.

|

Financial Statements and Supplementary Data

|

21

|

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

21

|

|

Item 9A.

|

Controls and Procedures

|

21

|

|

Item 9B.

|

Other Information

|

22

|

|

PART III

|

||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

22

|

|

Item 11.

|

Executive Compensation

|

24

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

25

|

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

27

|

|

Item 14.

|

Principal Accountant Fees and Services

|

27

|

|

PART IV

|

||

|

Item 15.

|

Exhibits and Financial Statement Schedules

|

28

|

3

PART I

Item 1. Business

Overview

We are a multifaceted online marketing services company specializing in the development of performance based marketing programs and related software solutions for businesses interested in expanding their online advertising presence. The Company owns and operates www.cakemarketing.com, an internally-developed Software-as-a-Service, or SaaS, platform. Cake Marketing is a hosted software solution that provides an all-inclusive suite of management services for online marketing campaigns. From tracking and reporting to lead distribution, our patent-pending software enables advertisers, affiliate marketers and lead generators a fully scalable and accurate platform developed with a combination of innovative technology and an imaginative approach to doing business online.

The Company has an extensive portfolio of approximately 5,500 URLs, also known as domain names. Our URL portfolio is currently used to build consumer-based financial portals, microsites, blogs, and landing pages used for lead generation initiatives. In addition, we own and develop various portals, and websites, including: www.secfilings.com, which provides to subscribers real-time alerts based on reports filed by various companies and individuals with the Securities and Exchange Commission, or the SEC. Also through www.accelerizefinancial.com the Company offers advertisers access to an audience of active individual investors, institutional investors, financial planners, registered advisors, journalists, investment bankers and brokers. Our financial portals and URL portfolio target a niche demographic that is qualified by the content they seek. This media strategy drives new membership, which results in recurring user traffic to our websites and allows us to generate highly relevant responses and leads for our online advertising and lead generation customers.

In February 2011 we decided to discontinue our Lead Generation Division, in order to focus our efforts and resources on our SaaS products and services. After careful review by our management, it became clear that although the Lead Generation Division was a substantial source of revenue for the Company, it was only marginally profitable, and required substantial management attention and financial resources, which would otherwise be invested in more profitable channels. In addition, we decided to discontinue our Lead Generation Division to avoid potential conflicts of interest with our SaaS customers, who are providing similar lead generation services. Subsequently, we sold certain assets related to our Lead Generation Division. Commencing March 1, 2011, we no longer offer lead generation services.

As of the end of 2008 we closed our debt settlement referrals division. However in 2009 and 2010 we still received fees for sales and marketing support we provided in connection with debt settlement solutions prior to closing this unit. These payments gradually decreased in 2009 and 2010, and we expect that they will be eliminated by the end of 2011.

On January 1, 2011 we moved our principal offices to 204 Riverside Avenue, Newport Beach, CA 92663. Our telephone number there is: (949) 515 2141. Our corporate website is: www.accelerizenewmedia.com, the contents of which are not part of this annual report.

Industry and Market Opportunity

Software-as-a-Service, Online Advertising and Performance Based Marketing Statistics

|

|

·

|

IDC expects the market for SaaS to grow at a compound annual growth rate of 25.3% between 2009 and 2014, compared to just 5.8% for packaged software.

|

|

|

·

|

IDC projects that SaaS's market share will expand from less than 5% of the total software market in 2009 to more than 11% by 2014.

|

|

|

·

|

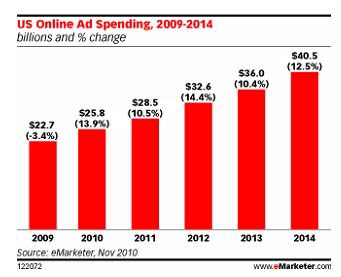

IDC projects that SaaS revenues will increase to $40.5 billion by 2014, from just $13.1 billion in 2009.

|

|

|

·

|

Gartner projects that 25% of new business software will be delivered as SaaS by 2011 (0.7 probability).

|

|

|

·

|

AMR International, according to a March 4, 2010 article in eMarketer Digital Intelligence, predicts that business-to-business online advertising spending will increase at a compounded annual growth rate of 12% between 2009 and 2013.

|

|

|

·

|

62% of businesses have insufficient ability to measure effectiveness of their advertising campaigns, according to Marketing and Media Ecosystem's 2010 Survey.

|

|

|

·

|

58% of leading companies believe that direct partnerships with media companies are important, according to Marketing and Media Ecosystem's 2010 Survey.

|

|

|

·

|

IDC expects internet advertising to grow 15% to 20% per year to reach $106.6 billion this year (Digital Marketplace Model and Forecast). Meanwhile, the U.S. will lead the world in both total advertising spending and online ad spending with expenditures in 2011 of more than $265 billion and $45 billion, respectively.

|

|

|

·

|

The Yankee Group expects the U.S. online ad market to hit $50.3 billion in 2011, when online will comprise nearly 25% of all media consumption and 15% of the ad spend, with the underlying reasons being the disparity between current media usage and spending by marketers.

|

4

(http://bitcadet.com/wp-content/uploads/online_ad_foecasts_2011.gif)

Additional Characteristics

Online marketing is still a costly proposition. CPMs tend to be slightly higher than other traditional media. Accordingly, customer acquisitions costs can easily become astronomical, if left unchecked. Risks associated with customer acquisition costs are as follows:

|

|

·

|

Anonymity of customer base: it is extremely difficult to identify the demographics and psychographics of online users, even with existing search tools;

|

|

|

·

|

Fraudulent procurement or creation of customer leads: some publishers provide fraudulent data to advertisers to increase their revenue;

|

|

|

·

|

Psychographics of the Internet: this leaves several paid leads unutilized; and

|

|

|

·

|

Marketing programs: performance is still poorly measured and not automated.

|

Our Solutions

We believe that our business depends upon the continuing increase of consumer and business use of the Internet as a primary tool to facilitate research, communications and transactions, especially in the following segments:

5

Software-as-a-Service for Performance Based Marketing

The company owns and operates www.cakemarketing.com, an internally-developed SaaS platform. Cake Marketing is a hosted software solution that provides an all-inclusive suite of management services for online marketing campaigns. From tracking and reporting to lead distribution, our patent-pending software enables advertisers, affiliate marketers and lead generators a fully scalable and accurate platform developed with a combination of innovative technology and an imaginative approach to doing business online.

Cake Marketing allows users the ability to qualify leads and conversions using proprietary business rules, thus reducing the number of fraudulent leads. It also allows for real-time management of customer acquisition costs and realization rates for each marketing program. Additional performance tools allow for analysis of customer-centric performance as well as real-time consolidated data. Also, our software enables access to certain psychographics and demographics for each potential lead, revealing trends relevant to marketers.

We leverage off the expertise of the following third-party companies in providing our services:

|

●

|

TARGUSinfo, a provider of On-Demand Insight® to various brands, links and delivers real-time attributes to drive smarter customer interactions on the Web, over the phone and at the point of sale.

|

|

●

|

The Planet, provides On Demand IT Infrastructure solutions, hosting more than 20,000 small- and medium-size businesses and 15.7 million Web sites worldwide; and

|

|

●

|

Rackspace Hosting, which operates in the hosting and cloud computing industry. It provides information technology (IT) as a service, managing Web-based IT systems for small and medium-sized businesses, as well as large enterprises worldwide.

|

Online Marketing Services

We own and develop various portals, and websites, including: www.secfilings.com, which provides to subscribers real-time alerts based on reports filed by various companies and individuals with the SEC. Also, through www.accelerizefinancial.com the Company offers advertisers and publicly-traded companies access to an audience of active individual investors, institutional investors, financial planners, registered advisors, journalists, investment bankers and brokers. Our financial portals and URL portfolio target a niche demographic that is qualified by the content they seek.

We leverage off the expertise of the following third-party companies in providing our services:

|

●

|

Edgar Online, Inc. provides financial content and engages in the creation and distribution of fundamental financial data and public filings for equities, mutual funds, and other publicly traded assets principally in the United States. It produces data that assists in the analysis of the financial, business, and ownership conditions of an investment. The company delivers its information products via the Internet in the form of end-user subscriptions and data feeds;

|

|

●

|

Financial Content Services, Inc., provides stock market data, business news and content syndication services;

|

|

●

|

Maximum ASP, LLC hosts our servers and provides comprehensive network protection, automated server patching, and advanced server monitoring, with a strong focus on hosting solutions that combine avanced monitoring and management tools |

|

●

|

Zacks Investment Research Inc. markets segments of our ad inventory. Zacks is a Chicago based firm with over 25 years of experience in providing institutional and individual investors with the analytical tools nd financial information necessary to the success of their investment process;

|

|

●

|

Opt-Intelligence Inc. in partnership with Zacks, assists us with real-time consumer opt-in advertising (commonly called Co-registration). Opt-Intelligence clients include TheStreet.com, Match.com and StarMagazine.com. Their advertiser list includes, eBay, Wal-Mart, The Home Depot, NASCAR, Nokia and Procter & Gamble. Co-registration is the practice of one organization, on its own subscription and membership registration forms, offering subscriptions, memberships, or leads to another organization; and

|

|

●

|

Lake Group Media whose services include list brokerage, list management and interactive programs.

|

How we market our services

Software-as-a-Service for Performance Based Marketing

We use our internal sales force to market Cake Marketing to lead generation firms, affiliate marketers and advertising agencies. Additionally we market our software through www.cakemarketing.com, and by attending industry trade shows and events. Our clients utilize our software to provide performance based marketing services to corporations worldwide.

6

Online Marketing Services

Utilizing our internal sales force and www.accelerizefinancial.com we market our online marketing services to advertisers and publicly-traded companies. Targeting a niche demographic we offer advertisers and publicly-traded companies access to an audience of active individual investors, institutional investors, financial planners, registered advisors, journalists, investment bankers and brokers.

Our online marketing services are provided primarily through the following financial portals:

|

·

|

www.secfilings.com, a financial business networking portal delivering free, accurate SEC data and user-generated content. Users can retrieve historical filings, subscribe to free email alerts and RSS feeds, and can track SEC filings by company, industry or person;

|

|

·

|

www.executivedisclosure.com, a financial and business networking blog offering news and information about salaries, bonuses, option grants, and stock award data provided by all publicly-held companies;

|

|

·

|

www.investerms.com, which provides investors with real-time news and education, syndicated across a wide network of distribution partners. Content is aimed to help readers fully understand the news by presenting it in an easy-to-understand manner;

|

|

·

|

www.otcroadshow.com, which generates investor awareness for public and private companies. Our team creates company reports, marketing materials and supplementary materials that are then put in front of a targeted audience to garner company awareness, business leads, and real time feedback on products/services;

|

|

·

|

www.theotcinvestor.com, a provider of OTC-BB and Pinksheet news, research and insights. The growing number of members can give many micro-cap companies the exposure they are looking for while an expert team of financial writers produces quality content to keep investors coming back for more;

|

|

·

|

www.form10-k.com, an example of one of our "micro-site" properties, offering to customers and users select functionality from our main portals including the ability to search financial information and drive targeted leads for our customers;

|

|

·

|

www.chinesepubliccompanies.com, a source of information on Chinese stocks and U.S. listed Chinese ADR securities listed both on central exchanges and OTC.BB. In an uncertain and difficult to interpret market, the website provides an independent, unbiased source for news, research, insights and other information about foreign companies based in or operating in China; and

|

|

·

|

www.biotechstocktrader.com, a leading news and information portal for investors in pharmaceutical and biotechnology firms.

|

Intellectual Property

Our employees are required to execute confidentiality and non-use agreements that transfer any rights they may have in copyrightable works or patentable technologies to us. In addition, prior to entering into discussions with potential business partners or customers regarding our business and technologies, we generally require that such parties enter into nondisclosure agreements with us. If these discussions result in a license or other business relationship, we also generally require that the agreement setting forth the parties’ respective rights and obligations include provisions for the protection of our intellectual property rights. For example, the standard language in our agreements provides that we retain ownership of all patents and copyrights in our technologies and requires our customers to display our copyright and trademark notices. We do not currently have any registered or pending patents or trademarks, except the trademark “Knockout Debt” (USPTO Reg. No. 2,810,014) and a US Provisional Patent Application (S/N 61/301, 811), which was filed on February 5, 2010, encompassing our SaaS lead generation management software. In addition, we filed a utility application (No.: 13/020,240) on the above-mentioned Provisional Patent on February 3, 2011.

Competition

Our primary online marketing services competitors include:

Edgar Online, Inc., which engages in the creation and distribution of fundamental financial data and public filings for equities, mutual funds, and other publicly traded assets principally in the United States. It produces data that assists in the analysis of the financial, business, and ownership conditions of an investment. The company delivers its information products via the Internet in the form of end-user subscriptions and data feeds. Edgar Online, Inc., is also one of our business partners providing us with SEC filings and other data.

TheStreet.com, Inc., which together with its wholly-owned subsidiaries, operates as a financial media company. Its flagship site, TheStreet.com, provides financial commentary, analysis, and news with financial coverage to individual investors. TheStreet.com also offers investigative journalism, commentary on market trends, specific stock and mutual fund analysis, and personal finance and lifestyle sections.

ValueClick, Inc., which provides online advertising campaigns and programs for advertisers and advertising agency customers in the United States and internationally. It operates in four segments: Media, Affiliate Marketing, Comparison Shopping, and Technology. ValueClick Inc. customers include advertisers, advertising agencies, and traffic distribution partners.

QuinStreet, Inc. provides online direct marketing and media services. The company offers online messaging, email broadcasting, search engine marketing, and brand management services. It caters to education, financial services, healthcare, advertising, and tourism sectors. QuinStreet, Inc. also operates web portal which offers comprehensive consumer information service and companion insurance brokerage service to self-directed insurance shoppers. The company was founded in 1999 and is based in Foster City, California.

7

Other large competitors in the business information industry are Reuters, Standard & Poor’s and Thomson Financial. Competition for information focused on financial data or credit risk comes from companies such as S&P’s Capital IQ, Dun & Bradstreet and Factset. Competition for legal information comes from companies such as Thompson’s Global Securities Information. Other competitors include companies such as 10-K Wizard Technology, which focus on simple SEC data offerings, and MSN Money and Yahoo! Finance, which are more focused on serving individual investors.

The principal competitive factors relating to attracting and retaining users include the quality and relevance of our search results, and the usefulness, accessibility, integration and personalization of the online services that we offer. In the case of attracting advertisers, the principal competitive factors are reach, effectiveness and efficiency of our marketing services.

Our Marketing Services competitors have significantly greater capital, technology, resources, and brand recognition than we do.

Our primary SaaS Competitors include:

DirectTrack owned by Digital River Inc., a leading affiliate marketing and tracking platform powering affiliate networks and in-house affiliate programs.

Commission Junction owned by ValueClick Inc., a global leader in affiliate marketing.

Other competitors in the SaaS industry include www.linktrust.com and www.pontiflex.com.

Our SaaS competitors have significantly greater capital, technology, resources, and brand recognition than we do.

Government Regulation

Although there are currently relatively few laws and regulations directly applicable to the Internet, it is possible that new laws and regulations will be adopted in the United States and elsewhere. The adoption of restrictive laws or regulations could slow or otherwise affect Internet growth. The adoption of laws or regulations restricting or limiting debt settlement could affect our lead generation business. The application of existing laws and regulations governing Internet issues such as property ownership, libel and personal privacy is also subject to substantial uncertainty. There can be no assurance that current or new government laws and regulations, or the application of existing laws and regulations (including laws and regulations governing issues such as property ownership, taxation, defamation and personal injury), will not expose us to significant liabilities, slow Internet growth or otherwise hurt us financially.

Research and Development

During 2010 we incurred research and development expenses of approximately $420,000 in order to further develop our Cake Marketing software.

Employees

As of December 31, 2010, we had 17 full-time employees, including all of our executive officers, and 5 consultants. None of our employees are covered by collective bargaining agreements, and we believe our relationships with our employees to be good.

Item 1A. Risk Factors

If we are unable to obtain financing necessary to support our operations, we may be unable to continue as a going concern.

We have generated revenues since inception but they were not an adequate source of cash to fund future operations. Historically we have relied on private placement issuances of equity and debt. We will need to raise additional working capital to fund our ongoing operations and growth. The amount of our future capital requirements depends primarily on the rate at which we increase our revenues and correspondingly decrease our use of cash to fund operations. Cash used for operations will be affected by numerous known and unknown risks and uncertainties including, but not limited to, our ability to successfully market our products and services and the degree to which competitive products and services are introduced to the market. As long as our cash flow from operations remains insufficient to completely fund operations, we will continue depleting our financial resources and seeking additional capital through equity and/or debt financing. If we raise additional capital through the issuance of debt, this will result in increased interest expense. If we raise additional funds through the issuance of equity or convertible debt securities, the percentage ownership of our company held by existing stockholders will be reduced and those stockholders may experience significant dilution. In addition, new securities may contain rights, preferences or privileges that are senior to those of our Common Stock. There can be no assurance that acceptable financing to fund our ongoing operations can be obtained on suitable terms, if at all. If we are unable to obtain the financing necessary to support our operations, we may be unable to continue as a going concern. In that event, we may be forced to cease operations and our stockholders could lose their entire investment in us. Our audited financial statements included in this annual report for the period ended December 31, 2010 contain additional note disclosures describing the circumstances that lead to this disclosure by our independent auditors.

8

We have a history of losses, and we expect to continue to operate at a loss and to have negative cash flow from operations for the foreseeable future.

We have a history of continuing losses and negative cash flow from operations. At December 31, 2009 and December 31, 2010, we had cumulative net losses of approximately $2.4 million and $1.2 million, respectively. Our operations have been financed primarily through proceeds from the issuance of equity and borrowings under promissory notes. On December 31, 2009 and December 31, 2010, we had approximately $128,000 and $92,000 in cash, respectively. We expect that our expenses will increase substantially as we continue to develop and market our products and services. As a result, we expect to continue to incur losses for the foreseeable future.

Because we expect to continue to incur net losses, we may not be able to implement our business strategy and the price of our stock may decline.

Although our net loss has decreased substantially in 2010 compared to 2009 and previous years, there is no assurance that we will reach profitability in 2011. In addition, in February 2011 we have closed our Lead Generation Division, which was a substantial source of revenue and marginally profitable. Accordingly, our ability to operate our business and implement our business strategy may be hampered by negative cash flows in the future, and the value of our stock may decline as a result. Our capital requirements may vary materially from those currently planned if, for example, we incur unforeseen capital expenditures, unforeseen operating expenses or make investments to maintain our competitive position. If this is the case, we may have to delay or abandon some or all of our development plans or otherwise forego market opportunities. We will need to generate significant additional revenues to be profitable in the future, and we may not generate sufficient revenues to be profitable on either a quarterly or annual basis in the future.

Our quarterly financial results will fluctuate, making it difficult to forecast our results of operation.

Our revenues and operating results may vary significantly from quarter to quarter due to a number of factors, many of which are beyond our control, including:

|

●

|

Variability in demand and usage for our products and services;

|

|

●

|

Market acceptance of new and existing services offered by us, our competitors and potential competitors;

|

|

●

|

Governmental regulations affecting the use of the Internet, including regulations concerning intellectual property rights and security features; and

|

|

●

|

The recent downturn in the economy which led to a large increase in home foreclosures, business failures, unemployment and substantial growth in consumer debt.

|

Our current and future levels of expenditures are based primarily on our growth plans and estimates of expected future revenues. If our operating results fall below the expectation of investors, our stock price will likely decline significantly.

We face risks related to the recent credit crisis.

Current uncertainty in the global economic conditions resulting from the recent disruption in credit markets poses a risk to the overall economy and has adversely affected the online advertising market, which is now highly competitive. These economic conditions have impacted consumer and customer demand for our products, as well as our ability to borrow money to finance our operations, to maintain our key employees, and to manage normal commercial relationships with our customers, suppliers and creditors. For example, customers spend less on on-line advertising and other services, and may extend the payment periods for our lead generation services. If another economic crisis were to occur, our business and results of operations will continue to be negatively impacted.

We face intense competition from other providers of business and financial information.

We compete with many providers of business and financial information, including other Internet companies, for consumers' and advertisers' attention and spending. Our primary competitors are Edgar Online, Inc. and The Street.com, Inc., both of which provide services similar to ours and each of which has a well-established market presence. These and other competitors have substantially greater capital, longer operating histories, greater brand recognition, larger customer bases and significantly greater financial, technical and marketing resources than we do. These competitors may also engage in more extensive development of their technologies, adopt more comprehensive marketing and advertising campaigns than we can. Our competitors may develop products and service offerings that we do not offer or that are more sophisticated or more cost effective than our own. For these and other reasons, our competitors' products and services may achieve greater acceptance in the marketplace than our own, limiting our ability to gain market share and customer loyalty and to generate sufficient revenues to achieve a profitable level of operations. Our failure to adequately address any of the above factors could harm our business and operating results.

In addition, as the barriers to entry in our market segment are not substantial, an unlimited number of new competitors could emerge, thereby making our goal of establishing a market presence even more difficult. Because our management expects competition in our market segment to continue to intensify, there can be no assurances we will ever establish a competitive position in our market segment.

9

We may not be successful in marketing our new proprietary software.

In 2010, we expanded into the rapidly growing performance based software business through the formation of our new Cake Marketing Software Division. Our proprietary software streamlines the management of large scale online marketing campaigns for affiliate marketers and advertisers, while its unique ability to simplify online marketing efforts generates immediate cost saving for clients. The software is available for a monthly licensing fee to affiliate marketers, advertising agencies and corporations using a SaaS model. We have invested a substantial amount of time and money in developing and launching our proprietary platform. Various technical delays and malfunctions may result in additional expenses and difficulties.

We may not be successful in increasing our brand awareness.

We believe that developing and maintaining awareness of the Cake Marketing brand and our other brands is critical to achieving widespread acceptance of our existing and future services and is an important element in attracting new customers. In addition, our future success will depend, in part, on our ability to increase brand awareness of our websites. In order to build brand awareness, we must succeed in our marketing efforts, provide high quality services and increase traffic to our websites. Our efforts to build our brands will involve significant expense. Brand promotion activities may not yield increased revenue, and even if they do, any increased revenue may not offset the expenses we incurred in building our brands. If we fail to successfully promote and maintain our brands, or incur substantial expenses in an unsuccessful attempt to promote and maintain our brands, we may fail to attract enough new customers or retain our existing customers to the extent necessary to realize a sufficient return on our brand-building efforts, and our business could suffer.

We may not be successful in improving our existing products or in developing new products.

We have not yet completed development and testing of certain proposed new products and proposed enhancements to our systems, some of which are still in the planning stage or in relatively early stages of development. Our success will depend in part upon our ability to timely introduce new products into the marketplace. We must commit considerable time, effort and resources to complete development of our proposed products, service tools and product enhancements. Our product development efforts are subject to all of the risks inherent in the development of new products and technology, including unanticipated delays, expenses and difficulties, as well as the possible insufficiency of funding to complete development.

Our product development efforts may not be successfully completed. In addition, proposed products may not satisfactorily perform the functions for which they are designed, they may not meet applicable price or performance objectives and unanticipated technical or other problems may occur which result in increased costs or material delays in development. Despite testing by Accelerize and potential end users, problems may be found in new products, tools and services after the commencement of commercial delivery, resulting in loss of, or delay in, market acceptance and other potential damages.

We may not be successful in developing new and enhanced services and features for our websites.

Our market is characterized by rapidly changing technologies, evolving industry standards, frequent new product and service introductions and changing customer demands. To be successful, we must adapt to the rapidly changing market by continually enhancing our existing services and adding new services to address customers' changing demands. We could incur substantial costs if we need to modify our services or infrastructure to adapt to these changes. Our business could be adversely affected if we were to incur significant costs without generating related revenues or if we cannot adapt rapidly to these changes. Our business could also be adversely affected if we experience difficulties in introducing new or enhanced services or if these services are not favorably received by users. We may experience technical or other difficulties that could delay or prevent us from introducing new or enhanced services.

We depend on receipt of timely feeds from our content providers.

Our operations depend on receipt of timely feeds from our content providers, and any failure or delay in the transmission or receipt of such feeds could disrupt our operations. We also depend on Web browsers, ISPs and online service providers to provide access over the Internet to our product and service offerings. Many of these providers have experienced significant outages or interruptions in the past, and could experience outages, delays and other difficulties due to system failures unrelated to our systems. These types of interruptions could continue or increase in the future.

We rely on third-party computer hardware and software that may be difficult to replace or which could cause errors or failures of our service.

We rely on computer hardware purchased or leased and software licensed from third parties in order to offer our services, including database software from Microsoft Corporation, and servers hosted at Rackspace Hosting, Inc., Maximum ASP, LLC. and SoftLayer Technologies, Inc. This hardware and software may not continue to be available to us at reasonable prices, or on commercially reasonable terms, or at all. Any loss of the right to use any of this hardware or software could significantly increase our expenses and otherwise result in delays in the provisioning of our service until equivalent technology is either developed by us, or, if available, is identified, obtained and integrated, which could harm our business. Any errors or defects in third-party hardware or software could result in errors or a failure of our service which could harm our business.

10

If our security measures are breached and unauthorized access is obtained to a customer’s data or our data or our information technology systems, our service may be perceived as not being secure, customers may curtail or stop using our service and we may incur significant legal and financial exposure and liabilities.

Our service involves the storage and transmission of customers’ proprietary information, and security breaches could expose us to a risk of loss of this information, litigation and possible liability. These security measures may be breached as a result of third-party action, including intentional misconduct by computer hackers, employee error, malfeasance or otherwise, during transfer of data to additional data centers or at any time, and result in someone obtaining unauthorized access to our customers’ data or our data, including our intellectual property and other confidential business information, or our information technology systems. Additionally, third parties may attempt to fraudulently induce employees or customers into disclosing sensitive information such as user names, passwords or other information in order to gain access to our customers’ data or our data, including our intellectual property and other confidential business information, or our information technology systems. Because the techniques used to obtain unauthorized access, or to sabotage systems, change frequently and generally are not recognized until launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. In addition, our customers may authorize third party technology providers, via our various Application Programming Interfaces, to access their customer data. Because we do not control the transmissions between our customers and third-party technology providers, or the processing of such data by third-party technology providers, we cannot ensure the complete integrity or security of such transmissions or processing. Any security breach could result in a loss of confidence in the security of our service, damage our reputation, disrupt our business, lead to legal liability and negatively impact our future sales.

Interruptions or delays in service from our third-party data center hosting facilities could impair the delivery of our service and harm our business.

We currently serve our customers from third-party data center hosting facilities located in the United States and United Kingdom. Any damage to, or failure of, our systems generally could result in interruptions in our service. As we continue to add data centers and add capacity in our existing data centers, we may move or transfer our data and our customers’ data. Despite precautions taken during this process, any unsuccessful data transfers may impair the delivery of our service. Further, any damage to, or failure of, our systems generally could result in interruptions in our service. Interruptions in our service may reduce our revenue, cause us to issue credits or pay penalties, cause customers to terminate their subscriptions and adversely affect our renewal rates and our ability to attract new customers. Our business will also be harmed if our customers and potential customers believe our service is unreliable.

As part of our current disaster recovery arrangements, our production environment and all of our customers’ data is currently backed up in near real-time to offsite storage. We do not control the operation of any of these facilities, and they are vulnerable to damage or interruption from earthquakes, floods, fires, power loss, telecommunications failures and similar events. They may also be subject to break-ins, sabotage, intentional acts of vandalism and similar misconduct. Despite precautions taken at these facilities, the occurrence of a natural disaster or an act of terrorism, a decision to close the facilities without adequate notice or other unanticipated problems at these facilities could result in lengthy interruptions in our service. Even with the disaster recovery arrangements, our service could be interrupted.

Defects or disruptions in our service could diminish demand for our service and subject us to substantial liability.

Because our service is complex and we have incorporated a variety of new computer hardware and software, both developed in-house and acquired from third party vendors, our service may have errors or defects that users identify after they begin using it that could result in unanticipated downtime for our subscribers and harm our reputation and our business. Internet-based services frequently contain undetected errors when first introduced or when new versions or enhancements are released. We have from time to time found defects in our service and new errors in our existing service may be detected in the future. In addition, our customers may use our service in unanticipated ways that may cause a disruption in service for other customers attempting to access their data. Since our customers use our service for important aspects of their business, any errors, defects, disruptions in service or other performance problems with our service could hurt our reputation and may damage our customers’ businesses. If that occurs, customers could elect not to renew, or delay or withhold payment to us, we could lose future sales or customers may make warranty or other claims against us, which could result in an increase in our provision for doubtful accounts, an increase in collection cycles for accounts receivable or the expense and risk of litigation.

We may rely on a limited number of major customers for most of our revenues.

While during the fiscal year ended December 31, 2010, none of our customers accounted for a substantial percentage of our revenues, during the fiscal year ended December 31, 2009, one of our customers accounted for 14% of our revenues. The loss of any customer that accounts for a significant portion of our revenues from time to time, could adversely affect our business, operating results and financial condition due to the substantial decrease in revenue such loss would represent.

Our future performance and success depend on our ability to retain our key personnel.

Our future performance and success is heavily dependent upon the continued active participation of our current senior management team, including, our President and Chief Executive Officer, Brian Ross, our General Counsel, Damon Stein, our Chief Revenue Officer and the President of our Cake Marketing Division, Jeff McCollum, and our President of Online Marketing Services, Daniel Minton. The loss of any of their services could have a material adverse effect on our business development and our ability to execute our growth strategy, resulting in loss of sales and a slower rate of growth. We do not maintain any "key person" life insurance for any of our employees.

We may be subject to infringement claims on proprietary rights of third parties for software and other content that we distribute or make available to our customers.

We may be liable or alleged to be liable to third parties for software and other content that we distribute or make available to our customers:

|

●

|

If the content or the performance of our services violates third party copyright, trademark, or other intellectual property rights; or

|

|

●

|

If our customers violate the intellectual property rights of others by providing content through our services.

|

11

Any alleged liability could harm our business by damaging our reputation, requiring us to incur legal expenses in defense, exposing us to awards of damages and costs including treble damages for willful infringement and diverting management's attention which could have an adverse effect on our business, results of operations and financial condition.

We cannot assure you that third parties will not claim infringement by us with respect to past, current, or future technologies. Participants in our markets may be increasingly subject to infringement claims as the number of services and competitors in our industry segment grows. In addition, these risks are difficult to quantify in light of the continuously evolving nature of laws and regulations governing the Internet. Any claim relating to proprietary rights, whether meritorious or not, could be time-consuming, result in costly litigation, cause service upgrade delays or require us to enter into royalty or licensing agreements, and we cannot assure you that we will have adequate insurance coverage or that royalty or licensing agreements will be available on terms acceptable to us or at all. Further, we plan to offer our services and applications to customers worldwide including customers in foreign countries that may offer less protection for our intellectual property than the United States. Our failure to protect against misappropriation of our intellectual property, or claims that we are infringing the intellectual property of third parties could have a negative effect on our business, revenues, financial condition and results of operations.

Evolving Government regulation could adversely affect our business prospects.

We do not know with certainty how existing laws governing issues such as property ownership, debt-settlement, copyright and other intellectual property issues, taxation, illegal or obscene content, retransmission of media, personal privacy and data protection will apply to the Internet or to the distribution of multimedia and other proprietary content over the Internet. Most of these laws were adopted before the advent of the Internet and related technologies and therefore do not address the unique issues associated with the Internet and related technologies. Depending on how these laws developed and are interpreted by the judicial system, they could have the effect of:

|

●

|

Limiting the growth of the Internet;

|

|

●

|

Creating uncertainty in the marketplace that could reduce demand for our products and services;

|

|

●

|

Increasing our cost of doing business;

|

|

●

|

Exposing us to significant liabilities associated with content distributed or accessed through our products or services; or

|

|

●

|

Leading to increased product and applications development costs, or otherwise harm our business.

|

Because of this rapidly evolving and uncertain regulatory environment, both domestically and internationally, we cannot predict how existing or proposed laws and regulations might affect our business.

In addition, as Internet commerce continues to evolve, increasing regulation by federal, state or foreign agencies becomes more likely. For example, we believe increased regulation is likely in the area of data privacy, and laws and regulations applying to the solicitation, collection, processing or use of personal or consumer information could affect our customers’ ability to use and share data, potentially reducing demand for our software solutions and restricting our ability to store, process and share data with our customers. In addition, taxation of services provided over the Internet or other charges imposed by government agencies or by private organizations for accessing the Internet may also be imposed. Any regulation imposing greater fees for Internet use or restricting information exchange over the Internet could result in a decline in the use of the Internet and the viability of Internet-based services, which could harm our business.

Dilutive securities may adversely impact our stock price.

As of March 29, 2011, the following securities issuable, convertible or exercisable into shares of our Common Stock were outstanding:

|

●

|

4,900,000 and 11,662,500 shares of Common Stock issuable upon the possible conversion of outstanding 10% Series A Convertible Preferred Stock and 8% Series B Convertible Preferred Stock, respectively;

|

|

●

|

2,432,793 and 2,605,815 shares of Common Stock issuable in payment of PIK dividends to our 10% Series A Convertible Preferred Stock holders, or the Series A PIK Dividends, and 8% Series B Convertible Preferred Stock holders, or the Series B PIK Dividends, respectively;

|

|

●

|

Convertible Promissory Notes in a total principal amount of $637,000, which may be converted at the note holders' option at conversion price of $0.40 per share;

|

|

●

|

Warrants to purchase up to a total of 13,680,524 shares of our Common Stock at a price range of $0.15 to $0.75 per share, of which 2,350,000 shares have a cashless exercise feature; and

|

|

●

|

up to 9,488,334 shares of Common Stock issuable under our stock option plan.

|

These securities represent as of March 29, 2011, approximately 56% of our Common Stock on a fully diluted, as converted basis. The exercise of these options or warrants and the conversion of the preferred stock, both of which have fixed prices, may materially adversely affect the market price of our Common Stock and will have a dilutive effect on our existing stockholders.

12

Our internal control over financial reporting was not considered effective as of December 31, 2009 and 2010, and may continue to be ineffective in the future, which could result in our financial statements being unreliable, government investigation or loss of investor confidence in our financial reports.

Pursuant to Section 404 of the Sarbanes-Oxley Act of 2002, and the SEC rules promulgated there under, we are required to furnish an annual report by our management assessing the effectiveness of our internal control over financial reporting. This assessment must include disclosure of any material weaknesses in our internal control over financial reporting identified by management. Management's reports as of the years ended December 31, 2009 and December 31, 2010, identified several material weaknesses and concluded that we did not have effective internal control over financial reporting. Ineffective internal controls can result in errors or other problems in our financial statements. Even if material weaknesses identified do not cause our financial statements to be unreliable, if we continue to be unable to assert that our internal controls are effective, our investors could still lose confidence in the accuracy and completeness of our financial reports, which in turn could cause our stock price to decline. Failure to maintain effective internal control over financial reporting could also result in investigation or sanctions by regulatory authorities.

In the event that our independent registered public accounting firm is unable to rely on our internal controls in connection with their audit of our financial statements, and in the further event that they are unable to devise alternative procedures in order to satisfy themselves as to the material accuracy of our financial statements and related disclosures, it is possible that we would receive a qualified or an adverse audit opinion on those financial statements which could also adversely affect the market price of our Common Stock and our ability to secure additional financing as needed.

We have not voluntarily implemented various corporate governance measures, in the absence of which, stockholders may have more limited protections against interested director transactions, conflicts of interest and similar matters.

Federal legislation, including the Sarbanes-Oxley Act of 2002, has resulted in the adoption of various corporate governance measures designed to promote the integrity of the corporate management and the securities markets. Some of these measures have been adopted in response to legal requirements. Others have been adopted by companies in response to the requirements of national securities exchanges, such as the New York Stock Exchange or the Nasdaq Stock Market, on which their securities are listed. Among the corporate governance measures that are required under the rules of national securities exchanges are those that address board of directors' independence, audit committee oversight, and the adoption of a code of ethics. We have not yet adopted some of these corporate governance measures and, since our securities are not listed on a national securities exchange, we are not required to do so. We have not adopted corporate governance measures such as an audit or other independent committees of our board of directors. We intend to expand our board membership to include additional independent directors and we may then seek to establish an audit and other committees of our board of directors. It is possible that if we were to adopt some or all of these corporate governance measures, stockholders would benefit from somewhat greater assurances that internal corporate decisions were being made by disinterested directors and that policies had been implemented to define responsible conduct. For example, in the absence of audit, nominating and compensation committees comprised of at least a majority of independent directors, decisions concerning matters such as compensation packages to our senior officers and recommendations for director nominees may be made by a majority of directors who have an interest in the outcome of the matters being decided. Prospective investors should bear in mind our current lack of corporate governance measures in formulating their investment decisions.

The limited market for our Common Stock will make our stock price more volatile. Therefore, you may have difficulty selling your shares.

The market for our Common Stock is limited and we cannot assure you that a larger market will ever be developed or maintained. Currently, our Common Stock is traded on the OTCBB and the OTCQB Marketplace. Securities traded on the OTCBB and the OTCQB Marketplace typically have low trading volumes. Market fluctuations and volatility, as well as general economic, market and political conditions, could reduce our market price. As a result, this may make it difficult or impossible for our shareholders to sell our Common Stock.

There are no restrictions on the sale of our outstanding Common Stock. Sales by existing shareholders may depress the share price of our Common Stock and may impair our ability to raise additional capital through the sale of equity securities when needed.

As of March 29, 2011 we had 35,803,593 shares of Common Stock issued and outstanding, all of which were freely tradable under Rule 144 under the Securities Act, or registered for re-sale. The possibility that substantial amounts of outstanding Common Stock may be sold in the public market may adversely affect prevailing market prices for our Common Stock. This could negatively affect the market price of our Common Stock and could impair our ability to raise additional capital through the sale of equity securities.

Our Common Stock is subject to the “penny stock” rules of the SEC, and the trading market in our Common Stock is limited. This makes transactions in our Common Stock cumbersome and may reduce the value of your shares.

The SEC has adopted Rule 3a51-1 which establishes the definition of a "penny stock," for the purposes relevant to us, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, Rule 15g-9 requires:

|

·

|

that a broker or dealer approve a person's account for transactions in penny stocks; and

|

|

·

|

the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased.

|

In order to approve a person's account for transactions in penny stocks, the broker or dealer must:

|

·

|

Obtain financial information and investment experience objectives of the person; and

|

13

|

·

|

make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks.

|

The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prescribed by the SEC relating to the penny stock market, which, in highlight form:

|

·

|

sets forth the basis on which the broker or dealer made the suitability determination; and

|

|

·

|

that the broker or dealer received a signed, written statement from the investor prior to the transaction.

|

Generally, brokers may be less willing to execute transactions in securities subject to the "penny stock" rules. This may make it more difficult for investors to dispose of our Common Stock and cause a decline in its market value.

Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

During January 2009, we entered into an office lease for approximately 2,200 sq. ft. space in Newport Beach, California, effective as of February 1, 2009. Under the terms of the lease, we pay monthly base rent of $4,100. The lease is renewable on a monthly basis. On January 1, 2011 we moved our corporate headquarters from our Los Angeles, California office (the lease of which expired on December 31, 2010), to our Newport Beach office.

During June 2010, we entered into a one year lease for approximately 1,200 sq. ft. office space in Whitefish, Montana, which commenced on June 1, 2010. Under the terms of the lease, we are required to pay monthly base rent of $1,400.

During December 2010, we entered into a one year lease for approximately 800 sq. ft. office space in Santa Monica, California, which commenced on January 1, 2011. Under the terms of the lease, we are required to pay monthly base rent of $1,800, but we also receive $1350 a month in subtenant payments.

We believe that our current leases are adequate and sufficient for the Company's needs in the foreseeable future.

Item 3. Legal Proceedings.

On February 8, 2011, we filed a complaint against PathwayData, Inc. doing business as Consumer Direct, or Consumer Direct, a Nevada corporation, in the California Superior Court for Orange County, for breach of agreement and failure to pay a total amount of $76,841, which is due and owing to us, based on agreements entered between us and Consumer Direct on January 18, 2010 and on October 26, 2009. On March 7, 2011, Consumer Direct filed their answer, and a case management conference is scheduled for July 18, 2011.

Other than as described above, we are currently not a party to any material pending litigation, government investigation or any other legal proceedings.

Item 4. (Removed and Reserved)

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our Common Stock began quotation on the Over-the-Counter Bulletin Board on January 9, 2008, and is quoted under the symbol "ACLZ.OB". The following table sets forth the high and low bid quotations for the Common Stock as reported on the Over-the-Counter Bulletin Board for each quarter during the last two fiscal years. These quotations reflect prices between dealers, do not include retail mark-ups, markdowns, and commissions and may not necessarily represent actual transactions.

|

Fiscal Year Ended December 31, 2009

|

High

|

Low

|

||||||||

|

First Quarter Ended March 31, 2009

|

$ | 0.38 | $ | 0.20 | ||||||

|

Second Quarter Ended June 30, 2009

|

$ | 0.52 | $ | 0.25 | ||||||

|

Third Quarter Ended September 30, 2009

|

$ | 0.60 | $ | 0.40 | ||||||

|

Fourth Quarter Ended December 31, 2009

|

$ | 0.80 | $ | 0.52 | ||||||

14

|

Fiscal Year Ended December 31, 2010

|

High

|

Low

|

||||||||

|

First Quarter Ended March 31, 2010

|

$ | 0.65 | $ | 0.51 | ||||||

|

Second Quarter Ended June 30, 2010

|

$ | 0.65 | $ | 0.48 | ||||||

|

Third Quarter Ended September 30, 2010

|

$ | 0.64 | $ | 0.48 | ||||||

|

Fourth Quarter Ended December 31, 2010

|

$ | 0.65 | $ | 0.50 | ||||||

|

High

|

Low

|

|||||||||

|

First Quarter through March 29, 2011

|

$ | 0.65 | $ | 0.38 | ||||||

Stockholders

As of March 29, 2011, there were 109 stockholders of record of our Common Stock.

Dividend Policy

We have not declared or paid any cash dividends on our Common Stock since inception and we do not intend to pay any cash dividends in the foreseeable future. We intend to retain any future earnings for use in the operation and expansion of our business. Any future decision to pay dividends on Common Stock will be at the discretion of our Board of Directors and will be dependent upon our fiscal condition, results of operations, capital requirements and other factors our Board of Directors may deem relevant.

The holders of our 10% Series A Preferred Stock are entitled to receive a cumulative preferential dividend of 10% per annum on the stated value of the 10% Series A Preferred Stock owned by them. The dividend is payable at our option in cash or shares of Common Stock valued at $0.15 per share. We do not intend to pay any cash dividend in the near future. Dividends are payable on a quarterly basis on each of September 1, December 1, March 1, and June 1, and commenced September 1, 2006.

The holders of our 8% Series B Preferred Stock are entitled to receive a cumulative preferential dividend of 8% per annum on the stated value of the 8% Series A Preferred Stock owned by them. The dividend is payable at our option in cash or shares of Common Stock valued at $0.35 per share. We do not intend to pay any cash dividend in the near future. Dividends are payable on a quarterly basis on each of September 1, December 1, March 1, and June 1, and commenced December 1, 2007.

Unregistered issuance of Securities

On March 1, 2011 we issued a total of 130,699 shares of Common Stock as PIK Dividends to the holders of our Series A Preferred and 178,962 shares of Common Stock as PIK Dividends to the holders of our Series B Preferred.

On January 3, 2011, in connection with a loan agreement, we issued to the lender, Agility Capital II, LLC, a warrant to purchase up to 283,019 shares of our Common Stock, at an exercise price equal to the lower of: (i) the average closing price of our Common Stock for the 15 days before the closing date, or (ii) the price per share on our next equity financing, provided it is not less than $0.35 per share. The warrant expires in January 2016. The loan agreement includes a default clause, which would provides that in case of a default, we may be required to issue up to an additional 350,000 shares of Common Stock under the warrant, as well as a $5,000 default fee.

On December 1, 2010 we issued a total of 132,148 shares of Common Stock as PIK Dividends to the holders of our Series A Preferred and 159,670 shares of Common Stock as PIK Dividends to the holders of our Series B Preferred.

On December 1, 2010 we issued a total of 23,945 shares of Common Stock to note holders as interest pursuant to our 10% and 12% convertible notes payable.

During September 2010 in connection with a private placement to a total of 7 accredited investors, we issued a total of 3,000 units at a price of $100 each. Each unit consists of 250 shares of our Common Stock and a Warrant to purchase up to an additional 250 shares of Common Stock at an exercise price of $0.65 per share. The Warrants expire 3 years after the date of issuance.

From January to April 2010 in connection with a private placement to a total of 14 accredited investors, we issued a total of 5,115 units at a price of $100 each. Each unit consists of 250 shares of our Common Stock and a 3-year Warrant to purchase up to an additional 250 shares of Common Stock at an exercise price of $0.65 per share. The Warrants expire 3 years after the date of issuance.

Share Repurchases

During the fiscal year ended December 31, 2009 we repurchased 500,000 shares of Common Stock from Christopher Meredith, a former director of the Company, and during the fiscal year ended December 31, 2010, we repurchased an additional 140,000 shares of Common Stock from Mr. Meredith, and retired the entire 640,000 shares of Common Stock.

15

Item 6. Selected Financial Data.

Not Applicable.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following information should be read in conjunction with our financial statements and accompanying notes included in this Annual Report on Form 10-K.

Overview

We are a multifaceted online marketing services company specializing in the development of performance based marketing programs and related software solutions for businesses interested in expanding their online advertising presence. The Company owns and operates www.cakemarketing.com, an internally-developed SaaS, platform. Cake Marketing is a hosted software solution that provides an all-inclusive suite of management services for online marketing campaigns. From tracking and reporting to lead distribution, our patent-pending software enables advertisers, affiliate marketers and lead generators a fully scalable and accurate platform developed with a combination of innovative technology and an imaginative approach to doing business online.

The Company has an extensive portfolio of approximately 5,500 URLs, also known as domain names. Our URL portfolio is currently used to build consumer-based financial portals, microsites, blogs, and landing pages used for lead generation initiatives. In addition, we own and develop various portals, and websites, including: www.secfilings.com, which provides to subscribers real-time alerts based on reports filed by various companies and individuals with the SEC. Also through www.accelerizefinancial.com the Company offers advertisers access to an audience of active individual investors, institutional investors, financial planners, registered advisors, journalists, investment bankers and brokers. Our financial portals and URL portfolio target a niche demographic that is qualified by the content they seek. This media strategy drives new membership, which results in recurring user traffic to our websites and allows us to generate highly relevant responses and leads for our online advertising and lead generation customers.

In February 2011 we decided to discontinue our Lead Generation Division, in order to focus our efforts and resources on our SaaS products and services. After careful review by our management, it became clear that although the Lead Generation Division was a substantial source of revenue for the Company, it was only marginally profitable, and required substantial management attention and financial resources, which would otherwise be invested in more profitable channels. In addition, we decided to discontinue our Lead Generation Division to avoid potential conflict of interest with our SaaS customers, who are providing similar lead generation services. Subsequently, we sold certain assets related to our Lead Generation Division. Commencing March 1, 2011, we no longer offer lead generation services.

As of the end of 2008 we closed our debt settlement referrals division, however in 2009 and 2010 we still received fees for sales and marketing support we provided in connection with debt settlement solutions prior to closing this unit. These payments gradually decreased in 2009 and 2010, and we expect that they will be eliminated by the end of 2011.

Results of Operations

|

ACCELERIZE NEW MEDIA, INC.

|

||||||||||||||||

|

RESULTS OF OPERATIONS

|

||||||||||||||||

|

Year ended

|

Increase/

|

Increase/

|

||||||||||||||

|

December 31,

|

(Decrease)

|

(Decrease)

|

||||||||||||||

|

2010

|

2009

|

in $ 2010

|

in % 2010

|

|||||||||||||

|

vs 2009

|

vs 2009

|

|||||||||||||||

|

Revenue:

|

||||||||||||||||

|

Lead generation revenues

|

$ | 1,869,946 | $ | 2,724,706 | $ | (854,760 | ) | -31.4 | % | |||||||

|

Online marketing services

|

973,567 | 447,586 | 525,981 | 117.5 | % | |||||||||||

| Software-as-a-service | 482,675 | - | 482,675 | NM | ||||||||||||

|

Debt solution revenues

|

377,302 | 701,285 | (323,983 | ) | -46.2 | % | ||||||||||

|

Total revenues:

|

3,703,490 | 3,873,577 | (170,087 | ) | -4.4 | % | ||||||||||

|

Operating expenses:

|

||||||||||||||||

|

Cost of revenue

|

1,452,263 | 2,360,326 | (908,063 | ) | -38.5 | % | ||||||||||

|

Research and development

|

418,898 | 13,060 | 405,838 | 3,107.5 | % | |||||||||||

|

Selling, general and administrative

|

2,459,831 | 3,393,982 | (934,151 | ) | -27.5 | % | ||||||||||

|

Total operating expenses

|

4,330,992 | 5,767,368 | (1,436,376 | ) | -24.9 | % | ||||||||||

|

Operating loss

|

(627,502 | ) | (1,893,791 | ) | 1,266,289 | -66.9 | % | |||||||||

|

Other expense:

|

||||||||||||||||

|

Interest expense

|

(129,389 | ) | (119,693 | ) | (9,696 | ) | 8.1 | % | ||||||||

| (129,389 | ) | (119,693 | ) | (9,696 | ) | 8.1 | % | |||||||||

|

Net loss

|

(756,891 | ) | (2,013,484 | ) | 1,256,593 | -62.4 | % | |||||||||

|

Less dividends issued for series A and B preferred stock

|

407,176 | 410,812 | $ | (3,636 | ) | -0.9 | % | |||||||||

|

Net loss attributable to common stock

|

$ | (1,164,067 | ) | $ | (2,424,296 | ) | $ | 1,260,229 | -52.0 | % | ||||||

|

NM: Not Meaningful

|

||||||||||||||||

Revenues

Revenues primarily consist of fees related to lead generation, online marketing services, sale of our software licenses, and sales and marketing of debt settlement referrals.

Our decrease in lead generation revenues during the year ended December 31, 2010, when compared to the prior year is due primarily to a decrease in the number of leads we sold.

Our increase in online marketing services revenues during the year ended December 31, 2010 when compared to the prior year is due to the increased number of customers using our advertising and other services.

Our increase in SaaS revenues during the year ended December 31, 2010 when compared to the prior year is due to the SaaS Division commencing operation in 2010. We are unable to ascertain if our expected increased revenues from licensing our software will offset the decreased revenues from the loss of the lead generation division.