Attached files

Table of Contents

Index to Financial Statements

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 333-150853-4

Forbes Energy Services Ltd.

(Exact name of registrant as specified in its charter)

| Bermuda | 98-0581100 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 3000 South Business Highway 281 Alice, Texas |

78332 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (361) 664-0549

Securities registered pursuant to Section 12(b) or Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | ¨ | Accelerated Filer | ¨ | |||

| Non-Accelerated Filer | x | Smaller Reporting Company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). ¨ Yes x No

The aggregate market value of the stock held by non-affiliates of the registrant as of the last business day of the most recently completed second fiscal quarter, June 30, 2010, was approximately USD 24,699,600 based on the closing sales price of the registrant’s common stock as reported by the Toronto Stock Exchange on June 30, 2010 of USD $0.4227 per share, converted from CDN$ to USD$ based on the exchange rate on June 30, 2010 of CDN $1.00 equaling USD $0.9393 as reported in the Wall Street Journal.

Indicate the number of common shares outstanding of each of the registrant’s classes of common shares, as of the latest practicable date.

At March 28, 2011, there were 83,673,700 common shares outstanding.

Table of Contents

Index to Financial Statements

FORBES ENERGY SERVICES LTD. AND SUBSIDIARIES (a/k/a the “Forbes Group”)

TABLE OF CONTENTS

| Page | ||||||

| PART I | ||||||

| Item 1. |

1 | |||||

| Item 1A. |

10 | |||||

| Item 1B. |

21 | |||||

| Item 2. |

21 | |||||

| Item 3. |

22 | |||||

| Item 4. |

22 | |||||

| PART II | ||||||

| Item 5. |

23 | |||||

| Item 6. |

25 | |||||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

27 | ||||

| Item 7A. |

43 | |||||

| Item 8. |

44 | |||||

| Item 8A. |

45 | |||||

| Item 9. |

Changes in or Disagreements with Accountants on Accounting and Financial Disclosure |

83 | ||||

| Item 9A. |

83 | |||||

| Item 9B. |

85 | |||||

| PART III | ||||||

| Item 10. |

85 | |||||

| Item 11. |

85 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

85 | ||||

| Item 13. |

Certain Relationships and Related Transaction, and Director Independence |

85 | ||||

| Item 14. |

85 | |||||

| PART IV | ||||||

| Item 15. |

86 | |||||

Table of Contents

Index to Financial Statements

This Annual Report on Form 10-K and any oral statements made in connection with it include certain forward-looking statements within the meaning of the federal securities laws. You can generally identify forward-looking statements by the appearance in such a statement of words like “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” or “should” or other comparable words or the negative of these words. When you consider our forward-looking statements, you should keep in mind the risk factors we describe and other cautionary statements we make in this Annual Report on Form 10-K. Our forward-looking statements are only predictions based on expectations that we believe are reasonable. Our actual results could differ materially from those anticipated in, or implied by, these forward-looking statements as a result of known risks and uncertainties set forth below and elsewhere in this Annual Report on Form 10-K. These factors include or relate to the following:

| • | supply and demand for oilfield services and industry activity levels; |

| • | potential for excess capacity; |

| • | spending by the oil and natural gas industry given the continuing worldwide economic downturn; |

| • | our level of indebtedness in the current depressed market; |

| • | possible impairment of our long-lived assets; |

| • | our ability to maintain stable pricing; |

| • | competition; |

| • | substantial capital requirements; |

| • | significant operating and financial restrictions under our indentures; |

| • | technological obsolescence of operating equipment; |

| • | dependence on certain key employees; |

| • | concentration of customers; |

| • | substantial additional costs of compliance with reporting obligations, the Sarbanes-Oxley Act and indenture covenants; |

| • | material weaknesses in internal controls over financial reporting; |

| • | seasonality of oilfield services activity; |

| • | collection of accounts receivable; |

| • | environmental and other governmental regulation, including potential climate change legislation; |

| • | the potential disruption of business activities caused by the physical effects , if any, of climate change; |

| • | risks inherent in our operations; |

| • | market response to global demands to curtail use of oil and natural gas; |

| • | ability to fully integrate future acquisitions; |

| • | variation from projected operating and financial data; |

| • | variation from budgeted and projected capital expenditures; |

| • | volatility of global financial markets; |

| • | risks associated with our foreign operations; and |

| • | the other factors discussed under “Risk Factors” on page 10 of this Annual Report on Form 10-K. |

We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. To the extent these risks, uncertainties and assumptions give rise to events that vary from our expectations, the forward-looking events discussed in this Annual Report on Form 10-K may not occur. All forward-looking statements attributable to us are qualified in their entirety by this cautionary statement.

Available Information

Information regarding Forbes Energy Services Ltd. and its subsidiaries can be found on our internet website at http://www.forbsenergyservices.com. In addition, our annual reports on Form 10-K, quarterly reports on Form 10-Q and amendments to those reports filed or furnished in accordance with Sections 13 or 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, are made available free of charge on our internet website as soon as reasonably practicable after these reports have been electronically filed with, or furnished to, the Securities and Exchange Commission, or the SEC. Information filed with the SEC may be read or copied at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet website (http://www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically.

Table of Contents

Index to Financial Statements

| Item 1. | Business |

Overview

Forbes Energy Services Ltd., or FES Ltd, and its domestic subsidiaries, Forbes Energy Services LLC, or FES LLC, Forbes Energy Capital Inc., or FES CAP, C.C. Forbes, LLC, or CCF, TX Energy Services, LLC, or TES, Superior Tubing Testers, LLC, or STT, and Forbes Energy International, LLC, or FEI, are headquartered in Alice, Texas and conduct business primarily in Texas, Mississippi, Pennsylvania and Mexico. On October 15, 2008, FES LLC and FEI formed Forbes Energy Services México, S. de R.L. de C.V., or FES Mexico Subsidiary, a Mexican limited liability company, (sociedad de responsabilidad limitada de capital variable), to conduct operations in Mexico. On December 3, 2008, Forbes Energy Services Mexico Servicios de Personal, S. de R.L de C. V., or FES Mexico Servicios, a Mexican limited liability company, was formed to provide employee services to FES Mexico Subsidiary, and on June 8, 2009, FES LTD formed a branch in Mexico. The Mexican branch of FES Ltd and the two Mexican limited liability companies are hereinafter referred to, collectively, as “FES Mexico.”

As used in this Annual Report on Form 10-K, the “Company,” the “Forbes Group,” “we,” and “our” mean FES Ltd and its subsidiaries on and after May 29, 2008; FES LLC and its subsidiaries from January 1, 2008 to May 28, 2008; CCF, TES and STT from June 29, 2007 to December 31, 2007; and C.C. Forbes, L.P., Texas Energy Services, L.P. and Superior Tubing Testers L.P., prior to June 29, 2007.

All historical financial data contained in this Annual Report on Form 10-K as of and for the year ended December 31, 2007 and prior periods are of the Forbes Group on a combined basis, and are identified herein as Predecessor – Combined, and shall be identified as such. This financial information is presented on a combined basis because the operating subsidiaries were under common management prior to the reorganization under a common Delaware parent, Forbes Energy Services LLC. All financial statements and other financial data contained in this Annual Report on Form 10-K for all periods after January 1, 2008 are of the Forbes Group on a consolidated basis, or Successor – Consolidated, whether or not specifically identified as such.

We are an independent oilfield services contractor that provides a wide range of well site services to oil and natural gas drilling and producing companies to help develop and enhance the production of oil and natural gas. These services include fluid hauling, fluid disposal, well maintenance, completion services, workovers and recompletions, plugging and abandonment, and tubing testing. Our operations are concentrated in the major onshore oil and natural gas producing regions of Texas, with locations in Baxterville and Laurel, Mississippi; Indiana, Pennsylvania; and Poza Rica, Mexico.

We believe that our broad range of services listed in the preceding paragraph, which extends from initial drilling, through production, to eventual abandonment, is fundamental to establishing and maintaining the flow of oil and natural gas throughout the life cycle of our customers’ wells.

Since our inception in September 2003, we have grown organically from a small South Texas operational base with two well servicing rigs and eight vacuum trucks to a major regional provider of an integrated offering of production and well services. During the period from 2007 to 2009, we successfully executed an aggressive organic growth strategy focused on fleet expansion with the construction of new equipment in a segment of the oilfield services industry characterized by competitors with aging fleets. We believe that our new well servicing rigs and equipment, with an average age of less than four years, significantly differentiate us from our competitors.

We currently provide a wide range of services to a diverse group of over 1,115 companies. Our blue-chip customer base includes ConocoPhillips Company, Apache Corporation, Chesapeake Energy Corporation, Devon Energy Corporation, Dominion Resources, Inc., EOG Resources, Inc., Penn Virginia Corporation, and Petróleos Mexicanos, or PEMEX, among others. John E. Crisp and Charles C. Forbes, our senior management team, have cultivated deep and ongoing relationships with these customers during their average of over 30 years of experience in the oilfield services industry. For the year ended December 31, 2010, we generated revenues of approximately $334.1 million.

We currently conduct our operations through the following two business segments:

| • | Well Servicing. The well servicing segment accounted for 46.5% of our consolidated revenues for the year ended December 31, 2010. At December 31, 2010, our well servicing segment utilized our modern fleet of 173 owned or leased well servicing rigs, which included 162 workover rigs and 11 swabbing rigs, and related assets and equipment. These assets are used to provide (i) well maintenance, including remedial repairs and removal and replacement of downhole production equipment, (ii) well workovers, including significant downhole repairs, re-completions and re-perforations, (iii) completion and swabbing activities, and (iv) plugging and abandoning services. In addition, we have a fleet of nine tubing testing units that are used to conduct pressure testing of oil and natural gas production tubing. |

1

Table of Contents

Index to Financial Statements

| • | Fluid Logistics and Other. The fluid logistics segment accounted for 53.5% of our consolidated revenues for the year ended December 31, 2010. Our fluid logistics segment utilizes our fleet of owned or leased fluid transport trucks and related assets, including specialized vacuum, high-pressure pump and tank trucks, frac tanks, water wells, salt water disposal wells and facilities, and related equipment. These assets are used to provide, transport, store, and dispose of a variety of drilling and produced fluids used in, and generated by, oil and natural gas production. These services are required in most workover and completion projects and are routinely used in daily operations of producing wells. Beginning in the fiscal year 2010, the Company began providing additional services in which Wolverine Construction, Inc., a related party, completed such services as a sub-contractor. These services involve site preparation and are complementary to the traditional services offered by the Company. |

We believe that our two business segments are complementary and create synergies in terms of selling opportunities. Our multiple lines of service are designed to capitalize on our existing customer base to grow within existing markets, generate more business from existing customers, and increase our operating performance. By offering our customers the ability to reduce the number of vendors they use, we believe that we help improve our customers’ efficiency. This is demonstrated by the fact that 74.2% of our revenues for the year ended December 31, 2010 were from customers that utilized services of both of our business segments. Further, by having multiple service offerings that span the life cycle of the well, we believe that we have a competitive advantage over smaller competitors offering more limited services.

The following table summarizes the major components of our equipment fleet at the dates indicated.

| December 31, | ||||||||||||||||||||||||

| Successor-Consolidated | Predecessor- Combined |

|||||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||||||

| Locations |

26 | 28 | 27 | 18 | 12 | |||||||||||||||||||

| Well Servicing Segment |

||||||||||||||||||||||||

| Workover rigs (1) |

162 | 162 | 162 | 95 | 41 | |||||||||||||||||||

| Swabbing rigs |

11 | 9 | 8 | 6 | 2 | |||||||||||||||||||

| Tubing testing units |

9 | 6 | 6 | 6 | 4 | |||||||||||||||||||

| Fluid Logistics Segment |

||||||||||||||||||||||||

| Vacuum trucks(1) |

285 | 290 | 294 | 205 | 147 | |||||||||||||||||||

| High-pressure pump trucks |

19 | 19 | 19 | 14 | 7 | |||||||||||||||||||

| Other heavy trucks |

57 | 57 | 57 | 43 | 25 | |||||||||||||||||||

| Frac tanks(1) |

1,368 | 1,369 | 1,370 | 951 | 568 | |||||||||||||||||||

| Salt water disposal wells |

15 | 18 | 14 | 14 | 9 | |||||||||||||||||||

| (1) | At December 31, 2010, 16 of the vacuum trucks, 10 of the workover rigs, 3 swab rigs and 143 of the frac tanks were leased. |

Reorganizations

Effective January 1, 2008, the members of each of CCF, TES and STT (which included Messrs., John Crisp and Charles Forbes and Ms. Janet Forbes) transferred all of the membership interests they held in such companies to FES LLC in exchange for all of the outstanding membership interests in FES LLC, or the Delaware Reorganization.

In connection with a reorganization completed on May 29, 2008, or the Bermuda Reorganization, each of these members transferred 63% of their respective membership interests in FES LLC to FES Ltd in exchange for Class B shares of FES Ltd. Of the proceeds from the Canadian initial public offering and simultaneous U.S. private placement of 24,644,500 common shares by FES Ltd in May 2008, or the Initial Equity Offering, $120 million was contributed by FES Ltd as additional capital to FES LLC and used to pay the cash consideration for the repurchase by FES LLC of the remaining membership interests held by the individuals who were members of such company. The purchase price for such transaction was determined on the basis of the price per common share under the initial public offering. Mr. John E. Crisp, the Chairman of the Board, President and Chief Executive Officer of FES Ltd, Mr. Charles C. Forbes, the Executive Vice President and Chief Operating Officer of FES Ltd, and Ms. Janet L. Forbes, a director of FES Ltd, each received approximately $36 million from FES LLC upon the repurchase of their remaining membership interests, or approximately 20.9% each of the gross proceeds of the Initial Equity Offering.

In connection with the Bermuda Reorganization, John E. Crisp, our President and Chief Executive Officer, Charles C. Forbes, our Executive Vice President and Chief Operating Officer, and Janet L. Forbes, one of our directors, who were the founders of the Forbes Group and were also the three largest owners of each of the entities comprising the original Forbes Group, along with all of the other members of FES LLC, received Class B shares of FES Ltd. The Class B shares were convertible at any time at the discretion of each holder into common shares and were converted into common shares by the Class B holders in May 2010.

2

Table of Contents

Index to Financial Statements

Upon completion of the Bermuda Reorganization, FES LLC became the wholly owned subsidiary of FES Ltd. Our headquarters and executive offices are located at 3000 South Business Hwy 281, Alice, Texas 78332. We can be reached by phone at (361) 664-0549.

Our Competitive Strengths

We believe that the following competitive strengths position us well within the oilfield services industry:

| • | Young and Modern Fleet. We believe we operate one of the youngest and most modern fleets of well servicing rigs among the large well-servicing companies, based on an average age of well servicing rigs. Approximately 87.9% of our 173 well servicing rigs at December 31, 2010 were built in the last five years. Many of our customers tell us that a younger and more modern fleet is more attractive to them because newer well servicing rigs require less down time for maintenance and generally are more reliable than older equipment. As part of our strategy, we have undertaken to enhance our design specifications to improve the operational and safety characteristics of our equipment compared with older equipment. |

| • | Exposure to Revenue Streams Throughout the Life Cycle of the Well. Our maintenance and workover services expose us to demand from our customers throughout the life cycle of a well, from drilling through production and eventual abandonment. Each new well that is drilled provides us a potential multi-year stream of well services revenue, as our customers attempt to maximize and maintain a well’s productivity. Accordingly, demand for our services is generally driven by the total number of producing wells in a region and is generally less volatile than demand for new well drilling services. |

| • | High Level of Customer Retention with a Blue Chip Customer Base. Our top customers include many of the largest integrated and independent oil and natural gas companies operating onshore in the United States and the government owned energy company, PEMEX, in Mexico. We believe we have been successful in growing in our existing markets as well as expanding to new markets with existing customers due to the quality of our well servicing rigs, our personnel and our safety record. Members of our senior management have maintained excellent working relationships with our top customers in the United States during their average of over 30 years of experience in the oilfield services industry. We believe the complementary nature of our two business segments also helps retain customers because of the efficiency we offer a customer that has multiple needs at the wellsite. Notably, 74.2% of our revenues from the year ended December 31, 2010 were from customers that utilize services of both of our business segments. |

| • | Industry-Leading Safety Record. For 2010, we had approximately 88.0 % fewer reported incidents than the industry average. Our customers tell us that our safety record and reputation are critical factors to purchasing and operations managers in their decision-making process. Over several years, we have developed a strong safety culture based on our training programs and safety seminars for our employees and customers. For example, for several years, members of our senior management have played an integral part in monthly joint safety training meetings with customer personnel. In addition, our deployment of new well servicing rigs with enhanced safety features has contributed to our strong safety record and reputation. |

| • | Experienced Senior Management Team and Operations Staff. Our senior management team of John E. Crisp and Charles C. Forbes has over 65 years of combined experience within the oilfield services industry. In addition, our next level of management, which includes our location managers, has an average of approximately 24 years of experience in the industry. |

Our Business Strategy

Our strategy is to continue to do the following:

| • | Maintain maximum asset utilization. We constantly monitor asset usage and industry trends in order to maximize utilization. We accomplish this through moving assets from regions with less activity to those with more activity or that are increasing in activity. In the current economic environment, we are focusing on basins that are either predominantly oil or contain natural gas with high liquids content, such as the Eagle Ford basin in South Texas, as these areas are forecast to experience substantial growth for the foreseeable future. |

3

Table of Contents

Index to Financial Statements

| • | Focus on Proven and Established Oil and Natural Gas Basins. We focus our operations on customers that operate in well-established basins which have proven production histories and that have maintained a higher level of activity throughout various oil and natural gas pricing environments. We believe that this creates a more stable revenue stream for us as the production related services we provide our customers are tied more to ongoing production from proven wells and less to exploratory activity that was negatively influenced by the recent precipitous decreases in oil and natural gas prices throughout 2009. Our experience shows that production-related services have generally withstood the current depressed economic conditions better than exploratory services. |

| • | Establish and Maintain Leadership Position in Core Operating Areas. Based on our estimates, we believe that we have a significant market share in well servicing and fluid logistics in South Texas. We strive to establish and maintain market leadership positions within all of our core operating areas. To achieve this goal, we maintain close customer relationships and offer high-quality services and the newest equipment for our customers. In addition, our significant presence in our core operating areas facilitates employee retention and hiring, and brand recognition. |

| • | Maintain a Disciplined Growth Strategy. Through the third quarter of 2008, we grew our business by following our customers to new locations which have been in reasonably close proximity to our existing locations. In 2007, we expanded from our initial presence in the Cotton Valley with a location in Marshall to Kilgore and Carthage, Texas. We have followed the same strategy in the Permian Basin, where we established an initial presence in Ozona and subsequently expanded to San Angelo, Monahans, Odessa and Big Spring, Texas. In 2008 we expanded to Mexico, acquiring a presence in the city of Poza Rica. We believe that this growth strategy allows us to create synergies in geographic areas and then permits us to expand profitably from those geographic areas in which we have created a critical mass. During 2009, we severely curtailed our expansion due to the severe downturn in the industry, expanding into only two new locations in Franklin, Texas and Indiana, Pennsylvania, while closing one location in Denver City, Texas. During the fourth quarter of 2009 and throughout 2010, we began to experience an upturn in the industry resulting in higher utilization of our assets. During 2010, in response to customer demand, we opened new rig yards in Laurel, Mississippi, and Lamesa, Texas as well as moving our Pennsylvania rig yard from Washington, Pennsylvania to Indiana, Pennsylvania. We also closed four yards. We exited North Texas with the closing of our Godley well service yard. We also closed three additional yards and absorbed those assets into existing yards; Edinburg, Texas, Liberty, Texas, and Franklin, Texas. Given our limited working capital and restrictive covenants under our indentures, we plan to continue to delay new asset additions for the near term. It is anticipated that new capital requirements, as limited by the restrictive covenants under our indentures, in the near term will be met through cash flow from operations, operating leases or equipment rentals. In prior filings, we disclosed that we were working on an agreement for the use of two workover rigs in Colombia. At the present time, it does not appear that this transaction will be completed. |

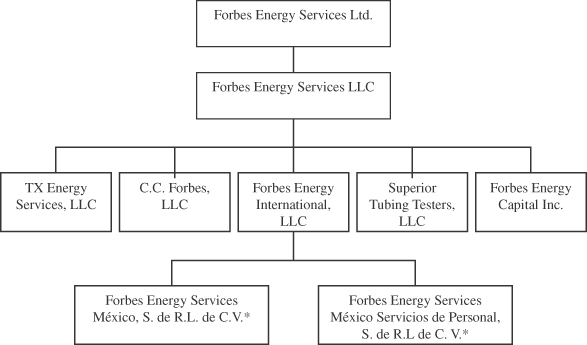

Corporate Structure

FES Ltd is a Bermuda exempt company created on April 9, 2008 to serve as the holding company for FES LLC and its subsidiaries. FES LLC is a Delaware limited liability company and the U.S. holding company for our operating entities. We operate primarily through the following four subsidiaries which are all Delaware limited liability companies directly owned by FES LLC - CCF, TES, STT and FEI. FEI was formed to hold the equity securities of FES Mexico Subsidiary and FES Mexico Servicios, Mexican limited liability companies that were originally formed to hold our Mexican operations. Subsequently Mexican operations were moved to the Mexican branch of FES Ltd. FES LLC also holds the equity securities of FES CAP, a Delaware corporation created solely to be a co-issuer of our senior secured notes. The following chart graphically illustrates our current structure:

4

Table of Contents

Index to Financial Statements

| * | Forbes Energy Services México, S. de R.L. de C.V. and Forbes Energy Services Mexico Servicios de Personal, S. de C.V. are each 99.99% owned by Forbes Energy International, LLC and 0.01% owned by Forbes Energy Services LLC. |

Description of Business Segments

Well Servicing Segment

Through a modern fleet of 173 well servicing rigs, as of December 31, 2010, situated in 21 operational areas across Texas, two in Mississippi, one in Pennsylvania, and one in Mexico, we provide a comprehensive offering of well servicing activities to oil and natural gas companies in Texas and our other locations, including completions of newly drilled oil and natural gas wells, wellbore maintenance, workovers and re-completions, tubing testing, and plugging and abandonment services. Our well servicing rig fleet has an average age of less than four years. As part of our operational strategy, we enhanced our design specifications to improve the operational and safety characteristics of our well servicing rigs compared with older well servicing rigs operated by others in the industry. These include increased derrick height and weight ratings, and increased mud pump horsepower. We believe these enhanced features translate into increased demand for our equipment and services along with better pricing for our equipment and personnel. In addition, we augment our well servicing rig fleet with auxiliary equipment, such as mud pumps, power swivels, mud plants, mud tanks, blow-out preventers, lighting plants, generators, pipe racks and tongs, which results in incremental rental revenue and increases the profitability of a typical well service job.

We provide the following services in our well servicing segment:

| • | Completions. Utilizing our well servicing rig fleet, we perform completion services, which involve perforating and/or stimulating a wellbore to allow it to flow oil or natural gas, along with swabbing operations that are utilized to clean a wellbore prior to production. Completion operations are generally shorter term in nature and involve our equipment operating on a site for a period of two to three days. |

| • | Maintenance. Through our fleet of well servicing rigs, we provide for the removal and repair of sucker rods, downhole pumps and other production equipment, the repair of failed production tubing, and the removal of sand, paraffin and other downhole production-related byproducts that impair well productivity. These operations typically involve our well servicing rigs operating on a wellsite for five to seven days. |

| • | Workovers and Re-completions. We provide workover and re-completion services for existing wellbores. These services are designed to significantly enhance productivity by re-perforating to initiate or re-establish productivity from an oil or natural gas wellbore. In addition, we provide major downhole repairs such as casing repair, production tubing replacement, and deepening and sidetracking operations used to extend a wellbore laterally or vertically. These operations are typically longer term in nature and involve our well servicing rigs operating on a wellsite for one to two weeks at a time. |

5

Table of Contents

Index to Financial Statements

| • | Tubing Testing. Through a fleet of nine downhole testing units, we provide downhole tubing testing services that allow operators to verify tubing integrity. Tubing testing services are performed as production tubing is run into a new wellbore or on older wellbores as production tubing is replaced during a workover operation. Tubing testing services are complementary to our other service offerings and provide a significant opportunity for cross-selling. |

| • | Plugging and Abandonment. Our well servicing rigs are also used in the process of permanently closing oil and natural gas wells that are no longer capable of producing in economic quantities. Plugging and abandonment work can be performed with a well servicing rig along with wireline and cementing equipment; however, this service is typically provided by companies that specialize in plugging and abandonment work. Many well operators bid this work on a “turnkey” basis, requiring the service company to perform the entire job, including the sale or disposal of equipment salvaged from the well as part of the compensation received, and complying with state regulatory requirements. We perform plugging and abandonment work in conjunction with equipment provided by other service companies. In January 2011 we hired several experienced plugging and abandonment employees and plan to expand our presence in this segment. |

Fluid Logistics Segment

Our fluid logistics segment provides an integrated array of oilfield fluid sales, transportation, storage, and disposal services that are required on most workover, drilling, and completion projects and are routinely used in daily operation of producing wells by oil and natural gas producers. We have a substantial operational footprint with 16 fluid logistics locations across Texas as of December 31, 2010, and an extensive fleet of transportation trucks, high-pressure pump trucks, frac tanks, and salt water disposal wells. This combination of services enables us to provide a one-stop source for oil and natural gas companies. We believe that the vast majority of our smaller competitors in this segment can provide some, but not all, of the equipment and services required by customers, thereby requiring them to use several companies to meet their requirements and increasing their administrative burden. In addition, by pursuing an integrated approach to service, we experience increased asset utilization rates, as multiple assets are usually required to provide a given service.

We provide the following services in our fluid logistics segment:

| • | Fluid Hauling. At December 31, 2010, we owned or leased 361 fluid service vacuum trucks, trailers, and other hauling trucks equipped with a fluid hauling capacity of up to 150 barrels per unit. Each fluid service truck unit is equipped to pump fluids from or into wells, pits, tanks, and other on-site storage facilities. The majority of our fluid service truck units are also used to transport water to fill frac tanks on well locations, including frac tanks provided by us and others, to transport produced salt water to disposal wells, including injection wells owned and/or operated by us, and to transport drilling and completion fluids to and from well locations. In conjunction with the rental of frac tanks, we use fluid service trucks to transport water for use in fracturing operations. Following completion of fracturing operations, our fluid service trucks are used to transport the flowback produced as a result of the fracturing operations from the wellsite to disposal wells. |

| • | Disposal Services. Most oil and natural gas wells produce varying amounts of salt water throughout their productive lives. Under Texas law, oil and natural gas wastes and salt water produced from oil and natural gas wells are required to be disposed of in authorized facilities, including permitted salt water disposal wells. Injection wells are licensed by state authorities and are completed in permeable formations below the fresh water table. At December 31, 2010, we operated 15 disposal wells in 13 locations across Texas, with an aggregate injection capacity of approximately 115,500 barrels per day, that are permitted to dispose of salt water, and incidental non-hazardous oil and natural gas wastes throughout our operational bases in Texas. Our transport trucks frequently transport fluids that are disposed of in these salt water disposal wells. The salt water disposal wells are strategically located in close proximity to the producing wells of our customers. We maintain separators at all 15 disposal wells, which permits us to salvage residual crude oil that is used in operations or later sold. |

| • | Equipment Rental. At December 31, 2010, we owned or leased a fleet of 1,368 fluid storage tanks that can store up to 500 barrels of fluid each or an aggregate storage capacity of approximately 684,000 barrels. This equipment is used by oilfield operators to store various fluids at the wellsite, including fresh water, brine and acid for frac jobs, flowback, temporary production, and mud storage. We transport the tanks with our trucks to well locations that are usually within a 75-mile radius of our nearest location. Frac tanks are used during all phases of the life of a producing well. A typical fracturing operation can be completed within four days using five to 25 or more frac tanks. We believe we maintain one of the youngest frac tank fleets in the industry with an average equipment age of less than four years. |

| • | Fluid Sales. We sell and transport a variety of fluids used in drilling, completion and workover operations for oil and natural gas wells. Although a relatively small percentage of our overall business, the provision of these fluids drives asset utilization rates and revenue from associated equipment. Through these services, we provide fresh water used in fracturing fluid, completion fluids, cement, and drilling mud. In addition, we provide potassium chloride for completion fluids, brine water, and water-based drilling mud. |

| • | Site Preparation Services. In the fiscal year 2010, the Company began providing site preparation services that are complementary to the traditional services offered by the Company. Wolverine Construction, Inc., a related party, completed such services as a sub-contractor. We billed the cost to the customer with a margin of between 5%-10%. |

6

Table of Contents

Index to Financial Statements

Financial Information about Segments and Geographic Areas

See Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 14 to our consolidated financial statements for the year ended December 31, 2010 included in this Annual Report on Form 10-K for further discussion regarding financial information by segment and geographic location. For a discussion of the risks associated with our foreign operations, please see Item 1A “Risk Factors – Our international operations could be adversely affected” and “Our operations in Mexico are subject to risks associated with contract bidding” on page 19 of this Annual Report on Form 10-K.

Seasonality

Our operations are impacted by seasonal factors. Please see Item 1A “Risk Factors – Activity in the oilfield services industry is seasonal and may affect our revenues during certain periods” on page 16 of this Annual Report on Form 10-K for additional information.

Sales and Marketing

Sales and marketing functions are performed at two levels: at the field level and through our sales representatives and executives. At the field level, our operations and rig supervisors are in constant contact with their counterparts at our customers. This contact includes working closely in the field, problem resolution efforts, and 24-hour availability. Employees of our customers become accustomed to working closely with and depending on our personnel for assistance, guidance, advice and in other areas where teams typically interact. Our objective is for our customers to see our employees as an extension of the customers’ employees and resources. These relationships not only secure business long-term, but also generate additional business as new opportunities arise.

Our sales representatives and executives perform more traditional sales activities such as calling on customers, sending proposals, and following up on jobs to ensure customer satisfaction. This includes heavy participation in customer safety programs where our executives and sales staff either participate in or teach safety classes at various customer locations. From a sales standpoint, this close involvement and support is key to establishing and maintaining long-term relationships with the major oil and natural gas companies.

We operate a decentralized sales and marketing organization, where local management teams are largely responsible for developing stronger relationships with customers at the field level. Our customers typically are relationship driven, and make decisions at the local level.

We cross-market our well servicing rigs along with our fluid logistics services, thereby offering our customers the ability to minimize vendors, which we believe improves the efficiency of our customers. This is demonstrated by the fact that 74.2% of our revenues for the year ended December 31, 2010 were from customers that utilized services of both of our business segments.

Employees

At December 31, 2010, we had 1,893 employees. We provide comprehensive employee training, and implement recognized standards for health and safety. None of our employees are represented by a union or employed pursuant to a collective bargaining agreement or similar arrangement. We have not experienced any strikes or work stoppages, and we believe we have good relations with our employees. As of December 31, 2010, we had increased our overall workforce by approximately 18.2% or 291 employees when compared to December 31, 2009. This is a direct result of the current positive industry trends which have resulted in the need for additional personnel to service the increased activity levels.

Continued retention of existing qualified management and field employees and availability of additional qualified management and field employees will be a critical factor in our continued success as we work to ensure that we have adequate levels of experienced personnel to service our customers. Given industry trends, this continues to be increasingly challenging.

Competition

Our competition includes small regional service providers as well as larger companies with operations throughout the continental United States and internationally. Our four largest competitors are Basic Energy Services, Inc., Complete Production Services, Inc., Key Energy Services, Inc. and Nabors Industries Ltd. We believe that these larger competitors primarily have centralized management teams that direct their operations and decision-making primarily from corporate and regional headquarters. In addition, because of their size, these companies market a large portion of their work to the major oil and natural gas companies. We compete primarily on the basis of the young age and quality of our equipment, our safety record, the quality and expertise of our employees and our responsiveness to customer needs.

7

Table of Contents

Index to Financial Statements

Customers

We served in excess of 1,115 customers during the year ended December 31, 2010. For the years ended December 31, 2010, 2009 and 2008, our largest customer, PEMEX, comprised approximately 13.7%, 11.7%, and 8.6% of our consolidated revenues, our five largest customers comprised approximately 35.9%, 37.7%, and 30.3% of our consolidated revenues, and our ten largest customers comprised approximately 51.9%, 49.8%, and 42.9% of our consolidated revenues. During 2010, PEMEX comprised 13.7% of our consolidated revenues. During 2009, PEMEX and ConocoPhillips comprised of 11.7% and 11.1% of our consolidated revenues, respectively. During 2008 no customers comprised greater than 10.0% of our consolidated revenues. We had been expanding our market base and adding new customers until the decrease in activity in the oil and gas industry that began in the fourth quarter of 2008. Activity in the oil and gas industry began to improve in the last half of 2010 through the current period and we are again expanding revenues within our existing customer base. Nevertheless, the loss of our top customer or of several of the customers in the top ten would materially adversely affect our revenues and results of operations. We believe that customers lost could be replaced with other customers, but there can be no assurance that lost revenues could be replaced in a timely manner or at all, especially given the market competitiveness.

Our business segments charge customers by the hour, day or project for services, equipment and personnel.

We have master service agreements in place with most of our customers, under which jobs or projects are awarded on the basis of price, type of service, location of equipment, and the experience level of work crews.

Suppliers

Historically, we have purchased or leased our well servicing rigs from several third-party or related party suppliers. During the year ended December 31, 2010, we leased 2 swab units, and purchased no well service rigs or swab units.

We purchase well servicing chemicals, drilling fluids, and related supplies from various third-party suppliers. We purchase potassium chloride from two suppliers Agri-Empresa, Inc. and Tetra Technologies, Inc. For all other well servicing products, such as barite, surfactants, and drilling fluids, we purchase from various suppliers of well servicing products when needed.

Although we do not have written agreements with any of our suppliers (other than leases with respect to certain of our rigs and equipment), we have not historically suffered from an inability to purchase or lease equipment or purchase raw materials.

Insurance

Our operations are subject to risks inherent in the oilfield services industry, such as equipment defects, malfunctions, failures and natural disasters. In addition, hazards such as unusual or unexpected geological formations, pressures, blow-outs, fires or other conditions may be encountered in drilling and servicing wells, as well as the transportation of fluids and our assets between locations. We have obtained insurance coverage against certain of these risks which we believe is customary in the industry, including $1 million in general liability per occurrence, $25 million in umbrella coverage and $50 million of excess liability coverage. Such insurance is subject to coverage limits and exclusions and may not be available for all of the risks and hazards to which we are exposed. In addition, no assurance can be given that such insurance will be adequate to cover our liabilities or will be generally available in the future or, if available, that premiums will be commercially justifiable. If we incur substantial liability and such damages are not covered by insurance or are in excess of policy limits, or if we incur such liability at a time when we are not able to obtain liability insurance, our business, results of operations and financial condition could be materially and adversely affected.

Environmental Regulations

Our operations are subject to various federal, state and local laws and regulations in the United States and Mexico pertaining to health, safety and the environment. Laws and regulations protecting the environment have become more stringent over the years, and in certain circumstances may impose strict liability, rendering us liable for environmental damage without regard to negligence or fault on our part. Moreover, cleanup costs, penalties and other damages arising as a result of new, or changes to existing, environmental laws and regulations could be substantial and could have a material adverse effect on our financial condition, results of operations and cash flows. We believe that we conduct our operations in substantial compliance with current United States and Mexican federal, state and local requirements related to health, safety and the environment.

8

Table of Contents

Index to Financial Statements

The following is a summary of the more significant existing environmental, health and safety laws and regulations to which our operations are subject and for which compliance may have a material adverse effect on our results of operation or financial position. See Item 1A “Risk Factors—Due to the nature of our business, we may be subject to environmental liability” on page 16 of this Annual Report on Form 10-K for further details.

Hazardous Substances and Waste

The Comprehensive Environmental Response, Compensation, and Liability Act, as amended, or CERCLA, and comparable state laws in the United States impose liability without regard to fault or the legality of the original conduct on certain defined persons, including current and prior owners or operators of the site where a release of hazardous substances occurred and entities that disposed or arranged for the disposal of the hazardous substances found at the site. Under CERCLA, these responsible persons may be liable for the costs of cleaning up the hazardous substances, for damages to natural resources, and for the costs of certain health studies. In the course of our operations, we generate materials that are regulated as hazardous substances and, as a result, may incur CERCLA liability for cleanup costs. Also, claims may be filed for personal injury and property damage allegedly caused by the release of hazardous substances or other pollutants.

We also generate solid wastes that are subject to the requirements of the Resource Conservation and Recovery Act, as amended, or RCRA, and comparable state statutes. Certain materials generated in the exploration, development, or production of crude oil and natural gas are excluded from RCRA’s hazardous waste regulation, but these wastes, which include wastes currently generated during our operations, could be designated as “hazardous wastes” in the future and become subject to more rigorous and costly disposal requirements. Any such changes in the laws and regulations could have a material adverse effect on our operating expenses.

Although we have used operating and disposal practices that were standard in the industry at the time, hydrocarbons or other wastes may have been released at properties owned or leased by us now or in the past, or at other locations where these hydrocarbons and wastes were taken for treatment or disposal. Under CERCLA, RCRA and analogous state laws, we could be required to clean up contaminated property (including contaminated groundwater), perform remedial activities to prevent future contamination, or pay for associated natural resource damages.

In Mexico, hazardous wastes must be handled in accordance with the provisions of the General Law for the Prevention and Integral Management of the Wastes and its Regulations. This law requires, among other things, that persons who generate hazardous waste (i) register the amount and kind of hazardous waste generated; (ii) label, package and store the hazardous waste in a prescribed manner; (iii) maintain duly completed manifests regarding generation, transportation and final disposition of the hazardous waste; (iv) obtain a registration from Mexican authorities; (v) ensure that all subcontractors dealing with the transportation, treatment and final disposition of the hazardous waste have the proper registration issued by Mexican authorities; and (vi) avoid soil contamination and/or spills.

Water Discharges

We operate facilities that are subject to requirements of the Clean Water Act, as amended, or CWA, and analogous state laws that impose restrictions and controls on the discharge of pollutants into navigable waters. Pursuant to these laws, permits must be obtained to discharge pollutants into state waters or waters of the United States, including to discharge storm water runoff from certain types of facilities. Spill prevention, control, and countermeasure requirements under the CWA require implementation of measures to help prevent the contamination of navigable waters in the event of a hydrocarbon spill. The CWA can impose substantial civil and criminal penalties for non-compliance.

Employee Health and Safety

We are subject to the requirements of the federal Occupational Safety and Health Act, as amended, or OSHA, and comparable state laws that regulate the protection of employee health and safety. OSHA’s hazard communication standard requires that information about hazardous materials used or produced in our operations be maintained and provided to employees, state and local government authorities and citizens. We believe that our operations are in substantial compliance with OSHA requirements.

Climate Change Regulation

The U.S. Congress has been considering legislation to reduce the emissions of certain gases, commonly referred to as “greenhouse gases,” including carbon dioxide and methane, which, according to certain scientific studies, might contribute to the warming of the Earth’s atmosphere and other climatic changes. On June 26, 2009, the U.S. House of Representatives passed the American Clean Energy and Security Act of 2009, or ACESA, which would establish an economy-wide cap-and-trade program to reduce U.S. emissions of these greenhouse gases. ACESA would require a 17% reduction in greenhouse gas emissions from 2005 levels by 2020 and just over an 80% reduction of such emissions by 2050. Under the ACESA, the Environmental Protection Agency, or the EPA, would issue a capped and steadily declining number of tradable emissions allowances to major sources of greenhouse gas emissions permitting such sources to continue to emit greenhouse gases into the atmosphere. The cost of these allowances would be expected to increase significantly over time. ACESA would impose increasing costs on the combustion of carbon-based fuels such as oil and natural gas. The U.S. Senate began work on its own legislation for restricting domestic greenhouse gas emissions and President Obama has indicated his support of legislation to reduce greenhouse gas emissions through an emission allowance system. Although it is not currently possible to predict when or if the Senate may act on climate change legislation or how any such bill would be reconciled with ACESA, any future federal laws or implementing regulations that may be adopted to address the emission of greenhouse gases could adversely affect demand for our services by reducing demand for the oil and natural gas produced by our customers. Such legislation could also increase our operating costs.

9

Table of Contents

Index to Financial Statements

Additionally, on December 7, 2009, the EPA announced its finding that greenhouse gas emissions presented an endangerment to human health and the environment. This endangerment finding allows the EPA to proceed with the adoption and implementation of regulations that would restrict emissions of greenhouse gases under existing provisions of the federal Clean Air Act. In September 2009, the EPA proposed regulations in anticipation of finalizing its endangerment finding that would require a reduction in greenhouse gas emissions from motor vehicles and, could also trigger permit review for greenhouse gas emissions from certain stationary sources. On October 30, 2009, the EPA published a final rule requiring the reporting of greenhouse gas emissions from specified large greenhouse gas emission sources in the United States beginning in 2011 for emissions occurring in 2010. On November 30, 2010, the EPA issued regulations that expanded reporting requirements to include onshore and offshore petroleum and natural gas production; natural gas processing, distribution and storage; and facilities that inject and store carbon dioxide underground for the purposes of geologic sequestration or enhanced oil and gas recovery. Reporting requirements under these new regulations are mandatory beginning in 2012 for emissions occurring in 2011.

In Mexico, emissions generated as a result of the development of oil and other petrochemicals, including work related to oil wells, are governed by Mexican regulation which requires a license issued by Mexican authorities. The license must be updated annually by filing an annual operation report.

The adoption and implementation of additional regulations that would impose reporting obligations on, or limiting emissions of greenhouse gases from, our equipment and operations and the equipment and operations of our customers could require us to incur increased operating costs and could adversely affect demand for crude oil and natural gas produced by our customers, which would adversely affect demand for our services. The potential increase in the costs of our operations and the operations of our customers could include additional costs to operate and maintain equipment and facilities, install new emission controls on equipment and facilities, acquire allowances to authorize greenhouse gas emissions, pay any taxes related to greenhouse gas emissions and administer and manage a greenhouse gas emissions program. While we may be able to include some or all of such increased operating costs in the rates we charge for our services, any recovery of such costs is uncertain. Even if such legislation is not adopted at the national level, a number of states, acting either individually or through multi-state regional initiatives, have already begun implementing legal measures to reduce emissions of greenhouse gases. While no such legislation is currently being considered in Texas, many of our customers operate nationally and would be adversely affected by the requirements of such legislation. Any one of these climate change regulatory and legislative initiatives could have a material adverse effect on our business, financial condition and results of operations.

Other Laws and Regulations

We operate salt water disposal wells that are subject to the CWA, Safe Drinking Water Act, and state and local laws and regulations, including those established by the Environmental Protection Agency’s Underground Injection Control Program which establishes the minimum program requirements. Our salt water disposal wells are located in Texas, which requires us to obtain a permit to operate each of these wells. We have such permits for each of our salt water disposal wells. The Texas regulatory agency may suspend or modify any of these permits if such well operation is likely to result in pollution of fresh water, substantial violation of permit conditions or applicable rules, or leaks to the environment. We maintain insurance against some risks associated with our well service activities, but there can be no assurance that this insurance will continue to be commercially available or available at premium levels that justify its purchase by us. The occurrence of a significant event that is not fully insured or indemnified could have a materially adverse effect on our financial condition and operations.

In Mexico, all work related to the development of oil and other petrochemicals, including work related to oil wells, must be authorized by Mexican authorities, that require an environmental impact statement related to such work.

| Item 1A. | Risk Factors |

The following information describes certain significant risks and uncertainties inherent in our business. You should take these risks into account in evaluating us. This section does not describe all risks applicable to us, our industry or our business, and it is intended only as a summary of known material risks that are specific to the company. You should carefully consider such risks and uncertainties together with the other information contained in this Form 10-K. If any of such risks or uncertainties actually occurs, our business, financial condition or operating results could be harmed substantially and could differ materially from the plans and other forward-looking statements included in Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on page 26 of this Annual Report on Form 10-K and elsewhere herein.

10

Table of Contents

Index to Financial Statements

RISKS RELATING TO OUR COMMON SHARES

The dividend, liquidation and redemption rights of the holders of our Series B Senior Convertible Preferred Shares may adversely affect our financial position and the rights of the holders of our common shares.

The Company has Series B Senior Convertible Preferred Shares, or the Series B Preferred Shares, outstanding. The Forbes Group will have the obligation to pay to the holders of its Series B Preferred Shares quarterly dividends of five percent per annum of the original issue price, payable quarterly in cash or in-kind. No dividends may be paid to holders of common shares while accumulated dividends remain unpaid on the Series B Preferred Shares. Currently, dividends for the quarterly periods ended November 28, 2010 and February 28, 2011 have not been paid on the Series B Preferred Shares. Therefore, the Company is prohibited at this time from issuing dividends on its common shares. The Company has not paid this dividend in cash due to certain restrictions in the Company’s indentures and has not paid this dividend in-kind because the Toronto Stock Exchange has taken the position that, in light of the market price of the Company’s common shares, the issuance of additional Series B Preferred Shares as a dividend in-kind would violate Toronto Stock Exchange rules regarding the issuance of discounted shares, unless the Company receives shareholder approval for such an issuance. The Company intends to seek shareholder approval for a pool of Series B Preferred Shares to be issued as in-kind dividends for this particular quarterly period and for future quarterly periods. Should the shareholders not approve these dividend payments in-kind, as contemplated under the Certificate of Designation of the Series B Senior Convertible Preferred Shares, the Company could be required to delist from the Toronto Stock Exchange.

Further, the Company is required, at the seventh anniversary of the issuance of the Series B Preferred Shares on May 28, 2017, to redeem any such outstanding shares at their original issue price, plus any accumulated and unpaid dividends, to be paid, at the election of the Company, in cash or common shares. The payment of the redemption price in cash is expected to result in reduced capital resources available to the Company. The payment of the redemption price in common shares would directly dilute the common shareholders. The payment of dividends in-kind would also have a dilutive effect on the common shareholders (as any Series B Preferred Shares issued as dividends will be themselves convertible into common shares). In the event that the Company is liquidated while Series B Preferred Shares are outstanding, holders of the Series B Preferred Shares will be entitled to receive a preferred liquidation distribution, plus any accumulated and unpaid dividends, before holders of common shares receive any distributions.

Holders of the Series B Preferred Shares have certain voting and other rights that may adversely affect holders of our common shares, and the holders of our Series B Preferred Shares may have different interests from, and vote their shares in a manner deemed adverse to, holders of our common shares.

As mentioned in the preceding risk factor, the Company has not paid a dividend on its Series B Preferred Shares for the quarterly periods ended November 28, 2010 and February 28, 2011. In the event that we fail to pay dividends, in cash or in-kind, on the Series B Preferred Shares for an aggregate of at least eight quarterly dividend periods (whether or not consecutive), the holders of the Series B Preferred Shares will be entitled to vote at any meeting of the shareholders with the holders of the common shares and to cast the number of votes equal to the number of whole common shares into which the Series B Preferred Shares held by such holders are then convertible. If the holders of the current Series B Preferred Shares were able to vote pursuant to this provision at this time or converted the Series B Preferred Shares into common shares, we believe that those holders would be entitled to an aggregate of 15,005,799 votes resulting from their ownership of Series B Preferred Shares. This together with common shares already held by these shareholders (as reported to the Company by such shareholders), would entitle these shareholders to just under 20%, in the aggregate, of the voting power of the Company. Further, the holders of Series B Preferred Shares may have certain voting rights with respect to the approval of amendments to the organizational documents of the Company or certain transactions between the Company and affiliate shareholders.

The holders of Series B Preferred Shares may have different interests from the holders of our common shares and could vote their shares in a manner deemed adverse to the holders of common shares.

RISKS RELATING TO OUR BUSINESS

The industry in which we operate is highly volatile, and there can be no assurance that demand for our services will continue to improve from previous depressed levels.

The demand, pricing and terms for oilfield services in our existing or future service areas largely depend upon the level of exploration and development activity for both crude oil and natural gas in the United States. Oil and natural gas industry conditions are influenced by numerous factors over which we have no control, including oil and natural gas prices, expectations about future oil and natural gas prices, levels of consumer demand, the cost of exploring for, producing and delivering oil and natural gas, the expected rates of current production, the discovery rates of new oil and natural gas reserves, available pipeline and other oil and natural gas transportation capacity, weather conditions, political, regulatory and economic conditions, and the ability of oil and natural gas companies to raise equity capital or debt financing.

11

Table of Contents

Index to Financial Statements

In the fourth quarter 2008 and during 2009, the level of activity in the oil and natural gas industry in the United States experienced a severe downturn. The industry decline resulted in the reduction of oil and natural gas prices. Although oil prices and our utilization trends improved during 2010, there can be no assurance that depressed natural gas prices will improve or that the current improving trend in oil prices or our utilization will continue. We expect that a continuation of the recent severe reduction in natural gas prices or a reduction in oil prices would have a negative effect on oil and natural gas production levels and therefore affect the demand for drilling and well services by oil and natural gas companies. Any addition to, or elimination or curtailment of, government incentives for companies involved in the exploration for and production of oil and natural gas could have a significant effect on the oilfield services industry in the United States. Lower oil and natural gas prices could also cause our customers to seek to terminate, renegotiate or fail to honor our services contracts. It could affect the fair market value of our equipment fleet which, under specific circumstances, in turn could trigger a write down of our assets for accounting purposes. Lower oil and natural gas prices could also affect our ability to retain skilled oilfield services personnel and our ability to obtain access to capital to fund and grow our business. A reversal in the current trend of improving industry activity and pricing at current levels could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We may be adversely affected by uncertainty in the global financial markets and the continuing worldwide economic downturn.

Our future results may be impacted by the continuing worldwide economic downturn, continued volatility or deterioration in the debt and equity capital markets, inflation, deflation, or other adverse economic conditions that may negatively affect us or parties with whom we do business resulting in their non-payment or inability to perform obligations owed to us such as the failure of customers to honor their commitments, or the failure of major suppliers to complete orders. Additionally, credit market conditions may change slowing our collection efforts as customers may experience increased difficulty in obtaining requisite financing, potentially leading to lost revenue and higher than normal accounts receivable. This could result in greater expense associated with collection efforts and increased bad debt expense.

The current global economic environment may adversely impact our ability to issue additional debt. A continuation of the economic uncertainty may cause institutional investors to respond to their customers by increasing interest rates, enacting tighter lending standards or refusing to refinance existing debt upon maturity or on terms similar to expiring debt. Even with the net proceeds of the December 2009 common equity offering and our May 2010 preferred equity offering, we may require additional capital in the future. However, due to the above listed factors, we cannot be certain that additional funding will be available if needed and, to the extent required, on acceptable terms.

Our business depends on domestic spending by the oil and natural gas industry, and this spending and our business may be adversely affected by industry and financial market conditions that are beyond our control.

We depend on our customers’ willingness to make operating and capital expenditures to explore, develop and produce oil and natural gas in the United States. Current low natural gas prices, a decline in oil prices and global economic uncertainty may reduce the availability of capital for operating and capital expenditures and may curtail spending thereby reducing demand for our services and equipment.

Industry conditions are influenced by numerous factors over which we have no control, such as the supply of and demand for oil and natural gas, domestic and worldwide economic conditions, political instability in oil and natural gas producing countries and merger and divestiture activity among oil and natural gas producers. The volatility of the oil and natural gas industry and the consequent impact on exploration and production activity could adversely impact the level of drilling and workover activity by some of our customers. Any such reduction may cause a decline in the demand for our services or adversely affect the price of our services. In addition, reduced discovery rates of new oil and natural gas reserves in our market areas also may have a negative long-term impact on our business, even in an environment of stronger oil and natural gas prices, to the extent existing production is not replaced and the number of producing wells for us to service declines.

During 2009, adverse changes in capital markets caused a number of oil and natural gas producers to announce reductions in capital budgets for future periods. In the fourth quarter of 2009 and in 2010, several of these producers announced increased capital budgets relative to their lows in mid-2009. Even so, limitations on the availability of capital, or higher costs of capital, for financing expenditures may cause these and other oil and natural gas producers to limit capital budgets in the future even if commodity prices remain at historically high levels.

12

Table of Contents

Index to Financial Statements

These same economic factors impact our customers’ ability to pay amounts due to us on a timely basis. During 2009, this impacted a significant number of our customers resulting in several million dollars in uncollectable accounts receivable. While the severity of the negative financial impact of the industry downturn has subsided, there can be no assurances that another slowdown or downturn may not occur creating additional significant levels of uncollectable accounts receivable.

Our indebtedness could restrict our operations and make us more vulnerable to adverse economic conditions.

As of December 31, 2010, our long-term debt, including current portions, was $219.4 million. In the event the current industry upward trend reverses and we experience a decline in activity as we experienced in 2009, our level of indebtedness may adversely affect operations and limit our growth. Our level of indebtedness may affect our operations in several ways, including the following:

| • | by increasing our vulnerability to general adverse economic and industry conditions; |

| • | due to the fact that the covenants that are contained in the indentures governing our indebtedness limit our ability to borrow funds, dispose of assets, pay dividends, make certain investments and make certain capital expenditures; |

| • | due to the fact that any failure to comply with the covenants of our indentures (including failure to make the required interest payments) could result in an event of default, which could result in some or all of our indebtedness under our indentures becoming immediately due and payable; and |

| • | due to the fact that our level of debt may impair our ability to obtain additional financing in the future for working capital, capital expenditures, acquisitions or other general corporate purposes. |

These restrictions could have a material adverse effect on our business, financial position, results of operations and cash flows and the ability to satisfy the obligations under our indentures. Further, due to cross-default provisions in the indenture governing our 11% senior secured notes, or Second Priority Notes, and the indenture governing our first lien floating rate notes, or First Priority Notes, a default and acceleration of outstanding debt under one indenture would result in the default and possible acceleration of outstanding debt under our other indenture. Accordingly, an event of default could result in all or a portion of our outstanding debt under our indentures becoming immediately due and payable. If this occurred, we might not be able to obtain waivers or secure alternative financing to satisfy all of our obligations simultaneously which might even force us to seek bankruptcy protection.

Impairment of our long-term assets may adversely impact our financial position and results of operations.

We evaluate our long-term assets including property, equipment, and identifiable intangible assets in accordance with generally accepted accounting principles in the U.S. We use estimated future cash flows in assessing recoverability of our long-lived assets. The cash flow projections are based on our current estimates and judgmental assessments. We perform this assessment whenever facts and circumstances indicate that the carrying value of the net assets may not be recoverable due to various external or internal factors, termed a “triggering event.” Based on our evaluation for the year ended December 31, 2010, no impairment was recorded.

We may be unable to maintain pricing on our core services.

As a result of pressures stemming from deteriorating market conditions and falling commodity prices, we entered 2009 with rapidly dropping pricing. Although pricing has increased in 2010 and the first two months of 2011, there can be no assurances that we can maintain these increases in the event of an industry decline such as the one experienced in 2009. We have and will likely continue to face pricing pressure from our customers and our competitors. The inability to maintain prices at the current levels would have a material negative impact on our financial position, operating results, and cash flows.

Industry capacity may adversely affect our business.

As a result of the worldwide economic downturn and decline in U.S. onshore exploration and production activities experienced in 2008 and 2009, and in spite of the improving conditions experienced in 2010, demand in the industry is much lower than in the past which also means that neither we nor our competitors are fully utilizing our respective rig fleets and related equipment. Lower utilization of our fleet has led to reduced pricing for our services from historical levels. Capacity that exceeds current demand in the industry has further exacerbated the pricing pressure for our services. In light of such conditions, the excess capacity could cause us to experience continued pressure on the pricing for our services and our utilization. This could have a material negative impact on our financial position, operating results, and cash flows.

13

Table of Contents

Index to Financial Statements

The industry in which we operate is highly competitive.

The oilfield services industry is highly competitive and we compete with a substantial number of companies, some of which have greater technical and financial resources than we have. Our four largest competitors are Basic Energy Services, Inc., Complete Production Services, Inc., Key Energy Services Inc. and Nabors Industries Ltd. Our ability to generate revenues and earnings depends primarily upon our ability to win bids in competitive bidding processes and to perform awarded projects within estimated times and costs. There can be no assurance that competitors will not substantially increase the resources devoted to the development and marketing of products and services that compete with ours, or that new or existing competitors will not enter the various markets in which we are active. In certain aspects of our business, we also compete with a number of small and medium-sized companies that, like us, have certain competitive advantages such as low overhead costs and specialized regional strengths. In addition, reduced levels of activity in the oil and natural gas industry could intensify competition and the pressure on competitive pricing and may result in lower revenues or margins to us.