Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K MARCH 29, 2011 - CHARMING SHOPPES INC | form8kmar292911.htm |

| EX-99.1 - PRESS RELEASE DATED MARCH 29, 2011 - CHARMING SHOPPES INC | exh991mar292011.htm |

3rd Annual

CONSUMER CONFERENCE

CONSUMER CONFERENCE

March 30, 2011

> 2

Anthony M. Romano

President and

President and

Anthony M. Romano

President and

President and

Chief Executive Officer

Chief Executive Officer

Eric M. Specter

Executive Vice President and

Executive Vice President and

Eric M. Specter

Executive Vice President and

Executive Vice President and

Chief Financial Officer

Chief Financial Officer

> 3

Forward Looking Statements

The Company’s presentation may contain certain forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995 concerning the Company's operations, performance, and financial condition. Such forward-

looking statements are subject to various risks and uncertainties that could cause actual results to differ materially from

those indicated. Such risks and uncertainties may include, but are not limited to: the failure to successfully execute our in-

stock inventory strategy could result in higher than planned levels of promotional activity in order to sell through excess

inventory, the failure to successfully execute our business plans could result in lower than planned sales and profitability,

the failure to realize the benefits from the sale of our credit card program to, and the operation of our credit card program

by, our third-party provider, the impact of changes in laws and regulations governing credit cards could limit the availability

of, or increase the cost of, credit to our customers, the failure to enhance the Company's merchandise and marketing and

accurately predict fashion trends, customer preferences and other fashion-related factors, the failure of growth in the

women's plus apparel market, the failure to continue receiving financing at an affordable cost through the availability of

credit we receive from our bankers, suppliers and their agents, the failure to effectively implement our planned store closing

plans, the failure to continue receiving accurate and compliant e-commerce and third-party processing services, the failure

to achieve improvement in the Company's competitive position, the failure to maintain efficient and uninterrupted order-

taking and fulfillment in our e-commerce and direct-to-consumer businesses, extreme or unseasonable weather conditions,

economic downturns, escalation of energy and transportation costs, adverse changes in the costs or availability of fabrics

and raw materials, a weakness in overall consumer demand, the failure to find suitable store locations, increases in wage

rates, the ability to hire and train associates, trade and security restrictions and political or financial instability in countries

where goods are manufactured, the failure of our vendors to deliver quality and timely shipments in compliance with

applicable laws and regulations, the interruption of merchandise flow from the Company's centralized distribution facilities

and third-party distribution providers, inadequate systems capacity, inability to protect trademarks or other intellectual

property, competitive pressures, and the adverse effects of natural disasters, war, acts of terrorism or threats of either, or

other armed conflict, on the United States and international economies. These, and other risks and uncertainties, are

detailed in the Company's filings with the Securities and Exchange Commission, including the Company's Annual Report on

Form 10-K, Quarterly Reports on Form 10-Q and other Company filings with the Securities and Exchange Commission.

Charming Shoppes assumes no duty to update or revise its forward-looking statements even if experience or future

changes make it clear that any projected results expressed or implied therein will not be realized.

Litigation Reform Act of 1995 concerning the Company's operations, performance, and financial condition. Such forward-

looking statements are subject to various risks and uncertainties that could cause actual results to differ materially from

those indicated. Such risks and uncertainties may include, but are not limited to: the failure to successfully execute our in-

stock inventory strategy could result in higher than planned levels of promotional activity in order to sell through excess

inventory, the failure to successfully execute our business plans could result in lower than planned sales and profitability,

the failure to realize the benefits from the sale of our credit card program to, and the operation of our credit card program

by, our third-party provider, the impact of changes in laws and regulations governing credit cards could limit the availability

of, or increase the cost of, credit to our customers, the failure to enhance the Company's merchandise and marketing and

accurately predict fashion trends, customer preferences and other fashion-related factors, the failure of growth in the

women's plus apparel market, the failure to continue receiving financing at an affordable cost through the availability of

credit we receive from our bankers, suppliers and their agents, the failure to effectively implement our planned store closing

plans, the failure to continue receiving accurate and compliant e-commerce and third-party processing services, the failure

to achieve improvement in the Company's competitive position, the failure to maintain efficient and uninterrupted order-

taking and fulfillment in our e-commerce and direct-to-consumer businesses, extreme or unseasonable weather conditions,

economic downturns, escalation of energy and transportation costs, adverse changes in the costs or availability of fabrics

and raw materials, a weakness in overall consumer demand, the failure to find suitable store locations, increases in wage

rates, the ability to hire and train associates, trade and security restrictions and political or financial instability in countries

where goods are manufactured, the failure of our vendors to deliver quality and timely shipments in compliance with

applicable laws and regulations, the interruption of merchandise flow from the Company's centralized distribution facilities

and third-party distribution providers, inadequate systems capacity, inability to protect trademarks or other intellectual

property, competitive pressures, and the adverse effects of natural disasters, war, acts of terrorism or threats of either, or

other armed conflict, on the United States and international economies. These, and other risks and uncertainties, are

detailed in the Company's filings with the Securities and Exchange Commission, including the Company's Annual Report on

Form 10-K, Quarterly Reports on Form 10-Q and other Company filings with the Securities and Exchange Commission.

Charming Shoppes assumes no duty to update or revise its forward-looking statements even if experience or future

changes make it clear that any projected results expressed or implied therein will not be realized.

> 4

PRESENTATION

> 5

We Have A Strong And Unique Platform Of

Leading Plus Apparel Brands

Leading Plus Apparel Brands

The Plus-Size Authority

> 6

> More than half of American women wear size 14 or larger

> #1 in market share in women’s specialty plus-size

apparel*

apparel*

> #2 in market share in women’s plus-size apparel, a

$17.6B market, second only to Wal-Mart*

$17.6B market, second only to Wal-Mart*

> Lane Bryant’s Cacique® brand ranks #3 in women's total

intimate plus-size apparel, a $3.2B market*

intimate plus-size apparel, a $3.2B market*

> Charming Shoppes ranks #1 in market share in women's

specialty plus-size denim apparel, a $655M market*

specialty plus-size denim apparel, a $655M market*

*According to The NPD Group, Inc./Consumer Tracking Service 12 months ended January 2011

Our Market And Leadership Positions

> 7

Classic / Traditional

Fashion

Brand Positioning

> 8

www.lanebryant.com

She is 35-55 years old

She is a woman of many

lifestyles - work, casual, active

lifestyles - work, casual, active

Likes to experiment with fashion

She shops frequently and likes

to buy clothes with good quality

at a reasonable price

to buy clothes with good quality

at a reasonable price

She is brand-conscious and

prefers retailers that offer

fashionable choices

prefers retailers that offer

fashionable choices

Lane Bryant - ‘One Brand - One Vision’

> 9

www.cacique.com

Known for solutions, fit,

quality, fashion and style

quality, fashion and style

Represents 31% of sales

from the full-line

Lane Bryant chain

from the full-line

Lane Bryant chain

Offers key intimates

categories and

complementary products

categories and

complementary products

Introducing caciquebody

Cacique

> 10

She is 30-50 years old

She is value-minded

Loves the challenge of

finding a great deal with

coupons and store

promotions that are easy

to understand

finding a great deal with

coupons and store

promotions that are easy

to understand

Likes to shop for

complete outfits

complete outfits

www.fashionbug.com

Fashion Bug

> 11

www.catherines.com

She’s our baby-boomer,

45+ years old

45+ years old

Classic styling with an

emphasis on fit and

comfort

emphasis on fit and

comfort

Offering styling for the

woman wearing extended

sizes

woman wearing extended

sizes

She prefers clothing that is

more appropriate for her

age - she does not want to

dress “younger” than she is

more appropriate for her

age - she does not want to

dress “younger” than she is

Likes to look “put together”

Catherines

>12

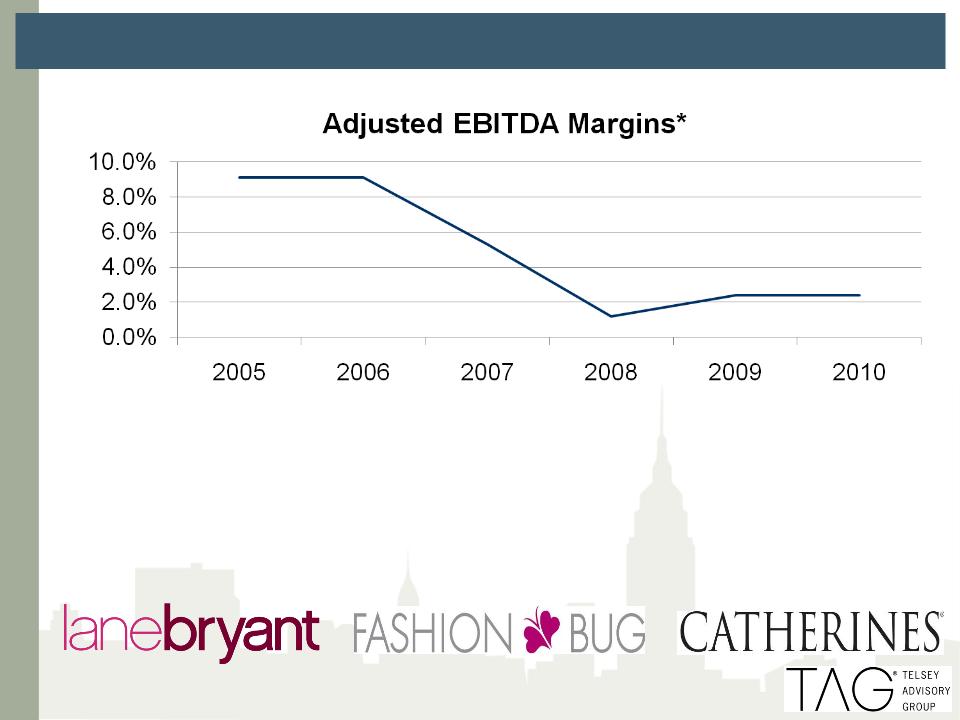

Historical Profitability

> Significant progress made in 4th Quarter 2010

– 7% increase in total sales

¡ +9% comparable store sales; 41% increase in e-commerce

– +$24M improvement in adjusted EBITDA*

*Refer to GAAP to non-GAAP reconciliation at

http://www.charmingshoppes.com/investors/manage/index.asp

http://www.charmingshoppes.com/investors/manage/index.asp

> 13

>Then

– Fit

– In-stock

– Core basics

Then and Now - What is Different

>Now

– Fashion

– Relevance

– Outfitting

– Fit

– In-stock

– Value

>Size is no longer our sole differentiator

> 14

> For each of our brands,

returning to profitability

requires:

returning to profitability

requires:

– Eliminating negative EBITDA

stores

stores

Returning To Profitability

> 15

> For each of our brands,

returning to profitability

requires:

returning to profitability

requires:

– Eliminating negative EBITDA

stores

stores

– Improving our product

assortments

assortments

Returning To Profitability

> 16

> For each of our brands,

returning to profitability

requires:

returning to profitability

requires:

– Eliminating negative EBITDA

stores

stores

– Improving our product

assortments

assortments

– Increasing inventory

productivity

productivity

Returning To Profitability

> 17

> For each of our brands,

returning to profitability

requires:

returning to profitability

requires:

– Eliminating negative EBITDA

stores

stores

– Improving our product

assortments

assortments

– Increasing inventory

productivity

productivity

– Continued growth in digital

sales

sales

Returning To Profitability

> 18

> For each of our brands,

returning to profitability

requires:

returning to profitability

requires:

– Eliminating negative EBITDA

stores

stores

– Improving our product

assortments

assortments

– Increasing inventory

productivity

productivity

– Continued growth in digital

sales

sales

– Distorting resources to our

higher margining Lane Bryant

brand

higher margining Lane Bryant

brand

Returning To Profitability

> 19

> One Brand - One Vision

– Align Lane Bryant and Lane Bryant

Outlet

Outlet

– Consistency of product, design,

sourcing, marketing, and pricing

strategies

sourcing, marketing, and pricing

strategies

> Cacique company-wide

opportunity

opportunity

> Distort resources to Lane Bryant

> Brand image and marketing

activities

activities

> Expanding our Lane Bryant

and Cacique opportunities

and Cacique opportunities

Leveraging Our Lane Bryant and Cacique Opportunities

> 20

FINANCIAL REVIEW

> 21

Financial Review - 4th Quarter 2010

*Refer to GAAP to non-GAAP reconciliation at

http://phx.corporate-ir.net/phoenix.zhtml?c=106124&p=irol-audioarchives

|

($ in millions, except EPS)

|

4th Quarter 2010

|

4th Quarter 2009

|

Change

|

|

Net Sales

|

$575.8

|

$539.0

|

+680 bps

|

|

Same Store Sales

|

+9%

|

-12%

|

|

|

Gross Profit

|

$247.6

|

$235.4

|

+$12.0

|

|

Gross Margin

|

43.0%

|

43.7%

|

-70 bps

|

|

Total Operating

Expenses |

$255.1

|

$267.0

|

-$11.9

|

|

Expense to Sales

|

44.3%

|

49.5%

|

-520 bps

|

|

Adjusted EBITDA

|

$10.7

|

$(12.9)

|

+$23.6

|

|

EBITDA to Sales

|

1.9%

|

(2.4)%

|

+430 bps

|

|

Non-GAAP loss

per diluted share |

$(0.08)

|

$(0.36)

|

+$0.28

|

> 22

Financial Review - Fiscal Year 2010

*Refer to GAAP to non-GAAP reconciliation at

http://phx.corporate-ir.net/phoenix.zhtml?c=106124&p=irol-audioarchives

|

($ in millions, except EPS)

|

2010

|

2009

|

Change

|

|

Net Sales

|

$2,061.8

|

$2,064.6

|

-10 bps

|

|

Same Store Sales

|

+3%

|

-13%

|

|

|

Gross Profit

|

$1,015.0

|

$1,023.6

|

-$8.6

|

|

Gross Margin

|

49.2%

|

49.6%

|

-40 bps

|

|

Total Operating

Expenses |

$1,033.2

|

$1,049.5

|

-$16.3

|

|

Expense to Sales

|

50.1%

|

50.8%

|

-70 bps

|

|

Adjusted EBITDA

|

$50.2

|

$50.5

|

-$0.3

|

|

EBITDA to Sales

|

2.4%

|

2.4%

|

- - -

|

|

Non-GAAP loss

per diluted share |

$(0.26)

|

$(0.52)

|

+$0.26

|

> 23

>Cash of $117 million

>$154 million available on our fully committed and

undrawn revolving line of credit

undrawn revolving line of credit

– Liquidity of $271 million

>Convertible debt

– $140 million of 1.125% convertible notes due 2014

– No financial covenants

– Repurchased $49.2 million (face value) for $38.3 million

during 2010

during 2010

Balance Sheet and Liquidity at January 29, 2011

> 24

> 2,064 stores at year end

> Capital for store growth being distorted to Lane Bryant

– 5-7 new, and 10-13 relocations for Lane Bryant and Lane

Bryant Outlet locations

Bryant Outlet locations

– Continue to migrate from unprofitable malls to lifestyle

strip centers

strip centers

> Eliminating negative EBITDA stores

– Generated $6 million in negative EBITDA in 2010

– 240 stores closing in 2011

– 30 Catherines outlet locations closing over next two years

Stores

> 25

SUMMARY

> 26

>Intensifying brand focus on each primary target

customer

customer

>Improve profitability at both the corporate and

brand level

brand level

>Increase inventory productivity

>Build a winning corporate culture by attracting

and retaining key talent

and retaining key talent

Summary

> 27

>In support of a cleaner environment, we have not

brought investor materials for distribution

brought investor materials for distribution

>Should you wish to have materials sent to you,

please request materials by visiting our website at

https://www.charmingshoppes.com/investors/cont

act/contactus.asp or by emailing us at

IR@charming.com

please request materials by visiting our website at

https://www.charmingshoppes.com/investors/cont

act/contactus.asp or by emailing us at

IR@charming.com

Investor Materials

> 28

Q & A

3rd Annual

CONSUMER CONFERENCE

CONSUMER CONFERENCE

March 30, 2011