Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CHOICE HOTELS INTERNATIONAL INC /DE | d8k.htm |

Investor Presentation

March 2011

Exhibit 99.1 |

2

DISCLAIMER

Certain

matters

discussed

throughout

all

of

this

presentation

constitute

forward-looking

statements

within

the

meaning

of

the

federal

securities

laws.

Generally,

our

use

of

words

such

as

“expect,”

“estimate,”

“believe,”

“anticipate,”

“will,”

“forecast,”

“plan,”

“project,”

“assume”

or

similar

words

of

futurity

identify

statements

that

are

forward-looking

and

that

we

intend

to

be

included

within

the

Safe

Harbor

protections

provided

by

Section

27A

of

the

Securities

Act

and

Section

21E

of

the

Securities

Exchange

Act

of

1934.

Such

forward-looking

statements

are

based

on

management’s

current

beliefs,

assumptions

and

expectations

regarding

future

events,

which

in

turn

are

based

on

information

currently

available

to

management.

Such

statements

may

relate

to

projections

for

the

company’s

revenue,

earnings

and

other

financial

and

operational

measures,

company

debt

levels,

payment

of

stock

dividends,

and

future

operations.

We

caution

you

not

to

place

undue

reliance

on

any

forward-looking

statements,

which

are

made

as

of

the

date

of

this

presentation.

Forward-looking

statements

do

not

guarantee

future

performance

and

involve

known

and

unknown

risks,

uncertainties

and

other

factors.

Several

factors

could

cause

actual

results,

performance

or

achievements

of

the

company

to

differ

materially

from

those

expressed

in

or

contemplated

by

the

forward-looking

statements.

Such

risks

include,

but

are

not

limited

to,

changes

to

general,

domestic

and

foreign

economic

conditions;

operating

risks

common

in

the

lodging

and

franchising

industries;

changes

to

the

desirability

of

our

brands

as

viewed

by

hotel

operators

and

customers;

changes

to

the

terms

or

termination

of

our

contracts

with

franchisees;

our

ability

to

keep

pace

with

improvements

in

technology

utilized

for

reservations

systems

and

other

operating

systems;

fluctuations

in

the

supply

and

demand

for

hotel

rooms;

and

our

ability

to

manage

effectively

our

indebtedness.

These

and

other

risk

factors

are

discussed

in

detail

in

the

Risk

Factors

section

of

the

company’s

Form

10-K

for

the

year

ended

December

31,

2010,

filed

with

the

Securities

and

Exchange

Commission

on

March

1,

2011.

We

undertake

no

obligation

to

publicly

update

or

revise

any

forward-

looking

statement,

whether

as

a

result

of

new

information,

future

events

or

otherwise. |

3

CHOICE HOTELS OVERVIEW

Leading gainer of US hotel market share*

–

9.5% share of branded US hotels (+120

basis points over trailing 5 years)*

–

2

nd

largest U.S. hotelier

70+ year-old hotel distribution company

with well-known, diversified brands

suitable for various stages of hotel life

cycle

Core competencies and services drive

demand for our brands and deliver

business for our franchisees

Global pipeline of 621 hotels under

construction, awaiting conversion or

approved for development

Source: Choice Internal Data, December 31, 2010

* Based on number of hotels as of December 31, 2010 (Smith Travel Research)

Fee-for-service business model

Predictable, profitable, long-term growth

in a variety of lodging and economic

environments

Cumulative free cash flows of more than

$1 billion since 1997

–

>90% returned to shareholders through

share repurchases and dividends

Capital “light”

model generates strong

after-tax returns on invested capital

Long-term franchise contracts and scale

represent barriers to entry

Strong, Growing, Global Hotel

Franchising Business

Highly Attractive Business Model

With Strong Financial Returns |

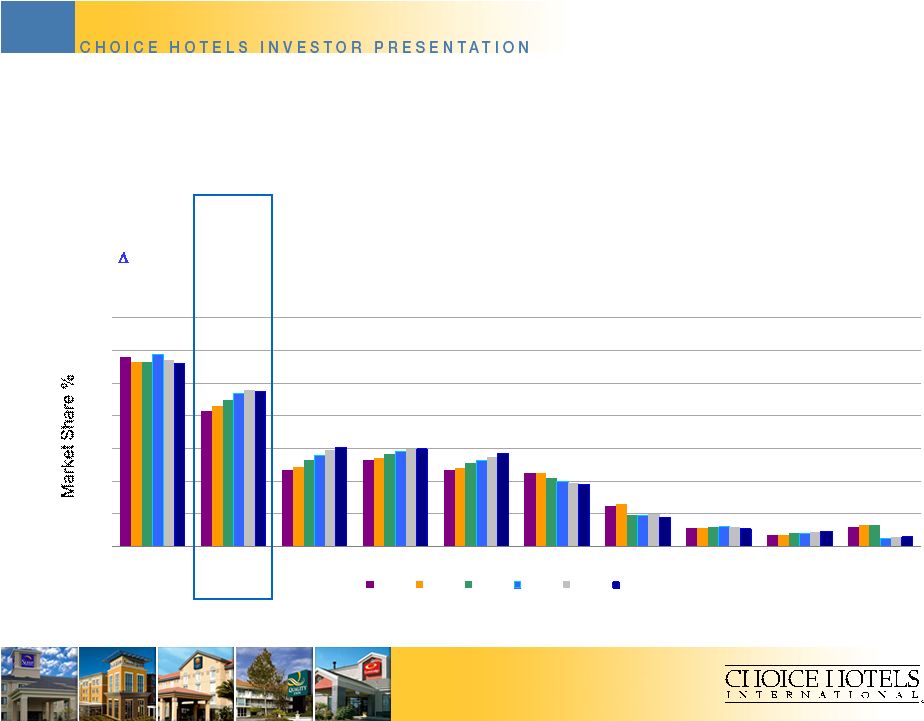

4

Source: Smith Travel Research, December 31, 2010

0

2

4

6

8

10

12

14

Wyndham

Choice

Hilton

IHG

Marriott

Best Western

Accor

Carlson

Starwood

Hyatt

2005

2006

2007

2008

2009

2010

ONE OF THE LARGEST HOTELIERS

Market

Share %

11.2%

9.5%

6.1%

6.0%

5.7%

3.8%

1.8%

1.1%

0.9%

0.6%

5 yr. bps

(05-10)

-20

+120

+140

+70

+100

-70

-60

+10

+20

-60

Market Share (% of Hotels Open in U.S.) |

5

Conversion

$45,000+

$105,000+

$50

$70

$100+

Targeted

Average Daily Rate

$85

FAMILY OF WELL-KNOWN

AND DIVERSIFIED BRANDS

New Construction

* Excludes cost of land; based on average domestic per-room investment.

Source: Choice Internal Data, April 2010

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

® |

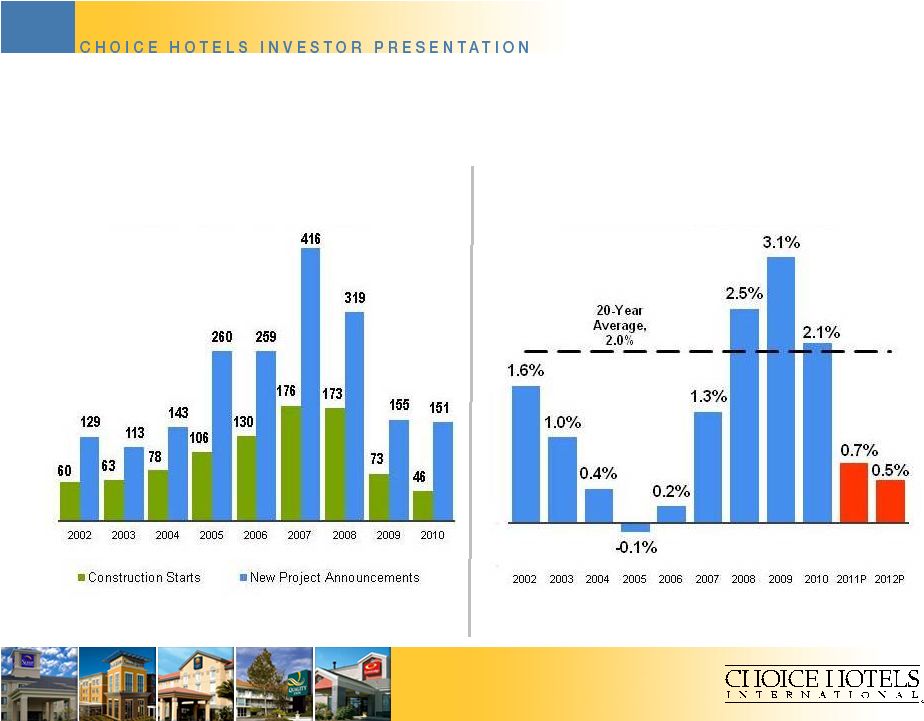

6

CHALLENGING NEAR-TERM ENVIRONMENT FOR

NEW CONSTRUCTION HOTEL DEVELOPMENT

0%

Source:

Lodging

Econometrics

(Q4

2010)

–

New

Construction

Pipeline

Source: 2011-2012 supply growth projections are based on January 2011 STR

forecast U.S. Lodging Industry Change

in Room Supply (YOY %)

New Construction

Pipeline Rooms (000's) |

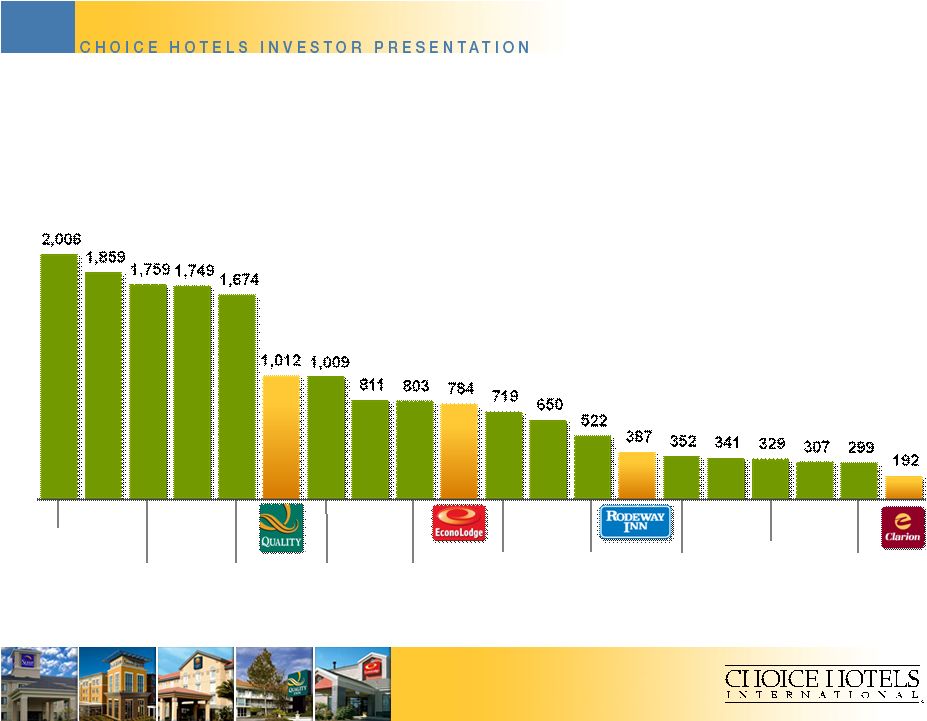

7

STRONG LIMITED SERVICE NEW

CONSTRUCTION BRANDS POSITIONED

WELL FOR LONG-TERM GROWTH

Source: Smith Travel Research, Choice Internal Data, December 31, 2010

|

8

SIGNIFICANT GROWTH OPPORTUNITIES

REMAIN IN LARGE CONVERSION MARKET

Chart does not include

17,000+ independent hotels

in budget, economy and

mid-scale

segments

Domestic Hotels

Hampton Inn /

Hampton Inn

& Suites

Holiday Inn

Express

Days Inn

Motel 6

America’s

Best

Value Inn

Holiday

Inn /

Holiday

Inn Select

La Quinta

Inn / La Quinta

Inn & Suites

Fairfield

Inn

Ramada /

Ramada

Limited

Travelodge

Red Roof

Inn

Howard

Johnson

Knight’s

Inn

Microtel

Best

Western

Super 8

Source: Smith Travel Research, Choice Internal Data, December 31, 2010

®

®

®

®

®

®

® |

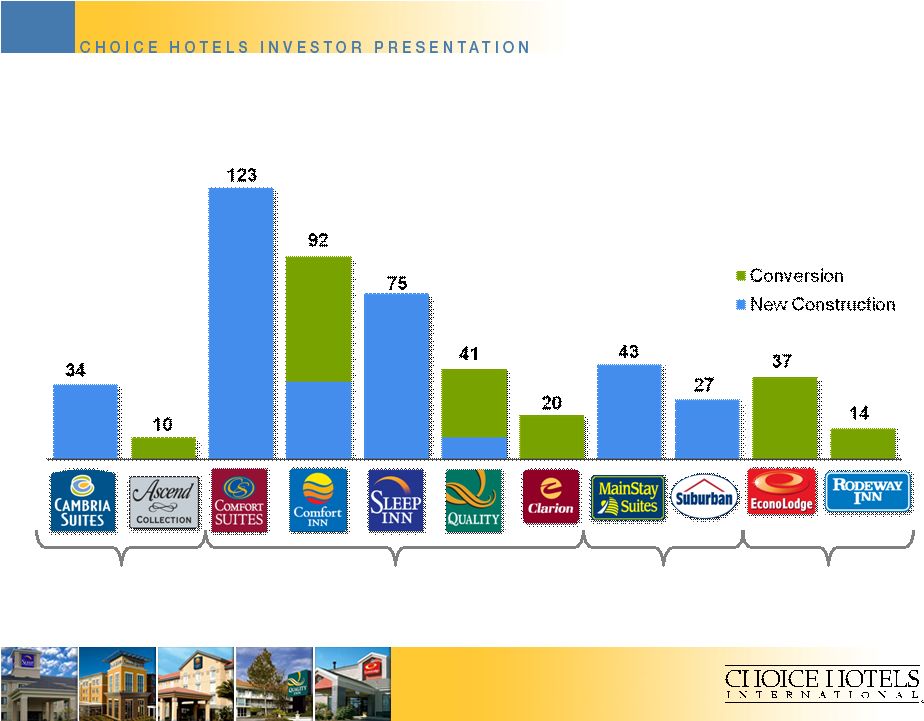

9

DOMESTIC PIPELINE OF 516 HOTELS

Mid-scale

Extended Stay

Economy

Upscale

Source: Choice Internal Data, December 31, 2010

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

®

® |

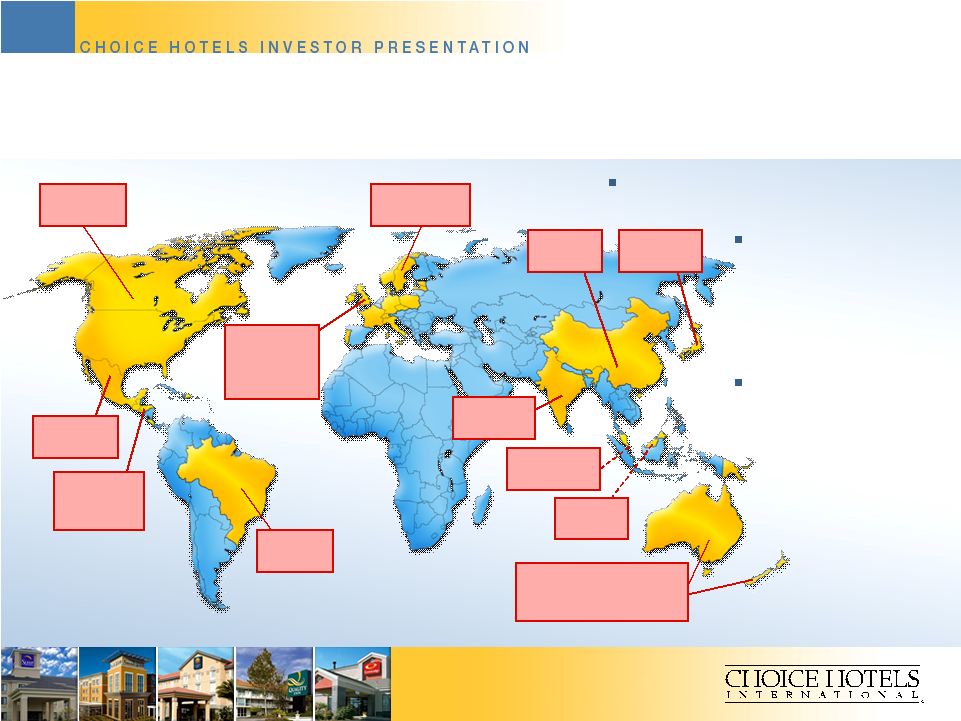

10

1,149 properties in 30 countries

and territories on five continents

Multi-year

investments in

IT and marketing

planned to enhance

value proposition for

international hotels

Significant long-term

growth opportunity

in underrepresented

regions/countries

STRONG PRESENCE IN MAJOR

TRAVEL MARKETS OUTSIDE OF THE U.S.

Source: Choice Internal Data, December 31, 2010

19 hotels

Mexico

294 hotels

Canada

247 hotels

Continental

Europe, UK

& Ireland

161 hotels

Scandinavia

57 hotels

Brazil

52 hotels

Japan

3 hotels

China

1 hotel

Malaysia

26 hotels

India

12 hotels

Central

America

1 hotel

Singapore

276 hotels

Australia, New Zealand

& Papua New Guinea |

11

SERVICES LIFECYCLE IMPROVES

BRANDS AND PROPERTY PERFORMANCE

FRANCHISED

FRANCHISED

PROPERTIES

PROPERTIES

RETURN ON

RETURN ON

INVESTMENT

INVESTMENT

Brand Planning

and Management

•

Targeted, differentiated

programs, amenities and

services for each brand

Brand Performance

•

Revenue and guest service

consulting

•

Inventory and rate management

•

Local sales and marketing

•

Independent third-party quality

assurance

Training

•

On-site

•

Regional

•

Web-based

•

GM Certification

Opening Services

•

Ensure hotels open

successfully and meet or

exceed brand standards

Portfolio

Management

•

Repositioning

•

Relicensing

•

Termination

Procurement Services

•

Value-engineered prototypes

and design packages

•

Negotiated vendor

relationships |

12

MARKETING AND CENTRAL

RESERVATION SYSTEM LEVERAGES

SIZE, SCALE AND DISTRIBUTION

$300-plus million in annual marketing and reservation system fees

Leverage expertise and innovation in on-line, targeted interactive

marketing to influence guest hotel stay decisions

Powerful advertising campaigns

Focus on driving guests to Choice central channels

Facilitate “one-stop”

shopping

Strong and growing global loyalty program

Increasing brand awareness

Source: Choice Internal Data, December 2010 |

13

STRONG AND GROWING

AIDED BRAND AWARENESS

Source: Percentage of survey respondents. Millward Brown, December 2010.

*Econo Lodge, Rodeway Inn and Suburban Extended Stay measured among economy

hotel users. |

14

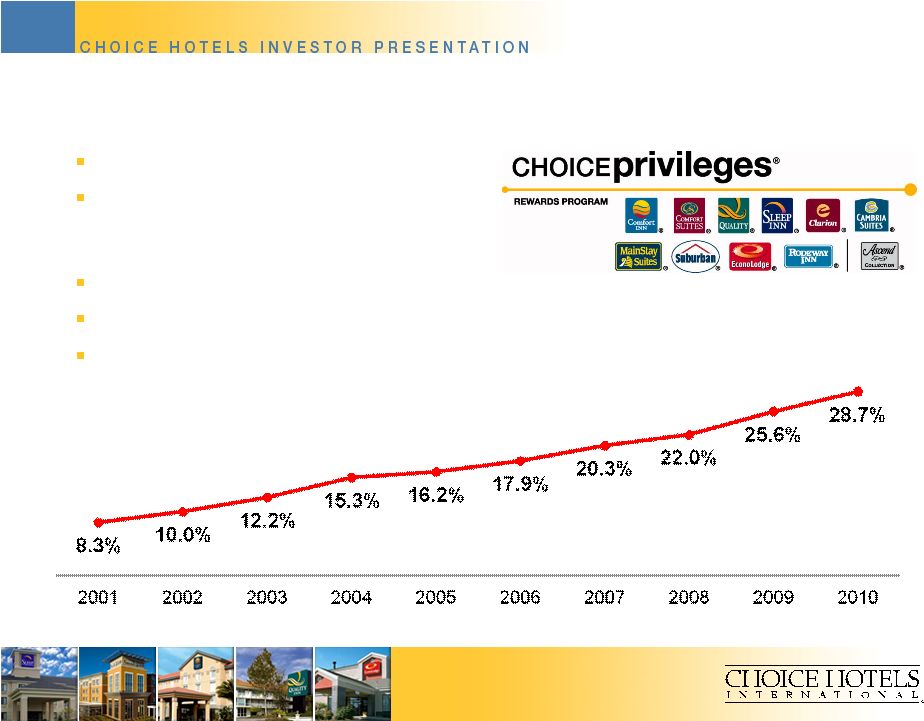

STRONG, GROWING LOYALTY PROGRAM

Choice Privileges Revenue as Percent

of Domestic Gross Room Revenues*

Source: Choice Internal Data, December 31, 2010

* 2001-2008 Data Excludes Econo Lodge and Rodeway Inn brands

Comprehensive loyalty rewards program

12 million members worldwide –

contribute over ¼

of domestic

gross room revenues

2.5 million new members added in 2010

Delivers incremental business to all Choice brand hotels

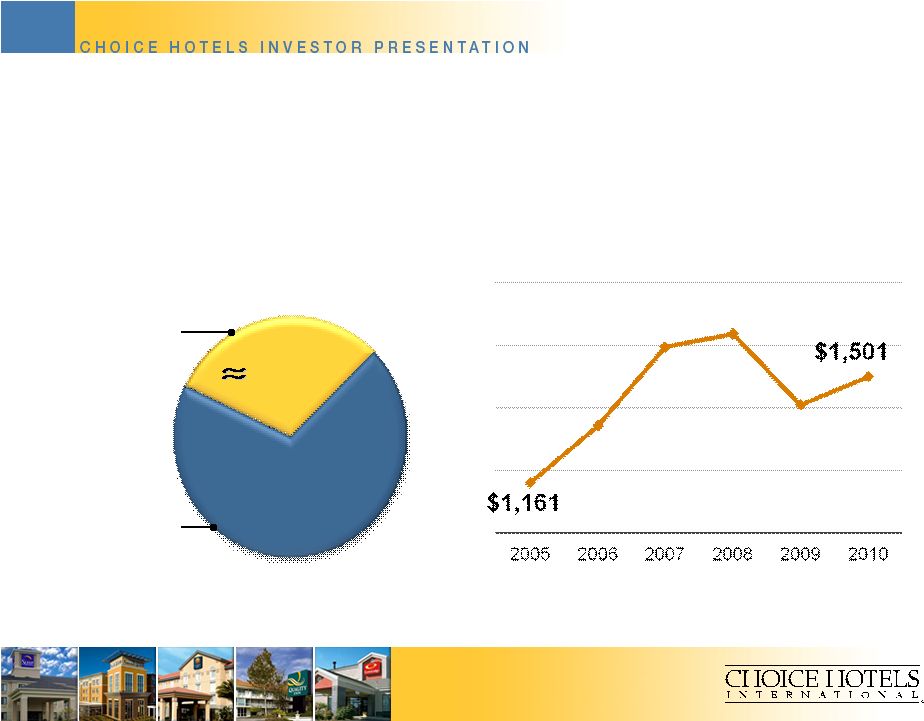

Important selling point for franchise sales |

15

CENTRAL RESERVATIONS SYSTEM (CRS)

DELIVERY PUTS “HEADS IN BEDS”

All Hotel

Direct

Reservation

Choice Central

Reservation

Contribution

1/3

1/3

Domestic Franchise System

Gross Room Revenue Source

Domestic Choice CRS

Net Room Revenue

Source: Choice Internal Data, December, 2010 |

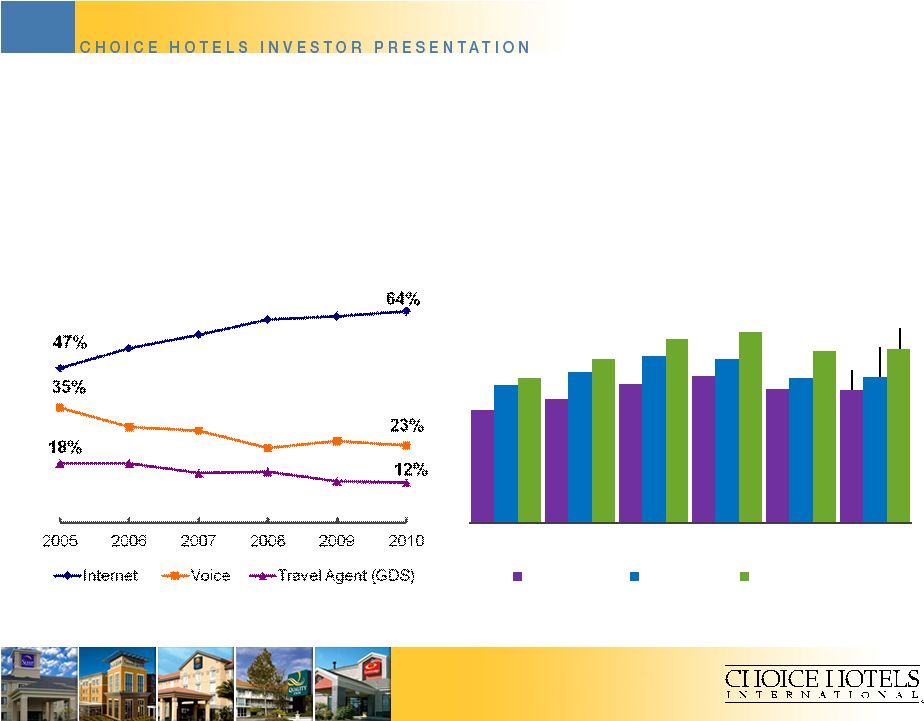

16

Central Channel ADR

“Premium”

Domestic Choice CRS

Net Channel Share

CENTRAL RESERVATIONS BOOKINGS

CREATE SIGNIFICANT VALUE

FOR FRANCHISEES

Source: Choice Internal Data, December, 2010

$66.11

$70.43

$71.59

$73.54

$73.35

$80.04

2005

2006

2007

2008

2009

2010

Systemwide

Call Center

choicehotels.com |

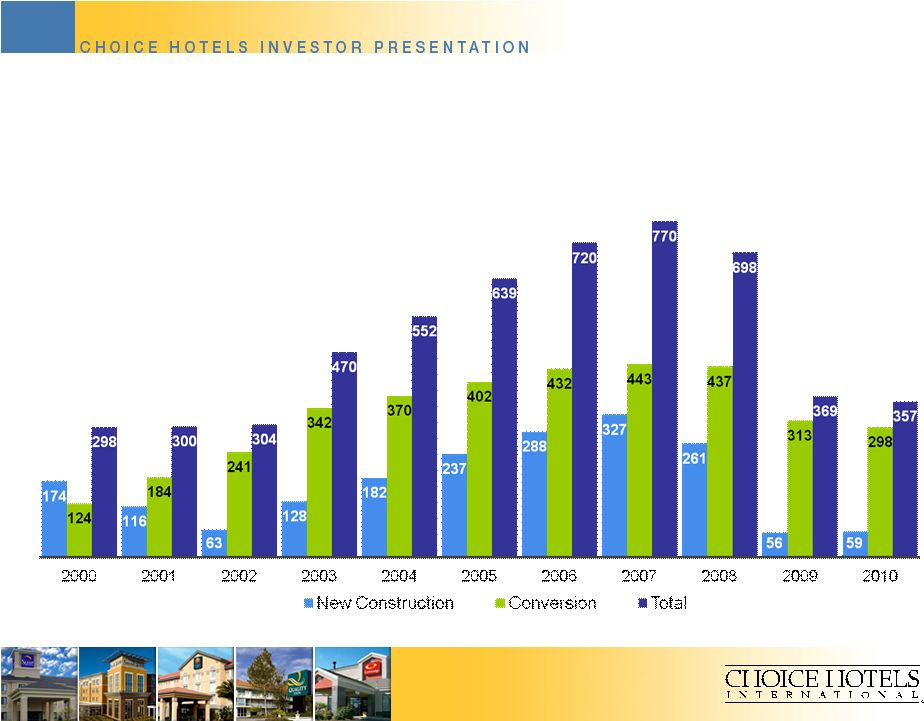

17

CONVERSION BRAND FRANCHISE

SALES OPPORTUNITY IN SOFT NEW

CONSTRUCTION ENVIRONMENT

Source: Choice Internal Data, December, 2010 |

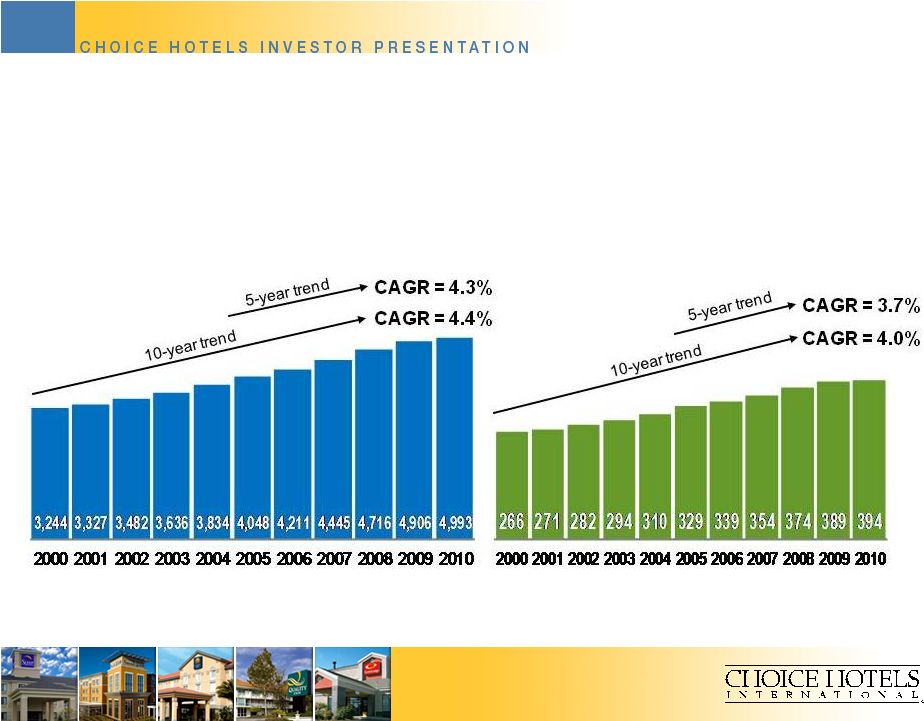

18

STRONG, STEADY FRANCHISE

SYSTEM GROWTH

Domestic Hotels On-Line

Domestic Rooms On-Line

(in thousands)

Source: Choice Internal Data, December, 2010 |

19

FRANCHISING REVENUE STREAM

LESS VOLATILE THAN REVPAR

$0

$50

$100

$150

$200

$250

$300

$350

-17%

-12%

-7%

-2%

3%

8%

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

CHH RevPAR

STR Chain Scale (Supply Weighted)

Industry RevPAR

Franchising Revenue

($ in millions)

Source: Smith Travel Research, Choice Internal Data, December 2010

|

20

ADJUSTED EBITDA LESS VOLATILE

THAN INDUSTRY PROFITABILITY

0

50

100

150

200

250

0

5

10

15

20

25

30

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Industry Profits

Adjusted EBITDA

Source: Smith Travel Research, Choice Internal Data, December 2010

($ in millions)

($ in billions) |

21

CAPITAL “LIGHT”

MODEL GENERATES

STRONG RETURNS ON INVESTED CAPITAL

15.2%

16.1%

14.7%

19.5%

27.6%

36.7%

49.7%

62.9%

78.5%

68.8%

59.5%

48.1%

48.0%

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

After-Tax Return On Invested Capital

Source: Choice Internal Data, December 2010 |

22

TRACK RECORD OF STRONG EARNINGS

PER SHARE PERFORMANCE

$0.40

$0.51

$0.51

$0.58

$0.76

$0.93

$1.07

$1.25

$1.48

$1.73

$1.73

$1.68

$1.81

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Adjusted Diluted Earnings Per Share

Note: See appendix for reconciliation of adjusted diluted earnings per share to

diluted earnings per share. To improve comparability certain employee severance

amounts included in the determination of adjusted diluted earnings per share in

this presentation for 2007 through 2010 differ from amounts reported in

Exhibits 8 of our various earnings announcements.

Source: Choice Internal Data, December 2010. Per Share Amounts Retroactively

Adjusted For 2005 Stock Split. |

23

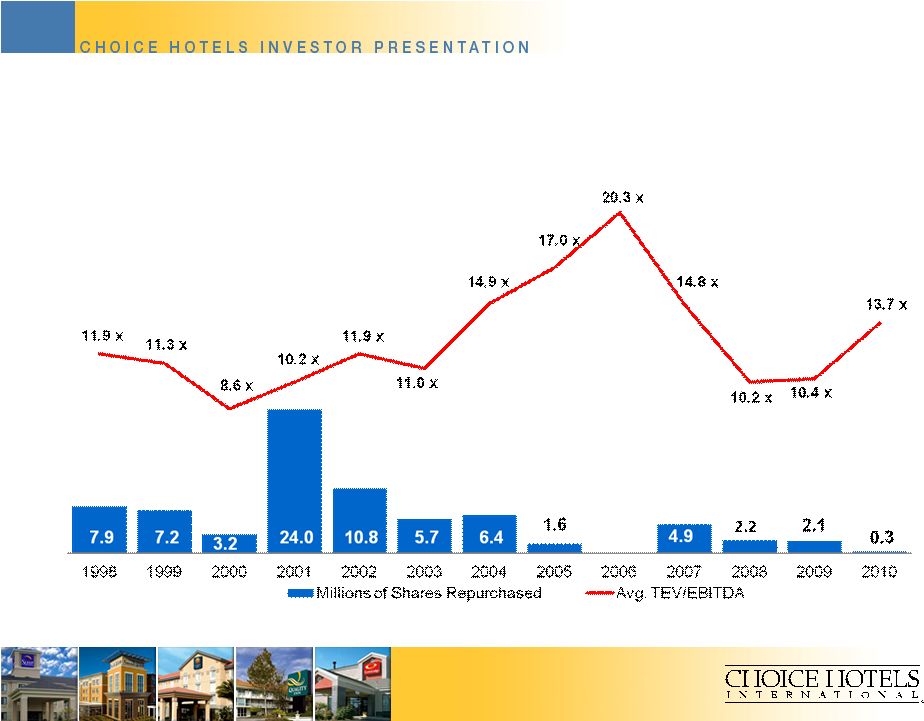

Remaining authority on current authorization –

3.6 million shares as of December 31, 2010

OPPORTUNISTIC SHARE REPURCHASES KEY

PART OF CAPITAL ALLOCATION STRATEGY

Source: Capital IQ, December 2010, Choice Internal Data, December 30, 2010.

Share amounts for 2005 and prior years retroactively adjusted for 2005

two-for-one stock split. |

24

1.9%

0.0%

0.0%

0.0%

3.3%

0.9%

0.0%

0.0%

0.5%

1.9%

HIGH CASH DIVIDEND YIELD COMPARED

TO OTHER LODGING C-CORPS

Choice

Great

Wolf

Wyndham

Gaylord

Hyatt

Orient-

Express

Starwood

Red Lion

Marriott

IHG

Source: Bloomberg Financial, March 10, 2011 |

25

STRONG CREDIT POSITION

Investment grade credit rating

–

Moody’s Baa3

–

Standard & Poor’s BBB

Strong liquidity position

Substantial financial flexibility

Minimal contingent liability exposure

Source: Choice Internal Data, December 2010 |

26

STRATEGY FOR CHOICE’S BRANDS,

GROWTH AND SHAREHOLDERS

Improve and Grow Brands

–

Increase portfolio profitability of the Comfort brand family

–

Refresh Sleep Inn to improve long-term brand growth potential

–

Invest

in

and

expand

emerging

brands/segments

–

Cambria,

Ascend,

International

Capture Greater Share of Reservations Via Central Channels

–

Grow

Choice

Privileges

loyalty

program

–

target

2.0

million

new

members

in

2011

–

Continue to enhance ChoiceHotels.com to increase traffic and conversion

Allocate Free Cash Flows To “Best And Highest”

Use

–

Continue shareholder-friendly capital allocation policies

–

Leverage financial capacity/strength to support expansion of emerging brands

–

Evaluate opportunities to enter new segments

–

Invest in IT infrastructure to shore up value proposition for international

properties |

27

Appendix

Reconciliation of Non-GAAP

Financial Measurements to GAAP |

28

DISCLAIMER

Adjusted franchising margins, adjusted earnings before interest,

taxes

depreciation and amortization (EBITDA), adjusted net income, adjusted diluted

earnings per share (EPS), franchising revenues, net operating profit after

tax (NOPAT),

return

on

average

invested

capital

(ROIC)

and

free

cash

flows

are

non-

GAAP financial measurements. These financial measurements are presented as

supplemental disclosures because they are used by management in reviewing

and analyzing the company’s performance. This information should not be

considered as an alternative to any measure of performance as promulgated

under accounting principles generally accepted in the United States (GAAP), such

as operating income, net income, diluted earnings per share, total revenues

or net cash

provided

by

operating

activities.

The

calculation

of

these

non-GAAP

measures may be different from the calculation by other companies and therefore

comparability may be limited. The company has included the following

appendix which reconcile these measures to the comparable GAAP

measurement. |

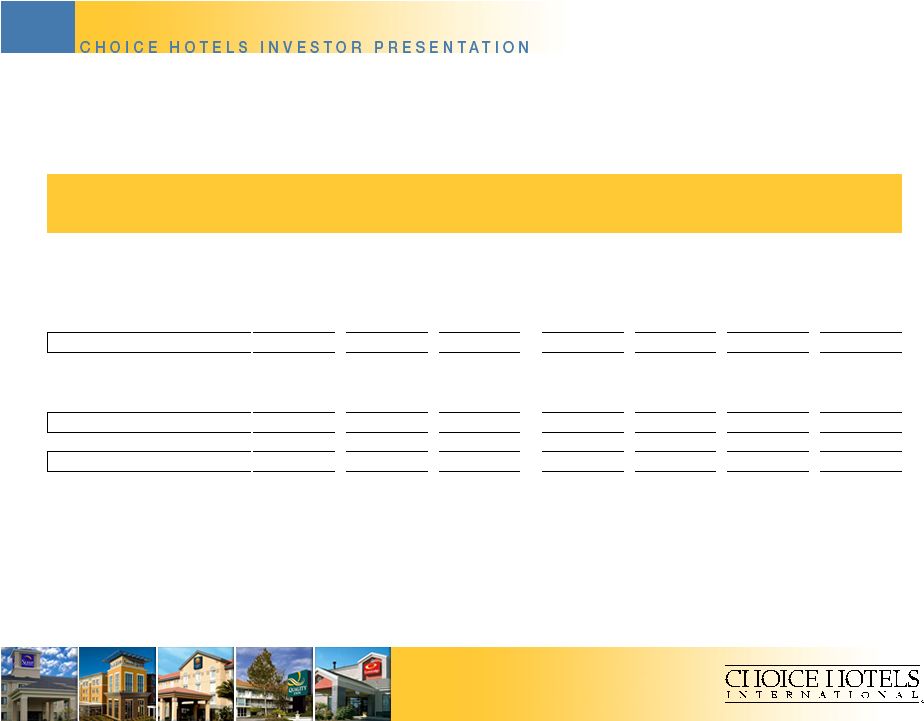

29

FRANCHISING REVENUES AND ADJUSTED

FRANCHISING MARGINS

Note: To improve comparability certain employee severance amounts included in the

determination of adjusted franchising margins in this presentation for 2007

through 2010 differ from amounts reported in exhibit 8 of our year-end earnings

announcements for those years. Source: Choice Internal Data, December

2010 ($ amounts in thousands)

Year Ended

December 31,

Year Ended

December 31,

Year Ended

December 31,

Year Ended

December 31,

Year Ended

December 31,

Year Ended

December 31,

Year Ended

December 31,

2010

2009

2008

2007

2006

2005

2004

Total Revenues

$ 596,076

$ 564,178

$ 641,680

$ 615,494

$ 539,903

$ 472,098

$ 428,208

Adjustments:

Marketing and Reservation

(329,246)

(305,379)

(336,477)

(316,827)

(273,267)

(237,822)

(220,732)

Product Sales

-

-

-

-

-

-

-

Hotel Operations

(4,031)

(4,140)

(4,936)

(4,692)

(4,505)

(4,293)

(3,729)

Franchising Revenues

$ 262,799

$ 254,659

$ 300,267

$ 293,975

$ 262,131

$ 229,983

$ 203,747

Operating Income

$ 160,762

$ 148,073

$ 174,596

$ 185,199

$ 166,625

$ 143,750

$ 124,983

Adjustments

Hotel Operations

(845)

(987)

(1,502)

(1,451)

(1,311)

(1,068)

(725)

Acceleration of Management Succession Plan

-

-

6,605

-

-

-

-

Executive Termination Benefits

1,217

3,321

-

3,690

-

-

-

Curtailment of SERP

-

1,209

-

-

-

-

-

Loss on Sublease of Office Space

-

1,503

-

-

-

-

-

Loan Reserves Related to Impaired Notes

Receivable

-

-

7,555

-

-

-

-

Product Sales

-

-

-

-

-

-

-

Impairment of Friendly Investment

-

-

-

-

-

-

-

Net

$ 161,134

$ 153,119

$ 187,254

$ 187,438

$ 165,314

$ 142,682

$ 124,258

Adjusted Franchising Margin

61.3%

60.1%

62.4%

63.8%

63.1%

62.0%

61.0% |

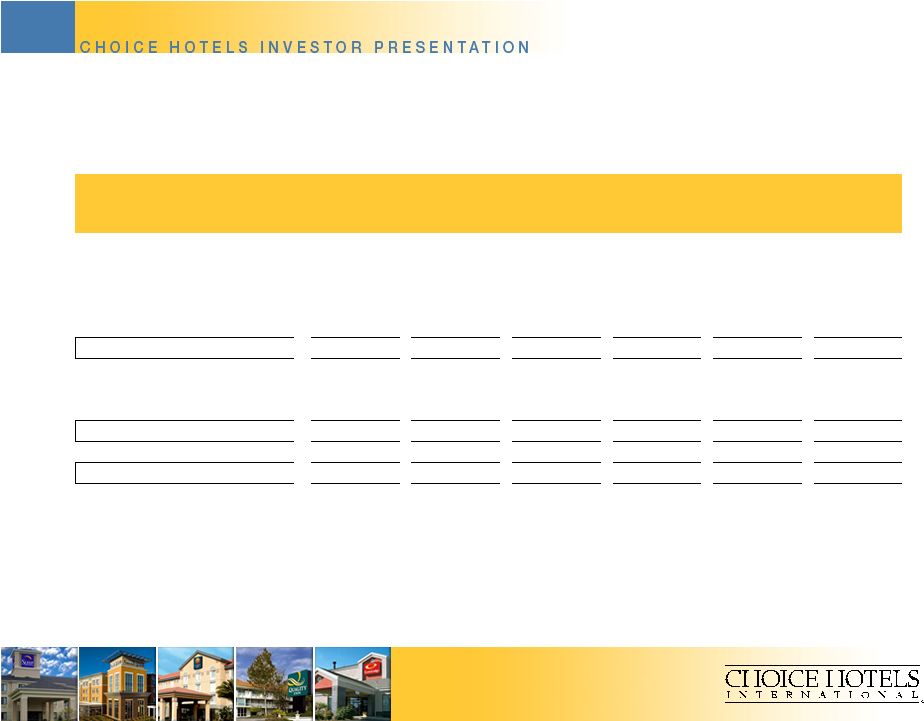

30

FRANCHISING REVENUES AND ADJUSTED

FRANCHISING MARGINS (Continued)

($ amounts in thousands)

Year Ended

Year Ended

Year Ended

Year Ended

Year Ended

Year Ended

December 31,

2003

December 31,

2002

December 31,

2001

December 31,

2000

December 31,

1999

December 31,

1998

Total Revenues

$ 385,866

$ 365,562

$ 341,428

$ 352,841

$ 324,203

$ 165,474

Adjustments:

Marketing and Reservation

(195,219)

(190,145)

(168,170)

(185,367)

(162,603)

-

Product Sales

-

-

-

-

(3,871)

(20,748)

Hotel Operations

(3,565)

(3,331)

(3,215)

(1,249)

-

(1,098)

Franchising Revenues

$ 187,082

$ 172,086

$ 170,043

$ 166,225

$ 157,729

$ 143,628

Operating Income

$ 113,946

$ 104,700

$ 73,577

$ 92,427

$

94,170

$ 85,151

Adjustments

Hotel Operations

(842)

(385)

(714)

(640)

-

35

Acceleration of Management Succession Plan

-

-

-

-

-

-

Executive Termination Benefits

-

-

-

-

-

-

Curtailment of SERP

-

-

-

-

-

-

Loss on Sublease of Office Space

-

-

-

-

-

-

Loan Reserves Related to Impaired Notes Receivable

-

-

-

-

-

-

Product Sales

-

-

-

-

12

(1,216)

Impairment of Friendly Investment

-

-

22,713

-

-

-

Net

$ 113,104

$ 104,315

$ 95,576

$ 91,787

$ 94,182

$ 83,970

Adjusted Franchising Margin

60.5%

60.6%

56.2%

55.2%

59.7%

58.5%

Source: Choice Internal Data, December 2010 |

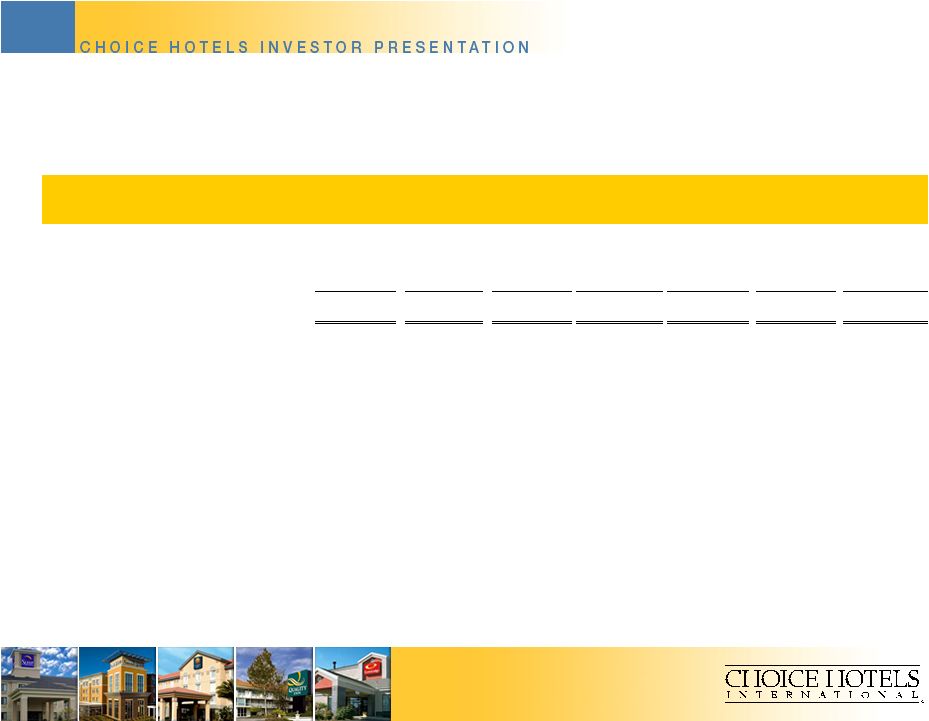

31

RETURN ON INVESTED CAPITAL

($ in millions)

Year Ended

December 31,

2010

Year Ended

December 31,

2009

Year Ended

December 31,

2008

Year Ended

December 31,

2007

Year Ended

December 31,

2006

Year Ended

December 31,

2005

Year Ended

December 31,

2004

Operating Income (a)

$160.8

$148.1

$174.6

$185.2

$166.6

$143.8

$125.0

Tax Rate(a)

32.1%

34.8%

36.3%

36.0%

27.4%

33.0%

35.1%

After-Tax Operating Income

109.2

96.6

111.2

118.5

121.0

96.3

81.1

+ Depreciation & Amortization

8.3

8.3

8.2

8.6

9.7

9.1

9.9

-

Maintenance CAPEX

8.3

8.3

8.2

8.6

9.7

9.1

9.9

Net Op. Profit After-tax (NOPAT)

$109.2

$96.6

$111.2

$118.5

$121.0

$96.3

$81.1

Total Assets

411.7

340.0

328.2

328.4

303.3

265.3

263.4

-

Current Liabilities

165.3

131.8

135.1

147.5

139.8

120.3

102.1

Invested Capital

246.4

208.2

193.1

180.9

163.5

145.0

161.3

Return on Average Invested Capital

48.0%

48.1%

59.5%

68.8%

78.5%

62.9%

49.7%

(a) Operating income and tax rate for the year ended December 31, 2001 have been

adjusted to exclude the effect of a $22.7 million impairment charge related

to the write-off of the company’s investment in Friendly Hotels.

Source: Choice Internal Data, December 2010 |

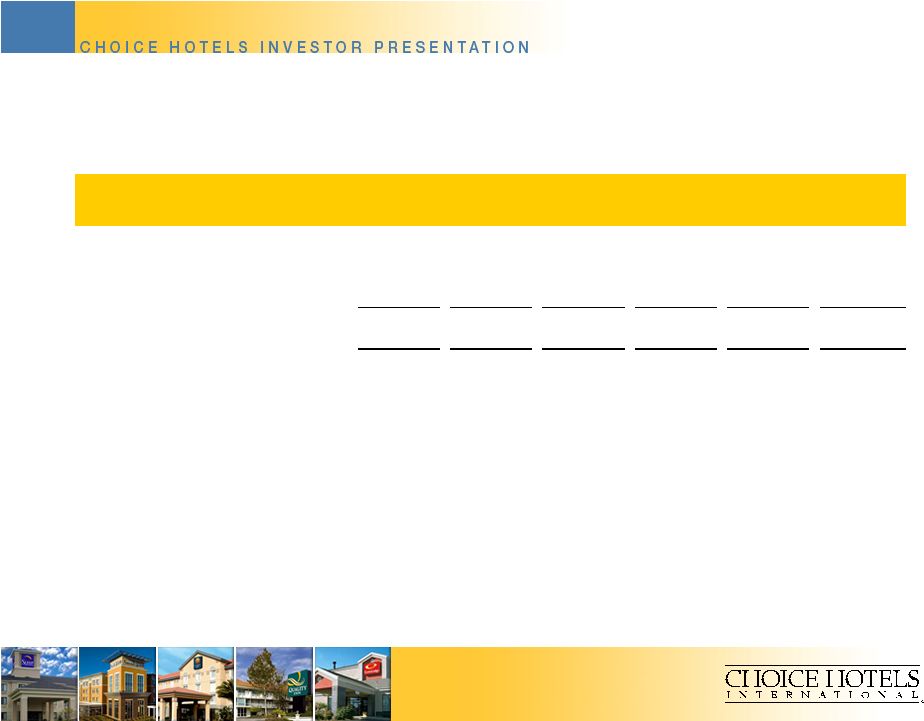

32

RETURN ON INVESTED CAPITAL (Continued)

($ in millions)

Year Ended

December 31,

2003

Year Ended

December 31,

2002

Year Ended

December 31,

2001

Year Ended

December 31,

2000

Year Ended

December 31,

1999

Year Ended

December 31,

1998

Operating Income (a)

$113.9

$104.7

$96.3

$92.4

$94.2

$85.2

Tax Rate(a)

36.1%

36.5%

35.0%

39.0%

39.5%

41.7%

After-Tax Operating Income

72.8

66.5

62.6

56.4

57.0

49.7

+ Depreciation & Amortization

11.2

11.3

12.5

11.6

7.7

6.7

-

Maintenance CAPEX

11.2

11.3

12.5

11.6

7.7

6.7

Net Op. Profit After-tax (NOPAT)

$72.8

$66.5

$62.6

$56.4

$57.0

$49.7

Total Assets

267.3

316.8

321.2

484.1

464.7

398.2

-

Current Liabilities

102.2

84.3

71.2

93.8

88.7

64.7

Invested Capital

165.1

232.5

250.0

390.3

375.9

333.6

Return on Average Invested Capital

36.7%

27.6%

19.5%

14.7%

16.1%

15.2%

(a) Operating income and tax rate for the year ended December 31, 2001 have been

adjusted to exclude the effect of a $22.7 million impairment charge related

to the write-off of the company’s investment in Friendly Hotels.

Source: Choice Internal Data, December 2010 |

33

FREE CASH FLOWS

($ in thousands)

Year Ended

December 31,

2010

Year Ended

December

31, 2009

Year Ended

December 31,

2008

Year Ended

December 31,

2007

Year Ended

December 31,

2006

Year Ended

December 31,

2005

Year Ended

December 31,

2004

Net Cash Provided by Operating Activities

$ 144,935

$ 112,216

$ 104,399

$ 145,666

$ 153,680

$ 133,588

$ 108,908

Net Cash Provided (Used) by Investing Activities

(32,155)

(3,349)

(20,265)

(21,284)

(17,244)

(24,531)

(14,544)

Free Cash Flows

$ 112,780

$ 108,867

$ 84,134

$ 124,382

$ 136,436

$ 109,057

$ 94,364

Source: Choice Internal Data, December 2010 |

34

FREE CASH FLOWS (Continued)

($ in thousands)

Year Ended

December 31,

2003

Year Ended

December 31,

2002

Year Ended

December 31,

2001

Year Ended

December 31,

2000

Year Ended

December 31,

1999

Year Ended

December 31,

1998

Net Cash Provided by Operating Activities

$ 115,304

$ 99,018

$ 101,712

$ 53,879

$ 65,040

$ 38,952

Net Cash Provided (Used) by Investing Activities

27,784

(14,683)

87,738

(16,617)

(36,031)

(9,056)

Free Cash Flows

$ 143,088

$ 84,335

$ 189,450

$ 37,262

$ 29,009

$ 29,896

Source: Choice Internal Data, December 2010 |

35

Note: To improve comparability certain employee severance amounts included in the

determination of adjusted EBITDA in this presentation for 2007 through 2010

differ from amounts reported in exhibits 8 of our various earnings announcements.

Source: Choice Internal Data, December 2010

ADJUSTED EBITDA

($ in thousands)

Year Ended

December 31,

2010

Year Ended

December 31,

2009

Year Ended

December 31,

2008

Year Ended

December 31,

2007

Year Ended

December 31,

2006

Year Ended

December 31,

2005

Year Ended

December 31,

2004

Operating Income

$ 160,762

$ 148,073

$ 174,596

$ 185,199

$ 166,625

$ 143,750

$ 124,983

Adjustments

Acceleration of Management

Succession Plan

-

-

6,605

-

-

-

-

Loss on Sublease of Office Space

-

1,503

-

-

-

-

-

Executive Termination Benefits

1,217

3,321

-

3,690

-

-

-

Curtailment of

SERP

-

1,209

-

-

-

-

-

Loan Reserves Related to Impaired Notes

Receivable

-

-

7,555

-

-

-

-

Product Sales

-

-

-

-

-

-

-

Impairment of Friendly investment

-

-

-

-

-

-

-

Depreciation and Amortization

8,342

8,336

8,184

8,637

9,705

9,051

9,947

Adjusted EBITDA

$ 170,321

$ 162,442

$ 196,940

$ 197,526

$ 176,330

$ 152,801

$ 134,930 |

36

ADJUSTED EBITDA (Continued)

($ in thousands)

Year Ended

December 31,

2003

Year Ended

December 31,

2002

Year Ended

December 31,

2001

Year Ended

December 31,

2000

Year Ended

December 31,

1999

Year Ended

December 31,

1998

Operating Income

$ 113,946

$ 104,700

$ 73,577

$ 92,427

$ 94,170

$ 85,151

Adjustments

Acceleration of Management Succession Plan

-

-

-

-

-

-

Loss on Sublease of Office Space

-

-

-

-

-

-

Executive Termination Benefits

-

-

-

-

-

-

Curtailment of SERP

-

-

-

-

-

-

Loan Reserves Related to Impaired Notes

Receivable

-

-

-

-

-

-

Product Sales

-

-

-

-

12

(1,216)

Impairment of Friendly investment

-

-

22,713

-

-

-

Depreciation and Amortization

11,225

11,251

12,452

11,623

7,687

6,710

Adjusted EBITDA

$ 125,171

$ 115,951

$ 108,742

$ 104,050

$ 101,869

$ 90,645

Source: Choice Internal Data, December 2010 |

37

ADJUSTED DILUTED EARNINGS PER SHARE

Year Ended

Year Ended

Year Ended

Year Ended

Year Ended

Year Ended

December 31,

December 31,

December 31,

December 31,

December 31,

December 31,

(In thousands, except per share amounts)

2010

2009

2008

2007

2006

2005

Net Income

107,441

$

98,250

$

100,211

$

111,301

$

112,787

$

87,565

$

Adjustments:

Loss(Gain) on Extinguishment of Debt, Net of Taxes

-

-

-

-

217

-

Acceleration of Management Sucession Plan, Net of Taxes

-

-

4,135

-

-

-

Executive Termination Benefits, Net of Taxes

762

2,079

-

2,310

-

-

Loss on Sublease of Office Space, Net of Taxes

-

941

-

-

-

-

Curtailment of SERP, Net of Taxes

-

757

-

-

-

-

Loan Reserves Related to Impaired Notes Receivable, Net of Taxes

-

-

4,729

-

-

-

Resolution of Provisions for Income Tax Contingencies

-

-

-

-

(12,791)

(4,855)

Income

Tax Expense Incurred Due to Foreign Earnings Repatriation -

-

-

-

-

1,192

Loss(Gain) on Sunburst Note Transactions, Net of Taxes

-

-

-

-

-

-

Impairment of and Equity Losses in Friendly Hotels PLC Investment, Net of Taxes

-

-

-

-

-

-

Adjusted Net Income

108,203

$

102,027

$

109,075

$

113,611

$

100,213

$

83,902

$

Weighted Average Shares

Outstanding-Diluted 59,656

60,224

62,994

65,766

67,490

66,759

Diluted

Earnings Per Share 1.80

$

1.63

$

1.59

$

1.69

$

1.67

$

1.31

$

Adjustments:

Loss(Gain) on Extinguishment of Debt, Net of Taxes

-

-

-

-

-

-

Acceleration of Management Sucession Plan, Net of Taxes

-

-

0.07

-

-

-

Executive Termination Benefits, Net of Taxes

0.01

0.02

-

0.04

-

-

Loss on Sublease of Office Space, Net of Taxes

-

0.02

-

-

-

-

Curtailment of SERP, Net of Taxes

-

0.01

-

-

-

-

Loan Reserves Related to Impaired Notes Receivable, Net of Taxes

-

-

0.07

-

-

-

Resolution of Provisions for Income Tax Contingencies

-

-

-

-

(0.19)

(0.08)

Income Tax Expense Incurred Due to Foreign Earnings Repatriation

-

-

-

-

-

0.02

Loss(Gain) on Sunburst Note Transactions, Net of Taxes

-

-

-

-

-

-

Impairment of and Equity Losses in Friendly Hotels PLC Investment, Net of Taxes

-

-

-

-

-

-

Adjusted Diluted Earnings Per Share (EPS)

1.81

$

1.68

$

1.73

$

1.73

$

1.48

$

1.25

$

Note: To improve comparability certain employee severance amounts included in the

determination of adjusted franchising margins in this presentation for 2007

through 2010 differ from amounts reported in exhibit 8 of our year-end earnings

announcements for those years. Source: Choice Internal Data, December

2010 |

38

ADJUSTED DILUTED EARNINGS PER SHARE

(Continued)

Year Ended

Year Ended

Year Ended

Year Ended

Year Ended

Year Ended

Year Ended

December 31,

December 31,

December 31,

December 31,

December 31,

December 31,

December 31,

(In thousands, except per share amounts)

2004

2003

2002

2001

2000

1999

1998

Net Income

74,345

$

71,863

$

60,844

$

14,327

$

42,445

$

57,155

$

55,305

$

Adjustments:

Loss(Gain) on Extinguishment of Debt, Net of Taxes

433

-

-

-

-

-

(7,232)

Acceleration of Management Sucession Plan, Net of Taxes

-

-

-

-

-

-

-

Executive Termination Benefits, Net of Taxes

-

-

-

-

-

-

-

Loss on Sublease of Office Space, Net of Taxes

-

-

-

-

-

-

-

Curtailment of SERP, Net of Taxes

-

-

-

-

-

-

-

Loan Reserves Related to Impaired Notes Receivable, Net of Taxes

-

-

-

-

-

-

-

Resolution of Provisions for Income Tax Contingencies

(1,182)

-

-

-

-

-

-

Income Tax Expense Incurred Due to Foreign Earnings Repatriation

-

-

-

-

-

-

-

Loss(Gain) on Sunburst Note Transactions, Net of Taxes

-

(3,383)

-

-

4,721

-

-

Impairment of and Equity Losses in Friendly Hotels PLC Investment, Net of Taxes

-

-

-

37,166

7,532

-

-

Adjusted Net Income

73,596

$

68,480

$

60,844

$

51,493

$

54,698

$

57,155

$

48,073

$

Weighted Average Shares

Outstanding-Diluted 69,000

73,349

80,114

89,144

106,506

111,334

119,096

Diluted Earnings Per

Share 1.08

$

0.98

$

0.76

$

0.16

$

0.40

$

0.51

$

0.46

$

Adjustments:

Loss(Gain) on Extinguishment of Debt, Net of Taxes

0.01

-

-

-

-

-

(0.06)

Acceleration of Management Sucession Plan, Net of Taxes

-

-

-

-

-

-

-

Executive Termination Benefits, Net of Taxes

-

-

-

-

-

-

-

Loss on Sublease of Office Space, Net of Taxes

-

-

-

-

-

-

-

Curtailment of SERP, Net of Taxes

-

-

-

-

-

-

-

Loan Reserves Related to Impaired Notes Receivable, Net of Taxes

-

-

-

-

-

-

-

Resolution of Provisions for Income Tax Contingencies

(0.02)

-

-

-

-

-

-

Income Tax Expense Incurred Due to Foreign Earnings Repatriation

-

-

-

-

-

-

-

Loss(Gain) on Sunburst Note Transactions, Net of Taxes

-

(0.05)

-

-

0.04

-

-

Impairment of and Equity Losses in Friendly Hotels PLC Investment, Net of Taxes

-

-

-

0.42

0.07

-

-

Adjusted Diluted Earnings Per Share (EPS)

1.07

$

0.93

$

0.76

$

0.58

$

0.51

$

0.51

$

0.40

$

Source: Choice Internal Data, December 2010 |