Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - CIGMA METALS CORP | ex32_1.htm |

| EX-31.1 - EXHIBIT 31.1 - CIGMA METALS CORP | ex31_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

|

x

|

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2009

|

|

o

|

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM ____ TO ____

|

Commission file number 0-27355

CIGMA METALS CORPORATION

(Exact Name of registrant as specified in its charter)

|

Florida

|

98-0203244

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

c.Velazquez 150, Madrid, Spain

|

E-28002

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

Registrant’s telephone number, including area code

|

(+34) 60 900 1424

|

|

Securities registered under Section 12(b) of the Exchange Act:

|

|

|

None

|

|

|

Securities registered under Section 12 (g) of the Exchange Act:

|

|

|

Common stock, par value $0.0001 per share

|

Pink Sheets

|

|

Title of each class

|

Name of each exchange on which registered

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

x Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

o Yes x No

1

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer: o

|

Accelerated Filer: o

|

|

Non-accelerated filer: o (Do not check if a smaller reporting company)

|

Smaller reporting company: þ

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

o Yes x No

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

$14,710,500 as of June 30, 2009

Indicate the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date: 53,500,000 shares of Common Stock were outstanding as of September 13, 2010.

2

|

Part I

|

||

|

Item 1.

|

4

|

|

|

Item 1A

|

7

|

|

|

Item 1B

|

11

|

|

|

Item 2

|

11

|

|

|

Item 3

|

20

|

|

|

Item 4

|

20

|

|

|

PART II

|

||

|

Item 5

|

20

|

|

|

Item 6

|

22

|

|

|

Item 7

|

22

|

|

|

Item 7A

|

29

|

|

|

Item 8

|

29

|

|

|

Item 9

|

30

|

|

|

Item 9A

|

30

|

|

|

Item 9B

|

32

|

|

|

PART III

|

||

|

Item 10

|

32

|

|

|

Item 11

|

38

|

|

|

Item 12

|

41

|

|

|

Item 13

|

42

|

|

|

Item 14

|

43

|

|

|

PART IV

|

||

|

Item 15

|

44

|

|

|

46

|

PART I

BUSINESS

This annual report contains statements that plan for or anticipate the future and are not historical facts. In this Report these forward looking statements are generally identified by words such as “anticipate,” “plan,” “believe,” “expect,” “estimate,” and the like. Because forward-looking statements involve future risks and uncertainties, these are factors that could cause actual results to differ materially from the estimated results. These risks and uncertainties are detailed in Item 1. “Business,” Item 2. “Properties,” Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” Item 8. “Financial Statements and Supplementary Data” and Item 13. “Certain Relationships and Related Transactions and Director Independence”.

The Private Securities Litigation Reform Act of 1995, which provides a “safe harbor” for such statements, may not apply to this report.

|

Item 1.

|

Business

|

Business Development

We were incorporated under the laws of the State of Florida on January 13, 1989 as "Cigma Ventures Corporation". On April 17, 1999 we changed our name to “Cigma Metals Corporation” and are in the business of location, acquisition, exploration and, if warranted, development of mineral properties. Through our Russian subsidiary, we are engaged in the exploration of gold and silver mining properties located in the Russian Federation and the Republic of Kazakhstan, and have not yet determined whether our properties contain mineral reserves that may be economically recoverable.

Our general business strategy is to acquire mineral properties either directly or through the acquisition of operating entities. Our continued operations and the recoverability of mineral property costs is dependent upon the existence of economically recoverable mineral reserves, confirmation of our interest in the underlying properties, our ability to obtain necessary financing to complete the development and upon future profitable production.

Since 1999 we have acquired and disposed of a number of properties. We have not been successful in any of our exploration efforts to establish reserves on any of the properties that we owned or in which we have or have had an interest.

We currently have interest in three (3) properties none of which contain any reserves. Please refer to “Description of Properties.” The accompanying consolidated financial statements have been prepared in accordance with generally accepted accounting principles applicable to a going concern which contemplates the realization of assets and the satisfaction of liabilities and commitments in the normal course of business. As discussed in Note 1 to the consolidated financial statements, the Company has not generated revenue and has experienced recurring losses from operations since inception, and has a working capital deficit. We will not generate revenues even if any of our exploration programs indicate that a mineral deposit may exist on our properties. Accordingly, we will be dependent on future financings in order to maintain our operations and continue our exploration activities. These conditions raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans regarding these matters are also described in Note 1 to the consolidated financial statements. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

We have not been involved in any bankruptcy, receivership or similar proceedings.

Our Principal Products and Their Markets

We are a junior mineral exploration company. Our strategy is to concentrate our investigations into: (i) existing operations where an infrastructure already exists; (ii) properties presently being developed and/or in advanced stages of exploration which have potential for additional discoveries; and (iii) grass-roots exploration opportunities.

We are currently concentrating our property exploration activities in the Russian Federation and the Republic of Kazakhstan.

Our properties are in the exploration stage only and are without a known body of mineral reserves. Development of the properties will follow only if satisfactory exploration results are obtained. Mineral exploration and development involves a high degree of risk and few properties that are explored are ultimately developed into producing mines. There is no assurance that our mineral exploration and development activities will result in any discoveries of commercially viable bodies of mineralization. The long-term profitability of our operations will be, in part, directly related to the cost and success of our exploration programs, which may be affected by a number of factors. Please refer to “Item 1A. Risks Factors”

Significant Developments in fiscal 2009 and Subsequent Events

For the year ended December 31, 2009 we recorded exploration expenses of $623,794 compared to $2,941,613 in fiscal 2008. The following is a breakdown of the exploration expenses by property: Republic of Kazakhstan $623,794 (2008 - $2,941,613) and Russian Federation $0 (2008 - $0).

In February 2009, 500,000 common shares were authorized for issuance at $0.20 per share for cash proceeds of $100,000. The shares were to a company who resides outside the United States of America (in accordance with the exemption from registration requirements afforded by Regulation S as promulgated thereunder).

In March 2009, 1,000,000 common shares were authorized for issuance at $0.20 per share for cash proceeds of $200,000. The shares were to a company who resides outside the United States of America (in accordance with the exemption from registration requirements afforded by Regulation S as promulgated thereunder).

In July 2009, 3,900,000 common shares were authorized for issuance at $0.30 per share for cash proceeds of $1,170,000. The shares were to an individual and companies who reside outside the United States of America (in accordance with the exemption from registration requirements afforded by Regulation S as promulgated thereunder).

On December 31, 2009, the Company entered into an Equity Purchase Agreement with Copperbelt AG, a Swiss corporation, for the sale of the Company’s 100% interest in its Kazakhstan subsidiary to Copperbelt AG for $1,500,000 and other consideration, the value of which has not been determined as of yet. The purchase price will be paid at the time of closing. In December 2009, the Company received a deposit from Copperbelt AG in the amount of $450,000. The transaction is subject to the approval of the Company’s shareholders so no accounting effects have been recorded yet.

On March 9, 2010, the Company signed a property purchase agreement with Alphamin Resources Corp. (“Alphamin”) regarding the sale and transfer by Alphamin of a 100% interest in the Aurora mining concessions located in the State of Guerrero, Mexico to the Company, in consideration for $150,000 and 1,000,000 common shares of Cigma. Alphamin will retain a 1.5% Net Smelter Returns Royalty on production from the Property. On June 11, 2010 the Company’s wholly owned Mexican subsidiary, Exploraciones Cigma, S.A. de C.V., filed the Assignment Agreement for the Aurora II mining concession between Alphamin’s wholly owned Mexican subsidiary, Exploraciones La Plata, S.A. de C.V. and Exploraciones Cigma, S.A. de C.V. with the Mexican Public Registry of Mining. This purchase has not yet closed as of this date.

Distribution Methods of Our Products and Services

We are a mineral exploration company and are not in the business of distributing any products or services.

Status of Any Publicly Announced New Product or Service

We have no plans for new products or services that we do not already offer.

Competitive Business Conditions and Our Competitive Position in the Industry and Methods of Competition

Vast areas of Kazakhstan have been explored and in some cases staked through mineral exploration programs. Vast areas also remain unexplored. The cost of staking and re-staking new mineral claims and the costs of most phase one exploration programs are relatively modest. Additionally, in many more prospective areas, extensive literature is readily available with respect to previous exploration activities. These facts make it possible for a junior mineral exploration company such as ours to be very competitive with other similar companies. We are also competitive with senior companies who are doing grass roots exploration. In the event our exploration activities uncover prospective mineral showings, we anticipate being able to attract the interest of better financed industry partners to assist on a joint venture basis in more extensive exploration. We are at a competitive disadvantage compared to established mineral exploration companies when it comes to being able to complete extensive exploration programs on claims which we hold or may hold in the future. If we are unable to raise capital to pay for extensive claim exploration, we will be required to enter into joint ventures with industry partners which will result in our interest in our claims being substantially diluted.

Management of our company remains committed to building a portfolio of mineral exploration properties principally through their own efforts. We are one small company in a large competitive industry with many other junior exploration companies who are evaluating and re-evaluating prospective mineral properties in Kazakhstan and Mexico.

Sources and Availability of Raw Materials and the Names of Principal Suppliers

As a mineral exploration company, we do not require sources of raw materials and do not have principal suppliers in the way which applies to manufacturing companies. Our raw materials are, in effect, mineral exploration properties which we may stake or acquire from third parties. Our management team seeks to assemble a portfolio of quality mineral exploration properties in Brazil. Initially, we will operate in the field with our president, Technical director and various consultants on an as needed basis. This will enable us to assemble a portfolio of properties through grass roots exploration and staking. We will also acquire new properties through option agreements where new properties can be acquired on favorable terms.

Dependence on One or a Few Major Customers

We are in the business of mining exploration. We are not selling any product or service and therefore have no dependence on one or a few major customers.

Patents, Trademarks, Licenses, Franchises, Concessions, Royalty Agreements or Labor Contracts, Including Duration

Our Company does not own any patents or trademarks. We are not party to any labor agreements or contracts. Licenses, franchises, concessions and royalty agreements are not part of our business.

Need for any government approval of principal products or services

As a mineral exploration company, we are not in a business which requires extensive government approvals for principal products or services.

In the event mining claims which we acquire in the future prove to host viable ore bodies, we would likely sell or lease the deposit to a company whose business is the extraction and treatment of ore. This company would undertake the sale of metals or concentrates and pay us a net smelter royalty as specified in a future lease agreement. All responsibility for government approvals pertaining to mining methods, environmental impacts and reclamation would be the responsibility of this contractor. All costs to obtain the necessary government approvals would be factored into technical and viability studies in advance of a decision being made to proceed with development of an ore body.

The mining industry in the Republic of Kazakhstan and the Russian Federation is highly regulated. Our president and Technical director have extensive industry experience and are familiar with government regulations respecting the initial acquisition and early exploration of mining claims in the Republic of Kazakhstan and the Russian Federation. The Company is required under law to meet government standards relating to the protection of land and waterways, safe work practices and road construction. We are unaware of any proposed or probable government regulations which would have a negative impact on the mining industry in The Republic of Kazakhstan and the Russian Federation. We propose to adhere strictly to the regulatory framework which governs mining operations in the Republic of Kazakhstan and the Russian Federation.

Effect of existing or probable governmental regulations on our business.

Management is unaware of any existing or probable government regulations which would have a positive or negative impact on our company's business.

Costs and effects of compliance with environmental laws (federal, state and local)

At the present time, our costs of compliance with environmental laws are minimal. In the event that claims which we may acquire in the future host a viable ore body, the costs and affects of compliance with environmental laws will be incorporated in the exploration plan for these claims. These exploration plans will be prepared by qualified mining engineers.

Number of total employees and number of full time employees

As of September 13, 2010 there were five part time employees.

|

Item 1A.

|

Risk Factors

|

We are an exploration stage company and have incurred substantial losses since inception.

We have never earned any revenues. In addition, we have incurred net losses of $11,137,482 for the period from our inception (January 13, 1989) through December 31, 2009 and, based upon our current plan of operation, we expect that we will incur losses for the foreseeable future.

Potential investors should be aware of the difficulties normally encountered by mineral exploration companies and the high rate of failure of such companies. We are subject to all of the risks inherent to an exploration stage business enterprise, such as limited capital mineralized materials, lack of manpower, and possible cost overruns associated with our exploration programs. Potential investors must also weigh the likelihood of success in light of any problems, complications, and delays that may be encountered with the exploration of our properties.

Because we are small and do not have much capital, we must limit our exploration activity. As such we may not be able to complete an exploration program that is as thorough as we would like. In that event, an existing ore body may go undiscovered. Without an ore body, we cannot generate revenues and you will lose your investment.

Our independent registered public accounting firm has expressed substantial doubt about our ability to continue as a going concern, which may hinder our ability to obtain future financing.

Our independent registered public accounting firm has issued its report, which includes an explanatory paragraph for going concern uncertainty on our consolidated financial statements as of and for the year ended December 31, 2009. Because we have not yet generated revenues from our operations our ability to continue as a going concern is currently heavily dependent upon our ability to obtain additional financing to sustain our operations. Such financing may take the form of the issuance of common or preferred stock or debt securities, or may involve bank financing. Although we have completed several equity financings, the fact that our auditors have issued a “going concern” opinion may hinder our ability to obtain additional financing in the future. Currently, we have no commitments to obtain any additional financing, and there can be no assurance that financing will be available in amounts or on terms acceptable to us, if at all.

Our failure to timely file certain periodic reports with the SEC poses significant risks to our business, each of which could materially and adversely affect our financial condition and results of operations.

We did not timely file with the SEC our Annual Report on Form 10-K for the fiscal year ended December 31, 2008 and our Quarterly Report on Form 10-Q for the quarterly periods ended March 31, June 30, and September 30, 2009. Consequently, we were not compliant with the periodic reporting requirements under the Securities Exchange Act of 1934, as amended. In addition, our failure to timely file those and possibly future periodic reports with the SEC could subject us to enforcement action by the SEC and shareholder lawsuits. Any of these events could materially and adversely affect our financial condition and results of operations and our ability to register with the SEC public offerings of our securities for our benefit or the benefit of our security holders.

Because we do not have any revenues, we expect to incur operating losses for the foreseeable future.

We have never generated revenues and we have never been profitable. Prior to completing exploration on our mineral properties, we anticipate that we will incur increased operating expenses without realizing any revenues. We therefore expect to incur significant losses into the foreseeable future. If we are unable to generate financing to continue the exploration of our properties, we will fail and you will lose your entire investment.

None of the properties in which we have an interest or the right to earn an interest have any known reserves.

We currently have an interest or the right to earn an interest in three properties, none of which have any reserves. Based on our exploration activities through the date of this Form 10-K, we do not have sufficient information upon which to assess the ultimate success of our exploration efforts. If we do not establish reserves we may be required to curtail or suspend our operations, in which case the market value of our common stock may decline and you may lose all or a portion of your investment.

We have only completed the initial stages of exploration of our properties, and thus have no way to evaluate whether we will be able to operate our business successfully. To date, we have been involved primarily in organizational activities, acquiring interests in properties and in conducting preliminary exploration of properties. We have not earned any revenues and have not achieved profitability as of the date of this Form 10-K.

We are subject to all the risks inherent to mineral exploration, which may have an adverse affect on our business operations.

Potential investors should be aware of the difficulties normally encountered by mineral exploration companies and the high rate of failure of such enterprises. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the exploration of the mineral properties that we plan to undertake. These potential problems include, but are not limited to, unanticipated problems relating to exploration and additional costs and expenses that may exceed current estimates. If we are unsuccessful in addressing these risks, our business will likely fail and you will lose your entire investment.

We are subject to the numerous risks and hazards inherent to the mining industry and resource exploration including, without limitation, the following:

|

|

·

|

interruptions caused by adverse weather conditions;

|

|

|

·

|

unforeseen limited sources of supplies resulting in shortages of materials, equipment and availability of experienced manpower.

|

The prices and availability of such equipment, facilities, supplies and manpower may change and have an adverse effect on our operations, causing us to suspend operations or cease our activities completely.

It is possible that our title for the properties in which we have an interest will be challenged by third parties.

We have not obtained title insurance for our properties. It is possible that the title to the properties in which we have our interest will be challenged or impugned. If such claims are successful, we may lose our interest in such properties.

Our failure to compete with our competitors in mineral exploration for financing, acquiring mining claims, and for qualified managerial and technical employees will cause our business operations to slow down or be suspended.

Our competition includes large established mineral exploration companies with substantial capabilities and with greater financial and technical mineralized materials than we have. As a result of this competition, we may be unable to acquire additional attractive mining claims or financing on terms we consider acceptable. We may also compete with other mineral exploration companies in the recruitment and retention of qualified managerial and technical employees. If we are unable to successfully compete for financing or for qualified employees, our exploration programs may be slowed down or suspended.

Compliance with environmental regulations applicable to our operations may adversely affect our capital liquidity.

All phases of our operations in the Republic of Kazakhstan and the Russian Federation, where our properties are located, will be subject to environmental regulations. Environmental legislation in the Republic of Kazakhstan and the Russian Federation is evolving in a manner which will require stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects and a heightened degree of responsibility for companies and their officers, directors and employees. It is possible that future changes in environmental regulation will adversely affect our operations as compliance will be more burdensome and costly.

Because we have not allocated any money for reclamation of any of our mining claims, we may be subject to fines if the mining claims are not restored to its original condition upon termination of our activities.

Our directors may face conflicts of interest in connection with our participation in certain ventures because they are directors of other mineral mineralized material companies.

Messrs. Gomez de Segura and Mueller, who serve as directors, may also be directors of other companies (including mineralized material exploration companies) and, if those other companies participate in ventures in which we may participate, our directors may have a conflict of interest in negotiating and concluding terms respecting the extent of such participation. It is possible that due to our directors’ conflicting interests, we may be precluded from participating in certain projects that we might otherwise have participated in, or we may obtain less favourable terms on certain projects than we might have obtained if our directors were not also directors of other participating mineral mineralized materials companies. In an effort to balance their conflicting interests, our directors may approve terms equally favourable to all of their companies as opposed to negotiating terms more favourable to us but adverse to their other companies. Additionally, it is possible that we may not be afforded certain opportunities to participate in particular projects because those projects are assigned to our directors’ other companies for which the directors may deem the projects to have a greater benefit.

Our future performance is dependent on our ability to retain key personnel, loss of which would adversely affect our success and growth.

Our performance is substantially dependent on performance of our senior management. In particular, our success depends on the continued efforts of Mr. Gomez de Segura. The loss of his services could have a material adverse effect on our business, results of operations and financial condition as our potential future revenues would most likely dramatically decline and our costs of operations would rise. We do not have employment agreements in place with any of our officers or our key employees, nor do we have key person insurance covering our employees.

The value and transferability of our shares may be adversely impacted by the limited trading market for our shares.

There is only a limited trading market for our common stock on the Pink Sheets. This may make it more difficult for you to sell your stock if you so desire.

Our common stock is a penny stock and because "penny stock” rules will apply, you may find it difficult to sell the shares of our common stock.

Our common stock is a “penny stock” as that term is defined under Rule 3a51-1 of the Securities Exchange Act of 1934. Generally, a "penny stock" is a common stock that is not listed on a national securities exchange and trades for less than $5.00 a share. Prices often are not available to buyers and sellers and the market may be very limited. Penny stocks in start-up companies are among the most risky equity investments. Broker-dealers who sell penny stocks must provide purchasers of these stocks with a standardized risk-disclosure document prepared by the Securities and Exchange Commission. The document provides information about penny stocks and the nature and level of risks involved in investing in the penny stock market. A broker must also give a purchaser, orally or in writing, bid and offer quotations and information regarding broker and salesperson compensation, make a written determination that the penny stock is a suitable investment for the purchaser, and obtain the purchaser's written agreement to the purchase. Consequently, the rule may affect the ability of broker-dealers to sell our securities and also may affect the ability of purchasers of our stock to sell their shares in the secondary market. It may also cause fewer broker dealers to make a market in our stock.

Many brokers choose not to participate in penny stock transactions. Because of the penny stock rules, there is less trading activity in penny stock and you are likely to have difficulty selling your shares.

In addition to the "penny stock" rules promulgated by the Securities and Exchange Commission, FINRA has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low-priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer's financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low priced securities will not be suitable for at least some customers. FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock and have an adverse effect on the market for our shares.

Future sales of shares by us may reduce the value of our stock.

If required, we will seek to raise additional capital through the sale of our common stock. Future sales of shares by us could cause the market price of our common stock to decline and may result in further dilution of the value of the shares owned by our stockholders.

|

Item 1B.

|

Unresolved Staff Comments

|

Not Applicable.

|

Item 2.

|

Properties

|

Office Premises

We conduct our activities from our principal and technical office located at 18, 80 Furmanova Str, Almaty, Republic of Kazakhstan. We believe that these offices are adequate for our purposes. We do not own any real property or significant assets. Management believes that this space will meet our needs for the next 12 months.

Mining Properties

Our properties are in the preliminary exploration stage and do not contain any known bodies of ore.

We conduct exploration activities from our principal and technical office located at 18, 80 Furmanova Street, Almaty, Republic of Kazakhstan. The telephone number is (+7) 327-2611 026. We believe that these offices are adequate for our purposes and operations.

Our strategy is to concentrate our efforts on: (i) existing operations where an infrastructure already exists; (ii) properties presently being developed and/or in advanced stages of exploration which have potential for additional discoveries; and (iii) grass-roots exploration opportunities.

We are currently concentrating our property exploration activities in the Republic of Kazakhstan and the Russian Federation.

Our properties are in the exploration stage only and are without a known body of mineral reserves. Development of the properties will follow only if satisfactory exploration results are obtained. Mineral exploration and development involves a high degree of risk and few properties that are explored are ultimately developed into producing mines. There is no assurance that our mineral exploration and development activities will result in any discoveries of commercially viable bodies of mineralization. The long-term profitability of our operations will be, in part, directly related to the cost and success of our exploration programs, which may be affected by a number of factors. Please refer to “Item 1A. Risk Factors.”

We currently have an interest in three (3) projects, two located in the Tomsk Oblast region in the Russian Federation and one located in the Republic of Kazakhstan. We have conducted only preliminary exploration activities to date and may discontinue such activities and dispose of the properties if further exploration work is not warranted.

Properties

Russian Federation

Haldeevskaya License

Cigma (80%) -Haldej Zoloto SPA was executed by 22 June 2005

The Haldeevskaya exploration licence has expired by 31 Dec 2007. In 2009 no activity has been shown on Licence property.

The Haldeevskaya exploration license covers an area of 576 km2 (57,600ha) and is located approximately 16 kilometres NE from Tomsk via paved highway. Excellent infrastructure is currently in place, including, maintained tarmac access roads, high tension power lines at 500 kilowatts per line, gravel vehicular access roads over the project area with close-spaced, 100 metre, cut lines over the target areas. The area is also close to the railheads in Tomsk, with links to the Trans Siberian Railway, and all infrastructures associated with a regional centre.

Geology of Haldeevskaya area is represented by the mid Devonian volcanogenic-sedimentary sediments of the Mitrofan suite, terrigenous (“black shale”) sediments of the Jurginsk, Pachinsk, Salamat suites of upper Devonian, and the Yarsk, Lagernosadsk stratus of the lower Carboniferous age. The rock formations are deformed into the linear folds with the north-north-eastern strike and they are cut by the series of longitudinal, lateral and diagonal fractures of different type and order. The area is located at the front zone of the Tomsk thrust above the granitoid intrusions that are inferred by geophysics. Dolerite and Monzonite dikes intrude Paleozoic rocks forming the series of dike zones with a north-western trend with an echelon-like arrangement of some dikes and their groups. Mineralization is focussed into areas associated with the thrusting. Towards the end of 19th and first half of the 20th centuries the region was one of the most prolific gold mining spots in Russia. The coarse gold was panned from the Tom river and the numerous drainage systems around the city of Tomsk. In late 1980 Geosphera made its first gold discoveries in hard rock. As a result of the geochemical and geophysical surveys a series of 6 highly prospective gold soil anomalies have been outlined Of the 6 large anomalies the area currently considered the most perspective are the Semiluzhenskoye, Verkhnekamensk and Sukhorechenskoye prospects. The Verkhnekamensk anomaly is located in the eastern part of the Haldeiskaja license on the tectonic contact between the clay shales and volcanics. As a result of the litho-geochemical, geological and geophysical studies, conducted by Cigma, two mineralized zones of east-west strike have been outlined and plotted at 1:20,000. These zones were traced across the area for 3 kilometres with widths ranging from 250 to 700 meters. Within these zones 3 anomalies were found and appear prospective for gold mineralization. The first diamond drilling program has outlined vast areas of hydrothermal alteration, preliminary mineralogical investigations have discovered free gold in drill core from the upper part of the mineralization zone.

Tugojakovsk License

Cigma (80%)-Geosphera (20%) JV Agreement was executed by 03 Mar 2006.

The Tugojakovsk exploration license (expiry 01 Dec 2009) covers an area of 164 km2 (16,400ha) and is located 25 kilometres SE from the regional centre of Tomsk via paved highway. An excellent infrastructure is in place including excellent sealed roads, close access to railheads and the infrastructure associated with the regional centre of Tomsk.

The geology of Tugojakovsk area is represented by the sedimentary rock formations of Carboniferous age composed of carbonaceous shales, siltstones and sandstones united under the common term "black shale". The rocks are deformed into linear folds and cut by the series of longitudinal, lateral and diagonal faults. The dolerite and monzonite dikes intrude Palaeozoic rocks forming a series of dike zones controlling quartz stock works with gold mineralization.

The Baturinsk occurrence, located within the Tugojakovsk license is composed of a series silicified shear zones (mylonite zones) consisting of numerous, locally intense, small quartz veinlets carrying gold. The surrounding geological units are composed of mineralised carbonaceous shales. In 2006 there have been drilled 1,900 metres of core drilling. The gold mineralization zone, which is available on surface was not intercepted by the drill holes. Cigma made the decision to discontinue further expenditures on this licence area (Report 10-K of 2006).

The Tugojakovsk exploration license has expired by 01 Dec 2009.

Republic of Kazakhstan

Maykubinsk exploration and mining licence

|

Figure 1 -

|

Astana is an important regional centre for the project infrastructure both as an international airport and as the location of all the exploration/mining authorities.

|

The Company, through its 100% subsidiary Dostyk LLP holds high potential Maykubinsk exploration and mining license located in Pavlodar Oblast Region in Kazakhstan. Accordingly to Kazakhstan Mining Law an exploration and mining licence (also called a Contract with the Government) could be obtained by any private or corporate body, including those with 100% of foreign ownership, through an open tender published by government. If the licence is already issued then it could be acquired through direct negotiations with the owner and re-registered by State authorities. Cigma acquired Dostyk LLP from Eureka Mining Ltd, a UK based public company.

The Dostyk acquisition steps were as follows:

The Company through execution of Shares Purchase Agreement with Eureka Mining Ltd has acquired 100% shares of Dostyk in following steps and conditions:

|

|

·

|

On 27 Jan 2007 Cigma has been granted 51% of Dostyk LLP in return for commitment to spend US$300,000 for Exploration on Maykubinsk licence.

|

|

|

·

|

By by spending further US$700,000 Cigma had rights to obtain further 20% of Dostyk LLP

|

|

|

·

|

Cigma had the right to obtain a further 19% of Dostyk LLP by spending further US$1,000,000 to increase sharing in Dostyk to 90%.

|

|

|

·

|

Cigma paid Eureka US$400,000 to obtain the remaining 10% of Dostyk and so became 100% owner of Dostyk LLP and consequently of Maykubinsk licence.

|

Figure 2

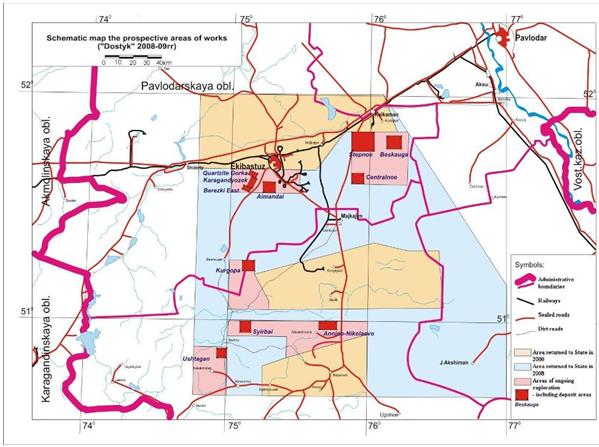

The Dostyk property (Figure 2) originally has covered an area of 14,000 square kilometres (1,400,000ha), in northern Kazakhstan in a region which has been producing gold and base metals for decades including Zinc, Copper, Nickel, Lead and Gold in various geological environments. Geologically the area comprises granites, granodiorite and monzonite with associated continental volcanogenic formations, island arc formations and mafic and felsic intrusives. Currently, over 130 known mineral occurrences occur on the property, and the Company has selected 2 targets as the focus of the 2009 exploration campaign.

The licence area has a well-developed infrastructure (figure 2) including a network of railways and power lines that service the needs of the entire country and parts of the Urals in neighbouring Russia. Access to any of the exploration prospects is available trough the year by sealed, gravel or dirt roads of good quality. High voltage power lines criss-crossing the Dostyk project area. Actually this region produces the cheapest electricity in Kazakhstan. Water sources are represented by number of abandoned coaleries and fresh water lakes in vicinity to exploration prosects.

The region’s economy of Central Kazakhstan is predicated on mining, power generation and agriculture. Mining consists of giant coal mining at Karaganda, Ekibastuz and Maikube, mining of polymetallic, gold-rich volcanogenic massive sulphide deposits at Abyz, Maikain, Alpys and Souvenir. Roads and trails criss-cross the region to serve the agriculture and mining areas. Numerous high-tension power lines radiate out of several power generation stations in Ekibastuz to serve Kazakhstan and for power export to Russia.

Regional Geology and mineralization

Central Kazakhstan geological structure is represented by strong folded and dislocated Cambrian-Ordovician submarine volcanic and sedimentary rocks, covered by Silurian-Devonian sediments and Devonian felsitic volcanic suites with a whole series of stocks, dikes and sills of various ages. Late Paleozoic rocks are represented by Carboniferous and Jurassic marine and continental suites.

Mineral deposits are related in time and space to the various lithologies:

|

-

|

Gold-rich volcanogenic massive sulphide (VMS) deposits associated with Ordovician submarine volcanic rocks.

|

|

-

|

Porphyry gold-copper deposits associated with altered sub-volcanic dioritic intrusives presumable of Ordovician age.

|

|

-

|

Epithermal gold deposits associated with quartz veins and quartz-sulphide stockworks in Ordovician, Devonian and Permian intrusives of diorite to granite composition.

|

|

-

|

Lead-zinc mineralization associated with Silurian-Devonian siltstone and carbonate beds.

|

|

-

|

Coal deposits associated with Carboniferous marine and deltaic sedimentary rocks.

|

|

-

|

Titanium and zirconium-rich sands in Late Carboniferous beach sands.

|

|

-

|

Bauxite and nickel laterite deposits formed from modern weathering of Paleozoic limestones and Cambrian ultramafic rocks.

|

License and Contract commitments

License #785 for an original area of 14,000 square kilometres (1,400,000ha) in Central Kazakhstan was issued on January 8, 1996. In accordance with new legislation the Licence was converted on Oct 11, 2001 to Subsoil Contract # 759 with exploration and mining rights valid until Jan 8 2021. Extension of mining term is warranted till full depletion of mineral resources. The Contract #759 was issued to Dostyk Ltd. The exploration term expires on Dec 31, 2009. Dostyk has currently submitted to the Kazakhstan Authorities an application for exploration extension till Dec 2011.

In accordance with Kazakhstan regulations an exploration ground proved to be barren for further exploration should be returned to State by end of each year. By end of 2008 the Dostyk has retained 2,774 sq. km (274,400ha) of exploration ground. The contract territory will be returned to the State by December 2011 except areas, which Dostyk would claim as commercial discoveries i.e. those prospects on which Kazakh style resources of C1-C2 categories would be proved. No maintenance or any other fees and payments are required to retain the Licence/Contract. No production sharing arrangements are related to the Dostyk properties. A royalty interest is payable to be the State once Dostyk goes into production. The royalty rate for mineral deposits in Kazakhstan range from 0.3% to 3.0% in different projects and is subject to a feasibility study and direct negotiations with the State authority. Cigma is the sole owner of the Dostyk LLP, i.e. no body has any claims or interest in Dostyk except Cigma.

In order to retain exploration and mining rights and to convert the exploration licence/contract into a mining licence Dostyk LLP should by end of exploration term, which is 31 Dec 2010, submit and prove with State Resources Commission of Kazakhstan a Report of C1-C2 Mineral Resources. That warranties to Dostyk exclusive and irrevocable rights for mining of the mineral resources proved with government of Kazakhstan.

The surface of the licence area is represented by poor-quality pastoral ground with quite spare life stock on it. Accordingly to Kazakhstan law, the sub-soil contract prevails above surface agricultural or other facilities. However Dostyk is required every year to obtain an exploration permit from local authorities.

Exploration Works 2009

The exploration work has been supervised by Kiintas Mining Management Pty Ltd, an Australian company, providing exploration and mineral resource service in Central Asia.

The quality control of drilling, sampling, assaying has been carried out on site by Micromine Ltd, an Australian Resource company and by Alex Stewart Laboratories, an internationally accredited UK company with laboratory in Kyrgyzstan. Dostyk assays 100% of its samples in this lab.

Total exploration expenditures incurred by the Company during 2009 on the Dostyk Project amounted to $ 623,794.

The funds were spent on the Berezki East Prospect and the Quartzite Gorka Prospect represented by gold-copper porphyry mineralization zones. The main exploration expenditures were diamond drilling (11 drill holes for 3,350 meters) and assays. The breakdown of the costs is shown in the table below.

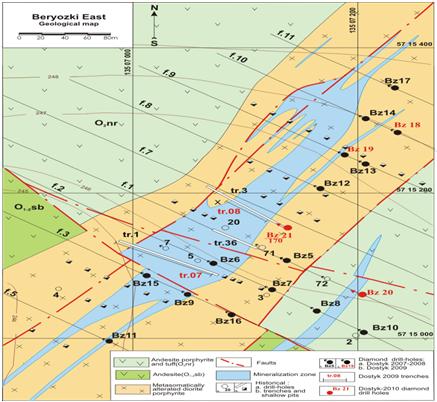

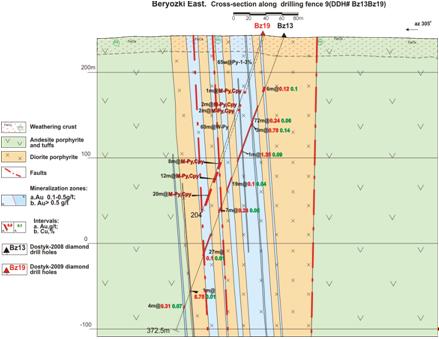

On Berezki East Prospect (figures 3 & 4), we continued extension drilling on Northern and Southern flanks targeting deeper levels of mineralization zone. As a result of the 2009 drilling program, the mineralization has been extended on strike for further 340 meters and in depth direction to 300 meters. The total explored length of the zone is 650 meters by average width 25 to 30 meters by grade 1.06g/t of gold and 0.14% of copper.

Figure 3

Figure 4

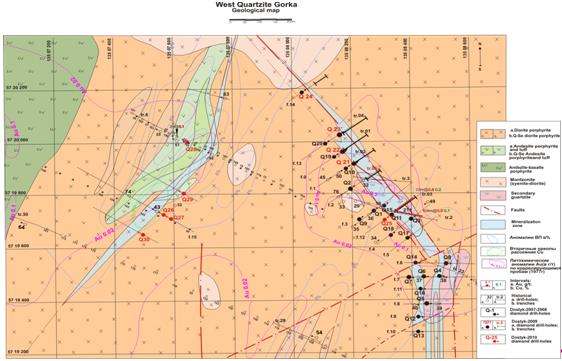

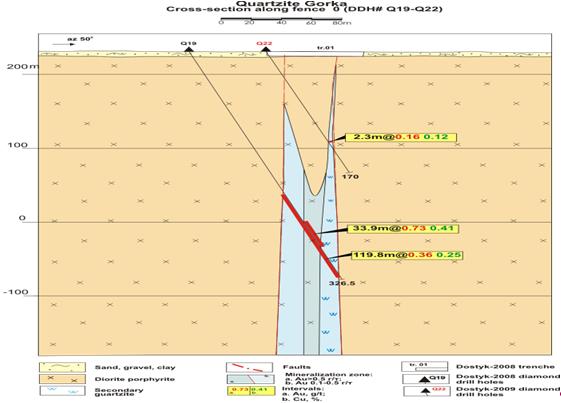

In 2009 , we continued the exploration program on the Quartzite Gorka Prospect (figures 5 & 6), targeting the Western extension of gold-copper mineralization zone and its extension to depth direction. 5 holes have been drilled for a total of 1,520 meters. The drilling results have revealed a pinch out of mineralization in northwest direction with reduced zone width zone and decreased values of the gold (0.3g/t) and copper (0.1%).

Figure 5

Figure 6

In 2010 we will focus on conducting a metallurgical study of the mineralization zones on the Berezki East and Quartzite Gorka prospects explored in 2007 - 2009.

|

Berezki East 2009

|

||||||||||||

|

Type of work

|

Volume

|

USD

|

||||||||||

|

Drill holes

|

drill holes

|

6 | ||||||||||

|

meters drilled

|

m | 1,830 | 183,000 | |||||||||

|

samples treatment

|

sample

|

1,750 | ||||||||||

|

Fire assays

|

assay

|

1,710 | 41,000 | |||||||||

|

IP assays

|

assay

|

1,050 | ||||||||||

|

Metallurgical test

|

34,000 | |||||||||||

|

Data processing & administration

|

59,000 | |||||||||||

|

Wages -geological staff

|

49,000 | |||||||||||

|

Berezki East total

|

366,000 | |||||||||||

| Budget 2010 |

3 drill holes for 1300m, 1,100 assays

|

200,000 | ||||||||||

|

Quartzite Gorka 2009

|

||||||||||||

|

Type of work

|

Volume

|

USD

|

||||||||||

|

Drill holes

|

drill holes

|

5 | ||||||||||

|

meters drilled

|

m | 1,520 | 152,000 | |||||||||

|

samples treatment

|

sample

|

1,430 | ||||||||||

|

Fire assays

|

assay

|

1,400 | 22,000 | |||||||||

|

IP assays

|

assay

|

1,050 | ||||||||||

|

Data processing & administration

|

61,000 | |||||||||||

|

Wages - geological staff

|

48,000 | |||||||||||

|

Quartzite Gorka total

|

283,000 | |||||||||||

| Budget 2010 |

4 drill holes for 1400m, 1,200 assays

|

300,000 | ||||||||||

Apart of continuing drilling on two above prospects a serious exploration program in 2010 is proposed on Beskauga copper-gold prospect. Exploration works will include geophysical survey on area of 6.5sq. km, a drilling of six core drill holes for 3,000m, assaying, metallurgical test, JORC compliant resource estimation with total costs of US$ 600,000.

|

Item 3.

|

Legal Proceedings

|

The Company is not involved in any legal proceedings at this time.

|

Item 4.

|

(Removed and Reserved)

|

PART II

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

Our Common Stock is quoted on the OTC Markets “Pink Sheets”. The following table sets forth the high and low bid prices for the Common Stock for the calendar quarters indicated as reported by the Pink Sheets for the last two years. These prices represent quotations between dealers without adjustment for retail mark-up, markdown or commission and may not represent actual transactions. Our stock is also quoted on the Frankfurt Exchange under the symbols “C9K.FSE,” and “C9K.ETR” and on the Berlin-Bremen Exchange under the symbol “C9K.BER.”

|

First

Quarter

|

Second

Quarter

|

Third

Quarter

|

Fourth

Quarter

|

|||||||||||||

|

2010 – High

|

$ | 0.59 | $ | 044 | $ | 0.20 | (1) | |||||||||

|

2010 – Low

|

$ | 0.21 | $ | 0.10 | $ | 0.10 | (1) | |||||||||

|

2009 – High

|

$ | 0.40 | $ | 0.42 | $ | 0.65 | $ | 0.65 | ||||||||

|

2009 – Low

|

$ | 0.18 | $ | 0.21 | $ | 0.29 | $ | 0.21 | ||||||||

|

2008 – High

|

$ | 0.72 | $ | 0.56 | $ | 0.51 | $ | 0.40 | ||||||||

|

2008 – Low

|

$ | 0.27 | $ | 0.31 | $ | 0.13 | $ | 0.13 | ||||||||

(1) The high and low bid prices for our Common Stock for the Third Quarter of 2010 were for the period July 1, 2010 to September 13, 2010.

As of December 31, 2009, there were 17 holders of record of the Common Stock.

No cash dividends were paid in 2009 or 2008. No cash dividends have been paid subsequent to December 31, 2009. The amount and frequency of cash dividends are significantly influenced by metal prices, operating results and our cash requirements.

We do not have securities authorized for issuance under an equity compensation plan.

In February 2009, 500,000 common shares were authorized for issuance at $0.20 per share for cash proceeds of $100,000. The shares were to a company who resides outside the United States of America (in accordance with the exemption from registration requirements afforded by Regulation S as promulgated thereunder).

In March 2009, 1,000,000 common shares were authorized for issuance at $0.20 per share for cash proceeds of $200,000. The shares were to a company who resides outside the United States of America (in accordance with the exemption from registration requirements afforded by Regulation S as promulgated thereunder).

In July 2009, 3,900,000 common shares were authorized for issuance at $0.30 per share for cash proceeds of $1,170,000. The shares were to an individual and companies who reside outside the United States of America (in accordance with the exemption from registration requirements afforded by Regulation S as promulgated thereunder).

We did not make any repurchases of our securities during the fourth quarter of our fiscal year ended December 31, 2009 or the subsequent period through to September 13, 2010.

Dividend Policy

We have never paid cash dividends on our capital stock and do not anticipate paying any cash dividends in the foreseeable future, but intend to retain our capital mineralized materials for reinvestment in our business. Any future determination to pay cash dividends will be at the discretion of the Board of Directors and will be dependent upon our financial condition, results of operations, capital requirements and other factors as the board of directors deems relevant.

|

Item 6.

|

Selected Financial Data

|

Not applicable

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

The following information should be read in conjunction with our audited consolidated financial statements and related notes thereto for the years ended December 31, 2009 and 2008 included elsewhere in this Form 10-K. We also urge you to review and consider our disclosures describing various risks that may affect our business, which are set forth under the heading “RISK FACTORS.”

|

(A)

|

General

|

We are a mineral exploration company engaged in the exploration of base, precious metals and industrial minerals worldwide. We were incorporated under the laws of the State of Florida on January 13, 1989, under the name "Cigma Ventures Corporation." We conduct our exploration and property acquisition activities through our head office which is located at is located at 18, 80 Furmanova Str, Almaty, Republic of Kazakhstan. The telephone number is (+7) 327 – 2611 026.

We had no revenues during fiscal 2009 and 2008. Funds raised in fiscal 2009 and 2008 were used for exploration of our properties and general administration.

|

(B)

|

Results of Operations

|

Year Ended December 31, 2009 (Fiscal 2009) versus Year Ended December 31, 2008 (Fiscal 2008)

For the year ended December 31, 2009 we recorded a loss of $2,235,894 or $0.04 per share, compared to a loss of $3,482,650 or $0.08 per share in 2008.

General and administrative expenses – For the year ended December 31, 2009 we recorded general and administrative expenses of $602,503 (fiscal 2008 - $534,132). The fiscal 2009 amount includes professional fees - accounting $69,277 (fiscal 2008 - $3,033) and legal $18,283 (fiscal 2008 - $55,053). Recent developments in capital markets have restricted access to debt and equity financing for the Company. As a result, the Company reduced its 2010 capital spending requirements in light of the current and anticipated, global economic environment.

Exploration expenditures - For the year ended December 31, 2009, we recorded total exploration costs of $623,794 compared to $2,941,613 in fiscal 2008. The following is a breakdown of the exploration expenses by property: Kazakhstan $623,794 (2008 - $2,941,613); Haldey Gold Project located in the Tomsk Oblast region of the Russian Federation totalled $0 (2008 - $0) and Tugojakovsk Project located in the Tomsk Oblast region of the Russian Federation totalled $0 (2008 - $0).

Depreciation expense – For the year ended December 31, 2009 we recorded depreciation expense of $20,909 compared to $19,707 in fiscal 2008.

|

(C)

|

Capital Resources and Liquidity

|

December 31, 2009 versus December 31, 2008:

Recent developments in capital markets have restricted access to debt and equity financing for many companies. The Company’s exploration properties are in the exploration stage, have not commenced commercial production and consequently the Company has no history of earnings or cash flow from its operations. As a result, the Company is reviewing its 2010/2011 exploration and capital spending requirements in light of the current and anticipated, global economic environment.

The Company currently finances its activities primarily by the private placement of securities. There is no assurance that equity funding will be accessible to the Company at the times and in the amounts required to fund the Company’s activities. There are many conditions beyond the Company’s control which have a direct bearing on the level of investor interest in the purchase of Company securities. The Company may also attempt to generate additional working capital through the operation, development, sale or possible joint venture development of its properties, however, there is no assurance that any such activity will generate funds that will be available for operations. Debt financing has not been used to fund the Company’s property acquisitions and exploration activities and the Company has no current plans to use debt financing. The Company does not have “standby” credit facilities, or off-balance sheet arrangements and it does not use hedges or other financial derivatives. The Company has no agreements or understandings with any person as to additional financing.

At December 31, 2009, we had cash of $52,609 (2008 - $29,247) and a working capital deficiency of $1,164,762 (2008 working capital deficiency - $1,151,940) respectively. Total liabilities as of December 31, 2009 were $2,424,619 as compared to $2,076,879 on December 31, 2008, an increase of $347,740.

In February 2009, 500,000 common shares were authorized for issuance at $0.20 per share for cash proceeds of $100,000. In March 2009, 1,000,000 common shares were authorized for issuance at $0.20 per share for cash proceeds of $200,000. In July 2009, 3,900,000 common shares were authorized for issuance at $0.30 per share for cash proceeds of $1,170,000. In January 2008 the Company issued 300,000 common shares valued at $114,000 as a finder’s fee in consideration for arranging property acquisitions in Kazakhstan. In June and October 2008 the Company issued 6,500,000 and 1,600,000 common shares respectively, the total amount received was $1,950,001 and $400,000, respectively.

Our general business strategy is to acquire mineral properties either directly or through the acquisition of operating entities. Our consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America and applicable to a going concern which contemplates the realization of assets and the satisfaction of liabilities and commitments in the normal course of business. As discussed in note 1 to the consolidated financial statements, the Company has incurred recurring operating losses since inception, has not generated any operating revenues to date and used cash of $765,617 from operating activities in 2009. The Company requires additional funds to meet its obligations and maintain its operations. We do not have sufficient working capital to (i) pay our administrative and general operating expenses through December 31, 2010 and (ii) to conduct our preliminary exploration programs. Without cash flow from operations, we may need to obtain additional funds (presumably through equity offerings and/or debt borrowing) in order, if warranted, to implement additional exploration programs on our properties. While we may attempt to generate additional working capital through the operation, development, sale or possible joint venture development of its properties, there is no assurance that any such activity will generate funds that will be available for operations. Failure to obtain such additional financing may result in a reduction of our interest in certain properties or an actual foreclosure of its interest. We have no agreements or understandings with any person as to such additional financing.

Our exploration properties have not commenced commercial production and we have no history of earnings or cash flow from its operations. While we may attempt to generate additional working capital through the operation, development, sale or possible joint venture development of its property, there is no assurance that any such activity will generate funds that will be available for operations.

Cash Flow

Operating activities: The Company used cash of $765,617 (used cash in 2008 - $3,115,799) through the year ended December 31, 2009. The following is a breakdown of cash used for operating activities: Depreciation and amortization of $20,909 (2008 - $19,707), expenses satisfied with issuance of common stock $0 (2008 - $114,000), impairment of mineral properties of $1,009,597 (2008 - $0), and realized loss on sale of equipment $0 (2008 - $12,342). Changes in prepaid expenses and other assets resulted in a decrease of $18,361 compared to an increase of $23,484 in 2008. There was a decrease in accounts payable and accrued liabilities of $160,866 compared to an increase of $173,036 in 2008. There was an increase in accounts payable to related party in 2009 of $132,276 compared to an increase of $71,250 in 2008. There was an increase in deposits in 2009 of $450,000 compared to an increase of $0 in 2008

Investing Activities: During the year ended December 31, 2009 investing activities consisted of expenditures on the purchase of assets of $660 (2008 - $89,714), proceeds from sale of equipment $0 (2008 - $35,717) and acquisition of mineral property costs of $0 (2008 - $400,000).

Financing Activities: We intend to finance our activities by raising capital through the equity markets. Proceeds from the sale of common stock were $1,020,000 (2008 - $2,800,001). In fiscal 2009 the Company repaid loans of $231,174 (2008 - $402,220).

Dividends

The Company has neither declared nor paid any dividends on its Common stock. The Company intends to retain its earnings to finance growth and expand its operations and does not anticipate paying any dividends on its Common shares in the foreseeable future.

Asset-Backed Commercial Paper

The Company has no asset-backed commercial paper.

Fair Value of Financial Instruments and Risks

Fair value estimates of financial instruments are made at a specific point in time, based on relevant information about financial markets and specific financial instruments. As these estimates are subjective in nature, involving uncertainties and matters of significant judgment, they cannot be determined with precision. Changes in assumptions can significantly affect estimated fair value.

The carrying value of cash, accounts payable and accrued expenses, accounts payable-related parties, and deposits approximate their fair value because of the short-term nature of these instruments. Available for sale securities are recorded at the current market value.

Management is of the opinion that the Company is not exposed to significant interest or credit risks arising from these financial instruments.

The Company operates outside of the United States of America (primarily in Kazakhstan) and is exposed to foreign currency risk due to the fluctuation between the currency in which the Company operates in and the U.S. dollar.

Share Capital

At September 17, 2010, the Company had:

|

◦

|

Authorized share capital of 100,000,000 common shares with par value of $0.0001 each.

|

|

◦

|

53,500,000 common shares were issued and outstanding as at September 17, 2010 (December 31, 2008 – 48,100,000).

|

Outlook

General Economic Conditions

Current problems in credit markets and deteriorating global economic conditions have lead to a significant weakening of exchange traded commodity prices in recent months, including precious and base metal prices. Volatility in these markets has also been unusually high. It is difficult in these conditions to forecast metal prices and demand trends for products that we would produce if we had current mining operations. Credit market conditions have also increased the cost of obtaining capital and limited the availability of funds. Accordingly, management is reviewing the effects of the current conditions on our business.

It is anticipated that for the foreseeable future, the Company will rely on the equity markets to meet its financing need. The Company will also consider entering into joint venture arrangements to advance its projects.

Capital and Exploration Expenditures

We are reviewing our capital and exploration spending in light of current market conditions. As a result of our review, the Company may curtail a portion of its capital and exploration expenditures during 2010/2011.

We are currently concentrating our exploration activities in Kazakhstan and examining data relating to the potential acquisition or joint venturing of additional mineral properties in either the exploration or development stage.

Off-Balance Sheet Arrangements

During the year ended December 31, 2009, the Company was not a party to any off-balance-sheet arrangements that have, or are reasonably likely to have, a material current or future effect on the results of operations, financial condition, revenues or expenses, liquidity, capital expenditures or capital resources of the Company.

Market Risk Disclosures

We have not entered into derivative contracts either to hedge existing risks or for speculative purposes.

Forward-Looking Statements

This annual report contains forward-looking statements which involve assumptions and describe our future plans, strategies, and expectations, are generally identifiable by use of the words “may,” “will,” “should,” “expect,” “anticipate,” “estimate,” “believe,” “intend,” or “project” or the negative of these words or other variations on these words or comparable terminology. These statements are expressed in good faith and based upon a reasonable basis when made, but there can be no assurance that these expectations will be achieved or accomplished.

Such forward-looking statements include statements regarding, among other things, (a) the potential markets for our technologies, our potential profitability, and cash flows (b) our growth strategies, (c) expectations from our ongoing sponsored research and development activities (d) anticipated trends in the technology industry, (e) our future financing plans and (f) our anticipated needs for working capital. This information may involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from the future results, performance, or achievements expressed or implied by any forward-looking statements. These statements may be found under “MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS” and “DESCRIPTIONS OF OUR BUSINESS AND PROPERTY,” as well as in this Form 10-K generally. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors, including, without limitation, the risks outlined under “RISK FACTORS” and matters described in this form 10-K generally. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this filing will in fact occur. In addition to the information expressly required to be included in this filing, we will provide such further material information, if any, as may be necessary to make the required statements, in light of the circumstances under which they are made, not misleading.

Although forward-looking statements in this report reflect the good faith judgment of our management, forward-looking statements are inherently subject to known and unknown risks, business, economic and other risks and uncertainties that may cause actual results to be materially different from those discussed in these forward-looking statements. Readers are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. We assume no obligation to update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this report, other than as may be required by applicable law or regulation. Readers are urged to carefully review and consider the various disclosures made by us in our reports filed with the Securities and Exchange Commission which attempt to advise interested parties of the risks and factors that may affect our business, financial condition, results of operation and cash flows. If one or more of these risks or uncertainties materialize, or if the underlying assumptions prove incorrect, our actual results may vary materially from those expected or projected. We will have little likelihood of long-term success unless we are able to continue to raise capital from the sale of our securities until, if ever, we generate positive cash flow from operations.

Plans for the Next Twelve Months

The following Plan of Operation contains forward-looking statements that involve risks and uncertainties, as described below. The Company’s actual results could differ materially from those anticipated in these forward-looking statements. The following discussion should be read in conjunction with the audited financial statements and notes thereto and the Plan of Operation included in this Annual Report on Form 10-K for the fiscal year ended December 31, 2009.

Our audited financial statements are stated in United States Dollars and are prepared in accordance with United States Generally Accepted Accounting Principles.

During the next 12 months we intend to raise additional funds through equity offerings and/or debt borrowing to meet our administrative/general operating expenses and to conduct work on our exploration properties. There is, of course, no assurance that we will be able to do so.

Our exploration properties have not commenced commercial production and we have no history of earnings or cash flow from its operations. While we may attempt to generate additional working capital through the operation, development, sale or possible joint venture development of its property, there is no assurance that any such activity will generate funds that will be available for operations.

On December 31, 2009, the Company entered into an Equity Purchase Agreement with Copperbelt AG, a Swiss corporation, for the sale of the Company’s 100% interest in its Kazakhstan subsidiary to Copperbelt AG for $1,500,000 and other consideration, the value of which has not been determined as of yet. The purchase price will be paid at the time of closing. The transaction is subject to the approval of the Company’s shareholders.

On March 9, 2010, the Company signed a property purchase agreement with Alphamin Resources Corp. (“Alphamin”) regarding the sale and transfer by Alphamin of a 100% interest in the Aurora mining concessions located in the State of Guerrero, Mexico to the Company, in consideration for $150,000 and 1,000,000 common shares of Cigma. Alphamin will retain a 1.5% Net Smelter Returns Royalty on production from the Property. On June 11, 2010 the Company’s wholly owned Mexican subsidiary, Exploraciones Cigma, S.A. de C.V., filed the Assignment Agreement for the Aurora II mining concession between Alphamin’s wholly owned Mexican subsidiary, Exploraciones La Plata, S.A. de C.V. and Exploraciones Cigma, S.A. de C.V. with the Mexican Public Registry of Mining.

We will concentrate our exploration activities on the Mexican property and examine data relating to the potential acquisition or joint venturing of additional mineral properties in either the exploration or development stage in Mexico and other South American countries. Additional employees will be hired on a consulting basis as required by the exploration properties.

|

(D)

|

Application of Critical Accounting Policies

|

The accounting policies and methods we utilize in the preparation of our consolidated financial statements determine how we report our financial condition and results of operations and may require our management to make estimates or rely on assumptions about matters that are inherently uncertain. Our accounting policies are described in note 2 of our December 31, 2009 Consolidated Financial Statements. Our accounting policies relating to mineral property and exploration costs and depreciation and amortization of property, plant and equipment are critical accounting policies that are subject to estimates and assumptions regarding future activities.

Depreciation is based on the estimated useful lives of the assets and is computed using the straight-line method. Equipment is recorded at cost. Depreciation is provided over the following useful lives: vehicles 10 years and machinery and equipment and other fixed assets, 2 to 10 years.

Exploration costs are charged to operations as incurred until such time that proven reserves are discovered. From that time forward, the Company will capitalize all costs to the extent that future cash flow from mineral reserves equals or exceeds the costs deferred. The deferred costs will be amortized over the recoverable reserves when a property reaches commercial production. As at December 31, 2009 and 2008, the Company did not have proven reserves.

Exploration activities conducted jointly with others are reflected at the Company's proportionate interest in such activities.

Costs related to site restoration programs are accrued over the life of the project.

US GAAP requires us to consider at the end of each accounting period whether or not there has been an impairment of the capitalized property, plant and equipment. This assessment is based on whether factors that may indicate the need for a write-down are present. If we determine there has been an impairment, then we would be required to write-down the recorded value of its property, plant and equipment costs which would reduce our earnings and net assets.

|

(E)

|

Related Party Transactions

|

Our proposed business raises potential conflicts of interests between certain of our officers and directors and us. Certain of our directors are directors of other mineral resource companies and, to the extent that such other companies may participate in ventures in which we may participate, our directors may have a conflict of interest in negotiating and concluding terms regarding the extent of such participation. In the event that such a conflict of interest arises at a meeting of our directors, a director who has such a conflict will abstain from voting for or against the approval of such participation or such terms. In appropriate cases, we will establish a special committee of independent directors to review a matter in which several directors, or management, may have a conflict. From time to time, several companies may participate in the acquisition, exploration and development of natural resource properties thereby allowing for their participation in larger programs, involvement in a greater number of programs and reduction of the financial exposure with respect to any one program. It may also occur that a particular company will assign all or a portion of its interest in a particular program to another of these companies due to the financial position of the company making the assignment.

In determining whether we will participate in a particular program and the interest therein to be acquired by it, the directors will primarily consider the potential benefits to us, the degree of risk to which we may be exposed and its financial position at that time. Other than as indicated, we have no other procedures or mechanisms to deal with conflicts of interest. We are not aware of the existence of any conflict of interest as described herein.

Other than as disclosed below, during the years ended December 31, 2009 and 2008, none of our current directors, officers or principal shareholders, nor any family member of the foregoing, nor, to the best of our information and belief, any of our former directors, senior officers or principal shareholders, nor any family member of such former directors, officers or principal shareholders, has or had any material interest, direct or indirect, in any transaction, or in any proposed transaction which has materially affected or will materially affect us.

There have been no transactions or proposed transactions with officers and directors during the last two years to which we are a party except as follows: