Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

Commission File No. 001-16501

Global Power Equipment Group Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 73-1541378 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

5199 N. Mingo Road

Tulsa, OK 74117

(Address of registrant’s principal executive offices and zip code)

Registrant’s telephone number, including area code: (918) 488-0828

Securities to be registered pursuant to Section 12(b) of the Act:

| Title of each class to be so registered |

Name of each exchange on which each class is to be registered | |

| Common Stock, par value $0.01 per share | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act. Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, as of the last business day of the registrant’s most recently completed second fiscal quarter was $250,575,185. For purpose of this calculation only, without determining whether the following are affiliates of the registrant, the registrant has assumed that (i) its directors and executive officers are affiliates; and (ii) no party who has filed a Schedule 13D or 13G is an affiliate.

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes x No ¨

The number of shares outstanding of the registrant’s Common Stock as of March 11, 2011 was 15,469,287.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for the registrant’s 2011 Annual Meeting of Stockholders are incorporated by reference into Part III of the Form 10-K to the extent stated herein. The Proxy Statement or an amended report on Form 10-K will be filed within 120 days of the registrant’s year ended December 31, 2010.

Table of Contents

Statements we make in this Form 10-K that express a belief, expectation or intention or otherwise are not limited to recounting historical facts are forward-looking statements. These forward-looking statements are subject to various risks, uncertainties and assumptions, including those noted under the headings “Cautionary Statement Regarding Forward Looking Statements” and “Risk Factors” in Items 1 and 1A of this Form 10-K.

3

Table of Contents

Cautionary Statement Regarding Forward-Looking Statements

This Form 10-K and its exhibits contain or incorporate by reference various forward-looking statements that express a belief, expectation or intention or are otherwise not statements of historical fact. Forward-looking statements generally use forward-looking words, such as “may,” “will,” “could,” “project,” “believe,” “anticipate,” “expect,” “estimate,” “continue,” “potential,” “plan,” “forecast” and other words that convey the uncertainty of future events or outcomes. Forward-looking statements include information concerning possible or assumed future results of our operations, including the following:

| • | business strategies; |

| • | operating and growth initiatives and opportunities; |

| • | competitive position; |

| • | market outlook and trends in our industry; |

| • | expected financial condition; |

| • | future cash flows; |

| • | financing plans; |

| • | expected results of operations; |

| • | future capital and other expenditures; |

| • | availability of raw materials and inventories; |

| • | plans and objectives of management; |

| • | future compliance with orders and agreements with regulatory agencies; |

| • | expected outcomes of legal or regulatory proceedings and their expected effects on our results of operations; and |

| • | any other statements regarding future growth, future cash needs, future operations, business plans and future financial results. |

These forward-looking statements represent our intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors, including unpredictable or unanticipated factors that we have not discussed in this Form 10-K. Many of those factors are outside of our control and could cause actual results to differ materially from the results expressed or implied by the forward-looking statements.

In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements might not occur or might occur to a different extent or at a different time than we have described. You should consider the areas of risk and uncertainty described above, as well as those discussed under “Item 1A–Risk Factors” in this Form 10-K. Except as may be required by applicable law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise and we caution you not to rely upon them unduly.

Overview

Global Power Equipment Group Inc. is a comprehensive provider of power generation equipment and maintenance services for customers in the domestic and international energy, power infrastructure and service industries. When we use the terms the “Company,” “we,” “us” or “our” in this Annual Report on Form 10-K, we mean Global Power Equipment Group Inc. and its subsidiaries on a consolidated basis, unless we state or the context implies otherwise.

We use the Braden Manufacturing, Consolidated Fabricators, Williams Industrial Services Group and Deltak trade names and the logos for each of those divisions and for Global Power Equipment Group. These trade names and logos are the property of Global Power Equipment Group Inc. or its subsidiaries. Product names and company programs appearing throughout in italics are trademarks of the Company or its subsidiaries. This Annual Report on Form 10-K also may refer to brand names, trademarks, service marks and trade names of other companies and organizations, and these brand names, trademarks, service marks and trade names are the property of their respective owners.

Unless we indicate otherwise, we base the information concerning our industry contained or incorporated by reference herein on our general knowledge of and expectations concerning the industry. Our market position, market share and industry market size are based on our estimates using our internal data and estimates, based on data from various industry analyses, our internal research and adjustments and assumptions that we believe to be reasonable. We have not independently verified data from industry analyses and cannot guarantee their accuracy or completeness. In addition, we believe that data regarding the industry, market size and our market position and market share within such industry provide general guidance but are inherently imprecise. Further, our estimates and assumptions involve risks and uncertainties and are subject to change based on various factors, including those discussed in the “Risk factors” section of this Annual Report on Form 10-K. These and other factors could cause results to differ materially from those expressed in the estimates and assumptions.

4

Table of Contents

Revenues for purposes of market size, market position and market share information are based on revenues in U.S. dollars.

We design, engineer and manufacture a comprehensive range of auxiliary and heat recovery equipment primarily used to enhance the efficiency and facilitate the operation of gas turbine power plants as well as for other industrial, energy and power-related applications. With a strong competitive position in our product lines, we benefit from a large installed base of equipment in domestic and international markets.

We provide on-site specialty maintenance and outage management services for nuclear power plants and specialty maintenance and other industrial services to fossil-fuel and hydroelectric power plants and other industrial operations in the United States. These services include a comprehensive range of industrial maintenance, modification and construction services for power generation, pulp and paper, chemical, refining, manufacturing and other industrial market segments. We have the capability to combine our services and equipment resources to offer turn-key solutions for aftermarket repair applications for the North American gas turbine power generation, process and cogeneration markets.

Through predecessor entities, we have over 41 years of experience providing custom engineered products that are critical for the operation of gas turbine power plants and more than 19 years of experience providing complex outage shutdown services to operators of nuclear power plants as well as other industrial maintenance services. Our current corporate structure dates to 2001 when we made our initial public offering and listed our stock on the New York Stock Exchange. We acquired our nuclear plant and other industrial services capabilities through a transaction completed in April 2005.

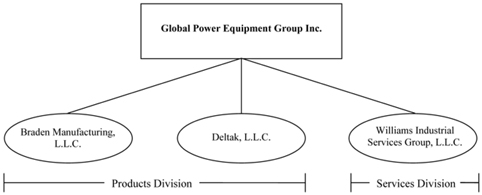

Corporate Structure Overview. The following chart shows the relationship between Global Power Equipment Group Inc., which is a Delaware corporation, and each of its three primary operating subsidiaries, each of which is a Delaware limited liability company.

Global Power Equipment Group Inc. and all of its U.S. subsidiaries filed voluntary Chapter 11 petitions under the United States Bankruptcy Code on September 28, 2006. We successfully exited Chapter 11 on January 22, 2008 pursuant to an approved Plan of Reorganization. For details regarding the events leading to, certain consequences of, and the terms of our emergence from bankruptcy, see the discussion below in Item 1 under the heading “Bankruptcy Reorganization.”

Business Segments

We operate through two business segments that we refer to as our Products Division and our Services Division. For information about our segments see Note 12 to our consolidated financial statements included in this Form 10-K.

Through our Products Division, we engineer, design and fabricate products worldwide for the gas turbine power generation, energy and process industries. We supply auxiliary power equipment and components under the Braden Manufacturing and Consolidated Fabricators brands and heat recovery equipment under the Deltak brand. A significant portion of our products revenue originates outside of the United States.

Through our Services Division, we provide industrial technical services under the Williams Industrial Services Group brand, focusing on specialty services, outage management and overhaul of power facilities and other heavy industrial plants. Virtually all of our services revenue is from operations conducted in the United States.

5

Table of Contents

Revenues by segment for 2010, 2009 and 2008 are as follows (in thousands):

| For the Years Ended December 31, | ||||||||||||||||||||||||

| 2010 | 2009 | 2008 | ||||||||||||||||||||||

| Products Division |

$ | 142,683 | 27 | % | $ | 193,150 | 36 | % | $ | 311,603 | 56 | % | ||||||||||||

| Services Division |

377,461 | 73 | % | 347,460 | 64 | % | 245,161 | 44 | % | |||||||||||||||

| $ | 520,144 | $ | 540,610 | $ | 556,764 | |||||||||||||||||||

Products Division

We manufacture and sell two primary product lines: auxiliary power equipment and heat recovery equipment. We sell our products to the gas turbine power generation, process and cogeneration market segments. Our principal customers are gas turbine original equipment manufacturers and engineering, procurement and construction contractors. We also provide replacement parts, filter elements and aftermarket retrofit equipment to both original equipment manufacturers and end users. Our products are critical to the efficient operation of gas turbine power plants and are custom engineered to meet customer-specific requirements.

The contracts under which we sell our products are generally fixed-price contracts, virtually all of which are “lump sum bid” contracts. Under lump sum bid contracts, we bid against other contractors based on relatively fixed customer specifications.

Auxiliary Power Equipment. We provide a comprehensive range of products critical to the operation of gas turbine power plants through our Braden Manufacturing subsidiary, headquartered in Tulsa, Oklahoma. Our auxiliary power equipment product offerings, which we market under the Braden and Consolidated Fabricators brand names, include:

| • | Filter Houses. A filter house cleans debris, dirt and other contaminants from the air that enters the turbine, using either a barrier filter or a pulse filter. Barrier filters use a series of filter elements contained in a large filter house to remove airborne contaminants. Pulse filters are self-cleaning filters that use blasts of air to expel dirt or ice from the filter element. In addition to a barrier or pulse filter, a filter house may include evaporative coolers, chiller coils, fog cooling systems, anti-icing systems and a broad range of other equipment to treat the air enters the turbine. |

| • | Inlet Systems. Inlet systems are large air intake ducts that connect the filter house to the gas turbine and provide silencing for the noise emanating from the gas turbine through the inlet. The major components of an inlet system are inlet silencers, expansion joints and inlet ductwork. |

| • | Exhaust Systems. Exhaust systems direct the hot exhaust from the turbine to the atmosphere. The main components of an exhaust system are exhaust ductwork, acoustic silencing equipment and the exhaust stack. Exhaust systems are custom engineered and complex due to the severe turbulence and heat exposure that they must endure. |

| • | Diverter Dampers. Diverter dampers divert the hot exhaust from the gas turbine into a heat recovery steam generator when the power plant is operated as a combined cycle facility or into the exhaust stack in the case of a simple cycle operation. We also design and manufacture various other types of dampers. |

| • | Selective Catalytic Emission Reduction Systems. These systems, commonly referred to as SCRs, are used in simple cycle gas turbine facilities and are focused on removing oxides of nitrogen and carbon monoxide from the exhaust gas. |

| • | Packaged Skids, Precision Parts and Specialty Fabrications. We engineer these products in our Auburn, Massachusetts plant and sell them under the Consolidated Fabricators brand. Packaged skids in various configurations support the operation of the gas turbine. Precision parts and specialty fabrications are used in both new gas turbine equipment and in aftermarket applications. |

Heat Recovery Equipment. We provide heat recovery steam generator, heat recovery system generators and specialty boilers and related products through our Deltak subsidiary, headquartered in Plymouth, Minnesota. We market these products under the Deltak brand name.

| • | Heat Recovery Steam Generators. A heat recovery steam generator (commonly referred to as an “HRSG”) is a boiler that creates steam in a combined cycle power plant or a cogeneration plant using the hot exhaust emitted by the gas turbine or other heat source. This steam is either used to drive a steam turbine to produce additional electricity in a combined cycle power plant or is used for process purposes in a cogeneration plant. Each HRSG is custom designed and engineered to meet the specifications of the customer, taking into account the type of gas turbine and the environmental locale, among other factors. We design and manufacture HRSGs for applications supporting turbines up to 85 megawatt capacity for both new combined cycle and retrofitted simple cycle power plants. We have an installed base of more than 300 mid-sized HRSGs in over 20 countries. |

| • | Specialty Boilers and Related Products. Specialty boilers are a highly customized class of equipment that capture waste heat and convert it to other working fluids or to create steam. We develop creative engineering solutions to produce specialty boilers used in process heat recovery and incineration systems, small power generation systems and marine cogeneration systems. Our specialty boilers are used in a wide range of markets, including oil and gas, pulp and paper, chemicals, petrochemical, marine and food industries. We have an installed base of more than 1,100 specialty boilers in over 30 countries. |

6

Table of Contents

Supply Chain Structure. We fabricate our equipment through a combination of in-house manufacturing at our own factories in the United States and Mexico and outsourced manufacturing in other countries around the world. Our network of high-quality international manufacturing partners, located in more than 20 countries, allows us to manufacture equipment worldwide and maintain a competitive cost structure. Outsourcing a portion of our manufacturing enables us to meet increasing demand without being restricted by internal manufacturing capacity limitations and also reduces our capital expenditure requirements. Our employees work closely with our international manufacturing partners to supervise the manufacture of our products at their facilities. Our use of manufacturing facilities around the world, whether our own or those of our manufacturing partners, allows us to respond to the particular sourcing initiatives of our customers, whether those initiatives call for global sourcing or for localized supply content.

Our technical engineering capabilities enable us to design and manufacture what we believe are among the broadest ranges of gas turbine power plant and other power-related equipment to meet each customer’s specific performance requirements. We provide products for gas turbine power plants to most of the leading power industry original equipment manufacturers and to a number of leading power generating companies and engineering, procurement and construction firms within the United States and abroad.

Gas Turbine Power Generation, Process and Cogeneration Market Overview. All gas turbine power plants combine a gas turbine with a generator to produce electricity. In a simple cycle gas turbine plant, the hot exhaust coming out of the gas turbine is vented to the atmosphere through an exhaust stack. In a combined cycle plant, the hot exhaust coming out of the gas turbine is fed into a heat recovery steam generator; the HRSG captures much of the heat from the gas turbine exhaust to generate steam, which in turn is used to power a steam turbine and generate more electricity before the exhaust is vented into the atmosphere. We manufacture products that are critical components of both simple cycle and combined cycle plants, including filter houses, inlet and exhaust systems and turbine and generator components. We also manufacture specialized diverter dampers that are used in combined cycle plants between the gas turbines and the HRSG.

We believe manufacturers of equipment and components supporting gas turbine power plants are well positioned to benefit from the need for new or more efficient power generation infrastructure. The advantages of power generation plants utilizing gas turbine technologies versus other technologies include:

| • | lower construction costs; |

| • | shorter construction periods; |

| • | improved operating efficiency; |

| • | lower emissions of CO2; |

| • | minimal other environmental impact; |

| • | flexibility to expand plant capacity; |

| • | smaller geographical footprint; and |

| • | rapid start-up and shutdown time. |

As a provider of equipment for simple and combined cycle gas turbine power plants, we expect to benefit from the growth of gas turbine power plant capacity that we expect to benefit from the factors listed above.

Services Division

Our Services Division, headquartered in Atlanta, Georgia, operates under the name Williams Industrial Services Group, L.L.C. (“Williams”). Through Williams, we provide routine and specialty maintenance services to a wide range of utilities and industrial customers, including nuclear, fossil-fuel and hydroelectric power plants and pulp and paper mills. Our service offerings include industrial painting and coating, removal of hazardous materials, industrial insulation, repair and replacement of roofing systems and nuclear, fossil fuel and hydroelectric power plant maintenance. The majority of these services are designed to improve or sustain operating efficiencies and extend the useful lives of process equipment in these facilities. In addition, these services provide our customers with a credible alternative to maintaining in-house maintenance capabilities. We provide maintenance services both on a constant presence basis and as a service provider for discrete projects. By providing high quality industrial services with exemplary safety performance, we have forged long-standing relationships with many leading utility companies.

We contract for approximately 85% of the services we provide on a cost-plus basis under contracts that provide for reimbursement of costs incurred plus an amount of profit in the form of a mark-up. We contract for the remaining approximately 15% of the services we provide on a fixed-price basis. In the case of lump sum bid contracts, we bid against other contractors based on customer specifications. Fixed-price contracts present certain inherent risks, including the possibility of ambiguities in the specifications received, problems with new technologies and economic and other changes that may occur over the contract period. Accordingly, fixed-price agreements are not our preferred form of contract. However, because of efficiencies that may be realized during the contract term, fixed-price contracts may offer greater profit potential than other types of contracts.

7

Table of Contents

Service offerings include the following:

| • | Nuclear Power Plant Maintenance. We perform a full range of critical services for the nuclear facility market, including routine maintenance and modification work performed during outages, decommissioning services, cooling tower and steam generator replacement support and vessel and heat exchanger replacements. We are one of a limited number of companies qualified to perform comprehensive services in United States nuclear power plants under rules issued by the U.S. Nuclear Regulatory Commission (“NRC”). Under these rules, owners of nuclear facilities must qualify contractors by requiring the contractors to demonstrate that they will comply with NRC regulations on quality assurance, reporting of safety issues, security and control of personnel access and conduct. |

| • | Fossil Fuel and Hydroelectric Power Plant Maintenance. We provide routine maintenance, repair and capital project services primarily in coal-fired, gas-fired and hydroelectric power plants, often managing hundreds of craft employees. Services provided include electrical and mechanical maintenance, outage support, turnarounds, welding, scaffolding, staff augmentation, grounds maintenance and janitorial and custodial services. |

| • | Industrial Painting and Coatings. We perform cleaning, surface preparation, coatings application, quality control and inspection testing, utilizing Williams Insight™, our proprietary analysis system, to help our customers schedule and prioritize major coating projects based on a detailed cost/benefit analysis. Coatings applied in industrial environments are typically designed for specific applications. To satisfy these exacting requirements, many of these coatings involve multiple component mixes, require specialized application equipment and are strictly monitored and tested. |

| • | Insulation. We provide a variety of industrial insulation services, primarily in process-piping installations. These services are commonly packaged with industrial coating projects. |

| • | Roofing Systems. We routinely replace, repair and upgrade industrial facility roofing systems, primarily within the highly corrosive environments of pulp and paper manufacturing facilities. Our proprietary Pro-Tec™ Panel system allows our employees to safely work above operational equipment on roofing projects while containing all refuse materials. This allows us to rehabilitate or completely replace the roof of an industrial facility without interrupting production. |

| • | Abatement. We provide two primary abatement services for the removal of hazardous materials: removal of asbestos and removal of heavy metal based coatings such as lead paint. These services involve the demolition of the contaminated area, the collection and containment of hazardous material and arrangements for their disposal or storage. We do not take ownership of hazardous materials and do not assume responsibility for the liability associated with the materials other than for our actions meeting applicable statutory and regulatory requirements. |

| • | Valve Services. We provide integrated valve and actuator services to our customer base. These services include inspection, preventative maintenance and repair of various types of valves and actuators. We offer a broad spectrum of valve services for diagnostic testing and analysis, project management, training and engineering. |

Industrial Services Industry and Market Overview. Industrial services in the U.S. is a multi-billion dollar industry broadly defined as routine maintenance and technical services provided to industrial facilities ranging from manufacturing facilities to power generation plants. The industry is currently experiencing a shift towards outsourcing as plant operators seek to alleviate financial constraints, reduce labor costs, increase labor utilization and productivity and eliminate operational redundancies.

We expect that power industry demand for industrial maintenance services will be driven by the following factors in the future:

| • | Aging Infrastructure. According to the U.S. Department of Energy’s Energy Information Administration, more than half of the electrical generating capacity in the United States was placed in service before 1980. Coupled with the limited number of large-scale power generation facilities being constructed, the efforts to maintain older plants of all types and take advantage of newer and more efficient technologies at existing sites have created opportunities for companies providing maintenance and modification services. |

| • | Increasing Demand for Nuclear Plant Maintenance. The United States has 104 operating nuclear reactors that generate approximately 20% of annual electric production. These nuclear reactors have been in operation for an average of 30 years and require extensive ongoing engineering and maintenance services to support operations and improve performance. Nuclear power plants in the United States are subject to a rigorous program of NRC oversight, inspection, preventive and corrective maintenance, equipment replacement and equipment testing. Nuclear power plants are required by the NRC to go offline to refuel at intervals of no more than 24 months and to perform condition monitoring and preventive maintenance during every refueling outage. NRC regulations also require that nuclear generating facilities be decommissioned, or returned to “greenfield” status, at the end of their operating lives. Initially, commercial nuclear power plants in the United States were licensed to operate for 40 years, reflecting the amortization period generally used by electric utility companies for large capital investments. In 2000, the NRC issued the first license renewal to a nuclear power plant, extending its license for an additional 20 years beyond its original 40-year license. The NRC has since issued 20-year license extensions for numerous reactors and is reviewing license renewal applications for others. We expect the extended operating licenses of nuclear power plants will also increase the maintenance requirements of these facilities. |

8

Table of Contents

| • | New Nuclear Plant Construction. We expect new nuclear plants to be constructed over the next 10 years. In February 2010, the federal government announced loan guarantees for the construction of the first new nuclear unit at Southern Nuclear Operating Company’s Vogtle Nuclear Plant near Waynesboro, Georgia. We believe we are well positioned to participate in new plant construction opportunities, through our Williams Services Division. The types of services we provide are generally required in the later stages of the construction process and they are frequently subcontracted by new build contractors. |

Customers and Marketing

Products. Our Products customers include original equipment manufacturers (“OEM”), engineering procurement and construction firms, utilities and independent operators of power generation facilities and firms engaged across several process related industries. The end users of most of our products are owners and operators of gas turbine power plants, process plants and refineries. We market our products globally through a sales network consisting of employees and independent representatives. We have employed sales representatives in China, Egypt, the Netherlands and the United States. Our sales teams travel extensively and work with our local manufacturing partners to assess local market conditions, utilize local contacts and respond quickly to our customers’ needs. We focus our sales and marketing efforts on end users of our products, including the developers and operators of gas turbine power plants, and on gas turbine original equipment manufacturers, which may order our products directly or specify the use of our products.

Services. Our Services customers include major private and government owned utilities throughout the United States as well as leaders in the United States paper and industrial sectors. We market our services using dedicated sales and marketing personnel, operations personnel, and external consultants retained for specific projects. We use specific services sales initiatives to emphasize long-term renewable contracts that are augmented by small to medium sized, fixed-price projects. Our services sales initiatives directly seek to apply operational strengths to specific facilities within the targeted markets, including nuclear power, pulp and paper and other industrial plants located throughout the United States.

Revenues by Customer and Geographic Region. Our top customers vary from year-to-year depending on the relative size and duration of our projects over time. Customers that accounted for more than 10% of our consolidated revenues in 2010, 2009 and 2008 were:

| For the Years Ended December 31, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| Entergy Services Inc. |

24 | % | 11 | % | * | |||||||

| Southern Company |

23 | % | 12 | % | 10 | % | ||||||

| General Electric Company |

* | 13 | % | 20 | % | |||||||

| Tennessee Valley Authority |

* | 11 | % | * | ||||||||

| * | Less than 10% |

Our revenues from each of the customers listed in the above table are derived from multiple purchase orders or contracts that are entered into, performed, and terminate independently of each other.

Our Products revenues by geographic regions for the years 2010, 2009 and 2008 are shown in the following table both on the basis of revenue recognition and on the basis of shipment destination (in thousands):

| Years ended December 31, | ||||||||||||||||||||||||

| 2010 | 2009 | 2008 | ||||||||||||||||||||||

| Revenue Recognized In |

Product Shipped To |

Revenue Recognized In |

Product Shipped To |

Revenue Recognized In |

Product Shipped To |

|||||||||||||||||||

| United States |

$ | 99,063 | $ | 52,764 | $ | 139,138 | $ | 66,320 | $ | 212,914 | $ | 105,301 | ||||||||||||

| Canada |

— | 9,585 | — | 11 | — | 22,050 | ||||||||||||||||||

| Europe |

32,009 | 11,668 | 38,471 | 31,345 | 80,792 | 20,704 | ||||||||||||||||||

| Mexico |

7,522 | 744 | 10,518 | 364 | 16,350 | 116 | ||||||||||||||||||

| Asia |

4,089 | 26,236 | 5,023 | 26,113 | 1,547 | 17,999 | ||||||||||||||||||

| Middle East |

— | 22,891 | — | 63,681 | — | 112,374 | ||||||||||||||||||

| Other |

— | 18,795 | — | 5,316 | — | 33,059 | ||||||||||||||||||

| Total |

$ | 142,683 | $ | 142,683 | $ | 193,150 | $ | 193,150 | $ | 311,603 | $ | 311,603 | ||||||||||||

Our Services revenues, virtually all of which are derived in the United States, were $377.5 million for 2010, $347.5 million for 2009 and $245.2 million for 2008.

Backlog

Our backlog consists of firm orders or blanket authorizations from our customers. Backlog may vary significantly reporting period to reporting period due to the timing of customer commitments. The time between receipt of an order and actual completion and delivery of our products varies from a few weeks, in the case of inventoried precision parts, to a year or more, in the case of custom-designed filter houses and other major plant components. We add a booking to our backlog for products when we receive an order accompanied by a written commitment from a customer. The maintenance services we provide through Williams are typically carried out under

9

Table of Contents

long-term contracts spanning several years. Upon signing a multi-year contract with a customer for services, we add to our backlog only the first twelve months of work that we expect to perform under the contract. Additional work that is not called for under the original contract is added to our backlog when we reach agreement with the customer as to the scope and pricing of that additional work. Capital project awards are typically defined in terms of scope and pricing at the time of contractual commitment from the customer. Upon receipt of a customer confirmation, capital project bookings are added to our backlog at the full contract value regardless of the time frame anticipated to complete the project.

The following table shows our backlog amounts, by segment, as of the end of each of the last three years (in thousands):

| Backlog as of December 31, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| Products |

$ | 119,420 | $ | 120,760 | $ | 168,904 | ||||||

| Services |

229,913 | 194,162 | 163,906 | |||||||||

| Total |

$ | 349,333 | $ | 314,922 | $ | 332,810 | ||||||

Approximately 24% of the December 31, 2010 backlog is comprised of orders from the major customers shown in the table included above under “Customers and Marketing.” Based on production and delivery schedules, we anticipate that of our December 31, 2010 backlog, approximately 96% of the Products backlog and 87% of the Services backlog will be recognized as revenues during 2011.

Backlog is not a measure defined by generally accepted accounting principles, and our methodology for determining backlog may vary from the methodology used by other companies in determining their backlog amounts. Backlog may not be indicative of future operating results and projects in our backlog may be cancelled, modified or otherwise altered by our customers.

Engineering, Design and Maintenance Capabilities

Products. We believe the design and engineering expertise of our Products Division makes us an industry leader in the field of power generation equipment. We provide original design, retrofit and upgrade engineering and after-sales maintenance and repair of our products. Our products are custom-designed and engineered to meet the specifications of our customers. Our extensive engineering experience and proprietary designs from completed projects enhance our ability to efficiently satisfy our customers’ needs on projects that require significant engineering. As of December 31, 2010, we employed 64 degreed engineers specializing in thermal, structural, electrical/controls, mechanical, acoustical, industrial and chemical engineering and other technical areas. Our engineers and designers use a PC-based network and engineering and drafting programs such as AutoCAD™, ANSYS™, STAAD™, Solidworks™ and several internally developed proprietary programs.

Services. We provide extensive training, certifications and ongoing safety monitoring to all of our maintenance employees. For over ten years, we have maintained a safety record above the industry average, benefitting both us and our customers. We maintain a broad range of professional certifications relevant to the performance of many of the specialized services we provide. We maintain memberships and selected certifications with organizations such as the National Association of Corrosion Engineers, the Society of Protective Coatings, the American Nuclear Society, the American Society of Mechanical Engineers, the National Board of Boiler & Pressure Vessel Inspectors, the American National Standard Institutes, the American Society for Nondestructive Testing, the American Welding Society, Institute of Nuclear Power Operations and other organizations. We are one of a limited number of companies qualified to work anywhere in a United States nuclear facility and have been one of the leading providers of coatings at United States nuclear facilities for more than 35 years.

Manufacturing, Outsourcing and Contract Labor

Products. We fabricate our products using a combination of in-house manufacturing and third-party subcontractors. Most of our subcontracting work is performed outside the United States. Our network of outsourcing relationships provides us the following benefits:

| • | the flexibility to rapidly expand or contract our manufacturing capacity, with minimal impact on our capital expenditure requirements and fixed expenses; |

| • | the ability to manufacture in low-cost countries, thereby reducing the overall cost of our products; and |

| • | the ability to satisfy local content requirements. |

Subcontractors account for a significant percentage of our manufacturing costs. We provide on-site technical advisors at our subcontracted facilities to ensure high levels of quality and workmanship. While we generally have proven long-term relationships with our subcontractors, we also routinely search for additional fabricators to enhance our ability to manufacture equipment at the lowest cost while maintaining high-quality standards and on-time delivery.

Services. We provide maintenance services throughout the United States with experienced, temporary craft labor and leased equipment, directed and supervised by an experienced team of project managers across our network. Our flexible staffing and equipment model enables us to meet seasonal and outage demand without being restricted by internal capacity limitations, thus minimizing our fixed cost requirements.

10

Table of Contents

Materials and Suppliers

The principal materials for our products are carbon steel plate, stainless steel products and other structural shapes, insulation and finned tubing. We obtain these products from a number of domestic and foreign suppliers. The markets for most of the materials we use are served by a large number of suppliers and we believe that we can obtain each of the materials we require from more than one supplier.

Competition

Products. We compete with a large number of U.S. and international companies along all of our major product lines. We compete based on the price, quality, reliability and reputation of our products and our ability to engineer and design products to meet each customer’s unique specifications. Our competitors, some of which are significantly larger than we are and have significantly greater financial resources than we do, vary with respect to each product category we offer. We believe that no single competitor offers our breadth of products to the gas turbine power generation, process and cogeneration industries.

Services. The barriers to entry in industrial services are both financially and logistically low with the result that the industry is highly fragmented with no single company being dominant. Our competitors vary depending on plant geography and scope of services to be rendered. Several national vendors, which are significantly larger than we are and have significantly greater financial resources than we do, will often compete for larger maintenance and specialty opportunities that become available. Additional smaller vendors that operate on a regional basis will often compete for smaller opportunities associated with open shop labor sources. The key competitive factors in industrial services are reputation, safety record, price, service, quality, breadth of service capabilities and the ability to identify and retain qualified personnel. We believe our project management capabilities, service diversity, long-term customer relationships and safety standards differentiate us from our competitors. We also believe that the fact that we maintain a constant presence at many of our customers’ sites is a key competitive advantage because it provides us with an intimate understanding of these facilities and thereby allows us to better identify our customers’ service needs.

Employees

We had 687 full and part time employees as of December 31, 2010. Of these, 107 were employed at our facility in Mexico under a collective bargaining agreement. We regularly hire unionized craft labor on a temporary basis in the operation of our Services Division, often deploying hundreds of employees simultaneously at a single site for intensive outage work. We believe that our relationships with our employees, both permanent and temporary, are satisfactory.

Intellectual Property

We use a variety of patents, trademarks and proprietary technologies in the ordinary course of business in both our Products and Services Divisions. We rely upon patents, nondisclosure and confidentiality agreements with our employees, subcontractors, customers and others, and on various other security measures to protect our proprietary rights. Our patents related to heat exchangers generally expire in 2011; our patents related to exhaust systems generally expire in 2016; and a patent relating to a filter element clipper expires in 2027. We do not believe that any single patent or proprietary technology is material to our business and we do not believe our competitive position would be materially affected by competitors also using similar technologies and systems.

Compliance with Government Regulations

We are subject to certain federal, state and local environmental, occupational health, nuclear regulatory, export and product safety laws applicable in the countries in which we operate. We also purchase materials and equipment from third-parties, and engage subcontractors, who are also subject to these laws and regulations.

Environmental. We are subject to extensive and changing environmental laws and regulations in the United States and in foreign jurisdictions where we do business. These laws and regulations relate primarily to air and water pollutants and the management and disposal of hazardous materials. We are exposed to potential liability for personal injury or property damage caused by any release, spill, exposure or other accident involving such pollutants, substances or hazardous materials.

Health and Safety Regulations. We are subject to the requirements of the United States Occupational Safety and Health Act (OSHA) and comparable state and foreign laws. Regulations promulgated by these agencies require employers and independent contractors who perform construction services, including electrical and repair and maintenance, to implement work practices, medical surveillance systems and personnel protection programs in order to protect employees from workplace hazards and exposure to hazardous chemicals and materials. In recognition of the potential for accidents within various scopes of work, these agencies have enacted very strict and comprehensive safety regulations.

Nuclear Regulatory Commission. Owners of nuclear power plants are licensed to build, operate, and maintain those plants by the NRC. Their license requires that they qualify their suppliers and contractors to ensure that the suppliers and contractors comply with NRC regulations. Our Services Division must demonstrate to its customers that we will comply with NRC regulations related to quality assurance, reporting of safety issues, security and control of personnel access and conduct.

Export Laws. To the extent we export technical services, data and products outside of the United States, we are subject to U.S. and international laws and regulations governing international trade and exports including but not limited to the Export Administration Regulations and trade sanctions against embargoed countries, which are administered by the Office of Foreign Assets Control within

11

Table of Contents

the U.S. Department of the Treasury. A failure to comply with these laws and regulations could result in civil or criminal sanctions, including the imposition of fines, the denial of export privileges and suspension or debarment from participation in U.S. government contracts.

While we believe that we operate safely and prudently and in material compliance with all environmental, occupational health, nuclear regulatory, export and product safety laws, there can be no assurance that accidents will not occur or that we will not incur substantial liability in connection with the operation of our business. However, we believe that all our operations are in material compliance with those laws and we do not anticipate any material capital expenditures or material adverse effect on earnings or cash flows as a result of complying with those laws.

Available Information

We file reports with the SEC, including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished to the SEC pursuant to the requirements of the Securities Exchange Act of 1934. The general public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room located at 100 F Street N.E., Washington, DC 20549. The public may also obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site, www.sec.gov, which contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

You may also obtain copies of our annual reports at our website at www.globalpower.com under the heading “Investor Information”. The information disclosed on our website is not incorporated by this reference and is not a part of this Form 10-K. We will make available on our website, free of charge, all of our future periodic filings with the Securities and Exchange Commission (the “SEC”), including our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to these reports, as soon as reasonably practicable after we electronically file with or furnish the reports to the SEC.

Bankruptcy Reorganization

Global Power Equipment Group Inc. and all of its U.S. subsidiaries filed voluntary petitions for relief under Chapter 11 of the U. S. Bankruptcy Code in the United States Bankruptcy Court for the District of Delaware on September 28, 2006. The bankruptcy stemmed principally from losses attributable to our large-scale HRSG product line within our Deltak L.L.C. (“Deltak”) subsidiary and associated financial reporting deficiencies. During the pendency of our bankruptcy case, we discontinued this product line, terminating personnel and divesting a foreign subsidiary that had been dedicated to that product line. We continue to serve the mid-sized HRSG segment with products that complement power generation turbines up to 85 megawatt capacity.

We successfully emerged from bankruptcy pursuant to an approved Plan of Reorganization on January 22, 2008. That plan provided for payment in full of allowed claims of all creditors other than unsecured creditors of Deltak. Those unsecured creditors are expected to share in recoveries through a $34 million fund established to satisfy allowed unsecured claims against Deltak. Upon our emergence from bankruptcy, our pre-petition equity holders received one share of our new common stock for each share of common stock held before the bankruptcy and a right to purchase additional shares of our new common stock on a pro-rata basis pursuant to a rights offering that commenced on November 6, 2007 and expired on December 13, 2007. Upon emergence from bankruptcy on January 22, 2008, we issued 5,266,885 shares of our new common stock to pre-petition equity holders in exchange for stock held before the bankruptcy. On that same date, pursuant to the rights offering, a related backstop private placement, and our Management Incentive Co-Investment Plan, we issued an additional 9,589,138 shares of our new common stock in exchange for $72.5 million in new capital. The applicable price of our common stock in the rights offering was $7.65 per share. As part of the plan, we also entered into a $150 million exit financing package comprised of a $90 million term loan and a $60 million revolver facility. (All of the share and per share numbers in this Form 10-K reflect the effect of the 1-for-9 reverse stock split of all of our outstanding shares of common stock that was effective June 30, 2010.)

Executive Officers of the Registrant

The following sets forth information regarding our current executive officers. Executive officers are appointed by, and hold office at the discretion of, our Board of Directors, subject to the terms of any employment agreements.

| Name | Position | |

| David L. Keller | President, Chief Executive Officer and Director | |

| David L. Willis | Senior Vice President and Chief Financial Officer | |

| Tracy D. Pagliara | General Counsel, Secretary, and Vice President of Business Development | |

| Dean J. Glover | Senior Vice President, President of Products Division | |

| Kenneth W. Robuck | Senior Vice President, President of Services Division | |

| Gene F. Schockemoehl | Senior Vice President and President of Braden Manufacturing, LLC | |

David L. Keller, 56, has served as our President and Chief Executive Officer and as a Director since September 2009. Mr. Keller served as the President and Chief Operating Officer of B&W, a wholly owned subsidiary of McDermott International, Inc., from March 2001 until his retirement in June 2007. B&W, a company with approximately $2 billion in revenues in 2006, supplies fossil-fuel

12

Table of Contents

fired boilers, commercial nuclear steam generators, environmental equipment and components, and boiler auxiliary equipment and provides related services, including construction services. Mr. Keller’s prior position was President of Diamond Power International, Inc., a wholly owned subsidiary of B&W, from March 1998 to February 2001. During his tenure with B&W, Mr. Keller served as a Board Chairman or Director of subsidiaries and joint ventures in the Peoples Republic of China, Denmark, the United Kingdom, Australia and South Africa.

He holds a Bachelor of Science degree in Mathematics from the University of Akron.

David L. Willis, 39, has been our Senior Vice President and Chief Financial Officer since January 2008. Mr. Willis has a broad range of leadership experience across a range of industries: restructuring advisory services, telecommunications, energy companies and public accounting. From October 2001 to January 2008, he was with the restructuring practice of Alvarez & Marsal LLC, a global professional services firm, where he served clients in advisory and interim management capacities, most recently as Senior Director, overseeing the development and implementation of initiatives to improve operational and financial performance.

Prior to Alvarez & Marsal, Mr. Willis held positions with The Williams Communications Group and Ernst & Young. Mr. Willis received his Bachelor of Business Administration degree from the Price College of Business at the University of Oklahoma and holds an M.B.A. from the University of Tulsa. He is a Certified Public Accountant and has a Certified Insolvency and Restructuring Advisor certification (inactive).

Tracy D. Pagliara, 48, has served as our General Counsel, Secretary, and Vice President of Business Development since April 2010. Prior to joining our company, Mr. Pagliara served as the Chief Legal Officer of Gardner Denver, Inc., a leading global manufacturer of highly engineered compressors, blowers, pumps and other fluid transfer equipment, from August 2000 through August 2008. He also had responsibility for other roles during his tenure with Gardner Denver, including Vice President of Administration, Chief Compliance Officer, and Corporate Secretary.

Prior to joining Gardner Denver, Mr. Pagliara held positions of increasing responsibility in the legal departments of Verizon Communications/GTE Corporation from August 1996 to August 2000 and Kellwood Company from May 1993 to August 1996, ultimately serving in the role of Assistant General Counsel for each company. Mr. Pagliara has a B.S. in Accounting and a J.D. from the University of Illinois. He is a member of the Missouri and Illinois State Bars and a Certified Public Accountant.

Dean J. Glover, 44, is Senior Vice President and President of the Products Division of Global Power Equipment Group Inc. Mr. Glover joined Braden Manufacturing in December 2005 as Chief Operating Officer and was promoted to his positions at Global Power and Deltak in September 2008. Mr. Glover has extensive international experience having lived in various international locations for most of his career. Mr. Glover has over 18 years of commercial and technical experience in the power industry. Prior to joining Global Power, Mr. Glover led the global supply chain, including manufacturing for Diebold Inc. Prior to this, Mr. Glover spent 13 years with General Electric in various managerial and technical roles and is a certified Six Sigma Master Blackbelt. Mr. Glover holds a Bachelors Degree in Mechanical Engineering from the University of Nebraska and an M.B.A. from the Kellogg Graduate School of Management, Northwestern University.

Kenneth W. Robuck, 51, is Senior Vice President and President of the Services Division of Global Power Equipment Group Inc. Mr. Robuck originally joined the Williams Group in 1995; he left the company for a brief period and returned in 2005 to run Williams Plant Services, LLC, the largest of the Williams’ subsidiaries, which is responsible for all major maintenance and construction services work. In early 2006, Mr. Robuck assumed the additional responsibility of Chief Operating Officer and was appointed President of the Williams Group in October 2007. Mr. Robuck has over 27 years experience in the nuclear power, fossil-fuel power, petrochemical and related industrial industries. Mr. Robuck is a graduate of Auburn University with a B.S. in Civil Engineering.

Gene F. Schockemoehl, 61, is Senior Vice President of Global Power Equipment Group Inc., and President of our subsidiary Braden Manufacturing, LLC. Mr. Schockemoehl has served as President of Braden since January 1994 and as Vice President of Global Power since June 1998. He was named President of Consolidated Fabricators Inc. in October 2003.

Mr. Schockemoehl began his employment at Braden in September 1968, progressing through the plant production area into management positions, and became Vice President of Operations in 1990. He served as Vice President of Sales from 1991 until his appointment as President in January 1994. Mr. Schockemoehl has a manufacturing and general business education background, having attended both Tulsa Community College and Rogers State College.

Our business, financial condition and results of operations may be impacted by one or more of the following factors, any of which could cause actual results to vary materially from historical and current results or anticipated future results.

Risk Factors Related to Our Operations

If the United States were to change its support of nuclear power, it could have a material adverse effect on our operations.

The U.S. government has been supportive of increased investment in nuclear power. However, if the federal government changed its policy or if public acceptance of nuclear technology declines, demand for nuclear power could be negatively affected and potentially increase the regulation of the nuclear power industry. It is unclear whether recent events in Japan regarding certain nuclear power plants will influence U.S. policy or public acceptance of commercial nuclear technology. Reduced demand for nuclear power or increased regulation would adversely affect our clients, which in turn could have a material adverse effect on our revenues.

13

Table of Contents

If our costs exceed the estimates we use to set the fixed-prices of our contracts, our earnings will be reduced.

Nearly all of our power generation equipment sales contracts are entered into on a fixed-price basis. As a result, our Products Division has a limited ability to recover any cost overruns. Contract prices are established based in part on our projected costs, which are subject to a number of assumptions. The costs that we incur in connection with each contract can vary, sometimes substantially, from our original projections. Because of the large scale and long duration of our contracts, unanticipated changes may occur, such as customer budget decisions, design changes, delays in receiving permits and cost increases, as well as delays in delivery of our products. We often are contractually subject to liquidated damages for late delivery. Unanticipated cost increases or delays may occur as a result of several factors, including:

| • | increases in the cost of commodities (primarily steel plate), labor or freight; |

| • | unanticipated technical problems (for example, difficulties in designing products that integrate well with new generations of gas turbines); |

| • | suppliers’ or subcontractors’ failure to perform (for example, substandard welding by a subcontractor), requiring modified execution plans or re-work. |

Cost increases or overruns that we cannot pass on to our customers or our payment of liquidated damages under our contracts will lower our earnings. Increases in commodity prices may adversely affect our gross margins.

If we are unable to control the quality or timely production of products manufactured or services provided by our subcontractors, our reputation could be adversely affected and we could lose customers. If we are unable to recover any advance progress payments made to subcontractors, our profitability would be adversely affected.

We rely on subcontractors to manufacture and assemble a substantial portion of our products as well as provide some specialty services. Subcontractors account for a significant percentage of our manufacturing costs. The quality and timing of production by our subcontractors is not totally under our control. Our subcontractors may not always meet the level of quality control and the delivery schedules required by our customers. The failure of our subcontractors to produce quality products in a timely manner could adversely affect our reputation and result in the cancellation of orders for our products, significant warranty and repair costs and the loss of customers. Alternatively, we could be required to move subcontract manufacturing to other locations, resulting in increased costs.

In addition, we make advance progress payments to subcontractors in anticipation of their completion of our orders. We may be unable to recover those advances if a subcontractor fails to complete an order, which may adversely affect our profitability.

Competition could result in decreased sales or decreased prices for our products and services.

We face, and will continue to face, significant competition for the sale of our products and services. Competition could result in a reduction in the demand for, or the prices that we can charge for, our products and services. Our success is dependent in large part on our ability to:

| • | anticipate or respond quickly to our customers’ needs and enhance and upgrade our existing products and services to meet those needs; |

| • | continue to price our products and services competitively and find low-cost subcontractors that can produce quality products; and |

| • | develop new products and services that are accepted by our customers and differentiated from our competitors’ offerings. |

Our competitors may:

| • | develop more desirable, efficient, environmentally friendly or less expensive products; |

| • | be willing to accept lower prices to protect strategic market positions or increase market share; |

| • | be better able to take advantage of acquisition opportunities; or |

| • | adapt more quickly to changes in customer requirements. |

During times of economic decline, when demand for our products decreases, our competitors may be willing to accept lower prices in order to absorb their fixed costs. As a result, we may need to lower our prices and/or devote significant resources to marketing our products in order to remain competitive. Lower prices and/or higher costs would reduce our revenues and our profitability.

Our future revenues and operating results may vary significantly from reporting period to reporting period.

Our quarterly and annual revenues and earnings have varied in the past and are likely to vary in the future. Our power generation equipment sales contracts stipulate customer-specific delivery terms that, coupled with other factors beyond our control, may result in uneven recognition of revenues and earnings over time. Customer-imposed delays can significantly impact the timing of revenue recognition. Due to our relatively large average contract size, our power generation equipment sales volume during any given period may be concentrated in relatively few orders, intensifying the magnitude of these fluctuations. Furthermore, some of our operating

14

Table of Contents

costs are fixed. As a result, we may have limited ability to reduce our operating costs in response to unanticipated decreases in our revenues or the demand for our products in any given reporting period. Therefore, our operating results in any reporting period may not be indicative of our future performance. Because we must make significant estimates related to potential costs when we recognize revenue on a percentage-of-completion basis, these costs may change significantly from reporting period to reporting period based on new project information. For example, if labor efficiency experienced on a project is lower than we estimated at the outset of the project, the costs incurred on the project will increase and the percentage of completion may be reduced from earlier estimates. In addition, most of our power generation equipment revenues are based on fixed-price contracts, and the relative profitability can vary significantly between contracts. As a result, our profitability can vary from reporting period to reporting period based on the specific contracts being recognized.

We may not be able to maintain or expand our business outside the United States because of numerous factors outside our control.

Our international operations are subject to a number of risks inherent in doing business outside the United States including:

| • | labor unrest; |

| • | regional economic uncertainty; |

| • | political instability; |

| • | restrictions on the transfer of funds into or out of a country; |

| • | currency exchange rate fluctuations; |

| • | export duties and quotas; |

| • | expropriations; |

| • | domestic and foreign customs and tariffs; |

| • | current and changing regulatory environments; |

| • | potentially adverse tax consequences; |

| • | availability of financing; |

| • | unfavorable commercial terms and conditions; and |

| • | potential for adverse dispute resolution outcomes. |

These factors may result in a decline in revenues or profitability and could adversely affect our ability to maintain or expand our business outside the United States.

We conduct our manufacturing and distribution operations on a worldwide basis and are subject to risks associated with doing business outside the United States.

We have manufacturing and distribution facilities and subcontractors in many countries outside of the United States including China, Poland, Romania and Mexico, and increasing our manufacturing footprint in low cost countries is an important element of our strategy. There are a number of risks associated with doing business internationally, including (a) exposure to local economic and political conditions, (b) social unrest such as risks of terrorism or other hostilities, (c) currency exchange rate fluctuations and currency controls, (d) export and import restrictions, and (e) the potential for shortages of trained labor. In particular, there has been social unrest in Mexico and any increased violence in or around our manufacturing facilities in Mexico could impact our business by disrupting our supply chain, and the delivery of products to customers. In addition, the increased violence in or around our manufacturing facilities in Mexico could present several risks to our employees who may be directly affected by the violence and may result in a decision by them to relocate from the area, or make it difficult for us to recruit or retain talented employees at our Mexican facilities. The likelihood of such occurrences and their potential effect on us is unpredictable and vary from country to country. Any such occurrences could be harmful to our business and our financial results.

A substantial portion of our revenues is from sales of equipment for gas turbine power plants. During periods of declining construction of new gas turbine power plants, the market for our products is significantly diminished.

The demand for our products depends on the continued construction of gas turbine power generation plants. The power generation equipment industry has experienced cyclical periods of slow growth or decline. In periods of decreased demand for new gas turbine power plants, our customers may be more likely to decrease expenditures on the types of products and systems that we supply and, as a result, our future revenues may decrease. These projects typically require funding from a healthy credit market as well. As long as credit markets are tight, funding could be difficult to obtain therefore delaying or even cancelling these types of projects entirely. A rise in the price or a shortage in the supply of natural gas could affect the profitability or operations of gas turbine power plants, which could adversely affect our future revenues. These and other factors may temper demand for our products. If in a particular geographic area prices of natural gas are so high or the supply of natural gas is so limited as to make the construction of new gas turbine power plants uneconomical in that geographic area, we may not derive any future revenues from projects in that geographic region unless and until those factors are reversed.

15

Table of Contents

Environmental laws and regulations have played a part in the increased use of gas turbine technology in various jurisdictions. These laws and regulations may change or other jurisdictions may not adopt similar laws and regulations. Changes in existing laws and regulations could result in a reduction in the building and refurbishment of gas turbine power plants. In addition, stricter environmental regulation could result in our customers seeking new ways of generating electricity that do not require the use of our products. Furthermore, although gas turbine power plants have lower carbon dioxide emissions per unit of electricity provided than coal-fired power plants, emissions from gas turbine power plants remain a concern and attempts to reduce or regulate emissions could increase the cost of gas turbine power plants and result in our customers switching to alternative sources of power.

Other current power technologies, improvements to these technologies and new alternative power technologies that compete or may compete in the future with gas turbine power plants could affect our sales and profitability. Any change in the power generation industry that results in a decline in the construction of new combined cycle power plants or a decline in the upgrading of existing simple cycle power plants to combined cycle power plants could materially adversely affect our sales.

A small number of major customers account for a significant portion of our revenues, and the loss of any of these customers could negatively impact our business.

We depend on a relatively small number of customers for a significant portion of our revenues. In 2010, two customers accounted for approximately 47% of our consolidated revenues and approximately 24% of our backlog at the end of the year. In 2009, two customers accounted for approximately 23% of our consolidated revenues and approximately 23% of our backlog at the end of the year. Other than their obligations under firm orders placed in our backlog, none of our customers have a long-term contractual obligation to purchase any material amounts of products or services from us. All of our firm orders contain cancellation provisions, which permit us to recover only our costs and a portion of our anticipated profit if a customer cancels its order. If a customer elects to cancel, we would not realize the full amount of future revenues included in our backlog. We expect to continue to depend upon a relatively small number of customers for a significant percentage of our revenues. Because our major customers represent a large part of our business, the loss of any of our major customers could negatively impact our business and results of operations. Several of our customers have the ability to internally source some of the products we manufacture. Any increase in this activity could reduce our sales.

The dollar amount of our backlog, as stated at any time, is not necessarily indicative of our future revenues.

When we receive a firm order for a project from a customer, it is added to our backlog. However, customers may cancel or delay projects for reasons beyond our control and we may be unable to replace any canceled orders with new orders. To the extent projects are delayed, the timing of our revenues could be affected. If a customer cancels an order, we may be reimbursed for the costs we have incurred. Typically, however, we have no contractual right to the full amount of the revenues reflected in our backlog contracts in the event of cancellation. In addition, projects may remain in our backlog for extended periods of time. Revenue recognition occurs over extended periods of time and is subject to unanticipated delays. Fluctuations in our reported backlog levels also result from the fact that we may receive a small number of relatively large orders in any given reporting period that may be included in our backlog. Because of these large orders, our backlog in that reporting period may reach levels that may not be sustained in subsequent reporting periods. Our backlog, therefore, is not necessarily indicative of our future revenues or of long-term industry trends.

The success of our business is partially dependent upon maintaining our safety record.

Our ability to obtain new business and retain our current business, particularly in our Services Division, is partially dependent on our continuing ability to maintain a safety record that exceeds the industry average. If we fail to maintain superior safety performance, or if serious accidents occur in spite of our safety procedures, our revenues and results of operations, particularly in our Services Division, could be materially and adversely affected.

We have been named as a defendant in asbestos personal injury lawsuits.

The Company has been named as a defendant in a limited number of asbestos personal injury lawsuits. Neither the Company nor its predecessors ever mined, manufactured, produced or distributed asbestos fiber, the material that allegedly caused the injury underlying these actions. The bankruptcy court’s discharge order issued upon emergence from bankruptcy extinguished the claims made by all plaintiffs who had filed asbestos claims against the Company before that time. The Company believes the bankruptcy court’s discharge order should serve as a bar against any later claim filed against it, including any of its subsidiaries, based on alleged injury from asbestos at any time before emergence from bankruptcy. In any event in all of the asbestos cases finalized post-bankruptcy the Company has been successful in having such claims dismissed without liability. Findings of liability on our part in any of these cases that were filed against us after we emerged from bankruptcy that remain unresolved could have an adverse effect on our financial position, results of operations or liquidity.

Efforts to increase our size through acquisitions will involve risks and could result in a material adverse effect on our business.

We intend to actively pursue additional acquisition opportunities, some of which may be material to our business and financial performance. We may not be able to grow our business in the future through acquisitions for a number of reasons, including:

| • | acquisition financing not being available on acceptable terms or at all; |

| • | encountering difficulties identifying and executing acquisitions; |

16

Table of Contents

| • | increased competition for targets, which may increase acquisition costs; |

| • | consolidation in our industry reducing the number of acquisition targets; and |

| • | competition laws and regulations preventing us from making certain acquisitions. |

In addition, there are potential risks associated with growing our business through acquisitions, including the failure to successfully integrate and realize the expected benefits of an acquisition. For example, with any past or future acquisition, there is the possibility that:

| • | the business culture of the acquired business may not match well with our culture; |

| • | technological and product synergies, economies of scale and cost reductions may not occur as expected; |

| • | management may be distracted from overseeing existing operations by the need to integrate acquired businesses; |

| • | we may acquire or assume unexpected liabilities; |

| • | unforeseen difficulties may arise in integrating operations and systems; |

| • | we may fail to retain and assimilate employees of the acquired business; |

| • | we may experience problems in retaining customers; and |

| • | problems may arise in entering new markets in which we may have little or no experience. |

These risks could have a material adverse effect on our business, financial condition and results of operations.

Compliance with environmental laws and regulations is costly, and our ongoing operations may expose us to environmental liabilities.

Our operations are subject to laws and regulations governing the discharge of materials into the environment or otherwise relating to the protection of the environment or human health and safety. We are subject to various U.S. federal statutes and the regulations implementing them, as well as similar laws and regulations at the state and local levels and in other countries in which we operate.