Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2010

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number 1-33094

AMERICAN CARESOURCE HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

DELAWARE | 20-0428568 | |||

(State or other jurisdiction of | (I.R.S. employer | |||

incorporation or organization) | identification no.) | |||

5429 LYNDON B. JOHNSON FREEWAY | ||||

SUITE 850 | ||||

DALLAS, TEXAS | ||||

75240 | ||||

(Address of principal executive offices) | ||||

(Zip code) |

(972) 308-6830

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, par value $.01 per share | The NASDAQ Capital Market |

Securities registered pursuant to Section 12(g) of the Exchange Act:

None

Indicate by checkmark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933 (the “Securities Act”). Yes o No x

Indicate by checkmark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 (the “Exchange Act”). Yes o No x

Indicate by checkmark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained in this form, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by checkmark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Non-accelerated filer o |

Accelerated filer o | Smaller Reporting Company x |

Indicate by checkmark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the voting and nonvoting Common Stock held by non-affiliates of the Registrant was $15,356,319, computed by reference to the price at which the Common Stock was last sold on The NASDAQ Capital Market on the last business day of the Registrant’s most recently completed second fiscal quarter (June 30, 2010).

The number of shares of the Registrant’s Common Stock, par value $.01 per share, outstanding as of March 14, 2011 was 16,922,042.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for the annual meeting of stockholders of American CareSource Holdings, Inc. to be held on May 23, 2011 and to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than April 30, 2011, are incorporated by reference into Part III of this Form 10-K.

AMERICAN CARESOURCE HOLDINGS, INC.

FORM 10-K

TABLE OF CONTENTS

PART I | ||

PART II | ||

PART III | ||

PART IV | ||

Index to Financial Statements | ||

Special Note Regarding Forward-Looking Statements

This annual report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements can be identified by forward-looking words such as “may,” “will,” “expect,” “intend”, “anticipate,” “believe,” “estimate” and “continue” or similar words and discuss the Company’s plans, objectives and expectations for future operations, including its services, contain projections of the Company’s future operating results or financial condition, and discuss its expectations with respect to the growth in health care costs in the United States, the demand for ancillary benefits management services, and the Company’s competitive advantages, or contain other “forward-looking” information.

Such forward-looking statements are based on current information, assumptions and belief of management, and are not guarantees of future performance. Substantial risks and uncertainties could cause actual results to differ materially from those indicated by such forward-looking statements, including, but not limited to, the Company’s inability to attract or maintain providers or clients or achieve its financial results, changes in national health care policy, federal or state regulation, and/or rates of reimbursement including without limitation the impact of the newly-enacted Patient Protection and Affordable Care Act, Health Care and Educational Affordability Reconciliation Act and medical loss ratio regulations, general economic conditions (including the recent economic downturns and increases in unemployment), lower than anticipated demand for ancillary services, pricing, market acceptance/preference, the Company’s ability to integrate with its clients, consolidation in the industry that may affect the Company’s key clients, changes in the business decisions by significant clients, increased competition, the Company’s inability to manage growth, implementation and performance difficulties, and other risk factors detailed from time to time in the Company’s periodic filings with the Securities and Exchange Commission, including in this annual report on Form 10-K for the year ended December 31, 2010.

Do not place undue reliance on these forward-looking statements, which speak only as of the date this document was prepared. All forward-looking statements included herein are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable securities laws and regulations, the Company undertakes no obligation to update or revise these forward-looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events.

ii

PART I

Item 1. Business.

Overview

American CareSource Holdings, Inc. (“ACS,” “Company,” the “Registrant,” “we,” “us,” or “our”) is an ancillary services company that offers cost effective access to a comprehensive national network of ancillary healthcare service providers. The Company sells its services to a number of healthcare companies including preferred provider organizations ("PPOs"), third party administrators (“TPAs”), insurance companies, large self-funded organizations and various employee groups. The Company offers payors this solution by:

• | lowering its payors’ ancillary care costs throughout our network of high quality, cost effective providers that the Company has under contract at more favorable terms than they could generally obtain on their own; |

• | providing payors with a comprehensive network of ancillary healthcare services providers that is tailored to each payor’s specific needs and is available to each payor’s covered persons for covered services; |

• | providing payors with claims management, reporting and processing and payment services; |

• | performing network/needs analysis to assess the benefits to payors of adding additional/different service providers to the payor -specific provider networks; and |

• | credentialing network service providers for inclusion in the payor -specific provider networks. |

Ancillary healthcare services encompass a broad array of services that supplement or support the care provided by hospitals and physicians and include the services listed under “-- Services and Capabilities--Ancillary care services” below.

The Company's primary focus is on direct payors. It is the Company's belief that it can best influence patient choice by working with payors who have the ability to alter benefit design in order to encourage patients to seek the most cost effective ancillary providers.

The Company's net revenue and operating results were impacted by multiple macro- and micro-economic factors in 2009 and 2010. The following macro-economic factors negatively impacted our business:

•High unemployment rates have resulted in fewer people participating in insurance programs;

• | Uncertainty surrounding the Patient Protection and Affordable Care Act and Health Care and Educational Affordability Reconciliation Act legislation; |

•Plan participants have sought to spend less money, resulting in less frequent use of our ancillary services; and

• | Payor and provider consolidation throughout the healthcare industry have reduced claims volume and may limit opportunities for growth. |

On a micro-economic basis, we have been severely impacted by the deterioration of the business of our two most significant clients. Those clients, both of which are PPO's, have seen significant declines in their number of covered lives. One client has lost payor groups due to various competitive factors, while the other client was party to a business combination, which resulted in a lengthy transition plan, reducing our business. Because we do not have a direct relationship with these organization's payors, it is difficult to competitively impact those relationships. Revenues from the two client relationships declined a combined 21% in 2010 as compared to 2009.

ACS was incorporated under the laws of the State of Delaware on November 24, 2003 as a wholly-owned subsidiary of Patient Infosystems, Inc. (“Patient Infosystems”) in order to facilitate Patient Infosystems’ acquisition of substantially all of the assets of American CareSource Corporation. American CareSource Corporation had been in operation since 1997. The predecessor company to American CareSource Corporation, Physician’s Referral Network, had been in operation since 1995. On December 23, 2005, the Company became an independent company when Patient Infosystems distributed by dividend to its stockholders substantially all of its shares of the Company. Ancillary Care Services, Inc. is a wholly owned subsidiary of the Company.

1

The Company’s principal executive offices are located at 5429 Lyndon B. Johnson Freeway, Suite 850, Dallas, TX 75240. Our Common Stock is listed on The NASDAQ Capital Market under the symbol “ANCI.” Our telephone number is (972) 308-6830. Our Internet address is www.anci-care.com.

Services and Capabilities

Ancillary care services

Ancillary healthcare services include a broad array of services that supplement or support the care provided by hospitals and physicians, including the non-hospital, non-physician services associated with surgery centers, free-standing diagnostic imaging centers, home health and infusion, supply of durable medical equipment, orthotics and prosthetics, laboratory and other services.

Ancillary healthcare services include, but are not limited to, the following categories:

· Acupuncture | · Massage Therapy |

· Cardiac Monitoring | · Occupational Therapy |

· Chiropractor | · Orthotics and Prosthetics |

· Diagnostic Imaging | · Pain Management |

· Dialysis | · Physical Therapy |

· Durable Medical Equipment | · Podiatry |

· Genetic Testing | · Rehab: Outpatient |

· Hearing Aids | · Rehab: Inpatient |

· Home Health | · Sleep |

· Hospice | · Skilled Nursing Facility |

· Implantable Devices | · Surgery Center |

· Infusion | · Transportation |

· Laboratory | · Urgent Care |

· Lithotripsy | · Vision |

· Long-term Acute Care | · Walk-in Clinics |

The Company has agreements with approximately 5,000 ancillary healthcare service providers operating in approximately 36,000 sites nationwide.

Provider Network

The Company views its ability to manage, organize and maintain its provider network and to recruit new providers as critical elements in its long-term success because its network is one of the most important reasons healthcare payors engage the Company. The Company has agreements with its network of ancillary healthcare service providers for the purpose of meeting contractual obligations to its healthcare payors to make available a comprehensive and client-specific ancillary healthcare provider network. The agreements define the scope of services to be provided to covered persons by each ancillary healthcare provider and the amounts to be charged for those services and are negotiated independently from the agreements reached with the Company’s client payors. The terms of each agreement between the Company and ancillary healthcare service providers make it clear that the Company is solely obligated to the service provider under the contract between them and do not contemplate any contractual relationship between the service providers and the Company’s payors or permit the service providers to pursue claims directly against the Company’s payors. The network is comprised of approximately 5,000 ancillary healthcare service providers that are located in 36,000 sites nationwide.

When providers initially enter the ACS provider network, the Company credentials them for inclusion in the Credentialed ACS network. The Company also re-credentials its providers on a periodic basis. From time to time, the Company reviews its provider relationships to determine whether any changes to the relationship are appropriate through sanction monitoring and other methods. The Company believes that credentialing providers represents a valuable service to both its payors and the providers in the network, who would, in the absence of such service, be forced to undergo the credentialing process with respect to each payor with whom they enter into a service relationship.

2

During 2010 and 2009, we generated revenue from ancillary healthcare services as follows:

Category | 2010 | 2009 | ||||

Dialysis | 28 | % | 27 | % | ||

Laboratory | 19 | 22 | ||||

Durable Medical Equipment | 13 | 12 | ||||

Diagnostic Imaging | 10 | 10 | ||||

Infusion | 7 | 9 | ||||

Rehab: Outpatient & Inpatient | 6 | 4 | ||||

Surgery Center | 4 | 5 | ||||

Chiropractor | 3 | 2 | ||||

Long Term Acute Care/Skilled Nursing Facilities | 2 | 4 | ||||

Orthotics and Prosthetics | 2 | 2 | ||||

Other | 6 | 3 | ||||

100 | % | 100 | % | |||

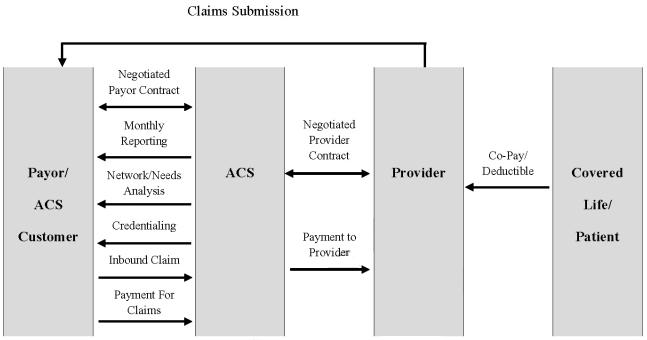

Our Model

The Company’s business model, illustrating the relationships among the persons involved, directly or indirectly, in the Company’s business and its generation of revenue and expenses is depicted below:

Payors route healthcare claims to us after service has been performed by participant providers in our network. We process those claims and charge the payor according to its contractual rate for the services according to our contract with the payor. In processing the claim, we are paid directly by the payor or the insurer for the service. We then pay the provider of service according to its independently-negotiated contractual rate. We assume the risk of generating positive margin, the difference between the payment we receive for the service and the amount we are obligated to pay the provider of service.

The Company may also receive a claims submission from a payor either electronically or via a paper based claim. As part of its relationship with the payors, the Company may pay an administrative fee to the payors for the modifications that may be required to the payor’s technology, systems and processes to create electronic connectivity with the Company, as well as for the aggregation of claims and the electronic transmission of those claims to us.

3

How We Deliver Services

Ancillary network analysis. The Company performs an analysis of the available claims history from each client payor and develops a specific plan to meet each payor’s needs. This analysis identifies service providers that are not already in our network. We attempt to enter into agreements with such service providers to maximize discount levels and capture a significant volume of previously out-of-network claims.

Ancillary custom network. ACS customizes its network to meet the needs of each payor. In particular, when a new payor joins and periodically for each existing payor, we review the payor’s “out-of-network” claims history through our network analysis service and develop a strategy to create a network that efficiently serves the payor’s needs. This may involve adding additional service providers for a payor or removing service providers if we determine it is beneficial for them to be excluded from the client’s network.

Ancillary network management. The Company manages ancillary service provider contracts, reimbursement and credentialing for its payors. This not only provides administrative benefits to our payors, but reduces the burden on our contracted service providers who typically must supply credentialing documentation to payors and engage in contract negotiations with separate payors.

Ancillary systems integration. The Company has created a proprietary software system that enables us to manage many different customized accounts and includes the following modules:

• | Provider network management |

• | Credentialing |

• | Data transfer management/electronic data interface |

• | Multi-level reimbursement management |

• | Posting, Explanation of Benefits, check, and e-funds processes |

• | Client service management |

• | Claims pricing |

• | Advanced data reporting |

Ancillary reporting. ACS offers a complete suite of reports to each payor on a monthly basis. These reports cover contracting efforts and capture rates, client savings, volumes by service category and complete claims and utilization reports and other information of value to the client.

Ancillary healthcare claims management. The Company can manage ancillary healthcare claims flow, both electronic and paper based, and integrate with a payor’s process electronically or through paper claims. The Company has the capability of performing a number of customized processes that may add additional value for each payor. As part of the claims management process, we manage the documentation requirements specific to each payor. In the event claims are submitted to us by a payor without the complete required documentation, we will work with the payor and/or service provider to obtain the required documentation so that the claim will be accepted by the payor. This service provides a labor cost savings to the payors and providers.

Ancillary claims collections management. The Company facilitates an expedited claims collection process by ensuring receipt of the claim by the payor, providing information to the payor required for processing the claim, tracking the status of the claim throughout the process and maintaining a team of customer service representatives to resolve any issues that might delay the collections process. The Company believes that the providers in its network are paid more effectively and efficiently than would otherwise be the case.

Ancillary data insights. The Company has developed and continues to develop an extensive database of ancillary healthcare claims history. The data provides insights into utilization and pricing across a wide variety of service categories, geographies, and service providers. The Company intends to market this data as a value added service to its payors in the design of custom networks, and the development of ancillary healthcare management programs.

4

Business Strategy

The Company’s focus is strictly on the ancillary healthcare services market, a growing market that now accounts for almost 30% of total annual healthcare spending in the United States and is estimated at $574 billion (as derived from 2006 data published by the Center for Medicare and Medicaid Services, National Health Statistics Group, U.S. Department of Commerce and Bureau of Economic Analysis and Census). Ancillary healthcare services are cost effective alternatives to physician and hospital-based services and ancillary providers offer services in 30 different categories, including those listed under “-- Services and Capabilities--Ancillary care services.” While most efforts are placed on managing outcomes and reducing healthcare costs associated with patient care in hospitals and in physician offices, the ancillary healthcare service market is an often over-looked, but very important emerging segment of the overall United States healthcare system. As more and more care is delivered in highly cost effective out-patient and ancillary care settings, the need for better organization and cost containment will only increase over the next several years.

We believe that companies who understand the nuances of the ancillary healthcare market and develop the expertise to manage this new, de-centralized system of patient care, are able to capitalize on this market opportunity. For example, contracting with ancillary healthcare service providers is difficult without a specific focus on the market. This is due to the disparate nature of ancillary healthcare services and the fact that these services are offered by a wide array of providers, ranging from small independent practitioners, regional specialty practices, national providers and within hospital systems. Since this market is so diverse, it has not been a focus of the major health plans and payors. In addition, many health plans are conflicted because their existing hospital contracts may encourage the use of the hospital systems’ more expensive in-house ancillary services. The Company believes that because it has developed a substantial network of providers, it has established a sustainable advantage in this market by becoming an aggregator of these services for health plans, and because it has been retained by substantial payors, it can offer healthcare providers a substantial number of patients who are entitled to receive services from payors. In addition, our "ancillary only" contracting focus allows us to be independent of any hospital relationships that may encourage retaining all ancillary services within the more expensive hospital setting.

Because the Company is solely focused on the nation-wide ancillary healthcare system designed specifically to help regional and mid-market payors across the country, expanding and maintaining a nation-wide, high-quality, multiple specialty ancillary provider network is a critical component of the Company’s strategy. The Company has invested to develop its ancillary service provider network both proactively, across geographical and healthcare specialties, and reactively to address specific client needs. While we have a national footprint of service providers, our intention is to focus on specific geographic markets where we can have a significant impact on a service provider’s patient load. With market strength in specific geographic areas, the Company has been able to develop favorable rates with ancillary service providers and create an attractive product offering (healthcare cost savings) to regionally-based clients in those areas.

In order to enhance its ability to recruit and manage its network of providers, the Company offers a suite of value added services specifically designed to help ancillary care service providers lower their cost of doing business by assuming the responsibility for the most complex and costly interactions with payors. The services include those listed under “-- Services and Capabilities--Ancillary care services.” The Company believes that by becoming an indispensable business partner to the ancillary healthcare service provider community, it will continue to grow its ancillary healthcare service provider network and continue to derive favorable contracting terms from these service providers.

While the Company markets its services to PPOs on an opportunistic basis, it is seeking growth from increasing its number of client payor and service provider relationships by focusing on providing in-network services for its payors and aggressively pursuing middle-market insurance companies, TPAs and direct payors. The Company continues to derive a significant amount of its net revenues from its traditional PPO relationships, but we have shifted our focus and we now aggressively target TPAs and direct payors. The Company believes that there is a large market opportunity involved in providing a highly competitive ancillary care solution to the standard service offered by the major national insurers in select regional markets across the country. The combination of our regionally specific networks of providers and the resulting contractual cost savings we are able to generate helps ACS’ payors compete more effectively against the major national insurers in their local markets.

The Company aggregates the lives of its various clients into buying power that exceeds the market power of any one of its clients individually. During 2010, the Company's contracts exposed us to 3.2 million covered lives. As a rapid aggregator of significant patient volume, the Company believes it will be able to continue to drive favorable contracting terms from the selected service providers in the ACS Network by directing patient volume to their practices and it will have the ability to negotiate exclusive contracts that will allow the Company to manage the full spectrum of a payor client’s ancillary healthcare benefit offerings. The volume of collective lives we manage allows us to obtain more favorable pricing than our clients can generally obtain on their own.

5

Sales and Marketing

The Company markets its services to PPOs on an opportunistic basis, but primarily targets direct payors such as TPAs, insurance companies, large self-funded organizations and employee groups. The Company utilizes both a new business sales organization of three senior sales professionals as well as an account management team of two professionals to contract with new payor organizations and then maximize the revenue and margin potential of each new payor. The new business sales team uses a variety of channels to reach potential clients including professional relationships, direct marketing efforts, attendance at industry-specific trade shows and conferences, and through strategic partnerships with market partners, independent brokers, and consultants. The account management team is engaged with each new payor to help manage the implementation process. In addition, an Account Manager is generally assigned to each new payor organization and is responsible for all aspects of the Company’s relationship with the entity including the expanded utilization of the Company’s services over time and the enhancement of the Company’s relationship with the payor.

The Company invests in on-going market research with its clients and maintains an informal client advisory group with a number of senior leaders in managed care organizations. From time to time, the Company meets with the advisory group to discuss changes in the marketplace and client needs. In the first quarter of 2009, the Company engaged a strategic marketing services company to conduct a “Market Pulse” which involved in-depth interviews with senior managers/decision-makers in current ACS client organizations. The purpose of the “Market Pulse” was to gain client feed-back on the Company’s optimal product messaging by market segment, differentiated “go-to-market” strategies, and new product ideas. The outcome from these sessions was used to formulate a solid base of sales, marketing and new product priorities for the next several years.

Clients

The Company’s healthcare payor clients engage the Company to manage a comprehensive array of ancillary healthcare services that they and their payors have agreed to make available to their insureds or beneficiaries or for which they have agreed to provide insurance coverage. The typical services the healthcare payors require the Company to provide include:

• | providing a comprehensive network of ancillary healthcare services providers that is available to the payor’s covered persons for covered services; |

• | providing claims management, reporting, and processing and payment services; |

• | performing network/needs analysis to assess the benefits to payors of adding additional/different service providers to the payor-specific provider networks; and |

• | credentialing network service providers for inclusion in the payor -specific provider networks. |

The terms of the agreement between the Company and the payors do not contemplate that the payors will have any relationship with the service providers and, in fact, prohibit payors from claiming directly against the service providers. The agreements between the Company and the payors provide that it is the Company’s obligation to deliver or make available the agreed-upon services. The Company is responsible irrespective of the existence or terms of any agreement the Company has with the service providers. The terms of the Company-payor agreement provide that the Company is obligated to provide or arrange for the provision of all of the services covered by such agreement and the Company is responsible for ensuring that the contractual terms are met and such services are provided (whether the services are those performed directly by the Company, such as claims management, processing and payment service, network/needs analysis and credentialing, or those performed by a service provider contracted by the Company).

The Company’s most significant payors include (i) HealthSmart (“HealthSmart”), which consists of HealthSmart and its affiliates, American Administrative Group (“AAG”), Interplan Health Group (“IHG”), Emerald Healthcare, and HealthSmart Accel Network (“Accel”), and (ii) Viant Holdings Inc. (“Viant”), consisting of Texas True Choice, Inc. and Beech Street Corporation. For the year ended December 31, 2010, ACS derived 48% of its total net revenue from HealthSmart (including its affiliates) and 27% of its total net revenue from Viant (including its affiliates). For the year ended December 31, 2009, ACS derived 47% of its total net revenue from HealthSmart and 38% of its total net revenue from Viant.

In early 2009, we entered into an amendment to our agreement with HealthSmart. The amendment extended the duration of the partnership between the Company and HealthSmart through December 31, 2012. In accordance with the amendment, we paid $1.0 million to HealthSmart for various integration services. In November 2009, HealthSmart completed a recapitalization with a private investment company and HealthSmart’s other lenders.

6

The client contract with Viant expires on May 20, 2011 and automatically renews for successive one-year periods unless either party delivers a written notice of non-renewal at least 90 days prior to expiration. Since the Company has not received written notice of non-renewal, the contract term has been automatically extended through May 20, 2012. Such contract may be terminated upon thirty (30) days’ notice in the event of a breach. In addition, in March 2010, Viant was acquired by MultiPlan, Inc., a provider of PPO network and related transaction-based solutions.

We have generated a significant portion of our net revenues from these two clients (75% in 2010 and 85% in 2009), but because of the nature of the relationships, we do not have the ability to impact the relationships these organizations have with their clients, which are direct payors. Because we have secondary relationships with these payors and cannot have a competitive impact on the payors, we have determined that it is in our best interest to pursue clients that are direct payors, primarily TPAs. We believe we can impact relationships with direct payors through various competitive avenues, such as assisting them with plan design. During 2010, of our 13 new clients, 12 were direct payors and generated approximately $5 million of revenue.

Competition

The Company faces four types of direct competitors.

• | The first group of competitors consists of larger, national health plans and insurers such as Aetna, Blue Cross/Blue Shield plans, Cigna, Humana, and United HealthCare. These larger carriers offer nation-wide, standardized products and often compete on a local level based of the cost-effectiveness of their national contracts. |

• | The second group of competitors is our own payors. Our payors have selected us based on our extensive network of service providers and cost-savings potential. However, they may choose to develop their own network instead of outsourcing ancillary management services to us in the future. |

• | The third group of competitors is more regionally-focused and consists of smaller regional PPOs, payors and community-based provider-owned networks. These regional competitors are generally managing their own home-grown network of ancillary care providers and are more likely to offer customized products and services tailored to the needs of the local community. These regional groups will often use their ownership and/or management of the full continuum of care in a local market to direct patients to the provider groups within their network. |

• | The fourth group of competitors focus on managing patients within a single ancillary specialty (e.g. dialysis, imaging or infusion), and offer comprehensive payor and provider services within their chosen ancillary category. |

Research and Development

The Company invests in its information technology infrastructure to enhance the capabilities of its databases, data retrieval tools, data exchange capabilities and claims processing engine. In addition, the Company believes that its extensive claims database of ancillary healthcare services and costs is a strategic asset. The Company’s capitalized development costs totaled approximately $402,000 and $628,000 during 2010 and 2009, respectively.

Government Regulation

The healthcare industry is extensively regulated by both the Federal and state governments. A number of states have extensive licensing and other regulatory requirements applicable to companies that provide healthcare services. Additionally, services provided to health benefit plans in certain cases are subject to the provisions of the Employee Retirement Income Security Act of 1974, as amended (“ERISA”).

Furthermore, state laws govern the confidentiality of patient information through statutes and regulations that safeguard privacy rights. The Company is subject to the Health Insurance Portability and Accountability Act of 1996 (“HIPAA”), which provides national standards for electronic health information transactions and the data elements used in such transactions. ACS and its clients may be subject to Federal and state laws and regulations that govern financial and other arrangements among healthcare providers. Furthermore, the Company and its clients may be subject to federal and state laws and regulations governing the submission of false healthcare claims to the government and private payors, mail pharmacy laws and regulations, consumer protection laws and regulations, legislation imposing benefit plan design restrictions, various licensure laws, such as managed care and third party administrator licensure laws, drug pricing legislation, and Medicare and Medicaid reimbursement regulations. Possible sanctions for violations of these laws and regulations include minimum civil penalties of between $5,000-$10,000 for each false claim and treble damages.

7

During 2010, President Obama signed the Patient Protection and Affordable Care Act (the "Affordable Care Act") and the Health Care and Educational Affordability Reconciliation Act legislating broad-based changes to the U.S. health care system. Among other things, the health reform legislation includes guaranteed coverage requirements, eliminates pre-existing condition exclusions and annual and lifetime maximum limits, restricts the extent to which policies can be rescinded, and imposes new and significant taxes on health insurers and health care benefits.

Provisions of the health reform legislation become effective at various dates over the next several years. The Department of Health and Human Services, the National Association of Insurance Commissioners, the Department of Labor and the Treasury Department have yet to issue necessary enabling regulations and guidance with respect to the health care reform legislation.

Due to the breadth and complexity of the health reform legislation, the scope of newly-issued implementing regulations and interpretive guidance, in addition to regulations and guidance yet to be issued, the phased-in nature of the implementation and possible changes to, or repeal of, the legislation by Congress, it is difficult to predict the overall impact of the health reform legislation on our business over the coming years. Possible adverse affects of the health reform legislation include reduced revenues, increased costs, exposure to expanded liability, and requirements for us to revise the ways in which we conduct business or risk of loss of business. In addition, our results of operations, our financial position, including our ability to maintain the value of our goodwill, and cash flows could be materially adversely affected.

Section 1001 of the Affordable Care Act amended Title 27 of the Public Health Service Act of 1944, as amended (the "Public Health Service Act") to add, among other things, a new Section 2718, 'Bringing Down the Cost of Health Care Coverage.' This new provision requires health insurance issuers to publicly report “the ratio of the incurred loss (or incurred claims) plus the loss adjustment expense (or change in contract reserves) to earned premiums” and account for premium revenue related to reimbursement for clinical services, activities that improve health care quality, and all other non-claims costs. The law also requires issuers to provide annual rebates to their enrollees if their medical loss ratio ("MLR") does not meet specific targets. For issuers in the large group market, the MLR must be at least 85%, and for issuers in the smaller and individual markets, the MLR must be at least 80%. The law also gives the National Association of Insurance Commissioners (“NAIC”), subject to certification of the Secretary of the Department of Health and Human Services (“HHS”), authority to develop definitions and standards by which to determine compliance with the requirements in the new § 2718(a).

On December 1, 2010, HHS published final MLR regulations, based upon the recommendations of the NAIC, implementing the new sections of the Public Health Service Act as mandated by the Affordable Care Act. The new regulations apply to issuers offering group or individual health insurance coverage. Under the MLR regulations, an issuer's MLR is calculated as the ratio of (i) incurred claims plus expenditures for activities that improve health care quality to (ii) premium revenue. The two key aspects to this calculation involve what comprises an 'incurred claim' and what qualifies as an 'expenditure for health care quality improvement.'

Incurred claims are reimbursement for clinical services, subject to specific deductions and exclusions. Specifically, incurred claims represent the total of direct paid claims, unpaid claim reserves, change in contract reserves, reserves for contingent benefits, the claim portion of lawsuits and any experience rating refunds. Prescription drug rebates received by the issuer and overpayment recoveries from providers must be deducted from incurred claims. Also, the following amounts are explicitly excluded and therefore may not be included in the calculation of incurred claims: (i) amounts paid to third party vendors for secondary network savings; (ii) amounts paid to third party vendors for network development, administrative fees, claims processing, and utilization management; or (iii) amounts paid, including amounts paid to a provider, for professional or administrative services that do not represent compensation or reimbursement for covered services provided to an enrollee. The regulation permits that some amounts “may” be included in incurred claims - market stabilization payments, state subsidies based on stop-loss methodologies, and incentive and bonus payments made to providers. The regulations themselves provide examples of specifically excluded amounts. With regard to amounts paid for network development (as noted in (ii) above), if an issuer contracts with a behavioral health, chiropractic network, or high technology radiology vendor, or a pharmacy benefit manager, and the vendor reimburses the provider at one amount but bills the issuer a higher amount to cover its network development, utilization management costs, and profits, then the amount that exceeds the reimbursement to the provider must not be included in incurred claims. With regard to administrative services (as noted in (iii) above), medical record copying costs, attorneys' fees, subrogation vendor fees, compensation to paraprofessionals, janitors, quality assurance analysts, administrative supervisors, secretaries to medical personnel and medical record clerks must not be included in incurred claims.

8

In order to properly classify what activities 'improve health care quality', the activity must be designed to improve health quality, increase the likelihood of desired health outcomes, be directed toward individual enrollees or incurred for the benefit of specific segments of enrollees, or be grounded in evidence based medicine. In addition, the activity must be primarily designed to improve health outcomes, prevent hospital readmissions, improve patient safety and reduce medical errors, implement, promote and increase wellness activities and/or enhance the use of health care data to improve quality. The regulations also contain a list of 14 expenditures that are specifically excluded from 'improvement of health care quality' activities. Among these excluded expenditures are: (1) those that are designed primarily to control or contain costs; (2) activities that can be billed or allocated by a provider for care delivery and which are, therefore, reimbursed as clinical services; (3) expenditures related to establishing or maintaining a claims adjudication system, including costs directly related to upgrades in health information technology that are designed primarily or solely to improve claims payment capabilities or to meet regulatory requirements for processing claims (for example, costs of implementing new administrative simplification standards and code sets adopted pursuant to HIPAA including the new ICD-10 requirements); (4) all retrospective and concurrent utilization review; (5) costs of developing and executing provider contracts and fees associated with establishing or managing a provider network, including fees paid to a vendor for the same reason; (6) provider credentialing; (7) marketing expenses; (8) costs associated with calculating and administering individual enrollee or employee incentives; (9) portions of prospective utilization that does not meet the definition of activities that improve health quality; and (10) any function or activity not expressly included, unless otherwise approved by and within the discretion of the Secretary.

It is possible that a portion of the fees our existing and prospective payors are contractually required to pay us and that do not qualify as 'incurred claims' may not be included as expenditures for activities that improve health care quality. Such a determination may make it more difficult for us to retain existing clients and/or add new clients, because our clients' or prospective clients' MLR may otherwise not meet the specified targets. This may reduce our net revenues and profit margins.

The Company must continually adapt to new and changing regulations in the healthcare industry. If we fail to comply with these applicable laws, we may be subject to fines, civil penalties, or criminal prosecution. If an enforcement action were to occur, our business and financial condition may be adversely affected.

Employees

As of March 14, 2011, the Company had 64 full-time employees and no part-time employees.

Item 1A. Risk Factors.

The Company’s stockholders and any potential investor in the Company’s Common Stock should carefully review and consider each of the following risk factors, as well as all other information appearing in this Annual Report on Form 10-K, relating to investment in our Common Stock. The Company’s business faces numerous risks and uncertainties, the most significant of which are described below. If any of the following risks actually occur, the business, financial condition, results of operations or cash flows of the Company could be materially adversely affected, the market price of the Company’s Common Stock could decline significantly, and a stockholder could lose all or part of an investment in the Company’s Common Stock.

The Company has a limited number of clients, two of which account for a substantial portion of its business, and failure to retain such clients or changes to these clients would have a material adverse effect on its business and results of operations. Business from these two clients has declined during the last two years, and will likely continue to decline.

Our two largest clients, HealthSmart Preferred Care, Inc. (“HealthSmart”) and Viant Holdings, Inc. (“Viant”), accounted for an aggregate of approximately 75% of our net revenue during 2010; of which 48% was derived from HealthSmart. In 2009, our two largest clients accounted for 85% of our net revenue, of which 47% was generated from HealthSmart. The loss of either one of these clients or significant declines in the level of use of our services by one or more of these clients (as would be the case, for example, if our clients decide to contract directly with ancillary healthcare service providers), without replacement by new business, would have a material adverse effect on the Company’s business and results of operations. After already declining in the year ended December 31, 2009, net revenues from our two largest clients declined $12.0 million, or 21%, for the year ended December 31, 2010, compared to the prior year.

9

The client contract with Viant expires on May 20, 2011 and automatically renews for successive one-year periods unless either party delivers a written notice of non-renewal at least 90 days prior to expiration. Since the Company has not received written notice of non-renewal, the contract term has been automatically extended through May 20, 2012. Such contract may be terminated upon thirty (30) days’ notice in the event of a breach. In addition, in March 2010, Viant was acquired by MultiPlan, Inc., a provider of PPO network and related transaction-based solutions. We expect that revenue from Viant will continue to decline as its business is integrated with its acquiror, and that even if our contract were to be renewed past May 20, 2012, it would be on a limited basis.

The client contract with HealthSmart, which was set to expire on July 31, 2009, was amended on December 31, 2008. The term was extended four years and will expire on December 31, 2012. There can be no assurance that any client will maintain its contract with us after the expiration of the then-current term or that it will renew its contract on terms favorable to us. Consequently, the Company’s failure to retain such clients could have a material adverse effect on our business and results of operations. Additionally, an adverse change in the financial condition of any of these clients, particularly HealthSmart or Viant, including an adverse change as a result of a change in governmental or private reimbursement programs, could have a material adverse effect on our business.

Proposed health care reforms could materially adversely affect our revenues, financial position and our results of operations.

The enactment of health care reforms at the federal or state level may affect certain aspects of our business, including contracting with ancillary healthcare service providers; administrative, technology or other costs; provider reimbursement methods and payment rates; premium rates; coverage determinations; mandated benefits; minimum medical expenditures; claim payments and processing; drug utilization and patient safety efforts; collection, use, disclosure, maintenance and disposal of individually identifiable health information; personal health records; consumer-driven health plans and health savings accounts and insurance market reforms; and government-sponsored programs.

During 2010, President Obama signed the Affordable Care Act and the Health Care and Educational Affordability Reconciliation Act legislating broad-based changes to the U.S. health care system. Among other things, the health reform legislation includes guaranteed coverage requirements, eliminates pre-existing condition exclusions and annual and lifetime maximum limits, restricts the extent to which policies can be rescinded, and imposes new and significant taxes on health insurers and health care benefits.

On December 1, 2010, HHS published final regulations implementing new sections of the Public Health Service Act as mandated by the Affordable Care Act. The new medical loss ratio ("MLR") regulations apply to issuers offering group or individual health insurance coverage. Under the MLR regulations, an issuer's MLR is calculated as the ratio of (i) incurred claims plus expenditures for activities that improve health care quality to (ii) premium revenue. The two key aspects to this calculation involve what comprises an 'incurred claim' and what qualifies as an 'expenditure for health care quality improvement.' It is possible that a portion of the fees our existing and prospective payors are contractually required to pay us and that do not qualify as 'incurred claims' may not be included as expenditures for activities that improve health care quality. Such a determination may make it more difficult for us to retain existing clients and/or add new clients, because our clients' or prospective clients' MLR may otherwise not meet the specified targets. This may reduce our net revenues and profit margins.

Other provisions of the health reform legislation become effective at various dates over the next several years. The Department of Health and Human Services, the National Association of Insurance Commissioners, the Department of Labor and the Treasury Department will issue necessary enabling regulations and guidance with respect to the health care reform legislation.

Due to the breadth and complexity of the health reform legislation, the scope of newly-issued implementing regulations and interpretive guidance, in addition to regulations and guidance yet to be issued, the phased-in nature of the implementation and possible changes to, or repeal of, the legislation by Congress, it is difficult to predict the overall impact of the health reform legislation on our business over the coming years. Possible adverse affects of the health reform legislation include reduced revenues, increased costs, exposure to expanded liability, and requirements for us to revise the ways in which we conduct business or risk of loss of business. In addition, our results of operations, our financial position, including our ability to maintain the value of our goodwill, and cash flows could be materially adversely affected.

10

The Company has a history of losses and has only achieved profitability in the past three years.

Although the Company achieved its third consecutive profitable year in 2010, it incurred losses in each year between its spinoff in 2003 through 2007 and has an accumulated deficit of approximately $1.0 million as of December 31, 2010. The Company will need to maintain similar levels of claims volume and revenue as it had in 2009 and 2010 in order to continue profitability. No assurances can be given that the Company will be able to continue its current operating volumes or continue to operate profitably in the future. The Company’s prospects must be considered in light of the numerous risks, expenses, delays and difficulties frequently encountered in an industry characterized by intense competition, as well as the risks inherent in the development of new programs and the commercialization of new services, particularly given its operating history through 2007.

The current financial crisis may reduce our revenue and profitability and harm our growth prospects.

Although the Company has continued to experience profitability from 2008 to 2010, its results have been impacted by the current economic crisis. First, the unemployment rate has caused fewer people to participate in insurance programs with our clients. Second, plan participants, seeking to spend less money, appear to be making less frequent use of some ancillary services. Third, the possibility exists that client and, or provider consolidation within our industry could adversely affect our business. To the extent that these trends continue, or become worse, we may receive less revenue and our profitability and growth could be adversely affected, depending on the extent of the declines. Finally, as with any business, the deterioration of the financial condition or sale or change of control of our significant clients could have a corresponding adverse effect on us.

Large competitors in the healthcare industry could choose to compete with us, reducing our margins. Some of these potential competitors may be our current clients.

Traditional health insurance companies, specialty provider networks, and specialty healthcare services companies are potential competitors of the Company. These entities include well-established companies that may have greater financial, marketing and technological resources than we have. Pricing pressure caused by competition has caused many of these companies to reduce the prices charged to clients for core services and to pass on to clients a larger portion of the formulary fees and related revenues received from service providers. Increased price competition from such companies’ entry into the market could reduce our margins and have a material adverse effect on our financial condition and results of operations. In fact, our clients could choose to establish their own network of ancillary care providers. As a result, we would not only lose the benefit of revenue from such clients, but we could face additional competition in our market.

The Company is dependent upon payments from third party payors who may reduce rates of reimbursement.

The Company’s profitability depends on payments provided by third-party payors. Competition for patients, efforts by traditional third party payors to contain or reduce healthcare costs and the increasing influence of managed care payors, such as health maintenance organizations, have resulted in reduced rates of reimbursement in recent years. If continuing, these trends could adversely affect the Company’s results of operations unless it can implement measures to offset the loss of revenues and decreased profitability. In addition, changes in reimbursement policies of private and governmental third-party payors, including policies relating to the Medicare and Medicaid programs, could reduce the amounts reimbursed to the Company’s clients for the Company’s services provided through the Company, and consequently, the amount these clients would be willing to pay for the Company’s services. Also, under the MLR regulations included in the Affordable Care Act, it is possible that a portion of the fees our existing and prospective payors are contractually required to pay us and that do not qualify as 'incurred claims' may not be included as expenditures for activities that improve health care quality. Such a determination may make it more difficult for us to retain existing clients and/or add new clients, because our clients' or prospective clients' MLR may otherwise not meet the specified targets. This may reduce our net revenues and profit margins.

The Company is dependent upon its network of qualified providers and its provider agreements may be terminated at any time.

The development of a network of qualified providers is an essential component of our business strategy. The typical form of agreement from ancillary healthcare providers provides that these agreements may be terminated at any time by either party with or without cause. If these agreements are terminated, such ancillary healthcare providers could enter into new agreements with our competitors which would have an adverse effect on our ability to continue our business as it is currently conducted.

11

For any given claim, the Company is subject to the risk of paying more to the provider than it receives from the payor.

The Company’s agreements with its payors, on the one hand, and the service providers, on the other, are negotiated separately. The Company has complete discretion in negotiating both the prices it charges its payors and the financial terms of its agreements with the providers. As a result, the Company’s profit is primarily a function of the spread between the prices it has agreed to pay the service providers and the prices the Company’s payors have agreed to pay the Company. The Company bears the pricing/margin risk because it is responsible for providing the agreed-upon services to its payors, whether or not it is able to negotiate fees and other agreement terms with service providers that result in a positive margin for the Company. For example, during 2010 and 2009, approximately 7% and 8% of claims were “loss claims” (that is, where the amount paid by the Company to the provider exceeded the amount received by the Company from the corresponding payor for that particular claim) and these loss claims, in the aggregate, comprised approximately $1.2 million in each year. There can be no assurances that the loss claim percentage will not be higher in future periods. If a higher percentage of the Company’s claims resulted in a loss, its results of operations and financial position would be adversely affected.

The Company has significantly increased in size and may not be able to effectively process the claims submitted by its providers in a timely manner.

Our size and the volume of claims has increased dramatically in the last few years. As a result, we have had to increase the size of our processing capabilities and our staff. If we are unable to effectively increase our processing speed and integrate new providers, we may be unable to process properly all claims submitted and this could have a negative impact on our relationships with clients, which in turn could lead to a loss of business.

An interruption of data processing capabilities and telecommunications could negatively impact the Company’s operating results.

Our business is dependent upon our ability to store, retrieve, process and manage data and to maintain and upgrade our data processing capabilities. An interruption of data processing capabilities for any extended length of time, loss of stored data, programming errors, other computer problems or interruptions of telephone service could have a material adverse effect on our business.

Changes in state and federal regulations could restrict our ability to conduct our business.

Numerous state and federal laws and regulations affect our business and operations. These laws and regulations include, but are not necessarily limited to:

• | Public Health Services Act, Patient Protection and Affordable Care Act and Health Care and Educational Affordability Reconciliation Act; |

• | healthcare fraud and abuse laws and regulations, which prohibit illegal referral and other payments; |

• | the Employee Retirement Income Security Act of 1974 and related regulations, which regulate many healthcare plans; |

• | mail pharmacy laws and regulations; |

• | privacy and confidentiality laws and regulations; |

• | consumer protection laws and regulations; |

• | legislation imposing benefit plan design restrictions; |

• | various licensure laws, such as managed care and third party administrator licensure laws; |

• | drug pricing legislation; |

• | Medicare and Medicaid reimbursement regulations; and |

• | Health Insurance Portability and Accountability Act of 1996. |

12

We believe we are operating our business in substantial compliance with all existing legal requirements material to the operation of our business. There are, however, significant uncertainties regarding the application of many of these legal requirements to our business, and there cannot be any assurance that a regulatory agency charged with enforcement of any of these laws or regulations will not interpret them differently or, if there is an enforcement action, that our interpretation would prevail.

If the Company fails to comply with the requirements of HIPAA, it could face sanctions and penalties.

HIPAA provides safeguards to ensure the integrity and confidentiality of health information. Violation of the standards is punishable by fines and, in the case of wrongful disclosure of individually identifiable health information, fines or imprisonment, or both. Although we intend to comply with all applicable laws and regulations regarding medical information privacy, failure to do so could have an adverse effect on our business.

Limited barriers to entry into the ancillary healthcare services market could result in greater competition.

There are limited barriers to entering our market, meaning that it is relatively easy for other companies to replicate our business model and provide the same or similar services that we currently provide. Major benefit management companies and healthcare companies not presently offering ancillary healthcare services may decide to enter the market. These companies may have greater financial, marketing and other resources than are available to us. Competition from other companies may have a material adverse effect on our financial condition and results of operations.

The Company may be unsuccessful in hiring and retaining skilled employees.

The future growth of our business depends on our ability to hire and retain skilled employees. The Company may be unable to hire and retain the skilled employees needed to succeed in our business. Qualified employees are in great demand throughout the healthcare industry. Our failure to attract and retain sufficient skilled employees may limit the rate at which our business can grow, which will result in harm to our financial performance.

An inability to adequately protect our intellectual property could harm the Company’s competitive position.

We consider our methodologies, processes and know-how to be proprietary. We seek to protect our proprietary information through confidentiality agreements with our employees, as well as our clients and contracted service providers. The Company’s policy is to have its employees enter into a confidentiality agreement at the time employment begins, with the confidentiality agreement containing provisions prohibiting the employee from disclosing our confidential information to anyone outside of the Company, requiring the employee to acknowledge, and, if requested, assist in confirming the Company’s ownership of new ideas, developments, discoveries or inventions conceived by the employee during his or her employment with the Company, and requiring the assignment by the employee to the Company of proprietary rights to such matters that are related to our business. There can be no assurance that the steps taken by the Company to protect its intellectual property will be successful. If the Company does not adequately protect its intellectual property, its competitors may be able to use its technologies and erode or negate the Company’s competitive advantage in the market.

Fluctuations in the number and types of claims processed by the Company could make it more difficult to predict the Company’s net revenues from quarter to quarter.

Monthly fluctuations in the number of claims we process and the types of claims we process will impact the quarterly and annual results of the Company. Our margins vary depending on the type of ancillary healthcare service provided, the rates associated with those services and the overall mix of these claims, each of which will impact our profitability. Consequently, it may be difficult to predict our net revenue from one quarter to another quarter.

13

Future sales of the Company’s Common Stock, or the perception that these sales may occur, could depress the price of the Company’s Common Stock.

Sales of substantial amounts of our Common Stock, or the perception in the public that such sales may occur, could cause the market price of the Company’s Common Stock to decline. This could also impair the Company’s ability to raise additional capital through the sale of equity securities. As of March 14, 2011, the Company had 16,922,042 shares of its Common Stock outstanding. The outstanding shares are either freely tradable without restriction or further registration under the Securities Act, unless the shares are held by one of our “affiliates” as such term is defined in Rule 144 of the Securities Act, or are “restricted shares” as that term is defined under the Securities Act, and may be sold from time to time pursuant to a registration statement which was declared effective on February 8, 2007 by the Securities and Exchange Commission (the “SEC”), or in reliance upon an exemption from registration available under the Securities Act. At March 14, 2011, warrants to purchase 225,000 shares of Common Stock of the Company were outstanding, and options to purchase 2,603,167 shares of Common Stock of the Company had been granted and were outstanding under the Company’s Amended and Restated 2005 Stock Option Plan and the 2009 Equity Incentive Plan. At March 14, 2011, restricted stock units (“RSUs”) relating to 85,873 shares of common stock were outstanding under our 2009 Equity Incentive Plan. In addition, an aggregate of 1,499,113 shares of the Common Stock of the Company remain available for future grants of RSUs and options to purchase shares of the Common Stock of the Company under the Company’s Amended and Restated 2005 Stock Option Plan and the 2009 Equity Incentive Plan. If all of the outstanding warrants are exercised, all options available under the Company’s Amended and Restated 2005 Stock Option Plan are issued and exercised and all RSUs are converted, there will be approximately 21,335,195 shares of Common Stock of the Company outstanding.

Some of our existing stockholders can exert control over us and may not make decisions that further the best interests of all stockholders.

As of March 14, 2011, our officers, directors and principal stockholders (greater than 5% stockholders) together control beneficially approximately 46.0% of the outstanding Common Stock of the Company. As a result, these stockholders, if they act individually or together, may exert a significant degree of influence over our management and affairs and over matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions. Furthermore, the interests of this concentration of ownership may not always coincide with our interests or the interests of other stockholders and, accordingly, they could cause us to enter into transactions or agreements which we would not otherwise consider. In addition, this concentration of ownership of the Company’s Common Stock may delay or prevent a merger or acquisition resulting in a change in control of the Company and might affect the market price of our Common Stock, even when such a change in control may be in the best interest of all of our stockholders.

We are subject to the listing requirements of the Nasdaq Capital Market and there can be no assurances that we will continue to satisfy these listing requirements.

Our common stock is listed on The NASDAQ Capital Market, and we are therefore subject to continued listing requirements, including requirements with respect to the market value of publicly-held shares and minimum bid price per share, among others, and requirements relating to board and audit committee independence. If we fail to satisfy one or more of the requirements, we may be delisted from The NASDAQ Capital Market. If we are delisted from The NASDAQ Capital Market and we are not able to list our common stock on another exchange, our common stock could be quoted on the OTC Bulletin Board or on the “pink sheets”. As a result, we could face significant adverse consequences including, among others, a limited availability of market quotations for our securities and a decreased ability to issue additional securities or obtain additional financing in the future.

Item 2. Properties.

The Company occupies a total of 16,449 square feet of office space, all of which is leased. The leased space comprises our principal executive offices, which is located at 5429 Lyndon B. Johnson Freeway, Suite 850, Dallas, TX 75240, pursuant to a lease that expires on March 31, 2013. Included in the 16,449 square feet are 7,100 square feet of space added to our original lease by means of an amendment to the lease executed in February 2009. The Company does not own or lease any other real property and believes its offices are suitable to meet its current needs.

Item 3. Legal Proceedings.

None.

Item 4. Reserved.

14

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market Information

The Company’s Common Stock has traded on The NASDAQ Capital Market (“NASDAQ”) under the symbol ANCI since September 29, 2008. Between October 19, 2006 and September 26, 2008, our stock traded on the American Stock Exchange (“Amex”) under the symbol XSI and between December 28, 2005 and October 19, 2006, public trading of our Common Stock occurred on the OTC Bulletin Board.

The following table sets forth, for the fiscal periods indicated, the range of the high and low sales prices for our Common Stock on NASDAQ from January 1, 2009 through December 31, 2010.

High | Low | |||||

2010 | ||||||

Fourth Quarter Ended December 31 | $ | 1.62 | $ | 1.30 | ||

Third Quarter Ended September 30 | 1.69 | 1.31 | ||||

Second Quarter Ended June 30 | 2.20 | 1.55 | ||||

First Quarter Ended March 31 | 2.91 | 1.46 | ||||

2009 | ||||||

Fourth Quarter Ended December 31 | $ | 4.49 | $ | 1.95 | ||

Third Quarter Ended September 30 | 4.73 | 3.57 | ||||

Second Quarter Ended June 30 | 8.74 | 3.50 | ||||

First Quarter Ended March 31 | 8.18 | 6.40 | ||||

The closing price on NASDAQ for our Common Stock on March 14, 2011 was $1.70.

Holders

As of March 14, 2011, in accordance with the records of our transfer agent, there were 137 record holders of ACS Common Stock. The number of record holders is based on the actual number of holders registered on the books of our transfer agent and does not reflect holders of shares in “street name” or persons, partnerships, associations, corporations or other entities identified in security position listings maintained by depository trust companies.

Dividends

We have not declared cash dividends on our Common Stock. We intend to retain all earnings to finance future growth and do not anticipate that we will pay cash dividends for the foreseeable future.

Securities Authorized for Issuance Under Equity Compensation Plans

The information required to be disclosed herein is incorporated by reference to "Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters."

Repurchases of Securities

There were no repurchases of the Common Stock of the Company by or on behalf of the Company or any affiliated purchasers during the fourth quarter of the Company’s fiscal year ended December 31, 2010.

15

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion should be read in conjunction with our consolidated financial statements, which present our results of operations for the twelve month periods ended December 31, 2010 and 2009 as well as our financial position at December 31, 2010 and 2009, contained elsewhere in this Annual Report on Form 10-K. Some of the information contained in this discussion and analysis or set forth elsewhere in this Annual Report on Form 10-K, including information with respect to our plans and strategy for our business, includes forward-looking statements that involve risks and uncertainties. You should review the “Special Note Regarding Forward Looking Statements” and “Risk Factors” sections of this Annual Report for a discussion of important factors that could cause actual results to differ materially from the results described in or implied by the forward-looking statements contained in the following discussion and analysis.

Overview

American CareSource Holdings, Inc. (“ACS,” “Company,” the “Registrant,” “we,” “us,” or “our”) is an ancillary services company that offers cost effective access to a comprehensive national network of ancillary healthcare service providers. The Company sells its services to a number of healthcare companies including preferred provider organizations ("PPOs"), third party administrators (“TPAs”), insurance companies, large self-funded organizations and various employee groups. The Company offers payors this solution by:

• | lowering its payors’ ancillary care costs throughout our network of high quality, cost effective providers that the Company has under contract at more favorable terms than they could generally obtain on their own; |

• | providing payors with a comprehensive network of ancillary healthcare services providers that is tailored to each payor’s specific needs and is available to each payor’s covered persons for covered services; |

• | providing payors with claims management, reporting and processing and payment services; |

• | performing network/needs analysis to assess the benefits to payors of adding additional/different service providers to the payor -specific provider networks; and |

• | credentialing network service providers for inclusion in the payor -specific provider networks. |

The Company’s business model, illustrating the relationships among the persons involved, directly or indirectly, in the Company’s business and its generation of revenue and expenses is depicted below:

16

Payors route healthcare claims to us after service has been performed by participant providers in our network. We process those claims and charge the payor according to its contractual rate for the services according to our contract with the payor. In processing the claim, we are paid directly by the payor or the insurer for the service. We then pay the provider of service according to its independently-negotiated contractual rate. We assume the risk of generating positive margin, the difference between the payment we receive for the service and the amount we are obligated to pay the provider of service.

The Company recognizes revenues for ancillary healthcare services when services by providers have been authorized and performed, the claim has been billed to the payor and collections from payors are reasonably assured. Cost of revenues for ancillary healthcare services consist of amounts due to providers for providing ancillary health care services, client administration fees paid to our client payors to reimburse them for routing the claims to us for processing, and the Company’s related direct labor and overhead of processing invoices, collections and payments. The Company is not liable for costs incurred by independent contract service providers until payment is received by it from the payors. The Company recognizes actual or estimated liabilities to independent contract service providers as the related revenues are recognized.

During 2010, we added thirteen new clients, which generated revenue of $5.9 million. 2010 was the second consecutive strong year in terms of sales as we generated $6.0 million from new clients in 2009. Despite the new clients, our overall net revenue was down 10% as compared to 2009 directly related to the continued declines in our two largest clients, both of which are PPOs. The Company is seeking growth in the number of client payors and service provider relationships it secures by focusing on providing in-network services for its payors and aggressively pursuing additional TPAs and other direct payors as its primary sales targets. The Company believes this strategy should increase the volume of claims the Company can process in addition to the expansion in the number of lives that are eligible to receive ancillary health care benefits. No assurances can be given that the Company can expand its service provider or payor relationships, nor that any such expansion will result in an improvement in the results of operations of the Company.

In addition, under the MLR regulations included in the Affordable Care Act, it is possible that a portion of the fees our existing and prospective payors are contractually required to pay us and that do not qualify as 'incurred claims' may not be included as expenditures for activities that improve health care quality. Such a determination may make it more difficult for us to retain existing clients and/or add new clients, because our clients' or prospective clients' MLR may otherwise not meet the specified targets. This may reduce our net revenues and profit margins..

Year Ended December 31, 2010 Compared to Year Ended December 31, 2009

Net Revenues