Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Lantheus Medical Imaging, Inc. | a11-7522_28k.htm |

| EX-4.1 - EX-4.1 - Lantheus Medical Imaging, Inc. | a11-7522_2ex4d1.htm |

| EX-99.1 - EX-99.1 - Lantheus Medical Imaging, Inc. | a11-7522_2ex99d1.htm |

| EX-99.3 - EX-99.3 - Lantheus Medical Imaging, Inc. | a11-7522_2ex99d3.htm |

Exhibit 99.2

Except from Preliminary Offering Memorandum

Overview

We are a leading specialty pharmaceutical company that develops, manufactures and distributes innovative diagnostic medical imaging products on a global basis. Our current imaging agents primarily assist in the diagnosis of heart, vascular and other diseases using nuclear imaging, echocardiography and magnetic resonance imaging (“MRI”) technologies. We also have a full clinical and preclinical development pipeline of next-generation and first-in-class products that use Positron Emission Tomography (“PET”) and MRI technologies. We believe that our products offer significant benefits to patients, healthcare providers and the overall healthcare system. As a result of more accurate diagnosis of disease, we believe our products allow healthcare providers to make more informed patient care decisions, potentially improving outcomes, reducing patient risk and decreasing costs for payors and the entire healthcare system.

Our principal branded products include DEFINITY, TechneLite, Cardiolite and Ablavar, which, in the aggregate, accounted for approximately 74% of our total revenues in 2010. For the year ended December 31, 2010, we generated total revenues, net income and Adjusted EBITDA of $354.0 million, $5.0 million and $85.2 million, respectively.

· DEFINITY. DEFINITY Vial for (Perflutren Lipid Microsphere) Injectable Suspension is the leading ultrasound contrast agent used in ultrasound exams of the heart, also known as echocardiographic exams. DEFINITY consists of gas-filled micro bubbles and is indicated in the United States for use in patients with suboptimal echocardiograms to opacify the left ventricular chamber of the heart and to improve the delineation of the left endocardial border of the heart. We estimate 20% of the approximately 25 million annual echocardiograms performed each year are suboptimal, which may require additional, more expensive testing. In September 2010, we filed an application with the U.S. Food and Drug Administration (“FDA”) for label expansion to include DEFINITY’s use in exercise and pharmacological stress as well as rest echocardiographic procedures. We launched DEFINITY in 2001, with the last patent in the United States currently expiring in 2016 and in numerous foreign jurisdictions in 2019. We estimate that DEFINITY has been used in approximately 2% of total echocardiograms performed in 2010. As we better educate the physician and healthcare provider community about the risks and benefits of this product, we believe we will experience further penetration of suboptimal echocardiograms. Since the relaunch of DEFINITY in June 2008 following the issuance by the FDA of a revised boxed warning on the product, U.S. sales of DEFINITY have continued to increase. DEFINITY sales have grown by approximately 417% as measured by comparing the first quarter of 2008 with the fourth quarter of 2010. In the year ended December 31, 2010, DEFINITY sales grew at a rate of approximately 40% from the year ended December 31, 2009. For the year ended December 31, 2010, DEFINITY generated total revenues of $60.0 million, and DEFINITY accounted for approximately 4%, 12% and 17% of our total revenues in 2008, 2009 and 2010, respectively.

· TechneLite. TechneLite is a technetium-based generator which provides the essential medical isotope used by radiopharmacies to radiolabel Cardiolite and other Tc-99m-based radiopharmaceuticals used

in nuclear medicine procedures. The generator consists of a glass column with fission-produced Moly adsorbed on alumina powder within the column. The terminally sterilized and sealed column is enclosed in a lead shield which is further sealed in a cylindrical plastic container. Cardiolite and other radiopharmaceuticals are activated by combining them with technetium, a daughter product of radio-decaying Moly, which has been eluted from the generator. For the year ended December 31, 2010, TechneLite generated total revenues of $122.0 million and accounted for approximately 23%, 31% and 34% of our total revenues in 2008, 2009 and 2010, respectively.

· Cardiolite. Cardiolite (Kit for Preparation of Technetium Tc99m Sestamibi for Injection), also known by its generic name as “sestamibi,” is a technetium-based radiopharmaceutical used in Single Photon Emission Computed Tomography (“SPECT”) myocardial perfusion imaging (“MPI”) procedures. Cardiolite is primarily used for detecting coronary artery disease. As of December 31, 2010, Cardiolite had been used to image more than 40 million patients. Cardiolite was approved by the FDA in 1990 and its market exclusivity expired in July 2008. In September 2008, the first of several competing generic products was launched, and while we have faced significant pricing pressure and have experienced a loss in share, we continue to price Cardiolite at a declining premium and have been able to retain share because of strong awareness and loyalty within the cardiology community, as well as our strong relationships with various distribution partners. We believe that Cardiolite was the MPI segment leader with approximately one-third share for 2010, while Myoview (a GE Healthcare product), had an estimated 26% share, Thallium (an older MPI agent also sold by us, among other companies) had an estimated 18% share, and generic sestamibi had an estimated 24% share. For the year ended December 31, 2010, Cardiolite generated total revenues of $77.4 million, and Cardiolite accounted for approximately 60%, 33% and 22% of our total revenues in 2008, 2009 and 2010, respectively.

· Ablavar. Ablavar is a gadolinium-based contrast agent indicated to evaluate aortoiliac occlusive disease in adults with known or suspected peripheral vascular disease and is the first contrast agent approved for a magnetic resonance angiography (“MRA”) indication in the United States. We purchased the U.S., Canadian and Australian rights to Ablavar from EPIX Pharmaceuticals, Inc. (“EPIX”) in April 2009, and we formally launched Ablavar in the United States in January 2010. We purchased the rest of the world rights to Ablavar from EPIX in June 2010. To date, the market acceptance of this agent has been slower than we initially anticipated. While we believe that Ablavar is superior to its competitors based on both safety and efficacy, the blood pool imaging attributes of the agent require extensive customer education and training to facilitate product adoption. Compared to other MRA contrast agents, Ablavar binds to human serum albumin, resulting in prolonged blood retention which facilitates imaging of the arteries, produces improved high-resolution images and assists in the identification of blood flow restrictions. As a result, Ablavar requires a lower dose than most other gadolinium-based agents to obtain a high-resolution image.

· Other Products. Our remaining product portfolio constituted approximately 26% of our total revenues in 2010. These products are important agents in specific segments, which provide a stable base of recurring revenue and have a favorable industry position as a result of our substantial infrastructure investment, our specialized workforce, our technical know-how and our established industry position and customer relationships. These products include:

· Neurolite, an injectable SPECT brain perfusion agent used to assist in stroke imaging;

· Thallium, an injectable used in MPI studies using either planar or SPECT techniques for the diagnosis and localization of myocardial infarction;

· Xenon Xe133 Gas, an inhaled gas used to assess pulmonary function and also for imaging blood flow, particularly in the brain;

· Gallium, an injectable useful in demonstrating the presence of certain cancers; and

· Samarium, an injectable used to treat severe bone pain associated with certain kinds of cancer.

We distribute our products in the United States and internationally through radiopharmacies, distributor relationships and our direct sales force. In the United States, our nuclear imaging products are primarily distributed through radiopharmacies, including Cardinal, UPPI and GE Healthcare. We have a strong distribution network and have long-term relationships with Cardinal and UPPI, who together accounted for what we estimate to be approximately 85% of SPECT doses sold by radiopharmacies in the United States in 2010, based on the percentage of doses sold in the first half of 2010. In addition, we both own radiopharmacies and sell directly to end-users in Canada, Puerto Rico and Australia. In the rest of the world, including Europe, Asia and Latin America, we utilize distributor relationships to distribute our products. In July 2010, we announced a new distribution arrangement for DEFINITY in India, a market which we believe has strong growth potential.

To supplement our portfolio of marketed products, we have an experienced research and development (“R&D”) team with expertise across the discovery, preclinical and clinical development continuum, including Phase 4 post-marketing studies. We currently have three products in development:

· a PET myocardial perfusion agent, flurpiridaz F-18 (formerly known as BMS747158-2), which we expect will commence Phase 3 clinical trials in the second quarter of 2011 and which we believe has the potential to become a leading next-generation myocardial perfusion agent;

· a PET cardiac neuronal imaging agent, (18)F LMI1195, which recently completed Phase 1 clinical trials, we believe has the potential to identify patients that would benefit from implantation of an implantable cardioverter defibrillator (“ICD”) in order to decrease risk of sudden cardiac death (“SCD”); and

· a vascular remodeling imaging agent, BMS 753951, currently in preclinical lead optimization which we believe has the potential for identifying vulnerable plaque located in the cardiovascular system.

All three of these products were developed in-house and are protected by patents or patent applications we own in the United States and numerous foreign jurisdictions.

Our Competitive Strengths

We believe that our industry position, business model, proven results, reputation for innovation and quality, clinical development capabilities, strong physician relationships and distribution arrangements provide us with a strong platform to reach our strategic goal, which is to provide cost effective, beneficial tools to physicians to improve patient care. Our competitive strengths include:

Established Leader in the Diagnostic Medical Imaging Industry

We are a pioneer in nuclear cardiology and a leader in the diagnostic medical imaging industry. We believe we are recognized throughout the industry for the development or commercialization of important diagnostic agents including DEFINITY, Cardiolite and TechneLite. Historically, we were the first to commercialize Thallium, the first MPI agent, in 1977. We launched Cardiolite, the best-selling radiopharmaceutical in history (over $4 billion in cumulative sales) in 1991. We launched DEFINITY, the leading cardiac ultrasound contrast agent, in 2001. We pioneered the terminally-sterilized TechneLite technetium-based generator, and we were the first to launch an FDA-approved MRA contrast agent in the United States—Ablavar in 2010. We believe we also have a proven track record of on-time delivery and a reputation as a high-quality and reliable provider, which we believe positions our products favorably with customers, key opinion leaders and professional societies. We have established strong sales and market share for a number of our leading products and believe that we are well-positioned to meet the changing demands of the industry.

Leading R&D Expertise and Branded Intellectual Property

We have an experienced R&D team with a wide range of capabilities from discovery through clinical development, including Phase 4 post-marketing studies. We believe that our R&D expertise, particularly utilizing radioisotopes and nuclear materials, will enable us to continue our track record of innovation and to develop both next-generation and first-in-class products. In addition, the nature of R&D in diagnostic imaging products provides an ability to typically determine proof of concept much earlier in the development process than many other pharmaceutical products. The results of our R&D efforts are evidenced by our development pipeline of three new products. We believe that each of these products represents large market opportunities and has the potential to significantly enhance current imaging methods or to fulfill currently unmet diagnostic medical imaging needs. We own patents and patent applications for DEFINITY, TechneLite and our three pipeline products, all three of which were discovered and developed in-house. In addition, we own patent rights to Ablavar, in the United States and numerous foreign jurisdictions, with the last U.S. patent not expiring until 2017, and, assuming we are granted our request for regulatory extension in the United States, not until 2020. Patent protection for our leading pipeline product would not expire in the United States until 2026. Patent protection relating to one of the remaining pipeline products, if granted, would not expire until 2027 and, for another, if granted, would not expire until 2029. In aggregate, we have an extensive and valuable portfolio of 373 issued patents and 101 pending patent applications as of February 28, 2011.

Complex Manufacturing Capabilities and Skilled Personnel

Our expertise in the design, development and validation of complex manufacturing systems and processes that our products require, as well as our track record of just-in-time manufacturing, has enabled us to become a leader in the diagnostic medical imaging industry. Regulatory requirements for the handling of nuclear materials are stringent. We have a highly experienced workforce and the technical expertise to manufacture and distribute radioactive products both safely and reliably.

Part of the Healthcare Solution

We believe that diagnostic medical imaging should play an important role in the ongoing transformation of the U.S. healthcare system, and that our products should be part of the solution to the dual challenges of improved outcomes and reduced costs. By improving the diagnosis of disease, we believe our products allow healthcare providers to make more informed and better therapeutic decisions for their patients. Consequently, we believe more patients will receive more appropriate levels of care, potentially improving outcomes, reducing patient risk and decreasing costs for payors and the entire healthcare system. We are engaged in extensive outreach and education efforts with political decision makers and policy experts to advocate this message.

Favorable Industry Trends

The diagnostic medical imaging industry continues to grow as a result of favorable demographic trends. According to GIA, sales of diagnostic medical imaging agents in North America were estimated to have grown at a compound annual growth rate of 9.0% from 2005 to 2010, and are projected to grow at a compound annual growth rate of 6.7% from 2010 to 2015. Several demographic trends drive an increasing demand for diagnostic medical imaging procedures, including the aging of the population and the increased incidence and prevalence of obesity and cardiovascular disease. Heart disease is currently the leading cause of death for both women and men in the United States, and according to Frost & Sullivan, from 2009 to 2012, the U.S. population with coronary artery disease is expected to grow at a compound annual growth rate of 5.3%. The need for early detection and effective treatment drives the demand for diagnostic services, which we believe will drive volume growth for our products.

Diversified Moly Supply Chain

In response to the recent global Moly supply shortage, we have diversified our global supply chain, including significantly expanding sourcing from South Africa and Belgium, and pursuing additional global solutions. In 2009, we entered into an agreement with NTP Radioisotopes (Pty) Ltd. (“NTP”) in South Africa to supply us with Moly manufactured from the SAFARI reactor in South Africa. NTP, in turn, has partnered with Institute for Radioelements (“IRE”) in Belgium to co-supply us from the Belgian Reactor 2 (“BR2”), the high flux reactor (“HFR”) located in The Netherlands and the OSIRIS reactor located in France, and more recently the Australian Nuclear Science and Technology Organisation (“ANSTO”) in Australia. This diversified supply improves our ability to continue to manufacture and sell technetium generators during periods when a particular reactor may be shut down. In an effort to continue diversifying our Moly supply chain, we are pursuing additional sourcing arrangements from potential new producers around the world.

We do not believe that recent events happening at nuclear power reactors in Japan will have any impact on our Moly supply because the reactors that produce Moly are not nuclear power reactors, but nuclear research reactors which are smaller, cooler and inherently safer. However, we cannot assure you that there will not be an unanticipated impact on our Moly suppliers. See “Risk Factors—The global supply of Moly is fragile and not stable. Our dependence on a limited number of third party suppliers for Moly could prevent us from delivering our products to our customers in the required quantities, within the required timeframe, or at all, which could result in order cancellations and decreased revenues.”

Strong Financial Profile

Historically, we have generated strong free cash flow, which is driven primarily by our significant operating margins, minimal maintenance capital expenditure requirements and favorable working capital dynamics. This has allowed us to repay a significant portion of our debt obligations prior to their maturity dates and provided us with the available liquidity to pursue key business development initiatives. On May 10, 2010, we completed a private offering of $250.0 million in aggregate principal amount of our existing 9.750% Senior Notes due 2017, and with the proceeds, among other things, retired the balance of the loan that was used to finance the Acquisition. Since the Acquisition, we have funded an expansive clinical development program, repaid the $296.5 million acquisition loan, redeemed approximately $160 million of Preferred Stock and paid for the $32.8 million acquisition of Ablavar patents and related assets with a combination of approximately equal amounts of cash from operations and new external debt. We ended 2010 with $75.5 million of liquidity, including $42.5 million of capacity under our revolving credit facility and $33.0 million of cash. The strength of our product portfolio, as evidenced by our leading position across most diagnostic modalities in which we participate, has contributed to our strong historical financial performance. We have historically and will continue to rely on our arrangements with leading distributors of radiopharmaceuticals for sales of our radiopharmaceutical products, providing cash flow stability and availability for deleveraging or funding of other future growth initiatives.

Stable, Experienced Management Team

Our senior management team has an average of approximately 25 years of healthcare industry experience and consists of industry leaders with significant expertise in product development and commercialization. Our management team is led by Don Kiepert, Chief Executive Officer and President, who has more than 35 years of healthcare industry experience. In addition, several top executives have been with us and our predecessors for more than 20 years. We believe that the strength of our management team demonstrates our expertise within the diagnostic medical imaging industry and our ability to operate in a highly regulated environment.

Business Strategy

Our objective is to enhance our position as a leading specialty pharmaceutical company. We believe that our long and distinguished history of innovation and our development and commercialization expertise in diagnostic medical imaging agents provide a strong foundation on which to grow our business. With fully integrated research, clinical and commercial operations, our growth strategy is focused around the following core initiatives:

Maximize Existing Product Portfolio

We compete primarily on the ability of our products to capture market share and generate free cash flow through their proven efficacy, reliability and safety, as well as our efficient manufacturing processes, distribution network, customer service and field sales organization. We believe our product characteristics and core competencies distinguish us from our competitors. We utilize our expertise in the design, development and validation of complex manufacturing systems and processes related to diagnostic medical imaging to ensure quality control and reliable delivery. We have historically achieved on-time delivery with available supply 98% of the time and have a proven track record of responding effectively to significant production increases due to fluctuations in demand. We believe our manufacturing facilities meet best-in-class compliance standards and support just-in-time manufacturing. To complement our manufacturing strength, we have a strong distribution network, multi-year distribution arrangements, diversified supplier relationships, strong brand awareness and loyalty in the cardiology community. We expect continued focus on these proven strategies to maintain or increase our revenues for most of our products. The strong free cash flow generated from these strategies allows us to invest in key R&D and business development initiatives.

Maintain Disciplined R&D Investments

For the year ended December 31, 2010, our R&D investment represented approximately 13% of our total revenues and provides our R&D organization with the resources to continue discovering and developing new diagnostic agents. We maintain full R&D capabilities from discovery through clinical development. Our disciplined approach has created a strong pipeline of three products which were developed in-house and are protected by patents and patent applications we own in the United States and numerous foreign jurisdictions. We believe a strong market opportunity exists for each of these potential products:

· We are currently developing flurpiridaz F-18, which we believe has the potential to become the leading next-generation myocardial perfusion agent. The application of PET technology in myocardial perfusion imaging represents a broad, emerging application for a technology typically associated with oncology and neurology. We expect to commence our Phase 3 clinical trials for flurpiridaz F-18 in the second quarter of 2011. Market exclusivity for this candidate would currently expire in the United States in 2026. We believe there is great potential for this agent as we believe PET adoption could increase significantly.

· We have finished Phase 1 trials for 18F LMI1195, a cardiac neuronal imaging agent being developed to help more accurately identify patients who need ICDs to decrease the risk of SCD. SCD claims as many as 450,000 lives every year in the United States. The cost of an ICD procedure, at $56,000 to $102,000 per procedure, is expensive and approximately 14 implants are needed over a five-year period to save one life. As a result, we believe patients and the healthcare system will both benefit from the ability to more accurately identify patients who will benefit from an ICD placement. We anticipate that market exclusivity for this potential product, if granted, would expire in 2027.

· We are also currently developing BMS 753951, a gadolinium-based MRI agent currently in lead optimization preclinical studies, to identify patients at risk of SCD for coronary plaque rupture. This method is non-invasive and images the arterial vessel wall allowing direct detection of plaque (in

contrast to angiography that images the lumen or open space within the artery). According to the American Heart Association, 309,000 deaths per year occur outside the hospital due to coronary artery disease, and a majority of the deaths occur in people with undiagnosed coronary artery disease because of the limitations of current diagnostic techniques.

We believe that these initiatives will enable us to further enhance our role as a leader in diagnostic medical imaging.

Pursue Strategic Opportunities

We focus on a range of imaging agents, indications and diagnostic modalities to further strengthen and diversify our product mix and business. We leverage our commercial team, R&D experience, proprietary technology and expertise in diagnostic medical imaging to identify and enter into complementary business relationships, positioning us to be a partner of choice for in-licensing arrangements and acquisition opportunities. In April 2009, we completed the acquisition of Ablavar patents and related assets from EPIX and in June 2010, we acquired the rest of the world rights to Ablavar. This acquisition expanded our portfolio of diagnostic medical imaging agents. We are also evaluating a number of other in-licensing and acquisition opportunities and will continue to do so in order to leverage our core competencies and create incremental value and growth.

Maintain Strong Physician Relationships

Throughout our over 50 years in business, we have established ourselves as a diagnostic medical imaging pioneer with a number of notable industry leading product introductions, including Thallium, TechneLite, Cardiolite, DEFINITY and Ablavar. These key product introductions were fostered by our sustained efforts to develop and maintain our strong relationships with physicians. Based on long positive experience, cardiologists, radiologists and nuclear medicine physicians trust our products to perform reliably, effectively and safely, and this relationship of trust has contributed to the historical and continued success of our key products. For example, despite the introduction of generic competition in September 2008, the strong brand awareness of Cardiolite among cardiologists, coupled with the agent’s track record for efficacy and safety, has led to strong, continued use of the branded product. Additionally, the strong relationship that cardiologists have with our products proved valuable when in October 2007, physicians within the cardiology and echocardiography communities, without our requesting them to do so, campaigned in support of DEFINITY to remove a boxed warning that the FDA had required be added to DEFINITY. The FDA subsequently revised the boxed warning in May 2008. When we launched Ablavar, we renewed our relationships with radiologists, discussing the benefits of our product and building on our strong relationships in the nuclear medicine and cardiology communities. Based on the sustained track record of our business, we believe these relationships are an important competitive advantage for our business and contribute to the success of our products.

Corporate History

Founded in 1956 as New England Nuclear Corporation, we were purchased by E. I. du Pont de Nemours and Company in 1981. BMS subsequently acquired the diagnostic medical imaging business as part of its acquisition of DuPont Pharmaceuticals in 2001. Avista acquired the medical imaging business from BMS in January 2008.

Our Sponsor

Avista is a leading private equity firm with offices in New York, NY, Houston, TX and London, UK. Founded in 2005 as a spin-out from the former DLJ Merchant Banking Partners (“DLJMB”) franchise, Avista’s strategy is to make controlling or influential minority investments primarily in growth-oriented energy, healthcare, media, consumer and industrial companies. Through its team of seasoned investment professionals and industry experts, Avista seeks to partner with exceptional management teams to invest in and add value to well-positioned businesses.

Recent Developments

Consent Solicitation

On March 4, 2011, we commenced a consent solicitation (the “Solicitation”) to holders of existing notes pursuant to a consent solicitation statement (the “Solicitation Statement”), dated March 4, 2011, in order to amend the indenture which governs the existing notes and under which the new notes will be issued. The Solicitation expired at 5:00 p.m., New York City time, on March 14, 2011 (the “Expiration Date”). The Solicitation sought to amend the restricted payments covenant of the indenture to allow us to use the net proceeds of the new notes as provided in “Use of Proceeds.”

As of the Expiration Date, we received consents from holders of 100% of existing notes and executed a supplemental indenture to amend the restricted payments covenant contained in the indenture to replace the consolidated leverage ratio test with a general $150.0 million restricted payments basket. The supplemental indenture will not become operative, and no Consent Payment (defined below) will be made, until the consummation of this offering of new notes and the satisfaction of the other conditions described in the Solicitation Statement.

Upon satisfaction or, where possible, waiver of the conditions set forth in the Solicitation Statement, including the consummation of this offering, we will make a cash payment (the “Consent Payment”) of $15 per $1,000 in principal amount of existing notes to each Holder of existing notes, as of March 2, 2011 at 5:00 p.m. New York City time.

Amendment to Revolving Credit Facility

In addition to the Solicitation, we received the consent of the lenders under our revolving credit facility to amend such agreement to allow us to use the net proceeds of the new notes as provided in “Use of Proceeds.” The amendment also increases the consolidated total leverage ratio to accommodate the additional $150.0 million of debt contemplated by this offering and decreases the consolidated interest coverage ratio to accommodate the associated increase in semi-annual interest payments. Additionally, it adjusts the effective interest rate for borrowings thereunder. The amendment is expected to be consummated concurrently with the consummation of this offering of new notes.

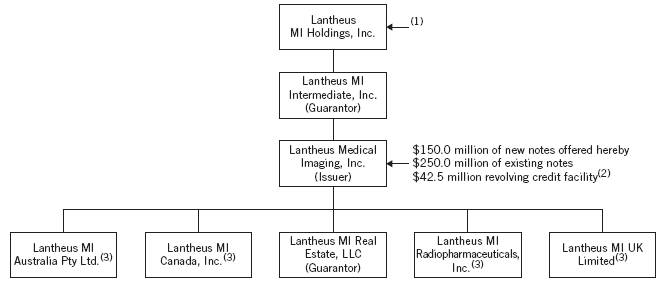

Corporate Structure

The following chart illustrates our ownership structure and principal indebtedness after giving effect to this offering and the use of proceeds therefrom:

(1) Prior to this offering, approximately $44.0 million of Series A preferred stock of Holdings (including accrued and unpaid dividends) was outstanding. As described in “Use of Proceeds,” we will dividend the net proceeds of this offering to Holdings, which will use a portion of such net proceeds to redeem all such preferred stock.

(2) See “Description of Other Indebtedness — Revolving Credit Facility.” As of the date of this offering memorandum, no amounts are outstanding under the revolving credit facility.

(3) Our non-U.S. subsidiaries will not guarantee the new notes.

Our Executive Offices

Our principal executive offices are located at 331 Treble Cove Road, North Billerica, Massachusetts 01862, and our telephone number at that address is (978) 671-8001. Our web site is www.lantheus.com. The information on our web site is not part of, and is not incorporated into, this offering memorandum.

Summary Consolidated Financial Data

The following table sets forth summary consolidated financial data for Lantheus Intermediate, our parent company and a guarantor of the notes, for the fiscal years ended December 31, 2008, 2009 and 2010 and as of December 31, 2010, which have been derived from the audited consolidated financial statements of Lantheus Intermediate included elsewhere in this offering memorandum.

The summary consolidated financial data set forth below and elsewhere in this offering memorandum are not necessarily indicative of our future performance. You should read this information together with “Capitalization,” “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the audited consolidated financial statements and related notes included elsewhere in this offering memorandum.

|

|

|

Year Ended December 31, |

| |||||||

|

|

|

2008 |

|

2009 |

|

2010 |

| |||

|

|

|

(dollars in thousands) |

| |||||||

|

Statement of Operations: |

|

|

|

|

|

|

| |||

|

Total revenues |

|

$ |

536,844 |

|

$ |

360,211 |

|

$ |

353,956 |

|

|

Cost of goods sold |

|

244,496 |

|

184,844 |

|

204,006 |

| |||

|

General and administrative expenses |

|

64,909 |

|

35,430 |

|

30,042 |

| |||

|

Sales and marketing expenses |

|

45,730 |

|

42,337 |

|

45,384 |

| |||

|

Research and development expense |

|

34,682 |

|

44,631 |

|

45,130 |

| |||

|

In-process research and development |

|

28,240 |

|

— |

|

— |

| |||

|

Operating income |

|

118,787 |

|

52,969 |

|

29,394 |

| |||

|

Interest expense |

|

(31,038 |

) |

(13,458 |

) |

(20,395 |

) | |||

|

Interest income |

|

693 |

|

73 |

|

179 |

| |||

|

Loss on early extinguishment of debt |

|

— |

|

— |

|

(3,057 |

) | |||

|

Other income, net |

|

2,950 |

|

2,720 |

|

1,314 |

| |||

|

Income before income taxes |

|

91,392 |

|

42,304 |

|

7,435 |

| |||

|

Provision for income taxes |

|

(48,606 |

) |

(21,952 |

) |

(2,465 |

) | |||

|

Net income |

|

$ |

42,786 |

|

$ |

20,352 |

|

$ |

4,970 |

|

|

Statement of Cash Flows Data: |

|

|

|

|

|

|

| |||

|

Net cash flows provided by (used in): |

|

|

|

|

|

|

| |||

|

Operating activities |

|

$ |

178,445 |

|

$ |

95,783 |

|

$ |

26,317 |

|

|

Investing activities |

|

(530,832 |

) |

(38,351 |

) |

(8,550 |

) | |||

|

Financing activities |

|

376,466 |

|

(49,102 |

) |

(17,550 |

) | |||

|

Other Financial Data: |

|

|

|

|

|

|

| |||

|

EBITDA(4) |

|

$ |

192,797 |

|

$ |

96,214 |

|

$ |

62,037 |

|

|

Adjusted EBITDA(4) |

|

253,882 |

|

104,060 |

|

85,228 |

| |||

|

Capital expenditures |

|

12,175 |

|

8,856 |

|

8,335 |

| |||

|

|

|

As of December 31, 2010 |

| ||||

|

|

|

Actual |

|

As Adjusted(1) |

| ||

|

|

|

(Dollars in thousands) |

| ||||

|

Balance Sheet and Other Data: |

|

|

|

|

| ||

|

Cash and cash equivalents |

|

$ |

33,006 |

|

$ |

26,656 |

|

|

Total assets |

|

495,881 |

|

494,381 |

| ||

|

Total long-term debt(2) |

|

250,000 |

|

396,250 |

| ||

|

Current portion of long-term debt |

|

— |

|

— |

| ||

|

Total stockholder’s equity |

|

153,434 |

|

3,434 |

| ||

|

Net debt(3) to Adjusted EBITDA(4) |

|

2.5x |

|

4.3x |

| ||

The following table sets forth the unaudited quarterly results for the fiscal year ended December 31, 2010 for Lantheus Intermediate, our parent company and a guarantor of the notes.

|

|

|

Three Months Ended |

|

Year Ended |

| |||||||||||

|

|

|

March 31, |

|

June 30, |

|

September 30, |

|

December 31, |

|

December 31, |

| |||||

|

|

|

(Dollars in thousands) |

| |||||||||||||

|

|

|

(unaudited) |

|

|

| |||||||||||

|

Total Revenues: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

United States: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Cardiolite |

|

$ |

13,856 |

|

$ |

11,306 |

|

$ |

12,163 |

|

$ |

13,082 |

|

$ |

50,407 |

|

|

Technelite |

|

19,761 |

|

21,708 |

|

35,765 |

|

31,028 |

|

108,262 |

| |||||

|

DEFINITY |

|

13,589 |

|

14,984 |

|

14,685 |

|

15,587 |

|

58,845 |

| |||||

|

Other currently marketed products |

|

11,416 |

|

12,792 |

|

12,103 |

|

10,921 |

|

47,232 |

| |||||

|

International: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Cardiolite |

|

7,096 |

|

6,213 |

|

5,925 |

|

7,781 |

|

27,015 |

| |||||

|

Technelite |

|

2,597 |

|

3,035 |

|

3,775 |

|

4,375 |

|

13,782 |

| |||||

|

DEFINITY |

|

333 |

|

229 |

|

322 |

|

239 |

|

1,123 |

| |||||

|

Other currently marketed products |

|

12,224 |

|

11,428 |

|

11,852 |

|

11,786 |

|

47,290 |

| |||||

|

Total revenues |

|

$ |

80,872 |

|

$ |

81,695 |

|

$ |

96,590 |

|

$ |

94,799 |

|

$ |

353,956 |

|

|

Adjusted EBITDA(1) |

|

$ |

19,953 |

|

$ |

18,133 |

|

$ |

21,989 |

|

$ |

25,153 |

|

$ |

85,228 |

|

(1) As adjusted amounts as of December 31, 2010 have been prepared to give effect to this offering and the use of proceeds therefrom.

(2) Total long-term debt consists of the new notes offered hereby and existing notes consisting of $250.0 million in aggregate principal amount of 9.750% senior notes due May 10, 2017, issued May 10, 2010, net of the $3.8 million fees related to the Solicitation, which will be amortized as an adjustment to interest expense over the remaining term of the debt.

(3) Net debt is a non-GAAP financial measure and is defined as total debt less cash and cash equivalents (other than any restricted cash).

(4) EBITDA is defined as net income plus interest, income taxes, depreciation and amortization. EBITDA is a measure used by management to measure operating performance. Adjusted EBITDA is defined as EBITDA further adjusted to exclude unusual items and other adjustments

required or permitted in calculating covenant compliance under the indenture governing the notes and our revolving credit facility. Adjusted EBITDA is also used by management to measure operating performance and by investors to measure a company’s ability to service its debt and meet its other cash needs. Management believes that the inclusion of the adjustments to EBITDA applied in presenting Adjusted EBITDA are appropriate to provide additional information to investors about our performance across reporting periods on a consistent basis by excluding items that we do not believe are indicative of our core operating performance. See “Non-GAAP Financial Measures.”

The following table provides a reconciliation of our net income to EBITDA and Adjusted EBITDA for the periods presented:

|

|

|

Year Ended December 31, |

|

Three Months Ended (Unaudited) |

| |||||||||||||||||

|

|

|

2008 |

|

2009 |

|

2010 |

|

March 31, |

|

June 30, |

|

September 30, |

|

December 31, |

| |||||||

|

|

|

(Dollars in thousands) |

| |||||||||||||||||||

|

Net income (loss) |

|

$ |

42,786 |

|

$ |

20,352 |

|

$ |

4,970 |

|

$ |

3,334 |

|

$ |

86 |

|

$ |

4,174 |

|

$ |

(2,624 |

) |

|

Interest expense, net |

|

30,345 |

|

13,385 |

|

20,216 |

|

2,466 |

|

4,588 |

|

6,760 |

|

6,402 |

| |||||||

|

Provision (benefit) for income taxes(a) |

|

46,131 |

|

20,392 |

|

1,215 |

|

2,312 |

|

(367 |

) |

1,501 |

|

(2,231 |

) | |||||||

|

Depreciation and amortization |

|

73,535 |

|

42,085 |

|

35,636 |

|

8,710 |

|

8,918 |

|

8,976 |

|

9,032 |

| |||||||

|

EBITDA |

|

192,797 |

|

96,214 |

|

62,037 |

|

16,822 |

|

13,225 |

|

21,411 |

|

10,579 |

| |||||||

|

Non-cash stock-based compensation |

|

1,368 |

|

1,209 |

|

1,634 |

|

143 |

|

433 |

|

(179 |

) |

1,237 |

| |||||||

|

Loss on early extinguishment of debt |

|

— |

|

— |

|

3,057 |

|

— |

|

3,057 |

|

— |

|

— |

| |||||||

|

Asset write-off(b) |

|

5,791 |

|

4,125 |

|

14,084 |

|

1,396 |

|

803 |

|

82 |

|

11,803 |

| |||||||

|

Inventory step-up expense(c) |

|

8,189 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| |||||||

|

Acquired in-process R&D(d) |

|

28,240 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| |||||||

|

Severance costs(e) |

|

13,775 |

|

— |

|

1,001 |

|

— |

|

130 |

|

— |

|

871 |

| |||||||

|

Transaction expenses(f) |

|

2,742 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| |||||||

|

Sponsor fee and other(g) |

|

980 |

|

1,060 |

|

1,090 |

|

250 |

|

250 |

|

250 |

|

340 |

| |||||||

|

Ablavar new manufacturer costs(h) |

|

— |

|

910 |

|

1,816 |

|

833 |

|

235 |

|

425 |

|

323 |

| |||||||

|

Ablavar launch costs(i) |

|

— |

|

542 |

|

509 |

|

509 |

|

— |

|

— |

|

— |

| |||||||

|

Adjusted EBITDA |

|

$ |

253,882 |

|

$ |

104,060 |

|

$ |

85,228 |

|

$ |

19,953 |

|

$ |

18,133 |

|

$ |

21,989 |

|

$ |

25,153 |

|

(a) Represents provision for income taxes less tax indemnification associated with an agreement with BMS.

(b) Represents non-cash losses incurred associated with the write-down of inventory and write-off of long-lived assets. The 2010 amount consists primarily of $10.9 million inventory write-down related to our Ablavar product. The 2009 amount is primarily related to the write-down of accessories related to our TechneLite product as a result of the global Moly shortage and Cardiolite inventory acquired from BMS. The 2008 amount was primarily related to our DEFINITY product as a result of the boxed warning in October 2007.

(c) Represents the revaluation of inventory as a result of the impact of purchase accounting in connection with the Acquisition.

(d) Represents in-process R&D relating to the Acquisition. Immediately following the closing of the Acquisition, the in-process R&D was expensed.

(e) In 2008, consists of severance costs relating to the closure of our European operations following the Acquisition. In 2010, consists of severance costs relating to one of our executive officers and a work force reduction in the fourth quarter.

(f) Represents legal, information technology and human resource advisory services and other advisory fees incurred in connection with the Acquisition.

(g) Represents annual sponsor monitoring fee and related expenses.

(h) Represents costs associated with establishing a second manufacturing source for Ablavar.

(i) Represents costs associated with the launch of Ablavar.