Attached files

| file | filename |

|---|---|

| EX-21 - EX-21 - LIN TELEVISION CORP | a2202711zex-21.htm |

| EX-32.2 - EX-32.2 - LIN TELEVISION CORP | a2202711zex-32_2.htm |

| EX-23.2 - EX-23.2 - LIN TELEVISION CORP | a2202711zex-23_2.htm |

| EX-31.1 - EX-31.1 - LIN TELEVISION CORP | a2202711zex-31_1.htm |

| EX-31.3 - EX-31.3 - LIN TELEVISION CORP | a2202711zex-31_3.htm |

| EX-23.3 - EX-23.3 - LIN TELEVISION CORP | a2202711zex-23_3.htm |

| EX-31.4 - EX-31.4 - LIN TELEVISION CORP | a2202711zex-31_4.htm |

| EX-31.2 - EX-31.2 - LIN TELEVISION CORP | a2202711zex-31_2.htm |

| EX-32.1 - EX-32.1 - LIN TELEVISION CORP | a2202711zex-32_1.htm |

| EX-23.1 - EX-23.1 - LIN TELEVISION CORP | a2202711zex-23_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2010 |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

LIN TV Corp.

(Exact name of registrant as specified in its charter)

Commission File Number: 001-31311

LIN Television Corporation

(Exact name of registrant as specified in its charter)

Commission File Number: 000-25206

| Delaware | Delaware | |

| (State or other jurisdiction of incorporation or organization) | (State or other jurisdiction of incorporation or organization) | |

05-0501252 |

13-3581627 |

|

| (I.R.S. Employer Identification No.) | (I.R.S. Employer Identification No.) |

One West Exchange Street, Suite 5A, Providence, Rhode Island 02903

(Address of principal executive offices)

(401) 454-2880

(Registrant's telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Class A common stock, par value $0.01 per share | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted to its corporate Web site, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding twelve months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes o No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates (based on the last reported sale price of the registrant's class A common stock on June 30, 2010 on the New York Stock Exchange) was approximately $297 million.

| Document Description | Form 10-K | |

|---|---|---|

| Portions of the Registrant's Proxy Statement on Schedule14A for the Annual Meeting of Stockholders to be held on May 24, 2011 | Part III |

DOCUMENTS INCORPORATED BY REFERENCE

NOTE:

This combined Form 10-K is separately filed by LIN TV Corp. and LIN Television Corporation. LIN Television Corporation meets the conditions set forth in general instruction I(1) (a) and (b) of Form 10-K and is, therefore, filing this form with the reduced disclosure format permitted by such instruction.

LIN TV Corp. Class A common stock, $0.01 par value, issued and outstanding as of March 7, 2011: 32,578,343 shares.

LIN TV Corp. Class B common stock, $0.01 par value, issued and outstanding as of March 7, 2011: 23,502,059 shares.

LIN TV Corp. Class C common stock, $0.01 par value, issued and outstanding as of March 7, 2011: 2 shares.

LIN Television Corporation common stock, $0.01 par value, issued and outstanding as of March 7, 2011: 1,000 shares.

2

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

This report contains certain forward-looking statements with respect to our financial condition, results of operations and business, including statements under the captions Item 1. "Business" and Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations". All of these forward-looking statements are based on estimates and assumptions made by our management, which, although we believe them to be reasonable, are inherently uncertain. Therefore, you should not place undue reliance upon such estimates or statements. We cannot assure you that any of such estimates or statements will be realized and actual results may differ materially from those contemplated by such forward-looking statements. Factors that may cause such differences include those discussed under the caption Item 1A. "Risk Factors", as well as the following:

- •

- volatility and periodic changes in our advertising revenues;

- •

- restrictions on our operations due to, and the effect of, our significant indebtedness;

- •

- our ability to continue to comply with financial debt covenants dependent on cash flows;

- •

- our guarantee of the General Electric Capital Corporation ("GECC") note;

- •

- effects of complying with accounting standards, including with respect to the treatment of our intangible assets;

- •

- inability or unavailability of additional debt or equity capital;

- •

- increased competition, including from newer forms of entertainment and entertainment media, changes in distribution

methods or changes in the popularity or availability of programming;

- •

- increased costs, including increased news and syndicated programming costs and increased capital expenditures as a result

of acquisitions or necessary technological enhancements;

- •

- effects of our control relationships, including the control that HM Capital Partners LLC ("HMC") and its affiliates

have with respect to corporate transactions and activities we undertake;

- •

- adverse state or federal legislation or regulation or adverse determinations by regulators, including adverse changes in,

or interpretations of, the exceptions to the FCC duopoly rule and the allocation of broadcast spectrum;

- •

- declines in the domestic advertising market;

- •

- further consolidation of national and local advertisers;

- •

- global or local events that could disrupt television broadcasting;

- •

- risks associated with acquisitions including integration of acquired businesses;

- •

- changes in television viewing patterns, ratings and commercial viewing measurement;

- •

- changes in our television network affiliation agreements;

- •

- changes in our retransmission consent agreements; and

- •

- seasonality of the broadcast business due primarily to political advertising revenues in even years.

Many of these factors are beyond our control. Forward-looking statements contained herein speak only as of the date hereof. We undertake no obligation to publicly release the result of any revisions to these forward-looking statements, to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

3

Overview

LIN TV Corp. ("LIN TV") is a local television and digital media company owning, operating or servicing 32 television stations and interactive television station and niche web sites in 17 U.S. markets. Our highly-rated stations deliver superior local news and community stories, along with top-rated sports and entertainment programming, to 9% of U.S. television homes, reaching an average of 9.9 million households per week. All of our television stations are affiliated with a national broadcast network and are primarily located in the top 75 Designated Market Areas ("DMA") as measured by Nielsen Media Research ("Nielsen"). We are a leader in the convergence of local broadcast television and the Internet through our television station web sites and a growing number of local interactive initiatives and Internet-based products and services. During 2010, we launched a new brand identity, LIN Media, to renew our market position and reflect our evolution to a leading multimedia company. In this report, the terms "Company," "we," "us" or "our" mean LIN TV Corp. and all subsidiaries included in our consolidated financial statements. Our class A common stock is traded on the New York Stock Exchange ("NYSE") under the symbol "TVL".

We provide free, over-the-air broadcasts of our programming 24 hours per day to the communities we are licensed to serve. We are committed to serving the public interest by making advertising time available to political candidates, by providing free daily local news coverage and making public service announcements.

We seek to have the largest local media presence in each of our local markets by combining strong network and syndicated programming with leading local news, and by pursuing our multi-channel strategy. This multi-channel strategy enables us to increase our audience share by operating multiple stations on multiple platforms in the same market. We currently deliver content over the air, on-line and on mobile applications. We also operate or service multiple stations in eleven of our markets.

Development of Our Business

Ownership and organizational structure

Our Company (including its predecessors) has owned and operated television stations since 1966 and was incorporated on February 11, 1998. A group of investors led by the predecessor of HMC acquired LIN Television Corporation ("LIN Television"), our wholly-owned subsidiary, on March 3, 1998 and was incorporated on June 18, 1990. On May 3, 2002, we completed our initial public offering and our class A common stock began trading on the NYSE. Our corporate offices are at One West Exchange Street, Suite 5A, Providence, Rhode Island 02903.

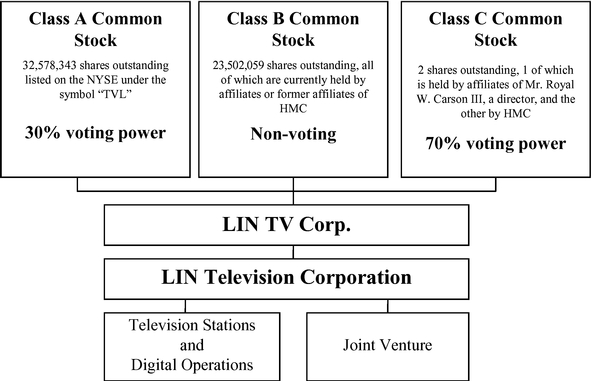

We have three classes of common stock. The class A common stock and the class C common stock are both voting common stock, with the class C common stock having 70% of the aggregate voting power. The class B common stock is held by affiliates of HMC and has no voting rights, except that without the consent of a majority of the class B common stock, we cannot enter into a wide range of corporate transactions.

This capital structure allowed us to issue voting stock while preserving the pre-existing ownership structure in which the class B stockholders did not have an attributable ownership interest in our television broadcast licenses pursuant to the rules of the Federal Communications Commission ("FCC").

4

The following diagram summarizes our corporate structure as of March 7, 2011:

All of the shares of our class B common stock are held by affiliates of HMC or former affiliates of HMC. The class B common stock is convertible into class A common stock or class C common stock in various circumstances. The class C common stock is also convertible into class A common stock in certain circumstances. If affiliates of HMC converted their shares of class B common stock into shares of class A common stock and the shares of class C common stock were converted into shares of class A common stock as of March 7, 2011, the holders of the converted shares of class C common stock would own less than 0.01% of the total outstanding shares of class A common stock and resulting voting power, and the affiliates of HMC would own 41.9% of the total outstanding shares of class A common stock and resulting voting power.

5

Our television stations

We own, operate or service 32 stations, including two stations pursuant to local marketing agreements, four stations pursuant to shared services agreements and one low-power station, which operates as a stand-alone station. We also have an equity investment in two other stations through a joint venture. The following table lists the stations that we own, operate or service, or in which we have an equity investment:

Market

|

DMA Rank(1) | Station | Primary Affiliation |

Digital Channel |

Status(2) | FCC license expiration |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Indianapolis, IN |

27 | WISH-TV(3) | CBS | 9 | 8/1/2013 | ||||||||||

|

WNDY-TV | MNTV | 32 | 8/1/2013 | |||||||||||

Hartford-New Haven, CT |

30 | WTNH-TV | ABC | 10 | 4/1/2015 | ||||||||||

|

WCTX-TV | MNTV | 39 | 4/1/2015 | |||||||||||

Columbus, OH |

34 | WWHO-TV | CW | 46 | 10/1/2013 | ||||||||||

Grand Rapids-Kalamazoo-Battle Creek, MI |

41 | WOOD-TV(3) | NBC | 7 | 10/1/2013 | ||||||||||

|

WOTV-TV | ABC | 20 | 10/1/2013 | |||||||||||

|

WXSP-CA | MNTV | Various | 10/1/2013 | |||||||||||

Norfolk-Portsmouth-Newport News, VA |

43 | WAVY-TV(3) | NBC | 31 | 10/1/2012 | ||||||||||

|

WVBT-TV | FOX | 29 | 10/1/2012 | |||||||||||

Austin, TX |

44 | KXAN-TV | NBC | 21 | 8/1/2014 | ||||||||||

|

KNVA-TV(3) | CW | 49 | LMA | 8/1/2014 | ||||||||||

|

KBVO-TV(4) | MNTV | 27 | 8/1/2014 | |||||||||||

Albuquerque, NM |

46 | KRQE-TV(3) | CBS | 13 | 10/1/2014 | ||||||||||

|

KASA-TV(3) | FOX | 27 | 10/1/2014 | |||||||||||

|

KWBQ-TV(3) | CW | 29 | SSA | 10/1/2014 | ||||||||||

|

KASY-TV | MNTV | 45 | SSA | 10/1/2006 | (5) | |||||||||

Buffalo, NY |

51 | WIVB-TV | CBS | 39 | 6/1/2015 | ||||||||||

|

WNLO-TV | CW | 32 | 6/1/2015 | |||||||||||

Providence, RI-New Bedford, MA |

53 | WPRI-TV | CBS | 13 | 4/1/2015 | ||||||||||

|

WNAC-TV(3) | FOX | 12 | LMA | 4/1/2007 | (5) | |||||||||

Mobile, AL/Pensacola, FL |

60 | WALA-TV | FOX | 9 | 4/1/2013 | ||||||||||

|

WFNA-TV | CW | 25 | 4/1/2013 | |||||||||||

Dayton, OH |

62 | WDTN-TV | NBC | 50 | 10/1/2013 | ||||||||||

|

WBDT-TV(6) | CW | 26 | SSA/JSA | 10/1/2013 | ||||||||||

Toledo, OH |

70 | WUPW-TV | FOX | 46 | 10/1/2013 | ||||||||||

Green Bay-Appleton, WI |

71 | WLUK-TV(3) | FOX | 11 | 12/1/2013 | ||||||||||

|

WCWF-TV(6) | CW | 21 | SSA/JSA | 12/1/2013 | ||||||||||

Fort Wayne, IN |

107 | WANE-TV | CBS | 31 | 8/1/2013 | ||||||||||

Springfield-Holyoke, MA |

110 | WWLP-TV(3) | NBC | 11 | 4/1/2015 | ||||||||||

Terre Haute, IN |

152 | WTHI-TV(3) | CBS | 10 | 8/1/2013 | ||||||||||

Lafayette, IN |

188 | WLFI-TV | CBS | 11 | 8/1/2013 | ||||||||||

NBCUniversal/LIN Joint Venture: |

|||||||||||||||

Dallas-Forth Worth, TX |

5 | KXAS-TV | NBC | 41 | JV | 8/1/2006 | (5) | ||||||||

San Diego, CA |

28 | KNSD-TV | NBC | 40 | JV | 12/1/2006 | (5) | ||||||||

- (1)

- DMA

estimates and rankings are taken from Nielsen Local Universe Estimates for the 2010-2011 Broadcast Season, effective

September 25, 2010. There are 210 DMAs in the United States. All Nielsen data included in this report represents Nielsen's estimates, and Nielsen has neither reviewed nor approved the data

included in this report.

- (2)

- We

own and operate all of our stations except for (i) those stations noted as "LMA" which indicates stations to which we provide

services under a local marketing agreement (see "Distribution of Programming—Local marketing agreements" for a description of these

agreements), (ii) stations noted as "SSA" which indicates stations to which we provide technical, engineering, promotional, administrative and other operational support services under a shared

services agreement, (iii) stations noted as "JSA" which indicates stations to which we provide advertising sales services under a joint sales agreement (see "Principles Sources of

Revenue—Other revenues" for a description of these agreements) and (iv) stations noted as "JV" which indicates stations owned and

operated by a joint venture to which we are a party.

- (3)

- WISH-TV includes a low-power station, WIIH-LD. WOOD-TV, WAVY-TV, KNVA-TV, KRQE-TV, KASA-TV, WLUK-TV, WWLP-TV and WTHI-TV each include a group of low-power stations. KRQE-TV includes two satellite stations, KBIM-TV and KREZ-TV. KWBQ-TV includes one satellite station KRWB-TV. WNAC-TV includes a digital sub-channel, ENAC-TV. We own,

6

operate or service all of these satellite stations and low-power stations, which broadcast either identical programming as the primary station or programming specific to such channel.

- (4)

- KBVO-TV

is a full power satellite station of KXAN-TV and its primary affiliate is MyNetworkTV.

- (5)

- License

renewal applications have been filed with the FCC and are currently pending. For further information on license renewals, see

"Federal Regulation of Television Broadcasting—License Renewals".

- (6)

- We exercised our option to acquire WCWF-TV and certain assets of WBDT-TV. We assigned our rights to acquire the remaining WBDT-TV assets, including the FCC license, to WBDT Television, LLC. Completion of these transactions is subject to regulatory approvals and certain other terms and conditions. We expect these transactions to close during 2011. For further information see Note 2—"Acquisitions" to our consolidated financial statements.

For more information about our joint venture with NBCUniversal, see "Joint Venture with NBCUniversal" below and Item 1A. "Risk Factors—The GECC Note could result in significant liabilities including (i) requiring us to make short-term cash payments to the NBCUniversal joint venture to fund interest payments and (ii) potentially giving rise to the acceleration of our existing indebtedness, which would cause such existing indebtedness to become immediately due and payable," as well as the description in the Liquidity and Capital Resources section under Item 7. "Management's Discussion and Analysis".

Description of Our Business

Our strategy is focused on becoming the industry leading local media company with diversified revenues and strong cash flow. We continue to execute on a number of key strategic and operating goals, which include: i) maximizing the strength and efficiency of our broadcast operations; ii) investing resources to expand our digital knowledge, offerings and revenues; and iii) innovating and investing in local multimedia products that build new audiences and brand loyalty.

The principal components of our strategy are to:

- •

- Preserve Our Local News Leadership. We operated the number one or number two local news station in 86% of our news markets(1) for the year ended December 31, 2010. Our stations are committed to a "localist" approach with a strong emphasis on the production of our local news content, which sustains our strong news positions and enhances our brand equity in the community. We are recognized for our local news expertise and have won many awards during the past year, including several Emmy, Associated Press and other local and regional awards. We believe that strong local news programming is among the most important elements in attracting local advertising revenue. In addition, news audiences serve as vital lead-ins for other programming and help minimize the impact of changes in network programming. Transitioning our newsrooms into multimedia content centers and improving our newsgathering and production process by sharing resources and training journalists to have a wide range of skills, including video camera operation, writing and editing, is a priority.

- (1)

- Source: Average of LIN Media's 2010 Nielsen Ratings Based on Key Demographics: February,

May and November. Monday-Friday, Early Morning, Early Evening, Late News.

- •

- Continue to Improve Our Operating Efficiencies. We have achieved company-wide operating efficiencies through economies of scale in the purchase of programming, ratings services, research services, national sales representation, capital equipment and other vendor services. In addition, we operate two regional technology centers that have centralized engineering, operations and administration for all of our major mid-west, New England and mid-Atlantic television stations, saving labor and reducing capital costs. In 2010, we began transitioning our television sales, traffic, promotions and billings to a new state-of-the-art software program that provides better insight and control, while generating cost savings. Our use of new technology to streamline operations has also helped modernize our newsrooms and create a standardized and instantaneous reporting culture that drives cost reduction and efficiency.

7

- •

- Continue to Invest in Digital Media. We strive to be at

the forefront of new technologies, forging unique partnerships and launching innovative products, services and programs for web, mobile and video platforms that engage audiences around our

market-leading brands and generate new advertising opportunities. Our 2009 acquisition of Red McCombs Media, LP ("RMM"), an online advertising and media services company based in

Austin, Texas, significantly expanded our local multi-platform offerings. As part of the reorganization of our sales departments to support multiple platforms, our sales teams have teamed

up with RMM's online sales force and media analysts to expand the scope of our offerings beyond our traditional markets. All of our television stations are now marketing RMM's targeted products,

including custom display, vertical display, search and e-mail marketing solutions. In addition, we have a unique multiplatform content syndication strategy and secured numerous national

and local video syndication partnerships in 2010. Our mobile marketing strategy is focused on making it more convenient for users to access our content on the most popular electronic devices. In 2009,

we developed iPhone applications for each of our local television stations and we were the first broadcast company in our local markets to launch Blackberry applications. We have since launched

Android and iPad applications, all of which enable users to access our content on a 24 hour/7 days a week basis. Finally, we leveraged strong content gathering capabilities and a

superior digital platform to launch onPolitix during this non-presidential political year. Our viewers can find national political content

on many web sites but onPolitix provides a unique opportunity for consumers to follow and actively engage in local, regional and national politics through varying levels of interaction. Since the

launch of our digital business in 2007, digital revenues, which include retransmission consent fees, have grown nearly 309% and now comprise 15% of our total net revenues.

- •

- Grow Our Revenue Share Through a Focus on Local

Programming. We are committed to improving the quality of our existing programs, developing new local programs, and generating new

sources of revenue. Local programming allows us to leverage our existing production teams and on-air talent while limiting our exposure to long-term syndicated programming

contracts. It also allows us to be more creative and offer unique local marketing solutions beyond :30 and :60 second spots. In 2010, we launched four new local lifestyle programs, including

"The Hampton Roads Show" in Norfolk, VA; "Mass Appeal", in Springfield, MA; "Studio 10" in Mobile, AL; and "New Mexico Style" in Albuquerque, NM. We added

approximately 1,400 and 1,500 more local programming hours in 2010 and 2009, respectively. We now have unique programs tailored to the communities we serve in the majority of our markets and have

plans to launch more local shows in 2011. We believe that our commitment to localism continues to build brand loyalty and differentiate us from our competition.

- •

- Continue to Pursue Our Multi-Channel

Strategy. We believe our spectrum has value beyond traditional television channels and digital technology enables us to separate a

portion of that spectrum for incremental services. We have been active in exploring uses of that spectrum and reinventing existing channels when we believe there is a revenue growth opportunity. In

2010, our President and Chief Executive Officer was elected President of the Open Mobile Video Coalition, providing a unique opportunity for our Company to build relationships with companies that are

at the forefront of developing new technology that will provide live, local and national over-the-air digital television to consumers via next-generation portable

and mobile devices and further enabling us to effectively pursue a multi-channel strategy. Such strategy helps us appeal to a wider audience and market of advertisers while providing

economies of scale to pursue additional and new programming services.

- •

- Secure Subscriber Fees from Pay-Television Operators. According to Nielsen, cable, satellite television and telecommunications companies currently provide video program services to approximately 90% of total U.S. television households. The surge of competition from satellite and telecommunications companies, combined with our strong local and national programming, provides us with compelling

8

- •

- Provide Superior Community Service. Our model of community service exemplifies broadcasting's great value and responsibility to the local community. Our viewers and advertising partners look to our television stations for their leadership in local and regional public service activities. We support numerous non-profit organizations, programs and events that help make the communities we serve better, stronger, and more vibrant places to live, work, and do business. We believe our commitment to the health and vitality of our communities contributes to the trusted and enduring relationships we have with both viewers and advertisers.

negotiating positions to obtain compensation for our channels. It is of critical importance to the broadcast industry that pay-television operators pay sub fees that are more in-line with the superior audience viewing levels our channels achieve relative to cable channels. We have negotiated and will continue to negotiate with pay-television operators in our local markets to ensure we receive our fair share of subscription fees.

Principal Sources of Revenue

Local, national and political advertising revenues

Local, national and political advertising, net of agency commissions, represented approximately 82%, 84% and 90% of our total net revenues for the years ended December 31, 2010, 2009 and 2008, respectively. We receive these revenues principally from advertising time sold in our local news, network and syndicated programming. In general, advertising rates are based upon a variety of factors, including:

- •

- size and demographic makeup of the market served by the television station;

- •

- a program's popularity among television viewers;

- •

- number of advertisers competing for the available time;

- •

- availability of alternative advertising media in the station's market area;

- •

- our station's overall ability to attract viewers in its market area;

- •

- our station's ability to attract viewers among particular demographic groups that an advertiser may be targeting; and

- •

- effectiveness of our advertising sales force.

Network compensation

The three oldest networks, ABC, CBS and NBC, have historically made cash compensation payments for our carriage of their network programming. However, in accordance with prevailing trends in our industry, our recent agreements with these networks now reflect a reduction and eventual elimination of network compensation payments to us and/or require us to pay compensation to the network.

The newer networks, such as FOX, CW and MyNetworkTV, provide less network programming, pay no network compensation and, in some instances, require us to pay network compensation. However, these newer networks provide us with more advertising inventory to sell than ABC, CBS or NBC.

Barter revenues

We occasionally barter our unsold advertising inventory for goods and services that are required to operate our television stations or are used in sales and marketing efforts. We also acquire certain syndicated programming by providing a portion of the available advertising inventory within the program, in lieu of cash payments.

9

Digital revenues

We generate digital revenues from advertising produced by our television stations' Internet web sites, from retransmission consent fees received from cable, satellite and telecommunications companies for the rights to carry our signals in their pay television services to consumers and by providing online advertising and media services through RMM.

Other revenues

We receive other revenues from sources such as renting space on our television towers, renting our production facilities, copyright royalties and providing television production services. Additionally, we earn fee income through shared services agreements for four stations located in the Albuquerque-Santa Fe, Green Bay-Appleton and Dayton markets, under which we provide technical, engineering, promotional, administrative and other operational support services from our stations that we own and operate within each of those markets. We also have a joint sales agreement for the stations in the Green Bay-Appleton and Dayton markets, under which we provide advertising sales services.

Sources and Availability of Programming

We program our television stations from the following program sources:

- •

- News and general entertainment programming that is produced by our local television stations;

- •

- Network programming such as "CSI" or "Modern Family";

- •

- Syndicated programming: off-network programs, such as "Criminal Minds" or "How I Met Your Mother" and

first-run programs, such as "Jeopardy", "Entertainment Tonight" or "Wheel of Fortune";

- •

- Paid programming: arrangements where a third party pays our stations for a block of time, generally in

one-half hour or one hour time periods to air long-form advertising or "infomercials"; and

- •

- Local Weather Station: we provide a 24-hour weather channel to local cable systems in certain of our television markets.

10

Locally produced news and general entertainment programming

Our stations produce an aggregate of 519 hours of local news programming per week that we broadcast on all but one of our stations. Local news programming also allows us greater control over our programming costs.

Our current network affiliations and number of weekly hours of network, local news and other local programming are as follows:

Network

|

DMA | DMA Rank | Station | Weekly Hours of Network Programming |

Weekly Hours of Local News Programming |

Weekly Hours of Other Local Programming |

Network Affiliation End Date |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

ABC |

Hartford-New Haven, CT |

30 | WTNH-TV | 86 | 29 | 3 | 8/31/2011 | |||||||||||||

|

Grand Rapids-Kalamazoo-Battle Creek, MI |

41 | WOTV-TV | 86 | 9 | 6 | 8/31/2011 | |||||||||||||

CBS |

Indianapolis, IN |

27 | WISH-TV | 92 | 34 | 7 | 12/31/2014 | |||||||||||||

|

Albuquerque, NM |

46 | KRQE-TV | 100 | 27 | 1 | 12/31/2014 | |||||||||||||

|

Buffalo, NY |

51 | WIVB-TV | 100 | 29 | 1 | 12/31/2014 | |||||||||||||

|

Providence, RI-New Bedford, MA |

53 | WPRI-TV | 100 | 30 | 1 | 12/31/2014 | |||||||||||||

|

Fort Wayne, IN |

107 | WANE-TV | 94 | 25 | 1 | 12/31/2014 | |||||||||||||

|

Terre Haute, IN |

152 | WTHI-TV | 94 | 18 | — | 12/31/2014 | |||||||||||||

|

Lafayette, IN |

188 | WLFI-TV | 94 | 23 | 1 | 12/31/2017 | |||||||||||||

NBC |

Grand Rapids-Kalamazoo-Battle Creek, MI |

41 | WOOD-TV | 98 | 32 | 6 | 1/1/2013 | |||||||||||||

|

Norfolk-Portsmouth-Newport News, VA |

43 | WAVY-TV | 96 | 32 | 1 | 1/1/2013 | |||||||||||||

|

Austin, TX |

44 | KXAN-TV | 95 | 29 | 1 | 1/1/2013 | |||||||||||||

|

Dayton, OH |

62 | WDTN-TV | 98 | 28 | 1 | 1/1/2013 | |||||||||||||

|

Springfield-Holyoke, MA |

110 | WWLP-TV | 96 | 33 | 4 | 1/1/2013 | |||||||||||||

FOX |

Norfolk-Portsmouth-Newport News, VA |

43 | WVBT-TV | 26 | 5 | 7 | 6/30/2013 | |||||||||||||

|

Albuquerque, NM |

46 | KASA-TV | 26 | 7 | 5 | 6/30/2013 | |||||||||||||

|

Providence, RI-New Bedford, MA |

53 | WNAC-TV(1) | 26 | 9 | — | 6/30/2013 | |||||||||||||

|

Mobile/Pensacola, FL |

60 | WALA-TV | 26 | 26 | 5 | 6/30/2013 | |||||||||||||

|

Toledo, Ohio |

70 | WUPW-TV | 26 | 9 | — | 6/30/2013 | |||||||||||||

|

Green Bay, WI |

71 | WLUK-TV | 26 | 44 | 6 | 6/30/2013 | |||||||||||||

CW |

Columbus, OH |

34 | WWHO-TV | 20 | — | — | 9/17/2016 | |||||||||||||

|

Austin, TX |

44 | KNVA-TV | 20 | 4 | — | 9/17/2016 | |||||||||||||

|

Buffalo, NY |

51 | WNLO-TV | 28 | 15 | — | 9/17/2016 | |||||||||||||

|

Mobile/Pensacola, FL |

60 | WFNA-TV | 20 | 1 | — | 9/17/2016 | |||||||||||||

MyNetworkTV |

Indianapolis, IN |

27 | WNDY-TV | 13 | 5 | 2 | 9/28/2014 | |||||||||||||

|

Hartford-New Haven, CT |

30 | WCTX-TV | 10 | 9 | 2 | 9/28/2014 | |||||||||||||

|

Grand Rapids-Kalamazoo-Battle Creek, MI |

41 | WXSP-CA | 10 | 4 | — | 9/28/2014 | |||||||||||||

|

Austin, TX |

44 | KBVO-TV | 10 | 3 | 2 | 9/28/2014 | |||||||||||||

|

1,616 | 519 | 63 | |||||||||||||||||

- (1)

- ENAC-TV is a digital sub-channel of WNAC-TV on which programming is provided through MyNetworkTV's program service and on which we broadcast ten hours of network programming and one hour of other local programming.

Network programming

All of our stations are affiliated with one of the national television networks. Our network affiliation agreements provide a local station certain exclusive rights and an obligation, subject to certain limited preemption rights, to carry the network programming. While the networks retain most of the advertising time within their programs for their own use, the local station also has the right to sell a limited amount of advertising time within the network programs. Other time periods, which are not programmed by the

11

networks, are programmed by the local station, for which the local station retains all of the advertising revenues. Networks also share certain of their programming with cable networks and make certain of their programming available through their web site or on web sites such as hulu.com. These outlets compete with us for viewers in the communities served by our stations.

The programming strength of a particular national television network may affect a local station's competitive position. Our stations, however, are diversified among the various networks, reducing the potential impact of any one network's performance. We believe that national television network affiliations remain an efficient means of obtaining competitive programming, both for established stations with strong local news franchises and for newer stations with greater programming needs.

Our stations that are affiliated with ABC, CBS, FOX and NBC generate a higher percentage of revenue from the sale of advertising within network programming than stations affiliated with CW and MyNetwork.

Our affiliation agreements have terms with scheduled expiration dates ranging through December 31, 2017. These agreements are subject to earlier termination by the networks under specified circumstances, including a change of control of our Company, which would generally result from the acquisition of shares having 50% or more of the voting power of our Company.

Syndicated programming

We acquire the rights to programs for time periods in which we do not air our local news or network programs. These programs generally include reruns of current or former network programs, such as "Criminal Minds" or "How I Met Your Mother", or first-run syndicated programs, such as "Jeopardy", "Entertainment Tonight" or "Wheel of Fortune". We pay cash for these programs or exchange advertising time within the program for the cost of the program rights. We compete with other local television stations to acquire these programs, which has caused the cost of program rights to increase over time. In addition, a television viewer can now choose to watch many of these programs on national cable networks or purchase these programs on DVDs or via downloads to computers, mobile video devices or web-based video players, which has contributed to increasing fragmentation of our local television audience.

Distribution of Programming

The programming that airs on our television stations can reach the television audience by one or more of the following distribution systems:

- •

- Full-power television stations;

- •

- Stations we operate under local marketing agreements;

- •

- Low-power television stations;

- •

- Digital channels;

- •

- Cable television;

- •

- Satellite television systems;

- •

- Telecommunications systems; and

- •

- Internet, mobile and other digital services.

Full-power television stations

We own, operate or service 31 full-power television stations that operate on digital over-the-air channels 7 through 50. Our full-power television stations include two full-power stations for which we provide programming, sales and other related services under local marketing agreements, and four

12

full-power stations for which we provide technical, engineering, promotional, administrative and other operational support services under shared services agreements (for two of these stations we also provide advertising sales services under a joint sales agreement). See "Our television stations" for a listing of our full-power television stations.

Local marketing agreements

The FCC television licenses for the two stations for which we provide programming, sales and other related services under local marketing agreements ("LMAs") are not owned by us. Revenues generated by these stations contributed 4%, 5% and 4% to our net revenues for the years ended December 31, 2010, 2009 and 2008, respectively. We incur programming costs, operating costs and capital expenditures related to the operation of these stations, and retain all advertising revenues. In Providence and Austin, the two local markets where these stations are located, we own and operate another station. These LMA stations are an important part of our multi-channel strategy. We have purchase options to acquire the FCC licenses for the LMA stations in Providence and Austin, which are exercisable if the legal requirements limiting ownership of these stations change.

Low-power television stations

We own and operate a number of low-power television stations. We operate these stations either as a stand-alone or satellite stations. These low-power broadcast television stations are licensed by the FCC to provide service to substantially smaller areas than those of full-power stations. These stations contributed approximately 1% or less of our total net revenues in the years ended December 31, 2010, 2009 and 2008.

In eight of our markets, Albuquerque, Austin, Grand Rapids, Green Bay, Indianapolis, Norfolk-Portsmouth-Newport News, Springfield and Terre Haute, we use our low power stations to extend the geographic reach of our primary stations in these markets. In Grand Rapids, we have affiliated WXSP-TV, a group of low-power television stations, with MyNetworkTV, to cover substantially all of the local market.

Cable, satellite television and telecommunications systems

According to Nielsen, cable, satellite television and telecommunications companies currently provide video program services to approximately 90% of total U.S. television households, with cable and telecommunications companies serving 61% of U.S. households and direct broadcast satellite ("DBS") providers serving 29%. As a result, cable, satellite television and telecommunications companies are not only primary competitors, but the primary means by which our television audience views our television stations. Most of our stations are distributed pursuant to retransmission consent agreements with multichannel video program distributors that operate in markets we serve. As of December 31, 2010, we had retransmission consent agreements with 113 distributors, including 109 Multiple System Operators ("MSOs") and regional telecommunications companies, the two major satellite television providers, and two national telecommunications providers. For an overview of FCC regulations governing carriage of television broadcast signals by multichannel video program distributors, see "Federal Regulation of Broadcasting—Cable and Satellite Carriage of Local Television Signals."

Internet, mobile and other digital services

We operate interactive television station and niche web sites in 17 U.S. markets and offer a growing portfolio of Internet-based products and services that provide traditional and new audiences around-the-clock access to our trusted local news and information. We launched our mobile business in 2009 with iPhone and BlackBerry smartphone applications and we have since launched Android and iPad applications. In addition, we also launched SMS/text messaging, video blogging and other advanced interactive features that further extend the distribution of our content.

13

Seasonality of Our Business

Our advertising revenues are generally highest in the second and fourth quarters of each calendar year, due generally to higher advertising in the spring season and in the period leading up to and including the end-of-year holiday season. Our operating results are also significantly affected by annual cycles, as advertising revenues are generally higher in even-numbered years due to additional revenues associated with election years from advertising spending by political candidates and incremental advertising revenues associated with Olympic broadcasts.

Our industry is cyclical in nature and affected by prevailing economic conditions. Since we rely on sales of advertising for a substantial majority of our revenues, our operating results are sensitive to general economic and regional conditions in each local market where we operate.

Joint Venture with NBCUniversal

We hold an approximate 20% equity interest, and NBCUniversal Media, LLC ("NBCUniversal") holds the remaining approximate 80% equity interest, in a joint venture which is a limited partner in a business that owns television stations KXAS-TV, an NBC affiliate in Dallas, and KNSD-TV, an NBC affiliate in San Diego. We and NBCUniversal each have a 50% voting interest in the joint venture. NBCUniversal operates the two stations pursuant to a management agreement.

The joint venture is the obligor on an $815.5 million non-amortizing senior secured note due 2023 (the "GECC Note") held by General Electric Capital Corporation ("GECC"), which provided financing to the venture. The GECC Note bears interest at a rate of 8% per annum until March 2, 2013 and 9% per annum thereafter. LIN TV has guaranteed the payment of principal and interest on the GECC Note.

In January 2011, Comcast Corporation acquired control of the business of NBCUniversal through acquisition of a 51% interest in NBCUniversal, LLC, while a majority owned subsidiary of General Electric Company ("GE") owns the remaining 49%. GECC remains a majority-owned subsidiary of GE.

Our joint venture with NBCUniversal has been adversely impacted by the economic downturn, and it did not distribute any cash to NBCUniversal or us during the years ended December 31, 2010 and 2009. In light of the adverse effect of the economic downturn on the joint venture's operating results, in 2009 we entered into an agreement with NBCUniversal, which covered the period from March 6, 2009 through April 1, 2010 (the "Original Shortfall Funding Agreement") and in 2010 we entered into a second agreement, which covered the period from April 2, 2010 through April 1, 2011 ("2010 Shortfall Funding Agreement"). These agreements provided that: i) we and NBCUniversal waived the requirement that the joint venture maintain debt service reserve cash balances of at least $15 million; ii) the joint venture would use a portion of its existing debt service reserve cash balances to fund interest payments on the GECC Note in 2009 and 2010; iii) NBCUniversal agreed to defer its receipt of 2008, 2009 and 2010 management fees; and iv) we agreed that if the joint venture does not have sufficient cash to fund interest payments on the GECC Note through April 1, 2011, we and NBCUniversal would each provide the joint venture with a shortfall loan on the basis of our percentage of economic interest in the joint venture.

During the year ended December 31, 2010, pursuant to the shortfall funding agreements with NBCUniversal, we made shortfall loans in the aggregate principal amount of $4.1 million to our joint venture, representing our approximate 20% share in cumulative debt service shortfalls at the joint venture. Concurrent with our funding of the shortfall loans, NBCUniversal funded shortfall loans in the aggregate principal amounts of $15.9 million to the joint venture, in respect of its approximate 80% share in the cumulative debt service shortfalls at the joint venture.

Because of anticipated future cash shortfalls at the joint venture, on March 14, 2011, we and GE entered into an agreement (the "2011 Shortfall Funding Agreement" and together with the Original Shortfall Funding Agreement and the 2010 Shortfall Funding Agreement the "Shortfall Funding Agreements") covering the period from April 2, 2011 through April 1, 2012. Under the terms of the

14

2011 Shortfall Funding Agreement, we agreed that if the joint venture does not have sufficient cash to fund interest payments on the GECC Note through April 1, 2012, we and GE would each provide the joint venture with a shortfall loan. Any shortfall loans funded by us under the 2011 Shortfall Funding Agreement will be calculated on the basis of our percentage of economic interest in the joint venture, and GE's share of shortfall loans will be calculated on the basis of NBCUniversal's percentage of economic interest in the joint venture. GE's obligation to fund shortfall loans under the 2011 Shortfall Funding Agreement is conditioned upon (a) amendment of the joint venture's Credit Agreement with GECC and the LLC Agreement governing the joint venture's operations, to permit the joint venture to obtain shortfall loans from GE, and (b) receipt of the consent of Comcast Corporation to the terms and conditions on which GE provides its proportionate share of any shortfall; provided that Comcast's consent may not be unreasonably withheld. NBCUniversal has acknowledged and agreed to the terms of the 2011 Shortfall Funding Agreement.

Under the terms of the joint venture's TV Master Service Agreement with NBCUniversal, management fees incurred by the joint venture to NBCUniversal during the term of the 2011 Shortfall Funding Agreement will continue to accrue, but are not payable if any existing joint venture shortfall loans remain outstanding. Management fees payable in arrears attributable to 2008, 2009, and 2010 are also not payable to NBCUniversal if any existing joint venture shortfall loans remain outstanding.

We recognize shortfall funding liabilities to the joint venture on our balance sheet when those liabilities become both probable and estimable, which occurs when joint venture management provides us with budget or forecast information of operating cash flows and working capital needs indicating that a debt service shortfall is probable to occur and when we have reached or intend to reach a shortfall funding agreement covering the budgeted or forecasted period. Based on 2011 forecast information provided by joint venture management and our estimate of joint venture cash flows through March 31, 2012, we estimate our share of shortfall funding could be approximately $1.9 million through March 31, 2012. Actual cash shortfalls at the joint venture could vary from our current estimates. Cash shortfalls at the joint venture beyond March 31, 2012 are not currently estimable or probable; therefore, we have not accrued for any potential obligations beyond $1.9 million.

Our ability to honor our shortfall loan obligations under the Shortfall Funding Agreements is limited by certain covenants contained in our Amended Credit Agreement, and the indentures governing our 83/8% senior notes and our 61/2% senior subordinated notes. If we are unable to make payments under the Shortfall Funding Agreements, or a future shortfall funding agreement, the joint venture may be unable to fund interest obligations under the GECC Note, resulting in an event of default. In addition, if the joint venture experiences further cash shortfalls beyond April 1, 2012, we may decide to fund such cash shortfalls, or to fund such shortfalls through further loans or equity contributions to the joint venture.

For more information about our joint venture with NBCUniversal, see Item 1A. "Risk Factors—The GECC Note could result in significant liabilities, including (i) requiring us to make short-term cash payments to the NBCUniversal joint venture to fund interest payments and (ii) potentially giving rise to the acceleration of our existing indebtedness, which would cause such existing indebtedness to become immediately due and payable," as well as the description in the Liquidity and Capital Resources section under Item 7. "Management's Discussion and Analysis".

Competitive Conditions in the Television Industry

The television broadcast industry has become highly competitive as a result of new technologies and new program distribution systems. In most of our local markets, we compete directly against other local broadcast stations, cable, satellite television and telecommunication systems for audience. We also compete with online video services, including local news web sites and web sites such as hulu.com, which provide access to some of the same programming, including network programming that we provide, and other emerging technologies including mobile television.

15

Federal Regulation of Television Broadcasting

Overview of Regulatory Issues. Our television operations are subject to the jurisdiction of the FCC under the Communications Act of 1934, as amended (the "Communications Act"). The Communications Act prohibits the operation of broadcast stations except pursuant to licenses issued by the FCC and empowers the FCC, among other things, to issue, renew, revoke and modify broadcasting licenses; assign frequency bands; determine stations' frequencies, locations and power; and regulate the equipment used by stations.

The Communications Act prohibits the assignment of a broadcast license or the transfer of control of a license without the FCC's prior approval. The FCC also regulates certain aspects of the operation of cable television systems, DBS systems and other electronic media that compete with broadcast stations. In addition, the FCC regulates matters such as television station ownership, network-affiliate relations, cable and DBS systems' carriage of television station signals, carriage of syndicated and network programming on distant stations, political advertising practices, children's programming and obscene and indecent programming.

License Renewals. Under the Communications Act, the FCC generally may grant and renew broadcast licenses for terms of eight years, though licenses may be renewed for a shorter period under certain circumstances. The Communications Act requires the FCC to renew a broadcast license if the FCC finds that (i) the station has served the public interest, convenience and necessity; (ii) there have been no serious violations of either the Communications Act or the FCC's rules and regulations by the licensee; and (iii) there have been no other serious violations that taken together constitute a pattern of abuse. In making its determination, the FCC may consider petitions to deny but cannot consider whether the public interest would be better served by issuing the license to a person other than the renewal applicant. We are in good standing with respect to each of our FCC licenses. The table on page 6 includes the expiration date of each of the licenses for the stations that we own, as well as for the stations to which we provide services or in which we have an equity investment through a joint venture. As indicated in the table, the licenses for these stations have expiration dates ranging between 2006 and 2015. License renewal applications were timely filed for each of these stations for which the license is now expired. Once an application for renewal is filed, each station remains licensed while its application is pending, even after its license expiration date has passed. Certain of our licenses have long-standing applications for renewal that remain pending with the FCC. Action on many license renewal applications may have been delayed for reasons, such as, the pendency of complaints that programming provided by the various networks contained indecent material and complaints regarding alleged violations of sponsorship identification rules. We cannot predict when the FCC will act on pending renewal applications. We expect the FCC to renew each of these licenses but we make no assurance that it will do so.

Ownership Regulation. The Communications Act and FCC rules limit the ability of individuals and entities to have ownership or other attributable interests in certain combinations of broadcast stations and other media. In 1999, the FCC modified its local television ownership rules. In 2003, the FCC issued an order that would have liberalized most of the ownership rules, permitting us to acquire television stations in certain markets where we are currently prohibited from acquiring additional stations. In 2004, the Third Circuit Court of Appeals stayed and remanded several of the FCC's 2003 ownership rule changes. In July 2006, as part of the FCC's statutorily required quadrennial review of its media ownership rules, the FCC sought comment on how to address the issues raised by the Third Circuit Court of Appeals' decision. In February 2008, the FCC released an order that re-adopted its 1999 local television ownership rules, and those rules are currently in effect. Several parties have appealed the FCC's February 2008 decision. In November, 2009 the FCC initiated its statutorily required quadrennial review process, but it has not yet proposed any rule changes. We cannot predict how pending appeals of prior FCC ownership rule decisions or the pending quadrennial review proceeding may result in changes to the FCC's broadcast ownership rules. The FCC's currently effective ownership rules that are material to our operations are summarized below.

16

Local Television Ownership. Under the FCC's current local television ownership (or "duopoly") rule, a party may own multiple television stations without regard to signal contour overlap provided they are located in separate Nielsen DMAs. In addition, the rules permit parties to own up to two TV stations in the same DMA so long as (i) at least one of the two stations is not among the top four-ranked stations in the market based on audience share at the time an application for approval of the acquisition is filed with the FCC, and (ii) at least eight independently owned and operating full-power commercial and non-commercial television stations would remain in the market after the acquisition. In addition, without regard to the number of remaining or independently owned television stations, the FCC will permit television duopolies within the same DMA so long as the digital noise limited signal contours of the stations involved do not overlap. Stations designated by the FCC as "satellite" stations, which are full-power stations that typically rebroadcast the programming of a "parent" station, are exempt from the local television ownership rule. Also, the FCC may grant a waiver of the local television ownership rule if one of the two television stations is a "failed" or "failing" station or if the proposed transaction would result in the construction of a new television station (an unbuilt-station waiver). We believe that we are currently in compliance with the local television ownership rule.

The FCC's 1999 ownership order established a rule attributing LMAs for ownership purposes. The FCC grandfathered LMAs that were entered into prior to November 5, 1996, permitting those stations to continue operations pursuant to the LMAs until the conclusion of the FCC's 2004 biennial review. The FCC stated it would conduct a case-by-case review of grandfathered LMAs and assess the appropriateness of extending the grandfathering periods. Subsequently, the FCC invited comments as to whether, instead of beginning the review of the grandfathered LMAs in 2004, it should do so in 2006. The FCC did not initiate any review of grandfathered LMAs in 2004 or as part of its 2006 quadrennial review. We do not know when, or if, the FCC will conduct any such review of grandfathered LMAs. Grandfathered local marketing agreements can be freely transferred during the grandfather period, but duopolies may be transferred only where the two-station combination continues to qualify under the duopoly rule. We currently have grandfathered LMAs under which we provide programming to stations in Providence, Rhode Island and Austin, Texas.

In 2010, we entered into shared services agreements ("SSAs") and certain other arrangements for stations in Dayton, Ohio and Green Bay-Appleton, Wisconsin. SSAs are permitted under the FCC's local television ownership rules and allow for technical, engineering, promotional, administrative and other operational support services. SSAs are different from LMAs in that programming is not provided under an SSA. In September 2010, we filed an application seeking to acquire the station in the Green Bay-Appleton, Wisconsin market under the "failing station" duopoly waiver standard discussed above, and a third party filed an application to acquire the station in the Dayton, Ohio market. In October 2010, Time Warner Cable Inc. ("TWC") filed petitions to deny both applications, alleging that the pertinent agreements give us excessive authority to act as an agent in negotiating retransmission consent agreements for the stations. TWC asked the FCC to deny the applications, set them for a hearing, and/or impose conditions on the parties. We believe that the agreements are permissible under the FCC's rules, and in November 2010 we filed oppositions to TWC's filings. The applications remain pending, and we cannot predict what the FCC will decide, or when.

National Television Ownership Cap. The Communications Act, as amended in 2004, limits the number of television stations one entity may own nationally. Under the rule, no entity may have an attributable interest in television stations that reach, in the aggregate, more than 39% of all U.S. television households. The FCC currently discounts the audience reach of a UHF station by 50% when computing the national television ownership cap. Our stations reach is approximately 9% of U.S. households.

17

Attribution of Ownership. Under the FCC's attribution policies, the following relationships and interests generally are attributable for purposes of the FCC's broadcast ownership restrictions:

- •

- holders of 5% or more of the licensee's voting stock, unless the holder is a qualified passive investor, in which case the

threshold is a 20% or greater voting stock interest;

- •

- all officers and directors of a licensee and its direct or indirect parent(s);

- •

- any equity interest in a limited partnership or limited liability company, unless properly "insulated" from management

activities; and

- •

- equity and/or debt interests which in the aggregate exceed 33% of a licensee's total assets, if the interest holder supplies more than 15% of the station's total weekly programming, or is a same-market broadcast company, cable operator or newspaper (the "equity/debt plus" standard).

Under the single majority shareholder exception to the FCC's attribution policies, otherwise attributable interests under 50% are not attributable if a corporate licensee is controlled by a single majority shareholder and the minority interest holder is not otherwise attributable under the "equity/debt plus" standard.

Because of these multiple ownership and cross-ownership rules, any person or entity that acquires an attributable interest in us may violate the FCC's rules if that purchaser also has an attributable interest in other television or radio stations, or in daily newspapers, depending on the number and location of those radio or television stations or daily newspapers. Such person or entity also may be restricted in the companies in which it may invest to the extent that those investments give rise to an attributable interest. If the holder of an attributable interest violates any of these ownership rules or if a proposed acquisition by us would cause such a violation, we may be unable to obtain from the FCC one or more authorizations needed to conduct our television station business and may be unable to obtain the FCC's consents for certain future acquisitions.

Digital Television. We terminated all analog broadcasts on our full power stations on or before June 12, 2009 in connection with the national transition to digital television. Following the transition, each of our full power stations broadcasts a 19.4 megabit-per-second (Mbps) data stream, rather than a single analog program stream. FCC regulations permit substantial flexibility in how we use that data stream. For example, we are permitted to provide a mix of high definition and standard television program streams free-to-air, additional program-related data, subscription video or audio streams, and non-broadcast services. A new technical standard, currently being tested, would permit digital stations to provide video and data streams that can be more readily received on mobile devices (such as computers and smart phones), if those devices incorporate the technology. These digital channels remain subject to specific FCC regulations. For example, we are required to carry additional children's educational programming if we transmit multiple program streams, and we must pay the U.S. Treasury 5% of gross revenues for any non-broadcast services we provide using our digital signals. The FCC is evaluating whether to impose further public interest programming requirements on digital broadcasters. The FCC's digital transition implementation plan maintained the secondary status of low-power television stations. The FCC is in the process of establishing a digital transition plan for low-power television stations.

Cable and Satellite Carriage of Local Television Signals. Pursuant to FCC rules, full power television stations can obtain carriage of their signals by multichannel program distributors in one of two ways: via mandatory carriage or via "retransmission consent." Once every three years each station must formally elect either mandatory carriage ("must-carry" for cable distributors and "carry one-carry all" for satellite television providers) or retransmission consent. The next election must be made by October 1, 2011, and will be effective January 1, 2012 through December 31, 2014. A mandatory carriage election invokes FCC rules that requires the distributor to carry a single program stream designated by the station and that program stream's related data in the station's local market. Distributors may decline carriage for certain reasons specified in the rules, including a lack of channel capacity, the station's failure to deliver a good

18

quality signal, the presence of a nearby affiliate of the same network or, in the case of satellite distributors, if the distributor does not carry any other local broadcast stations in the electing station's market. Distributors do not pay a fee to stations that elect mandatory carriage.

A station that elects retransmission consent waives its mandatory carriage rights, and the station and the distributor must negotiate in good faith for carriage of the station's signal. Negotiated terms may include channel position, service tier carriage, carriage of multiple program streams, compensation and other consideration. If a station elects to negotiate retransmission terms, it is possible that the station and the distributor will not reach agreement and that the distributor will not carry the station's signal.

FCC rules govern which local television signals a satellite subscriber may receive. Congress has also imposed certain requirements relating to satellite distribution of local television signals to "unserved" households that do not receive a useable signal from a local network-affiliated station or that reside in a market without a local affiliate of the pertinent network. The Satellite Television Extension and Localism Act of 2010 ("STELA") updated the blanket license scheme previously enacted under the Satellite Home Viewer Extension and Reauthorization Act of 2004 ("SHVERA") by, among other things, extending for five years, until December 31, 2014, statutory licenses that allow satellite television companies to retransmit broadcast signals from distant markets to eligible customers. A satellite provider also is permitted to import the signal of an out-of-market station, with that station's consent, to the specific counties and communities within a local market in which the out-of-market station is deemed to be "significantly viewed," subject to certain conditions. Such carriage previously was governed by the distant signal provisions. Under STELA, it is now treated as a retransmission into the station's local market, which means that the statutory copyright for such carriage will not sunset at the end of 2014. STELA also eliminated the requirement that DBS operators carry the local affiliate of a particular network before they could import an out-of-market station deemed to be significantly viewed in a given county or community. One subtle but potentially significant change in STELA is the new definition of an "unserved household" which could lead to an increase in satellite television operators' carriage of out-of-market signals in our markets. At this time, we are monitoring developments in this area but cannot determine whether this new legislation will result in significant changes to the satellite distribution scheme or whether or how any of the other changes in STELA will impact our broadcast business.

Several cable system and DBS operators have jointly petitioned the FCC to initiate a rulemaking proceeding to consider amending its retransmission consent rules. The FCC has solicited public comment on the petition and the FCC has announced that it intends to initiate a formal proceeding in March 2011 concerning the issues raised in the petition. We cannot predict the outcome of such a proceeding.

Programming and station operations. The Communications Act requires broadcasters to serve the public interest. Broadcast station licensees are required to present programming that is responsive to community problems, needs and interests and to maintain records demonstrating such responsiveness. Stations must follow various rules that regulate, among other things, children's television programming and advertising, political advertising, sponsorship identification, contest and lottery advertising and program ratings guidelines. The FCC has proposed to re-establish a number of formalized procedures that it believes will improve television broadcasters' service to their local communities. These proposals include the establishment of community advisory boards, quantitative programming guidelines and maintenance of a main studio in a station's community of license. If the FCC adopts such proposals, the burden of complying with such requirements could impose additional costs on our stations.

The FCC is also charged with enforcing restrictions or prohibitions on the broadcast of obscene and indecent programs and in recent years has increased its enforcement activities in this area, issuing large fines against radio and television stations found to have carried such programming (even if originated by a third-party program supplier, such as a network). In June 2007, the FCC increased the maximum monetary penalty for carriage of indecent programming tenfold to $325,000 per station per violation with a cap of $3 million for any "single act," and put the licenses of repeat offenders in jeopardy. Court challenges to the

19

FCC's indecency enforcement regime are pending at various stages. For example, the Second Circuit found in 2010 that the FCC's "fleeting expletive" policy was unconstitutionally vague. In a subsequent decision, the Second Circuit vacated an FCC decision imposing monetary forfeitures on 52 television stations that had broadcast an allegedly indecent scene in an episode of the ABC drama "NYPD Blue." We are unable to predict whether the enforcement of the indecency regulations will have a material adverse effect on our ability to provide competitive programming.

The FCC's rules require our stations to provide closed captioning for much of the programming that we broadcast. In addition, in September 2010, Congress passed the Twenty-First Century Communications and Video Accessibility Act. This law requires the FCC to adopt rules concerning video description of programming, for viewers with visual disabilities. Compliance with the new video description rules once they are promulgated by the FCC may impose additional costs on our stations.

Recent regulatory developments, proposed legislation and regulation. Congress and the FCC currently have under consideration, and may in the future adopt, new laws, regulations and policies regarding a wide variety of matters that could affect, directly or indirectly, the operation and ownership of our stations. The foregoing discussion summarizes the federal statutes and regulations material to our operations, but does not purport to be a complete summary of all the provisions of the Communications Act or of other current or proposed statutes, regulations, and policies affecting our business. The summaries should be read in conjunction with the text of the statutes, rules, regulations, orders, and decisions described herein. We are unable at this time to predict the outcome of any of the pending FCC rule-making proceedings referenced above, the outcome of any reconsideration or appellate proceedings concerning any changes in FCC rules or policies noted above, the possible outcome of any proposed or pending Congressional legislation, or the impact of any of those changes on our stations.

Employees

As of December 31, 2010, we employed approximately 1,825 full time employees, 214 of which were represented by labor unions. We believe that our relations with our employees are satisfactory.

Available Information

We file annual, quarterly, and current reports, proxy statements, and other documents with the Securities and Exchange Commission ("SEC") under the Securities Exchange Act of 1934 (the "Exchange Act"). The public may read and copy any materials that we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Also, the SEC maintains an Internet web site that contains reports, proxy and information statements, and other information regarding issuers, including our filings, which we file electronically with the SEC. The public can obtain any documents that we file with the SEC at http://www.sec.gov.

We also make available free-of-charge through our Internet web site (at http://www.linmedia.com) copies of our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and, if applicable, amendments to those reports filed or furnished pursuant to Section 13(a) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish such material, to the SEC.

We also make available on our web site our corporate governance guidelines, the charters for our audit committee, compensation committee, and nominating and corporate governance committee, and our code of business conduct and ethics, and such information is available there to any stockholder who is interested in reviewing this information. In addition, we intend to disclose on our web site any amendments to, or waivers from, our code of business conduct and ethics that are required to be publicly disclosed pursuant to rules of the SEC and the NYSE.

20

Risks Associated with Our Business Activities

Our operating results are primarily dependent on advertising revenues, which can vary substantially from period-to-period based on many factors beyond our control, including economic downturns and viewer preferences.

Our operations and performance are dependent on advertising revenues, which can be materially affected by a number of factors beyond our control, including economic conditions and viewer preferences. Advertising revenue, including local, national and political advertising revenues, net of agency commissions, consisted of approximately 82%, 84% and 90% of our total net revenues for the years ended December 31, 2010, 2009 and 2008, respectively. Local advertising revenues increased 8% for the year ended December 31, 2010 and decreased 13% and 9% for the years ended December 31, 2009 and 2008, respectively, compared to their respective prior periods. National advertising revenues increased 18% for the year ended December 31, 2010 and decreased 17% and 16% for the years ended December 31, 2009 and 2008, respectively, compared to their respective prior periods. This volatility in advertising revenue impacts our financial condition, cash flows and results of operations. While we saw recovery in 2010, decreases in advertising revenues caused by economic conditions could have a material adverse effect on our financial condition, cash flows and results of operations, which could impair our ability to comply with the covenants in our debt instruments, as more fully described below.

In addition to economic conditions, our ability to generate advertising revenues depends on factors such as:

- •

- the relative popularity of the programming on our stations;

- •

- the demographic characteristics of our markets; and

- •

- the activities of our competitors.

Our programming may not attract sufficient targeted viewership or we may not achieve favorable ratings. Our ratings depend partly upon unpredictable and volatile factors beyond our control, such as viewer preferences, competing programming and the availability of other entertainment activities. A shift in viewer preferences could cause our programming not to gain popularity or to decline in popularity, which could cause our advertising revenues to decline. We, and those on whom we rely for programming, may not be able to anticipate and react effectively to shifts in viewer tastes and interests of our local markets. In addition, political advertising revenue from elections and advertising revenues from Olympic Games, which generally occur in the even years, create large fluctuations in our operating results on a year-to-year basis. For example, during 2010, we had political advertising revenues of $49.4 million, compared to $13.2 million in the prior year.

We depend on automotive advertising to a significant degree.

Approximately 23%, 19% and 24% of our local and national advertising revenues for the years ended December 31, 2010, 2009, and 2008, respectively, consisted of automotive advertising. A significant decrease in these revenues in the future could have a material adverse effect on our results of operations and cash flows, which could affect our ability to fund operations and service our debt obligations and affect the value of our common stock.

21

The GECC Note could result in significant liabilities, including (i) requiring us to make short-term cash payments to the NBCUniversal joint venture to fund interest payments and (ii) potentially giving rise to the acceleration of our existing indebtedness, which would cause such existing indebtedness to become immediately due and payable.