Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the fiscal year ended December 31, 2010 | ||

| OR | ||

| ¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission File No. 0-25837

HEIDRICK & STRUGGLES INTERNATIONAL, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 36-2681268 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification Number) |

233 South Wacker Drive, Suite 4200, Chicago, Illinois 60606-6303

(Address of principal executive offices) (Zip Code)

(312) 496-1200

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title Of Each Class |

Name Of Each Exchange On Which Registered | |

| Common Stock, $.01 par value | The Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 of Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer ¨ Accelerated Filer x Non-Accelerated Filer ¨ Smaller Reporting Company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the registrant’s Common Stock held by non-affiliates of the registrant on June 30, 2010 was approximately $395,606,356 based upon the closing market price of $22.82 on that date of a share of Common Stock as reported on the Nasdaq Global Stock Market. As of March 10, 2011, there were 17,558,098 shares of the Company’s Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for its Annual Meeting of Stockholders to be held on May 26, 2011, are incorporated by reference into Part III of this Form 10-K.

Table of Contents

HEIDRICK & STRUGGLES INTERNATIONAL, INC. AND SUBSIDIARIES

Table of Contents

PART I

Overview

Heidrick & Struggles International, Inc. (“Heidrick & Struggles”) is a leadership advisory firm providing executive search and leadership consulting services. We help our clients build leadership teams by facilitating the recruitment, management and deployment of senior executives. Focusing on top-level services offers us several advantages that include access to and influence with key decision makers, increased potential for recurring search and consulting engagements, higher fees per search, enhanced brand visibility, and a leveraged global footprint, which create added barriers to entry for potential competitors. Working at the top of client organizations also allows us to attract and retain high-caliber consultants.

In addition to executive search, we provide a range of leadership consulting services to clients. These services include succession planning, executive assessment, talent retention management, executive development, transition consulting for newly appointed executives, and mergers & acquisitions human capital integration consulting.

Heidrick & Struggles has been a leadership advisor for nearly 60 years. We provide our services to a broad range of clients through the expertise of 347 consultants located in 36 countries throughout the world as of December 31, 2010. For many of our clients, our global access to and knowledge of regional and functional markets and candidate talent is an important differentiator of our business. We provide our executive search services on a retained basis, recruiting senior executives whose first year base salary and bonus averaged approximately $325,500 in 2010 on a worldwide basis. Our clients include the following:

| • | Fortune 1000 companies |

| • | Major non-U.S. companies |

| • | Middle market and emerging growth companies |

| • | Governmental, higher education and not-for-profit organizations |

| • | Other leading private and public entities |

The executive search industry is highly fragmented, consisting of several thousand executive search firms worldwide. Executive search firms are generally separated into two broad categories: retained and contingency. Retained executive search firms fulfill their clients’ senior leadership needs by identifying potentially qualified candidates and assisting clients in evaluating and assessing these candidates. Retained executive search firms generally are compensated for their services regardless of whether the client employs a candidate identified by the search firm and are generally retained on an exclusive basis. Retained executive search firms normally charge a fee for their services equal to approximately one-third of the first year’s total compensation for the position being filled. In contrast, contingency search firms are compensated only upon successfully placing a recommended candidate.

We are a retained executive search firm. Our search process typically consists of the following steps:

| • | Analyze the client’s business needs in order to understand its organizational structure, relationships, and culture; determine the required set of skills for the position; define the required experience; and identify the other characteristics desired of the successful candidate |

| • | Select, contact, interview and evaluate candidates on the basis of experience and potential cultural fit with the client organization |

| • | Present confidential written reports on the candidates who potentially fit the position specification |

| • | Schedule a mutually convenient meeting between the client and each candidate |

1

Table of Contents

| • | Complete references on the final candidate selected by the client |

| • | Assist the client in structuring the compensation package and supporting the successful candidate’s integration into the client team |

Available Information

We maintain an Internet website at http://www.heidrick.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports are available free of charge on this site as soon as reasonably practicable after the reports are filed with or furnished to the Securities and Exchange Commission. We also post news releases on our financial results, investor presentations and other documents containing additional information related to our company on this site. Our Internet website and the information contained in or accessible from our website are for informational purposes only and are not incorporated into this annual report on Form 10-K.

Organization

Our organizational structure, which is arranged by geography and industry/functional practices, is designed to enable us to better understand our clients’ cultures, operations, business strategies, industries and regional markets for executive talent.

Geographic Structure. We provide senior-level executive search and leadership consulting services to our clients worldwide through a network of more than 69 offices in 40 countries. Major locations are staffed with consultants, research associates, administrative assistants and other support staff. Administrative functions are centralized where possible, although certain support and research functions are situated regionally because of variations in local requirements.

Our worldwide network includes affiliate relationships in Finland, South Africa, Turkey and Portugal. We have no financial investment in these affiliates but receive licensing fees from them for the use of our name and our databases. Licensing fees are less than 1% of our net revenue.

Information by Geographic Segment. We operate our executive search and leadership consulting services in three geographic regions: the Americas; Europe, which includes the Middle East and Africa; and Asia Pacific.

Americas. As of December 31, 2010, we had 157 consultants in our Americas segment, which includes the United States, Canada, Mexico and Latin America. The largest offices in this region, as defined by net revenue, are located in New York, Chicago and Atlanta.

Europe. As of December 31, 2010, we had 116 consultants in our European segment. Our offices in the United Kingdom, Germany and France produced the highest levels of net revenue in this segment.

Asia Pacific. As of December 31, 2010, we had 74 consultants in our Asia Pacific segment. China (including Hong Kong), Australia/New Zealand and Singapore produced the highest levels of net revenue in this segment.

The relative percentages of net revenue attributable to each segment were as follows:

| Year Ended December 31, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| Americas |

52 | % | 51 | % | 51 | % | ||||||

| Europe |

26 | % | 30 | % | 33 | % | ||||||

| Asia Pacific |

22 | % | 19 | % | 16 | % | ||||||

2

Table of Contents

For financial information relating to each geographic segment, see Note 21, Segment Information, in the Notes to Consolidated Financial Statements.

Global Industry Practices. Our executive search business also operates in six broad industry groups: Financial Services, Industrial, Consumer Markets, Global Technology and Services, Life Sciences, and Education and Social Enterprise. These industry categories and their relative sizes, as measured by net revenue for 2010 are as follows:

| Global Industry Practices |

Percentage of Net Revenue |

|||

| Financial Services |

31 | % | ||

| Industrial |

23 | % | ||

| Global Technology & Services |

18 | % | ||

| Consumer Markets |

17 | % | ||

| Life Sciences |

8 | % | ||

| Education and Social Enterprise |

3 | % | ||

| 100 | % | |||

Within each broad industry group are a number of industry sub sectors. Consultants often specialize in one or more sub sectors to provide clients with market intelligence and candidate knowledge specific to their industry. For example, within the Financial Services sector our business is diversified among a number of industry sub sectors including Asset & Wealth Management, Consumer & Commercial Finance, Financial Services Practices & Infrastructure, Investment Banking, Global Markets, Hedge Fund, Insurance, Private Equity Investment Professionals, and Real Estate.

We service our clients through unified global executive search teams who specialize in industry practices. This go-to-market strategy allows us to better leverage our global diversity and market intelligence to provide better client service. Each client is served by one global account team, which we believe is a key differentiator from our competition.

Global Functional Practices. Our executive search consultants also specialize in searches for specific “C-level” functional positions, which are roles that generally report directly to the chief executive officer. These include chief financial officers, chief information officers, chief legal officers, chief marketing officers and chief human resources officers.

Our Global Functional Practices include Chief Executive Officer and Board of Directors; Chief Human Resources Officers; Financial Officers; Information Officers; Interim Executives; Legal, Risk, Compliance & Government Affairs; Marketing, Sales & Strategy Officers; Multicultural & Digital Marketing; Sales Officers; Research & Development; and Supply Chain & Transportation.

Our team of executive search consultants may service clients from any one of our offices around the world. For example, an executive search for a chief financial officer of an industrial company located in the United Kingdom may involve a consultant in the United Kingdom with an existing relationship with the client, another executive search consultant in the United States with expertise in our Industrial practice and a third executive search consultant with expertise in recruiting chief financial officers. This same industrial client may also engage us to perform skill-based assessments for each of its senior managers, which could require the expertise of one of our leadership advisory consultants trained in this service.

Seasonality

There is no discernible seasonality in our business, although as a percentage of total annual net revenue, the first quarter is typically the lowest. Revenue and operating income have historically varied by quarter and are

3

Table of Contents

hard to predict from quarter to quarter. In addition, the volatility in the global economy impacts our quarterly revenue and operating income. On average, the variance between the highest and lowest amount of quarterly net revenue, as expressed as a percentage of annual net revenue, is approximately 5 percentage points.

Clients and Marketing

Our consultants market the firm’s executive search and leadership consulting services through two principal means: targeted client calling and industry networking with clients and referral sources. These efforts are supported by proprietary databases, which provide our consultants with information as to contacts made by their colleagues with particular referral sources, candidates and clients. In addition, we benefit from a significant number of referrals generated by our reputation for high quality service and successfully completed assignments, as well as repeat business resulting from our ongoing client relationships.

Either by agreement with the clients or to maintain strong client relationships, executive search firms generally refrain from recruiting employees of a client, and possibly other entities affiliated with that client, for a specified period of time but typically not more than one year from the commencement of a search. We seek to mitigate any adverse effects of these off-limits arrangements by strengthening our long-term relationships, allowing us to communicate our belief to prospective clients that we can conduct searches without these off-limits arrangements impeding the quality of our work.

No single client accounted for more than 2% of our net revenue in 2010, 2009 or 2008. Our top ten clients in 2010, 2009 and 2008 in aggregate accounted for less than 12% of total net revenue.

Information Management Systems

We rely on technology to support our consultants and staff in the search process. Our technology infrastructure consists of internally developed databases containing candidate profiles and client records, coupled with online services and industry reference sources. We use technology to manage and share information on current and potential clients and candidates, to communicate to both internal and external constituencies and to support administrative functions.

Professional Staff and Employees

Our professionals are generally categorized either as consultants or associates. Associates assist consultants by providing research support, coordinating candidate contact and performing other engagement-related functions. As of December 31, 2010, we had 1,516 full-time equivalent employees, of whom 347 were executive search consultants, 436 were associates and 733 were other search, support and Global Operations Support staff.

In each of the past five years, no single consultant accounted for a material portion of our net revenue. We recruit our consultants from other executive search or human capital firms, or in the case of executive search, consultants new to search who have worked in industries or functions represented by our practices. In the latter case, these are often seasoned executives with extensive contacts and outstanding reputations who are entering the search profession as a second career and who we train in our techniques and methodologies. We are not a party to any collective bargaining agreement, and we consider relations with our employees to be good.

Competition

The executive search industry is highly competitive. While we face competition to some degree from all firms in the industry, we believe our most direct competition comes from four established global retained executive search firms that conduct searches primarily for the most senior-level positions within an organization. In particular, our competitors include Egon Zehnder International, Korn/Ferry International, Russell Reynolds Associates, Inc. and Spencer Stuart & Associates. To a lesser extent, we also face competition from smaller boutique and Internet-based firms that specialize in certain regional markets or industry segments. Each firm with which we compete is also a competitor in the marketplace for effective consultants.

4

Table of Contents

Overall, the search industry has relatively few barriers to entry. Higher barriers exist, however, for global retained executive search firms that can provide leadership consulting services at the senior level. At this level, clients rely more heavily on a search firm’s reputation, global access and the experience level of its consultants. We believe that the segment of executive search in which we compete is more quality-sensitive than price-sensitive. As a result, we compete on the level of service we offer, reflected by our client services specialties and, ultimately, by the quality of our search results. We believe that our emphasis on senior-level executive search, the depth of experience of our search consultants and our global presence enable us to compete favorably with other executive search firms.

Competition in the leadership consulting services markets in which we operate are highly fragmented, with no universally recognized market leaders.

5

Table of Contents

Our executive officers as of March 16, 2011 are as follows:

| Name |

Age | Position With Company | ||||

| L. Kevin Kelly |

45 | President and Chief Executive Officer; Director | ||||

| S. John Kim |

38 | Managing Partner, Global Practices | ||||

| Stephen W. Beard |

39 | Executive Vice President and General Counsel | ||||

| Richard J. Caldera |

53 | Executive Vice President and Chief Human Resources Officer | ||||

| Scott J. Krenz |

59 | Executive Vice President and Chief Financial Officer | ||||

There are no family relationships between any executive officer or director. The following information sets forth the business experience for at least the past five years for each of our executive officers as of March 16, 2011:

L. Kevin Kelly was elected Chief Executive Officer and a Director in September 2006. He was elected President in May 2007. Previously, Mr. Kelly was President, Europe, Middle East, Africa and Asia Pacific from March 2005 to September 2006; Regional Managing Partner, Asia Pacific from September 2002 to March 2005; and Office Managing Partner, Tokyo from February 2002 to September 2002. He joined us in 1997.

S. John Kim joined us in April 2008 and was elected Managing Partner, Global Practices in June 2010. Previously, Mr. Kim was global head of capital markets at another international search firm based in New York; prior to that he was a senior consultant with another large executive search firm based in New York. He focused on executive recruitment in the derivatives, structured products, equity and fixed income sales and trading in New York, London, and Hong Kong. Mr. Kim has also held senior positions at other search firms. During this period, Mr. Kim spent three years in one of the firm’s Seoul, Korea office specializing in senior-level executive search across a number of different industry sectors throughout the Asia Pacific region.

Stephen W. Beard was elected Executive Vice President and General Counsel in November 2010. Mr. Beard was Vice President, Deputy General Council and Chief Compliance Officer from 2008 through November 2010 and Assistant General Counsel from 2003 through 2008. He joined us in 2003. Previously, Mr. Beard worked with Schiff Hardin, LLP, in Chicago where he was a member of the firm’s corporate and securities practice group, representing public and private companies in mergers and acquisitions, corporate finance, securities and corporate governance matters.

Richard J. Caldera joined us in May 2008, when he was elected Executive Vice President and Chief Human Resources Officer. Previously, Mr. Caldera was Senior Vice President, Human Resources, Mergers and Acquisitions, for the Healthcare Sector at Royal Philips Electronics N.V. from 2004 to 2008; Senior Vice President, Human Resources, at Skanska AB from 2002 to 2004; and Vice President and Senior Human Resources Officer, Global Operations at CNA Financial Corporation from 1998 to 2002.

Scott J. Krenz joined us in August 2008, when he was elected Executive Vice President and Chief Financial Officer. Previously, Mr. Krenz was Executive Vice President and Chief Financial Officer at Navigant Consulting from 2007 to 2008; Chief Financial Officer at Sapient Corporation from 2004 to 2006; and held senior finance positions of increasing responsibility at Electronic Data Systems Corporation (EDS) from 1985 to 2004.

6

Table of Contents

In addition to other information in this Form 10-K, the following risk factors should be carefully considered in evaluating our business because such factors may have a significant impact on our business, operating results, cash flows and financial condition. As a result of the risks set forth below and elsewhere in this Form 10-K, and the risks discussed in our other Securities and Exchange Commission filings, actual results could differ materially from those projected in any forward-looking statements.

We depend on attracting and retaining qualified consultants.

Our success depends upon our ability to attract and retain consultants who possess the skills and experience necessary to fulfill our clients’ needs. Our ability to hire and retain qualified consultants could be impaired by any diminution of our reputation, decrease in compensation levels relative to our competitors or modifications of our total compensation philosophy or competitor hiring programs. If we cannot attract, hire and retain qualified consultants, our business, financial condition and results of operations may suffer.

We may not be able to prevent our consultants from taking our clients with them to another firm.

Our success depends upon our ability to develop and maintain strong, long-term relationships with our clients. Although we work on building these relationships between our firm and our clients, in many cases, one or two consultants have primary responsibility for a client relationship. When a consultant leaves one executive search firm and joins another, clients who have established relationships with the departing consultant may move their business to the consultant’s new employer. We may also lose clients if the departing consultant has widespread name recognition or a reputation as a specialist in executing searches in a specific industry or management function. If we fail to limit departing consultants from moving business to another employer, our business, financial condition and results of operations may be adversely affected.

Our success depends on our ability to maintain our professional reputation and brand name.

We depend on our overall professional reputation and brand name recognition to secure new engagements and hire qualified consultants. Our success also depends on the individual reputations of our consultants. We obtain many of our new engagements from existing clients or from referrals by those clients. A client who is dissatisfied with our work can adversely affect our ability to secure new engagements. If any factor hurts our reputation, including poor performance, we may experience difficulties in competing successfully for both new engagements and qualified consultants. Failure to maintain our professional reputation and brand name could seriously harm our business, financial condition and results of operations.

Our net revenue may be affected by adverse economic conditions.

Periods of slowed economic activity, such as that recently experienced, can adversely affect our net revenue. In particular, volatility in the capital markets can affect our net revenue in the Financial Services industry group. Unfavorable changes in economic conditions could cause our business, financial condition and results of operations to suffer.

Because our clients may restrict us from recruiting their employees we may be unable to fill or obtain new executive search assignments.

Clients frequently require us to refrain from recruiting certain of their employees when conducting executive searches on behalf of other clients. These restrictions generally remain in effect for no more than one year following the commencement of an engagement. However, the specific duration and scope of the off-limits arrangements depend on the length of the client relationship, the frequency with which the client engages us to perform searches, the number of assignments we have performed for the client and the potential for future business with the client.

7

Table of Contents

Client restrictions on recruiting their employees could hinder us from fulfilling executive searches. Additionally, if a prospective client believes that we are overly restricted by these off-limits arrangements from recruiting the employees of our existing clients, these prospective clients may not engage us to perform their executive searches. As a result, our business, financial condition and results of operations may suffer.

We face aggressive competition.

The global executive search industry is extremely competitive and highly fragmented. We compete with other large global executive search firms, smaller specialty firms, and more recently with Internet-based firms. Specialty firms can focus on regional or functional markets or on particular industries. Some of our competitors may possess greater resources, greater name recognition and longer operating histories than we do in particular markets or practice areas, or be willing to reduce their fees in order to attract clients and increase market share. There are limited barriers to entry into the search industry and new search firms continue to enter the market. Many executive search firms that have a smaller client base may be subject to fewer off-limits arrangements. In addition, our clients or prospective clients may decide to perform executive searches using in-house personnel. We may not be able to continue to compete effectively with existing or potential competitors. Our inability to meet these competitive challenges could have an adverse impact on our business, financial condition and results of operations.

We rely heavily on information management systems.

Our success depends upon our ability to store, retrieve, process and manage substantial amounts of information. To achieve our goals, we must continue to improve and upgrade our information management systems. We may be unable to license, design and implement, in a cost-effective and timely manner, improved information systems that allow us to compete effectively. In addition, business process reengineering efforts may result in a change in software platforms and programs. Such efforts may result in an acceleration of depreciation expense over the shortened expected remaining life of the software and present transitional problems. In addition, if we experience any interruptions or loss in our information processing capabilities, our business, financial condition and results of operations may suffer.

We face the risk of liability in the services we perform.

We are exposed to potential claims with respect to the executive search process. A client could assert a claim for violations of off-limits arrangements, breaches of confidentiality agreements or professional malpractice. The growth and development of our other leadership advisory services brings with it the potential for new types of claims. In addition, candidates and client employees could assert claims against us. Possible claims include failure to maintain the confidentiality of the candidate’s employment search or for discrimination or other violations of the employment laws or malpractice. In various countries, we are subject to data protection laws impacting the processing of candidate information. We maintain professional liability insurance in amounts and coverage that we believe are adequate; however, we cannot guarantee that our insurance will cover all claims or that coverage will always be available. Significant uninsured liabilities could have a negative impact on our business, financial condition and results of operations.

Our multinational operations may be adversely affected by social, political, legal and economic risks.

We generate substantial revenue outside the United States. We offer our services through a network of offices in 40 countries around the world. We are exposed to the risk of changes in social, political, legal and economic conditions inherent in international operations, which could have a significant impact on our business, financial condition and results of operations. In particular, we conduct business in countries where the legal systems, local laws and trade practices are unsettled and evolving. Commercial laws in these countries are sometimes vague, arbitrary and inconsistently applied. Under these circumstances, it is difficult for us to determine at all times the exact requirements of such local laws. If we fail to comply with local laws, our

8

Table of Contents

business, financial condition and results of operations could suffer. In addition, the global nature of our operations poses challenges to our management, and financial and accounting systems. Failure to meet these challenges could seriously harm our business, financial condition and results of operations.

A significant currency fluctuation between the U.S. dollar and other currencies could adversely impact our operating income.

With our operations in the Americas, Europe and Asia Pacific, we conduct business using various currencies. As we typically transact business in the local currency of our subsidiaries, our profitability may be impacted by the translation of foreign currency financial statements into U.S. dollars. Significant long-term fluctuations in relative currency values, in particular an increase in the value of the U.S. dollar against foreign currencies, could have an adverse effect on our profitability and financial condition.

We may not be able to align our cost structure with net revenue.

We must ensure that our costs and workforce continue to be in proportion to demand for our services. Failure to align our cost structure and headcount with net revenue could adversely affect our business, financial condition, and results of operations.

The global financial crisis could adversely affect the financial position of our clients.

The ongoing financial crisis has tightened credit markets and lowered liquidity levels. Some of our clients may experience serious financial problems due to reduced access to credit and lower revenues resulting in their inability to meet their payment obligation to us.

We may not be able to generate sufficient profits to realize the benefit of our net deferred tax assets.

We establish valuation allowances against deferred tax assets when there is insufficient evidence that we will be able to realize the benefit of these deferred tax assets. We reassess the realizability of the deferred tax assets as facts and circumstances dictate. If after future assessments of the realizability of the deferred tax assets, we determine that a lesser or greater allowance is required, we record a reduction or increase to the income tax expense and the valuation allowance in the period of such determination. The uncertainty surrounding the future realization of our net deferred tax assets could adversely impact our results of operations.

Our inability to successfully integrate consultants hired through acquisitions may have an adverse effect on our business.

We may continue to grow through selective acquisitions, however, we may not be able to identify appropriate acquisition candidates, consummate acquisitions on satisfactory terms or integrate the acquired businesses effectively and profitably into our existing operations. Our future success will depend in part on our ability to complete the integration of acquisitions successfully into our operations. Failure to successfully integrate new employees and complementary businesses may adversely affect our profitability by creating operating inefficiencies that could increase operating expenses as a percentage of net revenues and reduce operating income. Further, after any acquisition, the acquired businesses’ clients may choose not to move their business to us causing an adverse affect on our business, financial condition and results of operations.

We may experience impairment of our goodwill and other intangible assets.

In accordance with generally accepted accounting principles, we perform assessments of the carrying value of our goodwill and other intangible assets at least annually or whenever events occur or circumstances indicate that a carrying amount of these assets may not be recoverable which include, a significant change in business climate, attrition of key personnel, changes in financial condition or results of operations, a prolonged decline in

9

Table of Contents

our stock price and market capitalization, competition , and other factors. In performing these assessments, we must make assumptions regarding the estimated fair value of our goodwill and other intangible assets. These assumptions include estimates of future market growth and trends, forecasted revenue and costs, capital investments, discount rates, and other variables. If the fair market value of one of our reporting units or other long term assets is less than the carrying amount of the related assets, we could be required to record an impairment charge. During 2010, we conducted our annual goodwill impairment assessment which resulted in an estimated fair value over net carrying value of our European reporting unit of approximately five percent. Given the current market conditions and continued economic uncertainty, the fair value of our European reporting unit may deteriorate resulting in an impairment of our goodwill within that unit. Due to continual changes in market and general business conditions, we cannot predict whether, and to what extent, our goodwill and long-lived intangible assets may be impaired in future periods. Any resulting impairment loss could have an adverse impact on our business, financial condition and results of operations.

We have anti-takeover provisions that make an acquisition of us difficult and expensive.

Anti-takeover provisions in our Certificate of Incorporation, our Bylaws and the Delaware laws make it difficult and expensive for someone to acquire us in a transaction which is not approved by our Board of Directors. Some of the provisions in our Certificate of Incorporation and Bylaws include:

| • | a classified board of directors |

| • | limitations on the removal of directors |

| • | limitations on stockholder actions |

| • | the ability to issue one or more series of preferred stock by action of our Board of Directors |

These provisions could discourage an acquisition attempt or other transaction in which stockholders could receive a premium over the current market price for the common stock.

Our ability to access additional credit could be limited.

In the current economic environment, banks can be expected to strictly enforce the terms of our credit agreement. Although we are currently in compliance with the financial covenants of our revolving credit facility, a further deterioration of economic conditions may negatively impact our business resulting in our failure to comply with these covenants, which could limit our ability to borrow funds under our credit facility or from other borrowing facilities in the future. In such circumstances, we may not be able to secure alternative financing or may only be able to do so at significantly higher costs.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

Our corporate headquarters is located in Chicago, Illinois. We have leased offices in major metropolitan areas in 33 countries around the world. All of our offices are leased. We do not own any real estate. The aggregate square footage of office space under lease was 620,809 as of December 31, 2010. These office leases call for future minimum lease payments of approximately $213.3 million and have terms that expire between 2011 and 2024, exclusive of renewal options that we can exercise. Approximately 53,000 square feet of office space has been sublet to third parties.

10

Table of Contents

Our office space and future minimum lease payments by geographic segment as of December 31, 2010 are as follows:

| Square Footage |

Office Leases (in millions) |

|||||||

| Americas |

358,083 | $127.1 | ||||||

| Europe |

157,047 | 64.7 | ||||||

| Asia Pacific |

105,679 | 21.5 | ||||||

| Total |

620,809 | $213.3 | ||||||

We have contingent liabilities from various pending claims and litigation matters arising in the ordinary course of our business, some of which involve claims for damages that may be substantial in amount. Some of these matters are covered by insurance. Although our ultimate liability in the matters discussed below cannot be determined, based upon information currently available, we believe the ultimate resolution of such claims and litigation will not have a material adverse effect on our financial condition, results of operations or liquidity.

European Tax Audit

During the fourth quarter of 2005, a European country commenced a tax audit for the years 2001 through 2004, including an examination of our arrangement with professional service companies that provide consulting services to us. On November 24, 2006, the examining tax authority issued a final assessment in the amount for €4.3 million, consisting of unpaid withholding tax, plus unpaid Value Added Tax (“VAT”). We appealed this assessment, however, in accordance with the local law, we were required to provide a bank guarantee to the tax authority. In September 2009, we received a definitive and final ruling that our appeal with respect to the withholding tax portion of the assessment had been decided in our favor, thereby canceling that assessment. We recovered approximately €4.1 million of the original bank guarantee. In May 2010, we received a definite and final ruling that our appeal with respect to the VAT portion of the assessment had been decided in our favor, thereby canceling that assessment, and the remaining guarantee balance was released to us. See Note 5, Restricted Cash and Note 22, Guarantees.

UK Employee Benefits Trust

On January 27, 2010, HM Revenue & Customs (“HMRC”) in the United Kingdom notified us that it was challenging the tax treatment of certain of our contributions in the United Kingdom to an Employee Benefits Trust between 2002 and 2008. HMRC alleges that these contributions should have been subject to Pay As You Earn tax and Class 1 National Insurance Contributions in the United Kingdom; and HMRC is proposing an adjustment to our payroll tax liability for the affected years. The aggregate amount of HMRC’s proposed adjustment is approximately £3.9 million (equivalent to $6.1 million at December 31, 2010). We have appealed the proposed adjustment. At this time, we believe that the likelihood of an unfavorable outcome with respect to the proposed adjustment is not probable and the potential amount of any loss cannot be reasonably estimated. We also believe that the amount of a final adjustment, if any, would not be material to our financial condition.

Employee Litigation

In March 2010, a court of appeals in Europe reversed a 2008 lower court ruling and entered judgment in favor of a former employee. The former employee was separated from us in 2006 and subsequently commenced litigation, which resulted in 2008’s ruling in our favor. As a result of the 2010 reversal, we recorded a charge of $1.0 million reflecting the cost of the award, net of insurance coverage for which we have received commitments at this time. This amount is a component of other charges on the Consolidated Statement of Operations for the year ended December 31, 2010. We have appealed the reversal and are evaluating the availability of additional insurance coverage.

11

Table of Contents

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market for Registrant’s Common Equity

Our common stock is listed on the Nasdaq Global Stock Market under the symbol “HSII.” The following table sets forth the high and low stock price per share of the common stock for the periods indicated, as reported on the Nasdaq Global Stock Market.

| Year Ended December 31, 2010 |

High | Low | ||||||

| First Quarter |

$ | 32.15 | $ | 24.59 | ||||

| Second Quarter |

30.95 | 21.16 | ||||||

| Third Quarter |

23.30 | 16.29 | ||||||

| Fourth Quarter |

29.90 | 18.22 | ||||||

| Year Ended December 31, 2009 |

||||||||

| First Quarter |

$ | 22.29 | $ | 13.52 | ||||

| Second Quarter |

23.51 | 16.50 | ||||||

| Third Quarter |

26.46 | 15.65 | ||||||

| Fourth Quarter |

31.65 | 21.76 | ||||||

As of March 10, 2011, the last reported price on the Nasdaq Global Stock Market for our common stock was $25.79 per share, and there were 107 stockholders of record of the common stock.

12

Table of Contents

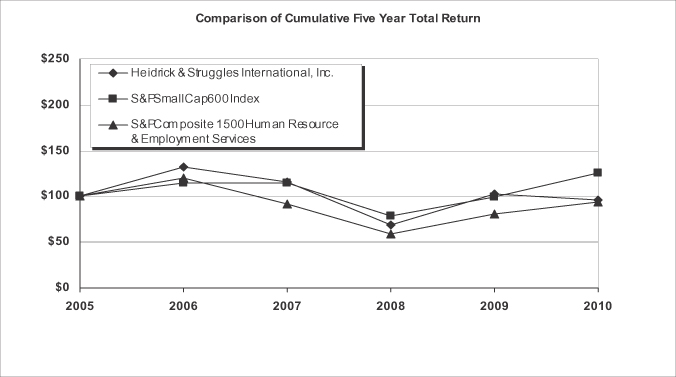

Performance Graph

We have presented below a graph which compares the cumulative total stockholder return on our common shares with the cumulative total stockholder return of the Standard & Poor’s SmallCap 600 Index and the Standard & Poor’s Composite 1500 Human Resource and Employment Services Index. Cumulative total return for each of the periods shown in the performance graph is measured assuming an initial investment of $100 on December 31, 2005.

The stock price performance depicted in this graph is not necessarily indicative of future price performance. This graph will not be deemed to be filed as part of this Form 10-K and will not be deemed to be incorporated by reference by any general statement incorporating this Form 10-K into any filing by us under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent we specifically incorporate this information by reference.

Comparison of Five-Year Cumulative Total Return*

Comparison is among Heidrick & Struggles, the S&P SmallCap 600 Index and the S&P Composite 1500 Human Resource & Employment Services Index. The S&P Composite 1500 Human Resource & Employment Services Index includes 13 companies in related businesses, including Heidrick & Struggles.

*Assuming $100 invested on 12/31/05 in HSII or index, including reinvestment of dividends.

Source: Standard & Poor’s

13

Table of Contents

Dividends

Since September 2007, we have paid a quarterly cash dividend of $0.13 per share as approved by our Board of Directors. In 2010, the total cash dividend paid was $0.52 per share.

The following table outlines the record date, payment date and amount of quarterly cash dividends paid during 2009 and 2010:

|

Quarter |

Record Date |

Payment Date |

Dividends | |||

| Q4 2008 |

February 6, 2009 |

February 20, 2009 | $2.1 | |||

| Q1 2009 |

May 1, 2009 |

May 15, 2009 | 2.2 | |||

| Q2 2009 |

August 7, 2009 |

August 21, 2009 | 2.2 | |||

| Q3 2009 |

November 6, 2009 |

November 20, 2009 | 2.2 | |||

| Q4 2009 |

February 5, 2010 |

February 19, 2010 | 2.2 | |||

| Q1 2010 |

May 7, 2010 |

May 21, 2010 | 2.3 | |||

| Q2 2010 |

August 6, 2010 |

August 20, 2010 | 2.3 | |||

| Q3 2010 |

November 5, 2010 |

November 19, 2010 | 2.3 |

Cash dividends payable of $2.3 million related to the fourth quarter 2010 cash dividend, which was paid in the first quarter of 2011, and cash dividends payable of $2.2 million related to the fourth quarter 2009 cash dividend, which was paid in the first quarter of 2010, are accrued in the Consolidated Balance Sheets as of December 31, 2010 and 2009, respectively.

In connection with the quarterly cash dividend, we also pay a dividend equivalent on outstanding restricted stock units. The amounts related to the dividend equivalent payments for restricted stock units are accrued over the vesting period and paid upon vesting. In 2010 and 2009, we paid $0.7 million and $0.6 million, respectively, in dividend equivalent payments.

Issuer Purchases of Equity Securities

The following table provides information related to our purchase of common shares for the quarter ended December 31, 2010. For further information of our share repurchase activity, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.”

|

Period |

Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

Approximate Dollar Value of Shares That May Yet Be Purchased Under Publicly Announced Plans or Programs |

||||||||||||

| Oct. 1, 2010 – Oct. 31, 2010 |

— | $ | — | — | $ | 22,788,650 | ||||||||||

| Nov. 1, 2010 – Nov. 30, 2010 |

— | — | — | 22,788,650 | ||||||||||||

| Dec. 1, 2010 – Dec. 31, 2010 |

— | — | — | 22,788,650 | ||||||||||||

| Total |

— | — | — | |||||||||||||

On May 24, 2007, our Board of Directors authorized management to repurchase shares of our common stock with an aggregate purchase price up to $50 million. We purchased 1,403,738 shares of our common stock for $50 million under the May 2007 authorization, which was completed during the first quarter of 2008.

On February 8, 2008, our Board of Directors authorized management to repurchase shares of our common stock with an aggregate purchase price up to $50 million. As of December 31, 2008, we purchased 951,160 shares of our common stock under the February 2008 authorization for a total of $27.2 million. We intend from time to time and as business conditions warrant, to purchase shares of our common stock on the open market or in negotiated or block trades. No time limit has been set for completion of this program. We did not repurchase any shares during 2009 or 2010. As of December 31, 2010 and 2009, $22.8 million remains available under this authorization.

14

Table of Contents

ITEM 6. SELECTED FINANCIAL DATA

The selected financial data presented below have been derived from our audited consolidated financial statements. The data as of December 31, 2010 and 2009 and for the years ended December 31, 2010, 2009 and 2008 are derived from the audited current and historical consolidated financial statements, which are included elsewhere in this Form 10-K. The data as of December 31, 2008, 2007 and 2006 and for the years ended December 31, 2007 and 2006 are derived from audited historical consolidated financial statements, which are not included in this report. The data set forth is qualified in its entirety by, and should be read in conjunction with, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the audited consolidated financial statements, the notes thereto, and the other financial data and statistical information included in this Form 10-K.

| Year Ended December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| (in thousands, except per share and other operating data) | ||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Revenue: |

||||||||||||||||||||

| Revenue before reimbursements (net revenue) |

$ | 493,091 | $ | 395,651 | $ | 615,904 | $ | 619,654 | $ | 478,523 | ||||||||||

| Reimbursements |

20,145 | 19,067 | 28,956 | 28,612 | 23,471 | |||||||||||||||

| Total revenue |

513,236 | 414,718 | 644,860 | 648,266 | 501,994 | |||||||||||||||

| Operating expenses: |

||||||||||||||||||||

| Salaries and employee benefits |

340,178 | 281,545 | 435,306 | 418,952 | 328,714 | |||||||||||||||

| General and administrative expenses |

130,622 | 115,758 | 125,061 | 121,198 | 99,352 | |||||||||||||||

| Other charges |

4,218 | (1) | — | — | — | — | ||||||||||||||

| Reimbursed expenses |

20,145 | 19,067 | 28,956 | 28,612 | 23,471 | |||||||||||||||

| Restructuring and impairment charges |

1,621 | (2) | 26,720 | (4) | — | — | 408 | |||||||||||||

| Other operating income |

(1,072 | )(3) | (1,661 | )(5) | — | — | — | |||||||||||||

| Total operating expenses |

495,712 | 441,429 | 589,323 | 568,762 | 451,945 | |||||||||||||||

| Operating income (loss) |

17,524 | (26,711 | ) | 55,537 | 79,504 | 50,049 | ||||||||||||||

| Non-operating income (expense): |

||||||||||||||||||||

| Interest income, net |

813 | 1,201 | 5,103 | 8,035 | 6,257 | |||||||||||||||

| Other, net |

(1,389 | ) | (4,189 | )(6) | 1,613 | (404 | ) | (1,040 | ) | |||||||||||

| Net non-operating income (expense) |

(576 | ) | (2,988 | ) | 6,716 | 7,631 | 5,217 | |||||||||||||

| Income (loss) before income taxes |

16,948 | (29,699 | ) | 62,253 | 87,135 | 55,266 | ||||||||||||||

| Provision for (benefit from) income taxes |

9,455 | (8,791 | ) | 23,179 | 30,672 | 21,023 | ||||||||||||||

| Net income (loss) |

$ | 7,493 | $ | (20,908 | ) | $ | 39,074 | $ | 56,463 | $ | 34,243 | |||||||||

| Basic earnings (loss) per common share |

$ | 0.43 | $ | (1.24 | ) | $ | 2.33 | $ | 3.16 | $ | 1.91 | |||||||||

| Basic weighted average common shares outstanding |

17,437 | 16,901 | 16,747 | 17,854 | 17,925 | |||||||||||||||

| Diluted earnings (loss) per common share |

$ | 0.42 | $ | (1.24 | ) | $ | 2.20 | $ | 2.97 | $ | 1.81 | |||||||||

| Diluted weighted average common shares outstanding |

17,869 | 16,901 | 17,727 | 18,984 | 18,916 | |||||||||||||||

| Dividends per share |

$ | 0.52 | $ | 0.52 | $ | 0.52 | $ | 0.26 | — | |||||||||||

| Balance Sheet Data (at end of period): |

||||||||||||||||||||

| Working capital |

$ | 140,010 | $ | 127,661 | $ | 140,139 | $ | 117,861 | $ | 135,880 | ||||||||||

| Total assets |

545,027 | 474,847 | 590,303 | 616,884 | 513,309 | (7) | ||||||||||||||

| Long-term debt, less current maturities |

— | — | — | — | — | |||||||||||||||

| Stockholders’ equity |

294,542 | 290,852 | 306,304 | 309,800 | 263,705 | |||||||||||||||

| Other Operating Data: |

||||||||||||||||||||

| Average number of consultants during the period |

353 | 385 | 413 | 401 | 348 | |||||||||||||||

15

Table of Contents

Notes to Selected Financial Data:

| (1) | In 2010, we recorded other charges of $4.2 million, which consists of $3.2 million of accelerated occupancy costs and depreciation, dilapidation costs, and professional fees related to the settlement of our lease obligations for our former London office which we vacated and $1.0 million due to an unfavorable judgment in a lawsuit filed by a former European employee separated from us in 2006. See Note 18, Other Charges, in the Notes to Consolidated Financial Statements. |

| (2) | In 2010, we recorded restructuring charges of $1.6 million. These charges consist of $0.6 million of severance associated with reductions in our workforce of 19 employees globally in connection with continued initiatives to reduce our overall costs and improve operational efficiencies and $1.0 million related to the default of two of our subtenants in previously restructured offices. By segment, the restructuring charges recorded in 2010 were $1.0 million in the Americas, $0.3 million in Europe, and $0.3 million in Global Operations Support. |

| (3) | In 2010, as a result of continued lower than expected 2010 revenue production from consultants acquired in the Ray and Berndston Sp. z o. o acquisition, we performed a fair value assessment of the potential future earnout payments under the purchase agreement. This assessment indicated that there would not be any future earnout payments and resulted in a $1.1 million adjustment. Under the acquisition method of accounting for business combinations, we recognized the fair value adjustment as other operating income in the Consolidated Statement of Operations. |

| (4) | In 2009, we recorded restructuring charges of $22.9 million in connection with initiatives to reduce overall costs and improve operational efficiencies. These charges relate to severance and other employee-related costs associated with reductions in our workforce of 363 employees globally and included 75 executive search consultants. By segment, the restructuring charges recorded in 2009 were $9.5 million in the Americas, $9.5 million in Europe, $2.4 million in Asia Pacific and $1.5 million in Global Operations Support. Additionally, during 2009 we recorded a reduction of $0.3 million in Europe related to a previously restructured office. As a result of our workforce reductions in January and May 2009 and continued business and economic uncertainty, we performed an evaluation of the remaining client relationship intangible asset associated with our 2006 acquisition of Highland Partners. Based on this analysis, we recorded an impairment charge related to the Americas region of $3.8 million. Additionally, the deterioration in business performance from the consultants acquired in the Ray and Berndtson Sp. z o. o acquisition triggered a review of the client relationship intangible assets associated with this acquisition, resulting in an impairment charge in the European region of $0.2 million. See Note 10, Goodwill and Other Intangible Assets, in the Notes to Consolidated Financial Statements. |

| (5) | In 2009, as a result of significantly lower than expected 2009 revenue production from consultants acquired in the Ray and Berndtson Sp. z o. o acquisition and uncertainty regarding their future performance, we performed a fair value assessment of the potential future earnout payments under the purchase agreement. This assessment resulted in a $1.7 million reduction to the original earnout accrual. Under the acquisition method of accounting for business combinations, we recognized the fair value adjustment as other operating income in the Consolidated Statement of Operations. |

| (6) | In 2009, we wrote-off our investment in VisualCV, Inc. of $3.0 million. |

| (7) | In 2007, we determined that the UK Employee Benefit Trust should not be consolidated and as a result reduced total assets and liabilities by $6.5 million in 2006. |

16

Table of Contents

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Management’s Discussion and Analysis of Financial Condition and Results of Operations as well as other sections of this annual report on Form 10-K contain forward-looking statements. The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements. The forward-looking statements are based on current expectations, estimates, forecasts and projections about the industry in which we operate and management’s beliefs and assumptions. Forward-looking statements may be identified by the use of words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “projects,” “forecasts,” and similar expressions. Forward-looking statements are not guarantees of future performance and involve certain known and unknown risks, uncertainties and assumptions that are difficult to predict. Actual outcomes and results may differ materially from what is expressed, forecasted or implied in the forward-looking statements. Factors that may affect the outcome of the forward-looking statements include, among other things, our ability to attract and retain qualified executive search consultants; further declines in the global economy and our ability to execute successfully through business cycles; the timing, speed or robustness of any future economic recovery; social or political instability in markets where we operate, the impact of foreign currency exchange rate fluctuations; price competition; the ability to forecast, on a quarterly basis, variable compensation accruals that ultimately are determined based on the achievement of annual results; our ability to realize our tax losses; the timing of the establishment or reversal of valuation allowance on deferred tax assets; the mix of profit and loss by country; an impairment of our goodwill and other intangible assets; delays in the development and/or implementation of new technology and systems; and the ability to meet and achieve the expected savings resulting from cost-reduction initiatives and restructuring activities. For more information on the factors that could affect the outcome of forward-looking statements, see Risk Factors in Item 1A of this Form 10-K. We caution the reader that the list of factors may not be exhaustive. We undertake no obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

Executive Overview

Our Business

We are a leadership advisory firm providing executive search and leadership consulting services. We help our clients build leadership teams by facilitating the recruitment, management and deployment of senior executives. Focusing on top-level services offers us several advantages that include access to and influence with key decision makers, increased potential for recurring search consulting engagements, higher fees per search, enhanced brand visibility, and a leveraged global footprint, which create added barriers to entry for potential competitors. Working at the top of client organizations also allows us to attract and retain high-caliber consultants.

In addition to executive search, we provide a range of leadership consulting services to clients. These services include succession planning, executive assessment, talent retention management, executive development, transition consulting for newly appointed executives, and mergers and acquisitions human capital integration consulting.

We provide our services to a broad range of clients through the expertise of 347 consultants located in 36 countries throughout the world as of December 31, 2010. Our executive search services are provided on a retained basis. Revenue before reimbursements of out-of-pocket expenses (“net revenue”) consists of retainers and indirect expenses billed to clients. Typically, we are paid a retainer for our executive search services equal to approximately one-third of the estimated first year compensation for the position to be filled. In addition, if the actual compensation of a placed candidate exceeds the estimated compensation, we often are authorized to bill the client for one-third of the excess. Indirect expenses are calculated as a percentage of the retainer with certain dollar limits per search.

17

Table of Contents

Key Performance Indicators

We manage and assess Heidrick & Struggles’ performance through various means, with the primary financial and operational measures including net revenue growth, operating income, operating margin, consultant headcount, confirmation trends, consultant productivity, and average revenue per search or project.

Revenue growth is driven by a combination of an increase in executive search wins and leadership consulting projects, higher consultant productivity, higher average revenue per search or project and the hiring of additional consultants. With the exception of compensation expense, incremental increases in revenue do not necessarily result in proportional increases in costs, particularly operating and administrative expenses, thus potentially improving operating margins.

The number of consultants, confirmation trends, number of searches or projects completed, productivity levels and the average revenue per search or project will vary from quarter to quarter, affecting revenue growth and operating margin.

Our Compensation Model

At the consultant level, individuals are largely rewarded for their performance based on a system that directly ties a significant portion of their compensation to the amount of net revenue for which they are responsible. A proportion of the rewards is based upon individual performance against a series of non-financial measures. Credit towards the variable portion of a consultant’s compensation is earned by generating net revenue for winning and executing work. Each quarter, we review and update the expected annual performance of all consultants and accrue variable compensation accordingly. The amount of variable compensation that is accrued for each consultant is based on a tiered payout model and adjusted for overall Company performance. The more net revenue that is generated by the consultant, the higher the percentage credited towards the consultant’s variable compensation and thus accrued by our company as expense. The mix of individual consultants who generate the revenue can significantly affect the total amount of compensation expense recorded and thus, operating margins. As a result, the variable portion of the compensation expense may fluctuate significantly from quarter to quarter. The total variable compensation is discretionary and is based on company-wide profitability targets approved by the Human Resources and Compensation Committee of the Board of Directors.

In 2008, the portion of bonus previously deferred into restricted stock units was changed to be in the form of deferred cash to be paid ratably over a three year period for consultants and management globally. In 2008, a premium of 10% was applied to the bonus amount deferred. In 2009 and 2010, we continued with the bonus cash deferral arrangement but did not apply a premium to the amounts deferred. The portion of the bonus that is deferred varies between 10% and 15% depending on the employee’s level or position.

The compensation expense related to the amounts being deferred is recognized on a graded vesting attribution method over the requisite service period. This service period begins on January 1 of the respective fiscal year and continues through the deferral date which coincides with our bonus payments in the first quarter of the following year and for an additional three year vesting period. The deferrals vest and are paid ratably over the three year vesting period and are recorded in accrued salaries and employee benefits and other non-current liabilities in the Consolidated Balance Sheets. We will continue to grant restricted stock units under other existing programs.

2010 Overview

Consolidated net revenue of $493.1 million increased 24.6% or $97.4 million in 2010, compared to 2009. Net revenue increased 26.9% in the Americas, 6.6% in Europe and 47.5% in Asia Pacific. Consultant productivity measured by net revenue per consultant increased to $1.4 million for the year ended December 31, 2010 compared to $1.0 million for the year ended December 31, 2009. Average revenue per executive search was $108,500 for the year ended December 31, 2010 compared to $101,000 for the year ended December 31, 2009.

18

Table of Contents

Operating income as a percentage of net revenue was 3.6% in 2010 compared to operating loss as a percentage of net revenue of 6.8% in 2009 primarily as a result of an increase in net revenue of 24.6%, a decrease in restructuring and impairment charges of $25.1 million, offset by increases in salaries and employee benefits expense of 20.8%, general and administrative expenses of 12.8%, other charges of $4.2 million and a decrease in other operating income of $0.6 million. Salaries and employee benefits expense as a percentage of net revenue decreased from 71.2% in 2009 to 69.0% in 2010. General and administrative expenses as a percentage of net revenue decreased from 29.3% in 2009 to 26.5% in 2010.

We ended the year with a combined cash and cash equivalents balance of $181.1 million, an increase of $58.1 million compared to a combined cash and cash equivalents balance of $123.0 million at December 31, 2009. We pay the majority of bonuses in the first quarter following the year in which they were earned. Employee bonuses are accrued throughout the year and are based on the Company’s performance and the performance of the individual employee. In early 2011, we expect to pay approximately $91 million related to the 2010 bonus accruals.

2011 Outlook

We are currently forecasting 2011 net revenue of between $515 million and $545 million and an operating margin of between 6 and 10 percent, for the year ending December 31, 2011.

Results of Operations

The following table summarizes, for the periods indicated, the results of operations (in thousands):

| Year Ended December 31, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| Revenue: |

||||||||||||

| Revenue before reimbursements (net revenue) |

$ | 493,091 | $ | 395,651 | $ | 615,904 | ||||||

| Reimbursements |

20,145 | 19,067 | 28,956 | |||||||||

| Total revenue |

513,236 | 414,718 | 644,860 | |||||||||

| Operating expenses (income): |

||||||||||||

| Salaries and employee benefits |

340,178 | 281,545 | 435,306 | |||||||||

| General and administrative expenses |

130,622 | 115,758 | 125,061 | |||||||||

| Other charges |

4,218 | — | — | |||||||||

| Reimbursed expenses |

20,145 | 19,067 | 28,956 | |||||||||

| Restructuring and impairment charges |

1,621 | 26,720 | — | |||||||||

| Other operating income |

(1,072 | ) | (1,661 | ) | — | |||||||

| Total operating expenses |

495,712 | 441,429 | 589,323 | |||||||||

| Operating income (loss) |

17,524 | (26,711 | ) | 55,537 | ||||||||

| Non-operating income (expense): |

||||||||||||

| Interest income, net |

813 | 1,201 | 5,103 | |||||||||

| Other, net |

(1,389 | ) | (4,189 | ) | 1,613 | |||||||

| Net non-operating income (expense) |

(576 | ) | (2,988 | ) | 6,716 | |||||||

| Income (loss) before income taxes |

16,948 | (29,699 | ) | 62,253 | ||||||||

| Provision for (benefit from) income taxes |

9,455 | (8,791 | ) | 23,179 | ||||||||

| Net income (loss) |

$ | 7,493 | $ | (20,908 | ) | $ | 39,074 | |||||

19

Table of Contents

The following table summarizes, for the periods indicated, our selected statements of operations data as a percentage of revenue before reimbursements (net revenue):

| Year Ended December 31, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| Revenue: |

||||||||||||

| Revenue before reimbursements (net revenue) |

100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Reimbursements |

4.1 | 4.8 | 4.7 | |||||||||

| Total revenue |

104.1 | 104.8 | 104.7 | |||||||||

| Operating expenses: |

||||||||||||

| Salaries and employee benefits |

69.0 | 71.2 | 70.7 | |||||||||

| General and administrative expenses |

26.5 | 29.3 | 20.3 | |||||||||

| Other charges |

0.9 | — | — | |||||||||

| Reimbursements |

4.1 | 4.8 | 4.7 | |||||||||

| Restructuring and impairment charges |

0.3 | 6.8 | — | |||||||||

| Other operating income |

(0.2 | ) | (0.4 | ) | — | |||||||

| Total operating expenses |

100.5 | 111.6 | 95.7 | |||||||||

| Operating income (loss) |

3.6 | (6.8 | ) | 9.0 | ||||||||

| Non-operating income (expense) |

||||||||||||

| Interest income, net |

0.2 | 0.3 | 0.9 | |||||||||

| Other, net |

(0.3 | ) | (1.1 | ) | 0.2 | |||||||

| Net non-operating income (expense) |

(0.1 | ) | (0.8 | ) | 1.1 | |||||||

| Income (loss) before income taxes |

3.4 | (7.5 | ) | 10.1 | ||||||||

| Provision for (benefit from) income taxes |

1.9 | (2.2 | ) | 3.8 | ||||||||

| Net income (loss) |

1.5 | % | (5.3 | )% | 6.3 | % | ||||||

| Note: | Totals and subtotals may not equal the sum of individual line items due to rounding. |

We operate our executive search and leadership consulting services in three geographic regions: the Americas; Europe, which includes the Middle East and Africa; and Asia Pacific.

For segment purposes, reimbursements of out-of-pocket expenses classified as revenue, restructuring and impairment charges and other operating income are reported separately and, therefore, are not included in the results of each geographic region. We believe that analyzing trends in revenue before reimbursements (net revenue), analyzing operating expenses as a percentage of net revenue, and analyzing operating income (loss) excluding restructuring and impairment charges and other operating income, more appropriately reflects our core operations. By segment the restructuring charges recorded in 2010 were $1.0 million in the Americas, $0.3 million in the European region, and $0.3 million in Global Operations Support. The other operating income of $1.1 million in 2010 was recorded in the European region. By segment, the restructuring and impairment charges recorded in 2009 were $13.3 million in the Americas, $9.5 million in Europe, $2.4 million in Asia Pacific and $1.5 million in Global Operations Support. The other operating income of $1.7 million in 2009 was recorded in the European region.

20

Table of Contents

The following table sets forth, for the periods indicated, our revenue and operating income (loss) by segment (in thousands):

| Year Ended December 31, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| Revenue: |

||||||||||||

| Americas |

$ | 255,690 | $ | 201,530 | $ | 314,412 | ||||||

| Europe |

127,267 | 119,441 | 201,462 | |||||||||

| Asia Pacific |

110,134 | 74,680 | 100,030 | |||||||||

| Revenue before reimbursements (net revenue) |

493,091 | 395,651 | 615,904 | |||||||||

| Reimbursements |

20,145 | 19,067 | 28,956 | |||||||||

| Total |

$ | 513,236 | $ | 414,718 | $ | 644,860 | ||||||

| Operating income (loss): |

||||||||||||

| Americas |

$ | 40,307 | $ | 18,509 | $ | 45,783 | ||||||

| Europe |

(604 | ) | 2,741 | 24,479 | ||||||||

| Asia Pacific |

24,517 | 9,457 | 15,351 | |||||||||

| Total regions |

64,220 | 30,707 | 85,613 | |||||||||

| Global Operations Support |

(46,147 | ) | (32,359 | ) | (30,076 | ) | ||||||

| Operating income (loss) before restructuring and impairment charges and other operating income |

18,073 | (1,652 | ) | 55,537 | ||||||||

| Restructuring and impairment charges |

(1,621 | ) | (26,720 | ) | — | |||||||

| Other operating income |

1,072 | 1,661 | — | |||||||||

| Total |

$ | 17,524 | $ | (26,711 | ) | $ | 55,537 | |||||

2010 Compared to 2009

Total revenue. Consolidated total revenue increased $98.5 million, or 23.8%, to $513.2 million in 2010 from $414.7 million in 2009. The increase in total revenue was due to the increase in revenue before reimbursements (net revenue).

Revenue before reimbursements (net revenue). Consolidated net revenue increased $97.4 million, or 24.6%, to $493.1 million in 2010 from $395.7 million in 2009. The positive impact of exchange rate fluctuations resulted in approximately one percentage point of the increase in 2010. Net revenue increased in all regions and industry groups with significant growth in the Global Technology & Services and Financial Services industry groups. In 2010, the number of confirmed executive searches increased 14.5% to 4,181 from 3,651 in 2009. The number of consultants decreased to 347 as of December 31, 2010 compared to 359 as of December 31, 2009. Productivity, as measured by annualized net revenue per consultant, increased to $1.4 million for the year ended December 31, 2010 from $1.0 million for the year ended December 31, 2009, and average revenue per executive search was $108,500 for the year ended December 31, 2010 compared to $101,000 for the year ended December 31, 2009.

Net revenue in the Americas was $255.7 million in 2010, an increase of $54.2 million, or 26.9% from $201.5 million in 2009. The positive impact of exchange rate fluctuations in Canada and Latin America resulted in approximately one percentage point of the increase in 2010. Net revenue in Europe was $127.3 million in 2010, an increase of $7.8 million, or 6.6% from $119.4 million in 2009. The negative impact of exchange rate fluctuations offset the increase in net revenue by approximately 3 percentage points in 2010. Net revenue in Asia Pacific was $110.1 million in 2010, an increase of $35.5 million, or 47.5% from $74.7 million in 2009. The positive impact of exchange rate fluctuations resulted in approximately 9 percentage points of the increase in 2010.

21

Table of Contents

Salaries and employee benefits. Consolidated salaries and employee benefits expense increased $58.6 million or 20.8% to $340.2 million in 2010 from $281.5 million in 2009. The increase in salaries and employee benefits expense is primarily a result of a $62.7 million increase in performance-related compensation expense reflecting higher bonus accruals associated with higher net revenue. Included in this increase is approximately $7.1 million of discretionary consultant compensation related to individual performance factors. The increase in performance-related compensation expense was offset by a $4.1 million decrease in fixed compensation primarily related to a year-over-year decline in stock-based compensation of $11.3 million as a result of a decrease in the amount of equity awards granted in 2009 and 2010 and significant forfeitures in 2010, and a $3.9 million decrease in amortization of deferred cash compensation associated with lower 2009 bonus accruals due to lower 2009 net revenue levels and consultant headcount. These decreases were partially offset by a $0.8 million increase in base compensation, payroll taxes, and other employee-related expenses associated with increased headcount and the restoration of salaries following a 5% salary reduction in 2009, additional severance expense of $2.7 million, and $1.5 million primarily due to the reinstatement of the Company’s 401(k) match in 2010. In 2010, we issued special recognition awards to certain of our consultants in order to incentivize future service to the Company which resulted in additional fixed compensation expense of $6.1 million. At December 31, 2010 we had 1,516 total employees, up 8.3% compared to 1,400 total employees at December 31, 2009.

Excluding a negative impact of $3.7 million due to exchange rate fluctuations, which we believe provides a better comparison of operational performance, consolidated salaries and employee benefits expense increased by 19.6% versus 20.8% as reported in 2010 compared to 2009.

As a percentage of net revenue, salaries and employee benefits expense decreased to 69.0% in 2010 from 71.2% in 2009.

General and administrative expenses. Consolidated general and administrative expenses increased $14.9 million, or 12.8%, to $130.6 million in 2010 from $115.8 million in 2009. The increase reflects $8.0 million in fees for professional services primarily related to investments in various initiatives intended to yield cost savings and improve productivity. These initiatives include additional hiring, increased training and development programs, the outsourcing of a portion of our information technology function, and the ongoing development of our internal search system. The increase also included non-recurring legal costs incurred in 2010, offset by a decrease in expenses related to a process improvement project aimed at increasing operational effectiveness and efficiency, which we substantially completed during 2010.