Attached files

| file | filename |

|---|---|

| EX-12 - EX-12 - STR HOLDINGS, INC. | a2202541zex-12.htm |

| EX-21 - EX-21 - STR HOLDINGS, INC. | a2202541zex-21.htm |

| EX-23 - EX-23 - STR HOLDINGS, INC. | a2202541zex-23.htm |

| EX-32.1 - EX-32.1 - STR HOLDINGS, INC. | a2202541zex-32_1.htm |

| EX-31.2 - EX-31.2 - STR HOLDINGS, INC. | a2202541zex-31_2.htm |

| EX-32.2 - EX-32.2 - STR HOLDINGS, INC. | a2202541zex-32_2.htm |

| EX-31.1 - EX-31.1 - STR HOLDINGS, INC. | a2202541zex-31_1.htm |

| EX-10.29 - EX-10.29 - STR HOLDINGS, INC. | a2202541zex-10_29.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

PART IV

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2010 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to . |

||

Commission file number 001-34529

STR Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

27-1023344 (I.R.S. Employer Identification No.) |

|

1699 King Street, Enfield, Connecticut (Address of principal executive offices) |

06082 (Zip code) |

Registrant's telephone number, including area code: (860) 758-7300

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock $0.01 par value per share | New York Stock Exchange |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ý NO o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES o NO ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ý NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES o NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES o NO ý

The aggregate market value of the registrant's voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2010 was $518,939,408 based on the price of the last reported sale on the New York Stock Exchange on that date.

On March 7, 2011, the registrant had 41,507,247 outstanding shares of Common Stock, $0.01 par value per share.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the registrant's Proxy Statement for the 2011 Annual Meeting of Stockholders, which will be filed by the registrant on or prior to 120 days following the end of the registrant's fiscal year ended December 31, 2010, are incorporated by reference into Part III of this Annual Report on Form 10-K.

Overview

STR Holdings, Inc. and its subsidiaries ("we", "us","our" or the "Company") conduct business in two segments.

We are a leading global provider of encapsulants to the solar module industry. The encapsulant is a critical component used in solar modules. We were the first to develop the original ethylene-vinyl-acetate ("EVA") encapsulants used in commercial solar module manufacturing in the 1970s in conjunction with the Jet Propulsion Laboratory of the California Institute of Technology under a NASA contract for the U.S. Energy Research and Development Administration, which later became known as the U.S. Department of Energy. We supply encapsulants to many of the major solar module manufacturers and believe we were the primary supplier of encapsulants to the majority of our top 10 customers in 2010. We believe this is due to our superior product performance, global manufacturing base, customer service and technical support. Our encapsulants are used in both crystalline silicon and thin-film solar modules.

Our Quality Assurance business is a leader in the consumer products quality assurance market. We believe our Quality Assurance business represents the only global testing services provider exclusively focused on the consumer products market. Our Quality Assurance business provides inspection, testing, auditing and consulting services that enable retailers and manufacturers to determine whether products and facilities meet applicable safety, regulatory, quality, performance, social and ethical standards.

Solar Energy Overview

Solar energy has emerged as one of the most rapidly growing renewable energy sources. A number of different technologies have been developed to harness solar energy. The most prevalent technology is the use of inter-connected photovoltaic ("PV") cells to generate electricity directly from sunlight. Solar energy has many advantages over other existing renewable energy sources and traditional non-renewable energy sources relative to environmental impact, delivery risk, distributed nature of generation and matching of peak generation with demand.

PV systems have been used to produce electricity for several decades. However, technological advances during the past decade and rising costs of electricity, combined with the recognition of the advantages of solar power as a renewable energy source and the availability of government subsidies and incentives for solar power, have led to solar power becoming one of the fastest growing renewable energy technologies.

According to Solarbuzz, an independent solar energy research firm, solar power industry revenues were approximately $82 billion in 2010 up from approximately $4 billion in 2003.

One of the key drivers of the growing demand for solar power is government incentive programs for the development of solar energy, which make solar energy more cost competitive. In recent years, the largest growth in the demand for solar energy has been in the European Union where government incentives are typically in the form of feed-in tariffs in which utility companies are legally obligated to purchase electricity from renewable energy sources at a guaranteed rate that is higher than the standard grid electricity price. However, some European countries are gradually reducing these incentives. For example, in 2008, Spain enacted new legislation that capped the incentive rate at 500 megawatts and Germany had an out of cycle reduction mainly in response to the reduced cost of solar panels and internal rate of returns in excess of what is required to stimulate growth. Germany and Italy enacted additional reductions that took place in the second half of 2010. In 2011, Germany also enacted further legislation to accelerate the annual year-end feed-in-tariff reduction to July 1, 2011

3

for roof-top systems and September 1, 2011 for ground-mount projects. In the United States, government incentive programs are generally in the form of tax credits, loan guarantees and grants. Also, many states, including California, have enacted renewable portfolio standards that require utilities to increase their production of renewable energy sources including solar PV. The United States, China and a number of other countries have recently enacted new legislation supporting solar energy. Government incentive programs have developed in response to the increasing scarcity and rising prices of conventional energy sources, the desire for energy security/energy independence to counter perceived geopolitical supply risks surrounding fossil fuels, increasing concerns about environmental pollution and global warming from fossil fuels and the consequent tightening of emission controls and changing consumer preferences toward renewable energy sources.

Despite the favorable conditions for the adoption of solar electricity generation, solar energy continues to represent only a very small fraction of the world's energy output.

Solar Energy Systems

Solar electricity is primarily generated by PV systems that are comprised of solar modules, mounting structures and electrical components. PV systems are either grid-connected or off-grid. Grid-connected systems are connected to the electricity transmission and distribution grid and feed solar electricity into the end-user's electrical system and/or the grid. Such systems are commonly mounted on the rooftops of buildings, integrated into building facades or installed on the ground using support structures and range in size from 2-3 kilowatts to multiple megawatts. Off-grid PV systems are typically much smaller and are frequently used in remote areas where they may be the only source of electricity for the end-user.

Solar Modules

PV cells are semiconductor devices that act as converters, taking sunlight and converting it directly into electricity by a process known as the photovoltaic effect. A solar module is an assembly of PV cells that are electrically inter-connected, laminated and framed in a durable and weatherproof package.

There are two primary commercialized categories of solar cells: crystalline silicon and thin-film. PV devices can be manufactured using different semiconductor materials, including mono- and poly-crystalline silicon for silicon cells, and amorphous silicon, gallium arsenide, copper indium gallium selenide and cadmium telluride for thin-film cells. In 2010, approximately 86% of PV cell production used crystalline silicon-based technology. However, due to lower production costs, it is expected that thin-film modules will account for an increasing percentage of PV cell production. Solarbuzz forecasts that the thin-film share will increase from approximately 14% in 2010 to roughly 24% of total PV cell production by 2015 in its "Green World Scenario," which we believe represents the most appropriate of three forecast scenarios published by Solarbuzz because it balances further growth resulting from increased development of governmental incentive programs with measured growth in industry production capacity.

Encapsulants

Regardless of the technology used to create solar energy from a PV system, the core component of the solar cell is the semiconductor circuit. To protect and preserve the embedded semiconductor circuit, solar module manufacturers typically use an encapsulant. Encapsulants are critical to the proper functioning of solar modules, as they protect cells from the elements, bond the multiple layers of a module together, and provide electrical insulation. Encapsulants must incorporate high optical transparency, stability at high temperatures and high levels of ultraviolet radiation, good adhesion to different module materials, adequate mechanical compliance to accommodate stresses induced by differences in thermal expansion coefficients between glass and cells, and good dielectric properties

4

(electrical insulation). Even slight deteriorations of any of these properties of the encapsulant over time could significantly impair the electrical output of the solar module, which is of critical importance in the solar industry where solar module manufacturers typically provide 20-to 25-year warranties for their products.

Over the years, various encapsulant materials have been used in solar modules, including EVA, polyvinyl butyral ("PVB") and poly dimethyl siloxane or silicone. We use EVA to make all of our encapsulant products. EVA is modified with additives to increase stability and make the encapsulant suitable for use in long-term outdoor applications, such as solar modules.

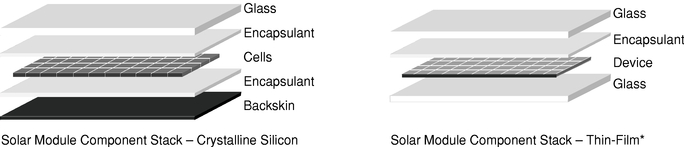

During the solar module assembly process, the encapsulation process is typically accomplished by vacuum lamination, wherein a "pre-lam" stack (as depicted in the diagram below) is fashioned into a singular part comprising multiple layers. Thin sheets of EVA are inserted between the PV cells and typically the top and rear surfaces. Heating the "sandwich" then causes the EVA melt and then to cure, or crosslink, thus bonding the module into one piece. This step occurs towards the end of the manufacturing process and is critical to the entire solar module as there is only one opportunity to laminate correctly.

- *

- Thin-film graphic is not representative of all thin-film modules, which can vary significantly in structure.

Shrinkage or inadequate adhesion can occur during the manufacturing process and may result in voids or holes in the encapsulant, during module lamination, which are considered defects and cause for rejection of the entire panel. Due to direct exposure to the elements, the encapsulant is susceptible to several performance failures that can jeopardize the integrity and performance of the entire solar module and lead to significant warranty costs for solar module manufacturers. The most significant failures include:

- •

- Browning—the propensity of an encapsulant to "brown" after long-term exposure to ultraviolet

("UV") light leading to a permanent loss of transparency. As the encapsulant loses its transparency, the entire solar module loses its ability to convert sunlight into electricity.

- •

- Module delamination—the loss of adhesion between the encapsulant and other module layers. Delamination in the field can occur in cases where the encapsulant was improperly cured or where incompatibilities between the encapsulant and other module components exist. Most of the delamination observed in the field has occurred at the interface between the encapsulant and the front surface of the solar cells in the module. Delamination is more frequent and more severe in hot and humid climates, sometimes occurring after less than five years of exposure. Delamination first causes a performance loss due to optical de-coupling of the encapsulant from the cells. Of greater concern from a module lifetime perspective is the likelihood that the void resulting from the delamination will provide a preferential location for moisture accumulation, greatly increasing the possibility of corrosion failures in metallic contacts.

Despite the critical nature of encapsulant to solar cell applications, the encapsulant represents a small percentage of the overall manufacturing cost of the total solar module.

5

We typically sell our encapsulants in square meters. However, because the solar industry's standard measurement for production volume and capacity is in watts, megawatts ("MW") or gigawatts ("GW"), we convert our capacity and production volume from square meters to approximate MW depending on the applicable conversion efficiencies that are specific to our customers and whether the module is thin-film or crystalline silicon. The conversion ranges from a rate of 10,100 to 15,500 square meters of encapsulant per MW. This rate is based on our calculations using publicly available information, our industry experience and assumptions that our management believes to be appropriate and reasonable. Certain production capacity and market metrics included in this Annual Report on Form 10-K are based on these calculations. Our calculations may not be accurate, and we may change the methodology of our calculations in the future as new information becomes available. In that case, period to period comparisons of such metrics may not be meaningful.

Financial Information About Our Segments and Geographic Areas

Financial information about our segments and geographic areas is included in Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations, and Note 17, Reportable Segments and Geographical Information, of the Notes to Consolidated Financial Statements, included in Item 8, Financial Statements and Supplementary Data, of this Annual Report on Form 10-K.

Our Solar Business

We are a leading global provider of encapsulants to the solar module industry. The encapsulant is a critical component used in solar modules. We were the first to develop the original EVA encapsulants used in commercial solar module manufacturing in the 1970s in conjunction with the Jet Propulsion Laboratory of the California Institute of Technology under a NASA contract for the U.S. Energy Research and Development Administration, which later became known as the U.S. Department of Energy. We have no ongoing relationships with any of these agencies. We have sold our EVA encapsulants commercially since the late 1970s. We have continually improved our encapsulants and we have developed many significant solar encapsulant innovations since we first commercialized our encapsulants, including encapsulants that maintain their dimensional stability and ultra-fast curing formulations. Our encapsulants are used in both of the prevailing solar panel technologies, crystalline silicon and thin-film, and are valued by our customers because they maintain their size and shape throughout the solar module manufacturing process, have fast curing times and have demonstrated long-term stability. These attributes are critical to solar module manufacturers, which typically provide 20- to 25-year warranties of the performance of their solar modules and continually seek to maximize manufacturing yield and optimize efficiency. Despite the critical nature of encapsulant to solar cell applications, the encapsulant represents a small percentage of the overall manufacturing cost of the total solar module.

Our PhotoCap® products consist primarily of EVA, which is modified with additives and put through our proprietary manufacturing process to increase product stability and make the encapsulant suitable for use in extreme, long-term outdoor applications. The inclusion of specific additives results in a limited shelf life before our encapsulants must be integrated into a solar module, making long-term stocking impractical. Encapsulants are generally made-to-order to customer specifications for use in their solar module manufacturing process.

Our Competitive Strengths

We believe that our Solar business possesses a number of key competitive strengths, including:

- •

- Primary Supplier to Leading Module Manufacturers. Since our encapsulants are designed into our customers' manufacturing process, offer long-term stability and substantial manufacturing

6

- •

- Superior Product

Technology. Our encapsulants play a critical role in permanently bonding and protecting sensitive solar module components while helping

to maintain solar module performance for extended periods under extreme environmental conditions. Our products, some of which have been in the field for over 30 years, are designed to provide

superior long-term clarity, which is critical to helping our customers meet their advertised and guaranteed performance levels throughout the solar module life. Our encapsulants are

manufactured to be non-shrinking so that they maintain their size and shape throughout the solar module manufacturing process, thereby reducing manufacturing defects. In addition to

providing dimensional stability, our highly engineered ultra-fast curing encapsulants provide for more rapid and efficient solar module manufacturing, enabling our customers to achieve

higher throughput rates and reduce their production costs. We believe our customers recognize the value of our products because they are able to avoid manufacturing defects on the factory floor and

the warranty costs associated with quality issues in installed panels and our products assist them in achieving high throughput and yield in their manufacturing processes.

- •

- History of

Innovation. We have a long history of innovation. We, in conjunction with the predecessor to the U.S. Department of Energy, utilized our

experience and technical expertise in the field of plastics to invent the original EVA encapsulant formulations used in commercial solar module manufacturing. In addition, we have developed many

significant encapsulant innovations since we first introduced our encapsulants commercially in the late 1970s. Our key innovations include:

- •

- non-shrinking encapsulants that provide superior dimensional stability;

- •

- ultra-fast curing encapsulants;

- •

- lay-flat laminates that increase production efficiency for solar module manufacturers;

- •

- flame-retardant encapsulants; and

- •

- enhanced long-term encapsulant clarity and stability.

- •

- Global Manufacturing and Distribution Base. We have invested heavily in developing our global production and distribution capacity through the acquisition and construction of new plants, by increasing the number of our production lines and by upgrading our manufacturing equipment to meet our customers' needs. We currently have five operational manufacturing plants located in the United States, Spain and Malaysia, with total annual global capacity of approximately 7.5 GW as of December 31, 2010. We believe we are the only encapsulant provider with manufacturing and distribution capabilities in North America, Europe and Asia, which provides

efficiencies, and are a small part of the overall cost of the solar module, we believe our customers will continue to be reluctant to switch to other encapsulant suppliers. We believe we were the primary encapsulant supplier to the majority of our top 10 customers in 2010, which include many of the fastest growing solar module manufacturers worldwide. As our customers look to secure materials or access to our production capacity to support their module production, we have recently entered into, or are in negotiations to enter into, contracts that may include periods of exclusivity and/or minimum purchase requirements. Although such contracts provide for the sale of encapsulants at lower prices than our shorter-term arrangements, they will provide greater predictability of demand. As of December 31, 2010, we had contracts with six of our top ten customers. We supply encapsulants to both crystalline silicon and thin-film solar module manufacturers. We believe we are well positioned to grow with the leading solar module manufacturers in the rapidly expanding solar module industry. We believe that our customers select our encapsulants because of their high quality and superior performance, our ability to meet their delivery requirements and our customer service and technical support.

7

- •

- Technical and Management Expertise. Our senior management team includes seasoned veterans with diverse business experiences who provide a broad range of perspectives and have enabled us to proactively manage our rapid organic growth, including the substantial expansion of our manufacturing operations. Our Vice President and STR Solar's President, Robert S. Yorgensen, has been with us for 25 years. During his tenure, Mr. Yorgensen has played a critical role in the technical development of our encapsulant products and has overseen the development of our major encapsulant innovations. Our senior management team, engineers and plant managers are also critical to the success of our product development efforts and maintaining the high quality of our products and our superior customer service.

us with a significant competitive advantage. Our multiple locations allow us to better meet the delivery requirements of our customers and to reduce shipping costs. In addition, our multiple locations provide us with additional manufacturing space to allow us to increase capacity to meet evolving customer needs, reduce risks relating to any production disruptions at a single facility and provide superior customer service in the local language and in the local time zone.

Our Growth Strategy

Our objective is to enhance our position as a leading global provider of encapsulants to solar module manufacturers. Our strategies to meet that objective are:

- •

- Leverage Global Infrastructure. Our manufacturing facilities are designed to provide the ability to expand our capacity to meet customer demand. To meet anticipated future growth in demand in the solar module market and increase our market share, we plan to continue to increase capacity by adding new production lines at our existing facilities and opening new facilities. In 2010, through the addition of new production lines and engineering and manufacturing process improvements that increased the capacity of our existing production lines by approximately 20%, our total global capacity increased to approximately 7.5 GW as of December 31, 2010. At the end of 2008, we completed the construction of a new manufacturing facility in Malaysia, which had initially been designed for up to 2.0 GW. The Malaysian facility currently has 2.4 GW of production capacity. We have also ordered an additional 1.2 GW of annual production capacity that is expected to become operational in the third quarter of 2011 in Malaysia. In addition, we are in the process of increasing the size of our Malaysia facility by the end of the first quarter of 2011 to provide for total capacity of up to approximately 5.0 GW. We believe that our Malaysian plant has enhanced our competitive position in various Asian markets by allowing us to take advantage of shorter shipping times and lower logistics costs.

In December 2010, we acquired a 275,000 square foot manufacturing facility in East Windsor, Connecticut. This facility will provide us needed space for capacity to meet future demand and enable us to consolidate our Connecticut-based Solar operations. We expect the transition of manufacturing operations to occur during 2011. In addition, we have ordered an additional 1.2 GW of production capacity to be installed in the East Windsor facility during the third quarter of 2011.

We expect our global production capacity to increase to approximately 11.0 GW by the end of 2011. An increase in capacity allows us to produce and sell more encapsulants and should permit us to decrease our manufacturing costs per unit by leveraging our global management, manufacturing and distribution base. It normally takes about one year for one of our production lines to become operational. As such, our 2012 expansion plans will require capital outlays in 2011, which we believe we have sufficient liquidity to fund.

8

- •

- Continue Product Innovation. Throughout the history of our Solar business, we have continued to innovate our encapsulant technologies. We intend to leverage our technical experience and the expertise derived from our greater than 30 years of innovation to continue to develop new products and technologies to meet evolving customer needs and to maintain and enhance our competitive position. For example, we began commercialization during 2010 of our new "Generation 3" fast-cure formulation that can double laminator throughput. We believe this innovative product provides a strong value proposition to our customers by increasing their manufacturing throughput, improving yields and reducing their overall cost of manufacturing. Also during 2010, we hired a Chief Technology Officer to oversee our Solar business's research and development and technical service functions with the intent of accelerating our development of next generation encapsulant technology and creating a pipeline of innovative products.

- •

- Asia Growth Strategy. Our strategy for growing our Asia business is called 1 + China Growth Strategy. Our plant in Malaysia represented the beginning stage of the execution of this strategy utilizing Malaysia as a conduit to Asia. We provide encapsulants to many of the leading solar module manufacturers worldwide and intend to continue to seek new customer relationships. During 2009, global solar demand shifted as module manufacturers located in Asia, particularly in China, obtained market share from European competitors. Also, many Asian governments announced solar incentive programs in 2009 to increase the demand for solar energy in their respective countries, such as the Golden Sun and Building Integrated Photovoltaic Programs in China. Based on these two emerging market patterns that continued in 2010, we are actively seeking to increase our market share in the Asia-Pacific region.

During 2011, we plan to increase our investments in research and development, including the addition of technical personnel and research scientists. Our East Windsor, Connecticut facility will house a 20,000 square foot, state-of-the art research and development laboratory. Overall, we expect our 2011 research and development capital investment to increase by approximately $2.0 million to $3.0 million.

- •

- Further Reduce Manufacturing Costs. We continuously seek to improve our competitive position by reducing our manufacturing costs, and we have identified a number of cost reduction opportunities. For example, we have made modifications to our production process to achieve a 20% increase in throughput with minimal additional capital investment. This improvement will

We are focused on increasing our participation in the Asian market through our Malaysian facility. The strategic location of this plant also serves as an advantageous gateway to other parts of Asia besides China, including South Korea, Japan, India and Taiwan. We have also expanded our local sales team, obtained local market intelligence and seeded the Asian market with our product. Also, many of the Asia module manufacturers have announced expansion plans with the proposed construction of plants in North America. We believe we will also obtain market share with these customers as they penetrate North America due to our strong U.S. manufacturing base.

We have begun product qualification with many of these potential customers, which is a process that can take over a year, and anticipate adding some of them as customers during 2011.

We promoted Bernardo E. Alvarez to the position of Director of Business Development—STR Solar for the People's Republic of China. Mr. Alvarez previously served as General Manager of our Asturias, Spain facility, since its inception in 2002 and was instrumental in its start-up, development and expansion.

We are evaluating the establishment of production capability in China that may include the construction of a plant. If we elect to construct a manufacturing facility, we anticipate that our additional capital outlays in 2011 and 2012 could range from $20 million to $25 million.

9

generate additional fixed cost absorption once that level of capacity is utilized. We are also in the process of developing an encapsulant that eliminates the use of a paper liner, which represents the second largest material-related cost of our encapsulants. During 2010, we experienced significant raw material cost inflation, primarily related to EVA resin which accounts for approximately 50% to 55% of our cost of sales. We expect this inflationary trend to continue. As such, we continually try to identify and qualify additional suppliers to improve our negotiating position and lower our raw material costs. Looking forward, we expect to continue to reduce our cost structure via improved fixed cost absorption associated with the leverage of future sales volume growth, optimize our global manufacturing and distribution footprint to reduce delivery and other logistical costs, reduce scrap rates and improve raw material utilization.

Our Solar Products

We have 12 commercial encapsulant formulations. We develop our formulations internally and work in conjunction with our customers to meet their varying requirements and draw on our considerable accumulated experience. Our encapsulant formulations offer a range of properties and processing attributes, including various curing times and temperatures that align with the requirements of our customers' lamination processes and module constructions. Our formulations can be used in both crystalline silicon and thin-film modules.

Our Solar Markets and Customers

Our customers are solar module manufacturers located in the United States, Europe and Asia. Our largest customers include manufacturers of both crystalline silicon and thin-film modules and include many of the world's largest solar module manufacturers. In 2010, we believe we were the primary supplier of encapsulants to the majority of our top 10 customers. First Solar, Inc. ("First Solar") and Suntech Power Holdings Co. Ltd. ("Suntech"), each of which accounted for more than 10% of our Solar net sales, together accounted for 27.8% of our Solar net sales for the year ended December 31, 2010. Sales to First Solar accounted for 27.1% and 19.1% of our Solar net sales in the years 2009 and 2008, respectively. Our top five customers in our Solar segment accounted for approximately 43.2%, 55.0% and 47.0% of our Solar net sales in 2010, 2009 and 2008, respectively.

We typically sell our encapsulants on a purchase order basis or through one year supply contracts that specify prices and delivery parameters, but can be canceled or postponed prior to production. In the past couple of years, we have been executing on a strategy of entering into formal contractual relationships. These contracts provide for better operational and capital efficiency as well as improved manufacturing visibility, allowing us to better serve the needs of our growing customers. We currently have contracts with six of our largest customers. In addition, we provide technical support to our customers and work with our customers when they are qualifying solar modules that utilize our products, which can take from two months to over a year. Historically, our sales strategy has focused on developing long-term relationships with solar module manufacturers and working with them during their product development efforts. We intend to expand our marketing and sales efforts by increasing the resources in our global sales organization. We also plan to use independent sales consultants in relation to our Asian growth strategy.

Our Solar Operations

Facilities and Equipment

We currently have five operational production facilities that are located in Enfield, Connecticut; Somers, Connecticut; St. Augustine, Florida; Asturias, Spain; and Johor, Malaysia. In December 2010, we acquired a 275,000 square foot manufacturing facility in East Windsor, Connecticut. This facility will

10

provide us needed space for capacity to meet future demand and enable us to consolidate our Connecticut-based Solar operations. We expect the build-out of the facility and transition of manufacturing operations to occur during 2011.

We currently have worldwide total annual production capacity of 7.5 GW. We expect our global production capacity to increase to approximately 11.0 GW by the end of 2011. We convert our capacity and production volume from square meters to MW depending on the applicable conversion efficiencies that are specific to our customers and whether the module is thin-film or crystalline silicon. The conversion ranges from a rate of 10,100 to 15,500 square meters of encapsulant per MW. This rate is based on our calculations using publicly available information, our industry experience and assumptions that our management believes to be appropriate and reasonable.

Our production lines incorporate our proprietary technology and processes. We rely on third-party equipment manufacturers to produce our manufacturing lines to our specifications, which we then further customize in-house. The majority of our production lines are interchangeable by having the capability to produce our 12 EVA formulations and can be used in any of our facilities. As such, this provides us with flexibility in meeting shifting trends in global module demand.

Encapsulant Production Process

Our production process typically begins by mixing EVA pellets with several additives to give the encapsulant its desired properties. The mixture is then melted, homogenized, pressurized and forced through a die to create an "EVA curtain," forming a continuous encapsulant sheet. The sheet then progresses to downstream equipment in a proprietary process, is wound into rolls with paper liner, slit to the desired width and packaged for shipment to customers.

Our manufacturing quality program is ISO 9000 certified. We have a high level of automation at each of our facilities that includes real-time computerized monitoring of the process. Such automation provides consistency across our facilities so that with few exceptions, we can typically manufacture customer orders at any of our locations. In addition, our inventory monitoring system allows us to efficiently plan our production schedule by location.

We test our products in real-time and at a high frequency after production. Each of our manufacturing facilities possesses a quality department that follow our global quality assurance program and has a mandate to discard products that do not meet required standards.

Raw and Other Materials

Resin and paper liner are the two primary materials used in our process, with resin accounting for more than half of our direct manufacturing costs. A number of additives as well as packaging materials represent the remainder of our raw material costs.

We have multiple qualified vendors for resin. We typically carry a 6 week supply of resin to provide protection against supply interruptions resulting from inclement weather, natural disasters and strikes as well as to provide an economic hedge against short-term price inflation. The stock is distributed among our production facilities and warehouses so that a disruptive event in one location would not affect our ability to continue production. We have qualified resin suppliers local to each of our manufacturing facilities and continue to pursue qualification of additional local resin suppliers.

We have multiple qualified suppliers of paper liner. Our primary paper suppliers are located in the United States and Europe, and we purchase paper based on pricing and required lead times. Our main U.S. paper supplier has an Asian distribution network, and we are working to identify local paper suppliers in Asia.

11

Seasonal Trends

Our Solar business could be adversely affected by seasonal trends due to economic incentives, weather patterns and other items. See "Item 1A—Risk Factors."

Our Solar Competition

We compete with a number of encapsulant manufacturers, including Bridgestone Corporation, Solutia Solar GmbH, Hangzhou First PV Material Co., Ltd. and Mitsui Chemicals Group, Inc. We also face limited competition from suppliers of non-EVA encapsulants including Dow Corning Corporation, Dai Nippon Printing Co., Ltd. and E.I. Du Pont De Nemours and Company ("Dupont"). Over the years, various encapsulant materials have been used in solar modules, including PVB and silicone. Some of our competitors are large, global companies with substantial financial, manufacturing and logistics resources and strong customer relationships. Also, low-cost solar module manufacturers are emerging in Asia, primarily in China, which compete with our customers. As the China solar market matures, we expect additional encapsulant providers from China and the greater Asian markets to compete with us. We compete on the basis of several factors, including:

- •

- product performance, including quality and superior technology;

- •

- product innovations in response to customer requirements;

- •

- customer service and technical support;

- •

- delivery timing and logistics;

- •

- production capacity; and

- •

- price.

We believe our relations with the leading solar module manufacturers, the proven performance of our products, our history of innovation, our global manufacturing base, our technical knowledge and management expertise provide us with significant competitive advantages.

Qualification and Certification

Design certification programs for solar modules measure the performance of solar modules under simulated environmental conditions. In certifying their solar modules, our customers must test any solar module with the encapsulant utilized in their product. The certification and qualification tests related to any solar modules are defined in the following standards: IEC 61215 (crystalline silicon), IEC 61646 (thin-film), UL 1703 and IEEE 1262.

A successful qualification test program typically means that the tested models/types of solar modules have been subjected to and passed the minimum requirements of the relevant test standards. Qualification or certification does not guarantee any performance but is designed to provide reasonable assurance that the solar modules of the tested model or type will perform reliably under field conditions.

Under guidelines developed by the IEC/TC82/WG2 committee in 2000, modifications to the encapsulation system for solar modules can require retesting of the solar module. Such guidelines call for various retesting if there is any change in the chemistry of the encapsulant used in the solar module.

Our Quality Assurance Business

We have offered quality assurance services since 1973. Since forming our Quality Assurance business, we have expanded our service offerings and have increased the scale of the business to meet

12

the growing worldwide needs of the consumer products industry. Our Quality Assurance business is a leader in the consumer products quality assurance market, and we believe our Quality Assurance business is the only global testing services provider exclusively focused on the consumer products market. We provide inspection, testing, auditing and consulting services that enable retailers and manufacturers to determine whether products and facilities meet applicable safety, regulatory, quality, performance, social and ethical standards.

Our consumer products Quality Assurance business includes corporate social responsibility auditing, laboratory testing, inspections and associated consultancy services. The primary markets for these services include clients in diverse industries such as electronics, footwear and leather goods, hard goods, textiles, toys and toy premiums, over-the-counter pharmaceuticals, nutritional supplements, food, household chemicals and health and beauty aids. We also provide laboratory and non-laboratory technical services required to bring engineered plastic materials and products to the marketplace. In addition, we work with brand owners and retailers to ensure that their supply chain partners comply with applicable local legal requirements, worker welfare and health and safety standards, as well as corporate codes of conduct.

Because our Quality Assurance business serves a diverse and global client base, we strive to operate where our clients operate. Our Quality Assurance business has an extensive network of 17 laboratories, 80 inspection and audit offices and 22 sales offices in over 40 countries. With an experienced team of over 950 scientists, technicians, engineers, auditors, trainers and inspectors, our Quality Assurance business enables retailers to effectively manage their quality control systems and helps promote the introduction of safe and high-quality products to the marketplace. We sell our quality assurance services through our direct sales force and marketing efforts. We are required to work with a partner in certain countries either because of local laws and regulations or because such arrangements are customary to doing business in such countries. Also, we may enter into strategic alliances with other quality assurance providers in order to meet client demands in countries where it may not be practicable for us to operate on a stand-alone basis.

Growth in the global consumer products testing industry is driven by factors such as increasing globalization of consumer products manufacturing in developing countries, the movement towards shorter product life-cycles and mass customization, as well as increasing regulatory oversight and requirements. The primary clients for consumer product quality assurance services are large North American and European retailers that manage global supply chains of manufacturers, vendors and importers. In particular, retailers, importers and manufacturers that choose to outsource production to developing countries rely on quality assurance services to evaluate product quality and standards.

Quality Assurance Competition

Our consumer product testing and quality assurance services compete with:

- •

- captive services—in-house quality assurance programs maintained and operated by retailers

themselves;

- •

- global competitors—including Bureau Veritas Group, Intertek Group plc and SGS SA, who compete

with us in the majority of our service offerings and industries, all three of which are larger and have greater geographic coverage than us;

- •

- local competitors—smaller, local competition is generally highly specialized and effective in situations in

which a client's needs are limited to the few services that these competitors offer; and

- •

- non-profit competitors—non-profit certification companies and standards-setting institutes that are usually more focused on safety and social issues but are increasingly offering product testing services.

13

The development of a technical reputation, the depth of industry knowledge and internationally recognized accreditations are the primary barriers to entry. The key competitive factors include the level of technical and industry knowledge, pricing, geographic footprint, level of client service, timeliness, accuracy, marketing, breadth of service offering, level of consultation and information usefulness and technical excellence in a given product category.

Quality Assurance Data Management System

Through a host of web-based tools presently in use and in development, we provide real-time vendor monitoring, on-demand report generation, quality trending and defect analysis. These features allow clients to view the performance of particular vendors and place some vendors on reduced inspection programs, which in turn reduces costs. Furthermore, this information provides quality managers with an opportunity to demonstrate the cost of quality and the effectiveness of their program. We plan to enhance these tools to allow clients to place orders, pay invoices and view an even greater amount of information via the Internet.

Quality Assurance Accreditations

Our Quality Assurance business's reputation for quality is demonstrated by our more than 50 internationally recognized accreditations and memberships, which require us to meet and maintain varying standards and requirements. Each quality assurance location is required to maintain a quality management system and is expected to continue to add industry-specific technical proficiency accreditations. Our Quality Assurance business is accredited for social compliance auditing by the Fair Labor Association, Social Accountability International ("SA 8000"), Worldwide Responsible Apparel Production, The International Council of Toy Industries and is a signatory of the United Nations Global Compact and a member of Business For Social Responsibility. In addition, we were the first foreign company to receive the Commodity Inspection and Quarantine ("CIQ") accreditation from the Chinese government, a requirement for all inspection companies conducting operations in China.

We also actively participate in quality assurance industry trade organizations, including the Ethical Trading Initiative, Business Social Compliance Initiative and Initiative Clause Sociale.

14

Key Global Accreditations and Memberships

Accreditations

• Underwriters Laboratories Inc. (UL) (Certified Agent Program (CAP) Engineering and Administrative Agency, Approved Data Acceptance Program (DAP) Agency) |

• American National Standards Institute (ANSI)—ISO/IEC Guide 65 Accredited as a Product Certification Body for SQF Code 2000 Food Safety Certifications |

|

• International Organization for Standardization (ISO) 17025 Accreditation |

• United Kingdom Accreditation Scheme (UKAS) (Accredited Laboratory) |

|

• Cashmere and Camel Hair Manufacturers Institute (CCMI) |

• Worldwide Responsible Accredited Production (WRAP) Accredited Monitor |

|

• Hong Kong Accreditation Service (HKAS) (Accredited Laboratory) |

• United Kingdom Accreditation Service (UKAS) (Notified Body) |

|

• China National Accreditation Service for Conformity Assessment (CNAS) |

• ISO 17025 Accreditation in U.K., Switzerland and Turkey |

|

• ANSI/ASQ National Accreditation Board (ANAB)—ISO/IEC 17021:2006 Accredited as a Management System Certification Body |

• Laboratory Accreditation, Correlation, Evaluation (LACE) Textile Laboratory Accreditation Scheme (Accredited Laboratory) |

|

• Social Accountability Accreditation Service (SAAS)—ISO/IEC 17021:2006 and SAAS Procedure 200 Accredited certification body |

• Responsible Jewellery Council (RJC) Accredited Third Party Conformity Assessment Bodies (CAB) |

|

• International Council of Toy Industries (ICTI): Accredited Audit Company |

• U.S. Consumer Products Safety Commission (CPSC) (Accredited Testing Laboratory) |

|

• Turkish Accreditation Agency (TURKAK) (Accredited Laboratory) |

• Swiss Accreditation Scheme (SAS) (Accredited Laboratory) |

|

• SQF Certification Body License issued by SQF (Safe Quality Food) to provide ANSI ISO/IEC Guide 65 SQF Code 2000 Certifications |

• Taiwan Accreditation Foundation (TAF) |

Memberships

• British Standards Institute (BSI) |

• Occupational Safety & Health Council (OSHC) |

|

• American Association of Textile Chemists and Colorists (AATCC) |

• American Society for Testing And Materials (ASTM) |

|

• Hong Kong Apparel Society Limited (HKAS) |

• Federation of Hong Kong Industries (FHKI) |

|

• The Business and Institutional Furniture Manufacturers Association (BIFMA) International |

• American Apparel & Footwear Association (AAFA) |

Quality Assurance Clients

Our Quality Assurance business has established relationships with many global retailers and manufacturers of consumer products, which we believe is the result of our relationship-based sales approach. We have a broad client base, serving over 5,000 clients in 2010, with our top five clients accounting for approximately 16.1%, 22.1% and 18.0% of our Quality Assurance net sales in the years

15

ended December 31, 2010, 2009 and 2008, respectively. The average length of our relationship with our top 10 clients in 2010 was approximately 12 years.

Employees

As of December 31, 2010, we employed approximately 2,200 people on a full or part-time basis. We maintain a non-unionized workforce, with the exception of some employees in our Solar manufacturing facility in Spain where unions are required and our Quality Assurance facilities in mainland China, where union representation is more typical. We have not experienced any significant work stoppages during the past five years.

Executive Officers

The following table sets forth the names and ages, as of December 31, 2010, of our executive officers. The descriptions below include each such person's service as a board member or an executive officer of STR Holdings, Inc. and our predecessor.

Name

|

Age | Position | |||

|---|---|---|---|---|---|

| Dennis L. Jilot | 63 | Chairman, President and Chief Executive Officer | |||

| Barry A. Morris | 56 | Executive Vice President and Chief Financial Officer | |||

| Robert S. Yorgensen | 47 | Vice President and President, STR Solar | |||

| Alan N. Forman | 50 | Vice President and General Counsel | |||

| Mark A. Duffy | 48 | Former Vice President and President, STR Quality Assurance | |||

Dennis L. Jilot. Dennis L. Jilot has been our President and Chief Executive Officer and a director since 1997 and has been our Chairman since 2002. Prior to joining us, Mr. Jilot was Executive Vice President of Corning Clinical Laboratories, President and Chief Executive Officer of Corning Nichols Institute and President and Chief Operating Officer of MetPath Incorporated. Mr. Jilot holds a B.S. from the University of Wisconsin at Stevens Point and completed the Executive M.B.A. program at the University of Virginia Darden School of Business.

Barry A. Morris. Barry A. Morris joined us as our Vice President and Chief Financial Officer in 2002 and became our Executive Vice President in September 2008. Prior to joining us, Mr. Morris was Chief Financial Officer of General Bearing Corporation as well as Director of Financial Services and Corporate Controller for BTR Inc. He holds a B.S. from American International College and an M.B.A. from the University of Connecticut.

Robert S. Yorgensen. Robert S. Yorgensen became our Vice President in November 2008 and has been the President of STR Solar since 1997. Mr. Yorgensen has been employed by us for 25 years. Mr. Yorgensen has held a variety of positions with us, including Extruded Products Manager and Senior Technical Specialist of Materials RD&E and Specialty Manufacturing, Technical Specialist of Materials RD&E and Specialty Manufacturing and Project Leader of Development Engineering and Specialty Manufacturing. He holds a Bachelor of Technology, Mechanical Engineering from the University of Connecticut and an A.S. from Hartford State Technical College.

Alan N. Forman. Alan N. Forman became our Vice President and General Counsel in May 2010. Mr. Forman is responsible for all legal affairs of the Company. Prior to joining us, Mr. Forman was a partner at Brown Rudnick LLP and a member of their CleanTech team. Mr. Forman brings extensive executive experience in corporate and securities law including intellectual property, licensing agreements, financing transactions, corporate governance and mergers and acquisitions. Mr. Forman holds a B.A. from Emory University in Economics and a J.D. from George Washington Law School.

16

Mark A. Duffy. Mark A. Duffy was our Vice President and President of STR Quality Assurance from August 2009 until December 31, 2010, the effective date of his resignation. Mr. Duffy has 25 years of experience in a wide range of consumer products and food ingredients businesses. Most recently, Mr. Duffy spent seven years as President for Griffith Laboratories USA. Prior to that, he was the Vice President of Sales, North America for the Johnson Wax Professional, a division of SC Johnson. Previously, Mr. Duffy was Director of Sales for Food Service for the Quaker Oats Company, a subsidiary of PepsiCo. He also held several sales and marketing positions of increasing responsibility in the Food Service Division of Nestle USA. He holds a B.S. from Boston College.

Each executive officer holds office for a term of one year and until his or her successor is duly elected and qualified, in accordance with our bylaws. We have initiated an outside search firm to aid in finding our successor for President of STR Quality Assurance. Currently, Mr. Jilot is directly overseeing STR Quality Assurance.

Intellectual Property

Our intellectual property consists of 12 encapsulant formulations, as well as several processes and sub-processes, a service mark on our corporate logo and our trademarks "STR®" and "PhotoCap®." As appropriate, we require employees, suppliers and customers to execute confidentiality agreements.

We own a number of trademarks, service marks, trade secrets and other intellectual property rights that relate to our products and services. We typically rely on trade secrets, rather than patents, to protect our proprietary processes, methods, documentation and other technology, including our encapsulant formulations, as well as certain other business information. Patent protection requires a costly and uncertain federal registration process that would place our confidential information in the public domain. However, we do hold a provisional global patent and we have filed a patent application with respect to one of our solar products in development due to the specific nature of the product. Typically, we utilize trade secrets to protect the formulations and processes we use to manufacture our products, including our encapsulants, and also to safeguard our proprietary formulations and methods. We believe we can effectively protect our trade secrets indefinitely through use of confidentiality agreements and other security measures. While we enter into confidentiality agreements with our employees and third parties to protect our intellectual property rights, such confidentiality provisions related to our trade secrets could be breached and may not provide meaningful protection for our trade secrets. Also, others may independently develop technologies or products that are similar or identical to ours. In such case, our trade secrets would not prevent third parties from competing with us. See "Item 3. Legal Proceedings—Galica /JPS."

Environmental Regulation

We are subject to a variety of environmental, health and safety, pollution-control laws and regulations in the jurisdictions in which we operate. The costs of compliance with these laws and regulations are not material and we do not believe the costs of compliance with these laws and regulations will be material. We use, generate and discharge hazardous substances, chemicals and wastes at some of our facilities in connection with our product development, testing and manufacturing activities. Any failure by us to control the use of, to remediate the presence of or to restrict adequately the discharge of such substances, chemicals or wastes could subject us to potentially significant liabilities, clean-up costs, monetary damages and fines or suspensions in our business operations. In addition, some of our facilities are located on properties with a history of use involving hazardous substances, chemicals and wastes and may be contaminated. For example, during 2010, we performed a Phase II environmental site assessment at our 10 Water Street, Enfield, Connecticut location. During our investigation, the site was found to contain a presence of volatile organic compounds. We have been in contact with the Department of Environmental Protection and we engaged a license contractor to remediate this situation. The estimated cost we expect to pay to remediate the current

17

contamination is approximately $0.1 million. Although we do not currently anticipate any material liabilities in connection with such contamination, we may be required to make expenditures for environmental remediation in the future.

Available Information

Information regarding us, including corporate governance policies, ethics policies and charters for the committees of the board of directors can be found on our internet website at http://www.strholdings.com and copies of these documents are available to stockholders, without charge, upon request to Investor Relations, STR Holdings, Inc., 1699 King Street, Enfield, CT 06082. The information contained in our website is not intended to be incorporated into this Form 10-K. In addition, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are made available free of charge on our internet website on the same day that we electronically file such material with, or furnish it to, the Securities and Exchange Commission (the "SEC"). Information filed with the SEC may be read or copied at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. These filings are also available to the public from commercial document retrieval services and at the internet website maintained by the SEC at http://www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

An investment in our common stock involves a high degree of risk. You should carefully consider the following risks, as well as the other information in this Annual Report on Form 10-K, before making an investment in our Company. If any of the following risks actually occurs, our business, results of operations or financial condition may be adversely affected. In such an event, the trading price of our common stock could decline and you could lose part or all of your investment.

Risks Related to Our Solar Business

Our Solar gross margins and profitability may be adversely affected by rising commodity costs.

We are dependent on certain raw and other materials, particularly resin and paper, for the manufacture of our encapsulants. During 2010, we experienced significant raw material inflation, primarily of EVA resin which comprises approximately 50% to 55% of our cost of encapsulant sales. EVA resin cannot be hedged in the commodity markets. In addition, the cost of equipment used to manufacture our encapsulants is affected by steel prices. The prices for resin, paper and steel have been volatile over the past few years and could increase. If the prices for the commodities and equipment we use in our Solar business increase, our gross margins and results of operations may be adversely affected.

Our dependence on a limited number of third-party suppliers for raw materials for our encapsulants and other significant materials used in our process could prevent us from timely delivering encapsulants to our customers in the required quantities, which could result in order cancellations and decreased revenues.

We purchase resin and paper liner, the two main components used in our manufacturing process, from a limited number of third-party suppliers. If we fail to develop or maintain our relationships with these suppliers or our other suppliers, or if the suppliers' facilities are affected by events beyond our control, we may be unable to manufacture our encapsulants or our encapsulants may be available only for customers in lesser quantities, at a higher cost or after a long delay. We may be unable to pass along any price increases relating to materials costs to our customers, in which case our gross margins

18

could be adversely affected. In addition, we do not maintain long-term supply contracts with our suppliers. Our inventory of raw materials for our encapsulants, including back-up supplies of resin, may not be sufficient in the event of a supply disruption. In 2005, we encountered a supply disruption when one of our resin suppliers had its facilities damaged by a hurricane, and another supplier had a reactor fire at the same time. This forced us to use our back-up supplies of resin. The failure of a supplier to supply materials and components, or a supplier's failure to supply materials that meet our quality, quantity and cost requirements in a timely manner, could impair our ability to manufacture our products to specifications, particularly if we are unable to obtain these materials and components from alternative sources on a timely basis or on commercially reasonable terms. If we are forced to change suppliers, our customers may require us to undertake testing to ensure that our encapsulants meet the customer's specifications.

If demand for solar energy in general and solar modules in particular does not continue to develop or takes longer to develop than we anticipate, sales in our Solar business may not grow or may decline, which would negatively affect our financial condition and results of operations.

We expect that a significant amount of the growth in our overall business will come from the sale of encapsulants by our Solar business. Because our encapsulants are used in the production of solar modules, our financial condition and results of operations and future growth are tied to a significant extent to the overall demand for solar energy and solar modules. The solar energy market is at a relatively early stage of development and the extent to which solar modules will be widely adopted is uncertain. Many factors may affect the viability and widespread adoption of solar energy technology and demand for solar modules, and in turn, our encapsulants, including:

- •

- cost-effectiveness of solar modules compared to conventional and non-solar renewable energy

sources and products;

- •

- performance and reliability of solar modules compared to conventional and non-solar renewable energy sources

and products;

- •

- availability and amount of government subsidies and incentives to support the development and deployment of solar energy

technology;

- •

- rate of adoption of solar energy and other renewable energy generation technologies, such as wind, geothermal and biomass;

- •

- seasonal fluctuations related to economic incentives and weather patterns;

- •

- fluctuations in economic and market conditions that affect the viability of conventional and non-solar

renewable energy sources, such as increases or decreases in the prices of fossil fuels and corn or other biomass materials;

- •

- changes in global economic conditions including increases in interest rates and the availability of financing and

investment capital that is required to fund solar projects. Any volatility or disruption in the economic environment or the credit markets similar to what was experienced during 2009 may slow the

growth of the solar industry, may cause our customers to experience a reduction in demand for their products and related financial difficulties and may adversely impact our Solar business;

- •

- fluctuations in capital expenditures by end users of solar modules, which tend to decrease when the overall economy slows

down;

- •

- the extent to which the electric power and broader energy industries are deregulated to permit broader adoption of solar electricity generation; and

19

- •

- the cost and availability of polysilicon and other key raw materials for the production of solar modules.

For example, in 2009, we experienced a decline in our Solar business mainly due to decreased global demand for solar energy as a result of legislative changes, such as the cap in feed-in tariffs in Spain implemented in 2008, the global recession and the worldwide credit crisis.

If demand for solar energy and solar modules fails to develop sufficiently, demand for our customers' products as well as demand for our encapsulants will decrease, and we may not be able to grow our business or Solar net sales and our financial condition and results of operations will be harmed.

A significant reduction or elimination of government subsidies and economic incentives or a change in government policies that promote the use of solar energy could have a material adverse effect on our business and prospects.

Demand for our encapsulants depends on the continued adoption of solar energy and the resultant demand for solar modules. Demand for our products depends, in large part, on government incentives aimed to promote greater use of solar energy. In many countries in which solar modules are sold, solar energy would not be commercially viable without government incentives. This is because the cost of generating electricity from solar energy currently exceeds, and we believe will continue to exceed for the foreseeable future, the costs of generating electricity from conventional energy sources.

The scope of government incentives for solar energy depends, to a large extent, on political and policy developments relating to environmental and energy concerns in a given country that are subject to change, which could lead to a significant reduction in, or a discontinuation of, the support for renewable energy in such country. Federal, state and local governmental bodies in many of the target markets for our Solar business, including Germany, Italy, Spain, the United States, France, Japan and South Korea, have provided subsidies and economic incentives in the form of feed-in tariffs, rebates, tax credits and other incentives to end users, distributors, system integrators and manufacturers of solar energy products to promote the use of solar energy and to reduce dependency on other forms of energy. These government economic incentives could be reduced or eliminated earlier than anticipated. For example, in Germany, which is currently the largest solar PV end-user market, the government enacted legislation that reduced feed-in tariffs beginning June 30, 2010. In early 2011, the German government enacted further legislation to accelerate the annual year-end feed-in-tariff reduction to July 1, 2011 for roof-top systems and September 1, 2011 for ground-mount projects. As such, this announcement may result in the pull-in of demand from solar module manufacturers due to increased end-user demand being driven by the incentive to purchase a solar system prior to the enactment of the decreased feed-in tariff incentives. As such, we may see atypical Solar sales during the first half of 2011 that might not occur during the second half of 2011. If solar module demand in Germany continues to grow at a rate that the German government believes is excessive, it may consider capping the amount of PV installations that may qualify for the feed-in-tariff incentives. Also, in September 2008, the Spanish parliament adopted new legislation that decreased the feed-in tariff for solar energy by approximately 27% and capped its subsidized PV installations at 500 MW for 2009. This event drove an over-supply of solar module inventory in the supply chain during the first half of 2009 and was one of the main drivers behind our sales volume decline in 2009 compared to 2008.

More recently, Italy has emerged as a significant solar market. The same risks identified for the German market now exist for the Italian market. Also, many European governments are currently experiencing sovereign debt issues. As such, a risk exists that some of these governments may reduce current subsidies provided for PV installations in conjunction with overall lower fiscal policy spending.

Moreover, electric utility companies, or generators of electricity from fossil fuels or other renewable energy sources, could also lobby for changes in the relevant legislation in their markets to protect their revenue streams. Reduced growth in or the reduction, elimination or expiration of government subsidies and economic incentives for solar energy, especially those in our target markets, could cause our Solar net sales to decline and harm our business.

20

Our Solar business is dependent on a limited number of customers, which may cause significant fluctuations or result in declines in our Solar net sales.

The solar module industry is relatively concentrated, and we expect this concentration to increase. As a result, we sell substantially all of our encapsulants to a limited number of solar module manufacturers. We expect that our results of operations will, for the foreseeable future, continue to depend on the sale of encapsulants to a relatively small number of customers. Sales to First Solar and Suntech, each of which accounted for more than 10% of our Solar net sales, together accounted for 27.8% of our Solar net sales for the year ended December 31, 2010. Sales to First Solar accounted for 27.1% and 19.1% of our Solar net sales in the years 2009 and 2008, respectively. In addition, the top five customers in our Solar segment accounted for approximately 43.2%, 55.0% and 47.0% of our Solar net sales in 2010, 2009 and 2008, respectively. Furthermore, participants in the solar industry, including our customers, are experiencing pressure to reduce their costs. Because we are part of the overall supply chain to our customers, any cost pressures experienced by them may affect our business and results of operations. Our customers may not continue to generate significant Solar net sales for us. Conversely, we may be unable to meet the production demands of our customers or maintain these customer relationships. Also, new entrants into the solar module manufacturing industry, primarily from China, could negatively impact the demand for, and pricing of, our customers' products, which could reduce the demand for our encapsulants. Over the last couple of years, we believe our European customers have lost market share to low-cost module manufacturers, primarily from China, that continue to penetrate the European solar market. If we are not able to supply encapsulants to these new entrants in the future, we could lose market share and also face competition from new encapsulant manufacturers.

In addition, a significant portion of our outstanding accounts receivable is derived from sales to a limited number of customers. The accounts receivable from our top five Solar customers with the largest receivable balances represented 33.8% and 38.7% of our accounts receivable balance as of December 31, 2010 and December 31, 2009, respectively. Moreover, many solar companies are facing and may continue to face significant liquidity and capital expenditure requirements, and as a result, our customers may have trouble making payments owed to us, which could affect our business, financial condition and results of operations. Any one of the following events may cause material fluctuations or declines in our Solar net sales and have a material adverse effect on our business, financial condition and results of operations:

- •

- reduction, postponement or cancellation of orders from one or more of our significant customers;

- •

- reduction in the price one or more significant solar customers are willing to pay for our encapsulants;

- •

- selection by one or more solar customers of products competitive with our encapsulants;

- •

- loss of one or more significant solar customers and failure to obtain additional or replacement customers; and

- •

- failure of any of our significant solar customers to make timely payment for products.

Our Solar business's growth is dependent upon the growth of our key Solar customers and our ability to keep pace with our customers' growth.

In addition to relying on a small number of customers, we believe we were the primary supplier to the majority of our top 10 Solar customers in 2010. The future growth and success in our Solar business depends on the ability of such customers to grow their businesses and our ability to meet any such growth, principally through the addition of manufacturing capacity. If our Solar customers do not increase production of solar modules, there will be no corresponding increase in encapsulant orders. Alternatively, in the event such customers grow their businesses, we may not be able to meet their increased demands, which would require such customers to find alternative sources for encapsulants. In

21

addition, it is possible that customers for whom we are the exclusive supplier of encapsulants will seek to qualify and establish a secondary supplier of encapsulants, which would reduce our share with such customers and could increase that customer's pricing leverage. If our Solar customers do not grow their businesses or they find alternative sources for encapsulants to meet their demands, it could limit our ability to grow our business and increase our Solar net sales.

Technological changes in the solar energy industry or our failure to develop and introduce or integrate new technologies could render our encapsulants uncompetitive or obsolete, which would adversely affect our business.

The solar energy market is very competitive, rapidly evolving and is characterized by continually changing technology requiring continuous improvements in solar modules to increase efficiency and power output and improve aesthetics. This requires us and our customers to continuously invest significant financial resources to develop new solar module technology and enhance existing solar modules to keep pace with evolving industry standards and changing customer requirements and to compete effectively in the future. Our failure to further refine our encapsulant technology and develop and introduce new or enhanced encapsulants or other products, or our competitors' development of products and technologies that perform better or are more cost effective than our products, could cause our encapsulants to become uncompetitive or obsolete, which would adversely affect our business, financial condition and results of operations. Product development activities are inherently uncertain, and we could encounter difficulties and increased costs in commercializing new technologies. As a result, our product development expenditures in our Solar business may not produce corresponding benefits.