Attached files

| file | filename |

|---|---|

| EX-3.02 - EXHIBIT 3.02 - Bank of Marin Bancorp | ex3_02.htm |

| EX-32.01 - EXHIBIT 32.01 - Bank of Marin Bancorp | ex32_01.htm |

| EX-31.01 - EXHIBIT 31.01 - Bank of Marin Bancorp | ex31_01.htm |

| EX-31.02 - EXHIBIT 31.02 - Bank of Marin Bancorp | ex31_02.htm |

| EX-23.01 - EXHIBIT 23.01 - Bank of Marin Bancorp | ex23_01.htm |

BANK OF MARIN BANCORP

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

T

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended: December 31, 2010

or

|

£

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from __________________ to __________________

Commission File number: 001-33572

Bank of Marin Bancorp

(Exact name of Registrant as specified in its charter)

|

California

|

20-8859754

|

|

(State or other jurisdiction of incorporation)

|

(IRS Employer Identification No.)

|

|

504 Redwood Blvd., Suite 100, Novato, CA

|

94947

|

|

(Address of principal executive office)

|

(Zip Code)

|

(415) 763-4520

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12 (b) of the Act:

None

Securities registered pursuant to section 12(g) of the Act:

|

Common Stock, No Par Value,

and attached Share Purchase Rights

|

NASDAQ Capital Market

|

|

(Title of each class)

|

(Name of each exchange on which registered)

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

Yes £

|

No T

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

|

Yes £

|

No T

|

Note – checking the box above will not relieve any registrant required to file reports pursuant to section 13 or 15(d) of the Exchange Act from their obligations under these sections.

Indicate by check mark whether the registrant (1) has filed all reports to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

Yes T

|

No £

|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

|

Yes £

|

No £

|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check One):

|

Large accelerated filer £

|

Accelerated filer T

|

|

Non-accelerated filer £

|

Smaller reporting company £

|

Indicate by check mark if the registrant is a shell company, as defined in Rule 12b(2) of the Exchange Act.

Yes £ No T

As of June 30, 2010, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting and non-voting common equity held by non-affiliates, based upon the closing price per share of the registrant’s common stock as reported by the NASDAQ, was approximately $163 million. For the purpose of this response, directors and officers of the Registrant are considered the affiliates at that date.

As of February 28, 2011 there were 5,300,685 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for the Annual Meeting of Shareholders to be held on May 17, 2011 are incorporated by reference into Part III.

Page - 2

BANK OF MARIN BANCORP

TABLE OF CONTENTS

|

5

|

||

|

5

|

||

|

5

|

||

|

12

|

||

|

20

|

||

|

20

|

||

|

20

|

||

|

20

|

||

|

21

|

||

|

21

|

||

|

23

|

||

|

24

|

||

|

24

|

||

|

24

|

||

|

25

|

||

|

28

|

||

|

29

|

||

|

33

|

||

|

33

|

||

|

34

|

||

|

36

|

||

|

37

|

||

|

37

|

||

|

38

|

||

|

41

|

||

|

44

|

||

|

44

|

||

|

45

|

||

|

45

|

||

|

45

|

||

|

46

|

||

|

46

|

||

|

46

|

||

|

ITEM 7A.

|

48

|

|

|

ITEM 8.

|

50

|

|

|

56

|

||

|

56

|

||

|

62

|

||

|

65

|

||

|

69

|

||

|

71

|

||

|

71

|

||

|

71

|

||

|

72

|

||

|

73

|

||

|

77

|

||

|

80

|

||

|

80

|

||

|

82

|

||

|

82

|

||

|

83

|

||

|

84

|

||

|

85

|

||

|

86

|

||

|

87

|

||

|

89

|

||

|

90

|

||

|

90

|

||

|

91

|

||

|

91

|

||

|

91

|

||

|

91

|

||

|

91

|

||

|

91

|

||

|

91

|

||

|

92

|

||

|

94

|

||

|

96

|

||

Forward-Looking Statements

This discussion of financial results includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, (the "1933 Act") and Section 21E of the Securities Exchange Act of 1934, as amended, (the "1934 Act"). Those sections of the 1933 Act and 1934 Act provide a "safe harbor" for forward-looking statements to encourage companies to provide prospective information about their financial performance so long as they provide meaningful, cautionary statements identifying important factors that could cause actual results to differ significantly from projected results.

Our forward-looking statements may include descriptions of plans or objectives of Management for future operations, products or services, and forecasts of our revenues, earnings or other measures of economic performance. Forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. They often include the words "believe," "expect," "intend," "estimate" or words of similar meaning, or future or conditional verbs such as "will," "would," "should," "could" or "may."

Forward-looking statements are based on Management's current expectations regarding economic, legislative, and regulatory issues that may impact our earnings in future periods. A number of factors - many of which are beyond Management’s control - could cause future results to vary materially from current Management’s expectations. Such factors include, but are not limited to, general economic conditions, the current financial turmoil in the United States and abroad, changes in interest rates, deposit flows, real estate values and competition; changes in accounting principles, policies or guidelines; changes in legislation or regulation; and other economic, competitive, governmental, regulatory and technological factors affecting our operations, pricing, products and services. These and other important factors are detailed in Item 1A Risk Factors section of this report. Forward-looking statements speak only as of the date they are made. We do not undertake to update forward-looking statements to reflect circumstances or events that occur after the date the forward-looking statements are made or to reflect the occurrence of unanticipated events.

|

ITEM 1.

|

BUSINESS

|

Bank of Marin (the “Bank”) was incorporated in August 1989, received its charter from the California Superintendent of Banks (now the California Department of Financial Institutions or “DFI”) and commenced operations in January 1990. The Bank is an insured bank under the Federal Deposit Insurance Act (“FDIC”). On July 1, 2007 (the “Effective Date”), a bank holding company reorganization was completed whereby Bank of Marin Bancorp (“Bancorp”) became the parent holding company for the Bank, the sole and wholly-owned subsidiary of Bancorp. On the Effective Date, each outstanding share of Bank of Marin common stock was converted into one share of Bank of Marin Bancorp common stock. Bancorp assumed the ticker symbol BMRC, which was formerly used by the Bank. Prior to the Effective Date, the Bank filed reports and proxy statements with the FDIC pursuant to Sections 12 of the Securities Exchange Act of 1934 (the “1934 Act”). Upon formation of the holding company, Bancorp became subject to regulation under the Bank Holding Company Act of 1956, as amended, which subjects Bancorp to Federal Reserve Board reporting and examination requirements.

References in this report to “Bancorp” mean Bank of Marin Bancorp, parent holding company for the Bank. References to “we,” “our,” “us” mean the holding company and the Bank that are consolidated for financial reporting purposes.

Virtually all of our business is conducted through Bancorp’s sole subsidiary, the Bank, which is headquartered in Novato, California. As of December 31, 2010, we operated through sixteen offices in San Francisco, Marin and Sonoma counties with a strong focus on supporting the local community. As discussed in Note 19 to the Consolidated Financial Statements in Item 8 of this report, in February 2011, we expanded our community banking footprint to Napa County through an FDIC-assisted acquisition of certain assets and assumption of certain liabilities of the former Charter Oak Bank. Our customer base is made up of business and personal banking relationships from the communities near the branch office locations. Our business banking focus is on small to medium-sized businesses, professionals and not-for-profit organizations.

We offer a broad range of commercial and retail deposit and lending programs designed to meet the needs of our target markets. Our loan products include commercial loans and lines of credit, construction financing, consumer loans, and home equity lines of credit. Merchant card services are available for our customers in retail businesses. Through a third party vendor, we offer a proprietary Visa® credit card product combined with a rewards program to our customers, as well as a Business Visa® program for business and professional customers. We also offer cash management sweep to business clients through a third party vendor.

We offer a variety of personal and business checking and savings accounts, and a number of time deposit alternatives, including time certificates of deposit, Individual Retirement Accounts (“IRAs”), Health Savings Accounts, and Certificate of Deposit Account Registry Service (“CDARS®”). CDARS® is a network through which we offer full FDIC insurance coverage in excess of the regulatory maximum by placing deposits in multiple banks participating in the network. We also offer remote deposit capture, direct deposit of payroll, social security and pension checks, fraud prevention services including an insurance protected Identity Theft Prevention Program and image lockbox services. A valet deposit pick-up service is available to our professional and business clients. Automatic teller machines (“ATM's”) are available at each branch location.

Our ATM network is linked to the PLUS and NYCE networks. In January 2009, we began offering free access to a network of nation-wide surcharge-free ATM’s called MoneyPass. We also offer our depositors 24-hour access to their accounts by telephone and through our internet banking products available to personal and business account holders.

We offer Wealth Management and Trust Services (“WMTS”) which include customized investment portfolio management, financial planning, trust administration, estate settlement and custody services, and advice of charitable giving. We also offer 401(k) plan services to small and medium businesses through a third party vendor.

We offer branch-based Private Banking as a natural extension of our services. Our Private Banking includes deposit services and loans, as well as a full range of banking services.

We do not directly offer international banking services, but do make such services available to our customers through other financial institutions with whom we have correspondent banking relationships.

We hold no patents, licenses (other than licenses required by the appropriate banking regulatory agencies), franchises or concessions. The Bank has registered the service marks "The Spirit of Marin", the words “Bank of Marin”, the Bank of Marin logo, and the Bank of Marin tagline “Committed to your business and our community” with the United States Patent & Trademark Office. In addition, Bancorp has registered the service marks for the words “Bank of Marin Bancorp” and for the Bank of Marin Bancorp logo with the United States Patent & Trademark Office.

All service marks registered by Bancorp or the Bank are registered on the United States Patent & Trademark Office Principal Register, with the exception of the words "Bank of Marin Bancorp" which is registered on the United States Patent & Trademark Office Supplemental Register.

Market Area

Our primary market area reaches from Sonoma County to San Francisco and lies between the Pacific Ocean on the west and San Francisco Bay to the east. See also Note 19 to the Consolidated Financial Statements in Item 8 of this report regarding our subsequent expansion into Napa County in February 2011. Our customer base is made up of business and personal banking relationships from the communities near the branch office locations.

We attract deposit relationships from individuals, merchants, small to medium-sized businesses, not-for-profit organizations and professionals who live and/or work in the communities comprising our market areas. As of December 31, 2010, approximately 82% of our deposits are in Marin and southern Sonoma counties, and approximately 56% of our deposits are from businesses and 44% are from individuals.

Competition

The banking business in California generally, and in our market area specifically, is highly competitive with respect to attracting both loan and deposit relationships. The increasingly competitive environment is impacted by changes in regulation, interest rate environment, technology and product delivery systems, and the consolidation among financial service providers. The banking industry is seeing extreme competition for quality loans. Larger banks are seeking to expand lending to small businesses, which are traditionally community bank customers. The Marin County market area is dominated by two major nation-wide banks, each of which has more branch offices than us in the defined service area. Additionally, there are several thrifts, credit unions and other independent banks.

As of June 30, 2010, the latest data available shows 89 banking offices with $8.8 billion in total deposits served the Marin County market. As of that same date, there were approximately 3 thrift offices in Marin with $0.6 billion in total deposits. We have the largest business core deposit market share, representing 24.3% of business core deposits in Marin County1. A significant driver of our franchise value is the growth and stability of our checking and savings deposits, which are a low cost funding source for our loan portfolio. We have also gained overall deposit market share in our primary market area in 20101. The four financial institutions with the greatest deposit market share in Marin County are Wells Fargo Bank, Bank of America, Bank of Marin, and Westamerica Bank with deposit market shares of 26.0% and 17.9%, 9.9%, and 8.6%, respectively1.

In the southern Sonoma County area of Petaluma, there are approximately 25 banking and thrift offices with $1.5 billion in total deposits as of June 30, 2010. Compared with our share of 4.5%, the four banking institutions with the greatest overall market share, Wells Fargo Bank, Bank of America, Bank of the West, and First Community Bank had deposit market shares in Petaluma of 28.7%, 15.6%, 9.3%, and 8.9%, respectively1.

We also compete for depositors' funds with money market mutual funds and with non-bank financial institutions such as brokerage firms and insurance companies. Among the competitive advantages held by some of these non-bank financial institutions are their ability to finance extensive advertising campaigns, and to allocate investment assets to regions of California or other states with areas of highest demand and, therefore, often higher yield.

Nationwide banks have the competitive advantages of national advertising campaigns and technology infrastructure to achieve economies of scale. Large commercial banks also have substantially greater lending limits and have the ability to offer certain services which are not offered directly by us.

In order to compete with the numerous, and often larger, financial institutions in our primary market area, we use, to the fullest extent possible, the flexibility and rapid response capabilities which are accorded by our independent status. Our competitive advantages also include an emphasis on personalized services, community involvement, philanthropic giving, local promotional activities and personal contacts. The commitment and dedication of our organizers, directors, officers and staff have also contributed greatly to our success in competing for business.

Employees

At December 31, 2010, we employed 203 full-time equivalent (“FTE”) staff. The actual number of employees, including part-time employees, at year-end 2010 included 4 executive officers, 77 other corporate officers and 142 staff. None of our employees are presently represented by a union or covered by a collective bargaining agreement. We believe that our employee relations are good. We have been recognized as one of the “Best Places to Work in the San Francisco Bay Area” by the San Francisco Business Times and the “Best Places to Work” by North Bay Business Journal.

SUPERVISION AND REGULATION

Bank holding companies and banks are extensively regulated under both federal and state law. The following discussion summarizes certain significant laws, rules and regulations affecting Bancorp and the Bank.

Bank Holding Company Regulation

Upon formation of the bank holding company on July 1, 2007, we became subject to regulation under the Bank Holding Company Act of 1956, as amended (“BHCA”) which subjects Bancorp to Federal Reserve Board reporting and examination requirements. Under the Federal Reserve Board’s regulations, a bank holding company is required to serve as a source of financial and managerial strength to its subsidiary banks.

_______________________________

1 Based on the latest available FDIC deposit market share data as of June 30, 2010.

The BHCA regulates the activities of holding companies including acquisitions, mergers and consolidations and, together with the Gramm-Leach Bliley Act of 1999, the scope of allowable banking activities.

Bank Regulation

Banking regulations are primarily intended to protect depositors’ funds, federal deposit insurance funds and the banking system as a whole. These regulations affect our lending practices, consumer protections, capital structure, investment practices and dividend policy.

As a state chartered bank, we are subject to regulation and examination by the DFI. We are also subject to regulation, supervision and periodic examination by the FDIC. If, as a result of an examination of the Bank, the FDIC or the DFI should determine that the financial condition, capital resources, asset quality, earnings prospects, management, liquidity, or other aspects of our operations are unsatisfactory, or that we have violated any law or regulation, various remedies are available to those regulators including issuing a “cease and desist” order, restricting our growth or removing officers and directors.

Dividends

The payment of cash dividends by the Bank to Bancorp is subject to restrictions set forth in the California Financial Code (the “Code”). Prior to any distribution from the Bank to Bancorp, a calculation is made to ensure compliance with the provisions of the Code and to ensure that the Bank remains within capital guidelines set forth by the DFI and the FDIC. As the Bank made a $28 million distribution to Bancorp in March 2009 in connection with Bancorp’s repurchase of preferred stock discussed in Note 9 to the Consolidated Financial Statements in Item 8 of this report, distributions from the Bank to Bancorp are subject to advance regulatory approval from the DFI for three years beginning in 2010. Management anticipates that there will be sufficient earnings at the Bank level to provide dividends to Bancorp to meet its funding requirements for the foreseeable future. See also Note 9 to the Consolidated Financial Statements, under the heading “Dividends” in Item 8 of this report.

FDIC Insurance Assessments

Our deposits are insured by the FDIC to the maximum amount permitted by law, which is currently $250,000 per depositor. The 2010 enacted Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) made the deposit insurance coverage permanent at the $250,000 level retroactive to January 1, 2008. The Dodd-Frank act also provides depositors at all FDIC-insured institutions with unlimited deposit insurance coverage on traditional checking accounts that do not pay interest and Interest on Lawyers Trust Accounts beginning December 31, 2010 through the end of 2012.

During 2009 and 2010, we elected to participate in the Temporary Transaction Account Guarantee Program, which provided full deposit insurance coverage to non-interest bearing transaction accounts (including low-interest negotiable order of withdrawal accounts and interest on lawyer trust accounts), by paying a 10 basis point surcharge on the non-interest bearing transaction accounts over $250,000 through December 31, 2009, and a 15 basis point surcharge through December 31, 2010, when the program ended.

Effective April 1, 2009, the FDIC revised its risk-based insurance assessment system, effectively increasing the overall assessment rate. The revised base assessment rates for banks in the best risk category range from twelve to sixteen cents annually for every $100 of domestic deposits held. In addition, the FDIC also imposed a one-time special Deposit Insurance assessment of five basis points on all insured institutions’ total assets minus Tier 1 capital at June 30, 2009 in order to replenish the Deposit Insurance Fund. On November 12, 2009, the FDIC finalized a Deposit Insurance Fund restoration plan that required banks to prepay, on December 30, 2009, their estimated quarterly risk-based assessments for the fourth quarter of 2009 and for all of 2010, 2011 and 2012. Under the plan, banks were assessed through 2010 according to the risk-based premium schedule adopted in April 2009.

On February 7, 2010, as required by the Dodd-Frank Act, the FDIC approved a rule that changes the FDIC insurance assessment base from adjusted domestic deposits to a bank’s average consolidated total assets minus average tangible equity, defined as Tier 1 capital. Since the new base is larger than the current base, the new rule lowers assessment rates to between 2.5 and 9 basis points on the broader base for banks in the lowest risk category, and 30 to 45 basis points for banks in the highest risk category. The change will be effective beginning with the second quarter of 2011 and payable at the end of September 2011. The new rule is expected to lower our FDIC insurance by more than 30%. Since we have a solid core deposit base and do not rely heavily on borrowings and brokered deposits, the benefit of the lower assessment rate (which is expected to drop by half for us) will significantly outweigh the effect of a wider assessment base.

The following discussion summarizes certain significant laws, rules and regulations affecting both Bancorp and the Bank

Community Reinvestment Act

We are subject to the provisions of the Community Reinvestment Act (“CRA”), under which all banks and thrifts have a continuing and affirmative obligation, consistent with safe and sound operations, to help meet the credit needs of their entire communities, including low and moderate income neighborhoods. The act requires a depository institution’s primary federal regulator, in connection with its examination of the institution, to assess the institution’s record in meeting the requirements in CRA. The regulatory agency’s assessment of the institution’s record is made available to the public. The record is taken into consideration when the institution establishes a new branch that accepts deposits, relocates an office, applies to merge or consolidate, or expands into other activities. CRA performance is evaluated by the FDIC under the intermediate small bank requirements. The FDIC’s last CRA and consumer compliance examination performed on us was completed on May 7, 2009 with a rating of “Satisfactory,” which is the highest rating possible.

Anti Money–Laundering Regulations

A series of banking laws and regulations beginning with the Bank Secrecy Act in 1970 require banks to prevent, detect, and report illicit or illegal financial activities to the federal government to prevent money laundering, international drug trafficking, and terrorism. Under the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001, financial institutions are subject to prohibitions against specified financial transactions and account relationships as well as enhanced due diligence and “know your customer” standards in their dealings with high risk customers, foreign financial institutions, and foreign individuals and entities. We have extensive controls in place to comply with these requirements.

Privacy and Data Security

The Gramm-Leach Bliley Act (“GLBA”) of 1999 imposes requirements on financial institutions with respect to consumer privacy. The GLBA generally prohibits disclosure of consumer information to non-affiliated third parties unless the consumer has been given the opportunity to object and has not objected to such disclosure. Financial institutions are further required to disclose their privacy policies to consumers annually. The GLBA also directs federal regulators, including the FDIC, to prescribe standards for the security of consumer information. We are subject to such standards, as well as standards for notifying consumers in the event of a security breach. We must disclose our privacy policy to consumers and permit consumers to “opt out” of having non-public customer information disclosed to third parties. We are required to have an information security program to safeguard the confidentiality and security of customer information and to ensure proper disposal of information that is no longer needed. Customers must be notified when unauthorized disclosure involves sensitive customer information that may be misused.

Consumer Protection Regulations

Our lending activities are subject to a variety of statutes and regulations designed to protect consumers, including the Fair Credit Reporting Act, Equal Credit Opportunity Act, the Fair Housing Act, and the Truth-in-Lending Act. Our deposit operations are also subject to laws and regulations that protect consumer rights including Funds Availability, Truth in Savings, and Electronic Funds Transfers. Additional rules govern check writing ability on certain interest earning accounts and prescribe procedures for complying with administrative subpoenas of financial records. Additionally, the provision of the Federal Reserve Regulation E has been changed effective July 1, 2010. It puts restrictions on institutions assessing overdraft fees on consumer’s accounts relating to electronic funds transfers. As a result, our overdraft fee income has been negatively impacted.

Restriction on Transactions between Member Banks and their Affiliates

Transactions between Bancorp and the Bank are quantitatively and qualitatively restricted under Sections 23A and 23B of the Federal Reserve Act and Federal Reserve Regulation W. Section 23A places restrictions on the Bank’s “covered transactions” with Bancorp, including loans and other extensions of credit, investments in the securities of, and purchases of assets from Bancorp. Section 23B requires that certain transactions, including all covered transactions, be on market terms and conditions. Federal Reserve Regulation W combines statutory restrictions on transactions between the Bank and Bancorp with Board interpretations in an effort to simplify compliance with Sections 23A and 23B.

Capital Requirements

The Federal Reserve and the FDIC have adopted risk-based capital guidelines for bank holding companies and banks. Bancorp’s ratios exceed the required minimum ratios for capital adequacy purposes and the Bank meets the definition for well capitalized. Undercapitalized depository institutions may be subject to significant restrictions. Payment of interest and principal on subordinated debt of the Bank could be restricted or prohibited, with some exceptions, if the Bank were categorized as "critically undercapitalized" under applicable FDIC regulations. For further information on risk-based capital, see Note 16 to the Consolidated Financial Statements in Item 8 of this Form 10-K.

Sarbanes-Oxley Act of 2002

We are subject to the requirements of the Sarbanes-Oxley Act of 2002 which implemented legislative reforms intended to address corporate and accounting improprieties.

Emergency Economic Stabilization Act of 2009 (the “EESA”)

In response to the financial crisis affecting the banking system and financial markets and going concern threats of investment banks and other financial institutions, on October 3, 2008, the EESA was signed into law, which gave the U.S. Treasury the authority to, among other things, inject $700 billion capital into the market to stabilize the financial industry. Pursuant to the EESA, the U.S. Treasury also purchased senior preferred shares from the largest nine financial institutions in the nation and the other financial institutions in a program known as the Treasury Capital Purchase Program (“TCPP”) that was carved out of the Troubled Asset Relief Program (“TARP”). As a result of our participation in the TCPP, we were subject to restrictions on executive compensation and limitations on dividends and stock repurchases from December 5, 2008 to March 31, 2009, the period that the preferred stock issued to the U.S. Treasury was outstanding.

The American Recovery and Reinvestment Act of 2009 (the “Recovery Act”)

The Recovery Act was signed into law on February 17, 2009 in an effort, among other things, to jumpstart the U.S. economy, prevent job losses, expand educational opportunities, and provide affordable health care and tax relief. Among the various measures in the Recovery Act, it imposes further restriction on executive compensation and corporate expenditure limits of recipients of the TCPP funds, while allowing them to repurchase the preferred stock at liquidation amount without regard to the original TCPP transaction terms. See Note 9 to the Consolidated Financial Statements in Item 8 of this report for discussion regarding our repurchase of preferred stock issued under the TCPP.

The Dodd-Frank Wall Street Reform and Consumer Protection Act

On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act, a landmark financial reform bill comprised of massive volume of new rules and restrictions that will impact banks going forward. It includes key provisions aimed at preventing a repeat of the 2008 financial crisis and a new process for winding down failing, systemically important institutions in a manner as close to a controlled bankruptcy as possible. The Act includes other key provisions as follows:

(1) The Act establishes a new Financial Stability Oversight Council to monitor systemic financial risks. The Board of Governors of the Federal Reserve (“Fed”) are given extensive new authorities to impose strict controls on large bank holding companies with total consolidated assets equal to or in excess of $50 billion and systemically significant nonbank financial companies to limit the risk they might pose for the economy and to other large interconnected companies. The Fed can also take direct control of troubled financial companies that are considered systemically significant.

The Act restricts the amount of trust preferred securities (“TPS”) that may be considered as Tier 1 Capital. For bank holding companies below $15 billion in total assets, TPS issued before May 19, 2010 will be grandfathered, so their status as Tier 1 capital does not change. Beginning January 1, 2013, bank holding companies above $15 billion in assets will have a three-year phase-in period to fill the capital gap caused by the disallowance of the TPS issued before May 19, 2010. However going forward, TPS will be disallowed as Tier 1 capital.

(2) The Act creates a new process to liquidate failed financial firms in an orderly manner, including giving the FDIC broader authority to operate or liquidate a failing financial company.

(3) The Act also establishes a new independent Federal regulatory body for consumer protection within the Federal Reserve System known as the Bureau of Consumer Financial Protection (the "Bureau"), which will assume responsibility for most consumer protection laws (except the Community Reinvestment Act). It will also be in charge of setting appropriate consumer banking fees and caps. The Office of Comptroller of the Currency will continue to have authority to preempt state banking and consumer protection laws if these laws "prevent or significantly" interfere with the business of banking.

(4) The Act effects changes in the FDIC assessment as discussed in section “FDIC Insurance Assessments” above.

(5) The Act places certain limitations on investment and other activities by depository institutions, holding companies and their affiliates, including comprehensive regulation of all over-the-counter derivatives.

The impact of the Act on our banking operations is still uncertain due to the massive volume of new rules still subject to adoption and interpretation.

Available Information

On our internet web site, www.bankofmarin.com, we post the following filings as soon as reasonably practicable after they are filed with or furnished to the SEC: Annual Report on Form 10-K, Proxy Statement for the Annual Meeting of Shareholders, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities and Exchange Act of 1934. The text of the Code of Ethical Conduct for Bancorp and the Bank is also included on the website. All such filings on our website are available free of charge. This website address is for information only and is not intended to be an active link, or to incorporate any website information into this document. In addition, copies of our filings are available by requesting them in writing or by phone from:

Corporate Secretary

Bank of Marin

504 Redwood Blvd., Suite 100

Novato, CA 94947

415-763-4523

|

ITEM 1A.

|

RISK FACTORS

|

An investment in our common stock is subject to risks inherent to our business. The material risks and uncertainties that Management believes may affect our business are described below. Before making an investment decision, investors should carefully consider the risks and uncertainties described below together with all of the other information included or incorporated by reference in this report. The risks and uncertainties described below are not the only ones facing our business. Additional risks and uncertainties that Management is not aware of or focused on or that Management currently deems immaterial may also impair business operations. This report is qualified in its entirety by these risk factors.

If any of the following risks actually occur, our financial condition and results of operations could be materially and adversely affected.

Our Earnings are Significantly Influenced by General Business and Economic Conditions

We are operating in an uncertain economic environment. While the economic recession ended in 2009 and there are signs of economic conditions improving, the persistent high unemployment rate, weak business and consumer spending, and the U.S. budget deficit underline that the economy remains very fragile. Economic recovery is expected to be slow and long. The housing market is not expected to recover soon amid a bleak job market. Business activity across a wide range of industries and regions is greatly affected. Local and state governments are in difficulty due to the reduction in sales taxes resulting from the lack of consumer spending and property taxes resulting from declining property values. Financial institutions continue to be affected by the contraction of the real estate market, elevated foreclosure rates, high unemployment rates and a stricter regulatory environment. While our service area has not experienced the same degree of challenge in unemployment as other areas2, the effects of these issues have trickled down to households and businesses in our markets. There can be no assurance that the recent economic improvement is sustainable and credit worthiness of our borrowers will not deteriorate.

Continued declines in real estate values and home sale volumes, financial stress on borrowers, including job losses, and customers’ inability to pay debt could adversely affect our financial condition and results of operations in the following aspects:

|

|

·

|

Demand for our products and services may decline

|

|

|

·

|

Low cost or non-interest bearing deposits may decrease

|

|

|

·

|

Collateral for our loans, especially real estate, may decline further in value

|

|

|

·

|

Loan delinquencies, problem assets and foreclosures may increase

|

Our deposit growth level has outpaced our loan growth recently, which leads to excess liquidity earning a less favorable yield. As the economy is still fragile, consumers are wary of their debts and are reducing their borrowing activities. We have noticed a decrease in loan demand due to an unfavorable economic climate and intensified competition for creditworthy borrowers, all of which could impact our ability to generate profitable loans.

_______________________________

2 Based on the latest available labor market information from Employment Development Department. Preliminary December 2010 results show that the unemployment rate in Marin County was the lowest in California at 7.9% and in Sonoma County at 10.0%, compared to the state of California at 12.3%.

Nonperforming Assets Take Significant Time To Resolve And Adversely Affect Our Results Of Operations And Financial Condition.

Our nonperforming assets have been maintained at a manageable level historically. As discussed in Note 19 to the Consolidated Financial Statements in Item 8 of this report, we acquired certain assets of the failed Charter Oak Bank on February 18, 2011. The acquisition may expose us to credit issues of acquired assets, which may become nonperforming in the future.

Nonperforming assets may adversely affect our net income in various ways. Until economic and market conditions improve, we expect to continue to incur additional losses relating to nonperforming assets. We do not record interest income on non-accrual loans, thereby adversely affecting our income and increasing our loan administration costs. When we take collateral in foreclosures and similar proceedings, we are required to mark the related loan to the then fair market value of the collateral, which may result in a loss. While we have tried to reduce our problem assets through workouts, restructurings and otherwise, decreases in the value of these assets, or the underlying collateral, or in these borrowers’ performance or financial conditions, whether or not due to economic and market conditions beyond our control, could adversely affect our business, results of operations and financial condition. In addition, the resolution of nonperforming assets requires significant commitments of time from management, which can be detrimental to the performance of other responsibilities. There can be no assurance that we will not experience further increases in nonperforming loans in the future.

Recently Enacted Legislation and Other Measures Undertaken by the Government May not Help Stabilize the U.S. Financial System and The Impact of New Financial Reform Legislation is Yet to be Determined

As discussed in Item 1, Section captioned “Supervision and Regulation” above, in 2010, President Obama signed into law a landmark financial reform bill—the Dodd-Frank Act. The current rules and interpretations being considered under the Dodd-Frank Act may change banking statutes and the operating environment of Bancorp and the Bank in substantial and unpredictable ways, and could increase the cost of doing business, decrease our revenues, limit or expand permissible activities or affect the competitive balance depending upon whether or how regulations are implemented. We may be forced to invest significant management attention and resources to make any necessary changes related to the Dodd-Frank Act and any regulations promulgated there under. The ultimate effect of the changes would have on the financial condition or results of operations of Bancorp or the Bank is uncertain at this time.

The actual impact of the recently enacted legislation and such related measures undertaken to alleviate the aftermaths of the credit crisis is unknown. The capital and credit markets have experienced volatility and disruption at an unprecedented level in the past few years. In some cases, the markets have produced downward pressure on credit availability for certain issuers without regard to those issuers’ underlying financial strength. If the recent years’ disruption and volatility return, there can be no assurance that we will not experience an adverse effect on our ability to access credit or capital.

In addition to changes resulting from the Dodd-Frank Act, recent proposals published by the Basel Committee on Banking Supervision, if adopted, could lead to significantly higher capital requirements, higher capital charges and more restrictive leverage and liquidity ratios. On September 12, 2010, the Basel Committee announced an agreement on additional capital reforms that increases required Tier 1 capital and minimum Tier 1 common equity capital and requires banks to maintain an additional capital conservation buffer during times of economic prosperity. If adopted, it could restrict our ability to grow or require us to raise additional capital. As a result, it may affect the result of our financial condition, or business’ prospects in the future.

The Recent Repeal of Federal Prohibitions on Payment of Interest on Demand Deposits Could Increase Our Interest Expense

The Dodd-Frank Act has lifted the prohibitions on payment of interest on demand deposits. Beginning on July 21, 2011, financial institutions can start paying interest on demand deposits in an effort to compete for deposits. Although we do not know what interest rates will be offered by our competitors, we would increase our interest expense and interest rate sensitivity and experience an overall decrease in the net interest margin if we were to offer interest on demand deposits to attract or retain customers. As a result, it may affect the result of our financial condition, or business’ prospects in the future.

We May Experience Unfavorable Outcomes with Growth

We seek to expand our franchise safely and consistently. A successful growth strategy requires us to manage multiple aspects of the business simultaneously, such as following adequate loan underwriting standards, balancing loan and deposit growth without increasing interest rate risk or compressing our net interest margin, maintaining sufficient capital, and recruiting, training and retaining qualified professionals. We have recently expanded into Santa Rosa and plan to expand to the town of Sonoma through a new branch opening. These new markets may have characteristics unfamiliar to us. We also expect significant increase in non-interest expenses associated with new branches with a lag in profitability.

Our growth strategy also includes merger and acquisition opportunities that either enhance our market presence or have potential for improved profitability through financial management, economies of scale or expanded services. As discussed in Note 19 to the Consolidated Financial Statement in Item 8 of this report, we acquired certain assets and certain liabilities of Napa-based Charter Oak Bank on February 18, 2011 through an FDIC-assisted transaction. While FDIC-assisted acquisitions provide attractive opportunities in part due to loans purchased at significant discounts, acquiring other banks or branches involves risks such as exposure to potential asset quality issues of the target company, potential disruption to our normal business activities and diversion of Management’s time and attention due to integration and conversion efforts. If we pursue our growth strategy too aggressively and fail to execute integration properly, we may not be able to achieve expected synergies or other anticipated benefits.

Interchange Reimbursement Fees and Related Practices Have Been Receiving Significant Legal and Regulatory Scrutiny, and the Resulting Regulations Could Have a Significant Impact on Interchange Fees We Earn

The Dodd-Frank Act includes provisions that will regulate the debit interchange rates and certain other network industry practices (the “Durbin Amendment”). In addition, the Federal Reserve now has the power to regulate network fees to the extent necessary to prevent evasion of the new rules on interchange rates. The Federal Reserve has proposed rules to restrict interchange fees on debit cards to about 12 cents per transaction for institutions with $10 billion or more in assets. Interchange represents a transfer of value between the financial institutions participating in a payments network such as Visa and NYCE, in which we participate. In connection with transactions initiated with cards in a payments system, interchange reimbursement fees are typically paid to issuers, the financial institutions such as us that issue debit cards to cardholders. They are typically paid by owners, the financial institutions that offer network connectivity and payment acceptance services to merchants.

In January 2010, Visa announced that it will implement a two-tiered pricing system for debit interchange -- one for banks with more than $10 billion in assets, and one for all those under the $10 billion threshold. However, it may still not alleviate the negative consequences that the Durbin amendment and the Federal Reserve’s proposed rules will have for banks of all sizes and consumers. Despite the statutory attempt to separate out smaller banks from the price controls embodied in the Durbin amendment, the marketplace may drive business to the lowest cost option. Merchants may switch to lower-cost cards and accounts of larger institutions, applying downward pressure on the fees paid to small institutions to compete. Community banks such as us may ultimately be harmed as a result. We may be forced to charge lower fees to customers, affecting our profitability. Owners of networks in which we do not participate could elect to charge higher discount rates to merchants, leading merchants not to accept cards for payment, or to steer Visa cardholders to alternate payment systems, hence reducing our transaction volumes.

Negative Conditions Affecting Real Estate May Harm Our Business

Concentration of our lending activities in the California real estate sector could negatively impact our results of operations if the adverse changes in the real estate market in our lending area intensify. Although we do not offer traditional first mortgages, nor have sub-prime or Alt-A residential loans or significant amount of securities backed by such loans in the portfolio, we are not immune from the effect of the set-back of the real estate market. Approximately 86% of our loans were secured by real estate at December 31, 2010, of which 65% were secured by commercial real estate and the remaining 21% by residential real estate. Real estate valuations are impacted by demand, and demand is driven by factors such as employment; when unemployment rises, demand drops. The unemployment rate has stayed at an elevated level since 2009. Most of the properties that secure our loans are located within Marin and Sonoma Counties. While we have seen improvement in real estate sales statistics3 after a few years of falling prices, there is no guarantee that the recent trend will continue.

_______________________________

3 Based on the latest available real estate information from Keegan & Coppin Company, Inc.

Loans secured by commercial real estate include those secured by small office buildings, owner-user office/warehouses, mixed-use residential/commercial properties and retail properties. In 2010, office vacancy rates in Marin County have fallen slightly from 26.3% to 25.7%, while industrial and retail rates have risen slightly from approximately 4% to 6%4. In Sonoma County, vacancy rates are generally higher than in Marin County: the rate of industrial, retail, and office vacancies decreased from 15.5%, 9.2%, and 24.8% in 2009 to 13.9%, 8.5%, and 22.3% in 2010, respectively4. There can be no assurance that the companies or properties securing our loans will generate sufficient cash flows to allow the borrowers to make full and timely loan payments to us.

In late 2006, Federal banking regulators issued final guidance regarding commercial real estate lending to address a concern that rising commercial real estate lending concentrations may expose institutions to unanticipated earnings and capital volatility in the event of adverse changes in the investor commercial real estate market. This guidance suggests that institutions that are potentially exposed to significant commercial real estate concentration risk will be subject to increased regulatory scrutiny. Institutions that have experienced rapid growth in commercial real estate lending, have notable exposure to a specific type of commercial real estate lending, or are approaching or exceed certain supervisory criteria that measure an institution’s commercial real estate portfolio against its capital levels, may be subject to such increased regulatory scrutiny. Although regulators have not notified us of any concern, there is no assurance that we will not be subject to additional scrutiny in the future.

We are Subject to Interest Rate Risk

Our earnings and cash flows are largely dependent upon our net interest income. Net interest income is the difference between interest income earned on interest-earning assets, such as loans and securities, and interest expense paid on interest-bearing liabilities, such as deposits and borrowed funds. Interest rates are sensitive to many factors outside our control, including general economic conditions and policies of various governmental and regulatory agencies and, in particular, the Board of Governors of the Federal Reserve System, which regulates the supply of money and credit in the United States. Changes in monetary policy, including changes in interest rates, could influence not only the interest we receive on loans and securities and interest we pay on deposits and borrowings, but could also affect (i) our ability to originate loans and obtain deposits, (ii) the fair value of our financial assets and liabilities, and (iii) the average duration of our mortgage-backed securities portfolio. Our portfolio of securities is subject to interest rate risk and will generally decline in value if market interest rates increase, and generally increase in value if market interest rates decline. Our mortgage-backed security portfolio is also subject to prepayment risk in a low interest rate environment.

In response to the recessionary state of the national economy, the gloomy housing market and the volatility of financial markets, the Federal Open Market Committee of the Federal Reserve Board (“FOMC”) started a series of decreases in Federal funds target rate with seven decreases in 2008, bringing the target rate to a historically low range of 0% to 0.25% through December 2010.

In the current environment of historically low interest rates, it is imperative for us to mitigate exposure to potential increases in interest rates. If interest rates rise by more than 100 basis points, we anticipate that net interest income will rise assuming no additional deposit rate sensitivity. However, it may still take several upward market rate movements for variable rate loans at floors to move above their floor rates. Further, a rise in index rates leads to lower debt service coverage of variable rate loans if the borrower’s operating cash flow doesn’t also rise. This creates a leveraged paradox of an improving economy (leading to higher interest rates), but lower credit quality as short-term rates move up faster than the cash flow or income of the borrowers. Higher interest rates may also depress loan demand, making it more difficult for us to grow loans.

_______________________________

4 Median price for single-family re-sales homes were up 3.3% in Marin County and 3.2% in Sonoma County in 2010.

Interest rate changes can create fluctuations in the net interest margin due to an imbalance in the timing of repricing or maturity of assets or liabilities. We manage interest rate risk exposure with the goal of minimizing the impact of interest rate volatility on the net interest margin. Although we believe we have implemented effective asset and liability management strategies, any substantial, prolonged low interest rate environment could have an adverse effect on our financial condition and results of operations. See the sections captioned “Net Interest Income” in Management’s Discussion and Analysis of Financial Condition and Results of Operations in Item 7 and Quantitative and Qualitative Disclosures about Market Risk in Item 7A of this report for further discussion related to management of interest rate risk.

We are Subject to Significant Credit Risk and Loan Losses May Exceed Our Allowance for Loan Losses in the Future

We maintain an allowance for loan losses, which is a reserve established through a provision for loan losses charged to expense, that represents Management’s best estimate of probable losses that may be incurred within the existing portfolio of loans. The level of the allowance reflects Management’s continuing evaluation of industry concentrations, specific credit risks, loan loss experience, current loan portfolio quality and present economic, political and regulatory conditions. The determination of the appropriate level of the allowance for loan losses inherently involves a high degree of subjectivity and requires us to make significant estimates of current credit risks and future trends, all of which may undergo material changes. Further, we generally rely on appraisals of the collateral or comparable sales data to determine the level of specific reserve and/or the charge-off amount on certain collateral dependent loans. Inaccurate assumptions in the appraisals or an inappropriate choice of the valuation techniques may lead to an inadequate level of specific reserve or charge-offs.

Changes in economic conditions affecting borrowers, new information regarding existing loans and their collateral, identification of additional problem loans and other factors, may require an increase in our allowance for loan losses. In addition, bank regulatory agencies periodically review our allowance for loan losses and may require an increase in the provision for loan losses or the recognition of further loan charge-offs. In addition, if charge-offs in future periods exceed the allowance for loan losses, we will need to record additional provision for loan losses. Any increases in the allowance for loan losses will result in an adverse impact on net income and capital.

We Face Intense Competition with Other Financial Institutions to Attract and Retain Banking Customers

We are facing significant competition for customers from other banks and financial institutions located in the markets we serve. We compete with commercial banks, saving banks, credit unions, non-bank financial services companies and other financial institutions operating within or near our serving areas. Many of our non-bank competitors are not subject to the same extensive regulations as ours, thus, are able to offer greater flexibility in competing for business. We anticipate intense competition will be continued for the coming year due to the recent consolidation of many financial institutions and more changes in legislature, regulation and technology.

Going forward, we may see tighter competition in the industry as banks seek to take market share in the most profitable customer segments, particularly the small business segment and the mass-affluent segment, which offers a rich source of deposits as well as more profitable and less risky customer relationships. Further, with the rebound of the equity markets, our deposit customers may perceive alternative investment opportunities as providing superior expected returns. Technology and other changes have made it more convenient for bank customers to transfer funds into alternative investments or other deposit accounts such as online virtual banks and non-bank service providers. The current low interest rate environment could increase such transfers of deposits to higher yielding deposits or other investments. Efforts and initiatives we undertake to retain and increase deposits, including deposit pricing, can increase our costs. When our customers move money into higher yielding deposits or in favor of alternative investments, we can lose a relatively inexpensive source of funds, thus increasing our funding costs.

We also compete with nationwide and regional banks much larger than our size, which may be able to benefit from economies of scale through their wider branch network, national advertising campaigns and sophisticated technology infrastructure.

We intend to seek additional deposits by continuing to establish and strengthen our personal relationships with our existing customers and by offering deposit products that are competitive with those offered by other financial institutions in our markets. If these efforts are unsuccessful, we may need to fund our asset growth through borrowings, other non-core funding or public offerings of our common stock which could be leveraged. Increased debt would further increase our leverage, reduce our borrowing capacity and increase our reliance on non-core funds and counterparties’ credit availability. A public offering may have a dilutive effect on earnings per share and share ownership.

Our Ability to Access Markets for Funding and Acquire and Retain Customers Could be Adversely Affected by the Deterioration of Other Financial Institutions or the Financial Service Industry’s Reputation.

Reputation risk is the risk to liquidity, earnings and capital arising from negative publicity regarding the financial services industry. The financial services industry continues to be featured in negative headlines about their roles in the past global and national credit crisis and the resulting stabilization legislation enacted by the U.S. federal government. These reports can be damaging to the industry’s image and potentially erode consumer confidence in insured financial institutions. Recent bank failures in California, including in our own markets, have had a negative impact and additional failures are expected. In addition, our ability to engage in routine funding and other transactions could be adversely affected by the actions and commercial soundness of other financial institutions. Financial services institutions are interrelated as a result of trading, clearing, counterparty or other relationships. As a result, defaults by, or even rumors or questions about, one or more financial services institutions, or the financial services industry generally, have led to market-wide liquidity problems, losses of depositor, creditor and counterparty confidence and could lead to losses or defaults by us or by other institutions. We could experience increases in deposits and assets as a direct or indirect result of other banks’ difficulties or failure, which would increase the capital we need to support such growth or we could experience severe and unexpected decreases in deposits which could adversely impact our liquidity and heighten regulatory concern.

Bancorp and the Bank are Subject to Extensive Government Regulation and Supervision

Bancorp and the Bank are subject to extensive federal and state governmental supervision, regulation and control. Holding company regulations affect the range of activities in which Bancorp is engaged. Banking regulations affect the Bank’s lending practices, capital structure, investment practices and dividend policy among other controls. Future legislative changes or interpretations may also alter the structure and competitive relationship among financial institutions.

The historic disruptions in the financial marketplace over the past few years have prompted the Obama administration to reform the financial market regulation. This proposed reform includes additional regulations over consumer financial products, bond rating agencies and the creation of a regime for regulating systemic risk across all types of financial service firms. In light of recent economic conditions as well as regulatory and congressional criticism, further restrictions on financial service companies may adversely impact our results of operations and financial condition, as well as increase our compliance risk.

Compliance risk is the current and prospective risk to earnings or capital arising from violations of, or nonconformance with, laws, rules, regulations, prescribed practices, internal policies, and procedures, or ethical standards set forth by regulators. Compliance risk also arises in situations where the laws or rules governing certain bank products or activities of our clients may be ambiguous or untested. This risk exposes Bancorp and the Bank to potential fines, civil money penalties, payment of damages and the voiding of contracts. Compliance risk can lead to diminished reputation, reduced franchise value, limited business opportunities, reduced expansion potential and an inability to enforce contracts.

For further information on supervision and regulation, see the section captioned “Supervision and Regulation” in Item 1 above.

Bancorp Relies on Dividends from the Bank to Pay Cash Dividends to Shareholders

Bancorp is a separate legal entity from its subsidiary, the Bank. Bancorp receives substantially all of its revenue from the Bank in the form of dividends, which is Bancorp’s principal source of funds to pay cash dividends to Bancorp’s common shareholders. Various federal and state laws and regulations limit the amount of dividends that the Bank may pay to Bancorp. In the event that the Bank is unable to pay dividends to Bancorp, Bancorp may not be able to pay dividends to its shareholders. As a result, it could have an adverse effect on Bancorp’s stock price and investment value.

Under federal law, capital distributions from the Bank would become prohibited, with limited exceptions, if the Bank were categorized as "undercapitalized" under applicable Federal Reserve or FDIC regulations. In addition, as a California bank, the Bank is subject to state law restrictions on the payment of dividends. Distributions from the Bank to Bancorp are subject to advance regulatory approval for three years beginning in 2010. For further information on the distribution limit from the Bank to Bancorp, see the section captioned “Bank Regulation” in Item 1 above and “Dividends” in Note 9 to the Consolidated Financial Statements in Item 8 below.

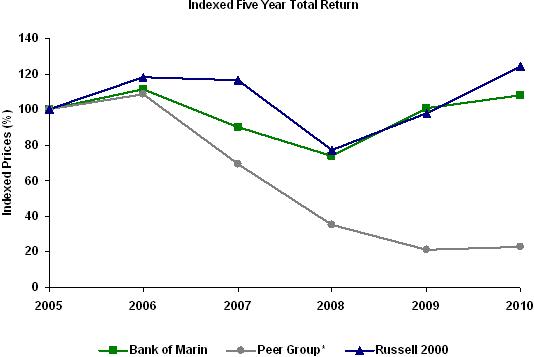

The Trading Volume of Bancorp’s Common Stock is Less than That of Other Larger Financial Services Companies

Our common stock is listed on the NASDAQ’s Capital Market. Our trading volume is less than that of nationwide or regional financial institutions. A public trading market having the desired characteristics of depth, liquidity and orderliness depends on the presence of willing buyers and sellers of common stock at any given time. This presence depends on the individual decisions of investors and general economic and market conditions over which we have no control. Given the lower trading volume of our common stock, significant trades of our stock in a given time, or the expectations of these trades, could cause the stock price to be more volatile.

Failure of Correspondent Banks and Counterparties May Affect our Liquidity

In the past few years, the financial services industry in general was materially and adversely affected by the credit crises. We have witnessed failure of banks in the industry in recent years and the trend is expected to continue. We rely on our correspondent banks for lines of credit. We also have two correspondent banks as counterparties in our derivative transactions (see Note 15 to the Consolidated Financial Statements). While we continually monitor the financial health of our correspondent banks and we have diverse sources of liquidity, should any one of our correspondent banks become financially impaired, our available credit may decline and/or they may be unable to honor their commitments.

Unexpected Early Termination of Our Interest Rate Swap Agreements May Impact Our Earnings

We have entered into interest-rate swap agreements, primarily as an asset/liability management strategy, in order to mitigate the changes in the fair value of specified long-term fixed-rate loans and firm commitments to enter into long-term fixed-rate loans caused by changes in interest rates. These hedges allow us to offer long-term fixed rate loans to customers without assuming the interest rate risk of a long-term asset by swapping our fixed-rate interest stream for a floating-rate interest stream. In the event of default by the borrowers on our hedged loans, we may have to terminate these designated interest-rate swap agreements early, resulting in severe prepayment penalties charged by our counterparties. On the other hand, when these interest-rate swap agreements are in an asset position, we are subject to the credit risk of our counterparties, who may default on the interest-rate swap agreements, leaving us vulnerable to interest rate movements.

Securities May Lose Value due to Credit Quality of the Issuers

We hold securities issued and/or guaranteed by Federal National Mortgage Association (“FNMA”) and Federal Home Loan Mortgage Corporation (“FHLMC”). In 2008, the U.S. Government placed both FNMA and FHLMC under conservatorship. Starting in December 2008, the U.S. Government also began purchasing mortgage-backed securities (“MBS”) issued by FNMA. Further, in December 2009, the U.S. Treasury also announced unlimited capital support for FNMA and FHLMC for the next three years. As a result, the MBS issued by FNMA and FHLMC has experienced an increase in fair value and our available-for-sale security portfolio has benefitted from this government support. However, the Obama administration released its report to Congress on reforming the housing-finance market on February 11, 2011. The proposal would wind down FNMA and FHLMC and incrementally shrink the government’s housing-finance footprint by, among other things, gradually increasing the firms’ guarantee pricing, reducing their conforming loan limits, and phasing in a 10-percent down-payment requirement. When the U.S. Government starts selling the MBS securities issued by FNMA and FHLMC, when the government support is phased-out or completely withdrawn, or if either the FNMA or FHLMC comes under further financial stress or deteriorates in their credit worthiness, the fair value of our securities issued or guaranteed by these entities could be negatively affected.

We also invest in obligations of state and political subdivisions, some of which are experiencing financial difficulties in part due to loss of property tax from falling home values and declines in sales tax revenues from a reduction in retail activities. The 2009 federal stimulus funds that flowed out to state governments across the country is running down and is expected to drop to $89.4 billion for 2011, $23.3 billion in 2012 and $14.3 billion in 2013. State and political subdivisions are expected to undergo further financial stress due to the reduced federal funding. While we seek to minimize our exposure by diversifying geographic location of our portfolio and investing in investment grade securities, there is no guarantee that the issuers will remain financially sound to be current with their payments on these debentures.

Deterioration of Credit Quality or Insolvency of Insurance Companies May Impede our Ability to Recover Losses

The recent financial crisis has led certain major insurance companies to the verge of bankruptcy. We have property, casualty and financial institution risk coverage underwritten by several insurance companies, who may not avoid the insolvency risk permeating in the insurance industry. In addition, some of our investment in obligations of state and political subdivisions is insured by several insurance companies. While we closely monitor credit ratings of our insurers and insurers of our municipality securities, and we are poised to make quick changes if needed, we cannot predict an unexpected inability to honor commitments. We also invest in bank-owned life insurance policies on certain members of senior management, which may lose value in the event of the carriers’ insolvency. In the event that our bank-owned life insurance policy carriers’ credit ratings fall below investment grade, we may exchange policies underwritten by them to another carrier at a cost charged by the original carrier, or we may terminate the policies which may result in adverse tax consequences.

Our loan portfolio is also primarily secured by properties located in earthquake or fire-prone zones. In the event of a disaster that causes pervasive damage to the region in which we operate, not only the Bank, but also the loan collateral may suffer losses not recovered by insurance.

We Rely on Technology and Continually Encounter Technological Change

The financial services industry is continually undergoing rapid technological change with frequent introductions of new technology-driven products and services. The effective use of technology will enable efficiency and meeting customer’s changing needs. Our future success depends, in part, upon our ability to address the needs of our customers by using technology to provide products and services that will satisfy customer demands, as well as to create additional efficiencies in our operations. Many of our competitors have substantially greater resources to invest in technological improvements. We may not be able to effectively implement new technology-driven products and services or be successful in marketing these products and services to retain and compete for customers. Failure to successfully keep pace with technological change affecting the financial services industry could have a material adverse impact of the long-term aspect our business and, in turn, our financial condition and results of operations.

We May Experience a Breach in Security

Our business requires the secure handling of sensitive client information. We also rely heavily on communications and information systems to conduct our business. A breach of security in the Bank, at our vendors or customers, or widely publicized breaches of other financial institutions could significantly harm our reputation, result in a loss of customer business, subject us to additional regulatory scrutiny, or expose us to civil litigation and possible financial liability. While we have systems and procedures designed to prevent security breaches, we cannot be certain that advances in criminal capabilities, physical system or network break-ins or inappropriate access will not compromise or breach the technology protecting our networks or proprietary client information.

We Rely on Third-Party Vendors for Important Aspects of Our Operation

We depend on the accuracy and completeness of information provided by certain key vendors, including but not limited to, data processing, payroll processing, technology support, investment security safekeeping and accounting. Our ability to operate, as well as the our financial condition and results of operations, could be negatively affected in the event of an interruption of an information system, an undetected error, or in the event of a natural disaster whereby certain vendors are unable to maintain business continuity.

We May Not Be Able To Attract and Retain Key Employees

Our success depends, in large part, on our ability to attract and retain key people. Competition for the best people in most activities engaged by us can be intense and we may not be able to hire skilled people or retain them. We do not currently have non-competitive agreements with any of our senior officers. The unexpected loss of services of key personnel could have a material adverse impact on our business because of the skills, knowledge of our market, years of industry experience and the difficulty of promptly finding qualified replacement personnel.

Severe Weather, Natural Disasters or Other Climate Change Related Matters Could Significantly Impact Our Business

Our primary market is located in an earthquake-prone zone in northern California. Other severe weather or disasters, such as severe rainstorms, wildfire or flood, could interrupt our business operations unexpectedly. Climate-related physical changes and hazards could also pose credit risks for us. For example, our borrowers may have collateral properties located in coastal areas at risk to rise in sea level. The properties pledged as collateral on our loan portfolio could also be damaged by tsunamis, floods, earthquake or wildfires and thereby the recoverability of our loan could be impaired. A number of factors affect our credit losses, including the extent of damage to the collateral, the extent of damage not covered by insurance, the extent to which unemployment and other economic conditions caused by the natural disaster adversely affect the ability of borrowers to repay their loans, and the cost of collection and foreclosure to us. Lastly, there could be increased insurance premiums and deductibles, or a decrease in the availability of coverage, due to severe weather-related losses. The ultimate impact on our business of a natural disaster, whether or not caused by climate change, is difficult to predict.

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

None.

|

ITEM 2.

|

PROPERTIES

|

We lease our corporate headquarters building, which houses our primary loan production, operations, and administrative offices, in Novato, California. We also lease other branch or office facilities within our primary market areas in the cities of Corte Madera, San Rafael, Novato, Sausalito, Mill Valley, Greenbrae, Petaluma, Santa Rosa, Sonoma, Napa and San Francisco, California. We consider our properties to be suitable and adequate for our present needs. For additional information on properties, see Notes 5 and 13 to the Consolidated Financial Statements included in Item 8 of this Form 10-K.

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

There are no pending, or to Management's knowledge any threatened, material legal proceedings to which we are a party, or to which any of our properties are subject. There are no material legal proceedings to which any director, any nominee for election as a director, any executive officer, or any associate of any such director, nominee or officer is a party adverse to us.

We are responsible for our proportionate share of certain litigation indemnifications provided to Visa U.S.A. by its member banks in connection with lawsuits related to anti-trust charges and interchange fees. For further details, see Note 13 to the Consolidated Financial Statements in Item 8 of this Form 10-K.

|

ITEM 4.

|

REMOVED AND RESERVED

|

|

ITEM 5.

|