Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - ACME UNITED CORP | acme_10k123110ex21.htm |

| EX-31.2 - EXHIBIT 31.2 - ACME UNITED CORP | acme_10k123110ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - ACME UNITED CORP | acme_10k123110ex311.htm |

| EX-32.1 - EXHIBIT 32.1 - ACME UNITED CORP | acme_10k123110ex321.htm |

| EX-23.2 - EXHIBIT 23.2 - ACME UNITED CORP | acme_10k123110ex232.htm |

| EX-23.1 - EXHIBIT 23.1 - ACME UNITED CORP | acme_10k123110ex231.htm |

| EX-32.2 - EXHIBIT 32.2 - ACME UNITED CORP | acme_10k123110ex322.htm |

| EX-10.11 - EXHIBIT 10.11 - ACME UNITED CORP | acme_10k123110ex1011.htm |

| EX-10.10 - EXHIBIT 10.10 - ACME UNITED CORP | acme_10k123110ex1010.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

|

[X]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

OR

|

|

[_]

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF

THE SECURITIES EXCHANGE ACT OF 1934

|

Commission file number 01-07698

ACME UNITED CORPORATION

Exact name of registrant as specified in its charter

| Connecticut | 06-0236700 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

| 60 Round Hill Road | |

| Fairfield, Connecticut | 06824 |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code (203) 254-6060

Securities registered pursuant to Section 12(b) of the Act:

| Name of each exchange on | |

| Title of each class | which registered |

| $2.50 par value Common Stock | NYSE Amex |

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES [_] NO [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

YES [_] NO [X]

Indicate by check mark whether the registrant (l) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

YES [X] NO [_]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

YES [X] NO [_]

1

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one).

| Large accelerated filer [_] | Accelerated filer [_] |

| Non-accelerated filer [_] |

Smaller Reporting Company [X]

|

Indicate by check mark whether the registrant is a shell company as defined in Rule 12b-2 of the Exchange Act.

YES [_] NO [X]

The aggregate market value of the voting stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter was $27,234,273. Registrant had 3,069,837 shares of its $2.50 par value Common Stock outstanding as of March 2, 2011.

Documents Incorporated By Reference

(1) Certain portions of the Company’s Proxy Statement for the Annual Meeting scheduled for April 25, 2011 is incorporated into the Company’s 2010 Annual Report on Form 10-K, Part III.

2

|

|

Page

|

|||||

| Part I | ||||||

|

Item 1.

|

Business

|

4

|

||||

|

Item 1A.

|

Risk Factors

|

6

|

||||

|

Item 1B.

|

Unresolved Staff Comments

|

8

|

||||

|

Item 2.

|

Properties

|

8

|

||||

|

Item 3.

|

Legal Proceedings

|

9

|

||||

|

Item 4.

|

Reserved

|

9

|

||||

| Part II |

|

|||||

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

10

|

||||

|

Item 6.

|

Selected Financial Data

|

12

|

||||

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

12

|

||||

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

16

|

||||

|

Item 8.

|

Financial Statements and Supplementary Data

|

17

|

||||

|

Item 9.

|

Changes In and Disagreements with Accountants on Accounting and Financial Disclosure

|

36

|

||||

|

Item 9A.

|

Controls and Procedures

|

36

|

||||

|

Item 9B.

|

Other Information |

36

|

||||

| Part III |

|

|||||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

37

|

||||

|

Item 11.

|

Executive Compensation

|

38

|

||||

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

38

|

||||

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

38

|

||||

|

Item 14.

|

Principal Accountant Fees and Services

|

39

|

||||

| Part IV |

|

|||||

|

Item 15.

|

Exhibits and Financial Statement Schedules

|

39

|

||||

|

|

Signatures

|

42

|

||||

3

PART I

Item 1. Business

General

Acme United Corporation (together with its subsidiaries, the "Company") was organized as a partnership in l867 and incorporated in l882 under the laws of the State of Connecticut. The Company is a leading worldwide supplier of innovative cutting, measuring and safety products to the school, home, office, hardware and industrial markets. The Company's operations are in the United States, Canada, Europe (located in Germany) and Asia (located in Hong Kong and China). The operations in the United States, Canada and Europe are primarily involved in product development, marketing, sales, administrative and distribution activities. The operations in Asia consist of sourcing, product development, production planning, quality control and sales activities. Net sales in 2010 were: United States (including Asia) - $47.2 million, Canada - $7.7 million, and Europe - $8.2 million.

The Company has grouped its operations into three reportable segments based on the Company’s geographical organization and structure: (1) United States (which includes its Asian operations); (2) Canada and (3) Europe. Refer to Note 10 of the Notes to Consolidated Financial Statements for additional segment information.

Business Strategy

The Company’s business strategy includes the following key elements:

· a commitment to technological innovation achieved through consumer insight, creativity and speed to market;

· a broad selection of products in both brand and private label;

· prompt response and same-day shipping;

· superior customer service; and

· value pricing.

Principal Products

The Company markets and sells under four main brands - Westcott®, Clauss®, Camillus® and PhysiciansCare®.

Cutting

Principal products within the cutting device category are scissors, shears, guillotine paper trimmers, rotary paper trimmers, rotary cutters, knives, hobby knives and blades, utility knives, pruners, loppers, saws, manicure products, medical cutting instruments and pencil sharpeners. Products introduced in 2010 included Westcott TrimAir® paper trimmers with patented titanium coating and a proprietary blade change system for rotary and personal trimmers. Products introduced in 2009 included Westcott Ultra Soft Handle scissors with anti-microbial product protection, True Professional™ sewing shears as well as a line of iPoint® pencil sharpeners utilizing the Company’s proprietary non-stick coating. The Company also added to its KleenEarth® family of recycled products by modifying the production process to allow for multi-colored products as opposed to the traditional black. Two years ago, the Company acquired the patents and intellectual property of Camillus Cutlery, the oldest knife company in the United States and in 2009, launched a new family of knives with proprietary designs and high performance titanium carbonitride coatings. In 2010 Camillus expanded the range of knives for tactical outdoor sporting use. In 2010 Clauss introduced high performance marine tools for saltwater fishing. In 2008 the Company began shipping the Clauss Speedpak utility knife with replaceable cartridges.

Measuring

Principal products within the measuring instrument category are rulers, math tools and tape measures. Recent product introductions included Westcott branded erasers, compasses and protractors and rulers and math kits with anti-microbial product protection.

Safety

Principal products within the safety product category are first aid kits, personal protection products and over-the-counter medication refills. The 2010 addition of Physicians Care Antacid followed additions of sinus and cough/cold medications in 2009. Products introduced in 2009 included PhysiciansCare Emergency Care Responder Kits, Flu Care Kits and a line of safety products with Microban.

4

Product Development

Our strong commitment to understanding our consumers and defining products that fulfill their needs through innovation drives our product development strategy, which we believe is and will be a key contributor to our success. The Company incurred research and development costs of $486,778 in 2010 and $440,378 in 2009.

Intellectual Property

The Company has many patents and trademarks that are important to its business. The Company’s success depends in part on its ability to maintain patent protection for its products, to preserve its proprietary technology and to operate without infringing upon the patents or proprietary rights of others. The Company generally files patent applications in the United States and foreign countries where patent protection for its technology is appropriate and available. The Company also considers its trademarks important to the success of its business. The more significant trademarks include Westcott, Clauss, Camillus and PhysiciansCare.

Product Distribution

Independent manufacturer representatives and direct sales are primarily used to sell the Company’s line of consumer products to wholesale, contract and retail stationery distributors, office supply super stores, school supply distributors, industrial distributors, wholesale florists, mass market retailers and hardware chains. In each of 2010 and 2009, the Company had one customer that individually exceeded 10% of consolidated net sales. Net sales to this customer amounted to approximately 21% of consolidated net sales in 2010 and 20% in 2009.

Competition

The Company competes with many companies in each market and geographic area. The major competitor in the cutting category is Fiskars Corporation. The major competitor in the measuring category is Helix International Ltd. The major competitor in the safety category is Johnson and Johnson.

Seasonality

Traditionally, the Company’s sales are stronger in the second and third quarters of the fiscal year due to the seasonal nature of the back-to-school business.

Compliance with Environmental Laws

The Company believes that it is in compliance with applicable environmental laws. The Company believes that there are no environmental matters that would have a material financial impact on the Company. The Company believes that no material adverse financial impact is expected to result from compliance with current environmental rules and regulations. In December 2008, the Company sold property it owned in Bridgeport, CT. Under the terms of the sales agreement, the Company is responsible for environmental remediation on the property in accordance with the Connecticut Transfer Act. See Note 16 of the Notes to Consolidated Financial Statements for additional information regarding the sale of the Bridgeport property.

Employees

As of December 31, 2010, the Company employed 132 people, all of whom are full time and none of whom is covered by union contracts. Employee relations are considered good and no foreseeable problems with the work force are evident.

Available Information

The Company files its annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K pursuant to Section 13(a) of the Securities Exchange Act of 1934 with the SEC electronically. The public may read or copy any materials filed by the Company with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549 on official business days during the hours of 10:00 a.m. and 3:00 p.m. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The address of that site is http://www.sec.gov.

5

You may obtain a free copy of the Company’s annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K and amendments to those reports on the Company’s website at http://www.acmeunited.com or by contacting the Investor Relations Department at the Company’s corporate offices by calling (203) 254-6060. Such reports and other information are made available as soon as reasonably practicable after such material is filed with or furnished to the SEC.

Item 1A. Risk Factors

The Company is subject to a number of significant risks that might cause the Company’s actual results to vary materially from its forecasts, targets or projections, including:

|

·

|

achieving planned revenue and profit growth in each of the Company's business segments;

|

|

·

|

changes in customer requirements and in the volume of sales to principal customers;

|

|

·

|

the timing of orders and shipments;

|

|

·

|

emergence of new competitors or consolidation of existing competitors; and

|

|

·

|

industry demand fluctuations.

|

The Company’s expectations for both short- and long-term future net revenues are based on the Company’s estimates of future demand. Orders from the Company’s principal customers are ultimately based on demand from end-users and end-user demand can be difficult to predict. Low end-user demand would negatively affect orders the Company receives from distributors and other principal customers which could, in turn adversely affect the Company’s revenues in any fiscal period. If the Company’s estimates of sales are not accurate and the Company experiences unforeseen variability in its revenues and operating results, the Company may be unable to adjust its expense levels accordingly and its profit margins could be adversely affected.

A number of the Company’s products are sold through distributors and large retailers. No assurances can be given that any or all of such distributors or retailers will continue their relationships with the Company. Distributors and other significant retail customers cannot easily be replaced and the loss of revenues and the Company’s inability to reduce expenses to compensate for the loss of revenues could adversely affect the Company’s net revenues and profit margins.

Uncertainty in the global economy could negatively impact our business.

Uncertainty in the global economy could adversely affect our customers and our suppliers and businesses such as ours. In addition, any uncertainty could have a variety of negative effects on the Company such as reduction in revenues, increased costs, lower gross margin percentages, increased allowances for doubtful accounts and/or write-offs of accounts receivable and could otherwise have material adverse effects on our business, results of operations, financial condition and cash flows.

Loss of a major customer could result in a decrease in the Company’s future sales and earnings.

In 2010 and 2009, the Company had one customer that individually exceeded 10% of consolidated net sales. Net sales to this customer amounted to approximately 21% in 2010 and 20% in 2009. The Company anticipates that a limited number of customers may account for a substantial portion of its total net revenues for the foreseeable future. The loss of a major customer or a disruption in sales to such a customer could result in a decrease of the Company’s future sales and earnings.

6

Reliance on foreign suppliers could adversely affect the Company’s business.

The Company purchases the majority of its products from foreign manufacturing partners and, as a result, its business is exposed to risks due to:

|

·

|

Increases in transportation costs;

|

|

·

|

New or increased import duties;

|

|

·

|

Transportation delays;

|

|

·

|

Work stoppages;

|

|

·

|

Capacity constraints;

|

|

·

|

Poor quality; and

|

|

·

|

Inflation and exchange rate fluctuations that could increase the cost of foreign manufactured goods.

|

The loss of key management could adversely affect the Company’s ability to run its business.

The Company’s success depends, to a large extent, on the continued service of its executive management team, operating officers and other key personnel. The Company must therefore continue to recruit, retain and motivate management and operating personnel sufficient to maintain its current business and support its projected growth.

The Company’s inability to meet its staffing requirements in the future could adversely affect its results of operations.

Failure to protect the Company’s proprietary rights or the costs of protecting these rights could adversely affect its business.

The Company’s success depends in part on its ability to obtain patents and licenses and to preserve other intellectual property rights covering its products and processes. The Company has obtained certain domestic and foreign patents, and intends to continue to seek patents on its inventions when appropriate. The process of seeking patent protection can be time consuming and expensive. There can be no assurance that pending patents related to any of the Company’s products will be issued, in which case the Company may not be able to legally prevent others from producing similar and/or compatible competing products. If other companies were to sell similar and/or compatible competing products, the Company’s results of operations could be adversely affected. Furthermore, there can be no assurance that the Company’s efforts to protect its intellectual property will be successful. Any infringement of the Company’s intellectual property or legal defense of such action could have a material adverse effect on the Company.

The Company may need to raise additional capital to fund its operations.

The Company’s management believes that, under current conditions, the Company’s current cash and cash equivalents, cash generated by operations, together with the borrowing availability under its revolving loan agreement with Wells Fargo Bank, will be sufficient to fund planned operations for the next twelve months. However, if the Company is unable to generate sufficient cash from operations, it may be required to find additional funding sources. If adequate financing is unavailable or is unavailable on acceptable terms, the Company may be unable to maintain, develop or enhance its operations, products and services, take advantage of future opportunities or adequately respond to competitive pressures.

The Company may not be able to maintain or to raise prices in response to inflation and increasing costs.

Future market and competitive pressures may prohibit the Company from raising prices to offset increased product costs, freight costs and other inflationary items. The inability to pass these costs through to the Company’s customers could have a negative effect on its results of operations.

The Company is subject to intense competition in all of the markets in which it competes.

The Company’s products are sold in highly competitive markets. The Company believes that the principal points of competition in these markets are product innovation, quality, price, merchandising, design and engineering capabilities, product development, timeliness and completeness of delivery, conformity to customer specifications and post-sale support. Competitive conditions may require the Company to match or better competitors’ prices to retain business or market shares. The Company believes that its competitive position will depend on continued investment in innovation and product development, manufacturing and sourcing, quality standards, marketing and customer service and support. The Company’s success will depend in part on its ability to anticipate and offer products that appeal to the changing needs and preferences of our customers in the various market categories in which it competes. The Company may not have sufficient resources to make the investments that may be necessary to anticipate those changing needs and the Company may not anticipate, identify, develop and market products successfully or otherwise be successful in maintaining its competitive position. There are no significant barriers to entry into the markets for most of the Company’s products.

7

Product liability claims or regulatory actions could adversely affect the Company's financial results and reputation.

Claims for losses or injuries allegedly caused by some of the Company’s products arise in the ordinary course of its business. In addition to the risk of substantial monetary judgments, product liability claims or regulatory actions could result in negative publicity that could harm the Company’s reputation in the marketplace or the value of its brands. The Company also could be required to recall possible defective products, which could result in adverse publicity and significant expenses. Although the Company maintains product liability insurance coverage, potential product liability claims are subject to a deductible or could be excluded under the terms of the policy.

The Company’s business is subject to risks associated with seasonality which could adversely affect its cash flow, financial condition, or results of operations.

The Company’s business, historically, has experienced higher sales volume in the second and third quarters of the calendar year, when compared to the first and fourth quarters. The Company is a major supplier of products related to the “back-to-school” season, which occurs principally during the months of May, June, July and August. If this typical seasonal increase in sales of certain portions of the Company’s product line does not materialize, the Company could experience a material adverse effect on its business, financial condition and results of operations.

To compete successfully, the Company must develop and commercialize a continuing stream of innovative new products that create consumer demand.

The Company’s long-term success in the current competitive environment depends on its ability to develop and commercialize a continuing stream of innovative new products that create and maintain consumer demand. The Company also faces the risk that its competitors will introduce innovative new products that compete with the Company’s products. The Company’s strategy includes increased investment in new product development and increased focus on innovation. There are, nevertheless, numerous uncertainties inherent in successfully developing and commercializing innovative new products on a continuing basis, and new product launches may not provide expected growth results.

The Company is subject to environmental regulation and environmental risks.

The Company is subject to national, state, provincial and/or local environmental laws and regulations that impose limitations and prohibitions on the discharge and emission of, and establish standards for the use, disposal and management of, certain materials and waste. These environmental laws and regulations also impose liability for the costs of investigating and cleaning up sites, and certain damages resulting from present and past spills, disposals, or other releases of hazardous substances or materials. Environmental laws and regulations can be complex and may change often. Capital and operating expenses required to comply with environmental laws and regulations can be significant, and violations may result in substantial fines and penalties. In addition, environmental laws and regulations, such as the Comprehensive Environmental Response, Compensation and Liability Act, or CERCLA, in the United States impose liability on several grounds for the investigation and cleanup of contaminated soil, ground water and buildings and for damages to natural resources on a wide range of properties. For example, contamination at properties formerly owned or operated by the Company, as well as at properties it will own and operate, and properties to which hazardous substances were sent by the Company, may result in liability for the Company under environmental laws and regulations. The costs of complying with environmental laws and regulations and any claims concerning noncompliance, or liability with respect to contamination in the future could have a material adverse effect on the Company’s financial condition or results of operations. Refer to Note 16 – Sale of Property - of the Notes to Consolidated Financial Statements for further discussion on the environmental costs related to the sale of property by the Company.

Item 1B. Unresolved Staff Comments

Not applicable to smaller reporting companies.

Item 2. Properties

The Company is headquartered at 60 Round Hill Road, Fairfield, Connecticut in 7,500 square feet of leased space. The Company owns and leases manufacturing and warehousing facilities in the United States totaling 175,000 square feet, and leases 44,000 square feet of warehousing space in Canada. The Company also leases approximately 2,000 square feet of office space in Canada. Distribution for Europe is presently being conducted at a 35,000 square foot facility owned by the Company in Solingen, Germany. The Company also leases office space in Hong Kong and Guangzhou, China.

Management believes that the Company's facilities, whether leased or owned, are adequate to meet its current needs and should continue to be adequate for the foreseeable future.

8

Item 3. Legal Proceedings

The Company is involved, from time to time, in disputes and other litigation in the ordinary course of business and may encounter other contingencies, which may include environmental and other matters. The Company presently believes that none of these matters, individually or in the aggregate, would be likely to have a material adverse impact on its financial position, results of operations or liquidity.

Item 4. Reserved

9

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

The Company's Common Stock is traded on the NYSE Amex under the symbol "ACU". The following table sets forth the high and low sale prices on the NYSE Amex for the Common Stock for the periods indicated:

|

Year Ended December 31, 2010

|

High

|

Low

|

Dividends

Declared

|

|||||||||

|

Fourth Quarter

|

$ | 10.64 | $ | 9.40 | $ | .06 | ||||||

|

Third Quarter

|

11.00 | 9.62 | .06 | |||||||||

|

Second Quarter

|

13.04 | 10.21 | .05 | |||||||||

|

First Quarter

|

11.73 | 8.55 | .05 | |||||||||

|

Year Ended December 31, 2009

|

||||||||||||

|

Fourth Quarter

|

$ | 10.29 | $ | 8.11 | $ | .05 | ||||||

|

Third Quarter

|

9.30 | 7.82 | .05 | |||||||||

|

Second Quarter

|

8.24 | 6.53 | .05 | |||||||||

|

First Quarter

|

8.37 | 5.95 | .05 | |||||||||

As of March 4, 2011 there were approximately 1,301 holders of record of the Company's Common Stock.

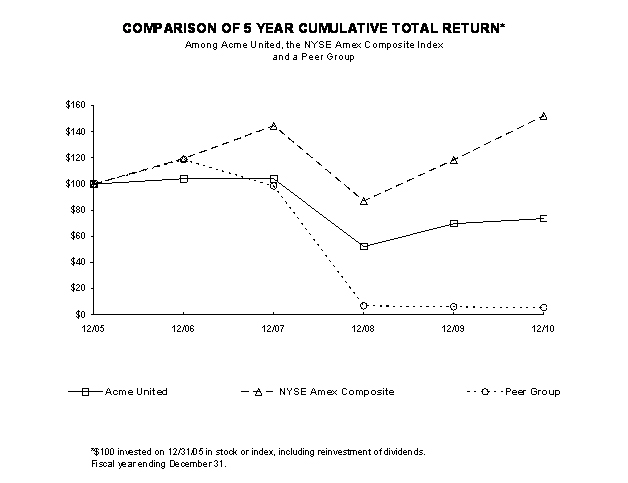

Performance Graph

The graph below compares the yearly cumulative total shareholder return on the Company’s Common Stock with the yearly cumulative total return of the following for the period 2006 to 2010: (a) the NYSE Amex Index and (b) a peer group of companies that, like the Company, (i) are currently listed on the NYSE Amex, and (ii) have a market capitalization of $30 million to $35 million.

The Company does not believe that it can reasonably identify a peer group of companies, on an industry or line-of-business basis, for the purpose of developing a comparative performance index. While the Company is aware that some other publicly-traded companies market products in the Company’s line-of-business, none of these other companies provide most or all of the products offered by the Company, and many offer products or services not offered by the Company. Moreover, some of these other companies that engage in the Company’s line-of-business do so through divisions or subsidiaries that are not publicly-traded. Furthermore, many of these other companies are substantially more highly capitalized than the Company. For these reasons, any such comparison would not, in the opinion of the Company, provide a meaningful index of comparative performance.

The comparisons in the graph below are based on historical data and are not indicative of, or intended to forecast, the possible future performance of the Company’s Common Stock. [Missing Graphic Reference]

10

Issuer Purchases of Equity Securities

During the fourth quarter of 2010, the Company announced a Common Stock repurchase program of 200,000 shares. This program does not have an expiration date. During the twelve months ended December 31, 2010, the Company repurchased 150,072 shares of its Common Stock at an average price of $10.44, all of which were purchased under a previously announced program. As of December 31, 2010, there were 200,000 shares that may be purchased under the repurchase program announced in 2010.

Set forth in the table below is certain information regarding purchases of Common Stock by the Company during the quarter ended December 31, 2010.

|

Period

|

Total Number of Shares Purchased

|

Average Price Paid per Share

|

Total Number of shares Purchased as Part of Publicly Announced Plans or Programs

|

Maximum Number of Shares that May Yet be Purchased Under these Plans or Programs

|

|||

|

October 1 - 31

|

$ -

|

-

|

0

|

||||

|

November 1 - 30

|

$ -

|

-

|

200,000

|

||||

|

December 1 - 31

|

$ -

|

-

|

200,000

|

11

|

Item 6. Selected Financial Data

|

||||||||||||||||||||

|

FIVE YEAR SUMMARY OF SELECTED FINANCIAL DATA

|

||||||||||||||||||||

|

(All figures in thousands except per share data)

|

||||||||||||||||||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

Net sales

|

$ | 63,149 | $ | 59,149 | $ | 68,719 | $ | 63,173 | $ | 56,863 | ||||||||||

|

Net income

|

$ | 2,573 | $ | 2,842 | $ | 4,467 | $ | 4,022 | $ | 3,886 | ||||||||||

|

Total assets

|

$ | 49,581 | $ | 42,309 | $ | 45,424 | $ | 42,222 | $ | 35,021 | ||||||||||

|

Long-term debt, less current portion

|

$ | 13,522 | $ | 9,154 | $ | 11,749 | $ | 10,187 | $ | 10,218 | ||||||||||

|

Net income

|

||||||||||||||||||||

|

Per share (Basic)

|

$ | 0.82 | $ | 0.86 | $ | 1.28 | $ | 1.14 | $ | 1.11 | ||||||||||

|

Per share (Diluted)

|

$ | 0.81 | $ | 0.85 | $ | 1.24 | $ | 1.09 | $ | 1.05 | ||||||||||

|

Dividends per share

|

$ | 0.22 | $ | 0.20 | $ | 0.18 | $ | 0.16 | $ | 0.12 | ||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Information

The Company may from time to time make written or oral “forward-looking statements” including statements contained in this report and in other communications by the Company, which are made in good faith by the Company pursuant to the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995.

These forward-looking statements include statements of the Company’s plans, objectives, expectations, estimates and intentions, which are subject to change based on various important factors (some of which are beyond the Company’s control). The following factors, in addition to others not listed, could cause the Company’s actual results to differ materially from those expressed in forward looking statements: the strength of the domestic and local economies in which the Company conducts operations, the impact of uncertainties in global economic conditions, changes in client needs and consumer spending habits, the impact of competition and technological change on the Company, the Company’s ability to manage its growth effectively, including its ability to successfully integrate any business which it might acquire, and currency fluctuations. All forward-looking statements in this report are based upon information available to the Company on the date of this report. The Company undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events, or otherwise, except as required by law.

Critical Accounting Policies

The following discussion and analysis of financial condition and results of operations are based upon the Company’s consolidated financial statements, which have been prepared in conformity with accounting principles generally accepted in the United States of America. The Company’s significant accounting policies are more fully described in Note 2 of the Notes to Consolidated Financial Statements. Certain accounting estimates are particularly important to the understanding of the Company’s financial position and results of operations and require the application of significant judgment by the Company’s management or can be materially affected by changes from period to period in economic factors or conditions that are outside the control of management. The Company’s management uses their judgment to determine the appropriate assumptions to be used in the determination of certain estimates. Those estimates are based on historical operations, future business plans and projected financial results, the terms of existing contracts, the observance of trends in the industry, information provided by customers and information available from other outside sources, as appropriate. The following discusses the Company’s critical accounting policies and estimates.

Estimates. Operating results may be affected by certain accounting estimates. The most sensitive and significant accounting estimates in the financial statements relate to customer rebates, valuation allowances for deferred income tax assets, obsolete and slow moving inventories, potentially uncollectible accounts receivable, and accruals for income taxes. Although the Company’s management has used available information to make judgments on the appropriate estimates to account for the above matters, there can be no assurance that future events will not significantly affect the estimated amounts related to these areas where estimates are required. However, historically, actual results have not been materially different than original estimates.

12

Revenue Recognition. The Company recognizes revenue from the sales of its products when ownership transfers to the customers, which occurs either at the time of shipment or upon delivery based upon contractual terms with the customer. The Company recognizes customer program costs, including rebates, cooperative advertising, slotting fees and other sales related discounts, as a reduction to sales.

Allowance for doubtful accounts. The Company provides an allowance for doubtful accounts based upon a review of outstanding accounts receivable, historical collection information and existing economic conditions. The allowance for doubtful accounts represents estimated uncollectible accounts receivables associated with potential customer defaults on contractual obligations, usually due to potential insolvencies. The allowance includes amounts for certain customers where a risk of default has been specifically identified. In addition, the allowance includes a provision for customer defaults based on historical experience. The Company actively monitors its accounts receivable balances and its historical experience of annual accounts receivable write offs has been negligible.

Customer Rebates. Customer rebates and incentives are a common practice in the office products industry. We incur customer rebate costs to obtain favorable product placement, to promote sell-through of products and to maintain competitive pricing. Customer rebate costs and incentives, including volume rebates, promotional funds, catalog allowances and slotting fees, are accounted for as a reduction to gross sales. These costs are recorded at the time of sale and are based on individual customer contracts. Management periodically reviews accruals for these rebates and allowances, and adjusts accruals when appropriate.

Obsolete and Slow Moving Inventory. Inventories are stated at the lower of cost, determined on the first-in, first-out method, or market. An allowance is established to adjust the cost of inventory to its net realizable value. Inventory allowances are recorded for obsolete or slow moving inventory based on assumptions about future demand and marketability of products, the impact of new product introductions and specific identification of items, such as discontinued products. These estimates could vary significantly from actual requirements if future economic conditions, customer inventory levels or competitive conditions differ from expectations.

Income Taxes. Deferred income tax liabilities or assets are established for temporary differences between financial and tax reporting bases and are subsequently adjusted to reflect changes in tax rates expected to be in effect when the temporary differences reverse. A valuation allowance is recorded to reduce deferred income tax assets to an amount that is more likely than not to be realized.

Intangible Assets. Intangible assets with finite useful lives are recorded at cost upon acquisition and amortized over the term of the related contract, if any, or useful life, as applicable. Intangible assets held by the Company with finite useful lives include patents and trademarks. The weighted average amortization period for intangible assets at December 31, 2010 was 14 years. The Company periodically reviews the values recorded for intangible assets to assess recoverability from future operations whenever events or changes in circumstances indicate that its carrying amount may not be recoverable. At December 31, 2010 and 2009, the Company assessed the recoverability of its long-lived assets and believed that there were no events or circumstances present that would that would require a test of recoverability on those assets. As a result, there was no impairment of the carrying amounts of such assets and no reduction in their estimated useful lives. The net book value of the Company’s intangible assets increased to $1,866,231 as of December 31, 2010, from $1,863,648 as of December 31, 2009.

Pension Obligation. The pension benefit obligation is based on various assumptions used by third-party actuaries in calculating this amount. These assumptions include discount rates, expected return on plan assets, mortality rates and other factors. Revisions in assumptions and actual results that differ from the assumptions affect future expenses, cash funding requirements and obligations. Our funding policy is to fund the Plan in accordance with the Internal Revenue Code and regulations.

These assumptions are reviewed annually and updated as required. The Company has a frozen defined benefit pension plan. Two assumptions, the discount rate and the expected return on plan assets, are important elements of expense and liability measurement.

13

We determine the discount rate used to measure plan liabilities as of the December 31 measurement date. The discount rate reflects the current rate at which the associated liabilities could be effectively settled at the end of the year. In estimating this rate, we look at rates of return on fixed-income investments of similar duration to the liabilities in the plan that receive high, investment grade ratings by recognized ratings agencies. Using these methodologies, we determined a discount rate of 4.42% to be appropriate as of December 31, 2010, which is a decrease of 0.64 percentage points from the rate used as of December 31, 2009. An increase of 1.0% in the discount rate would have decreased our plan liabilities as of December 31, 2010 by $0.5 million.

The expected long-term rate of return on assets considers the Company’s historical results and projected returns for similar allocations among asset classes. In accordance with generally accepted accounting principles, actual results that differ from the Company’s assumptions are accumulated and amortized over future periods and, therefore, affect expense and obligation in future periods. For the U.S. pension plan, our assumption for the expected return on plan assets was 8.25% for 2010. For more information concerning these costs and obligations, see the discussion in Note 6 – Pension and Profit Sharing, in the Notes to the Company’s Consolidated Financial Statements.

Accounting for Stock-Based Compensation. Stock based compensation cost is measured at the grant date fair value of the award and is recognized as expense over the requisite service period. The Company uses the Black-Scholes option - pricing model to determine fair value of the awards, which involves certain subjective assumptions. These assumptions include estimating the length of time employees will retain their vested stock options before exercising them (“expected term”), the estimated volatility of the Company’s common stock price over the expected term (“volatility”) and the number of options for which vesting requirements will not be completed (“forfeitures”). Changes in the subjective assumptions can materially affect estimates of fair value stock-based compensation, and the related amount recognized on the consolidated statements of operations. Refer to Note 11 - Stock Option Plans - in the Notes to Consolidated Financial Statements in this report for a more detailed discussion.

Results of Operations 2010 Compared with 2009

Net Sales

Net sales increased by $4,000,386 or 7% (6% in constant currency) in 2010 to $63,148,933 compared to $59,148,547 in 2009. The U.S. segment sales increased by $2,276,000 or 5% in 2010 compared to 2009. Sales in Canada increased by $687,000 or 10% (constant in local currency) in 2010 compared to 2009. European sales increased by $1,038,000 or 14% in U.S. dollars (22% in local currency) in 2010 compared to 2009.

The increase in net sales for the twelve months ended December 31, 2010 in the U.S. was primarily due to higher sales of the iPoint pencil sharpeners as the result of increased market share and increased sales of the Company’s non stick products. The increase in net sales in Europe for the twelve months ended December 31, 2010 was primarily due to an increase in sales into the mass market and office channels.

Gross Profit

Gross profit was 37% of net sales in 2010 and 2009. The increased leveraging effect from higher sales was offset by higher airfreight expense (approximately 100 bps). The higher airfreight expense was incurred primarily in the second quarter as the result of well publicized labor shortages in southeast China leading to slower production at the Company’s suppliers. The expedited freight costs were necessary to meet customer delivery schedules.

Selling, General and Administrative

Selling, general and administrative expenses were $20,385,000 in 2010 compared with $19,047,000 in 2009, an increase of $1,338,000 or 7%. SG&A expenses were 32% of net sales in 2010 compared to 32% in 2009. The increase in SG&A expenses was primarily related to incremental shipping and commission costs as a result of higher sales as well as higher personnel related expenses.

14

Operating Income

Operating income was $2,980,000 in 2010, compared with $3,027,000 in 2009, a decrease of $47,000. Operating income in the U.S. segment declined by approximately $498,000 mainly due to higher airfreight expense of approximately $500,000. Operating income increased in Canada by $391,000 mainly due to improved gross margins as the result of strong buying power of the Canadian dollar. The European operating loss declined by $59,000.

Interest Expense, Net

Net interest expense for 2010 was $142,000, compared with $26,000 for 2009, an increase of $116,000. The increase in interest expense, net for 2010 was primarily the result of higher average interest rates under the Company's bank revolving loan agreement combined with higher average borrowings during 2010 compared to 2009.

Other Income, Net

Net other income was $72,000 in 2010 compared to $452,000 in 2009. The decrease in other income, net for 2010 was primarily related to a $460,000 benefit recorded for the change in estimated costs associated with the remediation of the Bridgeport property in 2009 compared to $100,000 in 2010.

Income Tax

The effective tax rate in 2010 was 12%, compared to 18% in 2009. The lower effective tax rates in both years compared to historical rates were primarily the result of tax credits associated with donation of property, located in Bridgeport, CT, to the city of Bridgeport.

Off-Balance Sheet Transactions

The Company did not engage in any off-balance sheet transactions during 2010.

Liquidity and Capital Resources

During 2010, working capital increased by approximately $4.4 million compared to December 31, 2009. Inventory increased by approximately $4.9 million in anticipation of seasonal sales in 2011. Inventory turnover, calculated using a twelve month average inventory balance, increased to 2.1 from 1.9 at December 31, 2009.

Receivables increased approximately $1.6 million at December 31, 2010 compared to December 31, 2009. The average number of days sales outstanding in accounts receivable was 65 days in 2010 compared to 61 days in 2009.

|

The Company's working capital, current ratio and long-term debt to equity ratio follow:

|

||||||||

|

2010

|

2009

|

|||||||

|

Working Capital

|

$ | 33,409,776 | $ | 28,952,754 | ||||

|

Current Ratio

|

4.62 | 5.26 | ||||||

|

Long-Term Debt to Equity Ratio

|

53.3% | 37.3% | ||||||

During 2010, total debt outstanding under the Company’s revolving credit facility (referred to below) increased by approximately $4.4 million compared to total debt at December 31, 2009. As of December 31, 2010, $13,522,000 was outstanding and $4,478,000 was available for borrowing under the revolving credit facility.

On February 23, 2011, the Company modified its revolving loan agreement with Wells Fargo Bank; the amendments include an increase in the maximum borrowing amount from $18 million to $20 million; and an extension of the maturity date of the loan from February 1, 2012 to March 31, 2013. Funds borrowed under the Modified Loan Agreement may be used for working capital, general operating expenses, share repurchases and certain other purposes.

15

Under the provisions of the modified loan agreement, the Company, among other things, is restricted with respect to outside borrowings, investments and mergers. Further, the modified loan agreement requires the Company to maintain specific amounts of tangible net worth, a specified debt service coverage ratio and a fixed charge coverage ratio. This modified loan agreement continues to be secured by the assets of the U.S. parent company. This modification did not change the permissible use of funds or the quantitative covenants that the Company is required to comply with. The Company was in compliance with all financial covenants under the revolving loan agreement as of and through December 31, 2010, and believes it will be able to continue to comply with these covenants under the modified moan agreement for the remainder of the term of the credit facility.

Capital expenditures during 2010 and 2009 were $937,083 and $566,939, respectively, which were, in part, financed with borrowings under the Company’s revolving credit facility. Capital expenditures in 2011 are not expected to differ materially from recent years.

The Company believes that cash generated from operating activities, together with funds available under its revolving credit facility, are expected, under current conditions, to be sufficient to finance the Company’s planned operations for the next twelve months.

Recently Issued Accounting Standards

There were no recently issued or newly adopted accounting standards that were applicable to the preparation of our consolidated financial statements for 2010 or that may become applicable to the preparation of our consolidated financial statements in the future.

Item 7A. Quantitative and Qualitative Disclosure about Market Risk

Not applicable to smaller reporting companies.

16

|

Item 8. Financial Statements and Supplementary Data

|

||||||||

|

Acme United Corporation and Subsidiaries

|

||||||||

|

CONSOLIDATED STATEMENTS OF OPERATIONS

|

||||||||

|

For the years ended

December 31,

|

||||||||

|

2010

|

2009

|

|||||||

|

Net sales

|

$ | 63,148,933 | $ | 59,148,547 | ||||

|

Cost of goods sold

|

39,783,509 | 37,075,060 | ||||||

|

Gross profit

|

23,365,424 | 22,073,487 | ||||||

|

Selling, general and administrative expenses

|

20,385,268 | 19,046,864 | ||||||

|

Operating income

|

2,980,156 | 3,026,623 | ||||||

|

Non operating items:

|

||||||||

|

Interest:

|

||||||||

|

Interest expense

|

(301,304 | ) | (155,008 | ) | ||||

|

Interest income

|

159,555 | 129,334 | ||||||

|

Interest expense, net

|

(141,749 | ) | (25,674 | ) | ||||

|

Other income

|

72,440 | 452,005 | ||||||

|

Total other (expense) income , net

|

(69,309 | ) | 426,331 | |||||

|

Income before income tax expense

|

2,910,847 | 3,452,954 | ||||||

|

Income tax expense

|

337,883 | 610,867 | ||||||

|

Net income

|

$ | 2,572,964 | $ | 2,842,087 | ||||

|

Earnings per share:

|

||||||||

|

Basic

|

$ | 0.82 | $ | 0.86 | ||||

|

Diluted

|

$ | 0.81 | $ | 0.85 | ||||

|

See accompanying Notes to Consolidated Financial Statements.

|

||||||||

17

|

Acme United Corporation and Subsidiaries

|

||||||||

|

CONSOLIDATED BALANCE SHEETS

|

||||||||

|

December 31,

|

December 31,

|

|||||||

|

2010

|

2009

|

|||||||

|

ASSETS

|

||||||||

|

Current assets:

|

||||||||

|

Cash and cash equivalents

|

$ | 6,601,416 | $ | 6,519,065 | ||||

|

Accounts receivable, less allowance

|

12,330,665 | 10,703,433 | ||||||

|

Inventories

|

22,292,909 | 17,400,270 | ||||||

|

Deferred income taxes

|

206,732 | 180,241 | ||||||

|

Prepaid expenses and other current assets

|

1,195,613 | 952,946 | ||||||

|

Total current assets

|

42,627,335 | 35,755,955 | ||||||

|

Property, plant and equipment:

|

||||||||

|

Land

|

160,405 | 171,660 | ||||||

|

Buildings

|

2,438,073 | 2,558,572 | ||||||

|

Machinery and equipment

|

8,904,675 | 8,169,641 | ||||||

|

Total property, plant and equipment

|

11,503,153 | 10,899,873 | ||||||

|

Less: accumulated depreciation

|

9,287,397 | 8,811,705 | ||||||

|

Net plant, property and equipment

|

2,215,756 | 2,088,168 | ||||||

|

Note receivable

|

1,839,262 | 1,891,604 | ||||||

|

Intangible assets, less accumulated amortization

|

1,866,231 | 1,863,648 | ||||||

|

Deferred income taxes

|

943,606 | 621,270 | ||||||

|

Other assets

|

88,828 | 88,828 | ||||||

|

Total assets

|

$ | 49,581,018 | $ | 42,309,473 | ||||

|

LIABILITIES

|

||||||||

|

Current liabilities:

|

||||||||

|

Accounts payable

|

$ | 5,678,910 | $ | 3,546,139 | ||||

|

Other accrued liabilities

|

3,538,649 | 3,257,062 | ||||||

|

Total current liabilities

|

9,217,559 | 6,803,201 | ||||||

|

Long-term debt

|

13,522,000 | 9,154,000 | ||||||

|

Other accrued liabilities - non current

|

1,489,648 | 1,811,022 | ||||||

|

Total liabilities

|

24,229,207 | 17,768,223 | ||||||

|

STOCKHOLDERS' EQUITY

|

||||||||

|

Common stock, par value $2.50: authorized 8,000,000

|

||||||||

| shares; issued - 4,374,574 shares in 2010 and 4,313,024 | ||||||||

|

shares in 2009, including treasury stock

|

10,935,676 | 10,782,555 | ||||||

|

Treasury stock, at cost, 1,305,237 shares in 2010

|

||||||||

|

and 1,155,165 shares in 2009

|

(11,710,616 | ) | (10,144,325 | ) | ||||

|

Additional paid-in capital

|

4,603,194 | 4,208,112 | ||||||

|

Accumulated other comprehensive loss

|

(875,157 | ) | (812,970 | ) | ||||

|

Retained earnings

|

22,398,714 | 20,507,878 | ||||||

|

Total stockholders' equity

|

25,351,811 | 24,541,250 | ||||||

|

Total liabilities and stockholders' equity

|

$ | 49,581,018 | $ | 42,309,473 | ||||

|

See accompanying Notes to Consolidated Financial Statements.

|

||||||||

18

|

Acme United Corporation and Subsidiaries

|

||||||||||||||||||||||||||||

|

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY

|

||||||||||||||||||||||||||||

|

Outstanding Shares of Common Stock

|

Common Stock

|

Treasury Stock

|

Additional Paid-In Capital

|

Accumulated Other Comprehensive Income (Loss)

|

Retained Earnings

|

Total

|

||||||||||||||||||||||

|

Balances, December 31, 2008

|

3,343,368 | 10,732,555 | (8,406,722 | ) | 3,906,000 | (1,663,361 | ) | 18,319,191 | 22,887,663 | |||||||||||||||||||

|

Net income

|

2,842,087 | 2,842,087 | ||||||||||||||||||||||||||

|

Translation adjustment

|

709,421 | 709,421 | ||||||||||||||||||||||||||

|

Change in pension plan

|

||||||||||||||||||||||||||||

|

net prior service credit and

|

||||||||||||||||||||||||||||

|

actuarial losses, net of tax

|

||||||||||||||||||||||||||||

|

of $82,218

|

140,970 | 140,970 | ||||||||||||||||||||||||||

|

Comprehensive income

|

3,692,478 | |||||||||||||||||||||||||||

|

Stock compensation expense

|

308,337 | 308,337 | ||||||||||||||||||||||||||

|

Distribution to shareholders

|

(653,400 | ) | (653,400 | ) | ||||||||||||||||||||||||

|

Issuance of common stock

|

20,000 | 50,000 | (6,225 | ) | 43,775 | |||||||||||||||||||||||

|

Purchase of treasury stock

|

(205,509 | ) | (1,737,603 | ) | (1,737,603 | ) | ||||||||||||||||||||||

|

Balances, December 31, 2009

|

3,157,859 | $ | 10,782,555 | $ | (10,144,325 | ) | $ | 4,208,112 | $ | (812,970 | ) | $ | 20,507,878 | $ | 24,541,250 | |||||||||||||

|

Net income

|

2,572,964 | 2,572,964 | ||||||||||||||||||||||||||

|

Translation adjustment

|

(40,237 | ) | (40,237 | ) | ||||||||||||||||||||||||

|

Change in pension plan

|

||||||||||||||||||||||||||||

|

net prior service credit and

|

||||||||||||||||||||||||||||

|

actuarial losses, net of tax

|

||||||||||||||||||||||||||||

|

of $35,049

|

(21,950 | ) | (21,950 | ) | ||||||||||||||||||||||||

|

Comprehensive income

|

2,510,777 | |||||||||||||||||||||||||||

|

Stock compensation expense

|

385,732 | 385,732 | ||||||||||||||||||||||||||

|

Distribution to shareholders

|

(682,128 | ) | (682,128 | ) | ||||||||||||||||||||||||

|

Issuance of common stock

|

61,550 | 153,121 | 9,350 | 162,471 | ||||||||||||||||||||||||

|

Purchase of treasury stock

|

(150,072 | ) | (1,566,290 | ) | (1,566,290 | ) | ||||||||||||||||||||||

|

Balances, December 31, 2010

|

3,069,337 | 10,935,676 | (11,710,616 | ) | 4,603,194 | (875,157 | ) | 22,398,714 | $ | 25,351,811 | ||||||||||||||||||

|

See accompanying Notes to Consolidated Financial Statements.

|

||||||||||||||||||||||||||||

19

|

Acme United Corporation and Subsidiaries

|

||||||||

|

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

||||||||

|

For the years ended December 31,

|

||||||||

|

2010

|

2009

|

|||||||

|

Operating activities:

|

||||||||

|

Net income

|

$ | 2,572,964 | $ | 2,842,087 | ||||

|

Adjustments to reconcile net income to net

|

||||||||

|

cash (used) provided by operating activities

|

||||||||

|

Depreciation

|

755,334 | 803,902 | ||||||

|

Amortization

|

114,822 | 113,987 | ||||||

|

Stock compensation expense

|

385,732 | 308,337 | ||||||

|

Deferred income taxes

|

(348,713 | ) | (280,188 | ) | ||||

|

Change in estimated cost of environmental remediation

|

(100,000 | ) | (457,379 | ) | ||||

|

Changes in operating assets and liabilities

|

||||||||

|

Accounts receivable

|

(1,635,185 | ) | 49,438 | |||||

|

Inventories

|

(5,015,837 | ) | 4,668,500 | |||||

|

Prepaid expenses and other current assets

|

(137,266 | ) | 43,310 | |||||

|

Accounts payable

|

2,208,634 | (149,341 | ) | |||||

|

Other accrued liabilities

|

64,430 | (1,361,210 | ) | |||||

|

Total adjustments

|

(3,708,048 | ) | 3,739,356 | |||||

|

Net cash (used) provided by operating activities

|

(1,135,084 | ) | 6,581,443 | |||||

|

Investing activities:

|

||||||||

|

Purchase of property, plant and equipment

|

(937,083 | ) | (566,939 | ) | ||||

|

Purchase of patents and trademarks

|

(117,405 | ) | (132,244 | ) | ||||

|

Net cash used by investing activities

|

(1,054,488 | ) | (699,183 | ) | ||||

|

Financing activities:

|

||||||||

|

Net borrowings (repayments) of long-term debt

|

4,368,000 | (2,565,000 | ) | |||||

|

Distributions to shareholders

|

(655,832 | ) | (662,547 | ) | ||||

|

Purchase of treasury stock

|

(1,566,290 | ) | (1,737,603 | ) | ||||

|

Issuance of common stock

|

162,475 | 43,775 | ||||||

|

Net cash provided (used) by financing activities

|

2,308,353 | (4,921,375 | ) | |||||

|

Effect of exchange rate changes

|

(36,429 | ) | 333,616 | |||||

|

Net increase in cash and cash equivalents

|

82,351 | 1,294,501 | ||||||

|

Cash and cash equivalents at beginning of year

|

6,519,065 | 5,224,564 | ||||||

|

Cash and cash equivalents at end of year

|

$ | 6,601,416 | $ | 6,519,065 | ||||

|

Supplemental cash flow information

|

||||||||

|

Cash paid for income taxes

|

$ | 464,576 | $ | 1,334,358 | ||||

|

Cash paid for interest expense

|

$ | 278,165 | $ | 165,092 | ||||

See accompanying Notes to Consolidated Financial Statements.

20

Acme United Corporation and Subsidiaries

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Operations

The operations of Acme United Corporation (the “Company”) consist of three reportable segments. The operations of the Company are structured and evaluated based on geographic location. The three reportable segments operate in the United States (including Asian operations), Canada and Germany. Principal products across all segments are scissors, shears, knives, rulers, pencil sharpeners, first aid kits, and related products which are sold primarily to wholesale, contract and retail stationery distributors, office supply super stores, school supply distributors, drug store retailers, industrial distributors, wholesale florists, mass market retailers and hardware chains.

2. Accounting Policies

Estimates - The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. The most sensitive and significant accounting estimates relate to customer rebates, valuation allowances for deferred income tax assets, obsolete and slow-moving inventories, potentially uncollectible accounts receivable and accruals for income taxes. Actual results could differ from those estimates.

Principles of Consolidation - The consolidated financial statements include the accounts of the Company and its subsidiaries, all of which are wholly owned by the Company. All significant intercompany accounts and transactions are eliminated in consolidation.

Translation of Foreign Currency - For foreign operations, assets and liabilities are translated at rates in effect at the end of the year; revenues and expenses are translated at average rates in effect during the year. Resulting translation adjustments are made directly to accumulated other comprehensive loss. Foreign currency transaction gains and losses are recognized in operating results. Foreign currency transaction losses, which are included in other income, net, were $58,992 in 2010 and $35,519 in 2009.

Cash Equivalents - Investments with an original maturity of three months or less, as well as time deposits and certificates of deposit that are readily redeemable, at the date of purchase are considered cash equivalents. Included with the cash and equivalents are Certificates of Deposit totaling $3.0 million.

Accounts Receivable - Accounts receivable are shown less an allowance for doubtful accounts of $57,125 in 2010 and $71,629 in 2009.

Inventories - Inventories are stated at the lower of cost, determined by the first-in, first-out method, or market.

Property, Plant and Equipment and Depreciation – Property, plant and equipment is recorded at cost. Depreciation is computed by the straight-line method over the estimated useful lives of the assets, which range from 3 to 30 years.

Intangible Assets– Intangible assets with finite useful lives are recorded at cost upon acquisition, and amortized over the term of the related contract or useful life, as applicable. Intangible assets held by the Company with finite useful lives include patents and trademarks. Patents and trademarks are amortized over their estimated useful lives. The weighted average amortization period for intangible assets at December 31, 2010 was 14 years. The Company periodically reviews the values recorded for intangible assets to assess recoverability from future operations whenever events or changes in circumstances indicate that their carrying amounts may not be recoverable. At December 31, 2010 and 2009, the Company assessed the recoverability of its long-lived assets and believed that there were no events or circumstances present that would that would require a test of recoverability on those assets. As a result, there was no impairment of the carrying amounts of such assets and no reduction in their estimated useful lives.

21

Deferred Income Taxes - Deferred income taxes are provided for the differences between the financial statement and tax bases of assets and liabilities, and on operating loss carryovers, using tax rates in effect in years in which the differences are expected to reverse.

Revenue Recognition – The Company recognizes revenue from the sales of its products when ownership transfers to the customers, which occurs either at the time of shipment or upon delivery based upon contractual terms with the customer. The Company recognizes customer program costs, including rebates, cooperative advertising, slotting fees and other sales related discounts, as a reduction to sales.

Research and Development – Research and development costs ($486,778 in 2010 and $440,378 in 2009) are expensed as incurred.

Shipping Costs – The costs of shipping product to our customers ($2,656,653 in 2010 and $2,529,743 in 2009) are included in selling, general and administrative expenses.

Advertising Costs – The Company expenses the production costs of advertising the first time that the related advertising takes place. Advertising costs ($1,039,302 in 2010 and $1,066,860 in 2009) are included in selling, general and administrative expenses.

Subsequent events - The Company has evaluated events and transactions subsequent to December 31, 2010 through the date our consolidated financial statements were included in this Form 10-K and filed with the SEC.

Concentrations – The Company performs ongoing credit evaluations of its customers and generally does not require collateral for the extension of credit. Allowances for credit losses are provided and have been within management's expectations. In 2010, with respect to concentration risk related to accounts receivable, the Company had one customer that accounted for greater than 10% of total net receivables. In 2010 and 2009, the Company had one customer that individually exceeded 10% of consolidated net sales. Net sales to this customer amounted to approximately 21% in 2010 and 20% in 2009.

|

3. Inventories

|

||||||||

|

Inventories consisted of:

|

2010

|

2009

|

||||||

|

Finished goods

|

$ | 21,108,954 | $ | 16,337,034 | ||||

|

Work in process

|

171,673 | 97,297 | ||||||

|

Materials and supplies

|

1,012,282 | 965,939 | ||||||

| $ | 22,292,909 | $ | 17,400,270 | |||||

Inventories are stated net of valuation allowances for slow moving and obsolete inventory of $470,749 as of December 31, 2010 and $421,685 as of December 31, 2009.

|

4. Intangible Assets

|

||||||||

|

Intangible assets consisted of:

|

2010

|

2009

|

||||||

|

Patents

|

$ | 1,794,754 | $ | 1,695,881 | ||||

|

Trademarks

|

554,590 | 534,058 | ||||||

| 2,349,344 | 2,229,939 | |||||||

|

Accumulated amortization

|

483,113 | 366,291 | ||||||

| $ | 1,866,231 | $ | 1,863,648 | |||||

Amortization expense for patents and trademarks for the years ended December 31, 2010, and 2009 were $114,822 and $113,987, respectively. The estimated aggregate amortization expense for each of the next five succeeding years, calculated on a similar basis, is as follows: 2011 - $118,190; 2012 - $116,733; 2013 - $116,594; 2014 - $103,365; and 2015 - $90,656.

22

|

5. Other Accrued Liabilities

|

||||||||

|

Other current and long-term accrued liabilities consisted of:

|

||||||||

|

2010

|

2009

|

|||||||

|

Customer rebates

|

$ | 2,436,993 | $ | 2,489,410 | ||||

|

Remediation liability

|

343,539 | 681,444 | ||||||

|

Pension liability

|

1,164,217 | 1,308,655 | ||||||

|

Other

|

1,083,548 | 588,575 | ||||||

| $ | 5,028,297 | $ | 5,068,084 | |||||

6. Pension and Profit Sharing

United States employees, hired prior to July 1, 1993, are covered by a funded, defined benefit pension plan. The benefits of this pension plan are based on years of service and the average compensation of the highest three consecutive years during the last ten years of employment. In December 1995, the Company's Board of Directors approved an amendment to the United States pension plan that terminated all future benefit accruals as of February 1, 1996, without terminating the pension plan.

The Company’s funding policy with respect to its qualified plan is to contribute at least the minimum amount required by applicable laws and regulations. In 2010, the Company contributed $265,000 to the plan and expects to contribute approximately $300,000 during 2011.

The plan asset weighted average allocation at December 31, 2010 and December 31, 2009, by asset category, were as follows:

|

Asset Category

|

2010

|

2009

|

|

Equity Securities

|

68%

|

70%

|

|

Fixed Income Securities

|

30%

|

30%

|

|

Other Securities / Investments

|

2%

|

0%

|

|

Total

|

100%

|

100%

|

The Company’s investment policy for the pension plan is to minimize risk by balancing investments between equity securities and fixed income securities, utilizing a weighted average approach of 65% equity securities, 30% fixed income securities, and 5% cash investments. Plan funds are invested in long-term obligations with a history of moderate to low risk.

As of each December 31, 2010 and 2009, equity securities in the pension plan included 10,000 shares of the Company's Common Stock, having a market value of $95,200 and $91,993, respectively.

The pension plan asset information included below is presented at fair value. ASC 820 establishes a framework for measuring fair value and requires disclosures about assets and liabilities measured at fair value. The fair value hierarchy prioritizes the inputs to valuation techniques used to measure fair value into three levels as follows:

|

·

|

Level 1 – Inputs to the valuation methodology based on unadjusted quoted market prices in active markets that are accessible at the measurement date.

|

|

·

|

Level 2 – Inputs to the valuation methodology that include quoted market prices that are not considered to be active or financial instruments for which all significant inputs are observable, either directly or indirectly.

|

|

·

|

Level 3 – Inputs to the valuation methodology are unobservable and significant to the fair value measurement.

|

The following table presents the pension plan assets by level within the fair value hierarchy as of December 31, 2010.

23

|

Level 1

|

Level 2

|

Level 3

|

Total

|

|||||||||||||

|

Money Market Fund

|

$ | 36,002 | $ | - | $ | - | $ | 36,002 | ||||||||

|

Acme United Common Stock

|

95,200 | - | - | 95,200 | ||||||||||||

|

Equity Common and Collected Funds

|

- | 795,384 | - | 795,384 | ||||||||||||

|

Fixed Income Common and Collected Funds

|

- | 388,842 | - | 388,842 | ||||||||||||

|

Total

|

$ | 131,202 | $ | 1,184,226 | $ | - | $ | 1,315,428 | ||||||||

|

Other disclosures related to the pension plan follow:

|

||||||||

|

2010

|

2009

|

|||||||

|

Assumptions used to determine benefit obligation:

|

||||||||

|

Discount rate

|

4.42 | % | 5.06 | % | ||||

|

Changes in benefit obligation:

|

||||||||

|

Benefit obligation at beginning of year

|

$ | (2,555,196 | ) | $ | (2,641,926 | ) | ||

|

Interest cost

|

(122,416 | ) | (151,990 | ) | ||||

|

Service cost

|

(25,000 | ) | (25,000 | ) | ||||

|

Amendment

|

- | - | ||||||

|

Actuarial loss

|

(117,417 | ) | (99,923 | ) | ||||

|

Benefits and plan expenses paid

|

340,384 | 363,643 | ||||||

|

Benefit obligation at end of year

|

(2,479,645 | ) | (2,555,196 | ) | ||||

|

Changes in plan assets:

|

||||||||

|

Fair value of plan assets at beginning of year

|

1,246,541 | 1,261,036 | ||||||

|

Actual return on plan assets

|

144,274 | 241,408 | ||||||

|

Employer contribution

|

264,997 | 107,740 | ||||||

|

Benefits and plan expenses paid

|

(340,384 | ) | (363,643 | ) | ||||

|

Fair value of plan assets at end of year

|

1,315,428 | 1,246,541 | ||||||

|

Funded status

|

$ | (1,164,217 | ) | $ | (1,308,655 | ) | ||

|

Accrued benefits costs are included in other accrued liabilities (non-current).

|

||||||||

| 2010 | 2009 | |||||||

|

Assumptions used to determine net periodic benefit cost:

|

||||||||

|

Discount rate

|

5.06 | % | 6.19 | % | ||||

|

Expected return on plan assets

|

8.25 | % | 8.25 | % | ||||

|

Components of net benefit expense:

|

||||||||

|

Interest cost

|

$ | 122,416 | $ | 151,990 | ||||

|

Service cost

|

25,000 | 25,000 | ||||||

|

Expected return on plan assets

|

(95,422 | ) | (94,951 | ) | ||||

|

Amortization of prior service costs

|

9,154 | 9,154 | ||||||

|

Amortization of actuarial loss

|

154,555 | 167,500 | ||||||

|

Net periodic benefit cost

|

$ | 215,703 | $ | 258,693 | ||||

24

The Company employs a building block approach in determining the long-term rate of return for plan assets. Historical markets are studied and long-term historical relationships between equity securities and fixed income securities are preserved consistent with the widely-accepted capital market principle that assets with higher volatility generate higher returns over the long run. Our expected 8.25% long-term rate of return on plan assets is determined based on long-term historical performance of plan assets, current asset allocation and projected long-term rates of return.

The following table discloses the change recorded in other comprehensive income related to benefit costs:

|

2010

|

2009

|

|||||||

|

Balance at beginning of the year

|

$ | 1,925,609 | $ | 2,148,797 | ||||

|

Change in net loss

|