Attached files

| file | filename |

|---|---|

| 8-K - KAMAN CORPORATION FORM 8-K DATED 3-10-11 - KAMAN Corp | form8-k.htm |

Kaman Corporation (NASDAQ-GS: KAMN)

Kaman Corporation (NASDAQ-GS: KAMN)

Investor Presentation

March 10, 2011

2

Investment Summary

§ Significant long-term organic growth opportunities in Aerospace

and Industrial Distribution

and Industrial Distribution

§ High margin Aerospace business anchored by market leading

position in specialty bearings

position in specialty bearings

§ Military platforms in Aerospace provide recurring revenue stream

§ Industrial Distribution business benefiting from industrial sector

momentum and gaining scale via recent acquisitions

momentum and gaining scale via recent acquisitions

§ Investing in new product development, new product applications,

acquisitions and technology for long-term growth

acquisitions and technology for long-term growth

§ Strong balance sheet to drive growth and strategic initiatives

§ Experienced management team

3

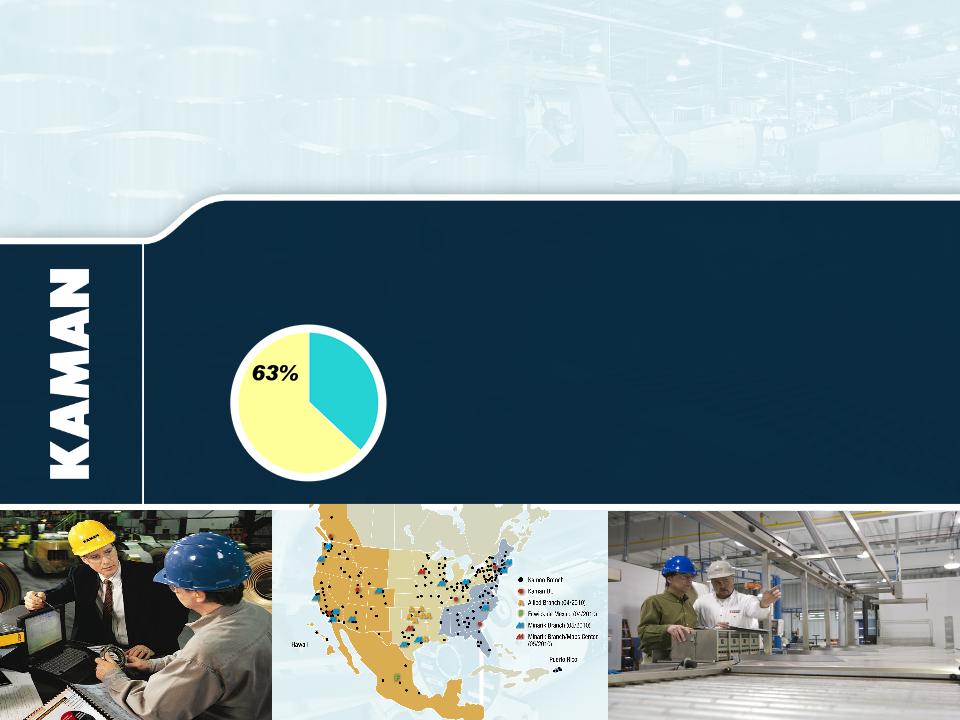

Distribution

63%

Aerospace

37%

2010 Sales

§ Kaman Corporation is a diversified company that conducts

business in the aerospace and industrial distribution markets

business in the aerospace and industrial distribution markets

§ The Company has two segments

– Industrial Distribution

• Third largest distributor in the power transmission / motion

control market

control market

• Distributes over four million SKUs to over 50K customers

via 207 branches

– Aerospace

• Manufacturer and subcontractor in the global commercial

and military aerospace and defense market

and military aerospace and defense market

• Diverse customer base of government divisions and blue

chip customers

chip customers

§ Publicly listed on NASDAQ with a market capitalization of

$843 million as of March 8, 2011

$843 million as of March 8, 2011

§ 2010 Sales $1.3 billion; 4,300 Employees

Corporate Overview

(1) Operating profit after depreciation and before interest and corporate charges

Distribution

31%

Aerospace

69%

2010 Segment

Operating Income (1)

4

|

|

2009

|

2010

|

Change

|

|

Sales

|

$ 1,146

|

$ 1,319

|

+15.0%

|

|

Earnings per share

|

$ 1.27

|

$ 1.59(2)

|

+25.2%

|

|

Free cash flow

|

$ 56.9

|

$ 15.8(1)

|

-72.2%

|

|

Market capitalization

|

$ 594.9

|

$ 756.6

|

+27.2%

|

|

Price per share

|

$ 23.09

|

$ 29.07

|

+25.9%

|

(In millions except per share amounts)

(1) Includes a $25 million voluntary pension plan contribution

(2) Adjusted - excludes $6.4 million goodwill impairment charge, $2.0 million aerospace

contract settlement and $6.6 million look-back interest benefit

Key Metrics

5

§ Acquisitions and expansions

– Industrial Distribution

• Acquired Minarik Corporation of Glendale, CA, a national

distributor of motion control and automation products

distributor of motion control and automation products

• Acquired Allied Bearings Supply Company of Tulsa, OK

• Acquired the assets of Fawick de Mexico, S.A. de C. V. of Mexico

City, Mexico

City, Mexico

– Aerospace

• Acquired Global Aerosystems, LLC, a provider of aerostructure

engineering design analysis and FAA certification services to the

aerospace industry

engineering design analysis and FAA certification services to the

aerospace industry

• Opened a new, state of the art manufacturing facility in

Chihuahua, Mexico

Chihuahua, Mexico

Recent Significant Events

6

Recent Significant Events

§ Contract Awards

– During 2010 awarded purchase orders for JPF fuzes totaling $126

million

million

– Awarded a contract with a potential value in excess of $60 million to

manufacture cabins for the AH-1Z attack helicopter

manufacture cabins for the AH-1Z attack helicopter

– Awarded a contract from Bombardier to manufacture composite

doors for the Learjet 85 business jet

doors for the Learjet 85 business jet

– Team K-MAX awarded a $45.8 million contract for the evaluation of

unmanned aircraft systems for the USMC

unmanned aircraft systems for the USMC

§ Financing

– Completed new four-year $275 million revolving credit facility

– Completed $115 million offering of 3.25% convertible senior notes

due 2017

due 2017

– S&P reaffirmed Kaman’s BBB- investment grade credit rating

7

AEROSPACE

2010 Sales $487 Million

8

Aerospace

OBJECTIVE:

§ $1 billion in sales - “high teens” operating profit margin by 2014

STRATEGY:

§ GROWTH - Increased capabilities through both internal development

and acquisitions to win major OEM and Tier 1 programs

and acquisitions to win major OEM and Tier 1 programs

§ BALANCE - Expand commercial content via growth initiatives to

achieve a better balance of aerospace revenues

achieve a better balance of aerospace revenues

§ PROFITABILITY - Expand engineering capability to provide

differentiation and improved margins

differentiation and improved margins

9

Aerospace Sales

Business/

Regional

3%

Military

72%

Commercial

25%

Based on 2010 Sales

10

Fixed trailing edge

Fuel tank access doors

Top covers

Red denotes bearing products

Nose landing gear

Rudder

Main landing gear

Flaps

Horizontal stabilizer

Door assemblies

Engine/thrust reverser

Aircraft Programs/Capabilities

Flight controls

Doors

11

Manufacture of cockpit

Blade erosion coating

Manufacture and assembly

of tail rotor pylon

of tail rotor pylon

Manufacture, sub assembly

and joining of fuselage

and joining of fuselage

Blade manufacture,

repair and overhaul

repair and overhaul

Driveline couplings

Bushings

Flight control bearings

Aircraft Programs/Capabilities

Red denotes bearing products

12

Aerospace - Budget Impact on Military Programs

§ Backlog is comprised largely of programs that are unaffected by the

proposed budget cuts

proposed budget cuts

– UH-60 BLACK HAWK Program

– Joint Programmable Fuze

– Joint Strike Fighter

– A-10

– AH-1Z

§ C-17 has a firm backlog into 2013

§ Canceled programs had minimal overall impact to the company

– Nuclear ballistic missiles

– Naval surface ships

– F-22

– Future Combat System

13

Strong Base Business

§ BLACK HAWK

§ Joint Programmable Fuze (JPF)

§ C-17

14

Growth Programs

§ A-10 re-wing

§ Boeing 787

§ F-35 (Joint Strike Fighter)

§ Airbus A380

§ Bell Helicopter - AH-1Z/Commercial

§ Unmanned K-MAX®

§ Learjet 85

15

§ Teamed with Lockheed Martin to

develop an unmanned military

version of the Kaman K-MAX

commercial helicopter

develop an unmanned military

version of the Kaman K-MAX

commercial helicopter

§ Lockheed Martin / Kaman team

awarded a $45.8 million contract

for the evaluation of unmanned

aircraft systems by the USMC

awarded a $45.8 million contract

for the evaluation of unmanned

aircraft systems by the USMC

Contract Award - Unmanned K-MAX®

16

New Program - Bell Helicopter AH-1Z

§ Latest version of the AH-1 attack

helicopter for the USMC

helicopter for the USMC

§ Leverages capabilities of the

Aerospace Group

Aerospace Group

– New cabins will be

manufactured in Jacksonville

facility

manufactured in Jacksonville

facility

– Tooling will be designed and

built by UK tooling division

built by UK tooling division

§ Initial period of performance

runs through 2015

runs through 2015

§ Program value could exceed $60

million

million

17

§ LJ85 mid-size eight passenger

business jet

business jet

§ Kaman will manufacture:

– Passenger door composite

assembly

assembly

– Stair assembly

– Over wing emergency exit door

§ First significant award from

Bombardier for aerostructures

Bombardier for aerostructures

New Program - Learjet 85

18

19

UP

24%

$533 Million

at 12/31/10

$431 Million

at 12/31/09

Backlog

20

INDUSTRIAL DISTRIBUTION

2010 Sales $832 Million

21

§ Third largest industrial distribution firm serving $15 billion of the $23

billion power transmission / motion control market.

billion power transmission / motion control market.

§ 207 branches and 5 distribution centers

§ Major product categories:

– Bearings

– Mechanical and electrical power transmission

– Fluid Power

– Motion control

– Automation

– Material handling

§ Metrics:

– $470,000 sales per employee (2010)

– 2,000 employees (approximately one third outside sales)

– 4.0 million SKUs

– 50,000+ customers

Industrial Distribution Overview

22

Industrial Distribution

OBJECTIVE:

§ $1.5 billion in sales - 7% operating profit margin by 2014

STRATEGY:

§ GROWTH - Broaden product offering organically and through

acquisitions. Expand geographic footprint to enhance position in the

national accounts market

acquisitions. Expand geographic footprint to enhance position in the

national accounts market

§ PRODUCTIVITY - Execute organizational realignment and implement

multi-faceted technology investments

multi-faceted technology investments

§ PROFITABILITY - Recognize sales and cost synergies from the three

acquisitions completed in 2010. Enhance margins through new higher

margin product lines, a focus on pricing management and leverage

increased purchasing scale

acquisitions completed in 2010. Enhance margins through new higher

margin product lines, a focus on pricing management and leverage

increased purchasing scale

23

Executing Strategy and Building Network

24

§ Strong organic growth

– Q410 up 23.0%, Q310 up 17.1%, Q210 up 17.5%

– OEM markets extremely strong

– MRO markets turned positive in Q2

– Broad based growth across geographies and end markets

– January and February 2011 daily sales were above comparable fourth

quarter 2010 levels

quarter 2010 levels

Positive Sector Fundamentals Contributing

to Growth

to Growth

25

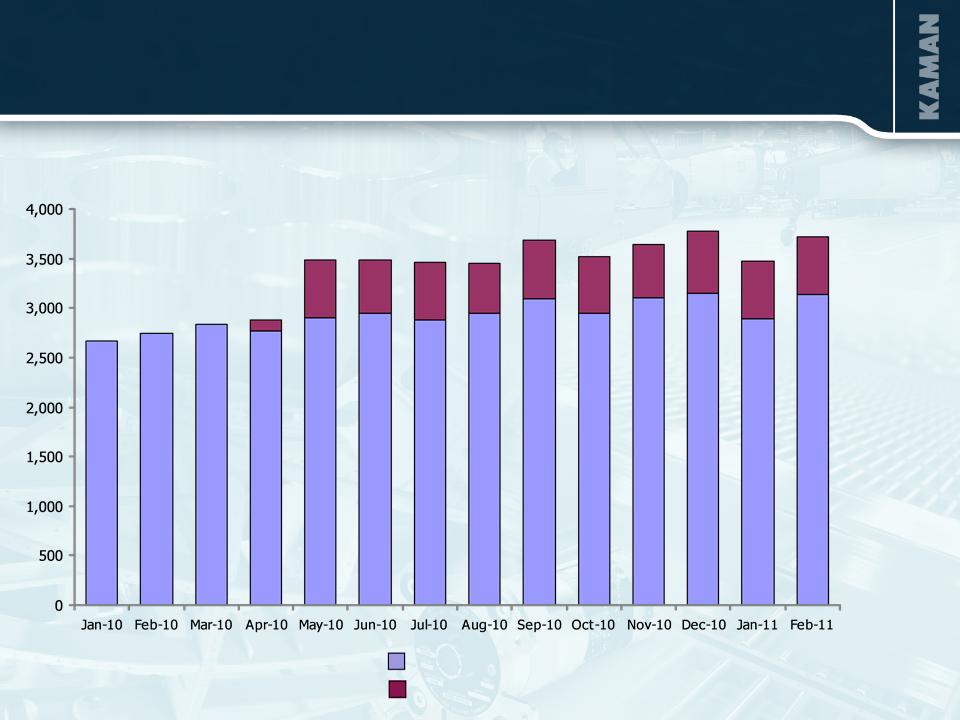

Industrial Distribution

Organic Sales Per Day vs. Prior Year

Organic Sales Per Day vs. Prior Year

26

§ Strong organic growth

– Q410 up 23.0%, Q310 up 17.1%, Q210 up 17.5%

– OEM markets extremely strong

– MRO markets turned positive in Q2

– Broad based growth across geographies and end markets

§ Acquisitions accelerating top line and building scale

– Added geographic coverage, product line expansions, strong franchises

– Acquisitions added $96.2 million in sales in 2010

– Minarik and Allied were accretive in 2010

Acquisitions Contributing to Growth

27

Industrial Distribution

Sales Per Day

Sales Per Day

2,670

2,744

2,839

2,880

3,481

3,490

3,457

3,454

3,685

3,518

3,636

3,771

3,469

3,718

Organic

Acquisition

28

Industrial Distribution Opportunities

§ Broaden product offering organically and through acquisition to win

additional business from existing customers and gain market share

additional business from existing customers and gain market share

§ Enhance margins through new higher margin product lines, a focus

on pricing management and leverage from higher sales

on pricing management and leverage from higher sales

§ Recognize sales and cost synergies from the three acquisitions

completed in 2010

completed in 2010

§ Expand geographic footprint through additional acquisitions to

enhance Kaman’s position in the competition for national accounts

enhance Kaman’s position in the competition for national accounts

§ Improve productivity through technology investments to enhance

return on sales

return on sales

29

Kaman Investment Merits

§ A Leading Market Position in Both Business Segments

§ Two Distinct Markets Balance Overall Company Performance

§ Continued Focus on Profit Optimization, Increasing Cash

Flows and Strengthening Competitive Position

Flows and Strengthening Competitive Position

§ Strong Liquidity and Conservative Financial Profile

§ Disciplined and Focused Acquisition Strategy

§ Experienced Management Team

30

FINANCIAL SUMMARY

37%

2010 Sales $1.32 Billion

31

(1)Adjusted - excludes $6.4 million goodwill impairment, $2.0 million aerospace contract settlement and

$6.6 look-back interest benefit

Financial Highlights - Full Year

32

(1)Adjusted - excludes $6.4 million goodwill impairment

Financial Highlights - Q4 2010

33

|

(In Millions)

|

As of 12/31/10

|

As of 12/31/09

|

As of 12/31/08

|

|

Cash and Cash Equivalents

|

$ 32.2

|

$ 18.0

|

$ 8.2

|

|

Notes Payable and Long-term Debt

|

$ 148.4

|

$ 63.6

|

94.2

|

|

Shareholders’ Equity

|

$ 362.7

|

$ 312.9

|

$ 274.3

|

|

Debt as % of Total Capitalization

|

29.0%

|

16.9%

|

25.6%

|

|

Capital Expenditures

|

$ 21.5

|

$ 13.6

|

$ 16.0

|

|

Depreciation & Amortization

|

$ 20.5

|

$ 16.1

|

$ 12.8

|

Balance Sheet and Capital Factors

34

APPENDIX

35

Industrial Distribution Acquisitions

3 Acquisitions Completed in 2010:

§ Minarik (April 30, 2010)

– Only national distributor of motion control & automation products

– 2009 sales: $84 million; Purchase price: $42.5 million

– Expands geographic coverage in 3 of the top 15 markets where Kaman has not been

well represented (e.g. San Jose, Cleveland, Chicago)

well represented (e.g. San Jose, Cleveland, Chicago)

– Diversifies traditional MRO customer base through primary OEM presence

– Expands product offering; positions Kaman as a leader in motion control &

automation

automation

§ Allied Bearings Supply (April 5, 2010)

– Distributor of bearings, power transmission, material handling, and industrial supplies

– 2009 sales: $22 million; Purchase price: $15 million

– Expands Kaman’s coverage in Oklahoma, Arkansas and Texas

– Adds volume in core product lines and provides access to chemical and petro-

chemical industries and oil and gas industries

chemical industries and oil and gas industries

§ Fawick de Mexico (February 26, 2010)

– Mexico City based fluid power distributor with coverage throughout most of Mexico

– 2009 sales: ~$4 million (USD); Purchase price: ~$5.0 million (USD)

36

Industrial Distribution

Improving Productivity Illustration

§ Ft. Wayne Processing Center

§ Processes accounts payable and accounts receivable transactions -

more than 1.4 million documents annually

more than 1.4 million documents annually

§ Disburses more than $600 million annually

§ Applies more than $700 million in cash collections annually

§ From 2007 to 2010 utilizing process improvements and new

technology improved productivity per employee 32% on a 19%

reduction in headcount

technology improved productivity per employee 32% on a 19%

reduction in headcount

37

Kamatics Lean Journey

§ Bloomfield Kamatics facility has successfully

implemented lean manufacturing processes

implemented lean manufacturing processes

§ Since introducing lean in 2000 Kamatics has:

– Doubled sales

– Increased return on identifiable assets by more than

5,400 basis points

5,400 basis points

– Kept headcount constant

– Doubled sales per employee

– Increased on-time deliveries to more than 90% from

less than 50%

less than 50%

– Developed industry leading lead-times of 4-8 weeks

from 12-18 weeks

from 12-18 weeks

38

Aerospace Awards

§ UTC Supplier Gold at Kamatics

§ Top 100 Supplier to Sikorsky

– Kamatics

– Aerostructures - Jacksonville

§ Aviation Week - Top Performing Companies

– 2009 Five-Year Most Improved

39

Pension Plan Funded Status

§ During 2010 Kaman took numerous actions to address the

company’s unfunded pension liability including:

company’s unfunded pension liability including:

– Executed comprehensive pension plan redesign

– Successfully implemented Liability Driven Investment strategy

– Made $25 million voluntary contribution in December 2010

• Funded with convertible bond proceeds

40

Forward Looking Statement

This presentation contains forward-looking information relating to the company's business and prospects, including the Aerospace and

Industrial Distribution businesses, operating cash flow, and other matters that involve a number of uncertainties that may cause actual results

to differ materially from expectations. Those uncertainties include, but are not limited to: 1) the successful conclusion of competitions for

government programs and thereafter contract negotiations with government authorities, both foreign and domestic; 2) political conditions in

countries where the company does or intends to do business; 3) standard government contract provisions permitting renegotiation of terms

and termination for the convenience of the government; 4) domestic and foreign economic and competitive conditions in markets served by

the company, particularly the defense, commercial aviation and industrial production markets; 5) risks associated with successful

implementation and ramp up of significant new programs; 6) potential difficulties associated with variable acceptance test results, given

sensitive production materials and extreme test parameters; 7) management's success in increasing the volume of profitable work at

the Wichita facility; 8) successful resale of the SH-2G(I) aircraft, equipment and spare parts; 9) receipt and successful execution of production

orders for the JPF U.S. government contract, including the exercise of all contract options and receipt of orders from allied militaries, as all

have been assumed in connection with goodwill impairment evaluations; 10) satisfactory resolution of the company’s litigation relating to the

FMU-143 program; 11) continued support of the existing K-MAX® helicopter fleet, including sale of existing K-MAX® spare parts inventory;

12) cost estimates associated with environmental remediation activities at the Bloomfield, Moosup and New Hartford, CT facilities and our U.K.

facilities; 13) profitable integration of acquired businesses into the company's operations; 14) changes in supplier sales or vendor incentive

policies; 15) the effects of price increases or decreases; 16) the effects of pension regulations, pension plan assumptions and future

contributions; 17) future levels of indebtedness and capital expenditures; 18) continued availability of raw materials and other commodities in

adequate supplies and the effect of increased costs for such items; 19) the effects of currency exchange rates and foreign competition on

future operations; 20) changes in laws and regulations, taxes, interest rates, inflation rates and general business conditions; 21) future

repurchases and/or issuances of common stock; and 22) other risks and uncertainties set forth in the company's annual, quarterly and current

releases, proxy statements and other filings with the U.S. Securities and Exchange Commission. Any forward-looking information provided in

this presentation should be considered with these factors in mind. The company assumes no obligation to update any forward-looking

statements contained in this presentation.

Industrial Distribution businesses, operating cash flow, and other matters that involve a number of uncertainties that may cause actual results

to differ materially from expectations. Those uncertainties include, but are not limited to: 1) the successful conclusion of competitions for

government programs and thereafter contract negotiations with government authorities, both foreign and domestic; 2) political conditions in

countries where the company does or intends to do business; 3) standard government contract provisions permitting renegotiation of terms

and termination for the convenience of the government; 4) domestic and foreign economic and competitive conditions in markets served by

the company, particularly the defense, commercial aviation and industrial production markets; 5) risks associated with successful

implementation and ramp up of significant new programs; 6) potential difficulties associated with variable acceptance test results, given

sensitive production materials and extreme test parameters; 7) management's success in increasing the volume of profitable work at

the Wichita facility; 8) successful resale of the SH-2G(I) aircraft, equipment and spare parts; 9) receipt and successful execution of production

orders for the JPF U.S. government contract, including the exercise of all contract options and receipt of orders from allied militaries, as all

have been assumed in connection with goodwill impairment evaluations; 10) satisfactory resolution of the company’s litigation relating to the

FMU-143 program; 11) continued support of the existing K-MAX® helicopter fleet, including sale of existing K-MAX® spare parts inventory;

12) cost estimates associated with environmental remediation activities at the Bloomfield, Moosup and New Hartford, CT facilities and our U.K.

facilities; 13) profitable integration of acquired businesses into the company's operations; 14) changes in supplier sales or vendor incentive

policies; 15) the effects of price increases or decreases; 16) the effects of pension regulations, pension plan assumptions and future

contributions; 17) future levels of indebtedness and capital expenditures; 18) continued availability of raw materials and other commodities in

adequate supplies and the effect of increased costs for such items; 19) the effects of currency exchange rates and foreign competition on

future operations; 20) changes in laws and regulations, taxes, interest rates, inflation rates and general business conditions; 21) future

repurchases and/or issuances of common stock; and 22) other risks and uncertainties set forth in the company's annual, quarterly and current

releases, proxy statements and other filings with the U.S. Securities and Exchange Commission. Any forward-looking information provided in

this presentation should be considered with these factors in mind. The company assumes no obligation to update any forward-looking

statements contained in this presentation.

Contact: Eric Remington

V.P., Investor Relations

(860) 243-6334

Eric.Remington@kaman.com