Attached files

| file | filename |

|---|---|

| EX-31.1 - EX-31.1 - KAPSTONE PAPER & PACKAGING CORP | a2202302zex-31_1.htm |

| EX-23.1 - EX-23.1 - KAPSTONE PAPER & PACKAGING CORP | a2202302zex-23_1.htm |

| EX-32.2 - EX-32.2 - KAPSTONE PAPER & PACKAGING CORP | a2202302zex-32_2.htm |

| EX-31.2 - EX-21.2 - KAPSTONE PAPER & PACKAGING CORP | a2202302zex-31_2.htm |

| EX-21.1 - EX-21.1 - KAPSTONE PAPER & PACKAGING CORP | a2202302zex-21_1.htm |

| EX-32.1 - EX-32.1 - KAPSTONE PAPER & PACKAGING CORP | a2202302zex-32_1.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

TABLE OF CONTENTS 2

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2010 |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to , |

||

Commission File No.: 001-33494

KapStone Paper and Packaging Corporation

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

20-2699372 (I.R.S. Employer Identification No.) |

KapStone Paper and Packaging Corporation

1101 Skokie Blvd. Suite 300

Northbrook, IL 60062

(Address of principal executive offices) (ZIP Code)

Registrant's telephone number, including area code: (847) 239-8800

SECURITIES REGISTERED PURSUANT TO SECTION 12(B) OF THE ACT:

| Title of Each Class | Name of Exchange On Which Registered | |

|---|---|---|

| Common Stock (Par Value $0.0001) | New York Stock Exchange |

SECURITIES REGISTERED PURSUANT TO SECTION 12(G) OF THE ACT: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definition of the above in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer o | Accelerated Filer ý | Non-Accelerated Filer o (Do not check if a smaller reporting company) |

Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the 38,901,244 shares of Common Stock held by non-affiliates of the registrant on June 30, 2010, was $433,359,858. This calculation was made using a price per share of Common Stock of $11.14; the closing price of the Common Stock on the New York Stock Exchange on June 30, 2010 the last day of the registrant's most recently completed second fiscal quarter of 2010. Solely for purposes of this calculation, all shares held by directors and executive officers of the registrant have been excluded. This exclusion should not be deemed an admission that these individuals are affiliates of the registrant.

On February 28, 2011, the number of shares of Common Stock outstanding, excluding 40,000 treasury shares, was 46,097,979.

DOCUMENTS INCORPORATED BY REFERENCE:

The registrant's Definitive Proxy Statement for its 2011 Annual Meeting of Stockholders will be filed with the Securities and Exchange Commission no later than 120 days after the end of the fiscal year covered by this Form 10-K pursuant to General Instruction G(3) of the Form 10-K. Information from such Definitive Proxy Statement will be incorporated by reference into Part III.

ii

Forward Looking Statements.

This Annual Report on Form 10-K includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We have based these forward-looking statements on our current expectations and projections about future events. These forward-looking statements are subject to known and unknown risks, uncertainties and assumptions about us, including the risks set forth in Item 1A. Risk Factors below, that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as "may," "should," "could," "would," "expect," "plan," "anticipate," "believe," "estimate," "continue," or the negative of such terms or other similar expressions. Factors that might cause or contribute to such a discrepancy include, but are not limited to, those described in our other Securities and Exchange Commission filings. All subsequent written and oral forward-looking statements attributable to KapStone or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements in this paragraph. KapStone disclaims any intention or obligation to publicly announce the results of any revisions to any of the forward-looking statements contained herein to reflect future events or developments.

Overview

KapStone Paper and Packaging Corporation ("KapStone" or the "Company") was formed in Delaware as a special purpose acquisition corporation on April 15, 2005 for the purpose of effecting a merger, capital stock exchange, asset acquisition or other similar business combination with an unidentified operating business in the paper, packaging, forest products and related industries.

On January 2, 2007, we consummated the purchase from International Paper Company ("IP") of substantially all of the assets and the assumption of certain liabilities of the Kraft Papers Business ("KPB") for $155.0 million less $7.8 million of working capital adjustments. The assets consisted of an unbleached kraft paper manufacturing facility in Roanoke Rapids, North Carolina, and Ride Rite® Converting, an inflatable dunnage bag manufacturer located in Fordyce, Arkansas, trade accounts receivable and inventories. The liabilities assumed consisted of trade accounts payable, accrued expenses and certain long-term liabilities. The purchase price included two contingent earn-out payments of up to $60.0 million if certain EBITDA targets are achieved. The acquisition was financed by cash on hand and a $95.0 million senior secured credit facility from LaSalle Bank National Association.

On July 1, 2008, we consummated the purchase from MeadWestvaco Corporation ("MWV") of substantially all of the assets and the assumption of certain liabilities of the Charleston Kraft Division ("CKD") for $485.0 million (net of cash acquired of $10.6 million) less $8.9 million of working capital adjustments. The assets consisted of an unbleached kraft paper manufacturing facility in North Charleston, South Carolina, including a cogeneration facility, chip mills located in Elgin, Hampton, Andrews and Kinards, South Carolina and a lumber mill located in Summerville, South Carolina, trade accounts receivable and inventories. The liabilities assumed consisted of trade accounts payable, accrued expenses and certain long-term liabilities. The acquisition was financed by cash on hand and a senior secured credit facility of $515.0 million consisting of a five-year term loan of $390.0 million, a seven-year term loan of $25.0 million and a $100.0 million revolving credit facility. In addition, $40.0 million of seven-year 8.30 percent senior notes were issued. In connection with the transaction the Company paid off the remaining amount due under its prior credit facility. There was no contingent earn-out for the CKD acquisition.

1

On March 31, 2009, we consummated the sale of our dunnage bag business to Illinois Tool Works Inc. for $36.0 million less $1.1 million of working capital adjustments. The Company considered the sale an opportunity to lower its debt and focus on its core business. The sale of the dunnage bag business accelerated a $4.0 million contingent earn-out payment to IP.

On January 4, 2011, we negotiated the early settlement of our final contingent earn-out payment with IP relating to the KPB acquisition. We paid $49.7 million to settle this liability in January 2011, approximately $5.3 million less than the maximum contractual amount which would have been settled in April 2012.

Acquisitions

In an effort to diversify and/or grow our business we have been, and continue to be, engaged in evaluating a number of potential acquisition opportunities. No assurance can be given that we will consummate additional transactions. The structuring and financing of any future acquisitions may be dependent on the terms and availability of additional financing to us that either replaces or does not conflict with the Company's existing senior secured credit facility.

General

We produce and sell a variety of unbleached kraft paper, linerboard, saturating kraft and unbleached folding carton board.

In 2009, the Company determined, in accordance with Accounting Standards Codification ("ASC") 280, Segment Reporting, to make changes to its reportable segments. All segment disclosures in this Report are presented in conformance with the new presentation. For additional information regarding the change in segments, and the results of our segments, see Note 19 of the Notes to Consolidated Financial Statements.

Industry Overview

We view the unbleached kraft market as including kraft paper, linerboard, saturating kraft and unbleached folding carton board.

The American Forest and Paper Association's ("AF&PA") estimate of the size of the U.S. kraft paper market is as follows:

(In millions)

|

2010 | 2009 | 2008 | |||

|---|---|---|---|---|---|---|

Total U.S. sales |

1.33 tons | 1.28 tons | 1.56 tons | |||

U.S. production |

1.36 tons | 1.24 tons | 1.49 tons | |||

Imports |

0.17 tons | 0.20 tons | 0.25 tons | |||

Exports |

0.21 tons | 0.16 tons | 0.18 tons | |||

U.S. operating rates |

84% | 76% | 93% |

The kraft paper market is comprised of three general product types. Multiwall paper is used to produce bags for agricultural products, pet food, baking products, cement and chemicals. Specialty converting paper has a large variety of uses within coating and laminating applications that requires a smooth surface. Specialty converting is also used to produce shingle wrap, end caps, roll wrap and dunnage bags. Grocery bag and sack paper is converted into retail shopping bags, grocery sacks, and lawn and leaf refuse bags.

Over the last two decades, unbleached kraft paper capacity has declined due to a shift in market demand from paper bags to plastic. The multiwall market has contracted due to conversion to plastics in certain end-use markets, primarily in the insulation, pet food, and lawn and garden markets. After bottoming in 2006, capacity increased 2.3 percent in 2007 and 4.6 percent in 2008 as the net impact of

2

machines shifting from other grades to kraft paper was realized. Capacity decreased 2.9 percent in 2009. According to AF&PA's annual survey kraft paper capacity was 1.6 million tons in 2010 and is expected to hold constant through 2011.

Linerboard is primarily used to manufacture corrugated containers for packaging products. U.S. demand for corrugated boxes and linerboard tends to be driven by industrial production of processed foods, nondurable goods and certain durable goods.

The AF&PA's estimate of the size of the U.S. linerboard market is as follows:

(In millions)

|

2010 | 2009 | 2008 | |||

|---|---|---|---|---|---|---|

Total U.S. sales |

21.1 tons | 19.6 tons | 21.3 tons | |||

U.S. production |

24.1 tons | 22.4 tons | 24.2 tons | |||

Imports |

0.41 tons | 0.37 tons | 0.56 tons | |||

Exports |

3.38 tons | 3.17 tons | 3.32 tons | |||

U.S. operating rates |

95% | 85% | 91% |

We target our linerboard for specialty independent corrugated and laminated products customers who focus on specialty niche packaging.

Our saturating kraft product, sold under the trade name Durasorb®, is used in multiple industries including construction, electronics manufacturing and furniture manufacturing around the world. The major end-use markets are in the thin high pressure laminates (HPL) that create decorative surfaces such as kitchen and bath countertops, home and office furniture and flooring. Originated in Europe, there is a growing and distinct HPL segment that involves a much thicker product called compact laminates, which create surfacing products such as exterior cladding, partitions and doors. In Asia, there is significant use of our products for the manufacturing of printed circuit boards (PCB) and copper clad laminates (CCL) and there is also a growing use for thin HPL in decorative surfaces. There is no published data reporting the size of the market. Barriers to entry for producing high quality saturating kraft are high as it is a technically difficult grade of paper to produce.

Our unbleached folding carton board product line, sold under the trade name Kraftpak®, is a unique, low density virgin fiber board. Kraftpak® applications are widely spread throughout end uses in the general folding carton segment of paperboard packaging. KapStone believes that the best growth opportunities for Kraftpak® are in consumer brands that are changing their images to promote environmental friendliness and sustainability, thus taking market share from coated recycled board, coated natural kraft board and solid bleached sulfate board which are much larger markets. There is no published data reporting the size of the market.

Customers

The Company has over 500 customers, many of which are leading world class converters. In 2007, the Company had approximately 100 customers. Upon acquiring CKD in July of 2008, the Company's number of customers increased to approximately 400, of which approximately 100 were based in foreign countries. No customer accounted for more than 10 percent of consolidated net sales in 2010 and 2009. Graphic Packaging accounted for 10.7 percent of consolidated net sales in 2008. KapStone continues to build long-term relationships, most of which were established by KPB and CKD before we acquired them. We believe that the risk of losing customers or business with customers is reduced due to the long-term relationships that have been established.

Kraft paper is sold to converters who produce multiwall bags for agricultural products, pet food, cement and chemicals, grocery bags and specialty conversion products such as wrapping paper products, dunnage bags and roll wrap. The Company's kraft paper product line accounted for approximately 21 percent of total unit sales for each of 2010 and 2009 and 43 percent for 2008.

3

Linerboard is sold to domestic and foreign converters in the corrugated box industry and to other converters for a variety of uses including laminated tier sheets and wrapping material, among others. Our focus is on independent producers who do not have their own mill systems or producers who commonly purchase linerboard in the open market. The Company's linerboard product line accounted for approximately 51 percent of total unit sales for each of 2010 and 2009 and 32 percent for 2008.

Our Durasorb® customer base is split among three geographic regions, the Americas, Europe and Asia. Approximately 78 percent of our sales are exports to customers in Europe, Latin America and Asia where growth opportunities are favorable. KapStone, or its predecessor, has done business with many of these customers for well over 30 years. Some customers have consolidated to form a greater presence in their markets. Customer consolidation is particularly evident in North America and is in the early phase in Europe. In Asia, there are numerous players and it is a highly fragmented market making entry difficult for some companies that do not have a presence in the region. KapStone has acquired a leadership position through knowledge of our markets and understanding the technical needs of our customers' manufacturing processes and the demanding requirements of their products. The Company's Durasorb® product line accounted for approximately 21 percent of total unit sales for each of 2010 and 2009 and 19 percent for 2008.

Our Kraftpak® customer base consists primarily of integrated and independent converters in the folding carton industry. The Company's Kraftpak® product line accounted for approximately 7 percent of total unit sales for each of 2010 and 2009 and 6 percent for 2008.

Sales and Marketing

The sales and marketing team works directly with our technical, manufacturing and product development teams to offer solutions and meet new customer demands and product requirements. We market and sell our products through a national sales force for our domestic sales. Our international sales are supported by sales teams based in Europe and Asia. We sell export linerboard to unaffiliated resellers and on a direct export basis.

Manufacturing and Distribution

Our manufacturing facilities are based in Roanoke Rapids, North Carolina and North Charleston, South Carolina and include production facilities consisting of integrated pulp and paper mills that produce kraft paper, linerboard, saturating kraft products sold under the DuraSorb® brand and folding carton board sold under the Kraftpak® brand.

The Company's paper mills' annual production capacity is approximately 1.3 million tons. Machinery and equipment is regularly inspected to maintain good working order through planned maintenance outages.

Softwood pulp used to make kraft paper, folding carton board and linerboard is produced from a combination of locally sourced roundwood and pine woodchips. After the wood is debarked and chipped, the chips are loaded into digesters for cooking. Woodchips, chemicals and steam are mixed in the digester to produce softwood pulp. Hardwood pulp is produced in North Charleston in a similar fashion for the production of DuraSorb® saturating kraft. The pulp is screened and washed through a series of washers, and then stored prior to the paper making process. The Company processes pulp using up to five paper machines. Management monitors productivity on a real-time basis with on-line reporting tools that track production values versus targets. Overall equipment efficiency is also monitored daily through production reporting systems.

The majority of our domestic sales are distributed directly to customers by a combination of third parties mainly by truck and rail. Export linerboard and saturating kraft are shipped to customers via ocean vessel.

4

Transitional Support

In conjunction with each acquisition we entered into transitional services agreements to provide for certain services, including information technology and centralized transaction processing, until we could convert the acquired operations to our own Enterprise Resource Planning ("ERP") systems. Our transitional support services from IP for the KPB acquisition ended on April 1, 2008 after a term of 15 months at a cost of $3.2 million. Our transitional service agreement with MWV for the CKD acquisition began on July 1, 2008 and ended on December 31, 2009 after a term of 18 months at a cost of $8.7 million.

The total cost of transferring services from IP to us was approximately $6.0 million, consisting primarily of installing a new ERP system which included general ledger, order entry and receivables management, purchasing and payment plus additional modules. We incurred approximately $5.8 million to migrate and upgrade the Charleston operations to our ERP system.

Suppliers

The raw materials needed to process unbleached kraft paper and related products consist primarily of round wood, woodchips and chemicals. In addition, we purchase coal, fuel oil and natural gas to run boilers and our cogeneration facility in South Carolina. We believe that these raw materials are readily available and that there are a number of suppliers from whom the materials can be bought in the open market.

In 2010, approximately 22 percent of our combined paper mills' fiber supply (round wood and woodchips) was delivered under a long-term supply agreement. Upon acquisition of the CKD business from MWV, we entered into a 15 year fiber supply agreement whereby MWV provides us with up to 25 percent of our South Carolina fiber requirements with prices tied to a market index. The balance of fiber is purchased through contracts and in the open market from third parties in North Carolina, Virginia, Georgia and South Carolina.

The primary chemical used in our pulp making process is caustic soda which we purchase at market prices. We have two contracts to purchase coal at fixed prices with one expiring on December 31, 2011 and the other on December 31, 2012. The contracts allow for a certain amount of coal to be purchased in the open market. Fuel oil is purchased from third parties at market prices.

Typical contracts for raw materials range from one to three years in length and are at fixed pricing, driven by market pricing, or tied to a documented moving index for each material. As costs for raw materials, supplies and services increase, we implement price increases to recover these rising material costs from our customers, when possible. We currently do not use futures contracts or enter into hedging arrangements to manage the risk of fluctuations in coal or fuel oil prices. Thus, if we cannot pass on the rise in energy or other costs to our customers, such increase in costs will have an adverse effect on our gross profit margins and net income.

Competition

We are one of the leading manufacturers of kraft paper in North America. Other key U.S. market suppliers are Georgia-Pacific, Longview Fibre, Delta Natural, and Smurfit Stone. A number of other competitors comprise the remainder of North American kraft paper production. We believe the key parameters on which North American unbleached kraft suppliers compete are supply reliability, delivered price and product quality. We have longstanding relationships with many of our customers and historically have entered into contracts with initial terms of at least two years. We believe our longstanding relationships are based on our ability to provide the best value proposition to our customers through quality products, consistent and reliable service and technical innovation.

5

Based on a report published by the AF&PA, the overall U.S. linerboard capacity is in excess of 25 million tons. As such, our market share is just over two percent. International Paper is the largest producer, followed by Smurfit Stone, Georgia-Pacific and Temple-Inland Packaging. Our emphasis is on the independent producers of corrugated packaging and other users of linerboard.

In the saturating kraft market, there are three major manufacturers (KapStone, International Paper and Kotkamills). The remainder is supplied by local producers of lower quality material in various regions of the world.

Kraftpak® competes primarily with uncoated recycled board which is produced by Newark, Rock-Tenn, Caraustar and Graphic Packaging, and a variety of smaller producers.

Environmental Regulation

Our operations are subject to environmental regulation by federal, state, and local authorities in the United States, including requirements that regulate discharge into the environment, waste management, and remediation of environmental contamination. Environmental permits are required for the operation of our facilities and are subject to revocation, modification and renewal. Governmental authorities have the power to enforce compliance with environmental requirements and violators are subject to injunctions, civil penalties and criminal fines. Third parties may also have the right to sue to enforce compliance with such regulations.

KapStone is committed to maintaining high environmental quality standards which meet or exceed those established by all relevant environmental laws, regulations and other applicable requirements including Sustainable Forestry Initiatives. KapStone's goal is 100 percent compliance with all environmental laws and regulations wherever we do business. This is achieved by identifying, understanding and giving priority consideration to the environmental aspects and impacts of KapStone's activities, products and services while integrating continual environmental improvement, pollution prevention and employee diligence into daily operations.

On December 8, 2009, the Environmental Protection Agency ("EPA") announced that for the first time in nearly 40 years, it is proposing to strengthen the nation's sulfur dioxide (SO2) air quality standard to protect public health. This standard and the impending Industrial Boiler Maximum Achievable Control Technology ("MACT") standard will affect fuel combustion sources at our facilities. Our North Carolina mill has received its draft air operating permit with state boiler MACT compliance requirements for comment and final review with expectation of compliance in 2013. We continue to monitor the process the EPA is undertaking to develop new standards for industrial boilers and process heaters so that we can determine our potential liability regarding any future related regulations. The Company's South Carolina paper mill does not have a state requirement for MACT compliance at this time

The EPA is continuing the development of new programs and standards, such as additional wastewater discharge allocations, water intake structure requirements and national ambient air quality standards. We believe that our operations are in compliance in all material respects with all current environmental regulations and we are not aware of any pending regulatory agency compliance actions.

The U.S. Congress is actively considering legislation to reduce emissions of greenhouse gases. In addition, several states have already taken legal measures to require the reduction of emissions of greenhouse gases by companies and public utilities, primarily through the planned development of greenhouse gas emission inventories and/or regional greenhouse gas cap and trade programs. Passage of climate control legislation by Congress or various states of the U.S., or the adoption of regulations by the EPA or analogous state agencies that restrict emissions of greenhouse gases in areas in which we conduct business, may have a material effect on our operations in the United States. We expect that we

6

will not be disproportionately impacted by these measures relative to typical owners of comparable properties in the United States.

Employees

At December 31, 2010, KapStone had approximately 1,600 employees. Of these employees, approximately 1,000 employees are covered by collective bargaining agreements with the United Steelworkers being the largest. Currently, there is a collective bargaining agreement in place with union employees in Roanoke Rapids, North Carolina, through August 2013 and union employees in North Charleston, South Carolina through July 2012. We believe that we have a good relationship with our employees and union leadership.

International Sales

For the years ended December 31, 2010, 2009 and 2008, the Company had export shipments from the United States to customers in foreign countries of $300 million, $239 million and $165 million, respectively. No foreign country accounted for more than 10 percent of our consolidated net sales for any year.

Website Access to Company Reports

The Company's annual reports on Form 10-K, including this Form 10-K, as well as the quarterly reports on Form 10-Q and current reports on Form 8-K, and all amendments to those reports are filed electronically with the Securities and Exchange Commission ("SEC") and are also available free of charge through our website, www.kapstonepaper.com, as soon as reasonably practicable after such material is filed electronically with, or furnished to, the SEC. Also, copies of our annual report will be made available, free of charge, upon written request.

You should carefully consider the following risk factors, together with the other information contained in this annual report on Form 10-K, in evaluating us and our business before making an investment decision regarding our securities. If any of the events or circumstances described in the following risk factors were to actually occur, our business, financial condition or results of operations could be materially and adversely affected. The risks listed below are not the only risks that we face.

Risks associated with our business

Recent changes in U.S. and global economic conditions could have a continuing adverse effect on the profitability of some or all of our businesses.

Recent concerns over declining consumer and business confidence, the availability and cost of credit, reduced consumer spending and business investment, the volatility and strength of the capital and credit markets, and inflation all affect the business and economic environment and, ultimately, the profitability of our business. In an economic downturn characterized by higher unemployment, lower family income, lower corporate earnings, lower business investment and lower consumer spending, the demand for our products is adversely affected. Adverse changes in the economy could negatively affect earnings and could have a material adverse effect on our business, results of operations, cash flows and financial position. We cannot predict whether or when such circumstances may occur, or what impact, if any such circumstances could have on our business, results of operations, cash flows and financial position.

7

Conditions in the global capital and credit markets and the economy generally may materially adversely affect our business, results of operations and financial position and we do not expect these conditions to improve in the near future.

Our results of operations and financial position could be materially affected by adverse changes in the global capital and credit markets and the economy generally, including recent declines in consumer and business confidence and spending, both in the U.S. and elsewhere around the world. The capital and credit markets have been experiencing extreme volatility and disruption over the last few years. In some cases, these markets have exerted downward pressure on availability of liquidity and credit and increased the costs of credit when such credit is available. Conditions in the capital and credit markets and the effects of the declines in consumer and business confidence and spending may adversely impact the ability of our lenders, suppliers and customers to conduct their business activities. The consequences of such adverse effects could include the interruption of production at the facilities of our customers, the reduction, delay or cancellation of customer orders, delays in or the inability of customers to obtain financing to purchase our products, and bankruptcy of customers or other creditors. Moreover, the current worldwide financial crisis has reduced the availability of liquidity and credit to fund or support the continuation and expansion of business operations worldwide as many lenders and institutional investors have reduced and, in some cases, ceased to provide funding to borrowers.

While we have procedures to monitor and limit exposure to credit risk, there can be no assurance such procedures will effectively limit our credit risk and avoid losses, which could have a material adverse effect on our business, results of operations and cash flows and financial position.

We rely on key customers and a loss of one or more of our key customers could adversely affect our business, results of operations, cash flows and financial position.

During the year ended December 31, 2010, no customer accounted for more than 10 percent of consolidated net sales. However, losses of key customers could significantly impact our business, results of operations, cash flows and financial position.

We are dependent upon key management executives the loss of whom may adversely impact our business.

We depend on the expertise, experience and continued services of corporate and mill management. The loss of such management, or an inability to attract or retain other key individuals, could materially adversely affect our business. There can be no assurance that our salaries and incentive compensation plans will allow us to retain the services of these key management executives or hire new key employees.

KapStone's indebtedness may adversely affect its financial health.

As of December 31, 2010, we had approximately $115 million of outstanding debt. As a result of the indebtedness, our ability to obtain additional financing for working capital, capital expenditures, acquisitions or other general corporate purposes may be impaired in the future. The debt could make us vulnerable to economic downturns and may hinder our ability to adjust to rapidly changing market conditions.

8

A portion of our cash flow from operations will be needed to meet the payment of principal and interest on our indebtedness. The business may not generate sufficient cash flow from operations to enable it to repay our indebtedness and to fund other liquidity needs, including capital expenditure requirements. The indebtedness incurred by us under our senior secured credit facility bears interest at variable rates, and therefore if interest rates increase, our debt service requirements would increase. In such case, we may need to refinance or restructure all or a portion of our indebtedness on or before maturity. We may not be able to refinance any of our indebtedness, including the senior secured credit facility, on commercially reasonable terms, or at all. If we cannot service or refinance our indebtedness, we may have to take actions such as selling assets, seeking additional equity or reducing or delaying capital expenditures, any of which could have a material adverse effect on our operations and financial condition.

Our senior secured credit facility contains restrictive covenants that limit our liquidity and corporate activities. Our credit facility imposes operating and financial restrictions that limit our ability to:

- •

- incur additional indebtedness;

- •

- create additional liens on our assets;

- •

- make investments;

- •

- engage in mergers or acquisitions;

- •

- pay dividends; and

- •

- sell all or any substantial part of our assets.

In addition, the credit facility also imposes other restrictions on us. Therefore, we would need to seek permission from the lenders in order to engage in certain corporate actions. The lenders' interests may be different from ours, and no assurance can be given that we will be able to obtain the lenders' permission when needed. This may prevent us from taking actions that are in our best interest.

The credit facility requires us to maintain certain financial ratios. The failure to maintain the specified ratios could result in an event of default if not cured or waived.

In the event of a default under our senior credit facility, the lenders generally would be able to declare all of such indebtedness, together with accrued interest, to be due and payable. In addition, borrowings under the credit facility are secured by a first priority lien on all of our assets and, in the event of a default under that facility the lenders generally would be entitled to seize the collateral. A default under any debt instrument, unless cured or waived, would likely have a material adverse effect on our business and financial condition.

If we fail to extend or renegotiate the collective bargaining agreements as they expire from time to time, or if our unionized employees were to engage in a strike or other work stoppage, our business and operating results could be materially harmed.

Most of our hourly paid employees are represented by trade unions. We are a party to collective bargaining contracts which apply to approximately 600 employees at the North Charleston mill and 400 employees at the Roanoke Rapids mill. No assurance can be given that we will be able to successfully extend or renegotiate the collective bargaining agreements as they expire from time to time. Currently, there is a collective bargaining agreement in effect with respect to Roanoke Rapids and North Charleston through August 2013 and July 2012, respectively. If we are unable to extend or negotiate new agreements without work stoppages, it could negatively impact our ability to manufacture our products and adversely affect results of operations.

9

Our operations are global in nature, and accordingly our business, results of operations, cash flows and financial position could be adversely affected by the political and economic conditions of the countries in which we conduct business, by fluctuations in exchange rates and other factors related to our international operations.

Approximately 38 percent of our 2010 and 2009 revenues were derived from export sales. As our international operations and activities expand, we face increasing exposure to the risks of selling to customers in foreign countries. These factors include:

- •

- Changes in foreign currency exchange rates which could adversely affect selling prices for our products, and therefore our

competitive position in a particular market.

- •

- Trade protection measures in favor of local producers of competing products, including government subsidies, tax benefits,

trade actions (such as anti-dumping proceedings) and other measures giving local producers a competitive advantage over the company.

- •

- Changes generally in political, regulatory or economic conditions in the countries in which we conduct business.

These risks could affect the cost of selling our products, our pricing, sales volume, and ultimately our financial performance. The likelihood of such occurrences and their potential effect on the company vary from country to country and are unpredictable.

We may be required to record a charge to our earnings if our goodwill becomes impaired.

We test for impairment of goodwill annually at the beginning of the fourth quarter in accordance with generally accepted accounting standards. When events or changes in circumstances indicate that the carrying value for such assets may not be recoverable, we review goodwill for impairment on an interim basis. Factors that may be considered a change in circumstances requiring our interim testing include a decline in stock price as compared to our book value per share, future cash flows and slower growth rates. In connection with future annual or interim tests, we may be required to record a non-cash charge to earnings during the period in which any impairment of goodwill is determined, which would adversely impact our results of operations.

See Note 2. "Significant Accounting Policies—Goodwill and Intangible Assets" in the Notes to the Consolidated Financial Statements for additional information related to testing for impairment of goodwill.

Our business depends on effective information management systems.

We rely on our enterprise resource planning (ERP) systems to support such critical business operations as processing sales orders and invoicing, inventory control, purchasing and supply chain management, payroll and human resources, and financial reporting. We periodically implement upgrades to such systems or migrate one or more of our affiliates, facilities or operations from one system to another. If we are unable to adequately maintain such systems to support our developing business requirements or effectively manage any upgrade or migration, we could encounter difficulties that could have a material adverse impact on our business, internal controls over financial reporting, financial results, or our ability to timely and accurately report such results.

We may incur business disruptions.

We take measures to minimize the risks of disruptions at our manufacturing facilities. However, the occurrence of a natural disaster, such as a hurricane, tropical storm, earthquake, tornado, flood, fire or other unanticipated problems such as labor difficulties, equipment failure or unscheduled maintenance could cause operational disruptions and could materially adversely affect our earnings and

10

cash flows. Any losses due to these events may not be covered by our existing insurance policies or may be subject to certain deductibles.

Environmental regulations could materially adversely affect our results of operations and financial position.

We are subject to environmental regulation by federal, state, and local authorities in the United States, including requirements that regulate discharge into the environment, waste management, and remediation of environmental contamination. Maintaining compliance with existing and new environmental laws may require capital expenditures for compliance.

Due to past history of industrial operations at the Roanoke Rapids and North Charleston mills, the possibility of onsite and offsite environmental impact to the soil and groundwater may present a heightened risk of contamination. If we are required to make significant expenditures for remediation, the costs of such efforts may have a significant negative impact on our results of operations and financial condition.

MWV retained responsibility for certain offsite environmental conditions resulting from the operations at the North Charleston mill existing prior to the closing of the CKD acquisition. The overall indemnification by MWV for certain losses includes assumed environmental liabilities, subject to an $8.5 million threshold and a cap equal to 15 percent of the purchase price of $485 million. MWV's obligation to indemnify us for any historical onsite liability or breach of certain environmental representations and warranties terminates on December 31, 2013. MWV's indemnification for certain offsite historical liabilities survive indefinitely. Because we are unable to presently make a determination as to whether the environmental impact, if any, would be widespread or significant, the negotiated cap and survival period may not be sufficient to cover future losses.

We may be required to pay income taxes related to the Alternative Fuel Mixture Tax Credit.

On March 31, 2009, we received approval from the Internal Revenue Service for our registration as an alternative fuel mixer, which provides for a refund of $0.50 per gallon of alternate fuel used in our pulp making process. We have generated refund claims of $178.3 million since becoming registered as an alternative fuel mixer. We have taken the position that the tax credit is similar to a federal excise tax refund, and as a result, is not taxable. To date, the Internal Revenue Service has issued no guidance concerning this issue.

As of December 31, 2010 we have recorded a $67.7 million liability for an unrecognized tax benefit relating to the taxability of alternative fuel mixture tax credits.

Our operations are dependent upon certain operating agreements for fiber.

We rely on certain supply arrangements to provide us roundwood and woodchips. If one of these suppliers suffered a setback, KapStone's supply of roundwood and woodchips may not be adequate to cover customer needs.

Risks Associated with KapStone's Common Stock

The market price for our common stock may be highly volatile.

The market price of our common stock may be volatile due to certain factors, including, but not limited to; quarterly fluctuations in our financial and operating results; general conditions in the paper and packaging industries; or changes in earnings estimates.

11

Shares available for future issuance, conversion and exercise could have an adverse effect on the earnings per share and the market price of our common stock.

Any future issuance of equity securities, including shares issued upon exercise of outstanding stock options, could dilute the interests of our existing stockholders and could substantially decrease the trading price of our common stock.

Our executive officers and directors control a substantial percentage of our common stock and thus may influence certain actions requiring a stockholder vote.

At December 31, 2010, our executive officers and directors owned 7.1 million shares of our common stock, or approximately 15.5 percent of our total outstanding common stock. Accordingly, our executive officers and directors may have considerable influence over the outcome of all matters requiring approval by our stockholders, including future acquisitions and the election of directors. In addition, our board of directors is divided into three classes, each of which will generally serve for a term of three years with only one class of directors being elected in each year. At the annual meeting, as a consequence of our "staggered" board of directors, only a minority of the board of directors will be considered for election and our officers and directors, because of their ownership position, will have considerable influence regarding the outcome of the election.

Risks associated with the paper, packaging, forest products and related industries

The paper, packaging, forest products and related industries are highly cyclical. Fluctuations in the prices of and the demand for products could result in smaller profit margins and lower sales volumes.

Historically, economic and market shifts, fluctuations in capacity and changes in foreign currency exchange rates have created cyclical changes in prices, sales volume and margins for products in the paper, packaging, forest products and related industries. The length and magnitude of industry cycles have varied over time and by product, but generally reflect changes in macroeconomic conditions and levels of industry capacity. Most paper products and many wood products used in the packaging industry are commodities that are widely available from many producers. Because commodity products have few distinguishing qualities from producer to producer, competition for these products is based primarily on price, which is determined by supply relative to demand. The overall levels of demand for these commodity products reflect fluctuations in levels of end-user demand, which depend in large part on general macroeconomic conditions in North America and regional economic conditions in our markets, as well as foreign currency exchange rates. The foregoing factors could materially and adversely impact sales and profitability of our company.

Difficulty obtaining wood fiber at favorable prices, or at all, may negatively impact companies in the paper and packaging industry.

Wood fiber is the principal raw material in many parts of the paper and packaging industry. Wood fiber is a commodity, and prices historically have been cyclical. Environmental litigation and regulatory developments have caused, and may cause in the future, significant reductions in the amount of timber available for commercial harvest in the United States. These reductions have caused the closure of plywood and lumber operations in some of the geographic areas in which a target company might operate. In addition, future domestic or foreign legislation and litigation concerning the use of timberlands, the protection of endangered species, the promotion of forest health and the response to and prevention of catastrophic wildfires could also affect timber supplies. Availability of harvested timber may further be limited by fire, insect infestation, disease, ice storms, wind storms, flooding and other causes, thereby reducing supply and increasing prices.

Industry supply of commodity paper and wood products is also subject to fluctuation, as changing industry conditions can influence producers to idle or permanently close individual machines or entire

12

mills. In addition, to avoid substantial cash costs in connection with idling or closing a mill, some producers will choose to continue to operate at a loss, sometimes even a cash loss, which could prolong weak pricing environments due to oversupply. Oversupply in these markets can also result from producers introducing new capacity in response to favorable short-term pricing trends. Industry supply of commodity papers and wood products is also influenced by overseas production capacity, which has grown in recent years and is expected to continue to grow. Wood fiber pricing is subject to regional market influences, and the cost of wood fiber may increase in particular regions due to market shifts in those regions. In addition, the ability to obtain wood fiber from foreign countries may be impacted by economic, legal and political conditions in those countries as well as transportation difficulties.

An increase in the cost of purchased energy and raw materials would lead to higher manufacturing costs, thereby reducing margins which would have an adverse effect on our results of operations.

Energy is a significant input cost for the paper and packaging industry. Increases in energy prices can be expected to adversely impact businesses. Energy prices, particularly for electricity, coal and fuel oil, have been volatile in recent years and currently coal and electricity exceed historical averages. These fluctuations have historically impacted manufacturing costs of companies in the industry, often contributing to reduced margins and increased earnings volatility. In addition, we could be materially adversely impacted by supply disruptions or the inability to pass on cost increases to our customers.

Paper and packaging companies face strong competition.

We face competition from numerous competitors, domestic as well as foreign. Some of our competitors will be large, vertically integrated companies that have greater financial and other resources, greater manufacturing economies of scale, greater energy self-sufficiency and/or lower operating costs.

Certain paper and wood products are vulnerable to long-term declines in demand due to competing technologies or materials.

Companies in the paper and packaging industry are subject to possible declines in demand for their products as the use of alternative materials and technologies grows and the prices of such alternatives become more competitive. Any substantial shift in demand from wood and paper products to competing technologies or materials could result in a material decrease in sales of our products and could adversely affect our results of operations. We cannot ensure that any efforts we might undertake to adapt our product offerings to such changes would be successful or sufficient.

Paper and packaging companies are subject to significant environmental regulation and environmental compliance expenditures, as well as other potential environmental liabilities.

Companies in the paper and packaging industry are subject to a wide range of general and industry specific environmental laws and regulations, particularly with respect to air emissions, wastewater discharges, solid and hazardous waste management, site remediation, forestry operations and endangered species habitats. We may incur substantial expenditures to maintain compliance with applicable environmental laws and regulations, which could adversely affect our results of operations. Failure to comply with applicable environmental laws and regulations could expose us to civil or criminal fines or penalties or enforcement actions, including orders limiting operations or requiring corrective measures, installation of pollution control equipment or other remedial actions.

13

Risks Associated with Acquisitions

Future acquisitions of businesses by us would subject us to additional business, operating and industry risks, the impact of which cannot presently be evaluated, and could adversely impact our capital structure.

We intend to pursue other acquisition opportunities in an effort to diversify our investments and/or grow our business. Any business acquired by us may cause us to be affected by numerous risks inherent in the acquired business' operations. If we acquire a business in an industry characterized by a high level of risk, we may be adversely affected by the currently unascertainable risks of that industry. We cannot ensure that we would be able to properly ascertain or assess all of the significant risk factors with any such acquisitions.

In addition, the financing of any acquisition completed by us could adversely impact our capital structure as any such financing would likely include the issuance of additional equity securities and/or the borrowing of additional funds. The issuance of additional equity securities may significantly reduce the equity interest of our stockholders and/or adversely affect prevailing market prices for our common stock. Increasing our indebtedness could increase the risk of a default that would entitle the holder to declare all of such indebtedness due and payable and/or to seize any collateral securing the indebtedness. In addition, default under one debt instrument could in turn permit lenders under other debt instruments to declare borrowings outstanding under those other instruments to be due and payable pursuant to cross default clauses. Accordingly, the financing of future acquisitions could adversely impact our capital structure and the value of your equity interest in us.

Except as required by law or the rules of any securities exchange on which our securities might be listed at the time we seek to consummate a subsequent acquisition, stockholders will not be asked to vote on any such proposed acquisition and no redemption rights in connection with any such acquisition will exist.

Item 1B. Unresolved Staff Comments

None.

We believe that our properties are well-maintained, in good operating condition and adequate for our present needs. The following table sets forth our principal properties, as of December 31, 2010:

Location

|

Segment | Owned/Leased | |||

|---|---|---|---|---|---|

| North Charleston, South Carolina | Unbleached kraft paper | Owned | |||

| Roanoke Rapids, North Carolina | Unbleached kraft paper | Owned | |||

| Northbrook, Illinois | Corporate | Leased | |||

The lease for our corporate headquarters expires in 2015.

14

We are party to various legal proceedings arising from our operations. We establish reserves for claims and proceedings when it is probable that liabilities exist and where reasonable estimates can be made. While it is not possible to predict the outcome of any these matters, based on our assessment of the facts and circumstances now known, we do not believe that any of these matters, individually or in the aggregate, are material. However, actual outcomes may be different from those expected and could have a material effect on our results of operations or cash flows in a particular period.

Disclosure of Certain Tax Penalties

The Company has no tax penalties owing to the Internal Revenue Service.

15

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company's common stock was traded on the NASDAQ Global Market from May 29, 2007 through January 3, 2010 under the symbol "KPPC". Effective January 4, 2010, the Company's common stock began trading on the New York Stock Exchange ("NYSE") under the "KS" trading symbol. The following table sets forth the high and low bid information for the Company's common stock from January 1, 2009 through December 31, 2010, as reported by the NYSE and NASDAQ Global Market. The quotations reflect inter-dealer prices, are without retail markup, markdowns or commissions, and may not represent actual transactions.

| |

2010 | 2009 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Quarter

|

Low | High | Low | High | |||||||||

1st |

$ | 8.08 | $ | 12.35 | $ | 1.05 | $ | 3.07 | |||||

2nd |

$ | 10.00 | $ | 13.40 | $ | 2.14 | $ | 5.01 | |||||

3rd |

$ | 10.25 | $ | 13.13 | $ | 4.50 | $ | 8.80 | |||||

4th |

$ | 12.01 | $ | 15.56 | $ | 6.48 | $ | 9.90 | |||||

At December 31, 2010, the closing share price on the NYSE was $15.30.

Number of Holders of Common Stock

The number of beneficial holders of record of our common stock on December 31, 2010 was 6,742.

Dividends

There were no cash dividends or other cash distributions made by us during the fiscal years 2010, 2009 or 2008. The Company's senior secured credit facility restricts the declaration or payment of cash dividends. The Company does not expect to pay dividends in the foreseeable future.

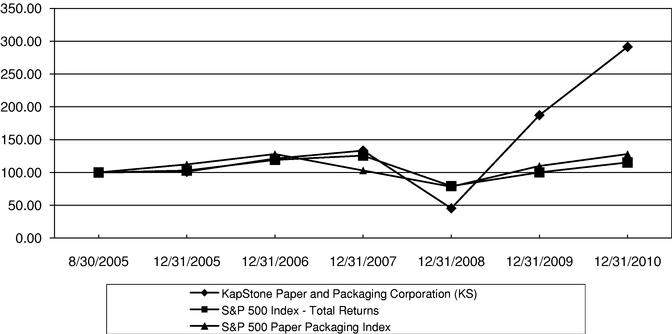

Stock Performance Graph

The performance graph shall not be deemed to be "soliciting material" or to be "filed" with the commission or subject to Regulation 14A or 14C, or to the liabilities of Section 18 of the Securities Exchange Act of 1934 as amended.

The following graph compares a $100 investment in Company stock on August 31, 2005 with a $100 investment in each of the S&P 500 and the S&P Paper and Packaging Index (the Company's peer group) also made on August 31, 2005. The graph portrays total return, 2005-2010, assuming reinvestment of dividends.

16

Comparison of 5 Year Cumulative Total Return

Assumes Initial Investment of $100

December 2010

Item 6. Selected Financial Data

The following table sets forth KapStone's selected financial information derived from its audited consolidated financial statements as of, and for the years ended, December 31, 2010, 2009, 2008, 2007 and 2006 as well as KPB Predecessor's audited financial statements as of, and for the year ended December 31, 2006.

The selected financial data presented below summarizes certain financial data which has been derived from and should be read in conjunction with Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations" and KapStone's audited consolidated financial statements included in Item 8.

| |

|

|

|

|

|

Predecessor KPB | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Years Ended December 31, | ||||||||||||||||||

| |

Year Ended December 31, 2006 |

||||||||||||||||||

In thousands, except per share amounts

|

2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||

Statement of Income Data: |

|||||||||||||||||||

Net sales |

$ | 782,676 | $ | 632,478 | $ | 524,549 | $ | 256,795 | $ | — | $ | 246,161 | |||||||

Operating income / (loss) |

$ | 68,703 | $ | 151,362 | $ | 50,656 | $ | 44,300 | $ | (1,976 | ) | $ | 33,951 | ||||||

Net income |

$ | 65,041 | $ | 80,280 | $ | 19,665 | $ | 26,963 | $ | 2,196 | $ | 19,967 | |||||||

Basic net income per share |

$ | 1.42 | $ | 2.32 | $ | 0.74 | $ | 1.08 | $ | 0.09 | n/a | ||||||||

Diluted net income per share |

$ | 1.38 | $ | 2.29 | $ | 0.57 | $ | 0.75 | $ | 0.07 | n/a | ||||||||

Balance Sheet Data: |

|||||||||||||||||||

Cash and cash equivalents |

$ | 67,358 | $ | 2,440 | $ | 4,165 | $ | 56,635 | $ | — | $ | 1 | |||||||

Total assets |

$ | 719,727 | $ | 669,123 | $ | 727,190 | $ | 225,450 | $ | 119,257 | $ | 257,382 | |||||||

Long-term liabilities |

$ | 185,539 | $ | 213,637 | $ | 419,545 | $ | 37,668 | $ | — | $ | 22,622 | |||||||

Total stockholders' equity |

$ | 418,634 | $ | 348,790 | $ | 180,767 | $ | 144,185 | $ | 116,045 | $ | 219,685 | |||||||

For the year ended December 31, 2006, net income allocable to holders of nonredeemable common stock was $1.5 million.

17

See Note 3 to Notes to Consolidated Financial Statements for acquisition information and Note 4 for information on the sale of the dunnage bag business.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

Executive Summary

We were formed as a special purpose acquisition corporation on April 15, 2005 for the purpose of effecting a merger, capital stock exchange, asset acquisition or other similar business combination with an unidentified operating business in the paper, packaging, forest products and related industries.

We have consummated two acquisitions since January 2007, as we drive towards our strategic objective of being a $2 billion revenue company by 2015. We continue to evaluate additional acquisition opportunities.

Our operations had a strong year in 2010 producing approximately 1.27 million tons of paper compared to 1.14 million tons in 2009. Our North Charleston mill successfully completed its first cold mill outage in three years while our Roanoke Rapids mill completed its annual outage in the fourth quarter. Our operating rate for the year increased to 98.5 percent up from 88.3 percent in 2009. Market driven price increases, occurring as a result of higher demand in 2010, increased our average selling prices by $62 per ton to $586. During 2010, we implemented significant price increases in linerboard and kraft paper. We expect our revenue to benefit in 2011 from the full year effect of 2010 price increases by approximately $40.0 to $45.0 million assuming normal sales volume and product mix.

Our operating results for 2010 and 2009 include $22.2 million and $164.0 million, respectively, of alternative fuel mixture tax credits which significantly improved earnings. In addition, the cash generated from these credits was used to make over $313.1 million of repayments in the aggregate in 2010 and 2009 on our long-term debt and notes. At December 31, 2010, we have recorded a liability of $67.7 million for uncertain tax benefits relating to alternative fuel mixture tax credits. Our position is that these tax credits are not taxable for federal income purposes. However, the Internal Revenue Service ("IRS") has not issued any specific guidance. The alternative fuel mixture tax credit expired on December 31, 2009.

In August 2010, the IRS approved the Company's registration as a producer of cellulosic biofuel for the tax year 2009. With this registration, the Company applied for a nonrefundable, taxable income tax credit of $1.01 per gallon of qualified cellulosic biofuel for the black liquor burned in early 2009 when the Company did not claim the alternative fuel mixture tax credit. A $21.0 million net tax benefit (net of U.S. federal and state taxes) related to cellulosic biofuel was reflected in the Company's income tax provision for the year ended December 31, 2010. The Company reported $33.9 million (gross tax credit) as a deferred tax asset as of December 31, 2010 in the Consolidated Balance Sheets which is available to offset taxable income in future years and expires in 2015, if unutilized.

On January 4, 2011, we negotiated the early settlement of our contingent earn-out with IP relating to the KPB acquisition. We paid $49.7 million to settle this liability in January 2011, approximately $5.3 million less than the maximum contractual amount which would have been settled in April 2012. There is no contingent earn-out for our CKD acquisition.

18

Results of Operations for the Years Ended December 31, 2010, 2009, and 2008

The following table compares results of operations for the years ended December 31, 2010 and 2009:

| |

Year Ended December 31, |

|

|

|

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

% of Net Sales | |||||||||||||||

| |

% Change |

||||||||||||||||

($ in thousands)

|

2010 | 2009 | 2010 | 2009 | |||||||||||||

Net sales |

$ | 782,676 | $ | 632,478 | 23.7 | % | 100.0 | % | 100.0 | % | |||||||

Cost of sales, excluding depreciation and amortization |

565,185 | 355,088 | 59.2 | % | 72.2 | 56.1 | |||||||||||

Freight and distribution expenses |

73,406 | 57,395 | 27.9 | % | 9.4 | 9.1 | |||||||||||

Selling, general and administrative expenses |

31,129 | 31,377 | (0.8 | )% | 4.0 | 5.0 | |||||||||||

Depreciation and amortization |

45,245 | 54,667 | (17.2 | )% | 5.7 | 8.6 | |||||||||||

Gain on sale of business |

— | 16,417 | (100.0 | )% | — | (2.6 | ) | ||||||||||

Other operating income |

992 | 994 | (0.2 | )% | (0.1 | ) | (0.1 | ) | |||||||||

Operating income |

68,703 | 151,362 | (54.6 | )% | 8.8 | 23.9 | |||||||||||

Foreign exchange gain (loss) |

(666 | ) | 219 | (404.1 | )% | (0.1 | ) | — | |||||||||

Interest income |

37 | 12 | 208.3 | % | — | — | |||||||||||

Interest expense |

5,440 | 19,176 | (71.6 | )% | 0.7 | 3.0 | |||||||||||

Income before income taxes |

62,634 | 132,417 | (52.7 | )% | 8.0 | 20.9 | |||||||||||

Provision (benefit) for income taxes |

(2,407 | ) | 52,137 | (104.6 | )% | (0.3 | ) | 8.2 | |||||||||

Net income |

$ | 65,041 | $ | 80,280 | (19.0 | )% | 8.3 | % | 12.7 | % | |||||||

Net sales for the year ended December 31, 2010 were $782.7 million compared to $632.5 million for the year ended December 31, 2009, an increase of 23.7 percent. Net sales in 2010 were higher than in 2009 by $150.2 million, of which $60.8 million was due to higher average selling prices, $82.4 million was due to an 11.8 percent increase in volume due to increased demand from improving economic conditions, and $18.8 million was due to a more favorable product mix due to a lower percentage of export linerboard sales. Partially offsetting the increase in net sales was a decrease of $6.9 million due to the sale of the dunnage bag business in March 2009. Exchange rates negatively impacted net sales by $4.9 million.

Cost of sales, excluding depreciation and amortization expense, for the year ended December 31, 2010 was $565.2 million compared to $355.1 million for the year ended December 31, 2009, an increase of $210.1 million or 59.2 percent. The increase in cost of sales was mainly due to a $141.8 million decrease in alternative fuel mixture tax credits (the tax credit expired December 31, 2009), $54.2 million due to volume and mix changes, $6.8 million related to the Charleston mill tri-annual planned maintenance outage, a $5.9 increase in compensation and benefit costs as the Company reinstated certain benefits in January 2010 and $6.7 million due to inflation on input costs. Partially offsetting the increase in cost of sales was $5.3 million of lower costs due to the sale of the dunnage bag business.

Freight and distribution expenses for the year ended December 31, 2010 totaled $73.4 million, compared to $57.4 million for the year ended December 31, 2009, an increase of $16.0 million. This increase was primarily due to $9.0 million reflecting an 11.8 percent increase in volume, $3.1 million due to inflation and $4.3 million due to a lower percentage of export linerboard shipments in which freight costs are paid by the customer, partially offset by $0.4 million due to the sale of the dunnage bag business.

Selling, general and administrative expenses for the year ended December 31, 2010 totaled $31.1 million compared to $31.4 million in 2009. The decrease of $0.3 million reflects savings of

19

$5.1 million for the termination of transitional services provided by MeadWestvaco in the fourth quarter of 2009, $0.5 million of lower bad debts, $0.5 million of lower audit fees and $0.3 million related to the sale of the dunnage bag business. Partially offsetting these decreases in selling, general and administrative expenses were $5.3 million of higher compensation and benefit expenses as the Company reinstated certain benefits, including management incentives, in January 2010 that were previously suspended as a result of poor economic conditions in early 2009, and $1.2 million of higher stock compensation expense. As a percentage of net sales, selling, general and administrative expenses dropped from 5.0 percent in 2009 to 4.0 percent in 2010.

Depreciation and amortization for the year ended December 31, 2010 totaled $45.2 million compared to $54.7 million for the same period in 2009. The decrease of $9.5 million was primarily due to $9.7 million of lower intangible asset amortization. The Company acquired a coal contract with below market prices in conjunction with the CKD acquisition. The contract and related amortization expired on December 31, 2009.

The $16.4 million gain on sale of business reflects the sale of the dunnage bag business to Illinois Tool Works Inc. on March 31, 2009.

Other operating income for the years ended December 31, 2010 and 2009 totaled $1.0 million. Other operating income includes commissions the Company receives from marketing bleached paper produced and sold by IP to KapStone customers.

Foreign exchange losses for the year ended December 31, 2010 were $0.7 million compared to a foreign exchange gain of $0.2 million for the year ended December 31, 2009. The change reflects the strengthening of the U.S. dollar in 2010 compared to the Euro.

Interest expense for the years ended December 31, 2010 and 2009 was $5.4 million and $19.2 million, respectively. Interest expense reflects interest on the Company's senior credit agreement and amortization of debt issuance costs. Interest expense was $13.8 million lower in 2010 compared to 2009 due to lower term loan balances, the extinguishment of senior notes and lower interest rates.

Provision (benefit) for income taxes for the years ended December 31, 2010 and 2009 was $(2.4) million and $52.1 million, respectively, reflecting an effective tax rate of (3.8) percent in 2010 compared to 39.4 percent 2009. The lower provision (benefit) for income taxes in 2010 mainly reflects the combined impact of the $21.0 million net benefit from the cellulosic biofuel producer's tax credit and a $69.8 million reduction in pre-tax income.

20

The following table presents a reconciliation of consolidated net sales and operating income to amounts reported by operating segment:

| |

Years Ended December 31, |

||||||

|---|---|---|---|---|---|---|---|

Operating Segment ($ 000s):

|

2010 | 2009 | |||||

Consolidated net sales: |

|||||||

Unbleached kraft |

$ | 782,676 | $ | 626,450 | |||

Other |

— | 6,927 | |||||

Elimination of intersegment sales |

— | (899 | ) | ||||

Total |

$ | 782,676 | $ | 632,478 | |||

Operating income / (loss): |

|||||||

Unbleached kraft |

$ | 89,521 | $ | 155,904 | |||

Other |

— | 748 | |||||

Gain on sale of business |

— | 16,417 | |||||

Corporate |

(20,818 | ) | (21,707 | ) | |||

Total |

$ | 68,703 | $ | 151,362 | |||

Unbleached Kraft

| |

Years Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | Change | % | |||||||||

Net sales |

$ | 782,676 | $ | 626,450 | $ | 156,226 | 24.9 | % | |||||

Operating income |

89,521 | 155,904 | (66,383 | ) | (42.6 | )% | |||||||

Operating income % of net sales |

11.4 | % | 24.9 | % | (13.5 | )% | |||||||

Average revenue per ton |

$ | 586 | $ | 524 | $ | 62 | 11.8 | % | |||||

Tons of paper sold |

1,285,145 | 1,149,595 | 135,550 | 11.8 | % | ||||||||

For the year ended December 31, 2010, unbleached kraft segment net sales increased by $156.2 million, or 24.9 percent, to $782.7 million compared to $626.5 million for the year ended December 31, 2009. The increase in net sales was mainly due to $60.8 million of higher average selling prices, $82.4 million of higher sales volume resulting from an 11.8 percent increase in tons of paper sold, and $18.8 million of a more favorable product mix due to a lower percentage of export linerboard sales. Average revenue per ton for 2010 was $586 per ton, or $62 per ton higher than average revenue per ton in 2009 as market prices for kraft paper and linerboard increased throughout 2010 due to higher overall industry demand. Exchange rates negatively impacted net sales by $4.9 million.

Unbleached kraft segment operating income decreased by $66.4 million, or 42.6 percent, to $89.5 million for the year ended December 31, 2010, compared to $155.9 million for the year ended December 31, 2009. Operating income decreased primarily due to $141.8 million from lower alternate fuel mixture tax credits (the tax credit expired on December 31, 2009), $6.8 million related to the Charleston mill tri-annual planned maintenance outage, $9.8 million of inflation on input and freight costs and $7.7 million of higher compensation and benefit expenses as the Company reinstated certain benefits in January 2010 that were previously suspended in early 2009 and $4.9 million due to foreign exchange rates. The decrease in operating income was partially offset by $60.8 million of higher average selling prices, $19.9 million from higher sales volume, $13.6 million of a more favorable product mix due to a lower percentage of export linerboard sales, $9.7 million of lower amortization expense related to an expired intangible asset and $0.5 million of lower bad debts.

Operating income for the years ended December 31, 2010, and 2009 includes $13.4 million and $6.0 million, respectively, of expenses relating to the Company's planned maintenance outages.

21

Operating income as a percentage of net sales decreased to 11.4 percent mainly due to lower alternative fuel mixture tax credits, the reinstatement of certain employee benefits and the planned maintenance outages partially offset by higher average selling prices.

Other

Other includes the Company's dunnage bag business which was sold on March 31, 2009 to Illinois Tool Works Inc.

Corporate

Corporate expenses for the year ended December 31, 2010, totaled $20.8 million compared to $21.7 million for the year ended December 31, 2009. The decrease of $0.9 million reflects savings of $5.1 million for the termination of transitional services provided by MeadWestvaco in the fourth quarter of 2009 and $0.5 million of lower audit fees partially offset by $3.5 million of higher compensation and benefit expenses as the Company reinstated the management incentive plan and retirement benefits in 2010 that were temporarily suspended in 2009 as a result of poor economic conditions and $1.2 million of higher stock compensation expense.

The following table compares results of operations for the years ended December 31, 2009 and 2008:

| |

Year Ended December 31, |

|

|

|

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

% of Net Sales | |||||||||||||||

| |

% Change |

||||||||||||||||

($ in thousands)

|

2009 | 2008 | 2009 | 2008 | |||||||||||||

Net sales |

$ | 632,478 | $ | 524,549 | 20.6 | % | 100.0 | % | 100.0 | % | |||||||

Cost of sales, excluding depreciation and amortization |

355,088 | 362,462 | (2.0 | )% | 56.1 | 69.1 | |||||||||||

Freight and distribution expenses |

57,395 | 50,154 | 14.4 | % | 9.1 | 9.6 | |||||||||||

Selling, general and administrative expenses |

31,377 | 30,411 | 3.2 | % | 5.0 | 5.8 | |||||||||||

Depreciation and amortization |

54,667 | 31,683 | 72.5 | % | 8.6 | 6.0 | |||||||||||

Gain on sale of business |

16,417 | — | 100.0 | % | (2.6 | ) | — | ||||||||||

Other operating income |

994 | 817 | 21.7 | % | (0.1 | ) | (0.2 | ) | |||||||||

Operating income |

151,362 | 50,656 | 198.8 | % | 23.9 | 9.7 | |||||||||||

Foreign exchange gain (loss) |

219 | (987 | ) | 122.2 | % | — | (0.2 | ) | |||||||||

Interest income |

12 | 927 | (98.7 | )% | — | 0.1 | |||||||||||

Interest expense |

19,176 | 18,449 | 3.9 | % | 3.0 | 3.5 | |||||||||||

Income before income taxes |

132,417 | 32,147 | 311.9 | % | 20.9 | 6.1 | |||||||||||

Provision for income taxes |

52,137 | 12,482 | 317.7 | % | 8.2 | 2.4 | |||||||||||

Net income |

$ | 80,280 | $ | 19,665 | 308.2 | % | 12.7 | % | 3.7 | % | |||||||

Net sales for the year ended December 31, 2009 were $632.5 million compared to $524.5 million for the year ended December 31, 2008, an increase of 20.6 percent. The full year of sales for CKD in 2009, compared to six months in 2008 (acquisition consummated on July 1, 2008), accounted for $188.2 million of the increase in net sales. Excluding the additional six months of CKD's sales and $26.1 million of lower sales due to the sale of the dunnage bag business on March 31, 2009, net sales in 2009 were lower than in 2008 by $54.1 million, of which $61.0 million was due to lower selling prices and $27.4 million was due to a less favorable product mix, as the Company had a higher percentage of linerboard sales, which has a lower average selling price than other products. This was partially offset by $34.3 million of higher volume in the second half of 2009.

22